Effects of positive jumps of assets on endogenous bankruptcy and optimal capital structure: Continuous- and periodic-observation models

Abstract.

In this paper, we study the optimal capital structure model with endogenous bankruptcy when the firm’s asset value follows an exponential Lévy process with positive jumps. In the Leland-Toft framework [18], we obtain the optimal bankruptcy barrier in the classical continuous-observation model and the periodic-observation model, recently studied by Palmowski et al. [22]. We further consider the two-stage optimization problem of obtaining the optimal capital structure. Detailed numerical experiments are conducted to study the sensitivity of the firm’s decision-making with respect to the observation frequency and positive jumps of the asset value.

AMS 2020 Subject Classifications: 60G40, 60G51, 91G40

JEL Classifications: C61, G32, G33

Keywords: Credit risk, endogenous bankruptcy, optimal capital structure, spectrally positive Lévy processes

1. Introduction

The classical Leland model [17] studies the decision-making faced by a firm on the determination of the time of bankruptcy and capital structures. The model features the endogenous bankruptcy determined to solve the trade-off between maximizing the tax benefits and minimizing the bankruptcy costs. The Leland-Toft model [18] is an extension of the Leland model [17], that successfully avoids the use of perpetual bonds by considering a particular debt profile. It is regarded as one of the most important models in the fields of both corporate finance and credit risk.

In this paper, we focus on the effects of positive jumps of the firm’s asset value by considering a spectrally positive Lévy process (a Lévy process with only positive jumps) in the Leland-Toft model. In the past, the classical geometric Brownian motion model has been generalized successfully to several exponential Lévy models. With the motivation of avoiding an undesirable conclusion drawn in the geometric Brownian motion model that the credit spread approaches zero as the maturity decreases, a majority of papers have focused on analyzing the effects of negative jumps of the firm’s asset price process (see Hilberink and Rogers [10], Kyprianou and Surya [15], and Surya and Yamazaki [26]). On the other hand, as discussed by Chen and Kou [5], who considered the double jump diffusion (with i.i.d. exponential jumps in both directions), positive jumps in the asset value also have significant effects on the optimal capital structure and the credit spread. In this paper, we revisit the study of analyzing the influence of positive jumps by incorporating several features that are not considered in [5] and other related studies.

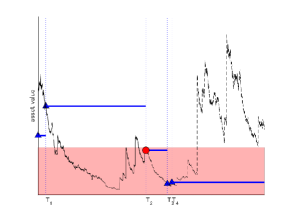

We consider the classical continuous-observation and periodic-observation models. In the continuous-observation model, the bankruptcy time is modeled by the first time the firm’s asset value , modeled by an exponential spectrally positive Lévy process, goes below a barrier :

| (1) |

The periodic-observation model, recently studied by Palmowski et al. [22] considers the scenario in which the asset value information is updated only at epochs , given by the jump times of an independent Poisson process with a fixed rate . The bankruptcy time is modeled as the first observation time at which the asset value process is below , namely,

As noted in [22], this is also written as the classical bankruptcy time (1) with replaced by the asset value if it is only updated at , namely,

| (2) |

where is the last observation time before . In Figure 1, we plot sample paths of , , and the corresponding bankruptcy time to illustrate these. We refer the reader to [22] for the detailed discussions on this model, in particular, regarding the connections with the reduced-form model and other models such as those by Duffie and Lando [6] and François and Morellec [9]. See also [3, 4, 7, 21, 24, 23] for optimal stopping and other stochastic control problems under Poisson observations.

|

In the periodic-observation model, as illustrated in Figure 1 (see in particular the interval between and ), the asset value can stay below between the observation times. It is of particular interest to study the event that the asset value recovers from the “bankruptcy zone” to the “non-bankruptcy zone” before the next observation time, and how the prospect of these events has effects on the firm’s decision-making. In the case of [22], where they focus on the spectrally negative case, this event can happen only by continuous increments. Its probability is thus significantly underestimated due to the assumption of no positive jumps. When positive jumps are allowed, the firm is expected to have a strong possibility for recovery. Thus, it is important to consider an asset value with positive jumps and analyze how these affect the firm’s decision-making.

We consider a general Lévy process with positive jumps of any arbitrary distribution. Chen and Kou [5] studied the case with exponential jumps in both directions. However, the exponential random variable has distinctive features that other random variables do not have. For example, as studied by Kou and Wang [11], double exponential diffusion admits the memoryless property that the distribution of the overshoot at up- or down-crossing times is conditionally the same as that of the original jumps. It is also in the class of distributions with completely monotone density, which are known to possess certain special properties. In [22], in the two-stage optimization problem (described subsequently), a completely monotone assumption on negative jumps was imposed to show the convexity of the firm value with respect to the leverage. Completely monotone assumptions of the Lévy measure are often assumed for the optimality of a barrier strategy in other stochastic control problems (see, e.g., Loeffen [19] for the optimal dividend problem). For these reasons, it is important to consider jumps with arbitrary distributions to analyze whether the same results hold as in [5]. Another feature we consider in this paper, which was not considered in [5], is the tax-benefit threshold. To avoid the overestimation of the tax benefits, as suggested in Hilberink and Rogers [10], we consider the cases in which tax benefits can be enjoyed only if the asset value is above a given threshold .

To solve both continuous-observation and periodic-observation cases, we use the fluctuation theory of Lévy processes. For the periodic-observation case, we use the recent results by Albrecher et al. [1] and Landriault et al. [16]. The firm/debt/equity values are expressed in terms of the so-called scale function, which is defined for a general spectrally one-sided Lévy process. In the continuous-observation model, the bankruptcy level satisfies the smooth fit condition. On the other hand, in the periodic-observation model, the bankruptcy level satisfies the continuous fit condition. The optimal capital structure is obtained by solving the two-stage optimization problem as proposed in [18]. We show the uniqueness of the optimal leverage for a general spectrally positive Lévy process (including the cases in which the jump size distribution does not have a completely monotone density).

Using these analytical results, we conduct a series of numerical experiments using the case driven by a mixture of Brownian motion and i.i.d. positive (folded) normal distributed jumps, whose scale function is approximated by fitting phase-type Lévy processes that admit an explicit form of the scale function. We verify the optimality of a selected bankruptcy level and then study the effects of the rate of observations and positive jumps. For the former, we confirm the monotonicity of the optimal bankruptcy level and its convergence to that in the continuous-observation case. For the latter, as conjectured above, positive jumps have significant effects on the optimal strategies. Interestingly, our numerical results reveal that is not monotone in the parameter of the jumps.

While we focus on the one-sided jump case, as discussed in [22], the periodic-observation case can be considered to be a case driven by processes with two-sided jumps (due to the equivalence of the bankruptcy time with the classical bankruptcy time (1) of the process ; see also Figure 1). While only a few models featuring asset value processes with two-sided jumps exist, we provide a new analytically tractable case for , that contains two-sided jumps even when does not have positive jumps. By suitably selecting the process and , a wide range of stochastic processes with two-sided jumps can be realized.

The rest of the paper is organized as follows. In Section 2, we introduce the relevant mathematical aspects of the driving stochastic process used in the models. We also introduce the general setting of the capital structure model for a firm, and the equity maximization problem. In Sections 3 and 4, we derive the fluctuation identities for spectrally positive Lévy processes under continuous and periodic observations, respectively, and show the existence of the optimal bankruptcy barriers that solve the Leland-Toft problem both in the continuous and periodic cases. Section 5 considers the two-stage problem to obtain the optimal capital structure, where we aim to maximize the value of the firm in terms of the total face value of the debt. Section 6 presents numerical examples that illustrate the results derived in the earlier sections. We conclude the paper in Section 7. Some proofs and a review of the fluctuation identities for the spectrally negative Lévy process are given in the Appendix.

2. Preliminaries

Let be a complete probability space hosting a Lévy process with . To be more precise, is a real-valued stochastic process with independent and stationary increments, and with càdlàg sample paths such that . In this work, we will work with spectrally positive Lévy processes, i.e., Lévy processes without negative jumps. These processes are characterized by their Laplace exponent

where, by the Lévy-Khintchine formula,

| (3) |

where , and is a measure, called the Lévy measure, supported on that satisfies

It is known that has paths of bounded variation if and only if and ; in this case we can write

where and is a driftless subordinator. In order to avoid having processes with monotonous paths, we set (when is of bounded variation).

2.1. Formulation of the Leland-Toft model

The value of the firm’s asset is assumed to evolve according to an exponential Lévy process given by

where the initial value is strictly positive. Let be the risk-free interest rate and the total payout rate to the firm’s investors.

The firm is partly financed by debt, which is being constantly retired and reissued in the following way: for some given constants , the firm issues new debt at a constant rate with maturity profile . Consequently, the face value of the debt issued in the time interval that matures in the time interval is given by . Assuming an infinite past, the face value of the debt held at time 0 and maturing in the interval is

and hence the total value of the debt is a constant given by

A bankruptcy event is determined endogenously by the firm’s shareholders, in terms of the firm’s assets and a given set of times . Given an asset value level , bankruptcy is triggered at the first time the asset value is observed to fall below this threshold. In other words, we define the time of bankruptcy as

Here and for the rest of the paper, we set . We will study the case of continuous-observations, i.e., when ; as well as the case of periodic observations, where is the set of jump times of a time-homogeneous Poisson process with rate independent of .

Upon bankruptcy, a fraction of the asset value is lost due to re-organization and operational costs, while the remaining asset value is paid out to bondholders. We assume that the debt is of equal seniority, so that a fraction of the remaining asset value is distributed equally among bondholders.

The debt pays out coupons at a constant rate , which are accumulated until maturity or bankruptcy, whichever comes first. Note that the remaining coupon payments are lost when bankruptcy occurs. In this setting, the value of the debt with unit face value and maturity date is

| (4) |

By integrating expression (4) and using Fubini’s Theorem, the total value of the debt becomes

| (5) |

We follow the trade-off theory and we assume that the value of the firm is determined by tax rebates on coupon payments, and by bankruptcy costs. Regarding the tax rebates, we assume that there is a corporate tax rate and a cutoff level that determines the effect of tax rebates on coupons. Whenever the asset value is above this level, the tax rebates are accrued continuously at rate , otherwise these rebates are equal to 0. On the other hand, we know that bankruptcy costs are given by . Under these assumptions the value of the firm is

| (6) |

Finally, the value of the firm’s equity is

| (7) |

The problem is to find the optimal bankruptcy threshold that maximizes the equity value subject to the limited liability constraint

| (8) |

3. Optimal bankruptcy level under continuous observations

Our first subject of study will be solving the optimal capital structure problem under the assumption that the firm’s assets are observed continuously. In this model the bankruptcy decision is taken instantaneously, as soon as the asset value falls below the level , and hence the bankruptcy time is defined as

We derive expressions for the debt, firm, and equity values by using results from the Fluctuation Theory for spectrally one-sided Lévy processes. From these expressions, we will be able to analyze and solve the Leland-Toft optimal capital structure problem, i.e., finding the bankruptcy-triggering level that maximizes the equity value under the limited liability constraint (8).

3.1. Fluctuation identities for spectrally positive Lévy processes

We present some fluctuation identities for spectrally positive Lévy processes, which will be given in terms of the so-called scale functions. For , we denote the expectation operator associated with the spectrally positive Lévy process started at by .

Recall the Laplace exponent of the spectrally positive Lévy process given in (3). We define its right-continuous inverse by:

Definition 1 (Scale function).

For each , the -scale function is the unique function such that for all , and, on , it is a strictly increasing and continuous function whose Laplace transform is given by

We also define the second scale function:

| (9) |

In particular, we write .

Remark 1 (Smoothness of the scale function).

For the case where is of unbounded variation, . On the other hand, when is of bounded variation, . For both cases, the right-hand derivative of exists for all . See, Chapter 8 of [15] for more details and related results.

For the spectrally positive Lévy process we denote the first passage time below and above by

| (10) |

Due to the absence of negative jumps, we have -a.s. for ,

| (11) |

Lemma 1.

For all and , the Laplace transform of is given by

| (12) |

Note that is differentiable on , with its derivative given by

| (13) |

Moreover, is right-differentiable at , and its right-hand derivative is given by

| (14) |

Remark 2.

Using (11) we have that for any and ,

We also define the function as

Observe that for all since implies that almost surely. The following result gives an explicit expression for the function .

Lemma 2.

For and we have

where

Note that this function is also differentiable on

| (15) |

It is also right-differentiable at with right-hand derivative given by

| (16) |

3.2. Determining the optimal bankruptcy level

Recall that in the context of the Leland-Toft model, we are seeking to maximize the expected equity value upon the event of bankruptcy.

Suppose and . When we have that , and hence implying . Hence, throughout the rest of the section we assume . Based on the calculations in Lemmas 1 and 2, and using the fact that on since has no negative jumps, we can express the value of the firm and the total value of the debt as

| (17) | ||||

| (18) |

Hence, the equity value is given by

| (19) |

In particular, when we have , and the equity value is given by

| (20) |

For the case , the equity value is given later in (30) (as we see immediately below, when the optimal barrier is zero, necessarily ).

Remark 3.

Since and satisfy and , we have that for all .

Our aim is to show that satisfying

| (21) |

is optimal if such level exists. First, by (19) and (20), together with (14) and (16),

| (22) |

where

| (23) |

with

| (24) |

Using that and we note that .

In other words, condition (21) is equivalent to

| (25) |

Remark 4.

We will find conditions under which the level satisfying (25) exists and is unique.

Lemma 3.

The function is strictly increasing on with

Proof.

(i) First, for , by differentiating (23),

with

where the term is understood as the right-hand derivative of , if it is not differentiable (see Remark 1). The function is non-negative because it is the -resolvent density of the descending ladder height process of (see Section 2.4 in Pistorius [25]). It follows that

| (26) |

On the other hand, using (23) we note that

| (27) |

Hence, identities (26) and (27) imply that is strictly increasing on .

Following equation (42) in [13], we have

and hence we have

| (28) |

This allows us to simplify the expression for as

| (29) |

As , we have . On the other hand, we have that the mapping is non-negative, and monotone increasing on , hence the limit as exists, and it is equal to 0. Thus, by substituting this limit into the alternate form of given in (29), we get

On the other hand, by noting that as and the fact that

we have

(ii) Now, when we have that is linear with unit slope on , hence it is strictly increasing and . Additionally, by (23) we have

∎

3.3. Optimality of

In order to show that is the optimal barrier, it suffices to verify the following.

-

(1)

Any level below violates the limited liability condition (8).

-

(2)

achieves a higher equity value than any level does.

-

(3)

fulfills the limited liability condition (8).

These are confirmed in the following three propositions.

Proposition 1.

Suppose . For , the limited liability constraint (8) is not satisfied.

Proof.

Proposition 2.

For all , we have .

Proof.

Fix . We will show that the mapping is monotonically decreasing on . By differentiating with respect to , we obtain

| (31) |

and, for ,

| (32) |

By applying expressions (31) and (32) in (19), we get for

| (33) |

where

After rearranging terms, we can rewrite as

| (34) |

Note that the first and second terms in the right-hand side of (3.3) are non-positive since , , is a non-negative and strictly increasing function, and because for . For the last term, if , and otherwise we use the fluctuation identity (28) to write

Hence the last term in (3.3) is non-positive as well. Thus, for all ,

| (35) |

Hence, the proof follows from the continuity of the mapping together with (35). ∎

Proposition 3.

The level satisfies the limited liability constraint (8).

Proof.

(i) Suppose . For by differentiating the equity value with respect to and using (13) together with (15) we get for

After rearranging terms and using (3.3), we obtain for and

| (36) |

where we understand as the right-hand side of (3.3) for the case .

The right hand-side of (3.3) is positive. Indeed, the sum of the first two terms in the right hand side of (3.3) is non-negative, since , , and is strictly increasing; the third term is non-negative in light of Proposition 2 by (35); using that together with (60) (in the appendix) we obtain that the fourth term is non-negative as well. Hence using (3.3) together with the fact that the mapping is continuous and Remark 3 we obtain that for .

∎

Theorem 1.

The optimal bankruptcy level is given by .

4. Optimal bankruptcy level under periodic observations

We turn our attention to the problem of determining the optimal bankruptcy-triggering level when the asset value process, , is not observed continuously, but at a set of discrete times given by the arrival times of an independent Poisson process with intensity . We denote the collection of these times by . This assumption makes the model more realistic in the sense that shareholders do not observe the evolution of the firm’s asset continuously and instead they observe it at discrete times, and hence the decision to declare bankruptcy is taken at these observation dates.

For such a collection of times and a bankruptcy barrier , we define the first observed bankruptcy time as the stopping time

| (37) |

It is more realistic to assume that the bankruptcy decision can be made at time zero so that the bankruptcy time becomes . However, similar to the continuous observation case, we obtain zero equity value if the initial value and therefore we focus on the case and hence in the rest of this section.

In this setting, we are interested in proving the existence of an optimal bankruptcy level, denoted by , which maximizes the equity value (7) and satisfies the limited liability constraint (8).

Remark 5.

Intuitively we expect that the first observed bankruptcy time will converge to the classical bankruptcy time as . We also expect that the expressions and results derived in this Section will converge to the ones shown in Subsection 3.2 as . These convergence results are confirmed numerically in Section 6.

We will develop expressions for the first observed passage time (37), the deficit and the resolvent measure under this setting of discrete time observations; in turn, these expressions will allow us to express the total value of debt (5), the value of the firm (6), and the equity value (7) in terms of the corresponding fluctuation identities.

4.1. Fluctuation identities for spectrally positive processes under periodic observations

In this setting, we are interested in the first observed time below of the Lévy process , which is defined as

| (38) |

as well as in the value of . In our setting, for a spectrally positive Lévy process started at the bankruptcy time given in (37) is equal to ; similarly, the asset value at bankruptcy is given by . The following lemma gives the joint Laplace transform of . This is a direct consequence of Theorem 3.1 in [1]; the proof is deferred to Appendix B.3.

Lemma 4.

For and , the joint Laplace transform of is given by

| (39) |

On the other hand, using the resolvent measure for spectrally negative Lévy processes observed at Poisson arrival times derived by Landriault et al. [16], we can obtain an expression for

| (40) |

The proof of the following proposition is given in Appendix B.4.

Proposition 4.

Let , and be fixed with . We have

| (41) |

Remark 6.

For and we have

4.2. Expression for the firm/debt/equity values in terms of the scale functions

We will use the expressions derived in Section 4.1 to write the firm, debt and equity values.

4.3. Determining the optimal bankruptcy level

Now we can move to finding the optimal bankruptcy threshold, denoted by . Our approach will be different from the calculations done in Section 3, since now we will find the optimal barrier through a continuous fit approach. In other words, we will find the optimal barrier as the solution of the equation

| (45) |

Our objective in this section is to show that there exists a unique solution to (45) under a certain condition, and that it is optimal in the sense of maximizing the equity value under the limited liability constraint (8).

First, note that for

| (46) |

where

| (47) | ||||

We need the following result in order to show the existence of .

Lemma 5.

The mapping is non-decreasing on with the limit

Proof.

Suppose . By (40) together with the spatial homogeneity of the Lévy process,

As we can note from the previous identity, we have that the mapping is non-decreasing, and by bounded convergence .

On the other hand, for identity (40) implies that . ∎

This result leads to the following proposition, which describes the limiting behavior of .

Proposition 5.

The mapping is strictly increasing on with the limits:

where

| (48) |

Proof.

4.4. Optimality of

We now verify that the barrier indeed maximizes the equity value subject to the limited liability constraint. To this end, we will verify the following.

Proposition 6.

Suppose . For the limited liability constraint is not satisfied.

Proof.

By the (strict) monotonicity as in Proposition 5 and because (given that ), we have for , and hence the constraint fails to hold. ∎

The following results describe the behavior of the mapping on .

Lemma 6.

For , we have

where, for ,

Proof.

First, for and , the derivative of (39) is given by

| (49) |

and hence

| (50) |

From the definition of given in (9), we get the identity

| (51) |

Hence, by differentiating (41), substituting (51), and grouping terms, we get

| (52) |

where the last equality holds by Remark 6. Now, from expression (44), and by the chain rule we have

The result now follows by substituting expressions (49)–(52) for . ∎

The next result shows that attains a higher equity value than any other does.

Proposition 7.

For , we have . Hence for all .

Proof.

Now it is left to show that the optimal barrier satisfies the limited liability condition.

Lemma 7.

Proof.

Proposition 8.

The barrier satisfies the limited liability constraint.

Proof.

(i) First, we suppose that , and take . By combining Proposition 7 and Lemma 7 and using that in view of (39), and that is the resolvent density (which is nonnegative), we get for

The claim follows by applying this, the continuity of the mapping , and by using that .

(ii) On the other hand when , which in turn implies that , we have

By the convexity of on , we have and . Hence

and therefore . Now

where the first inequality holds because also means . This implies , and hence is nonnegative. ∎

Theorem 2.

The optimal bankruptcy level in the periodic case is given by .

5. Two-stage problem

We turn our attention to the problem of determining an optimal value of the face value of debt , say , such that the firm value is maximized. As pointed out by Chen and Kou [5], this problem is entangled with the problem of determining the optimal bankruptcy-triggering level. We can see this in the expressions derived in Subsections 3.2 and 4.3, where and can be seen as functions of . Here we will find , and according to a two-stage optimization problem similar to those in Leland [17] and Leland and Toft [18]. In our case, we will solve the two-stage optimization problem both in the continuous- and in the periodic-observation cases. Recently, Palmowski et al. [22] solved it for the spectrally negative case under periodic observations.

The first-stage optimization is the problem of determining the optimal bankruptcy-triggering level which maximizes the equity value, subject to the limited liability constraint. From the calculations up to this point, we note that such level depends on the debt level , and hence we will write and , respectively. Once this bankruptcy level is determined for each , the firm will conduct a second-stage optimization in order to maximize its firm value in terms of . This second-stage optimization is formulated as

| (55) |

where we modify the notation of to emphasize the dependency on .

Assumption 1.

5.1. Continuous-observation case

We first consider the continuous-observation case. Here, recall defined in (24). By the following theorem, there exists an optimal value of that attains (55).

Theorem 3 (Continuous Observations).

In the case of continuous observations, we have the following.

-

(i)

First-stage optimization. (a) If , then for all . (b) Otherwise, define . Given a debt level , the optimal bankruptcy barrier is given by .

-

(ii)

Second-stage optimization. (a) If , then , which is linear (and hence convex) in . (b) Otherwise, for any , the firm value is strictly concave in on .

Proof.

(a) Suppose . Recalling the assumption that , we know from Section 3.2 that for this case for all , showing (i). Moreover, substituting into the value of the firm given by (6), yields that . This shows (ii).

(b) Now, suppose . We have that is strictly positive and by Remark 4, it satisfies the condition . Hence, from we get

| (56) |

proving (i).

5.2. Periodic-observation case

The formulation of the solution to the two-stage problem for the periodic case is similar to Palmowski et al. [22]. However in our case we do not need to make any additional assumption on the jump measure to guarantee the existence of the solution. Similar to Theorem 3, for the periodic-observation case, there exists an optimal value of such that (55) is attained.

Theorem 4 (Periodic Observations).

In the case of periodic observations, we have the following:

-

(i)

First-stage optimization. (a) If , where is defined in (48), we have for all . (b) Otherwise, with , then for all .

-

(ii)

Second-stage optimization. (a) If , then , which is linear (and hence convex) in . (b) Otherwise, for any , the firm value is a strictly concave function in on .

Proof.

(a) The fact that for the case , follows by construction as in Section 4.3. Moreover, by substituting into expression (42) we get .

(b) Now we consider the case . Recall that satisfies the continuous fit condition

Hence, by setting (46) equal to 0 and using (41), we obtain

which can be re-arranged as

| (57) |

proving (i). By (57), .

For (ii), we obtain from expression (42) together with (41) and (57), that the firm value is given by

By differentiating with respect to we get

Note that

Hence, with this fact and by grouping terms, we can write

Since the mapping is strictly decreasing for all , we conclude that is strictly decreasing in . Hence the value of the firm is a strictly concave function of on the interval , which proves our claim. ∎

6. Numerical Examples

We conclude this paper through a sequence of numerical results, focusing on the case where is given by a mixture of Brownian motion and a compound Poisson process with i.i.d. phase-type distributed jumps:

| (58) |

where is a standard Brownian motion, is a Poisson process with intensity and takes a phase-type random variable that approximates a (folded) normal random variable with mean zero and variance (whose parameters are given in [8]).

We use the same parameter sets as those used in [22] (who use the same parameters as those in [5, 10, 15, 17, 18]): we set , , , , , , and . Because , we must have and .

The scale function for the Lévy process of the form (58) admits an explicit expression written as a sum of exponential functions (usually with complex-valued coefficients); see e.g. [8, 13]. In particular, we consider the following parameters: , , ( is chosen so that the martingale property is satisfied). Unless stated otherwise, we set and, for the periodic case, (on average four times per year).

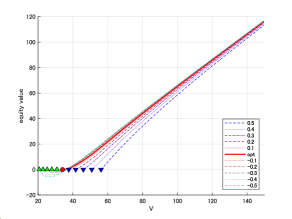

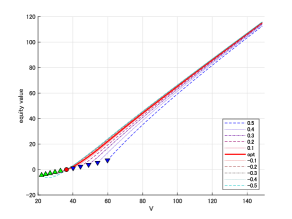

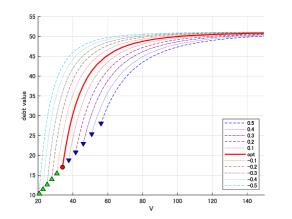

6.1. Optimality

We first confirm the optimality of the suggested barrier and for both continuous- and periodic-observation cases, which are given by (25) and (45), respectively. Because these functions are monotone, we can apply classical bisection methods. The corresponding firm/debt/equity values can be computed by (17), (18), and (19) for the continuous-observation case and (42), (43), and (44) for the periodic-observation case.

At the top of Figure 2, for both continuous and periodic cases, we plot and along with for and , respectively. The optimality as in Theorems 1 and 2 can be confirmed. For the continuous-observation case, the level satisfies the limited liability constraint (8), and any level lower than violates (8). The same can be observed for the periodic case. We also confirm the smooth fit for the continuous-observation case and continuous fit for the periodic-observation case.

|

|

| Continuous: equity value | Periodic: equity value |

|

|

| Continuous: debt value | Periodic: debt value |

|

|

| Continuous: firm value | Periodic: firm value |

6.2. Sensitivity with respect to of the equity value

We next study the impacts of the rate of observation on the optimal strategies. In Figure 3, the equity value is shown for various values of the observation frequency along with those in the continuous-observation case. As increases, the optimal barrier decreases and converges to that in the continuous observation case. The convergence of the equity value is also confirmed. These results confirm the discussions given in Remark 5.

|

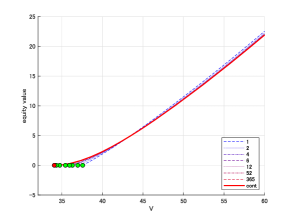

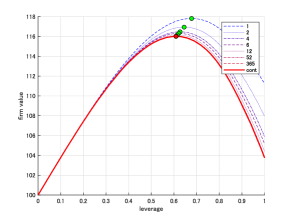

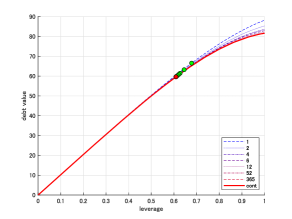

6.3. Two-stage problem

|

|

| firm value | debt value |

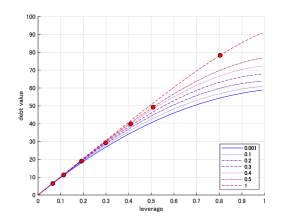

We now move onto the two-stage problem as studied in Section 5. In Theorems 3 and 4, the firm values and have been confirmed to be concave in for the case . To study if the same result holds when , we keep using as a function of .

For , we compute and for running from to (i.e. leverage running from to ) and then the corresponding firm and debt values for the continuous and periodic cases for various values of . The firm and debt values are given in Figure 4. At least in the considered cases, the concavity with respect to is confirmed. In addition, monotonicity with respect to of firm and debt values as well as the optimal barriers are also observed.

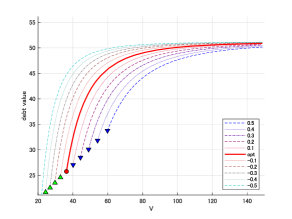

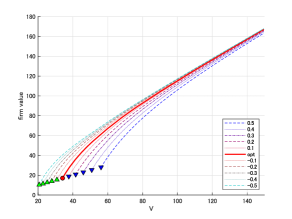

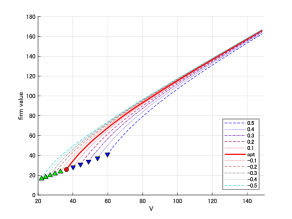

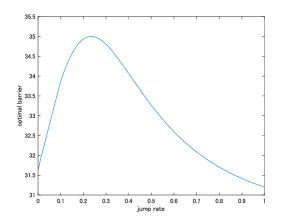

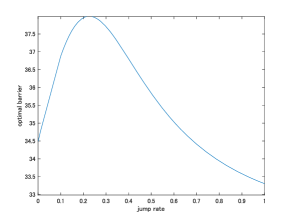

6.4. Sensitivity with respect to the jump rate

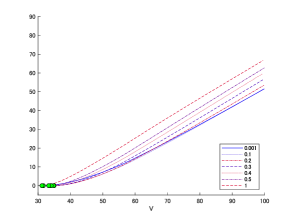

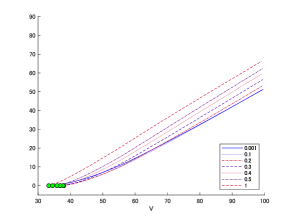

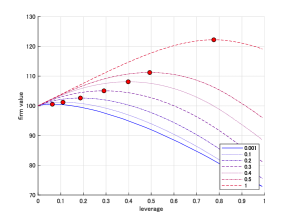

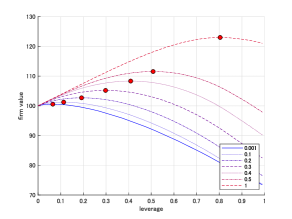

We now move onto analyzing the impact of the positive jumps of the process on the optimal bankruptcy levels as well as the optimal capital structure. To this end, we repeat the experiments conducted above for various values of the jump rate of positive jumps. In order to see easily the sensitivity with respect to , here we decide not to stick to the risk-neutral condition and simply change the value of (without changing the drift).

In Figure 5, we plot the equity values for various selections of and the bankruptcy levels and as functions of for both continuous- and periodic-observation cases, respectively. Interestingly, the equity value and the optimal bankruptcy level fail to be monotone. While this behavior with respect to is not entirely intuitive, our interpretation is given as follows.

When is sufficiently high, even when the current asset is low, one can expect sudden positive jumps to reach a healthy state above so that one can enjoy the tax shields, producing higher firm values. On the other hand, with low , this is unlikely to be achieved – as a result, the firm value does not increase as rapidly as the debt value does, resulting in the decrease of the equity value. Because the optimal barrier is the root of , it tends to increase, in , when is low but tends to decrease when is high.

In Figure 6, we further study how changes the optimal capital structures (similarly to what we studied in Figure 4). Contrary to what we observed in Figure 5, monotonicity with respect to holds at least in this considered case. In particular, the firm and debt values both tend to increase in . In addition, the optimal leverage increases as increases.

|

|

|

|

| continuous case | periodic case |

|

|

| Continuous: firm value | Continuous: debt value |

|

|

| Periodic: firm value | Periodic: debt value |

7. Concluding Remarks

In this paper, we studied the Leland-Toft optimal capital structure model when the asset value follows a spectrally positive Lévy process. We obtained explicitly the optimal endogenous bankruptcy level in both the continuous- and periodic-observation cases, written in terms of the scale function. The optimal capital structure was then obtained by considering the two-stage optimization problem. Our numerical results show that positive jumps of the asset value have significant impact on the firm’s decision-making. In particular, the optimal bankruptcy barrier fails to be monotone in the rate of positive jumps.

There are various venues for future research. By considering positive jumps of the asset value, this paper complements the results obtained in the spectrally negative model as in [10, 15, 26]. However, the assumption of no negative jumps has a drawback on the computation of credit spread, it tends to converge to zero as the maturity approaches zero. In order to analyze the credit spread more accurately, as done in [5], it is desirable to consider the cases with both positive and negative jumps. While a number of detailed analysis has been done in [5], it is of great interest to consider more general jump distributions and also periodic-observation cases. This may be possible for some Lévy processes such as the phase-type Lévy process [2] and the meromorphic Lévy process [12].

It is also of interest to consider other models of bankruptcy. The bankruptcy in the periodic-observation model considered in this paper can be seen as the Parisian ruin with exponential delay as discussed in the introduction of [22]. Bankruptcy is triggered at the first time the asset value stays continuously below the bankruptcy barrier for an independent exponential time. In this setting, the “distress level” of the firm is reset to zero each time the asset value goes above the barrier (before the exponential clock rings). On the other hand, as considered in [20], it is important to also consider the case the distress level accumulates (while the asset value is below the level) without being reset. For this extension, our approach using the fluctuation theory can potentially be used to obtain explicit solutions.

Appendix A Review of fluctuation identities for spectrally negative Lévy processes

In this section we review the fluctuation identities for spectrally negative Lévy processes. Let be the dual of , and let be the law of when (in particular, ).

We also recall the first passage time below a level under Poissonian observations defined in (38), which is equal in distribution to the first observed passage time above level of the dual process

Fix . The first identity is related to the first passage time above a level, and so as in Theorem 3.12 in [14] we have, for ,

| (59) |

In addition, as in Theorem 2.7 in [13] the -resolvent measure has a density written, for , as

| (60) |

For the case of periodic observations we have by Theorem 3.1 in [1] that, for ,

| (61) |

and by Theorem 3.1 in [16], for and ,

| (62) |

where, for ,

| (63) |

Appendix B Proofs

B.1. Proof of Lemma 1.

B.2. Proof of Lemma 2.

B.3. Proof of Lemma 4.

B.4. Proof of Proposition 4.

(i) Suppose . First, by the definition and using duality, we can write

where

We can use the identity (39) to compute which yields

| (66) |

For , we write the expectation in terms of the resolvent density. By applying (62), we have

where , and for the resolvent density is given by (63). Substituting the resolvent density gives

| (67) |

By the change of variable,

| (68) |

and

| (69) |

Substituting (68) and (69) back into (67) yields

| (70) |

(ii) On the other hand, if then for all and hence

References

- [1] H. Albrecher, J. Ivanovs, and X. Zhou, Exit identities for Lévy processes observed at Poisson arrival times, Bernoulli, 22 (2016), pp. 1364–1382.

- [2] S. Asmussen, F. Avram, and M. R. Pistorius, Russian and American put options under exponential phase-type Lévy models, Stochastic Processes and their Applications, 109 (2004), pp. 79–111.

- [3] B. Avanzi, E. C. Cheung, B. Wong, and J.-K. Woo, On a periodic dividend barrier strategy in the dual model with continuous monitoring of solvency, Insurance: Mathematics and Economics, 52 (2013), pp. 98–113.

- [4] B. Avanzi, V. Tu, and B. Wong, On optimal periodic dividend strategies in the dual model with diffusion, Insurance: Mathematics and Economics, 55 (2014), pp. 210–224.

- [5] N. Chen and S. G. Kou, Credit spreads, optimal capital structure, and implied volatility with endogenous default and jump risk, Mathematical Finance, 19 (2009), pp. 343–378.

- [6] D. Duffie and D. Lando, Term structures of credit spreads with incomplete accounting information, Econometrica, 69 (2001), pp. 633–664.

- [7] P. Dupuis and H. Wang, Optimal stopping with random intervention times, Advances in Applied Probability, 34 (2002), pp. 141–157.

- [8] M. Egami and K. Yamazaki, Phase-type fitting of scale functions for spectrally negative Lévy processes, Journal of Computational and Applied Mathematics, 264 (2014), pp. 1 – 22.

- [9] P. François and E. Morellec, Capital structure and asset prices: Some effects of bankruptcy procedures, The Journal of Business, 77 (2004), pp. 387–411.

- [10] B. Hilberink and L. C. G. Rogers, Optimal capital structure and endogenous default, Finance and Stochastics, 6 (2002), pp. 237–263.

- [11] S. G. Kou and H. Wang, First passage times of a jump diffusion process, Advances in Applied Probability, (2003), pp. 504–531.

- [12] A. Kuznetsov, A. E. Kyprianou, and J. C. Pardo, Meromorphic Lévy processes and their fluctuation identities, The Annals of Applied Probability, 22 (2012), pp. 1101–1135.

- [13] A. Kuznetsov, A. E. Kyprianou, and V. Rivero, The Theory of Scale Functions for Spectrally Negative Lévy Processes, Springer Berlin Heidelberg, Berlin, Heidelberg, 2013, pp. 97–186.

- [14] A. Kyprianou, Fluctuations of Lévy Processes with Applications: Introductory Lectures, Universitext, Springer Berlin Heidelberg, 2014.

- [15] A. E. Kyprianou and B. A. Surya, Principles of smooth and continuous fit in the determination of endogenous bankruptcy levels, Finance and Stochastics, 11 (2007), pp. 131–152.

- [16] D. Landriault, B. Li, J. T. Wong, and D. Xu, Poissonian potential measures for Lévy risk models, Insurance: Mathematics and Economics, 82 (2018), pp. 152 – 166.

- [17] H. E. Leland, Corporate debt value, bond covenants, and optimal capital structure, The Journal of Finance, 49 (1994), pp. 1213–1252.

- [18] H. E. Leland and K. B. Toft, Optimal capital structure, endogenous bankruptcy, and the term structure of credit spreads, The Journal of Finance, 51 (1996), pp. 987–1019.

- [19] R. L. Loeffen, On optimality of the barrier strategy in de Finetti’s dividend problem for spectrally negative Lévy processes, The Annals of Applied Probability, (2008), pp. 1669–1680.

- [20] F. Moraux, Valuing corporate liabilities when the default threshold is not an absorbing barrier, SSRN, (2002).

- [21] K. Noba, J.-L. Pérez, K. Yamazaki, and K. Yano, On optimal periodic dividend strategies for Lévy risk processes, Insurance: Mathematics and Economics, 80 (2018), pp. 29–44.

- [22] Z. Palmowski, J.-L. Pérez, B. Surya, and K. Yamazaki, The Leland-Toft optimal capital structure model under Poisson observations, Finance and Stochastics, published online (2020).

- [23] J.-L. Pérez and K. Yamazaki, American options under periodic exercise opportunities, Statistics & Probability Letters, 135 (2018), pp. 92–101.

- [24] J.-L. Pérez, K. Yamazaki, and A. Bensoussan, Optimal periodic replenishment policies for spectrally positive Lévy demand processes, arXiv preprint arXiv:1806.09216, (2018).

- [25] M. R. Pistorius, An Excursion-Theoretical Approach to Some Boundary Crossing Problems and the Skorokhod Embedding for Reflected Lévy Processes, Springer Berlin Heidelberg, Berlin, Heidelberg, 2007, pp. 287–307.

- [26] B. A. Surya and K. Yamazaki, Optimal capital structure with scale effects under spectrally negative Lévy models, International Journal of Theoretical and Applied Finance, 17 (2014), p. 1450013.