Drift estimation of the threshold Ornstein-Uhlenbeck process from continuous and discrete observations

Abstract

We refer by threshold Ornstein-Uhlenbeck to a continuous-time threshold autoregressive process. It follows the Ornstein-Uhlenbeck dynamics when above or below a fixed level, yet at this level (threshold) its coefficients can be discontinuous. We discuss (quasi)-maximum likelihood estimation of the drift parameters, both assuming continuous and discrete time observations. In the ergodic case, we derive consistency and speed of convergence of these estimators in long time and high frequency. Based on these results, we develop a test for the presence of a threshold in the dynamics. Finally, we apply these statistical tools to short-term US interest rates modeling.

Keywords: Threshold diffusion, maximum likelihood, regime-switching, self-exciting process, interest rates, threshold Vasicek Model, multi-threshold.

AMS 2010: primary: 62M05; secondary: 62F12; 60J60.

JEL Classification: primary: C58; secondary: C22, G12.

1 Introduction

We consider the diffusion process solution to the following stochastic differential equation (SDE)

| (1.1) |

with piecewise constant volatility coefficient, possibly discontinuous at ,

| (1.2) |

and similarly piecewise affine drift coefficient

| (1.3) |

Strong existence of a unique solution to (1.1) follows from the results of Le Gall (1985). Separately on and , the process follows the Ornstein-Uhlenbeck (OU) dynamics which, in the context of interest rates modeling, is referred to as Vasicek model. Following this nomenclature, Decamps et al. (2006) refer to (1.1) as Self Exciting Threshold (SET) Vasicek model. Su and Chan (2015, 2017) refer to such model as threshold diffusion (TD) or first-order continuous-time threshold autoregressive model (see also (Tong, 1990)).

The process is ergodic as long as the drift pushes the process up when the process reaches large, negative values, and down when it reaches large, positive values. Note that if , the drift points towards when is below the threshold , if , towards when is above . We allow here a null linear part, and if we need to push the process up when very negative and if we need to push it down when very positive. From these considerations, ergodicity can be easily checked (see explicit condition (2.1) below).

We also consider, in Section B, a multi-threshold version of (1.1), where we allow for discontinuity levels . In this case, ergodicity is determined by the same conditions, to be checked on the values of the coefficients on the intervals and .

In this paper we discuss the asymptotic behavior of maximum likelihood estimators (MLE) and quasi-maximum likelihood estimators (QMLE) for the drift parameters , both from continuous and discrete time observations.

Let be the number of observations, the time horizon and the largest interval between two consecutive observations.

In the ergodic case, if and as , we prove a central limit theorem (CLT) giving the convergence of the estimators with speed to the real parameters, i.e. asymptotic normality (see Theorem 2 below). To the best of our knowledge, this is the first result of this kind for TDs (SDEs with discontinuous -drift and diffusion- coefficients).

The discontinuity in the coefficients makes it difficult to pass from discrete to continuous time observations.

Indeed, a precise analysis of the error hinges on the behavior of certain discretizations of the local time of the diffusion at the threshold.

We also

prove, for fixed time horizon,

that the discrete (Q)MLE based on equally spaced observations converges in high frequency to the continuous (Q)MLE, with speed (see Theorem 3 below).

This slow convergence of the discrete (Q)MLE to the continuous (Q)MLE follows from the slow convergence, with speed , of the discretization of the local time.

Based on these results we provide a test to decide whether a threshold is present in the dynamics. Finally we use these tools to analyze short term US interest rates.

Literature review.

Su and Chan (2015, 2017) study the asymptotic behavior of the continuous time QMLE of a TD with drift as in (1.3) and piecewise regular diffusivity. In particular, they construct a hypothesis test to decide whether the drift is affine or piecewise affine.

The estimation of the volatility parameters in (1.1) from high-frequency data is studied in (Lejay and Pigato, 2018) and the drift estimation in case in (Lejay and Pigato, 2020). In the purely linear drift case , Kutoyants (2012) studies the problem of identifying the threshold parameter and Dieker and Gao (2013) and the related stream of research consider similar models, with (so that the drift function is continuous) in a multidimensional setting. The (related) problem of drift estimation in a skew OU process is considered in (Xing et al., 2020).

In this document the coefficients are discontinuous and the behavior at hard to handle; for high-frequency observations we do so using the discretization results in (Mazzonetto, 2019). The convergence in high frequency and long time for estimators of discretely observed diffusions have been discussed e.g. in (Kessler, 1997; Ben Alaya and Kebaier, 2013; Amorino and Gloter, 2020), but to the best of our knowledge ours is the first such result in the case of discontinuous coefficients.

Yu et al. (2020) study numerically an approximate MLE (AMLE) from discrete time observations simultaneously for threshold, drift and diffusion coefficients of threshold diffusions including OU process or CIR model. They compare their AMLE with QMLE, showing numerical evidence for consistency. The recent work (Hu and Xi, 2022) considers a generalized moment estimator for a TD which is discretely observed, with fixed time lag.

Threshold autoregressive (TAR) models in discrete time were introduced by H. Tong in the early 1980s (Tong, 1983, 2011, 2015). Within this class, self-exciting TAR (SETAR) models rely on a spatial segmentation, with a change in the dynamics according to the position of the process, below or above a threshold, and can be seen as a discrete analogue to the TD. We refer to (Chan, 1993; Rabemananjara and Zakoian, 1993; Yadav et al., 1994; Brockwell and Williams, 1997; Chen et al., 2011) and references therein for this class of econometric models and related inference problems.

Diffusion processes have been widely used to model interest rate dynamics, celebrated classical examples being (Vasicek, 1977; Cox et al., 1985; Hull and White, 1990; Black and Karasinski, 1991). These models are designed to capture the fact that interest rates are typically mean reverting, see (Wu and Zhang, 1996). However, non linear effects (e.g. multi-modality) are not captured by these models. Ait-Sahalia (1996) shows that mean-reversion for interest rates is strong outside a middle region, suggesting the existence of a target band. This is similar to what is observed in exchange rates (Krugman, 1991) and explainable with policy adjustments in response to changes in such rates. There is evidence for a “normal” low-mean regime and an “exceptional” high-mean regime, and in general for bi-modality (or even multi-modality) in interest rate dynamics, that one can model using TD (1.3). In general, non-linearities and regime changes in short-term interest rates have been widely documented, and several threshold models have been proposed both in discrete and continuous time, see (Gray, 1996; Pfann et al., 1996; Ang and Bekaert, 2002a, b; Kalimipalli and Susmel, 2004; Gospodinov, 2005; Ang et al., 2008; Archontakis and Lemke, 2008a, b). We refer to (Decamps et al., 2006) and bibliography therein for a thorough discussion of SET diffusions in interest rate modeling. In recent years TDs have been used in several aspects of financial modeling, such as option pricing (Lipton and Sepp, 2011; Gairat and Shcherbakov, 2016; Dong and Wong, 2017; Lipton, 2018; Pigato, 2019) and time series modeling (Ang and Timmermann, 2012; Lejay and Pigato, 2019). TD models for interest rates have been considered in (Pai and Pedersen, 1999; Decamps et al., 2006; Su and Chan, 2015, 2017). In this paper, we focus on (Q)MLE estimation of such models, and in particular on inference from high frequency observations and their convergence to continuous time estimators, as well as their convergence in long time to real values of the parameters.

Outline.

In Section 2 we present our main results on convergence of drift estimators for threshold OU. In Section 3 we implement the estimators, discuss threshold estimation and testing and work with US interest rates data. Proofs are collected in Section A and in Section B we discuss an extension to a multi-threshold setting.

2 (Quasi) maximum likelihood estimation

Let be the process strong solution to (1.1) where is a Brownian motion and is independent of (e.g., is deterministic).

We see in next equation (A.1) that is ergodic if

| (2.1) |

2.1 Maximum and quasi-maximum likelihood estimator from continuous time observations

We assume in this section to observe the process on the time interval , . For and , we define

| (2.2) |

and take as likelihood function the Girsanov weight

| (2.3) |

We also consider a quasi-likelihood defined as in (Su and Chan, 2015) as

| (2.4) |

Theorem 1.

Let .

-

i)

For every the MLE and QMLE are given by

(2.5)

Assume now that the process is ergodic.

-

ii)

The following law of large numbers (LLN) holds: i.e., the estimator is consistent.

-

iii)

The following CLT holds: where and are two independent, independent of , two-dimensional Gaussian random variables with covariance matrices respectively and where

(2.6) and are real constants such that (explicit expressions for such constants are given in next Lemma 2; more details on stable convergence can be found in Remark 1 below).

-

iv)

The local asymptotic normality (LAN) property (see Le Cam and Yang (2000)) holds for the likelihood evaluated at the true parameter with rate of convergence and asymptotic Fisher information

This means that there exists a random vector such that for all small perturbations it holds that the quantity

(2.7) converges to 0 in probability as .

Remark 1.

The notion of stable convergence was introduced by Rényi (1963). We refer to (Jacod and Shiryaev, 2003) or (Jacod and Protter, 2012) for a detailed exposition. In this document we just mention that this notion of convergence is stronger than convergence in law, but weaker than convergence in probability. We use in this paper the following crucial property: for random variables , (), and ,

| (2.8) |

2.2 Drift estimation from discrete observations

We assume in this section to observe the process on the discrete time grid , for , , and set . We define with .

The discrete versions of (2.2) are defined as follows: for and , let

| (2.9) |

We refer with discretized likelihood (corresponding to (2.3)) to

and with discretized quasi-likelihood (corresponding to (2.4)) to

For , , let

| (2.10) |

Theorem 2.

Let be a sequence in . For all , let above be , let be defined as in (2.10).

-

i)

For every the vector maximizes both the likelihood and the quasi-likelihood .

Assume now that the process is ergodic, i.e., (2.1) is satisfied, and that is the stationary solution to (1.1), i.e., follows the stationary distribution (cf. (A.2)). Moreover, assume

Remark 2.

If the largest time lag the conditions in Theorem 2 become and for consistency and and for asymptotic normality.

The next result states that, for fixed time horizon, in high frequency, the estimator from discrete observations converges, with an “anomalous” speed, towards the estimator from continuous observations. Let be a semi-martingale, let , and let . Then we recall that

| (2.11) |

is the symmetric local time of at , up to time .

Theorem 3.

Remark 3.

The right hand side of (2.12) has the same law as

Remark 4.

One usually expects such discretizations to converge with speed . In this case, the lower speed of convergence is due to the discontinuity in the coefficients, and appears in connection with the local time. Indeed, the asymptotic behavior of the estimators is intrinsically related to the one of the local time of the process at the threshold. More precisely the difference , can be rewritten involving terms , where is the following approximation of the local time from discrete time observations

| (2.13) |

for (see equation (A.13) for a more precise statement).

Remark 5 (The skew OU process).

Let us consider the solution to the following SDE involving the local time

| (2.14) |

with and piecewise constant functions , , possibly discontinuous at the threshold , as in (1.2) and (1.3).

Xing et al. (2020) assume and known and consider drift parameters estimation for , based on discrete observations, in the case of constant coefficients and local time at . In this setting, is referred to as “skew OU process” (see also (Feng, 2016)).

Consider now the more general case of as in (1.2) and (1.3). If we assume that only is known, all the results in Section 2 on drift estimation for hold similarly for drift estimation of . This follows from the fact that a simple transformation allows us to reduce the skew OU to a threshold OU with threshold at , getting rid of the local time in the dynamics.

Remark 6 (The threshold CIR process).

Su and Chan (2015, 2017) and Yu et al. (2020) consider diffusion processes with drift as in (1.3), with more flexibility on the diffusion coefficient , so that their analysis also applies to the process as in (1.1) with

| (2.15) |

We refer here to this process by threshold CIR (Cox-Ingersoll-Ross). In these works, the proposed estimators are always QMLE, maximising (2.4), that does not depend on the diffusivity . Here, with our (more restrictive) piecewise-constant choice for the diffusivity, we are able to show that the considered estimator is a genuine MLE. In our setting, we expect a result analogous to Theorem 1 to apply to the QMLE for the threshold CIR as well, but with a less explicit limit Gaussian law in the CLT, cf. also (Su and Chan, 2015). On the other hand, the proof of the discrete time Theorem 2 makes use of bounds on hitting times for the OU process. The corresponding result for the threshold CIR process does not seem to be a trivial extension.

3 Threshold estimation, testing and interest rates

We simulate the threshold OU process using the Euler scheme (Bokil et al., 2020) (an alternative approach for simulation consists in discretizing space instead of time, cf. (Ding et al., 2020)) and use the estimator based on discrete observations. The implementation has been done using R. Parameters are as in Table 1.

In Table 2 we show mean, standard deviation and mean squared error of the estimators on simulated trajectories.

| parameter | ||||

|---|---|---|---|---|

| mean | ||||

| MSE | ||||

| simulated sd | ||||

| predicted sd |

In Figure 2 we see an example of the convergence in Theorem 3, using that (2.12) can be rewritten as

| (3.1) |

To estimate the local time and the occupation times , we use the discrete time approximations in (2.13) and (2.9).

If we want to simulate a stationary version of process (1.1), we can simulate using explicit stationary density (A.2) or running the process until large time and then using the r.v. as initial condition. In Figure 3 we compare the empirical distribution obtained in this way with the theoretical stationary density. This constitutes an example of bi-modal stationary distribution (density) with two peaks, corresponding to the two different mean reversion levels.

3.1 On threshold estimation

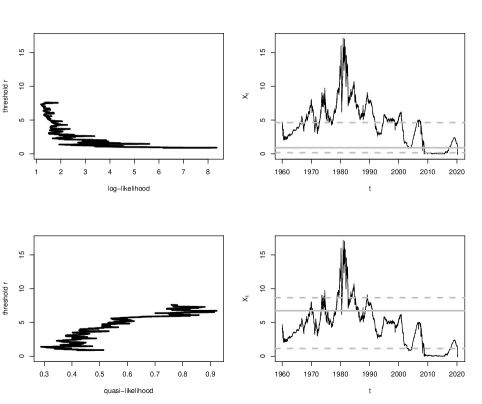

The estimation results in Section 2 suppose the previous knowledge of the threshold. In practice, this assumption is not realistic and the threshold has to be estimated as well. In (Su and Chan, 2015), threshold QMLE from continuous observations is shown to be -consistent. We implement here also the analogous threshold MLE, and we directly consider discrete observations starting from the convergence results in Theorem 2.

Given discrete observations of one trajectory up to time , we proceed as follows. First, for a given threshold , we compute (Q)MLE , and denote this estimator . For each fixed , we can then compute the quasi-likelihood function . We can also compute the likelihood function , after estimating using the quadratic variation estimators in (Lejay and Pigato, 2018). We take to be the -percentile and the percentile of the observed data (in the implementation we always take and vary on a discrete grid). Maximizing now the (quasi-)likelihood function over we obtain the (Q)MLE of the threshold, . The estimator of all the drift parameters is then .

We display a sample trajectory in Figure 4, together with the threshold estimated on that trajectory and mean reversion levels.

| parameter | |||||||

|---|---|---|---|---|---|---|---|

| (Q)MLE | |||||||

| sd |

Note that MLE and QMLE give the same parameter estimates once the threshold is fixed (Theorem 2.(i)). However, when maximizing also over the choice of the threshold, the MLE can also account of a possible change in the volatility, and this may give a different choice of the threshold. The model with different volatilities (SET Vasicek) is used by Decamps et al. (2006). Su and Chan (2015, 2017) use the QMLE, so their drift estimator does not account of possible changes in the volatility.

3.2 Testing for threshold

We aim to test the presence of a threshold in the diffusion dynamics. Su and Chan (2017) propose a test for the presence of a threshold based on quasi-likelihood ratio. Here, we derive a test from the CLT in Theorem 2.(iii); therefore, we suppose that its assumptions are satisfied. Moreover, we assume that the threshold parameter is given. In applications, a natural choice for will be the (Q)MLE . With fixed threshold, we can estimate the drift parameters obtaining . From Theorem 2.(iii), if goes to 0 as ,

| (3.2) |

which is a centered Gaussian vector with covariance matrix given by , invertible from Cauchy-Schwarz inequality. The inverse matrix can be expressed as a function of and . Note that can be estimated from one observed trajectory using quadratic variation as in (Lejay and Pigato, 2018) and can be estimated computing as Riemann sums on the observed trajectory, from (2.6). We denote the estimate of obtained from these estimations.

To test for the presence of a threshold in the drift we consider hypothesis

Under the null hypothesis the statistics

converges to a distribution with 2 degrees of freedom. We reject if the statistics is larger than , where is the quantile of a distribution with two degrees of freedom such that .

To conclude, note that (3.2) similarly allows to test separately the presence of a threshold in or in , i.e. testing for the presence of a discontinuity in the piecewise linear or in the piecewise constant part of the drift.

3.3 Interest rate analysis

We consider the 3 months US Treasury Bill rate, time series of daily closing rate on period Jan 04, 1960 - Apr 29, 2020 (source: Yahoo Finance). We perform quasi-maximum and maximum likelihood estimation using (2.10), adopting the convention that the “daily” time interval is months, while one month is the time unit. The number of observations is , whereas years. We choose as percentile for the search of the threshold . We report both our MLE and QMLE parameters.

We see in Figure 5 (bottom) that in the case of QMLE our result is consistent with the one in (Su and Chan, 2015), so that the estimation identifies two regimes. One is low rates, with negligible drift, so that in this regime the process is almost a martingale. In the high regime, a stronger reversion to lower rates is ensured by the drift when the rates are very high. When - in Figure 5 (top) - we use MLE (with estimated using quadratic variation), the estimation identifies a low regime corresponding to the period of extremely low rates, with minimal fluctuations, that followed the 2007-2008 financial crisis, whereas almost all the rest of the time series is in the high regime. Volatilities thus estimated are in the low regime, in the high regime. To compute standard deviations of these estimates we apply (Lejay and Pigato, 2018, Corollary 3.8.), in the form of (Lejay and Pigato, 2019, Proposition 3.1), with the same justification as after (Lejay and Pigato, 2019, Proposition 3.1). We get that the standard deviation is for and for . With this MLE for the drift, the mean reverting effect looks non-negligible both above and below the threshold. We note that parameter estimates obtained trough MLE and QMLE are substantially different. This is due to the different choice of the threshold, that in the QMLE does not depend on the behaviour of the volatility, while the MLE is influenced by the volatility as well. For this reason, when using the MLE, one of the two regimes isolated by the threshold only consists of the period of extremely low and stable rates that followed the 2008 financial crisis.

| parameter | |||||||

|---|---|---|---|---|---|---|---|

| MLE | |||||||

| MLE sd | |||||||

| QMLE | |||||||

| QMLE sd |

and corresponding standard deviation for and according to Theorem 2

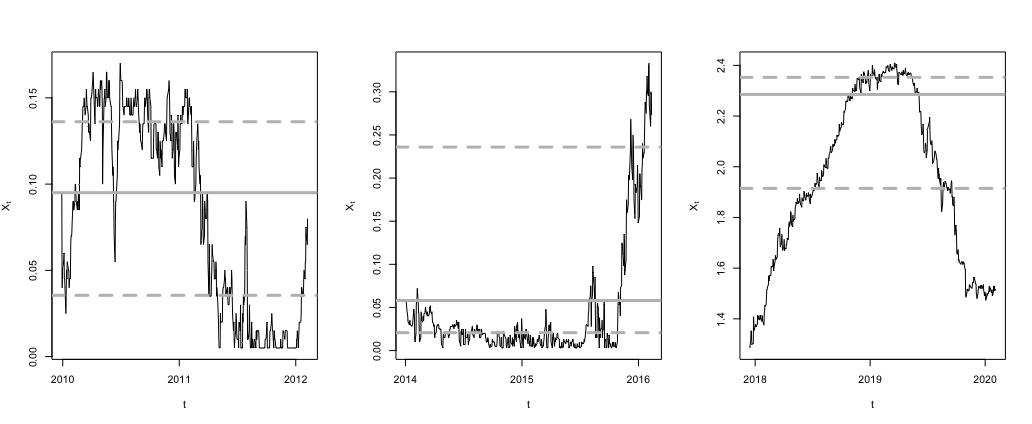

In this analysis, following Su and Chan (2015, 2017), we estimated our model parameters on the whole period 1960-2020. From an econometric perspective, it is natural to wonder whether it is reasonable to assume the stationarity of the process on such a long time interval. To address this issue, we consider within the period 2010-2020 five two-years time windows, with daily observations as before. With this choice, , and therefore we expect from Theorem 2 that the discretization error should be negligible, assuming that years is large enough for the theorem to apply.

With significance level, only in the subperiod Jan 2018-Dec 2019 the hypothesis (absence of a threshold in the parameters) is not rejected. In all other time windows (2010-2011, 2012-2013, 2014-2015, 2016-2017) we conclude that a threshold is present. In Figure 6 we see three examples of estimation in such windows. In order to check whether such test is reliable on time series with such sample sizes, we tried the same procedure (selection of threshold and successive test with significance level) on simulated time series with parameters and sample sizes of the same order as the estimated ones. We found that when there is no threshold present (constant parameters) is rejected of the times, when the threshold is present (non-constant parameters) is rejected of the times, which seems to confirm the validity of the procedure, even in these smaller time windows.

Appendix A Proofs

A.1 The regimes of the process

In this section, we establish for which values of the coefficients the process is (positively or null) recurrent or transient.

Since is a one-dimensional diffusion it is characterized by two quantities: scale function and speed measure.

is recurrent if and only if and , otherwise it is transient. Moreover a recurrent process is positive recurrent if the speed measure is a finite measure, otherwise null recurrent.

The scale density is continuous, unique up to a multiplicative constant, and its derivative satisfies . It follows that is recurrent if and only if [( and ) or ( and )] and [( and ) or ( and )]. The complementary leads to transience.

The density of the speed measure with respect to the Lebesgue measure is given by It is discontinuous if and only if is so. Assume is recurrent. The speed measure is a finite measure, and so is positive recurrent, if and only if

| (A.1) |

See Lemma 1 below. In these cases, the process is actually ergodic and the stationary distribution is equal to the renormalized speed measure:

| (A.2) |

Lemma 1.

Let and let

| (A.3) |

Then

Lemma 2.

Assume the process is ergodic. Let , given by (A.3), , , and be the stationary distribution. For all let be the constant such that . We have the following explicit formulas:

-

•

if , , then

-

•

if , , , then

-

•

, , , then

-

•

, , , then

A.2 Proof of Theorem 1

Proof of Item (i) of Theorem 1.

Let . It holds that

| (A.4) |

To find the maximum we compute the derivatives with respect to and observe that the gradient has a unique singular point given by (2.5) and the Hessian is negative definite.

Moreover the fact that and shows that the MLE for the drift parameters will be the same as the QMLE, i.e. (2.5). ∎

In order to study the asymptotic behavior of the estimator we introduce a different expression for the estimators in (2.5) based on the following notation. Given , let

with , . Observe that (1.1) yields for :

| (A.5) |

Moreover, , , and .

Lemma 3.

Let . The MLE and QMLE can be expressed as

| (A.6) |

that can be rewritten as

| (A.7) |

Proof.

A.3 Proof of Theorem 2

The proof of Item (i) of Theorem 2 is analogous to the proof of Item (i) of Theorem 1, therefore omitted. The proof of Items (ii)-(iii) of Theorem 2 follows from Lemma 4 below. Let us be more precise. For all it holds

The second term of the sum is handled with Theorem 1 (more precisely Item (iii)) providing the desired limit distribution. The first instead can be rewritten, using equations (2.5) and (2.10), as an expression which involves only terms of the kind

for , ,

Combining Lemma 4 with Lemma 2 and Theorem 2.2 in (Crimaldi and Pratelli, 2005) ensures, the consistency of the estimator if as , and if as then it implies also that

Lemma 4.

Proof.

Without loss of generality, we reduce to prove the statement for threshold . Indeed the quantities and for the process (with threshold ) can be written as linear combination (coefficients depending on and ) of the same quantities for the process (which solves (1.1) with threshold at and new drift coefficients and ). We keep denoting as (instead of ) and the drift coefficients. In this proof we use the round ground notation for . Moreover, without loss of generality, we assume for all .

Let us first note that for :

therefore

Analogously, observe that for it holds

Let us rewrite the integrand as

Triangular inequality, Hölder’s inequality, and Itô-isometry imply that

Step 1. Given and we show that for every there exists a constant depending only on such that

| (A.10) |

Let then

where a Wiener process independent of . So, given , is an OU with threshold (since has threshold 0). Now, e.g. (Hudde et al., 2021, Corollary 2.5) applied to implies (A.10).

Step 2. (Proof of (A.8)). Since is distributed as the stationary distribution then This, the tower property, and (A.10) imply that there exists depending only on such that

Step 3. (Proof of (A.9)). Let be fixed such that . Let us first note that we just need to consider . This, given , is bounded by where is the first hitting time of the level 0 of the OU process solution to the following SDE: with a Brownian motion independent of . If , (Lipton and Kaushansky, 2020, Section 6.2.1) with , , and , prove that

If and then

Therefore, using the stationary distribution (A.2), to establish Step 3 it suffices to prove that the following quantity vanishes as :

Let us first consider the case and . The desired quantity is bounded by

for constants depending on . Let us now consider the case and . The desired quantity is bounded by

for constants depending on . The latter term vanishes since The proof is thus completed. ∎

A.4 Proof of Theorem 3

The proof of Item (i) of Theorem 3 is along the lines of the one of Theorem 2.(i).

The proof of Item (ii) of Theorem 3 is based on Lemma 5 and Lemma 6 below.

Let us be more precise.

For all and the difference

can be rewritten, using Theorem 1.(i) and Theorem 3.(i), as an expression involving only terms of the kind

for , . The convergence is obtained combining Lemma 2 and Theorem 2.2 in (Crimaldi and Pratelli, 2005) with the convergences in probability in Lemma 5 and Lemma 6 below. The proof of (2.12) relies on Lemma 2, Theorem 2.2 in (Crimaldi and Pratelli, 2005) Lemma 6 and equation (A.11) in Lemma 5.

Lemma 5.

Let . Then and

| (A.11) |

where is a Brownian motion independent of .

Lemma 6.

Let .

Then

Moreover, if the threshold , then

for every .

The latter convergence result extends (Lejay and Pigato, 2018, Theorem 4.14), where only is considered. The proof strategies are the same.

A.4.1 Proof of Lemma 5

Without loss of generality we can assume deterministic and also reduce ourselves to prove all results of the section in the case of null drift, i.e. is an oscillating Brownian motion (OBM). Indeed all statements are about convergence in probability or stable convergence, and, once these convergences have been proved for the null drift case, they can be extended to the drifted case (piecewise linear drift) using the fact that Girsanov weight is an exponential martingale and dominated convergence theorem. In the case of convergence in probability one proves that for every sub-sequence there exists a sub-sub-sequence converging a.s., instead stable convergence follows by property (2.8) and Skorokhod representation theorem.

Therefore, in the remainder of the section, let be an OBM with deterministic starting point and let be fixed.

Lemma 7.

It holds that

Proof of Lemma 7.

We write , , and . Moreover we can assume (just note that given with threshold , has threshold and , ).

We observe that

Proposition 2 in Mazzonetto (2019) (or (Lejay et al., 2019, Proposition 2)) ensures that

Now consider the remaining term. In (Lejay and Pigato, 2018) (cf. proof of Theorem 3.5, page 3594) it is shown that there exists a constant such that

where is a Brownian motion independent of . Using (2.8) completes the proof. ∎

We are now ready to prove Lemma 5.

Proof of Lemma 5.

Let denote positive and negative part. Note that for all it holds -a.s. that . Applying Itô-Tanaka formula establishes that the following equalities hold -a.s.:

| (A.12) |

for . Next note that it holds -a.s. for all that

and

Combining this with (2.13) and (A.12) imply that it holds -a.s. that

| (A.13) |

The result follows from (Mazzonetto, 2019, Proposition 7), Lemma 7, and from the following convergence:

which follows from (Mazzonetto, 2019, Proposition 2) or (Lejay et al., 2019, Proposition 2). ∎

A.4.2 Proof of Lemma 6

As in the previous section, let be an OBM with deterministic starting point and let be fixed. We reduce to consider threshold because for it holds that and the same holds for .

The following result follows from Lemma 4.3 in (Lejay and Pigato, 2018) and the scaling property for OBM.

Lemma 8.

Let be a bounded function such that for . Then for all

| (A.14) |

where .

Let us denote by the natural filtration associated to the process (or equivalently to its driving BM). Let be fixed. For , we consider , , and

| (A.15) |

Observe that are martingale increments and

The following lemma proves the convergence of the two terms.

Lemma 9.

Let , , and let , and , defined by (A.15). Then

-

i)

and

-

ii)

Proof of Lemma 9.

In this proof we use the following notation: For every let , , be the real functions satisfying

with , , and

Let us show that the functions above satisfy the assumptions of Lemma 8. Indeed, since , it holds

This ensures that the coefficients (defined in (A.14)) , are finite. Moreover it can be shown that for . In particular note that

Hence Lemma 8 shows for all , , that

| (A.16) |

Let us first show an easy useful equality, which uses the explicit expression of the transition density of the OBM

| (A.17) |

Let be an OBM with starting point and threshold , then for all , , Fubini, (A.17), a change of variable yield

| (A.18) |

Let us now prove Item (i).

First step. Let be fixed.

We prove in this step that

| (A.19) |

Note that the Markov’s property and (A.18) ensure that

| (A.20) |

This vanishes because equation (A.16) holds and and when it holds . The proof of (A.19) is thus completed.

Second step. Let . We prove now that

| (A.21) |

By the Markov property, a simple change of variable, Fubini, and the explicit expression of the transition density of the OBM in (A.17) we obtain for all

Combining (A.16) with the fact that and it follows that the latter quantity converges in probability to with the speed which proves (A.21). Taking establishes Item (i).

Third step. (Proof of Item (ii)). Note that Jensen’s inequality implies that

This and (A.21) with ensure that it suffices to prove

By the Markov’s property and (A.18) we reduce to study the convergence of

It follows from (A.16) that the latter quantity converges to 0 in probability as . We have therefore obtained that

Applying Theorem 4.4 in (Lejay and Pigato, 2018) completes the proof. ∎

Appendix B The multi-threshold Ornstein-Uhlenbeck process

Let us consider in this section the multi-threshold version of the threshold OU process, by which we mean the solution to

| (B.1) |

with piecewise constant coefficients , , and possibly discontinuous at levels , . Let and , for . The volatility coefficient is given by

| (B.2) |

and similarly the drift coefficients are given by

| (B.3) |

In analogy to the result for we also denote by and by .

B.1 The regimes of the process

In this section, we establish for which values of the coefficients the process is (positively or null) recurrent or transient. Recall that we denote scale function and speed measure respectively by and . The derivative (up to a multiplicative constant) of the scale function satisfies for all and

where for all , we define the functions

The speed measure is .

Recall that is recurrent if and only if and , which happens if and only if [( and ) or ( and )] and [( and ) or ( and )]. The complementary leads to transience. If is recurrent and the speed measure is a finite measure, then is positive recurrent and ergodic. It admits a stationary distribution, denoted by , which is the renormalized speed measure. Hence we have the ergodicity condition (A.1) (the one for the single threshold case ).

B.2 MLE and QMLE from continuous time observations

We assume in this section to observe the process on the time interval , . For , , and we define

| (B.4) |

and take as likelihood function and as quasi-likelihood defined as in Section 2.

Lemma 11 (Multi-threshold version of Lemma 2).

Assume the process is ergodic: condition (A.1) holds. Then, for all , , the quantities defined as follows are finite constants:

Theorem 4.

-

i)

For every the MLE and QMLE are given by with

(B.5)

Assume now that the process is ergodic (i.e., (A.1) is satisfied).

-

ii)

The following LLN holds, i.e., the estimator is (strongly) consistent:

-

iii)

The following CLT holds:

where , are independent, independent of , two-dimensional Gaussian random variables with covariance matrices respectively and where

(B.6) and are real constants such that .

-

iv)

The LAN property holds for the likelihood evaluated at the true parameters with rate of convergence : there exists a random vector such that for small perturbations it holds that

converges to in probability as . The matrix is the asymptotic Fisher information

In order to study the asymptotic behavior of the estimator, we introduce a different expression for the estimators in (B.5) based on the following notation. Given , , and let

Observe that (B.1) yields for , :

| (B.7) |

Note that is -a.s. positive by Cauchy-Schwarz. By (B.7), we have the following reformulation of (B.5).

Lemma 12 (Multi-threshold version of Lemma 3).

B.3 Drift estimation from discrete observations

We assume now to observe the process on the discrete time grid , for , , and set . We define with .

The discrete versions of (B.4) are defined as follows: for , let

| (B.10) |

The discretized likelihood and the discretized quasi-likelihood are defined as in Section 2.

For and let with

| (B.11) |

Theorem 5.

Let be a sequence in . For all let be defined as in (B.11).

-

i)

For every the vector maximizes both the likelihood and the quasi-likelihood .

Assume that the process is ergodic and that follows the stationary distribution . Moreover, assume

-

ii)

The following LLN holds: (the estimator is consistent).

- iii)

-

iv)

If , the analogous of the LAN property holds for the discretized likelihood evaluated at the true parameters with rate of convergence and asymptotic Fisher information as in Theorem 4.

B.4 Proof of Theorem 5

Analogously to the case , the main ingredient of the proof is the following lemma.

Lemma 13 (Multi-threshold version of Lemma 4).

Before providing the proof of Lemma 13, we show how it intervenes in the proof of Items (ii)-(iii) of Theorem 5. For all

The second term of the sum is handled with Theorem 4 (more precisely Item (iii)) providing the desired limit distribution. The first instead can be rewritten, using equations (B.5) and (B.11), as an expression which involves only terms of the kind

for , , .

Combining Lemma 13 with Lemma 11 and Theorem 2.2 in (Crimaldi and Pratelli, 2005) ensures the consistency of the estimator if as , and if as then it implies also that

Proof of Lemma 13.

The proof is similar to the one of Lemma 4. We provide here the main idea of the key step, that is the proof of the analogous of (A.9): for all ,

| (B.12) |

We reduce to compute, given for , the probability that the first exit time of a standard Brownian motion from a suitable symmetric interval is smaller than : . Indeed starting from for some , at a suitable distance from the boundary of , if the Brownian motion driving the OU process does not exit in small time a suitable interval then the OU of parameters stays in because the drift is small. More precisely if let , let such that , and let

Note that . If , then is the first exit time of a Brownian motion from the interval . Moreover for it holds that is increasing, and

and so .

Then using that for every , it holds , we split the integrals into two parts to deal with in two different ways.

Note that

Therefore for big, since is small, the latter quantity goes like and it is .

The other integral satisfies:

Let , , and let denote the invariant measure, then

where the constant may change from line to line and is the length of the interval. For big enough , , , hence the latter integral is bounded from above by

where the constant may change from line to line. Thus, for some positive constant it holds that

and it is . The proof is thus completed. ∎

References

- Ait-Sahalia [1996] Y. Ait-Sahalia. Testing Continuous-Time Models of the Spot Interest Rate. The Review of Financial Studies, 9(2):385–426, 1996.

- Amorino and Gloter [2020] C. Amorino and A. Gloter. Contrast function estimation for the drift parameter of ergodic jump diffusion process. Scandinavian Journal of Statistics, 47(2):279–346, 2020.

- Ang and Bekaert [2002a] A. Ang and G. Bekaert. Regime Switches in Interest Rates. Journal of Business & Economic Statistics, 20(2):163–182, 2002a.

- Ang and Bekaert [2002b] A. Ang and G. Bekaert. Short rate nonlinearities and regime switches. Journal of Economic Dynamics and Control, 26(7):1243 – 1274, 2002b. Finance.

- Ang and Timmermann [2012] A. Ang and A. Timmermann. Regime Changes and Financial Markets. Annual Review of Financial Economics, 4:313–337, 2012.

- Ang et al. [2008] A. Ang, G. Bekaert, and M. Wei. The Term Structure of Real Rates and Expected Inflation. The Journal of Finance, 63(2):797–849, 2008.

- Archontakis and Lemke [2008a] T. Archontakis and W. Lemke. Bond pricing when the short-term interest rate follows a threshold process. Quantitative Finance, 8(8):811–822, 2008a.

- Archontakis and Lemke [2008b] T. Archontakis and W. Lemke. Threshold Dynamics of Short-term Interest Rates: Empirical Evidence and Implications for the Term Structure. Economic Notes, 37(1):75–117, 2008b.

- Ben Alaya and Kebaier [2013] M. Ben Alaya and A. Kebaier. Asymptotic Behavior of the Maximum Likelihood Estimator for Ergodic and Nonergodic Square-Root Diffusions. Stochastic Analysis and Applications, 31(4):552–573, 2013.

- Black and Karasinski [1991] F. Black and P. Karasinski. Bond and Option Pricing When Short Rates Are Lognormal. Financial Analysts Journal, 47(4):52–59, 1991.

- Bokil et al. [2020] V. Bokil, N. Gibson, S. Nguyen, E. Thomann, and E. Waymire. An Euler-Maruyama method for diffusion equations with discontinuous coefficients and a family of interface conditions. Journal of Computational and Applied Mathematics, 368:112545, 2020.

- Brockwell and Williams [1997] P. J. Brockwell and R. J. Williams. On the Existence and Application of Continuous-Time Threshold Autoregressions of Order Two. Advances in Applied Probability, 29(1):205–227, 1997.

- Chan [1993] K. S. Chan. Consistency and Limiting Distribution of the Least Squares Estimator of a Threshold Autoregressive Model. Ann. Statist., 21(1):520–533, 03 1993.

- Chen et al. [2011] C. W. S. Chen, M. K. P. So, and F.-C. Liu. A review of threshold time series models in finance. Statistics and its Interface, 4(2):167–181, 2011.

- Cox et al. [1985] J. C. Cox, J. E. Ingersoll, and S. A. Ross. An Intertemporal General Equilibrium Model of Asset Prices. Econometrica, 53(2):363–384, 1985.

- Crimaldi and Pratelli [2005] I. Crimaldi and L. Pratelli. Convergence results for multivariate martingales. Stochastic Process. Appl., 115(4):571–577, 2005.

- Decamps et al. [2006] M. Decamps, M. Goovaerts, and W. Schoutens. Self exciting threshold interest rates models. Int. J. Theor. Appl. Finance, 9(7):1093–1122, 2006.

- Dieker and Gao [2013] A. B. Dieker and X. Gao. Positive recurrence of piecewise Ornstein-Uhlenbeck processes and common quadratic Lyapunov functions. Ann. Appl. Probab., 23(4):1291–1317, 08 2013.

- Ding et al. [2020] K. Ding, Z. Cui, and Y. Wang. A Markov chain approximation scheme for option pricing under skew diffusions. Quantitative Finance, pages 1–20, 2020.

- Dong and Wong [2017] F. Dong and H. Y. Wong. Variance Swaps under the Threshold Ornstein-Uhlenbeck Model. Appl. Stoch. Model. Bus. Ind., 33(5):507–521, Sept. 2017.

- Feng [2016] A. Feng. Parameter Estimations for Skew Ornstein-Uhlenbeck Processes. International Journal of Science and Research (IJSR), pages 1776–1781, June 2016.

- Gairat and Shcherbakov [2016] A. Gairat and V. Shcherbakov. Density of skew Brownian motion and its functionals with application in finance. Mathematical Finance, 26(4):1069–1088, 2016.

- Gospodinov [2005] N. Gospodinov. Testing For Threshold Nonlinearity in Short-Term Interest Rates. Journal of Financial Econometrics, 3(3):344–371, 07 2005.

- Gray [1996] S. F. Gray. Modeling the conditional distribution of interest rates as a regime-switching process. Journal of Financial Economics, 42(1):27 – 62, 1996.

- Hu and Xi [2022] Y. Hu and Y. Xi. Parameter estimation for threshold Ornstein-Uhlenbeck processes from discrete observations. Journal of Computational and Applied Mathematics, 411:114264, 2022. ISSN 0377-0427. doi: https://doi.org/10.1016/j.cam.2022.114264. URL https://www.sciencedirect.com/science/article/pii/S037704272200108X.

- Hudde et al. [2021] A. Hudde, M. Hutzenthaler, and S. Mazzonetto. A stochastic Gronwall inequality and applications to moments, strong completeness, strong local Lipschitz continuity, and perturbations. Annales de l’Institut Henri Poincaré, Probabilités et Statistiques, 57(2):603 – 626, 2021. doi: 10.1214/20-AIHP1064. URL https://doi.org/10.1214/20-AIHP1064.

- Hull and White [1990] J. Hull and A. White. Pricing Interest-Rate-Derivative Securities. Review of Financial Studies, 3(4):573–92, 1990.

- Jacod and Protter [2012] J. Jacod and P. Protter. Discretization of processes, volume 67 of Stochastic Modelling and Applied Probability. Springer, Heidelberg, 2012.

- Jacod and Shiryaev [2003] J. Jacod and A. N. Shiryaev. Limit theorems for stochastic processes, volume 288 of Grundlehren der Mathematischen Wissenschaften. Springer-Verlag, Berlin, second edition, 2003.

- Kalimipalli and Susmel [2004] M. Kalimipalli and R. Susmel. Regime-switching stochastic volatility and short-term interest rates. Journal of Empirical Finance, 11(3):309 – 329, 2004.

- Kessler [1997] M. Kessler. Estimation of an Ergodic Diffusion from Discrete Observations. Scandinavian Journal of Statistics, 24(2):211–229, 1997.

- Krugman [1991] P. R. Krugman. Target zones and exchange rate dynamics. The Quarterly Journal of Economics, 106(3):669–682, 1991.

- Kutoyants [2012] Y. A. Kutoyants. On identification of the threshold diffusion processes. Ann. Inst. Statist. Math., 64(2):383–413, 2012.

- Le Cam and Yang [2000] L. Le Cam and G. L. Yang. Asymptotics in statistics. Springer Series in Statistics. Springer-Verlag, New York, second edition, 2000.

- Le Gall [1985] J.-F. Le Gall. One-dimensional stochastic differential equations involving the local times of the unknown process. Stochastic Analysis. Lecture Notes Math., 1095:51–82, 1985.

- Lejay and Pigato [2018] A. Lejay and P. Pigato. Statistical estimation of the Oscillating Brownian Motion. Bernoulli, 24(4B):3568–3602, 2018. doi: 10.3150/17-BEJ969.

- Lejay and Pigato [2019] A. Lejay and P. Pigato. A threshold model for local volatility: evidence of leverage and mean reversion effects on historical data. International Journal of Theoretical and Applied Finance, 22(4), 2019.

- Lejay and Pigato [2020] A. Lejay and P. Pigato. Maximum likelihood drift estimation for a threshold diffusion. Scandinavian Journal of Statistics, 47(3):609–637, 2020.

- Lejay et al. [2019] A. Lejay, E. Mordecki, and S. Torres. Two consistent estimators for the Skew Brownian motion. ESAIM: Probability and Statistics, 23:567–583, 2019.

- Lépingle [1995] D. Lépingle. Euler scheme for reflected stochastic differential equations. Math. Comput. Simulation, 38(1-3):119–126, 1995. Probabilités numériques (Paris, 1992).

- Lipton [2018] A. Lipton. Oscillating Bachelier and Black-Scholes Formulas. In Financial Engineering. World Scientific, 2018.

- Lipton and Kaushansky [2020] A. Lipton and V. Kaushansky. On the first hitting time density for a reducible diffusion process. Quantitative Finance, 20(5):723–743, 2020.

- Lipton and Sepp [2011] A. Lipton and A. Sepp. Filling the gaps. Risk Magazine, pages 66–71, 2011.

- Mazzonetto [2019] S. Mazzonetto. Rates of convergence to the local time of Oscillating and Skew Brownian Motions. arXiv preprint arXiv:1912.04858, 2019.

- Pai and Pedersen [1999] J. Pai and H. Pedersen. Threshold Models of the Term Structure of Interest Rate. In Joint day Proceedings Volume of the XXXth International ASTIN Colloquium/9th International AFIR Colloquium, Tokyo, Japan, pages 387–400. 1999.

- Pfann et al. [1996] G. A. Pfann, P. C. Schotman, and R. Tschernig. Nonlinear interest rate dynamics and implications for the term structure. Journal of Econometrics, 74(1):149 – 176, 1996.

- Pigato [2019] P. Pigato. Extreme at-the-money skew in a local volatility model. Finance and Stochastics, 23:827–859, 2019.

- Rabemananjara and Zakoian [1993] R. Rabemananjara and J. M. Zakoian. Threshold ARCH models and asymmetries in volatility. Journal of Applied Econometrics, 8(1):31–49, Jan. 1993.

- Rényi [1963] A. Rényi. On stable sequences of events. Sankhyā Ser. A, 25:293–302, 1963.

- Su and Chan [2015] F. Su and K.-S. Chan. Quasi-likelihood estimation of a threshold diffusion process. J. Econometrics, 189(2):473–484, 2015.

- Su and Chan [2017] F. Su and K.-S. Chan. Testing for threshold diffusion. J. Bus. Econom. Statist., 35(2):218–227, 2017.

- Tong [1983] H. Tong. Threshold models in nonlinear time series analysis, volume 21 of Lecture Notes in Statistics. Springer-Verlag, New York, 1983.

- Tong [1990] H. Tong. Non-linear Time Series: A Dynamical System Approach. Oxford University Press, 1990.

- Tong [2011] H. Tong. Threshold models in time series analysis — 30 years on. Statistics and its Interface, 4, 2011.

- Tong [2015] H. Tong. Threshold models in time series analysis—some reflections. J. Econometrics, 189(2):485–491, 2015.

- Vasicek [1977] O. Vasicek. An equilibrium characterization of the term structure. Journal of Financial Economics, 5(2):177 – 188, 1977.

- Wu and Zhang [1996] Y. Wu and H. Zhang. Mean Reversion in Interest Rates: New Evidence from a Panel of OECD Countries. Journal of Money, Credit and Banking, 28(4):604–621, 1996.

- Xing et al. [2020] X. Xing, D. Zhao, and B. Li. Parameter estimation for the skew Ornstein-Uhlenbeck processes based on discrete observations. Communications in Statistics - Theory and Methods, 49(9):2176–2188, 2020.

- Yadav et al. [1994] P. Yadav, P. Pope, and K. Paudyal. Threshold autoregressive modeling in finance: The price differences of equivalent assets. Mathematical Finance, 4(2):205–221, 1994.

- Yu et al. [2020] T.-H. Yu, H. Tsai, and H. Rachinger. Approximate maximum likelihood estimation of a threshold diffusion process. Computational Statistics & Data Analysis, 142:106823, 2020.