Stopping spikes, continuation bays

and other features of optimal stopping

with finite-time horizon

Abstract.

We consider optimal stopping problems with finite-time horizon and state-dependent discounting. The underlying process is a one-dimensional linear diffusion and the gain function is time-homogeneous and difference of two convex functions. Under mild technical assumptions with local nature we prove fine regularity properties of the optimal stopping boundary including its continuity and strict monotonicity. The latter was never proven with probabilistic arguments. We also show that atoms in the signed measure associated with the second order spatial derivative of the gain function induce geometric properties of the continuation/stopping set that cannot be observed with smoother gain functions (we call them continuation bays and stopping spikes). The value function is continuously differentiable in time without any requirement on the smoothness of the gain function.

Key words and phrases:

optimal stopping, free boundary problems, continuous boundary, smooth-fit, local time, one-dimensional diffusions.1. Introduction

In this paper we analyse in depth some fine properties of optimal stopping problems with finite-time horizon and state-dependent discounting, when the underlying process is a time-homogeneous one-dimensional diffusion and the stopping payoff is also time-homogeneous. Under very mild (local) regularity conditions on the stopping payoff and the diffusion process we provide results concerning the smoothness of the value function (in time) and the geometry of the optimal stopping boundary.

Denoting by the stopping payoff (or gain function) and by the underlying process, we show that when is just the difference of two convex functions the value function of the problem is continuously differentiable in time. Moreover, the geometry of the stopping set depends in a peculiar way on the interplay between the second-order weak derivative (interpreted as a signed measure) and the local-time of , via the so-called Lagrange formulation of the stopping problem, obtained as an application of Itô-Tanaka-Meyer formula. Among other things we are able to identify sufficient conditions for the formation of continuation bays and stopping spikes, neither of which would occur in the case of a smoother gain function. Both phenomena appear as a result of the presence of atoms in the measure : continuation bays are associated to positive atoms and stopping spikes are associated to negative ones. It is important to recognise that these features are far from being artificial and indeed occur in very natural optimal stopping problems, as illustrated in Examples 4.1 and 4.2 of Section 4, including the celebrated American put/call option problem.

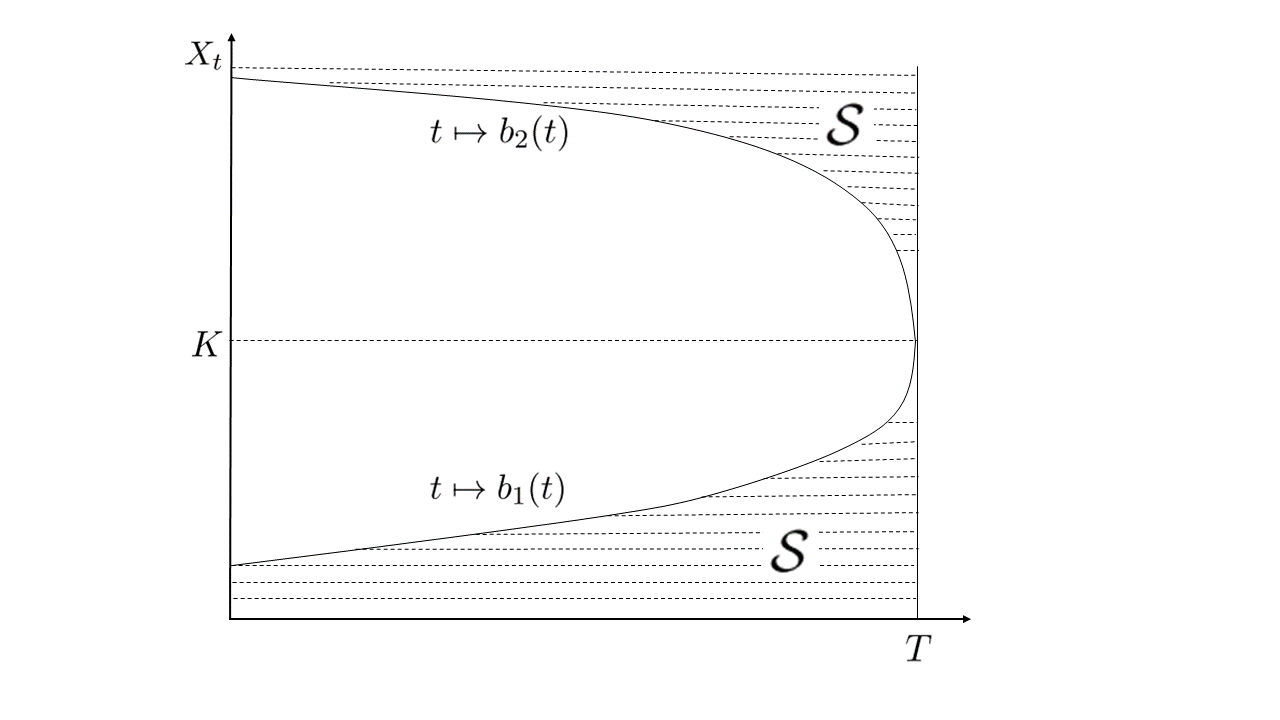

One key result of the paper concerns the strict monotonicity of time-dependent optimal stopping boundaries (Corollary 5.5). In the literature we can find a wealth of numerical illustrations of optimal boundaries that exhibit a smooth profile and strict (piecewise) monotonic behaviour (see, e.g., numerous examples in [38]). While the probabilistic study of continuity of the map has a relatively long history (classical tricks are presented in [38] and more recent results can be found in [9] and [37]) we are not aware of any rigorous probabilistic proof of the strict monotonicity. This question is addressed in Section 5 of the paper where we give simple sufficient conditions for the strict monotonicity of the optimal boundary and provide a proof based on probabilistic methods and reflecting diffusions. The result complements analogous classical results from the PDE literature, which normally require more stringent conditions on the problem data (traditional references are [3] and [20], among many others). As an application we show that the optimal exercise boundary of the American put in the classical Black and Scholes model is indeed strictly increasing as a function of time (Example 5.1). To the best of our knowledge this is the only existing probabilistic proof that does not require any assumption on the smoothness of the boundary itself (PDE methods were used for example in [4] and [16] and we are also aware of a probabilistic proof in [44], which however requires -regularity of the optimal boundary).

An important feature of our work, that sets it apart from the majority of papers in the field, is that we conduct a local study of the problem. That is, we provide our results under assumptions concerning the local behaviour of the underlying diffusion and of the gain function, rather than their global behaviour. This allows wide applicability of our methods to specific problems and extensions beyond our set-up are possible on a case by case basis. As part of our methodology here we study the boundary of the stopping set as a function of the spatial variable, i.e., , rather than as a function of time . This choice is natural, due to the time-homogeneity of both the gain function and the diffusion process, but it is not very common in the literature. Such parametrisation turns out to be very fruitful as we are able to perform a detailed study which includes continuity and strict (piecewise) monotonicity of the map , without requiring any convexity or monotonicity of the gain function (nor any structural assumption on the state-dependent discount rate). Then can be inverted locally to obtain a local representation of the optimal boundary as a function of time, , which is continuous and strictly monotonic.

There is a broad class of problems that falls directly within the framework of our paper. Along with the already mentioned American put problem (see, e.g., [24]), we find numerous other applications from American option pricing (e.g., chooser options [5] and strangle options [14]), options embedded in insurance policies (see, e.g., [6] and references therein) and technical analysis (see [12]). An early contribution to optimal stopping theory fitting in our set-up is [29], which proposes a constructive procedure to identify the optimal boundary, based on PDE methods, under the requirement that the gain function be three times continuously differentiable. Stopping problems related to Röst’s solution of the Skorokhod embedding problem are also covered by the present paper: [34] addresses the question from a PDE point of view, [10] from a probabilistic one and [11] obtains the optimal boundaries numerically ([8, Rem. 3.5] and [7, Rem. 17] also contain valuable insight on the connection between Röst embedding and optimal stopping). Finally, our set-up covers special cases of several theoretical papers on optimal stopping and free boundary problems. Just to mention some early contributions from both the PDE and the probabilistic strand of the literature, we refer to [43] and [32] which consider time-homogeneous gain function and underlying (multidimensional) arithmetic/geometric Brownian motions, [23] which also allows for time-inhomogeneous diffusions and, finally, [25] which includes both time-inhomogeneous gain function and underlying diffusion.

It is also worth drawing a parallel with the two closely related papers [31] and [30] (notice that [30] mentions [31] as a preprint). In [31], Lamberton and Zervos study infinite-time horizon optimal stopping problems for one-dimensional linear diffusions when the gain function is time-homogeneous and difference of two convex functions. That paper deals mainly with the variational characterisation of the value function but it also addresses optimal boundaries in specific examples. Differently to the present paper, in [31] the state space is one-dimensional and optimal boundaries are points on the real line. We can think of our paper as an analogue of [31] but in the finite-time horizon setting. The methods used in [31] are those from the theory of one-dimensional diffusions and ordinary differential equations, which do not apply here because the free boundary problems associated to our optimal stopping problems are of parabolic type. The analysis from [31] is then extended by Lamberton in [30] to the finite-time horizon framework. The underlying process is a one-dimensional linear diffusion and the gain function is time-homogeneous but it is only bounded and Borel measurable as function of the state-process. It is shown in [30] that the value function of the optimal stopping problem is continuous and it is the unique (bounded continuous) solution of a variational problem understood in the sense of distributions. Our work complements [30] by focussing on the study of the geometry of the optimal stopping set and on the regularity of its boundary.

The paper is organised as follows. In Section 2 we formulate the problem and recall useful facts on optimal stopping and one-dimensional linear diffusions. Then we show existence of an optimal boundary and prove its regularity in the sense of diffusions. Section 3 is devoted to proving that the time derivative of the value function is continuous in the whole space. Fine geometric properties of the continuation/stopping set are addressed in Section 4 whereas the continuity of the map (or equivalently the strict monotonicity of its inverse ) is studied in Section 5. The paper is completed by a technical appendix.

2. Setting

2.1. The underlying process and the gain function

Let us consider a complete probability space equipped with a Brownian motion and its filtration , which is augmented with -null sets. Let be a linear diffusion on an open (possibly unbounded) interval . We assume that be determined as the unique strong solution of the stochastic differential equation (SDE)

| (2.1) |

for a suitable . We also require that be a Feller process, hence strong Markov thanks to continuity of paths. We further assume that the diffusion is infinitely-lived, in the sense that the endpoints of the interval are natural in the terminology of [2, Chapter II] (in particular this means that and are not attainable by the process in finite time and the process cannot be started from those points).

To summarise we impose:

Assumption 2.1.

The process is strong Markov and it is the unique strong solution of (2.1). The endpoints and of are natural.

To keep the exposition simple, we also make the next mild assumption on the diffusion coefficient.

Assumption 2.2.

We have and strictly positive in . In particular, for any compact there exist constants such that

Assumptions 2.1 and 2.2 are enforced throughout the paper. Sometimes we will use the notation to keep track of the flow property of the process or, alternatively, we will denote .

Fix a time and continuous functions and such that, for any compact ,

| (2.2) |

The problem we are interested in is the following finite-time horizon optimal stopping problem:

| (2.3) |

where the supremum is taken over stopping times of the filtration .

Throughout the paper the minimal regularity assumption on the function is that

Then, its first (weak) derivative exists as a function of bounded variation (which can be taken to be either right or left continuous) and its second (weak) derivative exists as a signed measure on . For the sake of concreteness, and following [41, Chapter VI.1], we take as the left-derivative of . So is left-continuous with right-limits on . Finally, the measure is defined in the usual way via

Let us now introduce

| (2.4) |

Here denotes the local time of the process at a point , which is defined as

| (2.5) |

where is the quadratic variation of . For the analysis that follows in the next sections, it is convenient to decompose the signed measure into its positive and negative part (see also Section 4):

Throughout the paper we denote by the closure of a Borel set .

In order to derive the next formula (2.6) we need a mild integrability condition:

Assumption 2.3.

For every

Thanks to the regularity of and Assumption 2.3 we can use Itô-Tanaka-Meyer formula (see [41, Thm. VI.1.5]) to write the problem in the so-called Lagrange formulation:

| (2.6) |

Since the endpoints of are natural the expression above follows from [31, Lemma 3.2]. For completeness we provide a full proof in the Appendix.

From standard theory on one-dimensional diffusions it is known that admits a transition density with respect to the speed measure which is continuous in all its variables (see [2, Chapter II.1.4] and [22, p. 149]). In other words, there exists a continuous function

| (2.7) |

such that for all Borel sets and any , where denotes the speed measure of . In our case, since on , we have

| (2.8) |

where is the derivative of the scale function of the process (since is in natural scale it simply holds for ). Then admits a transition density with respect to the Lebesgue measure.

Before closing this section we make a couple of observations concerning the generality of our model.

Remark 2.4 (Gain function and discount rate).

The requirement that the discount rate be non-negative can be easily relaxed to for some constant . Further relaxations are also possible but at the cost of additional integrability requirements, and we leave such extensions aside for the sake of clarity of exposition.

If then the value function of problem (2.6) takes the more familiar form

If we add a running profit function , the original problem in (2.3) reads

Then the problem in (2.6) becomes

with

Since all the key results of the paper are based on properties of the measure , they immediately carry over to problems in which is replaced by defined above.

Remark 2.5 (The underlying process).

It is important to notice that there is (almost) no loss of generality in assuming zero drift in the dynamics (2.1) of the process . Indeed, let us consider instead a strong solution of the SDE

| (2.9) |

on some interval , with and drift and diffusion coefficients that guarantee existence and uniqueness of the strong solution. Assume the endpoints of the interval are natural. Let us then consider the stopping problem

with Borel measurable functions and . Then we can reduce to the setting of (2.1) and (2.3) by a simple change of scale. That is, letting be the scale function of , we have that solves (2.1) with , and the stopping problem takes the form of (2.3) with and . Obviously here .

This approach can be extended even further to consider SDEs with generalised drift (in the sense of, e.g., [46]), again by adopting the change of coordinates via the scale function. However, we insist on the requirement that the SDE admits a unique strong solution because we use pathwise uniqueness in our arguments below (recall that weak existence and pathwise uniqueness imply strong existence; see, e.g., [27, Corollary 5.3.23]).

2.2. Generalities on the value function and existence of a boundary

Since admits a continuous transition density with respect to its speed measure, then the two-dimensional process enjoys Feller property. The latter, combined with continuity of and with (2.2), is known to be sufficient to obtain that

thanks to standard results from [42, Lemma 3, Sec. 3.2.3 and Lemma 4, Sec. 3.2.4]. As a consequence of (2.2) we also have

| (2.10) |

Further, we know from [42, Thm. 1, Sec. 3.3.1 and Thm. 3, Sec. 3.3.3] that

is the minimal optimal stopping time, where

is the so-called stopping set (notice in particular that by definition). We will sometimes use the notation to emphasise the dependence of this stopping time on the initial position of the time-space process; that is

Letting also the continuation set be denoted by

we immediately see that is open and is closed (relative to ) thanks to lower semi-continuity of . Given an interval , it will be sometimes convenient to work with sets of the form

and the associated boundary . We should always understand as .

Finally, it follows from standard theory ([42, Sec. 3.4]) that for

| (2.11) |

and, equivalently, from (2.6)

| (2.12) |

If we replace with the two stopped processes above are martingales on .

In our setting, the process is time-homogeneous and the gain function is independent of time. Therefore, it is immediate to verify that for any and

| (2.13) | ||||

so that

| (2.14) |

Such monotonicity of the value function identifies some sort of ‘privileged’ direction in the state space, in the sense of the following simple statement

Then, we can uniquely determine the boundary of the continuation set by defining

Since is a closed set we have that for any and any sequence , as , it holds

hence

In conclusion we can summarise the above discussion in the next proposition.

Proposition 2.6.

The stopping set can be expressed as

where is lower semi-continuous.

Remark 2.7.

It is worth noticing that, in the literature on finite-time horizon optimal stopping problems on a one-dimensional diffusion, it is customary to describe the stopping set in terms of a boundary which is time-dependent, rather than space-dependent. However, proving existence of such boundaries requires to show that, e.g., the map is monotonic, or at least convex. This type of argument will fail in general, if is just the difference of two convex functions and in the presence of a state-dependent discount rate.

Instead, the existence of the boundary is an immediate consequence of the monotonicity in time of the value function, which holds under even wider generality than ours. Indeed, a quick look at the argument in (2.13) reveals that monotonicity of is solely a consequence of the reduction of the set of admissible stopping times and has nothing to do with either the process , the discount rate or the gain function (provided the latter three are time-homogeneous).

For some of the results that follow, it is convenient to work with a continuous value function . Continuity is normally easy to prove in specific examples but also general results exist. For example, if is bounded and continuous and [35, Thm. 4.3] guarantees continuity of when is just a Feller process on a locally compact and separable space (not necessarily a solution of an SDE). Alternatively, for a non-exploding linear diffusion on an interval and locally bounded and measurable, [30] proves continuity of when is just bounded and measurable. Rather than giving another proof of the continuity of the value function, when necessary we will invoke the next assumption.

Assumption 2.8.

We have .

For we denote by the class of locally -Hölder continuous functions on . Continuity of the value function, along with the martingale property, Assumption 2.2 and a standard PDE argument gives the next corollary (see, e.g., the proof of [28, Prop. 7.7, Ch. 2]).

Corollary 2.9.

Remark 2.10.

The argument of proof of the corollary is based on exit times from open bounded sets contained in . As such, it has a ‘local’ nature that allows to relax the continuity assumption on the diffusion coefficient and discount rate. For our purposes, in Theorem 5.2, we will consider the case in which with an open set. Then and it satisfies

| (2.15) |

2.3. Regularity of the boundary in the sense of diffusions

There is an important consequence to Proposition 2.6. Indeed, it turns out that the boundary of the continuation set, , is regular for the stopping set in the sense of diffusions. We will review this property in detail below.

Denote the hitting time to the stopping set by

As before we denote when we need to emphasise the initial point of the process : that is

For any , it is clear that , -a.s., by definition. By continuity of paths and the fact that and are open sets (provided they are not empty), it is also clear that , -a.s., for all . In principle the strict inequality might hold with positive probability at points on the boundary . We are going to prove below that this does not happen in our setting. For that we need the following simple lemma, which we believe to be well-known but whose proof may be hard to locate in the literature; we give a proof in the Appendix for completeness.

Lemma 2.11.

Consider a Brownian motion , an interval and the stopping time

For any and any sequence such that as , we have

It is worth noticing that with for . Then we have and Lemma 2.11 holds as soon as we show that , -a.s., for any and any sequence . It is well-known that is an increasing Lèvy process and it is -a.s. left-continuous [41, Prop. III.3.8]. Moreover, there is almost surely no interval over which it is continuous. However, for a fixed and any sequence we have , -a.s. [41, Prop. III.3.9]. Combining the latter with left-continuity we have that , -a.s., for any and any sequence . Noticing that for , it is immediate to extend the arguments to the family by considering also for . Thus, the result in Lemma 2.11 can be deduced also from these standard facts111I am grateful to G. Peskir for showing me this elegant argument..

Building upon the previous lemma we can prove our next result.

Proposition 2.12.

Let and let be a sequence that converges to . Then,

| (2.16) |

Proof.

We give the proof in two steps. For simplicity and with no loss of generality we assume that is continuous and it satisfies the law of iterated logarithm for all .

Step 1. (). First we prove the result for , so that is a standard Brownian motion, , and the main ideas in the proof are more transparent. Actually, here we prove a stronger result and show that

| (2.17) |

If , then by definition and . By the law of iterated logarithm we know that for any and any , there exist such that

Hence, , for all . Let us now fix and . Then there is such that

Therefore, taking sufficiently large we have and , so that

Hence, there must exist such that , which implies

Since was arbitrary we have (2.17).

Step 2. (Any ). Let us now consider a generic diffusion coefficient that satisfies Assumption 2.2. The rest of this proof is slightly technical due to the fact that we localise the dynamics of on a bounded open interval with .

Denote

and

| (2.18) |

The process is absorbed when leaves the interval , it is a martingale thanks to Assumption 2.2, and can be represented, by Dambis-Dubins-Schwarz theorem ([40, Thm. IV.34.11]; see also [40, Thm. V.47.1]), as a time-changed Brownian motion. That is , where is a standard Brownian motion. Notice that depend on the initial point but for now we omit the dependence for simplicity.

Since on by Assumption 2.2, we can define the inverse of the quadratic variation for (this is done by ). Thanks to strict monotonicity of both and , both processes are also continuous and clearly . Then, we have

| (2.19) |

Here, the process depends on , via the initial condition , the stopping time and the Brownian motion obtained via time-change. By construction we have that , -a.s., and for , -a.s. Moreover

so that, in particular,

| (2.20) |

In conclusion is a Brownian motion absorbed upon leaving the interval and it is adapted to the time-changed filtration .

Having defined we can write explicitly ( by ) as

| (2.21) |

Again, we notice that depends on . Since we are interested in the event and we want to restrict our attention to the behaviour of the process (equivalently ) for ‘small times’, here we will always consider . In particular, using that is strictly increasing, we can write

where the inequality is due to replacing with in the definition of , and the final expression by simply relabelling the time variable . Then, setting

we obtain . By construction we also have . Using these inequalities we obtain

| (2.22) | ||||

for any given and fixed. So, it is sufficient to prove that the final expression above converges to zero along any sequence .

It is not very convenient to work with the Brownian motion when varies. We therefore set

with our original Brownian motion. Then, for each we have the equivalence in law

| (2.23) |

From (2.22) and the equality in law we have

| (2.24) | ||||

for any .

The advantage of working with is that only depends on via its initial point and therefore we can apply arguments analogous to those used in step 1 above. An initial observation is that

| (2.25) |

thanks to Assumption 2.2 and by definition of . Take , so that . By the exact same argument as in step 1 above we obtain , -a.s. Then, (2.25) implies , -a.s. as well. Next we are going to prove that

| (2.26) |

so that in (2.24) we have

| (2.27) |

thanks to (2.25).

Since is the first exit time of the Brownian motion from an open interval, then is continuous for any (in the sense of Lemma 2.11). Fix . By continuity of paths and, in particular, there exists such that . By continuity of we can assume that for all , with sufficiently large.

Now, we can repeat the arguments from step 1. For any , there exist and such that

Clearly, for sufficiently large we have . Given that and by (2.25), we can also pick sufficiently large such that .

Therefore, taking sufficiently large we have

which implies

The argument holds for any . Hence, (2.26) holds by arbitrariness of , and (2.27) follows. From (2.24), (2.25) and (2.27) we have

where the final inequality is by Fubini’s theorem and using , -a.s. by Lemma 2.11. Since , letting we arrive at (2.16). ∎

3. Regularity of the value function

In this section we show that the value function has a modulus of continuity with respect to the time variable and, under mild additional assumptions, it is indeed a locally Lipschitz function of time. Our proof uses properties of the local time of the process (generalising [13, Example 17]). For that we recall that the scale function density is and that is the transition density of the process with respect to the speed measure (Section 2.1). First we state an estimate for the local time of the process.

Lemma 3.1.

Let and fix . Then, for any we have

| (3.1) |

Proof.

Thanks to (2.5) we can select a sequence such that as and

By Fatou’s lemma and the definition of in (2.4) we get

| (3.2) | ||||

where we used for the first inequality. Writing the expectation in terms of the transition density and the speed measure (see (2.7) and (2.8)) we obtain

| (3.3) |

where

for some , , upon recalling that . Notice that we are using continuity of on .

Next we obtain a modulus of continuity for the value function with respect to time. Recall the decomposition of the signed measure into its positive and negative part.

Proposition 3.2.

For any and any in we have

| (3.4) |

In particular, if there exists a constant , depending on and , such that

| (3.5) |

then is locally Lipschitz.

Proof.

Clearly by monotonicity of . For the remaining inequality we use the representation of the problem in terms of the function (see (2.6)). Let denote the optimal stopping time for the problem started at . Then is admissible and sub-optimal for the problem started at . This gives

Now, using Lemma 3.1 in the above expression, we obtain (3.4), after an application of Fubini’s theorem. ∎

Remark 3.3.

The condition on the transition density in (3.5), is perhaps more neatly expressed in terms of the standard transition density (with respect to the Lebesgue measure), denoted here by . Indeed we notice that since

For many known transition densities we have that is uniformly bounded as soon as for some . Moreover, it is often the case that has an exponential decay at infinity (when is unbounded) so that mild growth conditions on will guarantee (3.5).

Remark 3.4.

It is worth mentioning that Lipschitz continuity in time of the value function was also proved by [23] using scaling properties of Brownian motion (in particular that for one has , with ). However, for the argument in [23] some additional regularity on and is needed (e.g., local Lipschitz continuity of both functions).

Theorem 3.5 ( time regularity).

Proof.

For we have and continuous (provided ). Corollary 2.9 guarantees that is continuous in and therefore it remains to show that is also continuous across the boundary .

Fix , with , and take a sequence such that as . With no loss of generality we assume that and for all and some . Further, we denote .

Next, let us derive an upper bound for . Fix and take . Let be optimal for and fix . Then . Finally, set

By the (super)martingale property of we have

| (3.6) | ||||

where the final equality holds because on by monotonicity of . Now, thanks to (3.5) we can find a constant , independent of and , such that

Then, plugging the latter estimate into (3.6), recalling that , dividing by and letting we obtain

| (3.7) |

We are now interested in taking limits as and showing that the right-hand side of (3.7) goes to zero. First, let us rewrite

| (3.8) |

From Proposition 2.12 we know that as . We can estimate the second probability as follows. Define as

along with the process on , which is the unique (possibly weak) solution of

Existence of a unique in law, weak solution of the above SDE is guaranteed by Assumption 2.2 and classical results (see [27, Ch. 5.5]). By strong uniqueness of (2.1) we also have for all , -a.s., for . Recall that for all . Therefore, using Markov inequality and Doob’s martingale inequality we obtain

| (3.9) | ||||

where the last inequality uses that by construction.

Remarkably, the time derivative is continuous irrespective of the regularity of the function . This is in line with [13], but a direct application of results therein is not straightforward due to the lack of smoothness of .

Remark 3.6.

Continuity of has important consequences for the spatial regularity of the value function as well. For we denote the class of -Hölder continuous functions on the closure of a set .

Corollary 3.7.

Proof.

Continuity of on follows directly from (2.15) and continuity of both and on . ∎

4. Continuation bays and stopping spikes

In this section we begin the study of the fine geometric properties of the optimal boundary . In contrast with the case of a smooth gain function, i.e., , in this section we show that the possible presence of atoms in the measure produces effects that cannot be observed in the more regular cases. These will be illustrated in Example 4.1 and 4.2 below.

By Hahn-Jordan decomposition [21, Ch. VI, Sec. 29] we can find two measurable sets and such that and for any measurable set . It is somewhat expected that the stopping set should lie in , where accumulating local time in the formulation (2.6) is costly. This result is known to hold when and below we present some extensions to our setting.

We are going to need the next lemma.

Lemma 4.1.

Fix and . Let be a compact, define and let

Then, for any and we have .

Moreover, setting we also obtain

| (4.1) |

Proof.

Let us set . Since , then . Recalling Assumption 2.2 and applying Itô-Tanaka formula, triangular inequality and Jensen’s inequality we easily obtain

| (4.2) | ||||

where , with a compact set that contains .

For (4.1) we repeat steps similar to those in a proof given in [37, Lemma 15], being careful about the various constants cropping up in our case. Denote

and notice that by Dambis-Dubins-Schwarz theorem, where is another Brownian motion (analogous to (2.18)). By continuity of we have

with and as above. Then, using Itô-Tanaka’s formula as in (4.2) with we also have

Letting denote the local-time at zero of the Brownian motion , a further application of Itô-Tanaka’s formula and optional sampling gives (notice that by Assumption 2.2)

where the final inequality uses that (Assumption 2.2) and monotonicity of the local time. Notice that the notation keeps track of the fact that and that the Brownian motion , obtained via time-change, also depends on through the quadratic variation . Next we proceed with simple estimates:

| (4.3) | ||||

It is well-known that the next chain of equalities holds in law under :

Then, we have also

upon noticing that since the law of is independent of .

As immediate consequence of the lemma we have the next result.

Proposition 4.2.

Let be such that . Then .

Proof.

Fix . Set and, for arbitrary , denote and . Notice that , -a.s. for . Notice also that and therefore . Since is admissible for any , then we have

| (4.5) | ||||

From the first claim in Lemma 4.1 we have

| (4.6) |

where we notice that the compact can be taken independent of for a fixed . Since is continuous at we can pick sufficiently small and such that

Having fixed , thanks to (4.1) we can find sufficiently small, so that the right-hand side of (4.6) is strictly positive. Hence we conclude that . Since was arbitrary, then . ∎

Let us now introduce suitable subsets of that will be useful to prove properties of and . For we denote by an open neighbourhood of and we set

Proposition 4.3.

If , then .

Proof.

Take an arbitrary and let be such that . Then, with because . Fix and let . Below we will use the following fact

| (4.7) |

whose proof we also provide in the Appendix for completeness.

The stopping time is admissible and sub-optimal for the stopping problem with starting point and by the continuity of paths of . Then, using (2.6) we obtain

where in the equality we used that , -a.s. for and the final inequality is by (4.7) and Fubini’s theorem. Since then . Recalling that can be chosen arbitrarily gives . Since was also arbitrary, then as claimed. ∎

Next we show that at points and that the stopping set is connected in the sense of (4.9) below. For that, it is convenient to recall continuity of the value function and for simplicity we will also require the integrability condition

| (4.8) |

The latter strengthens slightly the requirement in (2.2) by adding uniform integrability of the discounted process .

Proposition 4.4.

Proof.

We divide the proof into two steps.

Step 1. (Proof of (i)). To prove the first statement we argue by contradiction. Let us first assume that and for all . We use ideas as in [9] but without requiring smoothness of . Consider the rectangular domain with parabolic boundary . By Corollary 2.9 and Remark 2.10 we know that is the unique solution of the boundary value problem

| (4.10) |

Monotonicity of and (4.10) imply

Let with and , multiply both sides of the inequality above by and integrate over . Integration by parts gives

Letting in the above we obtain

where the final equality uses dominated convergence, continuity of the value function and . Undoing the integration by parts we reach a contradiction with

where the strict inequality holds by arbitrariness of and . Then

| (4.11) |

By the exact same argument we can show that cannot contain isolated points in (otherwise we could construct a suitable rectangle and reach a contradiction as above).

Next we show that (4.9) holds for any two points in . Let us argue by contradiction again: take any two points in , set and assume there exists such that . Then, because the segments , , lie in the stopping set (recall that is the first time enters ). Then,

| (4.12) |

gives us a contradiction and (4.9) holds.

Since (4.9) holds in and the latter set has no isolated points in we conclude that for all . Indeed, assume by way of contradiction that there is such that . There are with and (4.9) holds for such and . Then we have reached a contradiction.

Step 2. (Proof of (ii)). It remains to prove the final statement. Let be such that . Fix and let for any , with . Since , then and we have

Here is the value function of a stopping problem of the form (2.6) but with replaced by the measure

with the Dirac’s delta at . Clearly this problem enjoys the same properties of the original one: the gain function associated to (i.e., ) is difference of two convex functions and, up to an affine transformation, it can be chosen so that for a suitable constant depending on ; hence (2.2) holds for thanks to (4.8). Differently to the measure is strictly positive on . That is, , where is the analogue of for the measure . Then, by the same argument as in the proof of Proposition 4.3 we have , where we denote . Notice that since , then .

Now, arguing by contradiction we assume . Then and the latter implies also , by the discussion above. This will lead to a contradiction. Fix and , and let

Then, letting be the optimal stopping time for , we have because and by assumption. Using the martingale property (2.12) for the value function and noticing that for all , we have

where is finite thanks to (2.10) applied to . By the exact same arguments as in the proof of Lemma 4.1 (see (4.2) and (4.4)) we obtain the upper bound

where , and . Since , then the same holds for and we can select sufficiently small that

Hence,

By continuity of paths of it is clear that as so that we can let in the limit. Then both terms on the right-hand side above go to zero, with the second term being strictly negative and vanishing as when . Assume that as , then there exists such that for and we reach a contradiction with .

It remains to show that as . For that, we define as

along with the process on , which is the unique (possibly weak) solution of

By strong uniqueness of (2.1) we have for all , -a.s., for . Therefore, using Markov inequality and Doob’s martingale inequality we obtain

which concludes the proof. ∎

Remark 4.5 (Flatness of ).

The argument we used in step 1 of the proof above to obtain (4.11) was originally designed in [9] to show continuity of optimal boundaries as functions of time. Here, as a byproduct of the proof we obtain that the map cannot exhibit a flat stretch, which is also strictly positive, on . That is, if there exists an interval such that for , then it must be . The proof is an exact repetition of the one for (4.11), so we omit it.

There is a nice monotonicity result that follows as a corollary from Proposition 4.4. First notice that given any interval the boundary attains a global minimum on by lower semi-continuity. Then we can define the set of minimisers

and for any . Notice that is a closed set by lower semi-continuity of the boundary.

Corollary 4.6.

Let Assumption 2.8 hold, let and assume for some . Then for some (with if ). Moreover, if then on . Finally, is strictly decreasing on and strictly increasing on (with ).

Proof.

Let belong to . Then and (4.9) implies that . Since is the global minimum, then for all . Hence and since were arbitrary and is closed we conclude that for some . If then on and this can only occur if (Remark 4.5).

For the final claim, assume and, arguing by contradiction, that there exist in such that . By definition of we have . Then by (4.9) and it must be . By the same argument there cannot exist such that and therefore we conclude that for all . From Remark 4.5 we know that cannot be flat, unless it is equal to zero. However, and therefore . Thus we have reached a contradiction and is strictly decreasing on . By the same argument we can prove that the boundary is strictly increasing on . ∎

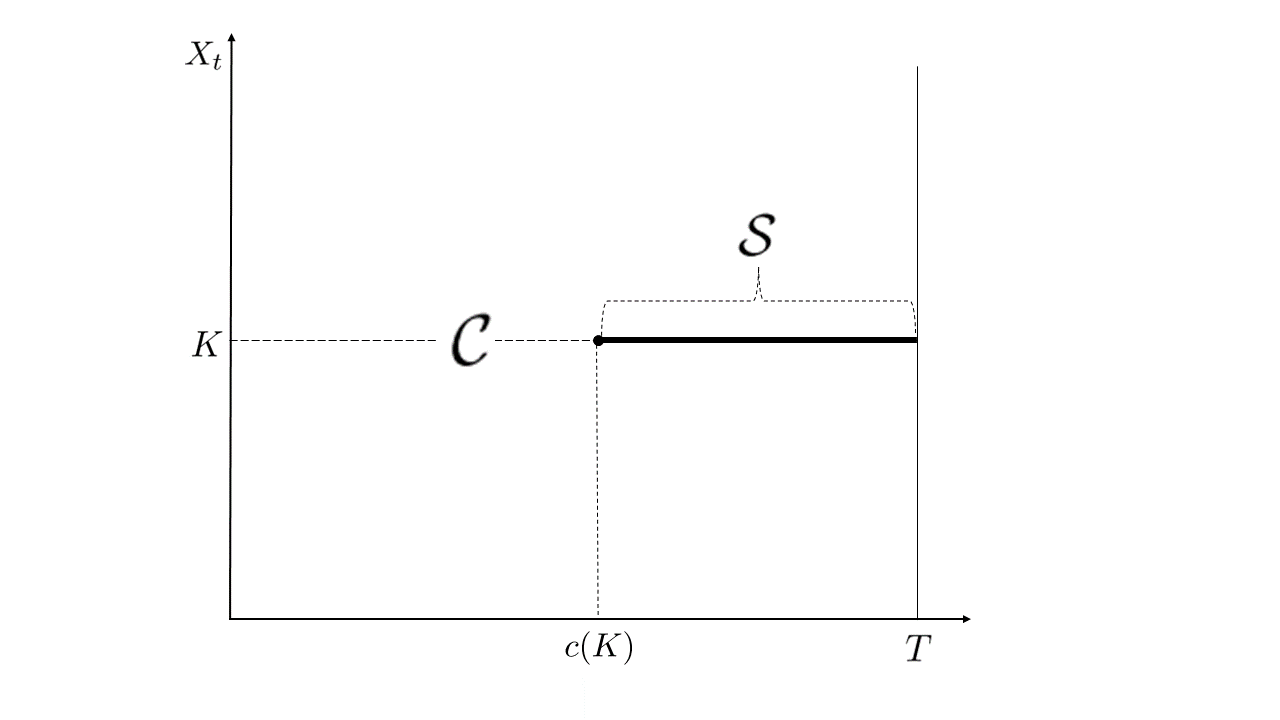

Proposition 4.2 holds at any point such that , irrespective of the sign of in a neighbourhood of . We will see in the next example that this argument, combined with Proposition 4.4, can produce very peculiar shapes of the continuation set. Loosely speaking we can say that we find a continuation bay in the middle of a stopping set.

Example 4.1 (Continuation bays).

A typical example of continuation bay arises in the American straddle option (see, e.g., [14]). Let us consider a simplified version here and let

be the stock’s dynamics with . Fix and and let us denote the value of the option by

Then, by an application of Itô-Tanaka’s formula we have

where .

Here we have and , which is a rather ‘singular’ situation. Intuitively, waiting is costly for the option holder at all times for which : indeed, she pays a cost at a rate . On the contrary, waiting is rewarding only at times when and the option holder receives a reward at the ‘rate’ of . As we will see shortly, it is precisely the kink in the payoff that guarantees and makes the problem mathematically non-trivial.

From (i) in Proposition 4.4 we obtain that for all , whereas Proposition 4.2 guarantees . By the same arguments we used to prove (4.9) we can also show that for any we have . Indeed, assume by contradiction that there exists such that for ; then, and we obtain the analogue of (4.12) with and replaced by . Hence a contradiction. Likewise, we can show that for any , we have . Finally, Corollary 4.6 implies that is strictly increasing on and strictly decreasing on , hence it can be inverted (locally) defining two boundaries which are continuous functions of time. Indeed, let for and for , then we can set

The functions and are continuous with . It may be worth noticing that a one-sided version of continuation bay appears by the same argument also in the American put and call options.

A reverse situation is observed at points such that . In this case, if on a neighbourhood of , we observe a stopping spike in the middle of the continuation region. This type of geometry of the stopping set is almost unique and certainly not very popular in the literature. The only examples of a similar geometry that we are aware of appear in [36] and [15] but the settings are different: in both references the gain function is time-dependent and in [36] it is discontinuous in the spatial variable whereas in [15] it is discontinuous in the time variable. So it is difficult to draw a clear parallel. More closely related is the situation of game call options where, for some parameter choice, the option seller will only stop if the underlying asset’s value equals the strike price (see, e.g., [17, 18, 45]).

This time we need to recall (ii) from Proposition 4.4.

Example 4.2 (Stopping spikes).

For simplicity we consider a converse to Example 4.1. That is, we take

and, for a fixed , we consider

Here the stopper may be the seller of a cancellable straddle option of European type, who must pay a fee of (in addition to the option’s current payoff) in order to cancel the contract. Although the problem is stated as a minimisation, it is clear that it is equivalent to

so that our arguments apply directly with . In particular, by the same calculations as in Example 4.1 we obtain , which gives us

So and, by (ii) in Proposition 4.4, we know that . Hence,

is just a spike in the continuation region.

Notice that, due to discounting and to the presence of a cancellation fee , if is sufficiently large we expect , as stopping at is not necessarily optimal if the time to maturity is long.

5. Continuity of the boundary

Here we address the question of continuity of the map and its link to strict monotonicity of time-dependent optimal stopping boundaries. For we denote the class of continuously differentiable functions on whose first order derivative is also -Hölder continuous on . Throughout the section we need to invoke Theorem 3.5 several times, so we state the next assumption:

Assumption 5.1.

The bound in (3.5) holds with a constant which is uniform for on compact subsets of .

The proof of the theorem hinges on the following two lemmas.

The proof is essentially an application of the maximum principle and we give it in Appendix for completeness.

The proof is inspired by [13] but we cannot directly invoke any of the results therein due to the local nature of our assumptions. However, if we strengthen the requirements in the lemma to, e.g., , then [13, Theorem 10] applies directly yielding . In several practical applications Lemma 5.4 may be better suited and therefore we give a full proof in Appendix.

Proof of Theorem 5.2.

Since changes its monotonicity at most once on (Corollary 4.6) and it is lower semi-continuous, we only need to rule out discontinuities of the first kind. In particular, with no loss of generality we may assume that is strictly increasing on as the argument is analogous for decreasing boundaries and combining the two we can handle the general case.

First we notice that since is strictly increasing and lower semi-continuous on , then it must be left-continuous. It then remains to prove that it is also right-continuous. Arguing by contradiction let us assume that there exists such that . Then and there exists and such that

| (5.1) |

thanks to Lemma 5.3 and the fact that is continuous. Setting and combining Lemma 5.4 and Theorem 3.5 (recall also Remark 3.6) we can also conclude that . Then for any there exists such that and

| (5.2) |

by uniform continuity on any compact. Classical results on interior regularity for solutions of PDEs guarantee and

| (5.3) |

(see, e.g., [19, Thm. 10, Ch. 3, Sec. 5]).

Since on , we may expect that be continuous at and equal to zero. From a PDE perspective that would enable the use of Hopf’s lemma to reach a contradiction. Here instead we present a probabilistic analogue based on the construction of a process which is normally reflected ‘near’ the discontinuity of the boundary. This approach avoids to deal with continuity up to the optimal boundary of the value function’s derivatives of order greater than one.

On the interval we consider a process that is equal to away from , it is reflected (upwards) at and it gets absorbed at . For the construction of such process we extend the diffusion coefficient outside to be and strictly separated from zero. With a slight abuse of notation let us denote such extension again by . Then, it is well-known (see, e.g., [33] or [1, Sec. 12, Chapter I]) that there exists a unique strong solution of the stochastic differential equation

where is a continuous, non-decreasing process, with , that guarantees

| (5.4) |

Setting the absorbed process is obtained as .

Letting we can apply Itô’s formula for semi-martingales and use (5.3) to obtain, for any

| (5.5) | ||||

where the inequality follows from (5.2) and for the term under expectation we use (5.4). For the expression on the left-hand side of (5), denoting and recalling that , thanks to (5.1) we have

Hence, setting for simplicity , from (5) we obtain

| (5.6) | ||||

The next step is to let . In order to take care of possible issues with the regularity of as we adopt an approach using test functions. Pick a non-negative function such that . Then, multiplying both sides of (5.6) by , integrating over and using Fubini’s theorem we obtain

| (5.7) | ||||

where we are also using that is independent of . Let us now look more closely at the integral on the right-hand side above: integration by parts and the second estimate in (5.2) give

where the final equality follows by integrating over . Using the expression above in (5.7) along with we obtain

where the final inequality uses that for and is the supremum norm on .

From the integral form of the dynamics of we obtain

and

Then, taking limits as gives

| (5.8) |

Showing that the left hand side above is positive will give us a contradiction. Hence there cannot be a discontinuity of at .

Setting and adopting the same time-change as in step 2 of the proof of Proposition 2.12 (see (2.18) and (2.19)) we obtain, using the same notation,

with and the first time the process leaves the interval (let us also recall that the Brownian motion depends on the initial point ). By construction and recalling (5.4) we have that the process solves (uniquely) the classical Skorokhod reflection problem

| (5.9) |

Therefore we have an explicit formula for the increasing process (see, [27, Lemma 6.14, Chapter 3]):

It may be worth noticing that reversing this construction gives another proof of the existence and uniqueness of the solution of the original reflected SDE for .

From (2.18) we have

where (recall that we extended to so that it is also strictly separated from zero). Hence

| (5.10) |

As in the proof of Proposition 2.12 (see (2.23)) we need to pass to auxiliary processes

in order to remove the dependence of the Brownian motion on the initial point. Then, setting and recalling , we have

since .

It is immediate to check that

with and where is a Brownian motion reflecting at . Hence, from (5.10) and the above construction we have

where in the second inequality we used that

and that, for each , the law of is the same as the law of (see, e.g., [27, Thm. 6.17, Sec. 3.6.C]).

Finally, using Fatou’s lemma in (5.8), and the discussion above, we conclude

where the final inequality uses that and arbitrary. Hence a contradiction and continuity of is proved. ∎

Thanks to Corollary 4.6 we know that the boundary admits a continuous inverse on and on . In particular, denoting and setting for and for we can define

| (5.11) |

Notice that if (respectively ) we understand (respectively ) to be constant and equal to for (respectively equal to for ). Combining Theorem 5.2 and Corollary 4.6 we obtain the next result.

Corollary 5.5.

This result immediately applies to the setting of Example 4.1. Moreover, as a by-product we obtain the first known probabilistic proof of the strict monotonicity of the American put boundary.

Example 5.1 (American put boundary).

Let us consider the classical Black and Scholes set-up where

is the stock’s dynamics with . Let be the strike price and , then the value of the American put option is

Although this problem is perhaps the best studied optimal stopping problem in the literature, it is convenient to rewrite some of the main results in the notation of our work so far. The scale function of the process (up to affine transformations) reads with . Recalling the argument from Remark 2.5 we set and find the dynamics

It is worth noticing that if the process is strictly negative, while if then the process is positive. For simplicity but with no loss of generality let us consider .

Setting and , the optimal stopping problem becomes

We now set and notice that has a positive atom at with . Then, using (2.6) (see also Remark 2.4) we obtain

where

Here we have , and , which is a similar situation to the one in Example 4.1. Intuitively, waiting is costly for the option holder at all times for which , whereas waiting is rewarding at times when (the option holder receives a reward at the ‘rate’ of ). Differently to Example 4.1, here so that the option holder incurs no costs and no benefits when waiting if .

From (i) in Proposition 4.4 we obtain that for all , whereas Proposition 4.2 gives . In addition one can easily prove for and all . Then for as well. By analogous arguments to those in the third paragraph of Example 4.1 for any we have . Finally, Corollary 4.6 implies that is strictly increasing on , hence it can be inverted defining a continuous, non-decreasing boundary . In the original coordinates the optimal exercise boundary reads . The latter is the familiar parametrisation of the American put exercise boundary (see, e.g., [38, Ch. VII, Sec. 25.2]). Now, applying Corollary 5.5 with and we conclude that must be strictly increasing. Hence is strictly increasing too.

Appendix

Proof of (2.6)

The process is a continuous local martingale, so Itô-Tanaka-Meyer formula ([41, Thm. VI.1.5]) gives:

| (5.12) |

Here the fact that is bound to evolve in implies that

| (5.13) |

since for . It is also worth recalling that can be chosen -a.s. continuous by [41, Thm. VI.1.7 and Corollary VI.1.8]. Then is a continuous semi-martingale and by Itô’s product rule and (5.12) we have

| (5.14) | ||||

where we used Fubini’s theorem to swap the order of integrals in the final term (this can be justified more formally using the same arguments as in (5.15) below, so we avoid repetitions here).

For the integral with respect to we use the occupation times formula. Let us rewrite in terms of its positive and negative part, i.e., . Since

is a positive Borel-measurable function, then [41, Corollary VI.1.6] holds and

for all , -a.s. Notice that even though may vanish when approaches the endpoints of , the final integral above is well-defined because the initial expression for is always finite. For a.e. the mapping

defines a (finite) signed measure on . Moreover, for simple functions (possibly depending on as well) it is easy to check that

Thus, by dominated convergence the equality extends to any bounded measurable function. In particular, choosing we deduce

| (5.15) | ||||

Almost sure finiteness of the last integral is guaranteed by finiteness of the initial expression in the equation. See also [40, Theorem 45.4, Chapter IV] and [41, Exercise 1.15, Chapter VI.1].

Combining (Proof of (2.6)) and (5.15), for any stopping time we obtain

| (5.16) |

with and as in (2.4). Let be a localising sequence for the local martingale in (5.16). Taking expectations we have

Letting we have and

by dominated convergence and (2.2). By monotone convergence we also obtain

Since Assumption 2.3 holds, the above implies

Then (2.6) follows by combining the limits above.

Proof of Lemma 2.11

For simplicity and with no loss of generality we adopt the standard convention that is continuous for all . In what follows we denote

the exit time from the closed interval . Fix and let be a sequence converging to .

Step 1. Here we show that

| (5.17) |

If , then for all simply by definition. Hence lower semi-continuity is obvious. If , then for all by continuity of Brownian paths. Fix and take an arbitrary such that . Then there exists such that for all and consequently for all and for all ’s such that . Therefore, and, since was arbitrary, we have

Recalling that was also arbitrary, lower semi-continuity holds as in (5.17).

Step 2. Here we show that

| (5.18) |

Fix and take an arbitrary such that . Then there exists such that . Since is an open set, we can find sufficiently large that for all . Hence

Since was arbitrary

and recalling that was also arbitrary, upper semi-continuity holds as in (5.18).

Step 3. Here we conclude the proof by showing that

| (5.19) |

For each let (notice that we include ). Then it follows from the strong Markov property for Brownian motion and the law of iterated logarithm that for each . Setting we have and

| (5.20) |

Thus, combining (5.17) and (5.18) with (5.20) we have

for all . This proves (5.19).

Proof of (4.7)

First of all we notice that since for all , then

because the discount factor is bounded from below by with .

Now we can use the same time-change as the one adopted in step 2 of the proof of Proposition 2.12 (see (2.18)–(2.19)) with therein replaced by . Thus we get

where depends on but we can drop this dependence from our notation as is fixed throughout the proof. Let us denote by the local time of the process at . From Itô-Tanaka’s formula we get

where the second equality is by [27, Prop. 3.4.8] and the final one is by Itô-Tanaka’s formula applied to . So our problem reduces to proving that

Recall that with . Moreover, setting , Assumption 2.2 gives . Then

Set for simplicity. Let be smooth approximations of such that uniformly on with pointwise and in the sense of distributions. Then, taking expectations in Itô-Tanaka’s formula and using dominated convergence yields

where we used Fubini’s theorem in the final line and is the transition density of the Brownian motion killed upon leaving the interval (cf. [2, p. 180, Eq. 1.15.8]). Since is continuous, then it is not difficult to check that

using integration by parts. That concludes the proof of (4.7).

Proof of Lemma 5.3

This proof repeats verbatim an argument from [6, Lemma 4.7] but adapted to out notation and setting. By contradiction we assume there is with such that . Since and , there must exist such that and , for some . By continuity of inside (recall Remark 2.10), and the fact that the set is open, there exists such that for .

Letting , we have that thanks to internal regularity results for solutions of partial differential equations applied to (2.15) (see, e.g., [19, Thm. 10, Ch. 3, Sec. 5]). Moreover, differentiating (2.15) with respect to time and recalling that is non-increasing, we obtain that solves

| (5.21) | |||

| (5.22) | |||

| (5.23) |

Setting

an application of Dynkin’s formula gives the following contradiction:

where the strict inequality holds because the process exits by crossing the segment with positive probability, i.e., .

Proof of Lemma 5.4

For future reference let us denote . Recall that by Corollary 2.9 and Remark 2.10. Then is continuous separately in and in the interior of the stopping set . Then we only need to look at the regularity across the boundary . An important observation which will be used several times below is that

| (5.24) |

for any , thanks to Corollary 3.7.

With no loss of generality we assume as the argument for is analogous. In this case Corollary 4.6 implies . If or then the boundary is strictly monotonic on . In the more general situation when we need to consider separately the intervals and where the boundary is strictly decreasing and strictly increasing, respectively. Below we develop our arguments only for as the remaining case follows along the same lines up to obvious changes.

Take and for any let

| (5.25) |

Take as an extension of outside the interval . Letting be the unique strong solution of

and the exit time of from we have -a.s. the equalities

| (5.26) |

We will use such equivalence later on.

Fix with and . Take such that and let . Taking optimal for and optimal for we notice that , -a.s. because the boundary is increasing on and, since , the process cannot enter the rectangle before hitting the stopping set (recall ). Then, letting for simplicity and using the martingale property of the value (see (2.11)) we have

Subtracting the two expressions we obtain

| (5.27) | ||||

First we obtain a lower bound. For the first term in (5.27) we recall that is bounded on compacts (see (2.10)), we set and use the mean value theorem and to obtain

| (5.28) | ||||

where

For the second term in (5.27), recalling that and by optimality of , we obtain

Since we have . Since is strictly increasing on with (Proposition 4.4), on the event it holds

with the continuous inverse of on . Then, for any , on the event the segment lies in and we can use the fundamental theorem of calculus (twice) to obtain

Due to the strict monotonicity of the boundary and the fact that for , there exists such that . Moreover, by definition of , on the event we also have . Then, recalling (5.24), on the event we have

for some , independent of . Hence,

| (5.29) | ||||

for some deterministic constant independent of , where we use that is bounded on since and . Then, substituting the estimates above back into (5.27) we have

| (5.30) | ||||

Thanks to (5.26) and due to the local nature of the argument we are using, we may substitute with in all our calculations above. Therefore, there is no loss of generality assuming that is continuously differentiable in all the expressions above (since is such by, e.g., [39, Ch. V.7]) and moreover the process evolves according to

In particular, admits a continuous modifications (which we use in the rest of the proof) and

Thanks to the arbitrariness of and the explicit formula for we can also assume with no loss of generality that

| (5.31) |

Dividing both sides of (5.30) by and rewriting

we obtain

where . By time-change arguments as in step 2 of the proof of Proposition 2.12 we can reduce to a Brownian motion and then apply Lemma 2.11 to obtain convergence in probability of to (analogously to (2.16)). Then, taking limits as , along a suitable sequence , we have , -a.s. Moreover,

for any stopping time . Since is strictly increasing on and for any , we have as so that for all and some (recall that and therefore, prior to being absorbed, the process can only leave the rectangle by either hitting or ).

Then, by continuity of on and dominated convergence (recall (5.31)) we obtain the lower bound

| (5.32) | ||||

For the upper bound, starting from (5.27) we have

by the same argument as in (5.28). For the second term in (5.27) we have

| (5.33) | ||||

The second term on the right-hand side can be treated with the same estimates as in (5.29) and gives

For the remaining term in (5.33) we notice that, on the event , strict monotonicity of the boundary implies , -a.s., with . Therefore, arguing as in (5.29) and using that on the event for all sufficiently large ’s, we get

where we are also using (5.24) to justify the limit of the double integral. Combining the above we obtain

We need a slightly more refined estimate for the last term above. In particular, recalling (5.29) and rearranging the indicator functions we have

As in (5.32), we take limits as along the same subsequence . In order to use dominated convergence we recall (5.31). Moreover, we notice that

| (5.34) |

are -a.s. bounded and continuous thanks to (5.24) and since for some , by strict monotonicity of , so that . Finally, recalling that and for a fixed and all , we find the upper bound

| (5.35) | ||||

It remains to take limits in (5.32) and (5.35) along an arbitrary sequence that converges to . Clearly there is no loss of generality in assuming with as above. Arguing by contradiction, assume that there is one such sequence for which

| (5.36) |

Thanks to Proposition 2.12 we can extract a subsequence, which we denote again by , such that , -a.s. By the same arguments (i.e., time-change and Lemma 2.11) we can also show that and , -a.s. (possibly selecting further subsequences). Since , recalling (5.31) we get

| (5.37) |

and

| (5.38) |

by dominated convergence. Moreover, and is continuous at (recall so that ). Then, by dominated convergence and the continuity arguments as in (5.34) we also get

| (5.39) | ||||

where the final equality holds and the right-limit exists because is continuous on (see (5.24)). Finally, we also have

| (5.40) |

by dominated convergence and continuity of at . We claim that so that combining the limits (5.37)–(5.40) with (5.32) and (5.35) we obtain

That contradicts (5.36) since the limit must be the same along any subsequence.

It remains to justify that . From the first two inequalities above we have so, arguing by contradiction, we assume . Notice that , with the continuous inverse of on , and the mapping is continuous in . We must consider separately the case and .

If , by the strict monotonicity of the boundary we can also assume with no loss of generality that and for (notice that is a continuous measure since ). Therefore defines a signed measure on with a single atom at . That is

| (5.41) |

Setting , by the super-harmonic property of the value function we have

where we used that for and there is a positive constant such that , thanks to Assumption 5.1 (which guarantees Theorem 3.5). Now we can use Itô-Tanaka-Meyer formula and (5.41) to rewrite the term under expectation and obtain

| (5.42) | ||||

where the second inequality uses that in . Since and , the measure is continuous and negative on . Then, the same estimates as in the proof of Lemma 4.1 (or Proposition 4.2) allow us to conclude that for sufficiently small we reach the contradiction

Hence as claimed.

If , either there is such that or (recall that is strictly decreasing on ). In the former case, we can repeat the same arguments as for the case but considering the interval and the stopping time in (5.42). In the latter case instead . Then is continuous (hence bounded) on by (5.24), with a single jump at . Since , and we are assuming , then . We can define the signed measure

| (5.43) |

and argue in a similar way as in (5.42). We then obtain the contradiction

with as in (5.25). Hence as claimed.

References

- [1] Bass, R.F., 1998. Diffusions and elliptic operators, Springer-Verlag, New York.

- [2] Borodin, A.N., Salminen, P., 2002. Handbook of Brownian motion: facts and formulae. 2nd Edition. Springer Basel AG.

- [3] Cannon, J.R., 1984. The one-dimensional heat equation (No. 23). Cambridge University Press.

- [4] Chen, X., Chadam, J., 2007. A mathematical analysis of the optimal exercise boundary for American put options. SIAM J. Math. Anal., 38(5), pp. 1613-1641.

- [5] Chiarella, C., Ziogas, A., 2005. Evaluation of American strangles. J. Econ. Dyn. Control, 29(1-2), pp. 31-62.

- [6] Chiarolla, M.B., De Angelis, T., Stabile, G., 2021. An analytical study of participating policies with minimum guarantee and surrender option. To appear in Finance Stoch. arXiv:2004.06982.

- [7] Cox, A.M., Peskir, G., 2015. Embedding laws in diffusions by functions of time. Ann. Probab., 43 (5), pp. 2481-2510.

- [8] Cox, A.M., Wang, J., 2013. Optimal robust bounds for variance options. arXiv:1308.4363.

- [9] De Angelis, T., 2015. A note on the continuity of free-boundaries in finite-horizon optimal stopping problems for one-dimensional diffusions. SIAM J. Control Optim., 53 (1), pp. 167-184.

- [10] De Angelis, T., 2018. From optimal stopping boundaries to Rost’s reversed barriers and the Skorokhod embedding. Ann. Inst. H. Poincaré Probab. Stat., 54 (2), pp. 1098-1133.

- [11] De Angelis, T., Kitapbayev, Y., 2017. Integral equations for Rost’s reversed barriers: existence and uniqueness results. Stoch. Process. Appl., 127 (10), pp. 3447-3464.

- [12] De Angelis, T., Peskir, G., 2016. Optimal prediction of resistance and support levels. Appl. Math. Finance, 23 (6), pp. 465-483.

- [13] De Angelis, T., Peskir, G., 2020. Global Regularity of the Value Function in Optimal Stopping Problems. Ann. Appl. Probab., 30(3), pp. 1007-1031.

- [14] Detemple, J., Emmerling, T., 2009. American chooser options. J. Econom. Dynam. Control, 33 (1), pp. 128-153.

- [15] Detemple, J., Kitapbayev, Y., 2018. American options with discontinuous two-level caps. SIAM J. Financial Math., 9 (1), pp. 219-250.

- [16] Ekström, E., 2004. Convexity of the optimal stopping boundary for the American put option. J. Math. Anal. Appl., 299 (1), pp. 147-156.

- [17] Ekström, E., Villeneuve, S., 2006. On the value of optimal stopping games. Ann. Appl. Probab., 16 (3), pp. 1576-1596.

- [18] Emmerling, T.J., 2012. Perpetual cancellable American call option. Math. Finance, 22 (4), pp. 645-666.

- [19] Friedman, A., 1964. Partial differential equations of parabolic type. Prentice Hall.

- [20] Friedman, A., 1975. Parabolic variational inequalities in one space dimension and smoothness of the free boundary. J. Funct. Anal., 18(2), pp. 151-176.

- [21] Halmos, P.R., 1974. Measure theory. Springer-Verlag, New York.

- [22] Itô, K., McKean, Jr., H.P., 1974. Diffusion processes and their sample paths. Springer-Verlag, Berlin.

- [23] Jaillet, P., Lamberton, D., Lapeyre, B., 1990. Variational inequalities and the pricing of American options. Acta Appl. Math., 21(3), pp. 263-289.

- [24] Jacka, S.D., 1991. Optimal stopping and the American put. Math. Finance, 1 (2), pp. 1-14.

- [25] Jacka, S.D., Lynn, J.R., 1992. Finite-horizon optimal stopping, obstacle problems and the shape of the continuation region. Stochastics, 39 (1), pp. 25-42.

- [26] Jeanblanc, M., Yor, M., Chesney, M., 2009. Mathematical methods for financial markets. Springer-Verlag, London.

- [27] Karatzas, I., Shreve, S.E., 1998. Brownian motion and stochastic calculus. Second Edition. New York, Springer.

- [28] Karatzas, I., Shreve, S.E., 1998. Methods of mathematical finance (Vol. 39). New York, Springer.

- [29] Kotlow, D.B., 1973. A free boundary problem connected with the optimal stopping problem for diffusion processes. Trans. Amer. Math. Soc., 184, pp. 457-478.

- [30] Lamberton, D., 2009. Optimal stopping with irregular reward functions. Stoch. Process. Appl., 119 (10), pp. 3253-3284.

- [31] Lamberton, D., Zervos, M., 2013. On the optimal stopping of a one-dimensional diffusion. Electron. J. Probab., 18 (34), pp. 1-49.

- [32] Laurence, P., Salsa, S., 2009. Regularity of the free boundary of an American option on several assets. Comm. Pure Appl. Math., 62 (7), pp. 969-994.

- [33] Lions, P.L., Sznitman, A.S., 1984. Stochastic differential equations with reflecting boundary conditions, Comm. Pure Appl. Math. 37, pp. 511-537.

- [34] McConnell, T.R., 1991. The two-sided Stefan problem with a spatially dependent latent heat. Trans. Amer. Math. Soc., 326 (2), pp. 669-699.

- [35] Palczewski, J., Stettner, Ł., 2011. Stopping of functionals with discontinuity at the boundary of an open set. Stoch. Process. Appl., 121, pp. 2361-2392.

- [36] Pedersen, J.L., 2003. Optimal prediction of the ultimate maximum of Brownian motion. Stochastics and Stoch. Reports, 75 (4), pp.205-219.

- [37] Peskir, G., 2019. Continuity of the optimal stopping boundary for two-dimensional diffusions. Ann. Appl. Probab., 29(1), pp.505-530.

- [38] Peskir, G., Shiryaev, A., 2006. Optimal stopping and free-boundary problems. Birkhäuser Basel.

- [39] Protter, P.E., 2005. Stochastic integration and differential equations. Springer.

- [40] Rogers, L.C.G., Williams, D., 2000. Diffusions, Markov processes and martingales: Volume 2, Itô calculus. Cambridge university press.

- [41] Revuz, D., Yor, M., 1999. Continuous martingales and Brownian motion. 3rd Edition. Springer-Verlag, Berlin, Heidelberg, New York.

- [42] Shiryaev, A.N., 2007. Optimal stopping rules (Vol. 8). Springer Science & Business Media.

- [43] Villeneuve, S., 1999. Exercise regions of American options on several assets. Finance Stoch., 3 (3), pp. 295-322.

- [44] Villeneuve, S., 1999. Options Américaines dans un modèle de Black–Scholes multidimensionnel. Doctoral dissertation, Univ. Marne-la-Vallée.

- [45] Yam, S.C.P., Yung, S.P., Zhou, W., 2014. Game call options revisited. Math. Finance, 24 (1), pp. 173-206.

- [46] Zervos, M., Rodosthenous, N., Lon, P.C., Bernhardt, T., 2019. Discretionary stopping of stochastic differential equations with generalised drift. Electron. J. Probab., 24 (140), pp.1-39.