A New Approach to Estimating Loss-Given-Default Distribution

Abstract.

Based on an idea of using a last passage time, we propose a new method for estimating loss-given-default distribution implied in current credit market and company-specific financial conditions. Since the market standard is the predetermined constant loss rate (60%) for all firms, it is hard to estimate loss-given-default distribution by just observing the market information such as default time distribution, default probability, and CDS spreads. To overcome this difficulty, we construct a hybrid model with the last passage time of the leverage ratio (defined as the ratio of a firm’s assets over its debt) to a certain level. The last passage time, which is not a stopping time, allows us to appropriately model the timing of severe firm-value deterioration which is not apparent to credit market participants. Under minimal and standard assumptions, our model captures asset value dynamics when close to default, while treating default as an unexpected event. We explicitly obtain the distribution of the leverage ratio at default time. As we base the model solely on the leverage ratio and do not introduce additional risk factors, both the model and the procedure for calibrating model parameters to the credit market are simple. We illustrate this procedure in detail by calculating the loss-given-default distribution implied in the credit market.

This version: . The first author is in part supported by Grant-in-Aid for Scientific Research (C) No.18K01683, Japan Society for the Promotion of Science. The second author is in part supported by JSPS KAKENHI Grant-in-Aid for Early-Career Scientists No. 21K13324.

Keywords: Loss given default; Asset process; Leverage ratio; Intensity; Last passage time; CDS spread

Mathematics Subject Classification (2010): 60J70

JEL classification: G32, C63

1. Introduction

There exists a large body of literature regarding the loss-given-default distribution because the information about this distribution is important for credit risk management. One example of its use is the estimation of loan-loss reserves in the banking industry. The loss-given-default distribution should reflect credit market conditions as well as company-specific financial conditions. However, as Doshi et al. (2018) and many other studies point out, it is a standard practice to assume, irrespective of company names, a constant recovery rate (approximately 40%) of the debt upon default. This loss rate is arbitrarily determined, possibly from the empirical distribution. In contrast to this standard assumption, the empirical literature has documented the evidence of time-varying realized loss rates. Hence we cannot overemphasize the effectiveness of a model that provides the loss-given-default distribution implied in the credit market and company-specific financial conditions.

With minimal and standard assumptions, the model to be presented in this paper allows us to obtain the loss-given-default distribution implied in the current CDS market. This model captures the dynamics of the asset value when close to default, while the default is treated as an unexpected event. The model can well describe default events observed in the real world with these features. In general, CDS spreads are determined by the three elements: default probability, default time, and loss given default. The predetermined 60% loss rate (i.e., 40% recovery rate) is usually assumed in CDS spread quoting. We develop a new method that provides a loss-given-default distribution consistent with the default probability and default time behind the quoted CDS spread. The market data we use are from Thomson Reuters, including default probability estimates.

We derive the distribution of the ratio of the firm’s total assets over its total debt upon default. We shall hereafter refer to this ratio as the leverage ratio and to the dynamics of this ratio as the leverage process. The value of the leverage ratio at default is the corporate-level recovery rate of the debt, and accordingly, the loss given default is obtained as (-recovery rate). In our framework, we are focusing on the loss rate of the debt of the whole company, not each individual debt obligation. Based on this corporate-level loss distribution, credit managers can calculate loss rates for individual debt obligations having distinct characteristics; for example, senior or subordinated, and with or without collateral.

While the firm-value approach proposed in Merton (1974) has been successful in estimating the default probability, one has some difficulties in calculating the loss given default under this method. For example, if the firm’s default is defined as the first passage time of the leverage process to a certain point, say , then the value of the leverage ratio upon default is necessarily equal to . It follows that the loss given default would be deterministic and would not depend on the credit market and company-specific financial conditions. To overcome this difficulty, we consider the last passage time of the leverage process to another threshold level . Let us denote this time by . In reality, the default may not occur when the leverage process hits some sufficiently low level for the first time if the debt payments are not due at that time. In fact, the firm may recover after the leverage process hits level . In contrast to this, the last passage time incorporates the fact that the firm will not be able to recover to its normal financial condition after . This makes highly relevant when modeling default time and consequently, loss given default.

To model the loss-given-default distribution, we explicitly incorporate the fact that after the last passage time , the business environment surrounding the company severely alters and the firm is not able to recover to normal operations. As is well known, the last passage time is not a stopping time and this is the reason why is appropriate for modeling the loss-given-default distribution: market observers (such as regular shareholders) do not know whether has occurred or not and do not see when this switch in the dynamics of the asset value takes place. The information about the time may be known only to the company insiders. Therefore, the last passage time is relevant in the sense that it accounts for the reality that market observers are facing.

After the firm’s leverage process passes the level for the last time, it is appropriate to switch the model parameters so that they reflect deteriorated business conditions of the company. Accordingly, we shall work, after time , with a transition semigroup (of the diffusion) that incorporates the fact that the leverage ratio would not return to the level . At this stage, we use the intensity-based approach to identify the default time which plays a major role in our model for the loss-given-default distribution. By suitably choosing an intensity process, we explicitly derive the distribution of the leverage ratio at the time of default. In identifying the default time, the use of the intensity-based model after time is appropriate because the market observers do not thereafter know the true state of the firm and would regard default as an unexpected shock. Finally, to be consistent with the credit market, we estimate the model parameters in a way that the model-implied default probability is consistent with the default probability (provided by Thomson Reuters) behind the quoted CDS spread.

In summary, we obtain the distribution of the leverage ratio of the firm at default time. The assumptions of our model are minimal and standard: we do not use jumps or additional risk factors. The key element is the last passage time which we cannot observe and after which the default is represented as an unexpected shock as in the intensity-based approach.

1.1. Literature Review

We have already mentioned that it is a standard practice to assume a constant loss rate of 60% for debt upon default. As the empirical literature has documented the evidence of time-varying realized loss rates, it is important to build a stochastic model for the loss given default.

Gambetti et al. (2019) analyzes determinants of recovery rate distributions and finds economic uncertainty to be the most important systematic determinant of the mean and dispersion of the recovery rate distribution. For their analysis, the authors use post-default bond prices of 1831 American corporate defaults during 1990-2013. Even though recovery rates vary with a firm’s idiosyncratic factors, Gambetti et al. (2019) states that the impact of systematic factors related to economic cycles should not be underestimated. For the summary of studies related to cross-sectional and time variation of recovery rates, we refer the reader to Gambetti et al. (2019).

Altman et al. (2004) provides a detailed review of how recovery rate and its correlation with default probability had been treated in credit risk models. The authors also discuss the importance of modeling the correlation between recovery rate and default probability. Altman et al. (2005) analyzes and measures the relationship between default and recovery rates of corporate bonds over the period of 1982-2002. They confirm that default rate is a strong indicator of average recovery rate among corporate bonds. Acharya et al. (2007) analyzes data of defaulted firms in the U.S. during 1982-1999 and finds that the recovery rate is significantly lower when the industry of the defaulted firm is in distress. The authors discover that industry conditions at the time of default are robust and important determinants of recovery rates. Their results suggest that recovery rates are lower during industry distress not only because of the decreased worth of a firm’s assets but also because of the financial constraints that other firms in the industry face. The latter reason is based on the idea that the prices, at which the assets of the defaulted firm can be sold, depend on the financial condition of other firms in the industry.

Doshi et al. (2018) uses information extracted from senior and subordinate credit default swaps to identify risk-neutral stochastic recovery rate dynamics of credit spreads and studies the term structure of expected recovery. Their study is related to Schläfer and Uhrig-Homburg (2014) which also uses the fact that debt instruments of different seniority face the same default risk but have different recovery rates given default. Doshi et al. (2018) uses 5-factor intensity-based model for CDS contracts allowing stochastic dynamics of the loss given default. The authors allow firm-specific factors to influence the stochastic recovery rate. Their empirical analysis of 46 firms through the time period of 2001-2012 shows that the recovery rate is time-varying and the term structure of expected recovery is on average downward-sloping. They also find that industry characteristics have significant impact on CDS-implied recovery rates; however, they do not find the evidence that firms’ credit ratings explain the cross-sectional differences in recovery rates. For the summary of the literature related to the relationship between default rates and realized recovery rates, refer to Doshi et al. (2018).

Yamashita and Yoshiba (2013) is an example of a study that uses stochastic collateral value process to incorporate stochastic recovery rate into the model which assumes that a constant portion of the collateral value is recovered upon default. Yamashita and Yoshiba (2013) uses a quadratic Gaussian process for the default intensity and discount interest rate and derives an analytical solution for the expected loss and higher moments of the discounted loss distribution for a collateralized loan. The authors assume that the default intensity, discount interest rate, and collateral value are correlated through Brownian motions driving Gaussian state variables.

Finally, Cohen and Costanzino (2017) is an example of a study that extends a structural credit risk model and incorporates stochastic dynamics of the recovery rate. In contrast to our approach which does not introduce an additional recovery risk factor and is based solely on the dynamics of the leverage process, Cohen and Costanzino (2017) models asset and recovery processes separately as correlated geometric Brownian motions. In their model, the asset risk driver serves as a default trigger and the recovery risk driver determines the amount recovered upon default. The authors explicitly compute the prices of bonds and CDS under this framework. See also Kijima et al. (2009).

The rest of the paper is organized as follows. Sections 2.1, 2.2, and 2.3 develop the models for asset process and default time. Section 2.4 derives the distribution of the loss given default and points out the difference between our approach and the conventional firm-value approach. Section 3 demonstrates the implementation of our model when the asset process follows geometric Brownian motion with alternating drift and volatility parameters. Section 3.3 gives a detailed description of the estimation procedure for deriving the loss-given-default distribution implied in the credit market. Section 4 illustrates and discusses the estimation result for Ford Motor Company as an example. For our analysis, the risk-free rate was obtained from the website of the U.S. Department of the Treasury. The remaining data used for the estimation was obtained from Thomson Reuters Eikon.

2. Model

Given the fixed probability space , let and denote filtrations satisfying the usual conditions where is a sub-filtration of (). All random variables are defined on . We assume this space is large enough to accommodate an exponential random variable with rate , independent of the filtration . Let denote the constant interest rate. As the size of the firm’s debt relative to its assets determines the firm’s default, we focus on the ratio of the asset value over debt in the sequel.

2.1. Process

Let the amount of debt be given by a positive deterministic process satisfying and with constant growth rate . We define the leverage process as where the nonnegative regular diffusion (with random switching) represents the asset process. We assume that the dynamics of is given by

| (2.1) |

where is a standard Brownian motion with respect to the filtration . The process is defined as

| (2.2) |

where denotes an indicator function for some set . Both processes and are measurable with respect to and continuous. Let us set the nonrandom initial value of the leverage process as . The level represents distress level and is to be determined later using market data. The modeling in (2.1) allows us to incorporate the fact that the firm’s business operations are altered when it is under financial distress.

We impose standard assumptions to ensure the existence of a strong solution to the stochastic differential equation with infinitesimal parameters and for each . Specifically, following Theorem 5.2.9 in Karatzas and Shreve (1998), we assume that global Lipschitz and linear growth conditions hold with some positive constant :

Note that these conditions also guarantee uniqueness of the corresponding strong solutions.

As we are interested in modeling the loss-given-default distribution, we assume that for the leverage process , the left-boundary is attracting and the right boundary is non-attracting. In this case, for (see Proposition 5.22 in Karatzas and Shreve (1998)) and the default occurs eventually with probability one.

2.2. Last Passage Time

The default time under the conventional firm-value approach to credit risk analysis (including Merton-type models) is given by

| (2.3) |

This implies that the value of debt , used as the barrier, would be repaid in full; that is, . However, in reality, this equality does not hold: may not represent the right leverage ratio at default. This in turn means that the mechanism based on the time may not be the right mechanism to estimate the loss given default. Accordingly, while we shall still in part rely on the firm-value model, we introduce the last passage time for our modeling purpose.

We define the last passage time of level by

| (2.4) |

with the convention that the supremum of the empty set is zero. To ensure that , we assume that . For modeling the loss-given-default distribution, we should explicitly incorporate the fact that after the last passage time , the business condition for the company is severely altered. Lost business opportunities, shrinking market share, and worsening trade terms would not allow the firm to recover to the normal situation. Therefore, we need another time clock that starts ticking at time . For our purposes, it is convenient to work with a new positive diffusion process that starts at point and does not recover to level before converging to the left boundary . To formally introduce the process , we derive the dynamics of the leverage process after time .

The technical tool that fits our objective is given in Meyer et al. (1972). The semigroup of the process after time is obtained by conditioning the process not to hit before converging to the left boundary. We illustrate this point. Let . Following Meyer et al. (1972), for any positive random variable measurable with respect to , we define

| (2.5) |

For the co-terminal (and co-optional) random variable , the family is a right-continuous filtration. According to Theorem 5.1 in Meyer et al. (1972), is a strong Markov process with respect to the filtration . For any , its transition semigroup is given by

| (2.6) |

Hence is a transition semigroup of the process conditioned not to hit before lifetime. In particular, this transition semigroup incorporates the fact that the diffusion never reaches level .

Let be a regular diffusion process on with the transition semigroup in (2.6). Using the semigroup (2.6), we compute drift and diffusion parameter of the process for in view of (2.1) and (2.2). We obtain

| (2.7) | ||||

where and are drift and diffusion parameters of when (see (2.1) and (2.2)) and denotes the scale function of a diffusion process with drift and diffusion parameter . Note that is an entrance boundary for the process .

Given the fact that the conventional firm-value approach does not provide appropriate information about the loss-given-default distribution, it is natural to consider another mechanism that determines the loss distribution upon default. We illustrate this mechanism in the next subsection. Our approach reflects the fact that the company’s business conditions radically change after its asset value (i.e., the present value of its future cash flow prospects) goes below a certain level. This time of drastic change in our model is captured by in (2.4) after which we consider the process . Note that the parameters of the process may not be easily estimated from the company’s stock prices since the deteriorated business conditions of the company may not be sufficiently reflected in the stock market.

Remark 1.

Note that, in our setup, the leverage process may drop to level before time . In reality, the asset process is unobservable and the leverage process may hit level multiple times before default. We provide two specific reasons why this is justified when modeling the loss-given-default distribution. First, as we have indicated in the introduction, the firm value may deteriorate to a low level and then recover before the debt payments are due. Another reason is as follows. The firm-value approach is based on the asset process which is estimated according to the option-theoretic approach using stock price data. Therefore, stock price fluctuations affect the asset value, and large stock market turmoil may cause it to drop to such a low level that the leverage process hits and hence in (2.3) would occur; however, this does not indicate a default in a practical and real sense. In contrast, the time is important because it incorporates the fact that the leverage process will never recover to level .

2.3. Default time and time

Here we define a random time that is suitable for estimating the loss-given-default distribution. For the modeling, we need an exponential random variable with rate , independent of the filtration . We let be a nonnegative piecewise continuous function and define the moment inverse of integral functional by

| (2.8) |

Here denotes the nonrandom initial value of the process . Following Bielecki and Rutkowski (2002, Sec.8.2), we assume that satisfies

| (2.9) |

We define time and model the default time as

| (2.10) |

where denotes the shift operator. It follows from (2.8) that and from (2.9) that . We also see that for every . Moreover, we have with (2.10). In our model, the time is treated as a special time in the sense that the firm goes into a different economic state. This is captured in (2.10) where the new clock starts ticking at time . We have constructed the time using the process which never returns to , this feature being represented in the transition semigroup (2.6). Below we explain the implication behind our modeling of the default time .

Recall that is a right-continuous filtration (see (2.5)). We set for and define . Recall that and have the same transition semigroup by assumption. It follows that in (2.8) has the same distribution as . Then, we have

and we see that the right-most element represents the -hazard process of under given . Note that the construction of the random time is similar to the canonical construction of the default time in the intensity-based approach (see Proposition 5.26 in Capiński and Zastawniak (2017)).

2.4. Loss-given-default distribution

For notational simplicity, we set in the sequel. Hence when we write , the initial value of is assumed to be an arbitrary . Recall the definition of the default time in (2.10). Let us define the loss given default as

| (2.11) |

With being an entrance boundary for , we obtain

| (2.12) |

Thus, we are able to find the loss-given-default distribution by focusing on only. This simplifies the analysis as we do not need to consider the shift operator in the definition (2.10).

Fix any and . According to (2.7), (2.8), (2.10) and Theorem IV.5.1 in Borodin (2017),

is the unique continuous solution to the problem

Here denotes the conditional expectation . We will provide an explicit form of later in Proposition 1. Using the solution to this ordinary differential equation, we obtain by the continuity of . Finally, produces the distribution of via (2.12). The Laplace transform of is given by .

In summary, we have the following standard assumptions:

-

(1)

the state space of the leverage process is where the left boundary is attracting and the right boundary is non-attracting,

-

(2)

, and

-

(3)

a technical condition (2.9) for the intensity process .

Our setup is summarized in Table 1.

| Default time | Distribution of the final value | |

|---|---|---|

| Conventional | ||

| Our approach |

3. Implementation

Let us assume that the firm value (market value of total assets) follows a geometric Brownian motion with random switching on . Let us set the drift and diffusion parameters in (2.1)

as

| (3.1) |

with and . Recall that the debt process is given by

where denotes a constant rate. The parameters , , and are such that the left boundary is attracting and the right boundary is non-attracting for the leverage process. In particular, we assume that and . This ensures that the default occurs eventually with probability one.

For convenience, we focus on the process given by . We reset our previous definitions in regards to this process. By fixing a certain level of , we reset the definition (2.4) as

On the set , and hence

| (3.2) |

We have the normalized process

by setting

| (3.3) |

Using (2.6) and (2.7), we see that the process with follows the dynamics

| (3.4) |

Note that since , when the process approaches from below, the drift approaches negative infinity so that the process shall never reach the point from the region . Mathematically, is an entrance boundary for and financially, the firm’s leverage ratio shall never recover to the threshold level .

3.1. Hazard rate and time

Here we construct the default time as defined in (2.10). Select a certain level . Observe that

| (3.5) |

To obtain a concrete result, we specify the function in (2.8) as

| (3.6) |

so that the integral in (2.8) (see the expression of in (3.7) below) represents the occupation time of the process under the level . We provide three reasons for using the setup (3.6). First, when assessing credit risk, it is natural to consider the time spent in a ‘danger zone’ by the leverage process after the last passage time . Second, our formulation in (3.6) makes the model mathematically tractable. Third, the occupation time of a region is widely used in credit-risk-related literature. For example, the bankruptcy rate function in Albrecher et al. (2011) is similar to (3.6). The innovative part of our usage is that we consider occupation time of a region after the last passage time . In this way, we look at the occupation time of a ‘danger zone’ after the firm’s credit conditions have deteriorated and it is not able to recover to its normal state anymore.

The definition of in (3.6) is equivalent to the definition with . With this definition, we obtain for

| (3.7) |

by (2.8) and the definition . Then, . Hence we identify the firm’s default once the leverage process (in its logarithmic form) spends a certain random time below level after time . This setup is quite reasonable since, as in other intensity-based models, the market observers are unaware of the firm’s state after a certain time (represented by in our model) and accept default as a sudden shock.

3.2. Laplace transform of and distribution of

We will use the following proposition to obtain the loss-given-default distribution and the Laplace transform of time .

Proposition 1.

Fix and . Let and . For , it holds that

| (3.8) |

Proof.

From (3.4) let us write where is an arbitrary constant initial value (see (3.3)). Note that is equivalent to and for , we have

| (3.9) |

where is a standard Brownian motion. By definition, when . As in Section 2.4, let us set for brevity where indicates the initial value of the process . Using the process in (3.9), we obtain

Thus, we focus on the process with arbitrary constant . We define

| (3.10) |

for . Then, by Theorem IV.5.1 in Borodin (2017), is the unique continuous solution to the o.d.e.

| (3.11) |

For notational simplicity, we assume in (3.11) and write instead of below. Note that is equivalent to .

(i) Consider the case when . Then, (3.11) is reduced to

According to Section IV.16.7 and Appendix 2.12 in Borodin (2017), its fundamental solutions are given by

| (3.12) |

Here is an increasing solution and it satisfies and because . On the other hand, is a decreasing solution and it satisfies and . Therefore, for , we have with constant . We have eliminated the first fundamental solution because the right-hand-side in (3.10) is bounded when .

(ii) Let . In this case, (3.11) is reduced to

As in the case (i) above, its fundamental solutions are given by and in (3.12). Thus, we have with constants and for .

(iii) Consider the case when . Then, (3.11) is reduced to

Its fundamental solutions are given by

The limiting behavior of and is the same as that of and , respectively. Therefore, in this case we have with constant . We have eliminated the second fundamental solution because the right-hand-side in (3.10) is bounded when .

Finally, from the continuity of and at and , we obtain

Finally, and this proves the proposition. ∎

Corollary 1.

Proof.

We have by the definitions of and . By taking the limit in (3.8), we obtain the desired result. ∎

Corollary 2.

The distribution of is given by

where .

Proof.

Corollary 3.

For and , set . For , the density satisfies

| (3.14) |

3.3. Estimation procedure

Fix any point in time as the current time. The model in this paper lets us estimate the loss-given-default distribution implied in the credit market and company-specific financial conditions which usually vary from day to day. The procedure outlined below estimates the loss-given-default distribution using the information available up to the current time. The parameters are estimated in a way that the default probability and default time distribution obtained from the model are consistent with the default probability provided by Thomson Reuters.

-

Step 1:

We set to some reasonable number and implement the procedure in the subsequent steps. When all the steps are carried out, we go back to Step 1, set a different value of , and do the estimation once again. For each level of , the parameters are estimated by making sure that the model-implied default probability is consistent with the default probability provided by Thomson Reuters. In the end, we choose the value of which provides the estimate of the model-implied default probability closest to the default probability from Thomson Reuters. For the steps below, is fixed.

-

Step 2:

We estimate the parameters of the asset process in (3.1) using the data of the firm’s equity and debt available up to the current time. The debt process represents a certain amount of debt to be repaid and we let it be the sum of short-term debt and a half of long-term debt (as in Moody’s KMV approach) since empirical evidence has demonstrated that such level is an appropriate default threshold for the firm’s assets.

We use the option-theoretic approach of Merton (1974) where the value of equity represents the value of the European call option written on the firm’s assets with the strike price equal to the future value of debt. We estimate the asset parameters using the maximum likelihood method of Duan (1994), Duan (2000), and Lehar (2005) with the constraints and . These conditions ensure that the default occurs eventually with probability one. We use 5-year U.S. Treasury yield at current time as the constant rate . We also impose a natural constraint in (3.1) because the firm’s financial state worsens when its leverage ratio is below .

For computational simplicity, we assume that so that only the drift parameter changes. This enables us to use the expression of the European call option price without random switching given in Lehar (2005) since Girsanov’s transformation removes the drift and only the diffusion coefficient is relevant. Assuming that debt is exogenous, the log-likelihood function to be maximized is given bywhere is a standard normal cumulative distribution function and is the time interval between two consecutive data points. We are using number of past data points for the estimation. In the above equation, is the solution to

(3.15) with respect to and where

As in Lehar (2005), we set the maturity of the call option to 1 year.

-

Step 3:

The goal of this step is to estimate the threshold in (3.6) in a way that the 5-year default probability obtained from the model is consistent with the 5-year default probability provided by Thomson Reuters. For this purpose, we need estimates of default time :

(i) We use the estimated parameters obtained in Step 2 and simulate sample paths of the leverage process. We retrieve the starting point of the asset path from the Black-Scholes equation (3.15) in Step 2 using the estimated diffusion parameter together with the current equity and debt values. The paths should be sufficiently long (e.g., 50 years for safety) to obtain the estimates . If the simulated leverage path never reaches , we set for that path.

(ii) We fix and sample the pair (which is also used in Step 5) using Corollaries 2 and 3. Specifically, we first sample from Corollary 2 in view of (2.12). Set this sampled value to, say, . We then sample using the joint density function in Corollary 3, which we retrieve from the Laplace transform (3.14). We use Zakian’s method of inversion as in Halsted and Brown (1972). The explicit form in Corollary 3 helps to reduce the variance caused in this step. We numerically integrate the density for the cumulative distribution function, from which we can obtain samples of by the inverse transform method.

(iii) From (i) and (ii), in view of (2.10), we obtain for each simulation path. We then calculate the proportion of the paths for which , obtaining the 5-year default probability. A higher value of provides a higher default probability. By changing iteratively, we find an appropriate value of that results in the 5-year default probability matching the one from Thomson Reuters. -

Step 4:

Using the estimated value of obtained in Step 3, we derive the loss-given-default distribution.

(i) We obtain the distribution of from Corollary 2 via (2.11).

(ii) However, in Step 2, we used the sum of short-term and a half of long-term debt as debt to estimate model parameters. Here we are interested in the loss-given-default distribution of the total debt which we shall denote by . Therefore, we make a transition as follows: Letting the processes and represent short- and long-term debts respectively, we have . For simplicity, we assume that the proportion of long-term debt remains constant. The loss rate of total debt , denoted by , is then given by(3.16) We set to the average value of the ratio of long-term debt to total debt which we calculate using number of the same past data points as in Step 2. Note that due to . On the other hand, the lower bound for is given by . The estimate of in Step 3 is reasonable if this lower bound is nonnegative. Otherwise, we need to go back to Step 1 and set a different value of .

-

Step 5:

Finally, we calculate the 5-year CDS spread based on our model and compare it to the quoted spread. Recall that the underlying credit risk behind CDS spread refers to the risk of the whole company, not a particular debt obligation, and that the market spread is calculated with the assumption of loss rate. In contrast, the value of the CDS spread we shall obtain from our model depends on the loss-given-default distribution. We set the principal amount to and assume the spread payments are made quarterly. We find the value of the spread for which the present value of spread payments (premium leg) and the present value of the payment in case of default (default leg) are equal.

(i) For each simulation path in Step 3, we have obtained . Now, by using the constant rate as the discount factor, we calculate the present value of spread payments until or maturity, whichever is earlier. By taking average for all simulated paths, we obtain the premium leg.

(ii) Next, we compute the default leg. We have the sampled pairs from Step 3. Using the values of , we obtain the sampled values of from (3.16) in view of and (2.11). We also have samples of from Step 3. Thus, we obtain the pair for each trial. From these sampled pairs, we can compute the present value of the recovery (on the dollar) upon default. Specifically, we calculate the value of . By taking the average for all trials, we find the value of default leg.

(iii) We match the premium leg to the default leg to obtain the model-implied CDS spread.

4. Example of Ford Motor Company

In this section, we consider an example of Ford Motor Company, hereafter denoted shortly as Ford. We estimate the loss-given-default distribution using the procedure in Section 3.3. When conducting simulation, we simulate 10,000 paths. The main purpose of presenting this example is to illustrate how to implement our method to obtain the loss-given-default distribution implied in the current credit market and company-specific financial conditions. Specifically, we estimate the model parameters in a way that the model-implied default probability (which is based on default time distribution) is consistent with the default probability provided by Thomson Reuters. Based on those parameters, we obtain the loss-given-default distribution.

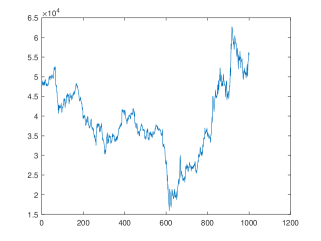

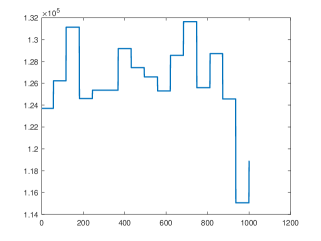

We choose October 1, 2021 as the current time and use the information available up to this time to obtain the loss-given-default distribution implied on that day. Specifically, we use the past 1000 daily data together with the current values from the period 2017/10/11 2021/10/01 for the estimation, corresponding roughly to 4 years. We use the 5-year U.S. Treasury yield curve rate (of October 1, 2021) as the constant rate . The quoted 5-year CDS spread for Ford is bps which is calculated based on loss rate. The values of the equity and debt during 2017/10/11 2021/10/01 are displayed in Figure 1. We use these data to estimate the parameters as described in Step 2 in Section 3.3. We interpolated daily debt values using standardized quarterly balance sheets. We defined the debt as the sum of the short-term debt (notes payables, short-term debt, current portion of long-term debt and capital leases) and one half of the long-term debt (long-term debt and capital leases).

Table 2 reports the estimated parameters which provide the 5-year default probability consistent with the 5-year default probability provided by Thomson Reuters, . The estimation results revealed that all the implied values of the leverage ratio are lower than the estimated value of during the estimation period. Therefore, we set and estimated only one drift parameter.

| 1.8 | ||

| 0.0102 | (0.0057) | |

| 0.1182 | (0.0030) | |

| 1.32 | ||

| 5Y DP | 0.1614 | (0.0037) |

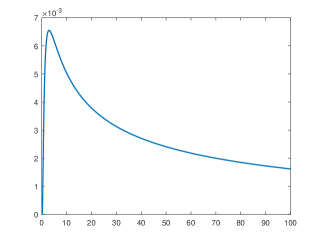

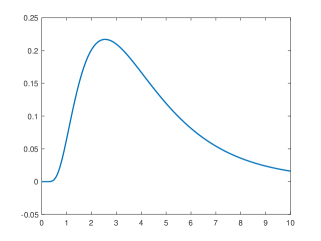

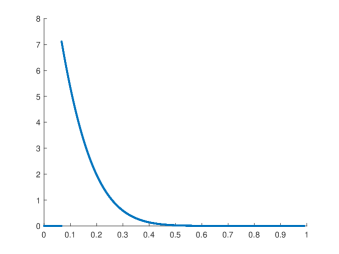

As in this example, we can use the explicit density of the last passage time obtained from Proposition 4 in Salminen (1984) and Proposition 3.1 in Egami and Kevkhishvili (2020). We numerically integrate this density to estimate the cumulative distribution function and simulate by the inverse transform method. The retrieved current value of the leverage ratio is . This means that the leverage ratio may not hit level before default. In fact, we have . The density functions of time and based on the estimated parameters are displayed in Figure 2\alphalph. We used Corollary 1 to obtain the density of using Zakian’s method of inversion as in Halsted and Brown (1972). The average value of the ratio of long-term debt to total debt is . Figure 3 displays the density function of the loss given default in (3.16) based on the estimated parameters. This density was obtained using Corollary 2 as described in Step 4 of Section 3.3.

The model-implied 5-year CDS spread is , while the market quoted spread is bps. One may think that this large discrepancy is detrimental to the evaluation of our model; however, this is not the case because the only reason for this discrepancy is the difference in the loss-given-default distribution. The market spread is based on the arbitrarily fixed loss rate which is a relatively high value if we look at the density in Figure 3. In the calibration, we used the information available both in the stock and credit markets. As a result, the estimated loss given default is distributed mainly in the range lower than 60% as we see in Figure 3. Having said that, we check the consistency between the model-implied CDS spread and the market spread by comparing standardized values as described below.

We estimate , the average loss given default, by simulation as a byproduct of Step 5 in Section 3.3. Then, we compare the ratios of the CDS spread to the average loss given default between the market quotes and our estimates. The ratio can be considered as the spread per 1% loss given default, which we denote by . See Table 3 for the results. In our case, , while the counterpart of the market quote is . We see that is within range from the market estimate . Therefore, our method is consistent to the market information.

Furthermore, to check the robustness of our results with respect to the ratio of long-term debt to total debt (denoted by ), we report the results for four additional values of together with (obtained in Step 4 of Section 3.3) in Table 3. We see that all of our estimates of are within range from the market estimate of . We also notice that these ’s themselves are stable with respect to . We conclude that the default time and loss-given-default distribution in our framework are consistent with the credit market and company-specific financial conditions.

| w | 0.57 | 0.58 | 0.5858 | 0.59 | 0.6 |

|---|---|---|---|---|---|

| CDS Spread | 45.2091 | 47.3975 | 48.6711 | 49.5858 | 51.7742 |

| Average LGD | 0.1265 | 0.1327 | 0.1362 | 0.1388 | 0.1449 |

| CDS Spread/Average LGD | 357.2617 | 357.3083 | 357.3335 | 357.3508 | 357.3897 |

While it is a standard practice to assume 60% loss given default, a mere usage of the market CDS spreads misguides the true risk level of the company. The arbitrarily fixed loss rate of 60% (used in the quoted CDS spread) may distort appropriate formation of credit spread. In fact, loss rates should differ from company to company. One could use the loss-given-default distribution from our model (see (3.16) and Figure 3) for the purpose of credit risk management. One example of practical applications is the estimation of loan-loss reserves in the banking industry which should reflect both the credit market conditions and company-specific financial conditions. In the end, we emphasize that one should not confuse the loss right upon the default, with the final loss after liquidation and/or bankruptcy procedure.

References

- Acharya et al. (2007) Acharya, V.V., Bharath, S.T., Srinivasan, A., 2007. Does industry-wide distress affect defaulted firms? Evidence from creditor recoveries. Journal of Financial Economics 85, 787–821.

- Albrecher et al. (2011) Albrecher, H., Gerber, H.U., Shiu, E.S.W., 2011. The optimal dividend barrier in the Gamma–Omega model. European Actuarial Journal 1, 43–55.

- Altman et al. (2004) Altman, E., Resti, A., Sironi, A., 2004. Default recovery rates in credit risk modelling: A review of the literature and empirical evidence. Economic Notes 33, 183–208.

- Altman et al. (2005) Altman, E.I., Brady, B., Resti, A., Sironi, A., 2005. The link between default and recovery rates: Theory, empirical evidence, and implications. The Journal of Business 78, 2203–2228.

- Bielecki and Rutkowski (2002) Bielecki, T.R., Rutkowski, M., 2002. Credit Risk: Modeling, Valuation and Hedging. Springer Verlag, Berlin.

- Borodin (2017) Borodin, A.N., 2017. Stochastic Processes. Birkhäuser.

- Capiński and Zastawniak (2017) Capiński, M., Zastawniak, T., 2017. Credit Risk. Cambridge University Press.

- Cohen and Costanzino (2017) Cohen, A., Costanzino, N., 2017. Bond and CDS pricing via the stochastic recovery Black-Cox model. Risks 5, 26.

- Doshi et al. (2018) Doshi, H., Elkamhi, R., Ornthanalai, C., 2018. The term structure of expected recovery rates. Journal of Financial and Quantitative Analysis 53, 2619–2661.

- Duan (1994) Duan, J., 1994. Maximum likelihood estimation using price data of the derivative contract. Mathematical Finance 4, 155–167.

- Duan (2000) Duan, J., 2000. Correction: Maximum likelihood estimation using price data of the derivative contract. Mathematical Finance 10, 461–462.

- Egami and Kevkhishvili (2020) Egami, M., Kevkhishvili, R., 2020. Time reversal and last passage time of diffusions with applications to credit risk management. Finance and Stochastics 24, 795–825.

- Gambetti et al. (2019) Gambetti, P., Gauthier, G., Vrins, F., 2019. Recovery rates: Uncertainty certainly matters. Journal of Banking and Finance 106, 371–383.

- Halsted and Brown (1972) Halsted, D.J., Brown, D.E., 1972. Zakian’s technique for inverting Laplace transforms. The Chemical Engineering Journal 3, 312–313.

- Karatzas and Shreve (1998) Karatzas, I., Shreve, S.E., 1998. Brownian Motion and Stochastic Calculus. 2nd ed., Springer ScienceBusiness Media, New York.

- Kijima et al. (2009) Kijima, M., Suzuki, T., Tanaka, K., 2009. A latent process model for the pricing of corporate securities. Mathematical Methods of Operations Research 69, 439–455.

- Lehar (2005) Lehar, A., 2005. Measuring systemic risk: A risk management approach. Journal of Banking and Finance 29, 2577–2603.

- Merton (1974) Merton, R.C., 1974. On the pricing of corporate debt: The risk structure of interest rates. The Journal of Finance 29, 449–470.

- Meyer et al. (1972) Meyer, P.A., Smythe, R.T., Walsh, J.B., 1972. Birth and death of Markov processes, in: Proceedings of the Sixth Berkeley Symposium on Mathematical Statistics and Probability, Volume 3: Probability Theory, University of California Press. pp. 295–305.

- Salminen (1984) Salminen, P., 1984. One-dimensional diffusions and their exit spaces. Math. Scand. 54, 209–220.

- Schläfer and Uhrig-Homburg (2014) Schläfer, T., Uhrig-Homburg, M., 2014. Is recovery risk priced? Journal of Banking and Finance 40, 257–270.

- Yamashita and Yoshiba (2013) Yamashita, S., Yoshiba, T., 2013. A collateralized loan’s loss under a quadratic Gaussian default intensity process. Quantitative Finance 13, 1935–1946.