Historical Context and Key Features of

Digital Money Tokens

Abstract

Digital money tokens have attracted the attention of financial institutions, central banks, regulators, international associations and fintechs. Their research and experimentation with digital money tokens has included creating innovative technical and operational frameworks. In this paper, we present a ‘money tree’ which places this recent concept of digital money tokens into a historical context by illustrating their evolution from more traditional forms of money. We then identify key features of digital money tokens with options and examples. We hope this paper will be of interest to the financial services industry and we look forward to feedback.

1 Introduction

Research and experimentation with digital money tokens is being conducted by financial institutions [29], central banks [38, 34], regulators [12, 40], international associations [17, 42] and fintechs [18, 30]. As an emerging technology, the innovative technical and operational frameworks are often bespoke. The terminology used to describe forms of digital money tokens is also inconsistent across these frameworks.

It can therefore be difficult to identify and understand the key features that distinguish different forms of digital money tokens, creating challenges in specifying and communicating new products and also potentially creating inappropriate opportunities for regulatory arbitrage across jurisdictions. To address this, some industry bodies are exploring standard taxonomies for digital money tokens. For example: (i) the Global Financial Markets Association (GFMA) has proposed an initial starting point for a classification of crypto-assets in their response [21] to a Basel Committee on Banking Supervision (BCBS) consultation on the treatment of crypto-assets [4] and also in their response [22] to an FSB consultation on challenges raised by global stablecoins [17] and (ii) the Association for Financial Markets in Europe (AFME) has recommended the publication of a more detailed taxonomy on the classification of crypto-assets in their response [2] to the European Commission consultation on a framework for crypto-asset markets [12].

This paper provides a historical context for digital money tokens by placing them within a ‘money tree’ illustrating their evolution from more traditional forms of money. We then identify key features of digital money tokens with options and examples.

We hope this money tree and list of key features will be of interest to the financial services industry. We look forward to feedback and continuing industry collaboration on the classification of digital money tokens.

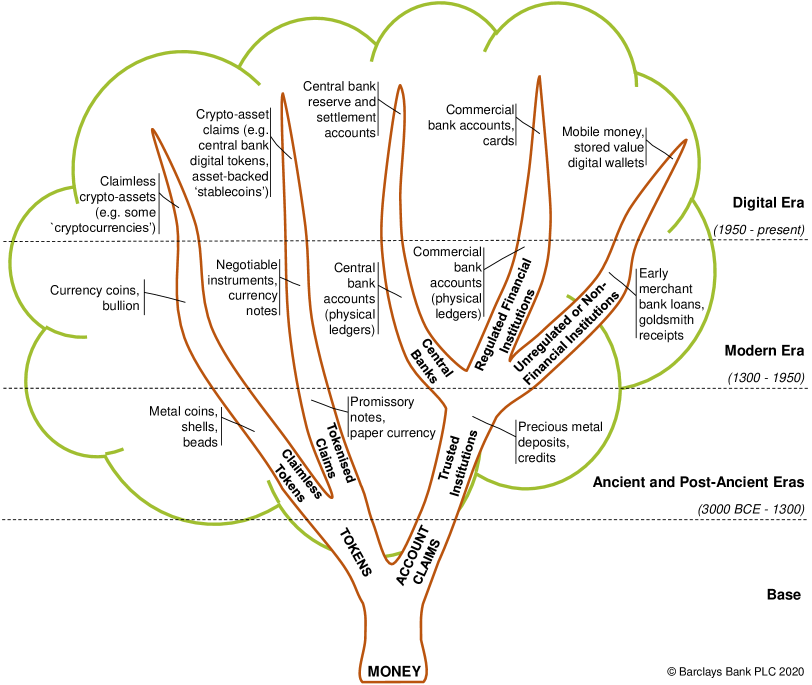

2 The Money Tree

Money is one of the fundamental inventions that support human societies and as a result its history has been studied extensively [33, 28, 35, 37, 23], from the first forms of account-based money and commodity money, through the development of fiat money and on to new digital forms of money.

While the history of money has been documented in considerable detail, we constructed a new summary visual representation to help us communicate the evolution of digital money tokens. This covers fours eras: the ancient and post-ancient eras (3000 BCE - 1300), the modern era (1300 - 1950), and the digital era (1950 - present). This is presented as the ‘money tree’ in Figure 1 with the hope that others may also find it useful.

2.1 Introduction to Money

-

•

a store of value with which to transfer purchasing power from today to some future time;

-

•

a medium of exchange with which to make payments for goods and services; and

-

•

a unit of account with which to measure the value of a particular good, service, saving or loan.

As money is a social convention [8], performing the above functions is not sufficient for something to be considered money because it also needs to be readily and easily accepted by others.

The money tree branches out from the base into two fundamental forms of money: tokens111We use the term ‘token’ to refer to all forms of money that can be transferred directly from one party to another without relying on an intermediary. However, note there is currently no commonly agreed definition for this term, e.g. some do not consider commodity money to be a token [33], some consider the term ‘object’ to be more suitable than ‘token’ [1], and some consider crypto-assets to be an account-based form of money [32]. and account claims, or more simply, accounts [33]. Token-based money (e.g. cash) can be transferred directly from one party to another without relying on an intermediary, but account-based money (e.g. money in a bank account) cannot be transferred directly from one party to another and instead depends on intermediaries (e.g. the bank(s) where the accounts are held) to effect transfers. Another key distinction between token-based money and account-based money is the form of verification needed when it is transferred, as described below (adapted from [11]):

-

•

Token-based money (or payment systems) rely critically on the ability of the payee to verify the validity of the payment object. With cash a key risk is counterfeiting, while in the digital world the key risk is whether the token or ‘coin’ is genuine or not (electronic counterfeiting) and whether it has already been spent.

-

•

By contrast, systems based on account money depend fundamentally on the ability to verify the identity of the account holders. A key concern is identity theft, which allows perpetrators to transfer or withdraw money from accounts without permission. Identification is needed to correctly link payers and payees and to ascertain their respective account histories.

2.2 Evolution of Account-based Money

Account-based money appears to pre-date token-based money, based on available information on ancient civilisations [33, 35]. The evolution of account-based money is tied closely to the evolution of account holding institutions.

The ‘Account’ side of the money tree depicts the following developments:

-

•

Ancient and Post-Ancient Eras: Accounts in the ancient and post-ancient eras were held at trusted institutions, such as temples in Mesopotamia and Greece, where people could deposit precious metals or record credits in a currency. These deposits and credits were recorded on, for example, clay and marble tablets [35, 23].

-

•

Modern Era: Depositories developed into dedicated financial institutions during the Italian Renaissance, leading to the creation of official state banks. Account holding institutions evolved into three main types over the course of the modern era, partly in response to the growth of currencies: central banks, regulated financial institutions, and unregulated or non-financial institutions such as goldsmiths and early merchant banks [23]. Each of these entities would hold accounts, usually denominated in a currency, with differing levels of access and trust. Transactions were recorded on paper ledgers using the ‘double-entry bookkeeping’ system. While currencies were traditionally backed by commodity assets such as gold, towards the end of the modern era this relationship was removed with the introduction of ‘fiat money’ i.e. money that is not convertible to gold or any other asset [3].

-

•

Digital Era: The digital era has seen the development of digitised accounts that are well understood and widely deployed. Transactions continue to be recorded using the ‘double-entry bookkeeping’ system using digital technologies. These have enabled account holders to have greater access to their money through digital and physical channels [8]. While central banks and regulated financial institutions have digitised accounts and introduced new digital products (e.g. cards), the unregulated or non-financial institution space has also seen a rapid evolution of new digital products (e.g. mobile money, stored value digital wallets) from recent entrants such as telecommunication and technology firms.

2.3 Evolution of Token-based Money

The ‘Token’ side of the money tree branches into two forms that have existed from the ancient era to the digital era: ‘tokenised claims’ that represent a claim on an entity or right on an underlying asset (e.g. currency notes) and ‘claimless tokens’ that don’t represent any such claim or right (e.g. coins). For tokenised claims, note the nature of the entity or asset on which the claim or right lies can be an important factor although, for simplicity, this has not been elaborated in the money tree.

The ‘Token’ side of the money tree depicts the following developments:

-

•

Ancient and Post-Ancient Eras: In the ancient and post-ancient eras, claimless tokens took the form of shells, beads or metal coins. Tokenised claims, such as paper promissory notes and currency notes issued in ancient China, represented a claim on the issuing merchant or monarchy [35].

-

•

Modern Era: The growth of currencies led to modern forms of money tokens created by dedicated financial institutions, non-financial institutions, central banks and governments. These entities issued metal coins and notes, representing the modern forms of claimless tokens and tokens that represented a claim or right [37]. Some tokens represented a claim on account-based forms of money (e.g. negotiable instruments drawn on banks). Maintaining the value of the currency against the value of the metal coins and honouring the claims on notes issued were challenges for the issuers. This was due to variations in the subjective value of the metals in the coins and poor management of the relationship between notes issued and the underlying assets which backed them [8]. With the introduction of fiat money towards the end of the modern era, the nature of the entity issuing the tokens became vital to determining a token’s ability to serve the three functions of money (i.e. store of value, medium of exchange and unit of account).

-

•

Digital Era: The digital era has seen the birth of new digital forms of money tokens [8]. Similar to tokens in previous eras, digital money tokens can either be tokenised claims (e.g. central bank digital tokens [11]) or claimless tokens (e.g. some ‘cryptocurrencies’). Again, the nature of the issuing entity remains critical to determining the token’s ability to serve the three functions of money.

3 Key Features of Digital Money Tokens

The field of digital money tokens is evolving rapidly. The terminology used by financial institutions, central banks, regulators, international associations and fintechs to describe forms of digital money tokens is not always consistent. This can make it challenging to understand the key features that distinguish different forms of digital money tokens being developed and to evaluate new product propositions. The current absence of a generally agreed taxonomy may also lead to a fragmented regulatory approach [44] potentially creating inappropriate opportunities for regulatory arbitrage [42].

The seminal work by Bech and Garratt [5] (that builds on earlier work [10, 6]) discusses and visually represents a taxonomy for money in the form of a ‘money flower’, which is described in the next section. It has since been heavily referenced (e.g [31, 43]) and also adapted (e.g. [11, 36]), becoming an key contribution to the taxonomy of money. However, this high-level taxonomy does not consider all of the key features of digital money tokens and so does not fully distinguish between these forms of money.

Adrian and Mancini-Griffoli presented a visual taxonomy for money [1] (coincidentally also named ‘money tree’) based on four features: type (claim or object), value (redemption rate for claims, unit of account for objects), the backstop for claims (government or private), and technology used (centralised or decentralisaed). This taxonomy comprises five means of payment: central bank money, crypto-currency, b-money (issued by banks), e-money (offered by new private sector providers), and i-money (issued by private investment funds). However, their use of ‘claim’ and ‘object’ as the two distinct and fundamental types of money leads to listing cash and central bank digital currencies as examples of ‘object’ money even though they are claims on central banks.

The Token Taxonomy Framework (TTF) [27] is a taxonomy for digital tokens developed by the InterWork Alliance, an industry association with members from the technology and financial industries. The TTF is based on features such as fungibility, unit of measure (fractional, whole or singleton), value (intrinsic or referential), uniqueness and the nature of the supply (fixed, capped-variable, gated or infinite) that are combined with behaviours (e.g. transferable, mintable, divisible) to create a set of base token types. These features, behaviours and base token types are generic and apply to money tokens, securities tokens and utility tokens. This taxonomy does not appear to include all of the key features of digital money tokens and is more focused on token implementation mechanics.

Efforts by regulators and international associations to develop taxonomies for digital tokens began in response to increasing consumer adoption of ‘cryptocurrencies’. This included a Financial Action Task Force (FATF) report [15] defining ‘virtual currencies’ and presenting a taxonomy based on convertibility and centralisation. These efforts to develop taxonomies continued partly in response to an increasing number of Initial Coin Offerings (ICOs). For example, guidelines by the Swiss Financial Market Supervisory Authority (FINMA) [39] used the term ‘payment token’ and advice from the European Banking Authority (EBA) to the European Commission [13] used the term ‘payment/exchange/currency token’. The UK’s Financial Conduct Authority (FCA) took a different approach in its final guidance on crypto-assets [16] by defining a taxonomy for tokens based on whether they are regulated. The two main categories were ‘regulated tokens’ (including ‘security tokens’ and ‘e-money tokens’) and ‘unregulated tokens’ (including ‘exchange tokens’ and ‘utility tokens’).

Recent consultations by BCBS [4], the European Commission [12] and the FSB [17], revised guidance from FINMA [40] and reports from BIS’ Committee on Payments and Market Infrastructures (CPMI) [20] and the International Organization of Securities Commissions (IOSCO) [42] in response to the rise of ‘stablecoins’ provided a more detailed view of features of digital money tokens. These features included stabilisation mechanisms, nature of asset linkage, type of asset linked, nature of the claim, accessibility, reach, redemption mechanics, permissioning model, transaction record model, and dependence on existing payments infrastructure. The IOSCO report states that “…many so-called stablecoins are neither ‘stable’ nor ‘coins’ in the true sense of either word. So, whilst stablecoin is a marketing term that has been widely adopted by industry, more neutral terms, may be more accurate starting points for regulatory analysis”.

The European Central Bank (ECB) has defined a visual taxonomy for stablecoins [14] in the form of a ‘crypto-cube’ based on three features: the existence of an issuer responsible for satisfying any attached claim, whether decision-making responsibilities over the stablecoin initiative are centralised, and what underpins the value of a stablecoin (currency, other off-chain assets, on-chain assets or expectations). This taxonomy comprises four types of stablecoins: tokenised funds, off-chain collateralised stablecoins, on-chain collateralised stablecoins and algorithmic stablecoins. Although the ‘crypto-cube’ is a useful visual tool for categorising stablecoins, it does not include all of the key features of digital money tokens.

GFMA’s initial approach for a classification of crypto-assets [22] is based on four features: issuer, mechanism or structure underlying the asset value (e.g. pegged to an underlying asset or access to a service), rights conferred (e.g. cash flows, redemption), and nature of the claim (e.g. claim on issuer or claim on underlying asset). They propose a taxonomy comprising six types of crypto-assets: ‘cryptocurrencies’, ‘value-stable crypto-assets’, ‘security tokens’, ‘settlement tokens’, ‘utility tokens’, and ‘other crypto-assets’.

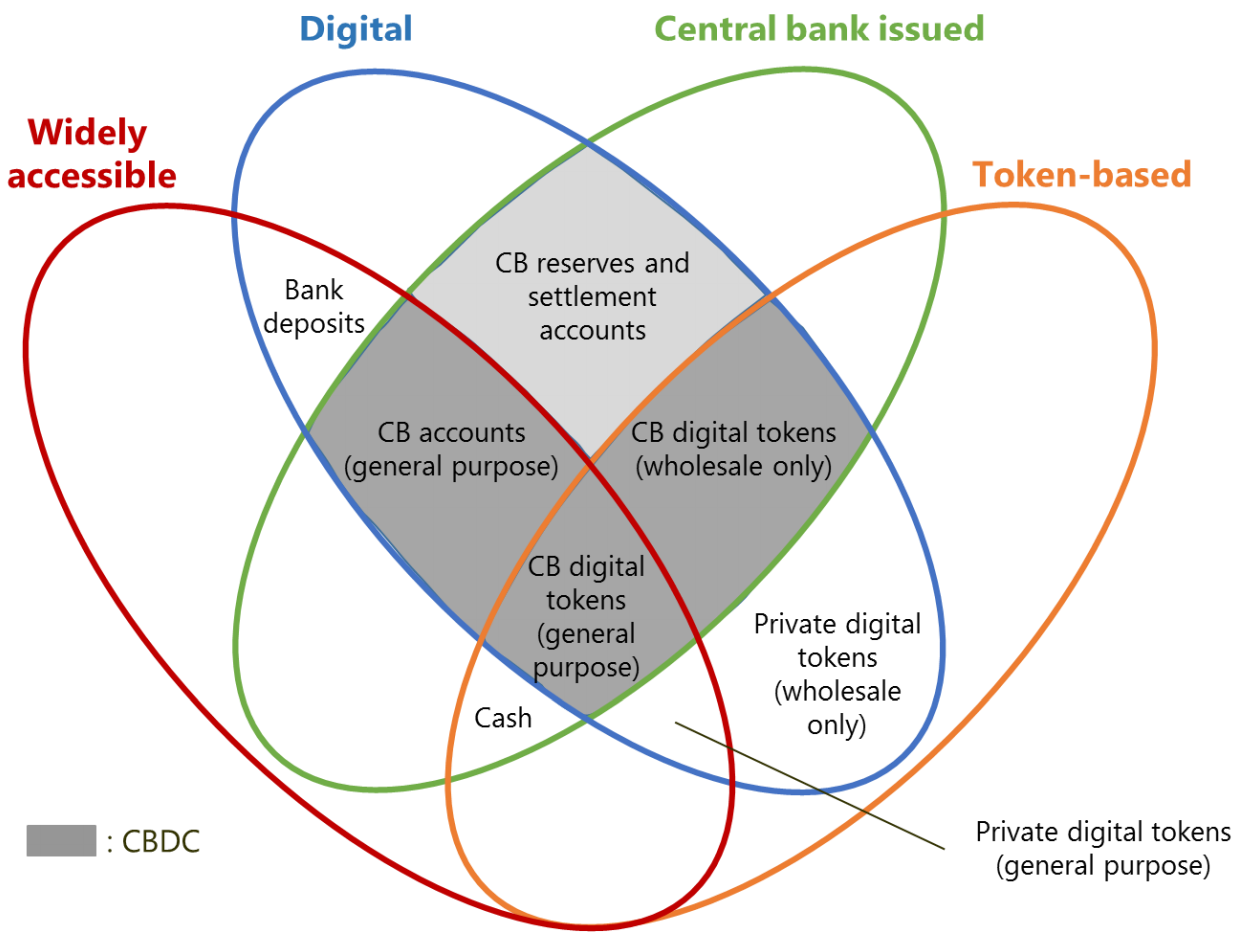

3.1 The Money Flower

Bech and Garratt created the money flower [5] to support a new taxonomy of money by showing how forms and specific examples of money fit into the overall monetary landscape. In this section, we reproduce CPMI’s adaption of the money flower [11] in Figure 2 which depicts a taxonomy based on four features: issuer (central bank or not), form (digital or physical), accessibility (widely or restricted), and technology (account-based or token-based).

CPMI describes other properties of money that are not depicted on their money flower, including 24x7 availability, anonymity, whether peer to peer transfers are supported, whether interest is borne, and if any limits are imposed on holdings.

Digital money tokens are represented on CPMI’s money flower as the intersection of the ‘Digital’ and ‘Token-based’ ellipses, i.e. the four areas labelled ‘CB digital tokens (wholesale only)’, ‘CB digital tokens (general purpose)’, ‘Private digital tokens (wholesale only)’, and ‘Private digital tokens (general purpose)’.

3.2 Identifying the Key Features

Mark Carney’s speech on ‘The Future of Money’ [8] explored the ability of ‘cryptocurrencies’ to serve the three functions of money, i.e. store of value, medium of exchange and unit of account. In this section, we adopt a similar approach in order to evaluate the significance of the features of digital money tokens and identify the key features as follows:

-

•

Issuer: An identifiable entity that controls the issuance of tokens, even if issued via a decentralised ‘smart contract’ 222We use the term ‘smart contract’ to refer to “…an automatable and enforceable agreement. Automatable by computer, although some parts may require human input and control. Enforceable either by legal enforcement of rights and obligations or via tamper-proof execution of computer code” [9] or an approved intermediary. While some digital money token arrangements do not have a specific issuer, in other arrangements an identifiable entity exercises control over this process even if token issuance is handled by a decentralised smart contract or an approved intermediary. The nature of this entity, its decisions regarding other key features (nature of claim, asset linkage, type of linked asset, redemption etc) and its ability to operate the token arrangement appropriately determine whether the digital money tokens issued can fulfill all three functions of money. As a result, this is likely to be the most significant feature.

-

•

Claim, Right or Interest: The nature of the claim, right or interest arising from ownership or control of a token. Depending on the digital token arrangement, the ownership of digital money tokens may or may not confer the owner with a claim, right or interest. The nature of this claim, right or interest can influence the token’s ability to serve as a store of value.

-

•

Asset Linkage: The nature of the linkage, if any, between the value of the token and an underlying asset or basket of assets. The linkage can be to part or all of an underlying asset. The nature of this linkage can affect the stability of the digital money tokens’ value and can thereby influence the token’s ability to serve as a store of value.

-

•

Type of Linked Asset: The type of asset linked to the token. The type of the linked asset can influence the token’s ability to serve as a store of value because volatility in the value of the asset will affect the value of the tokens. In addition, some linked asset types (e.g. cash denominated in a fiat currency) can also naturally serve as an underlying unit of account.

-

•

Redemption Rate 333We use the term ‘redemption rate’ instead of ‘exchange rate’ [20] because ‘exchanging’ the token is a more general term that includes other actions such as buying other assets from any entity using a token: The rate at which tokens are redeemed by the issuer or an approved intermediary against a pre-determined asset or set of assets. If the digital money token arrangement supports redemption of issued tokens, whether the redemption rate is fixed or variable impacts the stability of the token’s value, which can influence the token’s ability to serve as a store of value.

-

•

Denomination: The unit of account used to quantify token ownership. The denomination of a digital money token can affect its ability to serve as a unit of account. For example, retailers that quote prices in ‘cryptocurrencies’ typically update them frequently due to their volatility.

-

•

Accessibility: Accessibility distinguishes between tokens that are available everywhere to everyone and tokens that are restricted to certain agents or uses. This feature refers to restrictions, typically imposed by the issuer, such as only specific types of entities that can participate (e.g. regulated financial institutions) or only specific uses (e.g. wholesale banking transactions). Accessibility can influence the extent to which digital money tokens can serve as a medium of exchange.

As discussed previously, money is a social convention and it is therefore not sufficient for a digital money token to have all the above key features to be considered money because it also needs to be readily and easily accepted.

In addition to these key features, there are other features such as availability, anonymity, whether interest is borne, holding limits, reach, permissioning model, transaction record model, nature of supply, and dependence on existing payments infrastructure. While these features represent important design choices, they are likely to be of lesser significance because they are either subsumed under the above key features or have a smaller impact on whether a given digital money token can serve the three functions of money.

3.3 Options for the Key Features

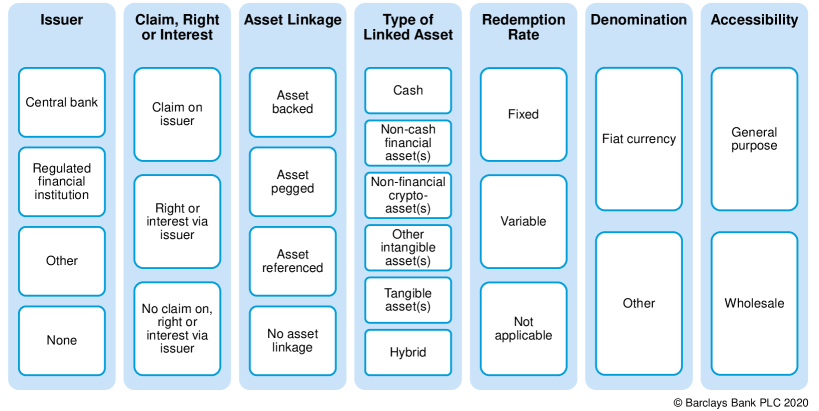

In order to develop a robust taxonomy, a list of key features and options is necessary. We now examine the potential options for each of the key features of digital money tokens, as summarised in Figure 3.

Table LABEL:table:digitaltokenmoney-features-options below describes these options for key features of digital money tokens, together with illustrative examples.

| Feature/Option | Description | Example(s) |

|---|---|---|

| Issuer | ||

| Central bank | Financial institution with privileged control over the production and distribution of money | e-Krona [38] |

| Regulated Financial Institution (FI) | Banks, Financial Market Infrastructures (FMIs) and other regulated FIs | USC [18], JPM Coin [29] |

| Other | Unregulated or non-financial entity | Tether [41] |

| None | No specific entity controls the issuance of tokens, issuance is managed entirely algorithmically | Bitcoin |

| Claim, Right or Interest | ||

| Claim on issuer | Legal claim on the issuer or an approved intermediary, typically exercised via instruction to the issuer or an approved intermediary | e-Krona, JPM Coin |

| Right or interest via issuer | No legal claim on the issuer, but right or interest (e.g. share of underlying asset) exercised via instruction to the issuer or an approved intermediary e.g. to redeem share | USC |

| No claim on, right or interest via issuer | No legal claim on the issuer, no right or interest exercised via issuer or no specific issuer | Bitcoin |

| Asset Linkage | ||

| Asset backed | Tokens are fully backed by underlying assets that are typically held or controlled by the issuer or an approved intermediary | USC, Single-currency Libra Coin [30] |

| Asset pegged | Tokens are not fully backed by assets but their value is fixed against one or more assets, typically by leveraging the financial strength and stability of the issuer | - |

| Asset referenced | Tokens are not fully backed by or pegged to assets but refer to assets to determine value | Dai [19] |

| No asset linkage | Tokens are not fully backed by, pegged to or referenced to any assets | Bitcoin |

| Type of Linked Asset 444We use the terms ‘tangible assets’, ‘cash’, ‘financial assets’ and ‘intangible assets’ based on the International Financial Reporting Standards (IFRS). The treatment of ‘crypto-assets’ is based on guidance from the IFRS Interpretations Committee [24] and the Institute of Singapore Chartered Accountants [26]. Linkage to an asset is different from linkage to a basket of assets of the same type, but these options are listed together for brevity | ||

| Cash | Tokens are linked to cash denominated in a fiat currency | USC |

| Non-cash financial asset(s) | Tokens are linked to a non-cash financial asset or a basket of such financial assets (e.g. securities, contractual rights) | ArCoin [7] |

| Non-financial crypto-asset(s) | Tokens are linked to a crypto-asset or a basket of crypto-assets that do not represent cash or other financial assets (e.g. Ether) | Dai |

| Other intangible asset(s) | Tokens are linked to an intangible asset not covered by the above options (e.g. intellectual property, digital goods) or a basket of such assets | - |

| Tangible asset(s) | Tokens are linked to a tangible asset (e.g commodities, real estate) or a basket of tangible assets | PMGT [25] |

| Hybrid | Tokens are linked to a basket of two or more of the above asset types | Single-currency Libra Coin |

| Redemption Rate | ||

| Fixed | Tokens can be redeemed against pre-determined assets at a fixed rate | USC, JPM Coin |

| Variable | Tokens can be redeemed against pre-determined assets at a variable rate | Multi-currency Libra Coin |

| Not applicable | Tokens cannot be redeemed or there is no issuer | Bitcoin |

| Denomination | ||

| Fiat currency | Tokens are denominated in a fiat currency or are redeemable in a fiat currency at a fixed rate | e-Krona, USC |

| Other | Tokens have their own independent denomination | Multi-currency Libra Coin |

| Accessibility | ||

| General purpose | Tokens are intended for general use, including both retail and wholesale purposes | e-Krona, Libra Coin |

| Wholesale | Tokens where access is restricted, for example to FIs or selected clients of FIs | USC, JPM Coin |

4 Summary

In this paper, we presented a ‘money tree’ which placed the recent concept of digital money tokens into a historical context by illustrating their evolution from more traditional forms of money. We then identified the key features of digital money tokens with options and examples. The money tree and the list of key features and options contributes to the design space for the emerging field of digital money tokens. We hope this paper will be of interest to the financial services industry as it innovates with digital money tokens. We welcome feedback and look forward to continuing industry collaboration on the the classification of digital money tokens. In particular, international collaboration between financial institutions, central banks, regulators, associations and fintechs will enable the development of global standards.

Acknowledgements

The author would like to thank Lee Braine (Barclays) for direction, input and review of this paper. Thanks are also due to Nicole Sandler (Barclays), Vikram Bakshi (Barclays), Richard Barnes (Barclays) and Simon Gleeson (Clifford Chance) for their helpful feedback.

References

- [1] Tobias Adrian and Tommaso Mancini-Griffoli. The Rise of Digital Money. FinTech Note 19/01, International Monetary Fund, 2019. https://www.imf.org/~/media/Files/Publications/FTN063/2019/English/FTNEA2019001.ashx.

- [2] Association for Financial Markets in Europe. Consultation response: European Commission Public Consultation - An EU Framework for Markets in Crypto-assets. 2020. https://www.afme.eu/Portals/0/DispatchFeaturedImages/2020%2003%2019%20AFME%20EC%20Legal%20Framework%20for%20Crypto-assets.pdf.

- [3] Bank of England. What is money? https://www.bankofengland.co.uk/knowledgebank/what-is-money, 2020. Accessed 13 July 2020.

- [4] Basel Committee on Banking Supervision. Designing a prudential treatment for cryptoassets. Discussion paper, BIS, 2019. https://www.bis.org/bcbs/publ/d490.pdf.

- [5] Morten Bech and Rodney Garratt. Central bank cryptocurrencies. In BIS Quarterly Review, pages 55–70. BIS, September 2017. https://www.bis.org/publ/qtrpdf/r_qt1709f.pdf.

- [6] Ole Bjerg. Designing New Money: The Policy Trilemma of Central Bank Digital Currency. Working Paper, Copenhagen Business School, 2017. https://research-api.cbs.dk/ws/portalfiles/portal/58550948/Designing_New_Money_The_policy_trilemma_of_central_bank_digital_currency.pdf.

- [7] Charles Bovaird. Arca Uses Ethereum In First SEC-Registered Fund For Digital Shares. https://www.forbes.com/sites/cbovaird/2020/07/06/arca-launches-first-sec-registered-fund-to-offer-digital-shares, 2020. Accessed 20 July 2020.

- [8] Mark Carney. The Future of Money. In Scottish Economics Conference. Edinburgh University, 2018. https://www.bankofengland.co.uk/-/media/boe/files/speech/2018/the-future-of-money-speech-by-mark-carney.pdf.

- [9] Christopher D Clack, Vikram A Bakshi, and Lee Braine. Smart contract templates: foundations, design landscape and research directions. The Computing Research Repository (CoRR), abs/1608.00771, 2016. https://arxiv.org/pdf/1608.00771.

- [10] Committee on Payments and Market Infrastructures. Digital Currencies. CPMI Papers 137, BIS, 2015. https://www.bis.org/cpmi/publ/d137.pdf.

- [11] Committee on Payments and Market Infrastructures. Central bank digital currencies. CPMI Papers 174, BIS, 2018. https://www.bis.org/cpmi/publ/d174.pdf.

- [12] Directorate-General for Financial Stability, Financial Services and Capital Markets Union. On an EU framework for markets in crypto-assets. Consultation document, European Commission, 2019. https://ec.europa.eu/info/sites/info/files/business_economy_euro/banking_and_finance/documents/2019-crypto-assets-consultation-document_en.pdf.

- [13] European Banking Authority. Report with advice for the European Commission on crypto-assets. 2019. https://eba.europa.eu/sites/default/documents/files/documents/10180/2545547/67493daa-85a8-4429-aa91-e9a5ed880684/EBA%20Report%20on%20crypto%20assets.pdf.

- [14] European Central Bank. Stablecoins - no coins, but are they stable? In Focus, Issue No 3, 2019. https://www.ecb.europa.eu/paym/intro/publications/pdf/ecb.mipinfocus191128.en.pdf.

- [15] Financial Action Task Force. Virtual Currencies: Key Definitions and Potential AML/CFT Risks. 2014. http://www.fatf-gafi.org/media/fatf/documents/reports/Virtual-currency-key-definitions-and-potential-aml-cft-risks.pdf.

- [16] Financial Conduct Authority. Guidance on Cryptoassets: Feedback and Final Guidance to CP 19/3. Policy Statement PS19/22, 2019. https://www.fca.org.uk/publication/policy/ps19-22.pdf.

- [17] Financial Stability Board. Addressing the regulatory, supervisory and oversight challenges raised by “global stablecoin” arrangements. Consultative document, 2020. https://www.fsb.org/wp-content/uploads/P140420-1.pdf.

- [18] Fnality International. What we do. https://www.fnality.org/what-we-do, 2019. Accessed 30 June 2020.

- [19] Maker Foundation. The Maker Protocol: MakerDAO’s Multi-Collateral Dai (MCD) System. https://makerdao.com/en/whitepaper, 2019. Accessed 29 July 2020.

- [20] G7 Working Group on Stablecoins. Investigating the Impact of Global Stablecoins. CPMI Papers 187, BIS, 2019. https://www.bis.org/cpmi/publ/d187.pdf.

- [21] Global Financial Markets Association. Consultation response: Basel Committee on Banking Supervision - Designing a Prudential Treatment for Crypto-Assets. 2020. https://www.gfma.org/wp-content/uploads/2020/04/gfma-bcbs-prudential-crypto-assets-final-consolidated-version-20200427.pdf.

- [22] Global Financial Markets Association. Consultation Response: Financial Stability Board - Addressing the regulatory, supervisory and oversight challenges raised by “global stablecoin” arrangements. 2020. https://www.fsb.org/wp-content/uploads/GFMA-1.pdf.

- [23] Noble Foster Hoggson. Banking Through the Ages. Dodd, Mead and Company, New York, 1926.

- [24] IFRS Interpretations Committee (IFRIC). Holding of Cryptocurrencies. IFRIC Interpretations, International Accounting Standards Board, June 2019. https://cdn.ifrs.org/-/media/feature/supporting-implementation/agenda-decisions/holdings-of-cryptocurrencies-june-2019.pdf.

- [25] InfiniGold. Perth Mint Gold Token: Whitepaper ver. 1.1. https://pmgt.io/static/assets/pmgt_whitepaper.pdf, 2019. Accessed 20 July 2020.

- [26] Institute of Singapore Chartered Accountants. Accounting for Cryptoassets: From a Holder’s Perspective. ISCA Financial Reporting Guidance FRG 2, 2020. https://isca.org.sg/media/2824062/frg-2-accounting-for-cryptoassets-from-a-holder-s-perspective.pdf.

- [27] InterWork Alliance. Token Taxonomy Framework. https://github.com/InterWorkAlliance/TokenTaxonomyFramework, 2020. Accessed 07 July 2020.

- [28] Katsuhito Iwai. Evolution of Money. In Ugo Pagano and Antonio Nicita, editors, Evolution of Economic Diversity, pages 396–441. Routledge, 1997. https://ssrn.com/abstract=1861952.

- [29] J.P. Morgan. J.P. Morgan Creates Digital Coin for Payments. https://www.jpmorgan.com/global/news/digital-coin-payments, 2019. Accessed 30 June 2020.

- [30] Libra Association Members. Libra White Paper v2.0. https://libra.org/en-US/white-paper, 2020. Accessed 30 June 2020.

- [31] Gerardo Licandro. Uruguayan e-Peso on the context of financial inclusion. In Conference on “Economics of Payments IX”. BIS, 2018. https://www.bis.org/events/eopix_1810/licandro_pres.pdf.

- [32] Alistair Milne. Argument by False Analogy: The Mistaken Classification of Bitcoin as Token Money. 2018. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3290325.

- [33] Alfred Mitchell-Innes. What is money? The Banking Law Journal, pages 377–408, 1913. https://www.newmoneyhub.com/www/money/mitchell-innes/what-is-money.html. Accessed 30 June 2020.

- [34] Monetary Authority of Singapore and Temasek. Project Ubin Phase 5: Enabling Broad Ecosystem Opportunities. 2020. https://www.mas.gov.sg/-/media/MAS/ProjectUbin/Project-Ubin-Phase-5-Enabling-Broad-Ecosystem-Opportunities.pdf.

- [35] David Orrell and Roman Chlupatý. The Evolution of Money. Columbia University Press, 2016.

- [36] Joe Thierry Arys Ruiz and Abdul-Hadi Bashir Subhia. Agau and the new taxonomy of money. Research Report, Tarco International, 2018. https://www.researchgate.net/profile/Joe_Thierry_Ruiz/publication/330564376_AGAU_AND_THE_NEW_TAXONOMY_OF_MONEY/links/5d6414d5299bf1f70b0ea813/AGAU-AND-THE-NEW-TAXONOMY-OF-MONEY.pdf. Accessed 07 July 2020.

- [37] Adam Smith. An Inquiry into the Nature and Causes of the Wealth of Nations. W. Strahan and T. Cadell, London, 1776.

- [38] Sveriges Riksbank. E-krona. https://www.riksbank.se/en-gb/payments--cash/e-krona, 2019. Accessed 30 June 2020.

- [39] Swiss Financial Market Supervisory Authority. Guidelines for enquiries regarding the regulatory framework for initial coin offerings (ICOs). 2018. https://www.finma.ch/en/~/media/finma/dokumente/dokumentencenter/myfinma/1bewilligung/fintech/wegleitung-ico.pdf?la=en.

- [40] Swiss Financial Market Supervisory Authority. Supplement to the guidelines for enquiries regarding the regulatory framework for initial coin offerings (ICOs). 2019. https://www.finma.ch/en/~/media/finma/dokumente/dokumentencenter/myfinma/1bewilligung/fintech/wegleitung-stable-coins.pdf?la=en.

- [41] Tether. Tether: Fiat currencies on the Bitcoin blockchain. https://tether.to/wp-content/uploads/2016/06/TetherWhitePaper.pdf, 2016. Accessed 21 August 2020.

- [42] The Board of the International Organization of Securities Commissions. Global Stablecoin Initiatives. Public Report OR01/2020, IOSCO, 2020. https://www.iosco.org/library/pubdocs/pdf/IOSCOPD650.pdf.

- [43] Orla Ward and Sabrina Rochemont. Understanding Central Bank Digital Currencies (CBDC). An addendum to “A Cashless Society - Benefits, Risks and Issues (Interim paper)”, The Institute and Faculty of Actuaries, 2019. https://www.actuaries.org.uk/system/files/field/document/Understanding%20CBDCs%20Final%20-%20disc.pdf.

- [44] World Federation of Exchanges. WFE Response to the Financial Stability Board’s Consultation Document. 2020. https://www.world-exchanges.org/storage/app/media/wfe-response-to-the-fsbs-consultation-on-global-stablecoin.pdf.