Abstract

The environmental Kuznets curve predicts an inverted U-shaped relationship between environmental pollution and economic growth. Current analyses frequently employ models which restrict nonlinearities in the data to be explained by the economic growth variable only. We propose a Generalized Cointegrating Polynomial Regression (GCPR) to allow for an alternative source of nonlinearity. More specifically, the GCPR is a seemingly unrelated regression with (1) integer powers of deterministic and stochastic trends for the individual units, and (2) a common flexible global trend. We estimate this GCPR by nonlinear least squares and derive its asymptotic distribution. Endogeneity of the regressors will introduce nuisance parameters into the limiting distribution but a simulation-based approach nevertheless enables us to conduct valid inference. A multivariate subsampling KPSS test is proposed to verify the correct specification of the cointegrating relation. Our simulation study shows good performance of the simulated inference approach and subsampling KPSS test. We illustrate the GCPR approach using data for Austria, Belgium, Finland, the Netherlands, Switzerland, and the UK. A single global trend accurately captures all nonlinearities leading to a linear cointegrating relation between GDP and CO2 for all countries. This suggests that the environmental improvement of the last years is due to economic factors different from GDP.

JEL Classification: C12, C13, C32, O44, Q20

Keywords: Cointegration Testing, Environmental Kuznets Curve, Generalized Cointegrating Polynomial Regression, Power Law Trends

1 Introduction

On page 370 of their seminal paper, Grossman and Krueger (1995) conclude:

“Contrary to the alarmist cries of some environmental groups, we find no evidence that economic growth does unavoidable harm to the natural habitat. Instead we find that while increases in GDP may be associated with worsening environmental conditions in very poor countries, air and water quality appear to benefit from economic growth once some critical level of income has been reached.”

The quote above suggests an inverted U-shaped relationship between environmental degradation and economic growth. This relationship is currently known as the Environmental Kuznets Curve (EKC) and it forms an active research area. Its relevance becomes clear if we look at some forecasts of long-run economic growth. The projected GDP per capita growth of the world is about 2.1% per year for the next decades (chapter 3 in Nordhaus (2013); Gillingham and Nordhaus (2018)) and this growth is partially powered by carbon-based energy resources, water usage, and material consumption. In absence of an EKC, economic growth will place more and more stress on the environment. Alternatively, if the EKC exists, then the inverted U-shape eventually implies a turning point after which economic growth and environmental improvement go hand in hand. Due to such considerations, there is now, some 25 years after its first conception, a rich literature that (1) reports on the experimental evidence on the existence/nonexistence of the EKC, (2) provides economic theory to explain the EKC, and/or (3) refines the econometric tools that are used to analyse the EKC.111Further references to these specific areas of research can be found in the review articles by Dasgupta et al. (2002), Stern (2004), and Carson (2009) among others. To quantify the volume of the literature we have entered the search query “Environmental Kuznets Curve” into the Web of Science: more than 4,200 references are found.222Web of Science, accessed on December 6, 2021, http://www.webofknowledge.com.

Driven by contradictory empirical results as well as the variability in estimated turning points, the EKC has been criticised on two main points. First, the income variable was initially treated as a stationary variable whereas later research shows that the unit root hypothesis often cannot be rejected (see Galeotti et al. (2009), p. 553; Stern (2017), p. 14–15). Nonstationarity has further implications because EKC regressions include higher integer powers of GDP as well. This combination of nonstationarity and nonlinearity places the EKC in the nonlinear cointegration literature and appropriate econometric techniques should be employed. Such techniques have been developed in Wagner (2015) and Wagner and Hong (2016) under the name of Cointegrating Polynomial Regressions (CPRs). CPRs contain deterministic variables, integrated processes, and their integer powers.333Stypka et al. (2017) reiterate the need to model the income variable as nonstationary. It is less important to use an estimation procedure acknowledging the fact that several integer powers of the same integrated process appear as regressors. That is, Stypka et al. (2017) find that the “standard estimator” which treats higher order powers of the integrated regressor as additional I(1) variables has the same limiting distribution as the CPR estimator. Multivariate generalizations of CPRs, Seemingly Unrelated Cointegrating Polynomial Regressions (SUCPRs), are discussed in Wagner et al. (2020) and Lin and Reuvers (2020).

As a second point of critique, there is an ongoing debate on the model specification. Various functional forms can describe the relationship between national income and the pollution variable. The quadratic specification is widespread but cubic relationships (Harbaugh et al. (2002); Wagner (2015)) and double-nonlinear transformation (Lin et al. (2020)) are also in use. Various specification tests are helpful while deciding on the right parametric specification (Hong and Phillips (2010); Wang and Phillips (2012); Wang et al. (2018)). Alternatively, one could resort to nonparametric estimation procedures altogether (Wang and Phillips (2009); Linton and Wang (2016)). Whereas such modelling approaches do allow for a more flexible relationship, they also implicitly assume that nonlinear environmental effects are solely attributable to economic growth. Relevant variables are thus potentially missing from the model specification. Such omitted variables are a valid concern because advances in green technology, pollution policy, and environmental awareness, may all influence pollution levels. However, such data is typically available for short time spans only (and for that reason often excluded from the model). Time effects can control for time-variation in unobserved effects (Vollebergh et al. (2009)).

Current developments on nonlinear cointegration emphasize the role of the nonstationary regressor yet pay less attention to time effects. Time effects are important. The small simulation exercise in Table 1 illustrates the point. Foreshadowing our proposed model, we consider a multivariate setting with a global nonlinear, smooth time trend. The global trend is omitted by the researcher and a quadratic EKC-specification is estimated: (), where and are unit-specific variables measuring income and environmental pollution, respectively. We test because a significantly negative coefficient in front of is typically interpreted as evidence of an EKC.444For the moment, we focus on the curvature parameter. Clearly, for an inverted U-shaped relationship the coefficient in front of the linear term should be positive. Panel (A) reveals exacerbated rejection frequency as curvature caused by the global deterministic trend is mistakenly interpreted as curvature caused by the income variable. In other words, negative and significant coefficients in front of squared GDP are possibly caused by omitted nonlinear deterministic trends rather than being indicative of an EKC. To be on the safe side, we recommend researchers to include a nonlinear trend component in their model specification. If unnecessary, then this is rather innocuous. Indeed, Panel (B) of Table 1 shows that significant results for nonlinear economic growth effects continue to be found with modest losses in statistical power.

| Panel (A): Omitted Global Trend | Panel (B): Redundant Global Trend | |||||||

| DGP | ||||||||

| Model | Correct Specification | |||||||

| FM-SOLS | FM-SUR | SimNLS | SimNLS | |||||

| 0 | 6.30 | 6.63 | 0 | 6.93 | 5.70 | |||

| -0.5 | 13.27 | 12.77 | -0.5 | 9.20 | 6.97 | |||

| -1 | 30.07 | 27.50 | -1 | 14.97 | 9.97 | |||

| -1.5 | 46.23 | 41.57 | -1.5 | 30.47 | 20.70 | |||

| -2 | 56.60 | 50.30 | -2 | 55.33 | 40.53 | |||

| -2.5 | 64.50 | 56.00 | -2.5 | 81.73 | 69.20 | |||

| -3 | 68.60 | 57.57 | -3 | 93.97 | 89.50 | |||

-

•

Note 1: For illustrative purpose, we consider a stylised example in this introduction. The exact parametrisation is available in Section of the Supplementary Material. More elaborate simulation results based on the empirical application are reported as simulation DGP2 in Section 4.

- •

The contributions of this paper are fourfold. First, we propose the Generalized Cointegrating Polynomial Regression (GCPR). This multivariate model features a global power law trend to capture time effects. Power law trends have been employed to model non-constant growth rates in technology indices (Duggal et al. (1999); Duggal et al. (2007)) and production functions (Klein et al. (2004)). Within the EKC context, this flexible trend can capture common time effects that are implicit in omitted variables. Alternatively, as in Li and Linton (2020), the reader can view the global flexible trend as an outside option (next to the income variable) to describe nonlinearities in the data. Limiting distributions for estimators in models with purely deterministic power law trends have been reported in Phillips (2007), Robinson (2012) and Gao et al. (2020). The presence of integrated variables requires an alternative asymptotic framework. Moreover, due to endogeneity, approaches assuming pre-determined integrated regressors (Park and Phillips (1999); Park and Phillips (2001); Chang et al. (2001)) are inappropriate and we instead opt for a proof along the lines of Chan and Wang (2015). The resulting limiting distribution is non-standard because (1) the scaling matrix with convergence rates is non-diagonal and parameter dependent, and (2) second-order bias terms are present. Second, we propose a simulation-based approach to conduct inference. Monte Carlo simulations show clear benefits of this simulation-based approach in terms of size control compared to existing methods. Third, in the spirit of Choi and Saikkonen (2010), we report a multivariate KPSS-type test to verify the stationarity of the error process thus enabling researchers to avoid spurious results or misspecified cointegrating relations. Fourth and finally, in the empirical application, we investigate the EKC for Austria, Belgium, Finland, the Netherlands, Switzerland and the UK over the period 1870–2014. Nonparametric estimates and tests confirm that the global trend captures all nonlinearities in the data. Nonlinear effects in log per capita GDP (and thus also evidence for an EKC) are absent. Given such findings, we offer a clear recommendation to researchers to check whether their EKC conclusions are robust to the inclusion of power law trends.

This paper is organized as follows. Section 2 introduces the model and the estimation framework. Asymptotic properties of the estimators and parameter inference are discussed in Section 3. The Monte Carlo simulations in Section 4 compare asymptotic results to finite sample performance. An in depth discussion of the Environment Kuznets Curve can be found in Section 5. Section 6 concludes. The proofs of the main theorems are collected in the Appendix and further information is available in the Supplementary Material.

Finally, some words on notation. The integer part of the number is denoted by . For a vector , its -norm is denoted by . For a matrix , say of dimension (), the induced -norm is defined as . We will omit the subscripts whenever . The identity matrix is denoted and signifies an -dimensional column vector with all entries equal to 1. The block-diagonal matrix stacks the matrices along its diagonal. We omit the integration bounds whenever the integration interval is . The symbol “” stands for equality in distribution, and “” and “” denote convergence in probability and in distribution. If convergence occurs conditionally on the sample, then we add a superscript “*” to the standard notation. The probabilistic Landau symbols are and . Finally, the generic constant can change from line to line.

2 The Model and NLS Estimation

Our model specification enriches the Seemingly Unrelated Cointegrating Polynomial Regressions (SUCPRs) from Wagner et al. (2020) with a flexible deterministic trend. That is, each individual series in the system is affected by specific deterministic variables and integrated regressors (and their integer powers) while a global flexible trend describes nonlinear behaviour that is prevalent across all series. The resulting Generalized Cointegrating Polynomial Regression (GCPR) is given by:

| (2.1) |

where with and . Alternatively, we write , where and . Finally, we stack all equations in (2.1) in matrix form to retrieve

| (2.2) |

with , , and the vector of length containing all local parameters.

We consider nonlinear least squares (NLS) estimators of the unknown parameters in (2.1). As such, we define the objective function and compute

| (2.3) |

The optimization problem in (2.3) is easy to solve. For any given , model (2.2) is linear-in-parameters and the minimizers for and can be found from an OLS regression by constructing and computing . We subsequently minimize the concentrated criterion function to obtain . At last, we plug in and recover and through a final OLS estimation.

Remark 1

Keeping the powers of fixed allows us to test for their significance and thereby distinguish between nonlinearities caused by deterministic and stochastic trends. This is important for our empirical application on the Environmental Kuznets Curve, see Section 5. Hu et al. (2021) study a model with a flexible power of the integrated regressor. That is, these authors derive the limiting distribution of the NLS estimators for and when with .

Remark 2

The GCPR of (2.1) can be extended in several directions. First, integer powers of deterministic trends can be added as long as is adjusted accordingly (to avoid collinearity). Second, multiple explanatory variables can be included. Related to the EKC, the literature suggests examples such as: population density (Selden and Song (1994)), trade openness (Jalil and Feridun (2011)), energy prices (Al-Mulali and Ozturk (2016)), and educational level (Maranzano et al. (2021)). For nonstationary variables, conditions similar to those on should be fulfilled (Assumption 2 below). Stationary variables should be strictly exogenous. Avoiding the elaborate notation which would otherwise arise, we focus on the baseline specification in (2.1).

3 Asymptotic Theory

We subsequently study the asymptotic properties of the NLS estimators. To this end we first collect all the unknown parameters in the vector . This vector is assumed to be an element of the parameter space . The true parameter vector is .

Assumption 1

The global trend is relevant, i.e. .

Assumption 2

Let be a sequence of i.i.d. random vectors with , , and for some .

-

(a)

with .

-

(b)

, where with and .

The first assumption is needed to avoid identification issues. That is, if , then is not identified and the Davies problem arrises when testing (see Davies (1977, 1987)). Such complications are not investigated here and this is further reflected in our model specification (2.1). That is, we consider flexible powers of the deterministic trends but fixed powers of the stochastic trends, hence allowing us to test zero restrictions on (elements of) . This is of crucial importance in the EKC application while determining whether nonlinear effects in the economic growth variables () remain significant after nonlinear time trends have been added to the model. Assumption 1 has been relaxed in the literature albeit for different models. Baek et al. (2015) and Cho and Phillips (2018) study the asymptotic behaviour of a quasi-likelihood ratio test when Assumption 1 is violated and the conditional mean of the data contains strictly stationary regressors and a flexible time trend. Alternatively, one can use drifting parameter sequences with different identification strengths as in Andrews and Cheng (2012).

Assumption 2 excludes cointegration among elements of and defines this vector as the partial sum of a short memory process. The latter implies that where denotes an -dimensional vector Brownian motion with covariance matrix . The one-sided long-run covariance matrix is partitioned similarly. Subscripts refer to specific elements. For example, and denote the th and th elements of and , respectively.

A concise exposition of our results asks for additional notation. An enumeration of various definitions is presented below.

-

(1)

Introduce to scale the deterministic and stochastic trends within each equation. For the full system of equation, define , and . Finally, set .

-

(2)

Define , , and .

-

(3)

For the second-order bias terms, we define and .

The proof of Theorem 1 is closely related to the work by Chan and Wang (2015). These authors provide the asymptotic distribution of NLS estimators under a set of general conditions in univariate, nonstationary time series models (see their theorem 3.1). The results in Chan and Wang (2015) and Wang et al. (2018) suggest that Assumption 2 can be replaced by a long memory specification for . However, long memory parameters will enter the limiting distribution and inference will be complicated further. We illustrate Theorem 1 with two examples. These examples highlight the two mathematical features that complicate parameter inference.

Example 1

We consider with innovations satisfying Assumption 2. The limiting distribution of the parameter estimators depends solely on the mean square Riemann-Stieltjes integrals and , and is therefore normally distributed (e.g., section 2.3 in Tanaka (2017)). We have

| (3.1) |

The scaling matrix in the LHS of (3.1), , depends on and is non-diagonal. The dependence on is unavoidable but asymptotic results for the case of a diagonal scaling matrix are obtainable at the expense of a singular joint distribution. That is, noting that and since , the continuous mapping theorem implies This limiting distribution coincides with the result in theorem 6.3 of Phillips (2007).

Example 2

If , then the limiting distribution of the NLS estimator is:

|

|

This limiting distribution exhibits second order bias when , or when and are correlated.

Two features of the limiting distribution of deserve further comments. First, as emphasised in Examples 1–2, the scaling matrix features two less common properties: (1) this matrix depends on the true parameters and , and (2) is not diagonal. These peculiarities are caused by the nonlinearity and nonstationarity of the model. More specifically, these features can be traced back to the presence of the global trend. Limiting distributions with a similar mathematical structure can be found in the structural breaks literature, cf. model setting II.b of Perron and Zhu (2005) and its detailed analysis in Beutner et al. (2020).

Second, the nonstationary regressor enters the model (2.1) through a polynomial transformation of the form (). In the terminology of Park and Phillips (2001) this part of the regression function is a linear combination of -regular functions. It is well-documented in the literature, e.g. Chang et al. (2001) and Chan and Wang (2015), that this leads to second-order bias terms and hence nonstandard inference (except for the special case of strictly exogenous nonstationary regressors).

3.1 Consistent Long-Run Covariance Matrix Estimation

Correcting for second-order bias terms typically involves estimating long-run variance (LRV) matrices. This subsection establishes that the NLS residuals can be used to construct consistent kernel estimators for the LRV matrices and . Defining with , these LRV estimators are defined as

| (3.2) |

for some kernel function and bandwidth parameter . The first elements of are the elements of the residual vector . The remaining elements are .

Assumption 3

-

(a)

, is continuous at zero, and .

-

(b)

, where .

-

(c)

The bandwidth parameters satisfies and .

The conditions on the kernel function , Assumptions 3(a)–(b), are identical to those in Jansson (2002). Jansson (2002) remarks that these assumptions “would appear to be satisfied by any kernel in actual use”. Commonly used kernel functions such as the Bartlett, Parzen, and Quadratic Spectral kernels indeed satisfy all these assumptions. Assumption 3(c) differs from the usual requirement, , by a factor . The difference is caused by the estimation error in . This error causes the residuals to be less close to the innovations and we balance this by including autocovariance matrices of higher lags at a slower pace.

3.2 Simulation-Based Inference

The limiting distribution in Theorem 1 is nonpivotal and thus not directly suited for inference. Some popular solutions for linear-in-parameters cointegration models are: Saikkonen’s (1992) dynamic least squares, the integrated modified OLS and fixed- approaches by Vogelsang and Wagner (2014), and the fully modified approach advocated in Phillips and Hansen (1990) and Phillips (1995). For a nonlinear-in-parameter model as in (2.1), a preliminary Monte Carlo exercise555The details are available in Section S5 of the Supplementary Material. The analytical results in that appendix also suggest that the convergence speed of to is too slow to recover the standard zero-mean Gaussian limiting distribution. shows poor performance for fully modified inference but promising results for a simulation based approach. We pursue the latter method for the remainder of this paper.

The main idea behind the simulation based approach is to replace nuisance parameters by consistent estimates and to rely on Monte Carlo (MC) simulations to approximate the limiting distribution. The empirical quantiles of these MC draws allow us to conduct inference. Clearly, this kind of approach will provide exact inference when the limiting distribution is invariant with respect to the nuisance parameters (e.g. Dufour and Khalaf (2002) and Dufour (2006)). In the absence of such invariance, Wang et al. (2018) and Bergamelli et al. (2019) show that the simulation approach remains asymptotically justified in several model specification. We adapt the algorithm from Wang et al. (2018) to the current setting and prove its asymptotic validity.

Algorithm 1 (Simulation-Based Inference)

-

Step 1:

Estimate and use the residuals to compute the estimators and from (3.2).

-

Step 2:

Repeat for ,

-

(a)

Draw random variables i.i.d. from .

-

(b)

Compute and the partial sum .

-

(c)

Let , where with (for ). For a given , construct the th simulated draw as

where is a consistent estimator of the lower-left subblock of , and with .

-

Step 3:

Use the empirical quantiles of elements of to conduct inference.

Algorithm 1 uses a discretisation in steps to approximate the limiting distribution of the parameters. In practice, and in accordance with Theorem 3, we can take . Remark 3 details how simulation-based inference can be used to test hypotheses concerning the model’s parameters. Discussions on size and power are also presented there.

Theorem 3 establishes the asymptotic validity of the simulation approach. That is, for a large enough , the empirical quantiles of the simulated distribution will coincide with the asymptotic distribution. Two remarks are important. First, even though the simulation algorithm is adapted from Wang et al. (2018), the proof of Theorem 3 is not. In particular, the method of proof is similar to Theorem 1 and continues to allow for endogeneity of the regressors. Second, the simulation approach mimics the stochastic integrals in the limiting distribution directly. It therefore suffices to draw normally distributed random variables in Step 2(a) and use consistent long-run covariance estimates to replicate the covariance structure of the underlying Brownian motions. Compared to a bootstrap procedure, this simulation approach has the advantage of avoiding tedious NLS re-estimation on bootstrap samples but it comes at the cost of forsaking possible asymptotic refinements.

Remark 3

Step 3 in Algorithm 1 has been kept general for notational convenience. An illustrative example is as follows. Assume we are interested in (irrelevance of the regressor ) when

Under , we have with being the kth basis vector in . Denoting the empirical -quantiles of by , a test of size will reject for or . Under the alternative , we rewrite the test statistic as . Statistical power is guaranteed because the simulation approach mimics the asymptotic distribution and is thus bounded, whereas the second term diverges.

3.3 KPSS-Type Test for the Null of Cointegration

The correct specification of the nonlinear cointegrating relation will result in a stationary error process . We consider a KPSS-type test statistic for the null of stationarity. The candidate statistic is , where and is a consistent estimator of . This statistic is stochastically bounded under the null hypothesis but diverges under the alternative. Rejections of the null hypothesis are an indication of a spurious relationship and/or an incorrect functional form of the nonlinear cointegrating relationship. Several authors have reported model settings in which the asymptotic null distribution of is known, e.g. Kwiatkowski et al. (1992) and Wagner and Hong (2016).

The estimation of contaminates the limiting distribution of with nuisance parameters.666Proposition 5 in Wagner and Hong (2016) shows that the limiting distribution of is free of nuisance parameters if is known and only a single integrated regressor occurs with integer powers greater than one. This result does not carry over to the current setting because of the estimation error in . Choi and Saikkonen (2010), Wagner and Hong (2016), Jiang et al. (2019), and Lin and Reuvers (2020), have shown that subsampling can resolve this issue. We will follow their approach and use subsamples of size to compute the test statistics.

Theorem 4

Theorem 4 does not provide any guidance on the choices for the starting value and the subsample size . First, for a given , Choi and Saikkonen (2010) argue that the use of a single subsample (instead of all observations) implies a significant loss of power. We follow their example and combine all subresidual series of length using a Bonferroni procedure. That is, we create subresiduals series by selecting adjacent blocks of residuals while alternating between the start and end of the sample. We calculate the KPSS-type test statistic for each subseries, say , and reject the null of stationarity at significance whenever exceeds which is defined by . Finally, we select the block size using Romano and Wolf’s (2001) minimum volatility rule. The approach is now completely data-driven.

4 Simulations

This section lists various Monte Carlo simulations showing that the asymptotic approximations from Section 3 provide useful guidance in finite samples. Further details on the implementation are as follows. The long-run covariance matrices in (3.2) are computed using the Barlett kernel, for (and zero otherwise), and the bandwidth selection method described in Andrews (1991). Simulated limiting distributions are based on replicates and we set . We test at 5% significance and report results based on Monte Carlo replications. Two data generating processes are studied: DGP1 and DGP2.

DGP1: Empirical size and power of the coefficient tests

This DGP is inspired by the simulation study in Wagner et al. (2020). It augments their quadratic seemingly unrelated cointegrating polynomial regression model with a global flexible trend. That is, we consider

| (4.1) |

and compute and recursively as

All recursions are initialized from zero, i.e. (). The innovations and are drawn independently as and , where

Regarding the global trend in (4.1), we set and consider . All other coefficient values are inspired by Wagner et al. (2020). That is, , and are identical across equations.777This homogenous parametrisation is particularly convenient to study the impact of the cross-sectional dimension. That is, we can vary without having to provide additional parameter values. DGP2 is directly inspired by the empirical application and thus more realistic. Also, we let and redefine these four parameters as . We vary , , and . In line with the typical EKC application, we test for the significance of . We set for and report the empirical size of the single equation test for and the joint test for .

| SimNLS | SimNLS() | FM-SOLS() | FM-SUR() | SimNLS | SimNLS() | FM-SOLS() | FM-SUR() | SimNLS | SimNLS() | FM-SOLS() | FM-SUR() | |||

| Panel A: Single-equation test | ||||||||||||||

| 0 | 4.77 | 4.63 | 9.53 | 10.77 | 4.43 | 4.90 | 10.03 | 12.80 | 4.37 | 4.47 | 9.70 | 16.63 | ||

| 0.3 | 4.80 | 4.77 | 10.47 | 11.97 | 4.53 | 4.63 | 10.00 | 13.00 | 4.23 | 4.27 | 11.60 | 19.00 | ||

| 0.6 | 4.83 | 4.53 | 11.90 | 12.93 | 3.93 | 4.17 | 11.87 | 16.50 | 5.13 | 4.90 | 14.23 | 31.70 | ||

| 0.8 | 4.50 | 4.67 | 14.00 | 19.10 | 4.90 | 4.60 | 15.23 | 26.53 | 5.27 | 4.43 | 16.83 | 56.47 | ||

| 0 | 4.43 | 4.10 | 8.03 | 8.63 | 4.43 | 4.20 | 7.33 | 8.33 | 4.50 | 4.67 | 8.60 | 11.73 | ||

| 0.3 | 4.20 | 4.60 | 8.13 | 9.20 | 4.37 | 4.77 | 8.97 | 9.80 | 4.43 | 4.23 | 8.67 | 12.83 | ||

| 0.6 | 5.80 | 5.70 | 10.23 | 11.80 | 4.97 | 4.97 | 10.17 | 12.73 | 4.40 | 4.30 | 10.83 | 18.77 | ||

| 0.8 | 4.97 | 4.43 | 11.17 | 13.40 | 4.60 | 4.53 | 12.07 | 19.37 | 4.03 | 3.53 | 13.67 | 36.53 | ||

| 0 | 4.67 | 4.67 | 7.00 | 7.20 | 4.77 | 4.73 | 6.57 | 7.53 | 4.27 | 4.23 | 7.37 | 9.20 | ||

| 0.3 | 4.77 | 4.37 | 7.67 | 7.77 | 4.43 | 4.73 | 7.37 | 7.40 | 4.80 | 4.67 | 7.90 | 9.57 | ||

| 0.6 | 5.60 | 5.07 | 9.43 | 9.50 | 5.43 | 5.43 | 8.77 | 10.30 | 5.30 | 4.83 | 9.57 | 14.10 | ||

| 0.8 | 4.70 | 4.50 | 8.73 | 9.20 | 5.10 | 5.23 | 9.27 | 13.87 | 5.80 | 5.20 | 11.47 | 24.63 | ||

| Panel B: Joint test | ||||||||||||||

| 0 | 4.23 | 4.03 | 12.70 | 15.10 | 4.10 | 4.07 | 14.50 | 21.57 | 3.63 | 3.47 | 25.67 | 51.23 | ||

| 0.3 | 4.80 | 4.57 | 14.37 | 17.33 | 3.80 | 3.70 | 19.50 | 26.90 | 3.70 | 3.77 | 31.63 | 59.73 | ||

| 0.6 | 4.27 | 4.03 | 18.03 | 22.07 | 3.80 | 3.57 | 23.67 | 37.77 | 3.13 | 3.03 | 40.27 | 82.17 | ||

| 0.8 | 3.13 | 2.93 | 23.37 | 30.47 | 3.33 | 2.73 | 31.60 | 57.20 | 2.00 | 1.50 | 49.73 | 82.60 | ||

| 0 | 4.80 | 4.73 | 10.07 | 10.87 | 4.30 | 4.37 | 10.63 | 14.83 | 3.77 | 3.80 | 18.17 | 31.80 | ||

| 0.3 | 4.77 | 4.97 | 11.60 | 12.93 | 4.67 | 4.67 | 14.03 | 17.70 | 3.40 | 3.47 | 19.13 | 36.53 | ||

| 0.6 | 4.93 | 4.40 | 14.33 | 14.87 | 3.77 | 3.90 | 17.50 | 25.63 | 3.10 | 3.10 | 29.20 | 59.97 | ||

| 0.8 | 3.87 | 3.40 | 17.40 | 20.97 | 3.33 | 2.77 | 22.97 | 38.80 | 2.60 | 2.13 | 37.87 | 86.33 | ||

| 0 | 4.27 | 4.53 | 7.37 | 8.03 | 4.33 | 4.13 | 8.50 | 10.83 | 3.97 | 4.07 | 12.90 | 19.23 | ||

| 0.3 | 4.93 | 5.17 | 9.23 | 10.00 | 4.80 | 4.53 | 10.57 | 12.30 | 4.60 | 4.50 | 14.87 | 24.03 | ||

| 0.6 | 4.07 | 3.80 | 11.63 | 12.43 | 4.57 | 4.73 | 12.30 | 16.97 | 4.30 | 4.23 | 21.73 | 38.80 | ||

| 0.8 | 5.00 | 4.53 | 12.77 | 14.37 | 3.57 | 3.80 | 15.67 | 25.33 | 3.60 | 3.57 | 26.43 | 66.63 | ||

For , the empirical size of various tests are displayed in Table 2.888The results for and are qualitatively the same. For brevity, we do not include these results in the main paper. The interested reader can find such simulation results in Section S6 of the Supplementary Material. These tests are based on four estimators: (1) the NLS estimator with simulated critical values as described in Section 3.2 (SimNLS); (2) the NLS estimator with simulated critical values and the true value for being provided (SimNLS()); (3) the FM-SOLS estimator based on (FM-SOLS()); and (4) the FM-SUR estimator based on (FM-SUR()). The main findings are as follows:

-

(a)

The simulation-based approaches SimNLS and SimNLS() offer better size control. The size improvements are particularly pronounced when and . The differences in the empirical size of SimNLS and SimNLS() are small.

-

(b)

Size distortions are more severe when increases and/or a joint test is performed. The same observation was made in Wagner et al. (2020). The behaviour of the simulation-based and fully modified tests is opposite in these cases. SimNLS and SimNLS() tend to become conservative whereas FM-SOLS and FM-SUR are oversized.

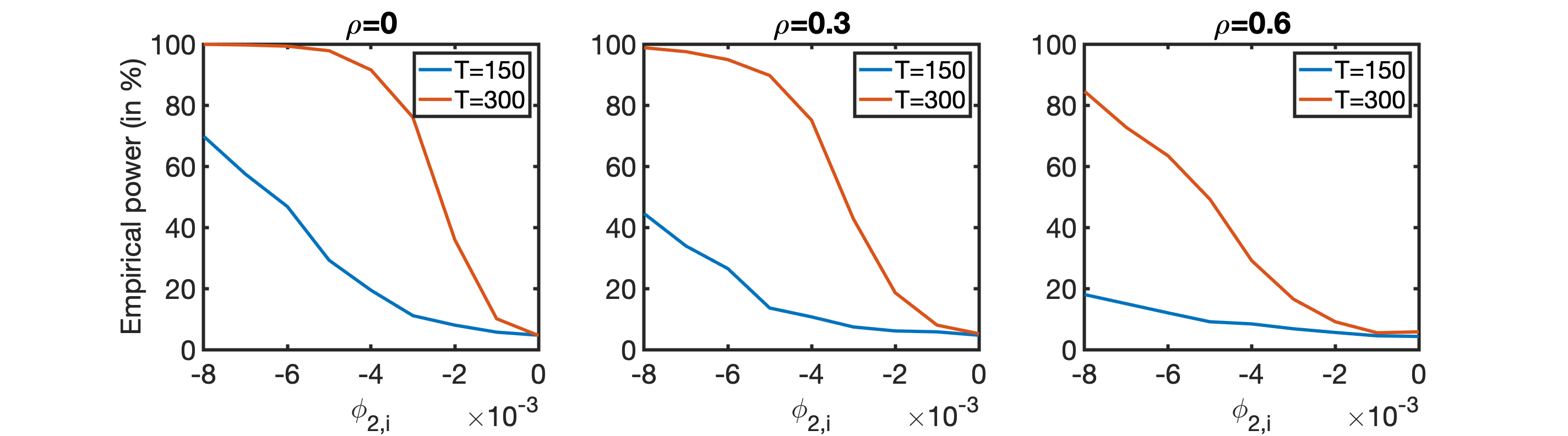

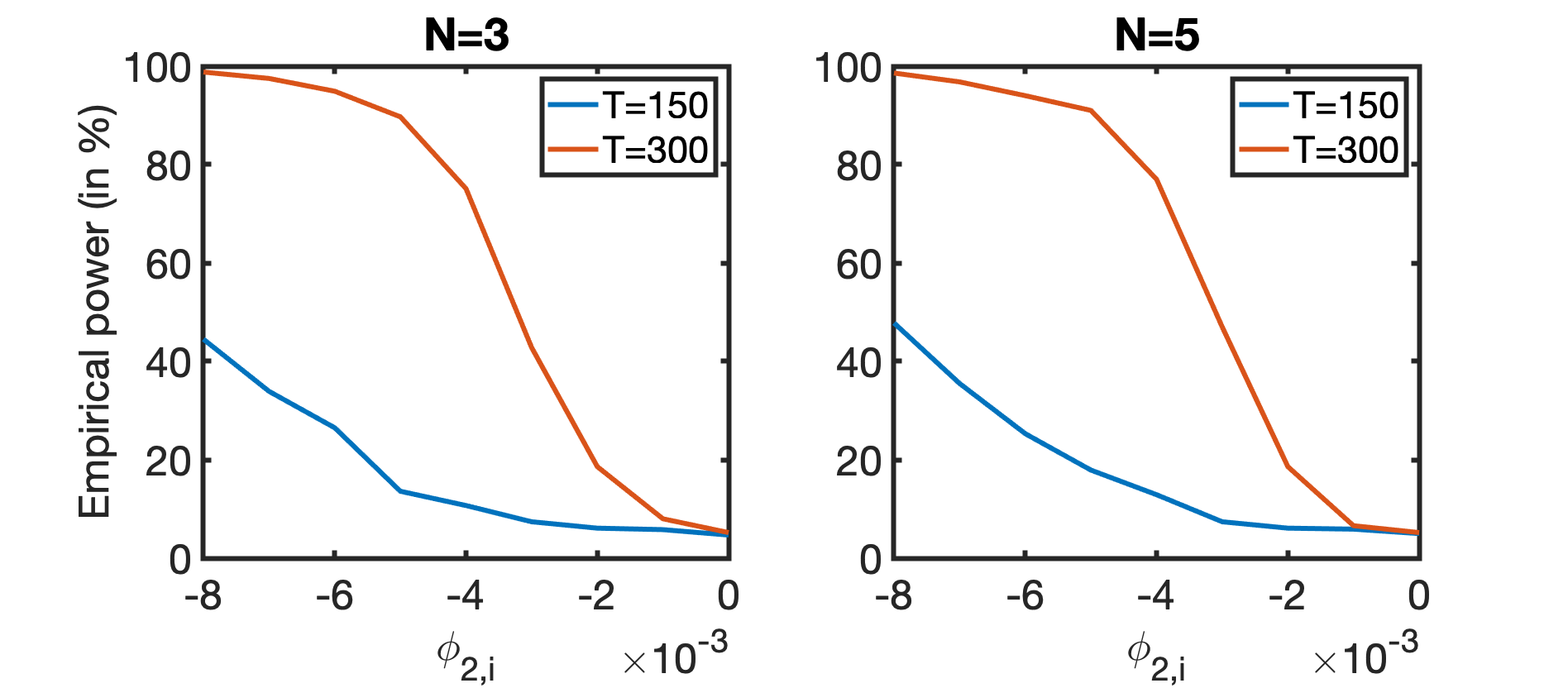

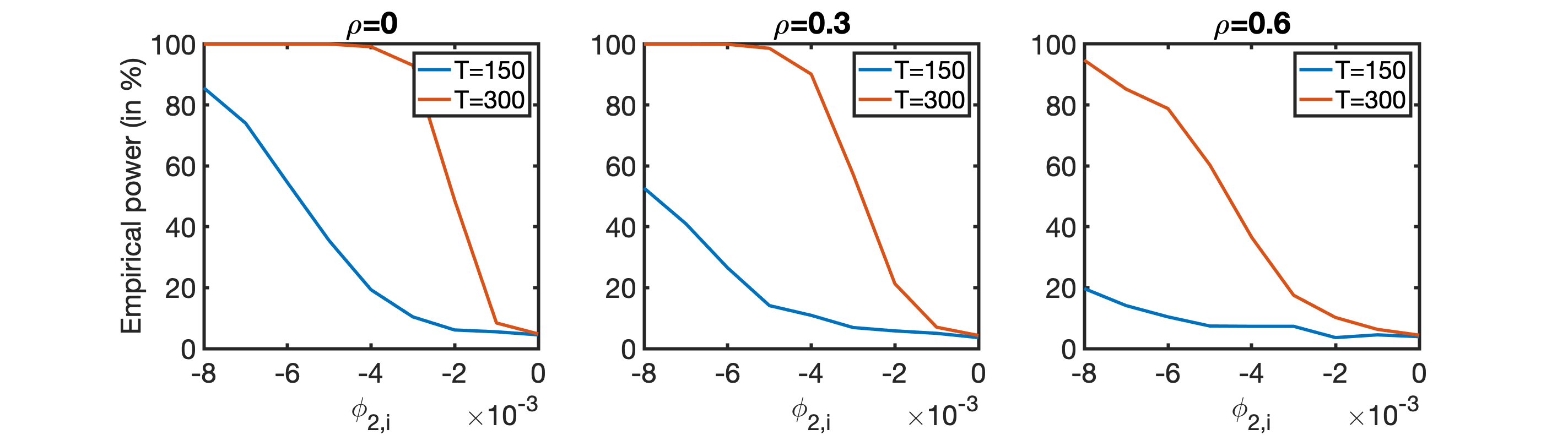

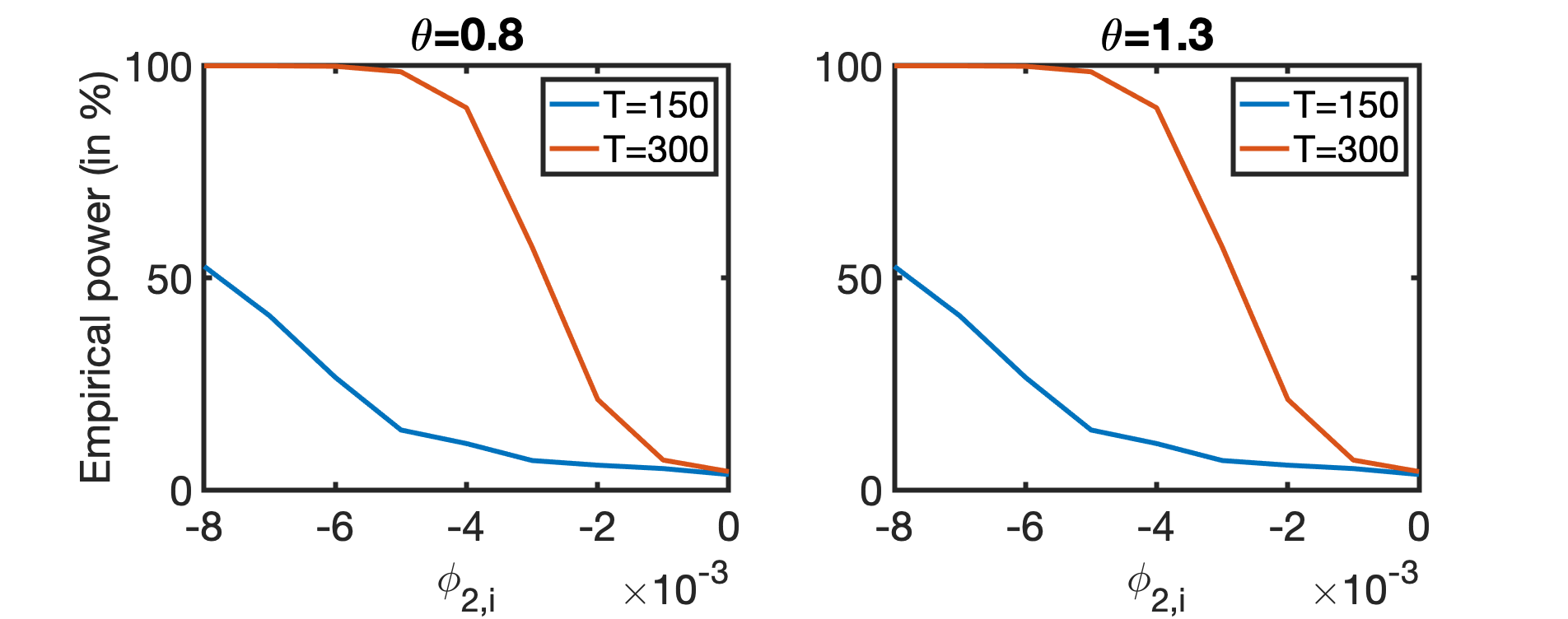

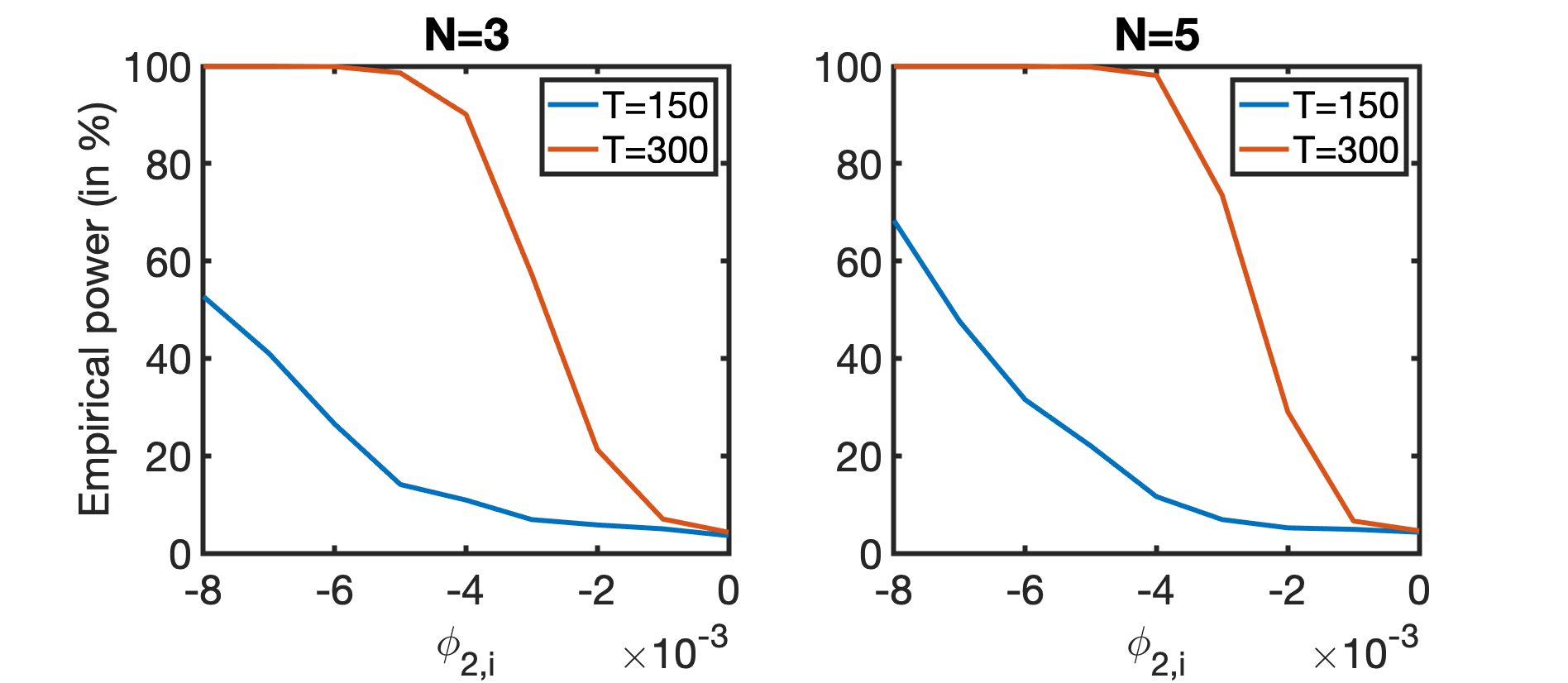

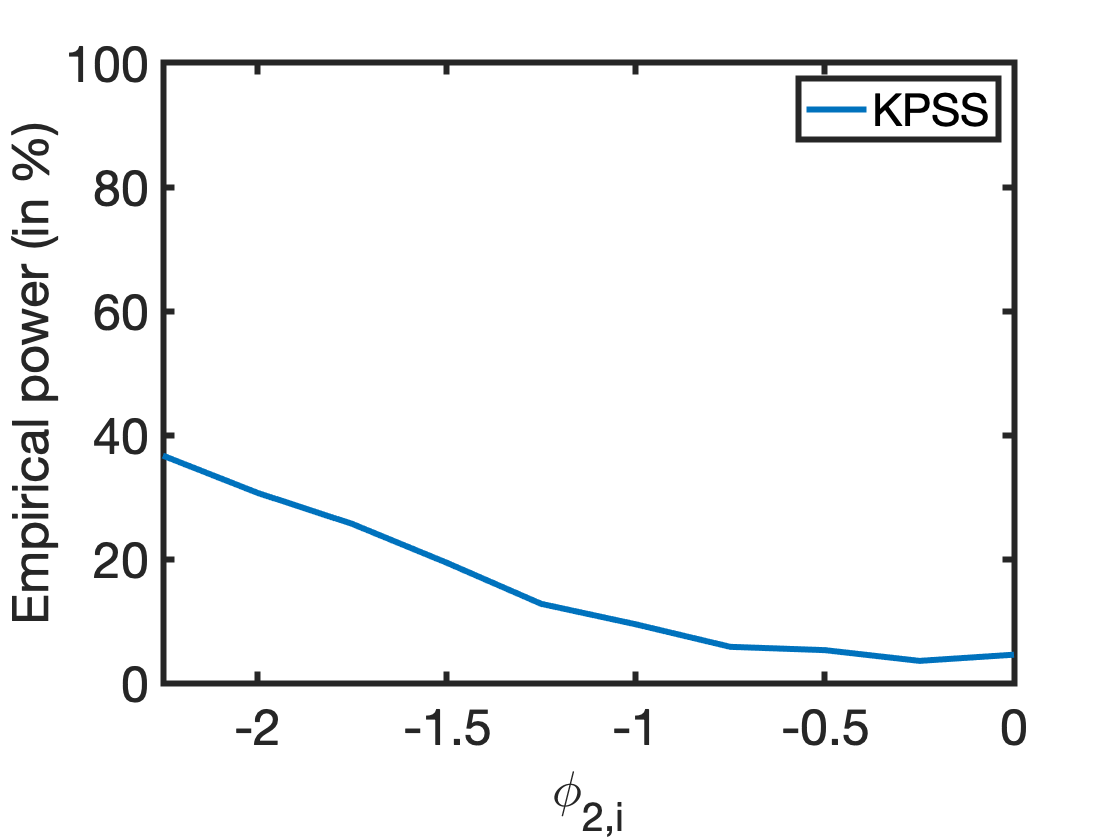

We subsequently simulate power curves.999Power curves are computationally more intensive. We economize computational time by (1) reducing the number of Monte Carlo replicates to 1,000 and (2) investigating a subset of all possible parameter configurations. The specification of the single equation test and joint test are as before but we now vary over the set . We take , and as the baseline scenario and subsequently vary these quantities one-by-one. Figures 1–2 show the results. As expected, power increases with increasing sample size, and as moves away from zero.

DGP2: Illustrative simulations in line with the empirical application

Our second set of simulations is tailored towards the empirical application. That is, we employ parametrizations that mimic the distributional properties of data. Generally speaking, we first estimate the baseline model specification on the data and subsequently fit a VAR(1) specification on the stacked vector of residuals and first-differenced explanatory variables.101010All details on the simulation designs for DGP2(a)–(c) are available in Section S7 of the Supplementary Material. In line with the empirical application, these simulations use and . All results are displayed in Figure 3. Below, we motivate the simulation settings in view of the EKC application and draw conclusions.

-

(a)

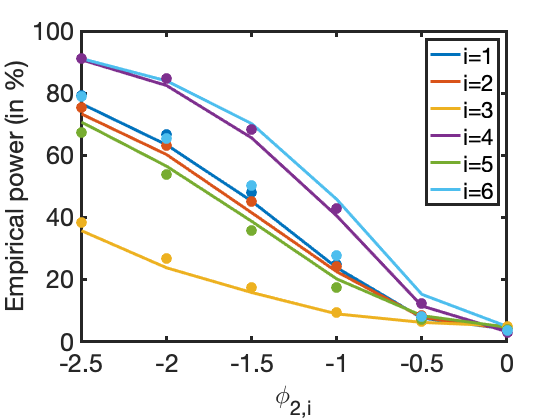

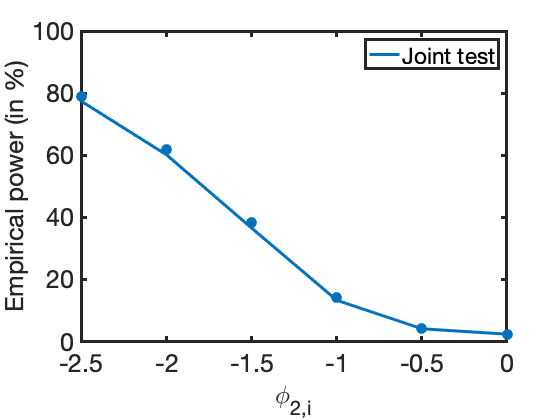

Correctly specified model: The specification with is estimated on the data. We subsequently move away from zero in the DGP and check whether we can detect the resulting curvature caused by the integrated variable. Power curves for the individual and joint test for the coefficients in front of are found in Figures 3(a) and 3(b), respectively. Clearly, nonlinear effects due to are detectable. The statistical power varies across units because (contrary to DGP1) time series properties are now heterogenous across equations.

-

(b)

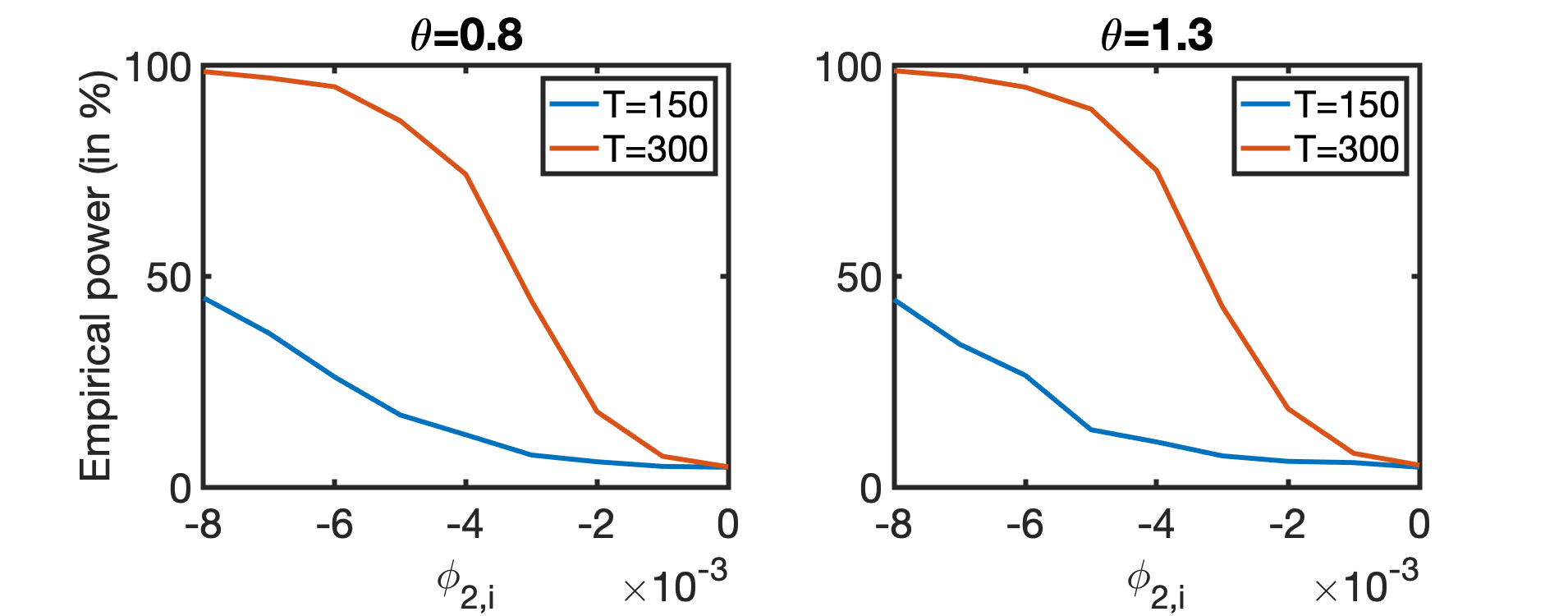

Redundant global trend: Assumption 1 requires the global trend to be relevant. This simulation DGP investigates how violations of this assumption affect the typical EKC coefficient test. We obtain parameter values by fitting the model with . As in (a), we vary and test for the significance of these parameters.

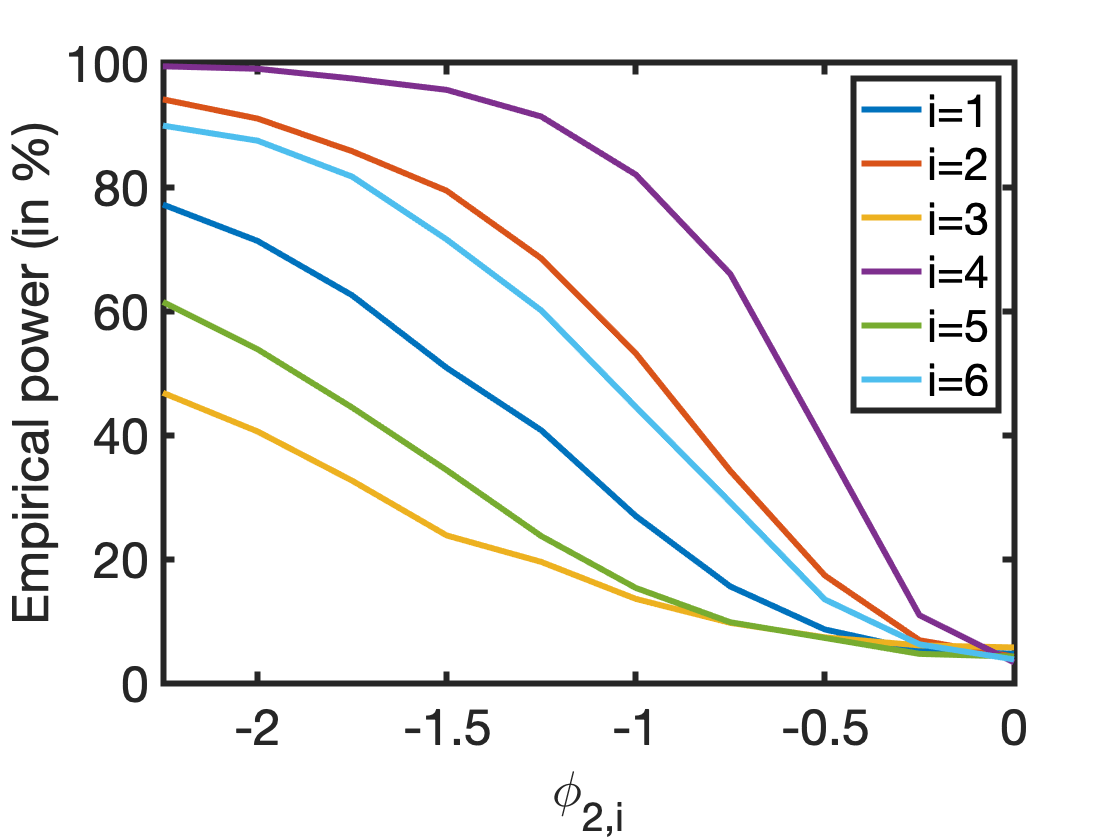

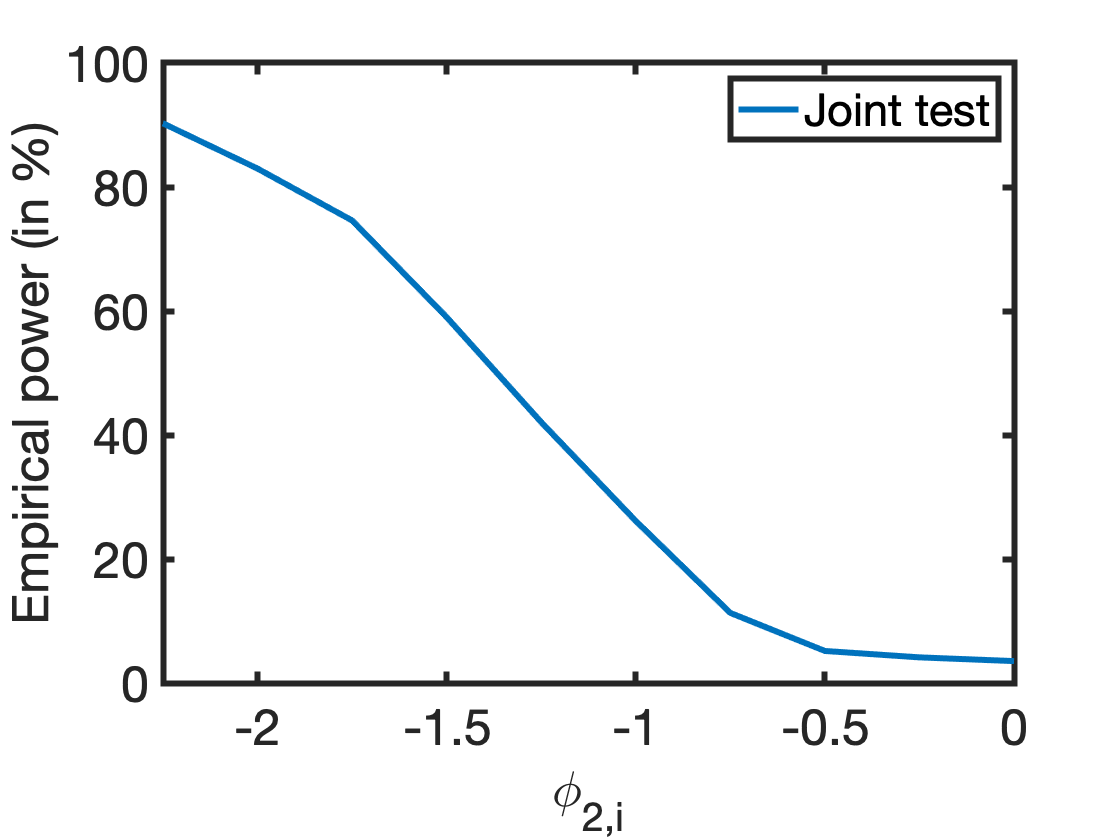

The solid lines in Figures 3(c) and 3(d) are power curves obtained using the correctly specified DGP whereas markers indicate the power when a redundant global trend is estimated as well. The redundant trend has virtually no influence on the statistical power of the coefficient tests of the first five series. There is a power loss for . An inspection of the coefficients offers an explanation. The estimated coefficients in front of the global trend are mostly small ( to ) and thus irrelevant. However, in a fraction of cases the flexible trend mimics the curvature in the th series causing the quadratic stochastic trend to become insignificant. As reported in the introduction, the power of the joint test does not suffer from the inclusion of a redundant trend.

-

(c)

KPSS test: Nonstationary residuals are an indication of model misspecification. That is, either the regression is spurious or the functional form of the cointegrating relation is misspecified. We look at the latter situation. The simulation DGP is the quadratic GCPR as in DGP2(a) but the quadratic component is missing in the fitted model. The empirical rejection frequency of the KPSS test (Figure 3) is signalling that there are specification issues. However, a comparison with Figures 3(a) and 3(b) also reveals that if the source of misspecification is known, then a dedicated coefficient test leads to higher power.

5 Empirical Application

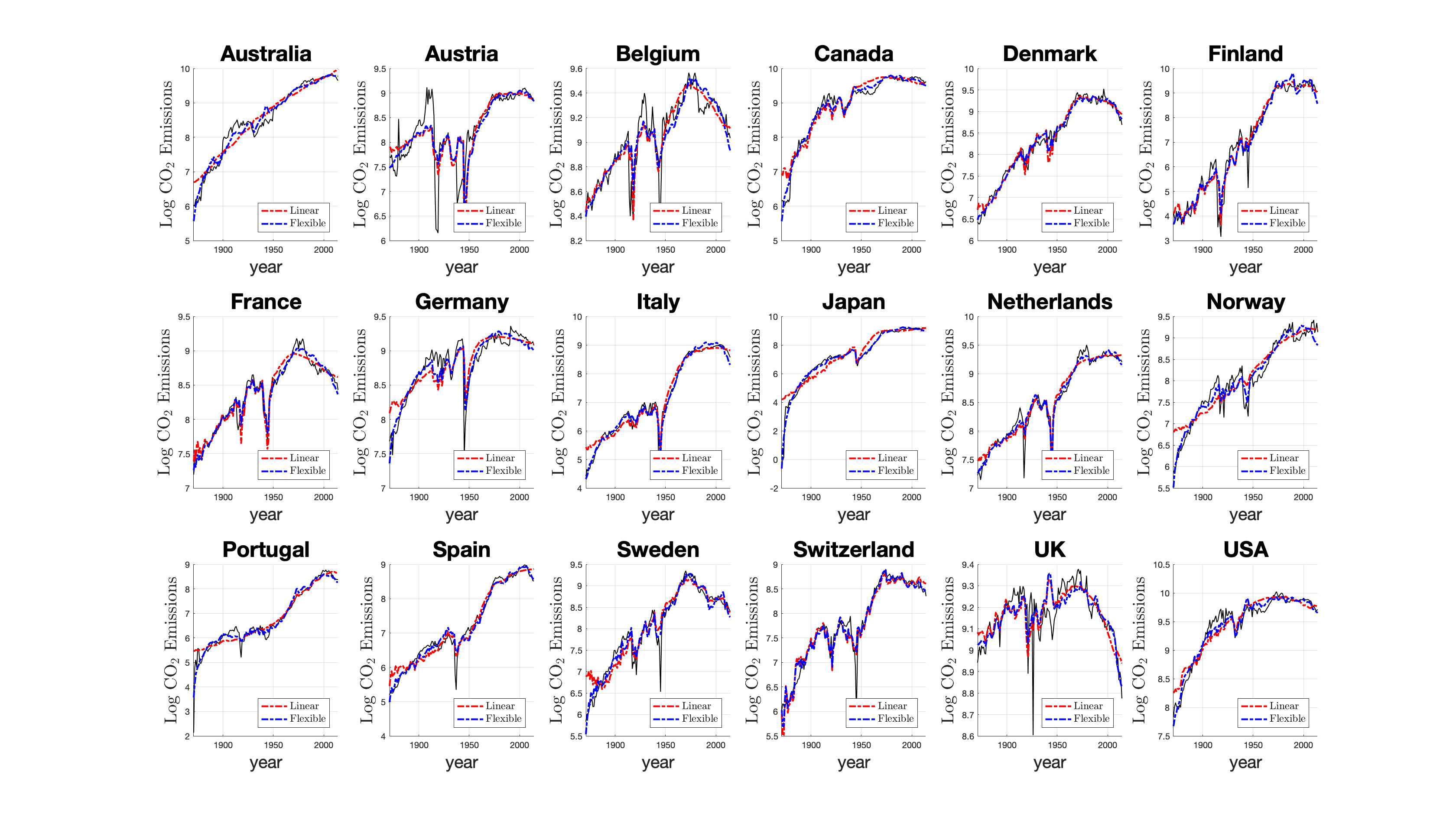

We examine the evidence for an EKC for a collection of 18 countries over the period 1870–2014 (). Economic growth is measured by GDP and we use carbon dioxide (CO2) emissions as a proxy for air pollution. The origin of these data is as follows. We use population and GDP data from the Maddison Project (see https://www.rug.nl/ggdc/historicaldevelopment/maddison/). Our carbon dioxide observations are fossil-fuel CO2 emissions as made available by the Carbon Dioxide Information Analysis Center (CDIAC, see https://cdiac.ess-dive.lbl.gov). The CDIAC database ceased operation in 2017 causing these time series to be available until 2014. Both GDP and CO2 emissions are expressed per capita and subsequently log-transformed. In accordance with the notation of this paper, we will denote them by and , respectively. The same data (or subsets thereof) have also been studied by Wagner (2015), Chan and Wang (2015), Wang et al. (2018), Wagner et al. (2020), and Lin and Reuvers (2020).111111The stationarity properties of the series have been extensively studied and discussed in these papers. We will not repeat this analysis but refer the interested reader to Section S8 of the Supplement. The exact numbers may show (minor) differences from previously reported results due to differences in: (1) the time span of the data, (2) the implemented long-run covariance estimator, and (3) the scaling of the data. Related to scaling, we follow the official guidelines and multiply by 3.667 and to convert thousand of metric tons of carbon into units of carbon dioxide. Since the data will be expressed in logarithms, this rescaling effectively amounts to a change of intercept. This conveniently allows us to compare results. All user choices (kernel specification, bandwidth selection, etc.) are kept the same as during the simulation study (see page 4).

5.1 An Illustration using Belgian Data

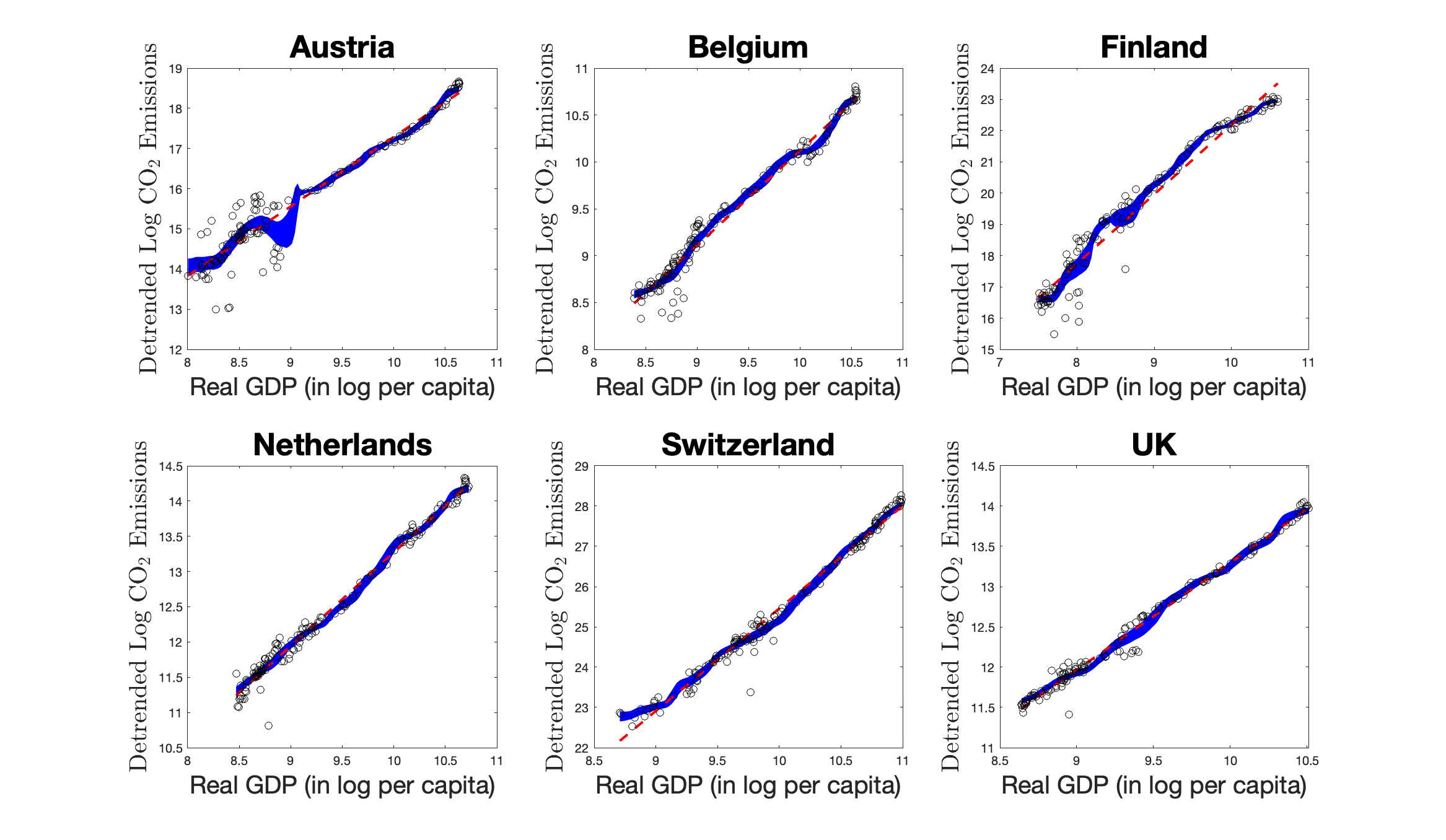

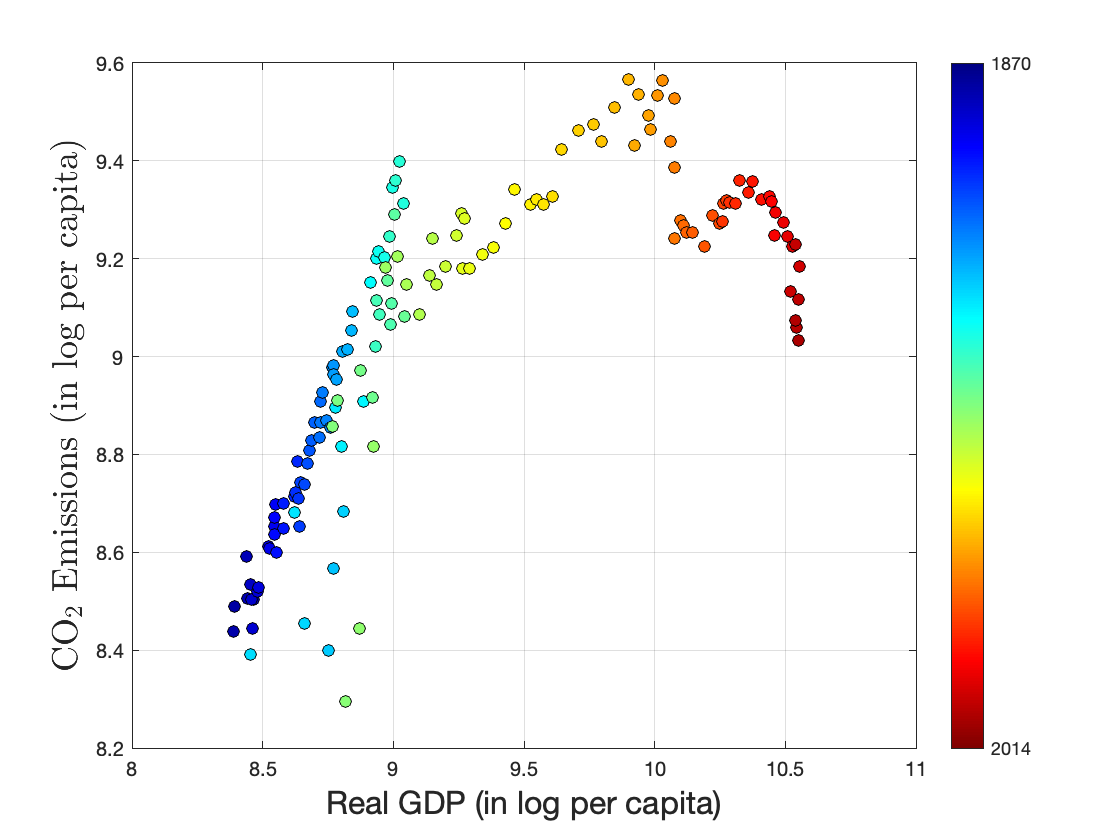

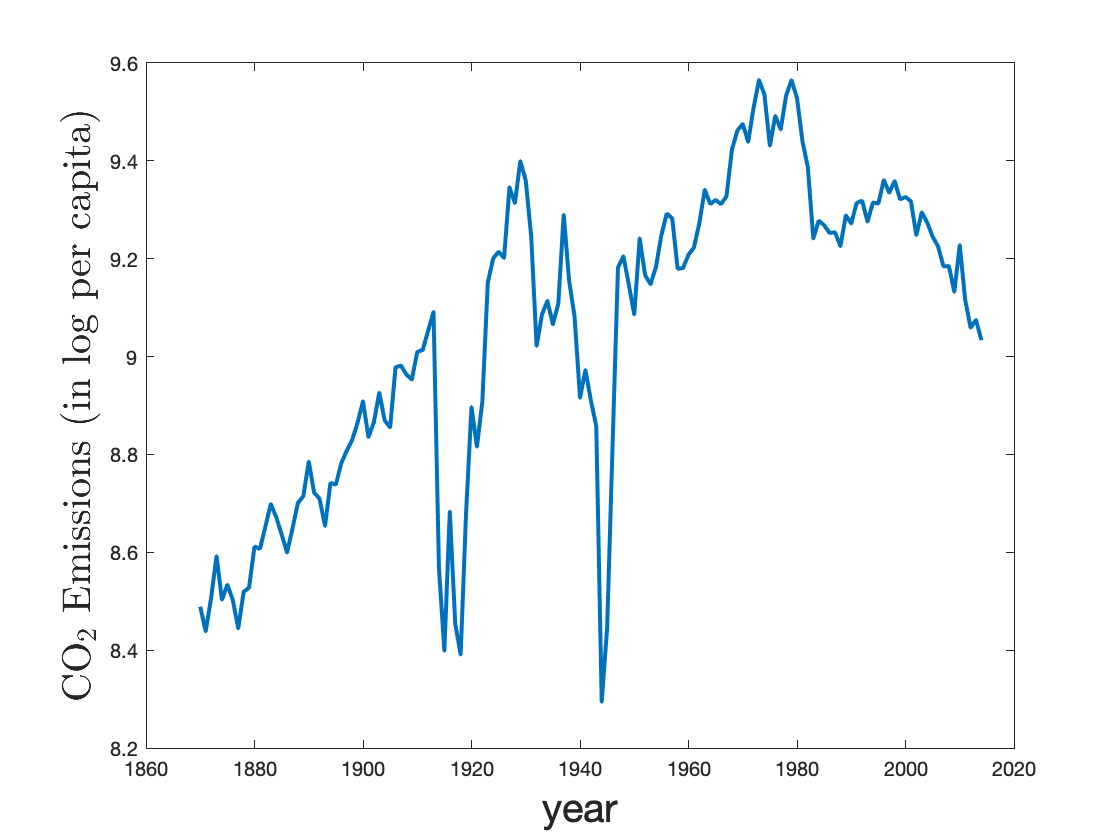

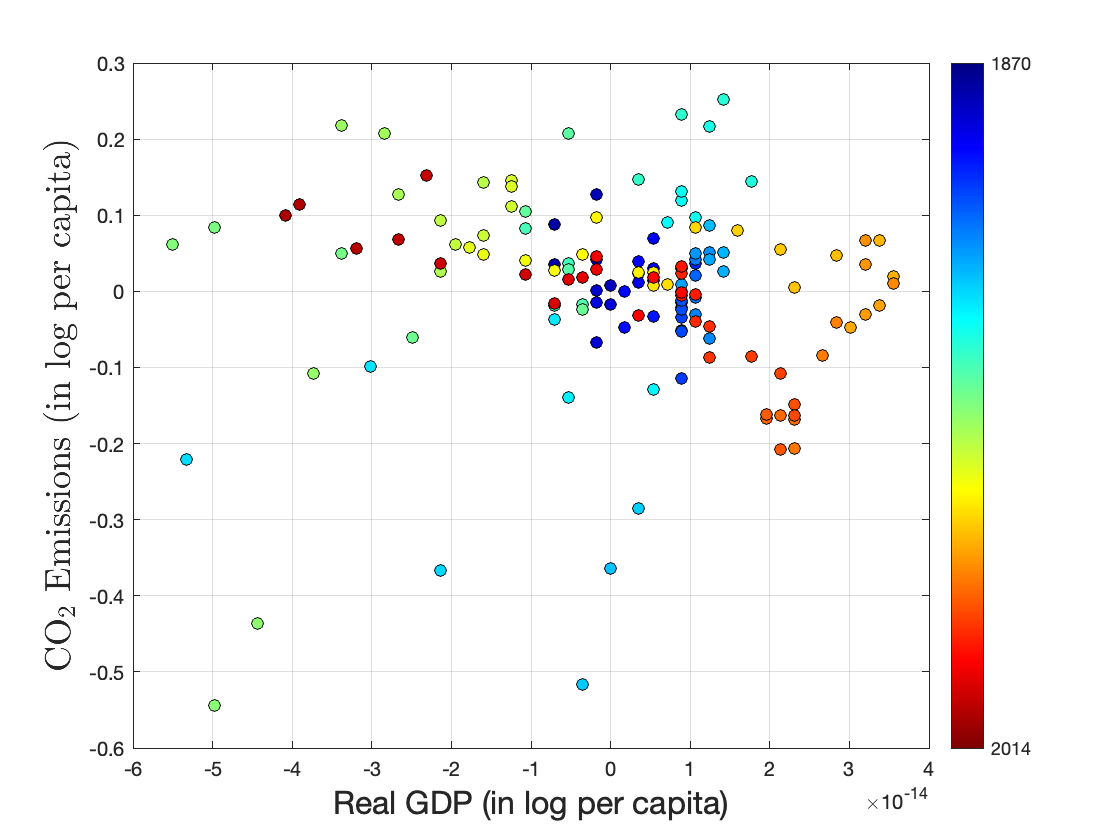

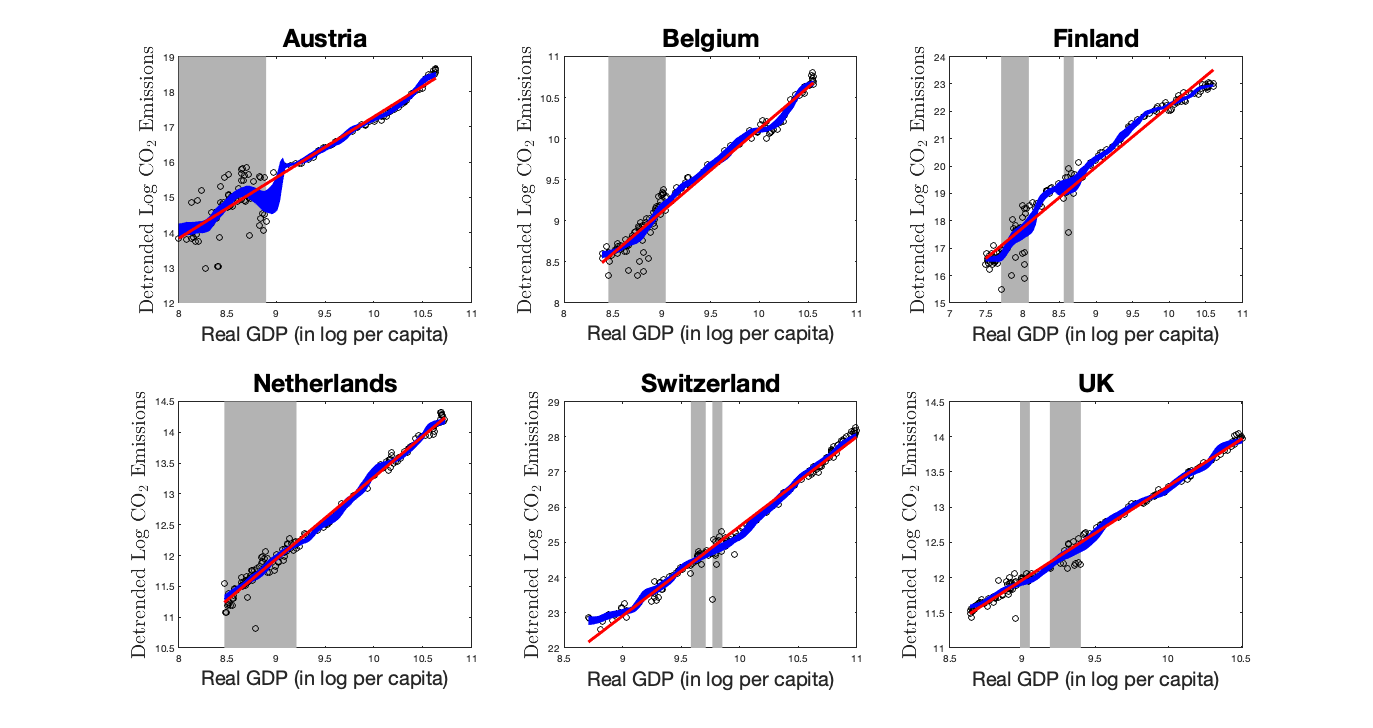

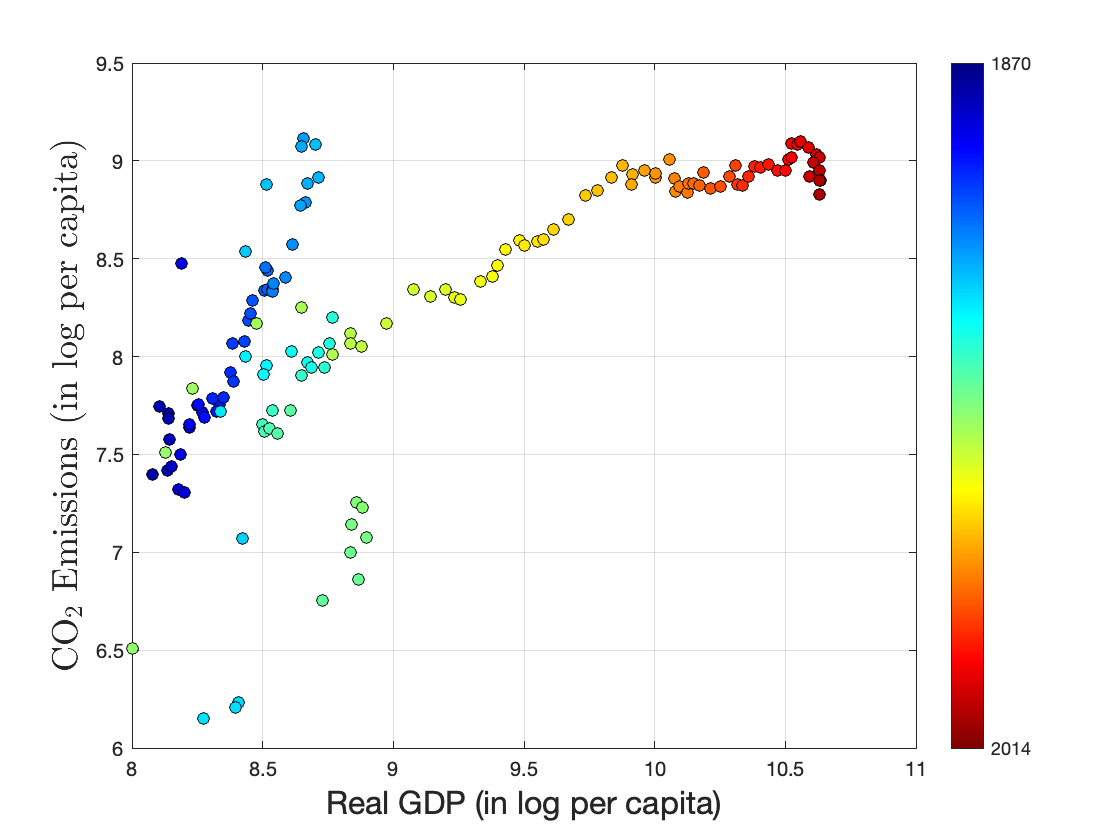

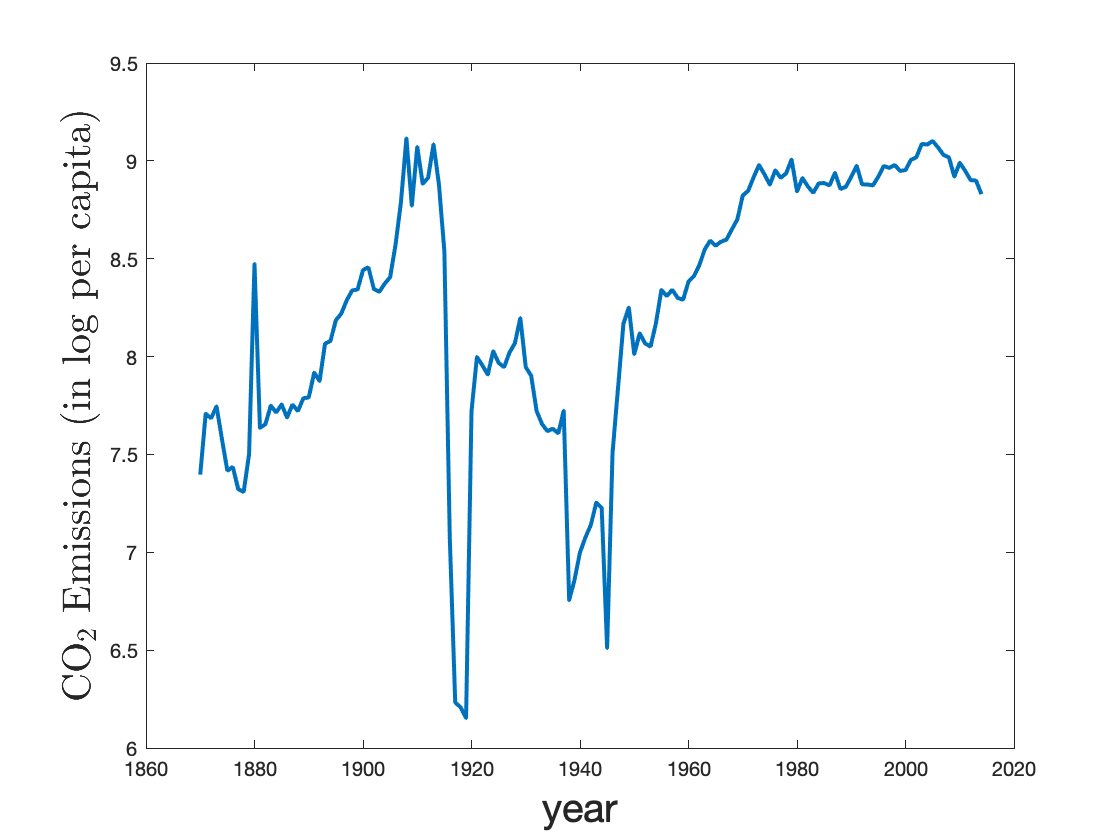

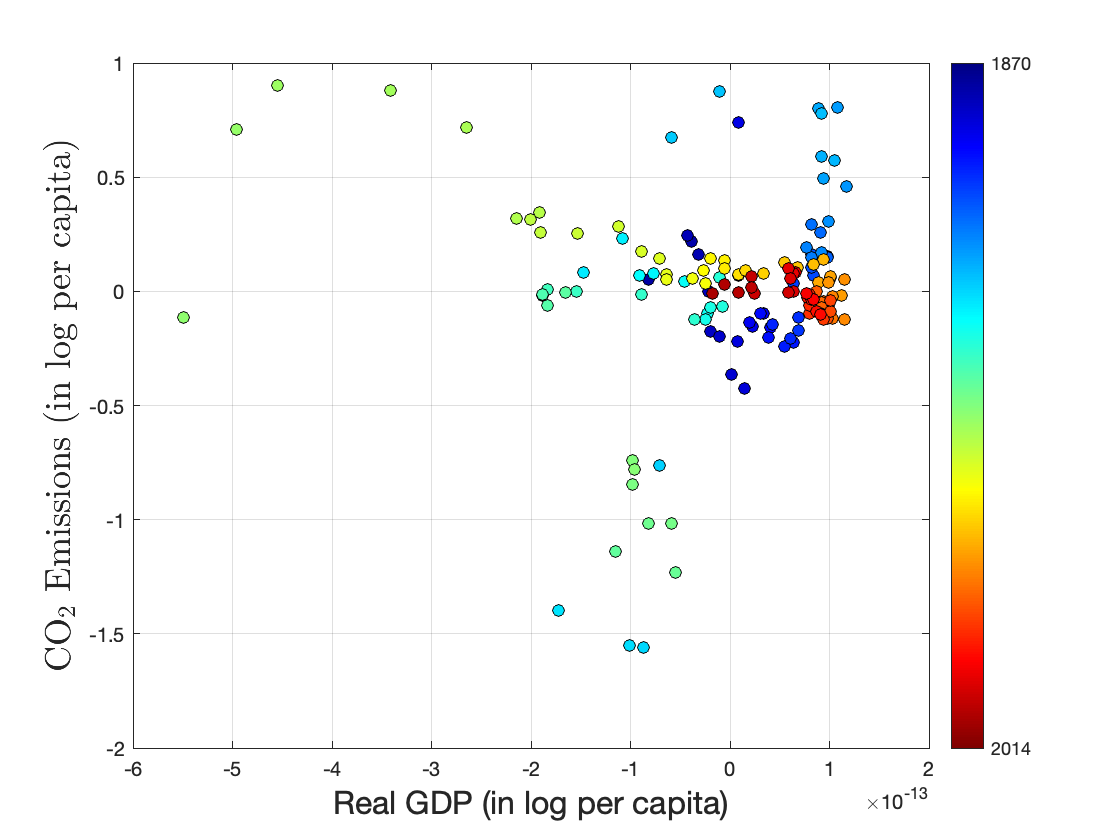

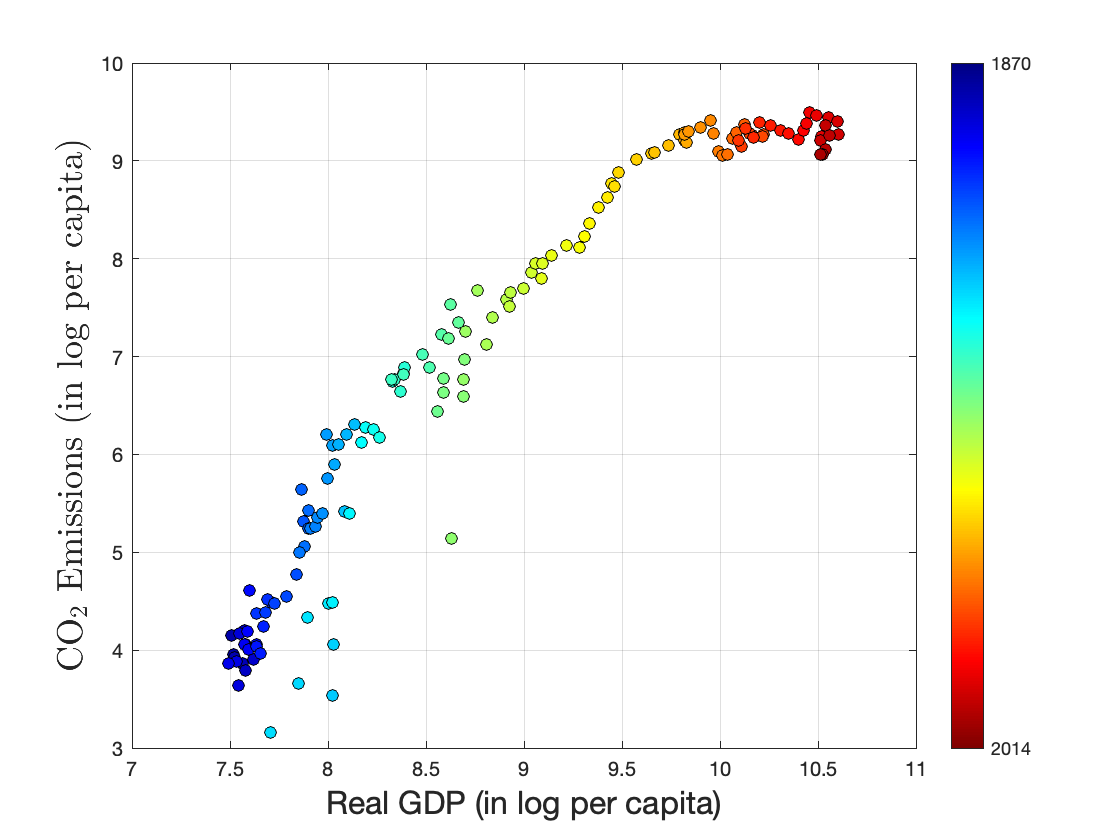

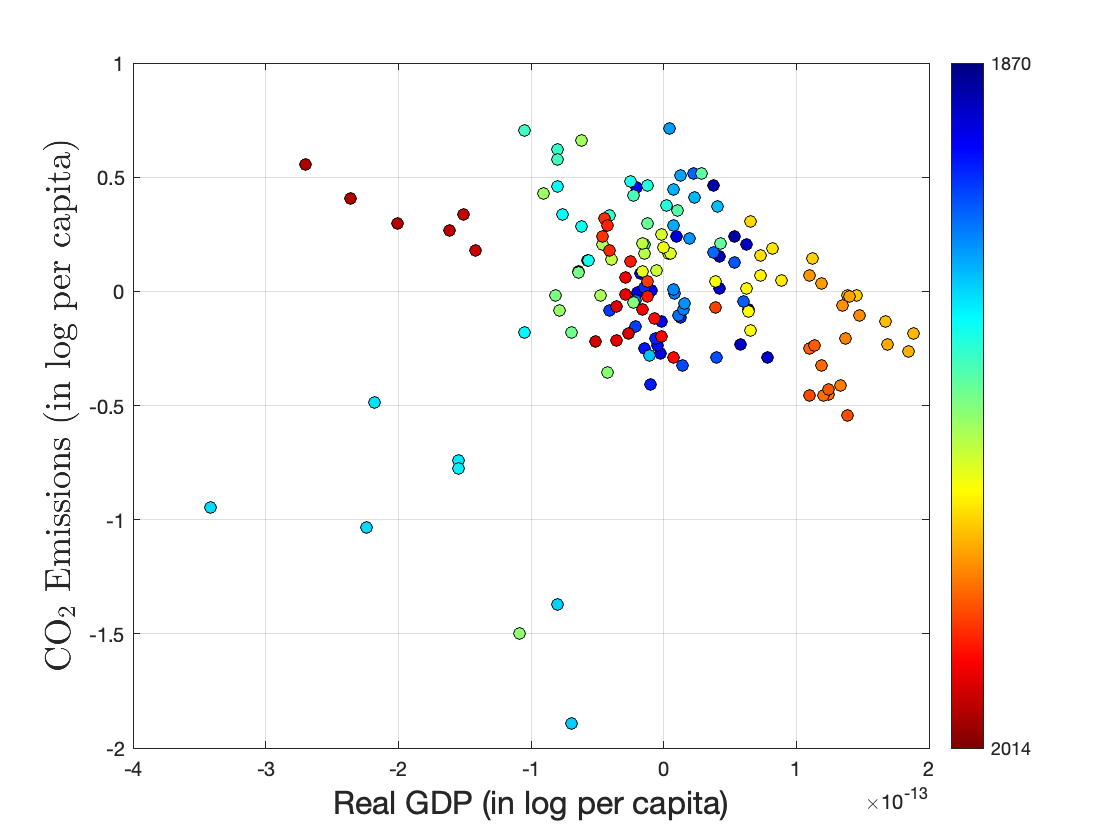

Prior to the analysis of a multivariate specification, we will first discuss several features of the individual time series (hence omitting subscripts “”). The example throughout this narrative is Belgium (Figure 4).121212The data for Austria, Belgium, and Finland are mentioned in both Wagner (2015) and Wagner et al. (2020) to behave in line with the EKC. We discuss Belgium in the main text but the interested reader can find the same figures for Austria and Finland in Section S8.3. Qualitatively, the findings for these other two countries are the same. An inverted U-shaped relationship between GDP and CO2 (both in log per capita) is clearly visible in Figure 4(a) and behavior like this has triggered research on the Environmental Kuznets Curve. However, the time heat map also shows that time is almost monotonically increasing along the curve. Time effects – e.g. increasing global environmental awareness, worldwide advances in sustainable technologies – can be valid alternative explanations for these nonlinearities and their omission can (falsely) exaggerate the influence of GDP. It is for this reason that we develop and analyse the Generalized Cointegrating Polynomial Regression (GCPR).

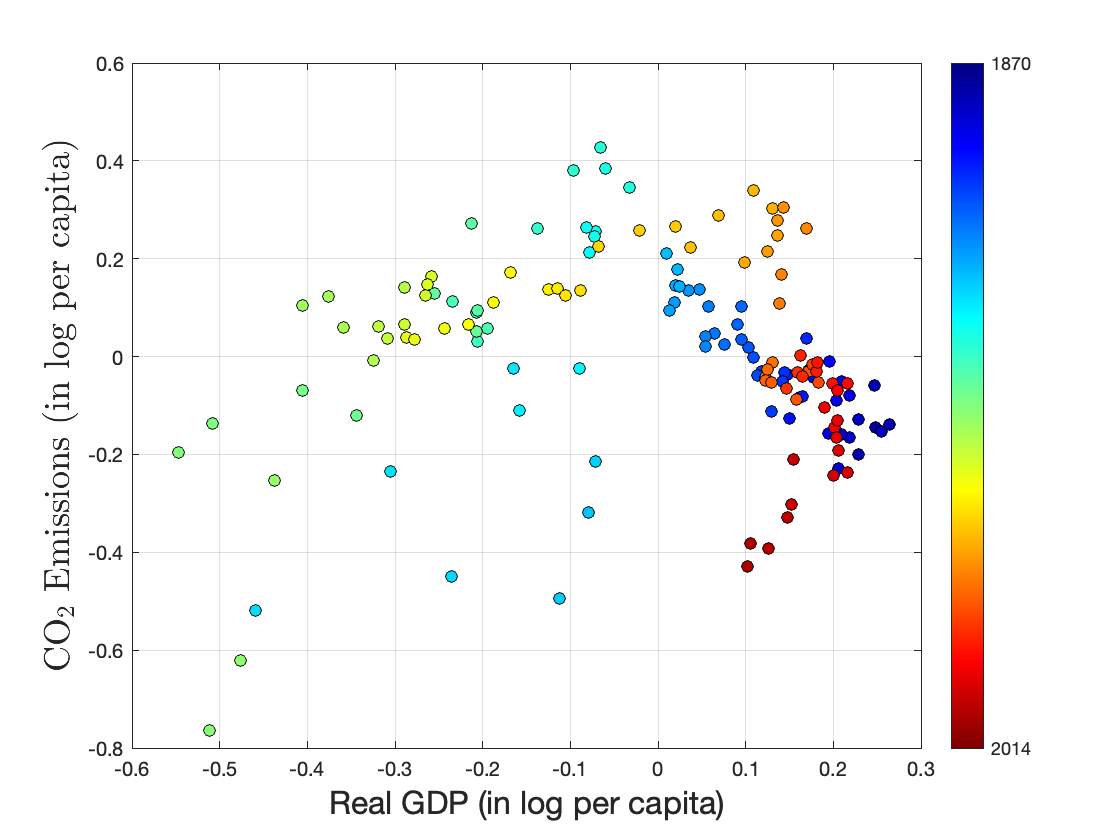

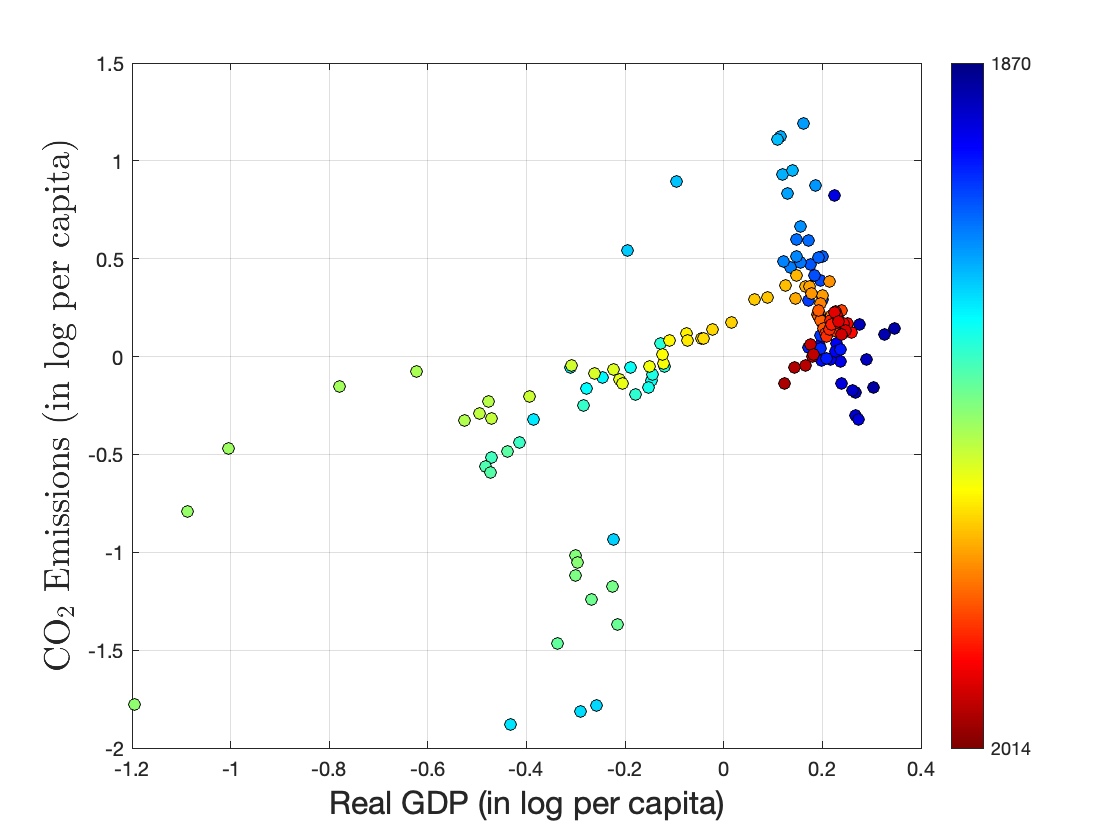

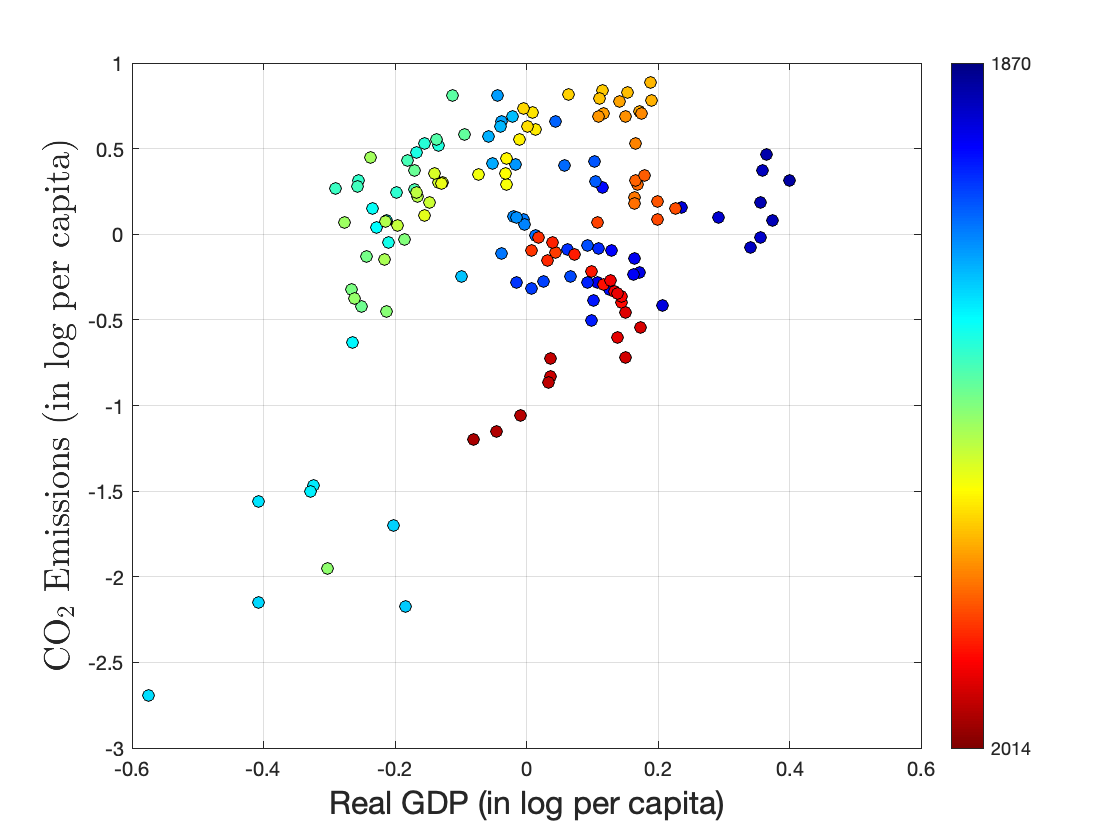

More evidence for the importance of time effects is available in Figure 4(b). This figure depicts the same per capita series after detrending.131313The Perron and Yabu (2009) test allows us to test for the presence of a deterministic trend irrespectively of the series being trend-stationary or having an unit root. The results of this test (see supplement) indicate that log per capita GDP is likely to have a deterministic trend component. It is thus recommended to have a deterministic trend in the model for log per capita emissions and the visual inspection of the relationship between GDP and emissions (in log per capita) should take place after partialling out this deterministic trend. The inverted U-shape is now (visually) less pronounced or even absent.

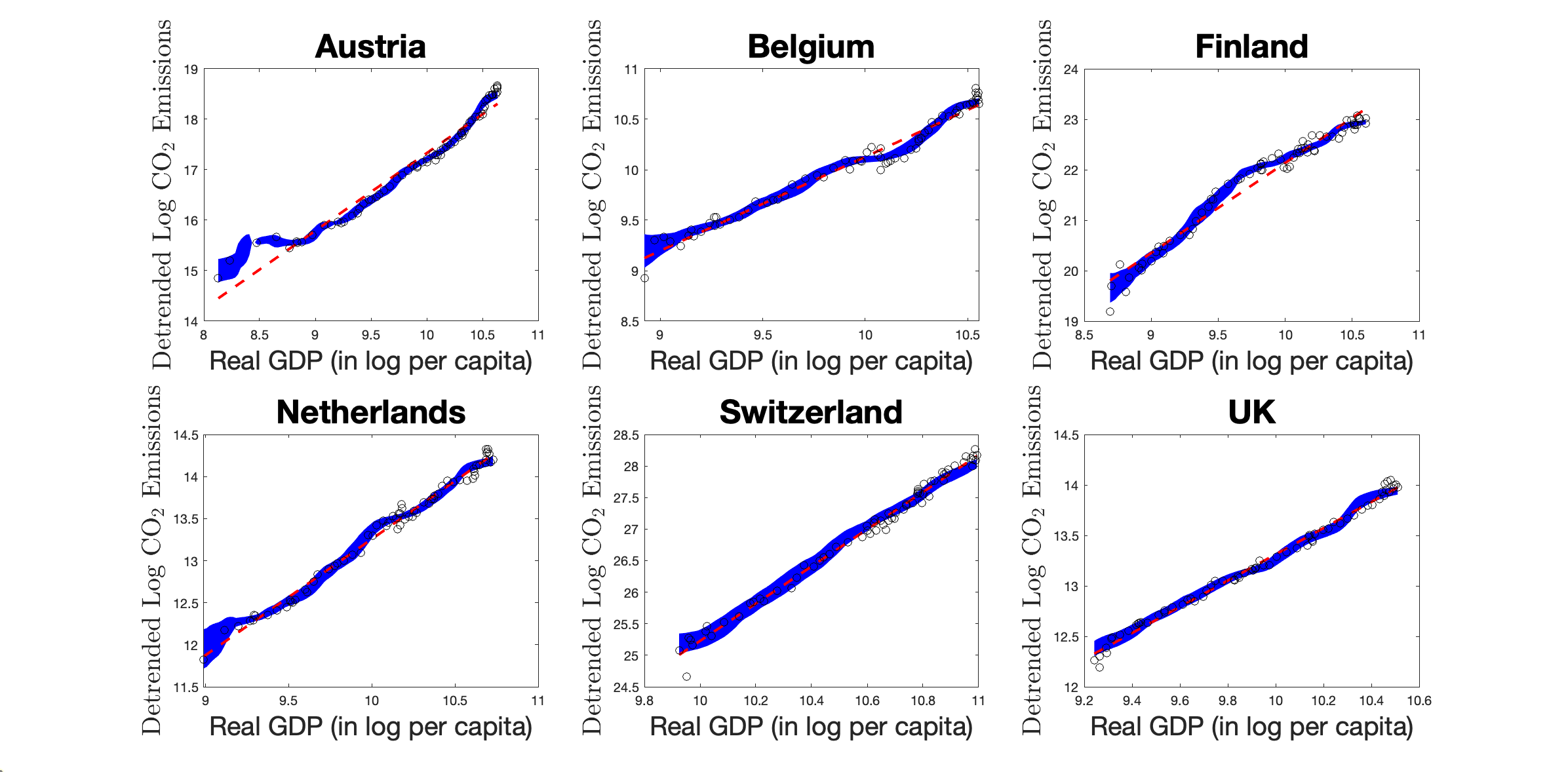

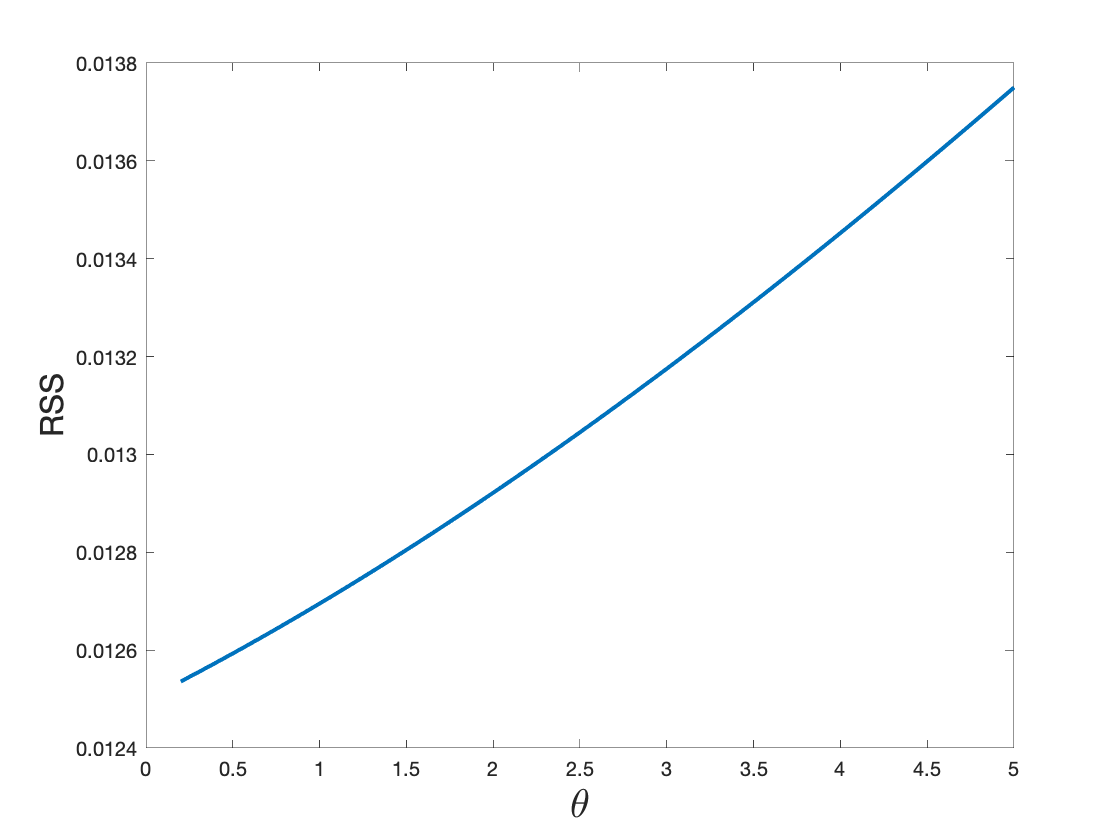

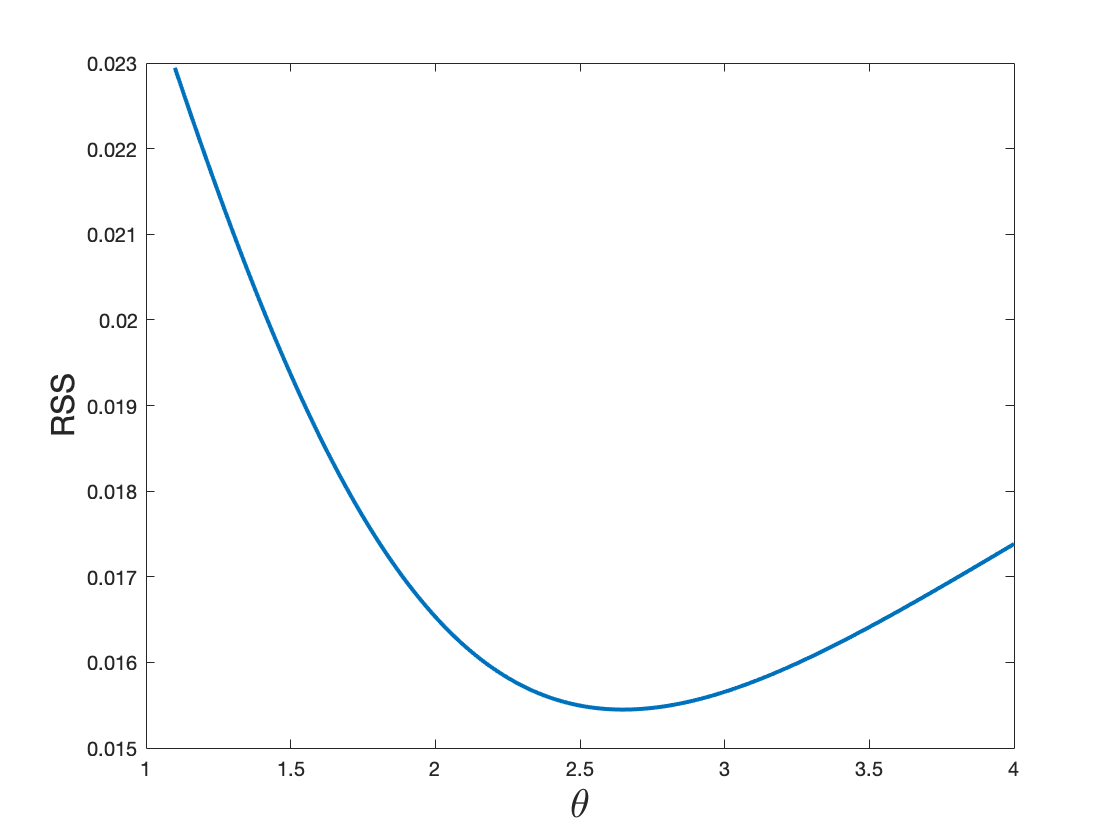

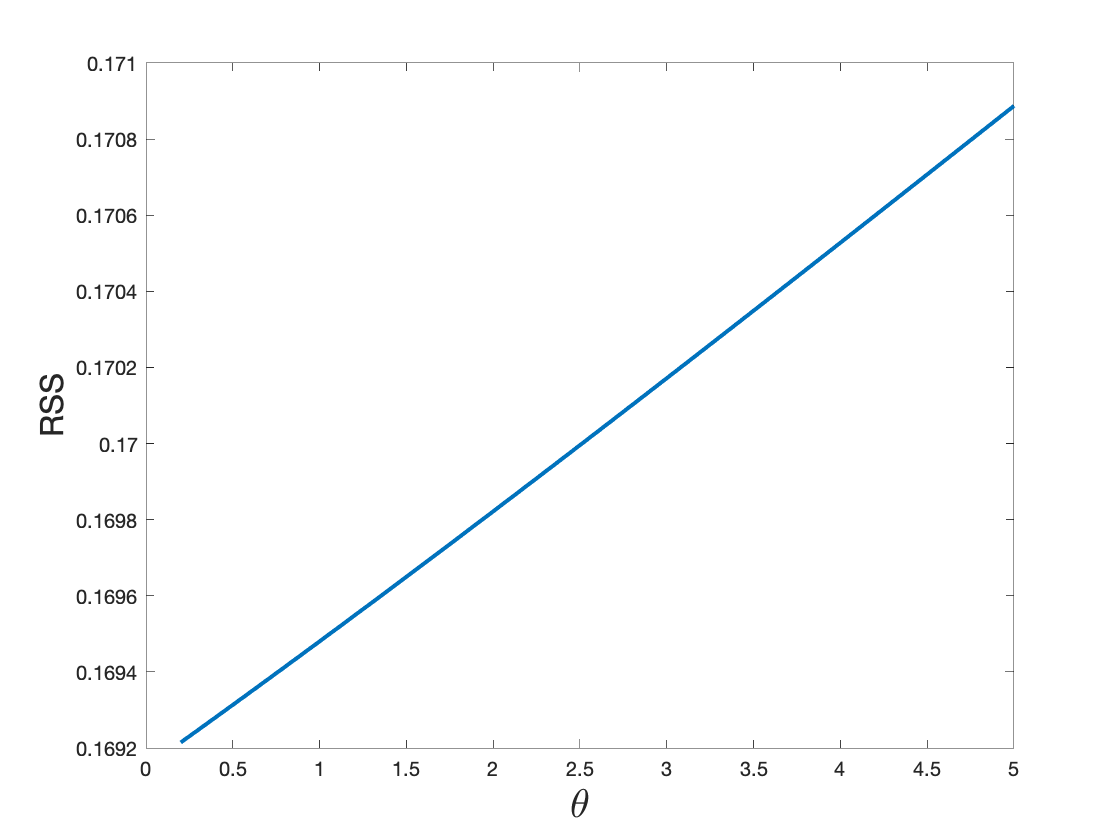

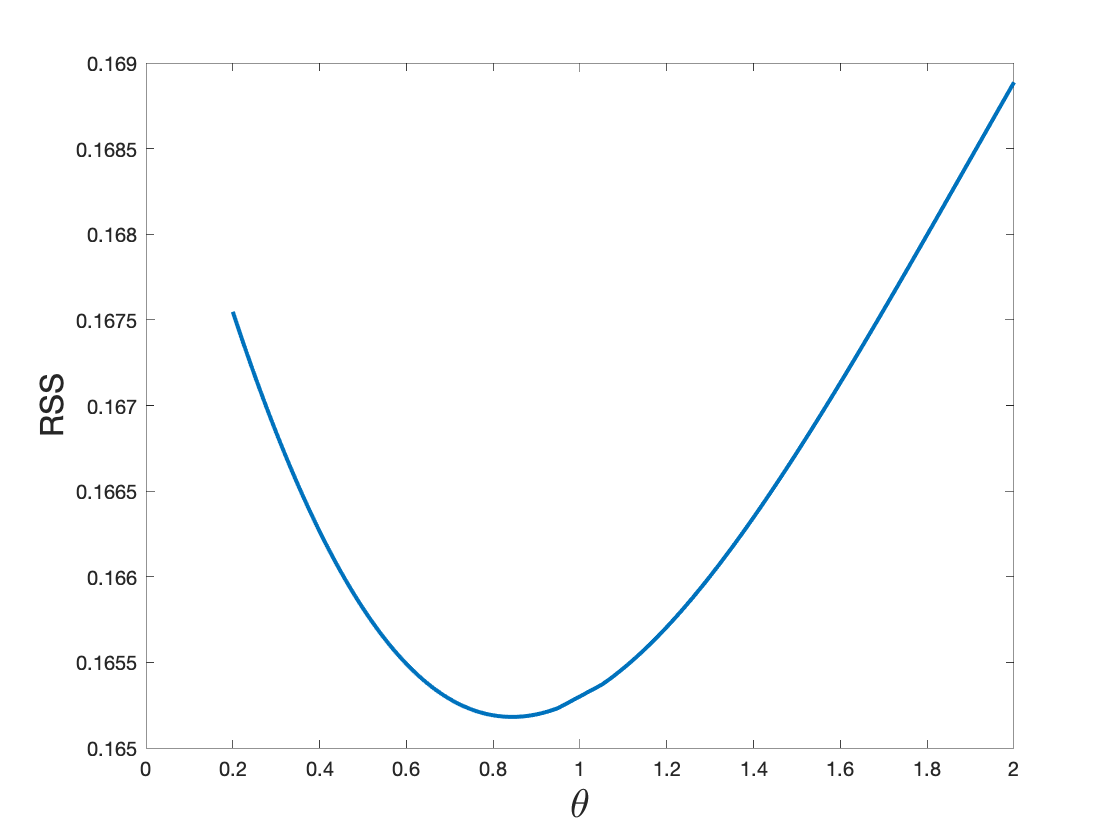

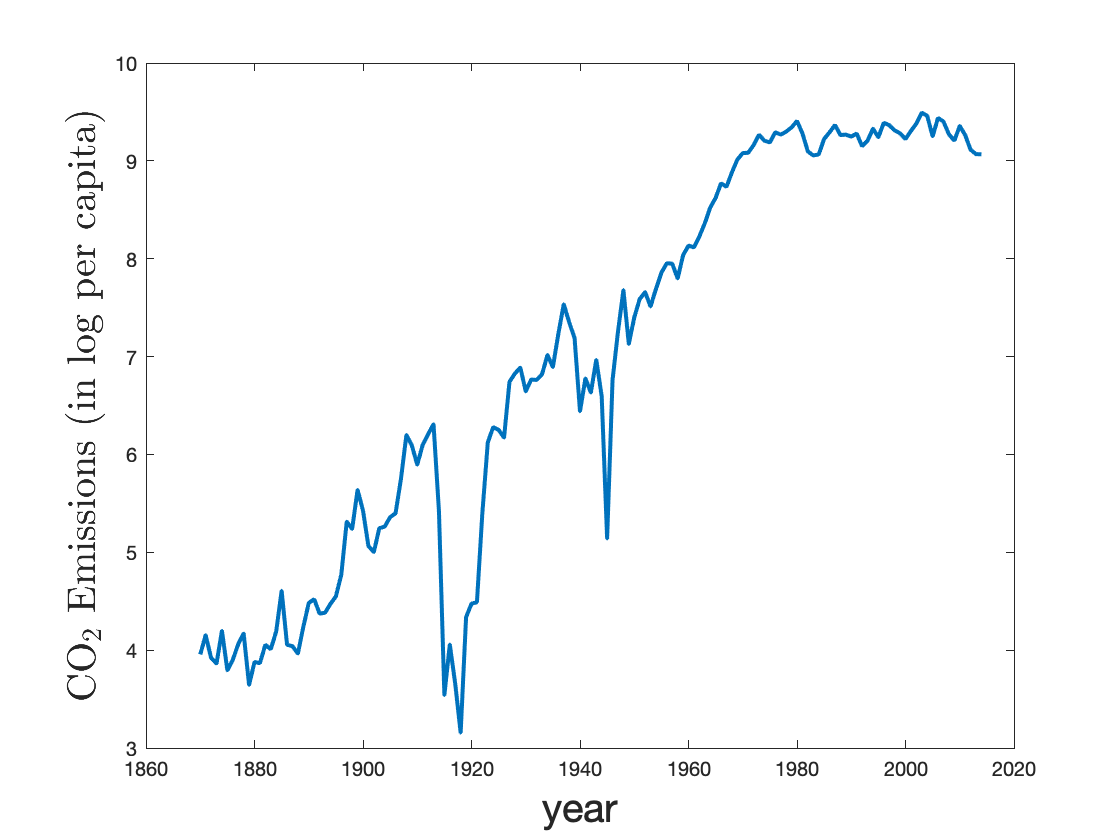

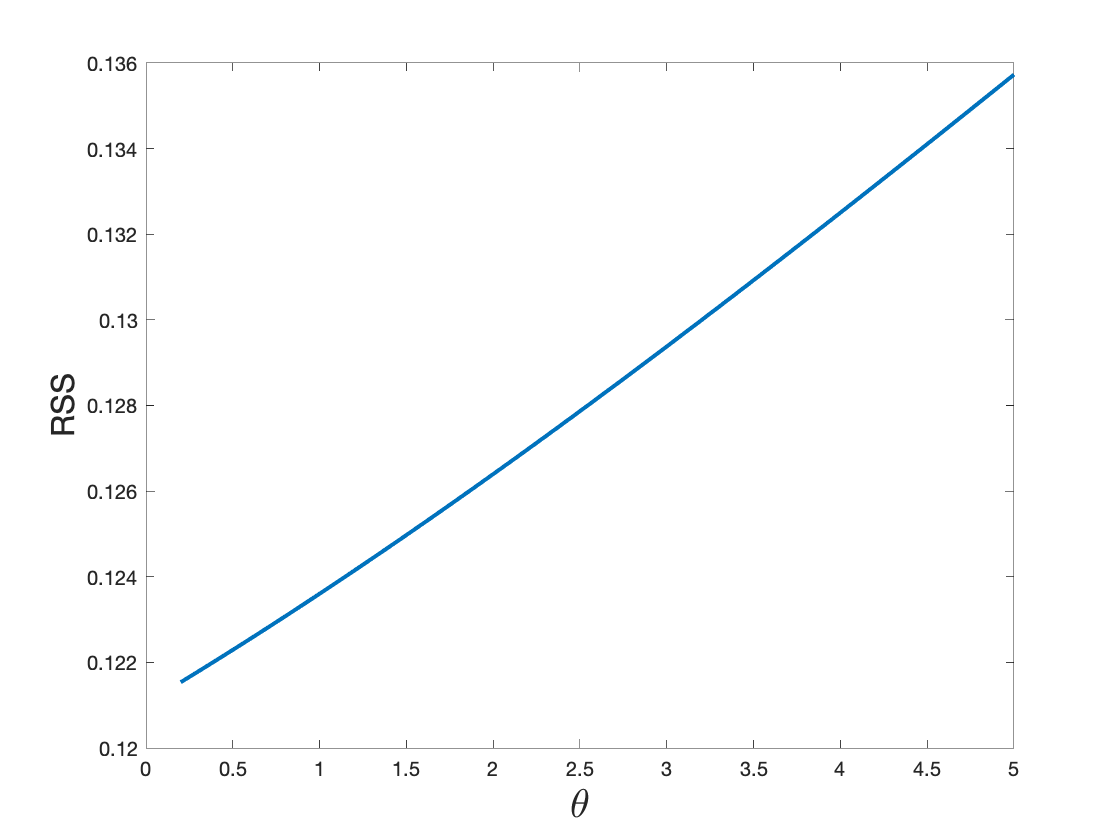

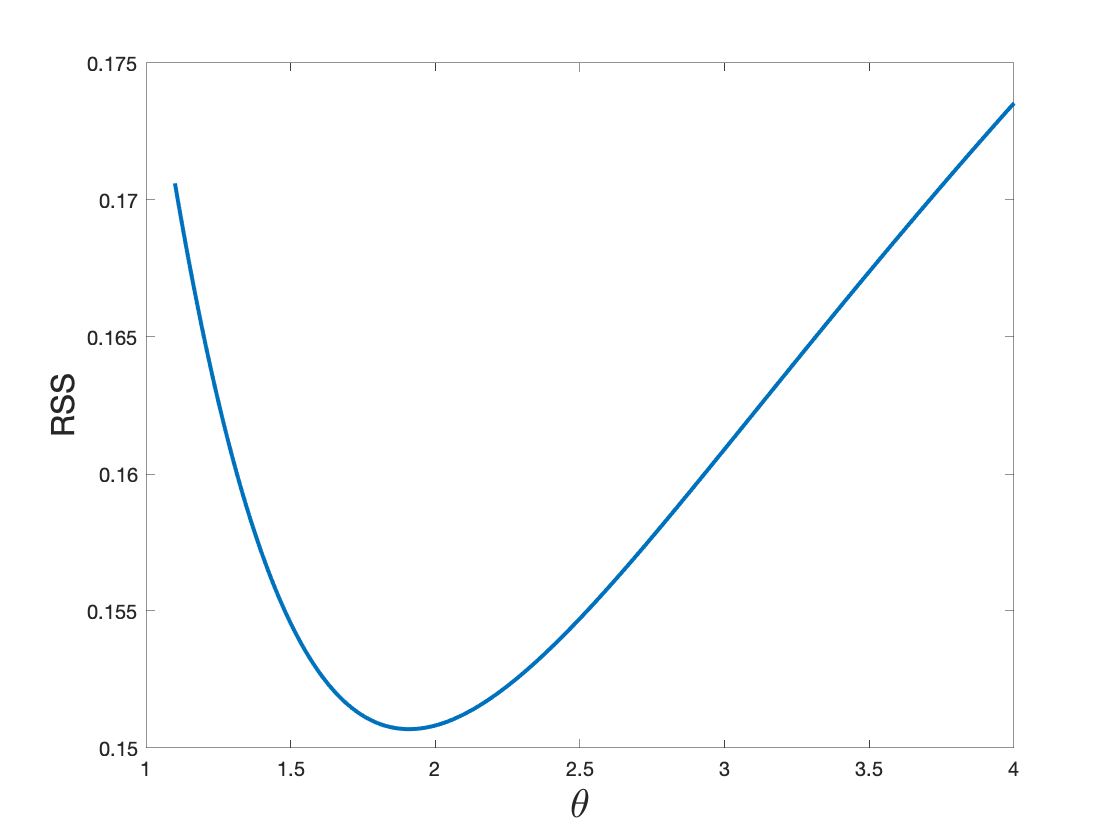

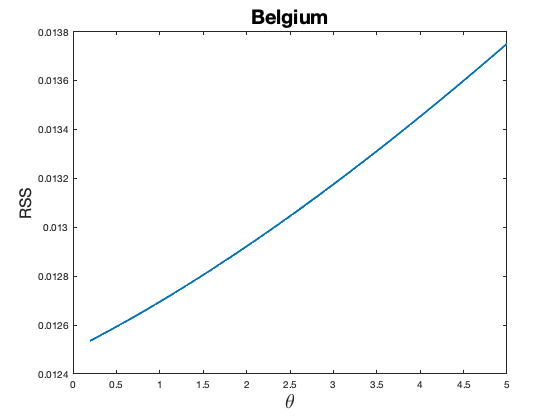

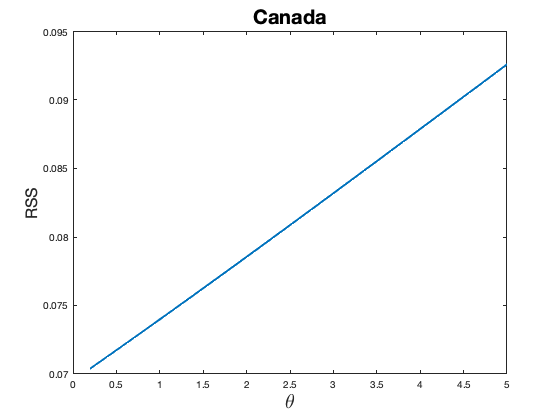

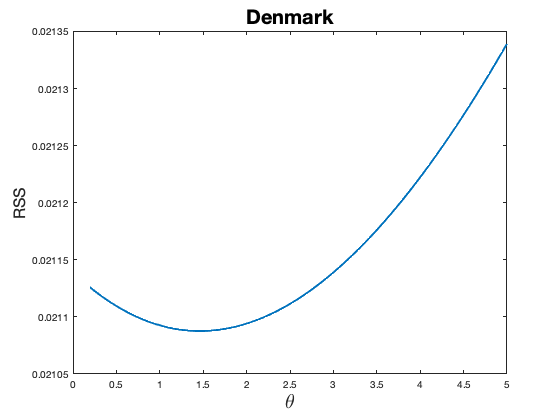

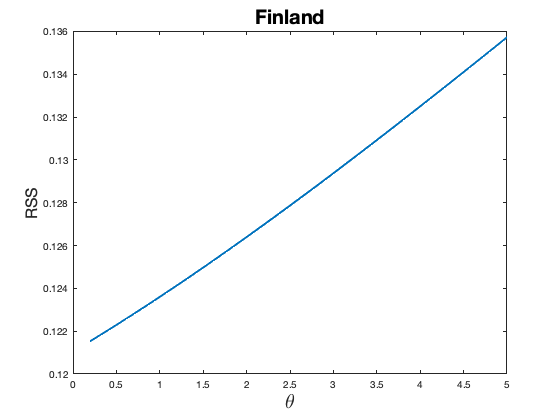

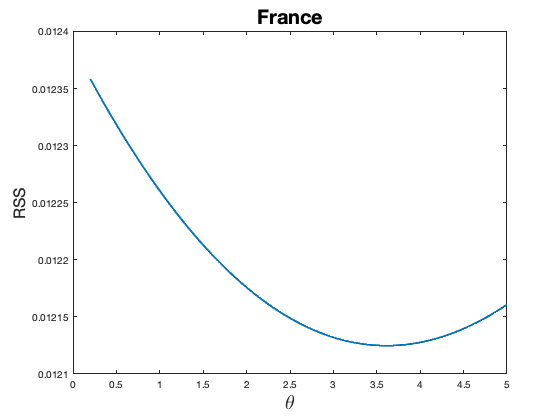

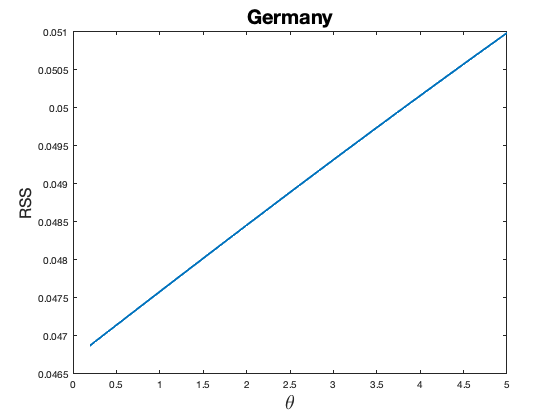

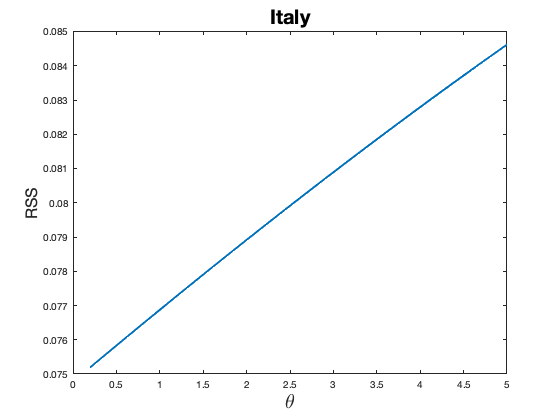

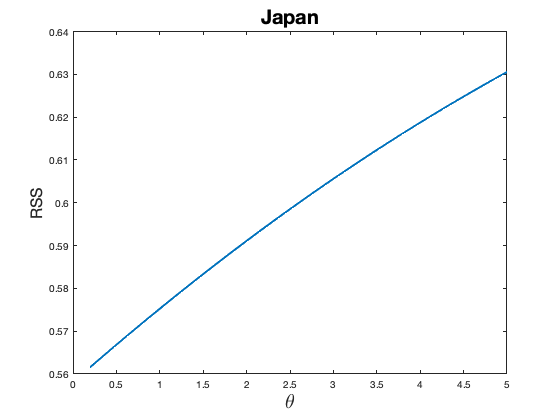

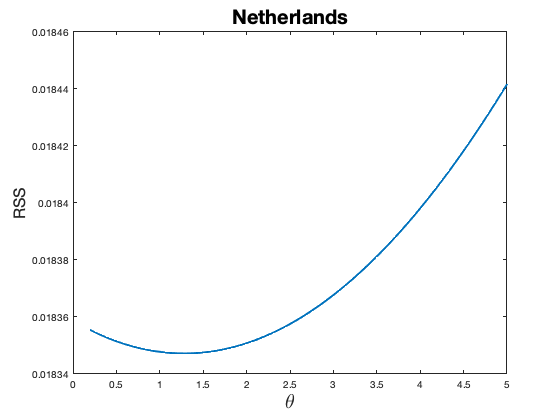

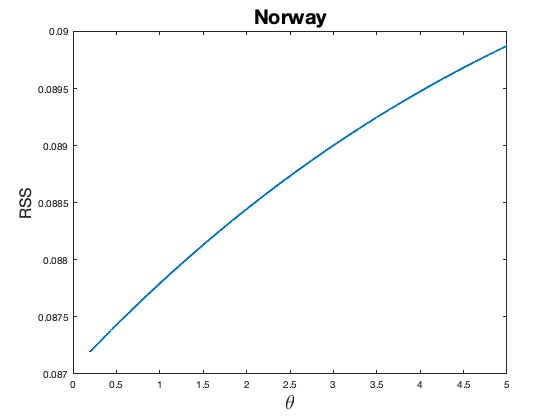

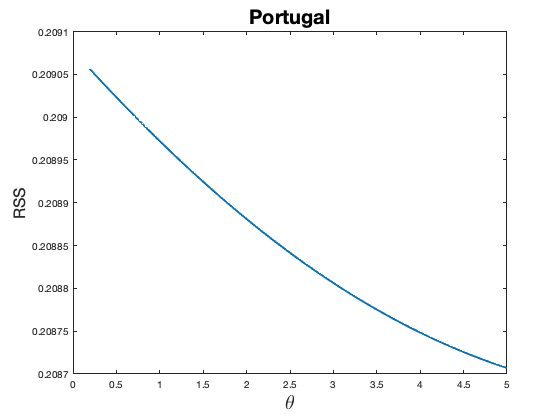

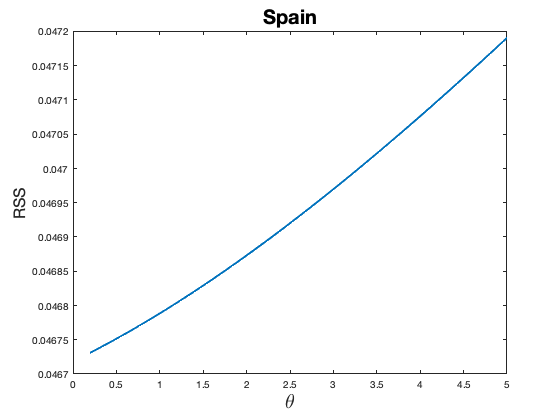

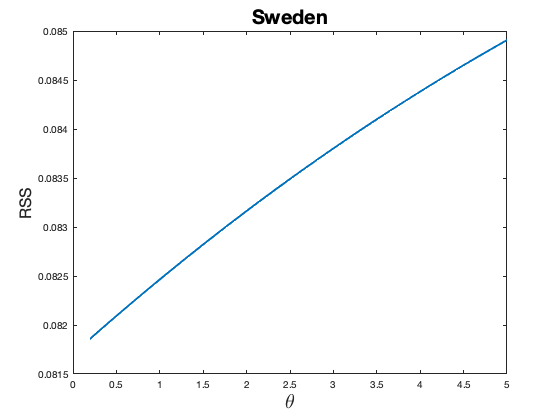

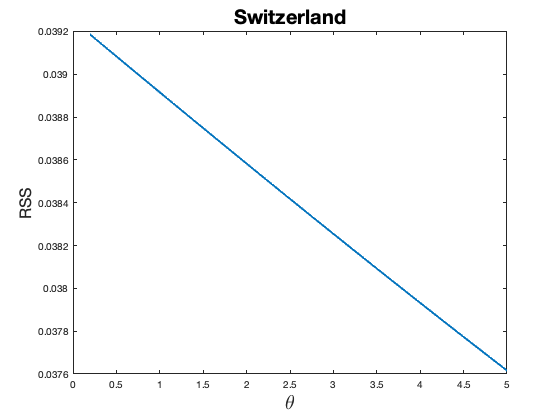

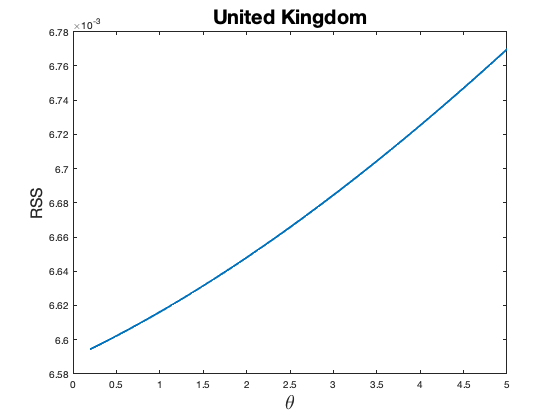

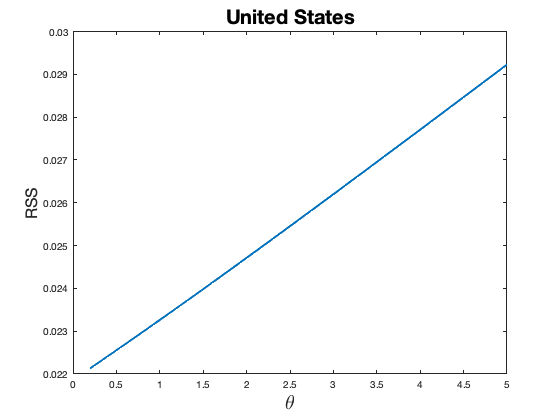

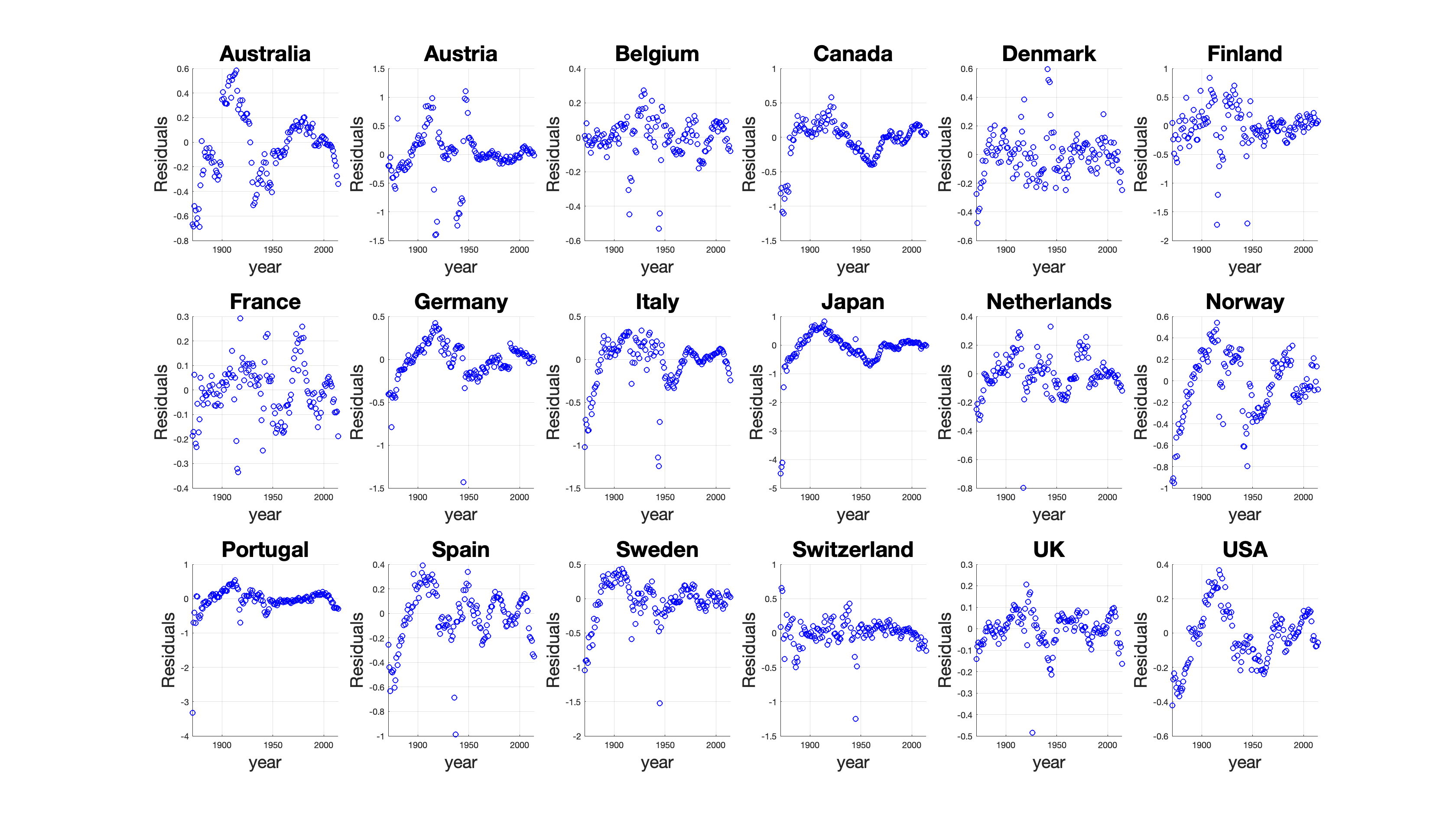

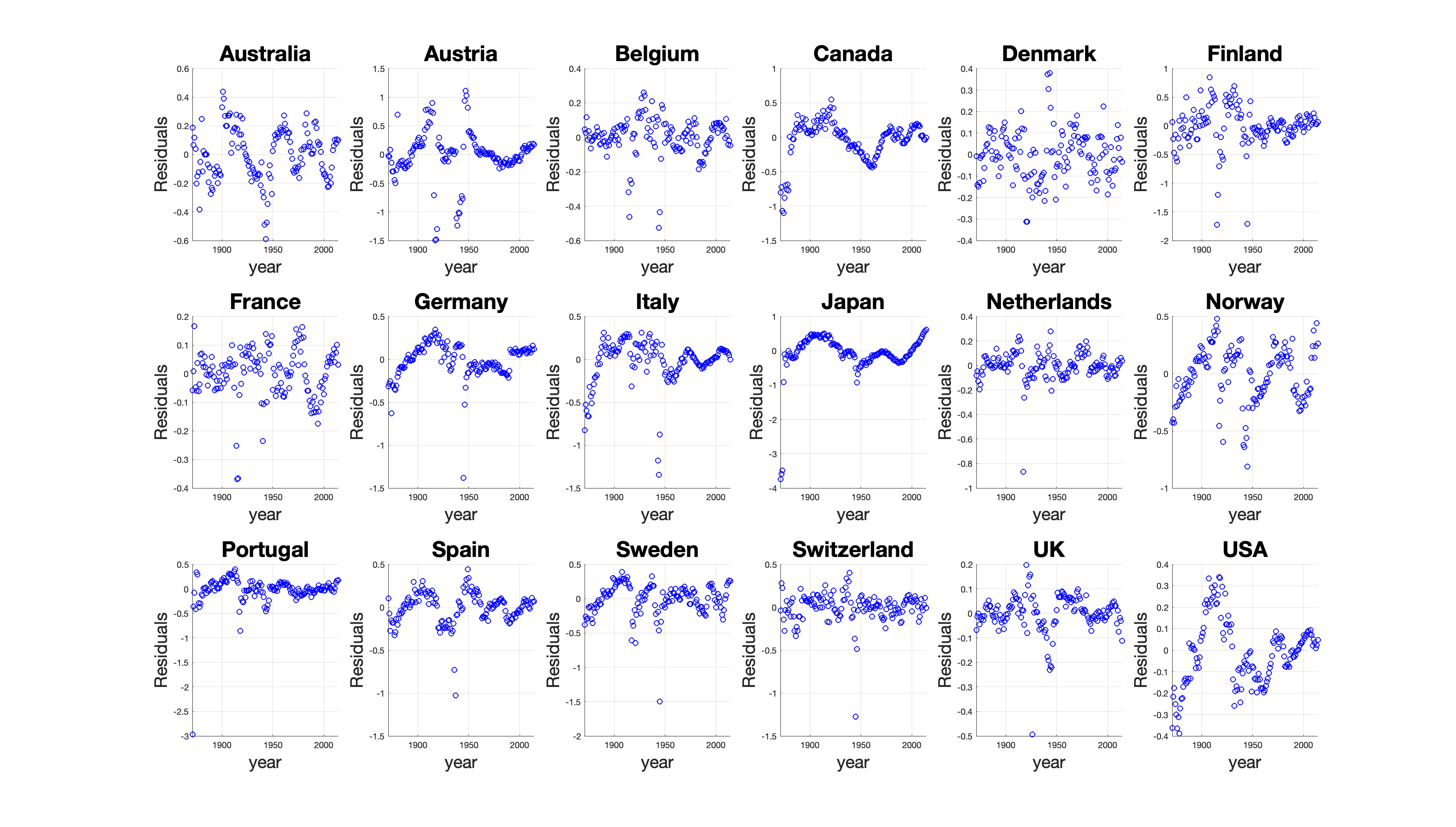

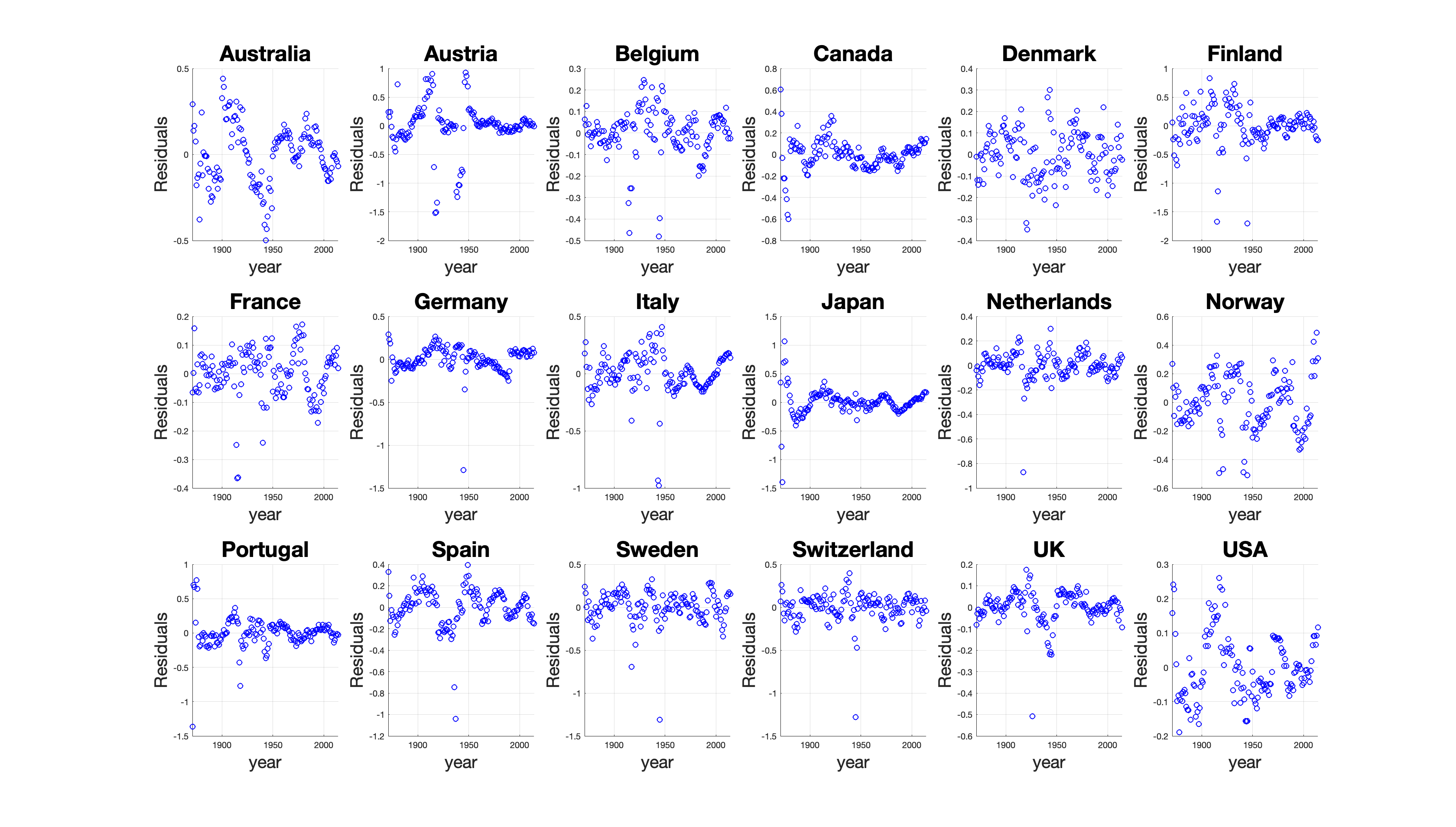

Finally, let us depart from a traditional linear cointegration specification: . This model cannot incorporate any nonlinear behaviour over time and is therefore ill-suited to fit the data displayed in Figure 4(c). Cointegrating polynomial regressions use integer powers of to describe the curvature over time. More general, as in Hu et al. (2021), we can allow for an integrated regressor with a flexible power and estimate . The residual sum of squares (RSS) of the NLS estimator for this specification is shown in Figure 4(d). The absence of a minimum at casts doubt on the commonly used quadratic specification in . Additionally, the lack of any minimum might be interpreted as a sign that log per capita GDP is not the source of nonlinearity. This finding is not specific for Belgium. There are no minima in the RSS for 15 out of 18 countries (see Section S8.4). For the remaining three countries – Denmark, France and the Netherlands – minima are found at , and , respectively. Alternatively, we can describe the nonlinearity in the data using a flexible deterministic trend as in . The RSS in Figure 4(e) now exhibits a clear minimum. Further empirical analysis on individual countries (see Section S8.5 of the Supplement) suggests that: (1) the inclusion of a flexible time trend renders all quadratic effects in squared log per capita GDP insignificant, and (2) models remain well-specified after removing quadratic income effects from the model. These results suggest – albeit in a univariate setting – that flexible time trends gives a more satisfactory (or at least competing) description of the nonlinearities in the data.

5.2 Seemingly Unrelated Regression

The interpretation of a country-specific flexible deterministic trend is complicated because of its high collinearity with GDP per capita. The multivariate analysis of this section allows us to separate country-specific environmental improvements caused by national income growth from global environmental improvements. We study the following six countries (): Austria, Belgium, Finland, the Netherlands, Switzerland, and the UK. The motivation behind this choice is as follows. First, based on data series to ours, Piaggio and Padilla (2012), Mazzanti and Musolesi (2013), and Wagner et al. (2020) report considerable evidence of parameter heterogeneity across countries.141414Parameter heterogeneity is also reported for other data sets. Examples are List and Gallet (1999), Cole (2005), and Dijkgraaf and Vollebergh (2005). The evidence in Mazzanti and Musolesi (2013) is anecdotal in the sense that these authors consider groups of similar countries and find different results for different groups. The lack of overlap among confidence intervals of country-specific parameters has also been interpreted as a sign of heterogeneity (section 4.2 in Piaggio and Padilla (2012)). Wagner et al. (2020) explicitly test for various forms of poolability and conclude that pooling is (at most) appropriate for small subgroups of countries. This lack of parameter homogeneity justifies a multivariate approach with small rather than a panel setting. Admittedly, in the current time-series setting, studying “large ” is also infeasible since consistent estimators for long-run covariance matrices are required. Second, prior studies already refute the existence of a carbon dioxide EKC for several countries and little seems lost by excluding these countries from the outset.151515Most of the parameters in the Generalized Cointegrating Polynomial Regression are country-specific. The estimation accuracy of these parameters should deteriorate little when focussing attention on a subset of countries. Losses will occur in the precision of the estimators for and . There is thus a trade-off between accurate global trend estimation (improving with large ) and accurate LRV estimation (deteriorating with large ). To strike a balance and to connect to the recent literature, we continue the analysis of Wagner et al. (2020) and take . That is, we consider the same countries as in Wagner et al. (2020), who decide on these countries because their prior cointegration analysis “leads to evidence for a quadratic cointegrating EKC including a constant and linear trend”.

| Omitted Global Trend | Global Trend | ||||||||||

| Model | (M1) | (M2) | (M3) | ||||||||

| FM-SOLS | FM-SUR | SimNLS | SimNLS | SimNLS | |||||||

| Austria | |||||||||||

| Belgium | |||||||||||

| Finland | |||||||||||

| Netherlands | |||||||||||

| Switzerland | |||||||||||

| UK | |||||||||||

| Joint -value | 0.00 | 0.00 | 0.16 | 0.39 | — | ||||||

| KPSS-statistic | 3.45 | 5.10 | 3.46 | 3.48 | 3.78 | ||||||

-

•

Note: Asterisks denote rejection of the null hypothesis at the , , and significance level. Depending on the specific table entry, the null hypothesis refers to coefficient(s) being zero or a well-specified cointegrating relation.

Having decided on the set of countries, we subsequently study the effect of the global flexible trend on EKC evidence. Table 3 shows the estimation results of the quadratic EKC specification

| (M1) |

This setting (possibly with the additional constraint ) has been explored in numerous papers, for example: Selden and Song (1994), Piaggio and Padilla (2012), Chan and Wang (2015), Wagner (2015), Wang et al. (2018), and Wagner et al. (2020). For Model (M1), an inverted-U relationship results when and and empirical evidence hereof is traditionally interpreted as the existence of an EKC. If these coefficients have the correct signs, then the country’s turning point – the level of economic growth at which environmental improvement starts – can be computed as . We assess the parameter values and their significance using FM-SOLS and FM-SUR (repeating the analysis of Wagner et al. (2020) for ease of comparison) and the simulated approach of Section 3.2. Regardless of estimation method and country, all coefficient signs are in agreement with the EKC hypothesis. The parameters are generally significantly different from zero but the significance of does vary across estimation methods. FM-SOLS and FM-SUR typically (strongly) reject () whereas evidence against these null-hypotheses is less pronounced for the simulation-based approach. The same behaviour emerges when testing jointly. This pattern reminds of the simulation results in Table 2 where the cross-sectional dimensions and cause over-sized tests for FM-SOLS and FM-SUR and conservative tests for simulation-based inference. The KPSS test does not indicate any signs of misspecification. Overall, Model (M1) leads to considerable evidence in favour of a quadratic cointegrating EKC.

The reported evidence in favour of the EKC should not come as surprise. First, the set of countries was selected based on this criteria. Second, the visualisations of the data clearly suggest nonlinear effects (recall Figures 4(a) and 4(c) for the case of Belgium). With Model (M1) being restrictive in the sense that nonlinearities over time are solely incorporable through , we expect this variable to be important. In line with our proposed Generalized Cointegrating Polynomial Regression (GCPR) framework, we subsequently add a global flexible trend and estimate

| (M2) |

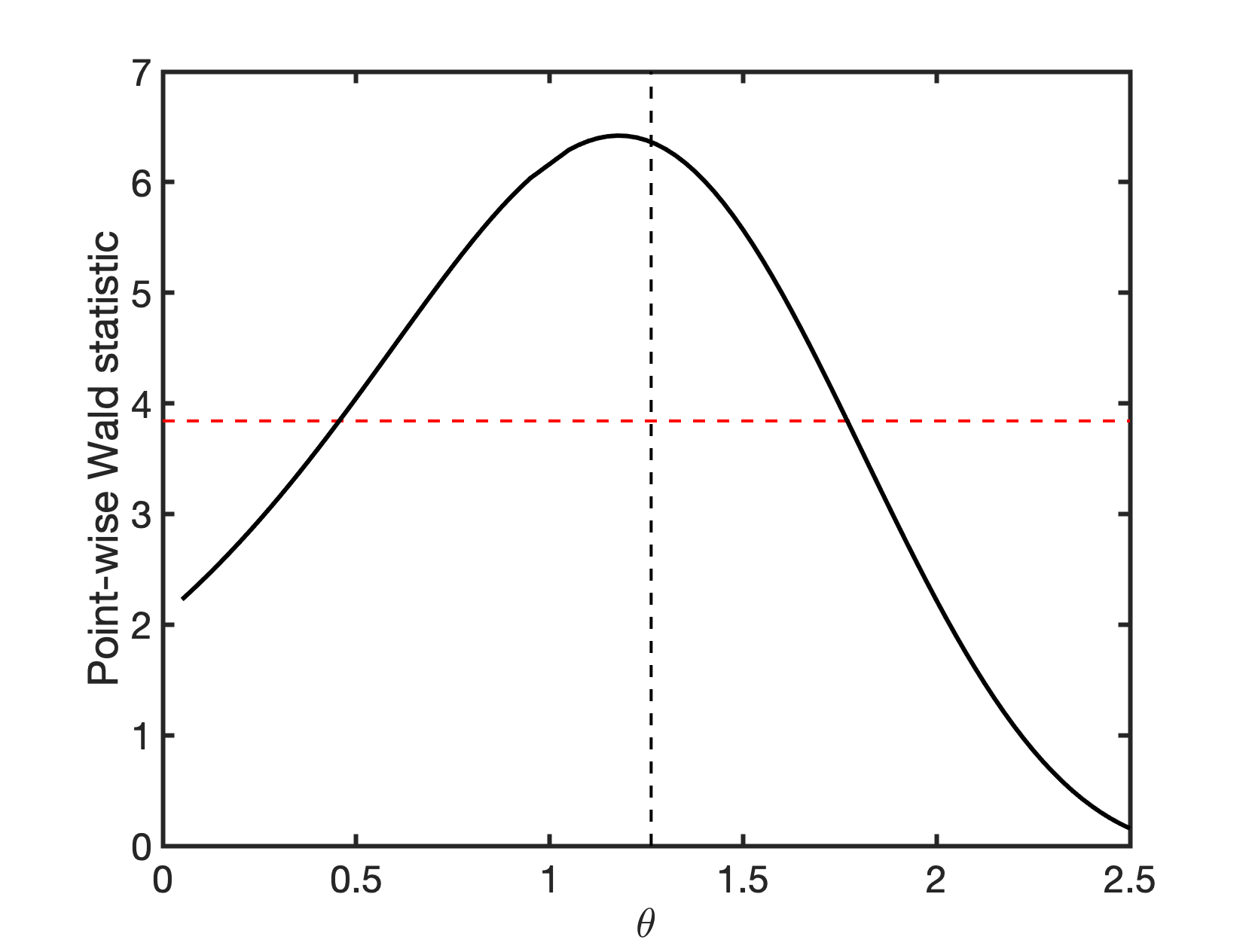

From a statistical perspective, the term opens a different channel through which nonlinearities can be described. We refer back to the introduction for a further elaboration on this point. From an economic perspective, captures changes in CO2 emissions that are common across series and thus unrelated to changes in national GDPs. Parameter inference for Model (M2) is also reported in Table 3. The contributions of are insignificant for both individual countries and all countries jointly. How about the significance of the global trend? The standard Wald test for is invalid because is unidentified under the null hypothesis (see Assumption 1 and the related discussion). As a heuristic alternative, we vary over the interval and compute Wald statistics while assuming to be fixed. Comparing these Wald statistics to the 95% quantile of a -distributed random variable (critical value: 3.842), the range of -values from about 0.5 to 1.75 implies a significant global trend (Figure 5). Having estimated , our analysis suggests that the global trend and not GDP per capita is the source of nonlinearity. Before interpreting this result, we first verify whether the model with shows signs of misspecification.

Omitting insignificant parameters from the previous model specification, we arrive at

| (M3) |

Model (M3) is linear in log per capita GDP. The positive parameter estimates for imply that at a given point in time increases in economic growth imply increases in CO2 emissions. However, as and , there will be common emission reductions over time. Also, the omission of the quadratic terms in log per capita GDP do not seem to result in a misspecified model. First, the KPSS test does not reject the null of cointegration. Second, there is no (visual) evidence that the linear functional form of (M3) is inappropriate. To arrive at this last conclusion, we compute and employ the nonparametric kernel estimator from Wang and Phillips (2009) to estimate for each individual country.161616The properties of nonparametric kernel estimators in nonlinear cointegration models have been studied by Wang and Phillips (2009), Gao et al. (2015) and Wang and Phillips (2016), among others. The latter reference is particularly relevant because it establishes that kernel estimators remain consistent and asymptotically (mixed) normal under serially correlated errors and endogeneity. None of these papers includes deterministic trends in the DGP. However, we conjecture that detrending does not affect the asymptotic properties of the kernel estimator due to the high convergence rates of the trend parameters in comparison to the slow convergence rates of the nonparametric estimator. Our bandwidth choice is . Figure 6 shows the nonparametric estimate in blue and the fit of Model (M3) in red. After removal of the global trend, there are some temporary departures from linearity but there is little curvature overall and certainly no visual turning point. In Table 4, we formally test the null of linearity using the model specification test as outlined in section 3 of Wang and Phillips (2016). Based on the full sample, linearity is rejected for Austria only. A comparison with the 95% confidence intervals of the kernel estimate (Figure 6) suggests that this rejection is caused by the sharp decline in CO2 emissions during World War II. We subsequently repeat the analysis using the observations after 1945. Linearity is never rejected.171717The high -values in Table 4 are caused by visually small deviations from the linear trend (see Section S8.6 in the Supplement for detailed graphs). Also, the relatively small sample size (for nonparametric settings) might adversely affect power. Matlab functions for nonparametric kernel regression and specification test are available at https://github.com/HannoReuvers. For remarks on bandwidth choice and detrending, we refer to footnote 16. All this align well with our earlier findings of a relevant global trend and irrelevant quadratic effects in log GDP per capita.

| Full Sample | After World War II | ||||||

|---|---|---|---|---|---|---|---|

| range | -value | range | -value | ||||

| Austria | [8.003,10.635] | 8.987 | 0.000 | [8.129,10.635] | 0.162 | 0.871 | |

| Belgium | [8.389,10.553] | 0.299 | 0.765 | [8.923,10.553] | 0.076 | 0.939 | |

| Finland | [7.494,10.602] | 0.105 | 0.916 | [8.693,10.602] | 0.020 | 0.984 | |

| Netherlands | [8.469,10.728] | 0.046 | 0.964 | [8.990,10.728] | 0.022 | 0.982 | |

| Switzerland | [8.708,10.993] | 0.028 | 0.977 | [9.925,10.993] | 0.009 | 0.993 | |

| UK | [8.641,10.510] | 0.022 | 0.982 | [9.242,10.510] | 0.021 | 0.984 | |

-

•

Note: The asymptotic properties of are established in Wang and Phillips (2016). That is, under suitable conditions, as with denoting the sojourning time of a standard Brownian motion around zero during the time interval . The -values are computed using the cumulative distribution function of , see (2.11) in Dong et al. (2017).

The preceding analysis suggests that the global flexible trend captures omitted determinants of CO2 emission levels that have been decreasing over time. In their analysis, Grossman and Krueger (1995) already included a global deterministic trend in their model because they “did not want to attribute to national income growth any improvements in local environmental quality that might actually be due to global advances in the technology for environmental preservation or to an increased global awareness of the severity of environmental problems”. Indeed, since reliable data on green technology adaptation181818Nordhaus (2014) discusses the link between climate change and technological changes. As another example, Figure 2 in Gillingham and Stock (2018) reports a steady decline in the price of solar panels and a steady growth in solar panel sales. Cheaper solar energy can substitute fossil energy thereby reducing pollution. and global awareness is scarcely available (certainly for time horizons allowing for a cointegration analysis), these variables are likely missing and thus requiring a proxy. Similar remarks are applicable to variables such as pollution control policies191919A policy variable, ‘Repudiation of Contracts by Government’, was included by Panayotou (1997) to proxy the quality of environmental policies and institutions.. In reduced-form models, an EKC finding is typically explained by national income being the proxy for these omitted variables. That is, at higher levels of national income, countries have access to cleaner technologies and its citizens show greater appreciation for the environment and pollution legislation. The current analysis contradicts these income effects and points towards improvements being captured by a global trend.

Our final model specification, Model (M3), is linear in log GDP per capita. Moreover, for a given year, the coefficient estimates suggest that increasing national income by 1% implies an increase in carbon-dioxide emissions of about 1%–2.5% (depending on the country). This result seems plausible for non-carbon-neutral economies. However, CO2 emissions in Austria, Belgium, Finland, the Netherlands, Switzerland, and the UK are jointly reducing at the end of the sample. What cause these global emission reductions? Mazzanti and Musolesi (2013) suggest that conglomerates of countries anticipate and respond to international climate agreements such as the Rio convention (1992) and Kyoto protocol (adopted in 1997; operational since 2005). Interestingly, the latter agreement contains emission reduction targets to be reached in 2020 and such “working-towards-a-common-reduction-deadline” does point towards a time effect.202020According to the Doha amendment of the Kyoto protocol, the reduction commitments were 92% (over the period 2008–2012) and 80% (over the period 2013–2020) of 1990 emission levels for Austria, Belgium, Finland, the Netherlands and the UK. For Switzerland, the reduction target was also 92% (over the period 2008–2012) but 84.2% (over the period 2013–2020). (source: https://unfccc.int/files/kyoto_protocol/application/pdf/kp_doha_amendment_english.pdf). Alternatively, given our sample of European countries, EU coordinated emission reduction efforts like the EU Emissions Trading System (ETS) can be a driving force behind these common emission decreases.

6 Summary and Conclusion

In this paper we have extended the Seemingly Unrelated Cointegrating Polynomial Regression (SUCPR) model of Wagner et al. (2020) with a global power law deterministic trend. This multivariate specification allows us to disentangle national income and unobserved time effects. The importance of this separation is well-documented (see, e.g. Vollebergh et al. (2009) and Mazzanti and Musolesi (2013)) but a methodological approach accounting for nonstationary regressors is currently unavailable. We fill this gap.

The unknown powers of the global trend are estimated jointly with the parameters in the cointegrating relation. The limiting distribution is nonstandard due to a non-diagonal scaling matrix and second order bias terms. We therefore suggest a simulation-based approach to conduct inference. The usual subsampling KPSS-type for stationarity of the innovations of the nonlinear cointegrating relation remains valid. Our results are supported by Monte Carlo simulation. The empirical application on the Environmental Kuznets Curve shows that a flexible trend can fully capture the nonlinearity in the data thereby making higher order powers of log per capita GDP redundant. Our resulting model is linear in log per capita GDP and suggests an alternative explanation in which time effects – e.g. technological progress, increasing environmental awareness, tightening pollution policy – rather than economic growth cause the recent slowdown in CO2 emissions. Contrary to the opening quote in the introduction, our analysis suggests that CO2 emissions increase with economic growth. Carbon dioxide emissions do decrease due to time effects.

7 Acknowledgements

Earlier versions of this paper have been presented at the 2019 CFE meeting in London, the Econometrics Internal Seminar (EIS) at Erasmus University Rotterdam, and the Brownbag Seminar at Vrije Universiteit Amsterdam. We gratefully acknowledge the comments by the participants. We extend our thanks to Eric Beutner, Dick van Dijk, Stephan Smeekes, and Xiaohu Wang for their valuable feedback. All remaining errors are our own.

References

- Adams and Essex (2016) Adams, R. A. and C. Essex (2016). Calculus: A Complete Course. Pearson Canada.

- Al-Mulali and Ozturk (2016) Al-Mulali, U. and I. Ozturk (2016). The investigation of Environmental Kuznets Curve hypothesis in the advanced economies: The role of energy prices. Renewable and Sustainable Energy Reviews 54, 1622–1631.

- Andrews and Cheng (2012) Andrews, D. W. and X. Cheng (2012). Estimation and inference with weak, semi-strong, and strong identification. Econometrica 80, 2153–2211.

- Andrews (1991) Andrews, D. W. K. (1991). Heteroskedasticity and autocorrelation consistent covariance matrix estimation. Econometrica 59, 817–858.

- Andrews and Sun (2004) Andrews, D. W. K. and Y. Sun (2004). Adaptive local polynomial whittle estimation of long-range dependence. Econometrica 72, 569–614.

- Baek et al. (2015) Baek, Y. I., S. J. Cho, and P. C. B. Phillips (2015). Testing linearity using power transforms of regressors. Journal of Econometrics 187, 376–384.

- Bergamelli et al. (2019) Bergamelli, M., A. Bianchi, L. Khalaf, and G. Urga (2019). Combining p-values to test for multiple structural breaks in cointegrated regressions. Journal of Econometrics 211, 461–482.

- Beutner et al. (2020) Beutner, E., Y. Lin, and S. Smeekes (2020). GLS estimation and confidence sets for the date of a single break in models with trends. Working Paper.

- Carson (2009) Carson, R. T. (2009). The Environmental Kuznets Curve: seeking empirical regularity and theoretical structure. Review of Environmental Economics and Policy 4, 3–23.

- Chan and Wang (2015) Chan, N. and Q. Wang (2015). Nonlinear regressions with nonstationary time series. Journal of Econometrics 185, 182–195.

- Chang et al. (2001) Chang, Y., J. Y. Park, and P. C. B. Phillips (2001). Nonlinear econometric models with cointegrated and deterministically trending regressors. The Econometrics Journal 4, 1–36.

- Cho and Phillips (2018) Cho, J. S. and P. C. B. Phillips (2018). Sequentially testing polynomial model hypotheses using power transforms of regressors. Journal of Applied Econometrics 33, 141–159.

- Choi and Saikkonen (2010) Choi, I. and P. Saikkonen (2010). Tests for nonlinear cointegration. Econometric Theory 26, 682–709.

- Cole (2005) Cole, M. (2005). Re-examining the pollution-income relationship: A random coefficients approach. Economics Bulletin 14, 1–7.

- Dasgupta et al. (2002) Dasgupta, S., B. K. H. Wang, and D. Wheeler (2002). Confronting the Environmental Kuznets Curve. Journal of Economic Perspectives 16, 147–168.

- Davies (1977) Davies, R. B. (1977). Hypothesis testing when a nuisance parameter is present only under the alternative. Biometrika 64, 247–254.

- Davies (1987) Davies, R. B. (1987). Hypothesis testing when a nuisance parameter is present only under the alternative. Biometrika 74, 33–43.

- Dijkgraaf and Vollebergh (2005) Dijkgraaf, E. and H. R. J. Vollebergh (2005). A test for parameter homogeneity in CO2 panel EKC estimations. Environmental and Resource Economics 32, 229–239.

- Dong et al. (2017) Dong, C., J. Gao, D. Tjøstheim, and J. Yin (2017). Specification testing for nonlinear multivariate cointegrating regressions. Journal of Econometrics 200, 104–117.

- Dufour (2006) Dufour, J.-M. (2006). Monte Carlo tests with nuisance parameters: A general approach to finite-sample inference and nonstandard asymptotics. Journal of Econometrics 133, 443–477.

- Dufour and Khalaf (2002) Dufour, J.-M. and L. Khalaf (2002). Simulation based finite and large sample tests in multivariate regressions. Journal of Econometrics 111, 303–322.

- Duggal et al. (1999) Duggal, V. G., C. Saltzman, and L. R. Klein (1999). Infrastructure and productivity: a nonlinear approach. Journal of Econometrics 92, 47–74.

- Duggal et al. (2007) Duggal, V. G., C. Saltzman, and L. R. Klein (2007). Infrastructure and productivity: An extension to private infrastructure and it productivity. Journal of Econometrics 140, 485–502.

- Galeotti et al. (2009) Galeotti, M., M. Manera, and A. Lanza (2009). On the robustness of robustness checks of the environmental Kuznets curve hypothesis. Environmental and Resource Economics 42, 551.

- Gao et al. (2015) Gao, J., S. Kanaya, D. Li, and D. Tjøstheim (2015). Uniform consistency for nonparametric estimators in null recurrent time series. Econometric Theory 31, 911–952.

- Gao et al. (2020) Gao, J., O. Linton, and B. Peng (2020). Inference on a semiparametric model with global power law and local nonparametric trends. Econometric Theory 36, 223–249.

- Gillingham and Stock (2018) Gillingham, K. and J. H. Stock (2018). The cost of reducing greenhouse gas emissions. Journal of Economic Perspectives 32, 53–72.

- Gillingham and Nordhaus (2018) Gillingham, P. C. K. and W. Nordhaus (2018). Uncertainty in forecasts of long-run economic growth. Proceedings of the National Academy of Sciences 115, 5409–5414.

- Grossman and Krueger (1995) Grossman, G. M. and A. B. Krueger (1995). Economic growth and the environment. The Quarterly Journal of Economics 110, 353–377.

- Hamilton (1994) Hamilton, J. D. (1994). Time Series Analysis. Princeton University Press.

- Harbaugh et al. (2002) Harbaugh, W. T., A. Levinson, and D. M. Wilson (2002). Reexamining the empirical evidence for an environmental Kuznets curve. Review of Economics and Statistics 84, 541–551.

- Hong and Phillips (2010) Hong, S. H. and P. C. B. Phillips (2010). Testing linearity in cointegrating relations with an application to purchasing power parity. Journal of Business & Economic Statistics 28, 96–114.

- Hu et al. (2021) Hu, Z., P. C. B. Phillips, and Q. Wang (2021). Nonlinear cointegrating power function regression with endogeneity. Econometric Theory 37, 1173–1213.

- Jalil and Feridun (2011) Jalil, A. and M. Feridun (2011). The impact of growth, energy and financial development on the environment in China: A cointegration analysis. Energy Economics 33, 284–291.

- Jansson (2002) Jansson, M. (2002). Consistent covariance matrix estimation for linear processes. Econometric Theory 18, 1449–1459.

- Jiang et al. (2019) Jiang, B., Y. Lu, and J. Y. Park (2019). Testing for stationary at high frequency. Journal of Econometrics 215, 341–374.

- Klein et al. (2004) Klein, L. R., V. G. Duggal, and C. Saltzman (2004). Contributions of input-output analysis to the understanding of technological change: the information sector in the United States. In E. Dietzenbacher and M. L. Lahr (Eds.), Wassily Leontief and Input-output Economics, Chapter 17, pp. 311–336. Cambridge University Press.

- Kwiatkowski et al. (1992) Kwiatkowski, D., P. C. B. Phillips, P. Schmidt, and Y. Shin (1992). Testing the null hypothesis of stationarity against the alternative of a unit root: How sure are we that economic time series have a unit root? Journal of Econometrics 54, 159–178.

- Li and Linton (2020) Li, S. and O. Linton (2020). When will the covid-19 pandemic peak? Journal of Econometrics 220, 130–157.

- Lin and Reuvers (2020) Lin, Y. and H. Reuvers (2020). Efficient estimation by fully modified GLS with an application to the Environmental Kuznets Curve. Working paper.

- Lin et al. (2020) Lin, Y., Y. Tu, and Q. Yao (2020). Estimation for double-nonlinear cointegration. Journal of Econometrics 216, 175–191.

- Linton and Wang (2016) Linton, O. and Q. Wang (2016). Nonparametric transformation regression with nonstationary data. Econometric Theory 32, 1–29.

- List and Gallet (1999) List, J. A. and C. A. Gallet (1999). The environmental Kuznets curve: Does one size fit all? Ecological Economics 31, 409–423.

- Maranzano et al. (2021) Maranzano, P., J. P. C. Bento, and M. Manera (2021). The role of education and income inequality on environmental quality. A panel data analysis of the EKC hypothesis on OECD. Nota di Lavoro 8.2021, Milano, Italy: Fondazione Eni Enrico Mattei.

- Mazzanti and Musolesi (2013) Mazzanti, M. and A. Musolesi (2013). The heterogeneity of carbon kuznets curves for advanced countries: Comparing homogeneous, heterogeneous and shrinkage/bayesian estimators. Applied Economics 45, 3827–3842.

- Nordhaus (2013) Nordhaus, W. D. (2013). The Climate Casino: Risk, Uncertainty, and Economics for a Warming World. Yale University Press.

- Nordhaus (2014) Nordhaus, W. D. (2014). The perils of the learning model for modeling endogenous technological change. The Energy Journal 35, 1–13.

- Panayotou (1997) Panayotou, T. (1997). Demystifying the environmental kuznets curve: Turning a black box into a policy tool. Environment and Development Economics 2, 465–484.

- Park (2002) Park, J. Y. (2002). An invariance principle for sieve bootstrap in time series. Econometric Theory 18, 469–490.

- Park and Phillips (1999) Park, J. Y. and P. C. B. Phillips (1999). Asymptotics for nonlinear transformations of integrated time series. Econometric Theory 15, 269–298.

- Park and Phillips (2001) Park, J. Y. and P. C. B. Phillips (2001). Nonlinear regressions with integrated time series. Econometrica 69, 117–161.

- Perron and Yabu (2009) Perron, P. and T. Yabu (2009). Estimating deterministic trends with an integrated or stationary noise component. Journal of Econometrics 151, 56–69.

- Perron and Zhu (2005) Perron, P. and X. Zhu (2005). Structural breaks with deterministic and stochastic trends. Journal of Econometrics 129, 65–119.

- Phillips (1995) Phillips, P. C. B. (1995). Fully modified least squares and vector autoregression. Econometrica 63, 1023–1078.

- Phillips (2007) Phillips, P. C. B. (2007). Regression with slowly varying regressors and nonlinear trends. Econometric Theory 23, 557–614.

- Phillips and Hansen (1990) Phillips, P. C. B. and B. E. Hansen (1990). Statistical inference in instrumental variables regression with I(1) processes. The Review of Economic Studies 57, 99–125.

- Piaggio and Padilla (2012) Piaggio, M. and E. Padilla (2012). CO2 emissions and economic activity: Heterogeneity across countries and non-stationary series. Energy Policy 46, 370–381.

- Robinson (2012) Robinson, P. M. (2012). Inference on power law spatial trends. Bernoulli 18, 644–677.

- Romano and Wolf (2001) Romano, J. P. and M. Wolf (2001). Subsampling intervals in autoregressive models with linear time trend. Econometrica 69, 1283–1314.

- Saikkonen (1992) Saikkonen, P. (1992). Estimation and testing of cointegrated systems by an autoregressive approximation. Econometric Theory 8, 1–27.

- Selden and Song (1994) Selden, T. M. and D. Song (1994). Environmental quality and development: Is there a Kuznets curve for air pollution emissions? Journal of Environmental Economics and Management 27, 147–162.

- Soong (1973) Soong, T. T. (1973). Random Differential Equations in Science and Engineering. Academic Press, Inc.

- Stern (2004) Stern, D. I. (2004). The rise and fall of the environmental kuznets curve. World Development 32, 1419–1439.

- Stern (2017) Stern, D. I. (2017). The environmental Kuznets curve after 25 years. Journal of Bioeconomics 19, 7–28.

- Stypka et al. (2017) Stypka, O., M. Wagner, P. Grabarczyk, and R. Kawka (2017). The asymptotic validity of “standard” fully modified OLS estimation and inference in cointegrating polynomial regressions. Working Paper.

- Tanaka (2017) Tanaka, K. (2017). Time Series Analysis: Nonstationary and Noninvertible Distribution Theory. John Wiley & Sons.

- Vogelsang and Wagner (2014) Vogelsang, T. J. and M. Wagner (2014). Integrated modified OLS estimation and fixed-b inference for cointegrating regressions. Journal of Econometrics 178, 741–760.

- Vollebergh et al. (2009) Vollebergh, H. R. J., B. Melenberg, and E. Dijkgraaf (2009). Identifying reduced-form relations with panel data: The case of pollution and income. Journal of Environmental Economics and Management 58, 27–42.

- Wagner (2015) Wagner, M. (2015). The Environmental Kuznets Curve, cointegration and nonlinearity. Journal of Applied Econometrics 30, 948–967.

- Wagner et al. (2020) Wagner, M., P. Grabarczyk, and S. H. Hong (2020). Fully modified OLS estimation and inference for seemingly unrelated cointegrating polynomial regressions and the Environmental Kuznets Curve for carbon dioxide emissions. Journal of Econometrics 214, 216–255.

- Wagner and Hong (2016) Wagner, M. and S. H. Hong (2016). Cointegrating polynomial regressions: Fully modified OLS estimation and inference. Econometric Theory 32, 1289–1315.

- Wang and Phillips (2009) Wang, Q. and P. C. B. Phillips (2009). Structural nonparametric cointegrating regression. Econometrica 77, 1901–1948.

- Wang and Phillips (2012) Wang, Q. and P. C. B. Phillips (2012). A specification test for nonlinear nonstationary models. The Annals of Statistics 40, 727–758.

- Wang and Phillips (2016) Wang, Q. and P. C. B. Phillips (2016). Nonparametric cointegrating regression with endogeneity and long memory. Econometric Theory 32, 359–401.

- Wang et al. (2018) Wang, Q., D. Wu, and K. Zhu (2018). Model checks for nonlinear cointegrating regression. Journal of Econometrics 207, 261–284.

Appendix A Proofs for Main Theorems

Proof of Theorem 1 In view of the identity , we also have

The proof proceeds along the lines of Lemma 1 of Andrews and Sun (2004) and Theorem 3.1 of Chan and Wang (2015). The proofs separate into two parts. The first part uses a Taylor expansion of around to recover a quadratic approximation for on the set . In the second part, we obtain the limiting distribution from this quadratic approximation.

Part 1: Let denote a deterministic sequence such that as . Define and select a such that is twice differentiable on . For any , the Taylor expansion of around reads

| (A.1) | ||||

where is a point on the line segment connecting and , and the various derivatives of are

Defining , , and , we finally arrive at

| (A.2) | ||||

Part 2: For any , let . We shall show that the minimum of over is attained in the interior of . The next two statements are proven later:

-

(a)

;

-

(b)

, where with .

Given claim (b), for any , we have as because . Define . Clearly, is an interior point of as long as . Subsequently select a , i.e. is a boundary point of . From (A.2), we have

where a random vector with , and is a point on the line segment connecting and . The point is defined similarly. Moreover, the final equality follows from

claim (a), and . The second part of claim (b), , implies that as . Therefore, for any boundary point and the minimum of must be attained at an interior point of , say . As in Andrews and Sun (2004), we can now construct a sequence such that , where , satisfying the first-order conditions as . As a result, we obtain

| (A.3) |

It remains to verify claims (a) and (b). We consider the sequence for and . There exists such that whenever ,

where is given in (S23), and with some constant . Claim (a) thus holds if . Since is fixed, we can bound element-wise. Using the identity and Lemma S3, it is easily shown that the supremum of each element is indeed . Claim (b) follows directly from the weak convergence results in Lemma S2. That is, and as . Theorem 1 now follows from (A.3). ∎

Proof of Theorem 2 The proof is to a large extent an application of theorem 2 in Jansson (2002). We provide the details in the Supplement. ∎

Proof of Theorem 3 We abbreviate . By simple rearrangements, we obtain

| (A.4) | ||||

while having defined and the quantities

-

(a)

,

-

(b)

,

-

(c)

.

(a) We have . To see this, note that and . (b) Looking at the elements of , we conclude that if results similar to those in Lemma S3(i)-(iii) continue to hold. Two conditions need to be verified:

-

(b1)

with similarly defined to (S23),

-

(b2)

the stochastic order of terms remains the same when replacing by , conditional on the sample .

For condition (b1), using set inclusions similar to those below (A.3), it suffices to show with large probability for some . This is trivial because

and thus . Continuing with (b2), by independence between and , the consistency of , and a FCLT for an sequence, we may have

| (A.5) |

in probability, c.f. Section 2 of Park (2002). Since contains partial sum processes of , its integer powers and deterministic terms, (b2) is satisfied. (c) We have where

| (A.6) | ||||

, and . All these stochastic orders are a consequence of (A.5) and a straightforward modification of Lemma S2. Overall, we have .

It remains to look at the leading terms in (A.4). The elements of and are always multiplicative in the construction. From , (A.5), and Lemma S2, we have

| (A.7) |

in probability. The last two terms in (A.7) equal , because . Similarly,

| (A.8) |

The theorem follows after combining the limiting distribution of these leading terms through (A.4). ∎

Proof of Theorem 4 Without loss of generality, we set . Subsequently, note that

| (A.9) |

where the stochastic order of the remainder terms – follows from Lemma S3 and Theorem 1:

-

(a)

,

-

(b)

,

-

(c)

.

The theorem follows from (A.9), a functional central limit theorem for linear processes, the continuous mapping theorem, and the rate requirements. ∎

Supplement to “Cointegrating Polynomial Regressions with Power Law Trends: Environmental Kuznets Curve or Omitted Time Effects?”

\startlisttoc

\printlisttoc

S1 Simulation DGP used for Introduction

The simulation DGPs of the introduction are based on the data for Austria, Belgium and Finland. Parameter values are (nonlinear) least squares estimates and innovations are mean-zero normally distributed random variables with a covariance matrix estimated from the residuals and . The specific parametrization for the model with global trend is

| (S1) |

where with

The simulations investigating the influence of the redundant trend follow

where with

Compared to the empirical application (and thus also DGP2 in Section 4), the main differences are the smaller and the omission of serial correlation in both the innovations and the increments of the integrated variables. These modifications allow us to showcase the influence of the omitted global trend while not having to worry about the effects of long-run covariance estimation on statistical size.

S2 Auxiliary Lemmas

Lemma S1

-

Proof

(i) This is shown in lemma 4 of Robinson (2012). (ii) Note that

(S2) where we define . For the given index ranges, we also have such that

(S3) The first summation in the RHS of (S3) is bounded in view of Lemma S1(i) and due to Assumption 2(a) (cf. Appendix 3.A. in Hamilton (1994)). (iii) Using the equality and a change in the order of summation, we find

and hence

(S4) For the first term in the RHS of (S4), we have by Lemma S1(ii) with . For the second term, note that

(S5) To deal with the supremum of over , we define for . If , then by Bernoulli’s inequality. If , then convexity of implies

We conclude that for all and . Combining this result with (S5), we have

where we used (the steps in the proof of (ii) require a small modification to establish this) to go to the last line, and (i) to obtain the final inequality. The proof is complete since we have bounded both terms in the RHS of (S4). (iv) If we divide the integral into integration intervals of width , then we find

(S6) using the triangle inequality. Clearly, is bounded by . For we can use the standard integral (cf. Adams and Essex (2016)), namely for , to obtain

We therefore conclude that

It remains to bound the term . Changing the integration variable to yields

(S7) We subsequently derive an upper bound for the integrand using an approach which mimics the derivations in (D.14) and (D.15) in Robinson (2012). For any (such that ), we have

(S8) by the triangle inequality and the fact that . For similar arguments as those found below (S5) give , and hence

(S9) since for all . For we first note that and therefore . Moreover, we use the factorization to obtain212121For any , we have the inequality . This implies that .

(S10) because and thus . Combining all previous results for gives

Since , we use the bounds on and to bound the integrand of (S7) as follows:

The asymptotic order of relies on the values of . We distinguish three cases: (1) if , then , (2) if , then , and (3) if , by Lemma S1(i). Overall, we have