Optimal Network Compression

Abstract

This paper introduces a formulation of the optimal network compression problem for financial systems. This general formulation is presented for different levels of network compression or rerouting allowed from the initial interbank network. We prove that this problem is, generically, NP-hard. We focus on objective functions generated by systemic risk measures under shocks to the financial network. We use this framework to study the (sub)optimality of the maximally compressed network. We conclude by studying the optimal compression problem for specific networks; this permits us to study, e.g., the so-called robust fragility of certain network topologies more generally as well as the potential benefits and costs of network compression. In particular, under systematic shocks and heterogeneous financial networks the robust fragility results of Acemoglu et al. (2015) no longer hold generally.

Keywords: Finance, systemic risk, financial networks, portfolio compression, systematic shocks, genetic algorithm.

1 Introduction

The financial crisis 2007-2009 has highlighted the importance of network structure on the amplification of the initial shock to the level of the global financial system, leading to an economic recession. In response to market dysfunctions, the US congress enacted the largest regulations of the financial market, in the form of the "Dodd-Frank Wall Street Reform and Consumer Protection Act" of 2010, to ensure financial stability and reduce systemic risk. Among the regulations is that the majority of over-the-counter (OTC) derivatives should be centrally cleared so as to reduce counterparty risk and ensure financial stability. Portfolio compression is another way to modify the financial network structure.111We interchangeably use the terms ‘portfolio compression’ and ‘network compression’ to mean the process of modifying the financial network structure by reducing the gross positions in the network while keeping net positions unchanged. Though ‘portfolio compression’ is more common in the literature (see, e.g., D’Errico and Roukny (2021); Veraart (2022)), we introduce the term ‘network compression’ as it explicitly describes the shrinking of the network size being studied. Several parties in the network enter into a multi-lateral netting agreement to essentially reduce the gross exposures while keeping the net positions unchanged. The main provider of such systems is TriOptima TriOptima (2021), who have compressed over quadrillion in gross notional.

For the purposes of this paper we consider a known initial finite network of obligations over which we seek an “optimal” network compression. This is in contrast to the random graph structure considered in Amini et al. (2016a); Elliott et al. (2014); Gai and Kapadia (2010). Though the initial network compression formulation is presented without consideration of the network clearing procedure, we will primarily focus on clearing based on Eisenberg and Noe (2001); Rogers and Veraart (2013) with collateral as presented in, e.g., Ghamami et al. (2022); Veraart (2022). Under the DebtRank Battiston et al. (2012); Bardoscia et al. (2015) clearing, a version of the optimal network compression problem as a mixed integer linear program was proposed in Diem et al. (2020). Other notions of contagion could be added to our clearing problem as well, e.g., portfolio overlap Cifuentes et al. (2005); Amini et al. (2016c); Feinstein (2017); such additional avenues of contagion would influence the systemic risk and may impact the optimal compression. We focus on the collateralized Eisenberg-Noe framework so as to remain in a, relatively, simple setting.

1.1 Literature Review

The optimal compression problem is related to studies in many other works in the Eisenberg-Noe clearing framework. For instance, the compression constraints can be viewed as the feasibility conditions for a network reconstruction problem via the network rerouting problem (see Example 2.3) in which only the aggregate statistics for each bank need be known; Anand et al. (2015); Upper and Worms (2004); Hałaj and Kok (2013); Gandy and Veraart (2016, 2019) propose methods to sample either deterministically or stochastically from this feasible region. Acemoglu et al. (2015) considered the optimal rerouting problem of a system of identical banks under i.i.d. Bernoulli shocks. That work found that the completely connected system has a “robust fragility” property, i.e., it is the most stable for small shocks but the least stable for large shocks (and vice versa for the ring network). Feinstein et al. (2018) studies the sensitivity of the Eisenberg-Noe clearing payments w.r.t. the relative liability matrix; that work uses these sensitivities in order to find the best and worst case directions for rerouting of the liability network. Capponi et al. (2016) utilizes majorization of the financial networks in order to guarantee the relative health of two financial networks (w.r.t. the number of defaulting banks). The network compression is also related to the literature on analyzing the consequences of different netting mechanisms in centrally cleared financial markets; see, e.g., Duffie and Zhu (2011); Duffie et al. (2015); Cont and Kokholm (2014); Armenti and Crépey (2017); Amini et al. (2020, 2016b); Glasserman et al. (2016); Capponi et al. (2015); Amini and Minca (2020).

We are primarily motivated in this study by two streams of literature: that of Acemoglu et al. (2015) which proposed the robust fragility of the completely connected network and those of D’Errico and Roukny (2021); Veraart (2022) which proposed frameworks for network compression without considering which levels of compression reduce systemic risk. In this paper we seek to unify these problems into a single optimization framework, which we call optimal network compression. We further merge these problems with the systemic risk measures of Chen et al. (2013); Kromer et al. (2016) so as to determine the compressed network that minimizes systemic risk; as shown in Veraart (2022), network compression need not improve systemic risk.

1.2 Primary Contributions and Organization

The primary innovations and results of this paper are in multiple directions. First, we introduce a general formulation of the optimal network compression problem for financial systems in the specific context of systemic risk measurement. This general formulation is presented for different levels of network compression or rerouting allowed from the initial interbank network. Furthermore, we prove that this optimal network compression problem is generically NP-hard. This motivates us to consider a machine learning approach to approximating the optimal financial network. In particular, we use a genetic algorithm and show that, in a simple example of three-bank system, the algorithm performs as well as the optimal network found using an interior point algorithm for the rerouting problem and non-conservative compression.

As a second contribution, we study the (sub)optimality of the maximally compressed network when considered through the lens of systemic risk measure objectives. The maximal compression problem, as studied in D’Errico and Roukny (2021), focuses on removing the maximal amount of liabilities in the system subject to certain financial constraints. Under the typical compression constraints, this problem is a linear programming problem and, thus, can be solved in polynomial time. We propose simple metrics to test the (sub)optimality of the maximally compressed network in general stochastic settings. We show that maximal and optimal compression coincide so long as the system is secure enough. Our numerical case studies illustrates that, under larger stresses, the maximal compression may rapidly become suboptimal.

Third, in order to find tractable analytical forms for the systemic risk measures, as in Banerjee and Feinstein (2022), we consider stress scenarios under systematic shocks. These analytical forms are novel extension of the formulas provided in Banerjee and Feinstein (2022) to the systemic risk measures of Chen et al. (2013); Kromer et al. (2016). Such systematic stress scenarios allow us numerically implement the optimal compression problem tractably. We implement this framework in two case studies. First, we extend the work of, e.g., Acemoglu et al. (2015) to consider the robustness of various network topologies for heterogeneous networks under systematic shocks. In particular, in numerical experiments, we show that under systematic shocks the robust fragility results of Acemoglu et al. (2015) no longer hold generally. Second, we consider a financial system calibrated to the 2011 European Banking Authority stress testing data to demonstrate numerical results for a large financial system.

The organization of this paper is as follows. In Section 2, we propose the general optimal network compression problem to be considered throughout this work. In so doing, we formulate four meaningful types of “compression” problems motivated by D’Errico and Roukny (2021); Acemoglu et al. (2015) and prove that the optimal compression problem is, generically, NP-hard given each of those constraint sets. We then focus on a meaningful form for the objective function, namely the systemic risk measures of Chen et al. (2013); Kromer et al. (2016), in Section 3. Specifically, in Appendix C, we present analytical forms for specific examples of these systemic risk measures under systematic shocks to the financial system. Within Section 4, we study the “maximal” compression algorithm (i.e., as proposed in D’Errico and Roukny (2021)) in order to study conditions on the optimality of this compressed network. This is followed by two case studies in Section 5. First, we consider a simple three bank system that serves the dual purposes of validating our algorithmic approach as well as testing the results of Acemoglu et al. (2015) in a heterogeneous system with systematic shocks. Second, we study a network calibrated to the 2011 European Banking Authority dataset; with this network we study the improvements in systemic risk via optimal compression and maximal compression on a large, realistic financial system. Section 6 concludes.

2 The optimization problem

Throughout this work we will consider a system of banks with obligations from bank to ; as is typical, we assume for every bank , i.e., no bank has any obligations to itself. Additionally, each bank will be assumed to have liabilities external to the banking network . These external obligations are sometimes called societal obligations; we will interchangeably use these terms throughout this work. The set of all such networks is denoted by .

In this section we present the primary optimization problem of interest in this work. To do so we introduce the notion of portfolio compression which we take from D’Errico and Roukny (2021). In this work we seek to find the optimal network compression problem, i.e., for an initial liability network , we wish to minimize some objective subject to compression constraints (which are formally presented in Definition 2.2 below).

| (1) |

The objective function can be directly computed from the network statistics (e.g., network entropy) or the results of systemic risk measures (see, e.g., Chen et al. (2013); Kromer et al. (2016)). Note that in general this function may also depend on the initial liability network , but we drop this from the notation for compactness. We will discuss the systemic risk measure based objective functions in the following sections. Notably, as these objective functions are in general nonconvex, this optimization problem might be hard; in fact, we will show that (generically) this problem is NP-hard given certain objectives and network compression based constraints in Theorem 2.4.

Remark 2.1.

Prior works on network compression, e.g., D’Errico and Roukny (2021), focus on removing the maximal amount of liabilities in the system subject to certain financial constraints. That is, with objective . In particular, with the compression constraints highlighted within this work, (1) becomes a linear programming problem and can be solved in polynomial time. Other, non-optimization based, algorithms for undertaking this compression are presented in D’Errico and Roukny (2021). In contrast, we are motivated, as in Veraart (2022), to study partial compression to determine the optimal level of compression; Veraart (2022) focuses on conservative compression (defined below) with a strict definition for optimality related to the set of defaulting banks.

The constraint set denotes the set of all possibly compressed or rerouted networks consistent with . Any such meaningful compression problem satisfies two properties: consistent net liabilities and feasibility as a network. This is encoded in the following definition consistent with prior works on network compression, e.g., D’Errico and Roukny (2021); Veraart (2022).

Definition 2.2.

Given an initial financial liability network , is a set of compressed networks if implies:

-

•

constant net liabilities: for every bank and

-

•

feasibility: .

Compare the definition of the set of compressed networks to the General Compression Problem defined in D’Errico and Roukny (2021). We wish to note that the set of compressed networks can often be defined as a convex polyhedron; in fact it is explicitly defined this way in D’Errico and Roukny (2021) and every specific example we consider in this work satisfy such a structure.

Example 2.3.

In this example we consider 3 types of network compression and, fourth, the rerouting problem, which we will consider throughout this work. These 3 network compression problems are detailed in D’Errico and Roukny (2021) with conservative compression studied further in Veraart (2022). We describe these compression problems in varying order from most to least restrictive; though each is financially meaningful, other types of compression can be implemented. To simplify notation, we will define for every bank for any network .

-

(i)

Bilateral compression: Given an initial network , bilateral compression allows for the reduction of bilateral exposures only. That is, the net obligations between banks and must always be kept consistent with the initial network construction; additionally, all obligations can only be reduced from their initial levels. As such, we can define bilateral compression as:

Bilateral compression is special insofar as the most the network can be compressed in this way is defined by obligations: . An example of bilateral compression is shown in Figure 1.

Figure 1: Example of bilateral compression with and . -

(ii)

Conservative compression: Given an initial network , conservative compression allows for the reduction of cyclical exposures only. That is, the net obligations owed around a directed cycle must always be kept consistent with the initial network construction; additionally, all obligations can only be reduced from their initial levels. As defined in D’Errico and Roukny (2021), this cyclical netting rule can be encoded by the fixed net liabilities condition for every bank . As such, we can define conservative compression as:

Conservative compression is shown in Figure 2 under and .

-

(iii)

Rerouting: Given an initial network , rerouting allows for the rewiring of the entire network. That is, all liabilities are redistributed throughout the system in such a way that net and gross liabilities are kept constant. As such, we can define rerouting as:

Rerouting is shown in Figure 2 under , and .

-

(iv)

Nonconservative compression: Given an initial network , nonconservative compression allows for, first, rerouting of the network and, second, the conservative compression of that network. That is, for every bank , net liabilities are kept constant while gross liabilities are allowed to be reduced from the initial setup. As such, we can define nonconservative compression as:

Sometimes one may also wish to fix the obligations owed to society; this is accomplished by taking the intersection where

We denote the nonconservative-0 compression as . Nonconservative compression is shown in Figure 2 under , and .

We conclude this section by showing that the optimal compression problem for the constraint sets of Example 2.3 are NP-hard in general. This result motivates us to consider specific settings and algorithms used later in this work.

Theorem 2.4.

The optimal network compression problem is NP-hard for the conservative, rerouting and nonconservative compression models.

The proof of this theorem is provided in Appendix A. By considering the network (relative liabilities) entropy () as our objective function we show that the optimal compression problem for each set of constraints is NP-hard. We prove this by performing reduction from instances of the NP-complete subset sum problem Karp (1972); defined by a set of positive integers and an integer target value , we wish to know whether there exist a subset of these integers that sums up to . We show that this can be viewed as a special case for the optimal network compression for each set of constraints.

Remark 2.5.

In contrast to using the maximum entropy to find the missing liabilities as in Mistrulli (2011), we can consider the minimum entropy as our objective function for compression, see e.g. Kovačević et al. (2012); Watanabe (1981). Indeed, the network maximizing the entropy will be close to the complete regular network. On the other hand, the network minimizing the entropy would correspond to a sparse network. So it makes sense to consider it as an objective function for compression; as this is shown in Watanabe (1981), many of the known algorithms in pattern recognition can be characterized as efforts to minimize the entropy. Consider for example the case of similar firms all having the same total assets and liabilities (and without obligations to society). Then it is easy to check that the network maximizing entropy will correspond to the complete regular network with which gives . On the other hand, the network minimizing the entropy would correspond to the (regular) ring which corresponds to .

Remark 2.6.

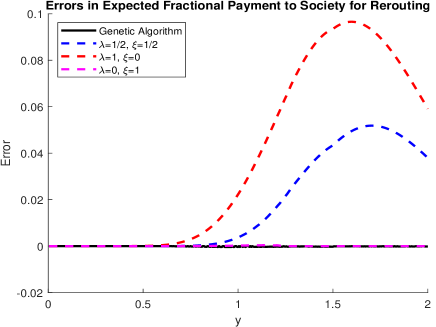

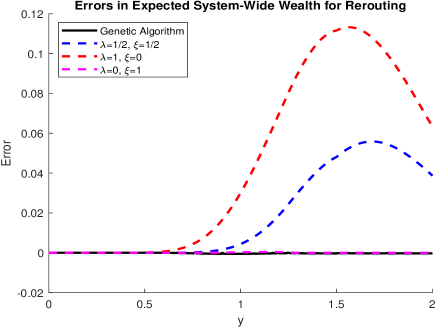

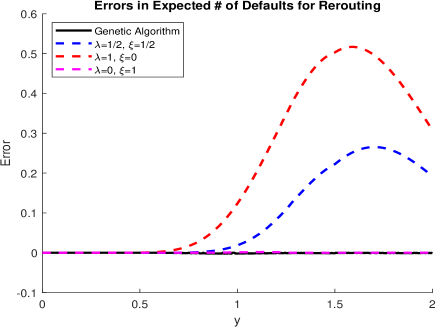

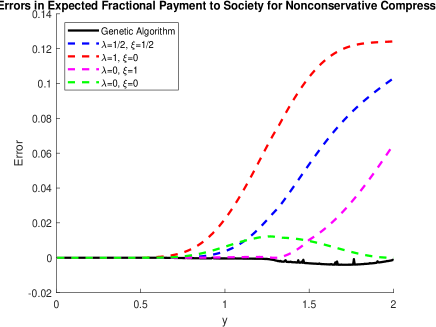

As the optimal compression problem (1) is generically nonconvex and NP-hard, we cannot rely on a gradient descent method to converge to the global optimum. As such we believe that machine learning tools and methods would be best for solving such problems in general. For this paper, as will be utilized and validated in Section 5, we will implement a genetic algorithm to solve the optimal compression problem; an overview of the genetic algorithm and its implementation is provided in Appendix B.222Briefly, all implementations of the genetic algorithm are completed using the “ga” function in the Global Optimization Toolbox of MATLAB. We direct the reader to Figures 6 and 7 for the validation of the genetic algorithm for the optimal compression and rerouting problems in a simple three bank setting.

3 Systemic risk objective

In this section we wish to give a specific structure to the objective function in our optimal compression problem (1). Specifically, we wish to consider the network compression that minimizes a systemic risk measure. These functions are decomposed as for a risk measure and an aggregation function . Such functions were first introduced in Chen et al. (2013); Kromer et al. (2016) and are detailed below; these mappings also coincide with the “insensitive systemic risk measures” of Feinstein et al. (2017); Ararat and Rudloff (2020). All results presented within this section are provided solely to provide background information on these systemic risk measures; we believe these mappings provide an important class of objective functions for the optimal compression problem. These systemic risk measures are utilized within Sections 4 and 5 below. In order to present this setting, and for the remainder of this paper, we fix some probability space . Let denote those random variables that are square-integrable.

In order to determine the health of a financial network, we first present a generic aggregation function in the following definition. These aggregation functions are mappings of two arguments: the endowment for the banks and the liability network. The purpose of such a function is to provide an aggregate statistic of the state of the financial system.

Definition 3.1.

The mapping is a aggregation function if it is a nondecreasing mapping in its first argument.

Example 3.2.

Throughout this work we specifically consider four different aggregation functions that are all fundamentally associated with the clearing mechanisms of Eisenberg and Noe (2001); Rogers and Veraart (2013) to incorporate initial margins and collateral similar to that presented in, e.g., Ghamami et al. (2022); Veraart (2022). That is, for endowments , margin , and recovery rates , the clearing payments are the maximal fixed point for

As such, the clearing procedure implies: if bank has nonnegative wealth , then it is solvent and its wealth is equal to its total assets minus its total liabilities; if bank has negative wealth then it is defaulting and its assets are reduced by the recovery rates while the collateral is used to cover of the liabilities. Due to the use of the collateral, a bank may be able to pay its obligations in full even while defaulting. We wish to note that we recover the clearing mechanisms of Eisenberg and Noe (2001); Rogers and Veraart (2013) with this structure when the margin is removed, i.e., .

Proposition 3.3.

Fix the margin and recovery rates . There exists a greatest and least clearing solution to within the lattice for any endowments and liability network .

Proof.

As is nondecreasing, the result follows trivially from Tarski’s fixed point theorem. ∎

With this clearing procedure, we consider the following four aggregation functions:

-

•

Number of banks paying in full: .

-

•

Number of solvent banks: .

-

•

System-wide wealth : .

-

•

External wealth: .

Additionally, we need to consider a risk measure in order to determine the risk that the system is incurring. Such functions map random variables into capital requirements.

Definition 3.4.

The mapping is a risk measure if it satisfies the following properties:

-

•

normalization: ;

-

•

monotonicity: if a.s.; and

-

•

translative: for .

These risk measures may satisfy additional conditions, e.g., convexity or positive homogeneity.

Example 3.5.

For the purposes of this work, we will focus on two standard risk measures parameterized by :

-

•

Value-at-Risk: . If then we recover the so-called worst-case risk measure: .

-

•

Expected shortfall: . If then we recover the so-called expectation risk measure: .

To measure the health of the financial system, we consider the systemic risk measures for risk measure and aggregation function as presented in, e.g., Chen et al. (2013).

Definition 3.6.

The mapping is a systemic risk measure if it can be decomposed into an aggregation function and a risk measure so that for every and .

Within the optimal compression problem (1), we specifically are interested in

for some (random) endowments . That is, given a stress scenario , we seek to find the optimal financial network (subject to compression constraints) such that the systemic risk is minimized. In Appendix C, a semi-analytic form for these systemic risk measures along the lines as Banerjee and Feinstein (2022) is provided under systematic stress scenarios.

Remark 3.7.

We wish to highlight two special cases which relate to the notions proposed in Acemoglu et al. (2015) in the uncollateralized setting. (In this uncollateralized setting, the number of solvent firms coincides exactly with the number of banks paying in full, i.e., .) Fix such that a.s. for every bank . In the context of the above general setting, we define the stress scenarios by the random field for any .

-

(i)

Consider the worst-case risk measure . In the notation from Acemoglu et al. (2015), is more resilient than if and only if

-

(ii)

Consider the expectation risk measure . In the notation from Acemoglu et al. (2015), is more stable than if and only if

Acemoglu et al. (2015) presents these notions for symmetric systems of banks with i.i.d. Bernoulli shocks . Notably, under such conditions, the number of solvent banks provides the full information on the health of the system; that is, any aggregation function that depends on only through the clearing payments , say , provides the same ordering of liability networks as :

We will revisit these problems, and compare our formulation with that with Acemoglu et al. (2015) further, in Section 5.1 below.

4 Optimality of maximal compression

Recall the maximal compression problem as defined in D’Errico and Roukny (2021) and detailed in Remark 2.1, i.e., the optimal network compression with . Herein we will focus entirely on compression without consideration for the rerouting problem. Within this section, our goal is to study the (sub)optimality of the maximally compressed network when studied through the lens of systemic risk measure objectives (i.e., ). Throughout this section, we will denote the maximally compressed network by for generic convex compression constraints . As stated in Remark 2.1, can be computed as the solution to a linear program under any of our proposed compression problems provided within Example 2.3.

Remark 4.1.

Consider the systemic risk objective presented above. If the only concern is the relative risk of the original network to the maximally compressed network, this can be compared directly by studying and . Specifically, if then maximal compression is worse than no compression and, as a direct consequence, must also be suboptimal for the optimal network compression problem (1).

Proposition 4.2.

Consider a financial network with maximally compressed version under compression constraints . Additionally, consider the optimal network compression problem over systemic risk measure subject to the stress scenario . Assume is differentiable. Denote the directional derivative of at in the direction of the initial liabilities by

If then is suboptimal, i.e., there exists some such that . If is the optimally compressed network then .

Proof.

If then there exists some such that , i.e., is suboptimal by construction. In contrast, if is the optimally compressed network then, by definition of optimality, the directional derivative of at is nonnegative in every direction; in particular, . ∎

In Remark 4.1 and Proposition 4.2, we propose simple metrics to test the (sub)optimality of the maximally compressed network in general stochastic settings. We wish to conclude this discussion of the optimality of the maximally compressed network under a specific systematic structure for the stress scenario. (As noted above, a semi-analytic form for the Value-at-Risk and expected shortfall under the aggregation functions of Example 3.2 are provided within Appendix C.) In contrast to, e.g., Banerjee and Feinstein (2022), this result permits a comparison of network structures in the vein of Acemoglu et al. (2015). As far as the authors are aware, such a result is completely novel in the literature.

Proposition 4.3.

Consider a financial network with maximally compressed version under compression constraints . Additionally, consider the optimal network compression problem over systemic risk measure with decomposition such that is a law-invariant risk measure and is an aggregation function. Assume is based on the margined clearing mechanism of Eisenberg and Noe (2001); Rogers and Veraart (2013) as provided within Example 3.2 with such that and if a larger fraction of obligations are paid under than , i.e., if for every bank . Finally, assume a parameterized stress scenario for such that (w.r.t. first order stochastic dominance) if and (w.r.t. first order stochastic dominance). Then there exists some such that for every (w.r.t. first order stochastic dominance).

Proof.

First, we wish to note that if a.s. then as well; this holds because either (i.e., no bank is defaulting under the maximally compressed network ) or (i.e., if a bank is defaulting then it must still pay all obligations in full due to the margin requirements). Take

then for any it must hold that by monotonicity of the aggregation function . ∎

Proposition 4.3 means that maximal and optimal compression coincide so long as the system is secure enough. Heuristically, under larger stresses, the maximal compression may rapidly become suboptimal as will be observed in the numerical case studies in Section 5 below.

Remark 4.4.

Though Proposition 4.3 introduces a number of conditions, these are naturally satisfied in many cases. Notably, every aggregation function introduced within Example 3.2 satisfies the monotonicity with respect to the fraction of obligations being repayed. Further, the parametric form for the stress scenarios with is taken to impose a systematic shock on the assets of the banks. This special structure is utilized throughout the case studies constructed within Section 5 below. Assuming , the monotonicity of the stress scenarios in the liabilities matrices is because, in the case studies, the margin is returned as liabilities are returned (and the shocks are limited to nonnegative random variables).

5 Case studies

In this section we will consider two case studies to demonstrate the results of this work. As mentioned in Remark 2.6, we implement a genetic algorithm to optimize (1); an overview of the genetic algorithm is provided in Appendix B.

First, we will present a small, 3 bank, financial system with heterogeneous (comonotonic) endowments. This system allows us to easily present analytical results to validate the genetic algorithm we utilize to consider optimal compression and rerouting. Additionally, this small system allows us to investigate the robust fragility results of Acemoglu et al. (2015) in a different setting to determine if those results hold for more general settings than presented in that work. In particular, we show that under systematic shocks, even for a simple heterogeneous three bank system, the robust fragility results of Acemoglu et al. (2015) no longer hold generally.

Second, we calibrate a financial system to the 2011 European Banking Authority stress testing data. With that system we compare the original network, the fully compressed networks, and optimally compressed networks. This framework allows us to numerically generalize Veraart (2022) to quantify the suboptimality of the full compression as utilized in D’Errico and Roukny (2021) on a large financial network calibrated to data in a specific example. Namely, we show that if the systemic risk measures are not explicitly part of the objective function of the optimal compression problem, we may end up with suboptimal outcomes or, even worse, increased systemic risk. We also find that the optimal network compression can find significant systemic risk improvements over the original network.

Broadly, these numerical examples demonstrate: (i) the optimal compression problem is computationally feasible; (ii) robust fragility with i.i.d. Bernoulli shocks as reported in Acemoglu et al. (2015) does not hold for heterogeneous systems; and (iii) maximal compression can be suboptimal in large “realistic” financial networks. As such, these case studies should be viewed through that lens, i.e. as numerical counterexamples to the widely reported robust fragility (Section 5.1) and the optimality of maximal compression in large, complex financial systems (Section 5.2). With these goals in mind, we want to emphasize that all networks considered herein are fully “nettable” in the sense that maximal conservative compression can net out the entire interbank network. Such a simple network structure was taken for demonstration purposes of the three noted goals only. Further studies with different network calibrations could be of interest for future works.

5.1 Three bank system

In Acemoglu et al. (2015) comparison of completely connected to ring structured networks was undertaken in an uncollateralized setting with fixed (random) stress scenarios. In that work, these networks were “symmetric” in that all banks were identical in assets and liabilities, but with i.i.d. Bernoulli shocks. That work focuses on stability and resilience, i.e., w.r.t. and , respectively, as provided in Remark 3.7. Notably, Acemoglu et al. (2015) determines, under i.i.d. Bernoulli shocks, that the dense network is more stable if shocks are small, but the sparse network is more stable if the shocks are large. We will explore this question further with a consideration of a 3 bank system under systematic shocks that allows for: a completely connected network and two ring networks. The general network structure is depicted in Figure 3. For the sake of notational simplicity, we will consistently refer to bank as the bank with endowment equal to . Without loss of generality we assume . We additionally assume that either , , or ; if then, due to the comonotonic endowments inherent for a systematic shock, all rerouted networks have identical systemic risk. We wish to note that both the net and gross liabilities of each bank are the same in all network setups. For direct comparison with Acemoglu et al. (2015), within this section we will focus entirely on the uncollateralized setting (i.e., ) with for any network . Notably, as mentioned in Remark 3.7, in this uncollateralized setting the number of solvent firms coincides exactly with the number of banks paying in full, i.e., ; because of this, we will not consider explicitly herein.

To approach the problem of studying optimal compression and rerouting for our 3 bank system, we first want to study the minimal solvency prices for our three banks. In order to study these problems we impose the following netting conditions on the obligations:

Given the network provided in Figure 3 with the aforementioned netting conditions, these values can be computed explicitly as:

where , , and

These values allow us to explicitly compute the statistics on the network as discussed in Appendix C.

To make these defaulting price levels more explicit, we wish to consider 4 simplified networks with and for all banks. These networks and resultant are:

-

(i)

Completely connected [CC]: Let for all with . First we note that, by construction, it must be that in this setup for any choice of bankruptcy costs and obligations to society. For notation to allow for easier comparisons later on, we will denote these thresholds as .

-

(ii)

Ring 123 [123]: Let and with . First we note that, by construction, it must be that in this setup for any choice of bankruptcy costs and obligations to society. For notation to allow for easier comparisons later on, we will denote these thresholds as .

-

(iii)

Ring 132 [132]: Let and with . For notation to allow for easier comparisons later on, we will denote these thresholds as .

-

(iv)

Compressed [0]: Let for all with . For notation to allow for easier comparison later on, we will denote these thresholds as .

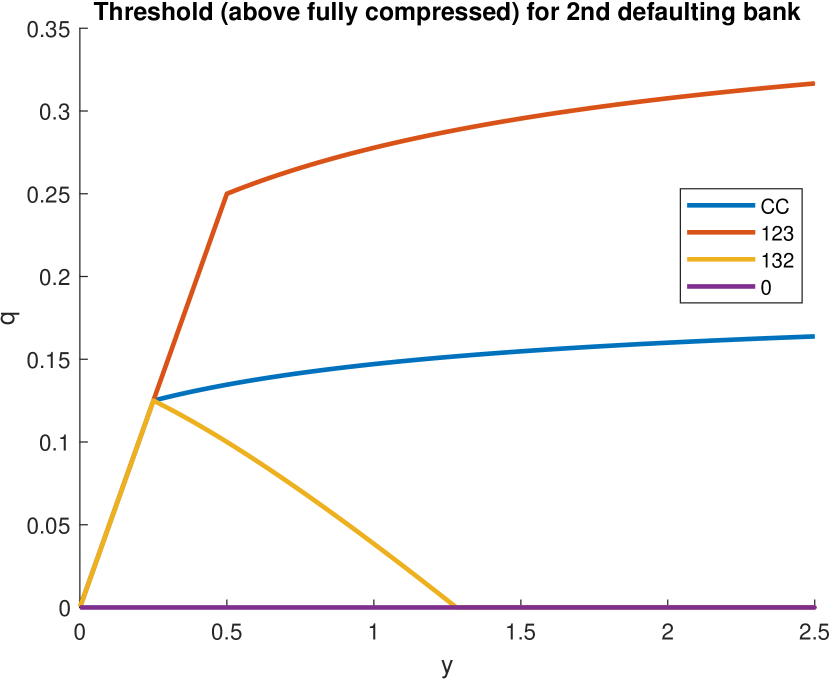

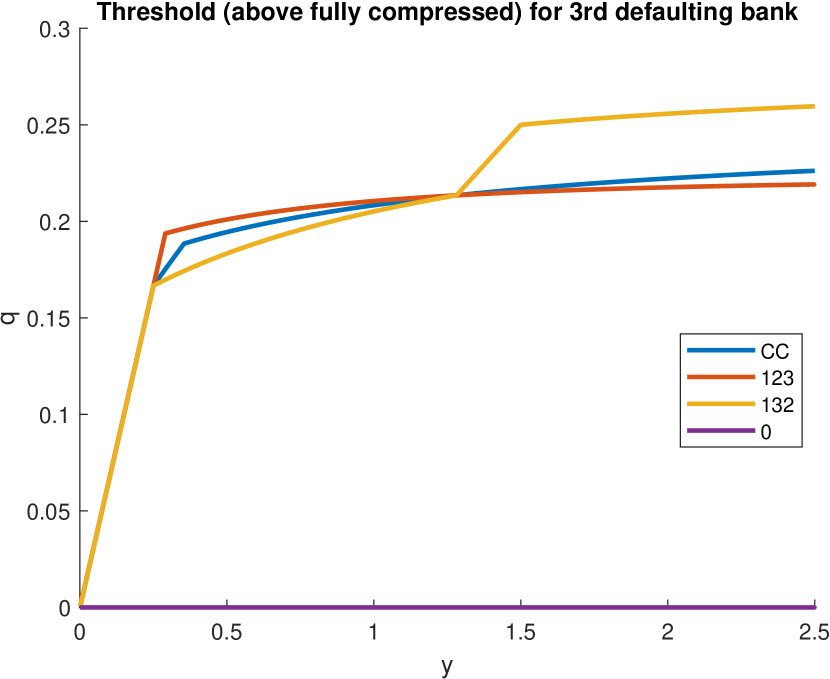

As for any network construction in this setup, we will compare these 4 networks for the defaulting thresholds for banks 2 and 3 only. In order to ease the notation for the remainder of this case study we will focus solely on the setting in which all three banks have gross obligations and for which and . Figure 4 displays the default thresholds, in excess of the fully compressed system, for the 2nd and 3rd bank ( and respectively) with . First, and notably, the default thresholds are lowest in the fully compressed system. This is further shown in Figure 7(c) in which the optimally compressed network with is the fully compressed one. However, for comparison to Acemoglu et al. (2015), we also want to investigate the rerouting problem. By investigating we can compare the stability and resilience of financial networks to systematic Bernoulli shocks. As displayed in Figure 4, and as can be verified analytically (for any ), for any . That is for “small” shocks the completely connected system is always more stable and resilient than Ring 123. For “large” shocks with small enough obligations to society , we find that ; for larger obligations to society the opposite ordering is found. That is, for “large” shocks the total obligations to society can alter the stability and resilience ordering between these two networks. This, generally, coincides with the robust fragility notion from Acemoglu et al. (2015) in which the completely connected system was more robust to small shocks but more fragile to large shocks. In contrast, the opposite relations hold between the completely connected network and Ring 132; that is, we find that the ring is more stable and resilient for “small” shocks () but the ordering for “large” shocks depends on the obligations to society (for small enough then , for large enough then ). As systematic shocks and heterogeneous financial networks are vital to the consideration of financial stability, optimal compression and rerouting take on new significance since, in this case, the robust fragility results of Acemoglu et al. (2015) no longer hold generally.

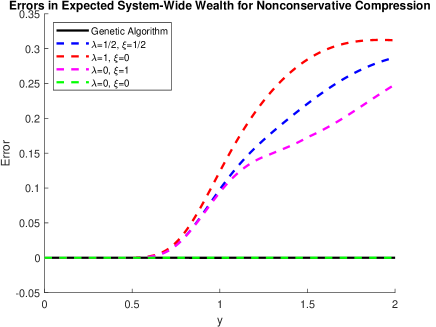

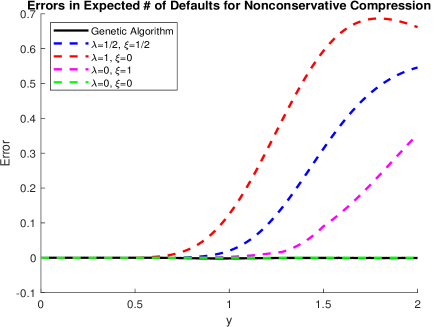

We now wish to validate the performance of our genetic algorithm for finding the optimal networks. That is, we wish to demonstrate that the genetic algorithm provides network compressions that equal, or even outperform, those found by other more standard optimization techniques. We will accomplish this by studying the expectation risk measure (as this was one of the risk measures utilized within Acemoglu et al. (2015)) with all of our sample aggregation functions (recalling that in this uncollateralized setting). The validation is accomplished by comparing the results of the genetic algorithm with those using an interior point algorithm (initialized at for all ).333The interior point algorithm was implemented with “fmincon” in MATLAB using the default options. We also wish to compare these optimal networks with the 4 sample networks (completely connected, 2 rings, and the fully compressed system) to investigate the optimality of these heuristic constructions. In Figure 6, we consider the optimal rerouting problem under change of obligations to society ; in Figure 7, we consider the optimal nonconservative compression (with fixed obligations to society) problem under change of obligations to society . First, and foremost, our genetic algorithm accurately matches or even outperforms the optimal network using an interior point algorithm (as seen in optimal nonconservative compression with ). Further, though the heuristic networks coincide with these optimal risk levels in specific cases, they do not uniformly perform as well as the optimal networks. Most interesting is the consideration of in which the optimally compressed network nearly coincides with the optimal rerouting problem for low .

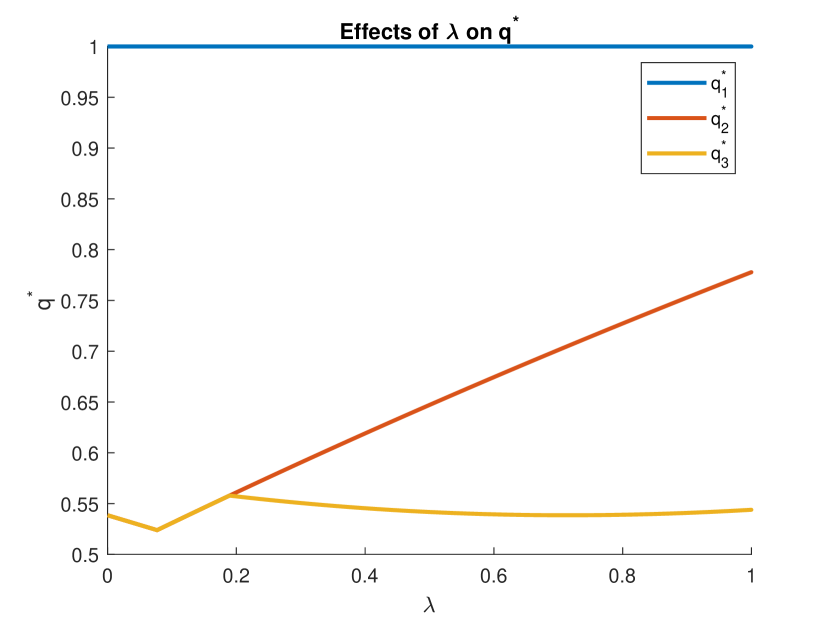

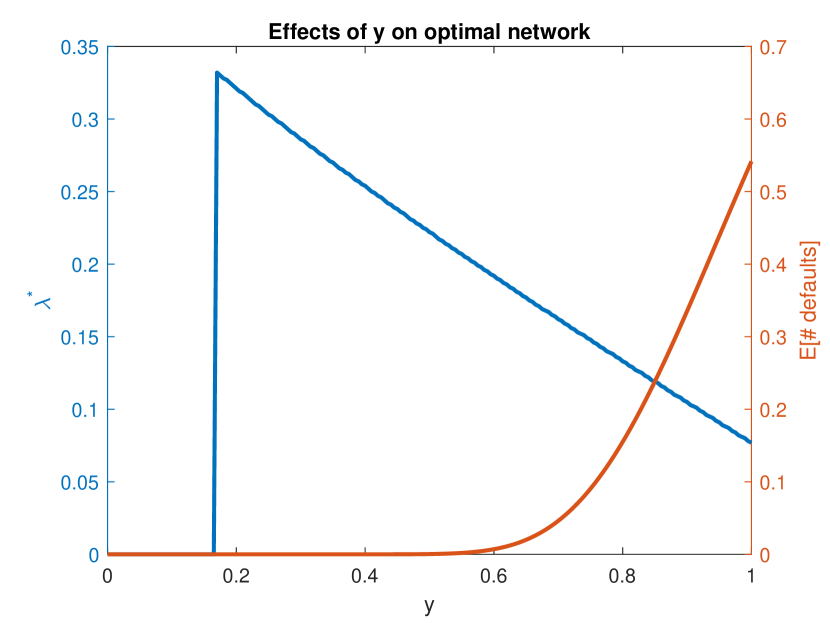

Consider now the optimal compression and rerouting problems for this three bank system. As above, throughout this example, we will fix for simplicity of comparison. First, we will consider the optimal rerouting problem to generalize the notions from Acemoglu et al. (2015). In order to ease the notation for the rerouting problem (with gross obligations of for each of the three banks) let . First, for the most direct comparison, in Figure 5(a) we consider how modifying affects the defaulting thresholds (with ). By inspection the most stable and resilient system is clearly for some small, but strictly positive, . These optimally stable networks are described in Figure 5(b); such a system is considered in which with . Notably, the optimal network depends on the obligations to society .

Remark 5.1.

As presented previously in Remark C.2, we can consider optimal network compression under general stress scenarios via Monte Carlo simulation. Intriguingly, and not displayed herein, the optimal network construction and expected risk is generally insensitive to the copula of the stress scenario; this was analyzed numerically over the Gaussian copula with non-negative correlations.

5.2 European banking system

In this section we demonstrate how our comonotonic approach with genetic algorithm for optimization can be applied in a larger financial network consisting of banks to come from the 2011 European Banking Authority EU-wide stress tests.444Due to complications with the calibration methodology, we only consider 87 of the 90 institutions. DE029, LU45, and SI058 were not included in this analysis. There are several previous empirical studies based on this dataset (see, e.g., Chen et al. (2016); Gandy and Veraart (2016)) and we calibrate this system by taking the same approach as Feinstein (2019). We wish to use this case study for two primary purposes. First, we use it to demonstrate that our methodology can be applied to large, and realistic, financial systems. Second, using this calibrated system, we can quantify the suboptimality of the full compression as considered in, e.g., Veraart (2022). Namely, we show that if the systemic risk measures are not explicitly part of the objective function of the optimal compression problem, we end up with suboptimal outcomes or, even worse, an increase in systemic risk. In contrast, we also find that the optimal network compression can find significant systemic risk improvements over the original network.

For the purposes of calibration, we consider a stylized balance sheet for each bank with only three types of assets and liabilities. The total interbank assets for bank is while the total interbank liabilities is . The external risk-free assets for bank is denoted by and the external risky assets are denoted by . On the other hand, the external liabilities for bank is and the bank is endowed with capital .

Note that the EBA dataset only provides the total assets , capital , and interbank liabilities for each bank . Therefore, we will make the following simplifying assumptions similar to Feinstein (2019); Chen et al. (2016); Glasserman and Young (2015). We assume that the external (risky) assets are the difference between the total assets and interbank assets. The external obligations owed to the societal node (denoted by ) will be assumed equal to the total liabilities less the interbank liabilities and capital. Further, we assume that the interbank assets are equal to the interbank liabilities for all banks, i.e., for all . Under these assumptions, the remainder of our stylized balance sheet (with collateralization ) can be constructed by setting

and,

which will guarantees that firm ’s net worth is equal to its capital, i.e., . Within this study we consider ; we limit in this way so as to guarantee that the assets are positive for every bank .555The maximum possible collateralization scheme guaranteeing nonnegative assets is .

We will also need to consider the full nominal liabilities matrix and not just the total interbank assets and liabilities. To achieve this, we will use the MCMC methodology of Gandy and Veraart (2016) which allows for randomized sparse structures to construct the full nominal liabilities matrix consistent with the total interbank assets and liabilities. Under the Gandy and Veraart (2016) methodology and the assumption used widely in the literature (see, e.g., Chen et al. (2016); Glasserman and Young (2015)), conservative compression (and therefore also, e.g., nonconservative compression) of the constructed network will result in all interbank obligations being netted out and a zero network remaining due to our initialization of the network. As this example is only for illustrative purposes, we will consider only a single calibration of the interbank network.

The remaining parameters of the system are calibrated as follows. We specify the systematic factor as a lognormal distribution with parameters described in millions of euros. Since during the period over which this data was collected, central banks were setting a low interest rate environment, we estimate that the risk-free interest rate is . Finally, from comparisons to annualized historical volatility of European markets in 2011, the volatility of the risky asset is estimated to be .

For the purposes of this example, we consider clearing based on the pure collateralized Eisenberg-Noe mechanism, i.e., with full recovery in case of default (). We will consider two systemic risk measures to optimize over: the 80% expected shortfall of the payments to society () and the number of banks paying in full () with stress scenarios so that any freed up collateral is invested comparably to the original portfolio. We consider expected shortfall herein as it is a coherent risk measure that is widely utilized in practice. We select these two aggregation functions so as to demonstrate that the conclusions we report below in Tables 1 and 2 on network compression are not specific to one particular aggregation function but appear more general.

Herein we compare two types of compression: “maximally compressed” corresponds to a compressed network that removes as much excess liabilities from the network as possible (as is considered in D’Errico and Roukny (2021) and Section 4) whereas “optimally compressed” attempts to minimize the appropriate systemic risk measure. These two types of compression are then compared over 4 possible compression scenarios: bilateral compression (), conservative compression (), nonconservative compression with fixed obligations to society (), and nonconservative compression (). In particular, we wish to compare the systemic risk exhibited by the original network to those found in either the maximally compressed or optimally compressed scenarios. These results are provided in Tables 1 and 2. We wish to remind the reader that the maximally compressed network under conservative, nonconservative-0, and nonconservative compression all result in all interbank obligations being netted out and zero network remaining. Thus, as seen in Tables 1 and 2, the gains and losses observed for maximal compression under these three compression algorithms are identical.

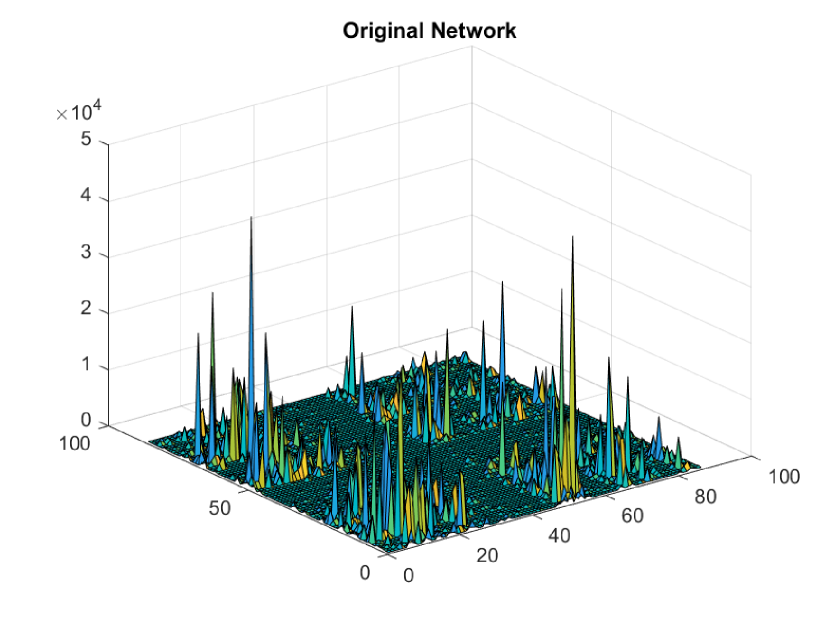

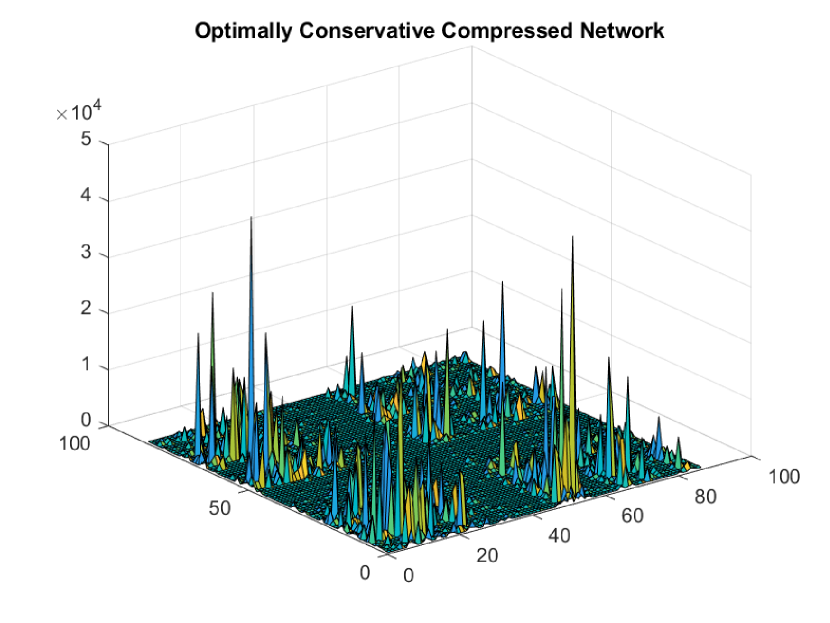

As shown in Table 1, under maximal compression, the more relaxed the constraints the worse the expected outcome for society in the 20% tail event; however, by using optimal compression, the systemic risk can be improved significantly under compression. This is true for all three sampled collateralization levels. Notably, the optimal bilateral and conservative compression only find marginal improvements in the payments to society, whereas the maximally compressed versions increase systemic risk by billions of euros, in all three collateralization settings. The nonconservative compressions find substantial benefits, but massive losses when maximally applied without consideration for systemic effects; in the uncollateralized setting, the optimal compression saves over €1.6 and €5.3 billion, but adds nearly €6.75 billion euros of cost when maximally applied. These uncollateralized networks are visualized in Figure 8; we wish to highlight that optimal bilateral and conservative compression appear quite similar and thus only conservative compression is displayed. We do not display the maximally compressed networks as, due to the assumptions for the network calibration, the interbank network is zeroed out for conservative, nonconservative-0, and the nonconservative compression. Finally, we wish to note that though the benefits of compression appear to drop as collateralization increases; this is more than offset by the improvement in systemic risk from the collateralization itself.

| Bilateral | Conservative | Nonconservative-0 | Nonconservative | ||

| Maximally Compressed: | 2717.449 | 6749.574 | 6749.574 | 6749.574 | |

| Optimally Compressed: | -0.033 | -0.033 | -1639.660 | -5339.976 | |

| Maximally Compressed: | 8176.074 | 20408.285 | 20408.285 | 20408.285 | |

| Optimally Compressed: | -0.208 | -0.208 | -1031.956 | -5062.909 | |

| Maximally Compressed: | 6421.291 | 16659.836 | 16659.836 | 16659.836 | |

| Optimally Compressed: | -0.026 | -0.026 | -304.968 | -4392.229 | |

In contrast in the uncollateralized setting , as shown in Table 2, the optimal and maximal compression algorithms provide identical systemic risk when attempting to minimize the expected number of defaults in the 20% tail events. In this scenario conservative compression outperforms bilateral compression and provides all the benefits of nonconservative compression; in such a setting we therefore find conservative compression the best as it allows all banks to remain with their original intended counterparties. However, once we include collateralization of obligations, the maximal compression schemes increase the number of defaults whereas optimal compression still reduces the number of defaults in the nonconservative compression scenarios (the improvement in the bilateral and conservative compression settings are marginal in the number of defaults). Finally, though the benefit of optimal compression appears to shrink (and the harm caused by maximal compression appears to grow) as collateralization increases, this is more than counteracted by the overall drop in the expected number of defaults as collateralization increases.

| Bilateral | Conservative | Nonconservative-0 | Nonconservative | ||

| Maximally Compressed: | -0.599 | -2.196 | -2.196 | -2.196 | |

| Optimally Compressed: | -0.599 | -2.196 | -2.196 | -2.196 | |

| Maximally Compressed: | 0.509 | 1.461 | 1.461 | 1.461 | |

| Optimally Compressed: | -0.000 | -0.000 | -0.386 | -0.732 | |

| Maximally Compressed: | 0.703 | 2.872 | 2.872 | 2.872 | |

| Optimally Compressed: | -0.000 | -0.000 | -0.119 | -0.169 | |

Remark 5.2.

Though we explicitly computed the systemic risk exhibited under maximal compression to demonstrate its (sub)optimality, we could equally have applied Proposition 4.2 for this purpose. Notably, the results of Proposition 4.2 could also be used to verify the (sub)optimality of the maximally compressed network . In fact, the directional derivatives of and at in the direction of the initial liabilities are negative in each case that we find maximal compression is suboptimal and positive when maximal compression is optimal (i.e., under number of banks with unpaid obligations).

We conclude this discussion by explicitly considering two features of network compression that can harm systemic risk in this case study. First, network compression functions like a system with both a senior and junior tranche of debt. The senior tranche (i.e., obligations that are compressed away) are paid in full leaving all non-payments to occur solely within the junior tranche (i.e., the compressed network). As we follow the Eisenberg-Noe clearing mechanism with pro-rata repayment, this seniority structure alters the relative liabilities and can spread losses differently in the system; in particular, if the entire interbank network is compressed away then all losses are absorbed by society by construction. We wish to note that the size of these losses need not be equivalent to those found prior to compression. Second, within this case study, we assume that all collateral is held in cash (i.e., not subject to the systematic shock), but held as a risky asset (and thus subject to the systematic shock) when returned to the obligor when a liability is compressed away. Therefore, as we are focused on the tail of the distribution – through the use of the expected shortfall risk measure – the collateral is, in some sense, worth more as collateral than as a risky asset. This change in the treatment of the collateral assets reduces the total amount of assets available in the system for repayments of obligations. As such, compression can result in additional losses or defaults. Both of these effects are seen within the losses reported from maximal compression in Tables 1 and 2.

6 Conclusion

In this work we presented a general formulation for the optimal network compression problem and found it to be NP-hard. We then focused on an objective function taking the form of systemic risk measures. In particular, we consider systematic shocks in order to find tractable analytical forms for these systemic risk measures. Such scenarios allow us to generalize the work of, e.g., Acemoglu et al. (2015) to consider the robustness of various network topologies. In particular, we found that for heterogeneous networks under systematic shocks, even for a simple heterogeneous three bank system, the robust fragility results of Acemoglu et al. (2015) no longer hold generally. We use a genetic algorithm and show that, in a simple example of three-bank system, the algorithm performs as well as the optimal network found using an interior point algorithm for the rerouting problem and non-conservative compression. Our numerical studies on the European banking system show that if the systemic risk measures are not explicitly part of the objective function of the optimal compression problem, we may end up with suboptimal outcomes or, even worse, an increase in systemic risk. Our illustrative example on this system shows that the optimal network compression can find significant systemic risk improvements over the original network. Further studies to systematically investigate the sensitivity of these results to the networks under study would be of general interest. This includes generalizing the robust fragility results of Acemoglu et al. (2015) beyond the symmetric i.i.d. assumptions used in that work.

We wish to highlight a few notable directions to extend the network compression problem. First, more complex compression rules should be studied; specifically, we may wish to impose different constraints so that compression can only occur over some given subsets of nodes in the initial network, such as compressing liabilities by country. It would be critical to understand the relation between systemic risk reduction and the choice of this subset of the initial financial network that are permitted to compress. Another area of interest would be to determine how the presence of multiple CCPs could affect the optimal network compression outcome. Further research may determine the sensitivity of the outcome to the CCPs capitalizations. Moreover, designing blockchains and smart contract technology that could integrate network compression remains an open problem. Furthermore, as suggested by an anonymous referee, the optimal compression problem can be utilized in a two-stage optimization setting in order to select between different solutions of the maximal compression problem (as, e.g., non-conservative compression generally leads to multiple solutions). We leave these and some other related issues on the effects of network compression on capital requirements and Basel III regulatory constraints for future research.

References

- Acemoglu et al. (2015) Acemoglu, D., Ozdaglar, A., and Tahbaz-Salehi, A. (2015). Systemic risk and stability in financial networks. American Economic Review, 105(2):564–608.

- Amini et al. (2016a) Amini, H., Cont, R., and Minca, A. (2016a). Resilience to contagion in financial networks. Mathematical Finance, 26(2):329–365.

- Amini et al. (2016b) Amini, H., Filipović, D., and Minca, A. (2016b). To fully net or not to net: Adverse effects of partial multilateral netting. Operations Research, 64(5):1135–1142.

- Amini et al. (2016c) Amini, H., Filipović, D., and Minca, A. (2016c). Uniqueness of equilibrium in a payment system with liquidation costs. Operations Research Letters, 44(1):1–5.

- Amini et al. (2020) Amini, H., Filipovic, D., and Minca, A. (2020). Systemic risk in networks with a central node. SIAM Journal on Financial Mathematics, 11(1):60–98.

- Amini and Minca (2020) Amini, H. and Minca, A. (2020). Clearing financial networks: Impact on equilibrium asset prices and seniority of claims. Available at SSRN 3632454.

- Anand et al. (2015) Anand, K., Craig, B., and Von Peter, G. (2015). Filling in the blanks: Network structure and interbank contagion. Quantitative Finance, 15(4):625–636.

- Ararat and Rudloff (2020) Ararat, c. and Rudloff, B. (2020). Dual representations for systemic risk measures. Mathematics and Financial Economics, 14(1):139–174.

- Armenti and Crépey (2017) Armenti, Y. and Crépey, S. (2017). Central clearing valuation adjustment. SIAM Journal on Financial Mathematics, 8(1):274–313.

- Banerjee and Feinstein (2022) Banerjee, T. and Feinstein, Z. (2022). Pricing of debt and equity in a financial network with comonotonic endowments. Operations Research. DOI: 10.1287/opre.2022.2275.

- Bardoscia et al. (2015) Bardoscia, M., Battiston, S., Caccioli, F., and Caldarelli, G. (2015). DebtRank: A microscopic foundation for shock propagation. PLOS ONE, 10(6):1–13.

- Battiston et al. (2012) Battiston, S., Puliga, M., Kaushik, R., Tasca, P., and Caldarelli, G. (2012). DebtRank: Too central to fail? Financial networks, the FED and systemic risk. Scientific reports, 2:541.

- Capponi et al. (2016) Capponi, A., Chen, P.-C., and Yao, D. D. (2016). Liability concentration and systemic losses in financial networks. Operations Research, 64(5):1121–1134.

- Capponi et al. (2015) Capponi, A., Cheng, W. A., and Rajan, S. (2015). Systemic risk: The dynamics under central clearing. Office of Financial Research, Working Paper, (15-08).

- Chen et al. (2013) Chen, C., Iyengar, G., and Moallemi, C. C. (2013). An axiomatic approach to systemic risk. Management Science, 59(6):1373–1388.

- Chen et al. (2016) Chen, N., Liu, X., and Yao, D. D. (2016). An optimization view of financial systemic risk modeling: The network effect and the market liquidity effect. Operations Research, 64(5):1089–1108.

- Cifuentes et al. (2005) Cifuentes, R., Shin, H. S., and Ferrucci, G. (2005). Liquidity risk and contagion. Journal of the European Economic Association, 3(2-3):556–566.

- Cont and Kokholm (2014) Cont, R. and Kokholm, T. (2014). Central clearing of otc derivatives: bilateral vs multilateral netting. Statistics & Risk Modeling, 31(1):3–22.

- D’Errico and Roukny (2021) D’Errico, M. and Roukny, T. (2021). Compressing over-the-counter markets. Operations Research, 69(6):1660–1679.

- Diem et al. (2020) Diem, C., Pichler, A., and Thurner, S. (2020). What is the minimal systemic risk in financial exposure networks? Journal of Economic Dynamics and Control, page 103900.

- Duffie et al. (2015) Duffie, D., Scheicher, M., and Vuillemey, G. (2015). Central clearing and collateral demand. Journal of Financial Economics, 116(2):237–256.

- Duffie and Zhu (2011) Duffie, D. and Zhu, H. (2011). Does a central clearing counterparty reduce counterparty risk? Review of Asset Pricing Studies, 1:74–95.

- Eisenberg and Noe (2001) Eisenberg, L. and Noe, T. H. (2001). Systemic risk in financial systems. Management Science, 47(2):236–249.

- Elliott et al. (2014) Elliott, M., Golub, B., and Jackson, M. O. (2014). Financial networks and contagion. American Economic Review, 104(10):3115–3153.

- Feinstein (2017) Feinstein, Z. (2017). Financial contagion and asset liquidation strategies. Operations Research Letters, 45(2):109–114.

- Feinstein (2019) Feinstein, Z. (2019). Obligations with physical delivery in a multi-layered financial network. SIAM Journal on Financial Mathematics, 10(4):877–906.

- Feinstein et al. (2018) Feinstein, Z., Pang, W., Rudloff, B., Schaanning, E., Sturm, S., and Wildman, M. (2018). Sensitivity of the Eisenberg and Noe clearing vector to individual interbank liabilities. SIAM Journal on Financial Mathematics, 9(4):1286–1325.

- Feinstein et al. (2017) Feinstein, Z., Rudloff, B., and Weber, S. (2017). Measures of systemic risk. SIAM Journal on Financial Mathematics, 8(1):672–708.

- Gai and Kapadia (2010) Gai, P. and Kapadia, S. (2010). Contagion in financial networks. Bank of England Working Papers 383, Bank of England.

- Gandy and Veraart (2016) Gandy, A. and Veraart, L. A. (2016). A Bayesian methodology for systemic risk assessment in financial networks. Management Science, 63(12):4428–4446.

- Gandy and Veraart (2019) Gandy, A. and Veraart, L. A. M. (2019). Adjustable network reconstruction with applications to CDS exposures. Journal of Multivariate Analysis, 172:193–209.

- Ghamami et al. (2022) Ghamami, S., Glasserman, P., and Young, H. P. (2022). Collateralized networks. Management Science, 68(3):2202–2225.

- Glasserman et al. (2016) Glasserman, P., Moallemi, C. C., and Yuan, K. (2016). Hidden illiquidity with multiple central counterparties. Operations Research, 64(5):1143–1158.

- Glasserman and Young (2015) Glasserman, P. and Young, H. P. (2015). How likely is contagion in financial networks? Journal of Banking and Finance, 50:383–399.

- Gouriéroux et al. (2012) Gouriéroux, C., Héam, J.-C., and Monfort, A. (2012). Bilateral exposures and systemic solvency risk. Canadian Journal of Economics, 45(4):1273–1309.

- Hałaj and Kok (2013) Hałaj, G. and Kok, C. (2013). Assessing interbank contagion using simulated networks. Computational Management Science, 10(2-3):157–186.

- Karp (1972) Karp, R. M. (1972). Reducibility among combinatorial problems. In Complexity of computer computations, pages 85–103. Springer.

- Kovačević et al. (2012) Kovačević, M., Stanojević, I., and Šenk, V. (2012). On the hardness of entropy minimization and related problems. In 2012 IEEE Information Theory Workshop, pages 512–516. IEEE.

- Kromer et al. (2016) Kromer, E., Overbeck, L., and Zilch, K. (2016). Systemic risk measures on general probability spaces. Mathematical Methods of Operations Research, 84(2):323–357.

- Mistrulli (2011) Mistrulli, P. E. (2011). Assessing financial contagion in the interbank market: Maximum entropy versus observed interbank lending patterns. Journal of Banking and Finance, 35(5):1114–1127.

- Rogers and Veraart (2013) Rogers, L. C. and Veraart, L. A. (2013). Failure and rescue in an interbank network. Management Science, 59(4):882–898.

- TriOptima (2021) TriOptima (Accessed: December 23, 2021). TriReduce - portfolio compression. Available https://www.trioptima.com.

- Upper and Worms (2004) Upper, C. and Worms, A. (2004). Estimating bilateral exposures in the German interbank market: Is there a danger of contagion? European Economic Review, 48(4):827–849.

- Veraart (2022) Veraart, L. A. (2022). When does portfolio compression reduce systemic risk? Mathematical Finance, 32(3):727–778.

- Watanabe (1981) Watanabe, S. (1981). Pattern recognition as a quest for minimum entropy. Pattern Recognition, 13(5):381–387.

Appendix A Proof of Theorem 2.4

We will consider the minimum relative liability entropy as the objective function:

| (2) |

where denotes the relative liability of firm toward firm . We refer to Remark 2.5 for the interpretation of this objective function for network compression.

Consider an instance of the NP-complete subset sum problem Karp (1972), defined by a set of positive integers and an integer target value , we wish to know whether there exist a subset of these integers that sums up to . We will show that this can be viewed as a special case for the optimal network compression in the case of network rerouting, nonconservative and conservative compression models.

Let and (otherwise, the subset sum decision is trivial). Given an instance of the subset sum problem, we define a corresponding instance of the optimal rerouting compression by considering the bipartite network of Figure 9 with two core nodes on one side and periphery nodes on the other side. We set the initial liabilities as and for all . Note that the total interbank receivables for and is respectively and , while the total interbank liabilities is zero for and . On the other hand, for all , the total interbank liabilities for node is while the total interbank receivables is zero.

The optimal rerouting compression model is thus equivalent to finding for and which satisfies , and minimizes

Since for all with equality only for , we infer , and the equality holds if and only if there exists such that . Hence, if the solution to optimal rerouting compression model corresponds to then there exist a subset of that sums up to .

Further, note that in the bipartite network of Figure 9, the optimal nonconservative compression is equivalent to optimal rerouting. Hence, the same argument shows that the optimal nonconservative compression is NP-hard.

Hence, it only remains to prove the case of conservative compression model. Given an instance of the subset sum problem, we define a corresponding instance of the optimal conservative compression by considering the network of Figure 10 with three core nodes and periphery nodes . We set the initial liabilities as and for all . Note that the net interbank liabilities for and is respectively and . On the other hand, for all , the net interbank liabilities for node is . Further, for the node the net interbank liabilities is zero.

It is then easy to show that the minimum relative liability entropy can be found by setting for all and consequently, and . The optimization problem is thus equivalent to find which gives and for all . The s should satisfy and minimizes again

The equality holds if and only if there exists such that . We conclude that if the solution to optimal conservative compression model corresponds to , then there exist a subset of that sums up to , which completes the proof.

Appendix B Overview of the genetic algorithm

The genetic algorithm is an optimization technique to numerically solve nonconvex problems. Furthermore, this approach does not rely on the differentiability of the objective function. While this algorithm can still return a local solution, this procedure is less prone to that then, e.g., the gradient descent approach.

Briefly, the idea behind this algorithm is to consider a population of candidate solutions that follow a notion of natural selection. In each step of the algorithm, the fitness (objective value) of all candidate solutions is evaluated; the best performing candidate solutions propagate to the next iteration along with “children” and “mutations” of these candidate solutions. This forms a new population of candidate solutions which and the procedure is repeated until some notion of convergence is reached. Algorithmically, this is presented below for the problem :

-

(i)

Generate a (random) population of feasible solutions .

-

(ii)

Evaluate the fitness of each candidate solution .

-

(iii)

If a termination condition is reached (e.g., the best solution found thus far has not changed in generations) then terminate and return the optimal fitness level and solution.

-

(iv)

Create the next generation of candidate solutions by:

-

(a)

Select of the population to consider (e.g., replace the worst performing solutions with copies of the best performing ones).

-

(b)

Recombine some of the new generation of solutions to create new candidates through binary operations.

-

(c)

Randomly alter some of the new generation of solutions through binary operations.

-

(a)

-

(v)

Return to step (ii).

Within the case studies of Section 5, we implemented the genetic algorithm using the “ga” function in the Global Optimization Toolbox of MATLAB. Each of these case studies was implemented with the following initial populations of solutions: (i) the uncompressed network , (ii) 50 random feasible compressed or rerouted networks, and (iii) if a compression problem (i.e., not the rerouting problem), then the maximally compressed network. The use of the initial and maximally compressed networks in the initial population are to prevent the genetic algorithm from being too biased by the 50 random networks. The recombining of solutions for the subsequent generation of the algorithm is implemented so as to use a weighted arithmetic mean of the two parent solutions; we utilize the “crossoverarithmetic” function in the Global Optimization Toolbox of MATLAB for this purpose. All other parameters considered are the defaults for “ga” in MATLAB.

Appendix C Systematic shocks

While the systemic risk measures provide a meaningful objective to minimize in order to optimize network compression, such constructs present additional computational challenges. Namely, even a simple systemic risk measure such as requires an exponential (in number of banks) time to compute explicitly Gouriéroux et al. (2012). Computationally, this can be overcome with Monte Carlo simulations though that is subject to estimation errors. Herein we will impose systematic shocks on the endowments on the banks, i.e., a comonotonic setting on the stress scenarios , on an aggregate function based around the collateralized Eisenberg-Noe clearing notion. This is in contrast to Acemoglu et al. (2015) in which shocks were i.i.d.

Remark C.1.

For the purposes of this section, we consider a fixed (random) stress scenario, which we denote by , that is not dependent on the financial network; we will revisit this assumption to allow for stress scenarios to depend on the network in the following section.

Remark C.2.

As noted above, any general stress scenario with a law-invariant risk measure can be utilized via Monte Carlo simulation of the systemic risk measure. As such, though we highlight systematic shocks within this work, the theory developed is applicable more generally.

Throughout this section let be a nondecreasing function and be some random variable such that . The stress scenario is then defined by . For the purposes of this section we will focus on systemic risk measures constructed from Value-at-Risk and expected shortfall (as defined in Example 3.5) and aggregate functions that depend on the endowments and liability network through Eisenberg-Noe clearing payments only. We refer to Example 3.2 for a brief discussion of the Eisenberg-Noe clearing problem; importantly, we define the clearing payments as a mapping from the endowments and liability network. As detailed below, this setup allows for polynomial time computation of these meaningful systemic risk measures. Much of this section follows from the logic of Banerjee and Feinstein (2022).

The systematic shock setting allows us to determine threshold market values () such that banks are on the cusp of failing to fulfill their obligations (respectively, such that the banks are on the cusp of defaulting); in particular, we take the view that denotes a systematic factor. These values are presented in Definition C.3 below. Though presented as a mathematical formulation, (Banerjee and Feinstein, 2022, Proposition 4.4) presents an iterative algorithm for finding (respectively, ) taking advantage of the monotonicity of .

Definition C.3.

Define so that is the minimal value such that firm is making payments in full under the liability network , i.e.

Similarly, define so that is the minimal value such that firm is not defaulting under the liability network , i.e.

As noted above, we consider only those aggregate functions whose dependence on the endowments and liability network come through the Eisenberg-Noe clearing payments , i.e., for every and for some monotonic function . In this setting, the threshold values provide a quick heuristic for the health of the financial system. Notably, if for every bank for two financial networks , then for any and, thus, for any nonnegative random variable .

Before proceeding to the representations for the systemic risk measures under systematic shocks, we need to introduce some notation that is provided in greater detail in Banerjee and Feinstein (2022). Namely, we want to consider a piecewise linear construction for the clearing payments which follows from the fictitious default algorithm of Rogers and Veraart (2013). That is,

for any endowment and liability network . In this piecewise linear construction, the mappings are defined by:

for denoting the set of defaulting institutions and is the liability network. In particular, for our comonotonic setting, we can simplify these notions as only a subset of possible sets of defaulting institutions is possible, i.e., we define:

Finally, we will use the notation that is the index of the greatest value of , i.e., . To simplify following formulae, and for every liability network .

We are now able to present the specific forms for the systemic risk measures under these systematic shocks.

Proposition C.4.

Consider a systematic stress scenario described by a nonnegative random variable . Consider an aggregate function whose dependence on the endowments and liability network come through the Eisenberg-Noe clearing payments , i.e., for every and for some monotonic function . Let denote the -quantile for , then the Value-at-Risk for level can be computed as

if . Additionally, the expected shortfall for level can be computed as

The proof of this proposition is provided in Appendix C.1. This result follows directly from the construction of Value-at-Risk and expected shortfall and the logic of Theorem 3.7 of Banerjee and Feinstein (2022) with the collateral .

We conclude this section with a consideration of a special case in which the expected shortfall can be described in closed form for our example aggregation functions from Example 3.2. Specifically, we consider a case in which the systematic factor follows a lognormal distribution.

Corollary C.5.

Consider the setting of Proposition C.4 in which , with and , and takes the form of the specific aggregate functions provided in Example 3.2. Let denote the CDF for the standard normal distribution and is the inverse CDF. For fixed level :

where is the unit vector with a singular in its component and

The proof of this corollary is provided in Appendix C.2. The form for these systemic risk measures is due to the construction of the expected shortfall as provided in Proposition C.4 and the manipulation of the lognormal distribution as in the Black-Scholes pricing formula for European options.

C.1 Proof of Proposition C.4

First we will consider Value-at-Risk with parameter . By construction, the comonotonic copula is nondecreasing in and, by definition, the aggregation function is nondecreasing in . Therefore, for any and ,

By definition of Value-at-Risk, this implies

Additionally, for any and ,

Thus the representation for the Value-at-Risk is proven with the secondary representation following directly by the construction of .

Consider now the expected shortfall with parameter . Similar to the Value-at-Risk above

for any . Partitioning -space by , we find

The second representation follows directly by the construction of .

C.2 Proof of Corollary C.5

First, by property of the lognormal distribution, and . Therefore, for any of our 4 aggregation functions,

by Proposition C.4.

Second, by construction of and the logic from the Black-Scholes formula,

Additionally, by construction,

Consider now the four specific aggregation functions. For simplicity of notation, let

We have

as desired.