Detection of Change Points in Piecewise Polynomial Signals Using Trend Filtering

Abstract

While many approaches have been proposed for discovering abrupt changes in piecewise constant signals, few methods are available to capture these changes in piecewise polynomial signals. In this paper, we propose a change point detection method, PRUTF, based on trend filtering. By providing a comprehensive dual solution path for trend filtering, PRUTF allows us to discover change points of the underlying signal for either a given value of the regularization parameter or a specific number of steps of the algorithm. We demonstrate that the dual solution path constitutes a Gaussian bridge process that enables us to derive an exact and efficient stopping rule for terminating the search algorithm. We also prove that the estimates produced by this algorithm are asymptotically consistent in pattern recovery. This result holds even in the case of staircases (consecutive change points of the same sign) in the signal. Finally, we investigate the performance of our proposed method for various signals and then compare its performance against some state-of-the-art methods in the context of change point detection. We apply our method to three real-world datasets including the UK House Price Index (HPI), the GISS surface Temperature Analysis (GISTEMP) and the Coronavirus disease (COVID-19) pandemic.

KEYWORDS: Change point detection, Trend filtering, Gaussian bridge process, Pattern recovery, COVID-19.

1 Introduction

The problem of change point detection is more than sixty years old. It was first studied by Page, (1954, 1955), and since then, has been of interest to many scientists including statisticians. Many of the earlier developments concerned the existence of at most one change point; however, considerable attention in recent years has been given to multiple change point analysis, which has found applications in many fields such as finance and econometrics, Bai and Perron, (2003); Hansen, (2001), bioinformatics and genomics, Futschik et al., (2014); Lavielle, (2005), climatology, Liu et al., (2010); Pezzatti et al., (2013), and technology, Siris and Papagalou, (2004); Oudre et al., (2011); Lung-Yut-Fong et al., (2012); Ranganathan, (2012); Galceran et al., (2017). Consequently, there is a vast and rich literature on the subject. In the following, we only review a body of literature on a retrospective change point framework closely related to our work and refer the interested readers to Eckley et al., (2011); Lee, (2010); Horváth and Rice, (2014); Truong et al., (2018) for more comprehensive reviews.

We consider the univariate signal plus noise model

| (1) |

where is a deterministic and unknown signal with equally spaced input points over the interval . The error terms are assumed to be independently and identically distributed Gaussian random variables with mean zero and finite variance . We assume that undergoes unknown and distinct changes at point fractions , where the number of change point fractions, can grow with the sample size . Additionally, we assume that is a piecewise polynomial function of order . These assumptions imply that, associated with , there are change points locations , which partition the entire signal into segments. More specifically, any subsignal of within segments created by the change points follows an -degree polynomial structure with or without a continuity constraint at the change points. For more detail, see Figure 2. Change in the level of a piecewise constant signal, known as the canonical multiple change point problem, and change in the slope of a piecewise linear signal are examples of the problem under consideration in this paper. In change point analysis, the objective is to estimate the number of change points, , as well as their locations based on the observations .

The canonical multiple change point problem, where the signal is modelled as a piecewise constant function, has been extensively studied in the literature. In this framework, there are many approaches and we only attempt to list a selection of them here. The majority of these techniques seek to identify all change points at once by solving an optimization problem consisting of a loss function, often the negative log-likelihood, and a penalty criterion. Yao, (1988); Yao and Au, (1989) used the square error loss along with the Schwarz Information Criterion (SIC) as a penalty function to consistently estimate the bounded number of change points and their locations for the data drawn from a Gaussian distribution. Within the same setting, incorporation of various penalty functions including Modified Information Criterion (MIC) Pan and Chen, (2006), modified Bayesian Information Criterion (mBIC) Zhang and Siegmund, (2007), Simultaneous Information Theoretic Criterion (SITC) Wu, (2008) and modified SIC Ciuperca, (2011, 2014), have been studied. Specific algorithms such as Optimal Partitioning Auger and Lawrence, (1989), Segment Neighbourhood Jackson et al., (2005), and pruning approaches such as PELT Killick et al., (2012) and PDPa Rigaill, (2015) are developed to solve such optimization problems.

Apart from penalty-based techniques, another frequently used class of change point detection approaches encompasses the greedy search procedures in which they search sequentially for one single change point at a time. The most popular methods in this class are Binary Segmentation Vostrikova, (1981) and its variants such as Circular Binary Segmentation (CBS) Olshen et al., (2004), and Wild Binary Segmentation (WBS) Fryzlewicz et al., (2014). In recent years, researchers have attempted to improve Binary Segmentation’s performance from statistical and computational viewpoints. Fryzlewicz et al., (2018) suggested a backward (bottom-up) mechanism, called Tail Greedy Unbalanced Haar (TGUH), which is computationally fast and statistically consistent in estimating both the number and the locations of change points. Also, Fryzlewicz, (2018) introduced Wild Binary Segmentation 2 (WBS2) to deal with the shortcomings of WBS in datasets with frequent changes. It has been shown that the method is fast in run time and accurate in detection.

Beyond the canonical change point problem, signals in which is modelled as a piecewise polynomial of order have attracted less attention in the literature despite many applications. For instance, piecewise linear signals are applied in monitoring patient health (Aminikhanghahi and Cook, (2017), Stasinopoulos and Rigby, (1992)), climate change (Robbins et al., (2011)), and finance (Bianchi et al., (1999)). In such a framework, Bai, (1997) introduced a method based on Wald-type sequential tests, and Maidstone et al., (2017) devised a dynamic programming applied to an -penalized least square procedure. In continuous piecewise linear models, Kim et al., (2009) developed a methodology called -trend filtering. Furthermore, Baranowski et al., (2019) put forward the method of Narrowest Over Threshold (NOT), and Anastasiou and Fryzlewicz, (2019) developed an approach called Isolate-Detect (ID) which both provide asymptotically consistent estimators of the number and locations of change points.

Our goal in this paper is to introduce a unifying method covering the canonical change point problem and beyond. More precisely, the method is cable of detecting change points in piecewise polynomial signals of order () with and without continuity constraint at the locations of change points.

The detection of change points in a sequence of data can be formulated as a penalized regression fitting problem. According to our notation, the quantity is nonzero if the signal undergoes a change at point , and is zero otherwise. Moreover, if we assume that change points are sparse, that is, the number of locations where changes, , is much smaller than the number of observations , change points can be estimated using the one-dimensional fused lasso problem

where .

This formulation of the canonical change point problem was first considered in Huang et al., (2005) and was applied to analyze a DNA copy number dataset. Harchaoui and Lévy-Leduc, (2010) considered the same formulation and proved the consistency of the respective change point estimates when the number of change points is bounded. Employing sparse fused lasso which is composed of both the -norm and the total variation seminorm penalties, Rinaldo et al., (2009) proposed a sparse piecewise constant fit and established the consistency of the corresponding estimates when the variance of the noise terms vanishes, and the minimum magnitude of jumps is bounded from below. However, Rojas and Wahlberg, (2014) argued that the consistency results achieved by Rinaldo et al., (2009) are incorrect when a frequently viewed pattern, called staircase, exists in the signal. The staircase phenomenon occurs in a piecewise constant model when there are either two consecutive downward jumps or upward jumps in its mean structure. The staircase pattern will be discussed in more detail in Section 6. Additionally, Qian and Jia, (2016) showed that the lasso problem of Tibshirani, (1996) when derived by transforming fused lasso does not satisfy the Irrepresentable Condition (Zhao and Yu, (2006)) that is necessary and sufficient for exact pattern recovery. In particular, Qian and Jia, (2016) proposed an approach called preconditioned fused lasso based on the puffer transformation of Jia et al., (2015) and established that it can recover the exact pattern with probability approaching one.

A similar approach to that of the piecewise constant signals can be considered for estimating change points in piecewise polynomial signals. In particular, a positive integer is a change location in an -th degree piecewise polynomial signal if -th element of the vector is non-zero, denoted by . Here is a penalty matrix that will be defined in Section 2.2. Hence, change points can be estimated from nonzero elements of , where is the solution of

| (2) |

The aforementioned problem was first studied by Steidl et al., (2006) in the context of image processing and was called higher order total variation regularization. It was later rediscovered by Kim et al., (2009) and termed trend filtering in the nonparametric regression setting. Kim et al., (2009) specifically explored linear trend filtering () which fits piecewise linear models. Tibshirani et al., (2014) extensively studied trend filtering and compared its performance with smoothing splines Green and Silverman, (1993) and locally adaptive regression splines Mammen et al., (1997) in the context of nonparametric regression. Tibshirani et al., (2014) also established that trend filtering enjoys desirable and strong theoretical properties of locally adaptive regression splines while being computationally less intensive due to its banded penalty matrix. Moreover, trend filtering has an adaptive knot selection property, which makes it well suited for change point analysis.

From a computational and algorithmic standpoint, Kim et al., (2009) described Primal-Dual Interior Point (PDIP) method for deriving the estimates of the linear trend filtering problem at a fixed value of . This can be easily carried over to the trend filtering problem of any order. Wang et al., (2014) suggested an algorithm based on a falling factorial basis while Ramdas and Tibshirani, (2016) derived an algorithm based on the Alternating Direction Method of Multipliers (ADMM) discussed in Boyd et al., (2011). The computational complexity of all these algorithms is of order .

In this paper, we develop a new methodology called Pattern Recovery Using Trend Filtering (PRUTF) for identifying unknown change points in piecewise polynomial signals with no continuity restriction at change point locations. Therefore, a change point is defined as a sudden jump in the signal and its all derivatives up to order . Figure 2 displays such change points for various . In this paper, we make the following contributions.

-

•

We propose a generic dual solution path algorithm along with the regularization parameter for trend filtering. This solution path, whose basic idea is borrowed from Tibshirani, (2011) enables us to determine change points at each level of the regularization parameter. Our algorithm, PRUTF, is different from that of Tibshirani, (2011) as we remove coordinates of dual variables after identifying each change point. This adjustment to the algorithm allows us to have independent dual variables between each pair of neighbouring change points. Besides, the elimination of coordinates at each step leads to faster implementation of the algorithm.

-

•

We establish a stopping criterion that plays an essential rule in the PRUTF algorithm used to find change points. Notably, we show that the dual variables of trend filtering between consecutive change points constitute a Gaussian bridge process. This finding allows us to introduce a threshold for terminating our proposed algorithm.

-

•

If the signal contains a staircase pattern, we prove that the method is statistically inconsistent, which makes it unfavourable. Explaining the reason for this end, we modify the PRUTF algorithm to produce estimates consistent in terms of both the number and location of change points.

This paper is organized as follows: we first describe how to characterize the dual optimization problem of trend filtering. In Section 3, we develop our main algorithm, PRUTF, to use in constructing the dual solution path of trend filtering and, in turn, identifying the locations of change points. Section 4 discusses the properties of this dual solution path. We establish that the dual variables derived from the solution path form a Gaussian bridge process that makes them favourable for statistical inference. Applying these properties, we develop a stopping rule for the change point search algorithm in Section 5. The quality of the PRUTF algorithm is validated in terms of pattern recovery of the true signal in Section 6. It is established that the proposed technique in its naive form fails to consistently identify the true signal when a special pattern, called staircase, is present in the signal. Section 7 elaborates on how to modify the algorithm in order to estimate the true pattern consistently. Simulation results, and real-world applications are presented in Section 8. We explore the performance of our proposed method for signals with frequent change points as well as models with dependent error terms in Section 9. We conclude the paper with a discussion in Section 10.

2 Notations and Fundamental Concepts

2.1 Notations

We begin this section with setting up notations that will be used throughout this article. For an matrix , we denote its rows by and express the matrix as . Now for the set of indices , the notation represents the submatrix of whose row labels are in the set . In a similar manner, for a vector of length , we let denote a subvector of whose coordinate labels are in . We write and to denote and , respectively, where is the set of indices in but not in . Furthermore, for selecting -th row of , the notation and for its -th element the notation are used. Also, extracts the -th elements of the vector . We write to denote the vector of the main diagonal entries of the matrix . Moreover, for a real number , denotes the greatest integer less than or equal , and denotes the least integer greater or equal . For a set , the indicator function is denoted by

2.2 The Dual Problem of Trend Filtering

Recall the trend filtering problem

| (3) |

where is the regularization parameter for controlling the effect of smoothing, and the penalty matrix is the difference operator of order . For , the first order difference matrix is defined as

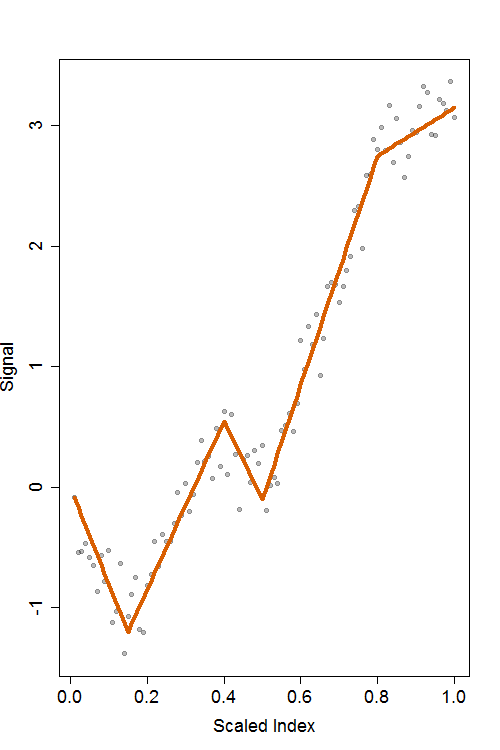

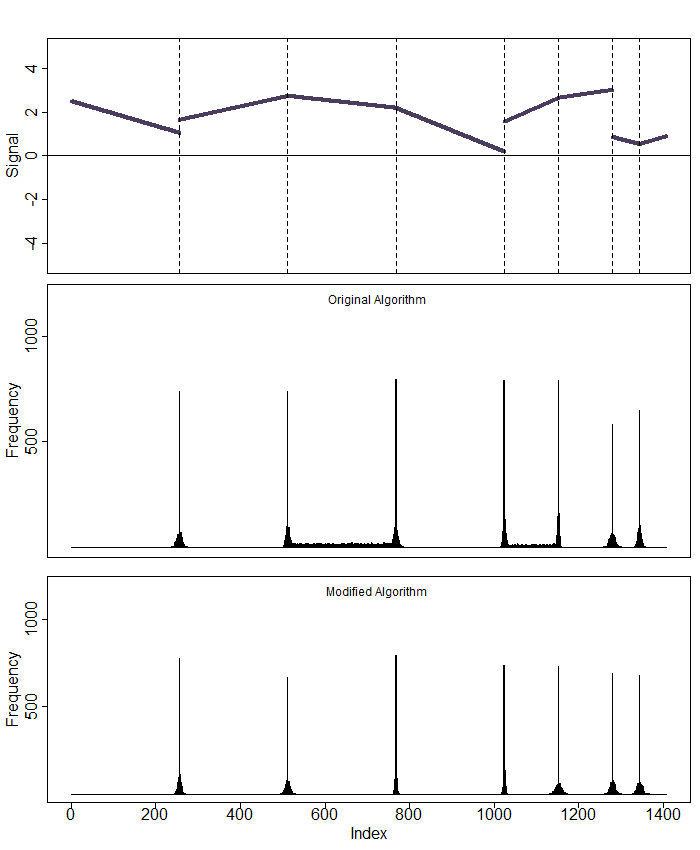

and for , the difference operator of order can be recursively computed by . Notice that, in this matrix multiplication, we consider only the submatrix consisting of the first rows and columns of the matrix . Figure 1 displays the trend filtering fits for for simulated data.

Although the objective function in the -th order trend filtering (3) is strictly convex and thus the minimization has a guaranteed unique solution, the penalty term is not differentiable in , so solving the optimization in its current form is difficult. To overcome this difficulty, we follow the argument in Tibshirani, (2011) and convert this optimization problem into its dual form. Since the objective function in the primal problem is strictly convex with no constraint, the strong duality holds, meaning that the primal and the dual solutions coincide.

The trend filtering problem (3) can be rewritten as

where, for ease in the notation, we use . For any given , the Lagrangian is

and, thus the dual function is given by

which is a concave function defined on , where and takes values in the extended real line . The vectors and are called the primal and dual variables, respectively. Taking the derivative of the Lagrangian with respect to and setting it to be equal to zero, we obtain

| (4) |

Now substituting this back into the Lagrangian , and performing certain algebraic manipulations, we obtain

Minimizing , or equivalently maximizing , with respect to leads us to the dual function . Notice that is the conjugate of the function in the context of conjugate convex functions. See Brezis, (2010) and Boyd and Vandenberghe, (2004). This conjugate function is given by

From all these, the dual function is given as

and, thus the dual problem is to find the maximum of the dual function . This is equivalent to

| (5) |

The constraint in (5) is an -ball or a hypercube centered at the origin with the boundaries given by the set . Since the matrix is full row rank, the problem (5) is strictly convex and has a unique solution, see Ali et al., (2019). In addition, notice that the dimension of the dual vector is , which is smaller than that of the primal vector and may lead to relatively faster computations. The connection between the primal and the dual solutions is given by the equations

| (6) |

| (7) |

where is a subgradient of computed at . This subgradient is given by

| (11) |

The statements in Equations (6)-(11) are equivalent to the KKT optimality conditions of the primal problem (3). The dual problem (5) demonstrates that is the projection, , of onto the convex polyhedron (or hypercube here) . From this, the primal solution (7) can be rewritten in the form of , representing the residual projection map of onto the polyhedron .

Our idea of applying trend filtering to discover change points in piecewise polynomial signals is inspired by Rinaldo et al., (2009) and its correction Rinaldo, (2014), in which change point detection is studied using fused lasso. Besides extending to piecewise polynomial signals, the novelty of our work is in providing an exact stopping criterion, which is based on the Gaussian bridge property of the trend filtering dual variables. In addition, we propose an algorithm which, unlike that proposed in Rinaldo et al., (2009), always produces consistent change points even in the presence of staircase patterns.

3 Solution Path of Trend Filtering and PRUTF Algorithm

In this section, we construct and study the solution path of dual variables as the regularization parameter decreases from to . In the following, the PRUTF algorithm is given to compute the entire dual solution path. This dual solution path identifies the corresponding primal solution using (7). For any given , we call any coordinate of a boundary coordinate if it is a vertex of the polyhedron , meaning that its absolute value becomes . In the process of constructing the solution path, for any , we trace several sets, introduced below.

-

•

The set , called the boundary set, contains the boundary coordinates identified by .

-

•

The vector , called the sign vector, represents collectively the signs of the boundary points in .

-

•

The set , called the augmented boundary set, contains the boundary coordinates in as well as the first coordinates immediately after.

-

•

The vector represents collectively the signs of the augmented boundary points in .

In the following, we discuss the need for the augmented boundary set . We begin by studying the structure of the dual vector in a piecewise polynomial signal of order , where the signal is partitioned into a number of blocks defined by the position of the change points. Because the signal is a piecewise polynomial of order , to compute the -th coordinate of the vector , we need points directly before the -th element of as well as points immediately after that. Consequently, the first elements of within each block cannot be computed. Moreover, within each block, the last elements of are all nonzero due to the existence of a change point. This observation is depicted in Figure 2 for . To explain this point clearly, consider the case of in Figure 2 in which the structure of is shown, where the true change points are at and . As can be seen, the points on the boundary – the nonzero coordinates of – are with their respective signs . Notice that does not exist at points 7 and 14. The augmented boundary set contains these points as well as the boundary points; that is . The respective signs of the coordinates in the augmented boundary set are given by . At each value of , we call the coordinates that belong to the augmented boundary set the augmented boundary coordinates, and the rest, the interior coordinates.

At the -th iteration with , we assume that the boundary set and its corresponding sign vector are and , respectively. Furthermore, we assume the augmented boundary set and its sign vector are and , respectively. Dual coordinates can be split into augmented boundary coordinates and interior coordinates . Recall from Section 2.1 that represents the subvector of with the coordinate labels in the set and represents the subvector of with the coordinate labels in the set . It is apparent from the definition of the boundary coordinates that

| (12) |

Replacing the boundary coordinate with in (5) and solving the resulting quadratic problem with respect to the interior coordinates, lead to their least square estimates, given by

| (13) |

It should be noted that for the purpose of simplicity, we denote and with and , respectively. Notice that in (13), the first term simply yields the least square estimate of regressing the response vector on the design matrix . The second term can be interpreted as a shrinkage term due to the condition . The expression (13) is true for until either an interior coordinate joins to the boundary or a coordinate in the boundary set leaves the boundary. The following argument explains how to specify values of while the interior coordinates change.

We define the joining time associated with the interior coordinate as the time at which this interior coordinate joins the boundary. To determine the next joining time, we reduce the value of in a linear direction starting from and solve . Note that the right-hand side of (13) can be expressed as , where

| (14) | ||||

| (15) |

The joining time for every is hence the solution of the equation with respect to , which is given by

Note that is uniquely defined because only one of the signs or yields .

Now we turn the attention to the characterization of a coordinate which leaves the boundary set . For , the leaving time is defined as the time that the coordinate leaves the boundary set . Since is the sign vector of changes captured by , then , which in turn, along with Equation (7), implies . Here, for any vector , denotes the diagonal matrix with the diagonal elements given by , and holds element-wise. Therefore, a coordinate leaves the boundary set if is violated. Using the relation

and the decomposition , we obtain

| (16) |

where

| (17) | ||||

| (18) |

Hence, a leaving time is obtained from the equation as

The conditions in the aforementioned equation is due to the fact that at the -th iteration with , the expression fails for , if both and are negative. An alternative way to determine the next leaving time is to use the KKT optimality conditions of (5). We refer the reader to the supplementary materials of Tibshirani, (2011).

The following algorithm, PRUTF, describes the process of constructing the entire dual solution path of trend filtering.

Algorithm 1 (PRUTF Algorithm)

-

1.

Initialize the set of change points locations as , the empty set.

-

2.

At step , initialize the boundary set and its associated sign vector , both with cardinality of , where is obtained by

(19) and , where is the -th element of the vector . The updated set of change points locations is now . We also record the first joining time and keep track of the augmented boundary set and its corresponding sign vector of length . The dual solution is regarded as , for .

-

3.

For step

-

(a)

Obtain the pair from

(20) and set the next joining time as the value of , for and .

-

(b)

Obtain the pair from

(21) and assign the next leaving time as the value of , for and .

-

(c)

Let , then the boundary set and its sign vector are updated in the following fashion:

-

–

Either append and the corresponding signs to and , respectively, provided that . Also, add to .

-

–

Or remove and the corresponding signs , from and , respectively, provided that . Also, remove from .

In the same manner, the augmented boundary set, and its sign, are formed by adding and to and , respectively, if or, otherwise, by removing the associated set and from and . Thus, the dual solution is computed as for interior coordinates and for boundary coordinates over .

-

–

-

(a)

-

4.

Repeat step 3 until .

The critical points indicate the values of the regularization parameter at which the boundary set changes.

Remark 1

Notice that the vector derived by the PRUTF algorithm represents the locations of change points for the dual variables. In order to obtain the locations of change points in primal variables, we must add to any element of , that is, . This relationship between the primal and dual change point sets is visible from Figure 2.

Remark 2

For fused lasso, , Lemma 1 of Tibshirani, (2011), known as the boundary lemma, is satisfied since the matrix is diagonally dominant, meaning that , for . This lemma states that when a coordinate joins the boundary, it will stay on the boundary for the rest of the path. Consequently, part (b) of step 3 in Algorithm 1 is unnecessary, and hence the next leaving time in part (c) is set to zero, i.e., , for every step . However, the boundary lemma is not satisfied for .

Remark 3

There is a subtle and important distinction between our proposed algorithm, PRUTF, and the one presented in Tibshirani, (2011). The latter work studies the generalized lasso problem for any arbitrary penalty matrix (unlike used in trend filtering, which must have a certain structure). The proposed algorithm in Tibshirani, (2011) relies on adding or removing only one coordinate to or from the boundary set at every step. The key attribute of our algorithm is to add or remove coordinates to or from the augmented boundary set, an approach inspired by the argument presented at the beginning of this section. Essentially, this attribute makes PRUTF, presented in Algorithm 1, well-suited for change point analysis. It is important to mention that PRUTF requires at least data points between neighbouring change points.

Remark 4

Remark 5

The number of iterations required for PRUTF, presented in Algorithm 1, is at most , where , see Tibshirani et al., (2013), Lemma 6. However, this upper bound for the number of iterations is usually very loose. The upper bound comes from the following realization discovered by Osborne et al., (2000) and later improved by Mairal and Yu, (2012). Any pair appears at most once throughout the solution path. In other words, if is visited in one iteration of the algorithm, the pair as well as cannot reappear again for the rest of the algorithm. Interestingly, this fact says that once a coordinate enters the boundary set, it cannot immediately leave the boundary set at the next step.

Moreover, note that at one iteration of the PRUTF algorithm with the augmented boundary set , the dominant computation is in solving the least square problem

| (22) |

One can apply QR decomposition of to solve the least square problem, and then update the decomposition as set changes. However, since is a banded Toeplitz matrix (see Section 4), a solution of (22) always exists and can be computed using a banded Cholesky decomposition. Thus, the computational complexity for the iteration is of order , which is linear in the number of interior coordinates as is fixed and usually small. Overall, if is the total number of steps run by the PRUTF algorithm, then the total computational complexity is . See Tibshirani, (2011) and Arnold and Tibshirani, (2016).

4 Statistical Properties of the Solution Path

An important component of the methodology that we develop in this work involves computing algebraic expressions based on the matrix . In this section, we describe the properties of such expressions. To begin with, let and be the augmented boundary set and its corresponding sign vector, respectively, after a number of iterations of Algorithm 1, where and for . This augmented boundary set corresponds to change points that partition all the dual variables into blocks for , with the conventions that and . In the following, we list some properties of matrix multiplications involving .

-

•

It follows from the definition of the matrix that it is a banded Toeplitz matrix with bandwidth . It tuns out that the matrix reveals the same property, meaning that it is a square banded Toeplitz matrix. Moreover, its nonzero row elements are consecutive binomial coefficients of order with alternating signs. In other words, -th element of for is . An example, for , is given in panel (a) of Figure 3. Note that is a symmetric, nonsingular and positive definite matrix (Demetriou and Lipitakis,, 2001).

-

•

The matrix is a block diagonal matrix whose diagonal submatrices correspond to blocks. More precisely, the -th submatrix on the diagonal of is a matrix with the first rows and columns of , see panel (b) of Figure 3. Notice that, due to its non-singularity, is always invertible. In fact, both and are block diagonal matrices. Another interesting result is that every row of the matrix is a contrast vector, meaning that for any ,

((a)) Structure of . ((b)) The structure of . Figure 3: Structure of quadratic forms of matrix . -

•

Another interesting term in analyzing the behaviour of the dual variables is . It can be shown that the vector can be partitioned into subvectors associated with the change points . The subvector associated with , is , whose elements are zero, except the first consecutive as well as the last consecutive elements. The first nonzero elements of are the binomial coefficients in the expansion of , and its last elements are the binomial coefficients in the expansion of . Furthermore, the first elements of the first subvector and the last elements of the last subvector are also equal to zero. For example, for a piecewise cubic signal, , with two change points and signs , the vector becomes

Consequently, the structure of allows us to write . Additionally, if the signs of two consecutive change points and are the same, then

(23) for .

-

•

Let be the projection matrix onto the row space of the matrix . Moreover, let be the design matrix of the -th polynomial regression on the indices of -th segment , that is,

Therefore, the orthogonal projection matrix is a block diagonal matrix whose -th block associated with the segment is equal to the projection map onto the column space of , i.e.,

(24)

Equation (12) says that the absolute values of the boundary coordinates are , that is,

| (25) |

On the other hand, the values of the interior coordinates are given by

| (31) |

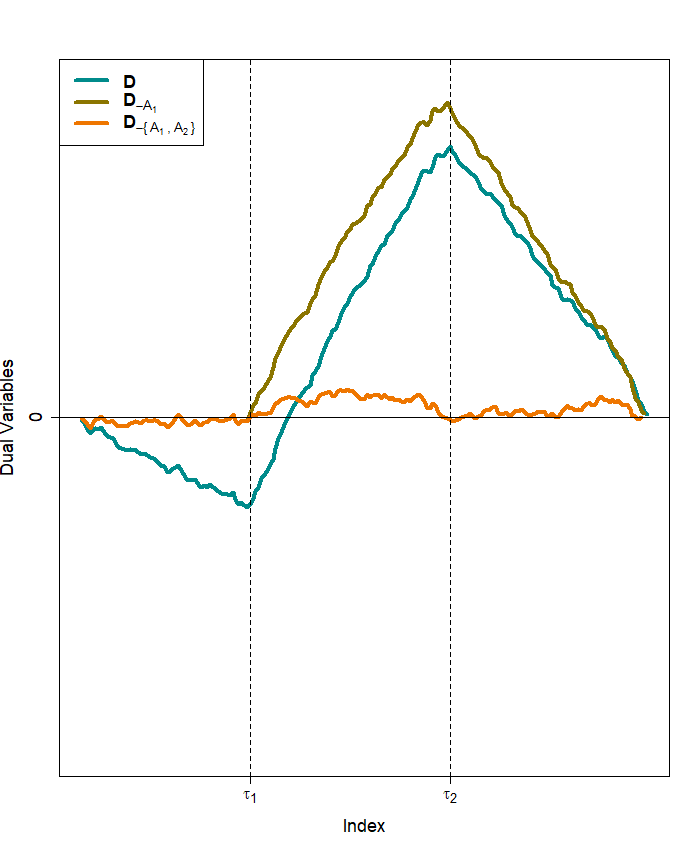

For a given , the dual variables for can be collectively viewed as a random bridge, that is, a conditioned random walk with drift whose end points are set to zero. Moreover, is bounded between and . The quantity can also be decomposed into a sum of several smaller random bridges which are formed by blocks created from the change points. Recall that the last consecutive elements of the block are , for any . Hence, for , the random bridge associated with the -th block is given by

| (32) |

with the conventions . It is important to note that similar to , the process satisfies the conditions and . From (32), the process is composed of the stochastic term

| (33) |

and the drift term

| (34) |

According to model (1) with Gaussian noises, it turns out that the discrete time stochastic process term can be embedded in a continuous time Gaussian bridge process. The following theorem describes the characteristics of this process.

Theorem 1

Suppose the observation vector is drawn from the model (1), where the error vector has a Gaussian distribution with mean zero and covariance matrix . For given and ,

-

(a)

Define

(35) for , where

(36) and, for . Then the stochastic process is a Gaussian bridge process with mean vector zero and covariance function

(37) for any .

-

(b)

The processes and are independent, for .

A proof is given in Appendix A.1.

This theorem could be extended to the case of non-Gaussian random variables and therefore establishes a Donsker type Central Limit Theorem for . Theorem 1 guarantees that the dual variable process associated with the -th block, i.e.

is a Gaussian bridge process with the drift term

| (38) |

and the covariance matrix stated in (37).

Recall that a standard Brownian bridge process defined on the interval is a standard Brownian motion conditioned on the event . It is often characterized from a Brownian motion with , by setting

The mean and covariance functions of the Brownian bridge are given by and for any , respectively. A Gaussian bridge process is an extension of the Brownian bridge process when the Brownian motion , in the definition of the Brownian bridge , is replaced by a more general Gaussian process . See, for example, Gasbarra et al., (2007).

Remark 6

The celebrated Donsker theorem Donsker, (1951) states that the partial sum process of a sequence of i.i.d. random variables, with mean zero and variance 1, converges weakly to a Brownian bridge process. See Van Der Vaart and Wellner, (1996) or Billingsley, (2013). A version of Theorem 1 involving non-Gaussian random variables would extend this result to weighted partial sum processes and show that the limiting process is a Gaussian bridge with a certain covariance structure. So the Gaussian assumption in Theorem 1 is not restrictive. It is also interesting to show that for , the process boils down to its respective CUSUM processes. To show this, consider the interval ,

-

•

For the piecewise constant signals, , the quantity can be written as

Notice that the above statement is the CUSUM statistic for the -th segment, that is

(39) where is the sample average of . It is well known that the CUSUM statistic (39) converges weakly to the Brownian bridge. In addition, for any , the covariance function becomes

which is identical to the covariance function of the Brownian bridge.

-

•

For the piecewise linear signals , the quantity reduces to

(40) where is the least square fit of the simple linear regression of onto . As proved in Theorem 1, the preceding statistic (40) is also a Gaussian bridge process. Furthermore, using the results in Hoskins and Ponzo, (1972), for any , the covariance function of this Gaussian bridge process is given by

where .

5 Stopping Criterion

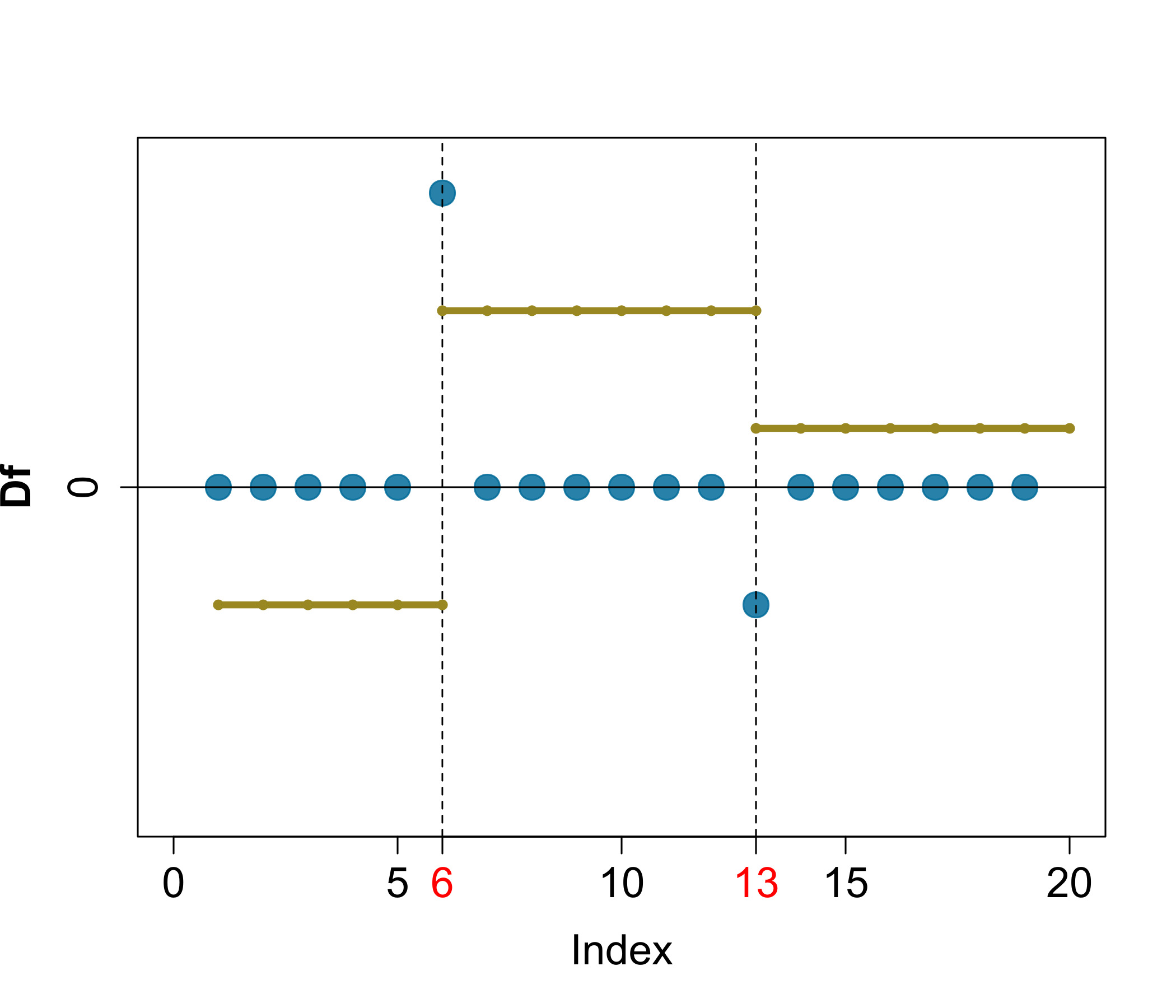

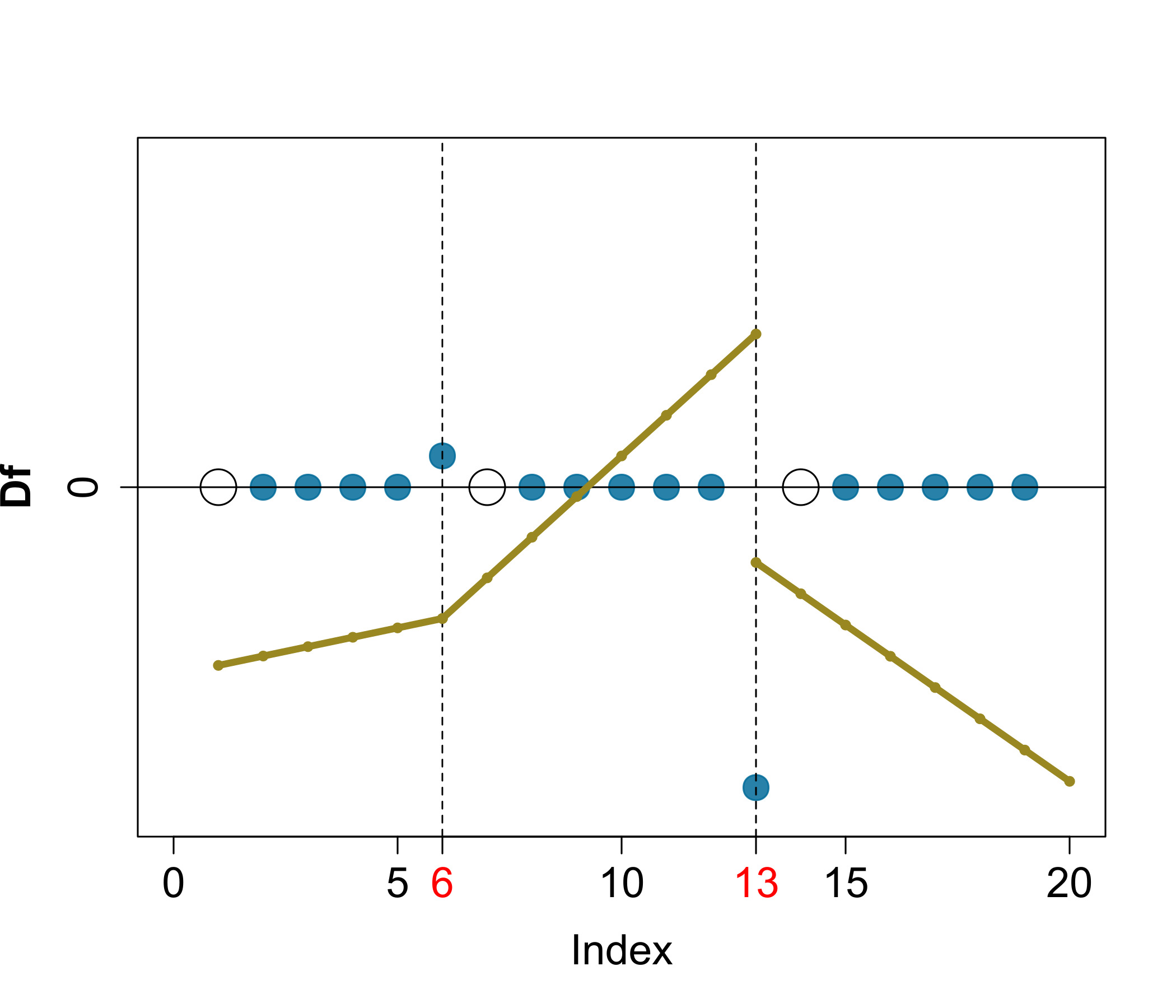

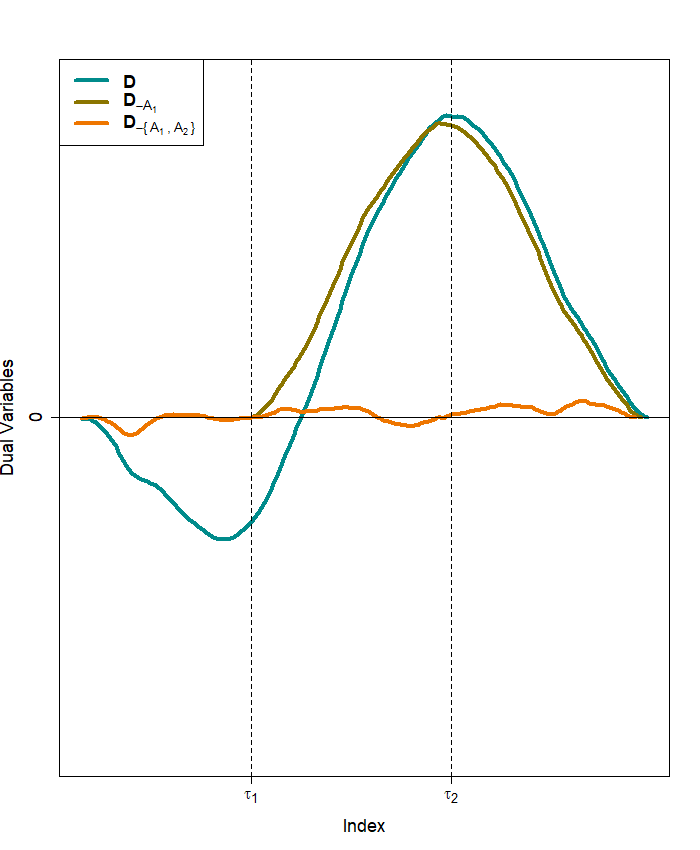

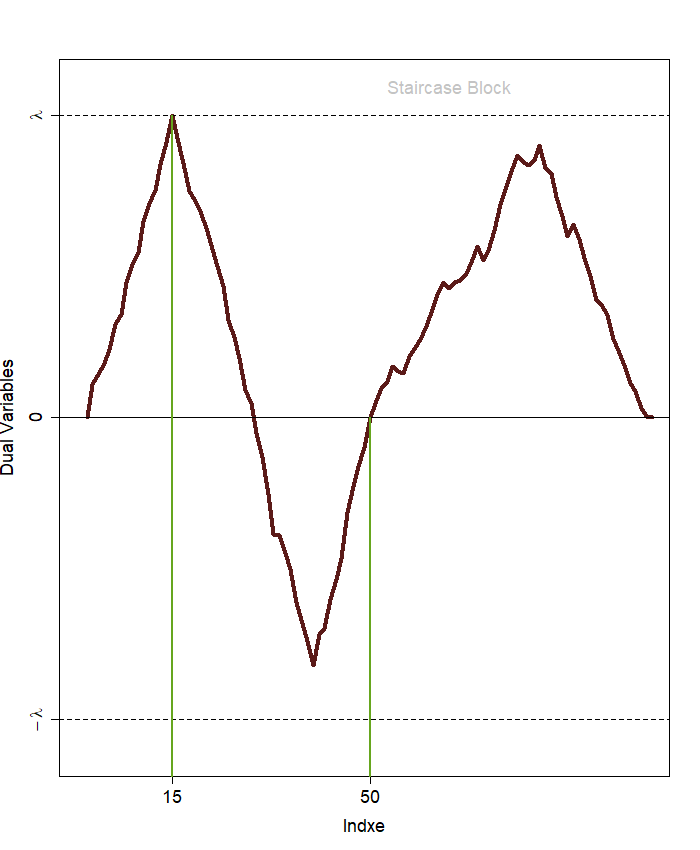

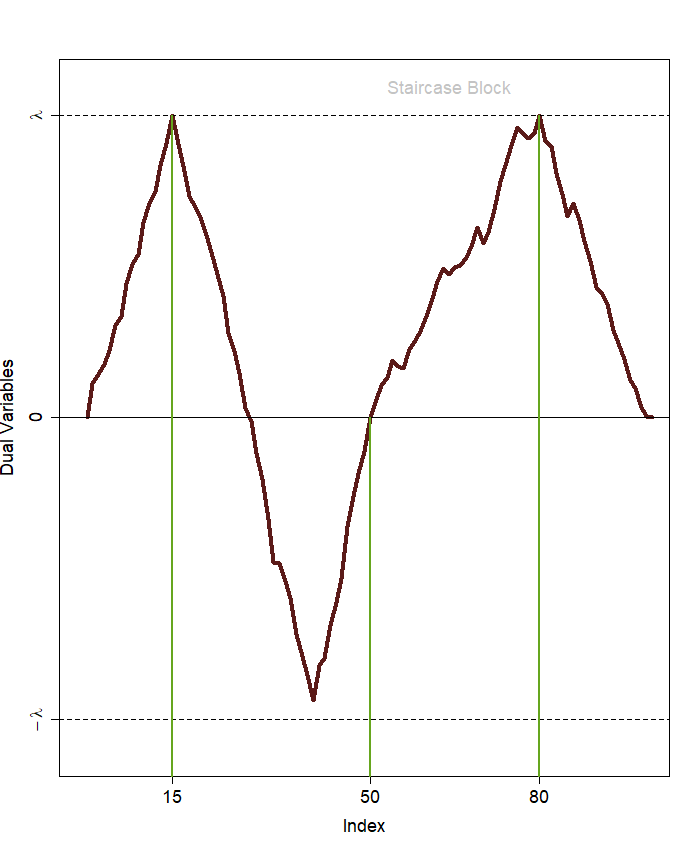

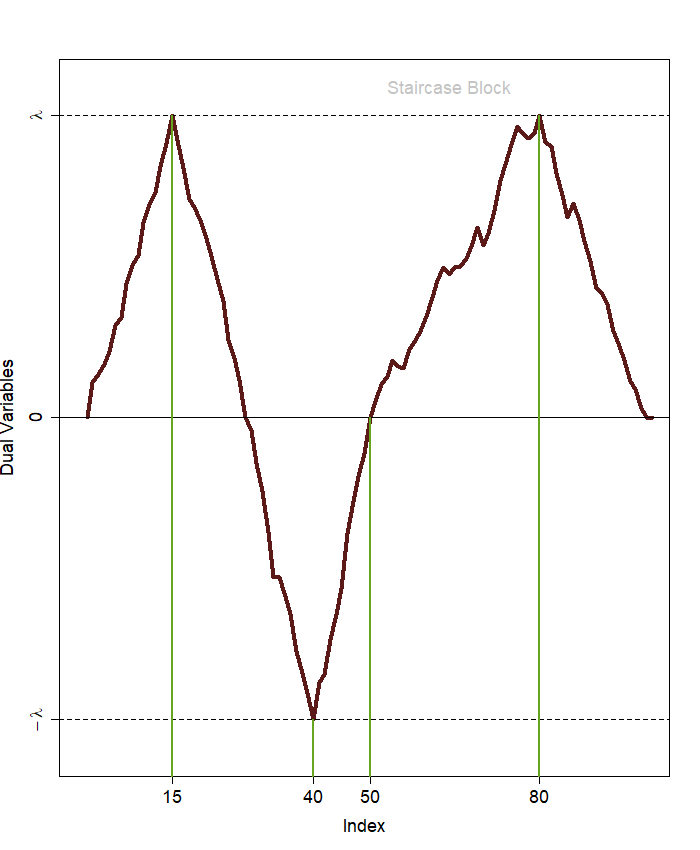

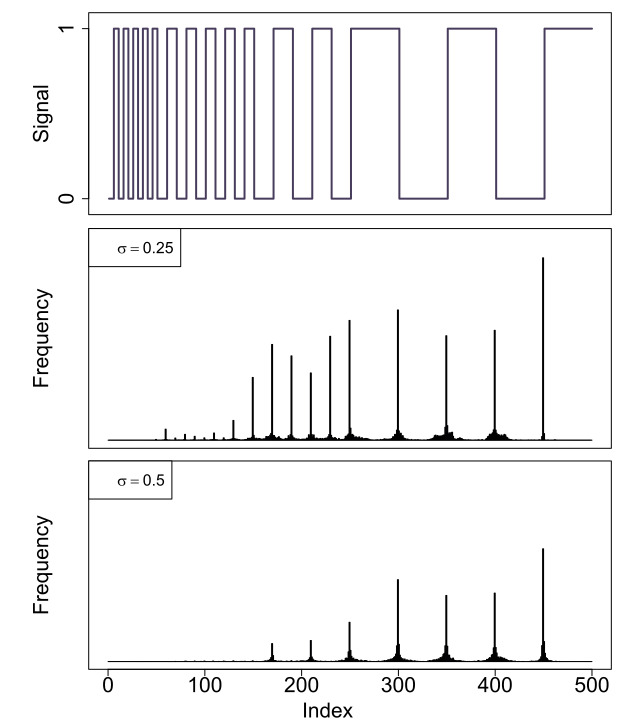

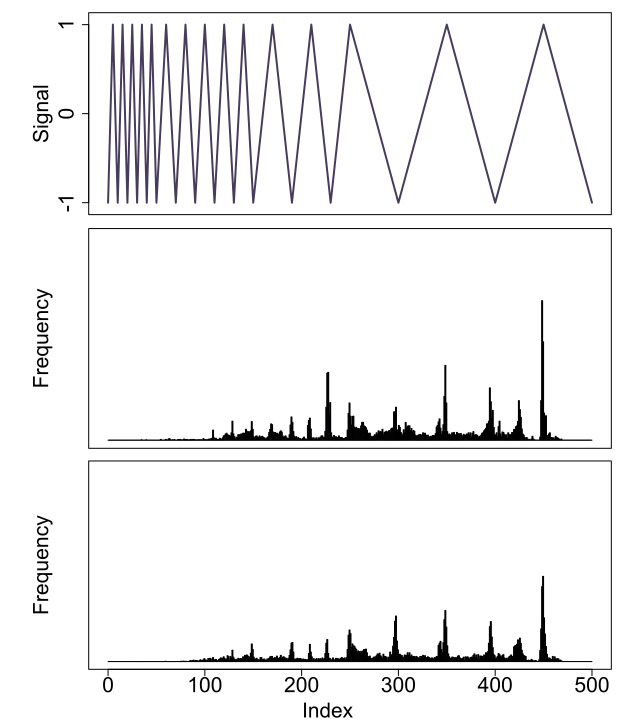

This section concerns developing a stopping criterion for the PRUTF algorithm. We provide tools for deriving a threshold value at which the PRUTF algorithm terminates the search if no values of dual variables exceed this threshold. Consider the dual variables at the first step of the algorithm, i.e. , for , which correspond to in (33) with . It turns out that is a stochastic process with local minima and maxima attained at the change points. This structure is displayed with cyan-colored lines ( ) in Figure 4 for both piecewise constant and piecewise linear signals. As the PRUTF algorithm detects more change points and forms the augmented boundary set , the local minima or maxima corresponding to these change points are removed from the stochastic process

| (41) |

for . This fact is shown by olive-colored lines ( ) in Figure 4. The last equality in (41) expresses that the is the stochastic term of the dual variables for all the interior coordinates and is derived by stacking the stochastic terms of the dual variables associated with -th block, , as defined in (33), for . This behaviour suggests a way to introduce a stopping rule for the PRUTF algorithm. As can be viewed from the orange-colored lines ( ) of Figure 4, if all true change points are captured by the algorithm and stored in the augmented set , the resulting process

contains no noticeable optimum points and tends to fluctuate close to the zero line (x-axis).

We terminate the search in Algorithm 1 at step by checking whether the maximum of , for , is smaller than a certain threshold. To exactly specify this threshold, as suggested by Theorem 1, we need to calculate the excursion probabilities of a Gaussian bridge process. As stated in Adler and Taylor, (2009), analytic formulas for the excursion probabilities are known to be available only for a small number of Gaussian processes. One of such Gaussian processes is the Brownian bridge process. It is well known that for the Brownian bridge process defined on the interval

| (42) |

See, for example, Adler and Taylor, (2009), and Shorack and Wellner, (2009). Hence for the piecewise constant signals, the required threshold for stopping Algorithm 1 can be obtained from (42), for a suitably chosen interval . That is, for a given value , we choose such that . Therefore, for and , , we stop Algorithm 1 at the iteration if

and .

For , the threshold is obtained in a similar fashion. Although the excursion probabilities for the Gaussian bridge processes are not known, we notice that by adopting the steps for the proof of (42) in Beghin and Orsingher, (1999), we can establish a similar formula for the Gaussian bridge process in Theorem 1 as

| (43) |

where , and the quantity is the -th diagonal element of the matrix

Hence, we stop Algorithm 1 at the iteration if

| (44) |

where is derived from the equation

| (45) |

6 Pattern Recovery and Theories

The main purpose of this section is to investigate whether the PRUTF algorithm can recover features of the true signal . We also demonstrate conditions under which the structure of the estimated signal matches the true signal . To verify the performance of PRUTF in the discovery the true signal, we first define what we mean by pattern recovery.

Definition 1

(Pattern Recovery): A trend filtering estimate recovers the pattern of the true signal if

| (46) |

where is the number of rows of matrix . We use the notation to briefly denote the pattern recovery feature of .

In the asymptotic framework, a trend filtering estimate is called pattern consistent if

| (47) |

where , to denote its dependency to the sample size . Pattern recovery is very similar to the concept of sign recovery in lasso (Zhao and Yu,, 2006; Wainwright,, 2009) as it deals with the specification of both locations of non-zero coefficients and their signs.

The problem of pattern recovery is studied for the special case of the fused lasso in several papers. Rinaldo et al., (2009) derived conditions under which fused lasso consistently identifies the true pattern. This was contradicted by Rojas and Wahlberg, (2014), who argued that fused lasso does not always succeed in discovering the exact change points. Rojas and Wahlberg, (2014) showed that fused lasso can be reformulated as the usual lasso, for which the necessary conditions for exact sign recovery have been established in the literature. Then, they proved that one such necessary condition, known as the irrepresentable condition, is not satisfied for the transformed lasso when there is a specific pattern called a staircase (Definition 2). Corrections to Rinaldo et al., (2009) were appeared in Rinaldo, (2014). Later on, Qian and Jia, (2016) proposed a method called puffer transformation, which is shown to be consistent in specifying the exact change points, including in the presence of staircases.

In the remaining part of this section, we use the dual variables to demonstrate the situations in which PRUTF can correctly recover the pattern of the true signal. Exact pattern recovery implies that the dual variables are comprised of consecutive bounded processes whose endpoints correspond to the true change points. The following lemma describes the situations in which exact pattern recovery can be attained. A particular case of this result in the context of piecewise constant signals was established in Rinaldo, (2014).

Theorem 2

Exact pattern recovery in PRUTF occurs when the discrete time processes , for , satisfy the following conditions simultaneously with probability one:

-

(a)

First block constraint: for ,

(48) -

(b)

Last Block constraint: for ,

(49) -

(c)

Interior Block constraints: for , if

(50) (51) and if , which corresponds to a staircase block, or .

In the foregoing equations, is a vector of size whose elements are all 1. A proof of the theorem is given in Appendix A.2.

We analyze the performance of the PRUTF algorithm in pattern recovery in two different scenarios; signals with staircase patterns and signals without staircase patterns. To our knowledge, Rojas and Wahlberg, (2014) was the first paper to carefully investigate the staircase pattern for the piecewise constant signals in the change points analysis setting. In Rojas and Wahlberg, (2014), a staircase pattern for a piecewise constant signal refers to the phenomenon of equal signs in two consecutive changes. We extend this concept to the general case, which covers any piecewise polynomial signals of order , by applying the penalty matrix .

Definition 2

Suppose that the true signal is a piecewise polynomial of order with change points at the locations . Moreover, let be blocks created by the change points in . A staircase occurs in block if

| (52) |

The following theorem investigates the consistency of PRUTF in pattern recovery, in both with and without staircases. Specifically, it shows that for a signal without a staircase, the exact pattern recovery conditions are satisfied with probability one. On the other hand, in the presence of staircases in the signal, the probability of these conditions holding, which is equivalent to the probability of a Gaussian bridge process never crossing the zero line, converges to zero.

In the literature, the consistency of a change point method is usually characterized by the signal size , the number of change points , the noise variance , the minimal spacing between change points,

and the minimum magnitude of jumps between change points,

All the above quantities are allowed to change as grows.

In the following, we present our main theorem providing conditions under which the output of the PRUTF algorithm consistently recovers the pattern of the true signal .

Theorem 3

Suppose that follows the model in (1). Let be the set of change points for the true signal . Additionally, assume that and are the set of change points estimates and the corresponding signal estimate obtained by the PRUTF algorithm, respectively. The followings hold for the PRUTF algorithm.

-

(a)

Non-staircase Blocks: Suppose there is no staircase block in the true signal . For some and with

if the conditions

-

•

(53) -

•

(54)

hold, then the PRUTF algorithm guarantees exact pattern recovery with probability approaching one. That is,

-

•

-

(b)

Staircase Blocks: On the other hand, if the true signal contains at least one staircase block, then the probability of exact pattern recovery by the PRUTF algorithm converges to zero. That is,

A proof is given in Appendix A.3.

Remark 7

The performance of PRUTF in terms of consistent pattern recovery relies on the quantity and the choice of . In the piecewise constant case, the former quantity reduces to the well-known signal-to-noise-ratio quantity, which is crucial for a consistent change point estimation (Fryzlewicz et al.,, 2014; Wang et al.,, 2020). The statements in 53 illustrate that the consistency of PRUTF in non-staircase blocks is achievable if the quantity is of order , for some . In addition, the number of the change points is allowed to diverge, provided

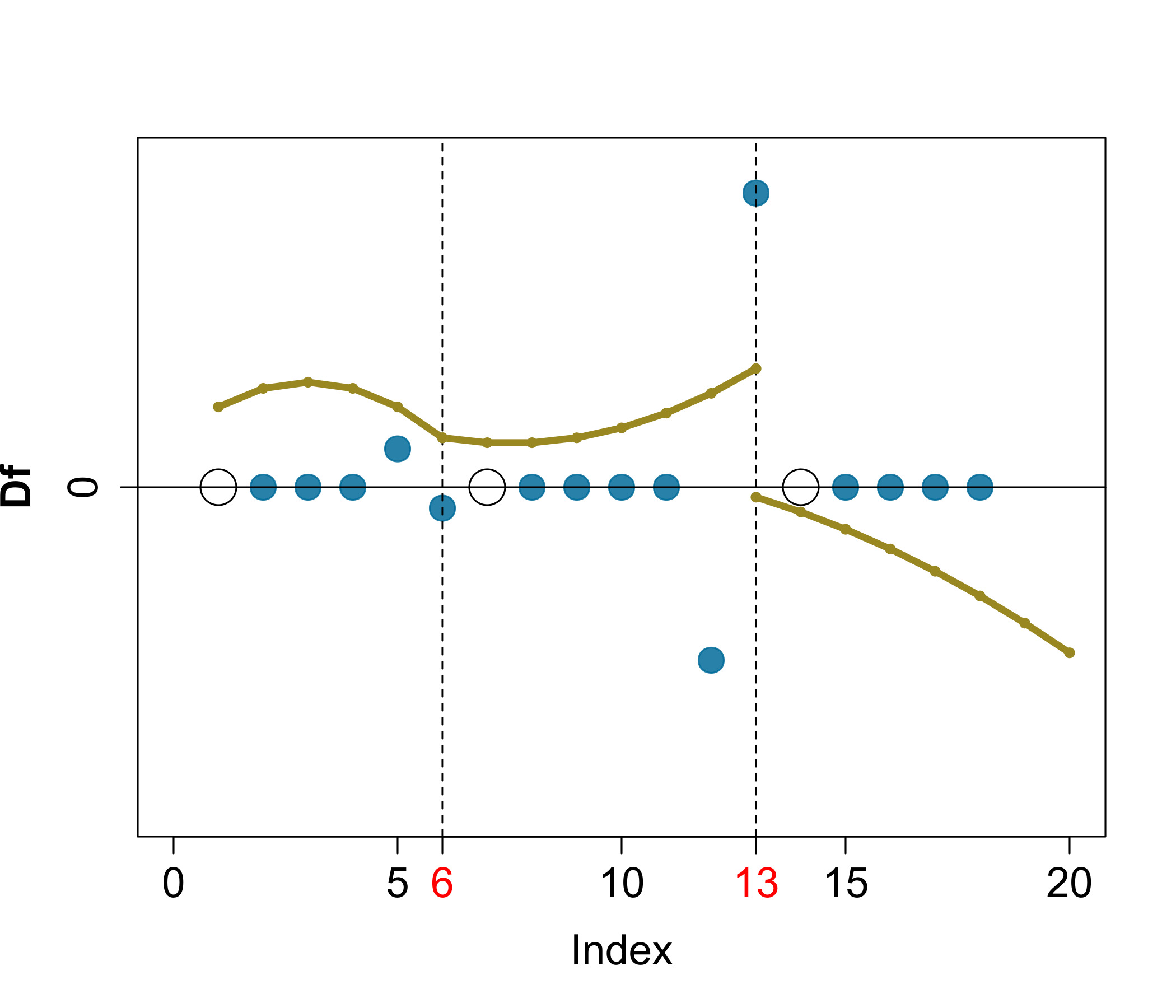

The drift term (34) plays a key role in assessing the performance of PRUTF in pattern recovery. From (23), this drift for a staircase block becomes , which is constant in for the entire block. Consequently, the interior dual variables for the staircase block contain only the stochastic term , which fluctuates around the line . Recall that the KKT conditions for the dual problem of trend filtering require to stay within the lines and . Thus, for a signal with staircase patterns, the PRUTF algorithm is sensitive to the variability of random noises and identifies change points once touches the boundaries. Examples of piecewise constant and piecewise linear signals, along with their corresponding dual variables, are depicted in Figure 5, in which the above argument can be clearly seen.

According to Theorem 3, if there is no staircase pattern in the underlying signal, the PRUTF algorithm consistently estimates the true signal, and fails to do so, otherwise. Given the results in Theorem 3, the natural question is whether Algorithm 1 could be modified to enjoy the consistent pattern recovery in any case. In the next section, we will present an effective remedy based on altering the sign of a change associated with a staircase block.

7 Modified PRUTF Algorithm

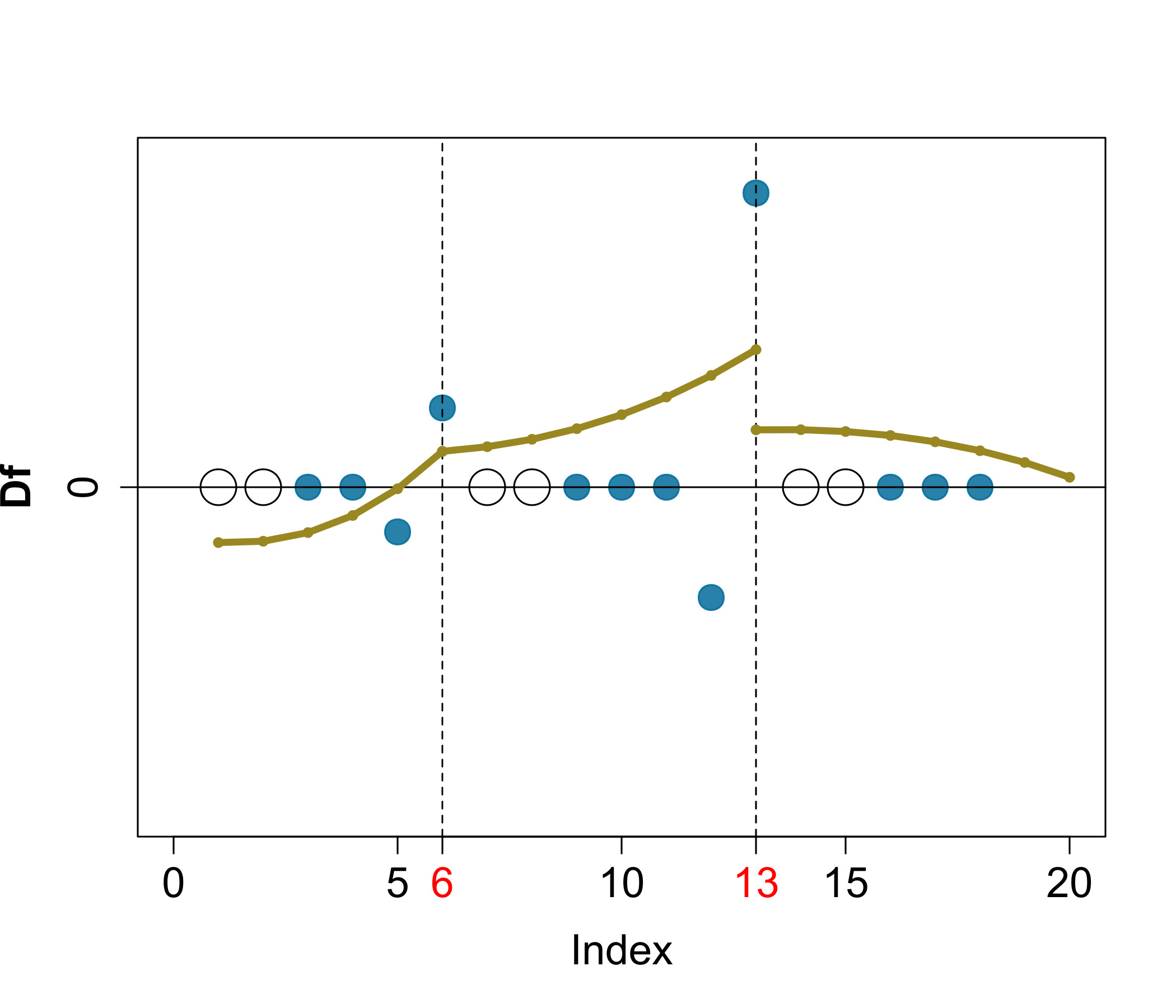

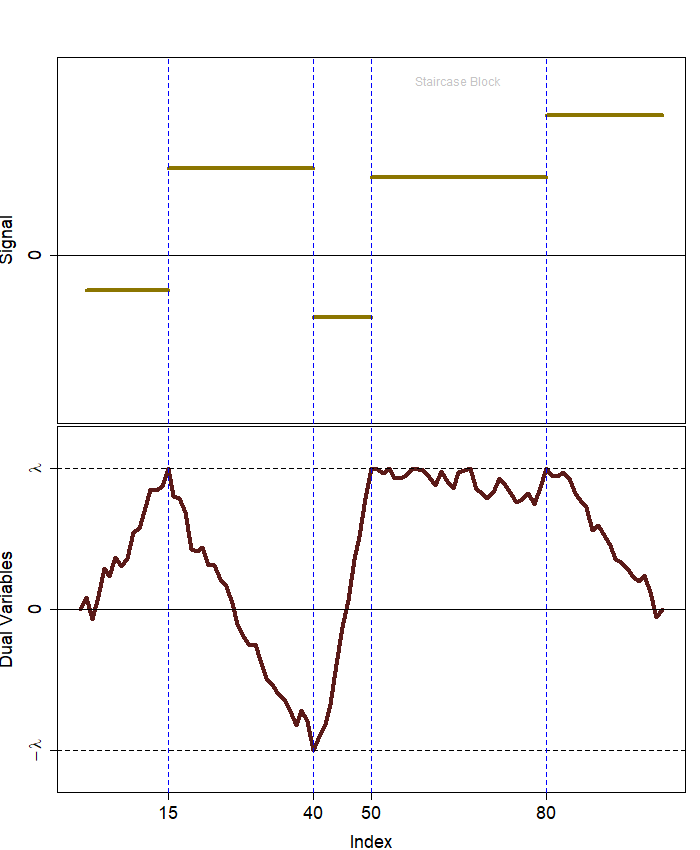

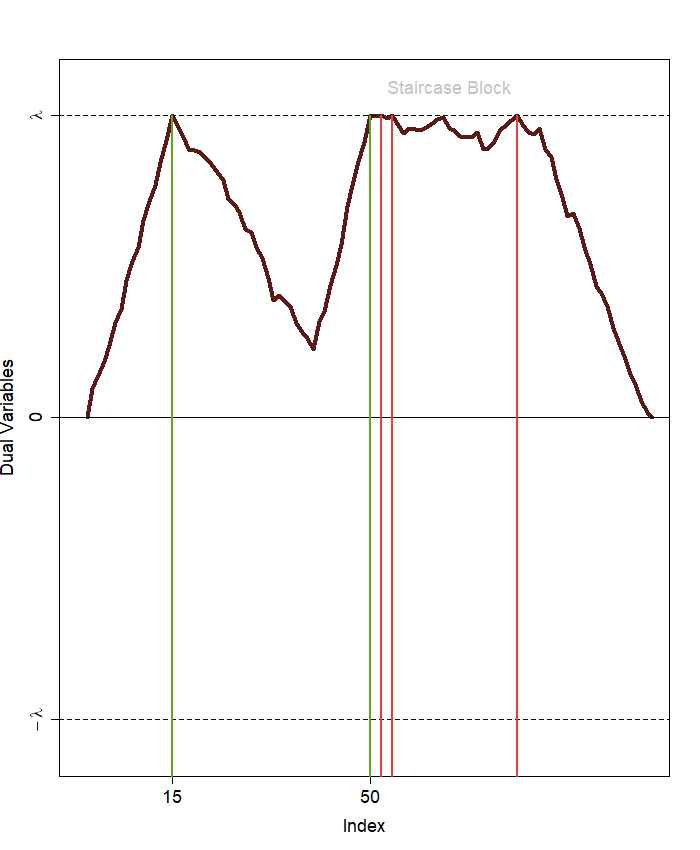

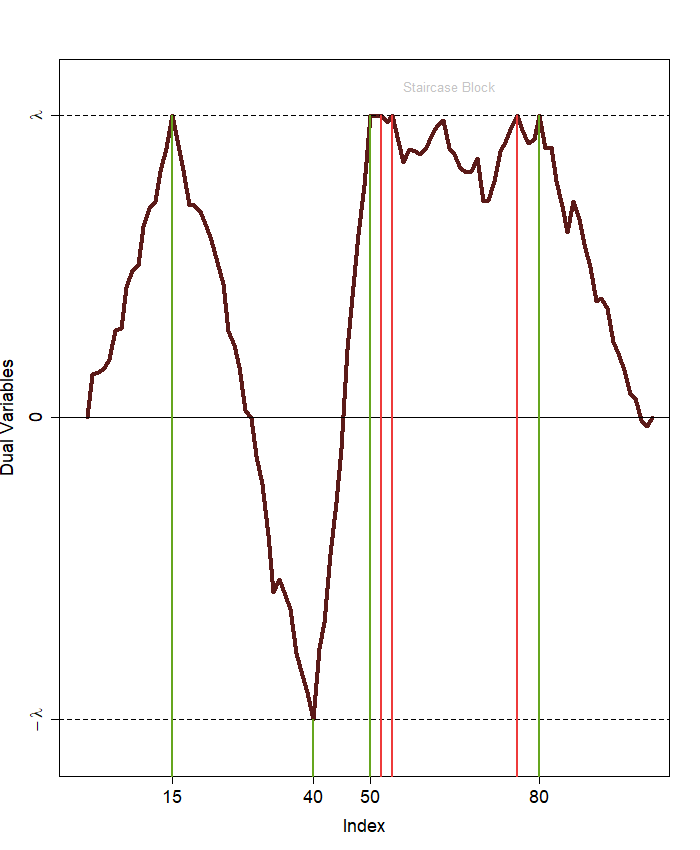

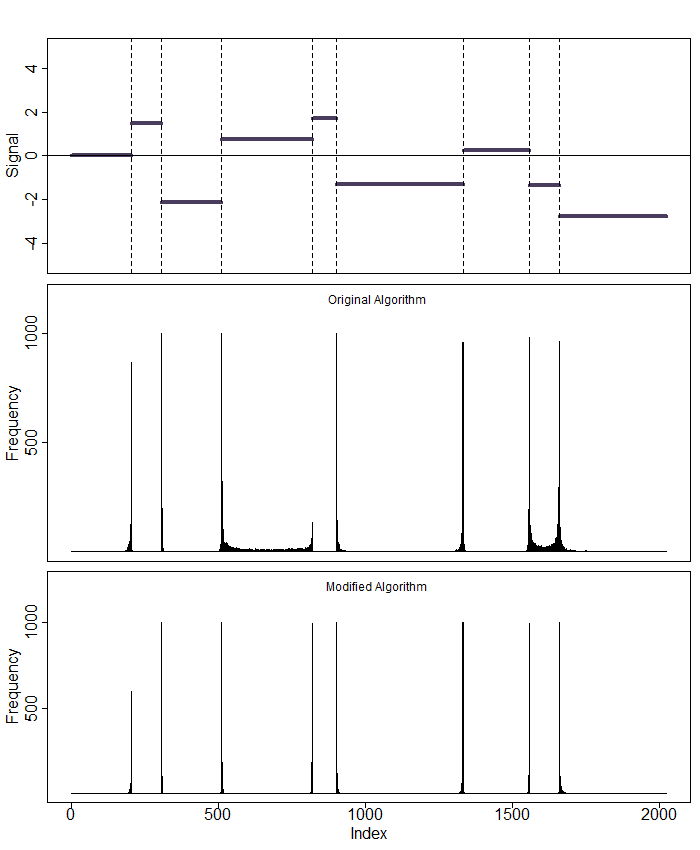

In this section, we attempt to modify the PRUTF algorithm in such a way that it produces consistent estimates of the number and locations of change points even in the presence of staircase patterns. As previously mentioned, for a staircase block, the drift term (34) is constant and leads to false discoveries in change points. This is shown in Figure 6 with a piecewise constant signal of size and the true change points at . The figure reveals that the staircase block leads to three false discoveries at the locations 52, 54 and 76.

The inconsistency of PRUTF in the presence of a staircase as established in Theorem 3, stems from the fact that the change signs of the two consecutive change points at both ends of the staircase block are identical. That is, for the staircase block , . Therefore, a question arises: can we modify Algorithm 1 in such a way that the change signs of two neighbouring change points never become equal but still yield the solution path of trend filtering? We suggest a simple but very efficient solution to the above question.

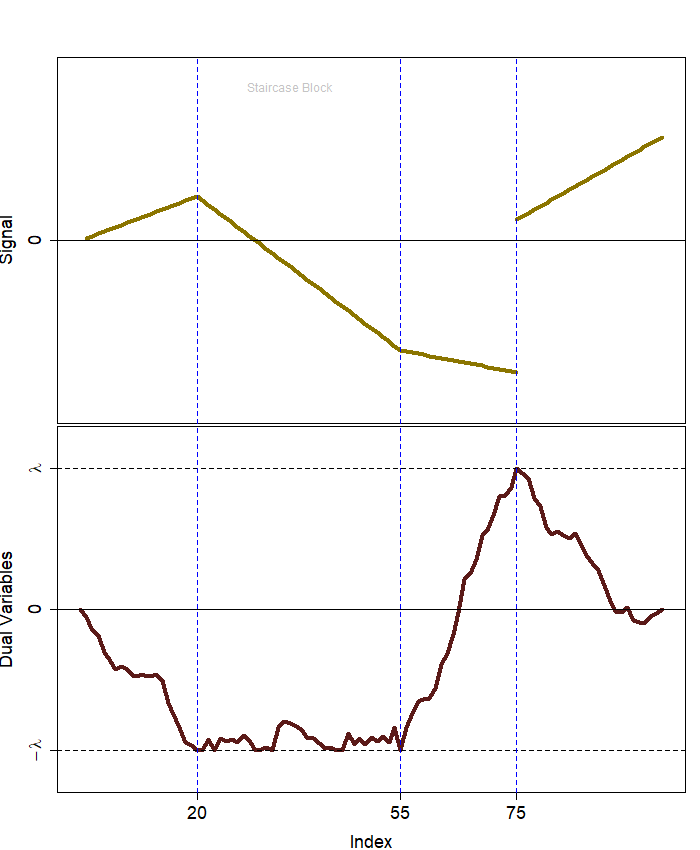

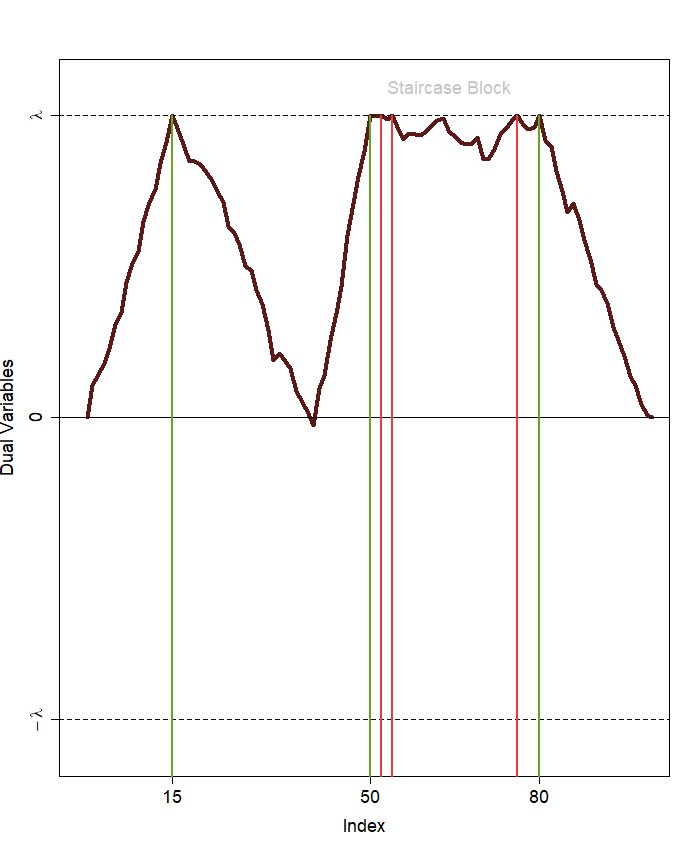

Once a new change point is identified, we check whether its -th order difference sign is the same as that of the change points right before and after. If these change signs are not identical, then the procedure continues to search for the next change point. Otherwise, we replace the sign of the neighbouring change point with zero. This replacement of the sign prevents the drift term (34) from becoming zero. This idea is implemented for the above signal, and the result is displayed in Figure 7. As shown in panel (b), the sign of the first change point at location 50 is set to zero since its sign is identical to the sign of the second change point at 15. This sign replacement vanishes false discoveries appeared in panel (b) of Figure 6.

Based on the above argument, PRUTF presented in Algorithm 1 can be modified as follows to avoid false discovery and to produce consistent pattern recovery.

Algorithm 2 (mPRUTF)

-

1.

Execute steps 1 and 2 of Algorithm 1.

-

2.

-

(a)

Execute part (a) of step 3 in Algorithm 1 to obtain and its sign . At this point, the algorithm checks whether is identical to the signs of the change points just before and after . If so, set the sign of change point which is identical to to zero. Then, repeat part (a) of step 3 again to obtain new and and update the sets and .

-

(b)

Execute parts and of step 3 in Algorithm 1.

-

(a)

-

3.

Repeat step 3 until either or a stopping rule is met.

The modified PRUTF (mPRUTF) algorithm produces consistent change point estimations, even in the presence of staircase patterns. This consistency has been achieved by converting the staircase patterns to non-staircase patterns that avoid false change point detection. In other words, running mPRUTF on an arbitrary signal (with or without staircases) is equivalent to running PRUTF on a signal without any staircase; see Figures 6 and 7. Thus, from part (a) of Theorem 3, the mPRUTF algorithm is consistent in pattern recovery.

Remark 8

In step 2, part (a) of the mPRUTF algorithm, presented in Algorithm 2, it is impossible for the sign of the new change point to be identical to the sign of both of its immediate neighbouring change points, because the algorithm has already checked the equality of signs at previous steps. If they are equal, the sign of the immediate neighbouring change point will be set to zero.

Recall that the KKT optimality conditions for solutions of the trend filtering problem in (5) requires the dual variables to be less than or equal to in absolute values, i.e., . This condition still holds when we replace the sign values ( or ) with 0. Consequently, we have the following theorem.

Theorem 4

The mPRUTF algorithm presented in Algorithm 2 is a solution path of trend filtering.

For brevity, we do not provide the proof of Theorem 4 here. We refer the reader to the similar arguments for the LARS algorithm of lasso in Tibshirani et al., (2013).

It is worth pointing out that the mPRUTF algorithm requires slightly more computation than the original PRUTF algorithm. The increase in computation time directly depends on the number of staircase blocks in the underlying signal. To show how mPRUTF resolves the problem of false discovery in signals with staircases, we ran both algorithms for 1000 generated datasets from a piecewise constant and piecewise linear signals. The frequency plot of the estimated change points for both algorithms are represented in Figure 8. The figure reveals that the original algorithm produces false discoveries within staircase blocks for both signals, whereas mPRUTF resolves this issue.

8 Numerical Studies

In this section, we provide numerical studies to demonstrate the effectiveness and performance of our proposed algorithm, mPRUTF . We begin with a simulation study and then provide real data analyses.

8.1 Simulation Study

In this section, we investigate the performance of our proposed method, mPRUTF, by a simulation study. We consider two scenarios, namely piecewise constant and piecewise linear signals with staircase patterns. We compare our method to some powerful state-of-the-art approaches in change point analysis. These methods, a list of their available packages on CRAN, and their applicability for different scenarios are listed in Table 1.

| Method | Reference | R Package | Signal | |||||

|---|---|---|---|---|---|---|---|---|

| PWC | PWL | |||||||

| PELT | Killick et al., (2012) | changepoint | ✓ | ✕ | ||||

| WBS | Fryzlewicz et al., (2014) | wbs | ✓ | ✕ | ||||

| SMUCE | Frick et al., (2014) | stepR | ✓ | ✕ | ||||

| NOT | Baranowski et al., (2019) | not | ✓ | ✓ | ||||

| ID | Anastasiou and Fryzlewicz, (2019) | IDetect | ✓ | ✓ | ||||

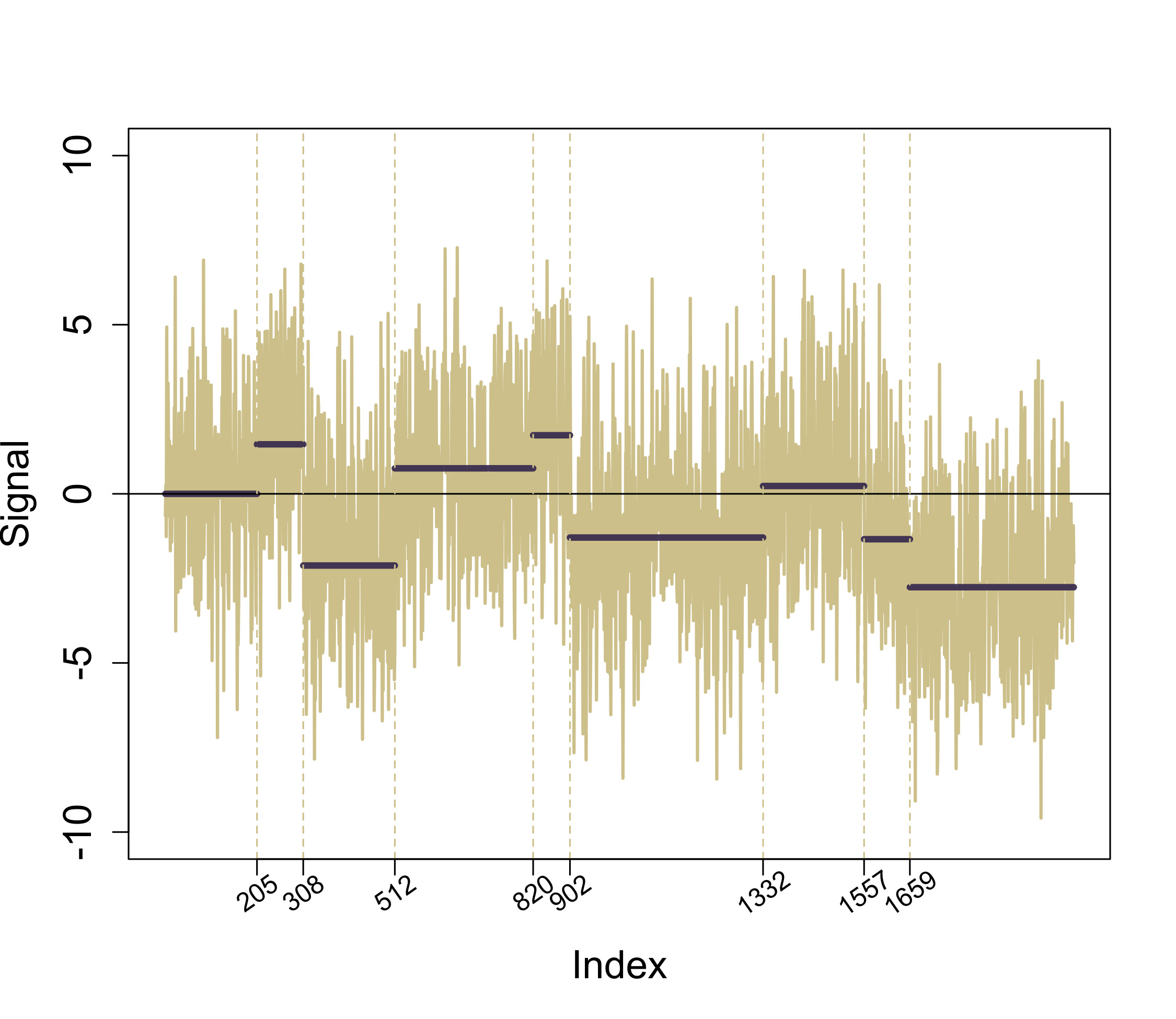

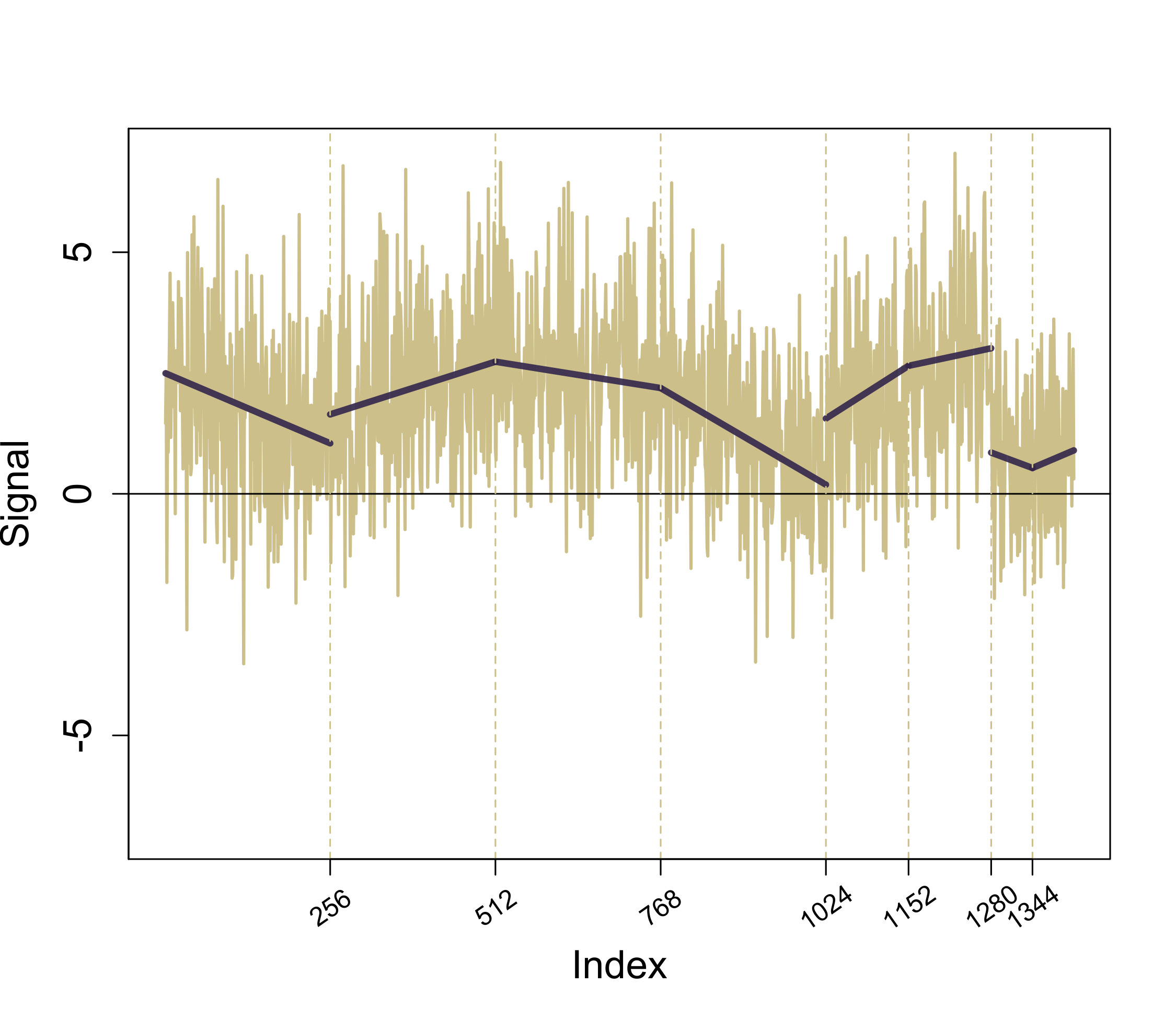

We have adopted the simulation setting of Baranowski et al., (2019), and consider piecewise constant and piecewise linear signals as follows.

-

(i)

A piecewise constant signal (PWC) of size with the number of change points . The locations of the true change points are 205, 308, 512, 820, 902, 1332, 1557, 1659 with jump sizes 1.464, -0.656, 0.098, 1.830, 0.537, 0.768, -0.574, -3.335. We set the starting intercept to 0.

-

(ii)

A piecewise linear signal (PWL) of size and the number of change points . The true change points are located at 256, 512, 768, 1024, 1152, 1280, 1344. The corresponding intercepts and slopes for 8 created blocks by are 0.111, 0.553, -0.481, 3.002, -7.169, -0.030, 7.217, -0.958 and -8, 6, -3, -11, 12, 4, -7, 8, respectively.

Figure 9 displays the true PWC and PWL signals, with their representative datasets generated using model (1). We note that both PWC and PWL signals contain two staircase blocks. These blocks for the PWC signal are , and for PWL signal are and .

We apply mPRUTF presented in Algorithm 2 to estimate the number and the locations of the change points for the PWC and PWL signals. In each iteration of the simulation study, we simulate a dataset according to model (1) under the assumption that the error terms are independently and identically distributed as . Moreover, we set the significance level to for the stopping rule in (44).

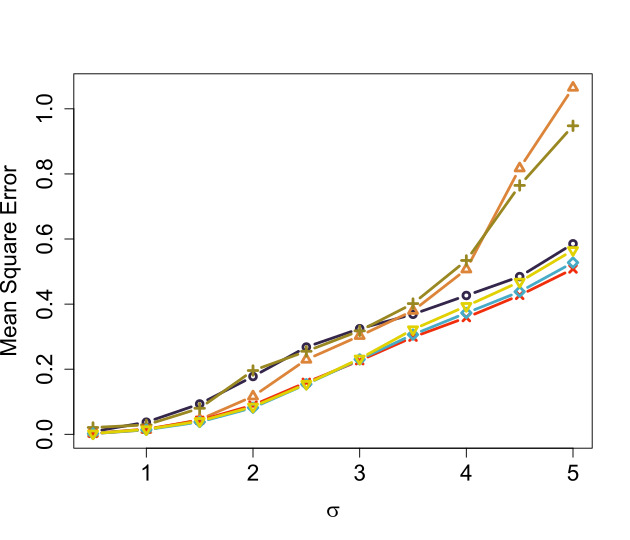

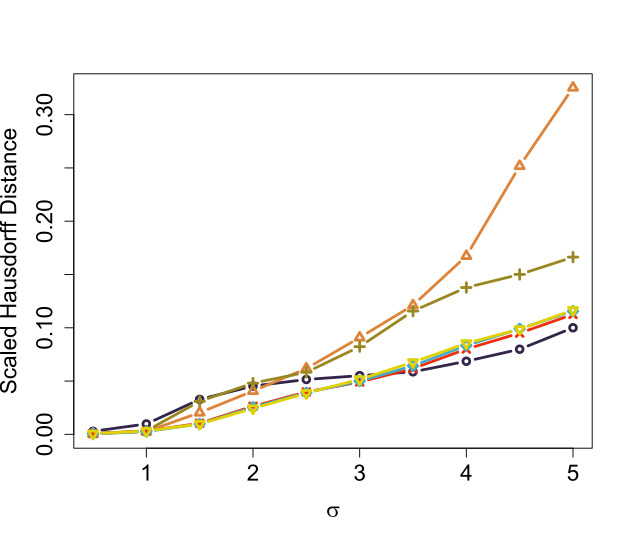

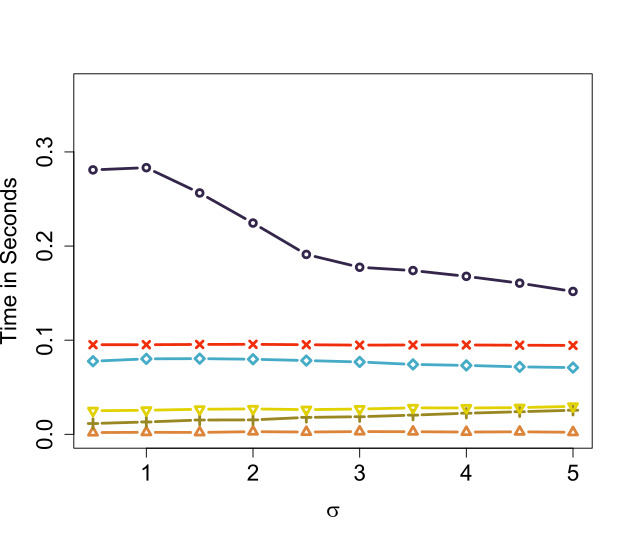

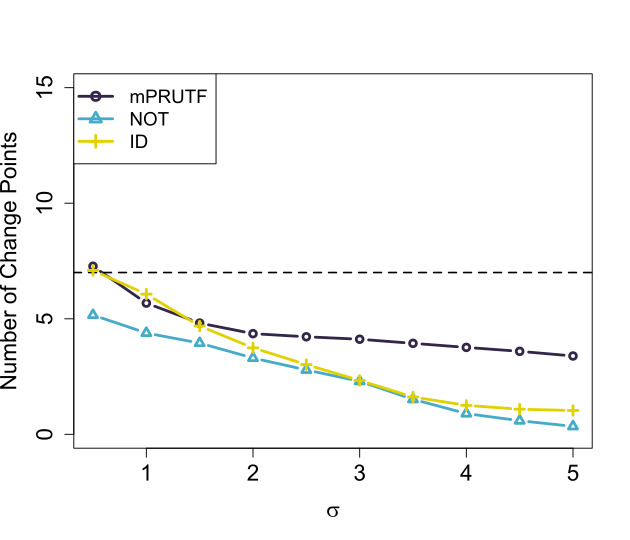

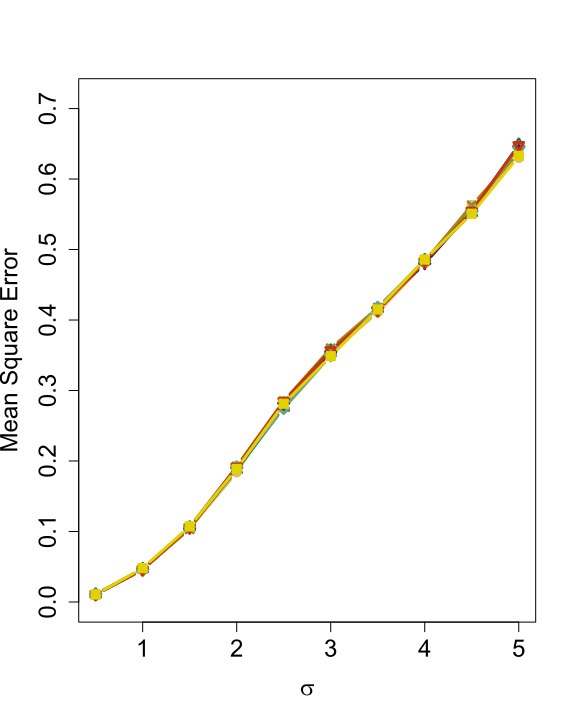

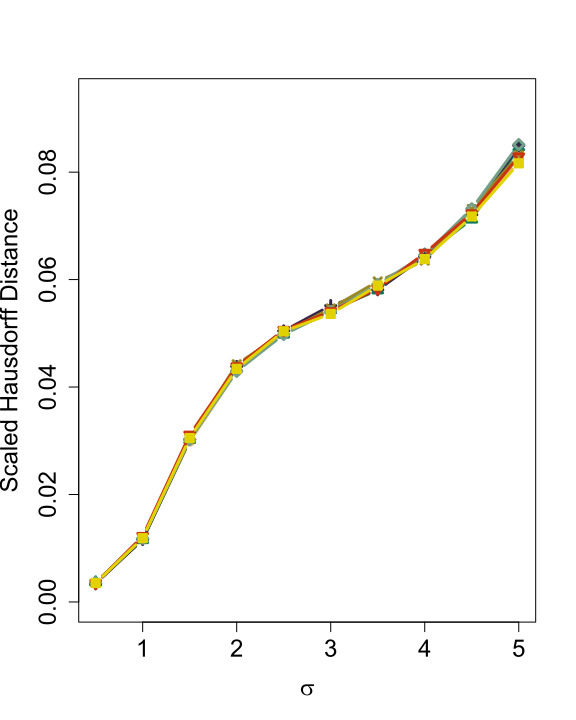

In order to explore the impact of different noise levels on the change point methods, we run each simulation for various values of in . We run the simulation times and report the results for each change point technique in terms of estimates of the number of change points, estimates of the mean square error given by , estimates of the scaled Hausdorff distance given by

and the computation time in seconds. These quantities are frequently used to assess the performance of a change point detection technique in the literature, for example, see Baranowski et al., (2019), Anastasiou and Fryzlewicz, (2019). The signal estimate, , is computed by the least square fit of a polynomial of order to the observations within segments created by each change point method. We also remark that the tuning parameters and stopping criteria for the methods listed in Table 1 are set to the default values by the packages.

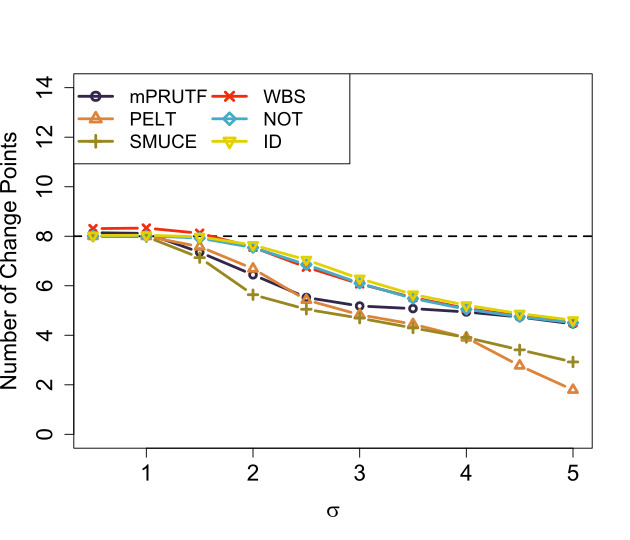

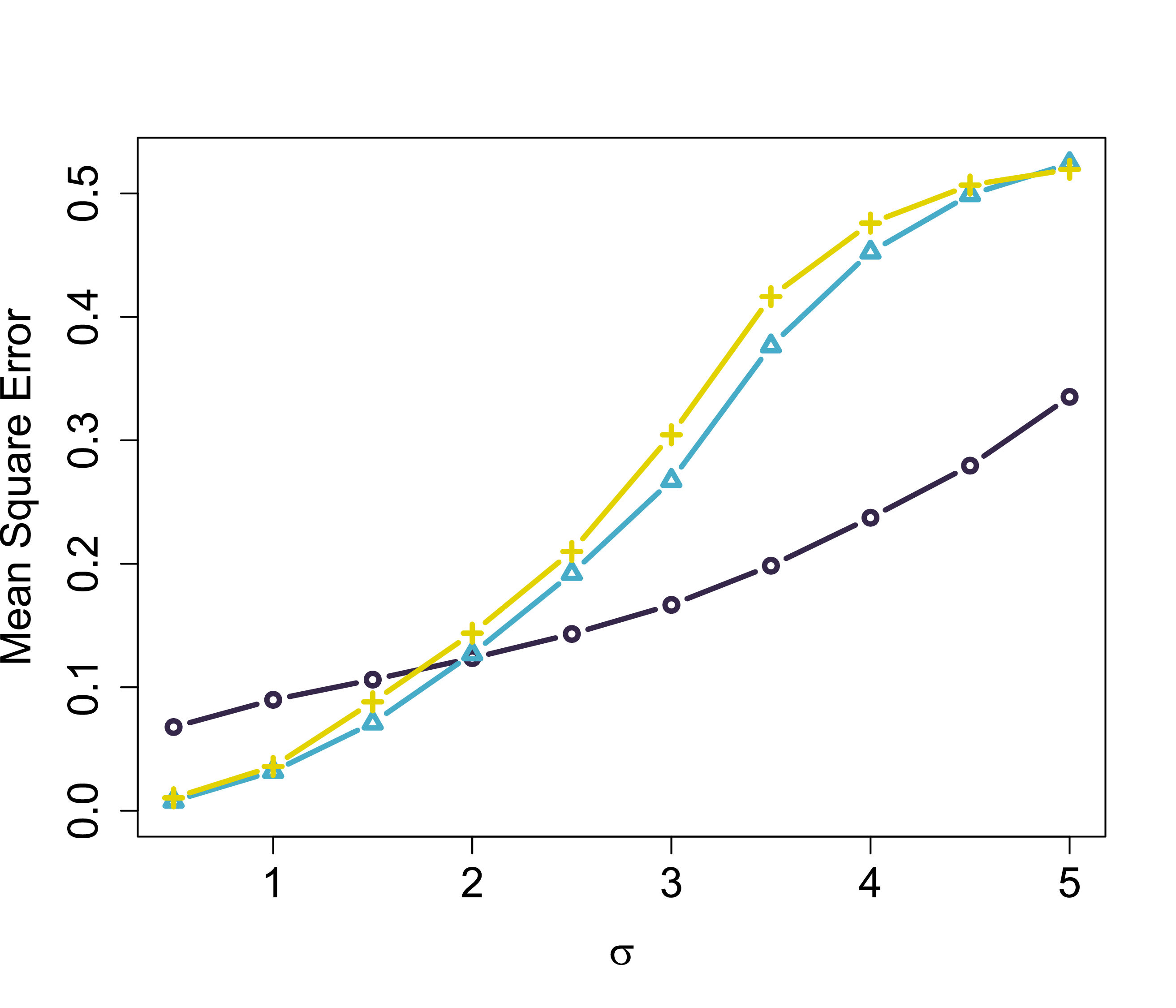

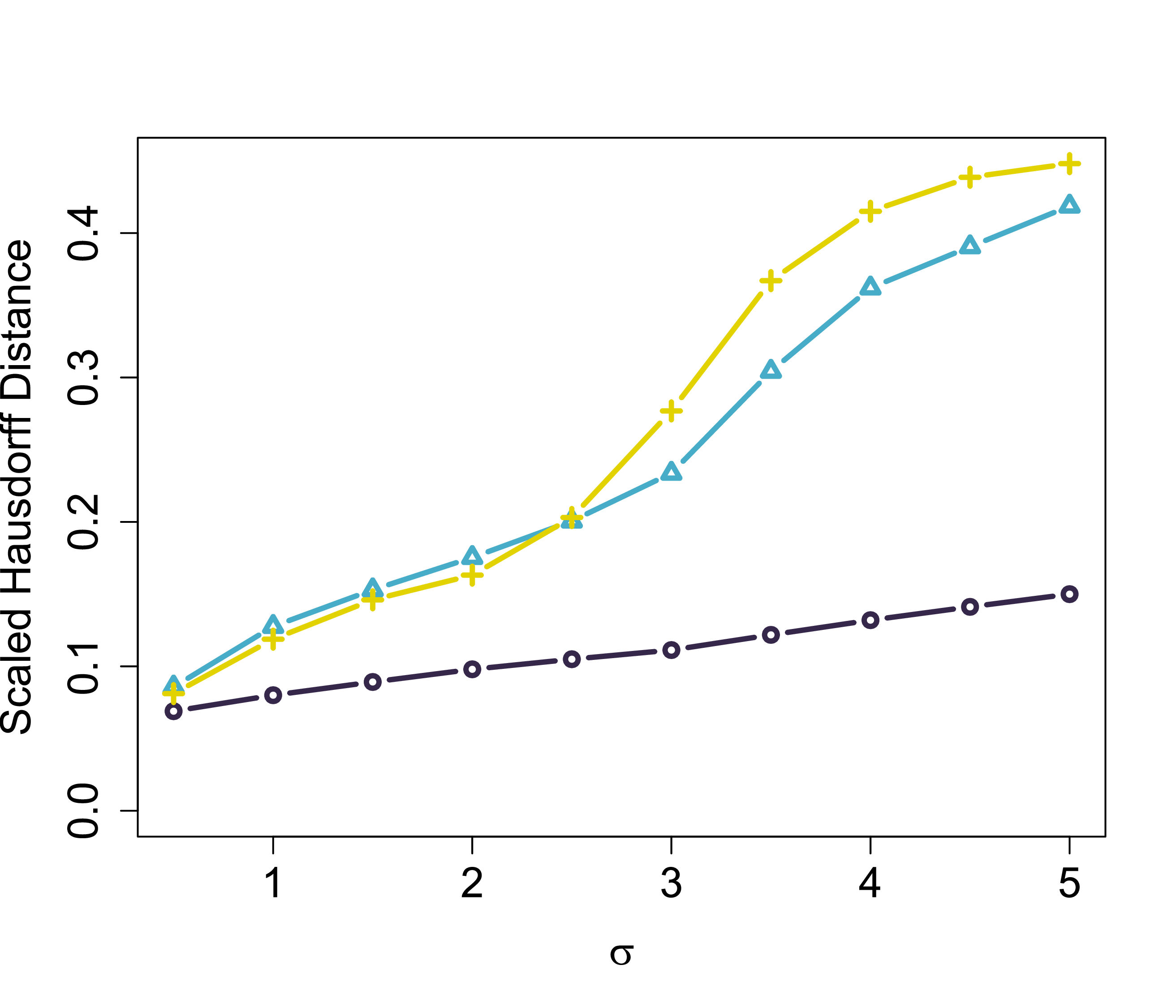

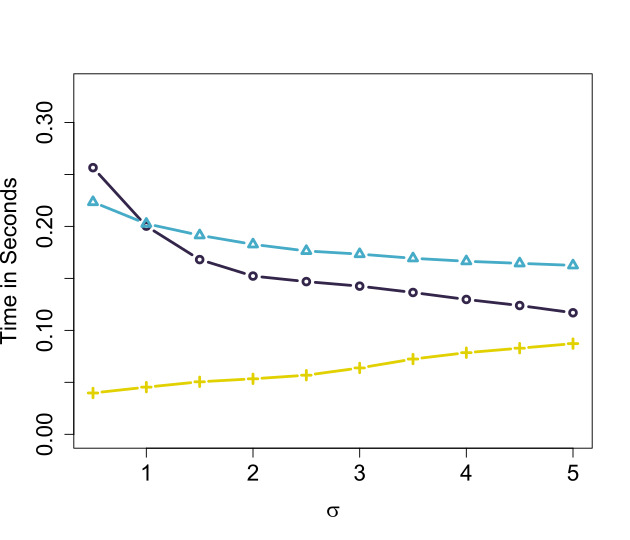

The results for the PWC and PWL signals are presented in Figures 10 and 11, respectively. In the case of piecewise constant signal, as in Figure 10, mPRUTF performs comparable to PELT and SMUCE in terms of the average number of change points, MSE and the scaled Hausdorff distance up to , and outperforms them as increases. For , similar performance to WBS, NOT and ID is viewed from these measurements. As indicated by the average number of change points, MSE and the scaled Hausdorff distance, WBS, NOT and ID outperform the other methods in almost all noise levels. From a computational point of view, mPRUTF takes a slightly longer time, mainly due to the matrix multiplications, however, this computation time decreases as noise level increases. As in panel (d) of Figure 10, the methods PELT, SMUCE and ID are the fastest ones.

In the case of piecewise linear signal, mPRUTF is only compared to NOT and ID methods, which are applicable to the piecewise polynomials of order . As in Figure 11 mPRUTF outperforms both NOT and ID in terms of the average number of change points and the scaled Hausdorff distance for all noise levels. In terms of MES, mPRUTF outperforms the other two for . As shown in Panel (d) of Figure 11, the computation time of mPRUTF ranks second after ID.

The mPRUTF method performs well in terms of the estimation of the number of change points, their locations, as well as the true signals. In fact, simulation results for most of the scenarios indicate that mPRUTF is among the most competitive change point detection approaches in the literature.

8.2 Real Data Analysis

In this section, we have analyzed UK HPI and GISTEMP and COVID-19 datasets, using our proposed algorithm. Because is unknown for these real datasets, we applied median absolute deviation (MAD) proposed by Hampel, (1974), to robustly estimate . More specifically, a MAD estimate of for piecewise constant signals is given by and for piecewise linear signals by , where represents the inverse cumulative density function of the standard normal distribution.

Example 1 (UK HPI Data)

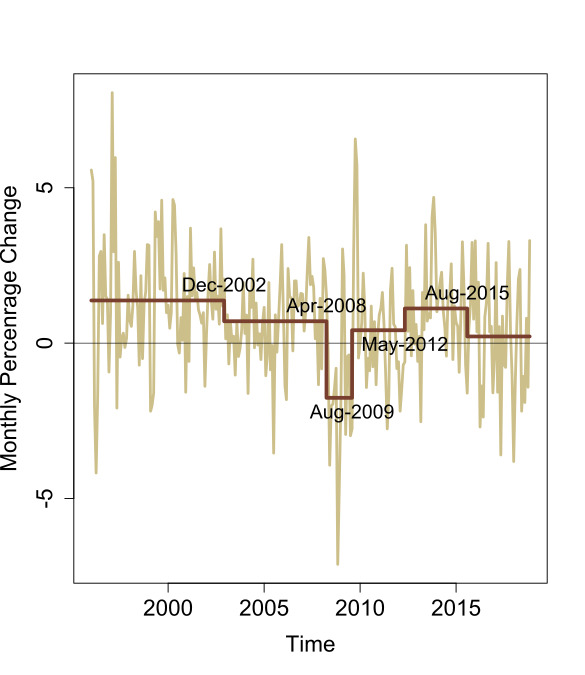

The UK House Price Index (HPI) is a National Statistic that shows changes in the value of residential properties in England, Scotland, Wales and Northern Ireland. The HPI measures the price changes of residential housing by calculating the price of completed houses sale transactions as a percentage change from some specific start date. The UK HPI uses the hedonic regression model as a statistical approach to produce estimates of the change in house prices for each period. For more details, see https://landregistry.data.gov.uk/app/ukhpi.Many researchers, including Fryzlewicz, (2018), Fryzlewicz et al., (2018) and Anastasiou and Fryzlewicz, (2019), have studied the UK HPI dataset in carrying out change point analysis. In the current study, we consider monthly percentage changes in the UK HPI at Tower Hamlets (an east borough of London) from January 1996 to November 2018.

We have applied the mPRUTF algorithm to the dataset. The algorithm have found five change points located at the dates December 2002, April 2008 and August 2009 (may be attributed to the Credit Crunch and Financial Crises), May 2012 (may be attributed to The London 2012 Summer Olympics) and August 2015 (may be attributed to regulatory and tax changes, and also by lower net migration from the EU). The dataset, the change points derived by mPRUTF and its piecewise constant fit are presented in panel (a) of Figure 12.

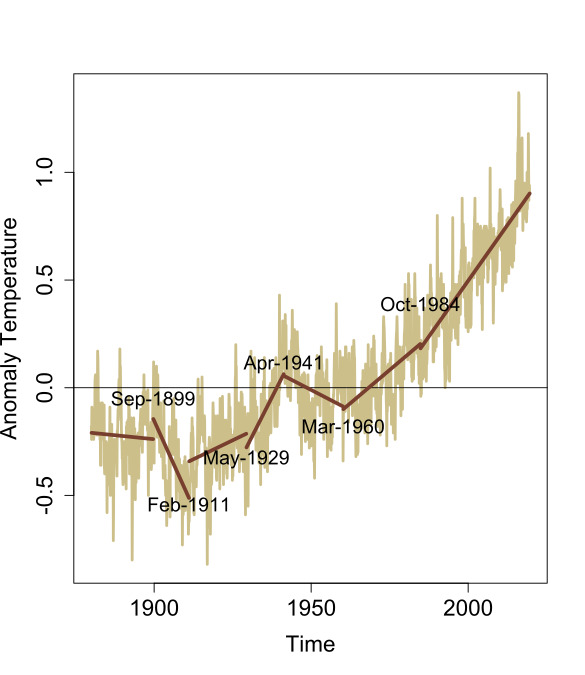

Example 2 (GISTEMP Data)

The Goddard Institute for Space Studies (GISS) monitors broad global changes around the world. The GISS Surface Temperature Analysis (GISTEMP) is an estimate of the global surface temperature changes (see https://www.giss.nasa.gov). In the analysis of GISTEMP data, the temperature anomalies are used rather than the actual temperatures. A temperature anomaly is a difference from an average or baseline temperature. The baseline temperature is typically computed by averaging thirty or more years of temperature data (1951 to 1980 in the current dataset). A positive anomaly indicates the observed temperature was warmer than the baseline, while a negative anomaly indicates the observed temperature was cooler than the baseline. For more details see Hansen et al., (2010) and Lenssen et al., (2019).

The GISTEMP dataset has been frequently explored in change point literature, for example see Ruggieri, (2013), James and Matteson, (2015) and Baranowski et al., (2019). Panel (b) of Figure 12 displays the monthly land-ocean temperature anomalies recorded from January 1880 to August 2019 (see https://data.giss.nasa.gov/gistemp). The plot reveals the presence of a linear trend with several change points in the dataset. For this dataset, we have identified six change points using mPRUTF located in September 1899, February 1911, May 1929, April 1941, March 1960, October 1984. The locations of change points and an estimate of the piecewise linear signal are presented in panel (b) of Figure 12.

Example 3 (COVID-19 Data)

Since the initial outbreak of Novel Coronavirus Disease 2019 (COVID-19) in Wuhan, China, in mid-November 2019, the virus has rapidly spread throughout the world. The pandemic has infected 21.26 million people and killed more than 761,000 https://covid19.who.int/, greatly stressing public health systems and adversely influencing global society and economies. Therefore, every country has attempted to slow down the transmission rate by various regional and national policies such as the declaration of national emergencies, quarantines and mass testing. Of vital interest to governments is understanding the pattern of the epidemic growth and assessing the effectiveness of policies undertaken. A scientist can investigate these matters by analyzing the sequence of infection data for COVID-19. Changepoint detection is one possible framework for studying the behaviour of COVID-19 infection curves. By detecting the locations of alterations in the curves, change point analysis gives us insights into changes in the transmission rate or efficiency of interventions. It also enables us to raise warning signals if the disease pattern changes.

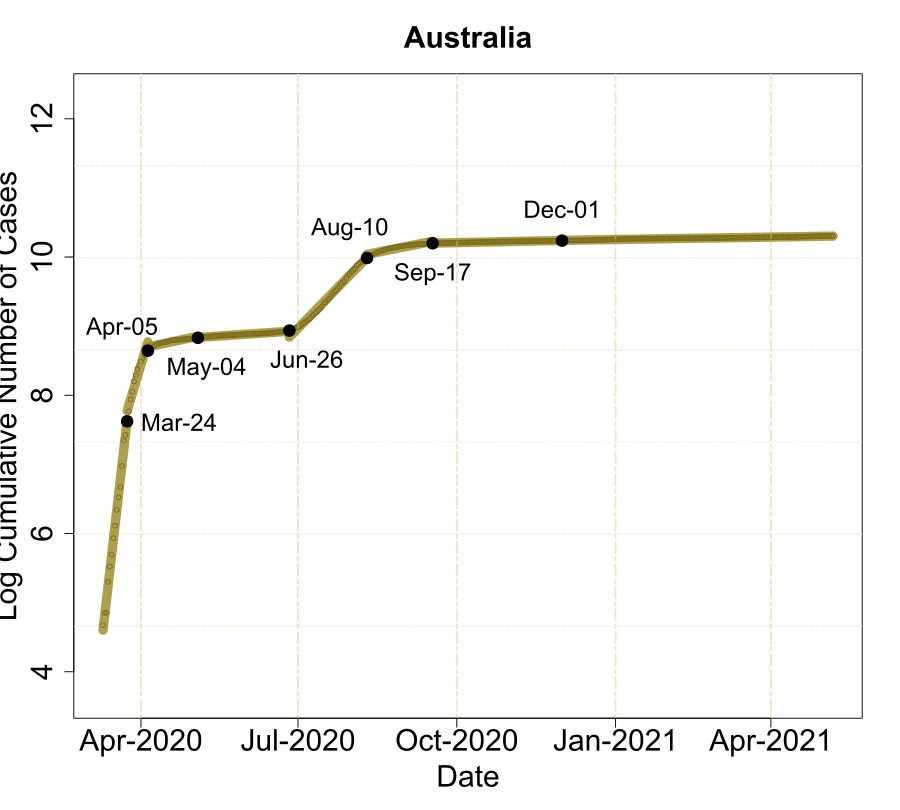

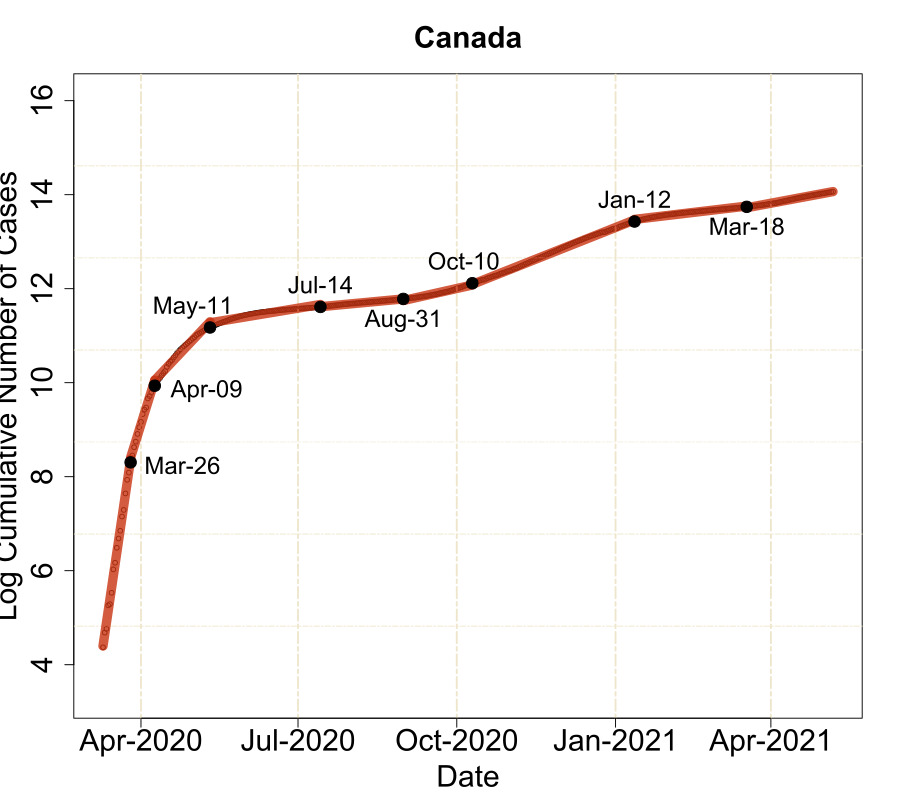

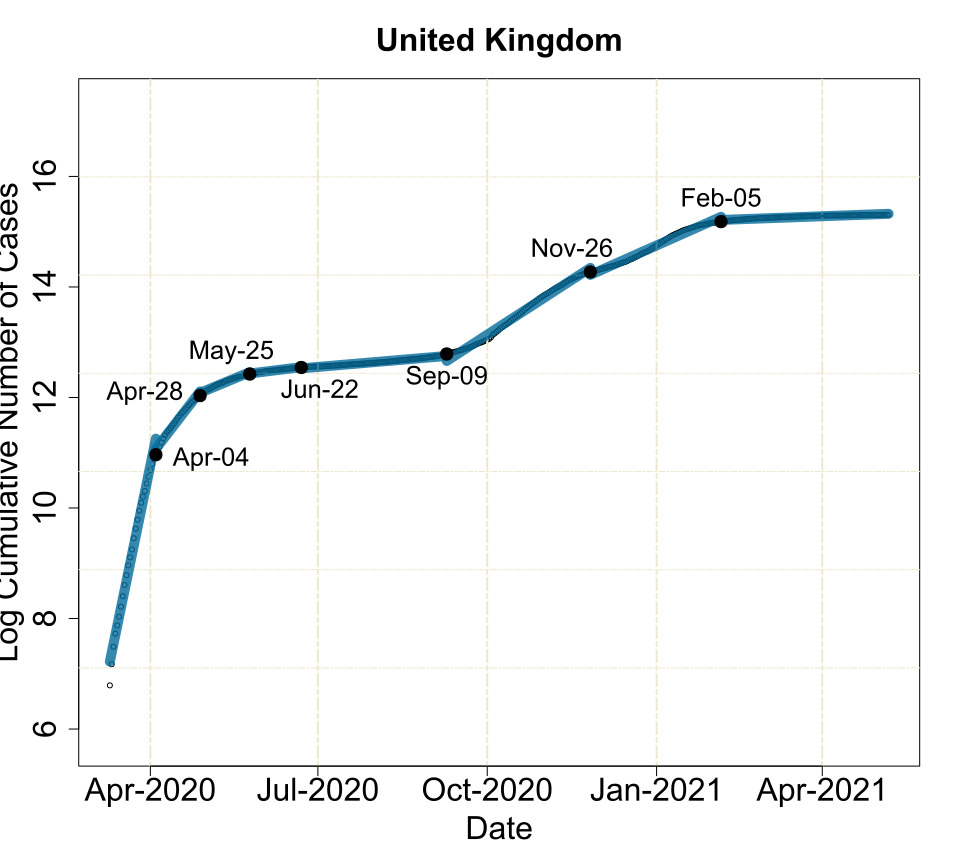

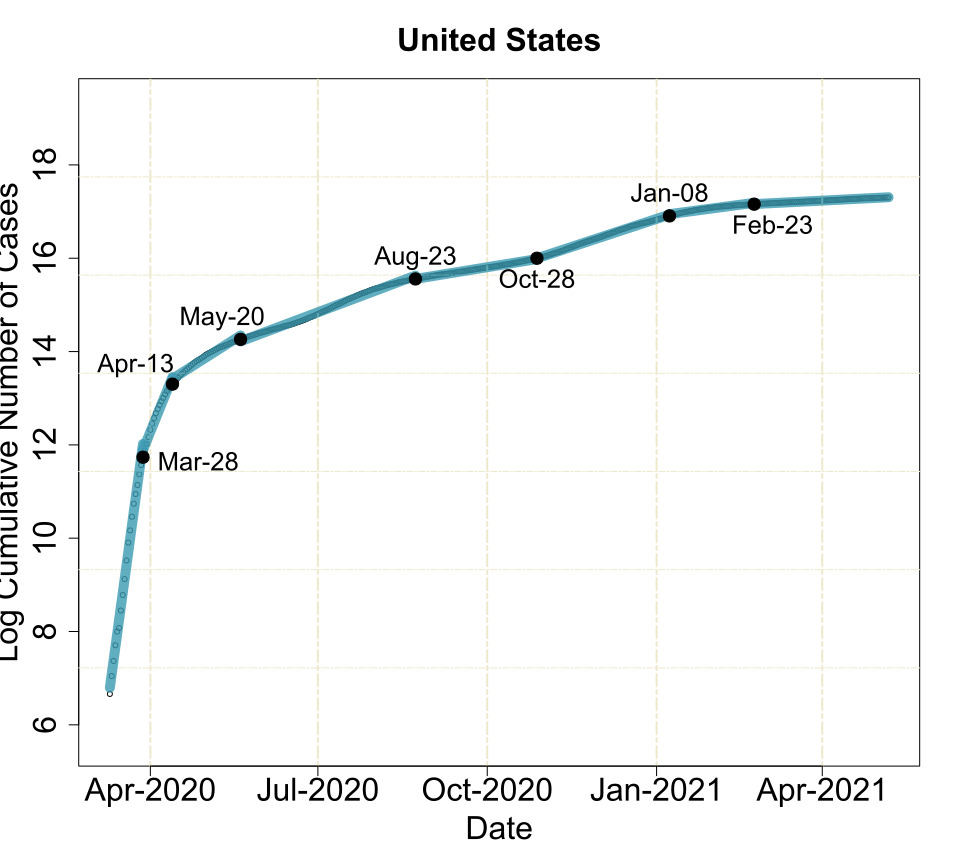

For this example, we consider the log-scale of the cumulative number of confirmed cases for Australia, Canada, the United Kingdom and the United States, during the period March 10, 2020 through April 30, 2021. We have applied mPRUTF to detect change points that have occurred in the data for each country. We then fitted a piecewise linear model to the data using the selected change points, which provides a more direct perception of how the growth rate changes over time.

Figure 13 displays the locations of change points detected by the mPRUTF algorithm as well as the estimated linear trends for the four countries. For example, our algorithm has identified eight change points for Canada, on March 26, 2020; April 9, 2020; May 11, 2020; July 14, 2020; August 31, 2020; October 10, 2020; January 12, 2021 and March 18, 2021. The figure shows segments created by the estimated change points as well as their growth rate. The growth rate for the first segment (from March 10, 2020 to March 26, 2020) is remarkably high, but starts to slightly decline after the first change point on March 26, 2020. This mild decline may be linked to the declaration of the the state of emergency, quarantine and international travel ban declared by the Government of Canada. The third segment (from April 9, 2020 to May 11, 2020), the fourth segment (from May 11, 2020 to July 14, 2020) and the fifth segment (from July 14, 2020 to August 31, 2020) have witnessed noticeable decreases in the growth rate. The decrease can perhaps/probably be explained by the mandatory use of face-coverings and the border closure with the United States for the third segment, and the use of COVID-19 serological tests and the national contact tracing for the fourth and fifth segments. An upward trend in the growth rate observed from August 31, 2020 to October 10, 2020 could have resulted from the opening of businesses and public spaces. It seems that the second wave started on October 10, 2020, with a remarkable increase in the rate that continued until January 12, 2021. After this date, the rate again declined until March 18, 2021, which could be the result of provincial states of emergency and lockdowns. The last segment witnessed another surge in the rate, perhaps due to new variants of Coronavirus.

The mPRUTF algorithm has also detected seven change points for the United Kingdom on the following dates: April 4, 2020; April 28, 2020; May 25, 2020; June 22, 2020; September 9, 2020; November 26, 2020 and February 5, 2021. As can be viewed from the figure, there are remarkable declines in the growth rates for the second segment (perhaps due to the nationwide lockdown), the third segment (perhaps due to the international travel ban) and the segments from May 25, 2020 to September 9, 2020 (perhaps due to mandatory use of face masks and comprehensive contact tracing). The country witnessed a significant increase in the growth rate starting from September 9, 2020, which aligns with the reopening of businesses, schools and universities. The second national lockdown could be linked to the very small decrease in the slope of the segment from November 26, 2020 to February 5, 2021. Finally, the growth rate in the last segment seemed to be under control, which could be the result of COVID vaccinations.

9 More on Models With Frequent Change Points or With Dependent Errors

This section empirically investigates the performance of mPRUTF in models with frequent change points as well as models with dependent random errors.

9.1 mPRUTF in Signals With Frequent Change Points

In order to evaluate the detection power of mPRUTF in signals with frequent change points, we employ a teeth signal for the piecewise constant case and a wave signal for the piecewise linear case. For the teeth signal, we consider a signal with 29 change points and varying segment lengths defined as follows:

-

•

for , if ; , otherwise,

-

•

for , if ; , otherwise,

-

•

for , if ; , otherwise,

-

•

for , if ; , otherwise.

The signal is displayed in the top-left panel of Figure 14.

The wave signal also has 29 change points with varying slopes which is defined as follows:

-

•

for , if ; , otherwise,

-

•

for , if ; , otherwise,

-

•

for , if ; , otherwise,

-

•

for , if ; , otherwise.

The top-right panel of Figure 14 shows this signal.

We generated independent samples of in model (1) with for both signals. The mPRUTF algorithm was then applied to these samples to estimate their change point locations. Figure 14 shows the histograms of the locations of these change points for the signals. The figure provides evidence that mPRUTF is unable to effectively detect change points in signals with frequent change points and short segments. It also shows that the results deteriorate when the noise variance or the polynomial order increase.

It turns out that the success of the mPRUTF algorithm critically relies on its stopping rule. Equation (44) verifies that estimating the noise variance and specifying the threshold from a Gaussian bridge process play crucial roles in the stopping rule. As discussed in Fryzlewicz, (2018), the two widely used robust estimators of , Mean Absolute Deviation (MAD) (used here) and Inter-Quartile Range (IQR), overestimate in frequent change point scenarios. In addition, determining the accurate value of the threshold using (45) is affected in such scenarios. These two factors prevent the stopping rule from being effective in the mPRUTF algorithm and lead to the underestimation of change points for these scenarios. We must note that such poor performance in frequent change point scenarios is not specific to mPRUTF. As investigated in Fryzlewicz, (2018), state-of-the-art methods such as PELT, WBS, MOSUM, SMUCE and FDRSeg are among the approaches that fail in such scenarios.

9.2 mPRUTF in Models With Dependent Error Terms

How can mPRUTF’s performance be affected by various types of random errors, such as non-Gaussian or dependent errors? This is of course an important question and will be the topic of future works. Notice that the dual solution path of trend filtering is not impacted by the type of random errors. However, the type of random errors plays a key role in the stopping rule of mPRUTF because the stopping rule is built based on Gaussian bridge processes established by Donsker’s Theorem.

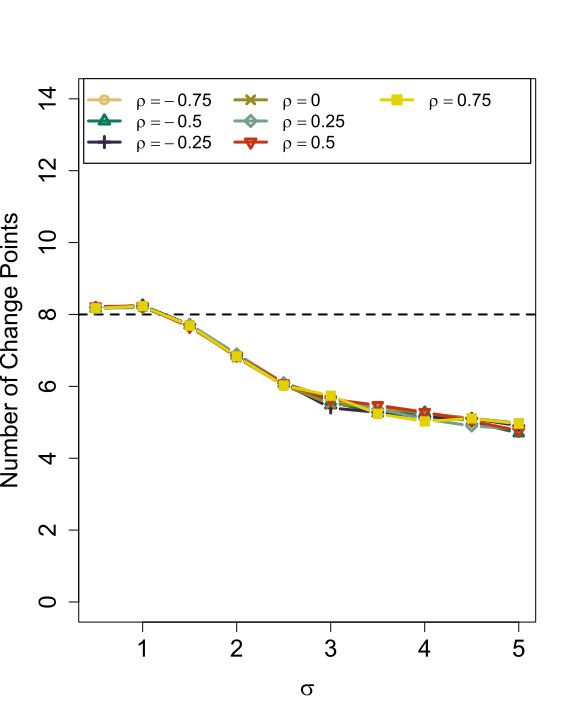

To empirically investigate the performance of mPRUTF for weakly dependent random errors, a simulation study is carried out here. To this end, we generate samples from model (1) with the PWC and PWL signals. We consider errors from an model with , for . Here, ’s are independent and identical random errors drawn from with and . The results of mPRUTF for both PWC and PWL signals are provided in Figure 15. As can be seen, the results are very similar, in terms of the average number of change points, MSEs and the scaled Hausdorff distances, for various values of . Therefore, it appears that the mPRUTF algorithm is quite robust against dependent error terms. Extensive studies of mPRUTF for non-Gaussian and dependent random errors will be carried out in future research.

10 Discussion

This paper proposed an algorithm, PRUTF, to detect change points in piecewise polynomial signals using trend filtering. We demonstrated that the dual solution path produced by the PRUTF algorithm forms a Gaussian bridge process for any given value of the regularization parameter . This conclusion allowed us to derive an efficient stopping rule for terminating the search algorithm, which is vital in change point analysis. We then proved that when there is no staircase block in the signal, the method guarantees consistent pattern recovery. However, it fails in doing so when there is a staircase in the underlying signal. To address this shortcoming in such a case, we suggested a modification in the procedure of constructing the solution path, which effectively prevents false discovery of change points. Evidence from both simulation studies and real data analysis reveals the accuracy and the high detection power of the proposed method.

Appendix A

A.1 Proof of Theorem 1

For , and a sequence of real numbers, let

Define the partial weighted sum process by

Obviously, for any , and any , the vector has a multivariate normal distribution, and therefore is a Gaussian process for any given .

-

a)

In our case, first note that

(A.1) (A.2) which is a partial weighted sum process of independent and identical Gaussian random variables . The first equality in (A.1) is derived from the fact that the structure of the true signal remains unchanged within the -th block, meaning that , for , which in turn implies

-

b)

Recall that the covariance matrix is a block diagonal matrix which states that the covariance matrix between two distinct blocks is zero. This completes the proof of the theorem.

A.2 Proof of Theorem 2

-

a)

For , and both signs , according to the KKT conditions, the dual variables must lie between and , that is,

(A.3) which yields the constraint for the first block in (48).

- b)

- c)

A.3 Proof of Theorem 3

-

(a)

The PRUTF algorithm is consistent in pattern recovery if the event

(A.6) occurs with probability approaching one. For ease of exposition, we first compute the probability of the statement in (A.6) for the piecewise constant case, . We then extend this probability computation to an arbitrary piecewise polynomial .

Case : In this case, the event in (A.6) is equivalent to where

(A.7) and

(A.8) For , observe that ; therefore,

which is captured in event . The last inequality in the above equation occurs because, from Theorem 2, we have as well as the fact that , for an arbitrary . In the following, we derive the conditions under which the probabilities of both events and converge to 1.

-

•

To compute the probability of , we first note that, for every ,

where is the average of observations in the segment created by block . The last inequality in the above statement is derived from the triangular inequality. Therefore, in order to verify , it is enough to show that, with the probability approaching one,

(A.9) where is the minimum jump between change points. Equivalently, it suffices to show that

(A.10) and

(A.11) The inequality in (A.10) holds if , where . Applying the union and Gaussian tail bounds, the probability of the complement of the event in (A.11) can be computed as

(A.12) (A.13) (A.14) The probability in (A.12) converges to zero if, for some ,

(A.15) -

•

Next, we verify conditions under which . Equivalently, it is enough to determine the conditions under which the following probability converges to zero.

(A.16) (A.17) (A.18) (A.19) The above probability converges to zero if, for some , the following conditions hold,

(A.20)

Case arbitrary : For the piecewise polynomial of order , we note that, for any ,

where is the projection map onto the row space of . In the preceding statement, the second equality is derived by plugging in the statement in (31) in place of . From (24), recall that is equivalent to the prediction matrix in the -th polynomial regression of onto indices . This fact allows us to derive an upper bound for the variance of (Yu and Chatterjee,, 2020),

Following a procedure similar to that used in the case ,

(A.21) For the case of an arbitrary , there is a slight modification in the definition of event :

(A.22) Again, in the same manner

(A.23) Therefore, for an arbitrary , the PRUTF algorithm is consistent in pattern recovery if, in addition to

-

•

-

(b)

As shown in part (c) of Theorem 2, in staircase blocks, the violation of the KKT conditions boils down to crossing the zero line for a Gaussian bridge process. Suppose -th block is a staircase block; therefore, PRUTF can attain the exact discovery if or , for all . Hence the probability of this event occurring is equal to . According to Beghin and Orsingher, (1999),

(A.24) where is the -th diagonal element of the matrix . As a result, the probability converges to zero as vanishes. This result implies that the PRUTF algorithm fails to consistently recover the true pattern in the presence of staircase patterns.

Bibliography

- Adler and Taylor, (2009) Adler, R. J. and Taylor, J. E. (2009). Random fields and geometry. Springer.

- Ali et al., (2019) Ali, A., Tibshirani, R. J., et al. (2019). The generalized lasso problem and uniqueness. Electronic Journal of Statistics, 13(2):2307–2347.

- Aminikhanghahi and Cook, (2017) Aminikhanghahi, S. and Cook, D. J. (2017). A survey of methods for time series change point detection. Knowledge and Information Systems, 51(2):339–367.

- Anastasiou and Fryzlewicz, (2019) Anastasiou, A. and Fryzlewicz, P. (2019). Detecting multiple generalized change-points by isolating single ones. arXiv preprint arXiv:1901.10852.

- Arnold and Tibshirani, (2016) Arnold, T. B. and Tibshirani, R. J. (2016). Efficient implementations of the generalized lasso dual path algorithm. Journal of Computational and Graphical Statistics, 25(1):1–27.

- Auger and Lawrence, (1989) Auger, I. E. and Lawrence, C. E. (1989). Algorithms for the optimal identification of segment neighborhoods. Bulletin of mathematical biology, 51(1):39–54.

- Bai, (1997) Bai, J. (1997). Estimating multiple breaks one at a time. Econometric theory, 13(3):315–352.

- Bai and Perron, (2003) Bai, J. and Perron, P. (2003). Computation and analysis of multiple structural change models. Journal of applied econometrics, 18(1):1–22.

- Baranowski et al., (2019) Baranowski, R., Chen, Y., and Fryzlewicz, P. (2019). Narrowest-over-threshold detection of multiple change points and change-point-like features. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 81(3):649–672.

- Beghin and Orsingher, (1999) Beghin, L. and Orsingher, E. (1999). On the maximum of the generalized brownian bridge. Lithuanian Mathematical Journal, 39(2):157–167.

- Bianchi et al., (1999) Bianchi, M., Boyle, M., and Hollingsworth, D. (1999). A comparison of methods for trend estimation. Applied Economics Letters, 6(2):103–109.

- Billingsley, (2013) Billingsley, P. (2013). Convergence of probability measures. John Wiley and Sons.

- Boyd et al., (2011) Boyd, S., Parikh, N., Chu, E., Peleato, B., Eckstein, J., et al. (2011). Distributed optimization and statistical learning via the alternating direction method of multipliers. Foundations and Trends® in Machine learning, 3(1):1–122.

- Boyd and Vandenberghe, (2004) Boyd, S. and Vandenberghe, L. (2004). Convex optimization. Cambridge university press.

- Brezis, (2010) Brezis, H. (2010). Functional analysis, Sobolev spaces and partial differential equations. Springer Science & Business Media.

- Ciuperca, (2011) Ciuperca, G. (2011). A general criterion to determine the number of change-points. Statistics & Probability Letters, 81(8):1267–1275.

- Ciuperca, (2014) Ciuperca, G. (2014). Model selection by lasso methods in a change-point model. Statistical Papers, 55(2):349–374.

- Demetriou and Lipitakis, (2001) Demetriou, I. and Lipitakis, E. (2001). Certain positive definite submatrices that arise from binomial coefficient matrices. Applied numerical mathematics, 36(2-3):219–229.

- Donsker, (1951) Donsker, M. D. (1951). An invariance principle for certain probability limit theorems.

- Eckley et al., (2011) Eckley, I. A., Fearnhead, P., and Killick, R. (2011). Analysis of changepoint models. Bayesian Time Series Models, pages 205–224.

- Frick et al., (2014) Frick, K., Munk, A., and Sieling, H. (2014). Multiscale change point inference. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 76(3):495–580.

- Fryzlewicz, (2018) Fryzlewicz, P. (2018). Detecting possibly frequent change-points: Wild binary segmentation 2 and steepest-drop model selection. arXiv preprint arXiv:1812.06880.

- Fryzlewicz et al., (2014) Fryzlewicz, P. et al. (2014). Wild binary segmentation for multiple change-point detection. The Annals of Statistics, 42(6):2243–2281.

- Fryzlewicz et al., (2018) Fryzlewicz, P. et al. (2018). Tail-greedy bottom-up data decompositions and fast multiple change-point detection. The Annals of Statistics, 46(6B):3390–3421.

- Futschik et al., (2014) Futschik, A., Hotz, T., Munk, A., and Sieling, H. (2014). Multiscale dna partitioning: statistical evidence for segments. Bioinformatics, 30(16):2255–2262.

- Galceran et al., (2017) Galceran, E., Cunningham, A. G., Eustice, R. M., and Olson, E. (2017). Multipolicy decision-making for autonomous driving via changepoint-based behavior prediction: Theory and experiment. Autonomous Robots, 41(6):1367–1382.

- Gasbarra et al., (2007) Gasbarra, D., Sottinen, T., and Valkeila, E. (2007). Gaussian bridges. In Stochastic analysis and applications, pages 361–382. Springer.

- Green and Silverman, (1993) Green, P. J. and Silverman, B. W. (1993). Nonparametric regression and generalized linear models: a roughness penalty approach. Chapman and Hall/CRC.

- Hampel, (1974) Hampel, F. R. (1974). The influence curve and its role in robust estimation. Journal of the American Statistical Association, 69(346):383–393.

- Hansen, (2001) Hansen, B. E. (2001). The new econometrics of structural change: dating breaks in us labour productivity. Journal of Economic perspectives, 15(4):117–128.