Mean-Variance Analysis in Bayesian Optimization under Uncertainty

ABSTRACT

We consider active learning (AL) in an uncertain environment in which trade-off between multiple risk measures need to be considered. As an AL problem in such an uncertain environment, we study Mean-Variance Analysis in Bayesian Optimization (MVA-BO) setting. Mean-variance analysis was developed in the field of financial engineering and has been used to make decisions that take into account the trade-off between the average and variance of investment uncertainty. In this paper, we specifically focus on BO setting with an uncertain component and consider multi-task, multi-objective, and constrained optimization scenarios for the mean-variance trade-off of the uncertain component. When the target blackbox function is modeled by Gaussian Process (GP), we derive the bounds of the two risk measures and propose AL algorithm for each of the above three problems based on the risk measure bounds. We show the effectiveness of the proposed AL algorithms through theoretical analysis and numerical experiments.

1 Introduction

Decision making in an uncertain environment has been studied in various domains. For example, in financial engineering, the mean-variance analysis [1, 2, 3] has been introduced as a framework for making investment decisions, taking into account the trade-off between the return (mean) and the risk (variance) of the investment. In this paper we study active learning (AL) in an uncertain environment. In many practical AL problems, there are two types of parameters called design parameters and environmental parameters. For example, in a product design, while the design parameters are fully controllable, the environmental parameters vary depending on the environment in which the product is used. In this paper, we examine AL problems under such an uncertain environment, where the goal is to efficiently find the optimal design parameters by properly taking into account the uncertainty of the environmental parameters.

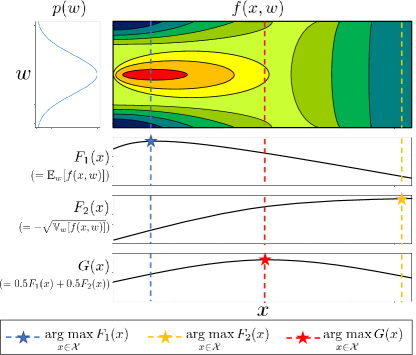

Concretely, let be a blackbox function indicating the performance of a product, where is the set of controllable design parameters and is the set of uncontrollable environmental parameters whose uncertainty is characterized by a probability distribution . We particularly focus on the AL problem where the mean and the variance of the environmental parameters,

| (1a) | ||||

| (1b) | ||||

respectively, are taken into account. Specifically, we work on these two uncertainty measures in three different scenarios: multi-task learning scenario, multi-objective optimization scenario, and constrained optimization scenario. In the first scenario, we study AL for optimizing a weighted sum of these two measures. In the second scenario, we discuss how to obtain the Pareto frontier of these two measures in an AL setting. In the third scenario, we consider optimizing one of the two measures under some constraint on the other measure. We refer to these problems and the proposed framework for solving them as Mean-Variance Analysis in Bayesian Optimization (MVA-BO). Figure 1 shows an illustration of a multi-task learning scenario.

In this study, we employ a Gaussian process (GP) to model the uncertainty of the blackbox function . In a conventional GP-based AL problem (without uncontrollable environmental parameters ), the acquisition function (AF) is designed based on how the uncertainty of the blackbox function changes when an input point is selected and the blackbox function is evaluated at the input point. On the other hand, in MVA-BO, we need to know how the uncertainties of the mean function (1a) and the variance function (1b) change by evaluating the blackbox function at the selected input point. Note that we face the difficulty of not being able to directly evaluate the target functions (1a) and (1b). It has been shown in a previous study [4] that, when follows a GP, the mean function (1a) also follows a GP. Unfortunately, however, the variance function (1b) does not follow a GP, indicating that we need to develop a new method to quantify how the uncertainty of the variance function changes by evaluating the blackbox function at the selected input point. In this study, we extend the GP-UCB algorithm [5] to realize MVA-BO in the above mentioned three scenarios by overcoming these technical difficulties. We demonstrate the effectiveness of the proposed MVA-BO framework through theoretical analyses and numerical experiments.

Related Work

Various problem setups and methods have been studied for AL and Bayesian optimization (BO) problems when there are multiple target functions. One of such problem setup is multi-task BO [6]. In this problem setup, the AF is designed to select input points that commonly contribute to optimizing multiple target functions. Another popular problem setup is multi-objective BO [7, 8, 9]. The goal of a multi-objective optimization is to obtain so-called Pareto-optimal solutions. The AF in this problem setup is designed to efficiently identify solutions on the Pareto frontier. Another common problem setup is constrained BO [10, 11, 12]. The goal of this problem setup is to find the optimal solution to a constrained optimization problem in a situation where both the objective function and constraint function are blackbox functions that are costly to evaluate. The AF in this problem setup is designed to select input points that are useful not only for maximizing the objective function but also for identifying the feasible region. In this paper, we study these three scenarios as concrete examples of MVA-BO. Unlike conventional multi-task, multi-objective and constrained BOs, the main technical challenges of MVA-BO are that the two target functions (1a) and (1b) cannot be directly evaluated and that the latter does not follow a GP.

Various studies have been published on BO under various types of uncertainty. The most relevant one to our study is on Bayesian quadrature optimization (BQO) [13], the goal of which is to optimize the mean function (1a). When the blackbox function follows a GP, the mean function (1a) also follows a GP, suggesting that one can efficiently solve BQO problems by properly modifying the AFs in conventional BO. By replacing the integrand in (1a) with different uncertainty measures, one can consider various types of AL problems under uncertainty [14, 15]. Another line of research dealing with uncontrollable and uncertain factors in BO is known as robust BO. The goal of robust BO is to make robust decisions that appropriately take into account the uncertainty of the BO process and the GP model. For example, input uncertainty in BO has been studied, in which probabilistic noise is inevitably added to the input points when evaluating the target blackbox function. Although research on BO in an uncertain environment has steadily progressed over the past few years, to our knowledge, there are no AL nor BO studies that take into account the trade-offs between multiple uncertainty measures such as mean-variance analysis.

Decision making under uncertainty is being examined in the field of robust optimization [16, 17, 18], with especially applications to financial engineering in mind [19, 20, 21]. It has been pointed out that when making decisions under uncertainty, it is important to balance multiple uncertainty measures appropriately, as represented by the Nobel prize-winning mean-variance analysis in portfolio theory [1, 2, 3]. Various risk measures, such as Value at Risk (VaR), have been proposed in financial engineering, and these multiple risk measures are used in combination, depending on the purpose of the decision making. However, to our knowledge, there have been AL or BO studies that have appropriately taken into account multiple uncertainty measures.

2 Preliminaries

2.1 Problem Setup

Let be a blackbox function which is expensive to evaluate, where and are a finite set 111We discuss the case where is a continuous set in appendix D. and a compact convex set, respectively. In our setting, a variable is probabilistically fluctuated by the given density function 222 Note that a probability mass function can also be considered when is a finite set. In that case, the subsequent discussions still hold if integral operations are replaced by summation operations. . At every step , a user chooses the next observation point , whereas will be given as a realization of the random variable, which follows the distribution . Next, the user gets the noisy observation , where is independent Gaussian noise following .

Furthermore, as a regularity assumption, we assume that is an element of reproducing kernel Hilbert space (RKHS) and has a bounded norm, which is also assumed in the standard BO literature [5]. Let be a positive definite kernel over and be an RKHS corresponding to . In this paper, for some positive constant , we assume with , where denotes the Hilbert norm defined on .

Models

Our algorithm uses the GP method [22] to navigate the optimization process. First, we assume as a prior of , where is a GP that is characterized by a mean function and a kernel function . Given the sequence of data , the posterior distribution of is the Gaussian distribution that has mean and variance defined as follows:

where , , is the identity matrix of size , and is the kernel matrix whose th element is .

We will make use of the following lemma, to construct the confidence bound of by using the posterior mean and the variance .

Lemma 2.1 (Theorem 3.11 in [23]).

Fix with . Given , let define

Then, the following holds with probability at least :

| (2) |

Based on the above lemma, the confidence bound of can be computed by

2.2 Objective Functions and Optimization Goal

Here, we consider the expectation and variance of under the uncertainty of as follows:

| (3) | ||||

| (4) |

Using these and , we define the objective functions and as follows:

| (5) |

Our goal is to maximize and simultaneously with as few function evaluations as possible. To this end, we handle these objective functions in multi-task and multi-objective optimization frameworks. 333In appendix B, as another formulation, we also consider the constrained optimization problem whose objective and constraint functions are and respectively.

Multi-task Optimization Scenario

First, we formulate the problem as a single-objective optimization problem whose objective function is defined as a weighted sum of and . Given a user-specified weight , let be a new objective function defined as follows:

In this formulation, our goal is to find efficiently. To rigorously determine the theoretical properties, we introduce the notion of an -accurate solution. Let be an estimated solution which is defined by the algorithm at step . Given a fixed constant , we say that is -accurate if the following inequality holds:

In section 4, for an arbitrarily small , we show that our algorithm can find the -accurate solution with high probability after finite step .

Multi-objective Optimization Scenario

In the multi-task scenario, we assume that the user can specify the weight before the optimization; however this is sometimes unrealistic. We also consider the more general formulation based on the Pareto optimality criterion. Hereafter, we use the vector representation of the objective functions like . First, let be a relational operator defined over or . Given , we write or provided that and hold simultaneously. We say that dominates if . Furthermore, we write or provided that either or holds.

The goal of this scenario is to identify the following Pareto set efficiently:

Moreover, Pareto front is defined by

Next, we introduce the notion of an -accurate Pareto set [8], which is an idea similar to the -accurate solution in the multi-task scenario. Given a non-negative vector , we define the relational operator , which is the relaxed version of . For , we write or if and hold simultaneously. Then, the -Pareto front is defined as:

We say that estimated Pareto set of the algorithm is an -accurate Pareto set if the following two conditions are satisfied:

-

1.

, where .

-

2.

For any , there is at least one point such that .

Intuitively, condition guarantees that the estimated solutions are worse than the true Pareto front by at most . Condition 2 indicates that can cover all points in the true Pareto set .

We emphasize that although many studies about multi-task or multi-objective optimization based on a GP have been reported, their methods cannot be directly applied to our setting because the objective functions and are not observed directly.

3 Proposed Method

First, we explain the basic idea of our proposed algorithms. To maximize and efficiently, one simple way is to consider the predicted distributions of and , and apply existing methods (e.g. expected improvement, entropy search). However, it is difficult to handle the predicted distribution of although is modeled by a GP. In this paper, we first derive the intervals in which and exist with high probability from the confidence bound of , and construct the algorithm based on these derived intervals. Hereafter, with a slight abuse of notation, we refer to these derived intervals as the confidence bounds of and .

3.1 Confidence Bounds of Objective Functions

First, we consider the confidence bound of . When (2) holds, the following inequity holds for any , :

This implies that for any , with probability at least for and defined as

We construct the confidence bound of in a similar way. First, we consider the quantity , which appears in the integrand of . Under condition (2), the following inequity holds:

| (6) |

where and . Next, the integrand of can be evaluated based on (6) as follows:

where

Finally, from the monotonicity of square root, the confidence bound of is computed using the following equations for and :

3.2 Algorithms

Multi-task Scenario

In the multi-task scenario, our algorithm chooses the next observation point based on the upper confidence bound (UCB) of the function . From and , the confidence bound of can be constructed by defining

At every step , the next observation point of our algorithm is defined by . Hereafter, we call this strategy Multi-Task (MT)-MVA-BO. The pseudo-code of MT-MVA-BO is shown as Algorithm 1.

Multi-objective Scenario

Next, we explain the proposed algorithm for finding the Pareto set efficiently. From the confidence bounds of and , we define and by and , which respectively represent the optimistic and pessimistic predictions of the objective functions at step . First, we define the estimated Pareto set at step by

| (7) |

For theoretical reasons, we define based on pessimistic predictions and the same idea is used in the existing GP-based optimization literatures [24, 8, 25, 26]. Furthermore, using , the potential Pareto set is defined by

An intuitive interpretation of is the set which excludes the points that are -dominated by other points with high probability. At every step , our algorithm chooses based on the uncertainty defined by the confidence bounds of and . In this paper, we adopt the diameter of rectangle as the uncertainty of :

| (8) |

Namely, the next observation point is defined by at every step .

Our proposed algorithm terminates when estimated Pareto set is guaranteed to be an -Pareto set with high probability. To this end, our algorithm checks the uncertainty set that is defined by

Intuitively, is the set of points where it is not possible to decide whether it is an -Pareto solution based on the current confidence bounds. Our algorithm terminates at a step where both and hold.

Hereafter, we call this algorithm Multi-Objective (MO)-MVA-BO. The pseudo-code of MO-MVA-BO is shown as Algorithm 2.

3.3 Extensions and Practical Considerations

In this section, we consider several extensions of the proposed method to deal with situations which arise in some practical applications, leaving the details for appendix C.

3.3.1 Unknown Distribution

Thus far, we have assumed that is known; however, this assumption is sometimes unrealistic. Considering how to deal with the case where is unknown, one simple way is to estimate during the optimization process. For example, if we estimate by using an empirical distribution, we can apply our algorithm by replacing with the following when computing the confidence bounds:

As a more advanced method, it may be possible to consider extension to the distributionally robust setting [26, 27]; however, we leave this as future work.

3.3.2 Extension to Noisy Input

One setting similar to that in this paper is the noisy input setting [14, 28]. In this setting, observation point is fluctuated by noise which follows the known density defined over . At every step , the user chooses and obtains observation as , . Our problem can be extended to the noisy input setting by defining and through expectation and variance defined as follows:

| (9) | ||||

| (10) |

We can apply the same algorithms as those in section 3.2 by constructing the confidence bounds via a way similar to that in section 3.1.

3.3.3 Simulator-Based Experiment

Some applications can be allowed to control the variable in the optimization. For example, the case that the user run the optimization process by evaluating with the computer simulation. Such scenarios have often been considered in similar studies reported in the BO literature that assumed the existence of an uncontrollable variable [13, 26, 27]. Our method can be extended to such a scenario by choosing according to after the selection of .

4 Theoretical Results

In this section, we show the theoretical results of the proposed algorithms. The details of the proofs are in appendix A.

First, we introduce the maximum information gain [5] as a sample complexity parameter of a GP. Now, Let be a finite subset of , and be a vector whose th element is . Maximum information gain at step is defined by

where denotes the mutual information between and . Maximum information gain is often used in BO, and its analytical form of the upper bound is derived in commonly used kernels [5].

The following two theorems show the convergence properties of the proposed algorithms for the multi-task and multi-objective scenarios, respectively.

Theorem 4.1.

Fix positive definite kernel , and assume with . Let and , and set according to at every step . Furthermore, for any , define by . When applying MT-MVA-BO under the above conditions, with probability at least , is an -accurate solution, where is the smallest positive integer which satisfies the following inequity:

| (11) |

Here, and .

Theorem 4.2.

Fix positive definite kernel , and assume with . Let and , and set according to at every step . When applying MO-MVA-BO under the above conditions, the following 1. and 2. hold with probability at least :

- 1.

-

The algorithm terminates at most step where T is the smallest positive integer that satisfies the following inequity:

(12) Here, , .

- 2.

-

When the algorithm terminates, estimated Pareto set is an -accurate Pareto set.

The first term of the left hand side in (11) and (12) also appears in the theoretical result of the existing algorithm, which only considers the expectation (e.g. Theorem 2 in [26]). The second term is specific to our problem. This term depends on the complexity parameter , which quantifies the variation of function around its expectation.

5 Numerical Experiments

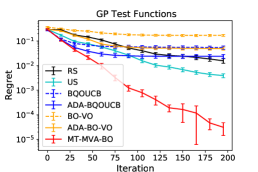

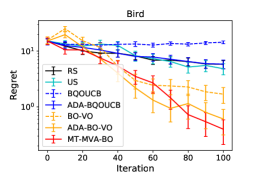

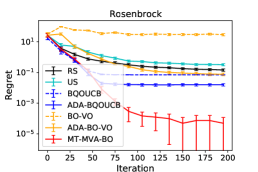

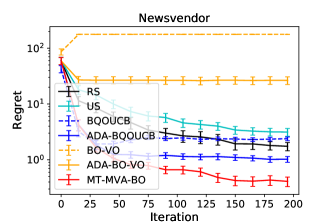

In this section, we show the performance of the proposed methods through numerical experiments. As the baseline methods in both the multi-task and multi-objective scenarios, we adopted random sampling (RS) and uncertainty sampling (US). RS choose from uniformly at random, and US choose such that achieve the largest average posterior variance . To measure the performance, in the multi-task scenario, we computed the regret, , at every step , where is the estimated solution defined by the algorithms. We defined as in RS, US, and proposed method (MT-MVA-BO). Furthermore, we set . Also, in the multi-objective scenario, we computed the gap of hyper-volume [7], to measure the performance, where HV and denote the hyper volumes computed based on the true Pareto set and the estimated Pareto set , respectively. The hyper volume gap measures how close the estimated Pareto front is to the true Pareto front. We defined by (7) in RS, US and the proposed method (MO-MVA-BO). Furthermore, in the multi-task scenario, to show the effect of difference of objective functions, we also adopt the two methods BQOUCB [26, 27] and BO-VO. BQOUCB is the existing method which aims to maximize , and BO-VO is the variant of our method which corresponds to the case . These methods choose as the maximizing point of and respectively. In addition, estimated solution is defined by and respectively. Moreover, we also make comparisons to the adaptive versions of these methods, ADA-BQOUCB and ADA-BO-VO. ADA-BQOUCB and ADA-BO-VO choose in the same way as do BQOUCB and BO-VO, but the estimated solutions are defined as .

5.1 Artificial Data Experiments

In this subsection, we show the results of the artificial-data experiments.

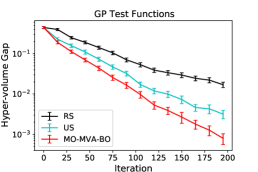

GP Test Functions

We experimented with the true oracle functions that are generated from the 2D GP prior. First, we divided into uniformly spaced grid points in each dimension and generated the sample path from the GP prior. Next, we created the GP model with these grid points and set the true oracle function as its GP posterior mean. In this experiment, we created sample paths from different seeds, and conducted experiments for each function. Thus, we report the average performance of a total of experiments. To create a GP sample path, we use the Gaussian kernel with , as well as to construct the confidence bound in the algorithms. Furthermore, we set noise variance as . In addition, we divided into grid points uniformly, and set and as these grid points. Moreover, we define by , where is the density function of the standard normal distribution.

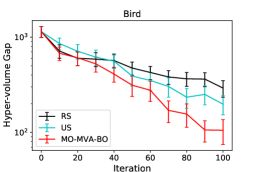

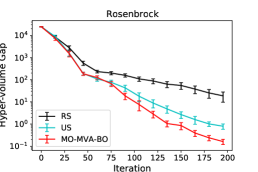

Benchmark Functions of Optimization

We also experimented with the Bird function (2D) and Rosenbrock function (3D), which are often used as the benchmark function in the field of the optimization. First, we scaled the input domain to divided into grid points in each dimension. In Bird function, we set and as the grid points of the first and the second dimensions, respectively. In the Rosenbrock function, we set as the grid points of the third dimension and the remaining points as . Furthermore, we set as in the same way as the experiment of the GP test functions. We use ARD Gaussian kernel , and tune these hyperparameters by maximizing the marginal likelihood at every step in the algorithms. Furthermore, we set the noise variance as and report the average performance of simulations with different seeds.

Figure 2 shows the results of the artificial data experiments. We confirmed that the proposed methods achieve better performances than the other methods. In the experiments of the multi-task scenario, we also confirmed that the regrets of BQOUCB, BO-VO, ADA-BQOUCB, and ADA-BO-VO stop decreasing at an early stage. Note that these are reasonable results because objective functions of these methods are inconsistent with our settings.

5.2 Real-data Experiment

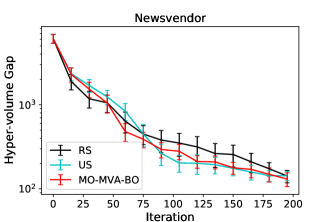

We applied the proposed methods to Newsvendor problem under dynamic consumer substitution [29], whose goal is to optimize the initial inventory levels under uncertainty of customer behaviors. The parameter and respectively correspond to the initial inventory level of products and the uncertain purchasing behaviors of customers, which follow mutually independent Gamma distributions. The goal of this problem is to find the which optimizes the profit under the uncertainty of . For this problem, we conducted the experiments in the simulator-based setting described in section 3.3.3 because profit can be evaluated based on a computer simulation. Figure 3 shows the average performances of simulations with different seeds.

6 Conclusion

We introduced the novel Bayesian optimization framework: MVA-BO, which simultaneously considers two objective functions: expectation and variance under an uncertainty environment. In this framework, we considered the three scenarios; multi-task, multi-objective and constraint optimization scenarios, which often appear in real-world applications. We studied the rigorous convergence properties of our MVA-BO algorithms and demonstrated the effectiveness of them through both artificial and real-data experiments.

Acknowledgement

This work was partially supported by MEXT KAKENHI (20H00601, 16H06538), JST CREST (JPMJCR1502), and RIKEN Center for Advanced Intelligence Project.

References

- [1] Markowitz HM. Portfolio selection. Journal of Finance, 7(1):77–91, 1952.

- [2] Harry M Markowitz and G Peter Todd. Mean-variance analysis in portfolio choice and capital markets, volume 66. John Wiley & Sons, 2000.

- [3] Michael C Keeley and Frederick T Furlong. A reexamination of mean-variance analysis of bank capital regulation. Journal of Banking & Finance, 14(1):69–84, 1990.

- [4] Anthony O’Hagan. Bayes–hermite quadrature. Journal of statistical planning and inference, 29(3):245–260, 1991.

- [5] Niranjan Srinivas, Andreas Krause, Sham M. Kakade, and Matthias W. Seeger. Gaussian process optimization in the bandit setting: No regret and experimental design. In Johannes Fürnkranz and Thorsten Joachims, editors, Proceedings of the 27th International Conference on Machine Learning (ICML-10), June 21-24, 2010, Haifa, Israel, pages 1015–1022. Omnipress, 2010.

- [6] Kevin Swersky, Jasper Snoek, and Ryan P Adams. Multi-task Bayesian optimization. In Advances in neural information processing systems, pages 2004–2012, 2013.

- [7] Michael Emmerich. Single-and multi-objective evolutionary design optimization assisted by Gaussian random field metamodels. Dissertation, LS11, FB Informatik, Universität Dortmund, Germany, 2005.

- [8] Marcela Zuluaga, Andreas Krause, and Markus Püschel. e-pal: An active learning approach to the multi-objective optimization problem. Journal of Machine Learning Research, 17(104):1–32, 2016.

- [9] Shinya Suzuki, Shion Takeno, Tomoyuki Tamura, Kazuki Shitara, and Masayuki Karasuyama. Multi-objective Bayesian optimization using Pareto-frontier entropy. In Proceedings of Machine Learning and Systems 2020, pages 10841–10850. 2020.

- [10] Jacob R Gardner, Matt J Kusner, Zhixiang Eddie Xu, Kilian Q Weinberger, and John P Cunningham. Bayesian optimization with inequality constraints. In ICML, volume 2014, pages 937–945, 2014.

- [11] Michael A. Gelbart, Jasper Snoek, and Ryan P. Adams. Bayesian optimization with unknown constraints. In Proceedings of the Thirtieth Conference on Uncertainty in Artificial Intelligence, UAI’14, page 250–259, Arlington, Virginia, USA, 2014. AUAI Press.

- [12] José Miguel Hernández-Lobato, Michael A Gelbart, Ryan P Adams, Matthew W Hoffman, and Zoubin Ghahramani. A general framework for constrained Bayesian optimization using information-based search. The Journal of Machine Learning Research, 17(1):5549–5601, 2016.

- [13] Saul Toscano-Palmerin and Peter I. Frazier. Bayesian optimization with expensive integrands. CoRR, abs/1803.08661, 2018.

- [14] Justin J Beland and Prasanth B Nair. Bayesian optimization under uncertainty. In NIPS BayesOpt 2017 workshop, 2017.

- [15] Shogo Iwazaki, Yu Inatsu, and Ichiro Takeuchi. Bayesian quadrature optimization for probability threshold robustness measure. arXiv preprint arXiv:2006.11986, 2020.

- [16] Aharon Ben-Tal, Laurent El Ghaoui, and Arkadi Nemirovski. Robust optimization, volume 28. Princeton University Press, 2009.

- [17] Hans-Georg Beyer and Bernhard Sendhoff. Robust optimization–a comprehensive survey. Computer methods in applied mechanics and engineering, 196(33-34):3190–3218, 2007.

- [18] Aharon Ben-Tal and Arkadi Nemirovski. Robust optimization–methodology and applications. Mathematical programming, 92(3):453–480, 2002.

- [19] Alexander Schied*. Risk measures and robust optimization problems. Stochastic Models, 22(4):753–831, 2006.

- [20] Gordon J Alexander and Alexandre M Baptista. Economic implications of using a mean-var model for portfolio selection: A comparison with mean-variance analysis. Journal of Economic Dynamics and Control, 26(7-8):1159–1193, 2002.

- [21] Frank J Fabozzi, Petter N Kolm, Dessislava A Pachamanova, and Sergio M Focardi. Robust portfolio optimization. The Journal of portfolio management, 33(3):40–48, 2007.

- [22] Carl Edward Rasmussen and Christopher K. I. Williams. Gaussian Processes for Machine Learning. MIT Press, 2006.

- [23] Yasin Abbasi-Yadkori. Online learning for linearly parametrized control problems. 2013.

- [24] Yanan Sui, Alkis Gotovos, Joel Burdick, and Andreas Krause. Safe exploration for optimization with Gaussian processes. In International Conference on Machine Learning, pages 997–1005, 2015.

- [25] Ilija Bogunovic, Jonathan Scarlett, Stefanie Jegelka, and Volkan Cevher. Adversarially robust optimization with Gaussian processes. In Advances in neural information processing systems, pages 5760–5770, 2018.

- [26] Johannes Kirschner, Ilija Bogunovic, Stefanie Jegelka, and Andreas Krause. Distributionally robust Bayesian optimization. In Silvia Chiappa and Roberto Calandra, editors, The 23rd International Conference on Artificial Intelligence and Statistics, AISTATS 2020, 26-28 August 2020, Online [Palermo, Sicily, Italy], volume 108 of Proceedings of Machine Learning Research, pages 2174–2184. PMLR, 2020.

- [27] Thanh Nguyen, Sunil Gupta, Huong Ha, Santu Rana, and Svetha Venkatesh. Distributionally robust Bayesian quadrature optimization. In Silvia Chiappa and Roberto Calandra, editors, Proceedings of the Twenty Third International Conference on Artificial Intelligence and Statistics, volume 108 of Proceedings of Machine Learning Research, pages 1921–1931, Online, 26–28 Aug 2020. PMLR.

- [28] Lukas Fröhlich, Edgar Klenske, Julia Vinogradska, Christian Daniel, and Melanie Zeilinger. Noisy-input entropy search for efficient robust Bayesian optimization. In Silvia Chiappa and Roberto Calandra, editors, Proceedings of the Twenty Third International Conference on Artificial Intelligence and Statistics, volume 108 of Proceedings of Machine Learning Research, pages 2262–2272, Online, 26–28 Aug 2020. PMLR.

- [29] Siddharth Mahajan and Garrett Van Ryzin. Stocking retail assortments under dynamic consumer substitution. Operations Research, 49(3):334–351, 2001.

- [30] Johannes Kirschner and Andreas Krause. Information directed sampling and bandits with heteroscedastic noise. In Proc. International Conference on Learning Theory (COLT), July 2018.

- [31] Yanan Sui, Vincent Zhuang, Joel W. Burdick, and Yisong Yue. Stagewise safe Bayesian optimization with Gaussian processes. In Jennifer G. Dy and Andreas Krause, editors, Proceedings of the 35th International Conference on Machine Learning, ICML 2018, Stockholmsmässan, Stockholm, Sweden, July 10-15, 2018, volume 80 of Proceedings of Machine Learning Research, pages 4788–4796. PMLR, 2018.

Appendix A Proofs

A.1 Proof of Theorem 4.1

From the definition of and Lemma 2.1, the following holds with probability at least :

| (13) |

Moreover, we give the following lemma about the confidence bound :

Lemma A.1.

Proof.

From the definition of and , we have

| (14) |

Similarly, from the definition of and , we get the following inequality:

| (15) |

Here, the last inequality is given by monotonicity of . In addition, noting that the definition of and we obtain

| (16) |

where the last inequality is obtained by using the fact that for any . Furthermore, we have

| (17) |

where . Moreover, we define and as

Then, and can be expressed as follows:

Here, if , then we have and

On the other hand, if , then we get and

Therefore, in all cases the following equality holds:

Next, since (13) holds, we get . This implies that

Hence, we have

Thus, the following inequality holds:

| (18) |

Moreover, can be bounded as

| (19) |

Hence, from (17), (18) and (19), we obtain

and

In addition, from the definition of , the following holds:

Here, the last inequality is obtained by using Jensen’s inequality and convexity of . Therefore, we have

| (20) |

Thus, by using (20) and Schwartz’s inequality for (16), we get

| (21) |

Therefore, from (14), (15) and (21), we have the desired inequality. ∎

Next, in order to evaluate and in the right hand side of the inequality of Lemma A.1, we introduce the following lemma given by [30]:

Lemma A.2.

Let be any non-negative stochastic process adapted to a filtration , and define . Assume that for . Then, for any , the following holds with probability at least :

Furthermore, from the assumption about the kernel function, we get and . Hence, from Lemma A.2, with probability at least , it holds that

| (22) |

Similarly, the following inequality holds with probability at least :

| (23) |

In addition, we introduce the following lemma given by [5] about the maximum information gain :

Lemma A.3.

Fix . Then, the following inequality holds:

| (24) |

Moreover, from Schwarz’s inequality and Lemma A.3, we get the following inequality:

| (25) |

Thus, from (22), (23), (24) and (25) we obtain the following corollary:

Proof.

Finally, we prove Theorem 4.1. Let , and define . Assume that (13) holds. Then, for any , it holds that . Thus, for any , we get

This implies that

| (27) |

Here, note that with probability at least , (13), (22) and (23) hold. Therefore, by combining Corollary A.1, the following holds with probability at least :

Hence, if satisfies (11), with probability at least , it holds that . Therefore, is the -accurate solution.

A.2 Proof of Theorem 4.2

In this subsection, we prove Theorem 4.2. First, we show several lemmas.

Lemma A.4.

For any , has at least one element (i.e., ).

Proof.

Let . We define and as

Assume that . Then, it holds that

This implies that .

On the other hand, if , then the following holds for any :

Here, if , it holds that . Similarly, if , it holds that

Noting that and , we have . Thus, we have . Form the definition of , we get . ∎

Lemma A.5.

Let , and assume that . Also let be an element of . Then, there exists an element such that

Proof.

Let , and . Assume that the following holds:

| (28) |

From the definition of , we have . Here, since , there exists such that

Therefore, there exists such that

Furthermore, by combining

we get . Thus, from (28) we obtain . By repeating the same argument, we have , where , . Next, we show that for any and with . In fact, if there exist and with such that , we get . Here, from , noting that the definition of and we get

Similarly, from the definition of and , we obtain

Thus, we get . However, it contradicts . Hence, it holds that for any and with . Therefore, the set is equal to . Recall that for any . By combining this and , we have . However, it contradicts Lemma A.4. Hence, the assumption (28) is incorrect. ∎

Lemma A.6.

Let be an element of , and let be a positive vector. Assume that at least one of the following inequalities holds for any :

Then, it holds that .

Proof.

In order to prove Lemma A.6, we consider the following two cases:

- (1)

-

For any , .

- (2)

-

There exist such that .

First, we consider (1). We define and as

From the definition of and , it holds that . Thus, from (1), we get . Hence, the following holds for any :

Therefore, we get . Note that . Here, let . Then, from the lemma’s assumption, at least one of the following inequalities holds:

If , we set . Noting that for any , we have . This implies that . Thus, the following holds:

Furthermore, since and , we obtain . Similarly, if , we set . Also in this case, by using the same argument, we get and

By combining this and (and ), we obtain .

Next, we consider (2). From (2), there exist such that

Here, without loss of generality, we may assume the following:

Let be an element of . Assume that there exists such that

Note that . In addition, there exists such that . Therefore, .

Similarly, assume that at least one of the following inequalities holds for any :

| (29) |

Here, if , from lemma’s assumption it holds that . Moreover, we define . Then, the following holds:

Furthermore, from the definition of , it holds that . Thus, noting that , we get . By combining these, we have . This implies that . On the other hand, if , from (29) we get . Therefore, from lemma’s assumption, we obtain . By using (29) again, we have . Hence, by repeating these procedures, we get and . Finally, noting that

we get . ∎

By using these lemmas, we prove Theorem 4.2.

Proof.

First, we prove that the algorithm terminates after at most iterations where is the positive integer satisfying . From the definition of , noting that and , we have

and

Then, for any , it holds that

| (30) |

and

| (31) |

Here, let be an element of . Then, from the definition of , for any , at least one of the following inequalities holds:

Thus, from (30) and (31), for any , it holds that . This implies that . Similarly, if , there exists such that for any . On the other hand, from Lemma A.5, there exists such that . Moreover, from (30) and (31), satisfies . However, it contradicts the definition of . Hence, we get .

Hereafter, we assume that (13), (22) and (23) hold. From the definition of , we obtain

This implies that

Therefore, from (15), (21), (22) and (23), we get

Hence, from (24) and (25), it holds that

| (32) |

Here, let be a positive integer such that the right hand side in (32) is less than or equal to . Then, there exists a positive integer such that and . Therefore, we have and . This means that the algorithm terminates after at most iterations.

Next, under (13) we show that is the -accurate Pareto set when and . First, we prove . Let be an element of . For any , it holds that because . Furthermore, noting that , for any , there exists such that . In addition, since , from the definition of , at least one of the following inequalities holds:

By combining this and , we get . Therefore, under (13) at least one of the following inequalities holds for any :

Moreover, it is clear that . Hence, from Lemma A.6, we get .

Finally, we show that for any , there exists such that . When , the existence of is obvious because . On the other hand, when , since there exists such that . Thus, under (13), this implies that . Hence, for any , there exists such that . From this and , we have that is the -accurate Pareto set. Here, note that (13), (22) and (23) hold with probability at least . Therefore, we get the desired result. ∎

Appendix B Extension to Constraint Optimization Problem

In real applications, there exists a situation where the known tolerance level for the value of the function is defined. For example, in the parameter tuning of an engineering system, this situation corresponds to the case where the variance of the performance must be below a certain level. In such a situation, it is necessary to treat the functions and as in the following constrained optimization problem:

where is a user-specified known threshold parameter. Moreover, in order to show theoretical guarantees, for a non-negative vector , we define an -accurate solution as a solution satisfying

Proposed Algorithm

First, we define and as

Here, we define if . Note that an element in the complement of or is not an -accurate solution with high probability. In addition, is a set that is determined to be a feasible region with high probability. Based on these definitions, we define a latent optimal solution set at the th step as follows:

In our proposed algorithm, we select the most uncertain point in the latent optimal solution set . In other words, the observation point at the th step is selected by using as defined by Equation (8) as follows:

| (33) |

Furthermore, if at the th step, then we define the estimated optimal solution by . In order to ensure that is an -accurate solution, the uncertainties of the function values and for the latent optimal solution should be sufficiently small. In the proposed method, the algorithm terminates at the th step which satisfies the following:

The pseudo code of the proposed method is shown as Algorithm 3.

Theoretical Analysis

For Algorithm 3, the following theorem holds:

Theorem B.1.

Let be a positive-definite kernel, and let with . Also let and , and define . Then, with probability at least , the following 1. and 2. hold:

- 1.

-

Algorithm 3 terminates after at most iterations, where is the smallest positive integer satisfying

Here, , and .

- 2.

-

If exists, then at the termination step . Moreover, is an -accurate solution.

Proof.

Assume that (13), (22) and (23) hold. Then, by using the same argument as in the proof of Theorem 4.2, we get

| (34) |

Here, from the definition of , the right-hand side of (34) is less than or equal to . Hence, there exists a positive integer such that . This implies that the algorithm terminates after at most iterations.

Next, we prove claim 2 of the theorem. Assume that exists. Here, we consider the two cases and . For case , since (13) holds, the following inequality holds:

This means that . Therefore, we have . Furthermore, noting that and , it holds that

| (35) | ||||

| (36) |

Here, if , then from (36), we get . Thus, from (13), we obtain . However, this contradicts the definition of , implying that and . Moreover, from (35) the following holds:

In addition, from the definition of , we have

On the other hand, if , then . Thus, from the definition of , it holds that . Therefore, we get

Furthermore, since , it holds that

Therefore, if exists, then we have and

| (37) | ||||

| (38) |

Note that (37) and (38) imply that is an -accurate solution when (13) holds. Finally, since (13), (22) and (23) hold with probability at least , we have Theorem B.1. ∎

Appendix C Details of Section 3.3

C.1 Noisy Input Setting

In this subsection, we consider the setting where the input contains a noise . Let be an input space for optimization. In addition, assume that is a finite set. Furthermore, let be a compact and convex set, and let be a random noise satisfying . Moreover, let be a black-box function on , and let be a positive-definite kernel with and .

For each step , we select an observation point , and the observed value is obtained as . Here, is the independent normal distribution , and is the observed value of .

In this setting, the expected value and variance of with respect to are given by

| (39) | ||||

| (40) |

where is a known probability density function of . Similarly as in (5), using (39) and (40) we define the optimization objective functions and . In addition, let , and denote the posterior mean, posterior variance and confidence bound of at the step , respectively.

Confidence Bound

Confidence bounds of objective functions and defined by using (39) and (40) can also be constructed by using the same procedure as in 3.1. First, assume that for any . Then, the following holds for any :

Therefore, the confidence bound of can be constructed as using

Similarly, the confidence bound of can be expressed as using

where and are given by

Using and above, we can construct the proposed algorithm in the same procedure.

C.2 Simulator Based Experiment

In this subsection, we consider the setting that can be selected in the optimization phase at each step. Furthermore, we show theoretical guarantees in this setting. Hereafter, we only discuss the multi-task scenario, but the same argument can be made for multi-objective and constraint optimization scenarios by selecting and in the same procedure.

In our proposed algorithm, at the step is selected by

In this algorithm, the following theorem holds:

Theorem C.1.

Let be a positive-definite kernel, and let with . Also let , , and define . Moreover, for any , define . Then, when the proposed algorithm in the simulator based setting is performed, is the -accurate solution with probability at least , where is the smallest positive integer satisfying

Here, and are given by and .

Proof.

Assume that (13) holds. Then, from Lemma A.1 we have

In addition, from the definition of , it holds that

Hence, we get

Furthermore, from (24) and (25), we obtain

Finally, by using the same argument as in the proof of Theorem 4.1, the following inequality holds:

Therefore, noting that the definition of , we get the desired result. ∎

Noisy Input Extension

Here, we extend the setting defined in subsection 3.3.2 to the simulator based setting. Since there is the noise instead of , we consider the observation point at the step as , where is given by

Then, similar theorems as in Theorem C.1 hold. However, the practical performance of this algorithm is not much different from that of Uncertainty Sampling, which was used as the base method in numerical experiments. For this reason, in the simulator based noisy input setting, we propose a method for selecting as follows:

In order to derive similar convergence results as in Theorem C.1, we assume that the probability density function of is a bounded function on , i.e., .

Theorem C.2.

Let , , and set . For any , define . Moreover, assume that . Then, when the proposed algorithm in the simulator based noisy input setting is performed, is the -accurate solution with probability at least , where is the smallest positive integer satisfying

Here, and are given by and .

Appendix D Extension to Continuous Set

In this section, we consider the setting where is a continuous set. First, in MT-MVA-BO, can be calculated by using a continuous optimization solver. However, in MO-MVA-BO, it is difficult to calculate the estimated Pareto set and set of latent optimal solutions . In this paper, based on [5] we extend the proposed algorithm by using a discretization set of .

Hereafter, let . Furthermore, assume that is an -Lipschitz continuous function, i.e., there exists such that

for any . Note that Lipschitz continuity holds if standard kernels are used [24, 31].

From Lipschitz continuity of , the following lemmas about and hold:

Lemma D.1.

Proof.

From the definition of and Lipschitz continuity of , the following inequality holds:

∎

Lemma D.2.

Let be an -Lipschitz continuous function, , and define as in (5). Then, the following inequality holds for any :

Proof.

From Lipschitz continuity of , for any , , it holds that

Here, if , then

On the other hand, if , it holds that . Therefore, for any , the desired inequality holds. ∎

Moreover, the following lemma holds:

Lemma D.3.

Let be the Pareto front for , and let be a positive vector. Define

Then, it holds that

Proof.

First, we show . Let be an element of . Then, there exists such that

Here, for any , satisfies or . If , from we get

On the other hand, if , then satisfies because the inequality implies that . However, it contradicts that . From and , we have

Therefore, it holds that . This implies that .

Next, we show . It is clear that . Thus, we only show that . Let be an element of . If , it holds that . On the other hand, if , at least one of the following inequalities holds for any :

If there exists such that , then . Next, we consider the case that for any . Let . Here, assume that for any . Then, from continuity of , there exists such that and . However, it contradicts . Hence, there exists an element such that . Moreover, there exists such that . This implies that there exist and such that , and . Therefore, it holds that . ∎

Next, we explain the method of constructing . Let be a set of grid points when each dimension of is divided into evenly spaced segments. Also let be a point closest to with respect to the -distance. Then, it holds that

| (41) |

In the proposed algorithm for the continuous set setting, Algorithm 2 is performed by using instead of . Then, we define the estimated Pareto set , latent Pareto set and uncertain set in Algorithm 2 as

Note that , not is used to calculate and .

In the algorithm using , the following theorem holds:

Theorem D.1.

Let , and let , where and . Define and . Then, the following (1) and (2) hold with probability at least :

- (1)

-

The algorithm terminates after at most iterations, where is the smallest positive integer satisfying

Here, and are given by and .

- (2)

-

When the algorithm is terminated, the estimated Pareto set is the -accurate Pareto Set.

Proof.

We omit the proof of (1) because its proof is the same as in the proof of Theorem 4.2. We only prove (2). From (41) and Lemma D.1–D.2, the following holds for any :

| (42) | ||||

| (43) |

Assume that (13) holds. Let be a Pareto front for . Then, for any , it holds that

| (44) |

where is the Pareto front for . Similarly, let

Then, for any , there exists such that

Here, from (42) and (43) we have

Thus, it holds that and . This implies that

Here, since is the open set, noting that we get , where is the interior of . In addition, from the definition of the interior and boundary (frontier), we obtain . Therefore, from and , it holds that . Hence, for any , . Thus, by using this and (44), from Lemma D.3, it holds that

Hence, for any , there exists such that

| (45) |

Furthermore, from Theorem 4.2, for any , there exists such that

By combining this and (45), we get

Therefore, we have .