On a Generalisation of the Marčenko-Pastur Problem

Abstract

We study the spectrum of generalized Wishart matrices, defined as , where and are matrices with zero mean, unit variance IID entries and such that . The limit corresponds to the Marčenko-Pastur problem. For a general , we show that the Stieltjes transform of is the solution of a cubic equation. In the limit , the density of eigenvalues converges to the Wigner semi-circle.

The celebrated Marčenko-Pastur problem concerns the eigenvalue spectrum of random covariance matrices in the large dimension limit. More precisely, consider an N-dimensional time series, , where and . Suppose that the ’s are IID random variables, of zero mean and unit variance. Then the empirical (or sample) covariance matrix is defined as

| (1) |

where is the matrix defined by . is called a (white) Wishart matrix.

Since our assumption is that the ’s are IID, the “true” covariance matrix is simply the identity matrix, which is the result obtained for in the limit , for a fixed value of . But there is another limit, which is very relevant in many applications, where and are both large; more precisely, where with a fixed ratio .

What is the spectrum of in that regime? The answer was provided by Marčenko and Pastur in 1967 [1], and is a classic result in Random Matrix Theory. When , the result for the density of eigenvalues is:

| (2) |

with . As expected when , i.e. when , becomes the identity matrix.

The problem we want to consider in this note is defined by the following symmetric cross-correlation matrix:111The singular value spectrum of the un-symmetrized matrix was considered for in [2, 3].

| (3) |

where and are two rectangular matrices of unit variance IID random variables, such that , where is the correlation coefficient between ’s and ’s. Clearly, when , and one recovers the Marčenko-Pastur problem. The aim of this work is to determine the spectrum of .

The most efficient way to approach this problem is by using the tools of free random matrix theory (see e.g. [4, 5]). In the large dimension limit, can be seen as the free addition of T two-dimensional projectors:

| (4) |

In the large limit, the spectrum of becomes independent of and is composed of zero eigenvalues and two non-zero eigenvalues, equal to . The corresponding Stieltjes function is thus:

| (5) |

from which we deduce the functional inverse defined as . To leading order in one finds:

| (6) |

Free matrix addition means that the -transform, defined as is additive. Hence the R-transform of is given by

| (7) |

From one backtracks to get and finally , the Stieltjes transform of that contains all the information about the density of eigenvalues of . Finally, is given by the appropriate solution of the following cubic equation:

| (8) |

This is the main result of the present paper. One can check that when one recovers the Stieltjes transform of a Wishart matrix, solution of the following quadratic equation:

| (9) |

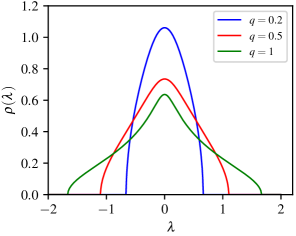

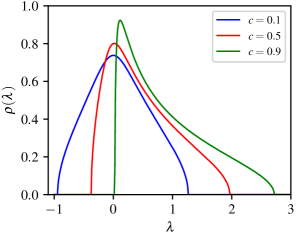

from which the Marčenko-Pastur result immediately follows. In Fig. 1 we show the spectrum of for some representative values of and , obtained as usual from the imaginary value of when . Note that when , a fraction of the eigenvalues are negative. In fact, the mean of the density of eigenvalues is equal to . The variance can be read-off the R-transform using .

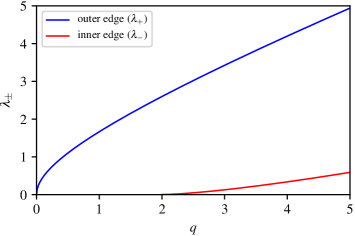

The case is particularly interesting. In this case the spectrum is an even function of , see Fig. 1. After a little work one can establish the following results:

-

1.

The edges of the spectrum, , are given by:

(10) where are the outer edges and are the inner edges (which only exist for ). They are plotted in Fig. 3.

-

2.

In the limit , the density becomes a Wigner semi-circle of radius ,

(11) When , one finds that all eigenvalues are zero, as expected since in this case .222More generally, when , all eigenvalues are equal to .

-

3.

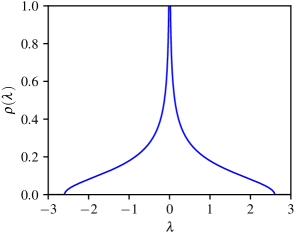

The case was studied before in the context of the addition of two non-symmetrized Wigner matrices, see [6, 7]. The corresponding distribution of eigenvalues was called the “tetilla” law [7].333It is also the distribution of eigenvalues of , where and are independent Wigner matrices. The explicit form for the density when is given by:

(12) Note that with our normalisation it has .

-

4.

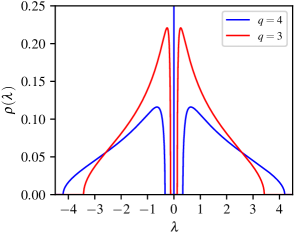

For , we also have a closed form expression for the density supported on :

(13) This density has a cubic-root singularity at (see Fig. 2):

(14) -

5.

For , a Dirac mass appears at . This is expected since in that case the two-dimensional projectors can no longer span the whole -dimensional space.

The above construction does not rely on the fact that the matrices and are real. In fact we can consider and to be with complex or even quaternion entries where the norm of each entry has unit variance, and define )/(2T). The eigenvalue spectrum in the complex () and quaternion () cases is then the same as the real case. These are three cases of the same beta-ensemble where as usual the density is independent of beta but not the eigenvalue fluctuations and correlations. The matrix potential of this ensemble satisfies for where is the correct root of the cubic equation (8), see e.g. [5].

Using -transforms to deal with free products of matrices, we know that the Marčenko-Pastur result can be generalised to the case where the “true” (population) covariance matrix of the ’s and of the ’s is a general definite positive matrix , i.e.:

| (15) |

with .

The same trick can be used in the present case as well, with now

| (16) |

Interestingly, when , one finds that the spectrum of is the same as that of and therefore independent of . Indeed for a trace-less matrix (such as with ) the free product with matrix is equivalent to a simple scaling of by . For , however, this is not true – as it is well known in the Marčenko-Pastur case, see e.g. [8, 5].

In conclusion, we have defined a new class of random correlation matrices with non-positive eigenvalues. We have determined the eigenvalue spectrum, which defines a two-parameter family of distributions that contain the Marčenko-Pastur law in one limit (, arbitrary) and the Wigner semi-circle in another limit (, ). The case provides a null-hypothesis to test the existence of cross-correlations between two time series, complementing the results of [3, 9].

We thank F. Benaych-Georges, M. Nowak and D. Savin for useful comments, in particular pointing us to references [6, 7].

References

- [1] V. A. Marčenko and L. A. Pastur. Distribution of eigenvalues for some sets of random matrices. Matematicheskii Sbornik, 114(4):507–536, 1967.

- [2] K. W. Wachter. The limiting empirical measure of multiple discriminant ratios. The Annals of Statistics, 8(5):937–957, 1980.

- [3] J.-P. Bouchaud, L. Laloux, M. A. Miceli, and M. Potters. Large dimension forecasting models and random singular value spectra. The European Physical Journal B, 55(2):201–207, 2007.

- [4] A. M. Tulino and S. Verdù. Random Matrix Theory and Wireless Communications. Now publishers, Hanover, Mass., 2004.

- [5] M. Potters, J. P. Bouchaud. A First Course In Random Matrix Theory, Cambridge University Press, in press, 2020.

- [6] A. Nica, R. Speicher, Commutators of free random variables. Duke Math. J. 92, no. 3, 553–592, 1998.

- [7] A. Deya and I. Nourdin. Convergence of Wigner integrals to the tetilla law. Latin American Journal of Probability and Mathematical Statistics, Instituto Nacional de Matematica Pura e Aplicada, 9, pp.101-127, 2012.

- [8] J. W. Silverstein and Z. Bai. On the empirical distribution of eigenvalues of a class of large dimensional random matrices. Journal of Multivariate Analysis, 54(2):175–192, 1995.

- [9] F. Benaych-Georges, J. P. Bouchaud and M. Potters. Optimal cleaning for singular values of cross-covariance matrices. preprint, arXiv:1901.05543, 2019.