newfloatplacement\undefine@keynewfloatname\undefine@keynewfloatfileext\undefine@keynewfloatwithin

Continuous Regularized Wasserstein Barycenters

Abstract

Wasserstein barycenters provide a geometrically meaningful way to aggregate probability distributions, built on the theory of optimal transport. They are difficult to compute in practice, however, leading previous work to restrict their supports to finite sets of points. Leveraging a new dual formulation for the regularized Wasserstein barycenter problem, we introduce a stochastic algorithm that constructs a continuous approximation of the barycenter. We establish strong duality and use the corresponding primal-dual relationship to parametrize the barycenter implicitly using the dual potentials of regularized transport problems. The resulting problem can be solved with stochastic gradient descent, which yields an efficient online algorithm to approximate the barycenter of continuous distributions given sample access. We demonstrate the effectiveness of our approach and compare against previous work on synthetic examples and real-world applications.

1 Introduction

In statistics and machine learning, it is often desirable to aggregate distinct but similar collections of information, represented as probability distributions. For example, when temperature data is missing from one weather station, one can combine the temperature histograms from nearby stations to provide a good estimate for the missing station [Sol+14]. Or, in a Bayesian inference setting, when inference on the full data set is not allowed due to privacy or efficiency reasons, one can distributively gather posterior samples from slices of the data to form a single posterior incorporating information from all the data [Min+14, SLD18, Sri+15, Sta+17].

One successful aggregation strategy consists in computing a barycenter of the input distributions. Given a notion of distance between distributions, the barycenter is the distribution that minimizes the sum of distances to the individual input distributions. A popular choice of distance is the Wasserstein distance based on the theory of optimal transport. The corresponding barycenter, called the Wasserstein barycenter was first studied in [AC11]. Intuitively, the Wasserstein distance is defined as the least amount of work required to transport the mass from one distribution into the other, where the notion of work is measured with respect to the metric of the underlying space on which the distributions are supported. The Wasserstein distance enjoys strong theoretical properties [Vil08, FG15, San15], and efficient algorithms for its computation have been proposed in recent years [Cut13, Gen+16, Seg+17, PC+19]. It has found success in many machine learning applications, including Bayesian inference [EM12] and domain adaptation [CFT14].

Finding the Wasserstein barycenter is not an easy task. To make it computationally tractable, the barycenter is typically constrained to be a discrete measure on a fixed number of support points [CD14, Sta+17, Dvu+18, CCS18]. This discrete approximation, however, can be undesirable in downstream applications, as it goes against the inherently continuous nature of many data distributions and lacks the capability of generating fresh samples when needed. To address this shortcoming, in this work we compute a continuous approximation of the barycenter that provides a stream of samples from the barycenter.

Contributions. We propose a stochastic algorithm to approximate the Wasserstein barycenter without discretizing its support. Our method relies on a novel dual formulation of the regularized Wasserstein barycenter problem where the regularization is applied on a continuous support measure for the barycenter. The dual potentials that solve this dual problem can be used to recover the optimal transport plan between each input distribution and the barycenter. We solve the dual problem using stochastic gradient descent, yielding an efficient algorithm that only requires sample access to the input distributions. The barycenter can then be extracted as a follow-up step. Compared to existing methods, our algorithm produces the first continuous approximation of the barycenter that allows sample access. We demonstrate the effectiveness of our approach on synthesized examples and on real-world data for subset posterior aggregation.

Related Work. In [AC11], the notion of Wasserstein barycenters was first introduced and analyzed theoretically. Although significant progress has been made in developing fast and scalable methods to compute the Wasserstein distance between distributions in both discrete [Cut13] and continuous cases [Gen+16, Seg+17], the search for an efficient and flexible Wasserstein barycenter algorithm has been overlooked in the continuous setting.

To have a tractable representation of the barycenter, previous methods assume that the barycenter is supported on discrete points. When the support is fixed a priori, the problem boils down to estimating the weights of the support points, and efficient projection-based methods can be used for discrete input measures [Ben+15, Sol+15, CP16] while gradient-based solvers can be used for continuous input measures [Sta+17, Dvu+18]. These fixed-support methods become prohibitive in higher dimensions, as the number of points required for a reasonable a priori discrete support grows exponentially. When the support points are free to move, alternating optimization of the support weights and the support points is typically used to deal with the non-convexity of the problem [CD14]. More recent methods use stochastic optimization [CCS18] or the Franke–Wolfe algorithm [Lui+19] to construct the support iteratively. These free-support methods, however, are computationally expensive and do not scale to a large number of support points.

If the support is no longer constrained to be discrete, a key challenge is to find a suitable representation of the now continuous barycenter, a challenge that is unaddressed in previous work. We draw inspiration from [Gen+16], where the Wasserstein distance between continuous distributions is computed by parameterizing the dual potentials in a reproducing kernel Hilbert space (RKHS). Their work was followed by [Seg+17], where neural networks are used instead of RKHS parameterizations. The primal-dual relationship exhibits a bridge between continuous dual potentials and the transport plans, which can the be marginalized to get a convenient continuous representation of the distributions. However, a direct extension of [Seg+17] to the barycenter problem will need to parameterize the barycenter measure, resulting in an alternating min-max optimization. By introducing a novel regularizing measure that does not rely on the unknown barycenter but only on a proxy support measure, we are able to encode the information of the barycenter in the dual potentials themselves without explicitly parameterizing the barycenter. This idea of computing the barycenter from dual potentials can be viewed as a generalization of [CP16] to the continuous case where the barycenter is no longer supported on a finite set known beforehand.

2 Background on Optimal Transport

Throughout, we consider a compact set equipped with a symmetric cost function . We denote by the space of probability Radon measures. For any , the Kantorovich formulation of optimal transport between and is defined as:

| (1) |

where is the set of admissable transport plans, and are the projections onto the first and second coordinate respectively, and denotes the pushforward of the measure by a function . When , the quantity is the -Wasserstein distance between and .

The primal problem (1) admits an equivalent dual formulation [San15]:

| (2) |

where is the space of continuous real-valued functions on , and . The inequality is interpreted as for -a.e. and -a.e. . We refer to and as the dual potentials.

Directly solving (1) and (2) is challenging even with discretization, since the resulting linear program can be large. Hence regularized optimal transport has emerged as a popular, efficient alternative [Cut13]. Let be the measure on which we enforce a relaxed version of the constraint that we call the regularizing measure. In previous work, is usually taken to be the product measure [Gen+16] or the uniform measure on a discrete set of points [Cut13]. Given a convex regularizer , we define the regularized version of (1) with respect to as

| (3) |

where denotes that is absolutely continuous with respect to . In this work, we consider entropic and quadratic regularization defined by

| (4) |

As in the unregularized case, the primal problem (3) admits an equivalent dual formulation for entropic [Gen+16, Cla+19] and quadratic [LMM19] regularization:

| (5) |

where the regularizer on the dual problem is determined as

| (6) |

The regularized dual problem has the advantage of being unconstrained thanks to the penalization of to smoothly enforce . We can recover the optimal transport plan from the optimal dual potentials using the primal-dual relationship [Gen+16, LMM19]:

| (7) |

The entropic regularizer is more popular, as in the discrete case it yields a problem that can be solved with the celebrated Sinkhorn algorithm [Cut13]. We will consider both entropic and quadratic regularization in our setup, although more general regularizers can be used.

3 Regularized Wasserstein Barycenters

We can now use the regularized Wasserstein distance (3) to define a regularized version of the classic Wasserstein barycenter problem introduced in [AC11].

3.1 Primal and dual formulation of the regularized Wasserstein barycenter

Given input distributions and weights , the (unregularized) Wasserstein barycenter problem111In some convention, there is an additional exponent in the summands of (8) such as for the 2-Wasserstein barycenter. Here we absorb such exponent in (1), e.g., . of these input measures with respect to the weights is [AC11]:

| (8) |

Since this formulation is hard to solve in practice, we instead consider the following regularized Wasserstein barycenter problem with respect to the regularized Wasserstein distance (3) for some , where refers to either quadratic or entropic regularization (4):

| (9) |

If we knew the true barycenter , we would set . Hence for (9) to make sense a priori, we must use another measure as a proxy for . We call such the barycenter support measure. If no information about the barycenter is known beforehand, we take , the uniform measure on . Otherwise we can choose based on the information we have.

Our method relies on the following dual formulation of (9):

Theorem 3.1.

3.2 Solving the regularized barycenter problem

Notice that (10) is convex in the potentials with the linear constraint . To get an unconstrained version of the problem, we replace each with . Rewriting integrals as expectations, we obtain the following formulation equivalent to (10):

| (11) |

This version is an unconstrained concave maximization of an expectation.

The optimization space of (11) is infinite-dimensional. Following [Gen+16], we parameterize the potentials and solve (11) using stochastic gradient descent (Algorithm 1). In their paper, the parameterization is done using reproducing kernel Hilbert spaces, which can be made more efficient using random Fourier features [RR08]; this technique gives convergence guarantees but is only well-suited for smooth problems. In [Seg+17], a neural network parameterization is used with the benefit of approximating arbitrary continuous functions, but its convergence guarantees are more elusive. We extend these techniques to solve (11). A comparison between neural network parameterization and random Fourier parameterization is included in Figure 2.

Once we approximate the optimal potentials , as observed in Remark 3.1.1, we can recover the corresponding transport plan via the primal-dual relationships (7).

This formulation can be easily extended to the discrete case. If the barycenter has a fixed discrete support known a priori, we can take to be the uniform measure on the discrete support and parameterize each as a real-valued vector. If the input distributions are discrete, we can use an analogous discrete representation for each .

3.3 Recovering the barycenter

Given the optimal transport plan for each , the barycenter equals for any by Theorem 3.1. While this pushforward is straightforward to evaluate when ’s are discrete, in the continuous setting such marginalization is difficult, especially when the dimension of is large. Below we suggest a few ways to recover the barycenter from the transport plans:

-

(a)

Use numerical integration to approximate with proper discretization of the space , if has density (if the input distributions and have densities by (7)).

-

(b)

Use Markov chain Monte Carlo (MCMC) methods to sample according to , again assuming it has (unnormalized) density, and then take the second components of all the samples.

Option (a) is only viable for small dimensions. Option (b) is capable of providing quality samples, but is slow in practice and requires case-by-case parameter tuning. Both (a) and (b) additionally require knowing the densities of input distributions to evaluate , which may not be available in practice.

A different kind of approach is to estimate a Monge map approximating each . Formally, a Monge map from to is a solution to such that . When the cost satisfies with a convex and has density, it is linked to the optimal transport plan between and by [San15]. With regularization, such exact correspondence may not hold. Nevertheless encodes the crucial information of a Monge map when the regularization is small. If we can find that realizes for each , then we can recover the barycenter as . In the unregularized case, all of should agree. In practice, we have found that taking the weighted average of ’s helps reduce the error brought by each individual . We consider the following variants of Monge map estimation:

- (c)

-

(d)

Recover an approximation of the Monge map using the gradient of the dual potentials [TJ19]. For the case when and the densities of the source distributions exist, there exists a unique Monge map realizing the (unregularized) optimal transport plan [San15]:

(13) While this does not strictly hold for the regularized case, it gives a cheap approximation of ’s.

-

(e)

Find as a solution to the following optimization problem [Seg+17], where is defined in (7):

(14) In [Seg+17] each is parameterized as a neural network. In practice, the regularity of the neural networks smooths the transport map, avoiding erroneous oscillations due to sampling error in methods like barycentric projection (c) where each is estimated pointwise.

Compared to (a)(b), options (c)(d)(e) do no require knowing the densities of the input distributions. See a comparison of these methods in Figure 1.

4 Implementation and Experiments

We tested the proposed framework for computing a continuous approximation of the barycenter on both synthetic and real-world data. In all experiments we use equal weights for input distributions, i.e., for all . Throughout we use the squared Euclidean distance as the cost function, i.e., . Note that our method is not limited to Euclidean distance costs and can be generalized to different cost functions in —or even to distance functions on curved domains. The source code is publicly available at https://github.com/lingxiaoli94/CWB.

Implementation details. The support measure is set to be the uniform measure on a box containing the support of all the source distributions, estimated by sampling.

For , we can simplify the (unregularized) Wasserstein barycenter problem by considering centered input distributions [Álv+16]. Concretely, if the mean of is , then the mean of the resulting barycenter is , and we can first compute the barycenter of input distributions centered at 0 and then translate the barycenter to have the right mean. We adopt this simplification since this allows us to reduce the size of the support measure when the input distributions are far apart. When computing the Monge map (c)(d)(e), for each , we further enforce to have zero mean by replacing with . We have found that empirically this helps reduce the bias coming from regularization when recovering the Monge map.

The stochastic gradient descent used to solve (11) and (14) is implemented in Tensorflow 2.1 [Aba+16]. In all experiments below, we use Adam optimizer [KB14] with learning rate and batch size or for the training. The dual potentials in (11) are each parameterized as neural networks with two fully-connected layers () using ReLU activations. Every in (14) is parameterized with layers (). We have tested with deeper/wider network architectures but have found no noticeable improvement. We change the choice of the regularizer and the number of training iterations depending on the examples.

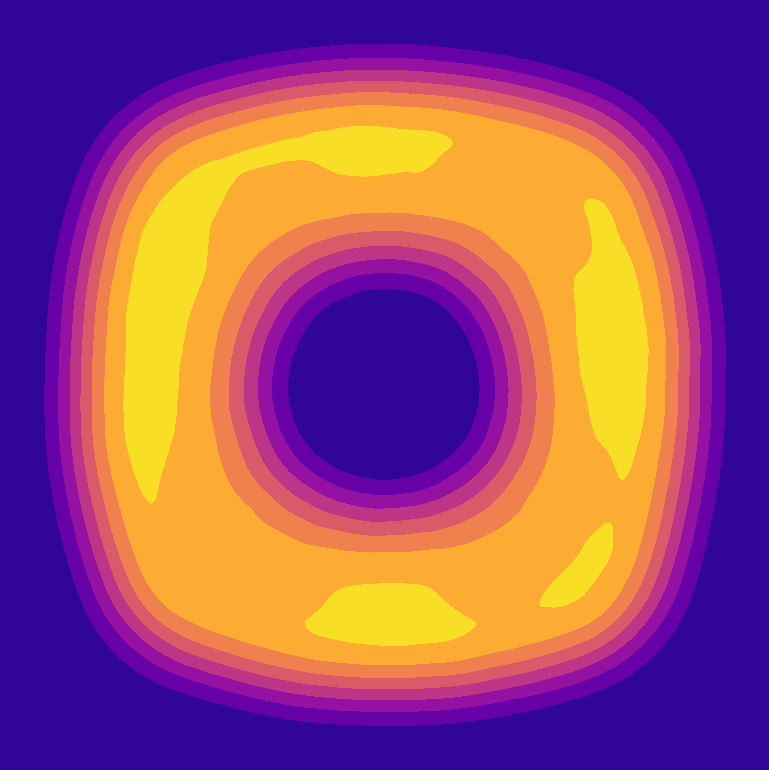

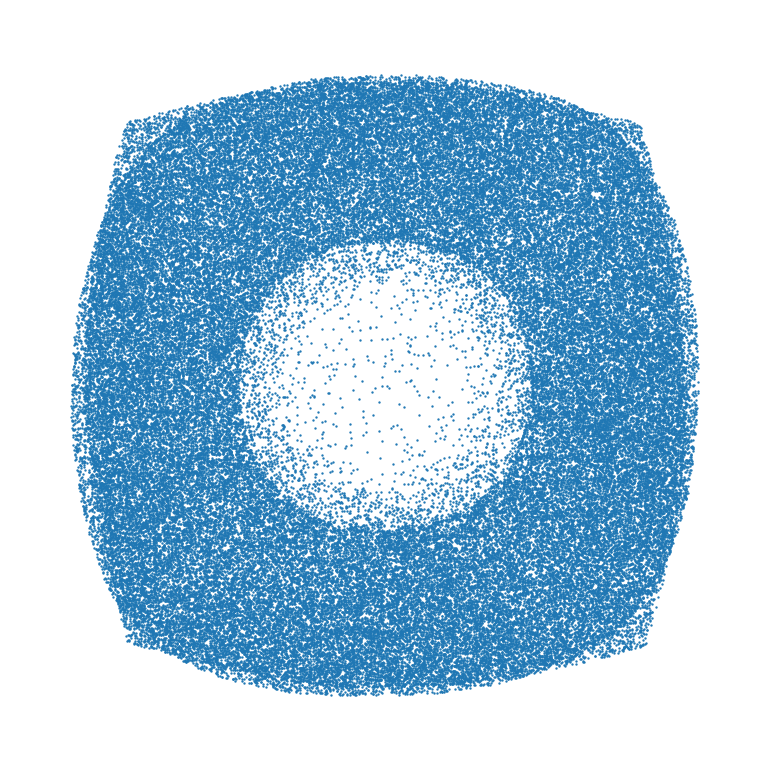

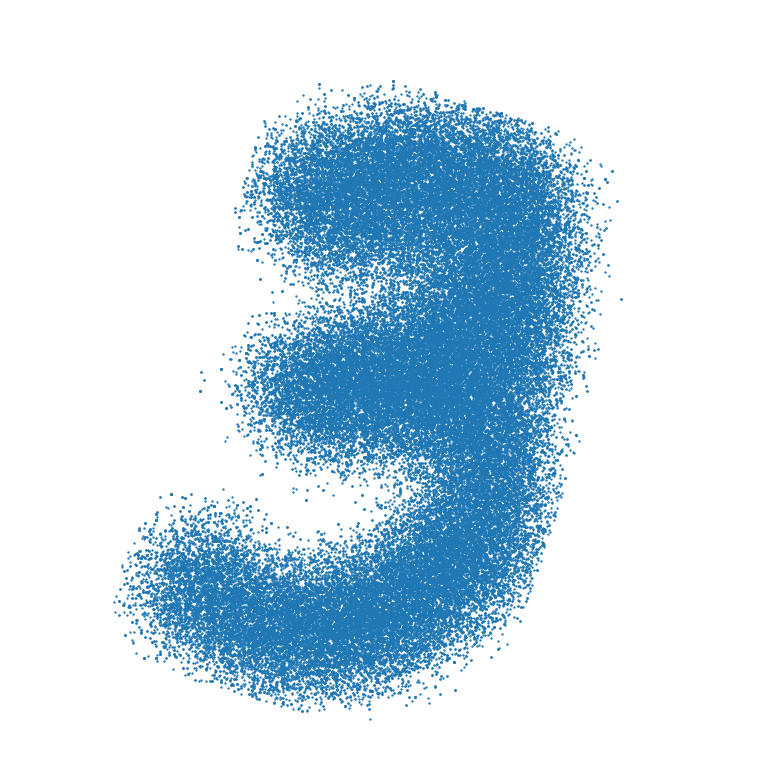

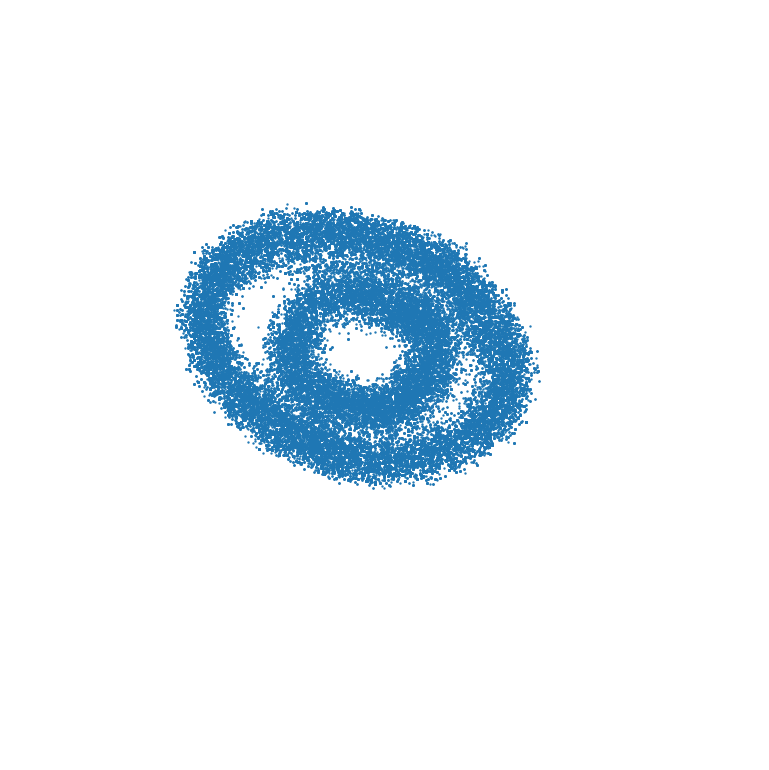

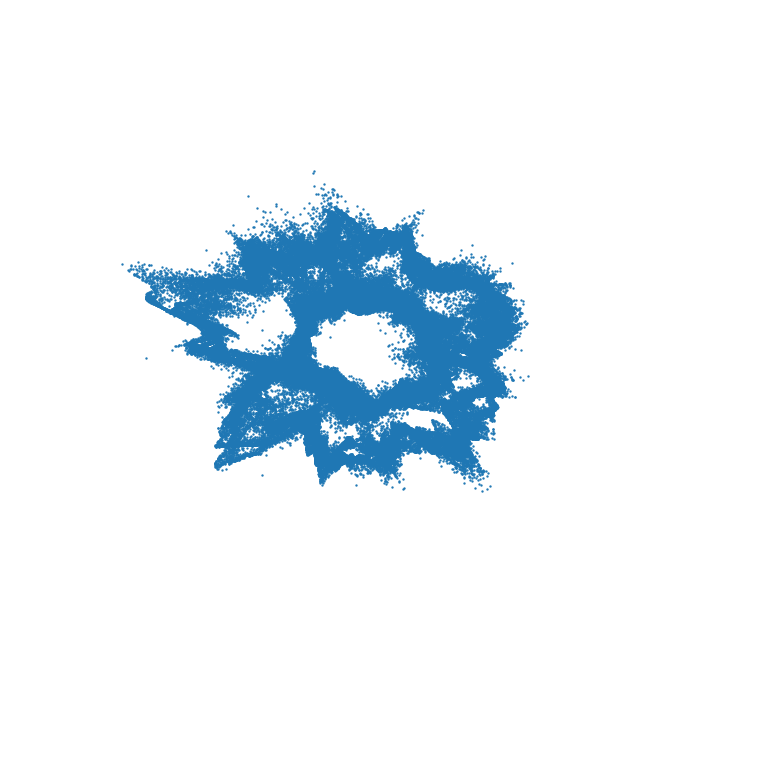

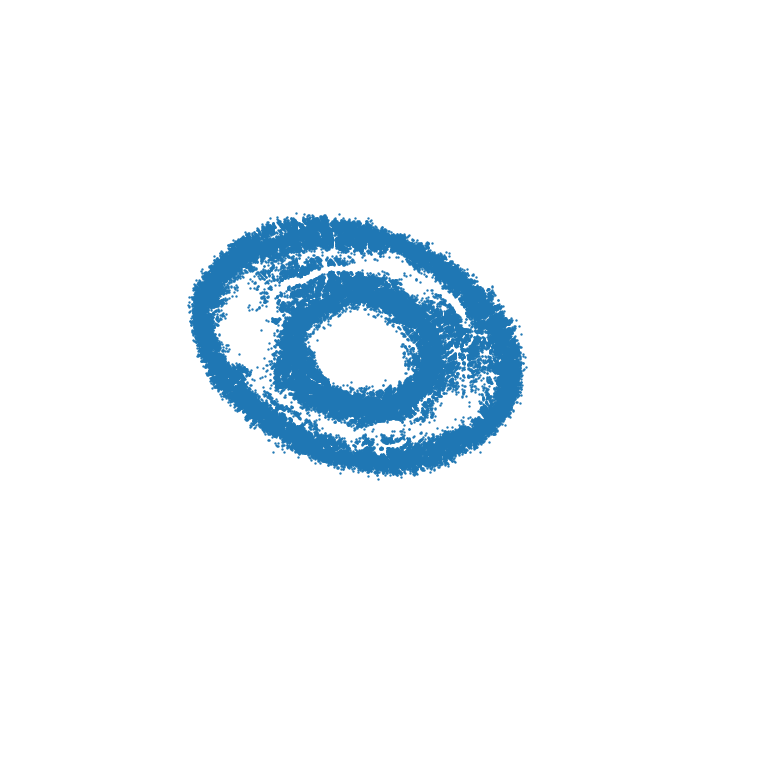

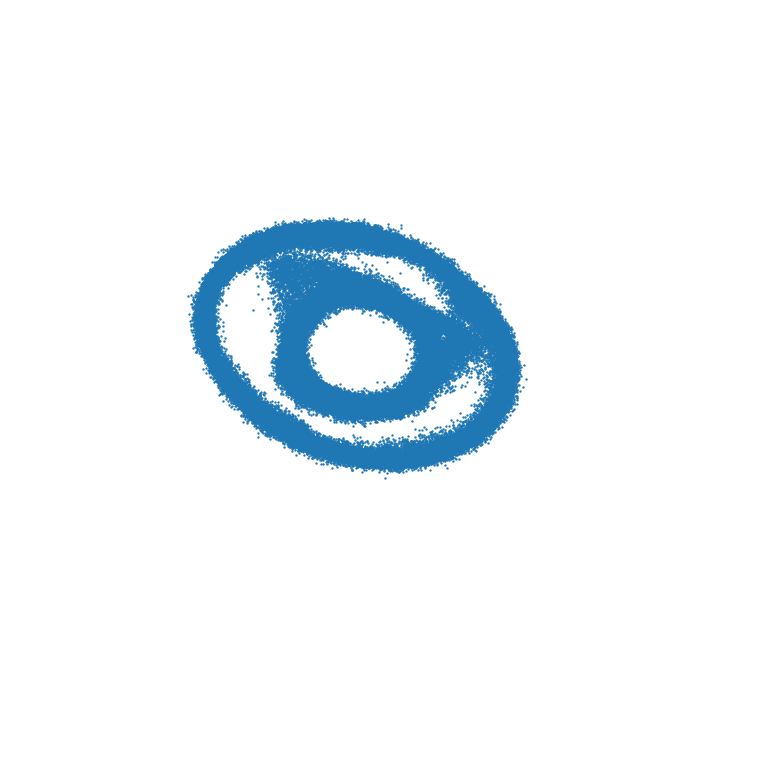

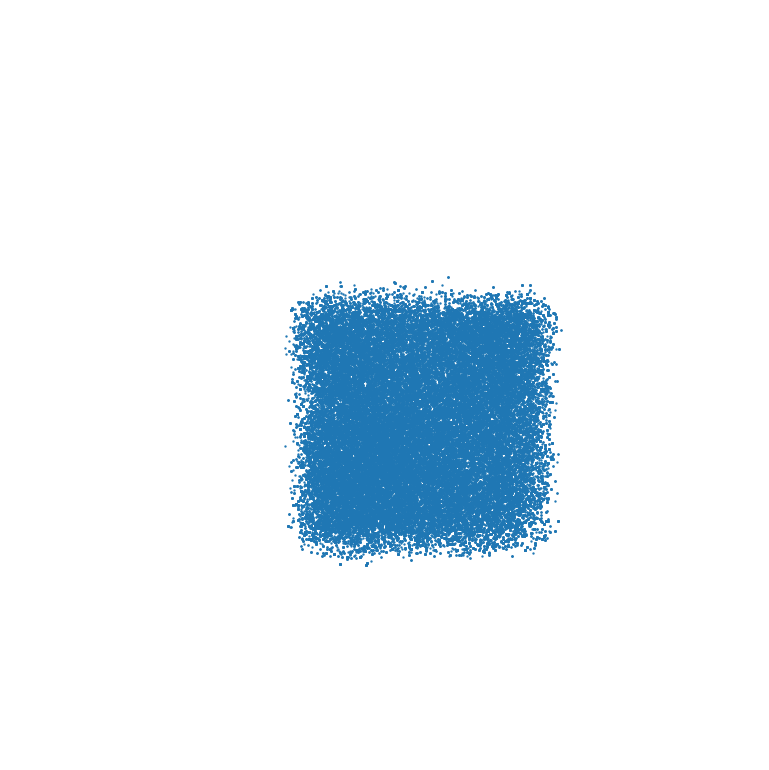

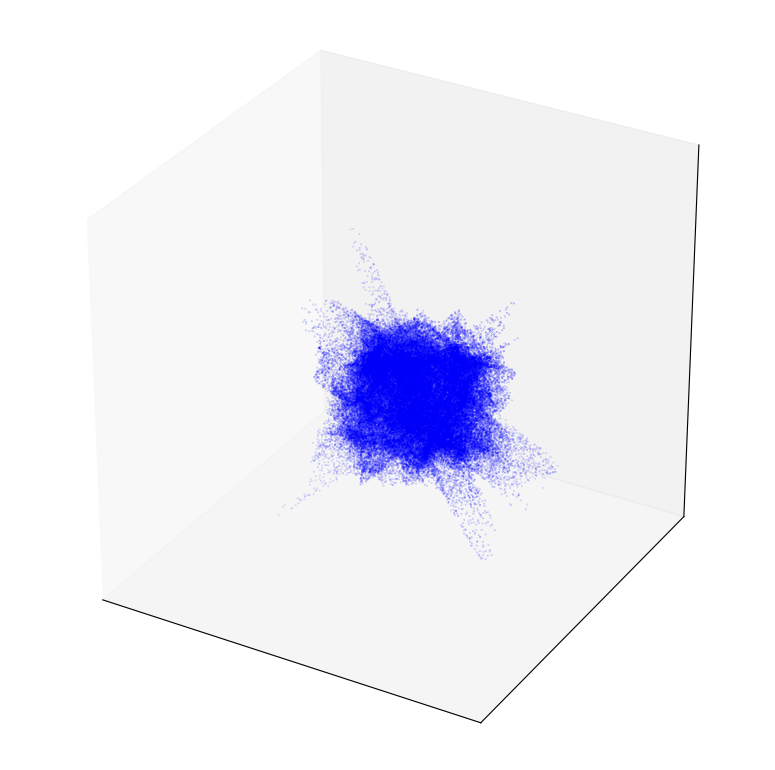

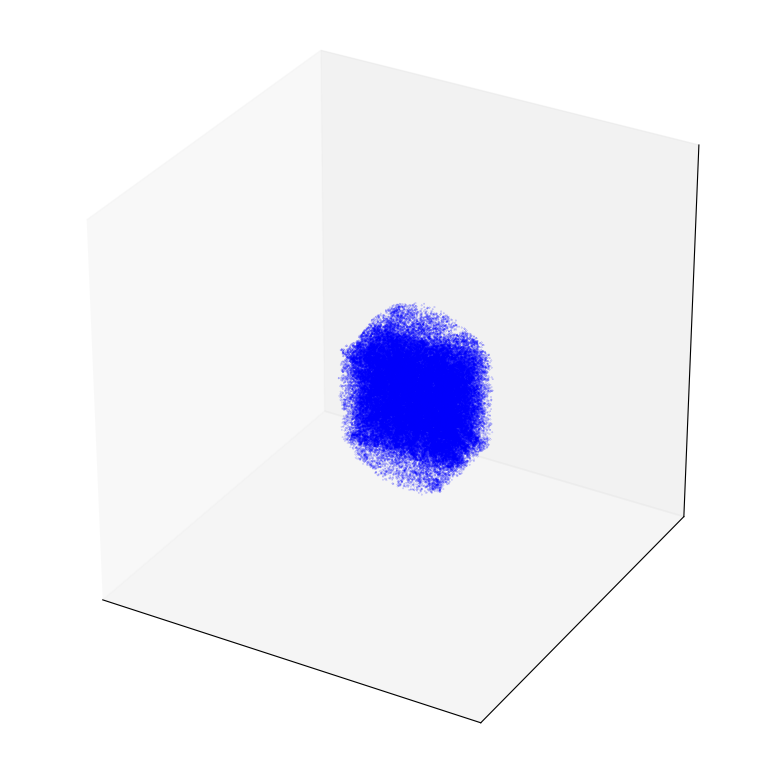

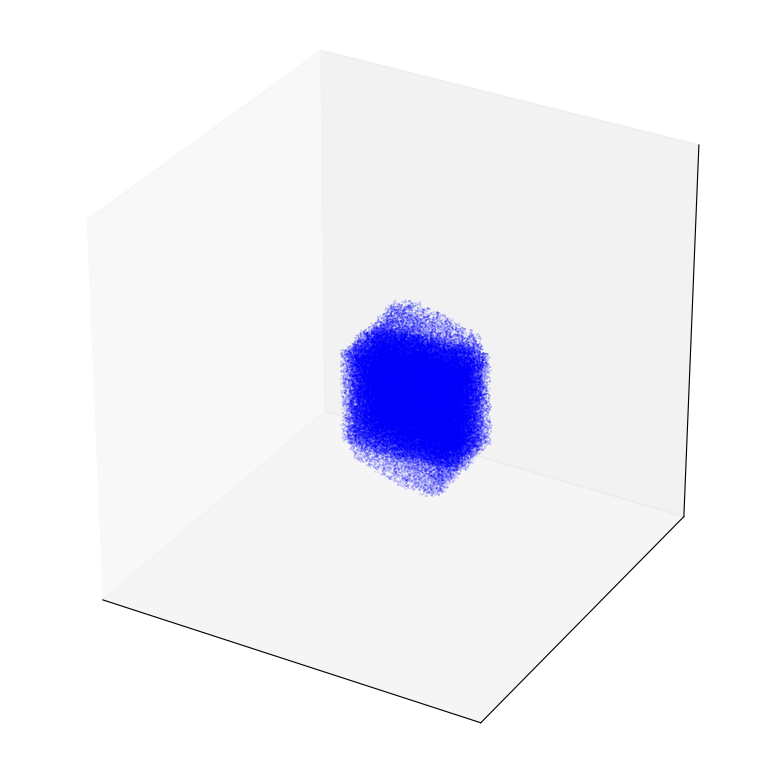

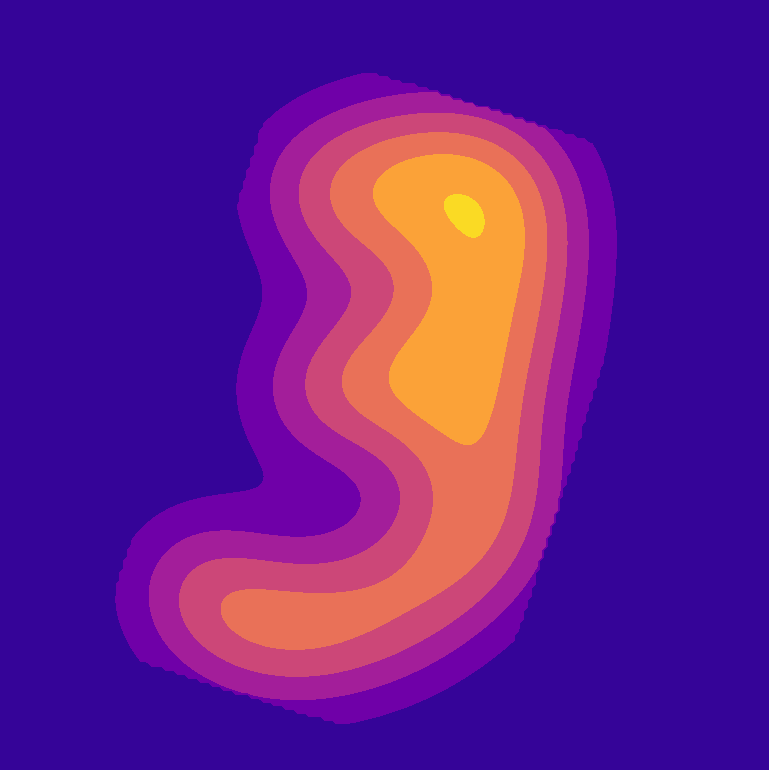

Qualitative results in 2 and 3 dimensions. Figure 1 shows the results for methods (a)-(e) from section 3.3 on various examples. For each example represented as a row, we first train the dual potentials using quadratic regularization with or . Then each method is run subsequently to obtain the barycenter. Algorithm 1 takes less than minutes to finish for these experiments.222We ran our experiments using a NVIDIA Tesla V100 GPU on a Google cloud instance with 12 compute-optimized CPUs and 64GB memory. For (a) we use a discretized grid with grid size in 2D, and grid size in 3D. For (b) we use Metropolis-Hastings to generate samples with a symmetric Gaussian proposal. The results from (a)(b) are aggregated from all transport plans. For (c)(d)(e) we sample from each input distribution and then push the samples forward using ’s to have samples in total.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Source | (a) Integrated | (b) MCMC | (c) Barycentric | (d) Gradient map | (e) [Seg+17] |

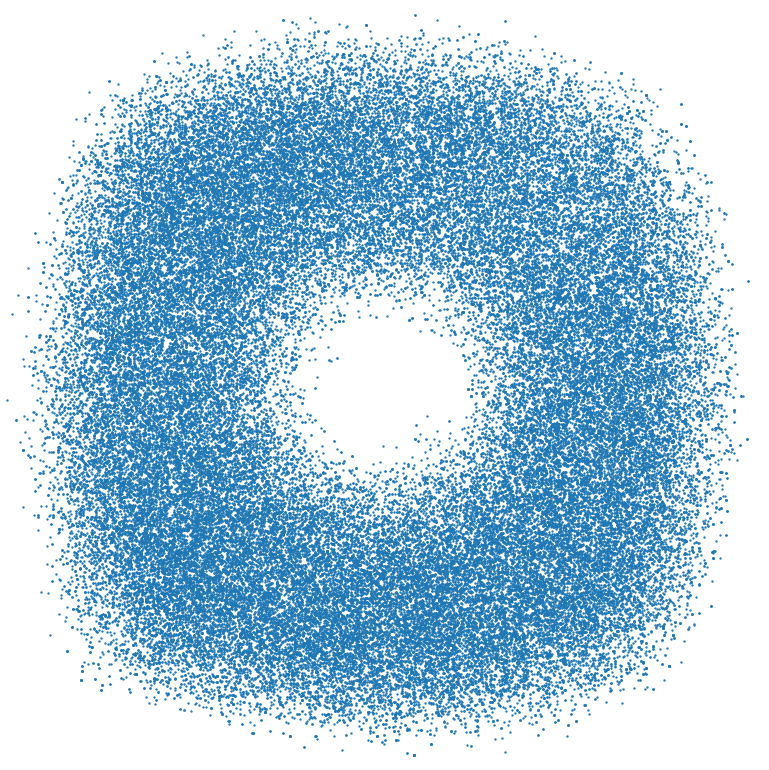

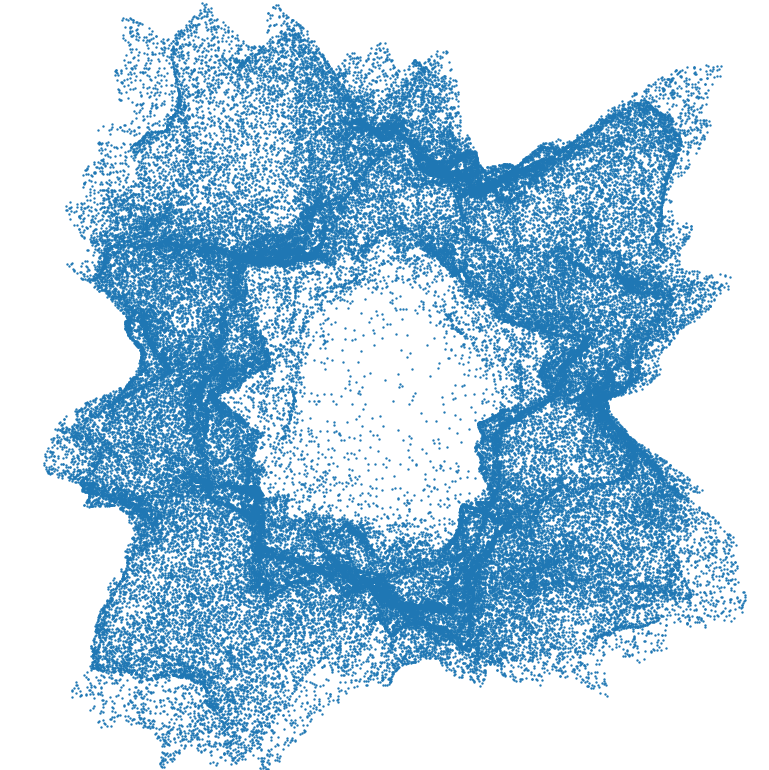

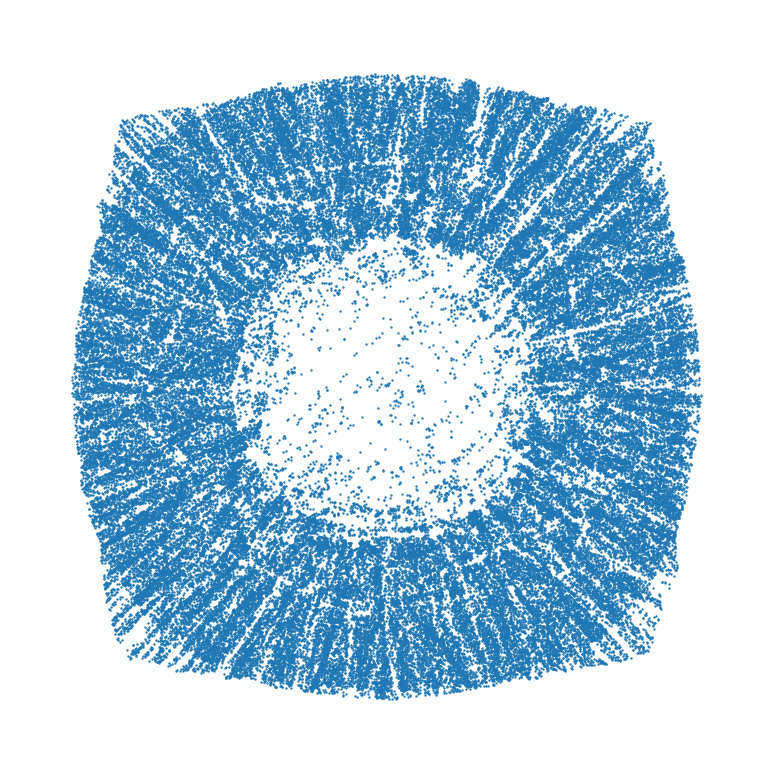

In short: (a) numerical integration shows the transport plans ’s computed by (7) are accurate and smooth; (b) MCMC samples match the barycenter in (a) but are expensive to compute and can be blurry near the boundaries; (c) barycentric projection yields poor boundaries due to the high variance in evaluating (12) pointwise; (d) gradient-based map has fragmented white lines in the interior; (e) the method by [Seg+17] can inherit undesirable artifact from the input distributions—for instance, in the last column of the second row the digit looks pixelated.

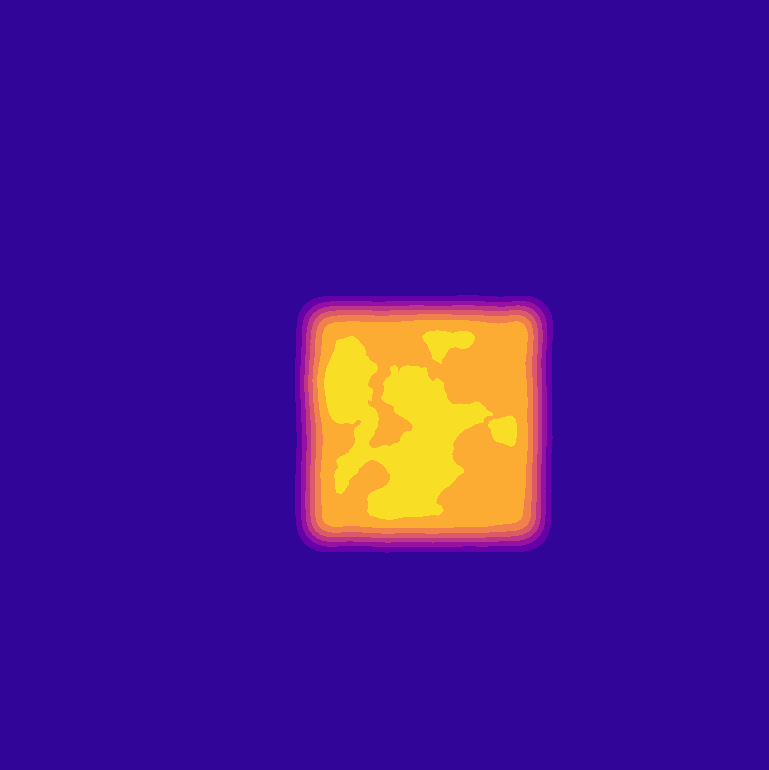

Next, we compare the impact of the choice of regularization and parameterization in Figure 2. We use the digit 3 example (row 2 in Figure 1) and run numerical integration (a) to recover the barycenter. The first three columns confirm that smaller gives sharper results as the computed barycenter tends to the unregularized barycenter. On the other hand, entropic regularization yields a smoother marginal, but smaller leads to numerical instability: we display the smallest one we could reach. The last two columns show that parameterization using random Fourier features [RR08] gives a comparable result as using neural networks, but the scale of the frequencies needs to be fine-tuned.

|

|

|

|

|

|

| RFF, | RFF, |

Multivariate Gaussians with varying dimensions. When the input distributions are multivariate Gaussians, the (unregularized) barycenter is also a multivariate Gaussian, and an efficient fixed-point algorithm can be used to recover its parameters [Álv+16]. We compute the ground truth barycenter of randomly generated multivariate Gaussians in varying dimensions using [Álv+16] and compare our proposed algorithm to other state-of-the-art barycenter algorithms. Since measuring the Wasserstein distance of two distributions in high dimensions is computationally challenging, we instead compare the MLE parameters if we fit a Gaussian to the computed barycenter samples and compare with the true parameters. See Table 1 for the results of our algorithm with quadratic regularization compared with those from other state-of-the-art free-support methods. Among the Monge map estimation methods, the gradient-based Monge map (d) works the best in higher dimensions, and the result of (e) is slightly worse: we believe this is due to the error accumulated in the second stochastic gradient descent used to compute (14). For brevity, we only include (d) in Table 1. Note that discrete fixed-support algorithms will have trouble scaling to higher dimensions as the total number of grid points grows exponentially with the number of dimensions. For instance, the covariance difference between the ground truth and those from running [Sta+17] with support points in is , which is significantly worse than the ones shown in Table 1. See the supplementary document for more details.

| Dimension | [CD14] | [CCS18] | Ours with (d) and |

|---|---|---|---|

| () | () | () | |

| () | () | () | |

| () | () | () | |

| () | () | () | |

| () | () | () | |

| () | () | () | |

| () | () | () |

In this experiment, we are able to consistently outperform state-of-the-art free-support methods in higher dimensions with the additional benefit of providing sample access from the barycenter.

Subset posterior aggregation. To show the effectiveness of our algorithm in real-world applications, we apply our method to aggregate subset posterior distributions using barycenters, which has been shown as an effective alternative to the full posterior in the massive data setting [Sri+15, SLD18, Sta+17]. We consider Poisson regression for the task of predicting the hourly number of bike rentals using features such as the day of the week and weather conditions.333http://archive.ics.uci.edu/ml/datasets/Bike+Sharing+Dataset We use one intercept and 8 regression coefficients for the Poisson model, and consider the posterior on the 8-dimensional regression coefficients. We randomly split the data into equally-sized subsets and obtain samples from each subset posterior using the Stan library [Car+17].

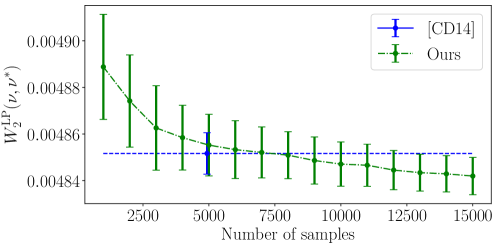

The barycenter of subset posteriors converges to the full data posterior [SLD18]. Hence, to evaluate the quality of the barycenter computed from the subset posterior samples, we use the full posterior samples as the ground truth and report the differences in covariance using sufficiently many samples from the barycenter, and compare against other free-support barycenter algorithms (Table 2). See the supplementary document for more details. To show how the quality of the barycenter improves as more samples are used from our barycenter, we plot the 2-Wasserstein distance versus the number of samples in Figure 3. Since computing requires solving a large linear program, we are only able to produce the result up to samples. This is also a limitation in [CD14] as each iteration of their alternating optimization solves many large linear programs; for this reason we are only able to use support points for their method. We see that as we use more samples, steadily decreases with lower variance, and we expect the decrease to continue with more samples. With samples our barycenter is closer to the full posterior than that of [CD14].

| [CD14] | [CCS18] | Ours with (d) and |

|---|---|---|

| () | () | () |

5 Conclusion

Our stochastic algorithm computes the barycenter of continuous distributions without discretizing the output barycenter, and has been shown to provide a clear advantage over past methods in higher dimensions. However the performance of our algorithm still suffers from a curse of dimensionality when the dimension is too high. Indeed in this case the support measure we fix from the beginning becomes a poor proxy for the true barycenter, and an enormous batch size is required to evaluate the expectation in (11) with reasonably small variance. One future direction is to find a way to estimate the support measure dynamically, but choosing a representation for this task is challenging. Another issue that can be addressed is to reduce regularization bias. This can either happen by formulating alternative versions of the dual problem or by improving the methods for estimating a Monge map.

Broader Impact

In this paper, we propose new techniques for estimating Wasserstein barycenters. The Wasserstein barycenter is a purely mathematical notion that can be applied to solve a variety of problems in practice. Beyond generic misuses of statistical and machine learning techniques, we are not aware of any unethical applications specifically of Wasserstein barycenters and hope that practitioners will find use cases for our methodology that can benefit society.

Acknowledgments

Justin Solomon and the MIT Geometric Data Processing group acknowledge the generous support of Army Research Office grants W911NF1710068 and W911NF2010168, of Air Force Office of Scientific Research award FA9550-19-1-031, of National Science Foundation grant IIS-1838071, from the CSAIL Systems that Learn program, from the MIT–IBM Watson AI Laboratory, from the Toyota–CSAIL Joint Research Center, from a gift from Adobe Systems, and from the Skoltech–MIT Next Generation Program.

References

References

- [Aba+16] Martin Abadi, Paul Barham, Jianmin Chen, Zhifeng Chen, Andy Davis, Jeffrey Dean, Matthieu Devin, Sanjay Ghemawat, Geoffrey Irving and Michael Isard “Tensorflow: A system for large-scale machine learning” In 12th USENIX Symposium on Operating Systems Design and Implementation (OSDI 16), 2016, pp. 265–283

- [AC11] Martial Agueh and Guillaume Carlier “Barycenters in the Wasserstein space” In SIAM Journal on Mathematical Analysis 43.2 SIAM, 2011, pp. 904–924

- [Álv+16] Pedro C Álvarez-Esteban, E Del Barrio, JA Cuesta-Albertos and C Matrán “A fixed-point approach to barycenters in Wasserstein space” In Journal of Mathematical Analysis and Applications 441.2 Elsevier, 2016, pp. 744–762

- [Ben+15] Jean-David Benamou, Guillaume Carlier, Marco Cuturi, Luca Nenna and Gabriel Peyré “Iterative Bregman projections for regularized transportation problems” In SIAM Journal on Scientific Computing 37.2 SIAM, 2015, pp. A1111–A1138

- [Car+17] Bob Carpenter, Andrew Gelman, Matthew D Hoffman, Daniel Lee, Ben Goodrich, Michael Betancourt, Marcus Brubaker, Jiqiang Guo, Peter Li and Allen Riddell “Stan: A probabilistic programming language” In Journal of Statistical Software 76.1 Columbia Univ., New York, NY (United States); Harvard Univ., Cambridge, MA …, 2017

- [CB19] Trevor Campbell and Tamara Broderick “Automated scalable Bayesian inference via Hilbert coresets” In The Journal of Machine Learning Research 20.1 JMLR.org, 2019, pp. 551–588

- [CCS18] Sebastian Claici, Edward Chien and Justin Solomon “Stochastic Wasserstein barycenters” In arXiv:1802.05757, 2018

- [CD14] Marco Cuturi and Arnaud Doucet “Fast computation of Wasserstein barycenters” In Journal of Machine Learning Research, 2014

- [CFT14] Nicolas Courty, Rémi Flamary and Devis Tuia “Domain adaptation with regularized optimal transport” In Joint European Conference on Machine Learning and Knowledge Discovery in Databases, 2014, pp. 274–289 Springer

- [Cla+19] Christian Clason, Dirk A Lorenz, Hinrich Mahler and Benedikt Wirth “Entropic regularization of continuous optimal transport problems” In arXiv:1906.01333, 2019

- [CP16] Marco Cuturi and Gabriel Peyré “A smoothed dual approach for variational Wasserstein problems” In SIAM Journal on Imaging Sciences 9.1 SIAM, 2016, pp. 320–343

- [Cut13] Marco Cuturi “Sinkhorn distances: Lightspeed computation of optimal transport” In Advances in Neural Information Processing Systems, 2013, pp. 2292–2300

- [Dvu+18] Pavel Dvurechenskii, Darina Dvinskikh, Alexander Gasnikov, Cesar Uribe and Angelia Nedich “Decentralize and randomize: Faster algorithm for Wasserstein barycenters” In Advances in Neural Information Processing Systems, 2018, pp. 10760–10770

- [EM12] Tarek A El Moselhy and Youssef M Marzouk “Bayesian inference with optimal maps” In Journal of Computational Physics 231.23 Elsevier, 2012, pp. 7815–7850

- [ET99] Ivar Ekeland and Roger Temam “Convex Analysis and Variational Problems” SIAM, 1999

- [FG15] Nicolas Fournier and Arnaud Guillin “On the rate of convergence in Wasserstein distance of the empirical measure” In Probability Theory and Related Fields 162.3-4 Springer, 2015, pp. 707–738

- [Gen+16] Aude Genevay, Marco Cuturi, Gabriel Peyré and Francis Bach “Stochastic optimization for large-scale optimal transport” In Advances in Neural Information Processing Systems, 2016, pp. 3440–3448

- [HG14] Matthew D Hoffman and Andrew Gelman “The No-U-Turn sampler: adaptively setting path lengths in Hamiltonian Monte Carlo.” In Journal of Machine Learning Research 15.1, 2014, pp. 1593–1623

- [KB14] Diederik P Kingma and Jimmy Ba “Adam: A method for stochastic optimization” In arXiv:1412.6980, 2014

- [LMM19] Dirk A Lorenz, Paul Manns and Christian Meyer “Quadratically regularized optimal transport” In Applied Mathematics & Optimization Springer, 2019, pp. 1–31

- [Lui+19] Giulia Luise, Saverio Salzo, Massimiliano Pontil and Carlo Ciliberto “Sinkhorn Barycenters with Free Support via Frank-Wolfe Algorithm” In Advances in Neural Information Processing Systems, 2019, pp. 9318–9329

- [Min+14] Stanislav Minsker, Sanvesh Srivastava, Lizhen Lin and David Dunson “Scalable and robust Bayesian inference via the median posterior” In International Conference on Machine Learning, 2014, pp. 1656–1664

- [PC+19] Gabriel Peyré and Marco Cuturi “Computational optimal transport” In Foundations and Trends in Machine Learning 11.5-6 Now Publishers, Inc., 2019, pp. 355–607

- [RR08] Ali Rahimi and Benjamin Recht “Random features for large-scale kernel machines” In Advances in Neural Information Processing Systems, 2008, pp. 1177–1184

- [San15] Filippo Santambrogio “Optimal Transport for Applied Mathematicians” In Birkäuser, NY 55.58-63 Springer, 2015, pp. 94

- [Seg+17] Vivien Seguy, Bharath Bhushan Damodaran, Rémi Flamary, Nicolas Courty, Antoine Rolet and Mathieu Blondel “Large-scale optimal transport and mapping estimation” In arXiv:1711.02283, 2017

- [SLD18] Sanvesh Srivastava, Cheng Li and David B Dunson “Scalable Bayes via barycenter in Wasserstein space” In The Journal of Machine Learning Research 19.1 JMLR.org, 2018, pp. 312–346

- [Sol+14] Justin Solomon, Raif Rustamov, Leonidas Guibas and Adrian Butscher “Wasserstein propagation for semi-supervised learning” In International Conference on Machine Learning, 2014, pp. 306–314

- [Sol+15] Justin Solomon, Fernando De Goes, Gabriel Peyré, Marco Cuturi, Adrian Butscher, Andy Nguyen, Tao Du and Leonidas Guibas “Convolutional Wasserstein distances: Efficient optimal transportation on geometric domains” In ACM Transactions on Graphics (TOG) 34.4 ACM New York, NY, USA, 2015, pp. 1–11

- [Sri+15] Sanvesh Srivastava, Volkan Cevher, Quoc Dinh and David Dunson “WASP: Scalable Bayes via barycenters of subset posteriors” In Artificial Intelligence and Statistics, 2015, pp. 912–920

- [Sta+17] Matthew Staib, Sebastian Claici, Justin M Solomon and Stefanie Jegelka “Parallel streaming Wasserstein barycenters” In Advances in Neural Information Processing Systems, 2017, pp. 2647–2658

- [TJ19] Amirhossein Taghvaei and Amin Jalali “2-Wasserstein Approximation via Restricted Convex Potentials with Application to Improved Training for GANs” In arXiv:1902.07197, 2019

- [Vil08] Cédric Villani “Optimal Transport: Old and New” Springer Science & Business Media, 2008

Appendix A Proof of Theorem 3.1

We restate Theorem 3.1 below.

Theorem A.1.

The dual problem of

| (A.1) |

is

| (A.2) |

Moreover, strong duality holds in the sense that the infimum of (A.1) equals the supremum of (A.2), and a solution to (A.1) exists. If solves (A.2), then each is a solution to the dual formulation (5) of where is a solution to (A.1). That is,

| (A.3) | ||||

where we write .

Proof.

We first prove the strong duality. We view as a normed vector space with the supremum norm. Let be the direct sum vector space endowed with the natural norm, i.e., for ,

For brevity, denote . We use the notation to suggest that a more general support measure can be used to establish the strong duality. Define to be, for ,

| (A.4) |

Let . By the Riesz–Markov–Kakutani representation theorem, the continuous dual space of is with the pairing for . Define as, for ,

Then the negative of (A.2) becomes

where the equality is component-wise (i.e. is the constant-zero function in ). Similarly we use to mean component-wise inequality in . Since is increasing in our assumption for quadratic and entropic regularization (6), the above program is the same as

| (A.5) |

This is because if , then for some , , and by replacing every with the objective (A.5) can only gets smaller.

The dual problem of (A.5) can be calculated as (see Chapter III.(5.23) in [ET99])

| (A.6) | ||||

| (A.7) | ||||

| (A.8) |

To get (A.7) we used the duality for regularized Wasserstein distance (5).

In order to apply classical results from convex analysis (for instance, Proposition 5.1 of Chapter III in [ET99]) to establish strong duality and the existence of solutions, we need to show:

-

(a)

is a convex l.s.c. (lower-semicontinuous) function.

-

(b)

is convex with respect to .

-

(c)

For any , , the map is l.s.c..

-

(d)

.

-

(e)

There exists such that .

-

(f)

The infimum in (A.5) is finite.

Since is linear and in our case, the conditions (b)-(e) are satisfied automatically. Convexity of (a) follows because is convex so that, for , , and ,

Next we show that is l.s.c. with respect to the norm topology on . Since is convex and does not take on values , by Proposition III.2.5 of [ET99], it is enough to show that is bounded above in a neighborhood of . Fix any . As before we write . Then implies for all . Since is compact, is bounded. Hence the integrand in (A.4) is bounded for as is increasing, and the conclusion that is bounded on follows from the fact that both and are probability measures for all . This proves is continuous, and hence l.s.c..

It remains to show the infimum in (A.5) is finite. Note that for such that , we have . Hence in this case, if like before we denote the uniform measure on , then

Thus by Proposition III.5.1 of [ET99], the problem (A.5) is stable (Definition III.2.2 in [ET99]), and in particular normal, so we have strong duality (Proposition III.2.1, III.2.2 in [ET99]), and the dual problem (A.8) has at least one solution. We comment that this does not imply (A.5) has a solution.

To show the solution to (A.8) is actually a probability measure, suppose . Consider the inner infimum in (A.6) for a particular . For any , we can set and . Then

where we used the fact that is increasing and . Either sending or shows that the minimizer must satisfy , for otherwise the infimum would be , which contradicts strong duality and (f).

Finally we prove the last statement of Theorem A.1. That is, if solves (A.2), then each pair solves (A.3). Suppose that solves (A.2). Let denote the solution to (A.1). Then . So the supremum of (A.2) equals

| (A.9) |

where the inequality follows from the duality (A.3) of the regularized Wasserstein distance. By strong duality we just showed, the supremum of (A.2) equals the infimum (A.1) which is (A.9). Hence inequality in (A.9) is equality, and we see that each pair solves (A.3). ∎

Appendix B Experimental details and additional results

Multivariate Gaussians with varying dimensions.

We generate the multivariate Gaussians in dimension used in Table 1 in the following manner. The mean is chosen uniformly at random in . The covariance matrix is obtained by first sampling a matrix with uniform entries in and then taking as the covariance matrix. We reject if its condition number (computed with respect to -norm) is not in .

We show in Table B.1 additional results for our algorithm with different choices of Monge map estimation methods and regularizers; in the last column we show the result of [CD14] where we use Sinkhorn algorithm [Cut13] instead of LP (see Table 1 for results with LP) to obtain the transport plan at every iteration.

| Ours with (d) and | Ours with (e) and | Ours with (d) and | [CD14] with Sinkhorn | |

|---|---|---|---|---|

| () | () | () | () | |

| () | () | () | () | |

| () | () | () | () | |

| () | () | () | () | |

| () | () | () | () | |

| () | () | () | () | |

| () | () | () | () |

To briefly comment on the runtime of our algorithm (with (d)) and that of [CD14] and [CCS18], in the 8-dimensional Gaussian experiment from Table 1, our algorithm takes around 15 minutes, [CD14] takes 20 minutes, while [CCS18] takes an hour or longer. The simple form of Algorithm 1 and the convex nature of (11) give rise to fast convergence of our approach.

Subset posterior aggregation.

We adopted the BikeTrips dataset and preprocessing steps from https://github.com/trevorcampbell/bayesian-coresets [CB19]. The posterior samples in the subset posterior aggregation experiment are generated using NUTS sampler [HG14] implemented by the Stan library [Car+17]. To enforce appropriate scaling of the prior in the subset posteriors we use stochastic approximation trick [SLD18], i.e. scaling the log-likelihood by the number of subsets. Please see the code for further details.

In Table B.2, we show additional results comparing [CD14] and our algorithm in three different losses: difference in mean, covariance, and the (unregularized) 2-Wasserstein distance computed using samples. See Figure 3 for a comparison with varying number of samples used to compute the 2-Wasserstein distance.

| Loss | [CD14] | Ours with (d) and | Ours with (e) and |

|---|---|---|---|

| ( | () | () | |

| () | () | () | |

| () | () | () |