Visualizing the Loss Landscape of Actor Critic Methods with Applications in Inventory Optimization

Abstract

Continuous control is a widely applicable area of reinforcement learning. The main players of this area are actor-critic methods that utilize policy gradients of neural approximators as a common practice. The focus of our study is to show the characteristics of the actor loss function which is the essential part of the optimization. We exploit low dimensional visualizations of the loss function and provide comparisons for loss landscapes of various algorithms. Furthermore, we apply our approach to multi-store dynamic inventory control, a notoriously difficult problem in supply chain operations, and explore the shape of the loss function associated with the optimal policy. We modelled and solved the problem using reinforcement learning while having a loss landscape in favor of optimality.

1 Introduction

Reinforcement learning agents explore the state and action space and develop behaviour policies using feedbacks from the environment. The size of the observation and policy space can make the methodology harder, even the most advanced computation systems can suffer from the curse of dimensionality. Approximate solution methods are one of the fundamental building blocks of reinforcement learning. Many reinforcement learning applications in challenging domains are available thanks to the recent developments in function approximation. Utilizing artificial neural networks as non-linear function approximators is a common practice in the literature. Policy gradient methods are examples of the literature that learns parameterized policies in continuous domains.

In this study, we would like to analyze the loss functions of some policy gradient methods. We selected two algorithms on continuous control domain one of which uses deterministic policy and the other uses stochastic policy while having state-of-art performance results on OpenAI tasks. (Brockman et al.,, 2016) However, they require separate hyperparameter tuning processes for different tasks. (Gu et al.,, 2016) It is also widely known that policy gradient methods are sensitive to hyperparameters and they require a serious hyperparameter tuning process. We modified special parts of the algorithms and examine their effects on loss shape and performance. In this way, we try to explain and visualize the reasons why some model settings are more successful to learn some tasks than others and make use of a visualization methodology in actor-critic method design.

In addition, we modelled a multi-store multi-product inventory control model as a Markov Decision Process. It is an important problem in supply chain operations yet it lacks a holistic approach. We trained a state-of-art agent on the model. Again, we provide loss function plots for this problem. The visualization methodology especially valuable for that kind of problem because convexity is a vital part of characterizing optimal policies in stochastic inventory theory.

2 Background

2.1 Visualizing the Loss Function

Neural networks are high dimensional models works on empirical risk minimization principle. To make use of neural networks, an appropriate loss function is optimized by adjusting the trainable parameters, also known as weights. The system can be described as a loss function and parameters. The number of parameters makes it impossible to plot the model loss and see curvature with respect to the parameters. We use the method proposed in Goodfellow et al., (2014) and generalized for three-dimensional plots in Li et al., (2018) as follows

| (1) |

where and are the reduced dimensions. is optimal parameters, and and are standard Gaussian random vectors of the same size as parameters. Note that, and are nearly orthogonal with high probability.

Using the representation in Equation 1, we are applying a huge dimensionality reduction on the loss function. We plot versus grids and to observe neighbourhood of the optimal point. In the resulting 3D graph, the non-convex structure asserts that the full loss function also has non-convexity. On the other hand, a convex 3D graph is only a clue of the low non-convexity of the loss function. The state of the approximator does not necessarily have the optimality property. One can initialize a neural network and visualize the current state of parameters, i.e. random weights. In that case, the visualization still works and shows the neighbourhood of the current part of the loss function. The existence of the cone shape in the plot is a sign of the training phase on the parameters.

In this study, we work on the loss functions of actor approximators. The network structure of our interest is fully connected layers accompanied by ReLU non-linearities. We used layer-wise normalization on to neutralize the scale invariance of such architecture. (Li et al.,, 2018)

2.2 Dynamic Inventory Model for Seasonal Products

Dynamic inventory management is a well-studied subject in Operations Research. In the general setting, it is modelled as a Markov Decision Process(MDP) for a single product. Karlin, (1960) and Scarf, (1959) showed that there exists an optimal policy for different cost settings. Our focus is on a more specific case where product procurement is done at the beginning of the season and the product is distributed periodically to the stores. This model can be applied to any real-life scenarios that include bulk procurement and periodic distribution. A natural application is in the fashion industry.

Multiple stores and multiple products are the sources of the complexity of the problem. Caro and Gallien, (2010) discussed a similar situation where the correlations between stores and products are ignored. They claim of usage of a heuristic algorithm and to best of our knowledge, there is neither any optimality guarantee for the problem nor a holistic modelling approach.

Our model can be defined by tuple where state space and action space are continuous. We model the single store multi product case as follows

| (2) |

The dynamic equation in Equation 2 means that and are the amount of inventories for depot and store at period for product . The decision is the flow amount of product between the depot and the store that is . Demands are stochastic and determined by probability distribution . The equation has two parts, is the immediate cost which occurs in period. We assume that holding inventory at the depot is free of charge. We also have a future cost part accompanied by discounting factor . Inventory level at depot is updated by the action, whereas, demand and action are in charge of the update of the inventory at the store. We assume that backordering is not allowed, namely, if there is no inventory on hand in any period a lost sales cost incurs.

Multi-store multi-depot model can be defined by the following dynamic equation

| (3) |

with immediate cost in period occurs according to

| (4) |

where product , store , depot and . In each period the elements of immediate cost consist of a fixed cost of ordering , a variable cost , a cost of lost sales , and a cost of holding inventory at a store . The update of inventory of product at store

| (5) |

and at depot

| (6) |

After periods the season ends and a leftover inventory cost occurs according to

| (7) |

where is the salvage cost of products.

The multi-depot model has dimensions of action space and dimensions of state space. The multi-store case can be modelled and managed with exercising a single depot. This setting performs a high level model while not losing much due to the pooling of possible multiple depots. We prefer to use single depot in this study. The action, , specifies the flow of product to store in each period. Hence, the action space has dimensions. Additionally, in each period actions are subject to a constraint defined by

| (8) |

Immediate cost function and store inventory variables are modified in a similar fashion. Therefore the state dimension of the environment is . We can represent the dynamic equation for multi-product multi-store model as follows

| (9) |

where and are matrices. Note that the demand distribution requires specific arrangements to build desired correlation between products and stores. We designate demand as Gaussian Process.

Having a large action and observation space is the primary reason for the difficulty of the problem. On top of that, the environment does not necessarily have a stationary distribution of demand, which distinguishes the application of reinforcement learning on inventory management than robotic control.

3 Experiments

We conducted two streams of experiments. In the next section, we give loss visualizations of two recently proposed successful off-policy policy gradient algorithms. Soft actor-critic algorithm(SAC) (Haarnoja et al., 2018b, ) utilizes stochastic policy via entropy maximization. The deterministic variant of the algorithm found to be unstable (Haarnoja et al., 2018a, ). We present a comparison of two settings through their loss landscape. Another algorithm in the continuous control domain is Twin Delayed Deep Deterministic Policy(TD3) (Fujimoto et al.,, 2018) algorithm which is a Double Q-Learning (Van Hasselt et al.,, 2016) variant. TD3 has improvements in value function overestimation through a delay mechanism to reduce the variance of policy updates. In particular, we will focus on the smoothing procedure that TD3 uses during action value calculations.

Moreover, we apply SAC on our multi-store multi-product inventory management environment under various demand scenarios.

3.1 MuJoCo Environments

In this section, we train SAC and TD3 on continuous control tasks of OpenAI Gym (Brockman et al.,, 2016) as provided in related papers.

We train models for 1 million episodes in different environments and have similar results claimed in their original papers. Then, we run trained models on related environments to get trajectories. The resulting trajectories have various lengths of states. We apply uniform sampling to get uniform length trajectories and calculate loss values on them.

We modify the following objective of SAC

| (10) |

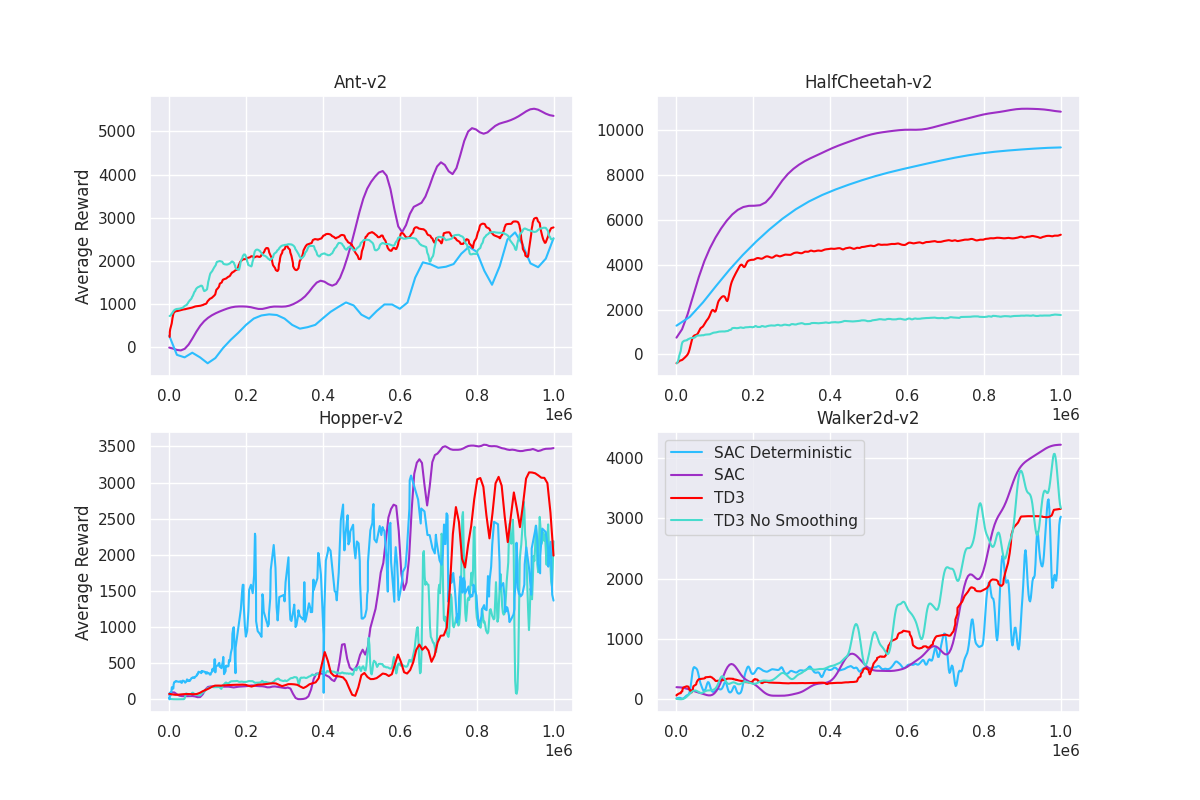

and used to get deterministic version of it while disregarding the entropy part. Note that is the temperature term that adjusts the importance of which is the entropy function. In the original paper SAC is trained for up to 10 million steps however we were able to distinguish performance differences after 1 million. The deterministic version of SAC has slightly worse performance among our four experiments in that category and has stability problems as discussed in the original paper.

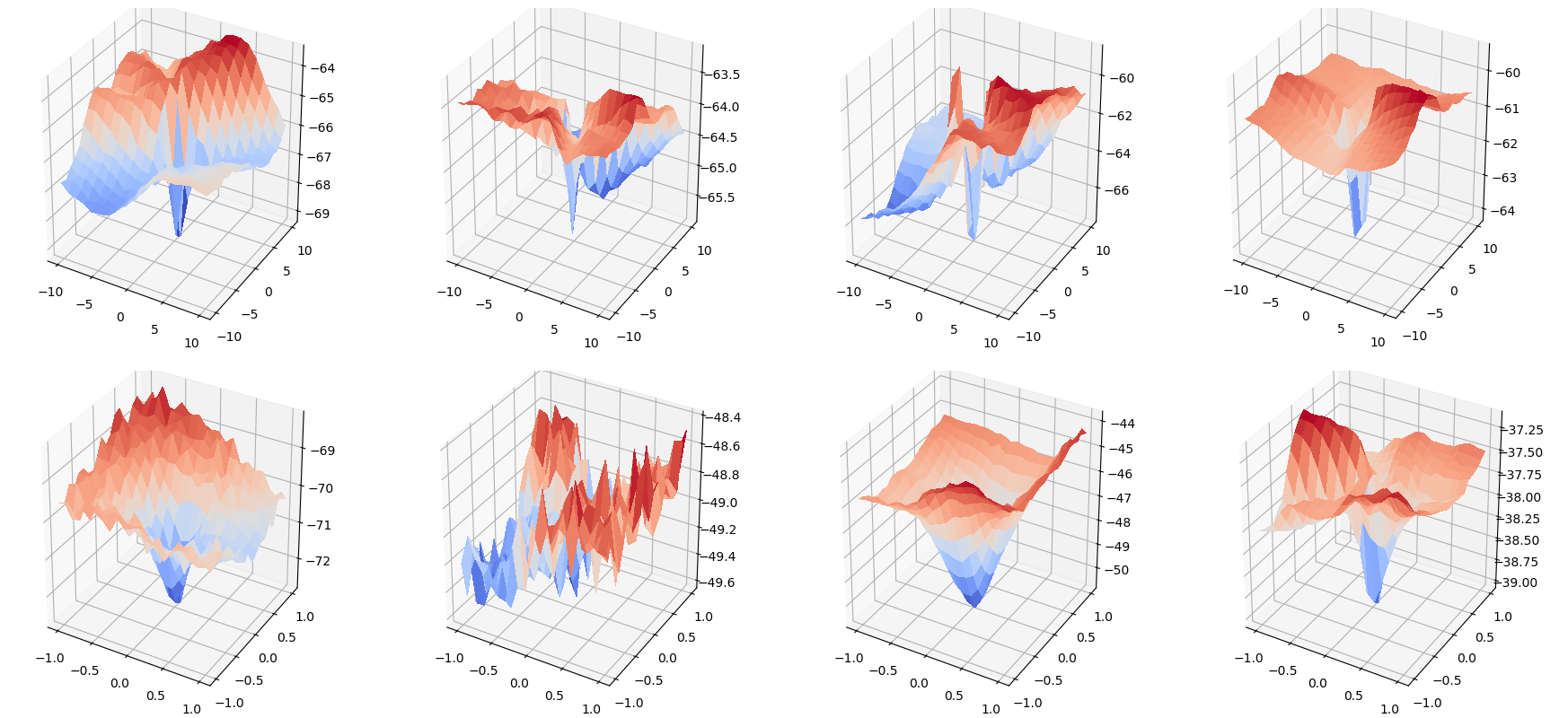

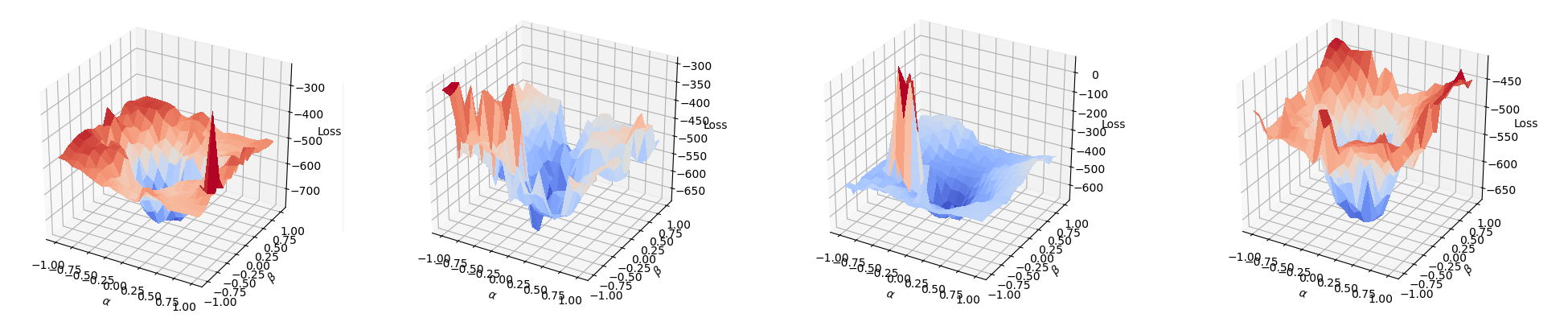

Figure 3 is quite explanatory for the instability of the deterministic policy compared with stochastic policy. It is very obvious that the loss functions on the four environments are promoting the global minimum while using stochastic policy. Whereas, the deterministic policy resulted in a chaotic loss landscape, especially on .

We experiment on TD3 with and without action smoothing. In the original paper (Fujimoto et al.,, 2018) target value is calculated by

| (11) |

where and are critic and actor networks, is the reward and is clipped Gaussian noise.

Without action smoothing the target value is calculated by

| (12) |

Action smoothing in TD3 is not as vital as the stochastic policy for SAC. As a result, we cannot observe a huge performance difference on average rewards. The results in Figure 4 validate this fact. We can see a little effect of smoothing between the upper and the lower rows of Figure 4. In fact, the average rewards of the smoothed algorithm are slightly higher than the one which does not utilize smoothing.

When we compare Figure 3 and Figure 4, we see that the nature of SAC, points the global minimum more harshly even though it is an entropy maximizer algorithm and utilizes soft policy evaluation and soft policy iteration. Note that, SAC over-performs TD3 in every task we analyzed. Hence, we can infer that the comparison of the smoothness of dimensionally reduced loss function in a specific task does not give any idea about the performances of different algorithms. Alternatively, we can think of harsh pointing of global minimum as the effect of a black hole on spacetime which creates strong gravity, therefore a strong force to find the global minimum. We also observe a high variability on task as a common behaviour. This effect can be inferred from figures 3 and 4 where the loss shapes of are chaotic except the one for SAC.

3.2 Multi-Product Multi-Store Seasonal Inventory Management

We designed the model in Section 2.2 as a reinforcement learning environment and use SAC to solve it. We call a full season as one episode. A primary design question is reward design. The problem is cost minimization by its nature. We tested periodic reward versus giving the reward at the end of the episode and decided to use the total cost at the end of the episode. Intuitively, this corroborates the fact that minimizing the cost of a period is not necessarily the right action to solve the general minimization problem. In addition to that, we scaled the reward and avoid constant negativity of rewards with the help of the following formula

| (13) |

where requires tuning.

We conducted the experiment over 20 periods and 5 different random seeds. We used fixed cost , variable cost of ordering , cost of lost sales , cost of holding inventory at stores , and salvage cost for and .

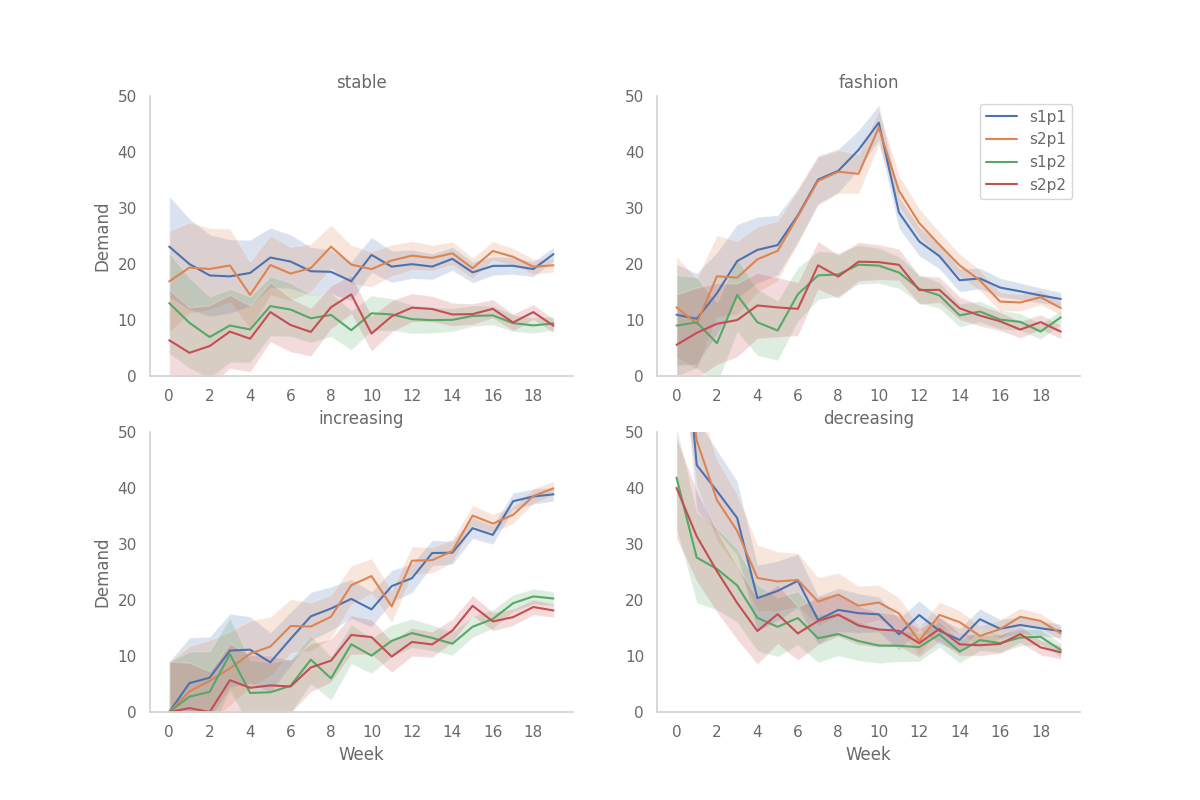

We modelled demand as Gaussian Process where the products in different stores correlated. We designed four different scenarios to capture different real-world settings. Increasing and decreasing scenarios have monotonic increasing and decreasing demand patterns throughout the episode. Fashion scenario resembles the fashion product life cycle in which demand enjoys growth, maturity, and decline periods respectively. Lastly, a stationary demand scenario does not have any trend as the name suggests. To see the relative performance of our implementation we created two different ordering procedures. The first procedure naively orders the mean demand rate. Moreover, we adapted a base stock policy that keeps the inventory at a designated level of .

| Improvement Over Ordering Mean (%) | |||||

|---|---|---|---|---|---|

| Demand Scenarios | Policy | Mean | Min | Max | Std Dev |

| Decreasing | Order up to | 5.68 | -6.42 | 11.44 | 6.61 |

| SAC | 27.24 | 14.53 | 35.39 | 7.21 | |

| Increasing | Order up to | 30.67 | 24.26 | 34.05 | 3.64 |

| SAC | 11.29 | 3.88 | 16.03 | 4.14 | |

| Fashion | Order up to | 16.19 | 4.82 | 24.89 | 6.84 |

| SAC | 15.27 | 1.52 | 23.27 | 7.31 | |

| Stationary | Order up to | 20.28 | 11.26 | 26.67 | 5.42 |

| SAC | 15.58 | 7.37 | 22.94 | 5.16 | |

We used 2-stores 2-products version of the model in our experiments. However, a real-life application of the problem for operations of a medium-sized global organization can have hundreds of stores and thousands of products which makes the problem interesting and challenging. Also, real-life decisions of promising domains will probably require discrete decisions. We think that modelling and solving the problem in continuous space can be done without diverging from optimality.

Ordering the mean level is the most costly policy as expected. We built our baseline on the mean level ordering policy and presented relative improvements of the other policies. Furthermore, we observe that the policy trained with SAC does not always perform best. Under increasing and stable scenarios, the order-up-to policy yielded a better cost and both algorithms perform similarly under the fashion scenario.

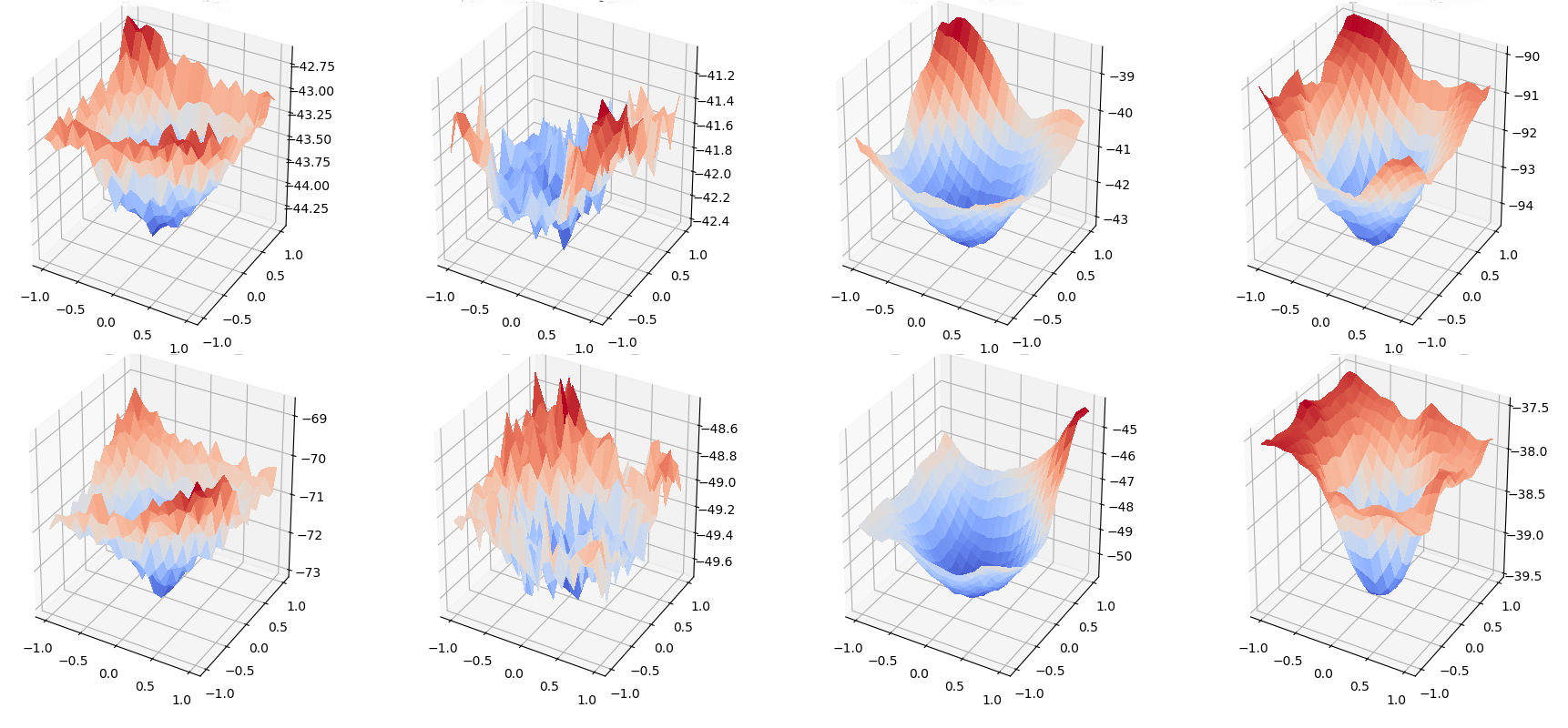

From Figure 6, we can observe that actor losses point out the minimum except for the increasing scenario. Other than increasing scenario, low dimensional representations of loss shapes tend to be convex. Thus, applying SAC on a multi-store multi-product inventory problem has promising results. Since we were able to beat the performance of the trained policy using classical intuitive policies, we can infer that the problem needs more special treatment to solve the problem more efficiently. Our interpretation about the reason behind the inability of SAC to be successful in even smaller 2-stores 2-products model is the nature of the problem which involves a conflict of interests between different products and different stores. The problem cannot be treated independently, besides, it should gain information from correlations of different interests. Therefore, an algorithm which designed for a single goal cannot be successful in that problem area. Possible research directions can include the generalization of continuous control on high dimensions using high-level representations of the space or dedicated algorithm design.

4 Conclusion

We applied a visualization technique that can be used to visualize highly parameterized statistical models in reinforcement learning and we presented the action loss landscapes of two actor-critic algorithms and their variants. The results we have, exhibit that the graphs produced using such a technique carries valuable information and can be beneficial for obtaining insights about the algorithms and their applications. An application of the technique can be tracing the convexity of dynamic programming models. We modelled and solved such a problem in inventory optimization. The results from that specific domain assert that multi-store multi-product dynamic inventory control can be done using reinforcement learning.

Acknowledgments and Disclosure of Funding

We would like to thank Compute Canada for providing computational resources.

References

- Barto et al., (1983) Barto, A. G., Sutton, R. S., and Anderson, C. W. (1983). Neuronlike adaptive elements that can solve difficult learning control problems. IEEE transactions on systems, man, and cybernetics, (5):834–846.

- Brockman et al., (2016) Brockman, G., Cheung, V., Pettersson, L., Schneider, J., Schulman, J., Tang, J., and Zaremba, W. (2016). Openai gym. arXiv preprint arXiv:1606.01540.

- Caro and Gallien, (2010) Caro, F. and Gallien, J. (2010). Inventory management of a fast-fashion retail network. Operations Research, 58(2):257–273.

- Fujimoto et al., (2018) Fujimoto, S., Van Hoof, H., and Meger, D. (2018). Addressing function approximation error in actor-critic methods. arXiv preprint arXiv:1802.09477.

- Goodfellow et al., (2014) Goodfellow, I. J., Vinyals, O., and Saxe, A. M. (2014). Qualitatively characterizing neural network optimization problems. arXiv preprint arXiv:1412.6544.

- Gu et al., (2016) Gu, S., Lillicrap, T., Ghahramani, Z., Turner, R. E., and Levine, S. (2016). Q-prop: Sample-efficient policy gradient with an off-policy critic. arXiv preprint arXiv:1611.02247.

- (7) Haarnoja, T., Zhou, A., Abbeel, P., and Levine, S. (2018a). Soft actor-critic: Off-policy maximum entropy deep reinforcement learning with a stochastic actor. arXiv preprint arXiv:1801.01290.

- (8) Haarnoja, T., Zhou, A., Hartikainen, K., Tucker, G., Ha, S., Tan, J., Kumar, V., Zhu, H., Gupta, A., Abbeel, P., et al. (2018b). Soft actor-critic algorithms and applications. arXiv preprint arXiv:1812.05905.

- Karlin, (1960) Karlin, S. (1960). Dynamic inventory policy with varying stochastic demands. Management Science, 6(3):231–258.

- Li et al., (2018) Li, H., Xu, Z., Taylor, G., Studer, C., and Goldstein, T. (2018). Visualizing the loss landscape of neural nets. In Advances in Neural Information Processing Systems, pages 6389–6399.

- Liao and Poggio, (2017) Liao, Q. and Poggio, T. (2017). Theory of deep learning ii: Landscape of the empirical risk in deep learning. arXiv preprint arXiv:1703.09833.

- Lillicrap et al., (2015) Lillicrap, T. P., Hunt, J. J., Pritzel, A., Heess, N., Erez, T., Tassa, Y., Silver, D., and Wierstra, D. (2015). Continuous control with deep reinforcement learning. arXiv preprint arXiv:1509.02971.

- Mnih et al., (2013) Mnih, V., Kavukcuoglu, K., Silver, D., Graves, A., Antonoglou, I., Wierstra, D., and Riedmiller, M. (2013). Playing atari with deep reinforcement learning. arXiv preprint arXiv:1312.5602.

- Mnih et al., (2015) Mnih, V., Kavukcuoglu, K., Silver, D., Rusu, A. A., Veness, J., Bellemare, M. G., Graves, A., Riedmiller, M., Fidjeland, A. K., Ostrovski, G., et al. (2015). Human-level control through deep reinforcement learning. Nature, 518(7540):529–533.

- O’Donoghue et al., (2016) O’Donoghue, B., Munos, R., Kavukcuoglu, K., and Mnih, V. (2016). Combining policy gradient and q-learning. arXiv preprint arXiv:1611.01626.

- Porteus, (2002) Porteus, E. L. (2002). Foundations of stochastic inventory theory. Stanford University Press.

- Scarf, (1959) Scarf, H. (1959). The optimality of (s, s) policies in the dynamic inventory problem.

- Sutton et al., (1998) Sutton, R. S., Barto, A. G., et al. (1998). Introduction to reinforcement learning, volume 135. MIT press Cambridge.

- Van Hasselt et al., (2016) Van Hasselt, H., Guez, A., and Silver, D. (2016). Deep reinforcement learning with double q-learning. In Thirtieth AAAI conference on artificial intelligence.

Appendix

Heuristic Ordering Policies

Let is the demand of the product at period . . is a Gaussian Process determined by sets of parameters and .

Baseline: Ordering Mean

Order amount is determined as follows

| (14) |

Order up to

The order amount is determined by the inventory position at the end of the previous period.

| (15) |

where is determined by where is the CDF of the Normal with mean and variance . Intuitively speaking, is the level that satisfies the demand in the period with probability 95%.