Eigenvalues and Eigenvectors of Tau Matrices

with Applications to Markov Processes and Economics

Abstract

In the context of matrix displacement decomposition, Bozzo and Di Fiore introduced the so-called algebra, a generalization of the more known algebra originally proposed by Bini and Capovani. We study the properties of eigenvalues and eigenvectors of the generator of the algebra. In particular, we derive the asymptotics for the outliers of and the associated eigenvectors; we obtain equations for the eigenvalues of , which provide also the eigenvectors of ; and we compute the full eigendecomposition of in the specific case . We also present applications of our results in the context of queuing models, random walks, and diffusion processes, with a special attention to their implications in the study of wealth/income inequality and portfolio dynamics.

Keywords: eigenvalues and eigenvectors, tau matrices, queuing models, random walks, diffusion processes, wealth and income inequality, portfolio dynamics

2020 MSC: 15A18, 15B05, 60K25, 60G50, 60J60, 91G10

1 Introduction

Consider the matrix

where are given parameters. For , the eigendecomposition of is already available in the literature. In particular, for , the matrix is the generator of the algebra originally introduced by Bini and Capovani [10]; its eigendecomposition, as well as the eigendecomposition of any tridiagonal Toeplitz matrix, has long been known [12, Section 2.2]. For , the matrix is the generator of the so-called algebra introduced by Bozzo and Di Fiore in [13]; its eigendecomposition for , , , was provided in [13, Section 4]. Finally, for , , , —actually for all —the eigendecomposition of can be derived, e.g., from the results in [15, Appendix 1]; see in particular [15, pp. 394–395].

For all , the asymptotic spectral distribution of in Weyl’s sense can be easily obtained from the theory of generalized locally Toeplitz sequences [19, 20], which immediately yields for the asymptotic spectral distribution function (or symbol) . Precise eigenvalue estimates can also be given on the basis of classical interlacing results [22, Section 4.3] after observing that is a small-rank perturbation of and the eigenvalues of are known. It should be noted, however, that both asymptotic spectral distribution results and interlacing estimates completely ignore the outliers of , i.e., the eigenvalues lying outside the interval (the range of the symbol ). On the other hand, the outliers, which are determined by the parameters , are precisely the objects one is interested in when dealing with several noteworthy applications. Such applications include, for example, queuing models and Markov chains/processes [5, 9, 21, 24], where the eigenvector corresponding to the (unique) outlier of (a suitable transform of) corresponds to the steady-state distribution of the considered chain/process.

In this paper, we study the spectral properties of and present a few applications in the context of Markov chains/processes, with a special focus on queuing models, random walks, diffusion processes and economics issues. The structure of the paper, including a summary of our contributions, is given below.

-

•

In Section 2, we study some basic spectral properties of that will simplify the analysis of later sections.

- •

- •

- •

-

•

In Section 6, we present a few applications in the context of Markov chains/processes, with a special focus on queuing models, random walks in a multidimensional lattice, multidimensional reflected diffusion processes and economics issues. In particular, we investigate the implications of our results within a model for wealth/income inequality and portfolio dynamics with an arbitrary number of assets: we provide analytical formulas for the steady-state (stationary) distribution of the underlying stochastic process (a multidimensional reflected diffusion process), we compute the convergence speed towards the steady state, and we also derive closed-form expressions for relevant moments of the stationary distribution such as the average wealth and the wealth variance.

-

•

In Section 7, we draw conclusions and outline possible future lines of research.

2 Basic Properties of the Eigenvalues and Eigenvectors of

In this section, we collect some basic properties of the eigenvalues and eigenvectors of which will allow us to tackle the analysis of the next sections with useful a priori knowledge. Throughout this paper, the eigenvalues of which do not belong to the interval are referred to as outliers. We denote by the vectors of the canonical basis of , and by the symmetric permutation matrix (flip matrix) whose rows are those of the identity matrix in reverse order:

Theorem 2.1.

The following properties hold.

-

1.

. It follows that is an eigenpair of if and only if is an eigenpair of .

-

2.

If and

then . Similarly, if and

then .

-

3.

has real distinct eigenvalues.

-

4.

If then all the eigenvalues of belong to .

-

5.

If or then all the eigenvalues of belong to except for at most outlier.

-

6.

If then all the eigenvalues of belong to except for at most outliers.

-

7.

If or then both and are not eigenvalues of .

Proof.

1. It follows from direct computation.

2. It follows from direct computation.

3. is nonderogatory just like any Hessenberg matrix with nonzero subdiagonal entries [22, p. 82]. Since is also real and symmetric (hence diagonalizable), we infer that has real distinct eigenvalues.

4. The result follows immediately from Gershgorin’s theorem [22, Theorem 6.1.1].

5. We prove the statement in the case where and (the proof in the other case is identical). Write

All the eigenvalues of belong to by Gershgorin’s theorem. Since the unique nonzero eigenvalue of the matrix is , it follows from a classical interlacing theorem [22, Corollary 4.3.3] that eigenvalues of belong to .

6. Write

All the eigenvalues of belong to by Gershgorin’s theorem. Since the unique nonzero eigenvalues of the matrix are and , it follows from [22, Corollary 4.3.3] that eigenvalues of belong to .

7. The result follows immediately from the fact that the matrix is irreducible and from the so-called Gershgorin’s third theorem [11, p. 80]. ∎

3 Asymptotics of the Outliers of

If and is large enough, property 2 of Theorem 2.1 says that is substantially an eigenpair of (it is an exact eigenpair if ). A similar consideration applies to . The next theorems formalize this intuition. We remark that, for every ,

with equality holding if and only if . In what follows, denotes the spectrum of the matrix .

Lemma 3.1.

The following properties hold.

-

1.

If then there exists an eigenvalue of such that as . Since , the eigenvalue is eventually an outlier.

-

2.

If then there exists an eigenvalue of such that as . Since , the eigenvalue is eventually an outlier.

Proof.

1. Let be an orthonormal basis of formed by eigenvectors of with corresponding eigenvalues :

Expand the vector on this basis:

| (3.1) | ||||

| (3.2) |

The equation in Theorem 2.1 becomes

| (3.3) |

Passing to the norms, we obtain

| (3.4) |

If we assume by contradiction that as , then there exists a positive constant such that

frequently as , hence

frequently as , which is a contradiction to (3.4). We conclude that as , which is the thesis.

2. It follows from item 1 applied to , taking into account that by Theorem 2.1. ∎

If , we set . If , we denote by the orthogonal projector onto the subspace generated by . In the case where , the projector is explicitly given by

| outlier | ||||||

|---|---|---|---|---|---|---|

| 8 | 3.3333333663723654 | |||||

| 16 | 3.3333333333333341 | |||||

| 32 | 3.3333333333333333 | |||||

| 64 | 3.3333333333333333 | |||||

| 128 | 3.3333333333333333 |

Theorem 3.1.

Suppose that and . Let be an eigenpair of such that as and for all . Then, the following properties hold.

-

1.

Eventually, is an outlier of and any other eigenvalue satisfies for some positive constant independent of .

-

2.

as , where .

Proof.

1. If then all eigenvalues of belong to except for at most 1 outlier (by Theorem 2.1). Since , it is clear that coincides eventually with the unique outlier of . Moreover, any other eigenvalue of satisfies the inequality with

If then all eigenvalues of belong to except for at most 2 outliers (by Theorem 2.1) and there exists an eigenvalue of such that (by Lemma 3.1). Since and (because by assumption), it is clear that, eventually, and are the unique two outliers of . Moreover, any eigenvalue of with satisfies eventually the inequality with

where is a fixed positive constant chosen so that .

The next theorem is completely analogous to Theorem 3.1 and can be proved by the same type of argument or by using the relation between and (see Theorem 2.1).

Theorem 3.2.

Suppose that and . Let be an eigenpair of such that as and for all . Then, the following properties hold.

-

1.

Eventually, is an outlier of and any other eigenvalue satisfies for some positive constant independent of .

-

2.

as , where .

| outlier | ||||||

|---|---|---|---|---|---|---|

| outlier | ||||||

| 8 | ||||||

| 16 | ||||||

| 32 | ||||||

| 64 | ||||||

| 128 | ||||||

To conclude our analysis, we address the case where and .

Theorem 3.3.

Suppose that and . Then, the following properties hold.

-

1.

There exist exactly two distinct eigenvalues of which are eventually the unique two outliers of and satisfy .

-

2.

Let and be eigenvectors of associated with and , respectively, and satisfying for all . Then, up to a renaming of and , we eventually have and . Moreover, and as , where and .

Proof.

1. We first recall that all eigenvalues of are distinct by Theorem 2.1. Also, an eigenvalue converging to exists for sure by Lemma 3.1 and more than two eigenvalues converging to cannot exist by Theorem 2.1 as . Suppose by contradiction that there exists a unique eigenvalue converging to and let be a corresponding eigenvector with . Let be an orthonormal basis of formed by eigenvectors of with corresponding eigenvalues :

We expand the vector on this basis as in (3.1) and we get (3.2)–(3.4). Since is the unique eigenvalue of converging to and eigenvalues of belong to for all , there exists a positive constant independent of such that

| (3.8) |

frequently as . Passing to a subsequence of indices , if necessary, we may assume that (3.8) is satisfied for all . Note that (3.8) is the same as (3.5). Hence, by reasoning as before, we infer that (3.6)–(3.7) hold and we conclude that (for the considered subsequence of indices ). This is impossible for the following reasons.

-

•

Since , we have and, by Theorem 2.1, is an eigenpair of if and only if the same is true for .

-

•

By Theorem 2.1, each eigenvalue of is simple and so for all eigenvectors of . In particular for all .

-

•

If then the relation cannot hold for all . Indeed, considering that is a multiple of , from and we deduce that , i.e., (see (3.2)), and

which are clearly incompatible with as the latter implies .

2. Let be an orthonormal basis of formed by eigenvectors of with corresponding eigenvalues :

Expand the vectors and on this basis:

| (3.9) | ||||

| (3.10) | ||||

| (3.11) | ||||

| (3.12) |

Keeping in mind that , the equations

in Theorem 2.1 yield

that is,

Passing to the norms, we obtain

| (3.13) | |||

| (3.14) |

Since are eventually the unique two outliers of , the other eigenvalues eventually belong to and from (3.11)–(3.14) we infer that

| (3.15) | |||

| (3.16) |

Now, recall from the proof of item 1 that (in the present case where ) all eigenvectors of satisfy . Since and , for the eigenvectors satisfying we have in the expansion (3.10), and for the eigenvectors satisfying we have in the expansion (3.9). It follows that, eventually, one among and (say ) must satisfy and the other (say ) must satisfy the “opposite” equation . Indeed, if we frequently had and , then we would also have frequently, which is impossible by (3.16). Similarly, if we frequently had and , then we would also have frequently, which is impossible by (3.15). By renaming and (if necessary), we can assume that the eigenvector associated with eventually satisfies , and the eigenvector associated with eventually satisfies . In particular, we eventually have

| (3.17) | ||||

| (3.18) |

Thus, by applying (3.9), (3.11), (3.15) and (3.17), we eventually obtain

Similarly, one can show that . ∎

| outlier | ||||||

|---|---|---|---|---|---|---|

| outlier | ||||||

| 8 | 2.2447548446486838 | |||||

| 2.1991364375014231 | ||||||

| 16 | 2.2255116405185864 | |||||

| 2.2244808853312168 | ||||||

| 32 | 2.2250002793612006 | |||||

| 2.2249997206340419 | ||||||

| 64 | 2.2250000000000821 | |||||

| 2.2249999999999180 | ||||||

| 128 | 2.2250000000000000 | |||||

| 2.2250000000000000 |

In Tables 3.1–3.3, we validate through numerical experiments the results presented in Theorems 3.1–3.3. The experiments have been performed via the high-performance computing language Julia [8] with a machine precision equal to (1024-bit precision). We note that the convergences predicted by Theorems 3.1–3.3 are quite fast. Actually, this could be expected on the basis of property 2 in Theorem 2.1, where we see that for the pairs and are substantially eigenpairs of already for moderate due to the exponential convergence to 0 of the error terms and .

4 Equations for the Eigenvalues and Eigenvectors of

In this section, we derive equations for the eigenvalues of . As we shall see, the equations for the outliers are formally the same as the equations for the non-outliers with the only difference that the trigonometric functions and must be replaced by the corresponding hyperbolic functions and . For all for which these equations can be solved, one obtains not only the eigenvalues but also the eigenvectors of . A special role in the following derivation is played by the theory of linear difference equations [23].

Let and , so that is a candidate eigenpair for the real symmetric matrix . We have

| (4.1) |

The characteristic equation of the linear difference equation (4.1) is given by

| (4.2) |

We consider five different cases.

4.1 Case 1:

In this case, we set with . The roots of the characteristic equation (4.2) are given by

and they are distinct because . The general solution of (4.1) is given by

where are arbitrary constants. Keeping in mind that , we have

We summarize in the next theorem the result that we have obtained.

Theorem 4.1.

For every , the number is an eigenvalue of if and only if

| (4.3) |

In this case, a corresponding eigenvector is given by

| (4.4) |

4.2 Case 2:

In this case, we set with . The roots of the characteristic equation (4.2) are given by

and they are distinct because . The general solution of (4.1) is given by

where are arbitrary constants. Keeping in mind that , we have

-

•

If , i.e., , then the equation is equivalent to and so

-

•

If , then the equation is equivalent to and so

As often happens in mathematics, the “limit” case merges with the case . Indeed, if then (because ) and

We summarize in the next theorem the result that we have obtained.

Theorem 4.2.

For every , the number is an eigenvalue of if and only if

| (4.5) |

In this case, a corresponding eigenvector is given by

| (4.6) |

4.3 Case 3:

In this case, the characteristic equation (4.2) has only one root with multiplicity 2. The general solution of (4.1) is given by

where are arbitrary constants. Keeping in mind that , we have

-

•

If , then the equation is equivalent to and so

-

•

If , then the equation is equivalent to and so

The case merges with the case , because if then and

We summarize in the next theorem the result that we have obtained.

Theorem 4.3.

The number is an eigenvalue of if and only if

| (4.7) |

In this case, a corresponding eigenvector is given by

| (4.8) |

4.4 Case 4:

In this case, we set with . The derivation is essentially the same as in Section 4.2; we leave the details to the reader and we report the analog of Theorem 4.2.

Theorem 4.4.

For every , the number is an eigenvalue of if and only if

| (4.9) |

In this case, a corresponding eigenvector is given by

| (4.10) |

4.5 Case 5:

The derivation is essentially the same as in Section 4.3; we leave the details to the reader and we report the analog of Theorem 4.3.

Theorem 4.5.

The number is an eigenvalue of if and only if

| (4.11) |

In this case, a corresponding eigenvector is given by

| (4.12) |

5 Eigendecomposition of for Specific Choices of and

5.1

As noted in the introduction, the eigendecomposition of for is already available in the literature. The purpose of this section is simply to show that it can also be obtained from Theorems 4.1, 4.3, and 4.5. Note that Theorems 4.2 and 4.4 are useless in this case as does not have outliers for ; see Theorem 2.1.

For , Theorem 4.1 immediately yields the eigenpairs , , with

For , using sine addition/subtraction formulas, we see that equation (4.3) is equivalent to

whose solutions in are , ; moreover, equation (4.7) is satisfied. Since, by prosthaphaeresis formulas,

we conclude by Theorems 4.1 and 4.3 that, for , a complete set of eigenpairs for is given by , , with

Similar derivations, using sine addition/subtraction and prosthaphaeresis formulas, can be done for all ; we leave the details to the reader.

5.2

We focus in this section on the case , which is crucial for the applications presented in Section 6. To the best of the authors’ knowledge, this case has never been addressed in the literature. Besides , we also assume that:

-

•

(because no additional difficulties are encountered if );

-

•

(because the case has already been addressed in Section 5.1).

Under these assumptions, we have

Using sine addition/subtraction formulas, we see that equation (4.3) is equivalent to

whose solutions in are , . Thus, Theorem 4.1 yields eigenpairs of , i.e., , , with

We still have to find one eigenvalue, which can be neither nor because, under our assumptions, equations (4.7) and (4.11) are not satisfied. In other words, the eigenvalue we are looking for is an outlier. Since equation (4.5) is equivalent to

it has a unique solution in given by . We then obtain the outlier and the corresponding eigenvector from Theorem 4.2:

After straightforward manipulations, involving also a renormalization of , we get for the outlier eigenpair the following simplified expressions:

Note that this outlier eigenpair could also be obtained from property 2 of Theorem 2.1. In conclusion, if we set

then the eigendecomposition of is given by

6 Applications

In this section, we present a few applications of our results in the context of Markov chains and processes. Section 6.1 deals with a queuing model. Sections 6.2 and 6.3 are devoted to random walks in unidimensional and multidimensional lattices, respectively. Finally, Sections 6.4 and 6.5 focus on multidimensional reflected diffusion processes and related economics applications.

6.1 Queuing Model

Consider a continuous-time Markov chain with states and with transition rate matrix (infinitesimal generator) given by

| (6.1) |

where . Markov chains of this kind are referred to as M/M/1/ queues (with ). They find applications in queuing theory [9, 21, 24], especially in telecommunications [21, Section 5.7]. In this section, we derive the eigendecomposition of

We begin with the following lemma, which can be proved by direct computation.

Lemma 6.1.

Let

be a real tridiagonal matrix such that for all . Then

where .

By applying Lemma 6.1 to the matrix , we obtain

where

A direct verification shows that

Since , the eigendecomposition of (and hence also of ) is immediately obtained from the results in Section 5.2. In particular, the eigenpairs of are given by , , where

| (6.2) |

and, for ,

| (6.3) |

Remark 6.1 (Steady-State Distribution).

Since

the steady-state (or stationary/limiting) distribution of the considered queuing model, i.e., the normalized positive eigenvector of associated with the eigenvalue 0, is given by

where it is understood that in the case we take the limit . For a different derivation of this result, see [21, Section 5.7].

Remark 6.2 (Second Eigenvalue).

It is clear from (6.3) and the geometric-arithmetic mean inequality that all nonzero eigenvalues of are negative. The largest of them, i.e., the second largest eigenvalue after 0, is . The second eigenvalue gives information about the convergence speed towards the steady-state distribution of power methods [11, p. 371]; see also [17] and [24, Section 7.2]. We will return to the role of the second eigenvalue in Section 6.5.

6.2 Random Walk in a Unidimensional Lattice

Consider a discrete-time Markov chain with states and with matrix of transition probabilities given by

| (6.4) |

where and . Markov chains of this kind are often referred to as random walks in the unidimensional lattice ; see Figure 6.1. The difference with respect to traditional random walks in is that states 1 and act as absorbing/reflecting barriers: when the system is in state 1, it cannot go to a hypothetical previous state 0 with probability (as it happens for all other states ), because the probability of going to a previous state 0 is absorbed in the probability of staying in state 1, which grows from to ; a similar discussion applies to state .

In this section, we derive the eigendecomposition of

To this end, simply note that

where is given by (6.1) for . By (6.2)–(6.3), the eigenpairs of are given by , , where

| (6.5) |

and, for ,

| (6.6) |

with

Remark 6.4 (Steady-State Distribution).

Since

the steady-state distribution of the unidimensional random walk, i.e., the normalized positive eigenvector of associated with the eigenvalue 1, is given by

where it is understood that in the case we take the limit .

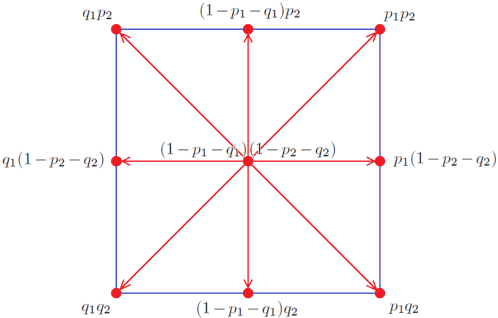

6.3 Random Walk in a Multidimensional Lattice

Let and . We denote by the multi-index range , where and inequalities between vectors such as must be interpreted componentwise. When writing , we mean that varies from to over the multi-index range following the standard lexicographic ordering:

We refer the reader to [20, Section 2.1.2] for more details on the multi-index notation.

Consider a discrete-time Markov chain with states and with matrix of transition probabilities

where

-

•

and satisfy and ,

-

•

the matrix is defined by (6.4) for ,

-

•

denotes the tensor (Kronecker) product.

Markov chains of this kind are often referred to as random walks in the -dimensional lattice . They are a generalization of the unidimensional random walks discussed in Section 6.2. By the properties of tensor products [20, Section 2.5], for all , the probability of going from state to state is given by

and it is equal to the product for of the probability of going from state to state in a unidimensional random walk with transition matrix as considered in Section 6.2. In short, a -dimensional random walk is the result of independent unidimensional random walks (one for each space dimension); see Figure 6.2 for a bidimensional illustration.

By the properties of tensor products and the results of Section 6.2, we can immediately obtain the eigendecomposition of . In particular, the eigenpairs of are given by , , where

Remark 6.5 (Steady-State Distribution).

The steady-state distribution of the -dimensional random walk is given by

i.e., it is the tensor product of the steady-state distributions of the individual unidimensional random walks that compose it.

6.4 Multidimensional Diffusion Processes

Consider a -dimensional diffusion process, where the diffusions in each dimension are independent of each other and subject to a reflecting boundary condition at each side. We assume for simplicity that, for every , the direction is discretized uniformly with nodes separated by a discretization step . This discretization gives rise to a lattice whose points are naturally indexed by a multi-index , with . The diffusion in direction is a Brownian motion characterized by two parameters: a drift and a variance . For the direction , the infinitesimal generator coincides with the generator of a 1-dimensional diffusion process with drift and variance discretized uniformly with nodes separated by a discretization step . In formulas, is an matrix, which in the case is given by

where , , and is defined in (6.1); and in the case is given by

where , , and is defined in (6.1). In short,

The differential operator (infinitesimal generator) of the -dimensional diffusion process is given by

| (6.7) |

where and . More details on the discretized multidimensional diffusion process considered here will be given in Section 6.5 along with an economics application; for more on diffusion processes, see [5] for a mathematical treatment and [2, 3, 17] for an economical application-oriented approach.

By the properties of tensor products and the results of Section 6.1, we can immediately obtain the eigendecomposition of . In particular, the eigenpairs of are given by , , where

| (6.8) |

Remark 6.6 (Steady-State Distribution).

The steady-state distribution of the -dimensional diffusion process generated by , i.e., the normalized positive eigenvector of associated with the eigenvalue , is given by

| (6.9) |

i.e., it is the tensor product of the steady-state distributions of the individual unidimensional diffusion processes generated by the operators , .

6.5 Dynamics of Wealth and Income Inequality

In this section, we present an economic application of the results obtained in Section 6.4. We begin with an overview of the topic, which may not be so familiar to non-economists.

6.5.1 Modeling the Evolution of Wealth and Income

The sources of the vast wealth and income inequality is a key topic of study within macroeconomics and finance; see [2, 3, 4, 6, 7] for empirical evidence and modeling approaches. Central to the questions of inequality are:

-

•

what is the source of heterogeneity that drives the stationary distribution of income or wealth?

-

•

how would the income or wealth distribution evolve over time given aggregate changes?

For example, researchers can ask how the stationary distribution of wealth will change—and how long it will take to be reached—given experiments such as a new income tax, technological changes driving more volatile wages, or increases in the returns on an asset such as housing. Methodologically, the analysis of income inequality is done through examining the stationary distribution of discrete- or continuous-time stochastic processes associated with income or wealth. Typically, researchers act as follows.

-

•

They choose a stochastic process for the assets of interest (for example, housing wealth, human wealth (i.e., wages), stocks, bonds, social security income, etc.).

- •

-

•

They solve for the stationary distribution associated with the stochastic process. In this way, they can examine properties of the distribution, relate it back to the data, and conduct hypotheticals on the impact of policy.

With this approach, the emphasis on the steady-state distribution has come out of necessity. Even the speed of convergence towards the steady state has recently become an active research field; see [18] for a theory of the convergence rates largely focused on infinite-dimensional univariate models, and [25] for earlier evidence and theory on transition rates of the firm size distribution (methodologically, much of the literature on income/wealth inequality is similar to the firm dynamics literature, where the goal is to understand the distribution of firm sizes or productivity as well as the role of firm or worker heterogeneity in generating that distribution [17, 25, 26]).

6.5.2 Continuous-State Formulation

Consider a portfolio of assets (e.g., housing wealth, wage income, social security, etc.). We emphasize the dependence on because the assets evolve over time. We assume that are independent Brownian motions with drifts and variances . Without loss of generality, we also assume that take values in , so that the portfolio determining an individual’s wealth is an element at any time . The resulting stochastic process for the considered set of assets is a -dimensional Brownian motion with drifts and variances , and with the edges of the hypercube acting as reflecting barriers. The probability density function for the asset at time is determined by the Kolmogorov forward equation (Fokker–Planck equation)

| (6.10) |

subject to the boundary conditions induced by reflecting boundaries at and :

| (6.11) |

The objects of interest are the following.

- •

-

•

Any function that maps a state to a scalar “wealth” or “payoff” . 111 As an example in the case , asset could be housing wealth at time and asset could be bank holdings at time in an individual’s portfolio. If is the per-unit value of a house and the per-unit value of a bank holding, then the “wealth” of an individual in state is . Clearly, is a random variable evolving over time together with the portfolio , and we are interested in quantities like the average wealth and the wealth variance computed in the steady-state distribution , that is,

6.5.3 Discrete-State Formulation

Suppose we discretize the hypercube by introducing a lattice with points in direction separated by a discretization step , as in Section 6.4. This essentially means that we allow each random variable (asset) to assume only a finite number of values. Consequently, the portfolio can only be in a finite number of states . The use of upwind finite differences allow us to convert the PDEs (6.10)–(6.11) to a unique system of ODEs

| (6.12) |

subject to an initial condition , where is the infinitesimal generator (6.7) and is the probability that the portfolio is in state at time . After this discretization, the continuous-state continuous-time Markov process of Section 6.5.2 is changed into a discrete-state continuous-time Markov chain. Here, the objects of interest are the discrete counterparts of those mentioned in Section 6.5.2, i.e., the following.

- •

-

•

Any function that maps a state to a scalar “wealth” or “payoff” . Clearly, is a random variable evolving over time together with the portfolio , and we are interested in quantities like the average wealth and the wealth variance computed in the steady-state distribution , that is,

(6.13) (6.14) where is the vector (tensor) of payoffs and is the componentwise square of (in general, operations on vectors that have no meaning in themselves must be interpreted in the componentwise sense).

Considering that is known from (6.9), formulas (6.13)–(6.14) allow us to compute both the average wealth and the wealth variance in the steady state of the process. This lets us analyze different hypothetical scenarios. For example, if the drift of the housing component of an individual’s portfolio increases, what would the impact be on the average wealth? Alternatively, we could ask how the wealth variance (a simple measure of inequality) would change if the variance of wages increases.

6.5.4 Convergence Speed to the Steady State

The results of Section 6.4 allow us to quantify the convergence speed to the steady state of the Markov chain presented in Section 6.5.3. Indeed, as we know from Section 6.4, all nonzero eigenvalues of are negative and the largest of them, i.e., the second largest eigenvalue after 0, is given by

| (6.15) |

The second eigenvalue provides a measure of the convergence speed towards the steady state. The reason is the following: for essentially every choice of the initial distribution , the quantities , , converge to their stationary counterparts , , in (6.9), (6.13), (6.14) with asymptotic convergence rates given by

| (6.16) | ||||

| (6.17) | ||||

| (6.18) |

For more details on the role of the second eigenvalue as a measure of the asymptotic convergence rate towards the steady state, see, e.g., [17] and [24, Section 7.2].

6.5.5 Derivatives with Respect to Drifts and Variances

For the convenience of economists, we here report the derivatives of the steady-state distribution in (6.9), the average wealth in (6.13), and the wealth variance in (6.14) with respect to the drifts and the variances . For , we have

| (6.19) | ||||

| (6.20) | ||||

| (6.21) | ||||

| (6.22) | ||||

| (6.23) | ||||

| (6.24) |

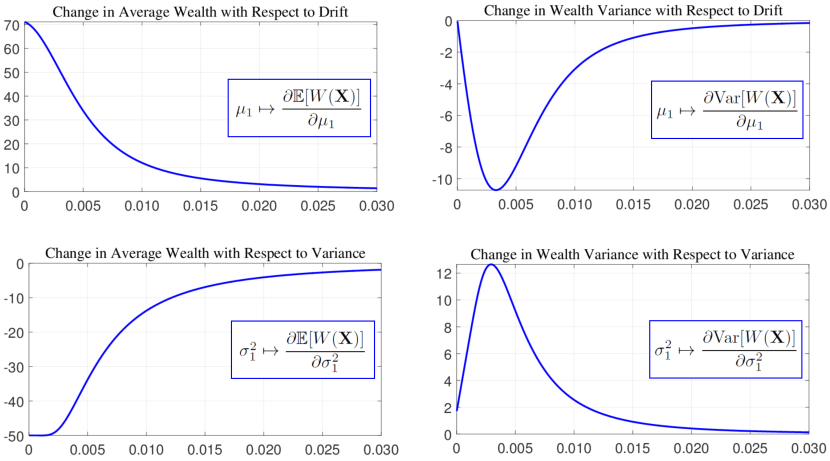

We remark that the above derivatives are defined even in the case and their values in this case are obtained by taking the limit of the corresponding expression as . The derivatives (6.19)–(6.20) enable an analysis of how the steady state changes when properties of the underlying process change. For example, if the volatility of housing prices increases, equations (6.19)–(6.20) provide the resulting impact on the steady state. The derivatives (6.21)–(6.24) can be used to examine how key moments of the stationary distribution change. For example, a researcher could analyze the impact on the steady-state variance of the wealth distribution, i.e., , in the case where the volatility of housing prices increases. Figure 6.3 illustrates this by showing how the mean and variance of the stationary wealth distribution change with respect to the parameters of the underlying stochastic process. The figure has been realized through a discretization of the square by a lattice with points in each direction and (consequently) two equal discretization steps . It should be noted, however, that the graphs in Figure 6.3 do not really depend on and , because they converge to limiting graphs as (and convergence is already reached for ).

7 Conclusions and Perspectives

We have studied the spectral properties of the generator of the algebra introduced by Bozzo and Di Fiore in the context of matrix displacement decomposition [13]. In particular:

-

•

we have derived precise asymptotics for the outliers of and the associated eigenvectors;

-

•

we have obtained equations for the eigenvalues of , which automatically provide also the eigenvectors of ;

-

•

we have computed the full eigendecomposition of in the case .

Finally, we have presented applications of our results to queuing models, random walks, diffusion processes, and economics, with a special emphasis on wealth/income inequality and portfolio dynamics. We conclude this paper by mentioning a few possible future lines of research.

-

1.

The applications presented herein do not exhaust all possible applications of the algebra. For example, matrices belonging to this algebra for suitable choices of and arise in the discretization of differential equations by finite difference methods, finite element methods and, as recently discovered, isogeometric methods [16, Section 3]. A future research could take care of investigating further discretizations where matrices arise and, consequently, the results of this paper find applications.

-

2.

On the economics side, Sections 6.4–6.5 are interesting and useful, but the reflected constant-coefficient diffusion process that has been considered therein is not sufficient to understand top income inequality, since in that case researchers need alternative specifications [6, 18]. That said, there could be a large class of stochastic processes that can be mapped to through an appropriate change of measure. Loosely, given a stochastic process , let be a mapping such that represents the “wealth” of an individual with portfolio . Then, there may exist a change of measure (i.e., a Radon–Nikodym derivative ) mapping to and to for a suitable . If so, then the computation of, say, the average wealth in the steady-state distribution of process could be traced back to computing the corresponding expectation for process as we have done in Section 6.5; see [14, Section 9.5] for an analysis of changes in probability measures and associated expectations, as well as for practical tools for working with such concepts. A careful investigation of all this topic may form the content of a future research that would extend the applicability of the results presented in this paper.

Acknowledgements

The authors wish to thank Carmine Di Fiore for useful discussions. This work has been supported by the MIUR Excellence Department Project awarded to the Department of Mathematics of the University of Rome Tor Vergata (CUP E83C18000100006), by the Beyond Borders Programme of the University of Rome Tor Vergata through the Project ASTRID (CUP E84I19002250005), by the Research Group GNCS (Gruppo Nazionale per il Calcolo Scientifico) of INdAM (Istituto Nazionale di Alta Matematica), and by the Swedish Research Council through the International Postdoc Grant (Registration Number 2019-00495).

References

- [1]

- [2] Achdou Y., Buera F. J., Lasry J.-M., Lions P.-L., Moll B. Partial differential equation models in macroeconomics. Philos. Trans. Royal Soc. A 372 (2014) 20130397.

- [3] Achdou Y., Han J., Lasry J.-M., Lions P.-L., Moll B. Income and wealth distribution in macroeconomics: a continuous-time approach. Working Paper 23732, National Bureau of Economic Research (2017).

- [4] Atkinson A. B., Piketty T., Saez E. Top incomes in the long run of history. J. Econ. Lit. 49 (2011) 3–71.

- [5] Baldi P. Stochastic Calculus: An Introduction Through Theory and Exercises. Springer, Cham (2017).

- [6] Benhabib J., Bisin A. Skewed wealth distributions: theory and empirics. J. Econ. Lit. 56 (2018) 1261–1291.

- [7] Benhabib J., Bisin A., Luo M. Wealth distribution and social mobility in the US: a quantitative approach. Am. Econ. Rev. 109 (2019) 1623–1647.

- [8] Bezanson J., Edelman A., Karpinski S., Shah V. B. Julia: a fresh approach to numerical computing. SIAM Rev. 59 (2017) 65–98.

- [9] Bini D. A. Matrix structures in queuing models. In: Benzi M., Simoncini V. (Eds.), “Exploiting Hidden Structure in Matrix Computations: Algorithms and Applications”. Lect. Notes Math. 2173 (2016) 65–159.

- [10] Bini D., Capovani M. Spectral and computational properties of band symmetric Toeplitz matrices. Linear Algebra Appl. 52–53 (1983) 99–126.

- [11] Bini D., Capovani M., Menchi O. Metodi Numerici per l’Algebra Lineare. Zanichelli, Bologna (1988).

- [12] Böttcher A., Grudsky S. M. Spectral Properties of Banded Toeplitz Matrices. SIAM, Philadelphia (2005).

- [13] Bozzo E., Di Fiore C. On the use of certain matrix algebras associated with discrete trigonometric transforms in matrix displacement decomposition. SIAM J. Matrix Anal. Appl. 16 (1995) 312–326.

- [14] Campolieti G., Makarov R. N. Financial Mathematics: A Comprehensive Treatment. CRC Press, Boca Raton (2014).

- [15] Ceccherini-Silberstein T., Scarabotti F., Tolli F. Harmonic Analysis on Finite Groups: Representation Theory, Gelfand Pairs and Markov Chains. Cambridge University Press, New York (2008).

- [16] Ekström S.-E., Furci I., Garoni C., Manni C., Serra-Capizzano S., Speleers H. Are the eigenvalues of the B-spline isogeometric analysis approximation of known in almost closed form? Numer. Linear. Algebra Appl. 25 (2018) e2198.

- [17] Gabaix X. Power laws in economics and finance. Annu. Rev. Econ. 1 (2009) 255–293.

- [18] Gabaix X., Lasry J.-M., Lions P.-L., Moll B. The dynamics of inequality. Econometrica 84 (2016) 2071–2111.

- [19] Garoni C., Serra-Capizzano S. Generalized Locally Toeplitz Sequences: Theory and Applications (Volume I). Springer, Cham (2017).

- [20] Garoni C., Serra-Capizzano S. Generalized Locally Toeplitz Sequences: Theory and Applications (Volume II). Springer, Cham (2018).

- [21] Giambene G. Queuing Theory and Telecommunications: Networks and Applications. Second Edition, Springer, New York (2014).

- [22] Horn R. A., Johnson C. R. Matrix Analysis. Second Edition, Cambridge University Press, New York (2013).

- [23] Kelley W. G., Peterson A. C. Difference Equations: An Introduction with Applications. Second Edition, Academic Press, San Diego (2001).

- [24] Lawler G. F. Introduction to Stochastic Processes. Second Edition, CRC Press, Boca Raton (2006).

- [25] Luttmer E. G. J. Selection, growth, and the size distribution of firms. Q. J. Econ. 122 (2007) 1103–1144.

- [26] Luttmer E. G. J. Slow convergence in economies with firm heterogeneity. Working Paper 696, Federal Reserve Bank of Minneapolis (2012).