Investigation of Flash Crash via Topological Data Analysis

Abstract

Topological data analysis has been acknowledged as one of the most successful mathematical data analytic methodologies in various fields including medicine, genetics, and image analysis. In this paper, we explore the potential of this methodology in finance by applying persistence landscape and dynamic time series analysis to analyze an extreme event in the stock market, known as Flash Crash. We will provide results of our empirical investigation to confirm the effectiveness of our new method not only for the characterization of this extreme event but also for its prediction purposes.

keywords:

Persistence landscape , Flash Crash , Time series analysisMSC:

[2020] 55N31 , 62R40 , 91G15 , 94A121 Introduction

Topological data analysis (TDA) is a relatively new, large, and growing field in mathematics using a wide variety of techniques based on homology theory and statistics. TDA extracts hidden intelligence from the shape of data that previous data analytic methods could not reveal, and various fields including medicine, image analysis, and genetics [7, 9] have tremendously benefited from this intriguing methodology. Nevertheless, in the field of finance, there has been only a small number of applications so far [5]. The purpose of this paper is to apply persistence landscape to detect extreme anomalies in financial market, and demonstrate how TDA can provide not only global characterization of data but also dynamic local features for prediction purposes.

In May 6, 2010, there was an unprecedented sudden intraday stock market crash in U.S. financial markets known as Flash Crash, and that event has recently emerged as an interesting research topic in finance [3, 4, 6, 8]. In this paper, we combine the methods of TDA including persistent landscape proposed by [5] and techniques of time series analysis, and create a new method for detecting intraday stock market crashes based on -norm of persistence landscape. We then empirically show that our method can characterize and predict the event of flash crash as well.

The rest of the paper is organized as follows: Section 2 introduces background and techniques of topological data analysis which are used in the paper, and provide a summary of the flash crash event. Section 3 describes our data constructed from major stock market indexes, and explains our new method based on TDA and statistical analysis. Section 4 reports empirical results to validate effectiveness of our methods for prediction purposes. Section 5 concludes the paper with further practical implications of our results.

2 Background

2.1 Topological Data Analysis

In this section, we gather key concepts of topological data analysis that will be used later in the paper. Consider a data set , which is a finite subset of a Euclidean space . Let denote the Vietoris-Rips complex for the data set and a distance , i.e., is the simplicial complex on the vertex set such that

| (1) |

Here is the Euclidean distance between and .

In what follows, let us denote by the -th homology group of a simplicial complex . Throughout this paper we only use homology with real coefficients. It follows from the very definition of Vietoris-Rips complex (1) that we have whenever . Using this we see that the Vietoris-Rips complexes , , form a filtration, which is called the Vietoris-Rips filtration. This filtration induces homomorphisms between homology groups. That is, for each , we get a canonical linear map,

| (2) |

The set of homology groups and the linear maps (2) form a persistence module in the sense of [2], which enables us to track the birth and death of homology classes as the parameter increases. More precisely, given and , let . By using the Vietoris-Rips filtration we see that there exist positive real numbers and satisfying and

-

1.

is not the image of the map if .

-

2.

For , there is whose image by the map is .

-

3.

For , the image of under the map is non-zero.

-

4.

The map sends to the zero in if .

Let denote the open interval corresponding to the birth and death of a given homology class . In what follows let denote the set of open intervals,

Here the elements of are counted with multiplicity, i.e., if and are distinct -dimensional homology classes, then and are regarded as different elements of even though these two open intervals may coincide.

Given a pair of real numbers , set

The persistence landscape associated with the data set is a function which encodes the information about the birth and death of homology classes [1]. It is defined by

Here -max denotes the -th largest value counted with multiplicity. Note that the persistence landscape can be seen as a sequence of functions .

For , the -norm of the persistence landscape is defined by

| (3) |

As is a finite set, all simplicial complexes , , are finite. This shows that for large enough, we have , and hence there is no issue of convergence of the series given in (3).

2.2 Flash Crash

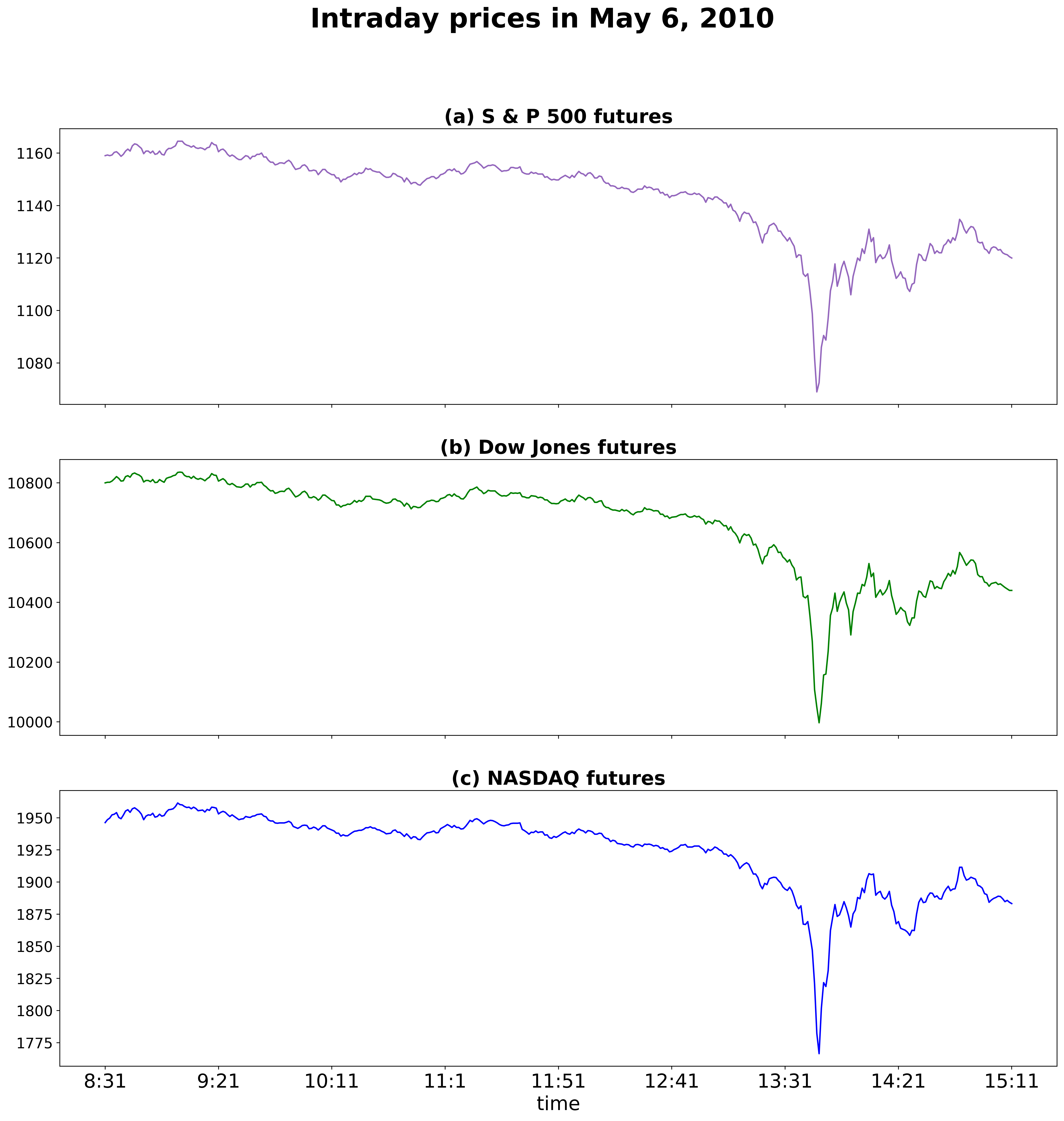

In May 6, 2010, there was a sudden intraday stock market crash in U.S. financial markets known as Flash Crash. The crash event, started at 2:32 p.m. EDT, lasted for approximately 36 minutes, during which major U.S. stock indexes such as the S&P 500, Dow Jones Industrial Average, and Nasdaq Composite dropped larger than 6% and rebounded very rapidly. Figure 1 shows intraday price time series of S&P 500 futures, Dow Jones futures, and NASDAQ futures in May 6, 2010. Since such an extreme price-swing event lasting only for a very short time had never been reported before in financial markets, many financial researchers have been trying to understand the Flash Crash [3, 4, 6, 8].

3 Data and Methods

We purchased one-minute price data for three futures based on three major U.S. stock market indexes: (a) S&P 500 futures, (b) Dow Jones futures, and (c) NASDAQ futures from April 1, 2010 to May 28, 2010 (42 trading days) from BacktestMarket (https://www.backtestmarket.com). For each future () and for each minute , we calculate one-minute log-return as , where represents the closing price of the futures at the minute . Thus, for each minute , we have a 3-dimensional vector defined by

Given a window size , and for each , we then construct the 3-dimesional time series defined by

For each 3-dimensional time series , we compute -norm of persistence landscape, , so we get a time series of -norm of persistence landscape,

as in [5]. In order to detect an abnormality of the time series , we develop a new abnormality measure based on the notions of Exponential Moving Average (EMA) and Exponential Moving Variance (EMVar) processes: Given the initial values,

the subsequent values, EMAi and EMVari, are computed using the following recursive formulae,

Then, our new abnormality measure is defined by

The new measure represents the extent to which the current value is deviated from the previous values.

4 Empirical Results

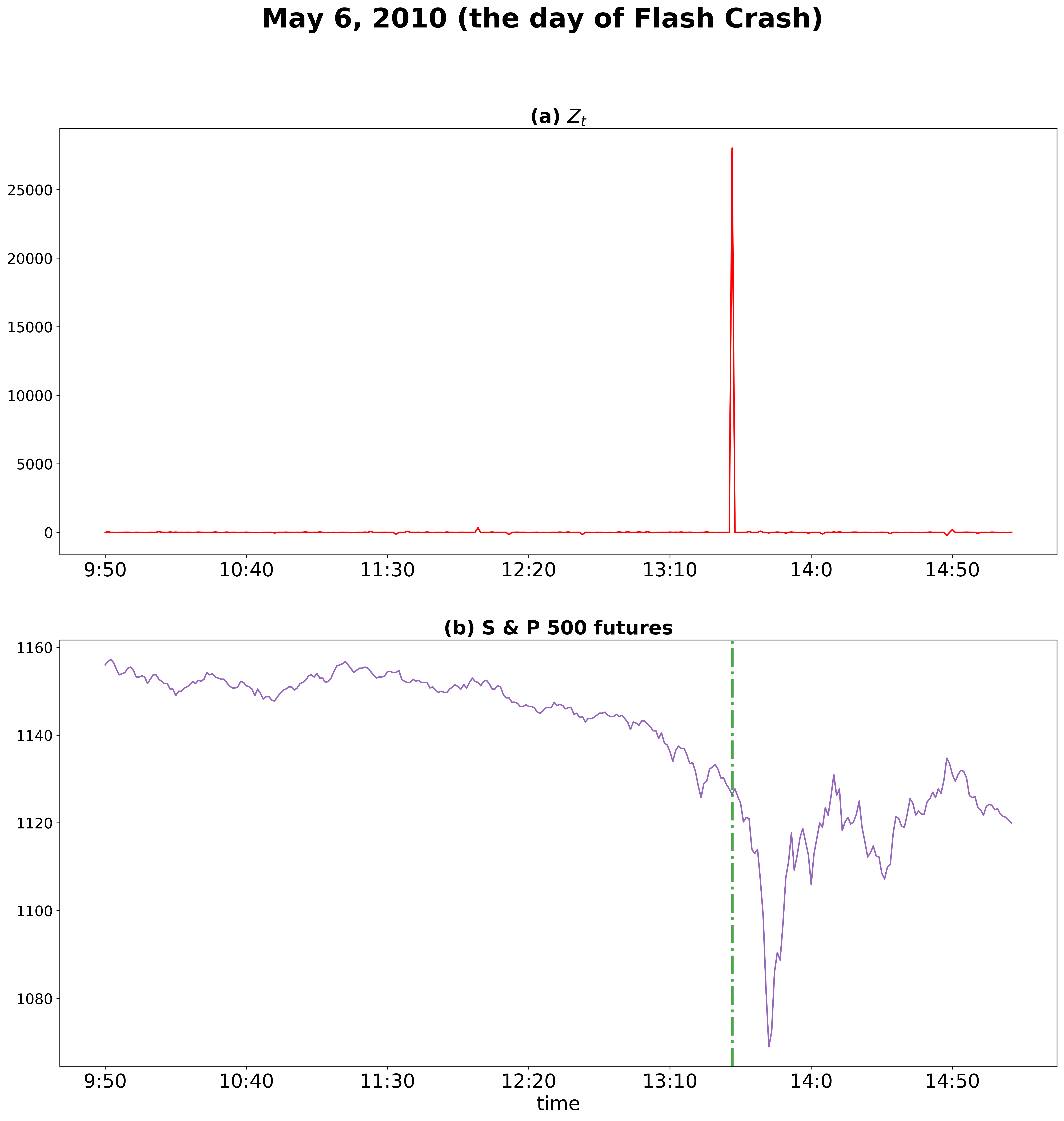

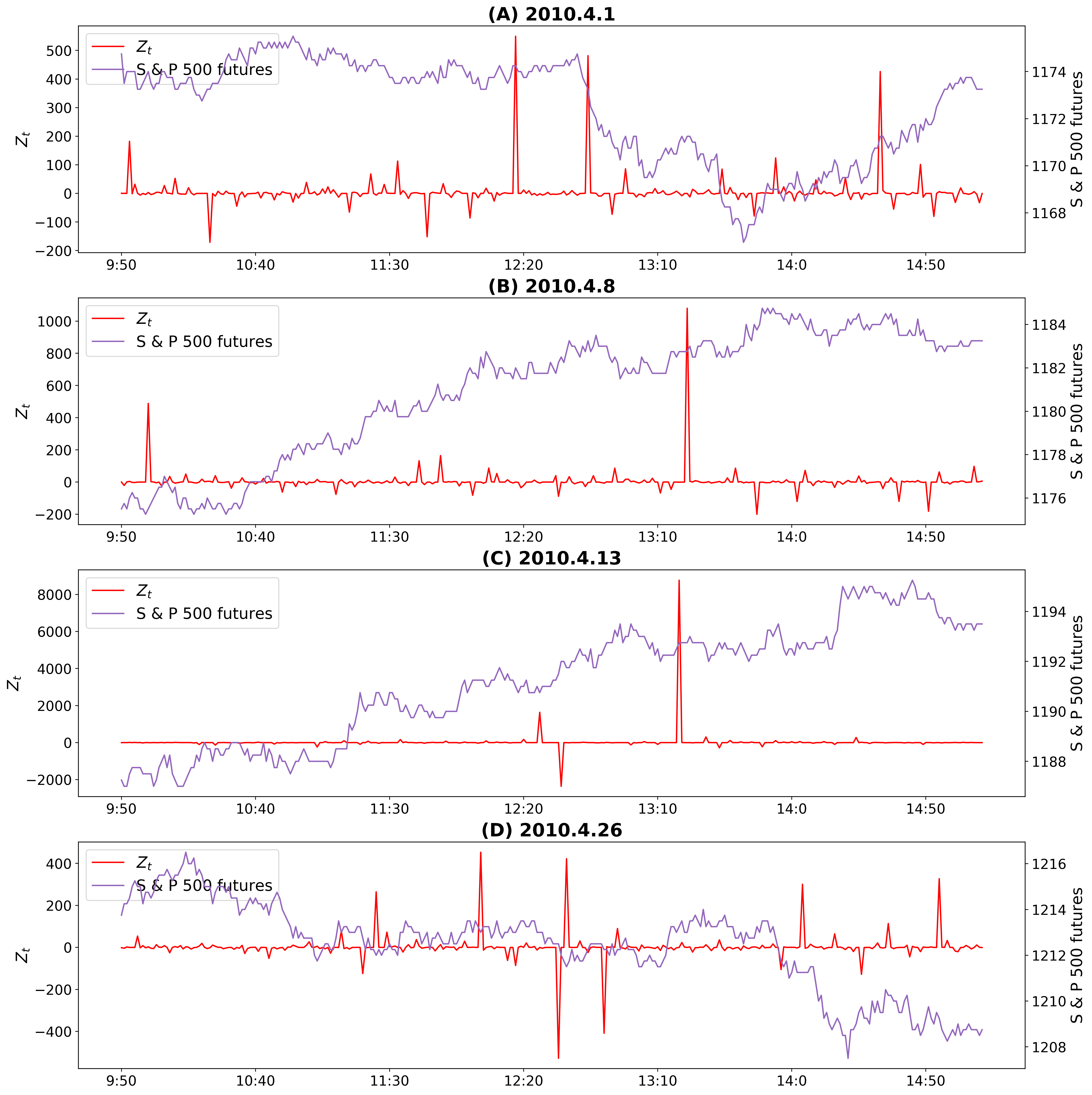

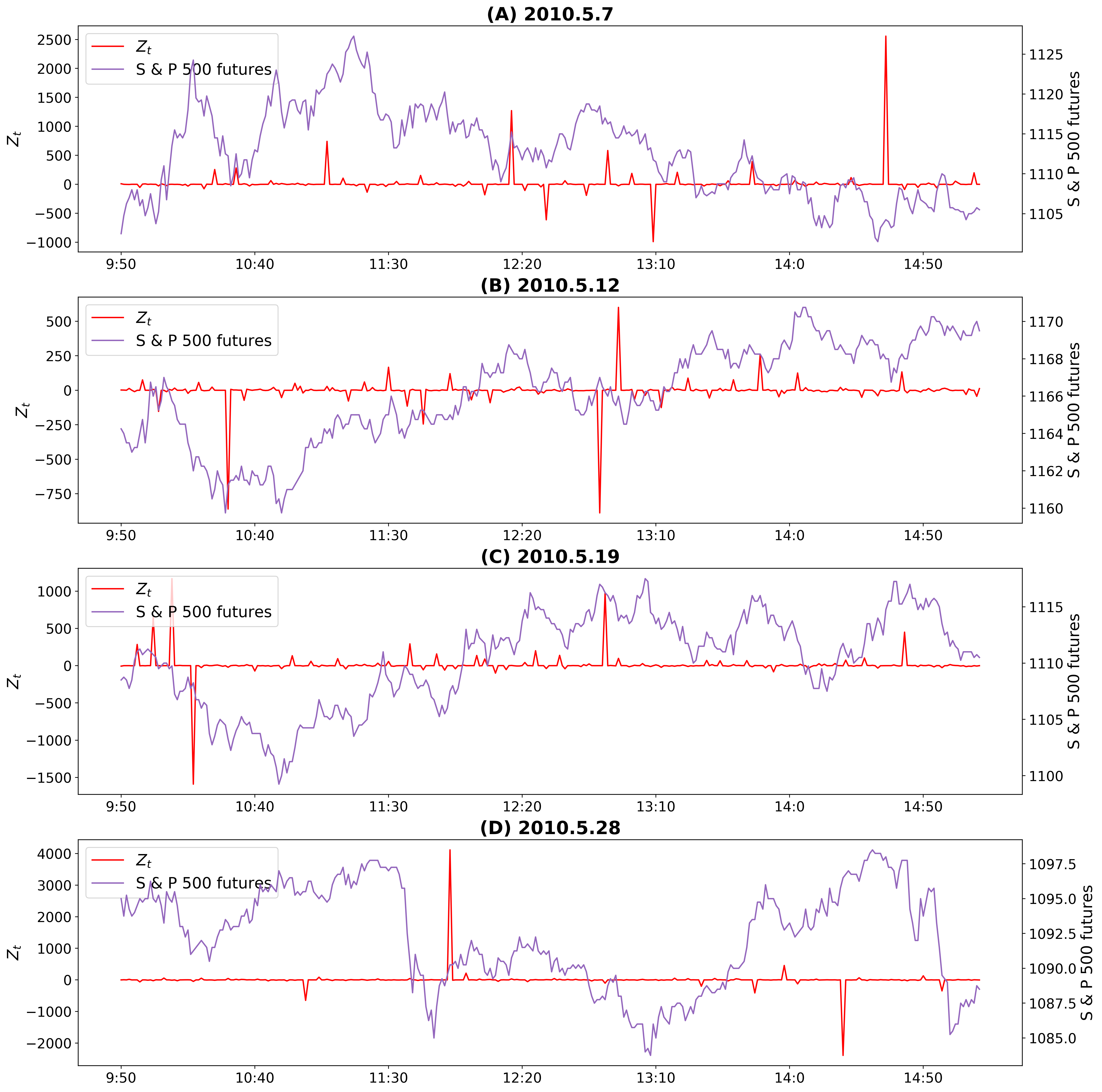

Figure 2 displays the intraday time series plots of our new abnormality measure and the prices of S&P 500 futures on May 6, 2010, the day of Flash Crash. As Figure 2 shows, just before the extreme price-swing of Flash Crash begins, the abnormality measure has the value of 28,034.92. The value is exceptionally huge compared to the values of at other times of the day. Figure 3 (resp., Figure 4) also presents the intraday time series plots of and S&P 500 futures in four randomly selected days before (resp., after) the day of Flash Crash out of our sample period. Figure 3 and 4 show that the largest value of in Flash Crash day, 28,034.92, is also extremely large compared to the values of in other days.

5 Conclusion

In this paper, we present a new method of detecting an abnormal phenomenon based on TDA and time series analysis, and investigate the event of Flash Crash via the new method. The empirical results from our study reveal that via the new method based on TDA, we can predict the event of Flash Crash. Therefore, our result shows that TDA not only can be used in forecasting long-term market crash events [5], but also can be used in predicting intraday market crash events.

References

- [1] P. Bubenik, Statistical topological data analysis using persistence landscapes, J. Mach. Learn. Res. 16 (2015) 77–102.

- [2] P. Bubenik, J.A. Scott, Categorification of persistent homology, Discrete Comput. Geom. 51 (2014) 600–627.

- [3] Commodity Futures Trading Commission, Securities & Exchange Commission, Findings regarding the market events of May 6, 2010. https://www.sec.gov/news/studies/2010/marketevents-report.pdf, 2010 (accessed 10.10.2019).

- [4] D. Easley, M.M.L. De Prado, M. O’Hara, The microstructure of the “flash crash”: Flow toxicity, liquidity crashes, and the probability of informed trading, J. Portf. Manag. 37 (2011) 118–128.

- [5] M. Gidea, Y. Katz, Topological data analysis of financial time series: Landscapes of crashes, Physica A 491 (2018) 820–834.

- [6] A. Kirilenko, A.S. Kyle, M. Samadi, T. Tuzun, The flash crash: High‐frequency trading in an electronic market, J. Finance 72 (2017) 967–998.

- [7] L. Li, W.-Y. Cheng, B.S. Glicksberg, O. Gottesman, R. Tamler, R. Chen, E.P. Bottinger, J.T. Dudley, Identification of type 2 diabetes subgroups through topological analysis of patient similarity, Sci. Transl. Med. 7 (2015) 1–16.

- [8] M. Paddrik, R. Hayes, A. Todd, S. Yang, P. Beling, W. Scherer, An agent based model of the E-Mini S&P 500 applied to Flash Crash analysis, in: Proceedings of the 2012 IEEE Conference on Computational Intelligence for Financial Engineering & Economics, IEEE, New York, NY, 2012, pp. 1–8.

- [9] G. Singh, F. Mémoli, G.E. Carlsson, Topological methods for the analysis of high dimensional data sets and 3d object recognition, in: M. Botsch, R. Pajarola, B. Chen, M. Zwicker (Eds.), Symposium on Point-Based Graphics 2007, Taylor & Francis Inc., Natick, MA, 2007, pp. 91–100.