Regularized Solutions to Linear Rational Expectations Models111Thanks are due to Thomas Lubik, Davide Debortoli and Fei Tan for helpful comments and suggestions.

Abstract

This paper proposes an algorithm for computing regularized solutions to linear rational expectations models. The algorithm allows for regularization cross-sectionally as well as across frequencies. A variety of numerical examples illustrate the advantage of regularization.

JEL Classification: C62, C63, E00.

Keywords: Linear rational expectations model, regularization, indeterminacy, computational methods.

1 Introduction

Recently, Al-Sadoon (2020) showed that non-unique solutions to multivariate linear rational expectations models (LREMs) are not generally continuous with respect to their parameters, invalidating crucial assumptions for both frequentis and Bayesian methods. For frequentist analyses, the objective function (e.g. the likelihood function) has to be at least continuous. For Bayesian analysis, the posterior cannot have atoms at unknown locations. Al-Sadoon (2020) demonstrated that these two conditions are not guaranteed under current methodology and proposed a regularization solution.

Regularization is a method for selecting from among infinitely many solutions to an LREM a unique solution that accords with prior information that the researcher may have about what a solution should look like (e.g. that its spectral density should concentrate in the range of observed business cycles). Al-Sadoon (2020) provided a theoretical analysis of regularizaiton. The aim of this paper is to provide an algorithm for computing such solutions based on the Sims (2002) framework.

This work is related to several more recent works. The main result of this paper builds on Lubik & Schorfheide (2003) and Al-Sadoon (2018). Farmer et al. (2015) and Bianchi & Nicolò (2019) provide alternative parametrizations of solutions to LREMs to Lubik & Schorfheide (2003). Funovits (2017) counts the dimension of the solution space to a given LREM. This paper can also be seen as part of the recent interest in frequency domain analysis of LREMs as exemplified by Onatski (2006), Tan & Walker (2015), and Tan (2019). Such methods have found important applications in addressing the identification problem for LREMs as seen in Komunjer & Ng (2011), Qu & Tkachenko (2017), Kociecki & Kolasa (2018), and Al-Sadoon & Zwiernik (2019).

This paper is organized as follows. Section 2 reviews results of Sims (2002) and Lubik & Schorfheide (2003). Section 3 shows how regularization can be achieved and provides the main result of this paper. Section 4 provides illustrative examples of how regularization works. Section 5 concludes. The Matlab code for reproducing the computations presented in this paper can be found in the accompanying file, regular.zip.

2 Review

We begin by reviewing results developed by Sims (2002) and Lubik & Schorfheide (2003). This is necessary in order to set the notation and obtain the basic ingredients that we will need. Because regularization is only defined in a stationary context, we will restrict attention to covariance stationary solutions.

Definition 1.

Given , an -dimensional i.i.d. process of mean zero and finite and positive definite variance matrix, and the formal LREM

| (1) |

a solution to (1) is a pair such that:

-

(i)

is an -dimensional process such that is measurable with respect to for all .

-

(ii)

is a -dimensional martingale difference sequence with respect to . That is, is measurable with respect to and almost surely for all , where .

-

(iii)

The process is jointly covariance stationary.

-

(iv)

The pair satisfies equations (1) almost surely.

A solution is unique if for every other solution , almost surely for all . (For ease of exposition, we will drop the “almost surely” in the subsequent analysis).

Assuming, as Sims (2002) does, that is not identically zero (i.e. it is impossible to cancel out by elementary algebraic operations), then by Theorem VI.1.9 and Exercise VI.1.3 of Stewart & Sun (1990), there are orthogonal matrices such that and are block upper triangular with either or blocks on the diagonal. Under the stronger assumption that for all with (i.e. the aforementioned cancellation is impossible and there are no unit roots in the system), then these matrices can be partitioned conformably as

| (2) |

where the polynomial has all its zeros outside the unit circle (this implies that is non-singular), and the polynomial has all its zeros inside the unit circle (this implies that is non-singular). As shown in the online appendix to Al-Sadoon (2018), this step is an implicit Wiener-Hopf factorization. Note that Sims (2002) and Lubik & Schorfheide (2003) use the complex QZ decomposition but never explain how the final answer is real; using the real QZ decomposition obviates any need for such a discussion.

Now suppose is a solution to (1), define , and rewrite the system as

If we partition

conformably with (2), then

| (3) |

where

is partitioned conformably with (2). Applying the conditional expectation we obtain

This implies that

Therefore,

where we have used the fact that (Williams, 1991, Theorem 9.7). The covariance stationarity of implies that . Since our choice of QZ decomposition ensures that the eigenvalues of are inside the unit circle, for large enough and then it must be the case that . Therefore,

Now plugging this back into (3) we have that

Multiplying on the right by , taking expectations, and utilizing the joint covariance stationarity of and , we arrive at

But since is invertible by assumption, a necessary condition for existence is

| (4) |

It also follows that

where is the Moore-Penrose generalized inverse of , and

Thus, for a given matrix whose columns form a basis for there is a martingale difference sequence with respect to , denoted by , such that

Every solution is therefore representable as

| (5) |

with

Note that inters into the system along independent directions, what Funovits (2017) calls the dimension of indeterminacy.

In fact, (4) is not only necessary but also sufficient for existence. To see this, simply construct the pair from (5) with set to the zero process; it is easily checked that this pair is a solution to (1).

Turning now to uniqueness, we see that the arbitrary plays no role in the solution if and only if or, equivalently, if and only if , which can be expressed as

| (6) |

Since (5), generated with for defines a solution for any matrix , it must be that (6) is necessary and sufficient for uniqueness. Note that Sims (2002) expresses (6) equivalently in terms of the row spaces of and .

To summarize, we have proven the following.

3 Regularization

Current methodology utilizes (5) or variants thereof. Al-Sadoon (2020) has demonstrated that these solutions can be discontinuous (as we will see shortly) and proposed using regularized solutions to ensure continuity. We now turn to the problem of computing such solutions.

We begin with the basic setting. Suppose a symmetric positive semi-definite matrix is given and we are interested in selecting among all solutions to (1), one that minimizes

If the solution to (1) is unique, there is nothing to solve for. If not, it will be convenient in the subsequent computations to introduce the martingale difference sequence, , defined as

The process is the residual from regressing on . This implies that

where and . Thus, finding a regularized solution is equivalent to minimizing

with respect to and . Using the properties of the trace of a produce of matrices,

where

Note that is the unique solution to the Lyapunov equation

See Section B.1.8 of Lindquist & Picci (2015). Taking the gradient of , we obtain the following first order conditions

If is invertible, there exists a unique regularized solution determined by

If is not invertible, there are infinitely many regularized solutions determined by

for arbitrary and of the appropriate sizes such that .

We have established the following. First, a regularized solution to (1) exists if and only if solutions to (1) exist. Second, the regularized solution is unique if and only if either the solution to (1) is unique, in which case the regularized solution is the unique solution,

| (7) |

or is invertible, in which case the regularized solution has the representation,

| (8) |

where

The intuition of this result is quite simple. Write

Now if is of full column rank, then the regularized solution is unique. That is, if attaches non-trivial weight to every contemporaneous instance of indeterminacy, then regularization eliminates indeterminacy. More generally, we have proven that regularization eliminates indeterminacy if and only if attaches non-trivial weight to every instance of indeterminacy whether contemporaneous or lagged. From a linear systems point of view, regularization leads to uniqueness if and only if the triple is input observable (Sain & Massey, 1969), which is to say, again, that the weight matrix detects all of the indeterminacy in the system.

The analysis above suggests a generalization of the basic setting. We have constructed an algorithm for minimizing

where is the spectral density of . The above expression allows us to choose different weights along the cross-section of . More generally, we may consider choosing weights on frequencies of oscillation of . In particular, we may consider minimizing

| (9) |

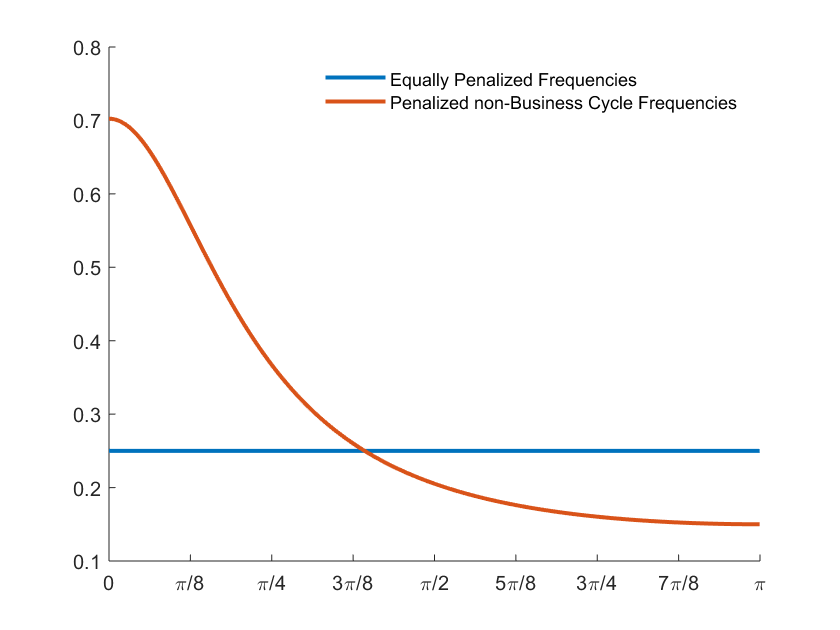

where is a bounded measurable function, with Hermitian positive semi definite and for all . If, for example, we like to impose that the solution should display the frequency characteristics of the business cycle, we could choose

which penalizes oscillations of period smaller than a year and greater than eight years in quarterly data. To that end, we first note that

This implies that

where

It is easily checked that is a real symmetric positive semi definite matrix and that it reduces to our previous expression when is constant. Following the same line of argument as above, we arrive finally at the main result of the paper.

4 Examples

4.1 The Cagan Model

Consider first, the Cagan model with mean zero, independent, and identically distributed shocks

There are infinitely many solutions to this system. To compute the regularized solution minimizing , we reformulate this model as

with

This implies that

Solving for the first element, we obtain , which was obtained analytically in Al-Sadoon (2020). This regularized solution is actually a white noise process and therefore has a flat spectral density. We may instead impose that the solution avoid empirically unlikely frequencies. If we use the weight matrix

we obtain a different regularized solution with the spectral density plotted in the Figure 1.

4.2 A New Keynesian Model

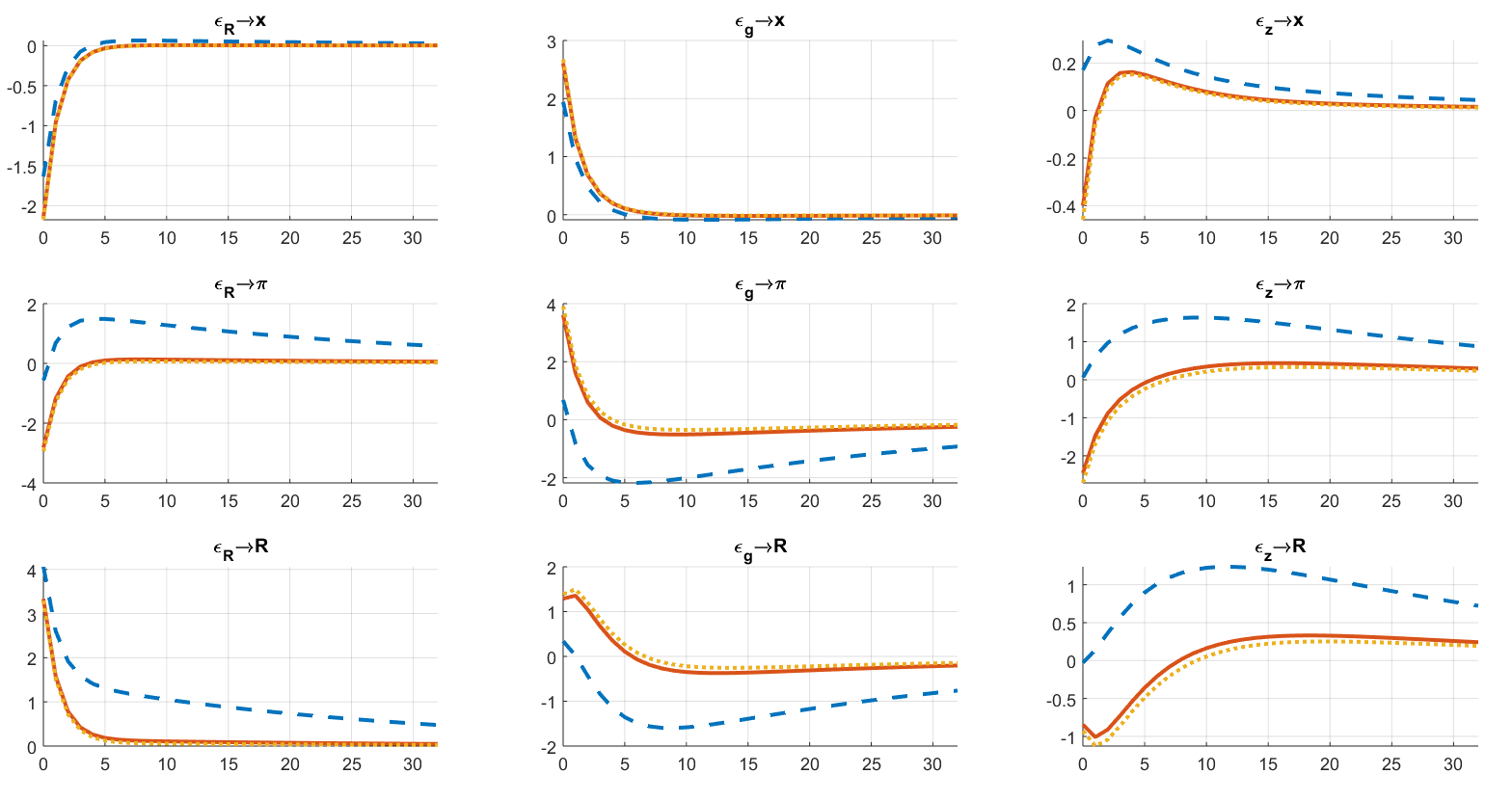

Consider next the New Keynesian model of Lubik & Schorfheide (2004).

The model is calibrated using Lubik & Schorfheide’s estimates reported in their Table 3 in the column titled “Pre-Volcker (Prior 1)”. Figure 2 plots the impulse responses of the first three variables to the three shocks. The impulse responses are generated from the non-regularized solution, the solution regularized with constant weight matrix with equal weights on the first three variables, and the solution regularized with a variable weight matrix emphasizing business cycle frequencies in the first three variables.

Clearly, regularization produces more stable dynamics. Unlike the case in Figure 1, however, regularizing by constant and variable weight matrices did not produce dramatically different results.

Dashed: non-regularized solution. Continuous: constant weight matrix. Dotted: variable weight matrix.

4.3 A Non-generic System

Consider now the system

The shocks are again zero mean, independent, and identically distributed. This system also has infinitely many solutions. Although it is simple, it concretely illustrates the failure of current methodology to account for discontinuity of solutions to LREMs. Al-Sadoon (2020) demonstrates its discontinuity analytically and studies its Gaussian likelihood function. We will now demonstrate its discontinuity numerically.

In order to reformulate this system into the form (1), we use the second equation to obtain

and then combine this equation with the first equation of the original system to obtain

This system is equivalent to the original one, provided . We can now set

with

The weight matrix is

For , the first three impulse responses of the non-regularized solution are

Clearly, these are quite far from the impulse responses of the model, which ought to be

On the other hand, the first three impulse responses of the regularized solution are

The continuity of regularized solutions is proven in Theorem 6 of Al-Sadoon (2020).

5 Conclusion

This paper has provided an algorithm for computing regularized solutions to LREMs. This work suggests at least three venues for further investigation. First, it is likely that regularization helps resolve identifiability issues in LREMs due to its imposition of uniqueness but since it is strictly more general than the class of solutions considered in Al-Sadoon & Zwiernik (2019) its identifiability requires separate examination. Second, the algorithm presented here is given without any claim to efficiency; it would be helpful to consider other methods of obtaining regularized solutions and compare their accuracy and speed. Finally, recent work has sought to relax the assumption that the information set includes all exogenous variables (e.g. Huo & Takayama (2015), Rondina & Walker (2017), Angeletos & Huo (2018), and Han et al. (2019)); regularization in that context would be a fruitful venue for follow up work.

References

- Al-Sadoon (2018) Al-Sadoon, M. M. (2018). The linear systems approach to linear rational expectations models. Econometric Theory, 34(03), 628–658.

- Al-Sadoon (2020) Al-Sadoon, M. M. (2020). The spectral approach to linear rational expectations models. arXiv preprint arXiv:2007.13804.

- Al-Sadoon & Zwiernik (2019) Al-Sadoon, M. M. & Zwiernik, P. (2019). The identification problem for linear rational expectations models. arXiv preprint arXiv:1908.09617.

- Angeletos & Huo (2018) Angeletos, G.-M. & Huo, Z. (2018). Myopia and anchoring. Technical report, National Bureau of Economic Research.

- Bianchi & Nicolò (2019) Bianchi, F. & Nicolò, G. (2019). A Generalized Approach to Indeterminacy in Linear Rational Expectations Models. Finance and Economics Discussion Series 2019-033, Board of Governors of the Federal Reserve System (U.S.).

- Farmer et al. (2015) Farmer, R. E., Khramov, V., & Nicolò, G. (2015). Solving and estimating indeterminate DSGE models. Journal of Economic Dynamics and Control, 54(C), 17–36.

- Funovits (2017) Funovits, B. (2017). The full set of solutions of linear rational expectations models. Economics Letters, 161, 47 – 51.

- Han et al. (2019) Han, Z., Tan, F., & Wu, J. (2019). Analytic policy function iteration. Available at SSRN 3512320.

- Huo & Takayama (2015) Huo, Z. & Takayama, N. (2015). Higher order beliefs, confidence, and business cycles. Report, Yale University.[1, 2].

- Kociecki & Kolasa (2018) Kociecki, A. & Kolasa, M. (2018). Global identification of linearized DSGE models. Quantitative Economics, 9(3), 1243–1263.

- Komunjer & Ng (2011) Komunjer, I. & Ng, S. (2011). Dynamic identification of dynamic stochastic general equilibrium models. Econometrica, 79(6), 1995–2032.

- Lindquist & Picci (2015) Lindquist, A. & Picci, G. (2015). Linear Stochastic Systems: A Geometric Approach to Modeling, Estimation, and Identification. Series in Contemporary Mathematics 1. Berlin Heidelberg: Springer-Verlag.

- Lubik & Schorfheide (2003) Lubik, T. A. & Schorfheide, F. (2003). Computing sunspot equilibria in linear rational expectations models. Journal of Economic Dynamics and Control, 28(2), 273 – 285.

- Lubik & Schorfheide (2004) Lubik, T. A. & Schorfheide, F. (2004). Testing for indeterminacy: An application to u.s. monetary policy. American Economic Review, 94(1), 190–217.

- Onatski (2006) Onatski, A. (2006). Winding number criterion for existence and uniqueness of equilibrium in linear rational expectations models. Journal of Economic Dynamics and Control, 30(2), 323–345.

- Qu & Tkachenko (2017) Qu, Z. & Tkachenko, D. (2017). Global identification in DSGE models allowing for indeterminacy. The Review of Economic Studies, 84(3), 1306–1345.

- Rondina & Walker (2017) Rondina, G. & Walker, T. (2017). Confounding dynamics. Technical report, Working paper.

- Sain & Massey (1969) Sain, M. & Massey, J. (1969). Invertibility of linear time-invariant dynamical systems. IEEE Transactions on Automatic Control, 14(2), 141–149.

- Sims (2002) Sims, C. A. (2002). Solving linear rational expectations models. Computational Economics, 20(1), 1–20.

- Stewart & Sun (1990) Stewart, G. W. & Sun, J. (1990). Matrix Perturbation Theory. New York, USA: Academic Press, Inc.

- Tan (2019) Tan, F. (2019). A frequency-domain approach to dynamic macroeconomic models. Macroeconomic Dynamics, 1–31.

- Tan & Walker (2015) Tan, F. & Walker, T. B. (2015). Solving generalized multivariate linear rational expectations models. Journal of Economic Dynamics and Control, 60, 95–111.

- Williams (1991) Williams, D. (1991). Probability with Martingales. Cambridge, UK: Cambridge University Press.