Ridge Regression Revisited:

Debiasing, Thresholding and Bootstrap

Abstract

The success of the Lasso in the era of high-dimensional data can be attributed to its conducting an implicit model selection, i.e., zeroing out regression coefficients that are not significant. By contrast, classical ridge regression can not reveal a potential sparsity of parameters, and may also introduce a large bias under the high-dimensional setting. Nevertheless, recent work on the Lasso involves debiasing and thresholding, the latter in order to further enhance the model selection. As a consequence, ridge regression may be worth another look since –after debiasing and thresholding– it may offer some advantages over the Lasso, e.g., it can be easily computed using a closed-form expression. In this paper, we define a debiased and thresholded ridge regression method, and prove a consistency result and a Gaussian approximation theorem. We further introduce a wild bootstrap algorithm to construct confidence regions and perform hypothesis testing for a linear combination of parameters. In addition to estimation, we consider the problem of prediction, and present a novel, hybrid bootstrap algorithm tailored for prediction intervals. Extensive numerical simulations further show that the debiased and thresholded ridge regression has favorable finite sample performance and may be preferable in some settings.

Keywords: Gaussian approximation, high-dimensional data, Lasso, prediction, regression, resampling.

1 Introduction

Linear regression is a fundamental topic in statistical inference. The classical setting assumes the dimension of parameters in a linear model is constant. However, in the modern era, observations may have a comparable or even larger dimension than the number of samples. To perform a consistent estimation with high-dimensional data, statisticians often assume the underlying parameters are sparse (i.e., the parameter vector contains lots of zeros), and proceed with statistical inference based on this assumption.

The success of the Lasso in the setting of high-dimensional data can be attributed to its conducting an implicit model selection, i.e., zeroing out regression coefficients that are not significant; see Tibshirani [1]. More recent work includes: Meinshausen and Bühlmann [2], Meinshausen and Yu [3], and van de Geer [4] for the Lasso estimator’s (model-selection) consistency and applications; Chatterjee and Lahiri [5], [6], Zhang and Cheng [7], and Dezeure et al. [8] for confidence interval construction and hypothesis testing; and Javanmard and Montanari [9], Fan and Li [10], and Chen and Zhou [11] for improvements of the Lasso estimator. Although the Lasso has the desirable property of zeroing out some regression coefficients, van de Geer et al. [12] proposed to further threshold the estimated coefficients, leading to a sparser fitted model. Furthermore, Javanmard and Montanari [13], and Dezeure et al. [8], proposed to debias the Lasso in constructing confidence intervals. See van de Geer [14] and Javanmard and Javadi [15] for recent works of debiased Lasso.

An alternative approach providing consistent estimators for a high dimensional linear model is the so-called post-selection inference. It first applies Lasso to select influential parameters, then fits an ordinary least squares regression on the selected parameters; see Lee et al. [16], Liu and Yu [17], and Tibshirani et al. [18]. We refer to Bühlmann and van de Geer [13] for a comprehensive overview of the Lasso method for high dimensional data.

Ridge regression is a classical method, and its estimator has a closed-form expression, making statistical inference easier than Lasso. However, there is relatively little research on the ridge regression under the high-dimensional setting. Shao and Deng [19] proposed a threshold ridge regression method and proved its consistency. Dai et al. [20] introduced a broken adaptive ridge estimator to approximate penalized regression. Dobriban and Wager [21] derived the limit of high dimensional ridge regression’s expected predictive risk. Bühlmann [22] used Lasso to correct the bias in a ridge regression estimator, while Lopes [23] applied a residual-based bootstrap to construct confidence intervals.

Three issues have prevented ridge regression from being suitable for a high dimensional linear model:

1. The ridge regression cannot preserve/recover sparsity. Typically, a ridge regression estimator of the parameter vector will not contain any zeros, even though the parameters may be sparse.

2. Bias in the ridge regression estimator can be large. To illustrate this, suppose the parameter of interest is in a linear model ; here, the dimension (the sample size), has rank , and is a known vector. The ridge estimator is with , for some , with denoting the -dimensional identity matrix. Performing a thin singular value decomposition (as in Theorem 7.3.2 in Horn and Johnson [24]), and assuming the error vector consists of independent identically distributed (i.i.d.) components, the bias and the standard deviation can be calculated (and controlled) as follows:

| (1) | |||

In the above, is the smallest singular value of , and is the Euclidean norm of a vector. If does not have a bounded order, the bias may tend to infinity. Another critical problem is that the absolute value of the bias can be significantly larger than the standard deviation, which makes constructing confidence intervals difficult.

3. When the dimension of parameters is larger than the sample size, ridge regression estimates the projection of parameters on the linear space spanned by rows of (Shao and Deng [19]). The projection (which can now be considered to be the ‘parameters’ of the linear model) is not sparse, bringing extra burdens for statistical inference.

The third issue comes from the nature of ridge regression, and it is not necessarily bad; our section 6 provides an example to illustrate this. The first two issues can be solved by thresholding and debiasing respectively, yielding an improved ridge regression that will be the focus of this paper. If the Lasso is in need of thresholding and debiasing –as van de Geer et al. [12], Dezeure et al. [8], and Bühlmann and van de Geer [13] seem to suggest– then it loses some of its attractiveness, in which case (improved) ridge regression may be worth another look. If (improved) ridge regression turns out to have comparable performance to threshold Lasso, then the former would be preferable since it can be easily computed using a closed-form expression. Indeed, numerical simulations in section 6 indicate that improved ridge regression has favorable finite-sample performance, and has a further advantage over the Lasso: it is robust against a non-optimal choice of the hyperparameters.

Apart from point estimation using improved ridge regression, this paper presents a Gaussian approximation theorem for the improved ridge regression estimator. Applying this result, we propose a wild bootstrap algorithm to construct a confidence region for with a known matrix and/or test the null hypothesis with a known vector, versus the alternative hypothesis . The wild bootstrap was developed in the 1980s by Wu [25] and Liu [26]; its applicability to high-dimensional problems was recognized early on by Mammen [27]. Here we will use the wild bootstrap in its Gaussian residuals version that has been found useful in high-dimensional regression; see Chernozhukov et al. [28]. Estimating and testing are important problems in econometrics, e.g., Dolado and Lütkepohl [29], Sun [https://urldefense.com/v3/__https://doi.org/10.1111/j.1368-423X.2012.00390.x__;!!Mih3wA!Q9aoQVO8cn4eWInRmrOzFAYeiX19a7xKzrpyC3_noHS-Dc6SZcpIQu17FxU-vidS2g$], [30], and Gonçalves and Vogelsang [31]. Besides, estimating directly contributes to prediction, which is an important topic in modern age statistics.

Finally, we consider statistical prediction based on the improved ridge regression estimator for a high-dimensional linear model. For a regression problem, quantifying a predictor’s accuracy can be as important as predicting accurately. To do that, it is useful to be able to construct a prediction interval to accompany the point prediction; this is usually done by some form of bootstrap; see Stine [32] for a classical result, and Politis [33] for a comprehensive treatment of both model-based and model-free prediction intervals in regression. As an alternative to the bootstrap, conformal prediction may be a tool to yield prediction intervals; see e.g. Romano et al. [34] and Romano et al. [35]. In our point of view, however, the bootstrap is preferable as it captures the underlying variability of estimated quantities; Section 5 in what follows gives the details.

The remainder of this paper is organized as follows: Section 2 introduces frequently used notations and assumptions. Section 3 presents the consistency result and the Gaussian approximation theorem for the improved ridge regression estimator. Section 4 constructs a confidence region for , and tests the null hypothesis versus the alternative hypothesis via a bootstrap algorithm. Section 5 constructs bootstrap prediction intervals in our ridge regression setting using a novel, hybrid resampling procedure. Finally, Section 6 provides extensive simulations to illustrate the finite sample performance, while Section 7 gives some concluding remarks; technical proofs are deferred to the Appendix.

2 Preliminaries

Our work focuses on the fixed design linear model

| (2) |

where the (unknown) parameter vector is -dimensional, and the fixed (nonrandom) design matrix is assumed to have rank . Define the known matrix of linear combination coefficients as so that has rows. The linear combination of interest are .

Perform a thin singular value decomposition as in Theorem 7.3.2 in Horn and Johnson [24]; here, and respectively is and orthonormal matrices that satisfy , where denotes the identity matrix. Furthermore, , and are positive singular values of .

Denote as the orthonormal complement of ; then we have

| (3) |

in the above, is the matrix having all elements . Define and , then , . According to Shao and Deng [19], the ridge regression estimates rather than .

Define , so . If the design matrix has rank , then does not exist. In this situation, we define , the dimensional vector with all elements . For a threshold , define the set . After selecting a suitable , define

| (4) |

Define as

| (5) |

We will use the standard order notations and . For two numerical sequences , we say if a constant such that for all , and if . For two random variable sequences , we say if for any , a constant such that ; and if ; see e.g. Definition 1.9 and Chapter 1.5.1 of Shao [36]. All order notations and convergences in this paper will be understood to hold as the sample size .

For a finite set , denotes the number of elements in . Notations and denote “there exists” and “for all” respectively. and respectively represent probability and expectation in the “bootstrap world”, i.e., they are the conditional probability and the conditional expectation .

Suppose is a cumulative distribution function and ; then the quantile of is defined as

| (6) |

In particular, given some order statistics , the sample quantile is defined as

| (7) |

Other notations will be defined before being used. Without being explicitly specified, the convergence results in this paper assume the sample size .

The high dimensionality in this paper comes from two aspects: the number of parameters may increase with the sample size , and (for statistical inference/hypothesis testing) the number of simultaneous linear combinations and can also increase with .

Our work adopts the following assumptions:

Assumptions

1. Assume a fixed design, i.e., the design matrix is deterministic. Also assume that there exist constants , , such that the positive singular values of satisfy

| (8) |

Furthermore, the Euclidean norm of is assumed to satisfy with .

2. The ridge parameter satisfies with a positive constant such that

3. The errors driving regression (2) are assumed to be i.i.d., with , and for some .

4. The dimension of the parameter vector satisfies for some constant where are as defined in Assumptions 1–3. Furthermore, the threshold is chosen as with constants and . We assume a constant such that , and .

5. (defined in (4)) is not empty and with where are as defined in Assumptions 1–3. Besides, assume constants such that for all . Also assume

| (9) |

6. a constant satisfying such that

| (10) |

7. , the matrix has rank , and one of the two following conditions holds true:

7.1.

| (11) |

7.2. and

| (12) | |||

Remark 1

The intuitive meaning of assumption 4 is that the s that are not being truncated should be significantly larger than the being truncated. Furthermore, note that

| (13) |

Therefore, assumption 7 implies that no single element in the matrix dominates the others. We use to prevent the normalizing parameters from being . We do not require that the design matrix has rank or that . However, when these conditions are not satisfied, the sparsity of , i.e., assumption 6, can be violated. Section 6 uses a numerical simulation to illustrate this problem.

3 Consistency and the Gaussian approximation theorem

Throughout, we will use the notations developed in section 2. For a chosen ridge parameter , define the classical ridge regression estimator and the de-biased estimator as

| (14) | |||

Then we have

| (15) |

Similar to , define the set , the estimator and as

| (16) |

Then, and constitute the improved, i.e., debiased and thresholded, ridge regression estimator for the parameter vector and respectively. Apart from parameter estimation, we need to estimate the error variance . The estimator for is

| (17) |

Theorem 1

2. Suppose assumptions 1 to 6 hold true. Then

| (19) |

Define and as

| (20) | |||

| Here are independent normal random variables with mean and variance . |

(defined in (4)) and may grow as the sample size increases. In this case, the estimator does not have an asymptotic distribution. However, the cumulative distribution function of still can be approximated by (whose expression changes as the sample size increases as well). Define as the quantile of ; theorem 2 implies that the set

| (21) |

is an asymptotically valid % confidence region for the parameter of interest .

Theorem 2

4 Bootstrap inference and hypothesis testing

An obstacle for constructing a practical confidence region or testing a hypothesis via theorem 2 are the unknown , , and . Besides, is too complicated to have a closed-form formula. Fortunately, statisticians can simulate normal random variables on a computer, so they may use Monte-Carlo simulations to find the quantile of . Based on this idea, this section develops a wild bootstrap algorithm similar to Mammen [27] and Chernozhukov et al. [28] for the following tasks: constructing the confidence region for the parameter of interest ; and testing the null hypothesis (for a known ) versus the alternative hypothesis . Similar to Zhang and Cheng [7], Chernozhukov et al. [28], and Zhang and Wu [37], we use the maximum statistic to construct a simultaneous confidence region.

Algorithm 1 (Wild bootstrap inference and hypothesis testing)

Input: Design matrix , dependent variables , linear combination matrix , ridge parameter , threshold , nominal coverage probability , number of bootstrap replicates

Additional input for testing:

2. Generate i.i.d. errors with having normal distribution with mean and variance , then calculate and ( is defined in section 2).

3. Calculate and .

4. Calculate and with for .

5. Calculate , , and such that

| (23) |

6.a (For constructing a confidence region) Repeat steps 2 to 5 for times to generate ; then calculate the sample quantile of . The confidence region for the parameter of interest is given by the set

| (24) |

6.b (For hypothesis testing) Repeat steps 2 to 5 for times to generate ; then calculate the sample quantile of . Reject the null hypothesis when

| (25) |

As in section 2, if has rank , we define , the dimensional vector with all elements .

According to theorem 1.2.1 in Politis et al. [38], the consistency of algorithm 25 –either for asymptotic validity of confidence regions or consistency of the hypothesis test– is ensured if

| (26) |

where is the quantile of the conditional distribution ; we prove this in theorem 3 below.

Theorem 3

Theorem 3 has two implications. On the one hand, the confidence region introduced in step 6.a of algorithm 25 is asymptotically valid, i.e., its coverage tends to . On the other hand, consider the hypothesis test of step 6.b of algorithm 25; Theorem 3 implies that, if the null hypothesis is true, them the probability for incorrectly rejecting the null hypothesis is asymptotically , i.e., the test is consistent.

5 Bootstrap interval prediction

Given our data from the linear model , consider a new regressor matrix , i.e., a collection of regressor (column) vectors that happen to be of interest; as with itself, is assumed given, i.e., deterministic. The prediction problem involves (a) finding a predictor for the future (still unobserved) vector , and (b) finding a prediction region so that as the (original) sample size . Here are i.i.d. errors with the same marginal distribution as , and is independent with .

The predictor of that is optimal with respect to total mean squared error is ; since is unknown, we can estimate it by as in (16), yielding the practical predictor . However, finding a prediction region for is more challenging. We adopt definition 2.4.1 of Politis [33], and define a consistent prediction region in terms of conditional coverage as follows.

Definition 1 (Consistent prediction region)

A set is called a consistent prediction region for the future observation if

| (28) |

Note that the convergence (28) is “in probability” since is a function of , and therefore random; see also Lei and Wasserman [39] for more on the notion of conditional validity.

Other authors, including Stine [32], Romano et al. [34], and Chernozhukov et al. [40], considered another definition of prediction interval consistency focusing on unconditional coverage, i.e., insisting that

| (29) |

However, the conditional coverage of definition 28 is a stronger property. To see why, define the random variables , noting that has dimension . Then, the boundedness of can be invoked to show that if , then as well. Hence, (28) implies (29); see Zhang and Politis [41] for a further discussion on conditional vs. unconditional coverage.

Consider the prediction error . If we can put bounds on the prediction error that are valid with conditional probability (asymptotically), then a consistent prediction region ensues. Note that the prediction error has two parts: and . Although the latter may be asymptotically negligible, it is important in practice to not approximate it by zero as it would yield finite-sample undercoverage; see e.g. Ch. 3 of Politis [33] for an extensive discussion.

Theorem 2 indicates that the asymptotically negligible estimation error can be approximated by normal random variables. On the other hand, the non-negligible error may not have a normal distribution; so in order to approximate the distribution of , we need to estimate the errors’ marginal distribution as well.

This section requires some additional assumptions.

Additional assumptions

8. The cumulative distribution function of errors is continuous

9. The number of regressors of interest is bounded, i.e.,

Since is increasing and bounded, if is continuous, then is uniformly continuous on . this property is useful in the proof of lemma 30.

Lemma 1

Suppose assumption 1 to 6 and 8 hold true. Define the residuals , as well as the centered residuals with . If we let , then

| (30) |

We emphasize that the dimension of parameters in lemma 30 can grow to infinity as long as assumption 4 is satisfied. Furthermore, the validity of lemma 30 –as well as that of theorem 4 that follows– does not require assumption 7.

We will resample the centered residuals (in other words, generate random variables with distribution ) in algorithm 31. Lemma 30 will ensure that the centered residuals can capture the distribution of the non-negligible errors.

For a high dimensional linear model, lemma 30 is not an obvious result; see Mammen [42] for a detailed explanation. Lemma 30 is the foundation for a new resampling procedure as follows; this is a hybrid bootstrap as it combines the residual-based bootstrap to replicate the new error with the normal approximation to the estimation error .

Algorithm 2 (Hybrid bootstrap for prediction region)

Input: Design matrix , dependent variables , a new linear combination matrix , ridge parameter , threshold , nominal coverage probability , the number of bootstrap replicates

2. Generate i.i.d. errors with having normal distribution with mean and variance . Then generate i.i.d. errors with having cumulative distribution function defined in lemma 30. Calculate .

3. Calculate and . Then derive , with for .

4. Calculate and . Define .

5. Repeat steps 2 to 4 for times, and generate . Calculate the sample quantile of . Then, the prediction region for is given by

| (31) |

If the design matrix has rank , then is defined to be .

Similar to section 4, here we define as the quantile of the conditional distribution , which can be approximated by by letting . Theorem 4 below proves as the sample size , which justifies the consistency of the prediction region (31).

Theorem 4

Suppose assumptions 1 to 6 and 8 to 9 hold true(here consider in assumption 5 as ). Then

| (32) |

For any fixed , it follows that

| (33) |

Note that the bootstrap probability is probability conditional on the data , thus justifying the notion of conditional validity of our definition 28.

6 Numerical Simulations

We define and the following four terms

| (34) |

see section 2 for the meaning of notations in the above. Assumptions 5 and 6 imply that these terms converge to 0 as the sample size . Indeed, if one of the is large, the debiased and threshold ridge regression estimator may have a large bias, which affects the performance of the bootstrap algorithms.

In this section, we generate the design matrix , the linear combination matrix , and the parameters through the following strategies:

Design matrix : define with . Generate as

i.i.d. normal random vectors with mean and covariance matrix .

We choose with diagonal elements equal to and off-diagonal equal to .

| (35) |

and when : choose in (35). Generate as i.i.d. normal with mean and variance , and generate as i.i.d. normal with mean and variance . Use for ; for ; and for . Choose with , , , , , and otherwise.

and when : choose in (35). Generate as i.i.d. normal with mean and variance , and generate as i.i.d. normal with mean and variance . Use for ; and for . Choose , , and otherwise. When , may not be identifiable [19], and may not equal (defined in section 2) despite . We consider both situations and evaluate the performance of proposed methods on the linear model and . We fix and in each simulation.

The different regression algorithms considered are the debiased and threshold ridge regression(Deb Thr), the ridge regression, Lasso, threshold ridge regression (Thr Ridge), threshold Lasso (Thr Lasso), and the post-selection algorithms, i.e., Lasso + OLS (Post OLS), and Lasso + Ridge (Post Ridge). We consider 6 cases for simulation involving a different ratio, and Normal vs. Laplace (2-sided exponential) errors; we present detailed information about each simulation case in table 1, compare the performance of different regression algorithms in figure LABEL:Figure1, and record the performance of bootstrap algorithms on estimation/hypothesis testing and interval-prediction in table 2. The optimal ridge parameter and threshold are chosen by 5-fold cross validation. To adapt to assumption 9, we choose as the first 100 lines of for prediction.

| Case | Residual | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 1000 | 500 | Normal | 800 | 300 | 12.978 | 56.453 | 0.343 | 1.370 | 0.0 | 0.013 | 1.712 |

| 2 | 1000 | 500 | Laplace | 800 | 300 | 12.561 | 36.728 | 0.354 | 1.636 | 0.0 | 0.014 | 1.769 |

| 3 | 1000 | 650 | Laplace | 800 | 300 | 8.226 | 56.432 | 0.396 | 1.553 | 0.0 | 0.016 | 3.085 |

| 4 | 1000 | 500 | Laplace | 800 | 700 | 12.847 | 55.317 | 0.346 | 1.510 | 0.0 | 0.014 | 1.730 |

| 5 | 1000 | 1500 | Normal | 800 | 300 | 9.766 | 1.201 | 0.228 | 6.938 | 129 / 0.0 | 8.214 | 3.962 |

| 6 | 1000 | 1500 | Laplace | 800 | 300 | 9.766 | 1.201 | 0.228 | 6.938 | 129 / 0.0 | 8.214 | 3.962 |

Case 5 and 6 consider both the linear model and , here . The difference in and affects the value of (but does not affect others), so we have two values in table 1.

Figure LABEL:Figure1 plots the Euclidean norm , with defined in (16), and defined in Section 2, for various linear regression methods. When the underlying linear model is sparse, thresholding decreases the ridge regression estimator’s error(from around 10 to around 2 in our experiment). However, the performance of the threshold ridge regression method is sensitive to the ridge parameter , i.e., can be significantly larger than its minimum despite is close to the minimizer of .

In reality, cross validation does not necessarily guarantee selection of the optimal , so it is risky to use the threshold ridge regression method. Debiasing helps decrease the ridge regression estimator’s error; more importantly, it is robust to changes in the choice of . Even if a cross validation selects a sub-optimal , the error of the debiased and threshold ridge regression estimator does not surge, and the estimator’s performance does not notably deteriorate. Therefore, we consider the debiased and threshold ridge regression as a practical method to handle real-life data.

Thresholding also helps improve the performance of Lasso, especially when the Lasso parameter is small. However, when the Lasso parameter becomes large, Lasso method already recovers the underlying sparsity of the linear model, and thresholding becomes unnecessary.

When the dimension of parameters is greater than the sample size , both parameters and (see section 2) could be considered as the ‘parameters’ for the linear model. Lasso methods estimate linear combinations of , while ridge regression methods estimate linear combinations of . Under this situation, the difference between and is the main factor for the estimators’ error. In reality, statisticians cannot distinguish between and based on data. So they need to design which parameters to estimate a priori and select a suitable regression method (e.g., Lasso, ridge regression, or their variations) reflecting their preferences.

As a summary of Figure LABEL:Figure1, apart from having a closed-form formula, the debiased and threshold ridge regression has the smallest estimation error among all ridge regression variations, and has comparable performance to the threshold Lasso. Furthermore, it is not overly sensitive on changes in the ridge parameter . Therefore, even when a sub-optimal is selected, the performance of the debiased and threshold ridge regression is not severely affected. When , this method (and other ridge regression methods) considers rather than to be the parameter of the linear model. So, in this case, ridge regression methods are suitable if the underlying linear model is indeed (in other words, the projection does not have effect on the parameters of the linear model).

Table 2 records the average errors of the proposed statistics (defined in (16)), (defined in (17)), and the coverage probability of the confidence region (24) as well as the coverage probability of the prediction region (31), in 1000 numerical simulations. We also record the frequency of model misspecification(i.e., ), . When the sample size is greater than the dimension of parameters , thresholding is likely to recover the sparsity of the parameters. In all these cases, i.e., Case 1–4, our confidence intervals achieve near-perfect coverage. The slight under-coverage in prediction intervals is a well-known phenomenon; see e.g. Ch. 3.7 of Politis [33].

However, in cases 5 and 6 where , is not necessarily sparse, and model misspecification may happen. Notably, ’s error in estimating linear combinations of does not surge even when . However, the difference between and introduces a large bias to . Besides, when , assumption 6 can be violated. Correspondingly the variance estimator may have a large error. The difference between and invalidates the confidence region (24). For prediction region (31), this problem still exists. However, the prediction region catches non-negligible errors apart from the asymptotically negligible errors and it is wider than the confidence region. Consequently, as long as the absolute values of difference are small, the prediction interval’s performance will not be severely affected.

| Estimation and Confidence region construction | Prediction | ||||

| Case | coverage | coverage | |||

| 1 | 0.185 | 0.144 | |||

| 2 | 0.183 | 0.228 | |||

| 3 | 0.209 | 0.232 | |||

| 4 | 0.191 | 0.224 | |||

| 5(use ) | 1.580 | 1.351 | |||

| 5(use ) | 0.259 | 1.349 | |||

| 6(use ) | 2.259 | 1.353 | |||

| 6(use ) | 0.260 | 1.352 | |||

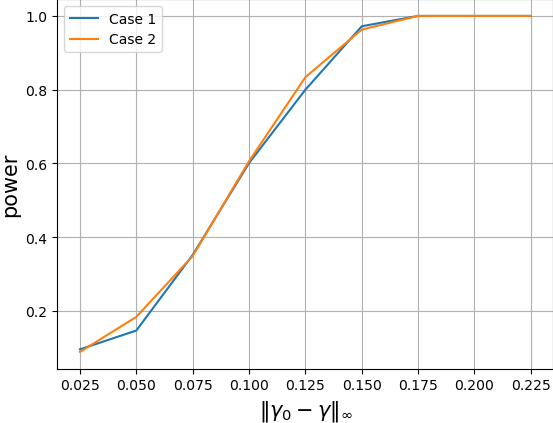

Figure 2 plots the power curve of the hypothesis test of versus ; here, we use and .

7 Conclusion

The paper at hand proposes an improved, i.e., debiased and thresholded, ridge regression method that recovers the sparsity of parameters and avoids introducing a large bias. Besides, it derives a consistency result and the Gaussian approximation theorem for the improved ridge estimator. An asymptotically valid confidence region for and a hypothesis test of are also constructed based on a wild bootstrap algorithm. In addition, a novel, hybrid resampling procedure was proposed that can be used to perform interval prediction based on the improved ridge regression.

Numerical simulations indicate that improved ridge regression has comparable performance to the threshold Lasso while having at least two major advantages: (a) Ridge regression is easily computed using a closed-form expression, and (b) it appears to be quite robust against a non-optimal choice of the ridge parameter . Therefore, ridge regression may be found useful again in applied work using high-dimensional data as long as practitioners make sure to include debiasing and thresholding.

References

- [1] Robert Tibshirani. Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society: Series B (Methodological), 58(1):267–288, 1996.

- [2] Nicolai Meinshausen and Peter Bühlmann. High-dimensional graphs and variable selection with the lasso. Ann. Statist., 34(3):1436–1462, 06 2006.

- [3] Nicolai Meinshausen and Bin Yu. Lasso-type recovery of sparse representations for high-dimensional data. Ann. Statist., 37(1):246–270, 02 2009.

- [4] Sara A. van de Geer. High-dimensional generalized linear models and the lasso. Ann. Statist., 36(2):614–645, 04 2008.

- [5] A. Chatterjee and S. N. Lahiri. Asymptotic properties of the residual bootstrap for lasso estimators. Proceedings of the American Mathematical Society, 138(12):4497–4509, 2010.

- [6] A. Chatterjee and S. N. Lahiri. Bootstrapping lasso estimators. Journal of the American Statistical Association, 106(494):608–625, 2011.

- [7] Xianyang Zhang and Guang Cheng. Simultaneous inference for high-dimensional linear models. Journal of the American Statistical Association, 112(518):757–768, 2017.

- [8] Ruben Dezeure, Peter Bühlmann, and Cun-Hui Zhang. High-dimensional simultaneous inference with the bootstrap. TEST, 26(4):685–719, Dec 2017.

- [9] Adel Javanmard and Andrea Montanari. Debiasing the lasso: Optimal sample size for gaussian designs. Ann. Statist., 46(6A):2593–2622, 12 2018.

- [10] Jianqing Fan and Runze Li. Variable selection via nonconcave penalized likelihood and its oracle properties. Journal of the American Statistical Association, 96(456):1348–1360, 2001.

- [11] Xi Chen and Wen-Xin Zhou. Robust inference via multiplier bootstrap. Ann. Statist., 48(3):1665–1691, 06 2020.

- [12] Sara van de Geer, Peter Bühlmann, and Shuheng Zhou. The adaptive and the thresholded Lasso for potentially misspecified models (and a lower bound for the Lasso). Electronic Journal of Statistics, 5(none):688 – 749, 2011.

- [13] Peter Bühlmann and Sara van de Geer. Statistics for High-Dimensional Data: Methods, Theory and Applications. Springer-Verlag Berlin Heidelberg, 1st edition, 2011.

- [14] Sara van de Geer. On the asymptotic variance of the debiased Lasso. Electronic Journal of Statistics, 13(2):2970 – 3008, 2019.

- [15] Adel Javanmard and Hamid Javadi. False discovery rate control via debiased lasso. Electronic Journal of Statistics, 13(1):1212 – 1253, 2019.

- [16] Jason D. Lee, Dennis L. Sun, Yuekai Sun, and Jonathan E. Taylor. Exact post-selection inference, with application to the lasso. Ann. Statist., 44(3):907–927, 06 2016.

- [17] Hanzhong Liu and Bin Yu. Asymptotic properties of lasso+mls and lasso+ridge in sparse high-dimensional linear regression. Electron. J. Statist., 7:3124–3169, 2013.

- [18] Ryan J. Tibshirani, Alessandro Rinaldo, Rob Tibshirani, and Larry Wasserman. Uniform asymptotic inference and the bootstrap after model selection. Ann. Statist., 46(3):1255–1287, 06 2018.

- [19] Jun Shao and Xinwei Deng. Estimation in high-dimensional linear models with deterministic design matrices. Ann. Statist., 40(2):812–831, 04 2012.

- [20] Linlin Dai, Kani Chen, Zhihua Sun, Zhenqiu Liu, and Gang Li. Broken adaptive ridge regression and its asymptotic properties. Journal of Multivariate Analysis, 168:334 – 351, 2018.

- [21] Edgar Dobriban and Stefan Wager. High-dimensional asymptotics of prediction: Ridge regression and classification. Ann. Statist., 46(1):247–279, 02 2018.

- [22] Peter Bühlmann. Statistical significance in high-dimensional linear models. Bernoulli, 19(4):1212–1242, 09 2013.

- [23] Miles Lopes. A residual bootstrap for high-dimensional regression with near low-rank designs. In Advances in Neural Information Processing Systems 27, pages 3239–3247, 2014.

- [24] Roger A. Horn and Charles R. Johnson. Matrix Analysis. Cambridge University Press, 2012.

- [25] C. F. J. Wu. Jackknife, Bootstrap and Other Resampling Methods in Regression Analysis. The Annals of Statistics, 14(4):1261 – 1295, 1986.

- [26] Regina Y. Liu. Bootstrap Procedures under some Non-I.I.D. Models. The Annals of Statistics, 16(4):1696 – 1708, 1988.

- [27] Enno Mammen. Bootstrap and Wild Bootstrap for High Dimensional Linear Models. The Annals of Statistics, 21(1):255 – 285, 1993.

- [28] Victor Chernozhukov, Denis Chetverikov, and Kengo Kato. Gaussian approximations and multiplier bootstrap for maxima of sums of high-dimensional random vectors. Ann. Statist., 41(6):2786–2819, 12 2013.

- [29] Juan J. Dolado and Helmut Lütkepohl. Making wald tests work for cointegrated var systems. Econometric Reviews, 15(4):369–386, 1996.

- [30] Yixiao Sun. Robust trend inference with series variance estimator and testing-optimal smoothing parameter. Journal of Econometrics, 164(2):345 – 366, 2011.

- [31] Sílvia Gonçalves and Timothy J. Vogelsang. Block bootstrap hac robust tests: the sophistication of the naive bootstrap. Econometric Theory, 27(4):745 – 791, 2011.

- [32] Robert A. Stine. Bootstrap prediction intervals for regression. Journal of the American Statistical Association, 80(392):1026–1031, 1985.

- [33] Dimitris N. Politis. Model-Free Prediction and Regression. Springer-Verlag New York, 2015.

- [34] Yaniv Romano, Evan Patterson, and Emmanuel Candès. Conformalized quantile regression. In Advances in Neural Information Processing Systems, volume 32, pages 3543–3553. Curran Associates, Inc., 2019.

- [35] Yaniv Romano, Matteo Sesia, and Emmanuel Candès. Deep knockoffs. Journal of the American Statistical Association, 115(532):1861–1872, 2020.

- [36] Jun Shao. Mathematical Statistics. Springer-Verlag New York, 2003.

- [37] Danna Zhang and Wei Biao Wu. Gaussian approximation for high dimensional time series. Ann. Statist., 45(5):1895–1919, 10 2017.

- [38] Dimitris N. Politis, Joseph P. Romano, and Michael Wolf. Subsampling. Springer-Verlag New York, 1999.

- [39] Jing Lei and Larry Wasserman. Distribution-free prediction bands for non-parametric regression. Journal of the Royal Statistical Society. Series B (Statistical Methodology), 76(1):71–96, 2014.

- [40] Victor Chernozhukov, Kaspar Wüthrich, and Yinchu Zhu. Distributional conformal prediction, 2019.

- [41] Yunyi Zhang and Dimitris N. Politis. Bootstrap prediction intervals with asymptotic conditional validity and unconditional guarantees. (arXiv:2005.09145), 2021.

- [42] Enno Mammen. Empirical process of residuals for high-dimensional linear models. Ann. Statist., 24(1):307 – 335, 1996.

- [43] Peter Whittle. Bounds for the moments of linear and quadratic forms in independent variables. Theory of Probability & Its Applications, 5(3):302–305, 1960.

- [44] Victor Chernozhukov, Denis Chetverikov, and Kengo Kato. Comparison and anti-concentration bounds for maxima of gaussian random vectors. Probability Theory and Related Fields, 162:47–70, 2015.

- [45] Mengyu Xu, Danna Zhang, and Wei Biao Wu. Pearson’s chi-squared statistics: approximation theory and beyond. Biometrika, 106(3):716–723, 04 2019.

Appendix A Some important lemmas

This section introduces three useful lemmas. Lemma 37 comes from Whittle [43], which directly contributes to the model selection consistency. Lemma 3 and 50 are similar to Chernozhukov et al. [28], they used a joint normal distribution to approximate the distribution of linear combinations of independent random variables.

Lemma 2

Suppose random variables are i.i.d., , and a constant such that . In addition suppose the matrix satisfies

| (36) |

Then a constant which only depends on and such that for ,

| (37) |

Proof.

Lemma 3

Suppose are joint normal random variables with mean , non-singular covariance matrix , and positive marginal variance , . In addition, suppose two constants such that for . Then for any given ,

| (40) |

only depends on and .

Proof of lemma 3.

First for any ,

| (41) |

Therefore, for any ,

| (42) | |||

is also joint normal with mean and marginal variance . From theorem 3 and (18), (19) in [44], by defining , we have

| (43) | |||

Choose , which only depends on . Then

| (44) |

∎

Lemma 4

Suppose are i.i.d. random variables with , and . is an () rank matrix. And constants such that for . is an estimator of and random variables are i.i.d. with having normal distribution . is independent of for . In addition, suppose one of the following conditions:

C1. a constant such that

| (45) |

C2. a constant such that

| (46) |

Then we have

| (47) |

In particular, if , by assuming one of the following conditions,

| (48) |

| (49) |

Then we have

| (50) |

Proof of lemma 50.

In this proof we define with . For , . From lemma A.2 and (8) in [28], and (S1) to (S5) in [45], for and , define

| (51) |

Here . Then is nonincreasing function. with , with , and

| (52) | |||

For any given , define function

| (53) | |||

Define . Direct calculation shows ;

| (54) | |||

Define as i.i.d. random variables with the same marginal distribution as , and is independent of . Therefore, for any . Since . According to (41), (53) and lemma 3, a constant which only depends on and such that for any given ,

| (55) | |||

Define . For any ,

| (56) | |||

Therefore, we have

| (57) |

For any , define , and , we have , and

| (58) | |||

Since , , from multivariate Taylor’s theorem and (54), for any and ,

| (59) | |||

Here with having normal distribution with mean and variance . Then

| (60) | |||

In particular, for any given , choose and suppose . For sufficiently large we have and

| (61) |

Suppose condition C1. For any , such that for sufficiently large ,

| (62) | |||

Choose . According to (60), for sufficiently large , (62) happens and with probability . If (62) happens,

| (63) | |||

For can be arbitrarily small, we prove (47).

Suppose condition C2. For any , there exists such that

| (64) |

Since

| (65) | |||

If (64) happens, by choosing

| (66) | |||

and we prove (47).

If . We choose , (60) can be modified to

| (67) |

Condition C1 implies , and condition C2 implies . The additional proportions in C1 and C2 accommodate the error introduced in estimating errors’ variance. Condition C1 is designed for the situation when the number of linear combinations is as large as the sample size ; and condition C2 can be used when is significantly smaller than .

The difference between lemma 50 and the classical central limit theorem is that can grow as increases. The maximum does not have an asymptotic distribution if . However, if the random variables are mixed well, approximating the distribution of by the distribution of the maximum of normal random variables is still applicable. With the help of lemma 50, we can establish the normal approximation theorem and construct the simultaneous confidence region for (defined in (16)).

Appendix B Proofs of theorems in section 3

This section applies notations in section 2.

Proof of theorem 1.

From (15),

| (70) | |||

From Cauchy inequality,

| (71) | |||

Therefore, for sufficiently large , from assumption 4 and lemma 37

| (72) | |||

Define and . For , if , (15) and (4) imply

| (73) | |||

From (4) and assumption 5, if , then for , so from Cauchy inequality and lemma 37,

| (74) | |||

Here is the constant defined in lemma 37. Combine with assumption 2, assumption 5, and (72), we prove (18).

If , since , we have

| (75) | |||

From assumption 3, . For the second term, from assumption 1 and (71),

| (76) | |||

Since

| (77) | |||

We have . For the third term, from assumption 6. we have

| (78) |

For the fourth term, from Cauchy inequality and (76),

| (79) | |||

For the fifth term,

| (80) |

For the last term,

| (81) | |||

From (18), . So we have

| (82) |

From assumption 2 and 6, we prove the second result. ∎

Define . From assumption 7, since the matrix with and , the matrix

also has rank . The proof of theorem 2 uses this result.

Proof of theorem 2.

From Cauchy inequality and assumption 2, suppose with . For ,

| (83) |

Define for and . From (15), (5), (73) and assumption 5, if , we have and a constant , for any and sufficiently large ,

| (84) | |||

According to theorem 19 and lemma 1, a constant and for any given , for sufficiently large and any ,

| (85) | |||

From assumption 1, 2, 5 and 7, for sufficiently large we have

| (86) | |||

and , here , , and

Define as the quantile of . The density of a multivariate normal random variable with a full rank covariance matrix is positive for . And , the set has positive Lebesgue measure. Therefore, is strictly increasing, and for any , . From theorem 2, for any given ,

| (91) |

as .

Appendix C Proofs of theorems in section 4

Proof of theorem 3.

From assumption 6,

| (94) | |||

Since , . According to (14) and (15), define ,

| (95) | |||

Similar to (74), rewrite in assumption 2 as with , we have

| (96) |

are normal random variables with mean and variance . Therefore , with a normal random variable with mean and variance . If , from (71) and lemma 37, a constant which depends on and such that for any ,

| (97) |

Suppose , , and for a constant . Since if ,

| (98) | |||

From assumption 4, for sufficiently large ,

| (99) |

From (71), lemma 37, assumption 1 and 4, we have

| (100) |

Suppose a constant such that (from lemma 37), and (since ) . From assumption 4, for sufficiently large ,

| (101) | |||

Correspondingly

| (102) | |||

which has order . If , then for . Similar to (83),

| (103) | |||

From theorem 1, for any , constant such that and with probability ,

| (104) |

If , according to lemma 3, assumption 7 and (86), a constant which only depends on such that

| (105) | |||

Function is continuous when , as , and as . So for sufficiently large .

On the other hand, if , then . From lemma 37, we may choose sufficiently large such that , since (Here is a normal random variable with mean and variance ) is a constant for given and , we have

| (106) | |||

Since , from (105) and (106), for any given and sufficiently large ,

| (107) |

As a summary, for any given , a constant such that for sufficiently large , the event , , , for constant and happen with probability . From (103), assumption 5 and lemma 3, we have for any , there exists a constant such that

| (108) | |||

If , then . Therefore, for sufficiently large , from (107) and (102), a constant such that

| (109) | |||

and we prove (27).

Appendix D Proofs of theorems in section 5

Proof of lemma 30.

Define the design matrix , , and . If , for ,

| (113) |

Define . From (52), for any given ,

| (114) | |||

Suppose assumption 1 to 6. From (76), (77), (78) and , for any , a constant such that with probability at least

| (115) | |||

According to Gilvenko-Cantelli lemma, almost surely. Therefore, for any and sufficiently large , . Choose sufficiently small and , from assumption 8. and (115), we prove (30). ∎

Proof of theorem 4.

Define . From theorem 19, since ,

| (116) |

For any given , choose a constant such that for any . Define for any , and for . is continuous according to assumption 8. With probability at least

| (117) | |||

For any and any

| (118) | |||

From (117) and assumption 8

| (119) |

If , , and , then

| (120) |

for some constant . Here . From (102), a constant such that

| (121) |

If ,

| (122) | |||

Form (74) and lemma 37, a constant which only depends on , and for any with a sufficiently large ,

| (123) |

Combine with (121), there exists a constant , with conditional probability at least

| (124) | |||

Since and if , we have

| (125) |

From lemma 30, for any ,

| (126) | |||

as . From theorem 1 and (92) to (94), for any , with probability at least a constant such that for sufficiently large , (120) happens with and . Correspondingly for sufficiently large , with probability at least ,

| (127) | |||

and we prove (32).