Bayesian modeling of time-varying conditional heteroscedasticity

Abstract

Conditional heteroscedastic (CH) models are routinely used to analyze financial datasets. The classical models such as ARCH-GARCH with time-invariant coefficients are often inadequate to describe frequent changes over time due to market variability. However, we can achieve significantly better insight by considering the time-varying analogs of these models. In this paper, we propose a Bayesian approach to the estimation of such models and develop a computationally efficient MCMC algorithm based on Hamiltonian Monte Carlo (HMC) sampling. We also established posterior contraction rates with increasing sample size in terms of the average Hellinger metric. The performance of our method is compared with frequentist estimates and estimates from the time constant analogs. To conclude the paper we obtain time-varying parameter estimates for some popular Forex (currency conversion rate) and stock market datasets.

Keywords: Autoregressive model, B-splines, Hamiltonian Monte Carlo (HMC), Non-stationary, Posterior contraction, Volatility

1 Introduction

For datasets observed over a long period, stationarity turns out to be an oversimplified assumption that ignores systematic deviations of parameters from constancy. Thus time-varying parameter models have been studied extensively in the literature of statistics, economics, and related fields. For example, the financial datasets, due to external factors such as war, terrorist attacks, economic crisis, political events, etc. exhibit deviation from time-constant stationary models. Accounting for such changes is crucial as otherwise time-constant models can lead to incorrect policy implications as pointed out by Bai (1997). Thus functional estimation of unknown parameter curves using time-varying models has become an important research topic today. In this paper, we analyze popular conditional heteroscedastic models such as AutoRegressive Conditional Heteroscedasticity (ARCH) and Generalized ARCH (GARCH) from a Bayesian perspective in a time-varying setup. Before discussing our new contributions in this paper, we provide a brief overview of some previous works in this areas.

In the regression regime, time-varying models have garnered a lot of recent attention; see, for instance, Fan and Zhang (1999), Fan and Zhang (2000), Hoover et al. (1998), Huang et al. (2004), Lin and Ying (2001), Ramsay and Silverman (2005), Zhang et al. (2002) among others. The models show time-heterogeneous relationship between response and predictors. Consider the following two regression models

where () are the covariates, is the transpose, and are the regression coefficients. Here, is a constant parameter and is a smooth function. Estimation of has been considered by Hoover et al. (1998), Cai (2007)) and Zhou and Wu (2010) among others. One popular way to decide if there is an evidence to favor time-varying models over the time-constant analogue is to perform hypothesis testing. See, for instance, Zhang and Wu (2012), Zhang and Wu (2015), Chow (1960), Brown et al. (1975), Nabeya and Tanaka (1988), Leybourne and McCabe (1989), Nyblom (1989), Ploberger et al. (1989), Andrews (1993) and Lin and Teräsvirta (1999). Zhou and Wu (2010) discussed obtaining simultaneous confidence bands (SCB) in model I, i.e. with additive errors. However their treatment is heavily based on the closed-form solution and it does not extend to processes defined by a more general recursion.

For time-varying AR, MA, or ARMA processes, the results from time-varying linear regression can be naturally extended. However, such an extension is not obvious for conditional heteroscedastic (CH hereafter ) models. These are, by the simple definition of evolution is difficult to estimate even in the time-constant case. However, one cannot possibly ignore its usefulness in analyzing and predicting financial datasets. These models (even the simple time-constant ones) have remained primary tools for analyzing and forecasting certain trends for stock market datasets since Engle (1982) introduced the classical ARCH model and Bollerslev (1986) extended it to a more general GARCH model. However, with the rapid dynamics of market vulnerability, the simple classical time-constant models fail in terms of estimation or prediction due to over-compensating the past data. Several references point out the necessity of extending these classical models to a set-up where the parameters can change across time, for example Stărică and Granger (2005), Engle and Rangel (2005) and Fryzlewicz et al. (2008a). Consider the simple tvARCH(1) model

Similar models can be defined for tvGARCH(1,1) as well where has an additional recursive term involving

When the two recursive parameters in a GARCH model sum up to 1, i.e. it is usually called an integrated GARCH (iGARCH; or bubble garch/explosive garch by some authors) process which employing the above display can also be extended towards a time-varying analog i.e. . A wide range of financial datasets exhibits iGARCH phenomena.

In the parlance of time-varying parameter models in the CH setting, numerous works discussed the CUSUM-type procedure, for instance, Kim et al. (2000) for testing change in parameters of GARCH(1,1). Kulperger et al. (2005) studied the high moment partial sum process based on residuals and applied it to residual CUSUM tests in GARCH models. Interested readers can find some more change–point detection results in the context of CH models in James Chu (1995), Chen and Gupta (1997), Lin et al. (1999), Kokoszka et al. (2000) or Andreou and Ghysels (2006).

A time-varying framework and a pointwise curve estimation using M-estimators for locally stationary ARCH models were provided by Dahlhaus and Subba Rao (2006). Since then, while several pointwise approaches were discussed in the tvARMA and tvARCH case (cf. Dahlhaus and Polonik (2009), Dahlhaus and Subba Rao (2006), Fryzlewicz et al. (2008a)), pointwise theoretical results for estimation in tvGARCH processes were discussed in Rohan and Ramanathan (2013) and Rohan (2013) for GARCH(1,1) and GARCH(,) models respectively. In a series of recent works Karmakar et al. (2020+); Karmakar (2018) such models were discussed in wide generality. However, the focus remained frequentist, and the main goal accomplished there was to build simultaneous inference. One strong criticism for the CH type models remained that one needs a relatively large sample size () to achieve nominal coverage levels. The recursive definition of the models and a subsequent kernel-based method of estimating make it difficult to achieve satisfying results for relatively smaller sample sizes. This motivated us to explore a Bayesian way of building and estimating these models and use the posteriors to construct posterior estimates of the coefficient curves .

In this paper, we develop a Bayesian estimation method for time-varying analogs of ARCH, GARCH, and iGARCH models. We model the time-varying functional parameters using cubic B-splines. In the context of general varying-coefficient modeling, spline bases are a popular choice for its convenience and flexibility (Hastie and Tibshirani, 1993; Gu and Wahba, 1993; Cai et al., 2000; Biller and Fahrmeir, 2001; Huang et al., 2002; Huang and Shen, 2004; Amorim et al., 2008; Fan and Zhang, 2008; Yue et al., 2014; Franco-Villoria et al., 2019). Specific to the literature of time-varying volatility modeling, B-spline-based models have also been explored (Engle and Rangel, 2008; Audrino and Bühlmann, 2009; Liu and Yang, 2016).

Our contributions in this paper are two-fold. Towards the methodological development, note that the tvARCH, tvGARCH, and tviGARCH models require complex shape constraints on the coefficient functions. We achieve those by imposing different hierarchical structures on B-spline coefficients. The constraints are designed to be able to develop an efficient sampling algorithm based on gradient-based Hamiltonian Monte Carlo (HMC) (Neal et al., 2011; betancourt2015hamiltonian; betancourt2017conceptual; livingstone2019geometric). Strong motivation towards implementing such a Bayesian methodology was to circumvent the requirement of a huge sample size which is almost essential for effective estimation using the frequentist and kernel-based methods. This requirement on sample size has been frequently pointed out in the literature of ARCH/GARCH models and thus this was one of our main motivations to see if a reasonable estimation scheme can be designed in a Bayesian way.

Secondly, the existing literature on obtaining posterior concentration rates for dependent data is thin, even for an extremely simple model. To the best of our knowledge, ours is the first such attempt towards a theoretical development for these models under Gaussian-link. Posterior contraction rates for these models with respect to the average Hellinger metric are established. The main challenge therein is to construct exponentially consistent tests for these classes of models. Using some recently developed tools from Jeong et al. (2019); Ning et al. (2020) we have developed such tests. We first establish posterior contraction rates with respect to average log-affinity and then the same rate is transferred to the average Hellinger metric. The frequentist literature on inference about time-varying needs very stringent moment assumption and local stationarity assumptions which are often difficult to verify. Moreover, for econometric datasets, the existence of even the fourth moment is often questionable. Thus this paper offers some alternative way to estimate coefficients under lesser assumptions.

The rest of the paper is organized as follows. Section 2 describes the proposed Bayesian model in detail. Section 3 discusses an efficient computational scheme for the proposed method. We calculate posterior contraction rate in Section 4. In Section 5 we study the performance of our proposed method in the light of. Section 6 deals with real data application of the proposed methods for the three separate models and concludes with a brief interpretation of the results. We wrap the paper up with discussions, some concluding remarks, and possible future directions in Section 7. The supplementary materials contain theoretical proofs and some additional results.

2 Modeling

We elaborate on the models and our Bayesian framework for time-varying analogs of three specific cases that are popularly used to analyze econometric datasets.

2.1 tvARCH Model

Let satisfy the following time-varying ARCH() model for given ,

| (2.1) | |||

| (2.2) |

where the parameter functions satisfy

| (2.3) |

In a Bayesian regime we put priors on and . To respect the shape-constraints as imposed by we reformulate the problem. With as the B-spline basis functions, let

The prior induced by above construction is -supported. The verification is very straightforward. In above construction, . Thus . Since , . Thus . We have if and only if , which has probability zero. On the other hand, we also have as we have . Thus, the induced priors, described above are well supported in .

2.2 tvGARCH Model

Let satisfy the following time-varying GARCH(, model for given ,

| (2.4) |

Additionally we impose the following constraints on parameter space for the time-varying parameters,

| (2.5) |

The condition on the AR parameters imposed by (2.5) is somewhat popular in time-varying AR literature. See Dahlhaus and Subba Rao (2006); Fryzlewicz et al. (2008b); Karmakar et al. (2020+) for example. Different from these references, we additionally do not assume existence of any unobserved local-stationary process that are close to the observed process.

To proceed with Bayesian computation, we again put priors on the unknown functions and ’s such that they are supported in . Again the restrictions imposed by (2.5) are respected. The complete description of prior is

Here ’s are the B-spline basis functions. The parameters ’s are unbounded. The verification of support condition 2.5 for the proposed prior is similar.

2.3 tviGARCH Model

Although the GARCH(1,1) remains one of the most popular models to analyze econometric datasets, empirical evidence shows that these datasets regularly raise suspicion to the parameter space restriction . Note that we used a time-varying analog of this restriction for the tvGARCH modeling in Section 2.2. This often creates a very stringent condition as the validity of is questionable. The special case for a time-constant GARCH model where this restriction fails is called an iGARCH model in the literature. We consider the following time-varying analog of iGARCH.

| (2.6) |

We impose the following constraints on parameter space for the time-varying parameters,

| (2.7) |

The prior functions that allow us to reformulate the problem keeping it consistent with (2.7) is described below:

3 Posterior computation and Implementation

3.1 tvARCH structure

The complete likelihood of the proposed Bayesian method is given by

where and . We develop efficient Markov Chain Monte Carlo (MCMC) algorithm to sample the parameter and from the above likelihood. The computation of derivatives allows us to develop an efficient gradient-based MCMC algorithm to sample these parameters. We calculate the gradients of negative log-likelihood with respect to the parameters , and . The gradients are given below,

| (3.1) | ||||

| , | (3.2) | |||

| (3.3) | ||||

where stands for the indicator function which takes the value 1 when .

3.2 tvGARCH / tviGARCH structure

The complete likelihood of the proposed Bayesian method of (2.4) is given by

We calculate the gradients of negative log-likelihood with respect to the parameters , , and . The gradients are given below,

| , | |||

| , | |||

While fitting tvGARCH, we assume for any , . Thus, we need to additionally estimate the parameter . The derivative of the likelihood concerning is calculated numerically using the jacobian function from R package pracma. For the tviGARCH, the derivatives are similar so we avoid computing them for the sake of brevity.

Based on these gradient functions, we develop gradient-based Hamiltonian Monte Carlo (HMC) sampling. Note that, parameter spaces of ’s have bounded support. We circumvent this by mapping any Metropolis candidate falling outside the parameter space back to the nearest boundary. HMC has two parameters, required to be specified. These are the leap-frog step and the step-size parameter. It is difficult to tune both of them simultaneously. We choose to tune the step size parameter to maintain an acceptance range between 0.6 to 0.8. After every 100 iterations, the step-length is adjusted (increased or reduced) accordingly if it falls outside. Neal et al. (2011) showed that a higher leapfrog step is better for estimation accuracy at the expense of greater computation. To maintain a balance between accuracy and computational complexity, we keep it fixed at 30 and obtain good results.

4 Large-sample properties

We now focus on obtaining posterior contraction rates for our proposed Bayesian models. The posterior consistency is studied in the asymptotic regime of increasing number of time points . We study the posterior consistency with respect to the average Hellinger distance on the coefficient functions which is

where and denotes the corresponding likelihoods.

Definition: For a sequence if in -probability for every sequence , then the sequence is called the posterior contraction rate.

All the proofs are postponed to the supplementary materials. The proof is based on the general contraction rate result for independent non-i.i.d. observations (Ghosal and Van der Vaart, 2017) and some results on B-splines based finite random series. The exponentially consistent tests are constructed leveraging on the famous Neyman-Pearson Lemma as in Ning et al. (2020). Thus the first step is to calculate posterior contraction rate with respect to average log-affinity . Then we show that implies . We also consider following simplified priors for and to get better control over tail probabilities,

| (4.1) |

4.1 tvARCH model

Let stands for the complete set of parameters. For sake of generality of the method, we put a prior on and with probability mass function given by,

| (4.2) |

for . These priors have not been considered while fitting the model as it would require computationally expensive reversible jump MCMC strategy. The contraction rate will depend on the smoothness of true coefficient functions and and the parameters and from the prior distributions of and . Let be the truth of .

Assumptions(A): There exists constants such that,

-

(A.1)

The coefficient functions satisfy and .

-

(A.2)

for some small .

-

(A.3)

.

Assumptions (A.1)-(A.3) ensure

by recursion.

Theorem 1.

Under assumptions (A.1)-(A.3), let the true functions and be Hölder smooth functions with regularity level and respectively, then the posterior contraction rate with respect to the distance is

where are specified in (4.2).

4.2 tvGARCH model

Let stands for the complete set of parameters. For sake of generality of the method, we put a prior on , and with probability mass function given by,

| (4.3) |

for . These priors have not been considered while fitting the model as it would require computationally expensive reversible jump MCMC strategy. The contraction rate will depend on the smoothness of true coefficient functions and and the parameters and from the prior distributions of and . Let be the truth of .

Assumptions(B): There exists constants such that,

-

(B.1)

The coefficient functions satisfy and .

-

(B.2)

for some small .

-

(B.3)

.

Assumptions (B.1) and (B.3) ensure

by recursion. Similarly we have .

Theorem 2.

Under assumptions (B.1)-(B.3), let the true functions , and be Hölder smooth functions with regularity level . and respectively, then the posterior contraction rate with respect to the distance is

where are specified in (4.3).

4.3 tviGARCH model

Let stands for the complete set of parameters. For sake of generality of the method, we put a prior on and with probability mass function given by,

| (4.4) |

for . These priors have not been considered while fitting the model as it would require computationally expensive reversible jump MCMC strategy. The contraction rate will depend on the smoothness of true coefficient functions and and the parameters and from the prior distributions of and . Let be the truth of .

-

(C.1)

The coefficient functions satisfy for some

-

(C.2)

for some .

Theorem 3.

Under assumptions (C.1)-(C.2), let the true functions and be Hölder smooth functions with regularity level . and respectively, then the posterior contraction rate with respect to the distance is

where are specified in (4.4).

5 Simulation

We run simulations to study the performance of our proposed Bayesian method in capturing the true coefficient functions under different true models. The hyperparameters and of the normal prior are all set 100, which makes the prior weakly informative. We consider 4, 5 and 6 equidistant knots for the B-splines when and respectively. We collect 10000 MCMC samples and consider the last 5000 as post burn-in samples for inferences. We shall compare the estimated functions with the true functions in terms of the posterior estimates of functions along with its 95% pointwise credible bands. The credible bands are calculated from the MCMC samples at each point . We take the posterior mean as the posterior estimate of the unknown functions.

Since, to the best of our knowledge, there is no other Bayesian model for these time-varying conditional heteroscedastic models, we compare our Bayesian estimates with corresponding frequentist time-varying estimates. For computing the time-varying estimates of these models, we use the kernel-based method from Karmakar et al. (2020+). The M-estimator of the parameter vector are obtained using the conditional quasi log-likelihood. For instance, in the tvARCH(1) case, say

where denotes the Gaussian log-likelihood. Note that these methods are fast but usually need a cross-validated choice of bandwidth . We use and an appropriately chosen bandwidth as suggested by the authors therein. Since our discussion also involves iGARCH formulation, we wrote a separate kernel-based frequentist estimation for iGARCH models analogously. Apart from these two time-varying estimates, we also obtain a time-constant fit on the same data to help initiate a discussion on whether there was a necessity of introducing coefficients varying with time. For this tseries and rugarch R packages are used respectively for ARCH/GARCH and iGARCH fits.

To compare these estimates, we evaluate the average mean square errors (AMSE) for the three estimates. Note that in an usual linear regression of response on predictor scenario, the fitted MSE is often defined as . Since here, , we use the following definition of AMSE

where the is computed with the fitted parameter values as per the model under consideration. For example, for a tvGARCH(1,1) model we have

where and are the estimated curves from the posterior. Replacing the response by is natural as often autocorrelations of are checked to gauge presence of CH effect. Moreover, one of the early methods to deal with CH models was to view approximated by an TVAR(1) process. See bose2003estimating and references therein. Similar estimators as our proposed AMSE to evaluate the fitting accuracy has been used in the literature previously. See starica2003garch; Fryzlewicz et al. (2008a); Rohan and Ramanathan (2013); Karmakar et al. (2020+) for example.

In the next three subsections, we provide the results for the three models, namely, tvARCH, tvGARCH, and tviGARCH. Our conclusions from these results are illustrated at the end of the section.

5.1 tvARCH case

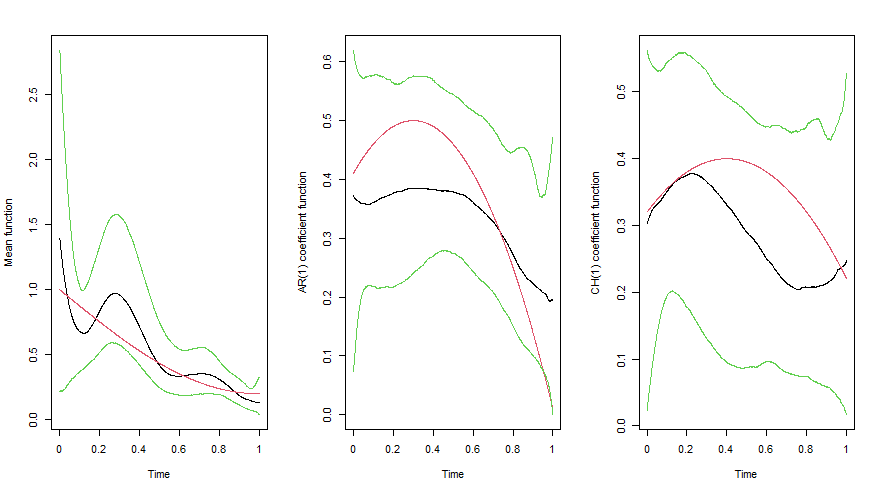

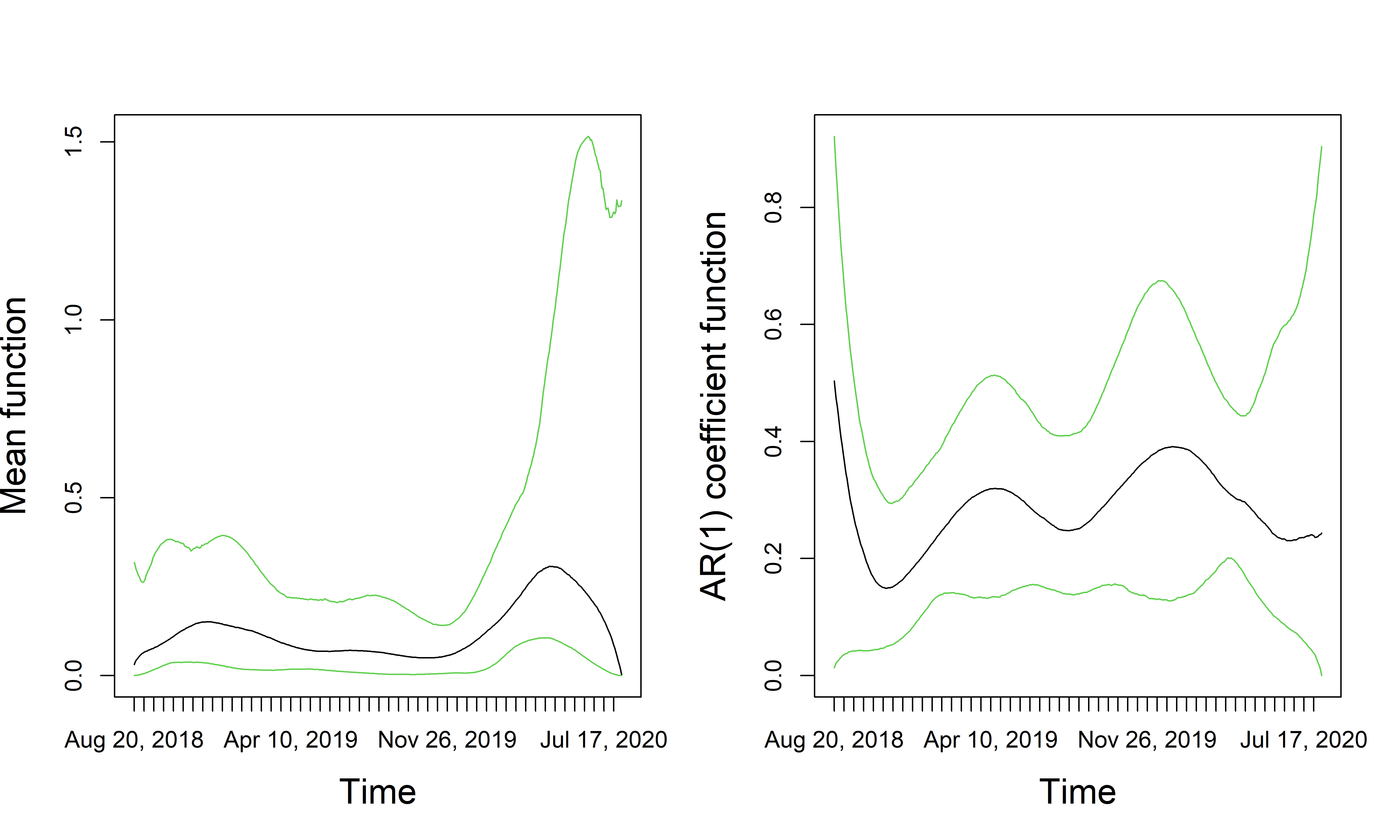

We start by considering the following tvARCH(1) model from 2.2. Three different choices for are considered, and . The true functions are,

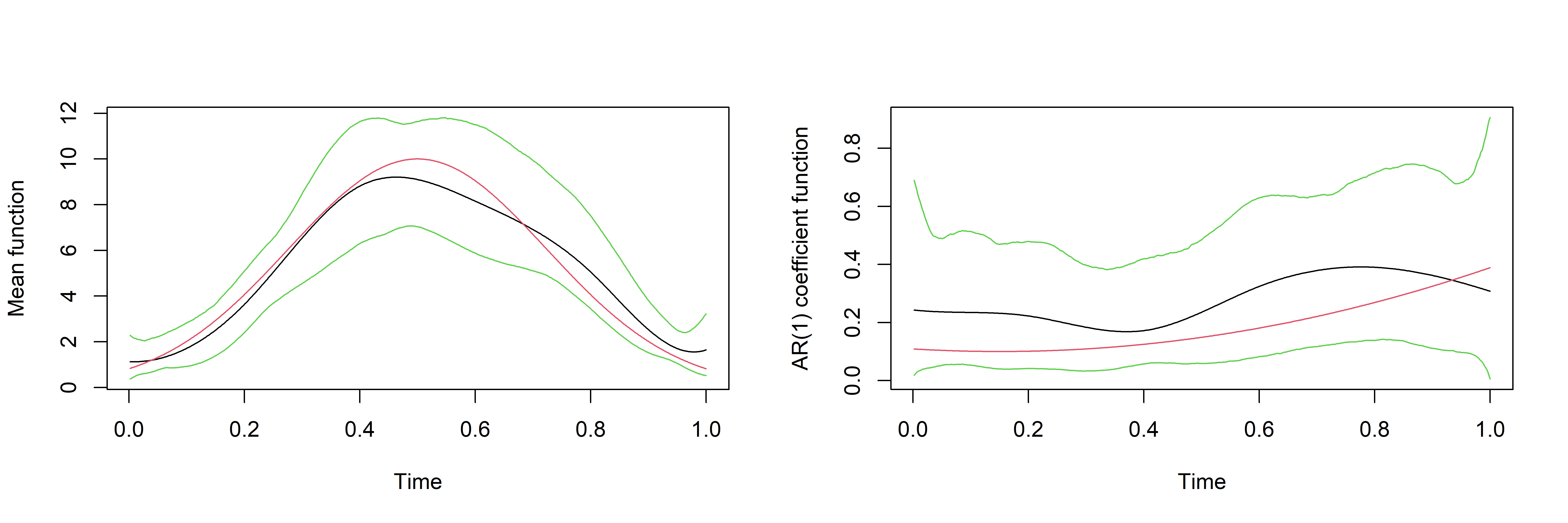

We compare the estimated functions with the truth for sample size 1000 in Figures 1. Table 1 illustrates the performance of our method with respect to other competing methods.

| ARCH(1) | Frequentist tvARCH(1) | Bayesian tvARCH(1) | |

|---|---|---|---|

| 96.42 | 90.34 | 85.22 | |

| 128.07 | 122.53 | 118.45 | |

| 138.06 | 130.33 | 127.06 |

5.2 tvGARCH case

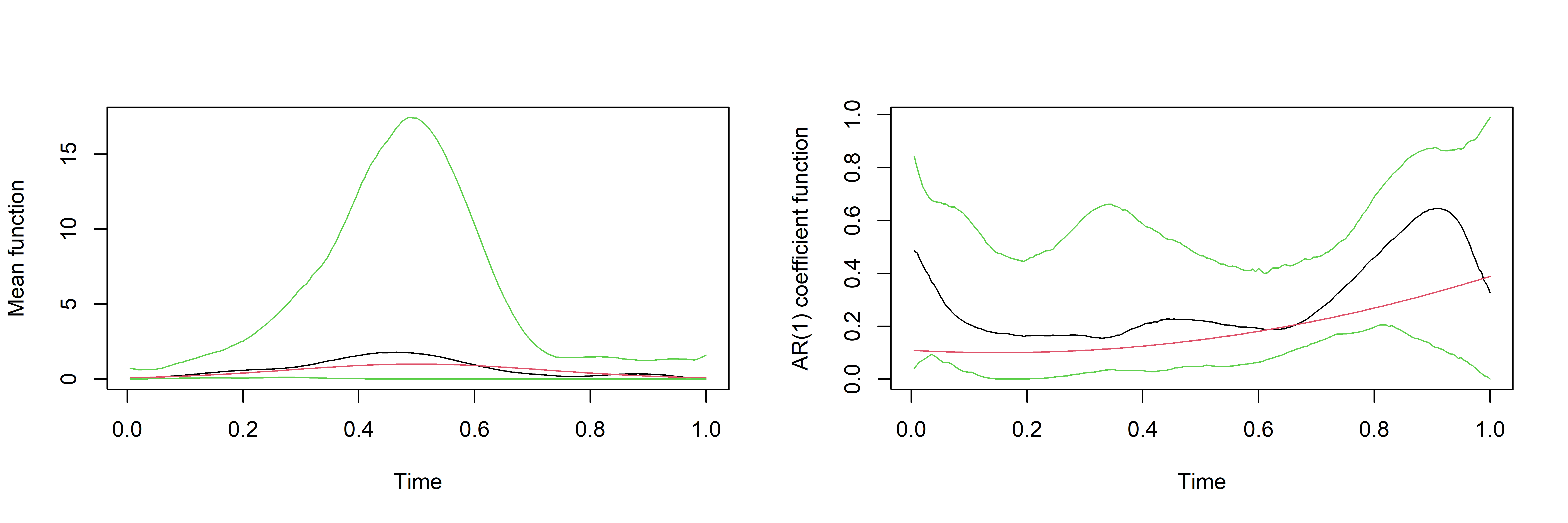

Next we explore the following GARCH(1,1) model (cf. 2.4)for different choices of . The true functions are,

Note that, estimation of GARCH, due to the additional parameter curves is a significantly more challenging problem and often requires a much higher sample size to have a reasonable estimation. We show by the means of the following pictures in Figure 2 that the estimation looks reasonable even for smaller sample sizes. The AMSE score comparisons are shown in Tables 2. The performance of our method is also contrasted with other competing methods.

| GARCH(1,1) | Frequentist tvGARCH(1,1) | Bayesian tvGARCH(1,1) | |

|---|---|---|---|

| 33.99 | 31.84 | 29.43 | |

| 45.46 | 34.77 | 33.33 | |

| 42.60 | 37.09 | 36.55 |

5.3 tviGARCH case

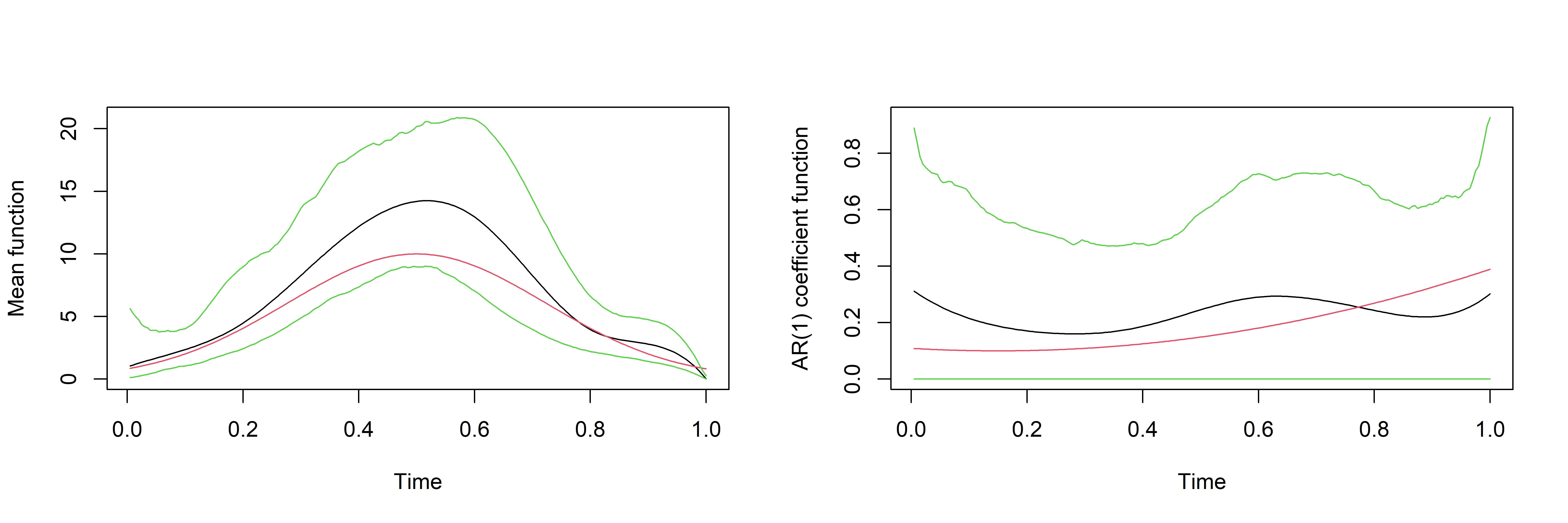

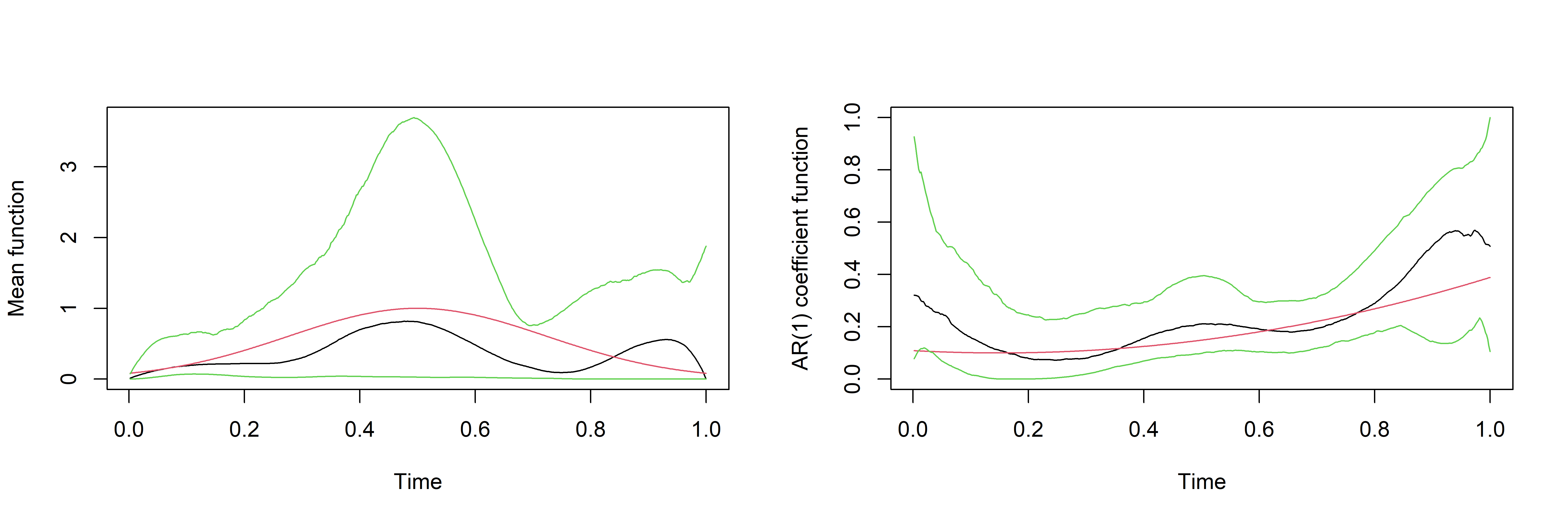

Finally we consider the tviGARCH(1,1) model (cf. 2.6) a special case of GARCH. Note that due to the constraint we only consider the mean function and AR(1) function for plotting. For this case, our true functions are as follows

The frequentist computation for tviGARCH method is carried out based on a kernel-based estimation scheme along the same line as Karmakar et al. (2020+). The estimated plots along with the 95% credible intervals are shown in Figure 3 for three sample sizes and the AMSE scores in Table 3.

| iGARCH(1,1) | Frequentist tviGARCH(1,1) | Bayesian tviGARCH(1,1) | |

|---|---|---|---|

| 200 | 8.20 | 23.86 | 8.14 |

| 500 | 9.06 | 18.72 | 9.06 |

| 1000 | 10.59 | 25.92 | 10.59 |

To summarize, our estimated functions are close to true functions for all the cases. We also find that the credible bands are getting tighter with increasing sample size. Thus estimates are improving in precision as sample size increases as shown in Figures 1 to 3. AMSEs of our Bayesian estimates are at least better for all the cases as in Tables 1 to 3. For tviGARCH, AMSE* is considered due to the huge and somewhat incomparable values of AMSE due to non-existent variance.

6 Real data application

Towards applying our methods on real-life datasets we stick to econometric data for varying time horizons. These datasets show considerable time-variation justifying our models to be suitable for understanding how the parameter functions have evolved. Typically we model the log-return data of the daily closing price of these data to avoid the unit-root scenario. The log-return is defined as follows and is close to the relative return

where is the closing price on the day. Conditional heteroscedastic models are popularly used for model building, analysis and forecasting. Here we extend such models to a more sophisticated and general scenario by allowing the coefficient functions to vary.

In this section, we analyze two datasets: USD to JPY conversion and NASDAQ, a popular US stock market data. We analyze the NASDAQ data through tvGARCH(1,1) and tviGARCH(1,1) models and USDJPY conversion rate data through tvARCH(1) models. We just fit one lag for these models as multiple lag fits are similar and larger lags seem to be insignificant. This result is consistent with the findings in Karmakar et al. (2020+), Fryzlewicz et al. (2008b) etc. Moreover, as Fryzlewicz et al. (2008b) claims, stock indices and Forex rates are more suited to GARCH and ARCH type of models respectively for their superior predictive performance. Each of these datasets was collected up to 31 July 2020. We exhibit our results for the last 200,500 and 1000 days which capture the last 6 months, around 1.5 years, and around 3 years of data respectively. All these datasets were collected from www.investing.com. Note that these datasets are usually available for weekdays barring holidays and typically there are about 260 data points every single year.

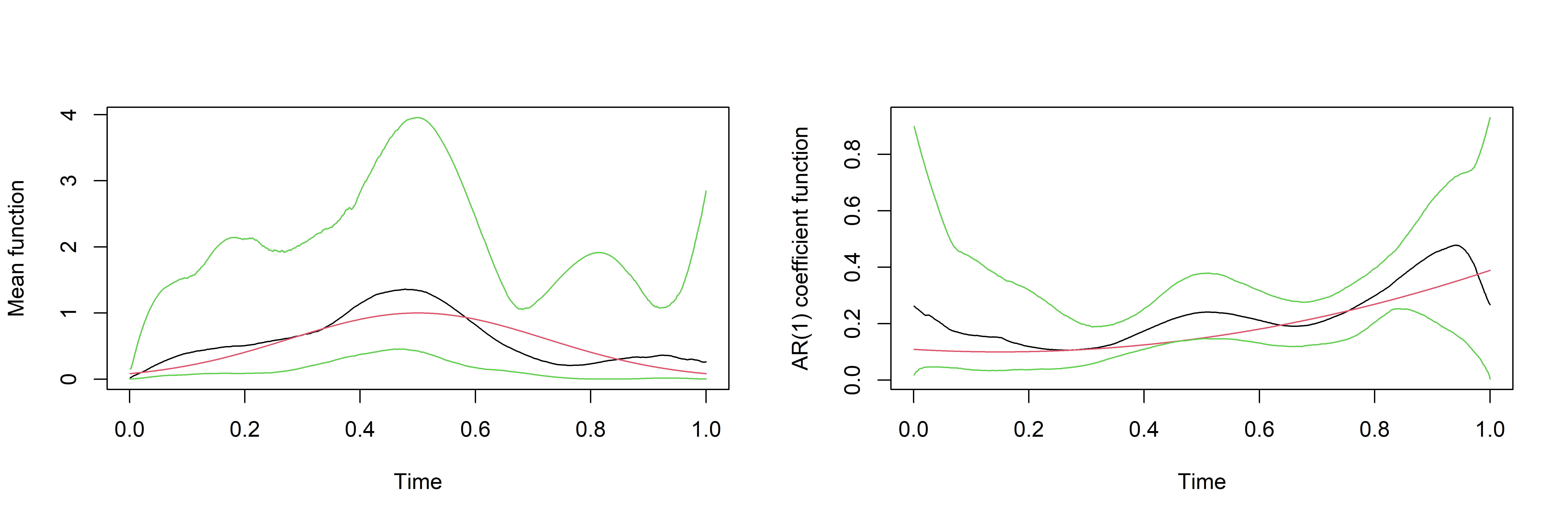

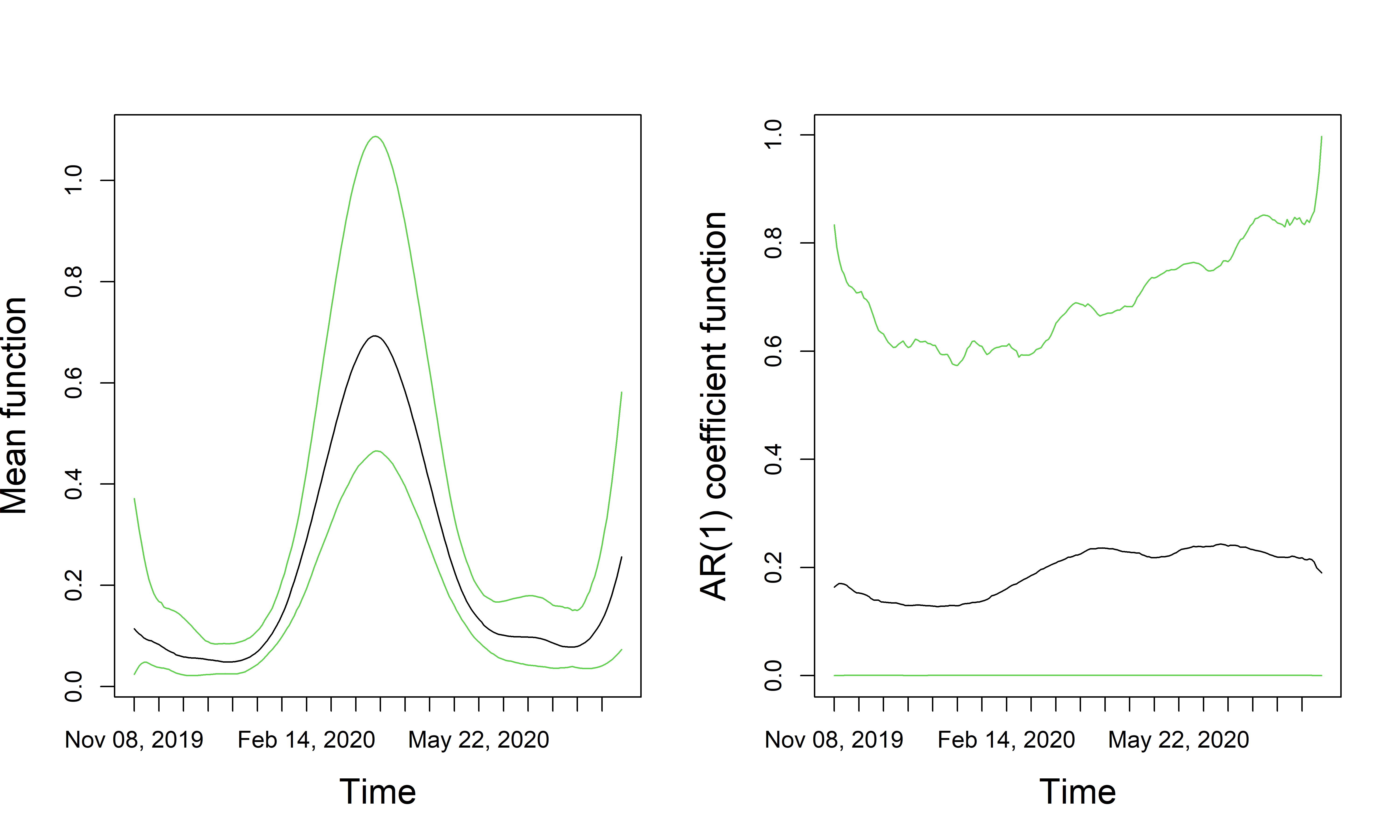

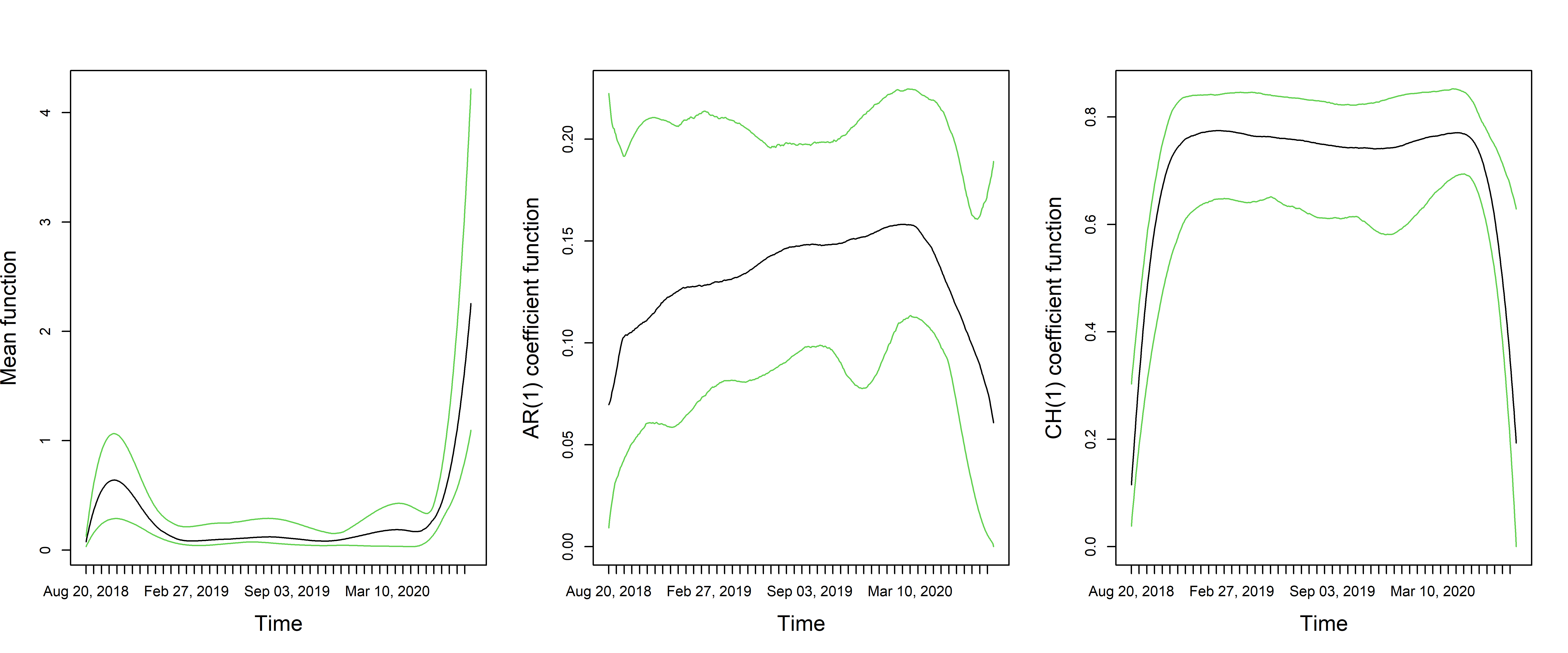

6.1 USDJPY data: tvARCH(1) model

We obtain the following Figure 4 that shows our estimation for fitting a tvARCH(1) model on the USD to JPY conversion data for the last 200,500 and 1000 days ending on 31 July 2020. The AMSE is also computed and contrasted with other competing methods in Table 4. Figure 4 depicts the estimated functions with 95% credible bands for different sample sizes. One can see the bands become much shorter for larger sample sizes. The mean coefficient function is generally time-varying for all three cases as one cannot fit a horizontal line through the 95% posterior bands. There seems to be a rise in the mean value around 100 days ago from July 31, 2020, which is right around the time the COVID-19 pandemic hit the world. With the analysis of days, we see that the volatility is quite high around October 2016 which coincides with the presidential election time of 2016. The AR(1) coefficient does not show the huge time-varying property. We also tabulate the AMSE for the three sample sizes in Table 4 and one can see for smaller sample sizes such as , the proposed Bayesian tvARCH achieves a significantly lower score but when the sample size grows then the performance becomes similar.

| ARCH(1) | Frequentist tvARCH(1) | Bayesian tvARCH(1) | |

|---|---|---|---|

| 1.4572 | 1.2259 | 1.1712 | |

| 0.6281 | 0.5313 | 0.5218 | |

| 0.4265 | 0.3773 | 0.3785 |

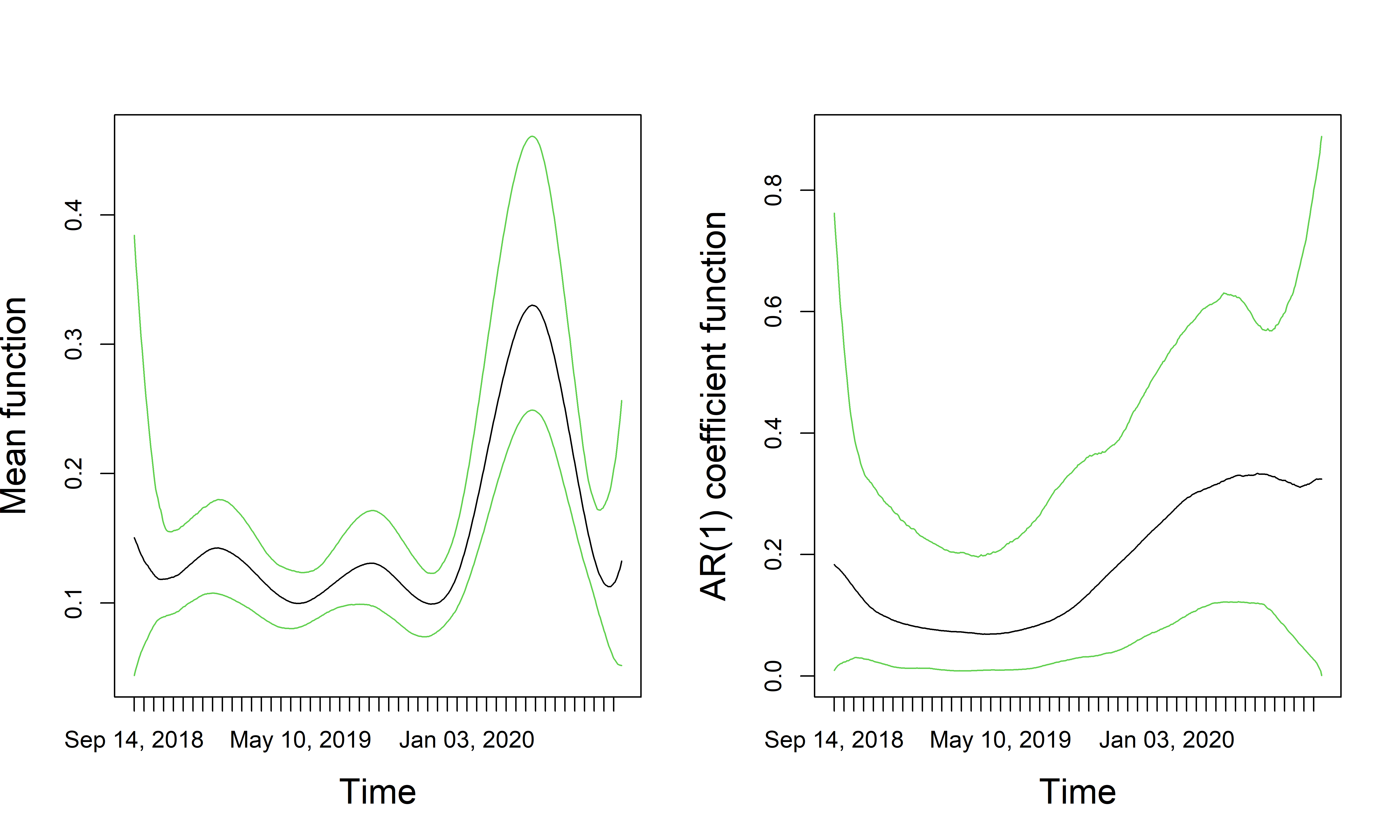

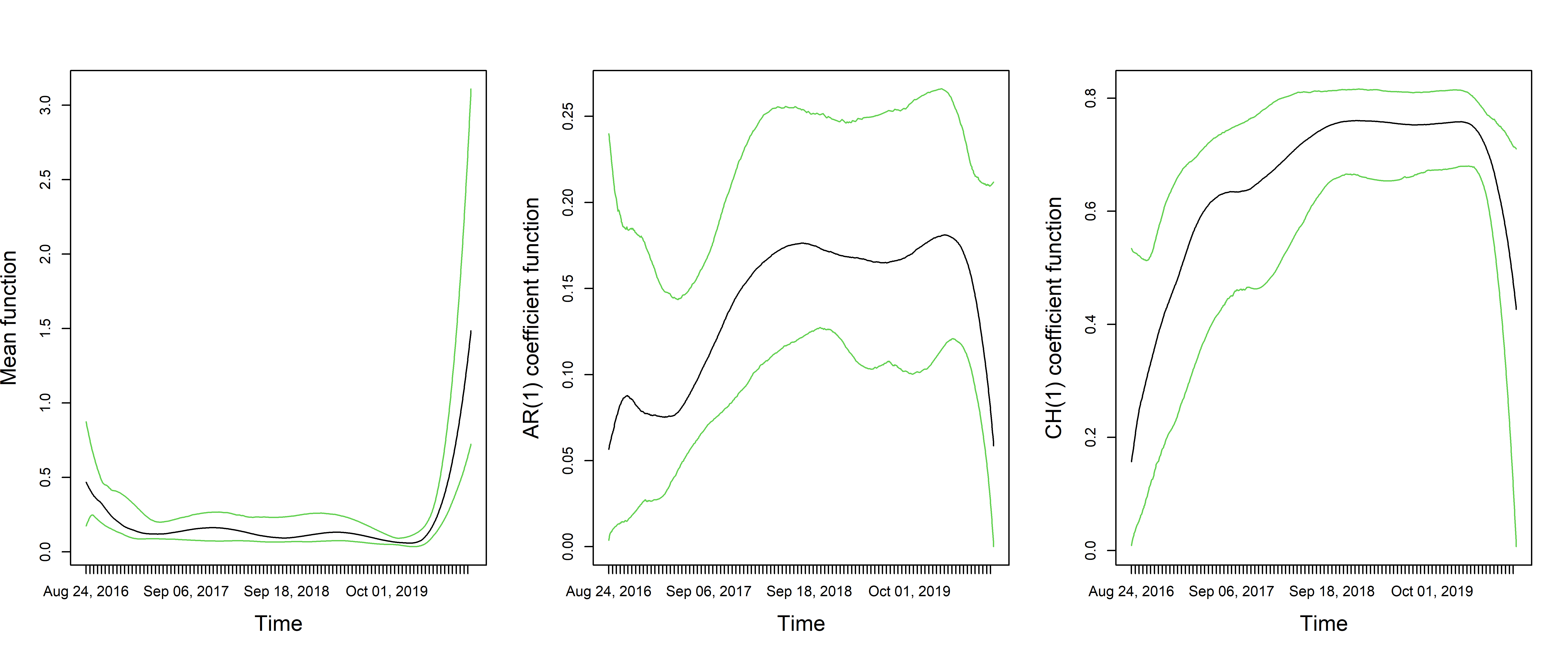

6.2 NASDAQ data: tvGARCH(1,1) model

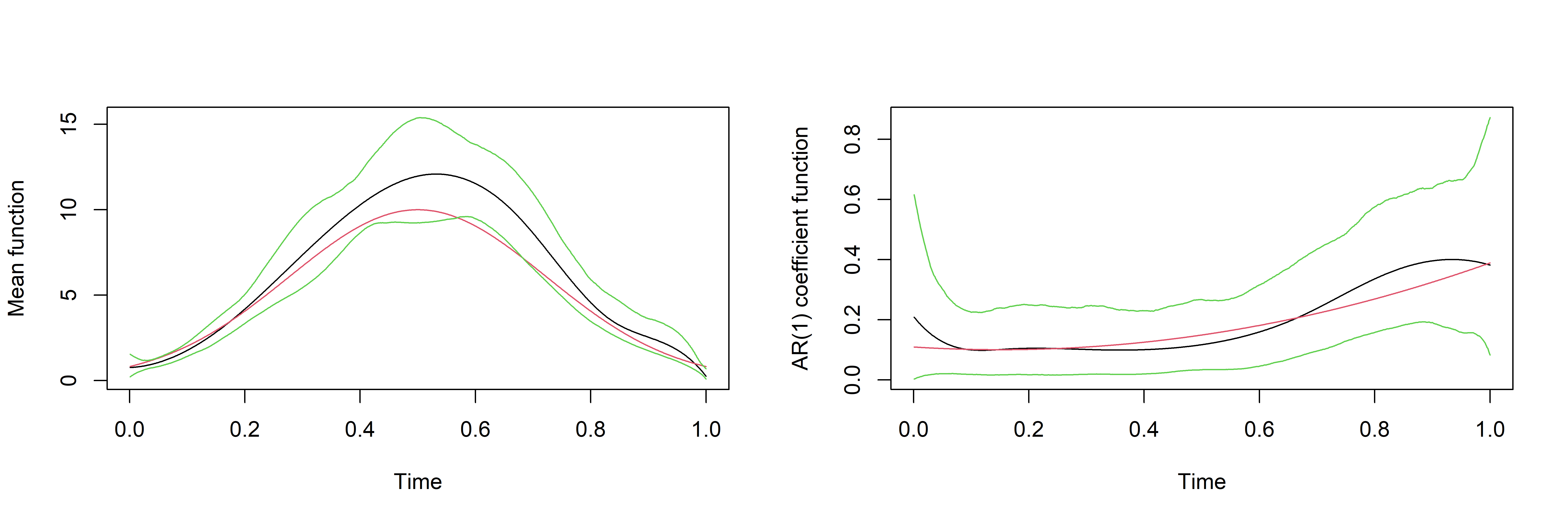

As has become standard in analyzing stock market datasets using GARCH models, we use time-varying GARCH for small orders. We obtain the following Figure 5 for fitting a tvGARCH(1,1) model on the NASDAQ data for the last 200,500, 1000 days ending on 31 July 2020. One can see the values are generally low and the values are higher which is consistent with how these outcomes turn out for time-constant estimates for econometric datasets. One can also see the role sample size plays in curating these time-varying estimates. For , the achieves high value of 0.6 around mid-March 2020 but for higher sample sizes it shows values as high as 0.8. One can also note the striking similarity for the analysis of the last 500 and 1000 days which is fairly consistent with the idea that estimation is more stable for such CH type models with a higher sample size. Nonetheless, the estimates for seem quite smooth as well which can be seen as a benefit of our methodology. Table 5 provides a comparison of AMSE scores across the three methods for three sample sizes. The Bayesian tvGARCH(1,1) performs relatively better than other methods and estimated curves have smaller credible bands with a growing sample size. The behavior of the mean function also shows higher volatility around the pandemic.

| GARCH(1,1) | Frequentist tvGARCH(1,1) | Bayesian tvGARCH(1,1) | |

|---|---|---|---|

| 203.5917 | 203.5917 | 202.6192 | |

| 104.7443 | 90.5395 | 90.3126 | |

| 46.16759 | 46.9225 | 45.5618 |

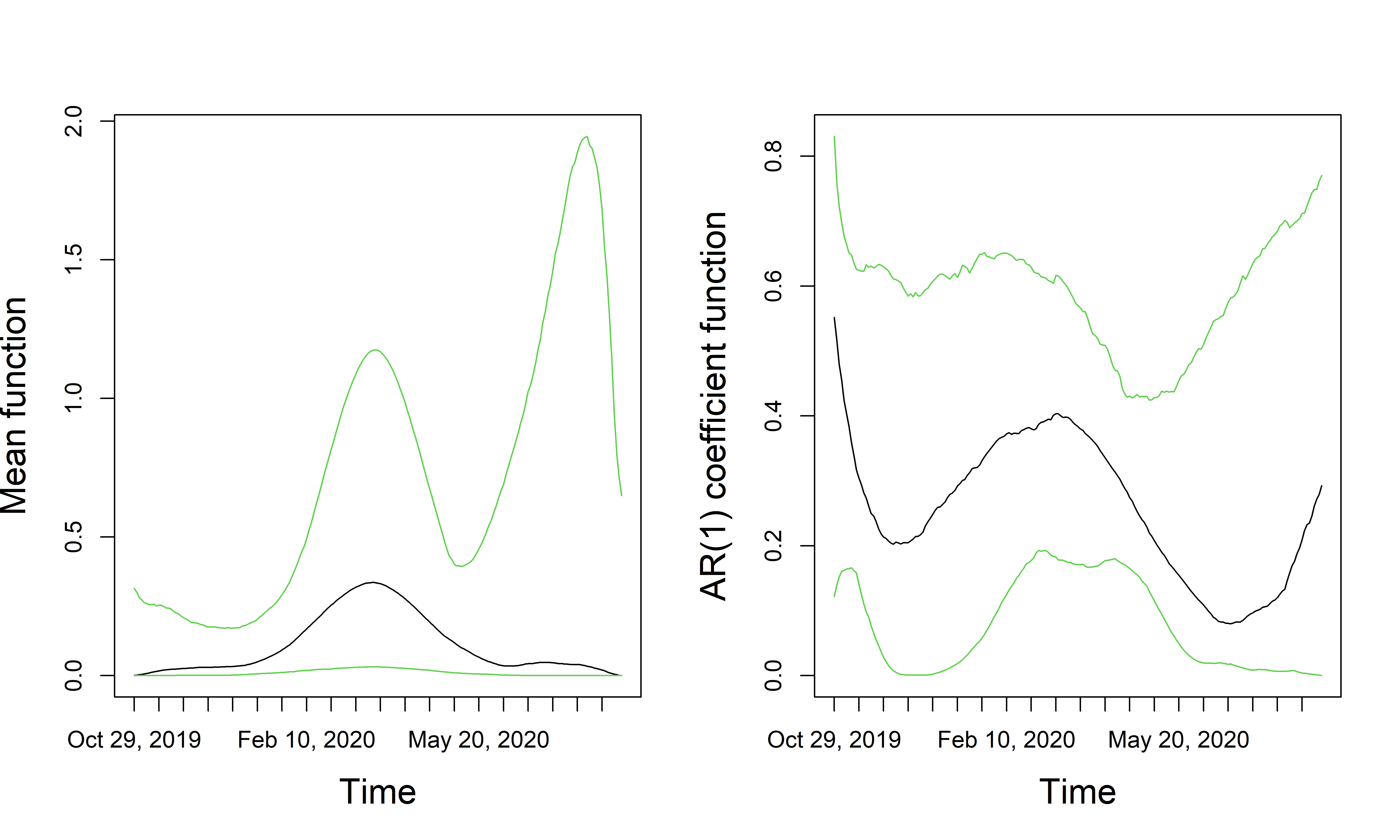

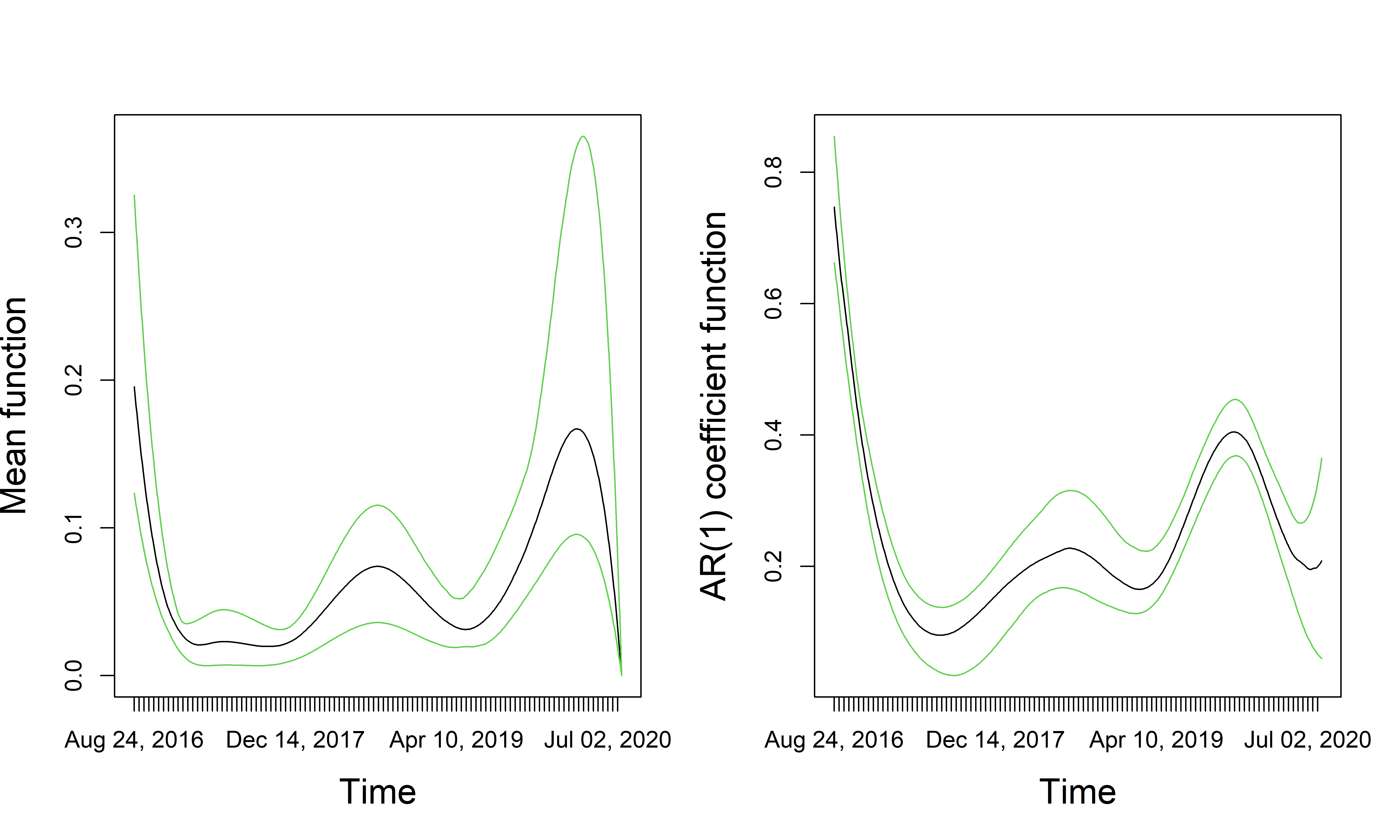

6.3 NASDAQ data: tviGARCH(1,1) model

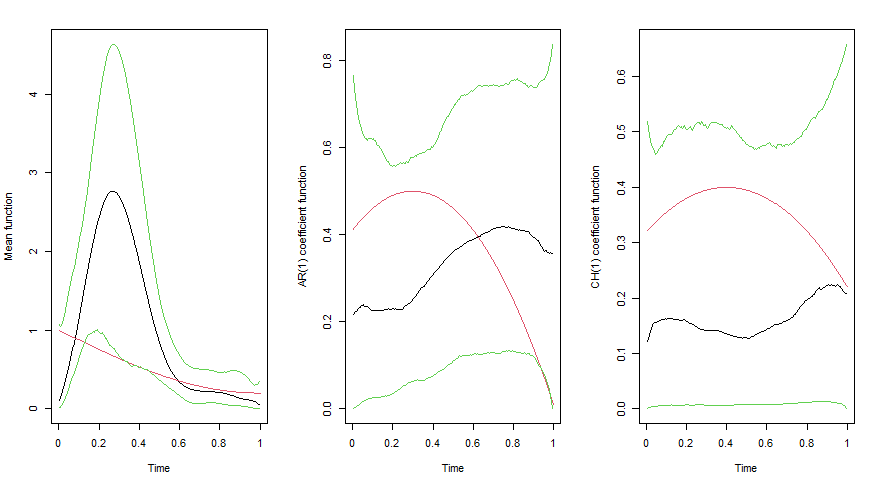

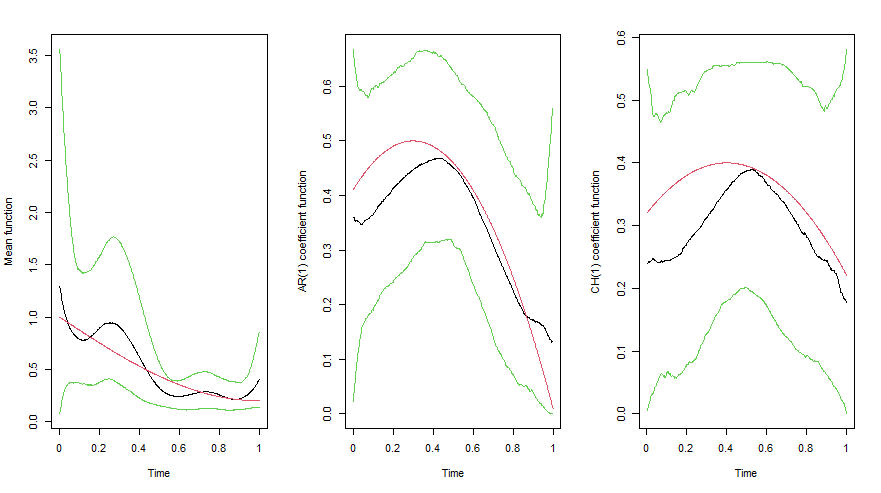

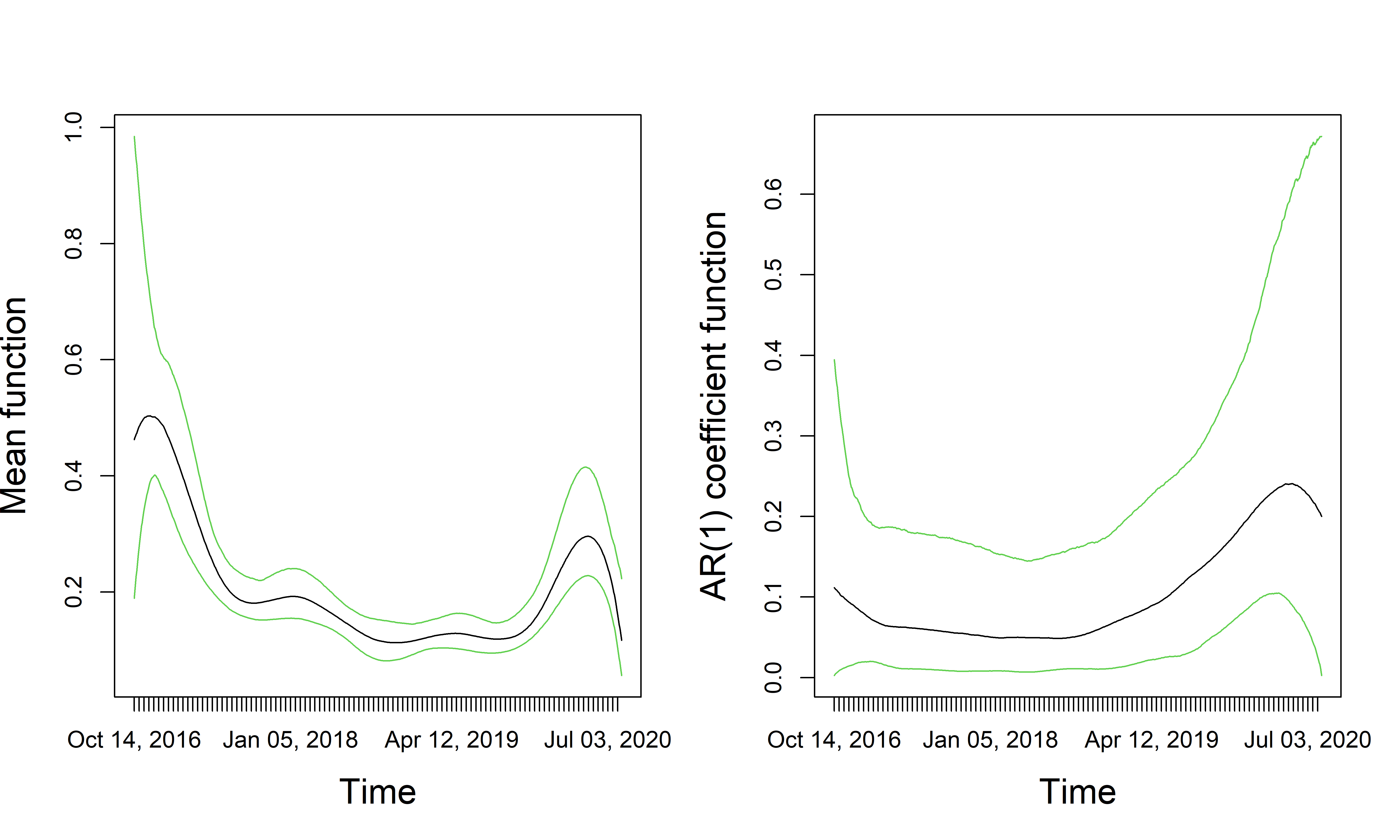

In Figure 5 the sum of estimated coefficient functions is close to 1 for a significant time-horizon. This motivates us to also fit tviGARCH(1,1) to analyze the same NASDAQ data. The estimated functions are presented in Figure 6 for the last and days. Table 6 compares the AMSE scores for the same three methods as before with varying sample sizes. The estimated mean and AR(1) functions of Figure 6 change a little from the estimated functions of tvGARCH(1,1) fit in Figure 5. Moreover, the effect of the three sample sizes is clear here with showing very precise bands and can reveal an interesting time-varying pattern.

In terms of AMSE, one can see in Table 6 that the frequentist methods did worse than even the time-constant versions. The time-constant estimates were computed using the rugarch package in R. The Bayesian tviGARCH method provides significantly better AMSE uniform overall sample sizes. Here the mean function also shows higher volatility around the time when the pandemic struck us. Volatility due to the presidential election in 2016 can also be observed here.

| iGARCH(1,1) | Frequentist tviGARCH(1,1) | Bayesian tviGARCH(1,1) | |

|---|---|---|---|

| 217.4988 | 278.4635 | 206.6886 | |

| 96.5001 | 132.544 | 90.4456 | |

| 54.1171 | 260.4696 | 46.3704 |

6.4 Model comparison

For the analysis of NASDAQ data, we have used two different models and thus it is pertinent to answer how should one choose between a competing class of models. We provide some measures in this subsection to decide between these two competing models. We start by comparing the performance of tvGARCH and tviGARCH models in terms of Bayes factor (kass1995bayes). Our calculation of the Bayes factor is based on the posterior samples using the harmonic mean identity of neton1994approximate. Let us denote and as the Bayes factors for three sample sizes where

for sample size and the corresponding dataset . The values we obtain are , and . According to guidelines from section 3.2 of kass1995bayes, there is ‘positive’ evidence in favor of tvGARCH for sample sizes 200 and 500. However, the same evidence becomes ‘strong’ for sample size 1000.

We also try to address out-of-sample predictive performance comparison here. Note that for a time-varying GARCH or time-varying iGARCH model this is generally a difficult task due to the assumed non-stationarity of the model. Thus, we take following approach to calculate out of sample joint predictive log-likelihoods for model comparison. Let us assume we have the data with data points. To evaluate the joint predictive log-likelihood for the last most recent data points, we fit the models in (2.4) and (2.6) with the first data. Note that the assumed time horizons for these two models are . Based on the estimated B-spline coefficients, and other parameters from each model, we can compute the joint predictive log-likelihood of the last data points as

where . For the tviGARCH model, we have .

Using this predictive log-likelihood we decide to evaluate the two fits from tvGARCH and tviGARCH in the following manner. For each of the sample sizes, we run it on three separate regimes of the data, the full data, and two halves of the data. In all these 8 settings, ( three sample sizes, three possible regions of the data, but the latest half of the 1000-sized data is the same as the full data for sample size 500) we compute 10, 20, and 50 steps ahead forecast. We tabulate these results in Table 7. One can see that generally speaking, there is somewhat conclusive evidence towards the iGARCH model for a smaller sample size. This supports our motivation why we additionally provide a tviGARCH(1,1) modeling on the same dataset.

Based on our model comparison exercises, we have an interesting phenomenon where for in-sample model fit, tvGARCH is better but in terms of out-of-sample prediction, tviGARCH outperforms tvGARCH in almost all the cases. Note that, tvGARCH has one additional free parameter and thus is expected to fit the data better but since the estimated and coefficients are close to one satisfying the iGARCH formulation, the out-of-sample performance for tviGARCH may have exceeded that for tvGARCH.

| Steps | Full | First Half | Second (Latest) Half | ||||

|---|---|---|---|---|---|---|---|

| () | GARCH | iGARCH | GARCH | iGARCH | GARCH | iGARCH | |

| 200 | 10 | 1.982 | 3.532 | 3.154 | 2.251 | ||

| 20 | 2.689 | 1.881 | 14.889 | 2.475 | 90281 | 2.278 | |

| 50 | 3.640 | 2.487 | 86.81 | 2.877 | 5.839 | 4.221 | |

| 500 | 10 | 2.842 | 2.068 | 10.260 | 1.898 | 1161 | 2.079 |

| 20 | 2.341 | 1.848 | 3897 | 1.407 | 343.49 | 1.893 | |

| 50 | 2.147 | 2.112 | 44.381 | 3.061 | 932.7 | 2.371 | |

| 1000 | 10 | 1.856 | 1.936 | 2.499 | 2.790 | 2.842 | 2.068 |

| 20 | 1.911 | 1.789 | 1.999 | 1.903 | 2.341 | 1.848 | |

| 50 | 2.266 | 2.214 | 1.893 | 1.536 | 2.147 | 2.112 | |

As per the suggestion from a reviewer, we also add a one-step-ahead point forecasting exercise between these models. Here the computation method remains the same as outlined in the predictive log-likelihood computation however we only restrict ourselves to to make the discussion concise. For this part of the exercise we choose to compute posterior mean of where to ensure out-of-sample prediction is estimated solely based on . As one-step-ahead forecasts can be prohibitively misleading given it depends so much on one single location, we decide to take an average of over 15 random starting points over the entire time spectrum of 10 years resulting in 2518 points). For each of the sample sizes, we tabulate the performance in the following Table 8. Note that, here we are only comparing the two Bayesian time-varying models to see which one fits our data better. The advantage of predicting the future coefficients using B-spline is not available in the kernel-based frequentist method and thus is not included here in the discussion.

| Bayesian tvGARCH(1,1) | Bayesian tviGARCH(1,1) | |

|---|---|---|

| 0.9914 | 0.3477 | |

| 1.5208 | 1.4102 | |

| 1.6378 | 1.7033 |

One can see, we again observe the same advantage of tviGARCH modeling over the tvGARCH one for smaller sample sizes. This is an interesting find of this paper in the context of the Bayesian model fitting to these datasets.

7 Discussion and Conclusion

In this paper, we consider a Bayesian estimation framework for time-varying conditional heteroscedastic models. Our prior specifications are amenable to Hamiltonian Monte Carlo for efficient computation. One of the key motivations towards going to a Bayesian regime was to achieve reasonable estimation even for a small sample size. Our simulation coverage shows good performance for all three models tvARCH, tvGARCH, tviGARCH for both small and large sample sizes. Importantly, in all three of the cases, we were able to establish posterior contraction rates. These calculations are, to the best of our knowledge, the first such work in even simple dependent models let alone the complicated recursions that these conditional heteroscedastic models demand. Moreover, the assumptions on the true functions and the number of moments needed were very minimal. An interesting future theoretical work would be to calculate posterior contraction rate with respect to empirical -distance which is a more desirable metric for function estimation. While analyzing real data, we see that the parameter curves vary significantly for the intercept terms, but not that much for AR or CH parameters. The associated codes to fit the three models are available at https://github.com/royarkaprava/tvARCH-tvGARCH-tviGARCH.

As future work, it will be interesting to explore multivariate time-varying volatility modeling (Tse and Tsui, 2002; Kwan et al., 2005) through a Bayesian framework similar to ours. Another interesting time-heterogeneity that we plan to explore through the glass of a Bayesian framework is regime-switching CH models where instead of the smooth time-varying functions the parameters change abruptly. We have a brief discussion in section 6.4 about how to choose between competing models. Those discussions can easily be extended to choose a proper number of lags or to choose between different types of ARCH/GARCH models. We believe this would provide an interesting parallel to the usual penalized likelihood-based methods for model selection in time-series. Finally note that, even though we do provide some insights onto future prediction for these datasets for real data applications, that was not the main focus in this paper. Forecasting for the time-varying model is extremely tricky since it requires ‘estimation’ of the future parameter values. Although in-filled asymptotics can help in this regard, still the literature so far is very sparse in this direction for both Bayesian and frequentist regimes. We plan to explore this extensively in near future.

Acknowledgement

We would like to thank the editor, the associate editor, and anonymous referees for their constructive suggestions that improved the quality of the manuscript.

References

- Amorim et al. (2008) Leila D Amorim, Jianwen Cai, Donglin Zeng, and Maurício L Barreto. Regression splines in the time-dependent coefficient rates model for recurrent event data. Statistics in medicine, 27(28):5890–5906, 2008.

- Andreou and Ghysels (2006) Elena Andreou and Eric Ghysels. Monitoring disruptions in financial markets. J. Econometrics, 135(1-2):77–124, 2006. ISSN 0304-4076. doi: 10.1016/j.jeconom.2005.07.023. URL http://dx.doi.org/10.1016/j.jeconom.2005.07.023.

- Andrews (1993) Donald W. K. Andrews. Tests for parameter instability and structural change with unknown change point. Econometrica, 61(4):821–856, 1993. ISSN 0012-9682. doi: 10.2307/2951764. URL http://dx.doi.org/10.2307/2951764.

- Audrino and Bühlmann (2009) Francesco Audrino and Peter Bühlmann. Splines for financial volatility. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 71(3):655–670, 2009.

- Bai (1997) Jushan Bai. Estimation of a change point in multiple regression models. The Review of Economics and Statistics, 79(4):551–563, 1997.

- Biller and Fahrmeir (2001) Clemens Biller and Ludwig Fahrmeir. Bayesian varying-coefficient models using adaptive regression splines. Statistical Modelling, 1(3):195–211, 2001.

- Bollerslev (1986) Tim Bollerslev. Generalized autoregressive conditional heteroskedasticity. J. Econometrics, 31(3):307–327, 1986. ISSN 0304-4076. doi: 10.1016/0304-4076(86)90063-1. URL http://dx.doi.org/10.1016/0304-4076(86)90063-1.

- Brown et al. (1975) R. L. Brown, James Durbin, and J. M. Evans. Techniques for testing the constancy of regression relationships over time. J. Roy. Statist. Soc. Ser. B, 37:149–192, 1975. ISSN 0035-9246. URL http://links.jstor.org/sici?sici=0035-9246(1975)37:2<149:TFTTCO>2.0.CO;2-7&origin=MSN. With discussion by D. R. Cox, P. R. Fisk, Maurice Kendall, M. B. Priestley, Peter C. Young, G. Phillips, T. W. Anderson, A. F. M. Smith, M. R. B. Clarke, A. C. Harvey, Agnes M. Herzberg, M. C. Hutchison, Mohsin S. Khan, J. A. Nelder, Richard E. Quant, T. Subba Rao, H. Tong and W. G. Gilchrist and with reply by J. Durbin and J. M. Evans.

- Cai (2007) Zongwu Cai. Trending time-varying coefficient time series models with serially correlated errors. J. Econometrics, 136(1):163–188, 2007. ISSN 0304-4076. doi: 10.1016/j.jeconom.2005.08.004. URL http://dx.doi.org/10.1016/j.jeconom.2005.08.004.

- Cai et al. (2000) Zongwu Cai, Jianqing Fan, and Qiwei Yao. Functional-coefficient regression models for nonlinear time series. Journal of the American Statistical Association, 95(451):941–956, 2000.

- Chen and Gupta (1997) Jie Chen and Arjun K Gupta. Testing and locating variance changepoints with application to stock prices. Journal of the American Statistical association, 92(438):739–747, 1997.

- Chow (1960) Gregory C. Chow. Tests of equality between sets of coefficients in two linear regressions. Econometrica, 28:591–605, 1960. ISSN 0012-9682. doi: 10.2307/1910133. URL http://dx.doi.org/10.2307/1910133.

- Dahlhaus and Polonik (2009) Rainer Dahlhaus and Wolfgang Polonik. Empirical spectral processes for locally stationary time series. Bernoulli, 15(1):1–39, 2009. ISSN 1350-7265. doi: 10.3150/08-BEJ137. URL http://dx.doi.org/10.3150/08-BEJ137.

- Dahlhaus and Subba Rao (2006) Rainer Dahlhaus and Suhasini Subba Rao. Statistical inference for time-varying ARCH processes. Ann. Statist., 34(3):1075–1114, 2006. ISSN 0090-5364. doi: 10.1214/009053606000000227. URL http://dx.doi.org/10.1214/009053606000000227.

- Engle (1982) Robert F. Engle. Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation. Econometrica, 50(4):987–1007, 1982. ISSN 0012-9682. doi: 10.2307/1912773. URL http://dx.doi.org/10.2307/1912773.

- Engle and Rangel (2005) Robert F Engle and J Gonzalo Rangel. The spline garch model for unconditional volatility and its global macroeconomic causes. 2005.

- Engle and Rangel (2008) Robert F Engle and Jose Gonzalo Rangel. The spline-garch model for low-frequency volatility and its global macroeconomic causes. The Review of Financial Studies, 21(3):1187–1222, 2008.

- Fan and Zhang (1999) Jianqing Fan and Wenyang Zhang. Statistical estimation in varying coefficient models. Ann. Statist., 27(5):1491–1518, 1999. ISSN 0090-5364. doi: 10.1214/aos/1017939139. URL http://dx.doi.org/10.1214/aos/1017939139.

- Fan and Zhang (2000) Jianqing Fan and Wenyang Zhang. Simultaneous confidence bands and hypothesis testing in varying-coefficient models. Scandinavian Journal of Statistics, 27(4):715–731, 2000.

- Fan and Zhang (2008) Jianqing Fan and Wenyang Zhang. Statistical methods with varying coefficient models. Statistics and its Interface, 1(1):179, 2008.

- Franco-Villoria et al. (2019) Maria Franco-Villoria, Massimo Ventrucci, Håvard Rue, et al. A unified view on bayesian varying coefficient models. Electronic Journal of Statistics, 13(2):5334–5359, 2019.

- Fryzlewicz et al. (2008a) Piotr Fryzlewicz, Theofanis Sapatinas, and Suhasini Subba Rao. Normalized least-squares estimation in time-varying ARCH models. Ann. Statist., 36(2):742–786, 2008a. ISSN 0090-5364. doi: 10.1214/07-AOS510. URL http://dx.doi.org/10.1214/07-AOS510.

- Fryzlewicz et al. (2008b) Piotr Fryzlewicz, Theofanis Sapatinas, and Suhasini Subba Rao. Normalized least-squares estimation in time-varying ARCH models. Ann. Statist., 36(2):742–786, 2008b. ISSN 0090-5364. doi: 10.1214/07-AOS510. URL http://dx.doi.org/10.1214/07-AOS510.

- Ghosal and Van der Vaart (2017) Subhashis Ghosal and Aad Van der Vaart. Fundamentals of nonparametric Bayesian inference, volume 44. Cambridge University Press, 2017.

- Ghosal et al. (2000) Subhashis Ghosal, Jayanta K Ghosh, Aad W Van Der Vaart, et al. Convergence rates of posterior distributions. Annals of Statistics, 28(2):500–531, 2000.

- Gu and Wahba (1993) Chong Gu and Grace Wahba. Smoothing spline anova with component-wise bayesian “confidence intervals”. Journal of Computational and Graphical Statistics, 2(1):97–117, 1993.

- Hastie and Tibshirani (1993) Trevor Hastie and Robert Tibshirani. Varying-coefficient models. Journal of the Royal Statistical Society: Series B (Methodological), 55(4):757–779, 1993.

- Hoover et al. (1998) Donald R. Hoover, John A. Rice, Colin O. Wu, and Li-Ping Yang. Nonparametric smoothing estimates of time-varying coefficient models with longitudinal data. Biometrika, 85(4):809–822, 1998. ISSN 0006-3444. doi: 10.1093/biomet/85.4.809. URL http://dx.doi.org/10.1093/biomet/85.4.809.

- Huang and Shen (2004) Jianhua Z Huang and Haipeng Shen. Functional coefficient regression models for non-linear time series: a polynomial spline approach. Scandinavian journal of statistics, 31(4):515–534, 2004.

- Huang et al. (2002) Jianhua Z Huang, Colin O Wu, and Lan Zhou. Varying-coefficient models and basis function approximations for the analysis of repeated measurements. Biometrika, 89(1):111–128, 2002.

- Huang et al. (2004) Jianhua Z. Huang, Colin O. Wu, and Lan Zhou. Polynomial spline estimation and inference for varying coefficient models with longitudinal data. Statist. Sinica, 14(3):763–788, 2004. ISSN 1017-0405.

- James Chu (1995) Chia-Shang James Chu. Detecting parameter shift in garch models. Econometric Reviews, 14(2):241–266, 1995.

- Jeong et al. (2019) Seonghyun Jeong et al. Frequentist properties of bayesian procedures for high-dimensional sparse regression. 2019.

- Karmakar (2018) Sayar Karmakar. Asymptotic theory for simultaneous inference under dependence. Technical report, University of Chicago, 2018.

- Karmakar et al. (2020+) Sayar Karmakar, Stefan Richter, and Wei Biao Wu. Simultaneous inference for time-varying models. In revision, https://sayarkarmakar.github.io/publications/sayar1.pdf, 2020+.

- Kim et al. (2000) Soohwa Kim, Sinsup Cho, and Sangyeol Lee. On the cusum test for parameter changes in garch (1, 1) models. Communications in Statistics-Theory and Methods, 29(2):445–462, 2000.

- Kokoszka et al. (2000) Piotr Kokoszka, Remigijus Leipus, et al. Change-point estimation in arch models. Bernoulli, 6(3):513–539, 2000.

- Kulperger et al. (2005) Reg Kulperger, Hao Yu, et al. High moment partial sum processes of residuals in garch models and their applications. The Annals of Statistics, 33(5):2395–2422, 2005.

- Kwan et al. (2005) CK Kwan, WK Li, and K Ng. A multivariate threshold garch model with time-varying correlations. Econometric reviews, 2005.

- Leybourne and McCabe (1989) S. J. Leybourne and B. P. M. McCabe. On the distribution of some test statistics for coefficient constancy. Biometrika, 76(1):169–177, 1989. ISSN 0006-3444. doi: 10.1093/biomet/76.1.169. URL http://dx.doi.org/10.1093/biomet/76.1.169.

- Lin and Teräsvirta (1999) Chien-Fu Jeff Lin and Timo Teräsvirta. Testing parameter constancy in linear models against stochastic stationary parameters. J. Econometrics, 90(2):193–213, 1999. ISSN 0304-4076. doi: 10.1016/S0304-4076(98)00041-4. URL http://dx.doi.org/10.1016/S0304-4076(98)00041-4.

- Lin and Ying (2001) D. Y. Lin and Z. Ying. Semiparametric and nonparametric regression analysis of longitudinal data. J. Amer. Statist. Assoc., 96(453):103–126, 2001. ISSN 0162-1459. doi: 10.1198/016214501750333018. URL http://dx.doi.org/10.1198/016214501750333018. With comments and a rejoinder by the authors.

- Lin et al. (1999) Shinn-Juh Lin, Jian Yang, et al. Testing shifts in financial models with conditional heteroskedasticity: an empirical distribution function approach. School of Finance and Economics, University of Technology, Sydney, 1999.

- Liu and Yang (2016) Rong Liu and Lijian Yang. Spline estimation of a semiparametric garch model. Econometric Theory, 32(4):1023, 2016.

- Nabeya and Tanaka (1988) Seiji Nabeya and Katsuto Tanaka. Asymptotic theory of a test for the constancy of regression coefficients against the random walk alternative. Ann. Statist., 16(1):218–235, 1988. ISSN 0090-5364. doi: 10.1214/aos/1176350701. URL http://dx.doi.org/10.1214/aos/1176350701.

- Neal et al. (2011) Radford M Neal et al. Mcmc using hamiltonian dynamics. Handbook of Markov Chain Monte Carlo, 2(11):2, 2011.

- Ning et al. (2020) Bo Ning, Seonghyun Jeong, Subhashis Ghosal, et al. Bayesian linear regression for multivariate responses under group sparsity. Bernoulli, 26(3):2353–2382, 2020.

- Nyblom (1989) Jukka Nyblom. Testing for the constancy of parameters over time. J. Amer. Statist. Assoc., 84(405):223–230, 1989. ISSN 0162-1459. URL http://links.jstor.org/sici?sici=0162-1459(198903)84:405<223:TFTCOP>2.0.CO;2-W&origin=MSN.

- Ploberger et al. (1989) Werner Ploberger, Walter Krämer, and Karl Kontrus. A new test for structural stability in the linear regression model. J. Econometrics, 40(2):307–318, 1989. ISSN 0304-4076. doi: 10.1016/0304-4076(89)90087-0. URL http://dx.doi.org/10.1016/0304-4076(89)90087-0.

- Ramsay and Silverman (2005) J. O. Ramsay and B. W. Silverman. Functional data analysis. Springer Series in Statistics. Springer, New York, second edition, 2005. ISBN 978-0387-40080-8; 0-387-40080-X.

- Rohan (2013) Neelabh Rohan. A time varying garch (p, q) model and related statistical inference. Statistics & Probability Letters, 83(9):1983–1990, 2013.

- Rohan and Ramanathan (2013) Neelabh Rohan and T. V. Ramanathan. Nonparametric estimation of a time-varying GARCH model. J. Nonparametr. Stat., 25(1):33–52, 2013. ISSN 1048-5252. doi: 10.1080/10485252.2012.728600. URL http://dx.doi.org/10.1080/10485252.2012.728600.

- Roy et al. (2018) Arkaprava Roy, Subhashis Ghosal, Kingshuk Roy Choudhury, et al. High dimensional single-index bayesian modeling of brain atrophy. Bayesian Analysis, 2018.

- Shen and Ghosal (2015) Weining Shen and Subhashis Ghosal. Adaptive bayesian procedures using random series priors. Scandinavian Journal of Statistics, 42(4):1194–1213, 2015.

- Stărică and Granger (2005) Cătălin Stărică and Clive Granger. Nonstationarities in stock returns. The Review of Economics and Statistics, 87(3):503–522, 2005.

- Tse and Tsui (2002) Yiu Kuen Tse and Albert K C Tsui. A multivariate generalized autoregressive conditional heteroscedasticity model with time-varying correlations. Journal of Business & Economic Statistics, 20(3):351–362, 2002.

- Yue et al. (2014) Yu Ryan Yue, Daniel Simpson, Finn Lindgren, Håvard Rue, et al. Bayesian adaptive smoothing splines using stochastic differential equations. Bayesian Analysis, 9(2):397–424, 2014.

- Zhang and Wu (2012) Ting Zhang and Wei Biao Wu. Inference of time-varying regression models. Ann. Statist., 40(3):1376–1402, 2012. ISSN 0090-5364. doi: 10.1214/12-AOS1010. URL http://dx.doi.org/10.1214/12-AOS1010.

- Zhang and Wu (2015) Ting Zhang and Wei Biao Wu. Time-varying nonlinear regression models: nonparametric estimation and model selection. Ann. Statist., 43(2):741–768, 2015. ISSN 0090-5364. doi: 10.1214/14-AOS1299. URL https://doi.org/10.1214/14-AOS1299.

- Zhang et al. (2002) Wenyang Zhang, Sik-Yum Lee, and Xinyuan Song. Local polynomial fitting in semivarying coefficient model. J. Multivariate Anal., 82(1):166–188, 2002. ISSN 0047-259X. doi: 10.1006/jmva.2001.2012. URL http://dx.doi.org/10.1006/jmva.2001.2012.

- Zhou and Wu (2010) Zhou Zhou and Wei Biao Wu. Simultaneous inference of linear models with time varying coefficients. J. R. Stat. Soc. Ser. B Stat. Methodol., 72(4):513–531, 2010. ISSN 1369-7412. doi: 10.1111/j.1467-9868.2010.00743.x. URL http://dx.doi.org/10.1111/j.1467-9868.2010.00743.x.

8 Proof of Theorems

We study the frequentist property of the posterior distribution in increasing regime assuming that the observations are coming from a true density characterized by the parameter . We follow the general theory of Ghosal et al. (2000) to study posterior contraction rate for our problem. In Bayesian framework, the density is itself a random measure and has distribution which is the prior distribution induced by the assumed prior distribution on . The posterior distribution of a neighborhood around given the observation is

8.1 General proof strategy

The posterior consistency would hold if above posterior probability almost surely goes to zero in probability as goes to , where is the true distribution of . Recall the definition of posterior contraction rate; for a sequence if in -probability for every sequence , then the sequence is called the posterior contraction rate. If the assertion is true for a constant , then the corresponding contraction rate becomes slightly stronger.

Note that for two densities characterized by and respectively, the Kullback-Leibler divergences are given by

Assume that there exists a sieve in parameter space such that and we have tests such that

for some . Say and . We can bound the posterior probability from above by,

| (8.1) |

Taking expectation with respect to , first term goes to zero by construction of . The second term goes to zero due to Lemma 8.21 of Ghosal and Van der Vaart (2017) for any sequence . We would require that . Then for the third term,

| (8.2) |

Thus we adhere to the following plan

Plan 4.

The proof had three major parts as follows:

-

(i)

(Prior mass Condition) We need ,

-

(ii)

(Sieve) Construct the sieve such that and

-

(iii)

(Test construction) Construct exponentially consistent tests .

We first study the contraction properties with respect to and then show that the same rate holds for average Hellinger . Note that can be taken as .

8.2 Proof of Theorem 1

For the sake of technical convenience we show our proof by fixing lag order at , however the results are easily generalizable for any fixed order . All the proofs go through for higher lags with the same technical tools.

8.2.1 KL Support

The likelihood based on the parameter space is given by Let be the distribution of with parameter space .

We have

| (8.3) | |||||

where and . Then

| (8.4) |

Our first goal is to estimate these two quantities in terms of the distances between and . In the light of , we bound the expectation of and separately.

Bounding the first term I: Note that, by the means of mean value theorem, for a random variable between and ,

| (8.5) |

where for the first term and is used for the second term due to the assumption (A.2). Thus the first term satisfies

in the light of assumption (A.3).

Bounding the second term II: For the second term we proceed as follows:

where we use the fact that and due to closeness of and . Consequently, we have the deterministic inequality

Taking expectation under truth we arrive at similar upper bound for as since

Thus we conclude that,

| (8.6) |

8.2.2 Posterior contraction in terms of average negative log-affinity

In this section, we focus on the requirements to calculate posterior contraction rate as in Section 4.We first show posterior consistency in terms of average negative log-affinity which is defined as between and . Here, we have . Then we show that, having implies that our distance metric .

Proceeding with the rest of the proof of Theorem 1, we use the results of B-Splines, where and , where such that . The Hölder smooth functions with regularity can be approximated uniformly up to order with many B-splines. Thus we have .

We start by providing a lower bound of the prior probability as required by (i) in Plan 4. We also have the result (8.6) and the prior probabilities based on the discussion of A2 from Shen and Ghosal (2015). The rate of contraction cannot be better than the parametric rate , and so . Thus (i) requires that in terms of pre-rate as . Now we construct a sequence of test functions having exponentially decaying Type I and Type II error. In our problem, we consider following sieve

| (8.7) |

where are at least polynomial in and is the standard deviation of and . We take with , with for technical need.

We need to choose these bounds carefully so that we have , which depend on tail properties of the prior. We have,

where is the vector of full set of coefficients of length and is the vector of coefficients of length . The quantity can be further upper bounded by , for some constant which can be verified from the discussion of the assumption A.2 of Shen and Ghosal (2015) for our choice of exponential prior. On the other hand,

for some constant which can be verified from the proof of Roy et al. (2018). Hence, . The two functions and in the last expression stand for the tail probabilities of the prior of and . We can calculate their asymptotic order as, and . We need . Hence, we calculate pre-rate from the following equation for some sequence ,

| (8.8) |

Now, we construct test such that

for some . To construct the test, we first construct the for point alternative vs . The most powerful test for such problem is Neyman-Pearson test . For , we have

It is natural to have a neighborhood around such the Type II error remains exponentially small for all the alternatives in that neighborhood under the test function . By Cauchy-Schwarz inequality, we can write that

In the above expression, the first factor is already exponentially decaying. The second factor can be allowed to grow at most of order for some positive small constant . We, in fact establish that the second factor is bounded by our choice of the sieve through the following claim.

Claim 5.

is bounded for every such that

| (8.9) |

Proof.

We have, in the light of AM-GM inequality,

| (8.10) |

Towards uniformly bounding the summand, we first compute and provide a deterministic upper bound to the conditional expectation of the same given . Denote and . Note that if , then

| (8.11) |

Now since

due to the definition of sieve at (8.2.2), we have in the light of assumption (8.9), . Assumption (8.9) allows us to bound the summand in (8.10) before expectation as well. Note that, in the light of (8.9), for large , we have the deterministic inequality

∎

The test function satisfying exponentially decaying Type I and Type II probabilities is then obtained by taking maximum over all tests ’s for each ball, having above radius. Take . Type I and Type II probabilities are given by and . Hence, we need to show that , where is the required number of balls of above radius needed to cover our sieve . We have

| (8.12) |

where are defined in (8.9). Given our choices of and , the two radii and are some fractional polynomials in . Thus which is required to be as in the prior mass condition. Based on (8.8), we have

and a pre-rate

The actual rate will be slower that pre-rate. Now, the covering number condition, prior mass conditions and basis approximation give us and . Combining all these conditions, we calculate the posterior contraction rate equal to

8.2.3 Posterior contraction in terms of average Hellinger

Write Reyni divergence as

We need to show implies that as goes to zero. If , we have which implies for small , we have . By Cauchy-Squarz inequality . Thus we have,

Since

Thus . Thus it is consistent under average Hellinger distance.

8.3 Proof of Theorem 2

Note that, the proof of Theorem 2 follows via exactly same route. We just jot down the important differences from the proof of Theorem 1. For Theorem 2 also, we restrict ourselves to tvGARCH(1,1) situation with the assurance that the proof easily extends to a general tvGARCH(p,q) case.

8.3.1 KL support

Note that the KL support step from subsubsection 8.2.1 follows almost similarly with the modified

To our advantage, we also have the lower bound for the additional function from assumption B.2. First we point out the proof is not exactly straightforward by adding an additional radii for the coefficient since the third term in the above expression of also involves which has evolved differently for and . We begin by estimating the difference of the third term

| (8.13) |

This leads to the recursion

We have

As ,

which will be used for bounding the terms and in (8.3). Towards bounding the first term , we have, along the lines of (8.5),

For bounding the second term , however, we first look at the summand as follows

Taking sum over , we have

Combining the bounds for and we arrive at

| (8.15) |

In the next part we modify the construction of the sieve to suit the tvGARCH structure.

8.3.2 Construction of exponentially consistent tests

For the part where we construct exponentially consistent test, note that the only challenge that remains for GARCH processes is to obtain a claim as Claim 5. Towards that, we use a new definition of sieve in the light of (8.2.2) as following:

| (8.16) |

where are at least polynomial in and is the standard deviation of and . We take with , for sufficiently large such that .

Claim 6.

is bounded for every such that

| (8.17) |

where .

Proof.

Within the sieve again we use a variant of above inequality.

By recursion,

| (8.18) |

where . The RHS is increasing in and thus we only need to find a bound for . and are chosen in such a way that . Based on that , and can be chosen. We also choose . Note that, with how we choose above, for which means for large , such choices of are valid. Finally we make the choices for radii as for .

The equivalence of Reyni divergence and Hellinger is exactly same as shown in Subsubsection 8.2.3.

8.4 Proof of Theorem 3

We prove Theorem 3 along very similar lines as outlined for Theorem 2. The only difference pops up in the KL difference step where existence of second moment is necessary but unfortunately for the tviGARCH case, the variance is infinite. Thus we handle the KL bound in a different way.

Our goal is to obtain a deterministic bound on . Denoting by we have

| (8.20) | |||||

where . In the first inequality of the above derivation, we have used satisfies the following

| (8.21) |

and and thanks to the closeness of with . For the third term, we have bounds on as follows . Consequently,

by a Taylor series approximation of the binomial term in the third line since is small. This along with (8.20) leads to the following bound

Note that for bounding in the KL term from (8.3), satisfy the exact same bounds as (8.4). For term as well the bounds follow along the lines of (8.3.1).

We consider following sieve for iGARCH:

| (8.22) |

Within the sieve,

Along the line of Claim 5 and Claim 6, the rest of the proof goes through if the radii satisfy , and .