Conditional empirical copula processes and generalized dependence measures

Abstract

We study the weak convergence of conditional empirical copula processes, when the conditioning event has a nonzero probability. The validity of several bootstrap schemes is stated, including the exchangeable bootstrap. We define general - possibly conditional - multivariate dependence measures and their estimators. By applying our theoretical results, we prove the asymptotic normality of some estimators of such dependence measures.

Keywords: empirical copula process, conditional copula, weak convergence, bootstrap.

MCS 2020: Primary: 62G05, 62G30; Secondary: 62H20, 62G09.

1 Introduction

Since their formal introduction by Patton in [40, 41], conditional copulas have become key tools to describe the dependence function between the components of a random vector , given that a random vector of covariates is available. This concept, generalized in [18], may be stated as an extension of the famous Sklar’s theorem: for every borelian subset and every vectors , the conditional joint law of given is written

| (1) |

for some random map that is a copula (denoted as hereafter to be short). Note that we have denoted inequalities componentwise. This will be our convention hereafter.

Now, Patton’s seminal paper [40] has been referenced more than times in the academic literature. The concept of conditional copulas (also sometimes called “dynamic copulas” or “time-varying copulas”) has been applied in many fields: economics ([43],[34]), financial econometrics ([28],[42],[9]), risk management ([39],[37]), agriculture ([24]), actuarial science ([7],[16] and [10] more recently), hydrology ([30],[25]), etc, among many others. The rise of pair-copula constructions, particularly vine models ([1],[5, 6]) has fuelled the interest around conditional copulas. Indeed, generally speaking, any -dimensional distribution can be described by bivariate conditional copulas and margins. Even if most vine models assume that such conditional copulas are usual copulas (the so-called ”simplifying assumption”; c.f. [26, 23, 11] and the references therein), there is here no consensus. Therefore, some recent papers propose some model specification for vines and the associated inference procedures by working directly on conditional copulas: see [49],[56],[33],[57], e.g.

Moreover, the statistical theory of conditional copulas is currently an active research topic. In the literature, the conditioning subset in (1) is pointwise most often, i.e. the authors consider for some particular vector . Typically, in a semi-parametric model, it is assumed that for some map and the main goal is to statistically estimate the latter link function, as in [3, 4, 2, 60]. Under a nonparametric point-of-view, the main quantity of interest is rather the empirical copula process given . For instance, [61, 22, 44] study the weak convergence of such a process.

To the best of our knowledge, almost all the papers in the literature until now have focused on pointwise conditioning events. In a few papers, some box-type conditioning events as are considered, where for every . For example, [52], p.1127, discusses a Spearman’s rho between two random variables and , knowing that and/or is above (or below) some threshold. Nonetheless, the limiting law of such a quantity is not derived. In the same spirit, [14] estimate similar quantities for measuring contagions between two markets, but they do not yield their asymptotic variances. They wrote that “this variance is usually difficult to get in a closed form and can be estimated by means of a bootstrap procedure”. See [15] too. Indeed, the limiting law of such statistics cannot be easily deduced from the asymptotic behavior of the usual empirical copula process, and necessitate particular analysis (see below). The aim of our paper is to state general theoretical results to solve such problems.

Actually, such box-type conditioning events provide a natural framework in many situations. For instance, it is often of interest to measure and monitor conditional dependence measures between the components of given belongs to some particular areas in , through a model-free approach. Therefore, bank stress tests will focus on for some quantiles of . Since the levels of the latter quantiles are often high, it is no longer possible to rely on marginal or joint estimators given pointwise conditioning events (kernel smoothing, e.g.). This justifies the bucketing of values. Moreover, when dealing with high-dimensional vectors of covariates, discretizing the -space is often the single feasible way of measuring conditional dependencies. Indeed, it is no longer possible to invoke usual nonparametric estimators, due to the usual curse of dimensionality. Since dependence measures are functions of the underlying copula, the key theoretical object will be here the conditional copula of given for some borelian subsets , and some of its nonparametric estimators.

The goal of this paper is threefold. First, in Section 2, we state the weak convergence of the empirical copula process indexed by borelian subsets under minimal assumptions, extending [54] written for usual copulas. Second, we prove the validity of the exchangeable bootstrap scheme for the latter process in Section 3. This provides an alternative to the usual nonparametric Efron’s bootstrap ([17]) and the multiplier bootstrap [46] for bootstrapping copula models. Third, Section 4 introduces a family of general “conditional” dependence measures as mappings of the latter copulas. This family virtually includes and generalizes all dependence measures that have been introduced until now. We apply our theoretical results to prove their asymptotic normality. We state our results with independent and identically variables, leaving aside the extensions to dependent data for further studies. It is important to note that our results obviously include the particular case of no covariate/conditioning event. Therefore, we contribute to the literature on usual copulas as much as on conditional copulas. Finally, Section 5 provides an empirical application of the latter tools to study conditional dependencies between stock returns.

2 Weak convergence of empirical copula processes indexed by families of subsets

2.1 Single conditioning subset

Let us consider a borelian subset so that is positive. Let be an i.i.d. sample of realizations of . The conditional copula of given , that will simply be denoted by , can be estimated by

Note that is the size of the sub-sample of the observations s.t. . It is a random integer in . When , simply set and formally.

The associated copula process is denoted as , i.e. for any . Equivalently, one can define the empirical copula as

invoking usual generalized inverse functions: for every univariate distribution . The associated copula process becomes , where

We assume hereafter that the conditional margins are continuous, . First note that the asymptotic behaviors of and are the same. Indeed, adapting the same arguments as in [45], Appendix C, it is easy to check that

almost everywhere, and then

| (2) |

since tends to a.s. In other words, tends to zero in probability in , endowed with its sup-norm. Therefore, the weak limits of and are the same.

In this section, we state the weak convergence of and/or in . For convenience and w.l.o.g., we will focus on in the next theorem.

Second, the random variable is uniformly distributed on , given , for every . We denote by the unobservable random vector , or simpler when there is no ambiguity. For every , the empirical distribution of the (unobservable) random variable given the event is

Note that and can be seen as an average of indicator functions, i.e. an average on a sub-sample of observations whose size is random. Obviously, tends to a.e. and its associated empirical process will be , . Note that the normalizing sample size is random here, contrary to the usual empirical processes. Nonetheless, this will not be a source of worry for asymptotic behaviors and could be replaced by in the definition of .

Third, set

for any , that tends to a.s. Note that if and only if for any , and . This implies

and the asymptotic behavior of will be deduced from the weak convergence of the process , where .

The unfeasible empirical counterpart of is

A key process is that is a random map from to . As every usual empirical process, it weakly tends in to a Brownian bridge.

In the meantime, define the instrumental empirical process

| (3) |

denoting par the partial derivative of the map w.r.t. . This new process will yield a nice approximation of the process of interest , as stated in the theorem below.

Condition 1.

For every , the partial derivative of w.r.t. exists and is continuous on the set .

The latter assumption is the standard “minimal” regularity condition, as stated in [54], so that the usual empirical copula process weakly converges in .

Theorem 1.

If and Condition 1 holds, then tends to zero in probability.

See the proof in the appendix, in Section A.1. Note that differs from the asymptotic approximation of the usual empirical copula process: compare with Equation (3.2) and Proposition 3.1 in [54], for instance. This is due to the additional influence of the random sample size , or, equivalently, the randomness of . This stresses that our results are not straightforward applications of the existing results in the literature.

Since the process is weakly convergent in - as any usual empirical process -, this yields the weak convergence of and then of in the same space.

Corollary 2.

If and Condition 1 holds, then the process weakly converges in towards the centered Gaussian process , where

denoting by a Brownian bridge, whose covariance function is given as

for every .

Thus, we deduce the asymptotic behavior of and , since . To this goal, recall that

Therefore, simple algebra yield

| (4) | |||||

We deduce from the latter relationship and Corollary 2 that is weakly convergent in .

Theorem 3.

If and Condition 1 holds, then and weakly tend to a centered Gaussian process in , where

By simple calculations, we explicitly write the covariance function of the limiting conditional copula process . Moreover, the latter covariance can be empirically estimated: see Appendix B.

When there is not conditioning subset, or when equivalently, then and a.s. (its variance is zero). In this case, we see that becomes the well-known weak limit of the usual empirical copula process, as in [17, 54]. Nonetheless, we stress that Theorem 3 cannot be straightforwardly deduced from the weak convergence of usual empirical copula processes, due to the dependencies between and .

Remark 4.

Theorem 3 is not a consequence of Theorem 5 in [45] either, where the authors state the weak convergence of the usual empirical copula process in for some set of functions from to . Indeed, first, such functions are assumed to be right-continuous and of bounded variation in the sense of Hardy-Krause (see their Assumption F) when we consider general borelian subsets . Second and more importantly, it is not possible to recover our processes or of interest with some quantities as for some particular function and a usual empirical copula process .

2.2 Multiple conditioning subsets

We now consider a finite family of borelian subsets such that w have for every and a given . Set . The subsets in may be disjoint or not. By the same reasonings as above in a -dimensional setting, we can easily prove the weak convergence of the process defined on as

for every , , where .

Theorem 5.

If, for every , and Condition 1 holds for , then weakly tends to a multivariate centered Gaussian process in , where

The proof is straightforward and left to the reader. The latter result is obviously true replacing by . It will be useful for building and testing the relevance of some partitions of the space of covariates, in the spirit of Pearson’s chi-square test. Typically, this means testing the equality between the copulas and for several couples .

We can specify the covariance function of and , for any vectors and in by recalling that

where , and by noting that

| (5) |

for every . Note we have not imposed that the subsets of are disjoint. Nonetheless, in the case of a partition (disjoint subsets ), calculations become significantly simpler because of the nullity of .

Simple (but tedious) calculations yield the covariance function of the limiting vectorial conditional copula process . Moreover, the latter covariance can be empirically estimated: see Appendix B.

3 Bootstrap approximations

The limiting laws of the previous empirical processes , (or even and ) are complex. Therefore, it is difficult to evaluate the weak limits of some functionals of the latter processes, in particular the asymptotic variances of some test statistics that may be built from them. The usual answer to this problem is to rely on bootstrap schemes. In this section, we study the validity of some bootstrap schemes for our particular empirical copula processes. We will prove the validity of the general exchangeable bootstrap for such processes, a result that has apparently never been stated in the literature even in the case of usual copulas, to the best of our knowledge. Moreover, we extend the nonparametric bootstrap and the multiplier bootstrap techniques to the case of conditioning events that have a non-zero probability (the case of pointwise events is dealt in [38]).

3.1 The exchangeable bootstrap

For the sake of generality, we rely on the exchangeable bootstrap (also called “wild bootstrap” by some authors), as introduced in [59]. For every , let be an exchangeable nonnegative random vector and its average. For any borelian subset , , the weighted empirical bootstrap process of that is related to our initial i.i.d. sample is defined as

We require the standard conditions on the weights (see Theorem (3.6.13) in [59]).

Condition 2.

Note that can be calculated, contrary to . Since its asymptotic law will be “close to” the limiting law of when tends to the infinifty, resampling many times the vector allows the calculation of many realizations of , given the initial sample. This yields a numerical way of approximating the limiting law of or some functionals of the latter process. This is the usual and fruitful idea of most resampling techniques.

The same reasoning will apply to the copula processes and , due to the relationships (3) and (4): to prove the validity of an exchangeable bootstrap scheme for the latter copula processes, we first approximate the unfeasible process by the weighted empirical bootstrapped process ; second, we invoke Theorem 1 to obtain a similar results for ; third, we use the relationship between and and deduce a bootstrap approximation for our “conditioned” copula processes.

To be specific, let us consider independent realizations of the vector of weights (that are mutually independent draws and independent of the initial sample), and the associated processes , . We first prove the validity of our bootstrap scheme for . Denote by the process defined on as

for every vectors in . Moreover, denote by a process on that concatenates independent versions of the Brownian bridge introduced in Corollary 2.

Theorem 6.

Under Condition 2, for any and when , the process weakly tends to in .

See the proof in Section A.2 of the appendix. The latter result validates the use of the considered bootstrap scheme. It has not to be confused with fidi weak convergence of , that is just a consequence of Theorem 6.

Thus, we can easily build a bootstrap estimator of , and then of . Recalling Equation (3), we evaluate the partial derivatives of as in [31]: for every ,

| (6) |

where , and with obvious notations. Now, the bootstrapped version of is defined as

| (7) |

Importantly, note the latter process is a valid bootstrapped approximation of too, because and have the same limiting law (Theorem 1).

Denote by the process defined on by

Moreover, denote by a process on that concatenates independent versions of , as defined in Corollary 2. Then, we are able to state the validity of the exchangeable bootstrap for .

Proof.

Recalling Equation (4), we deduce an exchangeable bootstrapped version of , defined as

| (8) |

Still considering independent random realizations of , we finally introduce the joint process whose trajectories are

for every in .

Corollary 8.

In other words, we can approximate the limiting law of by the law of , that is obtained by simulating many times independent realizations of the vector of weights , given the initial sample .

Remark 9.

Let be a sequence of i.i.d. random variables, with mean zero and variance one. Formally, we can set for every and every , even if the are not always nonnegative. The same formulas as before yield some feasible bootstrapped processes that are similar to those obtained with the multiplier bootstrap of [46], or in [54], Prop. 3.2. With the same techniques of proofs as above, it can be proved that this bootstrap scheme is valid, invoking Theorem 10.1 and Corollary 10.3 in [32] instead of Theorem 3.6.13 in [59]. Therefore, we can state that Corollary 8 applies, replacing with i.i.d. normalized weights. In other words, the multiplier bootstrap methodology applies with empirical copula processes “indexed by” borelian subsets.

It is straightforward to state some extensions of the latter results when considering several subsets simultaneously, as in Section 2.2. With the same notations, let us do this task in the case of our previous bootstrap estimates. To this goal, denote , , for every , ,

3.2 The nonparametric bootstrap

When is drawn along a multinomial law with parameter and probabilities , we recover the original idea of Efron’s usual nonparametric bootstrap, here applied to the estimation of the limiting law of . Nonetheless, our final bootstrap counterparts for or are not the same as the commonly met nonparametric bootstrap processes. In particular, our methodology is analytically more demanding than what is commonly met with nonparametric bootstrap schemes. Indeed, the usual way of working in the latter case is simply to resample with replacement the initial sample and to recalculate the statistics of interest with the bootstrapped sample exactly in the same manner as with the initial sample. In practical terms, all analytics and IT codes can be reused as many times as necessary without any additional work. This is not really the case when using the exchangeable bootstrap above, even in the simple case of multinomial weights: the formulas (7) or (8) necessitate to “rework” the initial estimation procedures. In particular, it is necessary to write our statistics of interest as for some regular functional . Thus, the bootstrapped statistic is . Sometimes, specifying may be boring because of the use of multiple step estimators and/or nuisance parameters.

This additional stage (the calculation of ) can be avoided. Indeed, note that the empirical copula may be seen as a regular functional of , the usual empirical distribution of , i.e. . Now, it is tempting to apply Efron’s initial idea by resampling with replacement realizations of among the initial sample, and to set , being the empirical cdf associated to the bootstrapped sample . Actually, this standard bootstrap scheme is valid but under slightly stronger conditions than for the exchangeable bootstrap schemes of Section 3.1. In the case of the usual empirical copula process, the validity of this nonparametric bootstrap has been proven in [17] by applying the functional Delta-Method. Similarly, this technique can be applied in our case.

To be specific, for every , set

the empirical counterpart of . Let be the empirical cdf of . Note that for some functional from the space of cadlag functions on , with values in the space of cadlag functions on , and defined by

It is easy to check that the latter function is Hadamard differentiable at every cdf on s.t. . Its derivative at is given by

Moreover, , introducing a map from the space of cadlag functions on to by

Assume the copula is continuously differentiable on the whole hypercube , a stronger assumption than our Condition 1, as pointed out by [54]. Then, Lemma 2 in [17] states that is Hadamard-differentiable tangentially to , the space of continuous maps on . By the chain rule (Lemma 3.9.3 in [59]), this means that is still Hadamard differentiable tangentially to and its derivative is This is the main condition to apply the Delta-Method for bootstrap (Theorem 3.9.11 in [59], e.g.).

The nonparametric bootstrapped empirical copula associated with is then defined as

and the associated bootstrapped copula process is given by

Obviously, (resp. ) is the associated empirical cdf (resp. empirical marginal cdfs’) associated to the nonparametric bootstrap sample . By mimicking the arguments of [17], Theorem 5, it is easy to state the validity of the nonparametric bootstrap scheme for . Details are left to the reader. To simply announce the result, introduce the random map

for every vectors in .

Theorem 11.

If the copula is continuously differentiable on and , then the process weakly converges in to a process that concatenates independent versions of .

As for the exchangeable bootstrap case, we can extend the latter results when dealing with several subsets simultaneously. Then, still considering borelian subsets in , for every , for every , , set

Theorem 12.

If the copulas are continuously differentiable on and for every , then, for every and when , the process weakly converges in to a process that concatenates independent versions of .

4 Application to Generalized dependence measures

4.1 A single conditioning subset

Dependence measures (also called “measures of concordance” or “measures of association” by some authors; see [35], Def. 5.1.7.) are real numbers that summarize the amount of dependencies across the components of a random vector. Most of the time, they are defined for bivariate vectors, as originally formalized in [48]. The most usual ones are Kendall’s tau, Spearman’s rho, Gini’s measures of association and Blomqvist’s beta. Denoting by the copula of a bivariate random vector , all these measures can be rewritten as weighted sums of quantities as for some measurable map , , or as for some measure on . For example, in the case of Kendall’s tau (resp. Spearman’s rho), the first case (resp. second case) applies by setting and (resp. , ). Gini’s index is , with . Blomqvist’s beta is obtained with , where denotes the Dirac measure at . See [35], Chapter 5, or [36] for some justifications of the latter results and additional results.

A few multivariate extensions of the latter measures have been introduced in the literature for many years. The axiomatic justification of such measures for -dimensional random vectors has been developed in [58], and many proposals followed, sometimes in passing. The most extensive analysis has been led in a series of papers by F. Schmid, R. Schmidt and some co-authors: c.f. [50, 51, 52, 53].

Actually, we can even more extend the previous ideas by considering general formulas for multivariate dependence measures, possibly indexed by subsets (of covariates), as in the previous sections. To be specific, we still consider a random vector and we will be interested in dependence measures between the components of , when belongs to some borelian subset in . For any (possibly empty) subsets and that are included in , let us define

| (9) |

for some measurable function . Obviously, denotes the conditional copula of given . In particular, , for every . When (resp. ) there is no integration w.r.t. (resp. ).

The latter definition virtually includes and/or extends all unconditional and conditional dependence measures that have been introduced until now. Indeed, such dependence measures are linear combinations (or even ratios, possibly) of our quantities , for conveniently chosen and . Note that, by setting , we recover unconditional dependence measures. Moreover, setting allows to study pointwise conditional dependence measures.

A few examples of such that have already been met in the literature:

- •

- •

- •

- •

-

•

, and corresponds to a conditional version of Blomqvist coefficient ([35]);

-

•

, and yields a conditional version of the tail-dependence coefficient considered in [51];

-

•

if is a density on , and , we get some conditional product measures of concordance, as defined in [58];

-

•

when is a weighted sum of reflection indicators of the type

where for every , we obtain some generalizations of dependence measures (Kendall’s tau, Blomqvist coefficient, etc), as introduced in [27]. For conveniently chosen weights, such linear combinations of for different subsets and yield dependence measures that are increasing w.r.t. a so-called “concordance ordering” property. See [58], Examples 7 and 8, too. Etc.

Note that our methodology includes as particular cases some multivariate dependence measures that are calculated as averages of “usual” dependence measures when they are calculated for many pairs , . This old and simple idea (see [29]) has been promoted by some authors. See such type of multivariate dependence measures in [53] and the references therein.

Generally speaking, it is possible to estimate the latter quantities after replacing the conditional copulas by their estimates in Equation (9). This yields the estimator

| (10) |

where we define

and similarly for the induced measure .

Then, the weak convergence of the process will provide the limiting law of . Indeed, the map

| (11) |

is Hadamard differentiable from , the space of cdfs’ on , onto . To prove the latter result, for every , denote

Lemma 13.

If is continuous on and the map is of bounded variation on , then the map is Hadamard-differentiable at every -dimensional copula , tangentially to the set of real functions that are continuous on . Its derivative is given by

for any continuous map .

When is not of bounded variation, we define the second integral of by an integration by parts, as detailed in [45]. See the proof of Lemma 13 in the appendix, Section A.3.

As a consequence, by applying the Delta Method (Theorem 3.9.4 in [59]) to the copula process , we obtain the asymptotic normality of .

As an example, let us consider the multivariate Spearman’s rho obtained when setting , , , , and , for some threshold in . In other words, we focus on

This measure is related to the average dependencies among the components of , knowing that all such components are observed in their own tails. Indeed, we are interested in the joint tail for every . Such an indicator has been introduced in [50] but its properties have not been studied. Indeed, the authors wrote: “Certainly, this version would be interesting to investigate, too, although its analytics and the nonparametrical statistical inference are difficult”. Therefore, they prefer to concentrate on other Spearman’s rho-type dependence measures. Now, we fill this gap by applying Theorem 14. With our notations, a natural estimator of is

Corollary 15.

If and Condition 1 holds, then

The analytic formula of is provided in Appendix B. The asymptotic variance can be consistently estimated after replacing the unknown quantities , , and its partial derivatives by some empirical counterparts, as in the latter appendix. Alternatively, the limiting law of can be obtained by several bootstrap schemes, as explained in Section 3. Indeed, since , a bootstrap equivalent of the latter statistics is or , with the same notations as above and conveniently chosen bootstrap weights.

4.2 Multiple conditioning subsets

Important practical questions arise considering several borelian subsets simultaneously. For instance, is the amount of dependencies among the ’s components the same when belongs to different subsets? This questioning can lead to a way of building relevant subsets , . Typically, a nice partition of the -space is obtained when the copulas are heterogeneous. This is why we now extend the previous framework to be able to answer such questions.

To this goal, let be a family of borelian subsets, for every . Moreover, denote by , some subsets of indices in . To lighten notations, set

for every . Note that we allow different measurable maps .

As above, we can deduce the asymptotic law of from the weak convergence of the random vectorial process (Theorem 5). Denote by the map from to defined by

| (12) |

Moreover, set for every cdf on . The next lemma is a straightforward extension of Lemma 13. Denote , for a given set of copulas on .

Lemma 16.

If, for every , the map is continuous on and is of bounded variation on , then is Hadamard-differentiable at , tangentially to the set of real functions that are continuous on . Its derivative is given by

for any continuous map , for every .

In the latter result, we have implicitly assumed that involves the function. By the Delta method, we deduce the joint asymptotic normality of our statistics of interest.

Theorem 17.

As an application, let us consider the test of the zero assumption

This can be tackled through any generalized dependence measure , for some fixed subsets and and a unique function . In other words, with our previous notations, for every . Indeed, we can build a test statistic of the form

where is any semi-norm on . For example, define the Cramer-von Mises type statistic

or the Kolmogorov-Smirnov type test statistic

Note that under the null hypothesis, these test statistics can be rewritten as

Therefore, under , Theorem 17 tells us that (once properly rescaled) is weakly convergent. Since its limiting law is complex, we advise to use bootstrap approximations to evaluate the asymptotic p-values associate to in practice, or simply its asymptotic variance. A bootstrapped version of such tests statistics is

where, in the case of the multiplier bootstrap, we set

and, in the case of the nonparametric bootstrap,

5 Application to the dependence between financial returns

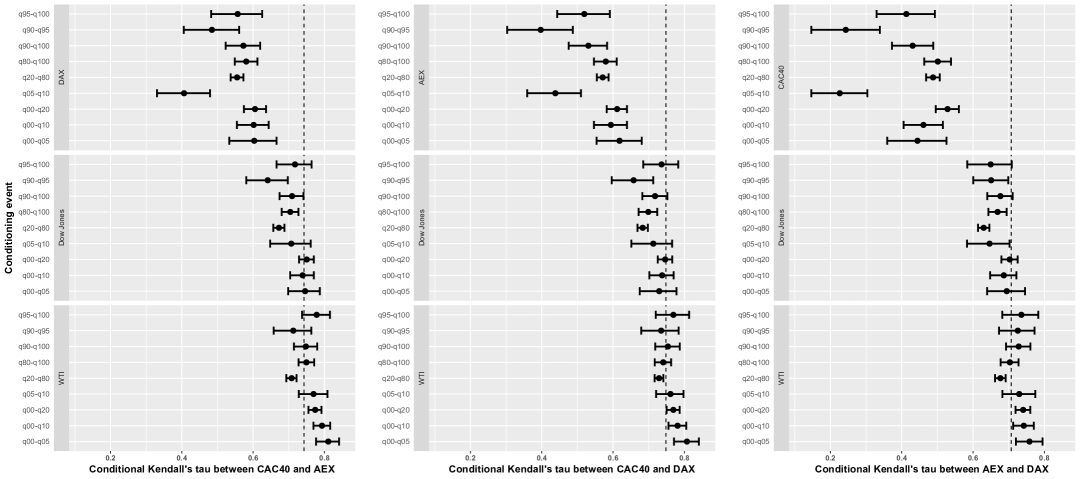

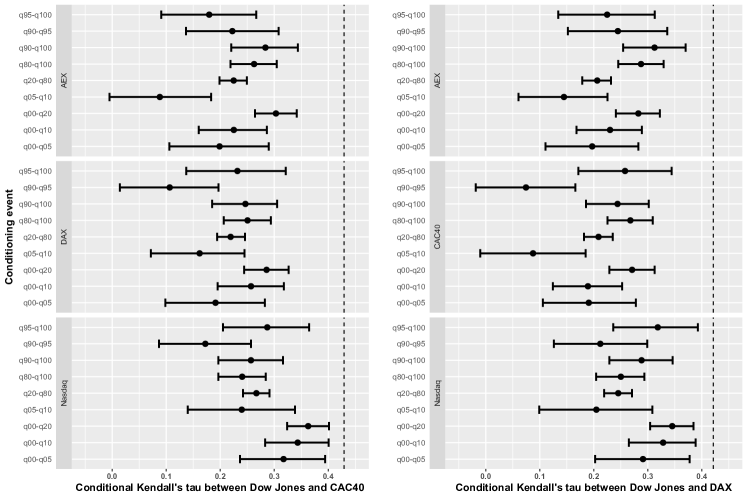

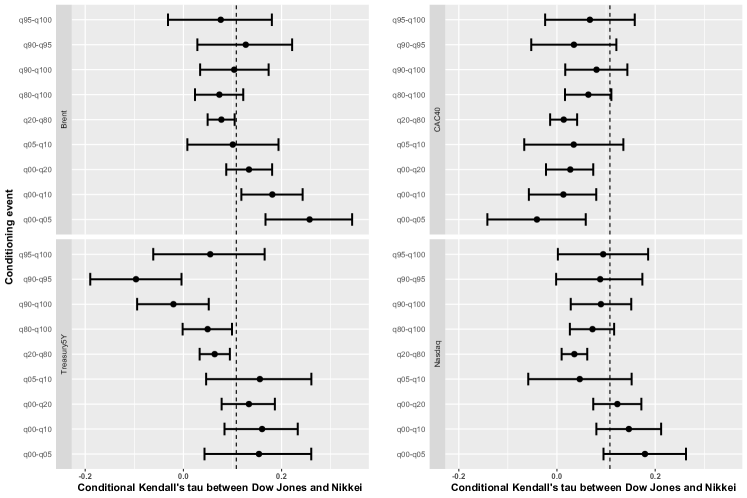

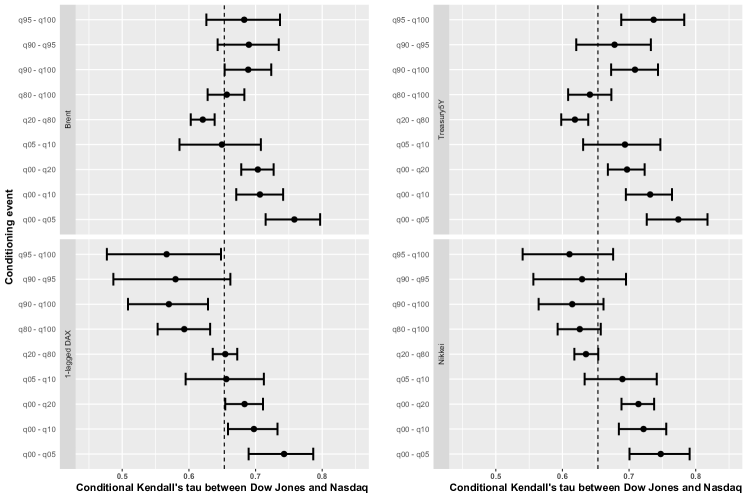

The data that we are considering is made up of three European stock indices (the French CAC40, the German DAX Performance Index and the Dutch Amsterdam Exchange index called AEX), two US stock indices (the Dow Jones Index and the Nasdaq Composite Index), the Japan Nikkei 225 Index, two oil prices (the Brent Crude Oil and the West Texas Intermediate called WTI) and the Treasury Yield 5 Years (denoted as Treasury5Y). These variables are observed daily from the 16th September 2008 (the day following Lehman’s bankruptcy) to the 11th August 2020. We compute the returns of all these variables. We realize an ARMA-GARCH filtering on each marginal return using the R package fGarch [63] and choosing the order which minimizes the BIC. The nine final variables are defined as the innovations of these processes.

Each variable , can play the role of the conditioning variable . When this is the case, we consider boxes determined by their quantiles. This yields nine boxes, defined as follows: , , , , , , , , . In the following, we always consider conditioning by one variable only.

Our measure of conditional dependence will be (conditional) Kendall’s tau. Because of the high number of triplets (i.e. couples given belongs to some subset), we do not consider every combination of conditioned and conditioning variable, but only report a few relevant ones. Figure 1 is devoted to the dependence between European indices. Figure 2 is related to the dependence between European indices and the Dow Jones. Figure 3 deals with dependencies between the Dow Jones and the Nikkei indices. Dependencies between US indices appear in Figure 4. In all figures, the dotted line represents the unconditional Kendall’s tau of the considered pair of variables.

Note that , where denotes disjoint union. Nevertheless, the unconditional Kendall’s tau cannot be decomposed (and then deduced) using only the conditional Kendall’s taus , and . Indeed,

| (13) | |||||

Formally, we can decompose the probability measure as for any borelian . Expanding in (13), we indeed get terms such as the conditional Kendall’s tau , but also “co-Kendall’s taus” that involve integrals with respect to some measures , . Therefore, it is possible that all conditional Kendall’s taus are strictly smaller (or larger) than the corresponding unconditional Kendall’s tau. This is indeed the case for the couple , and (see Figure 1).

Many interesting features appear on such figures. For instance, the levels of dependence between two European stock indices (CAC40 and AEX, e.g.) are significantly varying depending on another European index (say, DAX). At the opposite, they are globally insensitive to shocks on the main US index or on oil prices. This illustrates the maturity of the integration of European equity markets. Note that the strength of such moves matters: dependencies given average shocks (when belongs to or ) are generally smaller than those in the case of extreme moves (when belongs to or , e.g.). This is a rather general feature for most figures. Moreover, dependencies are most often larger when the conditioning events are related to “bad news” (negative shocks on stocks, sudden jumps for interest rates), compared to ”good news” (the opposite events): see Figure 4, that refers to the couple (Dow Jones, Nasdaq). When the pairs of stock returns are related to two different countries, dependence levels are globally smaller on average, but this does not preclude significant variations knowing another financial variable belongs to some range of values. Therefore, when Treasuries are strongly rising, the dependence between Dow Jones and Nikkei can become negative - an unusual value - although it is positive unconditionally.

6 Conclusion

We have made several contributions to the theory of the weak convergence of empirical copula processes, their associated bootstrap schemes and multivariate dependence measures. Now, all these concepts and results are stated not only for usual copulas but for conditional copulas too, i.e. for the copula of knowing that some vector of covariates (that may be equal to ) belongs to one or several borelian subsets. We only require that the probabilities of the latter events are nonzero. Therefore, we do not deal with pointwise conditioning events as for some particular vector . But the main advantage of working with -subsets instead of singletons is to avoid the curse of dimension that rapidly appears when the dimension of is larger than three.

Once we have proved the weak convergence of the conditional empirical copula process , possibly with multiple borelian subsets , the inference and testing of copula models becomes relatively easy. An interesting avenue for further research will be to use our results to build convenient discretizations of the covariate space (the space of our so-called random vectors ). There is a need to find efficient algorithms and statistical procedures to build a partition of with borelian subsets , so that the dependencies across the components of are “similar” when belongs to one of theses subsets, but as different as possible from box to box: “maximum homogeneity intra, maximum heterogeneity inter”. A constructive tree-based approach should be feasible, as proposed in [33] in the case of vine modeling.

Acknowledgements

Jean-David Fermanian’s work has been supported by the labex Ecodec (reference project ANR-11-LABEX-0047).

References

- [1] Aas, K., Czado, C., Frigessi, A. and Bakken, H. (2009). Pair-copula constructions of multiple dependence. Insurance Math. Econom., 44(2), .

- [2] Abegaz, F., Gijbels, I. and Veraverbeke, N. (2012). Semiparametric estimation of conditional copulas. J. Multivariate Anal., 110, .

- [3] Acar, E.F., Craiu, R.V. and Yao, F. (2011). Dependence Calibration in Conditional copulas: A Nonparametric Approach. Biometrics, 67, .

- [4] Acar, E.F., Craiu, R.V. and Yao, F. (2013). Statistical testing of covariate effects in conditional copula models. Electron. J. Stat., 7, .

- [5] Bedford, T. and Cooke, R.M. (2001). Probability density decomposition for conditionally dependent random variables modeled by vines. Ann. Math. Artif. Intell., 32(1-4), .

- [6] Bedford, T. and Cooke, R.M. (2002). Vines: A new graphical model for dependent random variables. Ann. Statist., .

- [7] Brechmann, E.C., Hendrich, K. and Czado, C. (2013). Conditional copula simulation for systemic risk stress testing. Insurance Math. Econom., 53(3), .

- [8] Bücher, A. and Kojadinovic, I. (2019). A note on conditional versus joint unconditional weak convergence in bootstrap consistency results. J. Theoret. Probab., 32(3), .

- [9] Christoffersen, P., Errunza, V., Jacobs, K. and Langlois, H. (2012). Is the potential for international diversification disappearing? A dynamic copula approach. The Review of Financial Studies, 25(12), .

- [10] Czado, C. (2019). Analyzing Dependent Data with Vine Copulas. Lecture Notes in Statistics, Springer.

- [11] Derumigny, A. and Fermanian, J.-D. (2017). About tests of the “simplifying” assumption for conditional copulas. Depend. Model., 5(1), 154-197.

- [12] Derumigny, A. and Fermanian, J.-D. (2019). On kernel-based estimation of conditional Kendall’s tau: finite-distance bounds and asymptotic behavior. Depend. Model., 7(1), 292-321

- [13] Derumigny, A. and Fermanian, J.-D. (2020). About Kendall’s regression. To appear in J. Multivariate Anal.

- [14] Durante, F. and Jaworski, P. (2010). Spatial contagion between financial markets: a copula-based approach. Appl. Stoch. Models Bus. Ind., 26(5), .

- [15] Durante, F., Pappadà, R. and Torelli, N. (2014). Clustering of financial time series in risky scenarios. Adv. Data Anal. Classif., 8(4), .

- [16] Fang, Y. and Madsen, L. (2013). Modified Gaussian pseudo-copula: Applications in insurance and finance. Insurance Math. Econom., 53(1), .

- [17] Fermanian, J.-D., Radulovic, D. and Wegkamp, M. (2004). Weak convergence of empirical copula processes. Bernoulli, 10(5), .

- [18] Fermanian J.-D. and Wegkamp, M. (2012). Time-dependent copulas. J. Multivariate Anal.. 110, .

- [19] Fermanian J.-D. and Lopez, O. (2018). Single-index copulas. J. Multivariate Anal., 165, .

- [20] Genest, C., Nelehová, J. and Ben Ghorbal, N. (2011). Estimators based on Kendall’s tau in multivariate copula models. Aust. N.Z. J. Stat., 53, .

- [21] Gijbels, I., Veraverbeke, N. and Omelka, M. (2011). Conditional copulas, association measures and their applications. Comput. Statist. Data Anal., 55, .

- [22] Gijbels, I., Veraverbeke, N. and Omelka, M. (2015a). Estimation of a Copula when a Covariate Affects only Marginal Distributions. Scand. J. Stat., 42, .

- [23] Gijbels, I., Omelka, M. and Veraverbeke, N. (2017). Nonparametric testing for no covariate effects in conditional copulas. Statistics, 51(3), .

- [24] Goodwin, B.K. and Hungerford, A. (2015). Copula-based models of systemic risk in US agriculture: implications for crop insurance and reinsurance contracts. American Journal of Agricultural Economics, 97(3), .

- [25] Hesami Afshar, M., Sorman, A.U. and Yilmaz, M.T. (2016). Conditional copula-based spatial–temporal drought characteristics analysis—a case study over Turkey. Water, 8(10), .

- [26] Hobæk Haff, I., Aas, K. and Frigessi, A. (2010). On the simplified pair-copula construction–simply useful or too simplistic? J. Multivariate Anal., 101, .

- [27] Joe, H. (1990). Multivariate concordance, J. Multivariate Anal., 35, .

- [28] Jondeau, E. and Rockinger, M. (2006). The copula-garch model of conditional dependencies: An international stock market application. J. Internat. Money Finance, 25, .

- [29] Kendall, M.G. and Babington Smith, B. (1940). On the method of paired comparisons. Biometrika, 31, .

- [30] Kim, J.Y., Park, C.Y. and Kwon, H.H. (2016). A development of downscaling scheme for sub-daily extreme precipitation using conditional copula model. Journal of Korea Water Resources Association, 49(10), .

- [31] Kojadinovic, I., Segers, J. and Yan, J. (2011). Large sample tests of extreme value dependence for multivariate copulas. Canad. J. Statist., 39(4), .

- [32] Kosorok, M.R. (2007). Introduction to empirical processes and semiparametric inference. Springer Science.

- [33] Kurz, M.S. and Spanhel, F. (2017). Testing the simplifying assumption in high-dimensional vine copulas. arXiv:1706.02338

- [34] Manner, H. and Reznikova, O. (2012). A survey on time-varying copulas: specification, simulations, and application. Econometric reviews, 31(6), .

- [35] Nelsen, R.B. (1999). An introduction to copulas, Lecture Notes in Statistics, vol. 139. Springer-Verlag, New York.

- [36] Nelsen, R.B. (2002). Concordance and copulas: A survey. In C. M. Cuadras, J. Fortiana, J. A. Rodriguez-Lallena (Eds.), Distributions with given marginals and statistical modelling (pp.16-177) Dordrecht: Kluwer.

- [37] Oh, D.H. and Patton, A.J. (2018). Time-varying systemic risk: Evidence from a dynamic copula model of cds spreads. Journal of Business & Economic Statistics, 36(2), .

- [38] Omelka, M., Veraverbeke, N. and Gijbels, I. (2013). Bootstrapping the conditional copula. J. Statist. Plann. Inference, 143, .

- [39] Palaro, H.P. and Hotta, L.K. (2006). Using conditional copula to estimate value at risk. Journal of Data Science, 4, .

- [40] Patton, A. (2006a) Modelling Asymmetric Exchange Rate Dependence, Internat. Econom. Rev., 47, .

- [41] Patton, A. (2006b) Estimation of multivariate models for time series of possibly different lengths. J. Appl. Econometrics, 21, .

- [42] Patton, A.J. (2009). Copula–based models for financial time series. In Handbook of financial time series (pp. 767-785). Springer, Berlin, Heidelberg.

- [43] Patton, A.J. (2012). A review of copula models for economic time series. J. Multivariate Anal., 110, .

- [44] Portier, F. and Segers, J. (2018). On the weak convergence of the empirical conditional copula under a simplifying assumption. J. Multivariate Anal., 166, .

- [45] Radulović, D., Wegkamp M. and Zhao, Y. (2017). Weak convergence of empirical copula processes indexed by functions. Bernoulli, 23(8), .

- [46] Rémillard, B. and Scaillet, O. (2009). Testing for Equality between Two copulas. J. Multivariate Anal., 100, .

- [47] Ruymgaart, F.H. and van Zuijlen, M.C.A. (1978). Asymptotic normality of multivariate linear rank statistics in the non-iid case. Ann. Statist., .

- [48] Scarsini, M. (1984). On measures of concordance. Stochastica, 8(3), .

- [49] Schellhase, C. and Spanhel, F. (2018). Estimating non-simplified vine copulas using penalized splines. Stat. Comput., 28(2), .

- [50] Schmid, F. and Schmidt, R. (2007). Multivariate extensions of Spearman’s rho and related statistics. Statist. & Probab. Lett., 77, .

- [51] Schmid, F. and Schmidt, R. (2007). Nonparametric inference on multivariate versions of Blomqvist’s beta and related measures of tail dependence. Metrika, 66(3), .

- [52] Schmid, F. and Schmidt, R. (2007). Multivariate conditional versions of Spearman’s rho and related measures of tail dependence. J. Multivariate Anal., 98(6), .

- [53] Schmid, F., Schmidt, R., Blumentritt, T., Gaißer, S. and Ruppert, M. (2010). Copula-based measures of multivariate association. In Copula theory and its applications (pp. 209-236). Springer, Berlin, Heidelberg.

- [54] Segers, J. (2012). Asymptotics of empirical copula processes under non-restrictive smoothness assumptions. Bernoulli, 18(3), .

- [55] Shorack, G.R. and Wellner, J.A. (2009). Empirical processes with applications to statistics. Society for Industrial and Applied Mathematics.

- [56] Spanhel, F. and M.S. Kurz (2017). The partial vine copula: A dependence measure and approximation based on the simplifying assumption. arXiv:1510-06971.

- [57] Spanhel, F. and Kurz, M.S. (2019). Simplified vine copula models: Approximations based on the simplifying assumption. Electron. J. Stat., 13(1), .

- [58] Taylor, M.D. (2007). Multivariate measures of concordance. Ann. Inst. Statist. Math., 59(4), .

- [59] van der Vaart, A. and Wellner, J. (1996). Weak convergence and empirical processes. Springer.

- [60] Vatter, T. and Chavez-Demoulin, V. (2015). Generalized additive models for conditional dependence structures. J. Multivariate Anal., 141, .

- [61] Veraverbeke, N., Omelka, M. and Gijbels, I. (2011). Estimation of a Conditional Copula and Association Measures. Scand. J. Stat., 38, .

- [62] Wolff, E.F. (1980). N-dimensional measures of dependence. Stochastica, 4(3), .

- [63] Wuertz, D. et al. (2020). fGarch: Rmetrics - Autoregressive Conditional Heteroskedastic Modelling. R package version 3042.83.2. https://CRAN.R-project.org/package=fGarch.

Appendix A Proofs

A.1 Proof of Theorem 1

Let us introduce the vector of (unobservable) empirical quantiles

Then, note that . As in [54], let us decompose

| (14) | |||||

As a usual empirical process, weakly tends to a Gaussian process in , here the Brownian bridge , defined in Corollary 2. In particular, it is equicontinuous. Note that tends to the infinity a.s. when tends to the infinity. Then, tends to zero a.s. for every , when (and then ) tends to the infinity. Therefore, the equicontinuity of implies

| (15) |

when .

Moreover, fix and define for any . By the mean value theorem, there exists s.t.

The latter identity is true whatever the values of , even if one of its components is zero (see the discussion in [54], p.769). Denote by the unit vector in corresponding to the -th component. For every and , we have, with obvious notations,

We deduce

and then , when the latter partial derivative exists.

Due to the Bahadur-Kiefer theorems (see [55], chapter 15), it is known that

for every , when tends to the infinity. We deduce

tends to zero in probability, as tends to the infinity.

A.2 Proof of Theorem 6

Let be the empirical measure associated to . Set the weighted bootstrap empirical process . For every and , denote by , and the maps from to defined by

The latter functions implicitly depend on the borelian subset . Set the classes of functions , and . Note that and are subsets of and that . Moreover, with some usual change of variables, we have

For every , we have

that tends to zero a.s. (see [55], Chapter 13). This yields. Since the process is weakly convergent in (Theorem 3.6.13 in [59]), it is equicontinuous and then . Therefore, the weak limit of on is the same as the weak limit of on (also denoted ).

Since is Donsker, Theorem 3.6.13 in [59] yields

Here, denotes the set of functions s.t. . Moreover, due to the weak convergence of in ,

Thus, the bounded Lipschitz metric between the measures and tends to zero in outer probability. Apply Lemma 2.2 in [8] (equivalence between the items (b) and (c)) to obtain the stated result.

A.3 Proof of Lemma 13

Let be the space of right-continuous functions that are of bounded variation on in the sense of Hardy-Krause (see [45] and the references therein, for instance), and whose total variation is bounded by a constant , as in [59], Lemma 3.9.17. We can define on the space by Equation (11). Let be a sequence of nonzero real numbers, when . Consider a sequence of functions from to s.t. belongs to and tends to a continuous function in sup-norm. Let us expand

If then . Otherwise, since tends to zero and

we get .

Moreover, if , then . Otherwise, can always be defined by an integration by parts formula (Theorem 15 in [45]) that involves a finite number of terms as

for some subsets of indices and some vectors , with obvious vectorial notations. Since is of bounded variation and tends to zero, this yields .

If , then . Otherwise, note that the total variation of is less than a constant . Therefore, the total variation of is less than . We deduce tends to zero when .

If , then because . To tackle the last term when , we use the uniform continuity of the function on the compact subset , as in Lemma 1 in [21]: for every , there exists a partition of with disjoint hyper-rectangles such that the stepwise function satisfies

Then, we obtain

Note that is bounded by a constant because it is uniformly convergent to the continuous map . Therefore, for some constant . Then, for a given and when is sufficiently large, . This means , concluding the proof.

Appendix B Covariance function of

For every and in and two borel subsets and in , denote

When , this is the covariance function of the Gaussian process , as given in Corollary 2. In the general case, it is given in (5). The goal is here to calculate the covariance function of the limiting processes obtained in Theorem 3 and 5. To lighten notations, simply write instead of and instead of , . By lengthly but simple calculations, we obtain

For a given subset , we get the covariance map of the limiting process . In this case, we denote . Then, check that , , and , for any indices in . Moreover, when ,

and Finally, and .

When there is a single subset , the covariance can be easily estimated by replacing every unknown term above by an empirical counterpart. Therefore, may be estimated by

Moreover any quantity and would be estimated by and (see Equation (6)) respectively.

With multiple subsets , the task is slightly more complex. Indeed, recall that

Reasoning as in Section 2.1, we easily see that any quantity can be empirically estimated by defined as

for every and every indices in . When and are disjoint, as in the case of partitions, the latter quantity is simply zero. In every case, is consistently estimated by .