Reinforcement Learning for Strategic Recommendations

Abstract

Strategic recommendations (SR) refer to the problem where an intelligent agent observes the sequential behaviors and activities of users and decides when and how to interact with them to optimize some long-term objectives, both for the user and the business. These systems are in their infancy in the industry and in need of practical solutions to some fundamental research challenges. At Adobe research, we have been implementing such systems for various use-cases, including points of interest recommendations, tutorial recommendations, next step guidance in multi-media editing software, and ad recommendation for optimizing lifetime value. There are many research challenges when building these systems, such as modeling the sequential behavior of users, deciding when to intervene and offer recommendations without annoying the user, evaluating policies offline with high confidence, safe deployment, non-stationarity, building systems from passive data that do not contain past recommendations, resource constraint optimization in multi-user systems, scaling to large and dynamic actions spaces, and handling and incorporating human cognitive biases. In this paper we cover various use-cases and research challenges we solved to make these systems practical.

Keywords Reinforcement Learning Recommendations

1 Introduction

In strategic recommendation (SR) systems, the goal is to learn a strategy that sequentially selects recommendations with the highest long-term acceptance by each visiting user of a retail website, a business, or a user interactive system in general. These systems are in their infancy in the industry and in need of practical solutions to some fundamental research challenges. At Adobe research, we have been implementing such SR systems for various use-cases, including points of interest recommendations, tutorial recommendations, next step guidance in multi-media editing software, and ad recommendation for optimizing lifetime value.

Most recommendation systems today use supervised learning or contextual bandit algorithms. These algorithms assume that the visits are i.i.d. and do not discriminate between visit and user, i.e., each visit is considered as a new user that has been sampled i.i.d. from the population of the business’s users. As a result, these algorithms are myopic and do not try to optimize the long-term effect of the recommendations on the users. Click through rate (CTR) is a suitable metric to evaluate the performance of such greedy algorithms. Despite their success, these methods are becoming insufficient as users incline to establish longer and longer-term relationship with their websites (by going back to them). This increase in returning users further violates the main assumption underlying supervised learning and bandit algorithms, i.e., there is no difference between a visit and a user. This is the main motivation for SR systems that we examine in this paper.

Reinforcement learning (RL) algorithms that aim to optimize the long-term performance of the system (often formulated as the expected sum of rewards/costs) seem to be suitable candidates for SR systems. The nature of these algorithms allows them to take into account all the available knowledge about the user in order to select an offer or recommendation that maximizes the total number of times she will click or accept the recommendation over multiple visits, also known as the user’s life-time value (LTV). Unlike myopic approaches, RL algorithms differentiate between a visit and a user, and consider all the visits of a user (in chronological order) as a system trajectory. Thus, they model the user, and not their visits, as i.i.d. samples from the population of the users of the website. This means that although we may evaluate the performance of the RL algorithms using CTR, this is not the metric that they optimize, and thus, it would be more appropriate to evaluate them based on the expected total number of clicks per user (over the user’s trajectory), a metric we call LTV. This long-term approach to SR systems allows us to make decisions that are better than the short-sighted decisions made by the greedy algorithms. Such decisions might propose an offer that is considered as a loss to the business in the short term, but increases the user loyalty and engagement in the long term.

Using RL for LTV optimization is still in its infancy. Related work has experimented with toy examples and has appeared mostly in marketing venues [50, 30, 73]. An approach directly related to ours first appeared in [49], where the authors used public data of an email charity campaign, batch RL algorithms, and heuristic simulators for evaluation, and showed that RL policies produce better results than myopic’s. Another one is [57], which proposed an on-line RL system that learns concurrently from multiple customers. The system was trained and tested on a simulator. A recent approach uses RL to optimizes LTV for slate recommendations [29]. It addresses the problem of how to decompose the LTV of a slate into a tractable function of its component item-wise LTVs. Unlike most of previous previous work, we address many more challenges that are found when dealing real data. These challenges, which hinder the widespread application of RL technology to SR systems include:

-

•

High confidence off-policy evaluation refers to the problem of evaluating the performance of an SR system with high confidence before costly A/B testing or deployment.

-

•

Safe deployment refers to the problem of deploying a policy without creating disruption from the previous running policy. For example, we should never deploy a policy that will have a worse LTV than the previous.

-

•

Non-stationarity refers to the fact that the real world is non-stationary. In RL and Markov decision processes there is usually the assumption that the transition dynamics and reward are stationary over time. This is often violated in the marketing world where trends and seasonality are always at play.

-

•

Learning from passive data refers to the fact that there is usually an abundance of sequential data or events that have been collected without a recommendation system in place. For example, websites record the sequence of products and pages a user views. Usually in RL, data is in the form of sequences of states, actions and rewards. The question is how can we leverage passive data that do not contain actions to create a recommendation systems that recommends the next page or product.

-

•

Recommendation acceptance factors refers to the problem of deeper understanding of recommendation acceptance than simply predicting clicks. For example, a person might have low propensity to listen due to various reasons of inattentive disposition. A classic problem is the ‘recommendation fatigue’, where people may quickly stop paying attention to recommendations such as ads and promotional emails, if they are presented too often.

-

•

Resource constraints in multi-user systems refers to the problems of constraints created in multi-user recommendation systems. For example, if multiple users in a theme park are offered the same strategy for touring the park, it could overcrowd various attractions. Or, if a store offers the same deal to all users, it might deplete a specific resource.

-

•

Large action spaces refers to the problem of having too many recommendations. Netflix for example employs thousands of movie recommendations. This is particularly challenging for SR systems that make a sequence of decisions, since the search space grows exponentially with the planning horizon (the number of decisions made in a sequence).

-

•

Dynamic actions refers to the problem where the set of recommendations may be changing over time. This is a classic problem in marketing where the offers made at some retail shop could very well be slowly changing over time. Another example is movie recommendation, in businesses such as Netflix, where the catalogue of movies evolves over time.

In this paper we address all of the above research challenges. We summarize in chronological order our work in making SR systems practical for the real-world. In Section 3 we present a method for evaluating SR systems off-line with high confidence. In Section 4 we present a practical reinforcement learning (RL) algorithm for implementing an SR system with an application to ad offers. In Section 5 we present an algorithm for safely deploying an SR system. In Section 6 we tackle the problem of non-stationarity. Technologies in sections 3, 4, 5 and 6 are build chronologically, where high confidence off-policy evaluation is leveraged across all of them.

In Section 7 we address the problem of bootstrapping an SR system from passive sequential data that do not contain past recommendations. In Section 8 we examine recommendation acceptance factors, such as the ‘propensity to listen’ and ‘recommendation fatigue’. In Section 9 we describe a solution that can optimize for resource constraints in multi-user SR systems. Sections 7, 8 and 9 are build chronologically, where the bootstrapping from passive data is used across.

In Section 10 we describe a solution to the large action space in SR systems. In Section 11 we describe a solution to the dynamic action problem, where the available actions can vary over time. Sections 10 and 11 are build chronologically, where they use same action embedding technology.

Finally, in Section 12 we argue that the next generation of recommendation systems needs to incorporate human cognitive biases.

2 Preliminaries

In this section, we present the general set of notations, which will be useful throughout the paper. In cases where problem specific notations are required, we introduce them in the respective section.

We model SR systems as Markov decision process (MDPs) [60]. An MDP is represented by a tuple, . is the set of all possible states, called the state set, and is a finite set of actions, called the action set. The random variables, , , and denote the state, action, and reward at time . The first state comes from an initial distribution, . The reward discounting parameter is given by . is the state transition function. We denote by the feature vector describing a user’s visit with the system and by the recommendation shown to the user, and refer to them as a state and an action. The rewards are assumed to be non-negative. The reward is if the user accepts the recommendation and , otherwise. We assume that the users interact at most times. We write to denote the history of visits with one user, and we call a trajectory. The return of a trajectory is the discounted sum of rewards, ,

A policy is used to determine the probability of showing each recommendation. Let denote the probability of taking action in state , regardless of the time step . The goal is to find a policy that maximizes the expected total number of recommendation acceptances per user: Our historical data is a set of trajectories, one per user. Formally, is the historical data containing trajectories , each labeled with the behavior policy that produced it.

3 High Confidence Off-policy Evaluation

One of the first challenges in building SR systems is evaluating their performance before costly A/B testing and deployment. Unlike classical machine learning systems, an SR system is more complicated to evaluate because recommendations can affect how a user responds to all future recommendations. In this section we summarize a high confidence off-policy evaluation (HCOPE) method [68], which can inform the business manager of the performance of the SR system with some guarantee, before the system is deployed. We denote the policy to be evaluated as the evaluation policy .

HCOPE is a family of methods that use the historical data in order to compute a -confidence lower bound on the expected performance of the evaluation policy [68]. In this section, we explain three different approaches to HCOPE. All these approaches are based on importance sampling. The importance sampling estimator

| (1) |

is an unbiased estimator of if is generated using policy [53], the support of is a subset of the support or , and where and denote the state and action in trajectory respectively. Although the importance sampling estimator is conceptually easier to understand, in most of our applications we use the per-step importance sampling estimator

| (2) |

where the term in the parenthesis is the importance weight for the reward generated at time . This estimator has a lower variance than (1), and remains unbiased.

For brevity, we describe the approaches to HCOPE in terms of a set of non-negative independent random variables, (note that the importance weighted returns are non-negative because the rewards are never negative, since in our applications the reward is when the user accepts a recommendation and otherwise). For our applications, we will use , where is computed either by (1) or (2). The three approaches that we will use are:

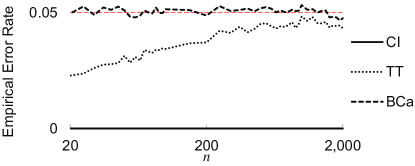

1. Concentration Inequality: Here we use the concentration inequality (CI) in [68] and call it the CI approach. We write to denote the confidence lower-bound produced by their method. The benefit of this method is that it provides a true high-confidence lower-bound, i.e., it makes no false assumption or approximation, and so we refer to it as safe. However, as it makes no assumptions, bounds obtained using CI happen to be overly conservative, as shown in Figure 1.

2. Student’s -test: One way to tighten the lower-bound produced by the CI approach is to introduce a false but reasonable assumption. Specifically, we leverage the central limit theorem, which says that is approximately normally distributed if is large. Under the assumption that is normally distributed, we may apply the one-tailed Student’s -test to produce , a confidence lower-bound on , which in our application is a confidence lower-bound on . Unlike the other two approaches, this approach, which we call TT, requires little space to be formally defined, and so we present its formal specification:

| (3) | |||

| (4) |

where denotes the inverse of the cumulative distribution function of the Student’s distribution with degrees of freedom, evaluated at probability (i.e., function in Matlab).

Because is based on a false (albeit reasonable) assumption, we refer to it as semi-safe. Although the TT approach produces tighter lower-bounds than the CI’s, it still tends to be overly conservative for our application, as shown in Figure 1. More discussion can be found in the work by [68].

3. Bias Corrected and Accelerated Bootstrap: One way to correct for the overly-conservative nature of TT is to use bootstrapping to estimate the true distribution of , and to then assume that this estimate is the true distribution of . The most popular such approach is Bias Corrected and accelerated (BCa) bootstrap [18]. We write to denote the lower-bound produced by BCa, whose pseudocode can be found in [69]. While the bounds produced by BCa are reliable, like t-test it may have error rates larger than and are thus semi-safe. An illustrative example is provided in Figure 1.

For SR systems, where ensuring quality of a system before deployment is critical, these three approaches provide several viable approaches to obtaining performance guarantees using only historical data.

4 Personalized Ad Recommendation Systems for Life-Time Value Optimization with Guarantees

The next question is how to compute a good SR policy. In this section we demonstrate how to compute an SR policy for personalized ad recommendation (PAR) systems using reinforcement learning (RL). RL algorithms take into account the long-term effect of actions, and thus, are more suitable than myopic techniques, such as contextual bandits, for modern PAR systems in which the number of returning visitors is rapidly growing. However, while myopic techniques have been well-studied in PAR systems, the RL approach is still in its infancy, mainly due to two fundamental challenges: how to compute a good RL strategy and how to evaluate a solution using historical data to ensure its ‘safety’ before deployment. In this section, we use the family of off-policy evaluation techniques with statistical guarantees presented in Section 3 to tackle both of these challenges. We apply these methods to a real PAR problem, both for evaluating the final performance and for optimizing the parameters of the RL algorithm. Our results show that an RL algorithm equipped with these off-policy evaluation techniques outperforms the myopic approaches. Our results give fundamental insights on the difference between the click through rate (CTR) and life-time value (LTV) metrics for evaluating the performance of a PAR algorithm [64].

4.1 CTR versus LTV

Any personalized ad recommendation (PAR) policy could be evaluated for its greedy/myopic or long-term performance. For greedy performance, click through rate (CTR) is a reasonable metric, while life-time value (LTV) seems to be the right choice for long-term performance. These two metrics are formally defined as

| (5) |

| (6) |

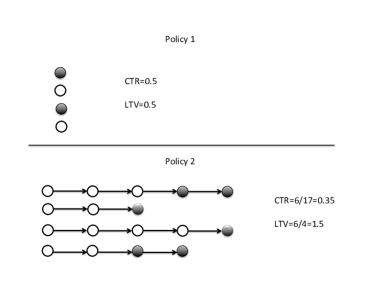

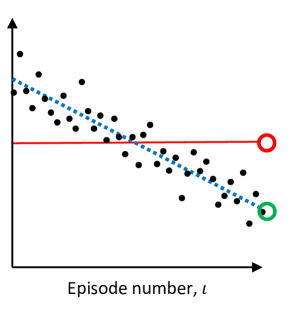

CTR is a well-established metric in digital advertising and can be estimated from historical data (off-policy) in unbiased (inverse propensity scoring; [38]) and biased (see e.g., [58]) ways. The reason that we use LTV is that CTR is not a good metric for evaluating long-term performance and could lead to misleading conclusions. Imagine a greedy advertising strategy at a website that directly displays an ad related to the final product that a user could buy. For example, it could be the BMW website and an ad that offers a discount to the user if she buys a car. users who are presented such an offer would either take it right away or move away from the website. Now imagine another marketing strategy that aims to transition the user down a sales funnel before presenting her the discount. For example, at the BMW website one could be first presented with an attractive finance offer and a great service department deal before the final discount being presented. Such a long-term strategy would incur more visits with the user and would eventually produce more clicks per user and more purchases. The crucial insight here is that the policy can change the number of times that a user will be shown an advertisement—the length of a trajectory depends on the actions that are chosen. A visualization of this concept is presented in Figure 2.

4.2 Ad Recommendation Algorithms

For greedy optimization, we used a random forest (RF) algorithm [11] to learn a mapping from features to actions. RF is a state-of-the-art ensemble learning method for regression and classification, which is relatively robust to overfitting and is often used in industry for big data problems. The system is trained using a RF for each of the offers/actions to predict the immediate reward. During execution, we use an -greedy strategy, where we choose the offer whose RF has the highest predicted value with probability , and the rest of the offers, each with probability

For LTV optimization, we used the Fitted Q Iteration (FQI) [20] algorithm, with RF function approximator, which allows us to handle high-dimensional continuous and discrete variables. When an arbitrary function approximator is used in the FQI algorithm, it does not converge monotonically, but rather oscillates during training iterations. To alleviate the oscillation problem of FQI and for better feature selection, we used our high confidence off-policy evaluation (HCOPE) framework within the training loop. The loop keeps track of the best FQI result according to a validation data set (see Algorithm 1).

For both algorithms we start with three data sets an , and . Each one is made of complete user trajectories. A user only appears in one of those files. The and contain users that have been served by the random policy. The greedy approach proceeds by first doing feature selection on the , training a random forest, turning the policy into -greedy on the and then evaluating that policy using the off-policy evaluation techniques. The LTV approach starts from the random forest model of the greedy approach. It then computes labels as shown is step 6 of the LTV optimization algorithm 1. It does feature selection, trains a random forest model, and then turns the policy into -greedy on the data set. The policy is tested using the importance weighted returns according to Equation 2. LTV optimization loops over a fixed number of iterations and keeps track of the best performing policy, which is finally evaluated on the . The final outputs are ‘risk plots’, which are graphs that show the lower-bound of the expected sum of discounted reward of the policy for different confidence values.

4.3 Experiments

For our experiments we used 2 data sets from the banking industry. On the bank website when users visit, they are shown one of a finite number of offers. The reward is 1 when a user clicks on the offer and 0, otherwise. For data set 1, we collected data from a particular campaign of a bank for a month that had 7 offers and approximately visits. About of the visits were produced by a random strategy. For data set 2 we collected data from a different bank for a campaign that had 12 offers and visits, out of which were produced by a random strategy. When a user visits the bank website for the first time, she is assigned either to a random strategy or a targeting strategy for the rest of the campaign life-time. We splitted the random strategy data into a test set and a validation set. We used the targeting data for training to optimize the greedy and LTV strategies. We used aggressive feature selection for the greedy strategy and selected of the features. For LTV, the feature selection had to be even more aggressive due to the fact that the number of recurring visits is approximately . We used information gain for the feature selection module [72]. With our algorithms we produce performance results both for the CTR and LTV metrics. To produce results for CTR we assumed that each visit is a unique visitor. We performed various experiments to understand the different elements and parameters of our algorithms. For all experiments we set and .

Experiment 1: How do LTV and CTR compare?

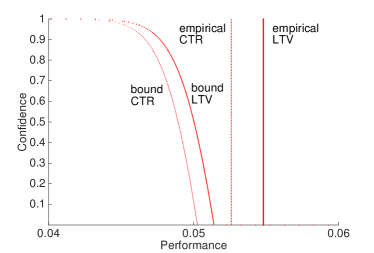

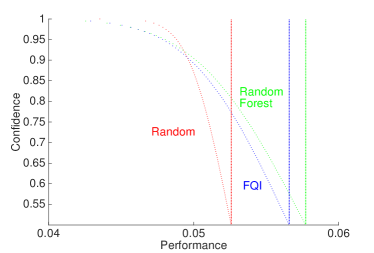

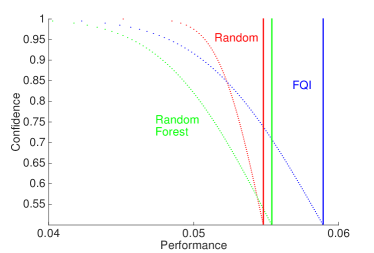

For this experiment we show that every strategy has both a CTR and LTV metric as shown in Figure 3 (Left). In general the LTV metric gives higher numbers than the CTR metric. Estimating the LTV metric however gets harder as the trajectories get longer and as the mismatch with the behavior policy gets larger. In this experiment the policy we evaluated was the random policy which is the same as the behavior policy, and in effect we eliminated the importance weighted factor.

Experiment 2: How do the three bounds differ?

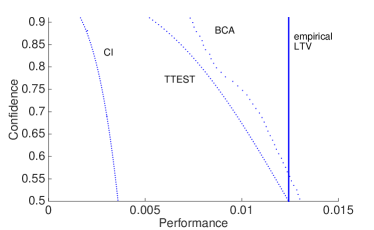

In this experiment we compared the 3 different lower-bound estimation methods, as shown in Figure 3 (Right). We observed that the bound for the -test is tighter than that for CI, but it makes the false assumption that importance weighted returns are normally distributed. We observed that the bound for BCa has higher confidence than the -test approach for the same performance. The BCa bound does not make a Gaussian assumption, but still makes the false assumption that the distribution of future empirical returns will be the same as what has been observed in the past.

Experiment 3: When should each of the two optimization algorithms be used?

In this experiment we observed that the GreedyOptimization algorithm performs the best under the CTR metric and the LtvOptimization algorithm performs the best under the LTV metric as expected, see Figure 4. The same claim holds for data set 2.

Experiment 4: What is the effect of ?

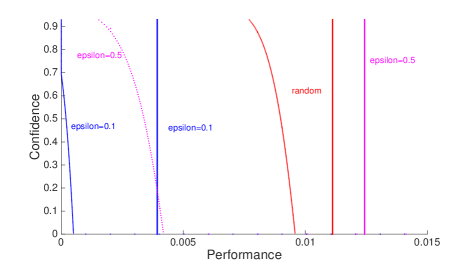

One of the limitations of out algorithm is that it requires stochastic policies. The closer the new policy is to the behavior policy the easier to estimate the performance. Therefore, we approximate our policies with -greedy and use the random data for the behavior policy. The larger the , the easier is to get a more accurate performance of a new policy, but at the same time we would be estimating the performance of a sub-optimal policy, which has moved closer to the random policy, see Figure 5. Therefore, when using the bounds to compare two policies, such as Greedy vs. LTV, one should use the same .

5 Safe Deployment

In the previous sections we described how to compute an SR in combination with high confidence off-policy evaluation for deployment with some guarantees. In the real world the deployment may need to happen incrementally, where at fixed intervals of time we would like to update the current SR policy in a safe manner. In this section we present a batch reinforcement learning (RL) algorithm that provides probabilistic guarantees about the quality of each policy that it proposes, and which has no hyper-parameter that requires expert tuning. Specifically, the user may select any performance lower-bound, , and confidence level, , and our algorithm will ensure that the probability that it returns a policy with performance below is at most . We then propose an incremental algorithm that executes our policy improvement algorithm repeatedly to generate multiple policy improvements. We show the viability of our approach with a digital marketing application that uses real world data [69].

5.1 Problem Formulation

Given a (user specified) lower-bound, , on the performance and a confidence level, , we call an RL algorithm safe if it ensures that the probability that a policy with performance less than will be proposed is at most . The only assumption that a safe algorithm may make is that the underlying environment is a POMDP. Moreover, we require that the safety guarantee must hold regardless of how any hyperparameters are tuned.

We call an RL algorithm semi-safe if it would be safe, except that it makes a false but reasonable assumption. Semi-safe algorithms are of particular interest when the assumption that the environment is a POMDP is significantly stronger than any (other) false assumption made by the algorithm, e.g., that the sample mean of the importance weighted returns is normally distributed when using many trajectories.

We call a policy, , (as opposed to an algorithm) safe if we can ensure that with confidence . Note that “a policy is safe” is a statement about our belief concerning that policy given the observed data, and not a statement about the policy itself.

If there are many policies that might be deemed safe, then the policy improvement mechanism should return the one that is expected to perform the best, i.e.,

| (7) |

where is a prediction of computed from . We use a lower-variance, but biased, alternative to ordinary importance sampling, called weighted importance sampling [53], for , i.e.,

Note that even though Eq. (7) uses , our safety guarantee is uncompromising—it uses the true (unknown and often unknowable) expected return, .

In the following sections, we present batch and incremental policy improvement algorithms that are safe when they use the CI approach to HCOPE and semi-safe when they use the -test or BCa approaches. Our algorithms have no hyperparameters that require expert tuning.

In the following, we use the symbol as a placeholder for either CI, TT, or BCa. We also overload the symbol so that it can take as input a policy, , and a set of trajectories, , in place of , as follows:

| (8) |

For example, is a prediction made using the data set of what the confidence lower-bound on would be, if computed from trajectories by BCa.

5.2 Safe Policy Improvement

Our proposed batch (semi-)safe policy improvement algorithm, PolicyImprovement, takes as input a set of trajectories labeled with the policies that generated them, , a performance lower bound, , and a confidence level, , and outputs either a new policy or No Solution Found (NSF). The meaning of the subscript will be described later.

When we use to both search the space of policies and perform safety tests, we must be careful to avoid the multiple comparisons problem [7]. To make this important problem clear, consider what would happen if our search of policy space included only two policies, and used all of to test both of them for safety. If at least one is deemed safe, then we return it. HCOPE methods can incorrectly label a policy as safe with probability at most . However, the system we have described will make an error whenever either policy is incorrectly labeled as safe, which means its error rate can be as large as . In practice the search of policy space should include many more than just two policies, which would further increase the error rate.

We avoid the multiple comparisons problem by setting aside data that is only used for a single safety test that determines whether or not a policy will be returned. Specifically, we first partition the data into a small training set, , and a larger test set, . The training set is used to search for which single policy, called the candidate policy, , should be tested for safety using the test set. This policy improvement method, PolicyImprovement, is reported in Algorithm 2. To simplify later pseudocode, PolicyImprovement assumes that the trajectories have already been partitioned into and . In practice, we place of the trajectories in the training set and the remainder in the test set. Also, note that PolicyImprovement can use the safe concentration inequality approach, CI, or the semi-safe -test or BCa approaches, TT, BCa.

PolicyImprovement is presented in a top-down manner in Algorithm 2, and makes use of the GetCandidatePolicy method, which searches for a candidate policy. The input specifies the number of trajectories that will be used during the subsequent safety test. Although GetCandidatePolicy could be any batch RL algorithm, like LSPI or FQI [37, 20], we propose an approach that leverages our knowledge that the candidate policy must pass a safety test. We will present two versions of GetCandidatePolicy, which we differentiate between using the subscript , which may stand for None or -fold.

Before presenting these two methods, we define an objective function as:

Intuitively, returns the predicted performance of if the predicted lower-bound on is at least , and the predicted lower-bound on , otherwise.

Consider GetCandidatePolicy, which is presented in Algorithm 3. This method uses all of the available training data to search for the policy that is predicted to perform the best, subject to it also being predicted to pass the safety test. That is, if no policy is found that is predicted to pass the safety test, it returns the policy, , that it predicts will have the highest lower bound on . If policies are found that are predicted to pass the safety test, it returns one that is predicted to perform the best (according to ).

The benefits of this approach are its simplicity and that it works well when there is an abundance of data. However, when there are few trajectories in (e.g., cold start), this approach has a tendency to overfit—it finds a policy that it predicts will perform exceptionally well and which will easily pass the safety test, but actually fails the subsequent safety test in PolicyImprovement. We call this method = None because it does not use any methods to avoid overfitting.

In machine learning, it is common to introduce a regularization term, , into the objective function in order to prevent overfitting. Here is the model’s weight vector and is some measure of the complexity of the model (often or squared -norm), and is a parameter that is tuned using a model selection method like cross-validation. This term penalizes solutions that are too complex, since they are likely to be overfitting the training data.

Here we can use the same intuition, where we control for the complexity of the solution policy using a regularization parameter, , that is optimized using -fold cross-validation. Just as the squared -norm relates the complexity of a weight vector to its squared distance from the zero vector, we define the complexity of a policy to be some notion of its distance from the initial policy, . In order to allow for an intuitive meaning of , rather than adding a regularization term to our objective function, , we directly constrain the set of policies that we search over to have limited complexity.

We achieve this by only searching the space of mixed policies , where . Here, is the fixed regularization parameter, is the fixed initial policy, and we search the space of all possible . Consider, for example what happens to the probability of action in state when . If , then for any , we have that . That is, the mixed policy can only move of the way towards being deterministic (in either direction). In general, denotes that the mixed policy can change the probability of an action no more than towards being deterministic. So, using mixed policies results in our searches of policy space being constrained to some feasible set centered around the initial policy, and where scales the size of this feasible set.

While small values of can effectively eliminate overfitting by precluding the mixed policy from moving far away from the initial policy, they also limit the quality of the best mixed policy in the feasible set. It is therefore important that is chosen to balance the tradeoff between overfitting and limiting the quality of solutions that remain in the feasible set. Just as in machine learning, we use -fold cross-validation to automatically select .

This approach is provided in Algorithm 4, where CrossValidate uses -fold cross-validation to predict the value of if were to be optimized using and regularization parameter . CrossValidate† is reported in Algorithm 5. In our implementations we use folds.

5.3 Daedalus

The PolicyImprovement algorithm is a batch method that can be applied to an existing data set, . However, it can also be used in an incremental manner by executing new safe policies whenever they are found. The user might choose to change at each iteration, e.g., to reflect an estimate of the performance of the best policy found so far or the most recently proposed policy. However, for simplicity in our pseudocode and experiments, we assume that the user fixes as an estimate of the performance of the initial policy. This scheme for selecting is appropriate when trying to convince a user to deploy an RL algorithm to tune a currently fixed initial policy, since it guarantees with high confidence that it will not decrease performance.

Our algorithm maintains a list, , of the policies that it has deemed safe. When generating new trajectories, it always uses the policy in that is expected to perform best. is initialized to include a single initial policy, , which is the same as the baseline policy used by GetCandidatePolicy. This online safe learning algorithm is presented in Algorithm 6.111If trajectories are available a priori, then and can be initialized accordingly. It takes as input an additional constant, , which denotes the number of trajectories to be generated by each policy. If is not already specified by the application, it should be selected to be as small as possible, while allowing Daedalus to execute within the available time. We name this algorithm Daedalus after the mythological character who promoted safety when he encouraged Icarus to use caution.

The benefits of -fold are biggest when only a few trajectories are available, since then GetCandidatePolicy is prone to overfitting. When there is a lot of data, overfitting is not a big problem, and so the additional computational complexity of -fold cross-validation is not justified. In our implementations of Daedalus, we therefore only use until the first policy is successfully added to , and = None thereafter. This provides the early benefits of -fold cross-validation without incurring its full computational complexity.

The Daedalus algorithm ensures safety with each newly proposed policy. That is, during each iteration of the while-loop, the probability that a new policy, , where , is added to is at most . The multiple comparison problem is not relevant here because this guarantee is per-iteration. However, if we consider the safety guarantee over multiple iterations of the while-loop, it applies and means that the probability that at least one policy, , where , is added to over iterations is at most .

We define Daedalus2 to be Daedalus but with line 11 removed. The multiple hypothesis testing problem does not affect Daedalus2 more than Daedalus, since the safety guarantee is per-iteration. However, a more subtle problem is introduced: the importance weighted returns from the trajectories in the testing set, , are not necessarily unbiased estimates of . This happens because the policy, , is computed in part from the trajectories in that are used to test it for safety. This dependence is depicted in Figure 6. We also modify Daedalus2 by changing lines 4 and 8 to , which introduces an additional minor dependence of on the trajectories in .

Although our theoretical analysis applies to Daedalus, we propose the use of Daedalus2 because the ability of the trajectories, , to bias the choice of which policy to test for safety in the future (, where ) towards a policy that will deem safe, is small. However, the benefits of Daedalus2 over Daedalus are significant—the set of trajectories used in the safety tests increases in size with each iteration, as opposed to always being of size . So, in practice, we expect the over-conservativeness of to far outweigh the error introduced by Daedalus2. Notice that Daedalus2 is safe (not just semi-safe) if we consider its execution up until the first change of the policy, since then the trajectories are always generated by , which is not influenced by any of the testing data.

5.4 Empirical Analysis

Case Study:

For our case study we used real data, captured with permission from the website of a Fortune 50 company that receives hundreds of thousands of visitors per day and which uses Adobe Target, to train a simulator using a proprietary in-house system identification tool at Adobe. The simulator produces a vector of real-valued features that provide a compressed representation of all of the available information about a user. The advertisements are clustered into two high-level classes that the agent must select between. After the agent selects an advertisement, the user either clicks (reward of ) or does not click (reward of ) and the feature vector describing the user is updated. Although this greedy approach has been successful, as we discussed in Section 4, it does not necessarily also maximize the total number of clicks from each user over his or her lifetime. Therefore, we consider a full reinforcement learning solution for this problem. We selected and . This is a particularly challenging problem because the reward signal is sparse. If each action is selected with probability always, only about of the transitions are rewarding, since users usually do not click on the advertisements. This means that most trajectories provide no feed-back. Also, whether a user clicks or not is close to random, so returns have relatively high variance. We generated data using an initial baseline policy and then evaluated a new policy proposed by an in-house reinforcement learning algorithm.

In order to avoid the large costs associated with deployment of a bad policy, in this application it is imperative that new policies proposed by RL algorithms are ensured to be safe before deployment.

Results:

In our experiments, we selected to be an empirical estimate of the performance of the initial policy and . We used CMA-ES [24] to solve all , where was parameterized by a vector of policy parameters using linear softmax action selection [60] with the Fourier basis [35].

For our problem domain, we executed Daedalus2 with CI, TT, BCa and None, -fold. Ideally, we would use for all domains. However, as decreases, the runtime increases. We selected for the digital marketing domain. increases with the number of trajectories in the digital marketing domain so that the plot can span the number of trajectories required by the CI approach without requiring too many calls to the computationally demanding PolicyImprovement method. We did not tune for these experiments—it was set solely to limit the runtime.

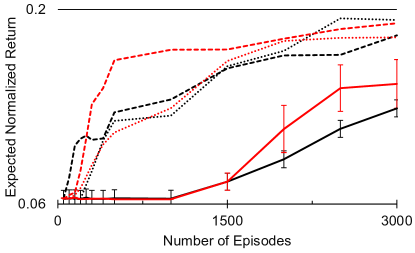

The performance of Daedalus2 on the digital marketing domain is provided in Figure 7. The expected normalized returns in Figure 7 are computed using Monte Carlo rollouts, respectively. The curves are also averaged over trials, respectively, with standard error bars provided when they do not cause too much clutter.

First, consider the different values for . As expected, the CI approaches (solid curves) are the most conservative, and therefore require the most trajectories in order to guarantee improvement. The BCa approaches (dashed lines) perform the best, and are able to provide high-confidence guarantees of improvement with as few as trajectories. The TT approach (dotted lines) perform in-between the CI and BCa approaches, as expected (since the -test tends to produce overly conservative lower bounds for distributions with heavy upper tails).

Next, consider the different values of . Using -fold cross-validation provides an early boost in performance by limiting overfitting when there are few trajectories in the training set. Although the results are not shown, we experimented with using -fold for the entire runtime (rather than just until the first policy improvement), but found that while it did increase the runtime significantly, it did not produce much improvement.

6 Non-Stationarity

In the previous sections we made a critical assumption that the domain can be modeled as a POMDP. However, real world problems are often non-stationary. In this section we consider the problem of evaluating an SR policy off-line without assuming stationary transition and rewards. We argue that off-policy policy evaluation for non-stationary MDPs can be phrased as a time series prediction problem, which results in predictive methods that can anticipate changes before they happen. We therefore propose a synthesis of existing off-policy policy evaluation methods with existing time series prediction methods, which we show results in a drastic reduction of mean squared error when evaluating policies using real digital marketing data set [70].

6.1 Motivating Example

In digital marketing applications, when a person visits the website of a company, she is often shown a list of current promotions. In order for the display of these promotions to be effective, it must be properly targeted based on the known information about the person (e.g., her interests, past travel behavior, or income). The problem now reduces to automatically deciding which promotion (sometimes called a campaign) to show to the visitor of a website.

As we have described in Section 4 the system’s goal is to determine how to select actions (select promotions to display) based on the available observations (the known information of the visitor) such that the reward is maximized (the number of clicks is maximized). Let be the performance of the policy in episode . In the bandit setting is the expected number of clicks per visit, called the click through rate (CTR), while in the reinforcement learning setting it is the expected number of clicks per user, called the life-time value (LTV).

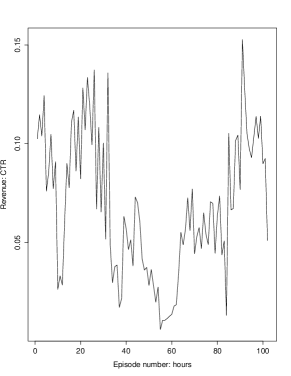

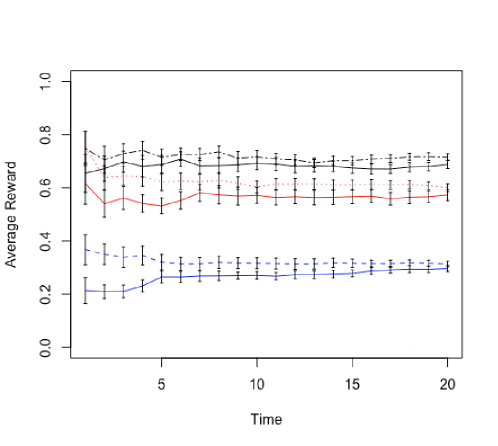

In order to determine how much of a problem non-stationarity really is, we collected data from the website of one of Adobe’s Test and Target customers: the website of a large company in the hotel and entertainment industry. We then used a proprietary policy search algorithm custom designed for digital marketing to generate a new policy for the customer. We then collected new episodes of data, which we used as , to compute for all using ordinary importance sampling. Figure 8 summarizes the resulting data.

In this data it is evident that there is significant non-stationarity—the CTR varied drastically over the span of the plot. This is also not just an artifact of high variance: using Student’s -test we can conclude that the expected return during the first and subsequent episodes was different with . This is compelling evidence that we cannot ignore non-stationarity in our users’ data when providing predictions of the expected future performance of our digital marketing algorithms, and is compelling real-world motivation for developing non-stationary off-policy policy evaluation algorithms.

6.2 Nonstationary Off-Policy Policy Evaluation (NOPE)

Non-stationary Off-Policy Policy Evaluation (NOPE) is simply OPE for non-stationary MDPs. In this setting, the goal is to use the available data to estimate —the performance of during the next episode (the episode).

Notice that we have not made assumptions about how the transition and reward functions of the non-stationary MDP change. For some applications, they may drift slowly, making change slowly with . For example, this sort of drift may occur due to mechanical wear in a robot. For other applications, may be fixed for some number of episodes, and then make a large jump. For example, this sort of jump may occur in digital marketing applications [64] due to media coverage of a relevant topic rapidly changing public opinion of a product. In yet other applications, the environment may include both large jumps and smooth drift.

Notice that NOPE can range from trivial to completely intractable. If the MDP has few states and actions, changes slowly between episodes, and the evaluation policy is similar to the behavior policy, then we should be able to get accurate off-policy estimates. On the other extreme, if for each episode the MDP’s transition and reward functions are drawn randomly (or adversarially) from a wide distribution, then producing accurate estimates of may be intractable.

6.3 Predictive Off-Policy Evaluation using Time Series Methods

The primary insight in this section, in retrospect, is obvious: NOPE is a time series prediction problem. Figure 9 provides an illustration of the idea. Let and for . This makes an array of times (each episode corresponds to one unit of time) and an array of the corresponding observations. Our goal is to predict the expected value of the next point in this time series, which will occur at . Pseudocode for this time series prediction (TSP) approach is given in Algorithm 7.

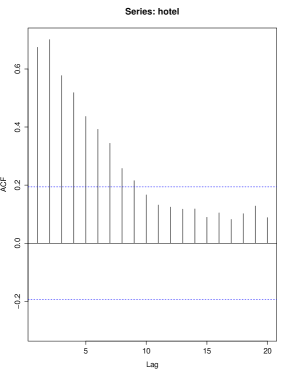

When considering using time-series prediction methods for off-policy policy evaluation, it is important that we establish that the underlying process is actually nonstationary. One popular method for determining whether a process is stationary or nonstationary is to report the sample autocorrelation function (ACF):

where is a parameter called the lag (which is selected by the researcher), is the time series, and is the mean of the time series. For a stationary time series, the ACF will drop to zero relatively quickly, while the ACF of nonstationary data decreases slowly.

ARIMA models are models of time series data that can capture many different sources of non-stationarity. The time series prediction algorithm that we use in our experiments is the forecast package for fitting ARIMA models [28].

6.4 Empirical Studies

In this section we show that, despite the lack of theoretical results about using TSP for NOPE, it performs remarkably well on real data. Because our experiments use real-world data, we do not know ground truth—we have for a series of , but we do not know for any . This makes evaluating our methods challenging—we cannot, for example, compute the true error or mean squared error of estimates. We therefore estimate the mean error and mean squared error directly from the data as follows.

For each we compute each method’s output, , given all of the previous data, . We then compute the observed next value, . From these, we compute the squared error, , and we report the mean squared error over all . We perform this experiment using both the current standard OPE approach, which computes sample mean of performance over all the available data, and using our new time series prediction approach.

Notice that this scheme is not perfect. Even if an estimator perfectly predicts for every , it will be reported as having non-zero mean squared error. This is due to the high variance of , which gets conflated with the variance of in our estimate of mean squared error. Although this means that the mean squared errors that we report are not good estimates of the mean squared error of the estimators, , the variance-conflation problem impacts all methods nearly equally. So, in the absence of ground truth knowledge, the reported mean squared error values are a reasonable measure of how accurate the methods are relative to each other.

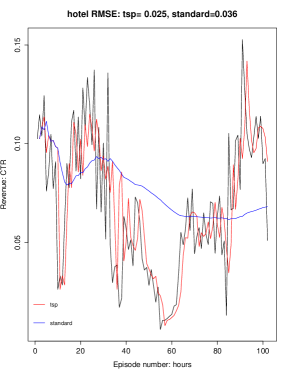

The domain we consider is digital marketing using the data from the large companies in the hotel and entertainment industry as described in Section 6.1. We refer to this domain as the Hotel domain. For this domain, and all others, we used ordinary importance sampling for . Recall that the performance of the evaluation policy appears to drop initially—the probability of a user clicking decays from a remarkably high down to a near-zero probability—before it rises back to close to its starting level. Recall also that using a two-sided Student’s -test we found that the true mean during the first trajectories was different from the true mean during the subsequent trajectories with , so the non-stationarity that we see is likely not noise.

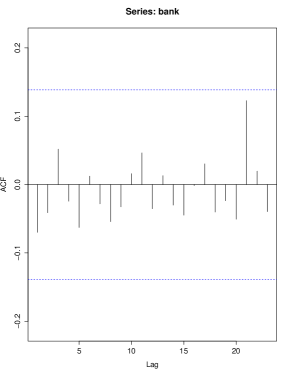

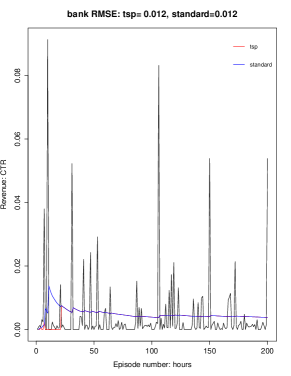

We collected additional data from the website of a large company in the financial industry, and used the same proprietary policy improvement algorithm to find a new policy that we might consider deploying for the user. There appears to be less long-term non-stationarity in this data, and a two-sided Student’s -test did not detect a difference between the early and late performance of the evaluation policy. We refer to this data as the Bank domain.

6.5 Results

We applied our TSP algorithm for NOPE, described in Algorithm 7, to the nonstationary hotel and bank data sets. The plots in Figure 10 all take the same form: the plots on the left are autocorrelation plots that show whether or not there appears to be non-stationarity in the data. As a rule of thumb, if the ACF values are within the dotted blue lines, then there is not sufficient evidence to conclude that there is non-stationarity. However, if the ACF values lie outside the dotted blue lines, it suggests that there is non-stationarity.

The plots on the right depict the expected return (which is the expected CTR for the hotel and bank data sets) as predicted by several different methods. The black curves are the target values—the observed mean OPE estimate over a small time interval. For each episode number, our goal is to compute the value of the black curve given all of the previous values of the black curve. The blue curve does this using the standard method, which simply averages the previous black points. The red curve is our newly proposed method, which uses ARIMA to predict the next point on the black curve—to predict the performance of the evaluation policy during the next episode. Above the plots we report the sample root mean squared error (RMSE) for our method, tsp, and the standard method, standard.

Consider the results on the hotel data set, which are depicted in Figure 10 (Top). The red curve (our method) tracks the binned values (black curve) much better than the blue curve (standard method). Also, the sample RMSE of our method is , which is lower than the standard method’s RMSE of . This suggests that treating the problem as a time series prediction problem results in more accurate estimates.

Finally, consider the results on the bank data set, which are depicted in Figure 10 (Bottom). The auto-correlation plot suggests that there is not much non-stationarity in this data set. This validates another interesting use case for our method: does it break down when the environment happens to be (approximately) stationary? The results suggest that it does not—our method achieves the same RMSE as the standard method, and the blue and red curves are visually quite similar.

An interesting research question is whether our high-confidence policy evaluation and improvement algorithms can be extended to non-stationary MDPs. However, following TSP algorithm, it can be noticed that estimating performance of a policy with high-confidence in non-stationary MDP can be reduced to time-series forecasting with high-confidence, which in complete generality is infeasible. An open research direction is to leverage domain specific structure of the problem and identify conditions under which this problem can be made feasible.

7 Learning from Passive Data

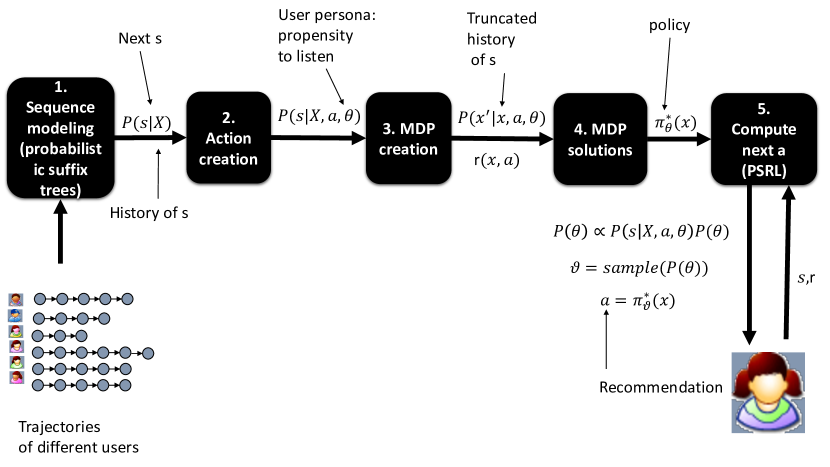

Constructing SR systems is particularly challenging due to the cold start problem. Fortunately, in many real world problems, there is an abundance of sequential data which are usually ‘passive’ in that they do not include past recommendations. In this section we propose a practical approach that learns from passive data. We use scalar parameterization that turns a passive model into active, and posterior sampling for Reinforcement learning (PSRL) to learn the correct parameter value. In this section we summarize our work from [65, 66].

The idea is to first learn a model from passive data that predicts the next activity given the history of activities. This can be thought of as the ‘no-recommendation’ or passive model. To create actions for recommending the various activities, we can perturb the passive model. Each perturbed model increases the probability of following the recommendations, by a different amount. This leads to a set of models, each one with a different ‘propensity to listen’. In effect, the single ‘propensity to listen’ parameter is used to turn a passive model into a set of active models. When there are multiple models one can use online algorithms, such as posterior sampling for Reinforcement learning (PSRL) to identify the best model for a new user [59, 47]. In fact, we used a deterministic schedule PSRL (DS-PSRL) algorithm, for which we have shown how it satisfies the assumptions of our parameterization in [66]. The overall solution is shown in Figure 11.

7.1 Sequence Modeling

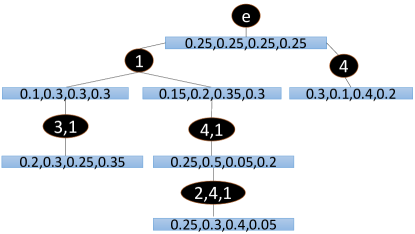

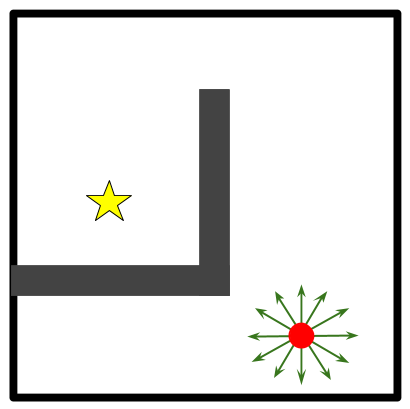

The first step in the solution is to model past sequences of activities. Due to the fact that the number of activities is usually finite and discrete and the fact that what activity a person may do next next depends on the history of activities done, we chose to model activity sequences using probabilistic suffix trees (PST). PSTs are a compact way of modeling the most frequent suffixes, or history of a discrete alphabet (e.g., a set of activities). The nodes of a PST represent suffixes (or histories). Each node is associated with a probability distribution for observing every symbol in the alphabet, given the node suffix [21]. Given a PST model one could easily estimate the probability of the next symbol given the history of symbols as . An example PST is shown in Figure 12.

The log likelihood of a set of sequences can easily be computed as , where are all the symbols appearing in the data and maps the longest suffixes (nodes) available in the tree for each symbol. For our implementation we learned PSTs using the pstree algorithm from [21]. The pstree algorithm can take as input multiple parameters, such as the depth of the tree, the number of minimum occurrence of a suffix, and parametrized tree pruning methods. To select the best set of parameters we perform model selection using the Modified Akaike Information Criterion (AICc) , where is the log likelihood as defined earlier and is the number of parameters [2] .

7.2 Action Creation

The second step involves the creation of action models for representing various personas. An easy way to create such parameterization, is to perturb the passive dynamics of the crowd PST (a global PST learned from all the data). Each perturbed model increases the probability of listening to the recommendation by a different amount. While there could be many functions to increase the transition probabilities, in our implementation we did it as follows:

| (9) |

where is an activity, a history of activities, and is a normalizing factor.

7.3 Markov Decision Processes

The third step is to create MDPs from and compute their policies in the fourth step. It is straightforward to use the PST to compute an MDP model, where the states/contexts are all the nodes of the PST. If we denote to be a suffix available in the tree, then we can compute the probability of transitioning from every node to every other node by finding resulting suffixes in the tree for every additional symbol that an action can produce:

where , is the longest suffix in the PST of suffix concatenated with symbol . We set the reward , where is a function of the suffix history and the recommendation. This gives us a finite and practically small state space. We can use the classic policy iteration algorithm to compute the optimal policies and value functions .

7.4 Posterior Sampling for Reinforcement Learning

The fifth step is to use on-line learning to compute the true user parameters. For this we used a posterior sampling for reinforcement learning (PSRL) algorithm called deterministic schedule PSRL (DS-PSRL) [66]. The DS-PSRL algorithm shown in Figure 13 changes the policy in an exponentially rare fashion; if the length of the current episode is , the next episode would be . This switching policy ensures that the total number of switches is .

Inputs: , the prior distribution of . . for do if then Sample . . else . end if Calculate near-optimal action . Execute action and observe the new state . Update with to obtain . end for

The algorithm makes three assumptions. First is assumes assume that MDP is weakly communicating. This is a standard assumption and under this assumption, the optimal average loss satisfies the Bellman equation. Second, it assumes that the dynamics are parametrized by a scalar parameter and satisfy a smoothness condition.

Assumption 7.1 (Lipschitz Dynamics).

There exist a constant such that for any state and action and parameters ,

Third, it makes a concentrating posterior assumption, which states that the variance of the difference between the true parameter and the sampled parameter gets smaller as more samples are gathered.

Assumption 7.2 (Concentrating Posterior).

Let be one plus the number of steps in the first episodes. Let be sampled from the posterior at the current episode . Then there exists a constant such that

The 7.2 assumption simply says the variance of posterior decreases given more data. In other words, we assume that the problem is learnable and not a degenerate case. 7.2 was actually shown to hold for two general categories of problems, finite MDPs and linearly parametrized problems with Gaussian noise [1]. Under these assumptions we the following theorem can be proven [66].

Theorem 7.3.

Notice that the regret bound in Theorem 7.3 does not directly depend on or . Moreover, notice that the regret bound is smaller if the Lipschitz constant is smaller or the posterior concentrates faster (i.e. is smaller).

7.5 Satisfying the Assumptions

Here we summarize how the parameterization assumption in Equation 9 satisfies assumptions 7.1 and 7.2.

Lipschitz Dynamics

We can show that the dynamics are Lipschitz continuous:

Lemma 7.4.

(Lipschitz Continuity) Assume the dynamics are given by Equation 9. Then for all and all and , we have

Concentrating Posterior

8 Optimizing for Recommendation Acceptance

Accepting recommendations needs deeper consideration than simply predicting click through probability of an offer. In this section we examine two acceptance factors, the ‘propensity to listen’ and ‘recommendations fatigue’. The ‘propensity to listen’ is a byproduct of the passive data solution shown in Section 7. The ‘recommendation fatigue’ is a problem where people may quickly stop paying attention to recommendations such as ads, if they are presented too often. The property of RL algorithms for solving delayed reward problems gives a natural solution to this fundamental marketing problem. For example, if the decision was to recommend, or not some product every day, where the final goal would be to buy at some point in time, then RL would naturally optimize the right sending schedule and thus avoid fatigue. In this section we present experimental results for a Point-of-Interest (POI) recommendation system that solves both, the ‘propensity to listen’ as well as ‘recommendation fatigue’ problems [65].

We experimented with a points of interest domain. For experiments we used the Yahoo! Flicker Creative Commons 100M (YFCC100M) [71], which consists of 100M Flickr photos and videos. This dataset also comprises the meta information regarding the photos, such as the date/time taken, geo-location coordinates and accuracy of these geo-location coordinates. The geo-location accuracy range from world level (least accurate) to street level (most accurate). We used location sequences that were mapped to POIs near Melbourne Australia222The data and pre-processing algorithms are publicly available on https://github.com/arongdari/flickr-photo. After preprocessing, and removing loops, we had 7246 trajectories and 88 POIs.

We trained a PST using the data and performed various experiments to test the ability of our algorithm to quickly optimize the cumulative reward for a given user. We used and did experiments assuming the true user to be any of those . For reward, we used a signal between indicating the frequency/desirability of the POIs. We computed the frequency from the data. The action space was a recommendation for each POI (88 POIs), plus a null action. All actions but the null action had a cost of the reward. Recommending a POI that was already seen (e.g in the current suffix) had an additional cost of of the reward. This was done in order to reduce the number of recommendations otherwise called the fatigue factor. We compared DS-PSRL with greedy policies. Greedy policies do not solve the underlying MDP but rather choose the action with maximum immediate reward, which is equivalent to the classic Thompson sampling for contextual bandits. PSRL could also be thought of as Thompson sampling for MDPs. We also compared with the optimal solution, which is the one that knows the true model from the beginning. Our experiments are shown in Tables 1 and 2 and Figure 14. DS-PSRL quickly learns to optimize the average reward. At the same time it produces more reward than the greedy approach, while minimizing the fatigue factor.

| GREEDY | MDP | |

|---|---|---|

| 0.45 | 0.5 | |

| TS | 0.32 | 0.42 |

| Time | GREEDY | MDP |

|---|---|---|

| 1 | 72 | 72 |

| 2 | 71 | 51 |

| 3 | 72 | 0 |

| 4 | 71 | 72 |

| 5 | 72 | 51 |

| 6 | 71 | 0 |

9 Capacity-aware Sequential Recommendations

So far we have considered recommendation systems that consider each user individually, ignoring the collective effects of recommendations. However, ignoring the collective effects could result in diminished utility for the user, for example through overcrowding at high-value points of interest (POI) considered in Section 8. In this section we summarize a solution that can optimize for both latent factors and resource constraints in SR systems [45].

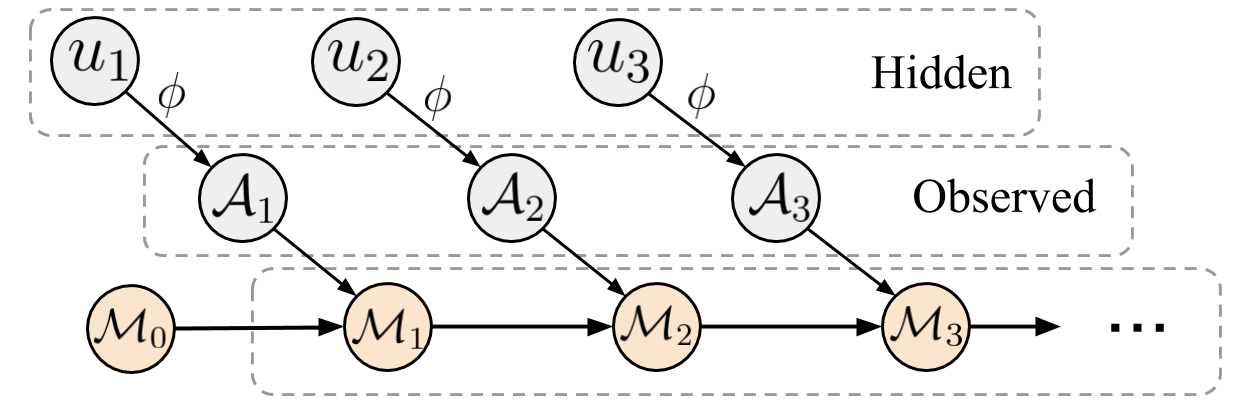

To incorporate collective effects in recommendation systems, we extend our model to a multi-agent system with global capacity constraints, representing for example, the maximum capacity for visitors at a POI. Furthermore, to handle latent factors, we model each user as a partially observable decision problem, where the hidden state factor represents the user’s latent interests.

An optimal decision policy for this partially observable problem chooses recommendations that find the best possible trade-off between exploration and exploitation. Unfortunately, both global constraints and partial observability make finding the optimal policy intractable in general. However, we show that the structure of this problem can be exploited, through a novel belief-space sampling algorithm which bounds the size of the state space by a limit on regret incurred from switching from the partially observable model to the most likely fully observable model. We show how to decouple constraint satisfaction from sequential recommendation policies, resulting in algorithms which issue recommendations to thousands of agents while respecting constraints.

9.1 Model of capacity-aware sequential recommendation problem

While PSRL (Section 7.4) eventually converges to the optimal policy, it will never select actions which are not part of the optimal policy for any , even if this action would immediately reveal the true parameters to the learner. In order to reason about such information gathering actions, a recommender should explicitly consider the decision-theoretic value of information [27]. To do so, we follow [12] in modeling such a hidden-model MDP as a Mixed-Observability MDP (MOMDP).

The state space of a MOMDP model factors into a fully observable factor and a partially observable factor , each with their own transition functions, and . An observation function exists to inform the decision maker about transitions of the hidden factor. However, in addition to the observations, the decision maker also conditions his policy on the observable factor . Given a parametric MDP over a finite set of user types , for example as generated in Section 7.3, we derive an equivalent MOMDP having elements

| (10) | ||||||||

The model uses the latent factor to represent the agent’s type, selecting the type-specific transition and reward functions based on its instantiation. Because a user’s type does not change over the plan horizon, the model is a ‘stationary’ Mixed-Observability MDP [41]. The observation function is uninformative, meaning that there is no direct way to infer a user’s type. Intuitively, this means the recommender can only learn a user’s type by observing state transitions.

This gives a recommender model for a single user , out of a total of users. To model the global capacities at different points of interest, we employ a consumption function and limit vector defined over POIs. The consumption of resource type is defined using function , where 1 indicates that the user is present at . The limit function gives POI ’s peak capacity. The optimal (joint) recommender policy satisfies the constraints in expectation, optimizing

| (11) |

For multi-agent problems of reasonable size, directly optimizing this joint policy is infeasible. For such models Column Generation (CG; [23]) has proven to be an effective algorithm [46, 75, 77]. Agent planning problems are decoupled by augmenting the optimality criterion of the (single-agent) planning problem with a Lagrangian term pricing the expected resource consumption cost , i.e.,

| (12) |

This routine is used to compute a new policy to be added to a set of potential policies of agent . These sets form the search space of the CG LP, which optimizes the current best joint mix of policies subject to constraints, by solving:

| (13) | |||||

| s.t. | |||||

Solving this LP results in: 1) a probability distribution over policies, having agents follow a policy with , and 2) a new set of dual prices to use in the subsequent iteration. This routine stops once , at which point a global optimum is found.

9.2 Bounded belief state space planning

Unfortunately, in every iteration of column generation, we need to find optimal policies satisfying Equation (12), which in itself has PSPACE complexity for MOMDPs [48]. Therefore, we propose a heuristic algorithm exploiting the structure of our problems: bounded belief state space planning (Alg. 8).

To plan for partially observable MDP models it is convenient to reason over belief states [31]. In our case, a belief state records a probability distribution over the possible types , with indicating how likely the agent is of type . Given a belief state , the action taken , and the observation received , the subsequent belief state can be derived using application of Bayes’ theorem. In principle, this belief-state model can be used to compute the optimal policy, but the exponential size of prohibits this. Therefore, approximation algorithms generally focus on a subset of the space .

When computing a policy for a truncated belief space we have to be careful that we compute unbiased consumption expectations , to guarantee feasibility of the Column Generation solution. This can be achieved if we know the exact expected consumption of the policy at each ‘missing’ belief point not in . For corners of the belief space, where (and for ), the fact that agent types are stationary ensures that the optimal continuation is the optimal policy for the . If we use the same policy in a non-corner belief, policy may instead be applied on a different , with probability . In general, the expected value of choosing policy in belief point is

| (14) |

For belief points close to corner , policy will be the optimal policy with high probability. If we take care to construct such that truncated points are close to corners, we can limit our search to the optimal policies of each type,

| (15) |

When we apply policy in a belief point that is not a corner, we incur regret proportional to the amount of value lost from getting the type wrong. Policy applied to obtains expected value by definition of optimality. Thus, the use of policy in belief point incurs a regret of

| (16) |

This regret function can serve as a scoring rule for belief points worth considering in belief space . Let stand for the probability of belief point , then we generate all subsequent belief points from initial belief that meet a threshold (for hyper-parameters minimum probability and shape ):

| (17) |

Algorithm 8 starts by computing the optimal MDP policy for each type , followed by determining the exact expected values of applying these policies to all different user types . The remainder of the algorithm computes expected values at each belief point in regret-truncated space , according to the typical dynamic programming recursion. However, in case of a missing point , the best policy is instead selected (line 15), and the expected value of using this MDP policy is computed according to the belief state. The resulting policy thus consists of two stages: the maximally valued action stored in is selected, unless , at which point MDP policy replaces for the remaining steps.

9.3 Empirical evaluation of scalability versus quality

By bounding the exponential growth of the state space, Algorithm 8 trades off solution quality for scalability. To assess this trade-off, we perform an experiment on the POI recommendation problem introduced in Section 8. We compare with the highly scalable PSRL on the one hand, and state-of-the-art mixed-observability MDP planner SARSOP [36] on the other. We consider a problem consisting of 5 POIs, 3 user types, 50 users and PST depth 1. For this experiment we measure the quality of the computed policy as the mean over 1,000 simulations per instance, solving instances per setting of the horizon. We consider two settings, the regular single recommendation case, and a dual recommendation case where the recommender is allowed to give an alternative to the main recommendation, which may provide more opportunities to gather information in each step.

Figure 15 presents the results. The top row presents the observed mean reward, while the bottom row presents the required planning time in minutes. We observe that for our constrained finite-horizon problems, SARSOP quickly becomes intractable, even when the discount factor is set very low. However, by not optimizing for information value, PSRL obtains significantly lower lifetime value. Our algorithm finds policies which do maximize information value, while at the same time remaining tractable through its effective bounding condition on the state space growth. We note that its runtime stops increasing significantly beyond , as a result of the bounded growth of the state space.

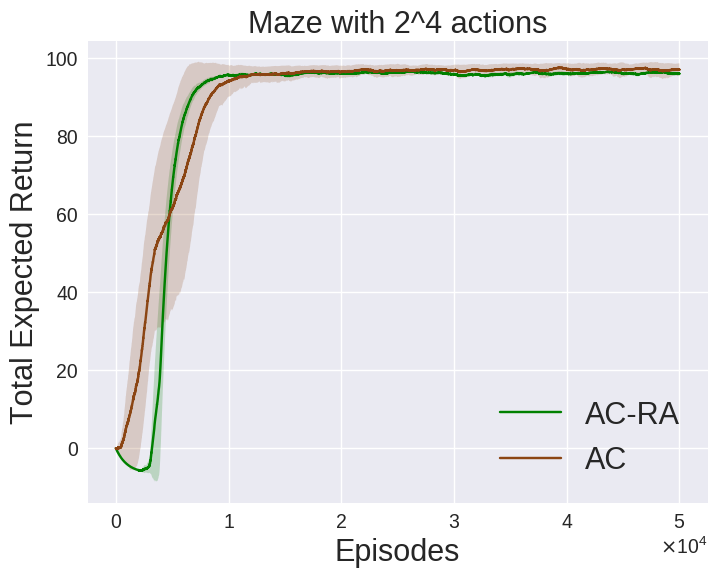

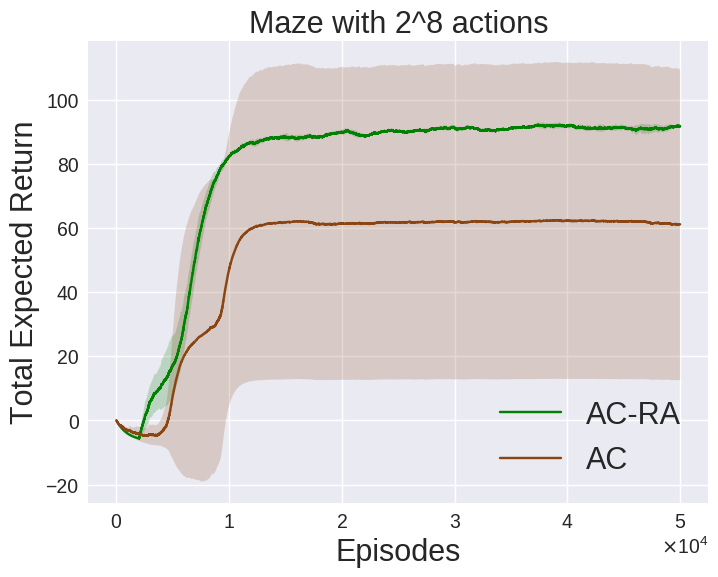

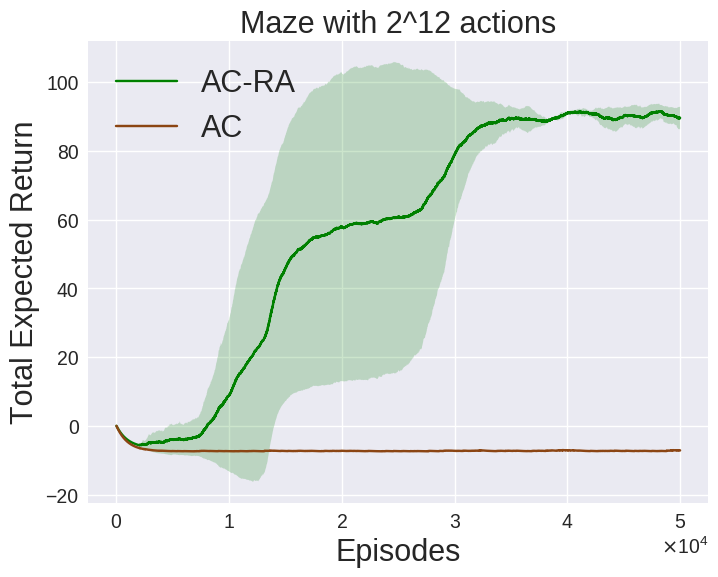

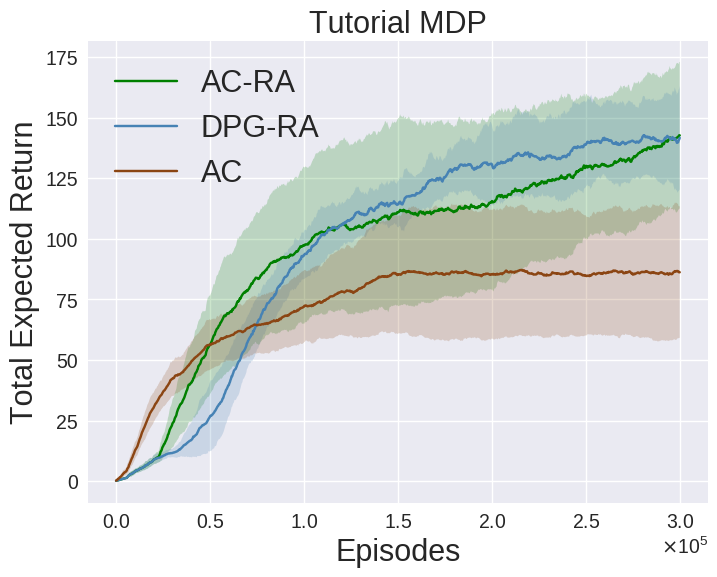

10 Large Action Spaces

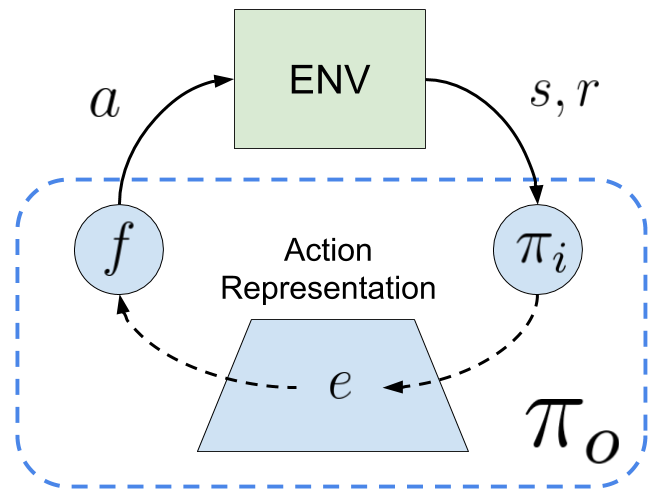

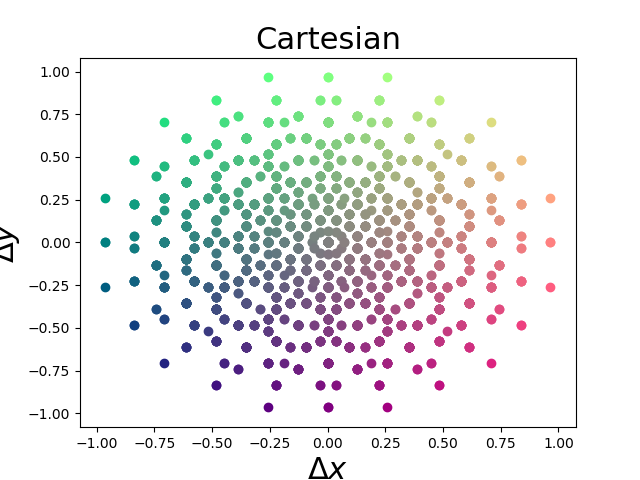

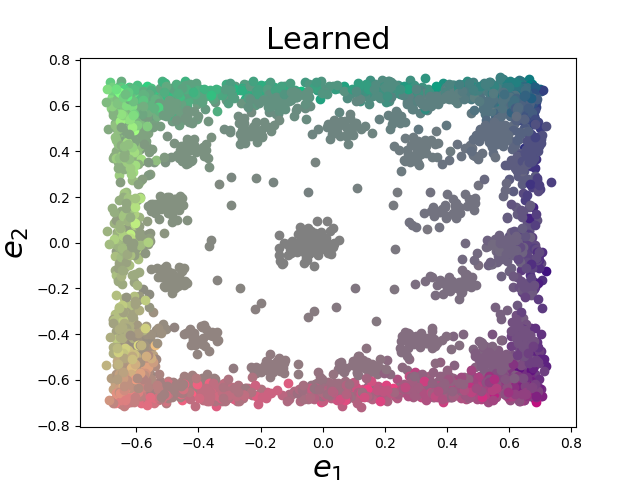

In many real-world recommendation systems the number of actions could be prohibitively large. Netflix for example employs a few thousands of movie recommendations. For SR systems the difficulty is even more severe, since the search space grows exponentially with the planning horizon. In this section we show how to learn action embeddings for action generalization. Most model-free reinforcement learning methods leverage state representations (embeddings) for generalization, but either ignore structure in the space of actions or assume the structure is provided a priori. We show how a policy can be decomposed into a component that acts in a low-dimensional space of action representations and a component that transforms these representations into actual actions. These representations improve generalization over large, finite action sets by allowing the agent to infer the outcomes of actions similar to actions already taken. We provide an algorithm to both learn and use action representations and provide conditions for its convergence. The efficacy of the proposed method is demonstrated on large-scale real-world problems [13].

10.1 Generalization over Actions

The benefits of capturing the structure in the underlying state space of MDPs is a well understood and a widely used concept in RL. State representations allow the policy to generalize across states. Similarly, there often exists additional structure in the space of actions that can be leveraged. We hypothesize that exploiting this structure can enable quick generalization across actions, thereby making learning with large action sets feasible. To bridge the gap, we introduce an action representation space, , and consider a factorized policy, , parameterized by an embedding-to-action mapping function, , and an internal policy, , such that the distribution of given is characterized by:

| (18) |

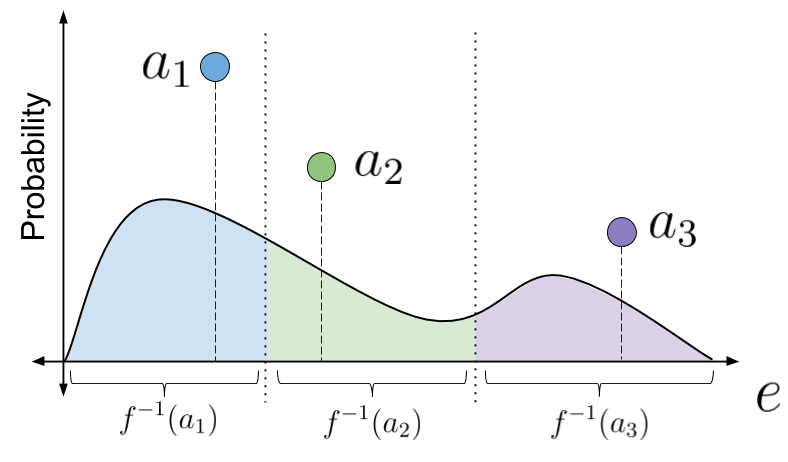

Here, is used to sample , and the function deterministically maps this representation to an action in the set . Both these components together form an overall policy, . Figure 16 (Right) illustrates the probability of each action under such a parameterization. With a slight abuse of notation, we use as a one-to-many function that denotes the set of representations that are mapped to the action by the function , i.e., .

In the following sections we discuss the existence of an optimal policy and the learning procedure for . To elucidate the steps involved, we split it into four parts. First, we show that there exist and such that is an optimal policy. Then we present the supervised learning process for the function when is fixed. Next we give the policy gradient learning process for when is fixed. Finally, we combine these methods to learn and simultaneously.

10.2 Existence of and to Represent an Optimal Policy

In this section, we aim to establish a condition under which can represent an optimal policy. Consequently, we then define the optimal set of and using the proposed parameterization. To establish the main results we begin with the necessary assumptions.

The characteristics of the actions can be naturally associated with how they influence state transitions. In order to learn a representation for actions that captures this structure, we consider a standard Markov property, often used for learning probabilistic graphical models [22], and make the following assumption that the transition information can be sufficiently encoded to infer the action that was executed.

Assumption 10.1.

Given an embedding , is conditionally independent of and :

Assumption 10.2.

Given the embedding the action, is deterministic and is represented by a function , i.e., .

We now establish a necessary condition under which our proposed policy can represent an optimal policy. This condition will also be useful later when deriving learning rules.

Lemma 10.3.

The proof is available in [13]. Following Lemma (10.3), we use and to define the overall policy as

| (20) |

Theorem 10.4.

Proof.

This follows directly from Lemma 10.3. Because the state and action sets are finite, the rewards are bounded, and , there exists at least one optimal policy. For any optimal policy , the corresponding state-value and state-action-value functions are the unique and , respectively. By Lemma 10.3 there exist and such that

| (21) |

Therefore, there exists and , such that the resulting has the state-value function , and hence it represents an optimal policy. ∎

Note that Theorem 10.4 establishes existence of an optimal overall policy based on equivalence of the state-value function, but does not ensure that all optimal policies can be represented by an overall policy. Using (21), we define . Correspondingly, we define the set of optimal internal policies as .

10.3 Supervised Learning of for a Fixed

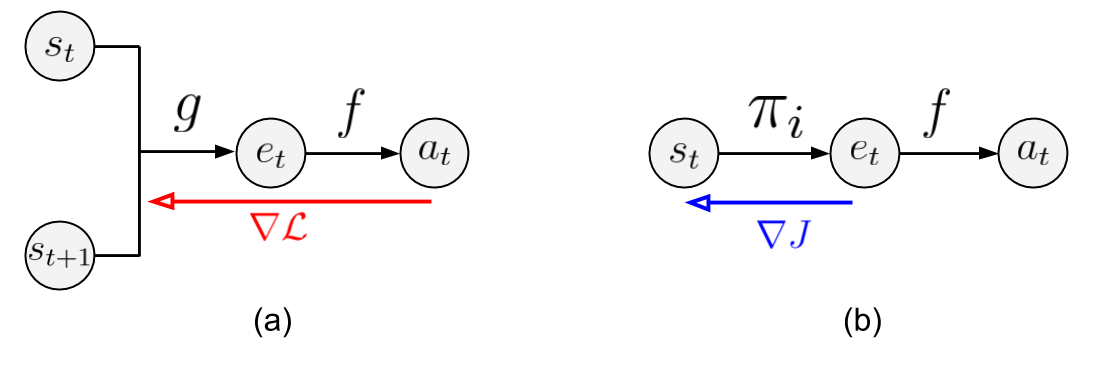

Theorem 10.4 shows that there exist and a function , which helps in predicting the action responsible for the transition from to , such that the corresponding overall policy is optimal. However, such a function, , may not be known a priori. In this section, we present a method to estimate using data collected from visits with the environment.

By Assumptions (10.1)–(10.2), can be written in terms of and . We propose searching for an estimator, , of and an estimator, , of such that a reconstruction of is accurate. Let this estimate of based on and be

| (22) |

One way to measure the difference between and is using the expected (over states coming from the on-policy distribution) Kullback-Leibler (KL) divergence

| (23) | ||||

| (24) |

Since the observed transition tuples, , contain the action responsible for the given to transition, an on-policy sample estimate of the KL-divergence can be computed readily using (24). We adopt the following loss function based on the KL divergence between and :

| (25) |

where the denominator in (24) is not included in (25) because it does not depend on or . If and are parameterized, their parameters can be learned by minimizing the loss function, , using a supervised learning procedure.

A computational graph for this model is shown in Figure 17. Note that, while will be used for in an overall policy, is only used to find , and will not serve an additional purpose.