definitionDefinition \newdefinitionremarkRemark \newdefinitionexampleExample

[1]This work was partially supported by the National Science Foundation grant CCF-1254218.

[1] \cortext[cor1]Corresponding author

Perturbation expansions and error bounds for the truncated singular value decomposition

Abstract

Truncated singular value decomposition is a reduced version of the singular value decomposition in which only a few largest singular values are retained. This paper presents a novel perturbation analysis for the truncated singular value decomposition for real matrices. First, we describe perturbation expansions for the singular value truncation of order . We extend perturbation results for the singular subspace decomposition to derive the first-order perturbation expansion of the truncated operator about a matrix with rank greater than or equal to . Observing that the first-order expansion can be greatly simplified when the matrix has exact rank , we further show that the singular value truncation admits a simple second-order perturbation expansion about a rank- matrix. Second, we introduce the first-known error bound on the linear approximation of the truncated singular value decomposition of a perturbed rank- matrix. Our bound only depends on the least singular value of the unperturbed matrix and the norm of the perturbation matrix. Intriguingly, while the singular subspaces are known to be extremely sensitive to additive noises, the newly established error bound holds universally for perturbations with arbitrary magnitude. Finally, we demonstrate an application of our results to the analysis of the mean squared error associated with the TSVD-based matrix denoising solution.

keywords:

singular subspace decomposition \septruncated SVD \sepperturbation expansions \seperror bounds1 Introduction

The singular value decomposition (SVD) is an invaluable tool for matrix analysis and the truncated singular value decomposition (TSVD) offers a formal approach for a rank-restricted optimal approximation of matrices by replacing the smallest singular values by zeros in the SVD of a matrix. TSVD has numerous applications in science, engineering, and math with examples including linear system identification [1, 2], collaborative filtering [3, 4], low-rank matrix denoising [5, 6], data compression [7], and numerical partial differential equations [8]. In addition, TSVD is well-known for solving classical discrete ill-posed problems [9, 10]. This paper is concerned with the effects of errors on the truncated singular value decomposition of a matrix.

Perturbation theory for the SVD studies the effect of variation in matrix entries on the singular values and the singular vectors of a matrix. Using perturbation bounds or perturbation expansions, one can characterize the difference between the SVD-related quantities associated with the perturbed matrix and those of the original matrix. The first perturbation bound on singular values was given by Weyl [11] in 1912, stating that no singular value can be changed by more than the spectral norm of the perturbation. Later, Mirsky [12] showed that Weyl’s inequality also holds for any unitarily-invariant norm. Perturbation bounds for singular vectors are often established in the context of singular subspace decomposition. In 1970, Davis and Kahan [13] introduced a fundamental bound on the distance between the subspaces spanned by a group of eigenvectors and their perturbed versions based the ratio between the perturbation level and the eigengap. This result is also referred as the so-called theorem for symmetric matrices in the literature. Shortly afterwards, Wedin [14] generalized part of this result to cover non-symmetric matrices using the singular value decomposition, bounding changes in the left and right singular subspaces in terms of the singular value gap and the perturbation magnitude. In a recent work, Cai and Zhang [15] further established separate matching upper and lower bounds for the left and right singular subspaces. When the structure of the error is concerned, one may draw interest in perturbation expansions to approximate the perturbed quantity as a function of the perturbation matrix. As the perturbation decreases towards zero, the approximation is more accurate since the higher-order terms in the expansion become successively smaller. In 1973, Stewart [16] showed that there exists explicit expression of the perturbed subspaces in the bases of the unperturbed subspaces, which can be leveraged to obtain error bounds for certain characteristic subspaces associated with the SVD. This breakthrough result has started a long line of research on perturbation expansions and error bounds for the SVD, including the work of Stewart [17], Sun [18], Li et al. [19], Vaccaro [20], Xu [21], Liu et al. [22], and more recently, Gratton et al. [23]. Specifically, in [17], Stewart utilized the bounding technique in [16] and obtained a second-order perturbation expansion for the square of the smallest singular value of a matrix. In a different approach based on the theory of implicit functions, Sun [18] provided the first analytical expression for the second-order perturbation expansion of simple non-zero singular values of a matrix. One of the first significant results on perturbation expansion of singular subspaces was introduced by Li and Vaccaro in 1991. In [19], the two authors analyzed a variety of subspace-based algorithms in array signal processing and developed the first-order perturbation expansion for the signal and orthogonal subspaces of the rank-deficient data matrix. Later on, Vaccaro [20] extended this result to the second-order perturbation expansion of these subspaces. A more fine-grained analysis of the perturbation expansion for the individual singular vectors rather than the singular subspaces was given by Liu et al. [22], uncovering the fact that the signal subspace has an impact on the first-order approximation of the individual singular vectors, but not on the first-order approximation of the signal subspace spanned by these vectors. We note that the aforementioned results on perturbation analysis of singular subspaces make an assumption that the unperturbed matrix is rank-deficient, i.e., all singular values corresponding to one of the singular subspaces are zero. In 2002, Xu [21] relaxed this constraint by only requiring those singular values to be equally small. Recently, Gratton and Tshimanga [23] were able to eliminate this constraint completely, presenting the second-order perturbation expansion for singular subspaces with no restriction on their corresponding singular values.111The only constraint is the singular-value separation between the two subspaces. It is notable that the last result is developed directly from those by Stewart in [16]. A more comprehensive description of the aforementioned results is given in Section 3. Interested readers can also find in-depth surveys on matrix perturbation theory in [24, 25] and references therein.

The aforementioned results on perturbation analysis of the SVD is the fulcrum for the perturbation analysis of the TSVD. While the former characterizes the effect of perturbation on the singular values/singular subspaces of a matrix, the later studies the combined effect (from both singular values and singular subspaces) on the resulting reduced-rank matrix. Analyzing such an effect helps understand the local behavior of algorithms that utilize the low-rank optimal approximation of matrices, such as SVD-based channel estimation methods in multi-input multi-output (MIMO) systems [26, 27, 28] and iterative hard-thresholding algorithms for low-rank matrix completion [4, 29, 30]. In a recent work, Gratton and Tshimanga [23] presented a second-order expansion for the singular subspace decomposition and make use of the result to deduce the second-order sensitivity of the TSVD solution to least-squares problems. However, since their application focuses on the expansion of the truncated pseudo-inverse rather than the TSVD itself, no specific result in perturbation expansion of the TSVD is mentioned. In a different approach to analyzing the TSVD operator, Feppon and Lermusiaux [31] studied the embedded geometry of the fixed-rank matrix manifold and characterized the projection onto it as a smooth () map. Based on this geometric interpretation, the authors provided an explicit expression for the directional derivative of the TSVD of order at a certain matrix with rank greater than or equal to .222Despite the fact that Theorem 25 in [31] reads “greater than ”, both the proof of the theorem and the direct communication with the authors (on September 17, 2020) suggest the result should also include the case of rank- matrices. On the one hand, the result directly suggests the first-order perturbation expansion of the TSVD. On the other hand, the differential geometry-based approach, while offering a clear path for calculating the derivatives, does not offer a direct recipe for obtaining the error bound on the first-order approximation or the higher order terms in the expansion. At the time of writing this manuscript, we are not aware of any explicit expression of the second-order derivative of the TSVD.

In this paper, we present a novel perturbation analysis of the truncated singular value decomposition. First, by utilizing the perturbation expansion for singular subspaces in [23], we derive the first-order perturbation expansion of the TSVD. Our result matches the result on the directional derivative of the TSVD in [31]. Furthermore, we extend our analysis to study the second-order perturbation expansion and show that when the matrix has exact rank , the TSVD of order admits a simple expression for its second-order expansion. To the best of our knowledge, this is the first explicit result for the second-order perturbation expansion of the TSVD. Third, we establish an error bound on the first-order approximation of the TSVD about a rank- matrix. Our bound holds universally for any level (or magnitude) of the perturbation. Finally, we demonstrate how the proposed perturbation expansions and error bounds can be applied to study the mean squared error associated with the TSVD-based matrix denoising solution.

2 Notation and definitions

Throughout the paper, we use and to denote the Frobenius norm and the spectral norm of a matrix, respectively. Occasionally, is used on a vector to denote the Euclidean norm. Boldfaced symbols are reserved for vectors and matrices. In addition, the all-zero matrix is denoted by and the identity matrix is denoted by . We also use to denote the -th vector in the natural basis of . When understood clearly from the context, the dimensions of vectors/matrices in the aforementioned notation may be omitted. As a slight abuse of notation, we define the big O notation for matrices as follows.

Definition 2.1.

Let be some matrix and be a matrix-valued function of . Then, for any positive number , if there exists some constant such that

We emphasize the difference between the commonly used big O notation in the literature and the notation used in this manuscript. While the former requires to be strictly greater than , our notation includes the case to imply both situations that approaches at a rate either equal or faster than . Similarly, when used for a vector, we replace the Frobenius norm by the Euclidean norm in Definition 2.1 to denote the corresponding quantity.

In the rest of the paper, unless otherwise specified, the symbol is used to denote an arbitrary matrix in . Here, without loss of generality, we assume that . The SVD of is written as where is a rectangular diagonal matrix with main diagonal entries are the singular values . For completeness, we denote the “ghost” singular values in the case . Additionally, and are orthogonal matrices such that and . We note that the left and right singular vectors of are the columns of and , i.e., and . Thus, can also be rewritten as the sum of rank- matrices: . Next, we define the singular subspace decomposition as follows.

Definition 2.2.

Given , the singular subspace decomposition of is given by:

| (1) |

where

with the singular values in descending order, i.e., , and

It is clear from Definition 2.2 that

Here the columns of and (or and ) provide the bases for the column-space (or row-space) of and its orthogonal complement, respectively.

Definition 2.3.

The orthonormal projectors onto the subspaces of are defined as:

Generally, matrices , , , and are not unique. In particular, for simple non-zero singular values, the corresponding left and right singular vectors are unique up to a simultaneous sign change. For repeated and positive singular values, the corresponding left and right singular vectors are unique up to a simultaneous right multiplication with the same orthogonal matrix. Finally, for zero singular values, the singular vectors can be any orthonormal bases of the left and right null spaces of . On the other hand, the singular subspaces spanned by the columns of , , , , and their corresponding projectors are unique provided that [9]. We are now in position to define the singular value truncation.

Definition 2.4.

The -truncated singular value decomposition of (-TSVD) is defined as

| (2) |

By Eckart-Young theorem [32], is the best least squares approximation of by a rank- matrix, with respect to unitarily-invariant norms. Therefore, this operator is also known as the projection of onto the non-convex set of rank- matrices. is unique if either or . In the special case when has exact rank , we have and the projectors onto the subspaces of , namely, and are unique. However, the matrices and can take any orthonormal basis in and , respectively, as their columns. Finally, for a rank- matrix, we define the pseudo inverse of as . It is worth mentioning that while in this case.

3 Preliminaries

Proposition 3.5.

Let be a perturbation of arbitrary magnitude. Denote with singular values . Then,

-

•

Weyl’s inequality: , for ,

-

•

Mirsky’s inequality: .

Proposition 3.5 asserts that the changes in the singular values can be bounded using only the norm of the perturbation. By leveraging the specific values of the entries of the perturbation matrix, the behavior of singular values under perturbations can be described more precisely through perturbation expansions. In [17], Stewart showed that if is non-zero and distinct from other singular values of , then its corresponding perturbed singular value can be expressed by

| (3) |

It is later known that the result in (3) also holds for any simple non-zero singular values [25]. In another approach, Sun [18] derived a second-order perturbation expansion for simple non-zero singular values. For a simple zero singular value, Stewart [17] claimed that deriving a perturbation expansion is non-trivial and proposed a second-order approximation for instead. Most recently, a generalization of (3) to a set of singular values that is well separated from the rest is proved in [33].

While the singular values of a matrix are proven to be quite stable under perturbations, the singular vectors, especially those correspond to a cluster of singular values, are extremely sensitive. It is therefore natural to bound the perturbation error based on the subspace spanned by the singular vectors. Consider the singular subspace decomposition in Definition 2.2. We define the singular gap as the smallest distance between a singular value in and a singular value in . When the spectral norm of the perturbation is smaller than this gap, Wedin’s theorem [14] provides an upper bound on the distances between the left and right singular subspaces and their corresponding perturbed counterparts in terms of the singular gap and the Frobenius norm of the perturbation. Furthermore, Stewart [16] showed that there exist explicit expressions of the perturbed subspaces in the bases of the unperturbed subspaces, which can be leveraged to obtain error bounds for certain characteristic subspaces associated with the SVD. Let us rephrase this result in the following proposition.

Proposition 3.6.

(Rephrased from Theorem 2.1 in [23], which is based on Theorem 6.4 in [16]) In addition to the setting in Definition 2.2, assume that . For a perturbation , denote the singular subspace decomposition of by

Let us partition conformally with and in the form

| (4) |

If

| (5) |

then there must exist unique matrices , whose norms are in the order of such that

| (6a) | |||

| (6b) | |||

Moreover, using

| (7a) | ||||

| (7b) | ||||

| (7c) | ||||

| (7d) | ||||

we can define semi-orthogonal matrices , , , and satisfying and , which provide bases to the same unique subspaces of , , , and , respectively, i.e., , , , and .

It is important to note that , , , and may differ from , , , and , respectively. However, their corresponding subspaces are identical. This result will be useful later when replacing and in the following version of the -TSVD with and . The substitution allows us to write an explicit expression of the -TSVD using and terms that are in order of such as and . Equation (6) also enables the perturbation expansion of the SVD through the coefficient matrices and . In 1991, Li and Vaccaro [19] considered a special case of rank- matrices () and introduced the first-order perturbation expansion for and as a method to analyze the performance of subspace-based algorithms in array signal processing. Later on, Vaccaro [20] extended their approach to study the second-order perturbation expansion for the singular subspace decomposition. A more general result in this approach was proposed by Xu [21] in 2002, through relaxing the constraint to , for small . It was not until recently the second-order analysis with no restriction on was provided by Gratton [23]. We summarize this result on second-order perturbation expansion for and as follows.

Proposition 3.7.

Corollary 3.8.

Suppose in Proposition 3.6, has rank , i.e., . Then

Finally, we devote the rest of this section to discuss condition (5) in Proposition 3.6. As mentioned earlier, the singular subspaces corresponding to , , , and are unique if and only if . By Weyl’s inequality (see Proposition 3.5), we have . Since and , one can further upper bound the -th perturbed singular value by

| (10) |

Following a similar argument, leads to

| (11) |

It follows from (10) and (11) that the gap between and is strictly greater than :

| (12) |

As mentioned in [23], condition (5) is more restrictive, but simpler, than the original condition specified in [16]. Based on the aforementioned preliminaries, we are ready to present our results.

4 Perturbation expansions for the -TSVD

This section presents perturbation expansion results for the -TSVD operator. In order to guarantee the uniqueness of the expansions, we assume throughout the section that the -th and -th singular values are well-separated and the perturbation has small magnitude relative to .

Let us begin with a non-trivial result on the first-order perturbation expansion of the -TSVD. The result is consistent with Theorem 25 from [31], in which Feppon and Lermusiaux utilized differential geometry to derive a closed-form expression for the directional derivative of the -TSVD. Using tools from perturbation analysis, we are able to obtain the same result on the first-order perturbation expansion of . The additional benefit of the technique used here, as can be seen later, is that it can be leveraged to further derive the second-order perturbation expansion and the bound on the approximation error of the first-order expansion about a rank- matrix.

Theorem 4.9.

Assume . Then, for some perturbation such that , the first-order perturbation expansion of the -TSVD about is uniquely given by333We recall that throughout this manuscript we assume .

| (13) |

The proof of Theorem 4.9 is based on perturbation expansions of the coefficient matrices and in Proposition 3.7. Interested readers are encouraged to find out the details in Appendix B. As mentioned earlier, the first-order term in (13) is equivalent to the directional derivative given by Theorem 25 in [31]:

| (14) |

It is worthwhile to mention that we arrive at the first-order perturbation expansion in Theorem 4.9 while working independently on the error bounds for TSVD (see Section 5).

Note that the condition guarantees a non-zero gap between the -th and the -th singular values of the perturbed matrix (see (12)), and hence guarantees on the LHS of (13) is unique. At the same time, each term on the RHS of (13) is well-defined due to the uniqueness of singular subspaces associated with each group of singular values of . The term can be viewed as the projection of onto the tangent space of the manifold of rank- matrices [34]. On the other hand, the double summation stems from the curvature of this manifold when does not lie on it (with rank greater than ). To demonstrate the first-order expansion in Theorem 4.9, let us consider the following examples.

Example 4.10.

Consider the matrix with its SVD as follows:

| (15) |

In this example, note that . From Definition 2.4, we have

| (16) |

In addition,

| (17) |

For the perturbation

| (18) |

(17) leads to

| (19) |

Now the double summation in (13) can be represented as

While the singular vectors of are not unique (due to ), the singular subspaces of are unique. Therefore, by representing as

| (20) |

we observe that is well-defined since , , , , , and are all unique quantities, namely,

| (21) |

Substituting the values of the aforementioned terms in (21) and the value of in (18) back into (20), we obtain

| (22) |

The substitution of (16), (18), (19), and (22) into (13) yields

| (23) |

On the other hand, running a simple numerical evaluation by Definition 2.4, we can compute and obtain

The approximation error of the first-order perturbation expansion has magnitude of , which is much smaller than the approximation error of the zero-order expansion, i.e., .

Example 4.11.

Let us consider a counter-example in which the condition is not satisfied. In particular, by setting

following similar calculation in Example 4.10 would yield

On the other hand, the -TSVD of can either be

It can be seen that our first-order approximation is no longer accurate if the later truncation is considered.

One immediate consequence of Theorem 4.9 is when the matrix has exact rank , the double summation on the RHS of (13) vanishes since for all . Thus, we obtain a simple expression for the first-order expansion of about a rank- matrix.

Corollary 4.12.

Let be a rank- matrix. Then, for some perturbation such that , the first-order perturbation expansion of the -TSVD about is uniquely given by

| (24) |

We observe that while the first-order term depends on the perturbation and the two projections and , it is independent of the singular values of . Motivated by the simple result in Corollary 4.12, we further study the second-order perturbation expansion of the -TSVD about a rank- matrix in the following theorem.

Theorem 4.13.

Let be a rank- matrix. Then, for some perturbation such that , the second-order perturbation expansion of the -TSVD about is uniquely given by

| (25) |

The proof of Theorem 4.13 is given in Appendix C. The theorem states that admits a simple second-order approximation that only depends on , , and in addition to and themselves. Notice the dependence of the three second-order terms on the RHS of (25) on the pseudo inverse of indicates the first-order approximation is sensitive to the least singular value of . In the next section, we shall prove that the error bound for the first-order approximation of depends linearly on .

Remark 4.14.

The differentiability of at a rank- matrix, as shown in Corollary 2 and Theorem 2, matches with the well-known result in differential geometry that a projection onto the base of the normal bundle of any smooth manifold is a smooth map on the tubular neighborhood [35]. In particular, is a classic smooth () map in a small open neighborhood containing the manifold of rank- matrices.

Remark 4.15.

It is known that the -TSVD is differentiable at any point (matrix) with a non-zero gap between the -th and -th singular values and hence, admits a first-order perturbation expansion about such point. While our result in Theorem 4.13 only considers a special case of rank- matrices, we suspect there exists a second-order perturbation expansion of the -TSVD about a matrix with rank greater than . However, given the complexity of the first-order expansion, it certainly requires more elaborate work. We leave this as a future research direction.

5 Error bounds for the -TSVD

This section introduces upper bounds on the difference between the -TSVD and its first-order approximation. While in Section 4 the perturbation expansions are derived under the assumption that , the error bounds in this section do not require this constraint and indeed they hold for with arbitrary magnitude. It is important to note that, without the constraint on the level of the perturbation, may not be unique since there is no guarantee that . The value of in case depends on the choice of the singular subspace decomposition of (see Definition 2.2). Nevertheless, we shall provide error bounds that hold independent of the choice of decomposition.

Let us consider the first-order expansion in (24). One trivial bound on the approximation error can be derived as follows (see details in Appendix D):

Lemma 5.16.

Let be a rank- matrix. For any and any valid choice of subspace decomposition of , we have

Lemma 5.16 suggests that for large , the approximation error grows at most linearly in the norm of . However, for small , the aforementioned bound is not tight since Corollary 4.12 implies the error should be in the order of . In order to tighten the bound for the small perturbation, we need to develop a different approach that is more meticulous about intermediate inequalities. We state our main result regarding the global error bound on the first-order approximation of the -TSVD as follows.

Theorem 5.17.

Let be a rank- matrix. Then, for any and any valid choice of subspace decomposition of , the first-order Taylor expansion of the -TSVD about is given by

| (26) |

where there exists a universal constant such that

| (27) |

Furthermore, the following inequality holds

| (28) |

The proof of Theorem 5.17 is given in Appendix E. It is noticeable that the first three terms on the RHS of (26) are uniquely given by the rank- singular subspace decomposition of . On the contrary, the LHS may not be unique (e.g., when ) and hence, so does the residual . However, it is interesting to note that the theorem makes no assumption on the norm of , as well as the choice of the r-TSVD of . The bound on the residual (or the remainder) in Theorem 5.17 is similar to the Lagrange error bound in univariate first-order Taylor series. It not only asserts that the approximation error can grow no faster than a quadratic rate but also determines the constant attached to . Furthermore, the bound depends only on the and , as one may expect from the second-order perturbation expansion of the -TSVD in Theorem 4.13.

Remark 5.18.

We conjecture but are unable to prove that the lower bound on is tight, i.e., . Partial result in this direction regarding of certain structure is also given in the proof of Theorem 5.17. In our numerical experiment, we ran multiple optimization procedures to maximize the quantity with respect to and obtained the same constant .

The bound in (28) suggests an interesting behavior of the residual . When the perturbation is small, the error depends quadratically on the magnitude of the perturbation and inversely proportional to the least singular value of . In particular, as approaches , the first-order approximation becomes less accurate. On the contrary, for large , the upper bound is linear in the norm of and independent of . Compared to the bound in Lemma 5.16, we observe that the dependence on is eliminated. Asymptotically as approaches , the simple bound in the lemma becomes tighter than the bound in (28).

We conclude this section by describing the behavior of the residual term for small perturbations. While it is challenging to establish a tight bound on (as a function of ) for large , it is possible to project the first-order approximation error for small perturbation based on the knowledge of the second-order perturbation expansion of the -TSVD (see Theorem 4.13). We provide the result in the following theorem, with the proof given in Appendix F.

Theorem 5.19.

Asymptotically as approaches , the norm of the residual term in Theorem 5.17 can be upper-bounded tightly by

6 An application to performance analysis in matrix denoising

This section presents an application of our result to the performance analysis of the TSVD for matrix denoising. In many applications such as image denoising [36], multi-input multi-output (MIMO) channel estimation [26], collaborative filtering [37], low-rank procedures are often motivated by the following statistical model:

where is the unknown matrix with rank and is a random matrix whose entries are normally distributed with zero mean and -variance, i.e., for and . To denoise the data, the TSVD is applied to the noisy matrix to obtain the following estimator:

We would like to assess the mean squared error (MSE) of this estimator using our perturbation analysis of the TSVD. As a baseline for our analysis, we consider the MSE of the noisy matrix :

| (29) |

Next, we study the MSE of the estimator , i.e., . To the best of our knowledge, there exists no closed-form expression of this quantity due to the non-linearity of the truncated singular value operator. In the following, we provide the first-order approximation, the second-order approximation, and the upper bound for based on the results presented in this paper.

-

1.

The first-order approximation:

Let be the first-order approximation of . We have

(by Lemma A.30-2) (30) Using the fact that and are projection matrices, is also a projection matrix, and hence, . Thus, (30) can be further simplified as

(by the cyclic property of the trace) Since , . Thus,

(31) where the second equality uses Lemma A.30-4 and the third equality stems from the fact that (and similarly ).

-

2.

The second-order approximation:

Let be the second-order approximation of . We have

(32) Since , the expected value of the third-order term on the RHS of (32) is zero, i.e.,

Therefore,

Since the first term on the RHS is given by (31), we proceed with the calculation of the second term on the RHS, i.e., . Since , the three terms inside the norm are orthogonal to each other, i.e., their inner products are zero. Hence,

(33) Using the cyclic property of the trace and the idempotence property of , the first term on the RHS of (33) can be computed as

Similarly, one can compute the second and the third terms on the RHS of (33), then taking the expectation to obtain

(34) Next, to compute the three terms on the RHS of (34), we consider the following lemma:

Lemma 6.21.

Assume the matrices and in each of the following statements are of compatible dimensions such that the matrix product is valid. Then,

-

(a)

,

-

(b)

.

The proof of Lemma 6.21 follows a similar derivation of the fourth-moment properties in [38] and hence is omitted. Applying Lemma 6.21 to the RHS of (34) and using the orthogonality between and , we obtain

(35) where the last equality stems from and . Substituting (31) and (35) into (32) yields

(36) -

(a)

-

3.

The upper bound:

From Corollary 4.12, we have

Hence, by the triangle inequality, it holds that

Taking the expectation of the squared norm yields

(37) Applying Minkowski inequality [39], we can bound the RHS of (35) as

(38) From (28), we can bound by

(39) where the last inequality is a special case of Jensen’s inequality [39] with the minimum of two linear functions as a concave function. The fourth-order term on the RHS of (39) can be computed as

(40) Substituting (31) and (40) back into (39), then taking the square root, we have

Substituting the bound in the last inequality and the equality in (31) into (38), we obtain the upper bound as

(41) Due to the nature of the bound given in (28), the bound in (41) is taken as the minimum between a component that is linear in the norm of and a component that is quadratic in the norm of .

Remark 6.22.

Asymptotically as , all the ratios of the first-order approximation (31), the second-order approximation (36), and the upper bound (41) to the MSE of the noisy matrix (29) converge to . In general, this ratio is less than or equal to , however, in low-rank scenarios it can be significantly smaller. This indicates the TSVD estimator is effective in noise reduction when the noise is small, especially when the matrix has low rank.

Remark 6.23.

The upper bound in (41) attains the same value of the baseline when , where

| (42) |

guaranteeing the superiority of the upper bound over the baseline in the case .

Remark 6.24.

Let us define the -knee point between two increasing functions of , e.g., and , as the point at which (for ). Then, the -knee point between the upper bound (41) and the first-order approximation (31) can be determined by

| (43) |

In addition, the -knee point between the second-order approximation (36) and the first-order approximation (31) is given by

| (44) |

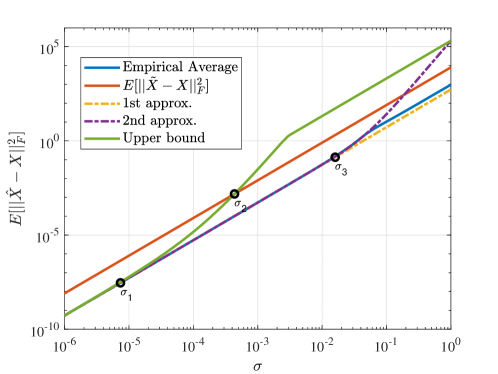

Figure 1 demonstrates the aforementioned analysis on the performance of the TSVD-based estimator for matrix denoising through a numerical experiment. Data generation. We generate a matrix with , and by (i) taking the product of two random matrices, whose entries are normally distributed , of sizes and , respectively; (ii) and dividing each entry of the obtained matrix by its Frobenius norm such that the resulting matrix satisfies . In the experiment, we consider values of in the interval of , namely . For each value of , we compute the following quantities:

-

1.

the empirical MSE of the TSVD-based estimator by averaging the quantity over instances of ,

-

2.

the MSE of the noisy matrix given in (29),

-

3.

the first-order approximation of the MSE of the TSVD-based estimator given in (31),

-

4.

the second-order approximation of the MSE of the TSVD-based estimator given in (32),

-

5.

the upper bound on the MSE of the TSVD-based estimator given in (41).

We display each of the aforementioned quantities as a function of in Fig. 1. In addition, we calculate the points corresponding to and using (43), (42), and (44), respectively, with , and include them in Fig. 1. Results and Analysis. It can be observed from the plot that the empirical MSE of the TSVD-based estimator (solid blue) increases quadratically as a function of (in the log-log scale, it appears as a straight line with slope equal to ). The first-order approximation (dash-dotted yellow) and the second-order approximation (dash-dotted purple) match the empirical average well for . In this range of , all of the three aforementioned quantities are lower than the MSE of the noisy matrix (solid red). On the other hand, the upper bound (solid green) holds tightly when , providing an efficient guarantee on the performance of the TSVD-based estimator for denoising with the presence of small additive noises. However, as the noise variance increases, the upper bound appears loose, exceeding the MSE of the noisy matrix when . The bound is developed for the worst-case noise scenario, in which the noise is adversarially selected to yield the largest perturbation error (see the proof of Theorem 5.17 in Appendix E) and not for the random noise case. Consequently, it is far more conservative, predicting a larger MSE than the actual MSE of the TSVD-based estimator. Developing bounds for average-case scenario is a potential direction for future research.

7 Conclusion

In this paper, we derived a first-order perturbation expansion for the singular value truncation. When the underlying matrix has exact rank-, we showed that the first-order approximation can be greatly simplified and further introduced a simple expression of the second-order perturbation expansion for the -TSVD. Next, we proposed an error bound on the first-order approximation of the -TSVD about a rank- matrix. Our bound is universal in the sense that it holds for perturbation matrices with an arbitrary norm. Two open questions raised by our analysis are: (i) when the underlying matrix has arbitrary rank, whether there exists an explicit expression for the second-order perturbation expansion of the TSVD; (ii) and given the result in Theorem 4.9, whether it is possible to establish a global error bound on the first-order approximation of the -TSVD.

Declaration of competing interest

There is no competing interest.

Acknowledgments

This work is partially supported by the National Science Foundation grant CCF-1254218.

Appendix A Auxiliary lemmas

This section summarizes some trivial results that will be used regularly in our subsequent derivation. The proofs of Lemmas A.25-A.29 can be found in [40] - Chapter 5. The proof of Lemma A.30 can be found in [41] - Chapter 2.

Lemma A.25.

Assume the same setting as in Definition 2.2. The following statements hold:

-

1.

, , and ,

-

2.

and ,

-

3.

and .

Furthermore, if has rank , then

-

1.

and ,

-

2.

,

-

3.

and .

Lemma A.26.

Assume the same setting as in Definition 2.2. The following statements hold:

-

1.

,

-

2.

.

Lemma A.27.

For any matrices and with compatible dimensions, the following inequalities hold

Lemma A.28.

(Pythagoras theorem for Frobenius norm) For any matrices and such that , it holds that

The matrices and in this case are said to be orthogonal to each other.

Lemma A.29.

Let be a semi-orthogonal matrix with orthonormal columns and . Then, for any matrices and that have compatible dimensions with , the followings hold

-

1.

and ,

-

2.

and .

Lemma A.30.

For any matrices , , , and with compatible dimensions such that the matrix products are valid, the following holds

-

1.

,

-

2.

,

-

3.

,

-

4.

.

Appendix B Proof of Theorem 4.9

Recall that in this proof, we consider a matrix having rank greater than or equal to . With a slight abuse of notation, let us define as follows:

| (45) | ||||

| (46) |

Since , applying Lemma A.26 to (46) yields

Denote and . By rewriting and , we can further simplify the last equation as

| (47) |

Lemma B.31.

The perturbations of singular subspaces satisfy

| (48a) | |||

| (48b) | |||

The proof of Lemma B.31 is given at the end of this section. From this lemma, it is clear that and are in the order of . Substituting into (47) and collecting second-order terms yield

| (49) |

Substituting (48a) into the first term on the RHS of (49), we obtain

Since and , we further have

| (50) |

Similarly, the second term on the RHS of (49) can be represented as

| (51) |

Substituting (50) and (51) back into (49), we have

| (52) |

Now we can vectorize (52) and apply Lemma A.30 to obtain

| (53) |

Let us now consider each term on the RHS of (53). From Proposition 3.7, it follows that

| (54) |

Replacing , for , and using Lemma A.30, (54) becomes

| (55) |

Since and are diagonal, so is . The following lemma provides an insight into the structure of this inversion.

Lemma B.32.

Let . Then

where , for and .

The proof of Lemma B.32 is given at the end of this section. Now using Lemma B.32 and left-multiplying both sides of (55) by , we obtain

| (56) |

Moreover, applying Lemma A.30-1, we have

| (57) |

and similarly,

| (58) |

Substituting (57) and (58) back into (56) and performing a change of variable , we obtain

| (59) |

Following a similar derivation, we also have

| (60) |

Substituting (59) and (60) back into (53) yields

| (61) |

Truncating the inner summation, with for , and applying Lemma A.30-2 to the RHS of (61), we obtain

Our theorem now follows on the definition of in (45).

B.1 Proof of Lemma B.31

B.2 Proof of Lemma B.32

Recall that

By the definition of the Kronecker product, we have

Therefore, we can invert this diagonal matrix by considering each of the blocks:

Now it is easy to verify that, for and , the -th diagonal entry of the -th diagonal block, is . Furthermore, since is a matrix of all zeros but the -th diagonal entry of the -th diagonal block is , we represent as the sum of rank- matrices:

Appendix C Proof of Theorem 4.13

By the definition of the -TSVD in (2), we have

| (64) |

Since we assume has exact rank , the perturbed matrix can be represented as . Substituting this back into (64) yields

| (65) |

Similar to the derivation of (63), we obtain and . Substituting the expressions of and back into (65), we obtain

| (66) |

By orthogonality, the product of three terms in the middle of the RHS of (66) can be expanded and simplified as

Therefore, (66) is equivalent to

| (67) |

Let us first focus on the first term on the RHS of (C). Similar to the result after (63), we have and , and hence

| (68) |

Recall that and . The product can be expanded as

| (69) |

In order to make up the first-order terms that involve , we need to decompose the perturbation into components corresponding to different subspaces as follows. Since and , we have

| (70) |

Reorganizing terms in (70) as

and using the definition of in (4), we further have

| (71) |

Thus, substituting (71) back into (69) and rearranging terms yield

| (72) |

Substituting (68) and (72) back into (C), we obtain

| (73) |

Applying (6), we have

| (74) |

and

| (75) |

Substituting (74) and (75) back into (73), we obtain

| (76) |

Since , and are first-order, and , are zero-order in terms of , we can collect all the third-order terms on the RHS of (76) and obtain

| (77) |

Finally, the matrices and in the second-order terms is eliminated by the following variant of (6):

The substitution and collection of third-order terms on the RHS of (77) yield

This completes our proof of the theorem.

Appendix D Proof of Lemma 5.16

By the triangle inequality, we have

| (78) |

The first term on the RHS of (78) can be bounded as follows. Since , applying the norm absolute homogeneity property yields

| (79) |

From Lemmas A.26 and A.29, we obtain

| (80) |

Since is a submatrix of containing small singular values of in the diagonal, it holds that

| (81) |

Additionally, using the triangle inequality we can bound by

| (82) |

From (79), (80), (81), and (82), we have

| (83) |

On the other hand, it follows from Lemma A.29 that the second term on the RHS of (78) satisfies

| (84) |

Substituting inequalities (83) and (84) into (78) completes the proof of the lemma.

Appendix E Proof of Theorem 5.17

The following proof is developed for the case of a rank- matrix . We first derive the proof of (27) and then use this result to prove (28).

E.1 Proof of the bound in (27)

Our goal is to prove that the residual in (26) is always bounded by

Let us begin with the upper bound on by showing that

| (85) |

Rearranging terms in (26) and replacing by , we have

| (86) |

Using the singular subspace decomposition in Definition 2.2 with descending order of singular values , let us decompose as follows

| (87) |

Since in this theorem we consider perturbations of any magnitude, can take any value including the case in which and the decomposition (87) may not be unique. Nevertheless, the proof holds for any valid choice of singular subspace decomposition. From such a choice in (87), is well-defined as: . Substituting into (47) and using the fact that and , we obtain

| (88) |

Here, from Lemma A.25, we can replace in the first term on the RHS of (88) and obtain

| (89) |

Taking the Frobenius norm and using its absolute homogeneity property, (89) becomes

By the triangle inequality, the norm of is then bounded by

| (90) |

Let us proceed to upper-bound by finding the upper bounds for each of the three terms on the RHS of (90) with respect to . Our proof technique utilizes the following lemmas.

Lemma E.33.

Lemma E.34.

The proofs of Lemmas E.33 and E.34 are given at the end of this subsection. Let us proceed with the task of bounding the first term in (90). Applying Lemma A.27 twice and using the fact that , we have

| (91) |

By Lemma E.33, the terms and can each be bounded by . Applying the upper bounds on the RHS of (91), we obtain the following bound on the first term in (90):

| (92) |

Next, we shall bound the second term in (90), i.e., . From Lemma A.29, we have

| (93) |

Since , the matrix on the RHS of (93) can be expanded as the sum of two orthogonal terms:

Notice that and are orthogonal. By Lemma A.28, we have

| (94) | |||||

Each term on the RHS of (94) can be bounded as follows. Applying Lemma A.27 twice, we initially bound the first term on the RHS of (94) as follows:

By Lemma E.33, we upper-bound by and obtain the bound on the first term on the RHS of (94):

| (95) |

To bound the second term on the RHS of (94), we apply Lemma E.34 and obtain

| (96) |

Substituting the bounds from (95) and (96) back into the RHS of (94), we have

Taking the square root of the last result and substituting it back to (93) yields

| (97) |

This offers a bound on the second term on the RHS of (90). Similarly, we bound the third term on the RHS of (90) by

| (98) |

Finally, summing up (92), (97), and (98), and substituting back into (90), we obtain (85) and thereby completes the first part of the proof.

For the second part of the proof, we show that by constructing a perturbation such that the ratio approaches . Consider perturbations of form

| (99) |

Since and are orthogonal, we can compute the norm of using Lemma A.28:

| (100) |

where the second equality uses and Lemma A.30-3. Using the SVD of and the definition of in (99), we have

| (101) |

After perturbation, the -th singular value of is changed from to and the -th changes from to , thereby making the singular value corresponding to larger than the singular value associated with . Thus, the -TSVD of is given by

| (102) |

On the other hand, since and , we have

| (103) |

where the second equality stems from the fact that

Substituting (101), (102), and (103) into (86), we obtain

Similar to (100), one can compute the norm of the residual by

| (104) |

Now maximizing over while taking to gives us a lower bound on :

| (105) |

The maximization can be obtained at . Therefore, substituting back into (105) yields . This completes our proof of the first half of Theorem 5.17. We recall from Remark 5.18 that we conjecture the structure of given in (99) yields the maximizer of .

E.1.1 Proof of Lemma E.33

Let us rewrite . Since , we obtain

| (106) | |||||

Substituting yields

where in the last equality we use the fact that and . Therefore,

| (107) |

By the triangle inequality and the absolute homogeneity, (107) implies

| (108) |

We shall bound each term on the RHS of (108) as follows. First, using Lemma A.29, we can remove the semi-orthogonal matrices from within the Frobenius norm without changing the value of the norm:

Since , we further obtain

| (109) |

In addition, recall that and are sub-matrices of and , respectively. Thus,

| (110) |

Moreover, by Mirsky’s inequality in Proposition 3.5, we have

| (111) |

From (109), (110), and (111), it follows that

| (112) |

Next, the second term on the RHS of (108), by Lemma A.29, is bounded by

| (113) |

Summing up (112) and (113), and combining the resulting inequality with (108), we conclude that

The proof of follows a similar derivation.

E.1.2 Proof of Lemma E.34

In this subsection, we shall show that . The proof of can be derived similarly. Since Definition 2.3 implies , we have

| (114) |

where the second equality is due to (see Lemma A.25). It is now sufficient to bound the norm of by . Let us consider two cases:

- •

-

•

If , we need to use a different approach as follows. First, from Lemma A.27, we have

(117) Let us examine the product . Let and . From Weyl’s inequality [11], we have

Thus, for any , it holds that

(118) Therefore, is invertible. We can now denote the pseudo inverse of by . We have

(119) On the other hand, applying Lemmas A.29 and A.27, and the fact that , we obtain

(120) From (118), we can bound by:

(121) From (119), (120), and (121), we obtain

(122) Finally, substituting (122) back into (117) immediately yields .

Since in both cases , we conclude from (114) that for any .

E.2 Proof of the bound in (28)

Taking Frobenius norm on both sides of equation (88) and using its absolute homogeneity property, we obtain:

| (123) |

Applying the triangle inequality to the RHS of (123), we have

| (124) |

To bound the RHS of (124), we proceed by bounding each of the terms on the RHS. The first term on the RHS of (124) can be bounded as follows. From (106), we have . Using Lemmas A.29 and E.33, it follows that

| (125) |

Next, the second term on the RHS of (124) can be rewritten as the sum of two orthogonal components

By Lemma A.28, we have

| (126) |

On the one hand, we consider the first term on the RHS of (126). Since

| (by Lemma A.25) | ||||

we obtain

| (127) |

Applying Lemma A.29 to the RHS of (127) in order to eliminate the three projection matrices, we obtain

| (128) |

Similarly, we have

| (129) |

Substituting (128), and (129) back into (126), we have

| (130) |

Similarly, we also obtain

| (131) |

Substituting (125), (130), and (131) back into (124), we obtain

| (132) |

The proof of (28) is concluded by taking the minimum between the bounds in (132) and (27).

Appendix F Proof of Theorem 5.19

Lemma F.35.

Let and be some bounded real-valued functions defined on the set . Then it holds that

Applying Lemma F.35 to (133), we obtain

| (134) |

On the other hand, by the triangle inequality, we have

| (135) |

From (134) and (135), it holds that

| (136) |

Thus, taking both sides of (136) to the limit and rearranging terms yield

It now is sufficient to show that

| (137) |

Indeed, due to the orthogonality among the addends, we have

| (138) |

Using the definition of in (4), (138) can be represented as

| (139) |

where the second equality stems from Lemma A.29. Using Lemma A.27 and the fact that , we can bound the RHS of (139) by

| (140) |

Lemma F.36 (Chebyshev’s sum inequality [39]).

For any , we have

Applying Lemma F.36 to (140) with and , we obtain

| (141) |

where the last equation stems from . From (141), taking the square root and then taking the supremum yield

| (142) |

To show that (142) implies (137), we describe a particular choice of such that the inequality holds. Let us choose

where , and are the corresponding left and right singular vectors of . Similar to (100), one can verify that . In addition, from Proposition 3.6, we have

| (143) |

Substituting (143) back into (139) yields

Therefore, the equality in (142) holds when , for any . This completes our proof of the theorem.

F.1 Proof of Lemma F.35

References

- Markovsky [2008] I. Markovsky, Structured low-rank approximation and its applications, Automatica 44 (2008) 891–909.

- Markovsky et al. [2005] I. Markovsky, J. C. Willems, S. Van Huffel, B. De Moor, R. Pintelon, Application of structured total least squares for system identification and model reduction, IEEE Transactions on Automatic Control 50 (2005) 1490–1500.

- Candès and Recht [2009] E. J. Candès, B. Recht, Exact matrix completion via convex optimization, Foundations of Computational Mathematics 9 (2009) 717.

- Jain et al. [2010] P. Jain, R. Meka, I. S. Dhillon, Guaranteed rank minimization via singular value projection, in: Advances in Neural Information Processing Systems, 2010, pp. 937–945.

- Shabalin and Nobel [2013] A. A. Shabalin, A. B. Nobel, Reconstruction of a low-rank matrix in the presence of Gaussian noise, Journal of Multivariate Analysis 118 (2013) 67–76.

- Yang et al. [2016] D. Yang, Z. Ma, A. Buja, Rate optimal denoising of simultaneously sparse and low rank matrices, Journal of Machine Learning Research 17 (2016) 3163–3189.

- Wei et al. [2001] J.-J. Wei, C.-J. Chang, N.-K. Chou, G.-J. Jan, ECG data compression using truncated singular value decomposition, IEEE Transactions on Information Technology in Biomedicine 5 (2001) 290–299.

- Li et al. [2011] Z.-C. Li, H.-T. Huang, Y. Wei, Ill-conditioning of the truncated singular value decomposition, Tikhonov regularization and their applications to numerical partial differential equations, Numerical Linear Algebra with Applications 18 (2011) 205–221.

- Hansen [1987] P. C. Hansen, The truncated SVD as a method for regularization, BIT Numerical Mathematics 27 (1987) 534–553.

- Hansen [1990] P. C. Hansen, Truncated singular value decomposition solutions to discrete ill-posed problems with ill-determined numerical rank, SIAM Journal on Scientific and Statistical Computing 11 (1990) 503–518.

- Weyl [1912] H. Weyl, Das asymptotische verteilungsgesetz der eigenwerte linearer partieller differentialgleichungen (mit einer anwendung auf die theorie der hohlraumstrahlung), Mathematische Annalen 71 (1912) 441–479.

- Mirsky [1960] L. Mirsky, Symmetric gauge functions and unitarily invariant norms, The quarterly journal of mathematics 11 (1960) 50–59.

- Davis and Kahan [1970] C. Davis, W. M. Kahan, The rotation of eigenvectors by a perturbation. iii, SIAM Journal on Numerical Analysis 7 (1970) 1–46.

- Wedin [1972] P.-Å. Wedin, Perturbation bounds in connection with singular value decomposition, BIT Numerical Mathematics 12 (1972) 99–111.

- Cai and Zhang [2018] T. T. Cai, A. Zhang, Rate-optimal perturbation bounds for singular subspaces with applications to high-dimensional statistics, The Annals of Statistics 46 (2018) 60–89.

- Stewart [1973] G. W. Stewart, Error and perturbation bounds for subspaces associated with certain eigenvalue problems, SIAM Review 15 (1973) 727–764.

- Stewart [1984] G. W. Stewart, A second order perturbation expansion for small singular values, Linear Algebra and its Applications 56 (1984) 231–235.

- Sun [1988] J.-G. Sun, A note on simple non-zero singular values, Journal of Computational Mathematics (1988) 258–266.

- Li and Vaccaro [1991] F. Li, R. J. Vaccaro, Unified analysis for DOA estimation algorithms in array signal processing, Signal Processing 25 (1991) 147–169.

- Vaccaro [1994] R. J. Vaccaro, A second-order perturbation expansion for the SVD, SIAM Journal on Matrix Analysis and Applications 15 (1994) 661–671.

- Xu [2002] Z. Xu, Perturbation analysis for subspace decomposition with applications in subspace-based algorithms, IEEE Transactions on Signal Processing 50 (2002) 2820–2830.

- Liu et al. [2008] J. Liu, X. Liu, X. Ma, First-order perturbation analysis of singular vectors in singular value decomposition, IEEE Transactions on Signal Processing 56 (2008) 3044–3049.

- Gratton and Tshimanga [2016] S. Gratton, J. Tshimanga, On a second-order expansion of the truncated singular subspace decomposition, Numerical Linear Algebra with Applications 23 (2016) 519–534.

- Stewart [1990] G. W. Stewart, Perturbation theory for the singular value decomposition, in: SVD and Signal Processing, II: Algorithms, Analysis and Applications, Elsevier, 1990, pp. 99–109.

- Stewart and Sun [1990] G. W. Stewart, J.-G. Sun, Matrix Perturbation Theory, Academic Press, 1990.

- Lindskog and Tidestav [1999] E. Lindskog, C. Tidestav, Reduced rank channel estimation, in: IEEE Vehicular Technology Conference, volume 2, 1999, pp. 1126–1130.

- Nicoli and Spagnolini [2005] M. Nicoli, U. Spagnolini, Reduced-rank channel estimation for time-slotted mobile communication systems, IEEE Transactions on Signal Processing 53 (2005) 926–944.

- Jing and Yu [2012] Y. Jing, X. Yu, ML-based channel estimations for non-regenerative relay networks with multiple transmit and receive antennas, IEEE Journal on Selected Areas in Communications 30 (2012) 1428–1439.

- Vu and Raich [2019a] T. Vu, R. Raich, Local convergence of the Heavy Ball method in iterative hard thresholding for low-rank matrix completion, in: Proceedings of the IEEE International Conference on Acoustics, Speech and Signal Processing, 2019a, pp. 3417–3421.

- Vu and Raich [2019b] T. Vu, R. Raich, Accelerating iterative hard thresholding for low-rank matrix completion via adaptive restart, in: Proceedings of the IEEE International Conference on Acoustics, Speech and Signal Processing, 2019b, pp. 2917–2921.

- Feppon and Lermusiaux [2018] F. Feppon, P. F. Lermusiaux, A geometric approach to dynamical model order reduction, SIAM Journal on Matrix Analysis and Applications 39 (2018) 510–538.

- Eckart and Young [1936] C. Eckart, G. Young, The approximation of one matrix by another of lower rank, Psychometrika 1 (1936) 211–218.

- Stewart [2006] M. Stewart, Perturbation of the SVD in the presence of small singular values, Linear Algebra and its Applications 419 (2006) 53–77.

- Absil and Malick [2012] P.-A. Absil, J. Malick, Projection-like retractions on matrix manifolds, SIAM Journal on Optimization 22 (2012) 135–158.

- Lee [2013] J. M. Lee, Smooth manifolds, in: Introduction to Smooth Manifolds, Springer, 2013, pp. 1–31.

- Guo et al. [2015] Q. Guo, C. Zhang, Y. Zhang, H. Liu, An efficient SVD-based method for image denoising, IEEE Transactions on Circuits and Systems for Video Technology 26 (2015) 868–880.

- Koren et al. [2009] Y. Koren, R. Bell, C. Volinsky, Matrix factorization techniques for recommender systems, Computer 42 (2009) 30–37.

- Neudecker and Wansbeek [1987] H. Neudecker, T. Wansbeek, Fourth-order properties of normally distributed random matrices, Linear Algebra and its Applications 97 (1987) 13–21.

- Hardy et al. [1952] G. Hardy, J. Littlewood, G. Pólya, Inequalities, Cambridge Mathematical Library, Cambridge University Press, 1952.

- Meyer [2000] C. D. Meyer, Matrix analysis and applied linear algebra, volume 71, Siam, 2000.

- Graham [2018] A. Graham, Kronecker products and matrix calculus with applications, Courier Dover Publications, 2018.