Constant Regret Re-solving Heuristics for Price-based Revenue Management

Abstract

Price-based revenue management is an important problem in operations management with many practical applications. The problem considers a retailer who sells a product (or multiple products) over consecutive time periods and is subject to constraints on the initial inventory levels. While the optimal pricing policy could be obtained via dynamic programming, such an approach is sometimes undesirable because of high computational costs. Approximate policies, such as the re-solving heuristics, are often applied as computationally tractable alternatives. In this paper, we show the following two results. First, we prove that a natural re-solving heuristic attains regret compared to the value of the optimal policy. This improves the regret upper bound established in the prior work of Jasin (2014). Second, we prove that there is an gap between the value of the optimal policy and that of the fluid model. This complements our upper bound result by showing that the fluid is not an adequate information-relaxed benchmark when analyzing price-based revenue management algorithms.

Keywords: re-solving, self-adjusting controls, price-based revenue management, dynamic pricing

1 Introduction

We study a classic price-based revenue management problem where a retailer sells either a single product or a group of products over a finite horizon given fixed initial inventory (Gallego and Van Ryzin 1994, 1997). More specifically, consider products and consecutive selling periods with an initial inventory level . At time , the retailer posts a price vector . Suppose is a fixed demand function. Let be a filtered probability space. The realized demand , realized revenue , and remaining inventory level at the end of period are governed by

| (1) |

where is a martingale difference sequence adapted to the filtration (see Sec. 3 for detailed assumptions.)

The retailer’s objective is to design an admissible pricing policy to maximize the expected revenue over the periods. A pricing policy can be represented by , where is a mapping from the inventory level to the price . A pricing policy is admissible or non-anticipating if the posted price only depends on the history up to the end of period , namely, is measurable with respect to . Given the initial inventory level , the expected revenue of an admissible policy is denoted by

| (2) |

1.1 Existing Results on the Fluid Model and the Re-solving Heuristic

An optimal policy maximizing defined in Eq. (2) can be in principle obtained via dynamic programming (DP). However, it is well known that the exact DP algorithm suffers from the curse of dimensionality, as the (discretized) state space grows exponentially in size with the number of products.

The seminal work of Gallego and Van Ryzin (1994) proposed a fluid approximation model of the optimal dynamic pricing problem. To define the fluid model, suppose there exists an inverse function of the demand rate function of . Let be the mean revenue in one period given the price vector . We assume is strictly concave and smooth on its domain (see Sec. 3 and Sec. 6 for the statements of these assumptions). The fluid model for the dynamic pricing problem is

| (3) | ||||

| s.t. |

Let and denote the optimal value and the (unique) optimal solution of the fluid model, respectively. The optimization problem (3) chooses a demand rate (or equivalently, setting the price to ) such that the revenue function is maximized subject to the initial inventory constraint. Intuitively, the fluid approximation model ignores the randomness caused by demand noises and replaces the stochastic inventory constraint with a deterministic constraint.

Theorem 1 (Gallego and Van Ryzin (1994, 1997)).

For any admissible policy and the initial inventory level , the expected revenue is upper bounded by . Furthermore, for a static pricing policy such that , the expected revenue is lower bounded by .

However, the main drawback of the static pricing policy is that it is not adaptive to demand randomness. Researchers have proposed various approaches to modify the static pricing policy, aiming to improve the gap in Theorem 1 (see Sec. 2 for a survey). One intuitive approach is to re-solve the fluid model in every period using the current inventory level:

| s.t. |

where is the normalized inventory level realized at the beginning of period . Let the solution to the above problem be (the superscript stands for “constrained”). The price is then reset to at the start of period . We will refer to this policy as the re-solving heuristic. In the work of Jasin (2014), the gap is reduced from to by using the re-solving heuristic, as shown by the following result.

1.2 Our Results: Constant Regret and Logarithmic Gaps

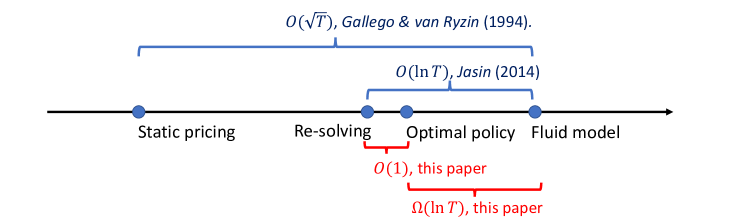

In this paper we establish two main results: constant regret for the re-solving heuristic, and a logarithmic regret lower bound on the gap between the value of the optimal pricing policy and the fluid model. Figure 1 summarizes results established in this paper and compares them with existing results in the prior literature.

Our first main result, as stated in Theorems 3 and 5 later in the paper, asserts that for any initial inventory level (except for certain boundary cases), the cumulative regret of the re-solving heuristic is upper bounded by a constant that is independent of , compared against the expected reward of the optimal dynamic pricing policy . Apart from the obvious improvement from to in regret bound, our proof technique is quite different from existing work that compares the expected reward of the re-solving policy to a certain information relaxed benchmark, such as the fluid model or the hindsight optimum benchmark. Instead, we compare the value of directly with the value of the optimal DP policy by carefully analyzing the stochastic inventory levels under the two policies.

Our second main result, as stated in Theorem 4 later in this paper, shows that there is an lower bound on the gap between the expected revenue of the re-solving heuristics and the optimal objective of the fluid model . Coupled with the regret upper bound established in Theorem 3, this shows that there is an lower bound on the gap between the value of the optimal policy and the fluid model as well. This demonstrates a fundamental limitation of using the fluid model as a benchmark to analyze the regret for the price-based revenue management problem.

2 Related Work

The idea of using simple, easy-to-compute pricing policies to approximate optimal dynamic pricing policies originates from Gallego and Van Ryzin (1994, 1997), who proposed a static price policy using fluid models and established regret. Later, Maglaras and Meissner (2006) showed that the re-solving heuristic has regret in the single resource case. The most relevant prior research to our paper is the work by Jasin (2014), who studied a price-based network revenue management problem and showed that re-solving heuristics attain asymptotic regret upper bound under mild conditions. Jasin (2014) also showed that infrequent re-solving has similar theoretical performance guarantees and is much more computationally efficient. In this paper, we improve the regret of the re-solving heuristic to an constant bound that is independent of . Our analysis is different from the one in Jasin (2014) in the sense that we directly compare the expected revenue of re-solving with the value of the optimal DP policy, instead of the fluid model. Additionally, we complement the result in Jasin (2014) by establishing an lower bound between the expected revenue of the optimal DP policy and the fluid model.

Re-solving heuristics have also been studied in quantity-based revenue management (Cooper 2002, Reiman and Wang 2008, Secomandi 2008, Jasin and Kumar 2013, Bumpensanti and Wang 2020). The decisions involved in a quantity-based revenue management problem are the opening and closing of available products, so the feasible decisions form a discrete set. In contrast, the price-based revenue management model studied in this paper assumes continuous prices in an infinite set. When the decision set is discrete, re-solving the fluid model will lead to fractional solutions that require rounding; it is shown that the design of the rounding procedures (e.g. by randomization, thresholding, etc.) plays a critical role in the performance of re-solving heuristics (Arlotto and Gurvich 2019, Bumpensanti and Wang 2020, Vera and Banerjee 2020). When the decision set is continuous, re-solving algorithms must precisely track the updated inventory level in the fluid model without using any rounding. As such, analysis for the (continuous) price-based revenue management problem is much different from the previous proofs for quantity-based revenue management. Moreover, existing proofs of constant regret in the quantity-based model often use an information relaxation bound called hindsight-optimum benchmark (see Appendix for a detailed discussion). However, the hindsight-optimum benchmark does not readily translate to the price-based revenue management setting, and our analysis does not rely on such a benchmark. It is worth mentioning that Vera et al. (2019) proposed a constant regret algorithm that works for both quantity-based and price-based revenue management problems. However, the price-based revenue management model considered in Vera et al. (2019) assumes a single product and a finite set of candidate prices. Because a finite set of prices implies that the feasible decision set has a discrete structure, the pricing setting studied in Vera et al. (2019) is significantly different from this paper. In fact, Maglaras and Meissner (2006) showed that a single-resource revenue management problem with discrete prices is equivalent to a quantity-based revenue management problem.

In this paper, we restrict our attention to stationary demand. Several other papers studied revenue management problems with non-stationary, time-correlated, or arbitrary demand sequences (e.g. Chen and Farias 2013, Ma et al. 2020, Ma and Simchi-Levi 2020). Revenue management problems with non-stationary demand are harder and therefore these papers consider different performance metrics such as approximation ratios or competitive ratios rather than regret. Chen and Farias (2013) studied a dynamic pricing problem under a general non-stationary demand setting. They showed that re-solving heuristics can achieve constant competitive ratios, whereas static pricing policies have asymptotically diminishing competitive ratios. Due to different model assumptions, the results in Chen and Farias (2013) are not directly comparable to ours.

Another stream of related literature studies dynamic pricing with demand learning, where the underlying demand function is unknown and needs to be learned on the fly from sales data. Many papers consider demand learning settings using the price-based finite-inventory revenue management model from Gallego and Van Ryzin (1994) as the ground truth model (e.g., Aviv and Pazgal 2005, Besbes and Zeevi 2009, 2012, Wang et al. 2014, Lei et al. 2014, den Boer and Zwart 2015, Ferreira et al. 2018). Re-solving heuristics have also been applied to demand learning algorithms (Jasin 2015, Ferreira et al. 2018). In contrast, our paper assumes that the retailer has full information about the demand curve and demand distributions, so we are able to show regret, which is tighter than typical regret bounds in the learning literature. Also, the lower bound result in this paper (Theorem 4) is proved using different techniques from lower bound proofs in the learning setting (e.g. Broder and Rusmevichientong 2012, Wang et al. 2020), as the latter relies on information-theoretical lower bounds.

3 Main Results

In this section, we consider a price-based revenue management problem with a single product. The extension to multiple products is deferred to Sec. 6. Although some of the results in this section are special cases of those in Sec. 6, presenting the single-product model helps illustrate the key insight of our analysis. We make the following assumptions on the single-product demand model.

-

A1.

(Monotonicity) The demand rate function is strictly decreasing with , . (We allow the case or .) Note that this implies the existence of the inverse function on .

-

A2.

(Strict Concavity) The expected revenue as a function of the demand rate is strictly concave. There exists a positive constant such that for all . The maximizer of is in the interior of the domain, i.e., .

-

A3.

(Smoothness) The third derivative of exists and satisfies for all . Furthermore, there exists a constant such that for all .

-

A4.

(Martingale Difference Sequence) Conditional on the price (), the demand noise is independent of and satisfies The conditional distribution of given is denoted by . In addition, for some constant .

-

A5.

(Wasserstein Distance) There exists a constant such that for any , it holds that , where is the -Wasserstein distance between , with being an arbitrary joint distribution with marginal distributions being and , respectively.

Assumptions (A1)–(A3) are standard assumptions for the price-based revenue management problem (Gallego and Van Ryzin 1994, Jasin 2014). In particular, the strict concavity of stems from the economic principle of diminishing marginal returns. Assumption (A4) allows demand noise to have general dependence on the price. Assumption (A5) states that if two prices are close to each other, then the demand noises given these prices should also have similar distributions. This assumption is satisfied when the demand distribution is modeled by a parametric family of distributions (e.g., Bernoulli, binomial, truncated normal) whose parameters depend continuously on price.

3.1 Constant Regret of the Re-solving Heuristic

Let and be the unconstrained optimal revenue rate and its maximizer, respectively. Because is strictly concave, in the case of a single product, it is easily verified that the unique optimal solution to the fluid model is equal to and hence the fluid optimal price is .

When the normalized initial inventory level exceeds the (unconstrained) optimal demand rate , it is easy to verify that both the static policy and the re-solving heuristic have constant regret.

Proposition 1.

Suppose . Let be the static pricing policy. Then . In addition, the re-solving heuristic satisfies .

Proof.

Proof of Proposition 1. For any , let be the normalized inventory level in period . The static pricing policy commits to the price . If , the re-solving heuristic also selects the price . Let denote either the static pricing policy or the re-solving heuristic . Let be the event that the inventory level never drops below from the start to the beginning of period . Then, we have

where the first equality uses the fact that is a martingale difference sequence and . By Doob’s martingale inequality, for any , we have

Thus, . The proof is complete by noting that using Theorem 1. ∎

However, analysis for the limited inventory case is much more complicated. The static price policy typically suffers regret in this case. The work by Jasin (2014) established that the regret of the re-solving heuristic when measured against the fluid benchmark is at most . (Note that the “positive dual variable” assumption in Jasin (2014) (see Theorem 2) is equivalent to the condition in the single product case.) Our next theorem improves the regret of to a constant.

Theorem 3.

Suppose . Let be the re-solving heuristic and be the optimal policy. For , it holds that .

Theorem 3 is the main result of this section and its proof is given in Sec. 4. Unlike the previous results by Gallego and Van Ryzin (1994) and Jasin (2014), Theorem 3 compares the expected revenue of directly with the optimal DP pricing policy , rather than comparing it with the fluid approximation value . This allows for tighter regret bounds. In fact, it is impossible to obtain regret using the fluid model as a benchmark, as we shall establish in the next subsection.

In light of Proposition 1 and Theorem 3, we know that the re-solving heuristic has constant regret either in the sufficient inventory case () or in the limited inventory case (). The only remaining scenario is the boundary case (). We will investigate this scenario using numerical experiments in Sec. 5. Our numerical result indicates that does not have constant regret in the boundary case. This observation is analogous to the situation for the quantity-based revenue management problem, where the re-solving heuristic has constant regret when the fluid model (a linear program) has non-degenerate solutions but does not have constant regret in certain boundary cases when the fluid model has degenerate solutions (Jasin and Kumar 2012, Bumpensanti and Wang 2020).

3.2 Logarithmic Gap of the Fluid Model Benchmark

In this section, we show that in the limited inventory case (), the regret of the re-solving policy measured against the fluid approximation value can be at least .

Theorem 4.

Suppose and let be the re-solving policy defined in Theorem 2. Suppose there exists such that for any . For sufficiently large , it holds that .

Theorem 4 is proved in Sec. 4. It implies that the logarithmic regret by Jasin (2014) (see Theorem 2 above), which uses the fluid model benchmark, is tight and cannot be improved. Because by Theorem 3, Theorem 4 also shows that there is an logarithmic gap between the value of the optimal DP pricing policy and the fluid approximation value. This is why our constant regret analysis does not use the fluid model as the benchmark.

Prior work on the quantity-based revenue management problem (Reiman and Wang 2008, Bumpensanti and Wang 2020, Vera et al. 2019) also considered different regret benchmarks that are tighter than the fluid model, including various versions of the “hindsight optimum” benchmark. The “hindsight optimum” model assumes a clairvoyant who knows the aggregate realized demands for the entire horizon at the start. In the Appendix of this paper, we show that one version of the hindsight optimum benchmark proposed by Vera et al. (2019) has regret when measured against the fluid approximation benchmark. By Theorem 4, this hindsight optimum benchmark is also away from the value of the optimal DP policy.

4 Proofs

Before presenting our proof, we first define some notations. For convenience, throughout this section, time indices are counted backwards: time index occurs when there are periods until the end of the selling horizon. Let and be the expected cumulative revenue of the optimal DP pricing policy and the re-solving policy , respectively, when there are remaining periods and units of remaining inventory. For , let and be the normalized inventory levels under policy and , when there are time periods remaining. These notations are summarized in Table 1, with some additional notations being defined later in the proof.

| Notation | Definition | Meaning |

|---|---|---|

| the optimal demand rate without inventory constraints | ||

| reward of with periods and inventory | ||

| reward of re-solving with periods and inventory | ||

| -algebra of | all the events known at the end of period | |

| remaining inventory divide by | normalized inventory levels under policy and | |

| see Eq. (4) | the optimal demand correction with periods remaining | |

| harmonic series of demand corrections up to | ||

| , | the stochastic demand noises at time under | |

| demand noises up to , under and | ||

| difference in harmonic demand noise series | ||

| joint distribution over | the joint distribution that minimizes | |

| see Eq. (7) | stopping time such that is well-behaved |

The rest of this section is organized as follows. In the first subsection we establish some properties of the optimal policy and the re-solving policy . More specifically, we establish upper and lower bounds of the expected rewards using the key quantities of (harmonic series of optimal demand corrections), (harmonic series of stochastic noise variables) and (a stopping time until which the demand noise process is well-behaved). We then proceed with the proofs of Theorems 3, 4 by carefully analyzing the differences in the Taylor expansions of .

4.1 Properties of the Optimal Policy and the Re-solving Heuristic

For any , let the random variable be the normalized inventory level (i.e., remaining inventory divided by remaining time) at period under policy . Let and be the actual inventory levels when and time periods are remaining. If the policy selects the demand rate , we have , which implies . Therefore, the value of the optimal policy is given by the following Bellman equation:

Let denote the maximizer of the above equation. Let be the realized demand noise, which is drawn from the distribution (by Assumption (A4)). The normalized inventory level in the next period is . The Bellman equation can be rewritten as

| (4) |

The above equation implies , but we remark that it does not required to be in the domain .

For any , let and be the harmonic series of demand noises up to time under the optimal policy. For , we also define . It then holds that

| (5) |

Next, we consider the re-solving heuristic . For any , let the random variable be the normalized inventory level under the re-solving heuristic. If , the re-solving heuristic selects the price . Let be the realized demand noise under this price, which is drawn from the distribution . The normalized inventory level in the next period is equal to . Thus, the value of the re-solving policy can be written as

| (6) |

Note that Eq. (6) does not hold for , in which case the re-solving policy would commit to the unconstrained optimal demand rate instead of . This motivates the definition of a certain stopping time in Eq. (7) below, which ensures that Eq. (6) holds for all . Comparing Eq. (6) with Eq. (4), we remark that the re-solving heuristics can be viewed a special case of the dynamic programming policy with the decision rule restricted to for all .

Define a time index as

| (7) |

where is the harmonic series of demand noises under the re-solving policy. Note that is a function of and measurable with respect to , so is indeed a stopping time. Because of the bound holds for all , we have

| (8) |

Intuitively, is the first time that the inventory level in the next period falls outside of the interval . In other words, the inventory levels of the re-solving heuristic satisfies Eq. (6) up to time . The additional term in Eq. (7) is needed for technical reasons in the proof (this term is equal to when is a quadratic function).

Lemma 1.

For and any , it holds that

| (9) |

Proof.

Lemma 2.

Let . Let be the stopping time defined in Eq. (7). Then, it holds that

| (10) |

Proof.

Proof of Lemma 2. For the optimal DP policy, the revenue collected in periods is . At the beginning of period , the remaining inventory level is . Therefore,

where the second equality holds because by applying Doob’s optional stopping theorem. Similarly, for the re-solving policy, because the revenue collected in periods is , we have

To complete the proof, note that for any admissible policy , we have by Theorem 1. ∎

4.2 Proof of Theorem 3

In this section we prove Theorem 3. By Lemma 2, for any , it holds that

| (11) | ||||

| (12) |

Recall that is the stopping time defined in Eq. (7). For any , we have by Eq. (5), by Eq. (8). For notational simplicity, define . So,

| (13) |

where the first inequality uses the strict concavity condition (A2) and the second inequality uses the smoothness condition (A3) of .

Define . Also, is measurable with respect to (note: as time are indexed backwards). By Doob’s optional stopping theorem, and . Taking expectations on both sides of Eq. (13) and summing over , we have

| (14) |

Define , and . By applying Eq. (13) to period , we have

| (15) |

where the second inequality holds because by definition and the last inequality follows by completing the square, because almost surely.

Subtracting (12) from (11), we obtain

| (16) |

where the second inequality holds because by definition, and is the maximizer of . The last inequality uses (14) (15) and the terms are defined as

Next, we analyze the four terms separately. Recall the definition , . For the term , with elementary algebra, it can be verified that

| (17) |

which implies that

Re-organizing all terms in by , we obtain

where the last equality uses . Note that the random variable is measurable with respect to , since the DP policy is non-anticipating. By Doob’s optional stopping theorem, we have and thus

| (18) |

Next we analyze the term . Note that has a similar structure as ; therefore

where the last equality uses Doob’s optional stopping theorem. Because , we have

| (19) |

where the last equality holds because the event .

Because the regret is defined as the difference between the expected revenues under the optimal DP policy and the re-solving heuristic, we can choose the joint distribution of freely, as long as their marginal distributions remain the same. We choose the joint distributions as follows. At each time period with posted prices and corresponding demand rates and , let such that the marginal distributions are , and furthermore

The existence of such a joint distribution is implied by (see Assumption (A5)). As a result, Eq. (19) can be simplified to

| (20) |

Combining Eq. (16) with Eqs. (17,18,20), we have

| (21) |

In the second inequality above, we use the fact that for any and . In the third inequality, we use the fact that for any .

Recall that , so and . Recall that , so . In sum, as , we have .

Furthermore, by the definition of the stopping time , we have , so . By Eq. (21), we get

| (22) |

To complete the proof, we upper bound each term in Eq. (22). First it is easy to verify that

| (23) |

We next focus on the terms involving . Recall the definition that . Let . Then is a martingale adapted to the filtration by Assumption (A4), which implies that is a submartingale. Let , then is also a submartingale. Since is stopping time, we have

It is easy to verify that

Subsequently,

| (24) |

To analyze the term , let . As before, is martingale and thus is a submartingale. Since and , we have

| (25) |

4.3 Proof of Theorem 4

Recall that for all , where is the stopping time defined in Eq. (7). Because this proof only concerns the re-solving policy, for convenience we will drop the superscript and denote by .

Invoking Lemma 2, we have

| (27) |

By the smoothness of (Assumption (A3)) and the fact that (see Eq. (7)), the second term in Eq. (27) is bounded by

where the last inequality holds since for all .

In the rest of the proof, we will bound the first term in Eq. (27). Expanding the difference at and using the strict concavity of (Assumption (A2)), we have

Therefore,

| (28) |

For the first term in Eq. (28), because , it holds that

| (29) |

by Doob’s optional stopping theorem (recall that is a stopping time). For the second term in Eq. (28), using , we have

| (30) |

Because is a stopping time and is a martingale difference sequence, we have and . So we have

Moreover, , so by the above equation and Eq. (30), we have

| (31) |

where the last equality holds by Lemma 1.

5 Numerical Results

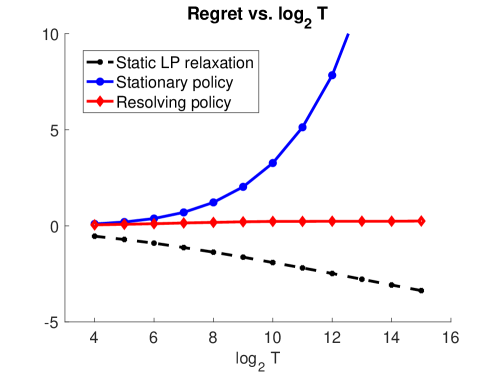

We corroborate the theoretical findings in this paper with a few simple numerical experiments. In the simulation we assume a linear demand curve with Bernoulli demand distribution: , with , and . The (normalized) initial inventory level is , meaning that for problem instances with time periods the initial inventory level is . It is easy to verify that the optimal demand rate without inventory constraints is , and the fluid approximation suggests a expected revenue. We select the Bernoulli demand distribution because the states of inventory levels are discrete and therefore the optimal dynamic programming pricing policy can be exactly obtained.

| 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | 15 | |

|---|---|---|---|---|---|---|---|---|---|---|

| Fluid Model | -0.90 | -1.13 | -1.37 | -1.63 | -1.91 | -2.19 | -2.48 | -2.78 | -3.08 | -3.37 |

| Static policy | 0.38 | 0.70 | 1.22 | 2.03 | 3.27 | 5.13 | 7.84 | 11.81 | 17.55 | 25.84 |

| Resolving heuristics | 0.11 | 0.15 | 0.18 | 0.21 | 0.23 | 0.23 | 0.24 | 0.24 | 0.24 | 0.25 |

In Table 2 we report the regret of the fluid approximation, the static policy and the re-solving heuristics . All regret is defined with respect to the value (expected reward) of the optimal DP pricing policy, and the regret for the fluid approximation benchmark is negative since the fluid model always upper bounds the value of any policy. Both the static policy and the re-solving heuristics are run for each value of ranging from to to obtain an accurate estimation of their expected rewards. We also plot the regret in Figure 2 to make the regret growth of each policy more intuitive.

As we can see from Table 2, the gap between the value of the optimal policy and the value of the fluid model grows nearly linearly as the number of time periods grows geometrically, which verifies the growth rate established in Theorem 4. On the other hand, the growth of regret of the re-solving heuristics stagnated at and is nearly the same for ranging from to . This shows the asymptotic growth of regret of is far slower than and is compatible with the regret upper bound we proved in Theorem 3.

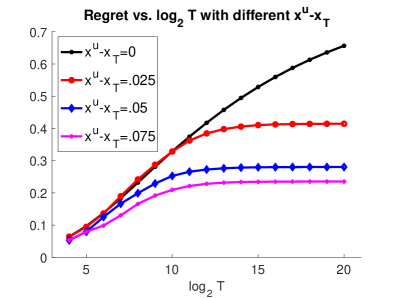

We report additional sets of numerical results in Figure 3, in which we only report the cumulative regret of the re-solving heuristic compared against the benchmark of the optimal DP policy.

On the left panel of Figure 3, we report the regret of the re-solving heuristic with ranging from to and different gap values. More specifically, all four curves are reported under the demand model , with unconstrained optimum and (normalized) initial inventory levels . Figure 3 clearly shows that the regret of the re-solving heuristic increases as the gap between and narrows, and furthermore in the boundary case (i.e., ) the regret seems to grow logarithmically in . It is an interesting direction of future research to formally establish the logarithmic regret for the boundary case and explore alternative policies that attain constant regret with .

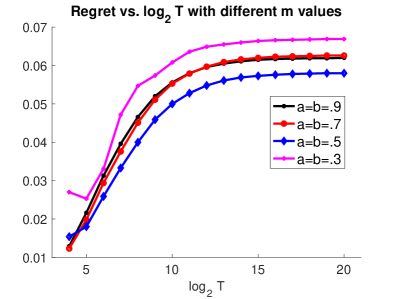

On the right panel of Figure 3, we report the regret of the re-solving heuristic with different values in the demand model , with . The normalized initial inventory level is fixed at . With different values of the slopes, the demand and revenue models exhibit different strong concavity parameter values, with and . Unlike the gap , the results reported in the right panel of Figure 3 do not paint a clear picture of the role the strong concavity parameters played in the regret. Overall, intermediate values () seem to result in the lowest regret of the re-solving heuristic.

6 Extension to Multiple Products

In this section, we extend our constant regret result to the case when there are products with correlated demand. We follow the convention in Section 4 and count time indices backwards. The seller starts with an initial inventory vector , where is the normalized initial inventory vector. When there are periods remaining, the seller posts a price vector and observes a realized demand vector , where is the demand curve and is a centered noise vector. The realized revenue at period is , which in expectation equals to . When the inventory level of a specific product dips below zero (), the seller is forced to set for all remaining time periods, resulting in almost surely.

Throughout this section, we use to denote the Euclidean norm of any vector , and to denote the spectral norm of any matrix . We extend the assumptions (A1)–(A5) to the multiple-product setting as follows:

-

B1.

(Invertibility) The demand rate function is a bijection, where . Let denote its inverse function. Assume is convex, compact, has nonempty interior, and satisfies .

-

B2.

(Strict Concavity) The expected revenue as a function of the demand rate vector is strictly concave. That is, there exists a positive constant such that for all . The maximizer of is in the interior of the domain .

-

B3.

(Smoothness) is three times continuously differentiable in the interior of .

-

B4.

(Martingale Difference Sequence) Conditional on any price vector (), the demand noise is independent of and satisfies The conditional distribution of given is denoted by . In addition, for some constant .

-

B5.

(Wasserstein Distance) There exists a constant such that for any , it holds that , where is the -Wasserstein distance between , with being an arbitrary joint distribution with marginal distributions being and , respectively.

Recall that is the normalized inventory level vector at the beginning of the time periods (i.e., the total inventory is ). The fluid approximation model is formulated as

At the beginning of each period , the re-solving heuristic solves

| (32) |

where is the normalized inventory level at the beginning of period . Since by Assumption (B1), Eq. (32) always has feasible solutions. Let the optimal solution to (32) be (the superscript stands for “constrained”). The re-solving policy sets the price vector to for period .

In (32), for any given , the products are partitioned into two disjoint sets based whether the inventory constraints are active at the point . The inventory-constrained product and the inventory-unconstrained product set , defined as

| (33) |

As a special case, in the single-product setting (), we have if , and if .

From the definitions in Eqs. (32, 33), it is clear that the sets and are determined by the inventory vector , which serves as the right-hand side of the fluid problem. We may thus write to emphasize such dependency. This leads to a partition of into sub-regions , where

| (34) |

We specify an additional assumption on the initial inventory level for the multi-product setting:

-

C1.

The initial inventory level is in the interior of for some . That is, given , there exists a neighborhood such that .

Intuitively, Assumption (C1) asserts that when the constrained inventory level fluctuates in a close neighborhood of , the set of active constraints in the fluid problem Eq. (32) remains unchanged. In the single-product case (), Assumption (C1) reduces to the condition .

We now characterize the expected value of the optimal DP policy and the re-solving heuristic for the multi-product pricing problem. Let be the expected revenue of the optimal policy when there are time periods left with the inventory level being . We have the following Bellman equation:

| (35) |

We denote the maximizer of Eq. (35) by . The DP policy selects the price vector . Let be the realized demand noise under this price.

The re-solving heuristic and its expected revenue , on the other hand, satisfies the following recursive equation

| (36) |

where is the solution to the fluid model with being the right-hand side. The following theorem extends the constant regret result in Sec. 3 to the multi-product setting.

Theorem 5.

Given a demand function and an initial inventory level satisfying Assumptions (B1)–(B5) and (C1), for all , we have

In the rest of this section we prove Theorem 5.

6.1 Partial Optimization on a Subset of Products

For any vector and subset , denote as the -dimensional sub-vector of whose coordinates are restricted to the subset . The following observation follows immediately from the definition of and the proof is omitted.

Lemma 3.

Suppose for some . Let . For any inventory vector with and , we have .

Given a fixed with , let be the projection of the domain onto the dimensions in . For every , define as the value of partial optimization of by changing the variables in while fixing the variables in :

| (37) |

The motivation for Eq. (37) is that in the region , the solution of the re-solving heuristic is only affected by the inventory levels of the constrained products in . The following lemma establishes some useful properties of the function .

Lemma 4.

The function has the following properties:

-

1.

For any , let . It holds that .

-

2.

is strictly concave and three times continuously differentiable for all and satisfies , with some constants .

-

3.

Given , let be the optimal solutions in (37). Then for some constant uniformly on .

Proof.

Proof of Lemma 4. The first property follows immediately from the definition of in Eq. (37) and the definition of in Eq. (34).

To prove the second property, consider the Lagrangian of (37). Since is concave, is a convex set with nonempty interior, and the optimization problem (37) satisfies Slater’s condition, has a saddle point satisfying

Note that the saddle point is unique because is strictly convex. By the envelop theorem for saddle point problems (Milgrom and Segal 2002, Theorem 5), when the saddle point is unique for every , the function is differentiable in the interior of with By the KKT conditions, , so

| (38) |

(Here denotes the restriction of to a subset .)

Denote the Hessian of at the point by

Let . By the KKT conditions again, we have . By the implicit function theorem, is continuously differentiable and the Jacobian matrix of is . Note that is invertible because is negative definite by Assumption (B2). Using Eq. (38) and the chain rule, we have

| (39) |

The right-hand side of Eq. (39) is the Schur complement of the block in the matrix . Since is negative definite by Assumption (B2), the Schur complement is also negative definite (Zhang 2005, Theorem 1.12), which implies that is strictly concave.

Next, we establish the smoothness condition of . Recall that , the Jacobian matrix is invertible, and is twice continuously differentiable by Assumption (B3). By the implicit function theorem for class (Krantz and Parks 2012, Theorem 3.3.1), is also twice continuously differentiable. By Eq. (39), is three times countinuously diffrentiable. Because the domain is compact by Assumption (B1), is uniformly bounded in .

Finally, the third statement of the lemma regarding the Lipschitz continuity of is straightforward, because the domain is compact and we have shown that is continuously differentiable in .

∎

6.2 Stopping Time with Bounded Expectation

Recall that are the stochastic demand noise vectors at each time period on the path of the re-solving heuristic policy . For any , define . Let . Note that by Assumption (C1). Define as

| (40) |

where is the constant parameter in Assumption (C1). Because is measurable with respect to , the event is adaptive to the filtration and therefore is a stopping time. We remark that implies the inequality . We will use this fact later in the proof of Theorem 5.

Recall that is the normalized inventory vector when time periods are remaining. The following lemma gives characterization of in terms of . It also gives an upper bound on , similar to Lemma 1.

Lemma 5.

Under Assumptions (B1)-(B5) and (C1), the following holds for all :

| (41) | ||||

where , as defined in Assumption (C1). For , we have . Furthermore, the stopping time is bounded by

Proof.

Proof of Lemma 5. We first prove Eq. (41) by induction. The base case of clearly holds because , which belongs to by Assumption (C1). Suppose Eq. (41) holds at period . Because , it holds that and therefore by Assumption (C1) and Lemma 3. Let be the demand rate chosen by the re-solving heuristic at period . Since , we know that and . Subsequently,

Next, we prove the upper bound on . By Assumption (B4), is a submartingale and . Using the identical proof by Doob’s martingale inequality in Lemma 1, we have . ∎

6.3 Complete Proof of Theorem 5

Given the initial inventory level , we first upper bound the value function of the optimal DP policy by considering a relaxed problem where the inventory of the products in is but the inventory of the products in is unbounded. Let be the path of inventory level process for this relaxed problem. Define . By Eq. (35), the value function of this relaxed problem is given by

Clearly, we have .

Below, we slightly abuse the notation and denote simply by . Then, it holds that , where and . By adapting Eq. (11) to the multi-product setting, we have

| (42) |

where

Next, we analyze the inventory process under the re-solving heuristic (for the original problem). Let . By Lemma 5, it holds that for all . In addition, for all , it holds that by Lemma 4 (recall that is the solution of the fluid model given the right-hand side ). We adapt Eq. (12) to the multi-product setting and get

| (43) |

Generalizing the arguments from Eqs. (28,29) and using the second property of Lemma 4, we obtain

| (44) |

where and .

Define , and , where denotes the element-wise positive part of . Eq. (15) can be generalized to

| (45) |

Let denote the element-wise product. Subtracting Eq. (43) from Eq. (42) and then combining Eq. (45) with Eq. (44), we obtain

| (46) |

where

Recall that in the definitions of , all vectors are restricted to . is an -dimensional vector, are -dimensional matrices and is a scalar. Using the same calculations as in Sec. 4, can be reduced to

| (47) | ||||

| (48) | ||||

| (49) |

Generalizing Eq. (19), it holds that

| (50) |

where the second inequality uses Assumption (B5) and the third inequality uses the third property in Lemma 4 with . As a result, can be upper bounded as

| (51) |

Because by the definition of , we have Combining Eq. (46) with Eqs. (47,48,51) and using the same derivation that leads to Eq. (22), we have

| (52) |

To complete the proof, we upper bound each term in Eq. (52). First it is easy to verify that

| (53) |

We next focus on the terms involving . Note that is a submartingale adapted to the filtration . Let , then is also a submartingale. Since is stopping time, we have

It is easy to verify that

Subsequently,

| (54) |

Since the Eucliean norm is convex, by Assumption (B4), is a submartingale. The expectation of can be upper bounded by

| (55) |

Finally, combining Eqs. (44,46,52,54,55) and using Lemma 5, we obtain

which completes the proof of Theorem 5.

7 Conclusion

In this paper, we analyze a natural re-solving heuristic for the classic price-based revenue management problem with either a single product or multiple products. The heuristic re-solves the fluid model in each period to reset the prices.

We establish two complementary theoretical results. First, the re-solving heuristic attains regret compared against the value of the optimal policy. The regret depends on the shape of the demand function as well as how close the initial inventory level is to certain “boundaries.” Going forward, an obvious question is whether the boundary condition can be removed. Our numerical experiment shows that the natural re-solving heuristic may not have regret when the initial inventory is on the boundary, so the pricing algorithm needs to be modified for that case.

Second, we show that there exists an gap between the value of the optimal policy and the value of the fluid model. For that reason, our regret analysis does not use the fluid model as a benchmark; the proof directly compares the value of the optimal policy and that of the heuristic. An interesting future direction is to find a different benchmark that is within of optimal value, which may help simplify our proof.

Appendix: The Hindsight-Optimum (HO) Benchmark.

The HO benchmark has been used to analyze re-solving algorithms for quantity-based network revenue management (Reiman and Wang 2008, Bumpensanti and Wang 2020). Since in quantity-based network revenue management the demand rates are not affected by the (adaptively chosen) prices, the formulation in Bumpensanti and Wang (2020) is not directly applicable to our setting. Instead, we formulate an HO benchmark following the strategy in Vera et al. (2019) which also considered price-based revenue management with a finite subset of pries.

Definition 1 (The HO benchmark).

For any define random variable as the total realized demand with fixed price . A policy is HO-admissible if at time , the price decision depends only on and . The HO-benchmark is defined as the expected revenue of the optimal HO-admissible policy .

At a higher level, the HO-benchmark equips a policy with the knowledge of the total realized demand for each hypothetical fixed price in hindsight. Clearly, such policies are more powerful than an ordinary admissible policy which only knows the expected demand but not the realized demand for a specific price .

Our next proposition shows that the HO-benchmark has a constant gap compared against the oracle in the single-product setting. Hence, it also has an gap from the re-solving heuristic and the optimal DP solution. The conclusion in Theorem 4 then holds with replaced by .

Proposition 2.

For any , it holds that where .

Proof.

Proof of Proposition 2. Consider a setting where are i.i.d. It is clear that knowing is equivalent to knowing , since for all . Now consider the policy of fixed prices . Since and , the expected regret of such a policy can be bounded as

which is to be demonstrated. ∎

References

- Arlotto and Gurvich (2019) Arlotto, Alessandro, Itai Gurvich. 2019. Uniformly bounded regret in the multisecretary problem. Stochastic Systems 9(3) 231–260.

- Aviv and Pazgal (2005) Aviv, Yossi, Amit Pazgal. 2005. Dynamic pricing of short life-cycle products through active learning. Working Paper, Olin School Business, Washington University, St. Louis, MO.

- Besbes and Zeevi (2009) Besbes, Omar, Assaf Zeevi. 2009. Dynamic pricing without knowing the demand function: Risk bounds and near-optimal algorithms. Operations Research 57(6) 1407–1420.

- Besbes and Zeevi (2012) Besbes, Omar, Assaf Zeevi. 2012. Blind network revenue management. Operations Research 60(6) 1537–1550.

- Broder and Rusmevichientong (2012) Broder, Josef, Paat Rusmevichientong. 2012. Dynamic pricing under a general parametric choice model. Operations Research 60(4) 965–980.

- Bumpensanti and Wang (2020) Bumpensanti, Pornpawee, He Wang. 2020. A re-solving heuristic with uniformly bounded loss for network revenue management. Management Science 66(7) 2801–3294.

- Chen and Farias (2013) Chen, Yiwei, Vivek F Farias. 2013. Simple policies for dynamic pricing with imperfect forecasts. Operations Research 61(3) 612–624.

- Cooper (2002) Cooper, William L. 2002. Asymptotic behavior of an allocation policy for revenue management. Operations Research 50(4) 720–727.

- den Boer and Zwart (2015) den Boer, Arnoud V, Bert Zwart. 2015. Dynamic pricing and learning with finite inventories. Operations Research 63(4) 965–978.

- Ferreira et al. (2018) Ferreira, Kris Johnson, David Simchi-Levi, He Wang. 2018. Online network revenue management using Thompson sampling. Operations Research 66(6) 1586–1602.

- Gallego and Van Ryzin (1994) Gallego, Guillermo, Garrett Van Ryzin. 1994. Optimal dynamic pricing of inventories with stochastic demand over finite horizons. Management Science 40(8) 999–1020.

- Gallego and Van Ryzin (1997) Gallego, Guillermo, Garrett Van Ryzin. 1997. A multiproduct dynamic pricing problem and its applications to network yield management. Operations Research 45(1) 24–41.

- Jasin (2014) Jasin, Stefanus. 2014. Reoptimization and self-adjusting price control for network revenue management. Operations Research 62(5) 1168–1178.

- Jasin (2015) Jasin, Stefanus. 2015. Performance of an lp-based control for revenue management with unknown demand parameters. Operations Research 63(4) 909–915.

- Jasin and Kumar (2012) Jasin, Stefanus, Sunil Kumar. 2012. A re-solving heuristic with bounded revenue loss for network revenue management with customer choice. Mathematics of Operations Research 37(2) 313–345.

- Jasin and Kumar (2013) Jasin, Stefanus, Sunil Kumar. 2013. Analysis of deterministic lp-based booking limit and bid price controls for revenue management. Operations Research 61(6) 1312–1320.

- Krantz and Parks (2012) Krantz, Steven G, Harold R Parks. 2012. The implicit function theorem: history, theory, and applications. Springer Science & Business Media.

- Lei et al. (2014) Lei, Yanzhe Murray, Stefanus Jasin, Amitabh Sinha. 2014. Near-optimal bisection search for nonparametric dynamic pricing with inventory constraint. Working Paper, Ross School of Business, University of Michigan.

- Ma and Simchi-Levi (2020) Ma, Will, David Simchi-Levi. 2020. Algorithms for online matching, assortment, and pricing with tight weight-dependent competitive ratios. Operations Research .

- Ma et al. (2020) Ma, Yuhang, Paat Rusmevichientong, Mika Sumida, Huseyin Topaloglu. 2020. An approximation algorithm for network revenue management under nonstationary arrivals. Operations Research 68(3) 834–855.

- Maglaras and Meissner (2006) Maglaras, Constantinos, Joern Meissner. 2006. Dynamic pricing strategies for multiproduct revenue management problems. Manufacturing & Service Operations Management 8(2) 136–148.

- Milgrom and Segal (2002) Milgrom, Paul, Ilya Segal. 2002. Envelope theorems for arbitrary choice sets. Econometrica 70(2) 583–601.

- Reiman and Wang (2008) Reiman, Martin I, Qiong Wang. 2008. An asymptotically optimal policy for a quantity-based network revenue management problem. Mathematics of Operations Research 33(2) 257–282.

- Secomandi (2008) Secomandi, Nicola. 2008. An analysis of the control-algorithm re-solving issue in inventory and revenue management. Manufacturing & Service Operations Management 10(3) 468–483.

- Vera and Banerjee (2020) Vera, Alberto, Siddhartha Banerjee. 2020. The bayesian prophet: A low-regret framework for online decision making. Management Science .

- Vera et al. (2019) Vera, Alberto, Siddhartha Banerjee, Itai Gurvich. 2019. Online allocation and pricing: Constant regret via bellman inequalities. arXiv preprint arXiv:1906.06361 .

- Wang et al. (2020) Wang, Yining, Boxiao Chen, David Simchi-Levi. 2020. Multi-modal dynamic pricing. Management Science (to appear) .

- Wang et al. (2014) Wang, Zizhuo, Shiming Deng, Yinyu Ye. 2014. Close the gaps: A learning-while-doing algorithm for single-product revenue management problems. Operations Research 62(2) 318–331.

- Zhang (2005) Zhang, Fuzhen. 2005. The Schur complement and its applications. Springer Science & Business Media.