Optimal market making under partial information

and numerical methods for impulse control games

with applications

by

Diego Zabaljauregui

Department of Statistics

London School of Economics and Political Science

A thesis

submitted for the degree of

Doctor of Philosophy

London, United Kingdom, 2019

© Diego Zabaljauregui 2019

Declaration

I certify that the thesis I have presented for examination for the PhD degree of the London School of Economics and Political Science is solely my own work other than where I have clearly indicated that it is the work of others (in which case the extent of any work carried out jointly by me and any other person is clearly identified in it). The copyright of this thesis rests with the author. Quotation from it is permitted, provided that full acknowledgement is made. This thesis may not be reproduced without my prior written consent. I warrant that this authorization does not, to the best of my belief, infringe the rights of any third party. I declare that my thesis consists of less than 100,000 words.

I confirm that Chapter 1 was jointly co-authored with my supervisor, Professor Luciano Campi, and I contributed 70% of this work.

I confirm that Chapter 2 was jointly co-authored with Professors René Aïd, Francisco Bernal, Mohamed Mnif and J.P. Zubelli, and I contributed 40% of this work.

Acknowledgments and dedication

I would like to thank my supervisor, my department, my family and friends; with a special dedication to my wife and parents for their unconditional support.

Abstract

The topics treated in this thesis are inherently two-fold. The first part considers the problem of a market maker who wants to optimally set bid/ask quotes over a finite time horizon, to maximize her expected utility. The intensities of the orders she receives depend not only on the spreads she quotes, but also on unobservable factors modelled by a hidden Markov chain. This stochastic control problem under partial information is solved by means of stochastic filtering, control and piecewise-deterministic Markov processes theory. The value function is characterized as the unique continuous viscosity solution of its dynamic programming equation. Afterwards, the analogous full information problem is solved and results are compared numerically through a concrete example. The optimal full information spreads are shown to be biased when the exact market regime is unknown, as the market maker needs to adjust for additional regime uncertainty in terms of P&L sensitivity and observable order flow volatility.

The second part deals with numerically solving nonzero-sum stochastic differential games with impulse controls. These offer a realistic and far-reaching modelling framework for applications within finance, energy markets and other areas, but the difficulty in solving such problems has hindered their proliferation. Semi-analytical approaches make strong assumptions pertaining very particular cases. To the author’s best knowledge, there are no numerical methods available in the literature. A policy-iteration-type solver is proposed to solve an underlying system of quasi-variational inequalities, and it is validated numerically with reassuring results. In particular, it is observed that the algorithm does not enjoy global convergence and a heuristic methodology is proposed to construct initial guesses.

Eventually, the focus is put on games with a symmetric structure and a substantially improved version of the former algorithm is put forward. A rigorous convergence analysis is undertaken with natural assumptions on the players strategies, which admit graph-theoretic interpretations in the context of weakly chained diagonally dominant matrices. A provably convergent single-player impulse control solver is also provided. The main algorithm is used to compute with high precision equilibrium payoffs and Nash equilibria of otherwise too challenging problems, and even some for which results go beyond the scope of the currently available theory.

Introduction

This thesis is divided in two main parts. The first one (Chapter 1) deals with the well-known and very relevant problem of optimal market making under a novel and realistic framework of partial information. The second one (Chapters 2 and 3), focuses on the development of numerical methods for a very general class of far-reaching models known as nonzero-sum stochastic differential games with impulse controls. From a mathematical viewpoint, stochastic control (in a broad sense) is the unifying underlying topic, spanning from classical ‘continuous’ controls, to impulse controls and impulse games; and covering the different levels of the problems: from the applications and motivation to the most technical aspects, from the theoretical analysis to the numerical methods and their implementation.

However, the problems, models and techniques used vary so widely, that a unique and comprehensive introduction is not only difficult, but likely counterproductive. For this reason, each chapter starts with a detailed introduction of its own. This section is therefore intended only to briefly motivate the problems to be studied, comment on the techniques used, and list the main resulting scientific contributions.

The optimal market making problem (Chapter 1) consists on determining how a liquidity provider for a given asset should (continuously) choose to set her bid/ask quotes if she wishes to maximize her expected utility. In doing so, she faces a complicated problem with both dynamic and static components, and several risks ranging from adverse price movements, exposure, execution costs and more. An increasingly popular approach, both academically and in practice, is the stochastic optimal control framework proposed by Avellaneda and Stoikov [AS08], where the liquidity taken from the market maker decays as a function of the spreads she quotes. Different variants of the first model have been proposed and thoroughly studied since, both for market making and optimal liquidation [AS08, BL14, CDJ17, CJ15, CJR14, FL12, FL13, Gué17, GL15, GLFT13].

Motivated by empirical evidence [CJ13], we consider a hidden Markov-chain model that unifies and generalizes features of all the previously mentioned ones, and admits the possibility that liquidity may also vary due to unobservable market conditions. We solve this combined control and partial information problem in full, using stochastic control, stochastic filtering and piecewise-deterministic Markov processes (PDMPs) theory [DF99]. The analogous and idealized problem in which the market maker can observe the market state is also solved, and results are compared numerically through a concrete example. Our main contributions are:

-

•

A general and realistic Avellaneda–Stoikov-type model for optimal market making, incorporating for the first time the liquidity dependence on hidden market conditions and allowing for very general intensity (liquidity) shapes.

-

•

A novel approach, within this framework, to characterize the value function of the market maker. The complexity of the dynamic programming equation in our model prevents us from using the most standard technique: proposing an ansatz and proving it valid by a verification theorem. Instead, we explicitly find the ansatz decomposition in terms of the value function of a new, diffusion-free, problem. This result is interesting in itself, as it opens the door to probabilistic and PDMPs numerical techniques when the dimension of the problem renders partial differential equations (PDEs) methods prohibitive.

-

•

Ultimately, we characterize the ‘reduced’ value function as the unique continuous viscosity solution [FS06] of its formally derived equation.

-

•

Having solved the idealized full information problem with a general verification theorem, we show that the corresponding optimal strategies become suboptimal when the market regime is unknown, as the market maker needs to manage a higher regime risk. We interpret the adjustment needed in terms of observable order flow volatility and sensitivity of the expected profit to observable regime changes. Ultimately we see and interpret why the bias of the full information optimal strategies becomes higher, the longer the waiting time in between orders.

Chapters 2 and 3 consider very general models known as nonzero-sum stochastic impulse control games [ABC+19, BCG19], in which players interact by shifting a certain continuous-time stochastic process at discrete (usually random) points in time. Such models have motivation and wide applicability within finance, energy markets, insurance and many other fields. Unfortunately, they are utterly challenging, what has rendered their study far too underdeveloped. In light of the evident need for numerical methods, and the nonexistence of any such one, Chapter 2:

-

•

puts forward the very first iterative algorithm to solve nonzero-sum stochastic impulse games. The method is of policy-iteration-type [AF16, BMZ09] and solves an underlying system of differential quasi-variational inequalities, involving highly nonlinear, nonlocal and noncontractive operators, as well as non-smooth solutions.

The proposed algorithm is admittedly heuristic and no convergence analysis is carried out in this chapter. Instead, it is validated numerically over a series of experiments, considering different games over both fixed and refining grids, performing simulations and comparing results with the only (almost) fully analytically tractable game in the literature [ABC+19]. The results suggest that the algorithm can effectively be used to gain insight into general nonzero-sum stochastic impulse games.

In Chapter 3, we specialize our study by putting the focus on symmetric games. This subclass is broad enough to include plenty of interesting applications, such as competition between central banks [ABC+19, AF16, CZ99, JP93, MØ98], cash management problems [BCG19] and the generalization of many impulse control problems to the two-player instance.

For this type of games, an iterative algorithm which substantially improves the one in Chapter 2 is presented and rigorously studied, using techniques from policy iteration for impulse control [AF16], fixed-point policy-iteration [HFL12] and graph-theoretic notions relating to weakly chained diagonally dominant (WCDD) matrices and their recently introduced matrix sequence counterpart [Azi19a]. The main contributions of this chapter are:

-

•

An iterative algorithm for the effective solution of symmetric nonzero stochastic impulse games, which improves the general one in terms of simplicity, efficiency, precision and stability.

-

•

Providing the missing convergence analysis, which is performed under very natural assumptions on the players strategies and interpreted in terms of WCDD matrices and their extension in [Azi19a]. The latter is applied to impulse control for the first time, to the author’s best knowledge.

-

•

Proof of properties of contractiveness, boundedness of iterates and convergence to solutions, as well as sufficient conditions for convergence.

-

•

As a by-product, a novel impulse control solver is also provided, and its convergence is proved.

-

•

An extensive numerical validation is carried out, considering different performance metrics and addressing practical matters of implementation.

-

•

Ultimately, equilibrium payoffs and Nash equilibria are computed with high precision, for games seemingly too challenging for the available analytical approaches, and even some for which results go beyond the scope of the currently available theory (including discontinuous impulses and very irregular discontinuous payoffs). The latter also motivate further research into this field, with an emphasis on the need for a viscosity solutions framework.

Chapter 1 Optimal market making under partial information with general intensities

Introduction

Given a financial market, a market maker (MM) can be understood as someone who provides liquidity for a certain asset. That is, she (almost) continuously posts bid/ask quotes for the asset, in the hope to profit from the bid-ask spread. In choosing how to do so, the MM faces a complicated problem on several levels; namely: the instantaneous margin/volume trade-off (the further away she quotes from the ‘fair price’, the less she gets executed, and vice-versa), adverse price movements and inventory risk (exposure), execution costs, and many others.

An increasingly popular mathematical approach to the MM problem, both in academia and in practice, is by means of stochastic optimal control. In particular, a line of research has focused on the modelling framework proposed by Avellaneda and Stoikov [AS08] (rooted in turn in [HS81]). Although widely motivated in the literature by order-driven markets such as equity markets, the shape of the limit order book is not explicitly taken into account. Thus, the framework is more easily understood and applied to over-the-counter (OTC) quote-driven markets such as the foreign exchange (FX) market, and we therefore choose to present it in this setting.

In this framework, the MM gives firm bid-ask quotes during a finite time interval by choosing bid/ask spreads with respect to a certain reference price.111Also referred to by some authors as micro-price [CJP15] or efficient price [DRR13] in the martingale case. Depending on the market, this price could be for example an aggregated mid-price or a dealer-to-dealer price, and it is frequently assumed to behave as an arithmetic Brownian motion. To explicitly model the margin/volume trade-off, the probability that the MM gets executed decays as a function of the corresponding spread. More precisely, it is assumed that the MM receives market orders according to counting processes of stochastic intensity. Most typically in the mathematical literature, intensities are assumed to decay exponentially on the spreads (mainly for tractability reasons). The goal of the MM is to find a strategy that allows her to maximize her expected terminal utility, which is taken as a constant absolute risk aversion (CARA) utility. The problem is then translated into a deterministic one: solving the associated Hamilton–Jacobi–Bellman (HJB) equation, which is a partial-integro differential equation (PIDE) for the MM’s value function, and ultimately retrieving the optimal strategy in feedback form.

Within the described framework, a lot variants have been put forward and extensively studied. In [BL14, GLFT12], Bayraktar and Ludkovski, and Guéant, Lehalle and Fernandez-Tapia, apply a one-trading-side version to optimal liquidation in the risk-neutral and risk averse contexts, respectively. The introduction of a constraint on the inventory in [GLFT13], allowed the authors to rigorously solve the original problem of [AS08] with exponential intensities, by means of a verification theorem. This constraint has been widely used moving forward, with the exception of [FL12, FL13], where strategies are derived without a verification theorem.

Guéant and Lehalle continued to actively contribute to the area. In [GL15], they revisit the risk averse optimal liquidation problem for general intensities satisfying a certain ordinary differential inequality, and in [Gué17] the same is done for market making.222The latter paper also considers the multi-asset case. This assumption had been firstly introduced in [BL14, Sect.5.3] under risk-neutrality.

Other prolific contributors in the field are Cartea, Jaimungal and their coauthors [CJ15, CJP15, CJR14], who introduced a quadratic running penalty on the inventory to manage the ‘accumulated’ inventory risk for an otherwise risk-neutral MM. Constraints on the MM’s spreads have also been considered in some of them. It is worth noting that [Gué17] shows how the two seemingly different subclasses of models (risk averse and ‘risk-neutral’ with running penalty) can ultimately be characterized by a unique system of ordinary differential equations (ODEs) when considering two appropriate ansatz.

A relevant issue in practice that has not been included in the previous models is the following one. Empirical evidence (see, e.g., [CJ13]) suggests that liquidity taken by clients depends not only on the quoted spreads but also on other unobservable factors. Indeed, the confluence of factors such as market sentiment towards the asset and the competition with other market makers also affects the intensities at which the MM receives orders. This complicated effect can be modelled in a simplified fashion by making the intensities depend as well on a hidden finite-state Markov chain, effectively reflecting the regime or state of the market (different levels from very slow to very active). To the best of our knowledge, this has only been briefly done in the Avellaneda–Stoikov framework by proposing an approximation for the optimal strategy with exponential intensities [CJ13, Sect.5.1] or studying a simple two-states version with power-law intensities [BL14, Sect.5.4]. Both of these papers deal only with the ‘risk-neutral’ (possibly penalized) case and make the unrealistic assumption that the current market regime is known by the MM.333[BL09, Sect.3.3] (arXiv version) also studies optimal trade execution under partial information, albeit with uncontrolled intensity.

When the state of the market is unknown, the problem becomes significantly more challenging for several reasons:

-

•

It becomes a combined problem of stochastic control and filtering. The MM needs to dynamically make her best possible prediction of the market regime (or more precisely, its distribution), based on the information she has (i.e., the orders she has received so far and the evolution of the reference price), and adjust her spreads accordingly. This prediction is known as a filter.

-

•

The associated HJB PIDE has higher dimension and more non-linearities.

-

•

The standard approach used in all of the previously cited papers relies on reducing the HJB PIDE to a system of ODEs by means of an ansatz, proving that such a system has a classical (smooth) solution, and recovering the value function via a verification theorem. Under partial information however, the reduced HJB equation is still a complicated PIDE such that, in general, a classical solution may not exist (or it may be too difficult to prove otherwise). Hence, the ansatz argument breaks down.

-

•

As a consequence, one needs to resort to the concept of viscosity solutions [FS06]. In addition, the numerical resolution unfailingly becomes a lot more involved than for simple systems of ODEs.

-

•

On a technical level, the construction of the model is not straightforward. The MM needs to adjust her strategy based on her observable information, such as the arriving orders, but this flow of information is in turn affected by the MM’s actions.

In this chapter (based on [CZ19]), we solve the problem of the MM under partial information. First, we start by unifying in one single formulation all the modelling features described so far. This allows us to simultaneously tackle all the models at once with a single approach, while generalising them at the same time. Indeed, our formulation allows for the interaction of any CARA utility (whether risk-neutral or risk averse) with running inventory penalty, terminal execution cost, inventory constraints and spread constraints. Further, motivated by practitioners’ needs, we strongly generalize the intensity shapes to any continuous, decreasing to zero functions, adding modelling flexibility.444This is done at the expense of renouncing to uniqueness in the optimal strategy. We also assume the decay to be ‘fast enough’ in certain cases. We even allow for the inventory to be unconstrained when no penalties are present. (This scenario is considered mainly for the sake of completeness and comparison, at almost no extra cost.)

Secondly, we let the intensities depend on a -dimensional hidden Markov chain. Following [CEFS16a], we use a weak formulation555That is, with controlled probability measures. to construct a well-defined model (with exogenous information) and solve the filtering problem by means of the reference probability approach of stochastic filtering [Bré81, Chpt.VI]. The rigorous setting of the model and its full characterization are carried out in Section 1.1, while the filtering problem is solved in Section 1.2.

The optimization problem of the MM is then reformulated in terms of the usual state variables together with the -dimensional observable distribution of the Markov chain (Section 1.3). At this point, the problem is too involved both analytically and numerically. We proceed by showing that, formally, there is an ansatz for the value function that reduces the dimensionality of the problem (i.e., the standard approach). However, as this methodology is not valid any more, we rigorously prove that the ansatz decomposition holds true (Theorem 1.3.1.1), and that the reduced value function can be characterized as the unique continuous viscosity solution of its formally derived equation (Theorem 1.3.1.3). The latter is done by harnessing results of piecewise-deterministic Markov process (PDMPs) [CEFS16a, DF99], as first defined in [Dav84].

Thirdly, we solve the idealized problem of a MM with full information, who can observe the Markov chain (Section 1.4). We show that a similar ansatz and the standard approach work out in this case. We prove that the MM’s value function is a classical solution of its HJB equation via a general verification theorem (Theorem 1.4.4.1) and we recover the well known strategies for one regime as particular cases.

Finally, we compare the optimal strategies under full and partial information through a concrete example, by numerical analysis (Section 1.5). In particular, we show that the optimal full information spreads are biased when the exact regime is unknown, and using them becomes suboptimal. We interpret the adjustment needed in terms of observable order flow volatility and sensitivity of the expected profit to observable regime changes; and we show how this effect becomes higher, the longer the waiting time in between orders (leading to higher uncertainty for the MM).

1.1 Setting and main assumptions

1.1.1 Preliminaries on the probability spaces

We start by setting up our framework in an abstract fashion, deferring the question of existence of a model to Proposition 1.1.4.1, and a characterization of all such models to Proposition 1.1.4.2. As mentioned in the Introduction, we seek to construct a model under a weak formulation, so that the information flow remains exogenous (i.e., unaffected by the MM’s actions).

Let be a given finite horizon and a right-continuous filtered measurable space with . Suppose it supports three adapted stochastic processes . (More assumptions to be added in the sequel.) Let be the natural filtration of these processes enlarged (‘completed’) by and define the set of admissible spreads as

| (1.1.1.1) |

where are fixed constants and denotes the closure of the interval in , for any . Note that for and , the admissible spreads are not uniformly bounded. The self-imposed constraints for the MM’s spreads can be taken to be different for the bid and the ask if wanted, without any additional effort.

Consider on the former space a family , , of equivalent probability measures such that the sigma algebra generated by their null sets is . Note that for each , is under the usual conditions and is the completed trivial sigma algebra. We refer to as the physical or historical probability given the admissible strategy (or control) , and we write for the expectation under . We will drop the ‘’ from the notation when there is no room for ambiguity.

Henceforth, all the processes (resp. properties) considered are supposed to be defined (resp. hold) on the space for all , unless otherwise stated. For example, a ‘Brownian motion’ is a process on that is an -Brownian motion for all . All subfiltrations are understood to have been augmented to satisfy the usual conditions (which in the case of the natural filtrations of Feller processes, it amounts simply to completing them). Càdlàg versions of the processes are used whenever available.

1.1.2 Description of the model

A market maker in a quote-driven market gives binding bid/ask quotes resp. for a certain financial asset, during the time interval . She receives unitary size market orders666Any constant size would work in the same way, but this convention simplifies the notation. See, e.g., [Gué17] for some formulas with arbitrary constant size under full information. to buy/sell according to counting processes starting at 0, with a.s. no common jumps and stochastic intensities resp. (see [Bré81, p.27, Def. D7]). Each intensity at time depends on the corresponding spread between the MM’s quotes and a reference price . may be interpreted, e.g., as an aggregated mid-price or a dealer-to-dealer price, depending on the market. We assume is a Brownian motion with drift, of the form

| (1.1.2.1) |

where is a Wiener process, and . Note that the MM can fully specify her quote by choosing the spread , since . We assume . In particular, the MM chooses her spreads based on the observation of . We refer to as the observable filtration.

In addition, the intensities also depend on a hidden Markov chain with state space , initial distribution and deterministic generator matrix . We assume is a continuous, stable and conservative -matrix, i.e.:

Assumptions 1.1.2.1 (Generator matrix).

For all and :

The previous are standing assumptions in the literature of Markov chains and they guarantee in particular the existence of a unique (up to evanescence) càdlàg version of , and the existence of the predictable intensity kernel for its jump measure, as given in (1.1.3.1) below. In addition, we suppose that

| (1.1.2.2) |

In this model, represents the market regime at time and results from the interaction of a range of different factors, such as market sentiment towards the asset and varying levels of competition with other liquidity providers. These effects are almost never explicitly modelled in the mathematical literature of market making. To this end, it is natural to assume that is not directly observable by the MM who can only see and . (As often assumed in filtering and control with hidden Markov chain models, the parameters of are known to the MM, who needs to model/estimate them in practice.)

We define the MM’s inventory process

| (1.1.2.3) |

and the cash account process

| (1.1.2.4) |

for some fixed initial values and . Note that

since have a.s. no common jumps.

We shall make some very natural modelling assumptions on the intensities. These strongly generalize those in [BL14, Gué17, GL15] to a context with several market regimes, without the need of any conditions on the derivatives or even smoothness.

Assumptions 1.1.2.2 (Orders intensities).

There exist functions for and with , such that:

-

(i)

if .

-

(ii)

is continuous, decreasing (not necessarily strictly) and if , for all .

Notation.

For the sake of readability, we will often write instead of .

is a self-imposed constraint on the MM’s inventory (whichever its sign) as originally proposed in [GLFT13]. When we are in the unconstrained context, while a finite effectively means that the MM will not buy (resp. sell) whenever (resp. ). In practice, the MM could achieve this either by abstaining from quoting or by quoting with an excessively large spread that prevents any transaction (i.e., a ‘stub’ or ‘placeholder quote’).777For simplicity and without loss of generality, only the first alternative is formalized in our model (as done in [Gué17, GL15, GLFT13]) and this is reflected in the admissible spreads being real-valued. We could also allow for different constraints depending on the sign of the inventory, but we refrain from this to simplify the notation.

Remark 1.1.2.3.

The last assumption states in particular that the intensities should decrease to zero when the spreads grow arbitrarily large. Furthermore, when we require that they decay faster than . Loosely speaking, this states that for any the ‘expected’ utility of the MM’s instantaneous margin, , should vanish for ‘stub quotes’. This is a reasonable assumption in practice, as the opposite could lead to unrealistic optimal strategies such as continuously quoting ‘infinite spreads’.

Remark.

Note that the above intensities are predictable, and since any admissible spreads are bounded, are in turn bounded. Accordingly, and are non-explosive (see, e.g., [Bré81, p.27 T8]). Furthermore, for any constant such that , it is easy to see that for all and ,

| (1.1.2.5) |

where and is the moment generating function of a random variable .888By possibly enlarging the space, one can consider a counting process with no common jumps with and stochastic intensity . Then the process is a Poisson with intensity that dominates . The claim follows immediately.

The following are some examples which we shall come to back in Section 1.4.5, when revisiting the standard assumptions in the literature. We remark that exponential, power-law and logistic intensities are the explicit ones most commonly used in the mathematical literature, for tractability reasons.

Examples 1.1.2.4.

-

1.

, with .

-

2.

, with .

-

3.

, with .

-

4.

, with .

To fix ideas, consider Example 1 and let us observe that if represents decreasing levels of competition for the MM, the values of (resp. ) should increase (resp. decrease) as increases. The same is true if represents increasing levels of positive sentiment (or ‘bullishness’) towards the asset. In practice, will result from the combination of these effects and many more.

Suppose the MM can hedge any remaining inventory at time at the reference price minus a certain execution cost and that she has a terminal CARA utility function

when and . The parameter is known as absolute risk aversion.

Neglecting discounting between and , we consider the optimization problem faced by the MM who tries to maximize the expected utility of her terminal penalized profit and loss (P&L),

| (1.1.2.6) |

where:

-

(i)

. When we are including in the model a running penalty, as firstly done in [CJ15], for the MM to further control her accumulated inventory risk. This is the same as subtracting the variance of the mark-to-market value of the inventory, weighted by .

-

(ii)

represents the final execution cost and is increasing on , decreasing on and . (And usually convex in practice.)

-

(iii)

If , we set .

The last restriction on the parameters states that the only case we will consider in which the inventory could be arbitrary large (whichever its sign) is that of a completely risk-neutral MM with negligible costs. The risk averse case is far more challenging and has not been treated in full mathematical detail even in the complete information case (see discussion in [GLFT13]). The model given by (iii) is of secondary interest in practice, yet, it will allow us to further understand the general problem and methodology and to have a more holistic view at almost no extra cost.

Remark.

Previous works in optimal market making do not consider both penalty and CARA utility (with ) in unison, and instead treat the two families of models separately [Gué17]. Besides the obvious interest in unifying the approach and generalizing existing models, allowing for and simultaneously adds flexibility to the risk managing capabilities of the MM. Indeed, in [Gué17] the author derives some HJB-type systems of ODEs for each problem with a unique risk aversion parameter , and then relates them by the introduction of an auxiliary parameter . The later is afterwards interpreted as measuring risk aversion to non-execution risk only and it is carried forward to the formulae of the ‘optimal strategies’. However, such strategies are not shown to result from any particular optimization problem for . By looking at the equations of the full information version of our model (Section 1.4) with a single market regime, one can immediately see that the equations in [Gué17] are obtained via the reparametrization and . Thus, the formulation in (1.1.2.6) allows us, in particular, to establish the optimality of the strategies in [Gué17] for any value of the non-execution risk aversion and, in general, to differentiate between aversion to different types of risks. We can say that, in our model, represents aversion to all types of risks, while the penalty is used to further increase the aversion to price risk only.

1.1.3 Jump measures

It will be useful in the sequel to understand which are the jump measures and intensity kernels involved in our model. Let (or simply ) be the jump (or counting) measure of (see def. in [Bré81, p.234] or [JS02, p.69]). We use a similar notation for the jump measures of and the pair . These are all finite random measures since the processes are non-explosive for any (see (1.1.2.5)), and they admit predictable intensity kernels (see [Bré81, p.235 D2]). If is the Dirac measure at a point , then the -predictable intensity kernels of and are respectively given by:

| (1.1.3.1) |

and

| (1.1.3.2) |

We denote by , and the corresponding -compensated measures.

1.1.4 Construction and characterization of the model

We now prove the existence of a model within our framework (Proposition 1.1.4.1). We construct it by means of a reference probability (an overview of which can be found, e.g., in [Bré81, Chpt.VI]) and, in particular, the Girsanov theorem for point processes.

For the following proposition, let us consider a filtered probability space under the usual conditions, with and the completed trivial sigma algebra. We refer to as the reference probability. Suppose this space supports a two-dimensional counting process (see def. in [Bré81, Chapt.II]), a Wiener process and a Markov chain with finite state space , initial distribution and time-dependent generator matrix satisfying Assumptions 1.1.2.1, such that verify (1.1.2.2). We set as before and suppose has intensity . ( is given.) Such a simpler model can be constructed for example as a product of canonical spaces, with the existence of the counting processes with the right intensities proved in [JP82, Thm.24 and Cor.31].999The finite-dimensional result has the same proof as in one dimension, starting from independent Poisson measures. Let for be functions under the Assumptions 1.1.2.2 ((ii)),for given and with , and define as in (1.1.1.1).

Proposition 1.1.4.1.

Let and define the process as the stochastic exponential

Then,

-

(i)

is a strictly positive uniformly integrable (UI) martingale. In particular, .

- (ii)

Proof.

are finite variation (FV) processes with no common jumps, hence -a.s. Therefore, the multiplicativity of the stochastic exponential [JS02, p.138] and the exponential formula for FV processes [Bré81, p.337 T4] yield the explicit expression , with

| (1.1.4.1) |

Then (i) follows from the strict positivity and boundedness of for , as in [Bré81, p.168 T4] with terminal time . The only difference is that in our case the -intensity of is instead of . The proof remains the same though, simply recalling that the -moment generating function of is dominated by the one of a standard Poisson random variable (see (1.1.2.5)). Uniform integrability is immediate.

(i) guarantees that , as defined in (ii), is an equivalent probability measure. The shape of the -intensities of is due to [Bré81, p.166 T3].

The fact that is still a Wiener process under is a consequence of the Girsanov–Meyer Theorem [Pro04, p.132 Thm.35] and Levy’s characterization Theorem.

As for , note first that its initial distribution does not change as , and the same goes for its infinitesimal generator operator. To see this, consider the -generator operator , . We know the process is a -local martingale. Once again, by the Girsanov–Meyer Theorem., is also a -local martingale ( since are FV processes satisfying (1.1.2.2)). Moreover, being bounded, is a true -martingale and solves, for , a well-posed martingale problem for . This implies is a -Markov chain with a uniquely determined law [EK09, p.184 Thm.4.2].101010Although our martingale problem is non-homogeneous in time, is deterministic, so this does not represent a problem. That is also the -generator matrix follows from uniqueness.

(1.1.2.2) clearly remains unchanged under an equivalent change of probability measure.

∎

Reciprocally, suppose we start with a family of filtered probability spaces as in Section 1.1.1, supporting a counting process and a Markov chain satisfying condition (1.1.2.2), together with a Wiener process . Suppose also that has finite state space , initial distribution and time-dependent generator matrix , and that our Assumptions 1.1.2.1 and 1.1.2.2 are in place. We put as always. We would like to characterize any such model in terms of a reference probability as in Proposition 1.1.4.1 by an inverse change of measure. However, we only claim the uniqueness of the reference probability on . We will come back to this result in the sequel.

Proposition 1.1.4.2.

Let and define

Then,

-

(i)

is a strictly positive UI martingale. In particular, .

-

(ii)

defined by is a probability measure equivalent to such that, for , is a counting process with intensity , is a Wiener process and is a Markov chain with state space , initial distribution and generator matrix . Furthermore, are independent.

-

(iii)

If we define as in Lemma 1.1.4.1 under , then (i.e., the two changes of measure are inverse of each other).

-

(iv)

For all , on .

Proof.

(i) and (ii) are proved just as in Proposition 1.1.4.1 (the processes are strictly positive and bounded for , and the intensities are bounded). The -independence of is a consequence of [JYC09, p.543 Lem.9.5.4.1]. That is, the -martingales have the predictable representation property with respect to resp. (see [Bré81, p.239 T8] for compensated counting measures) and they are -orthogonal, which implies their independence.

The explicit expressions for the stochastic exponentials (see (1.1.4.1)) show straightforwardly that , proving (iii).

(iv) is due to [Bré81, p.64 T8]. ∎

1.2 Filtering problem

Since the MM cannot directly observe all the information in but only (in particular, she cannot observe ), in order to solve the optimization problem (1.1.2.6) under partial information we want to reduce it first to an equivalent one under full information. Throughout this section we work under with fixed. We sometimes omit from the notation for simplicity.

Recall that for any càdlàg bounded process (not necessarily adapted) on a filtered probability space satisfying the usual conditions, the optional projection of on is the unique càdlàg process such that a.s. for each . Its existence is guaranteed by the Optional Projection Theorem (see, e.g., [JYC09, p.264] or [Nik06, p.357-358]). (We omit and/or when clear from the context.) Let us consider the optional projections

In other words, is the unique càdlàg version of the conditional distribution of given the observable information, i.e., . We now characterize the observable (that is, the -) predictable intensities of in terms of . Loosely speaking, the observable intensity of, say , is obtained projecting: [Bré81, p.32 Comment and Pseudo-Proof of T14]. The only technical difficulty is that of finding a predictable version of such process. has the desired projective property but it is not predictable in general. , on the other hand, is predictable but does not normally enjoy the projective property. In fact, the process we are looking for is ‘in between’ these two.

Proposition 1.2.1.1 (Observable intensities).

The -predictable intensities of and , resp., are

Notation.

We set ; thus, .

Proof.

We prove it just for , the others being analogous, and we omit for simplicity. It is clear that is predictable. We need to check that for any -predictable process ,

For any , each path of the càdlàg processes and has only countably many jumps. We can therefore interchange these processes and their left limits when integrating with respect to . By properties of the conditional expectation and Fubini’s Theorem,

∎

We give now the filtering (or Kushner-Stratonovich) equations for the observable distribution of . These are coupled stochastic differential equations (SDEs) governing the dynamics of .

Notation.

We denote by the -simplex (i.e., and by its interior relative to the hyperplane (i.e., ).

Proposition 1.2.1.2 (Observable distribution of ).

The process is the unique strong solution of the constrained system of SDEs

| (1.2.1.1) |

such that and for all a.s. Equivalently,

| (1.2.1.2) |

with and for all a.s.

Proof.

The equivalence between the constrained systems of SDEs (1.2.1.1) and (1.2.1.2) results from rearranging the terms and using .

Let us check that solves (1.2.1.2). Clearly, the constraint and the initial condition are satisfied. The verification of the SDEs is due to [CEFS16a, Prop.3.3] (with more details in [CEFS16b, App.A, Lemma A.2 and Prop.3.3]), albeit some considerations need to be made.

On the one hand, the authors work with a pure jump model, with strategies adapted to the natural filtration of the driving jump process only (i.e., there is no diffusion) and constant generator matrix for the Markov chain. However, mutatis mutandis the former differences yield no major change in the proofs.

On the other hand, the main assumption of the authors, [CEFS16a, Asm.2.1], postulates the existence of some deterministic measure on with compact support111111In [CEFS16a] the support is assumed to be a subset of , but this is only for a ‘return (or yield) process’ as in their case. such that for all , the measure is equivalent to and the Radon-Nikodym derivative is uniformly bounded and bounded away from zero -a.s.

Since the spread processes are fixed and bounded, we can assume without loss of generality that is finite. Setting we see straightforwardly that the two measures are equivalent with derivative

| (1.2.1.3) |

uniformly bounded by . However, our model allows for , which is a consequence of having vanishing intensities . This poses no issue nonetheless, as is only used in [CEFS16a, Prop.3.3] to guarantee (see Proposition 1.1.4.2). This condition, also satisfied in our model,121212This was ultimately a consequence of the decomposition in Assumptions 1.1.2.2 ((i)), that allowed for the vanishing factors of the intensities to be secluded as the reference probability intensities. allows to go from the physical probability to a reference probability and backwards.

We turn now to the proof of uniqueness. We remark first that the jump height coefficients in (1.2.1.2) will typically not be Lipschitz (classical results for SDEs such as [Pro04, p.253 Thm.7] cannot be applied) and the paths of the spreads need not be continuous between the jump times of (ruling out the most classical results of ODEs [CL55]). Nevertheless, we can still follow a pathwise ODEs approach. Let us fix a path and alternatively verify uniqueness inductively on the intervals , where and are the jump times of (including the terminal time even if there is no jump at that point). Then is bounded for all . Now observe that any càdlàg process , solving the constrained system of SDEs (1.2.1.2), must solve pathwise for the following system of ODEs in integral form, for :

| (1.2.1.4) |

with if , and . Elementary algebra of bounded Lipschitz functions shows that , defined by is Lipschitz in (uniformly in ). Let be the maximum Lipschitz constant of for and suppose (clearly satisfied for ). Then (1.2.1.4) yields , implying on by Grönwall’s inequality. As a consequence, the equality on follows by induction. It must clearly hold at time as well, either by continuity or (if there is a jump) because . ∎

Remark 1.2.1.3.

Consider the identification (resp. ) obtained by the substitution (where the choice of the -th coordinate over the rest is completely arbitrary). Then the constrained system of SDEs (1.2.1.1) (or equivalently, (1.2.1.2)) for becomes an ‘unconstrained’ system for . Henceforth, we shall use this identification whenever convenient.

We finish this section with a short lemma. It states that the conditional distribution can never reach the relative border of the simplex , provided it starts from the relative interior. This amounts to saying that all regimes have some positive probability at time zero.

Lemma 1.2.1.4.

If , then for all a.s.

Proof.

We want to show that for all a.s. We proceed by induction on the jump times of , for each path, as at the end of the proof of Proposition 1.2.1.2. Using the same notations, let and suppose for all (satisfied for by assumption). Then (1.2.1.4), Assumptions 1.1.2.1 and the fact that by definition, show that is absolutely continuous on the interval and satisfies

| (1.2.1.5) |

for -a.e. , subject to . Let us set . We need to prove that . By the continuity of , it must be . Consequently, (1.2.1.5) and the absolute continuity of on yield

If it were , the continuity of again and the former inequality would imply , proving by contradiction that and is positive on the whole interval . Positivity on now follows by induction, and it must clearly hold at time as well, as either there is a jump or we can reason as we just did. ∎

In light of the previous lemma, we will assume from here onwards that

| (1.2.1.6) |

and therefore work with instead of .

1.3 Value function and HJB equation

In this section, we tackle the control problem of the MM with the filter as an additional state variable. We define the MM’s value function and we aim to characterize it by means of an HJB equation.

Let . We consider our model ‘starting at ’ instead of . Whenever a process is defined from time ‘ onwards’ (i.e., from time onwards and decreeing its left-limit value at ) this implicitly means it is constant on . In particular, we use this convention for all integrals (stochastic or not) of the form and (with a slight abuse of notation) for the processes and . We work with instead of due to the jumps of the processes . However, since are quasi-left continuous,131313For example, because they are increasing càdlàg processes admitting continuous compensators for (any one of) the physical probabilities [JS02, p.70 Prop.1.19 or p.77 Prop.2.9]. for most intended purposes one can drop the left limit with no harm. We define and analogously.

Let and . The set of admissible spreads starting at is the set of which are independent of (equivalently, the which are -predictable). Consider for each the processes defined pathwise, outside some set , by (1.1.2.1), (1.1.2.4), (1.1.2.3), (1.2.1.1) resp., replacing the initial conditions at time by resp. at time . We remark that (since ) and all the processes defined in this section are adapted to this filtration. We further assume there exists a family of ‘physical’ probabilities such that their null sets generate , and for it holds that is a Wiener process and has predictable intensity , as defined in Proposition 1.2.1.1 in terms of and .

We define the penalized P&L from to (see (1.1.2.6) for parameter restrictions) as

| (1.3.1.1) |

and the value function of problem (1.1.2.6) as

| (1.3.1.2) |

Our goal is to compute optimal or ‘close to optimal’ strategies.141414By ‘close to optimal’ we mean that for each there exists a strategy such that the supremum in (1.3.1.2) is attained up to . The Dynamic Programming Principle and Ito’s Lemma allow us to formally derive (see, e.g., [Bou07]) the Hamilton–Jacobi–Bellman (or dynamic programming) partial-integro differential equation associated to :

| (1.3.1.3) |

with terminal condition , where:

and we convene the following:

Notation.

(i) The derivatives with respect to should be understood via the identification of Remark 1.2.1.3. (ii) Although it is not meaningful to evaluate on the inventories , this only happens in equation (1.3.1.3) when the corresponding term vanishes. This slight abuse of notation can be found throughout previous works and we will be using it as well.

Equation (1.3.1.3) can also be seen as a coupled system of PIDEs indexed in . (We will talk about system of equations or simply ‘equation’ indistinctly). Nonlinearity aside, (1.3.1.3) is rather complex, in particular due to being of second order, high-dimensional and with derivatives in almost all of these dimensions. Tackling it directly (either analytically or numerically) is utterly challenging. Consequently, it has become common practice for optimal market making and optimal liquidation models à la Avellaneda–Stoikov [AS08] to propose an ansatz for the solution [AS08, BL14, CDJ17, CJ15, CJR14, FL12, FL13, Gué17, GL15, GLFT13]. This approach however, relies heavily on the existence of a classical solution for the resulting simplified equation, so that the ansatz is ultimately proved valid by a suitable verification theorem. (See Section 1.4 for more details.) When the simplified equation does not admit (or cannot be guaranteed to admit) a classical solution, and a viscosity approach needs to be used instead, the previous argument breaks down.

If we attempted to solve our problem by the standard approach, a plausible ansatz for the value function could be

| (1.3.1.4) |

Formal substitution yields the following equation for :

| (1.3.1.5) |

with terminal condition , where:

The new system of PIDEs is of first order and no longer depends on the variables and (there is no diffusion anymore). This is a considerable simplification; one that will permit effective numerical solution in Section 1.5. But it is not good enough for us to assert existence of a classical solution. Notwithstanding, we are able to rigorously prove the decomposition (1.3.1.4) and explicitly find as a new ‘value function’ (Theorem 1.3.1.1). When the control space is compact, this ultimately allows us to characterize as the unique solution of the terminal condition PIDE (1.3.1.5) in the viscosity sense (Theorem 1.3.1.3), further simplified in the unconstrained inventory case. These two theorems constitute the main theoretical results of this chapter. They allow us to safely postulate reasonable candidates for optimal (or -optimal) strategies for the MM, i.e., those given by spreads that (at least approximately) realize the suprema in (1.3.1.5).

Theorem 1.3.1.1.

There exists a unique function such that the decomposition (1.3.1.4) holds true. Furthermore, there exists a family of equivalent probability measures , , such that

-

(i)

is the unique strong solution of (1.2.1.1) with initial condition under .

-

(ii)

has -predictable intensity kernel

-

(iii)

with

(1.3.1.6)

where and .

Proof.

For shortness, we make an abuse of notation and omit from the probability measures and expectations. Let us start by proving (1.3.1.4) and finding with the desired properties. Using integration by parts we can re-write the penalized P&L (1.3.1.1) as

| (1.3.1.7) |

Consider first the case . The integrals with respect to all have bounded integrands (and predictable for ), except in the case of unconstrained inventory: and (see (1.1.2.6)). Regardless, we still have Choosing the conclusion follows by taking expectation and by Propositions 1.2.1.1 and 1.2.1.2.

Consider now . Hence, we are in the case . We define

By Novikov’s condition, is a strictly positive UI martingale with , and therefore defines an equivalent probability measure via . Note that the Girsanov–Meyer Theorem. [Pro04, p.132 Thm.35] ensures the -intensities of remain the same when changing to . Let us set

where denote the corresponding -compensated (or equivalently, -compensated) processes. By the same arguments of Propositions 1.1.4.1 and 1.1.4.2, is a strictly positive UI martingale with and defines an equivalent probability measure via , such that (ii) holds true. Note that (i) is also trivially verified due to the equivalence of the probability measures.

Suppose for the time being that is defined as in (1.3.1.6) but taking supremum over the whole set of admissible controls instead. We will see afterwards that this makes no difference. To see (1.3.1.4), observe that the identity and (1.3.1.7) yield giving

On the other hand, by the same identity,

As a consequence, (1.3.1.4) is equivalent to the equality . We check instead the stronger statement

| (1.3.1.8) |

Using the explicit exponential formula (see equation (1.1.4.1)) and by straightforward computations:

which yields (1.3.1.8) after taking -expectation.

It remains to see that

Clearly . Let us check . As done in Proposition 1.1.4.2 we can define a family of ‘reference’ equivalent probability measures , , such that for it holds: is a Wiener process independent of the counting process and has predictable intensity (in particular, its law does not depend on ). Furthermore, the inverse change of measure is given by with

Let us fix . Denote by the Skorokhod space of càdlàg functions with its usual sigma algebra and by the laws (or pushforward measures) induced on by resp. when starting from . These laws do not depend on and characterize the joint law of on as , due to the independence of the two processes. Since is -predictable, by a monotone class argument one can show there exists a jointly measurable process such that and for -almost every , the process is in . Note also that we can write for some function . By Fubini’s theorem,

Since was arbitrary, we conclude that . ∎

Just as it occurs under full information (see Section 1.4), for a fully risk-neutral MM with negligible costs (i.e. ), can be further decomposed. Note, from their definition, that in this case and do not depend on . As it was proved in Theorem 1.3.1.1, when the family can be taken as the original physical probabilities, and these do not depend on either. The following corollary is now immediate.

Corollary 1.3.1.2.

If and then

with

In the context of the previous corollary, formal substitution in (1.3.1.3) or (1.3.1.5) yields the following PIDE for :

| (1.3.1.9) |

with terminal condition , where:

We now want to prove that (resp. ) is the unique continuous viscosity solution of the terminal condition PIDE (1.3.1.5) (resp. (1.3.1.9)). (See, e.g., [Son88, Def.2.1] for the relevant definition, or more in general [DF99, Def.7.3], recalling that in our case we have no boundary conditions other than that at terminal time.) A complication inevitably arises, as classical viscosity techniques [Bou07, FS06, ØS09] cannot be applied directly to weak formulation models such as ours. However, the decomposition of Theorem 1.3.1.1 (resp. Corollary 1.3.1.2) not only reduces the dimensionality of the problem, but also states that the MM may neglect the diffusion component of the state process altogether, focusing solely on the time-space state variable (resp. ). This is a PDMP as introduced in [Dav84] (detailed treatments also found in [BR11, Dav93]). Using results from PDMPs theory, our continuous-time problem is identified with a control problem for a discrete-time Markov decision model, as in [BR09, BR10, BR11, CEFS16a], and linked again with viscosity solutions of HJB PIDEs as in [CEFS16a, DF99].

An inevitable drawback is that the PDMPs approach relies on the use of the so-called randomized (or relaxed) controls and requires the control space to be compact. Hence, for the following theorem we will assume . Assuming a uniform lower constraint is hardly a problem. On the contrary, (or even some small positive number) is the most meaningful in practice, as negative spreads imply the MM is willing to offer her clients better prices than the reference price . ( is motivated in the literature by mathematical convenience rather than modelling accuracy.) A uniform upper bound , on the other hand, is harder to assess a priori. Fortunately, in most situations encountered in practice, the unconstrained optimization will yield bounded optimal spreads nonetheless, and the MM can dispense with if she wishes to do so (see Section 1.5 for an example).

Theorem 1.3.1.3.

Proof.

Case and : Let us write , with

Then can be regarded as the value function of an optimization problem in the standard Bolza-Lagrange formulation, i.e.,

where the state variable is a PDMP with bounded state space and initial condition , is the discount factor and are bounded functions. (These functions are bounded thanks to the control space being bounded.) The continuity of can be proved now in the same way as in [CEFS16a, Thm.4.10] albeit in a more straightforward manner. This is due to the boundedness of , the fact that never visits the relative border of the simplex , and that there is no exit time of the state space other than the terminal time. Assumptions [CEFS16a, Asm.4.7] are clearly verified in our model, and [CEFS16a, Asm.2.1] has already been accounted for at the beginning of the proof of Proposition 1.2.1.2.151515An additional detail now is that [CEFS16a, Asm.2.1] is also used in [CEFS16a, Lem.4.1], which states that the drift coefficient in equation (1.2.1.2) is Lipschitz in the state variable, uniform in time and control. This is routinely verified in our case, under our new assumption: . We remark that in our case the bounding function (see [CEFS16a, Lem.4.6]) can be taken simply as , for an large enough to prove contractiveness.

Having proved the continuity, the same proof of [CEFS16a, Thm.5.3] (or [DF99, Thm.7.5]) shows that is the unique continuous viscosity solution of its standard HJB equation. We remark once again that our case is simpler, in that is bounded and we do not have any boundary conditions other than the terminal time condition. In particular, there is no need for additional assumptions on the growth of .

Finally, the result for is obtained via the two increasing diffeomorphic transformations and .

Case and : The only difference with the previous case is that the Bolza-Lagrange representation of the problem is obtained directly, since

with no need for any transformation.

Case and : The same as the latter case but working instead with the state variable and the value function . ∎

1.4 Full information

In this section we consider the idealized case of a MM with full information. We assume the MM has inside information in such a way that she can observe the full filtration , and in particular she can observe . For example, if represents different levels of competition amongst liquidity providers, this would practically mean the MM has information regarding her competitors’ quotes. We will see that in this case the value function turns out to be a regular, classical solution, of its HJB equation. Afterwards, we will compare the results with those obtained in the more realistic setting of partial information.

1.4.1 Dimensionality reduction and the general system of ODEs

We consider problem (1.1.2.6) but under full information, with the set of admissible spreads:

Note that in this section, and when , we do not assume upper-boundedness of the spreads. Let and . Consider the processes as defined in Section 1.3 and a Markov chain with deterministic generator matrix , state space and such that . We assume the physical probabilities are defined for every and that Assumptions 1.1.2.1, 1.1.2.2 and (1.1.2.2) (starting at time ) are still in place. The value function in this case is

| (1.4.1.1) |

By means of the Dynamic Programming Principle and Ito’s Lemma one can formally derive the following HJB PIDE for :

| (1.4.1.2) |

with terminal condition .

In this new context, instead of formally proving a decomposition of as in Theorem 1.3.1.1, it is more straightforward to propose an ansatz and ultimately prove it valid with a verification theorem. (This is the standard approach used in the Avellaneda–Stoikov framework.) Let us consider an ansatz for the value function analogous to those used for the one regime case:

for some function , in time. Substituting in (1.4.1.2) and using Assumptions 1.1.2.1, we see that must satisfy a system of ODEs indexed in :

| (1.4.1.3) |

with terminal condition , where:

-

1.

, for .

-

2.

, for .

The original problem is simplified in this way, both by the dimension of the state variable and by the complexity of the equations, provided we can show that problem (1.4.1.3) admits a solution. With this aim in mind, let us prove first the following property of the Hamiltonian functions .

Lemma 1.4.1.1.

For all , it holds:

-

(i)

For each compact , there exists such that , for all .

-

(ii)

is locally Lipschitz.

Proof.

Fix and let be a compact set. We verify first that (i) is a consequence of Assumptions 1.1.2.2. Let such that for all . If , then we can take any since for all and . On the other hand, if , take some . It holds that and we can choose such that for all and . Replacing supremum by maximum is now immediate due to the continuity of on for all .

(ii) is routinely verified using that the family is equi-Lipschitz on . ∎

We want to prove now that the Cauchy problem (1.4.1.3) admits a unique global classical solution which is in time. To this purpose, we will treat the cases of the finite system () and infinite system () of equations separately.

1.4.2 Constrained inventory ODEs

For we are dealing with a finite system of ODEs. We know that under certain regularity conditions the Cauchy problem (1.4.1.3) is guaranteed to have a classical solution on some neighbourhood of . Nonetheless, it is not always the case that such a local solution can be extended to a global one on . Following [Gué17, GL15], we start by proving a comparison principle for (1.4.1.3) that will allow us, in particular, to show the existence of a global solution. The argument used is standard for comparison principles of HJB-type equations.

Proposition 1.4.2.1 (Comparison Principle).

Let be an interval containing and let be classical ( with respect to time) super- and sub-solutions resp. of (1.4.1.3). That is,

| (1.4.2.1) |

| (1.4.2.2) |

and

| (1.4.2.3) |

Then

Proof.

Suppose first for some and let . Since , there exists such that

| (1.4.2.4) |

If , then we must have

Let us see that the left-hand side is non-positive. By (1.4.2.1) and (1.4.2.2),

increasing (resp. increasing) and (1.4.2.4) imply that the last two terms (resp. the first one) are non-positive. We must have then that , and due to (1.4.2.4) and (1.4.2.3) for all :

Since was arbitrary, we obtain the desired result.

The case is now a consequence of comparing and on intervals of the form with . ∎

We can now prove the existence and uniqueness of a classical global solution of the Cauchy problem (1.4.1.3).

Theorem 1.4.2.2.

There exists a unique , in time, which (classically) solves the Cauchy problem (1.4.1.3).

1.4.3 Unconstrained inventory ODEs

We consider now , for which (1.4.1.3) becomes an infinite system of ODEs. Recall that in this case we assumed , i.e., the MM is fully risk-neutral and has negligible costs. This allows us to further reduce the dimensionality of the state variable by the additional ansatz

| (1.4.3.1) |

for some . Substituting in (1.4.1.3), we get that must solve the finite linear system of ODEs

| (1.4.3.2) |

with . By continuity of and (see Lemma 1.4.1.1), the previous system is known to have a unique global solution which can be computed by the variation of parameters method. Straightforward verification now gives the following:

1.4.4 General Verification Theorem

We give now the complete solution for the general model under full information. For the next theorem we note that given the function defined in Theorem 1.4.2.2 for (resp. Proposition 1.4.3.1 for and ) the difference or ‘jump’ terms of equation (1.4.1.3) are bounded by continuity. That is, is bounded on for (resp. is bounded on ).

Theorem 1.4.4.1 (Verification Theorem).

Notation.

Note that we make a slight abuse of notation, writing for the Borel functions in the theorem and for the spread processes.

Proof.

Let . We check first that we can choose a maximizer of in a measurable way with respect to . Lemma 1.4.1.1 tells us that there exists such that attains its maximum in for all . Due to Assumptions 1.1.2.2 ((ii)), is continuous and, in particular, a Carathéodory function [AB06, Def.4.50]. Thus, the Measurable Maximum Theorem [AB06, Thm.18.19] guarantees the existence of a Borel selector of the , . (Note that the weak measurability assumption is trivially verified in this case.)

From here onwards, let be some Borel selectors as above. By Lemma 1.4.1.1 again, these functions must be bounded from below, and the spread processes defined as in the theorem are clearly admissible.

We define now and we want to show that . Let us fix the initial time and values, , and consider an arbitrary strategy . For shortness, we omit these initial conditions and strategy from the notation of the processes and the expectation. We denote by , the set of jump heights of , and

By the identity , we can rewrite the utility of the MM’s penalized P&L as

| (1.4.4.1) |

Using integration by parts and Ito’s Lemma (recalling (1.1.2.2)), we re-express the last two terms as

and

where is the jump measure of . Substituting in (1.4.4.1),

| (1.4.4.2) |

Next, we want to verify that the process is a zero mean martingale. Since is bounded (either or ) it suffices to check

| (1.4.4.3) |

If ,

If (hence ), let be a lower bound for and . Integration by parts and Hölder inequality yield

and (1.4.4.3) is again consequence of (1.1.2.5) and Novikov’s condition (trivially satisfied).

In the same way, recalling that is bounded, is bounded from below and that is bounded by continuity, one can check that

and

Taking expectation in (1.4.4.2), the Brownian term vanishes and integration with respect to and is replaced by integration with respect to their dual predictable projections (see, e.g., [Bré81, p.27 T8 and p.235 C4]). That is,

as solves (1.4.1.2), with the equality attained for by definition. We conclude that and that the pair is optimal. ∎

Remark.

For , since the MM will not buy (resp. sell) whenever hits (resp. ), the value of (resp. ) at these stopping times is essentially irrelevant. From a strict mathematical perspective, the only constraint is that whichever the value we choose, the process needs to remain admissible.

1.4.5 Computing the optimal spreads: some particular cases

We have shown in Theorem 1.4.4.1 that the optimal spreads for the full information problem (1.4.1.1) can be computed in feedback form in terms of at each time . Practically, this means finding (typically, numerically) that solves the terminal condition system of ODEs (1.4.1.3), and finding the spreads by maximization:

| (1.4.5.1) |

(See the proof of Lemma 1.4.1.1 to see how to reduce the maximization to a compact domain in the cases of or .) The functions in (1.4.5.1) may admit multiple maximizers in general. In [BL14, Gué17, GL15] stronger assumptions are imposed on the orders intensities which guarantee, in particular, the uniqueness of the maximizers.

We now extend these assumptions to our context and give the corresponding characterization of the spreads. Henceforth, Assumption 1.1.2.2 ((ii)) is replaced by the following:

Assumptions 1.4.5.1.

for some and , for all .161616Lateral derivatives are considered on the domain border. The strict inequality is needed when and spreads are unconstrained.

Remark.

The intensity functions of Examples 1.1.2.4 1, 2 and 3 all verify these stronger assumptions, while Example 4 only does so for . As a matter of fact, by solving the differential inequality in Assumptions 1.4.5.1, one sees that any within this new framework has a strict upper bound of the form of Example 4. In particular, for , is necessarily satisfied.

Under Assumptions 1.4.5.1, the maximization of (1.4.5.1) (for fixed ) can be replaced essentially by solving a contractive fixed point equation and flooring and capping the results at and respectively. To make this precise, even when the intensity functions are not defined beyond , let us set

The following result shows how, up to constraints, the optimal spreads are given by a first term that maximizes the ‘expected’ utility of the MM’s instantaneous margin (see Remark 1.1.2.3), plus an additional risk adjustment taking into account the inventory held and the prospect of the market shifting. Note how the first term depends on , the percentage sensitivity of the liquidity to spread changes.

Proposition 1.4.5.2.

Proof.

For each , define

By Assumptions 1.4.5.1 and straightforward computations (see computations, e.g., in [Gué17, Lemma 3.1]), one verifies that and is strictly increasing on each variable.171717 denotes the sign function, with . It follows that for any and (resp. and ), (resp. ), which proves (1.4.5.2).

In the same way, if and , then and . Hence, the continuity of implies (1.4.5.3) (the uniqueness of the solution being due to the strict monotonicity of ). The cases of unconstrained spreads are proved as in [Gué17].

Lastly, the cases and follow in the same manner; and the new expressions for the Hamiltonians are immediate, putting . ∎

As done in [Gué17, Lemma 3.1], (1.4.5.3) can be replaced by the explicit formula

but the computation of , and still has to be carried out numerically, in general. We state now a few simplifications that arise in some particular cases, i.e., when the intensities are exponential or when , . These are all derived by straightforward substitution. We refer to [Gué17, Sect.4] for some asymptotic approximations when in the one regime case, with unconstrained spreads and .

Corollary 1.4.5.3.

If and , then

| (1.4.5.4) |

and if , then is the unique solution of the fixed point equation

| (1.4.5.5) |

If additionally , with for each , then

In other words, if and , then solving (1.4.1.3) is no longer necessary and one only needs to solve the fixed point equations (1.4.5.5). Further, the MM’s spreads do not depend on . This is to be expected, since in this case she is neutral to all types of inventory risks and the terminal execution cost is neglected. However, she does need to re-adjust for changes in the regime as these impact on her probability of getting orders. If additionally, the orders intensities are exponential, then the spreads are computed straightforwardly avoiding the need of any numerical scheme. Note also how this simple model makes evident a second component of the optimal spreads through equation (1.4.5.5): a drift adjustment by which the MM takes into account the overall tendency of the asset’s price.

Now we look at the results obtained for exponential intensities in general, and in particular for . Equation (1.4.5.3) becomes an explicit formula in this case, as the percentage liquidity sensitivities, , are constant.

Corollary 1.4.5.4.

If , with for each , then

1.5 Numerical analysis

In this section we present our numerical results, focusing on the difference in optimal behaviours between the partial and full information frameworks, and the intuition behind the filter. To exemplify our findings in a concrete manner, while keeping the presentation as simple as possible, we will assume throughout this section that:

-

•

The MM has risk aversion parameter .

-

•

There are only two possible states: state 1 represents a ‘bad’ regime with low liquidity taken by clients, and state 2 a ‘good’ regime with high liquidity.

-

•

The transition rate matrix is constant.

-

•

The intensities are symmetric, proportional and exponential, i.e., and .

The latter assumption allows us to perform the optimizations in equation (1.3.1.5) analytically. Practically, proportional intensities mean that while there is more active trading on the good regime, the way in which the clients react to movements in the spreads remains unaffected. As in [CJ15], we will allow for the three type of penalties to manage inventory risk: constraints on the maximum long and short positions, accumulated inventory penalty and a quadratic (possibly negligible) terminal penalty (or cost) for the MM. That is,

-

•

, for some .

Let us write for the conditional probability of being in the bad regime given the observable information. Note that is a scalar in this section, since neglects the need of the additional variable. The PIDE (1.3.1.5) at the point reads:

| (1.5.0.1) |

with terminal condition and partial information optimal spreads given by

| (1.5.0.2) |

-

(i)

is the observable transition rate to the bad regime.

-

(ii)

is the observable intensity increase from the bad regime (as a ratio).

-

(iii)

is the observable variance, of the square root, of the percentage intensity increase from the bad regime; i.e., a measure of observable order flow volatility.

The previous equations are valid for , or more precisely, for such that holds true over the whole domain. Otherwise, one needs to floor and cap the optimal spreads and change the Hamiltonians accordingly, as done in Proposition 1.4.5.2.

A finite differences scheme of simple implementation to solve (1.5.0.1) consists of reversing time and using an explicit upwind Euler scheme over a uniform grid for and . The terms of the form , where will typically fall outside of the grid, can be approximated by linear interpolation as in [DF14]. The limiting equations can be used for and provided that , which we assume henceforth. Such a scheme can be shown to be consistent, stable and monotone under an appropriate CFL condition. In light of equation (1.3.1.5) satisfying a comparison principle (see [CEFS16a, Thm.5.3] and why it holds for our model in the proof of Theorem 1.3.1.3), we know the scheme converges to the unique continuous viscosity solution [BS91], and we can recover the expected penalized P&L of the MM (Theorems 1.3.1.1 and 1.3.1.3). The optimal strategy to be followed by the MM is then given in feedback form by .181818As previously mentioned, these are technically only candidates for optimal (or in general, -optimal) strategies. We do not rigorously prove their optimality character here, but merely note that well known results of discrete time dynamic programming, together with the convergence of the discrete solutions of (1.5.0.1) to the analytical one, suggest that they can be safely used as such.

We will focus our attention on the optimal ask spread, with analogous observations holding for the bid spread. The parameter values in Table 1.1 were used for all the experiments presented in this section. For those present in the classical one regime models, we have chosen values used in previous works (in the case [CJ15]) to make the comparison clearer. In particular, the value of will be taken as either or , to be further specified in each experiment. The time horizon will always be the one displayed on the corresponding axis. Note that we work in a symmetric market, which justifies analyzing one side only.

| Parameter | m | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Value | 0 | 0.1 | 0.1 | 2 | 25 | 3 | 5 | 5 | 10 |

1.5.1 Comparing full and partial information optimal strategies

Under the standing assumptions of this section, the full information equation (1.4.1.3), for a function , becomes:

| (1.5.1.1) |

with terminal condition and full information optimal spreads given by

| (1.5.1.2) |

-

(i)

is the effective transition rate to the bad regime.

-

(ii)

is the effective intensity increase from the bad regime (as a ratio).

The previous equations are valid for , as in the partial information case.

Although similar, equation (1.5.1.1) for the bad regime (resp. good regime ) is not the limiting equation of (1.5.0.1) for (resp. ). Indeed, a MM with full information can expect to make a larger profit. Thus, in general, even in these extreme cases.191919Our numerical findings were indeed consistent with this intuitive statement. However, the corresponding optimal strategies do (at least approximately) agree, as Figures 1.1 and 1.2 show.

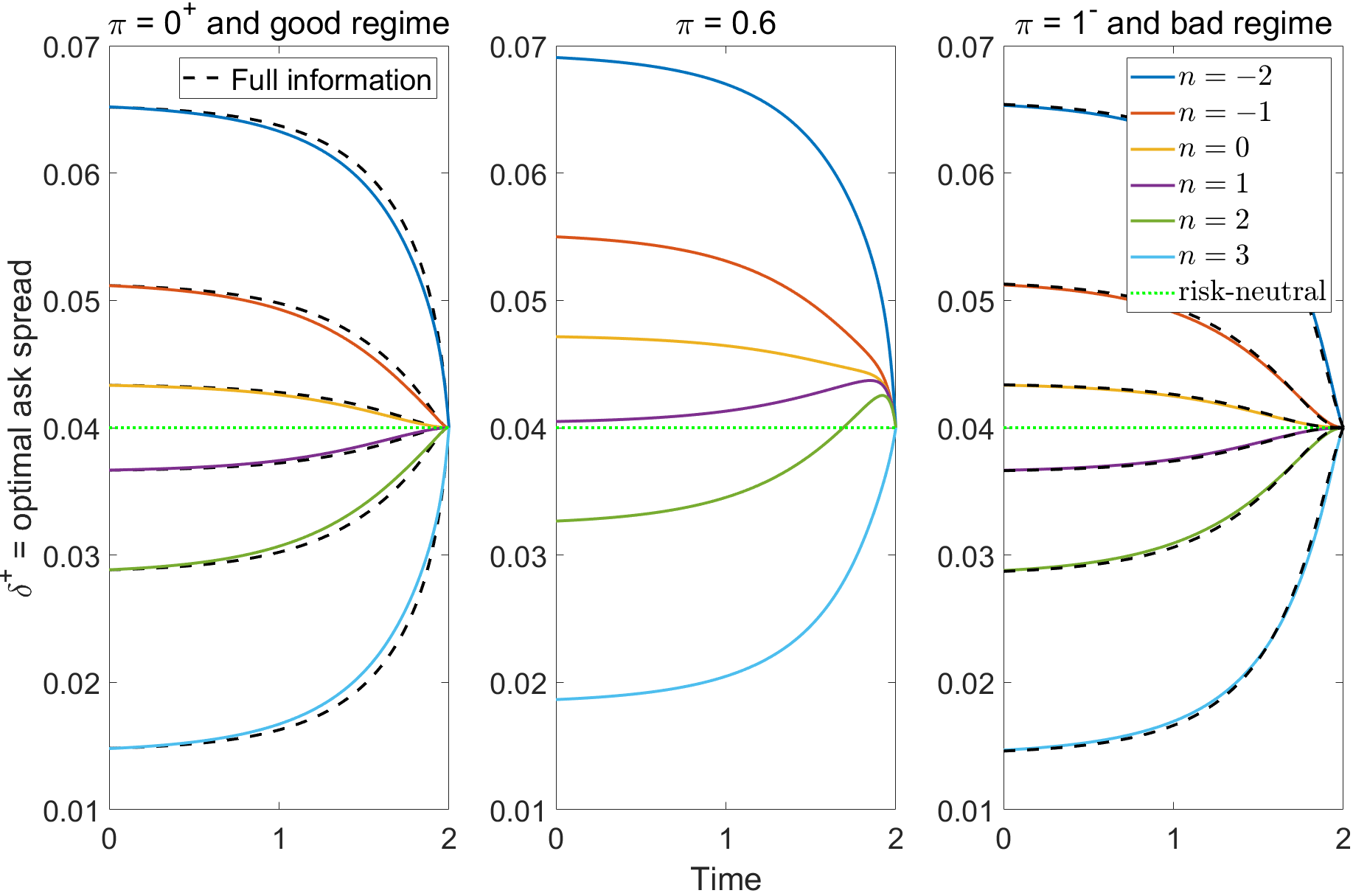

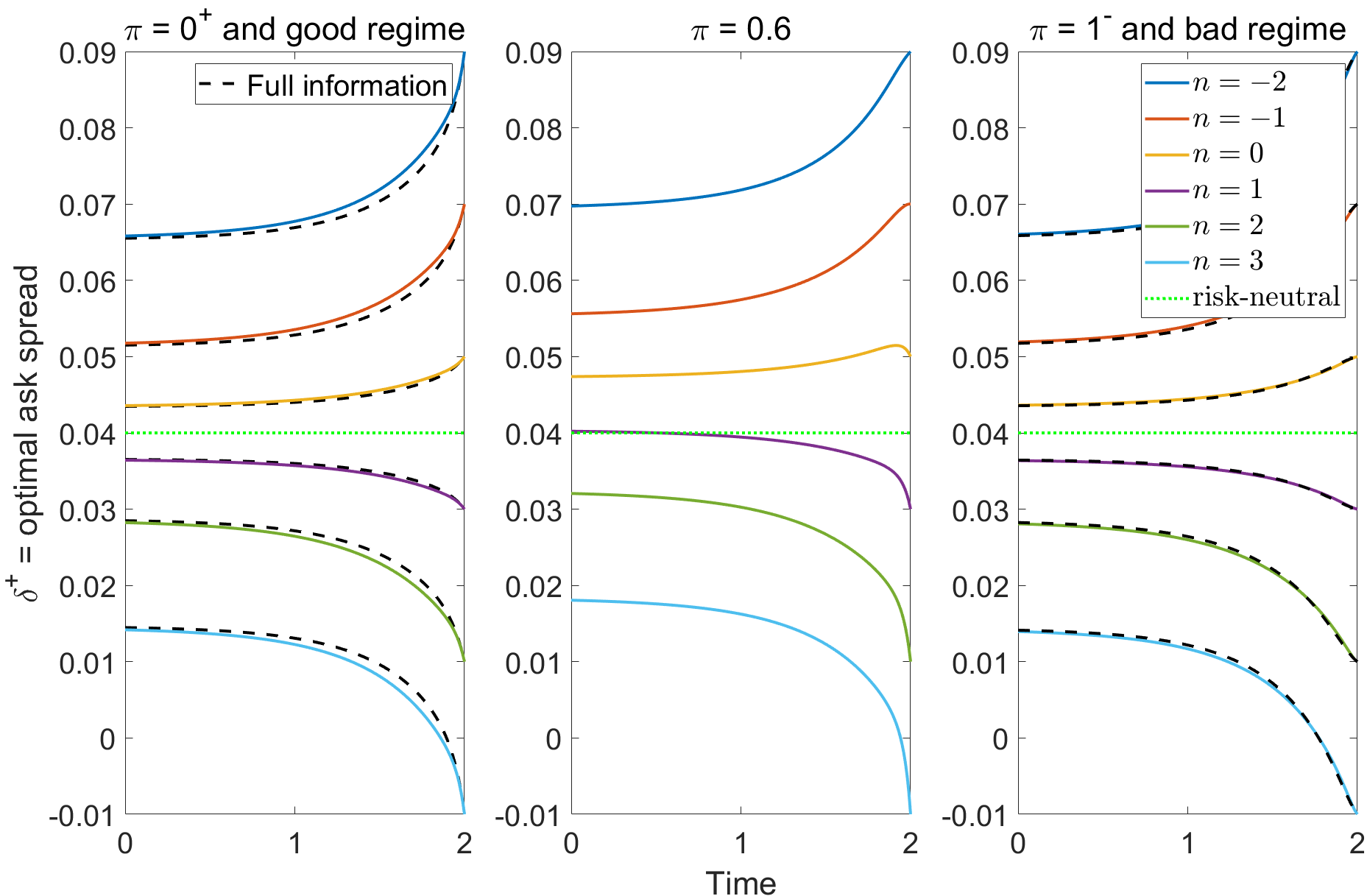

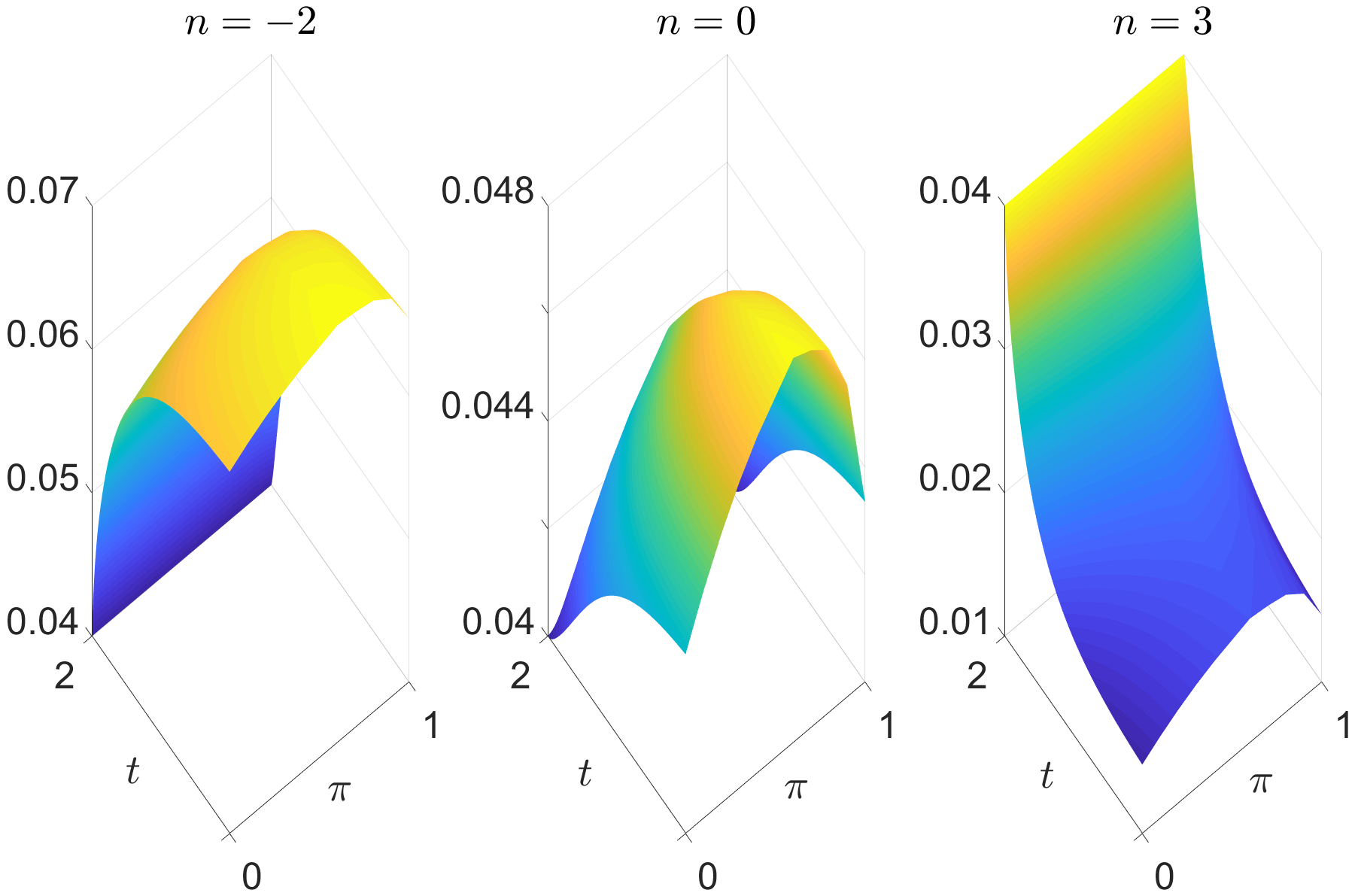

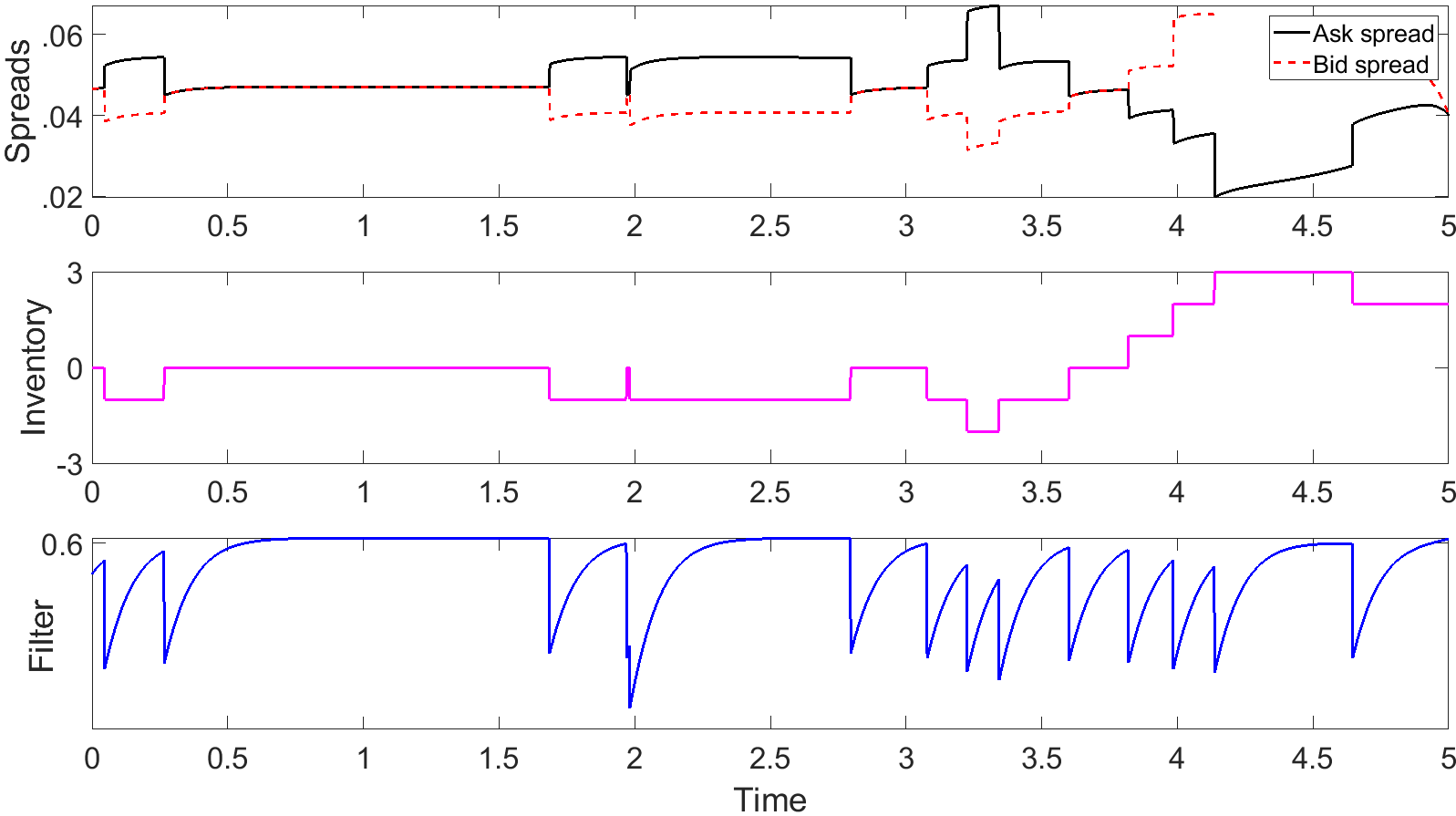

Figure 1.1 shows the optimal ask spread under partial information as a function of time, for different inventory levels (solid lines). It also displays how it changes for different filter values ( from left to right) and how it compares to the optimal ask spread under full information (dashed lines) in the good regime (left) and bad regime (right). The inventory levels increase from top to bottom in all cases, and the terminal execution cost is neglected (). We have chosen to display due to the effect of the filter being more pronounced around this value; it results in an optimal spread which is, for , between and higher (depending on the inventory level) than the corresponding ones under full information (a sizeable difference in practice). We will come back to this in Section 1.5.2. All other values show similar intermediate behaviours. Recall that when the inventory reaches the minimum , the MM will not sell any more (either abstaining from quoting or giving a ‘stub’ quote) until her inventory increases again, which is why there is no spread plotted for this position. We see that some of the features already present in one regime models are preserved for two regimes, both under full and partial information; namely:

-

•