Preference robust optimization with quasi-concave choice functions for multi-attribute prospects

Abstract

Preference robust choice models concern decision-making problems where the decision maker’s (DM) utility/risk preferences are ambiguous and the evaluation is based on the worst-case utility function/risk measure from a set of plausible utility functions/risk measures. The current preference robust choice models are mostly built upon von Neumann-Morgenstern expected utility theory, the theory of convex risk measures, or Yaari’s dual theory of choice, all of which assume the DM’s preferences satisfy some specified axioms. In this paper, we extend the preference robust approach to a broader class of choice functions which satisfy monotonicity and quasi-concavity in the space of multi-attribute random prospects. While our new model is non-parametric and significantly extends the coverage of decision-making problems, it also brings new computational challenges due to the non-convexity of the optimization formulations, which arises from the non-concavity of the class of quasi-concave choice functions. To tackle these challenges, we develop a sorting-based algorithm that efficiently evaluates the robust choice function (RCF) by solving a sequence of linear programming problems. Then, we show how to solve preference robust optimization (PRO) problems by solving a sequence of convex optimization problems. We test our robust choice model and computational scheme on a single-attribute portfolio optimization problem and a multi-attribute capital allocation problem.

Key words: preference robust optimization, quasi-concave choice functions, multi-attribute choice models

1 Introduction

Much of the focus of the literature on decision-making under uncertainty has been on exogenous uncertainties such as market returns, customer demand, traffic flow, and weather conditions. In some problems, there is also substantial endogenous uncertainty about the decision maker’s (DM’s) own preferences that we refer to as preference ambiguity. Such ambiguity may arise due to the DM’s inability to precisely articulate its own preferences, a lack of accurate models for human behavior, or scarce observations of the DM’s past choices. In behavioural economics, the DM’s preferences are characterized by a choice function where one random prospect is preferred to another if and only if the choice function value of the former is larger than that of the latter. Expected utility (Von Neumann and Morgenstern, 1945) (VNM), convex risk measures (Artzner et al., 1999), and Yaari’s dual theory of choice (Yaari, 1987) are all well known specific families of choice functions. The properties of the choice function match the structure of the DM’s preferences, and different families of choice functions correspond to different types of DMs. When information on the DM’s preferences is incomplete, the choice function used to characterize these preferences is ambiguous.

In this case we cannot provide an optimization problem for the DM that best reflects their preferences. Since the optimal decision is highly sensitive to the DM’s preferences, we are at risk of misspecifying the description of the DM’s preferences and arriving at a greatly sub-optimal solution. The preference robust optimization (PRO) paradigm is first developed in (Armbruster and Delage, 2015) to deal with this situation. In PRO, we use available partial information on the DM to construct an ambiguity set of possible choice functions. This information can include structural assumptions (e.g., monotonicity or concavity) and other auxiliary information about the DM (e.g., preference elicitation information from pairwise comparisons). Then, to mitigate the preference ambiguity, the optimal decision is based on the worst-case choice function from this ambiguity set.

Several PRO models have been considered for various types of DMs (corresponding to different families of choice functions). Armbruster and Delage (2015) and the follow-up utility-based PRO models (e.g., Delage et al. (2017)) presume the DM’s preferences are characterized by VNM-type expected utility. Alternatively, the PRO models in Delage and Li (2017), Li (2021) are based on DMs whose preferences are characterized by convex risk measures. The PRO models in Guo and Xu (2021), Wang and Xu (2020) are designed for DMs whose preferences are characterized by Yaari’s dual theory of choice.

In this paper, we build a new PRO model to support a wider range of DMs and their preferences. First, our new PRO model emphasizes quasi-concave choice functions to incorporate diversification-favoring preferences in the broadest possible way (while previous PRO models emphasize concavity/convexity to reflect diversification-favoring preferences). Second, our new PRO model naturally supports multi-attribute prospects (while previous PRO models largely emphasize the single-attribute case). Despite its greater generality, our model can still be applied efficiently to large-scale problems.

1.1 Motivating examples

We motivate our present work by discussing two multi-attribute decision-making problems. We also elaborate on the kinds of partial information we can elicit from the DM, even when their exact preferences are ambiguous.

Example 1.1 (Investment).

Consider a company which plans to invest in Europe. The company evaluates an investment based on three (possibly random) factors: market environment (), profitability (), and market share (). The company’s overall evaluation of an investment may be described by a choice function on random vectors , where is the company’s evaluation of a particular investment.

The company’s choice function captures the effects of each factor as well as their interacting effects on the overall evaluation of an investment. However, we cannot identify a unique choice function when there is incomplete information about the company’s preferences. Yet, we can still elicit some basic properties of the choice function . One is monotonicity, that is, a better market environment (e.g., less competitive, better regulated), and/or higher profitability, and/or a larger market share would all lead to higher values of . The other property is quasi-concavity. For two investment opportunities and , each of which has an evaluation equal to or exceeding some level , their convex combination will also give an overall evaluation of at least . This property corresponds to diversification-favouring behavior in the risk management literature (Simon, 1955, Brown and Sim, 2009, Brown et al., 2012).

These two properties restrict the company’s choice function to belong to a specific class (monotone and quasi-concave functions). It is possible to further narrow down the scope of possible choice functions with some questionnaires for the company. For example, we can pose pairs of alternative investments with different levels of the three factors and ask which one is preferred by the company. It is even possible to pose these questionnaires to all senior managers, and then synthesize the most conservative estimate of the group’s preferences. We refer to Armbruster and Delage (2015), Hu and Mehrotra (2015), Delage and Li (2017) for further discussion on pairwise preference elicitation.

Example 1.2 (Consumer preference).

Consumer preferences for mobile phones are determined by multiple features including price, storage capacity, water resistance, chip, battery, camera, video recording, software, and customer service. Although some of these features are deterministic upon purchase (e.g., price), many of them represent uncertainty due to fluctuation in actual performance from the specified standard (e.g., battery capacity), or the customer’s inability to quantify the attributes beforehand (e.g., quality of customer service). Let denote the customer’s level of appreciation of the nine features of a mobile. We suppose where is the mean value of attribute and is random error which represents fluctuations in a particular customer’s actual experience. We let denote the customer’s choice function and denote the corresponding choice function evaluation.

If we enhance one or more of the features, e.g., by reducing the price, increasing the capacity, or improving the service, then it will increase the overall evaluation of the product. This property corresponds to monotonicity of the choice function. For any two other mobiles and for which the consumer’s overall evaluation exceeds , we believe that any convex combination for will also give the consumer an overall evaluation of at least . In other words, if the consumer is satisfied with both and , then he/she should also be satisfied with any convex combination of them. This property corresponds to quasi-concavity of the choice function.

Suppose the customer’s preferences can be represented by the quasi-concave choice function

where denotes the customer’s weights on the attributes and is a piecewise function defined by:

with . We take the particular weights given in the following table.

| 0.1837 | 0.1668 | 0.0645 | 0.0124 | 0.0071 | 0.1737 | 0.1240 | 0.0442 | 0.2235 |

The weights can be obtained via surveys or decision analysis tools like Analytic Hierarchy Processes or Analytic Network Processes. In practice we do not know the true choice function, so we might then use expected power utility to describe the customer’s preference s

where is a parameter.

Suppose we estimate via logistic approach (see e.g. Lopez-Guzman et al. (2018)). With these specific parameter values, we can compare and for a specific mobile to obtain:

| Mobile 1 | Mobile 2 | |

|---|---|---|

| 1.980 | 1.970 | |

| 1.723 | 1.724 |

We see that a naive parametric expected utility function cannot make the right prediction about the customer’s preferences when they can only be represented by a quasi-concave choice function.

In both of these examples, the DM’s preferences are ambiguous but we still have some partial information. We build a robust choice model that uses this partial information to compute the most conservative estimate of the DM’s preferences, which can then be used in subsequent optimization problems.

1.2 Contributions

As our main contribution, we create a robust choice model for preference ambiguity where the underlying choice function is monotone, quasi-concave, and (possibly) multi-attribute. Many of the existing PRO models represent diversification-favoring behavior through the stronger properties of concavity (for utility) or convexity (for monetary risk measures). However, these properties do not capture all forms of diversification-favoring behavior. In full generality, diversification-favoring behavior means that if two prospects are acceptable at some level, then any mixture should also be acceptable at this same level. For translation-invariant monetary risk measures, diversification-favoring behavior implies convexity. However, as argued by Cerreia-Vioglio et al. (2011), it only leads to quasi-convexity if the DM’s choice function is not translation invariant (see El Karoui and Ravanelli (2009) for reasons why translation invariance fails).

As a specific example of the importance of quasi-concavity, it has been shown that VNM expected utility theory cannot be used to effectively describe some economic behaviours (see Allais (1953), Kahneman and Tversky (2013)). The Allais Paradox (Allais, 1953) demonstrates that a DM’s preferences can be inconsistent with expected utility theory for “any” utility function. Brown et al. (2012) show that the Allais Paradox can be resolved with a class of quasi-concave choice functions called aspirational measures. Quasi-concavity is the key structural property that enables us to represent diversification-favoring preferences in the most general way, and to do PRO for the entire class of diversification-favoring DM’s.

Our robust choice model is encapsulated by a robust choice function (RCF) which gives the most conservative estimate of the DM’s preferences based on available partial information. Our first task is to evaluate the RCF with an appropriate optimization formulation. We do this by identifying the class of majorants of quasi-concave choice functions, and then using them to enforce the property of quasi-concavity as a constraint in our optimization formulation. As a consequence of the property of quasi-concavity (which is not preserved by convex combination), this formulation is non-convex. Yet, we can exploit special problem structure to solve it efficiently with a two-stage approach. The first stage “value problem” determines the value of the RCF on a set of distinguished prospects and the second stage “interpolation problem” evaluates a new prospect based on these values. We propose a novel sorting algorithm to efficiently solve the non-convex value problem based on a sequence of LPs. The optimal solution of the value problem can then be taken as input to the simpler and less expensive interpolation problem to evaluate prospects as needed. We can also incorporate the property of law invariance into this procedure. While law invariance introduces exponentially many variables and constraints into our optimization formulations, we can reduce both of these to only a polynomial number and still solve these problems efficiently.

Next, we do PRO by optimizing the RCF (for both the base and law invariant cases). The acceptance sets of the RCF follow from the solution of the value problem and can be characterized explicitly. In particular, we show that they are all polyhedra. We can then efficiently optimize the RCF by doing binary search over its levels, where at each level we solve a convex optimization problem to check membership of the corresponding acceptance set. This method only requires us to solve a logarithmic number of convex optimization problems.

Our robust choice model supports multi-attribute problems, which are ubiquitous. For instance, several metrics are used in healthcare to measure the quality of life (Feeny et al., 2002, Smith and Keeney, 2005). Multi-attribute problems are also found in product design (Kim and Chhajed, 2002), auction mechanism design (Beil and Wein, 2003, Parkes and Kalagnanam, 2005, Chen-Ritzo et al., 2005), and competitive positioning of business strategy (Adner et al., 2014). Indeed, over the past few decades, there has been significant research on multi-attribute expected utility (Von Stengel, 1988, Fishburn and LaValle, 1992, Miyamoto and Wakker, 1996, Tsetlin and Winkler, 2006, 2007, 2009) and multi-attribute risk management (Jouini et al., 2004, Burgert and Rüschendorf, 2006, Hamel and Heyde, 2010, Galichon and Henry, 2012). The existing PRO models emphasize single-attribute problems, and their formulations do not directly extend to the multi-attribute case. However, our model supports the multi-attribute case without any modification. In our capital allocation problem, we demonstrate that our sorting algorithm for constructing the RCF (both with and without law invariance) has strong scalability in terms of the number of attributes. Similarly, the complexity of our binary search algorithm for optimizing the RCF also grows slowly in the number of attributes.

1.3 Literature review

1.3.1 Utility-based PRO models

There are two ingredients in VNM expected utility theory: (i) the utility function represents the DM’s risk attitudes and tastes; and (ii) the probability distribution represents the DM’s beliefs about the underlying uncertainty on the states of the world. Classical VNM expected utility theory assumes there is no ambiguity in either of these ingredients, while an important stream of research focuses on ambiguity in the DM’s tastes. Such ambiguity may arise from a lack of an accurate description of human behaviour (Thurstone (1927)), cognitive difficulty, or incomplete information (Karmarkar (1978) and Weber (1987)). Parametric and non-parametric approaches have been proposed to estimate the true utility function, these include discrete choice models (Train, 2009), standard and paired gambling approaches for preference comparisons, and certainty equivalence (Farquhar, 1984). We refer readers to Hu et al. (2018) for an overview of the utility estimation approach.

In decision-making under uncertainty, the DM may mitigate the overall risk by choosing the worst-case utility function among a set of plausible utility functions representing his/her risk preferences. This approach can be traced back to Maccheroni (2002). Armbruster and Delage (2015) give a comprehensive treatment of this topic from the perspective of minimax preference robust optimization (PRO). Specifically, they construct an ambiguity set that combines structural properties of utility functions such as monotonicity, concavity, and S-shapedness, along with user-specific preference information elicited through pairwise comparison questionnaires. They derive tractable reformulations for the resulting PRO problem by exploiting the affine majorants of the class of concave functions (which characterize the property of concavity) to obtain convex optimization problems.

Hu and Mehrotra (2015) also do PRO for VNM-type DMs, but they construct the ambiguity set differently. They establish an equivalence between increasing convex utility functions and CDFs. Then, they construct a moment-type ambiguity set for the DM’s utility function based on the certainty equivalent, pairwise comparisons, upper and lower bounds of the trajectories of the utility functions, and bounds on their derivatives. They derive a tractable LP reformulation of their resulting PRO problem based on a piecewise linear approximation.

Delage et al. (2017) propose a robust choice model for investors whose preferences are expressed by a shortfall risk measure and who are ambiguous about their utility loss function. They construct an ambiguity set for the utility loss function that can accommodate convexity, boundedness, coherence, and pairwise comparisons. Then, they obtain a tractable LP reformulation of their PRO problem. This model is extended by Zhang et al. (2020) to multivariate shortfall risk measures and by Zhang and Xu (2021b) to generalized shortfall risk measures based on cumulative prospect theory.

The problem of ambiguity in the DM’s tastes is also related to cautious expected utility (Cerreia-Vioglio et al., 2015) which considers the worst-case certainty equivalent from a given set of utility functions. Cerreia-Vioglio et al. (2015) show that the DM’s risk preferences can be represented by a worst-case certainty equivalent if and only if they are given by a binary relation satisfying the weak order, continuity, weak monotonicity, and negative certainty independence (NCI).111NCI states that if a sure outcome is not enough to compensate the DM for a risky prospect, then its mixture with another lottery which reduces the certainty appeal, will not be more attractive than the same mixture of the risky prospect and the lottery. We also point out the connection between utility-based PRO and optimization with stochastic dominance constraints (see, e.g., Dentcheva and Ruszczyński (2004)). Stochastic dominance constraints require all DM’s with utility functions in a certain class to prefer a candidate prospect to a benchmark.

1.3.2 Other PRO models

Delage and Li (2017), Li (2021) do PRO for the class of convex risk measures. They construct an ambiguity set of risk measures based on properties such as convexity, coherence, law invariance, and elicited preferences. They then develop tractable reformulations using the acceptance set representation for convex risk measures, which allows their PRO models to be solved with linear programming and convex optimization. Li (2021) further incorporates inverse optimization information into the construction of the ambiguity set by observing the DM’s past optimal decisions. The optimization formulations in Delage and Li (2017), Li (2021) are also based on the special properties of affine majorants/minorants of concave/convex functions (this special property is used earlier in Armbruster and Delage (2015) as well).

Wang and Xu (2020) consider preference ambiguity in spectral risk measures (SRM), which are based on Yaari’s dual theory of choice. They introduce a robust SRM model based on the worst-case risk spectrum from a ball centred at a nominal risk spectrum. A step-like approximation for the risk spectra is developed and used in optimization to get a tractable problem, and an error bound for the approximation is derived.

There is other work on robust multi-attribute choice models, for instance see Lam et al. (2013), Ehrgott et al. (2014). Noyan and Rudolf (2018) consider multi-attribute PRO for a general class of scalarization functions (i.e., the class of min-biaffine functions), where the vector of weights for the multiple attributes lies in a convex ambiguity set. Vayanos et al. (2020) study active preference elicitation for multi-attribute problems, under both the max-min utility and min-max regret decision criteria. They focus on the trade-offs between the multiple attributes, and show that their problem can be formulated as a two-stage (resp. multi-stage) robust optimization problem with decision-dependent information discovery and solved efficiently.

1.3.3 Quasi-concavity

Quasi-concave choice functions have already appeared widely in the literature. One of the most prevalent examples of a quasi-concave choice function is the certainty equivalent (see, e.g., Ben-Tal and Teboulle (2007)). The indices of acceptability proposed by Cherny and Madan (2009) are also quasi-concave choice functions.

Brown and Sim (2009) develop the class of satisficing measures, which are based on the idea of meeting a target (satisficing rather than optimizing), and which are quasi-concave. Their work is continued in Brown et al. (2012) where the authors develop the class of aspirational measures. This class of measures is allowed to be quasi-concave on a diversification-favoring set, and quasi-convex on a concentration-favoring set. The representation result in Brown et al. (2012) shows that aspirational measures can be expressed in terms of a family of risk measures and targets. We establish a similar result in this paper for our RCF.

In our earlier paper Haskell et al. (2022), we do PRO for optimization over lotteries. In particular, we optimize over a mixture of finitely many decision alternatives. This model is based on quasi-concave choice functions over lotteries (see, e.g., Frittelli et al. (2014) which discusses why this property is natural for preferences on lotteries). Our present paper is for optimization over prospects and applies to a much larger class of problems, since we do not need to restrict to finitely many alternatives. Furthermore, our present paper develops new and more efficient algorithms to construct the RCF and solve the PRO problem.

1.4 Organization

In Section 2, we review preliminaries on choice models and present our preference robust choice model. In Section 3, we show how to efficiently evaluate the RCF. In Section 4, we show how to evaluate the law invariant RCF which depends on an additional reduction to get formulations of manageable size. Section 5 details the construction of the acceptance sets of the RCF. Then, Section 6 shows how to do PRO with our model based on the acceptance sets of the RCF. In Section 7, we discuss some extensions of our robust choice model. Section 8 reports numerical experiments, and the paper concludes in Section 9. The proofs of all technical results are in the appendices.

2 Preference robust choice model

Notation. We use and to denote the set of vectors in with all non-negative components and all strictly positive components, respectively (for we just write and ). Let denote the positive integers. For any , we let . We let denote the optimal value of an optimization problem.

Let be a sample space with scenarios denoted by . We assume that has finitely many scenarios.

Assumption 2.1.

for .

This assumption appears throughout the risk preference literature (see, e.g., Artzner et al. (1999), Rockafellar and Uryasev (2013)). Armbruster and Delage (2015), Delage and Li (2017) also make this assumption in their preference robust models. In the case when the sample space is continuous, Assumption 2.1 may be regarded as a discrete sample/approximation, Guo and Xu (2021) give theoretical grounding for such an approximation.

Let be the space of all mappings for , equipped with the essential supremum norm:

We just write for the single-attribute case . Each represents a prospect - it is a mapping from scenarios in to a vector of attributes which represent gains/rewards and where larger values are preferred. Under Assumption 2.1, we can identify with and represent each prospect by the vector of its realizations . This convention also appears in the single-attribute PRO models in Armbruster and Delage (2015), Delage and Li (2017), Li (2021). We write when for all and (i.e., if dominates on all scenarios and for all attributes).

2.1 Choice functions

We begin with the definition of a choice function representing the DM’s preference relation on . Let denote the extended real line.

Definition 2.1 (Choice function).

Let be a preference relation on . The function is a choice function corresponding to if and only if for all with . For a choice function , is strongly preferred to if , and is weakly preferred to if .

The choice function is also known as a representation of the preference relation (see, e.g., Puppe (1991)). The expected utility model of Von Neumann-Morgenstern (see, e.g., Puppe (1991)) is a well-known type of choice function. Existence and uniqueness of a choice function depend on the prospect space and its associated preference relation . For example, there is a continuous choice function if and only if is a weak order and continuous.

Under Assumption 2.1, we can view choice functions as mappings , and we can state their properties in terms of mappings on . We let

denote the set of admissible choice functions. Next we elaborate on the axiomatic properties of the choice functions used in this paper.

Property 2.1.

[Usc] (Upper semi-continuity) For all , .

Property 2.2.

[Mon] (Monotonicity) For all , implies .

This definition of [Mon] is with respect to the preference relation , which is natural since is “equipped” with by construction. However, we assume that the scenario relation implies the preference relation, and so implies . Consequently, implies .

Property 2.3.

[QCo] (Quasi-concavity) For all and , .

[QCo] is part of the novelty of our robust choice model. It is the mathematical expression of the diversification-favoring principle: if prospects and are both preferred to , then so is any mixture for , see Cerreia-Vioglio et al. (2011). [QCo] is a weaker form of diversification-favoring behavior compared to concavity. We let denote the set of all quasi-concave choice functions on . Furthermore, we let

denote the set of choice functions satisfying our three fundamental properties.

Now we discuss some additional properties of the choice functions used in this paper. Law invariance is a widely accepted property where the DM only cares about the distribution of prospects on , and not on the dependence of on the underlying scenario .

Property 2.4.

[Law] (Law invariance) for all such that (where denotes equality in distribution).

Under [Law], prospects can be presented to the DM in terms of their outcome distributions on instead of as mappings . Some choice functions are intrinsically law invariant (e.g., expected utility), but this property is not automatic. The set of choice functions satisfying [Law] is

In addition to the structural properties just mentioned, we have specific preference elicitation data on the DM. We suppose we have offered the DM a questionnaire consisting of pairs of prospects, and that they have indicated which prospect is preferred for every pair.

Property 2.5.

[Eli] (Preference elicitation) For a set of pairs of prospects , for all .

We refer to the set of pairs in [Eli] as the ECDS (elicited comparison data set). We define to be the set of choice functions compatible with the ECDS.

We close with two additional properties that ensure our choice functions are well-defined. It is clear that for any constants and , we have

| (1) |

since [Usc], [Mon], and [QCo] are all preserved by multiplication by positive scalars and translation by scalars. Suppose corresponds to the preference relation , and let for any and . It follows that and also corresponds to . Conversely, if we have a preference relation induced by a choice function , then the same preference relation will be recovered from any positive linear transformation of . We refer to this property of as ‘invariance under positive linear transformation’. By this invariance, we can pin the choice functions in at a fixed value and recover the rest by scalar translation.

Property 2.6.

[Nor] (Normalization) for some .

We call in [Nor] the normalizing prospect, and we define . In some applications we can just take to be a constant prospect. In our model, we take to be the canonically most preferred prospect among the preference elicitation data so that holds for all .

By invariance under positive linear transformation, we can also constrain the variability of the choice functions in .

Property 2.7.

[Lip] (Lipschitz continuity) For , for all .

Lipschitz continuity is widely accepted in the risk management literature. Indeed, any risk measure that is (sub-)translation invariant is Lipschitz continuous with modulus , see Cerreia-Vioglio et al. (2009). We define the set of Lipschitz continuous choice functions to be

2.2 Robust choice functions

Our focus is on the situation where available information is inadequate to identify a unique choice function which captures the DM’s preferences precisely. This should be distinguished from “incomplete preferences” in the literature of economics (see, e.g., Ok et al. (2012)). The latter refers to the case where a DM is unable to make a choice between two prospects either because of incomplete information about the subjective probability distribution (ambiguity in brief/Knightian uncertainty) or an inability to compare two certain outcomes. Here we do not consider this type of incompleteness in preferences.

We make the following underlying assumption on the DM’s preferences to ensure that they are compatible with the observed ECDS.

Assumption 2.2.

The DM’s preferences can be described by a choice function in .

Under Assumption 2.2, the DM’s preferences are described by a function in . Preferences induced by a choice function are automatically complete, and so we can compare any two prospects.

Though we know the true choice function belongs to and also satisfies [Nor], [Lip], and [Eli], we cannot identify a unique choice function. This situation motivates us to consider robustness against ambiguity in the choice function, and we construct an ambiguity set that characterizes plausible choice functions. Then, we follow the convention in robust optimization of optimizing against the worst-case realization from the ambiguity set for a given input (which is a prospect ).

Definition 2.2 (Robust choice function).

The robust choice function (RCF) corresponding to the preference ambiguity set is defined via:

This definition matches the rest of the PRO literature. Armbruster and Delage (2015) consider the worst-case expected utility and Delage and Li (2017), Li (2021), Zhang and Xu (2021a) all consider the worst-case risk over various preference ambiguity sets. There are various interpretations of the RCF. In the context of group decision-making, it corresponds to the member of the group who is least satisfied with a given prospect.

2.3 Specific ambiguity sets

We consider two particular ambiguity sets in this paper: the base case

and the law invariant case

We will develop the base case first to demonstrate how to handle [QCo], and then we will incorporate [Law].

We have the following properties of our corresponding RCFs.

Proposition 2.3.

Let .

-

(i)

is well-defined over and .

-

(ii)

The preference relation induced by is invariant under .

Part (i) of the above proposition says that the RCF itself belongs to , since all of our axiomatic properties are preserved by the infimum. Part (ii) establishes that the Lipschitz modulus affects the value of the RCF but not its induced preference relation. This property implies that we do not need to identify precisely, we only need to know that Lipschitz continuity holds for some .

3 Evaluating the robust choice function

In this section we discuss numerical methods for evaluating for a fixed prospect . In particular, we show how to encode the property of quasi-concavity, and this is the main novelty of our optimization formulation. By Assumption 2.1, we are interested in the function values of the RCF over .

We define the prospect set

which consists of the normalizing prospect and all prospects in the ECDS. We also define to be the total number of prospects in .

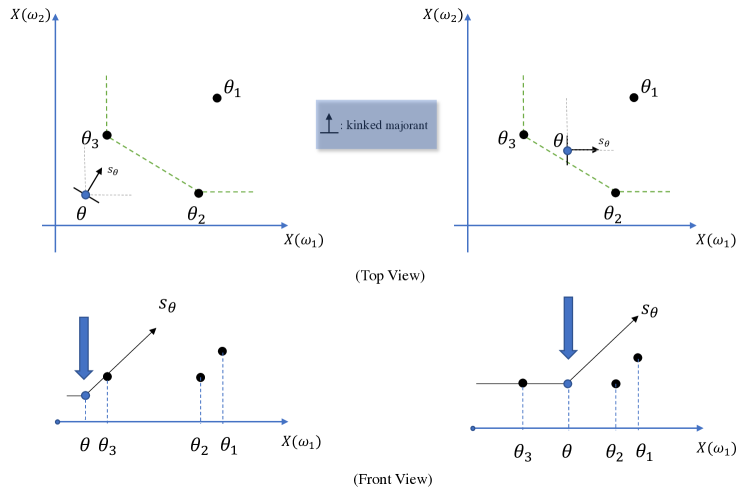

Next we introduce the concept of a kinked majorant. A quasi-concave function has a kinked majorant at every point, so they are the key to characterizing [QCo] numerically.

Definition 3.1 (Kinked majorant).

Let and fix . Let and , then is called a kinked majorant of at if for all . In that case, is said to be an upper subgradient of at . The set of all upper subgradients of at is called the upper subdifferential and denoted by .

Note that any such kinked majorant is automatically in (i.e., it has convex upper level sets).

Now we give an optimization formulation for . It is based on decision variables which correspond to the values of a quasi-concave choice function, and its kinked majorants, on . It shows that we can compute (which calls an infinite-dimensional optimization problem) by solving a finite-dimensional optimization problem. This formulation also leads to an efficient way to evaluate that we will explain momentarily.

Define to be the set of all edges in the set . We use to enforce quasi-concavity, since for every there must be a kinked majorant which dominates all other .

Theorem 3.1.

For any , is equal to the optimal value of:

| (2a) | |||||

| s.t. | (2g) | ||||

where and correspond to the values of the kinked majorants, and and correspond to the upper subgradients.

Problem (2) is referred to as a disjunctive programming problem (i.e., constraint (2g) is a disjunctive “or” constraint ), which are non-convex and generally hard to solve. Problem (2) has a reformulation as a mixed-integer linear program (MILP) by introducing binary variables to handle the disjunctive constraints, which results in binary variables. In the worst-case, this reformulation would need LPs to be solved to compute the globally optimal solution. We do not use the MILP approach for this reason. Rather, we will shortly propose a two-stage decomposition of Problem (2) and then demonstrate how to solve the decomposed problems more efficiently than MILP.

3.1 Outline of proof of Theorem 3.1

We first note that Problem (2) has an optimal solution by Lemma B.3. The connection between kinked majorants and the RCF is based on the following equivalence. For any , let

be the set of all choice functions in that match the values on (which may be empty).

Proposition 3.2.

Fix , then if and only if, for all , there exists a kinked majorant where is an upper subgradient of at with , such that for all .

By the previous proposition, is nonempty if and only if there is a kinked majorant at every point that majorizes all the others . The constraint can then be enforced by requiring the existence of kinked majorants for all , which gives the disjunctive constraints in Problem (2).

Next we see that

| (3) |

where we use the fact that . This equivalence means that can be calculated either by: (i) minimizing over directly; or (ii) fixing the relevant values on and then minimizing over that match these values.

By definition of , we can write the RCF as

| (4a) | ||||

| s.t. | (4b) | |||

By Proposition 2.3(i), the optimal value of this problem is always finite as it is lower bounded by . Note that the constraint is just the preference elicitation Constraint (2g) and the constraint is just the Lipschitz continuity Constraint (2g). Both of these conditions only constrain the values of on via . The constraint states that there must exist a function in that takes the values on . This requirement is enforced by: (i) Constraint (2g) (the majorization condition on the values corresponding to quasi-concavity); and (ii) Constraint (2g) (the requirement that the support functions that majorize on be increasing and Lipschitz continuous). Finally, Constraint (2g) is just the normalization condition .

It remains to explain how the objective function in Eq. (4a) can be evaluated (i.e., how to evaluate for fixed ), and how Constraint (4b) can be enforced. By Proposition 3.2 and Lemma B.2 (which characterizes Lipschitz continuous quasi-concave functions in terms of their kinked majorants), we know that over all increasing quasi-concave functions in , the one minimizing attains the value

where the constraints in the above display are captured by Constraint (2g). In particular, these constraints require the kinked majorant to majorize the points . In summary, we have established that the optimal value of Problem (2) recovers .

3.2 Two-stage decomposition

Problem (2) can be solved more easily by decomposing it into two separate problems. The first is the value problem where we solve:

| (5a) | |||||

| s.t. | (5e) | ||||

Notice that the value problem does not depend on the specific for which we are trying to evaluate , it only minimizes the sum of the values of the RCF on . The second is the interpolation problem where, for given values , we solve:

| (6a) | |||||

| s.t. | (6c) | ||||

The interpolation problem finds the smallest possible value for among functions that majorize the values on .

The next result connects the value and interpolation problems. It shows that we only have to solve the (harder) value problem once, and then we can solve the (easier) interpolation problem as needed for specific .

Theorem 3.3.

Problem has a unique optimal solution , where for all . For all , .

For the rest of the paper we let denote the optimal solution of , which correspond to the values of the RCF on .

Problem is the most expensive step in our method because there are disjunctive constraints in (5e). As for Problem (2), has an MILP reformulation with binary variables. This reformulation requires LPs to be solved in the worst-case which leads to computational intractability when the number of elicited pairwise comparisons is large.

3.3 A sorting algorithm for the value problem

We now propose a novel sorting algorithm for solving . This algorithm is based on solving a sequence of LPs, and it orders the prospects in according to their values. It is significantly more efficient than standard solution approaches (e.g., Big-M or convex hull) which may require an exponential number of LPs to be solved.

Our method relies on an intrinsic feature of kinked majorants. By definition, any kinked majorant of at satisfies and for all prospects . In particular, for those prospects satisfying , we automatically have . Thus, we do not need to know the exact RCF values of those less preferred prospects (i.e., those with smaller values) when determining the value of , and we can effectively just ignore them. In this way, we want to order the prospects in according to their values, while we compute the values along the way. By this observation about the kinked majorants, we can recursively sort the prospects in according to their values.

For this discussion, we associate each with its value as an ordered pair .

Definition 3.2.

We call an ordered list a decomposition of if: (i) is a permutation of ; and (ii) for all such that precedes in .

Our goal now is to construct a decomposition . For all , let

| (7) |

so . Moreover, by our convention the normalizing prospect is canonically the most preferred with value (by [Nor]), we always initialize the sorting with . We treat as ordered lists (rather than sets) because the order of their elements matters. For two ordered lists and , we let denote the ordered list obtained by concatenating and . With a slight abuse of notation, we say that if (i.e., if prospect has already been sorted).

Before introducing our sorting algorithm, we note that the value problem has an optimal solution with an important property. There is an optimal solution of Problem (5) that remains optimal if we replace the objective by alone, for any . In other words, solving Problem (5) is essentially the same as separately minimizing among feasible choice functions for all .

Given , we want to find such that has the largest value in , then we will add such a to to obtain . We predict the values of by solving the following program for each :

| (8a) | ||||

| s.t. | (8b) | |||

| (8c) | ||||

| (8d) | ||||

In this formulation, Constraint (8b) corresponds to Constraint (5e). The main difference is that because is decomposed into and , the inequality in Constraint (8b) is only required to hold for . Constraint (8c) corresponds to Constraint (5e). Constraint (8d) requires a bit more explanation. By writing , we mean that corresponds to a pairwise comparison in the ECDS for some . By [Eli], and thus we must have , or equivalently . On the other hand, since and , we have . Thus, the constraint must hold with equality.

Starting with , we always choose the prospect that is associated with the largest optimal value . Intuitively, because this particular prospect has the largest attainable value in , it corresponds to the largest value among prospects in . This procedure is the backbone of our sorting algorithm. It solves Problem (5) recursively by solving instances of the simpler Problem (8), and it terminates with a decomposition .

The following Example 3.1 illustrates our procedure for selecting the next prospect based on . This example shows that (given ) for any with , we may have but we will always choose with the largest to append to . In this case, we must have .

Example 3.1.

Suppose and so . Assume that and holds. We compute the optimal value of Problem (8) for all given , to see that and must hold. If ,222 This could happen because the preference relation is not reflected in the constraints of . We may imagine a situation where and are in symmetric positions (e.g., and in two-dimensional space), whereas , , and are closer to so that the RCF values at , , and have a stronger binding effect on the quasi-concavity of the RCF at than at . then we have

and consequently . Alternatively, if holds, then we have

and consequently .

Problem (8) significantly reduces the number of disjunctive constraints compared to from to , but it is still a disjunctive program. This observation motivates us to consider the following LP:

| (9a) | ||||

| s.t. | (9b) | |||

| (9c) | ||||

| (9d) | ||||

Problem is similar to , except that the linear Constraints (9b) are tighter than the corresponding disjunctive Constraints (8b). Consequently, . However, there is a fundamental relationship between and . We can show that the optimal value of is either or the optimal value of , whichever is smaller. That is,

| (10) |

where we refer to the function as the predictor.

To demonstrate this claim, we consider the two cases depending on (recall always holds):

- •

-

•

Case 2: (see Figure 1 (right)). In this case, since . It follows that .

The details of our sorting procedure are summarized in Algorithm 1. For fixed , we see that Algorithm 1 solves at most instances of Problem (9). In Case 1, is added to with RCF value . In Case 2, is added to with RCF value . Note that if we encounter which falls into Case 2, then the RCF at achieves . This is then chosen as , and there is no need to solve Problem (9) for other in .

Example 3.2.

Theorem 3.4.

We can compute the optimal solution of after solving at most instances of Problem (9).

In our experiments, we will see that, in line with Theorem 3.4, the computational complexity of our sorting algorithm grows much more slowly in the size of the ECDS compared to the convex hull reformulation of (see Table 1 and Table 2). The complexity of our model mostly depends on (which determines the number of LPs we need to solve). It is relatively less sensitive to the number of attributes and scenarios , because they only affect the size of the LP in each instance and LPs can be solved very efficiently.

3.4 Solving the interpolation problem

After obtaining the optimal solution of , we can evaluate the RCF for any prospect by solving . Following similar arguments to those in Subsection 3.3, solving is equivalent to calculating for the index which satisfies:

| (11) |

In order for Eq. (11) to have a solution for all values of , we artificially define to be a constant prospect with value , and we set . We will identify the correct index by solving a sequence of instances of , based on the relationships in the next proposition.

Proposition 3.5.

Suppose Eq. (11) holds for .

(i) . Moreover, for all , and for all .

(ii) for all , and for all .

Proposition 3.5(i) is a direct consequence of Eq. (10) and the fact that has the same objective but more constraints than for . To establish Proposition 3.5(ii), notice that for we have , and

Meanwhile if then and . Hence

We can identify the correct in Eq. (11) by choosing the least element of the set , so that by Proposition 3.5(i). This procedure is summarized in the following level search algorithm (we call it level search because we are trying to identify an appropriate level for such that the strict inequality holds).

Level search essentially enumerates the levels and finds after solving at most instances of . One can further reduce the complexity of solving the interpolation problem to with binary search (see Algorithm 5 in Appendix B).

Theorem 3.6.

Given , the value can be computed after solving at most instances of .

4 Law invariant case

In the previous section, we assume that the DM has an unknown choice function and may evaluate prospects differently even when they have the same law (i.e., the same outcome distribution on ). That is, the choice function may not be law invariant. Law invariance is a fundamental property of the preferences when the DMs only care about the outcome distribution. In this section, we incorporate [Law] into our RCF.

To begin, we introduce a reference probability measure on to assign distributions to prospects in (formally, the distribution on for any ).

Assumption 4.1.

The probability measure satisfies for all .

This assumption is without loss of generality if takes rational values on . When has rational values we can just take the underlying sample space to be sufficiently large and give equal weight to recover any desired rational probability (see Delage and Li (2017)). The empirical probability measure in sample average approximation automatically satisfies this assumption.

Let denote the set of all permutations on . Under Assumption 4.1, we can encode [Law] in terms of . For a permutation , we permute the sample space as . Similarly, we permute as . A law invariant choice function must satisfy for all and , since and have the same distribution on .

Let denote the distribution of . Then, under [Law] and Assumption 4.1, we can characterize the DM’s preferences in terms of outcome distributions. In particular, the relation is equivalent to for all . The ECDS can then be expressed equivalently in terms of distributions as , where the DM weakly prefers to for all .

Similar to Section 2, we make the following assumption on the DM’s preferences so that our law invariant RCF is well-defined.

Assumption 4.2.

The DM’s preferences can be described by a choice function in .

Recall is the ambiguity set for law-invariant choice functions. We give an optimization formulation for . Recall is the set of prospects used in the construction of the RCF. We define the augmented support set

with cardinality . Then, we define

to be the set of all edges in . Finally, we define the augmented ECDS

to be the set of all permutations of pairs in . We obtain the following formulation for , the proof is similar to Theorem 3.1.

Theorem 4.3.

For any , is equal to the optimal value of:

| (12a) | |||||

| s.t. | (12g) | ||||

where and correspond to the values of the kinked majorants, and and corresponds to the upper subgradients.

Law invariance adds a computational cost to Problem (12) over the base case since there is now an exponential number of constraints due to the indexing by permutations.

We will develop a two-stage decomposition scheme for evaluation of by leveraging our results for the base case. The law invariant value problem is:

| (13a) | |||||

| s.t. | (13e) | ||||

Problem is similar to , except that it has an exponential number of variables in , and an exponential number of constraints in Eqs. (13e) - (13e). For values , the law invariant interpolation problem is:

| (14a) | |||||

| s.t. | (14c) | ||||

Problem is similar to except that it has an exponential number of majorization constraints (but it does have the same variables which determine a single kinked majorant at ).

In the next proposition we confirm that an optimal solution of exists and is unique. Furthermore, we show that the values at the optimal solution are invariant under permutation.

Proposition 4.4.

Problem has a unique optimal solution . Furthermore, for all and .

It follows that we only need to compute for each , and then we can assign this same value to all permutations of . We may then characterize the optimal solution of with instead of . Subsequently, reduces to:

| (15a) | |||||

| s.t. | (15c) | ||||

We emphasize that this reduction is specific to the optimal solution of , and does not necessarily hold for arbitrary .

We now have the following two-stage decomposition result which connects the law invariant value and interpolation problems.

Theorem 4.5.

Let be the optimal solution of . Then, for all . Furthermore, for all .

Since we only have to determine the values of the law-invariant RCF on , we can solve with a decomposition of (instead of the much larger set ). We denote this decomposition as and to distinguish the law invariant case. Given for , we define to be the ordered list containing all permutations of prospects in . We know for all and , we can seat all permutations of the same next to each other in since they are sorted by value.

For and , we define the following LP:

| (16a) | ||||

| s.t. | (16b) | |||

| (16c) | ||||

| (16d) | ||||

Problem has an exponential number of constraints, but we can reduce it to a more tractable problem with a polynomial number of constraints (see Delage and Li (2017) where this idea is used for PRO with convex monetary risk measures). This reduction is based on strong duality results for the binary assignment problem.

Let be the vector of realizations corresponding to attribute of . For an upper subgradient corresponding to a kinked majorant, let be the vector of realizations of corresponding to attribute . We also let denote the unit vector in , and denote the transpose operation. For , the reduced LP is:

| (17a) | ||||

| s.t. | (17b) | |||

| (17c) | ||||

| (17d) | ||||

| (17e) | ||||

| (17f) | ||||

| (17g) | ||||

Note the LHS of Constraint (17c) is a matrix, so this inequality is understood to hold component-wise. In particular, note that has a polynomial number of constraints. We justify the reduction from to in the following proposition.

Proposition 4.6.

For all and , .

The law invariant sorting algorithm for is as follows (see Algorithm 6 in Appendix C for the detailed steps). Given , we compute the law invariant predictor

Then, one of the prospects that maximizes , as well as its predicted value, is chosen to append to , and we proceed to the next iteration. The algorithm terminates with a decomposition . The next theorem gives the computational complexity for solving using this method.

Theorem 4.7.

We compute the optimal solution of after solving at most instances of Problem (17).

We note the same order of complexity for the law invariant sorting algorithm compared to the base sorting algorithm (i.e., it is rather than ). We may also use binary search to solve the law invariant interpolation problem (see Algorithm 8), with the same logarithmic complexity as the base case.

Theorem 4.8.

Given , the value can be computed after solving at most instances of Problem (17).

In particular, the complexity of law invariant binary search for the interpolation problem depends on rather than .

5 Acceptance set representation

In this section we construct the acceptance sets of the RCF. This construction gives another representation of the RCF in terms of the epigraph formulation. Furthermore, this construction leads to our method for doing PRO efficiently.

The acceptance set at level induced by the RCF is

The epigraphical representation of the RCF in terms of its acceptance sets is:

| (18) |

Eq. (18) will be useful for optimization of the RCF in the next section, after we identify the explicit form of the acceptance sets.

We construct based on the optimal solution of (the normalizing prospect is canonically the most preferred so all prospects considered will have non-positive RCF values). This construction is based on a level selection rule which maps a level to a subset of prospects in , which is then used to construct the corresponding . Recall that has value , and .

Definition 5.1 (Level selection).

Given , .

For and , we use the prospects in to construct . The level selection rule enforces the condition corresponding to Eq. (11). The selection is unique under this convention since we must always choose with . There may be with (i.e., repeated values), but such are never selected. If there are multiple indices which give the same value , then will return the largest such index.

The next proposition shows that we can check if by solving for . It is based on the dependence of on for .

Proposition 5.1.

For and , if and only if .

The previous proposition leads to the characterization of by linear programming duality.

We denote the LP dual of by (see the explicit formulation in Eqs. (47a)-(47c)). By strong duality, we have and so the inequality is equivalent to . Since is a maximization problem, is just a feasibility problem, and its constraints lead to the explicit acceptance set representation in the following theorem. Let be the vector with all components equal to one. We define translations of the prospects in by (where we subtract from every component of ).

Theorem 5.2.

For ,

Theorem 5.2 shows that the acceptance sets have a piecewise linear structure, and that checking can be done by solving a linear feasibility problem. In view of as a translation of , we can interpret as the smallest monotone polyhedron that contains the convex hull of all translations of prospects for which .

The law invariant case follows the same idea. The acceptance sets of are:

and the epigraphical representation is:

| (19) |

By strong linear programming duality (see Eqs. (49) for the dual of ), we arrive at the following characterization of the law invariant acceptance sets.

Theorem 5.3.

For all , we have

Theorem 5.3 shows that the law invariant acceptance sets also have a piecewise linear structure, and checking can similarly be done by solving a linear feasibility problem. The representation of in Theorem 5.3 is based on the dual of the reduced LP , rather than , and so it has a polynomial number of variables and constraints.

6 Preference robust optimization

Now suppose the DM wants to optimize over a set of admissible prospects. In the face of ambiguity about the DM’s preferences, we cannot precisely identify a choice function to optimize, so we optimize the RCF. We show that this problem can be solved efficiently based on the acceptance set representation.

The DM’s optimization problem is as follows. Let be a set of feasible decisions for . Then, let be a stochastic reward function where is the vector of rewards/gains on scenario . Under Assumption 2.1, the stochastic function can be expressed in vector form for any . The following assumptions are typical in the stochastic optimization literature (see, e.g., Shapiro et al. (2014)).

Assumption 6.1.

(i) is compact and convex.

(ii) is concave (i.e., is concave in the vector-valued sense with respect to for all ).

Given a preference relation and a corresponding choice function representing , we would solve:

to identify an optimal solution for the DM. However, requires complete information about the choice function , and the optimal solution of is highly sensitive to .

Faced with this ambiguity, we will optimize the RCF:

for an ambiguity set . The objective of is quasi-concave under Assumption 6.1 for any , since the composition of an increasing quasi-concave function with a concave function is quasi-concave. It follows that is maximizing a quasi-concave function over a convex set, and so it can be solved via a sequence of convex feasibility problems.

We focus on solving the specific PRO problems and based on the acceptance sets of the RCF. By the epigraphical representation of the RCF, is equivalent to

We can solve the above reformulation of via a sequence of convex feasibility problems of the form:

| (20) |

where is fixed. Finding the largest for which Eq. (20) is feasible is equivalent to solving . Since we have the explicit form of , we can solve Eq. (20) (or determine it is infeasible) for any .

Conceptually, we can scan over all levels to find the largest such that Eq. (20) is feasible. However, Theorem 5.2 shows that the acceptance sets have a piecewise linear structure that depends on the level . So, the search over all can be broken up into separate feasibility problems for each :

| (21) |

where is also an optimization variable in Eq. (21).

Based on Theorem 5.2, the feasibility problem corresponding to Eq. (21) is explicitly:

| (22a) | ||||

| s.t. | (22b) | |||

| (22c) | ||||

| (22d) | ||||

for each . Problem can be interpreted as finding such that the prospect is acceptable at a level .

If is feasible for , then it is feasible for any since are non-increasing in . We want to find the least such that is feasible. Once we locate such a , we solve the following convex optimization problem:

| (23a) | ||||

| s.t. | (23b) | |||

| (23c) | ||||

| (23d) | ||||

which returns the optimal solution and optimal value of . We summarize this procedure in the following level search algorithm.

Algorithm 3 searches over the index set and finds the smallest such that is satisfied for some . This search procedure solves after solving at most instances of . We can get better complexity with binary search (see Algorithm 9 in Appendix E).

Theorem 6.2.

The computational complexity in Theorem 6.2 follows from the standard complexity of binary search (since we have alternatives to check). In line with this theorem, our numerical experiments show that the running time of Algorithm 9 is not really sensitive to . It is more sensitive to the problem dimension which is captured by and (see Table 4).

The law invariant case is similar, ) is equivalent to

which corresponds to a sequence of feasibility problems of the form . We can represent this feasibility problem explicitly as follows. For each , we introduce decision variables , , , , and and we consider the following feasibility problem:

| (24a) | ||||

| s.t. | (24b) | |||

| (24c) | ||||

| (24d) | ||||

| (24e) | ||||

Once we find the smallest such that is feasible, we solve the following convex optimization problem:

| (25a) | ||||

| s.t. | (25b) | |||

| (25c) | ||||

| (25d) | ||||

| (25e) | ||||

| (25f) | ||||

We can then solve by doing binary search over levels (see Algorithm 10 in Appendix E for the detailed steps).

Theorem 6.3.

We will see in our numerical experiments that both and can be solved quickly by binary search once the value problem has been solved (and the corresponding acceptance sets have been constructed). The complexity of is of the same order as , in terms of the number of convex optimization problems that need to be solved. However, the complexity is more sensitive to in the law invariant case than in the base case.

7 Discussion

7.1 Relation to aspirational measures

Our robust choice model is closely related to aspirational measures (developed in Brown et al. (2012)), which are target-oriented choice functions. We recall the following property.

Property 7.1.

[QCx] (Quasi-convexity) For all and , .

Property [QCx] represents concentration-favoring behavior. Next we recall the class of aspirational measures, which are originally defined for single-attribute problems on .

Definition 7.1.

(Brown et al., 2012, Definition 1) A choice function satisfying [Usc] is an aspirational measure if there exists a partition of into three disjoint subsets (diversification-favoring), (neutral), and (concentration-favoring) (some possibly empty) such that: (i) satisfies [QCo] on ; (ii) satisfies [QCx] on ; and (iii) for all , , and .

Brown et al. (2012) give the following representation result for single-attribute aspirational measures on (for ). They show that an aspirational measure can be constructed in terms of a family of risk measures and targets. Specifically, an aspirational measure can be evaluated by selecting the maximum index level such that the risk of beating the target at that level is acceptable.

Theorem 7.1.

(Brown et al., 2012, Theorem 1) A choice function is an aspirational measure (with partition , , and ) if and only if there exists a constant such that for all , and

where is a family of risk measures (monotonic, translation invariant, and normalized ), convex if , concave if , with closed acceptance set , and , the target function, is a constant prospect for all and nondecreasing in . Moreover, is non-decreasing in for all .

We now represent as an aspirational measure. We first define a set of risk measures corresponding to each level . Recall is the constant prospect with all components equal to one, and for all . Then define constants

and the acceptance sets

where we recall is defined in Eq. (7). Now we can define explicitly by

for all . We note that the risk measures are defined for multi-attribute prospects on for .

Proposition 7.2.

are monotone, convex, and translation invariant with respect to the direction (i.e., for all ). In addition, for all .

We introduce a target function to complete the representation of as an aspirational measure. Our target function is for all , where is the level selection rule from Definition 5.1.

Theorem 7.3.

(i) The target function is non-decreasing in .

(ii) We have

Our RCF is a special aspirational measure with empty concentration-favoring set (i.e., ), since the risk measures are all convex.

Theorem 7.3 builds on Brown et al. (2012) by supporting multi-attribute problems. This representation of is a choice function on for . The constituent risk measures are defined for multi-attribute prospects, and so we have to specify the direction in which they are translation invariant (this property does not necessarily hold for all vectors in ). Similarly, we have to specify that is the target for all attributes. We refer to Charpentier (2018) and Feinstein and Rudloff (2021) for a discussion of this type of translation invariance for risk measures on . Translation invariance in the direction corresponds to translation invariance with respect to in our representation of as .

Given with RCF value , the DM’s target is . The corresponding is a monetary risk measure of target attainment and is computed by solving an LP:

where the constant

is also computed by solving an LP.

7.2 Normalizing and benchmark prospects

Suppose we want to evaluate prospects with respect to a benchmark , as in the literature on stochastic dominance (see, e.g., Dentcheva and Ruszczyński (2003, 2004) and Armbruster and Delage (2015)). We define a new preference ambiguity set

where we do not constrain the value of (we do not impose [Nor]). We then define the RCF with respect to the benchmark by:

Here, the RCF is evaluated over the worst-case shortfall with respect to the benchmark. If then is weakly preferred to by all DM’s with choice functions in .

Next define and let be a modified preference ambiguity set where is normalized to satisfy . We have the following equivalence for this construction.

Proposition 7.4.

for all .

When we want to use a benchmark , we can replace with as the normalizing prospect and set . The rest of our development is the same based on .

7.3 Preference inconsistency

In practice, the DM might make comparisons which are inconsistent with his choice function (see, e.g., Bertsimas and O’Hair (2013), Armbruster and Delage (2015), Delage and Li (2017)). We consider the effect of different forms of preference inconsistency on our robust choice model.

First suppose there is error in the evaluation of the DM’s choice function, so that is evaluated as for a disturbance . To allow for this measurement error, we can relax the pairwise comparison constraint to , where is the error tolerance for the pairwise comparison. Given a budget for the total preference inconsistency, we can replace Constraint (2g) with:

where is treated as a decision variable.

Next suppose there is error in the perception of the outcome value (see Armbruster and Delage (2015)), so is perceived as for a disturbance . If the disturbance is bounded , we can relax the preference elicitation constraints to:

Finally, we can selectively relax a proportion of the preference elicitation constraints. Suppose we only require of the comparisons to hold for (this relaxation allows for the DM to be mistaken about at most comparisons). We can introduce binary variables where if the DM is mistaken about the comparison. For a sufficient large constant , we can then replace Constraint (2g) with:

However, these constraints cause integer variables to appear in Problem (2). Furthermore, the constraint couples different prospects together and so our sorting algorithm cannot be used.

8 Numerical experiments

In this section, we report numerical experiments for two applications: a single-attribute portfolio optimization problem and a multi-attribute capital allocation problem. The LPs that appear in the sorting algorithm, and the MILP reformulation of the value problem, are all solved by Gurobi with default settings. All experiments are run using Python 3.7 and Gurobi 9.0.2 on a 64-bit Windows 10 platform with an Intel Core i7 processor and 16GM RAM.

The perceived choice function

Our method does not get to see how the DM perceives his risk preference, and so we simply assume that the DM uses a “perceived choice function” which we take to be the certainty equivalent. We use this perceived choice function to simulate the DM’s preferences, but neither the DM nor our algorithms actually get to see this choice function.

The perceived choice function is constructed as follows. Let be a continuous, strictly increasing, and concave utility function such that . When , the certainty equivalent is

| (28) |

where is the inverse of . When , we let be a vector of non-negative weights and take the certainty equivalent of the weighted sum :

| (29) |

The choice function is monotone, quasi-concave, and law invariant.

For our implementation, we use the utility function

for parameter value . We use the corresponding choice function to generate the ECDS data.

Optimizing the perceived choice function

Suppose (conceptually) that the perceived choice function is precisely identified. Then, the DM would want to maximize and solve the convex optimization problem:

since is monotone non-decreasing. Since the objective is a mixture of concave functions, it can be solved efficiently by standard algorithms. We use the optimal solution of this problem as a benchmark for the purpose of comparison with our robust choice model.

8.1 Portfolio optimization

Suppose we have assets, we want to construct a portfolio from assets . Let be the set of feasible portfolios where is the proportion of wealth allocated to asset . The vector of random return rates is , where is the return rate of asset . The overall portfolio return is , and our preference robust portfolio optimization problem is:

| (30) |

Our data consists of the quarterly return rates of exchange traded funds (ETFs) and the US central bank (FED) for 212 assets over ten years, from January 2006 to December 2016 (constructed from the daily return rate data). We work with scenarios. First, we construct the ECDS by randomly sampling a pair of assets from the entire pool of assets, and the DM’s preference in each pair of assets is determined by using the perceived choice function Eq. (28). We then randomly choose a batch of feasible assets to construct portfolios.

8.1.1 Scalability

Our first set of experiments examines the scalability of the sorting algorithm in terms of the size of the ECDS. We compare the computation time required to solve the by our sorting algorithm and by the Gurobi solver applied to the MILP reformulation. Both the sorting algorithm and Gurobi solve the problem exactly and always obtain the same optimal value. The comparisons are conducted repeatedly for five groups, where the ECDS is randomly chosen from the pool of assets for each group. Table 1 shows that when the number of ECDS pairs exceeds sixty, the sorting algorithm becomes more efficient than Gurobi.

| ECDS Pairs | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Method | Group | 10 | 20 | 30 | 40 | 50 | 60 | 70 | |

| Sorting | 1 | 1.16s | 6.60s | 26.30s | 67.00s | 142.00s | 242.00s | 380.00s | |

| 2 | 1.09s | 6.80s | 25.50s | 69.00s | 144.00s | 240.00s | 374.00s | ||

| 3 | 1.10s | 6.83s | 25.70s | 69.00s | 142.00s | 236.00s | 380.00s | ||

| 4 | 1.09s | 6.76s | 26.20s | 67.00s | 144.00s | 238.00s | 383.00s | ||

| 5 | 1.08s | 6.74s | 25.60s | 67.00s | 145.00s | 237.00s | 376.00s | ||

| Average | 1.10s | 6.75s | 25.86s | 67.80s | 143.40s | 238.60s | 378.60s | ||

| MILP | 1 | 0.77s | 4.94s | 15.95s | 28.13s | 78.75s | 281.40s | 529.63s | |

| 2 | 0.43s | 5.17s | 16.05s | 28.79s | 81.56s | 254.67s | 493.08s | ||

| 3 | 0.68s | 5.16s | 15.78s | 28.03s | 83.01s | 246.25s | 484.30s | ||

| 4 | 0.72s | 5.24s | 15.90s | 28.38s | 79.97s | 259.67s | 499.56s | ||

| 5 | 0.64s | 5.19s | 15.13s | 31.89s | 80.82s | 262.24s | 493.64s | ||

| Average | 0.65s | 5.14s | 15.76s | 29.04s | 80.82s | 260.84s | 500.04s | ||

8.1.2 Effectiveness of robust framework

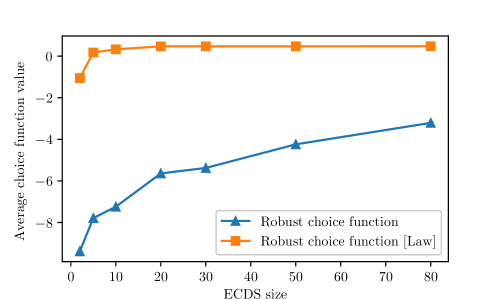

We investigate the effectiveness of our preference robust formulation by comparing the preference robust optimal solution and the “true” optimal solution with respect to the perceived choice function. We first study how the RCF value varies with increasing ECDS size. We randomly sample fifty assets , calculate the RCF value () of each asset (all normalized to the same scale), and then calculate the average. We run this experiment for several different ECDS sizes.

Figure 2 shows how the RCF gradually converges as new information is revealed. We see that RCF with [Law] will have a higher average perceived choice function value than RCF without [Law], for the same size of ECDS. This experiment indicates that if [Law] is enforced (by using ), then only a few comparisons (possibly fewer than ten ECDS pairs) are needed to make robust decisions of high quality.

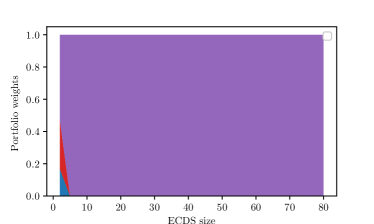

We also illustrate the relationship between the robust optimal portfolio weights and the number of ECDS pairs. In this experiment, we choose the batch size to be . The optimal portfolio always consists of a mixture of only Asset 1, Asset 4, and Asset 5.

In Figure 3, the result for the basic case without [Law] is shown in the left plot and the result with [Law] is shown in the right plot. The weight on Asset 5 is at the top (purple area), the weight on Asset 4 is in the middle (red area), and the weight on Asset 1 is on the bottom (blue area). The true optimal solution under the perceived choice function is to put all weight on Asset 5. We see that when there are more than five ECDS pairs, the law invariant model already reaches a stable solution that matches the “true” optimal solution under the perceived choice function. The model without [Law] reaches a stable solution once there are more than twenty ECDS pairs, with a small optimality gap.

In the next experiment, we compare the perceived choice function value of the optimal solutions of four different models: our RCF (base and law invariant cases), expected return, and the perceived choice function itself. In each experimental run, we randomly select twenty assets from the pool (which consists of all 212 assets) as the batch (the selected assets over which we do PRO). Then, for each instance, we calculate the perceived choice function values of the solutions proposed by PRO with and without [Law], expected return maximization, and perceived choice function maximization. We conduct 500 experimental runs and then calculate the average of the optimal choice function values, which serve as a measure of the performance of PRO. They represent how good the DM feels about the solutions proposed by an advisor using PRO.

In Figure 4, we see that the performance of PRO improves as the size of the ECDS increases. We also note that the law-invariant RCF always outperforms our basic RCF without [Law]. We conjecture that this is because the perceived choice function (certainty equivalent) is actually law-invariant. Finally, we see that the law-invariant RCF is fairly close to ground truth once the size of the ECDS is greater than ten. In this case, enforcing [Law] greatly improves the fidelity of our PRO approach with respect to the ground truth.

8.2 Capital allocation

Our next application is to scenario dependent capital allocation for a financial institution consisting of sub-units for . The overall financial institution is represented by the random vector

where we interpret each as the random revenue of sub-unit . Define

to be the set of admissible scenario-dependent financial recourse decisions subject to a budget constraint . Our problem is to maximize the RCF subject to the available budget:

| (31) |

We suppose there is a systematic risk factor common to all sub-units and an idiosyncratic risk factor specific to sub-unit . We then set the return to be (this is similar to the experimental setup in Esfahani and Kuhn (2018)). To construct ECDS for our experiments, we randomly generate samples of financial returns according to this setup. The DM’s preference for each pair of assets is determined by using the perceived choice function in Eq. (29). We randomly select the weight vector uniformly from the unit simplex, and set the budget to be .

8.2.1 Scalability

To test the scalability of our sorting algorithm, we model an institution with sub-units on scenarios. The run times of our sorting algorithm and Gurobi are presented in Table 2. As for the portfolio problem, here we also do comparisons among five groups where the ECDS is randomly generated for each group. We see the difference in required computation time between our sorting algorithm and Gurobi is more pronounced in this application compared to the portfolio optimization problem.

We next consider scalability of our law invariant sorting algorithm. Table 3 suggests that the law invariant sorting algorithm is highly scalable in terms of the number of scenarios and the number of attributes. Note that the most rapid growth in run time is in the number of ECDS pairs. This result is not surprising since the complexity of our sorting algorithm grows quadratically in the number of ECDS pairs by Theorem 4.7.

| ECDS Pairs | |||||||

|---|---|---|---|---|---|---|---|

| Method | Group | 10 | 20 | 30 | 40 | 50 | |

| Sorting | 1 | 15.6s | 97s | 364s | 841s | 1631s | |

| 2 | 13.2s | 107s | 350s | 826s | 1539s | ||

| 3 | 12.5s | 99s | 326s | 808s | 1483s | ||

| 4 | 12.6s | 107s | 342s | 823s | 1651s | ||

| 5 | 13s | 97s | 337s | 781s | 1545s | ||

| Average | 13.38s | 101.4s | 343.8s | 815.8s | 1569.8s | ||

| MILP | 1 | 7.16s | 56.13s | 185.78s | 3728.40s | 22109.66s | |

| 2 | 4.64s | 59.92s | 254.80s | 5312.21s | 31019.20s | ||

| 3 | 6.47s | 90.27s | 450.12s | 6560.72s | 38534.88s | ||

| 4 | 5.30s | 71.62s | 387.61s | 5666.33s | 36112.33s | ||

| 5 | 5.18s | 38.9s | 278.50s | 5449.45s | 32334.57s | ||

| Average | 5.75s | 69.48s | 296.90 | 5343.42s | 32022.13s | ||

| ECDS Pairs | |||||||||

| Settings | Group | 1 | 2 | 5 | 10 | 20 | 50 | 80 | |

| 20 Scen, 20 Attr | 1 | 52.9ms | 437ms | 7.19s | 52.4s | 506s | 6715s | 28284s | |

| 2 | 47.5ms | 420ms | 7.12s | 52.8s | 507s | 6822s | 30111s | ||

| 3 | 52ms | 445ms | 7.28s | 52.5s | 508s | 6720s | 27765s | ||

| 4 | 50.2ms | 440ms | 7.2s | 53s | 511s | 6669s | 28202s | ||

| 5 | 51.8ms | 444ms | 7.22s | 52.4s | 512s | 6733s | 28116s | ||

| Average | 50.88ms | 437.2ms | 7.202s | 52.62s | 508.8s | 6731.8s | 28495.6s | ||

| Number of Scenarios | |||||||||

| Settings | Group | 5 | 10 | 15 | 20 | 50 | 100 | 200 | |

| 10 Pairs, 20 Attr | 1 | 6.64s | 17s | 33.4s | 54.3s | 274s | 1141s | 4532s | |