Series expansions and direct inversion for the Heston model††thanks: Submitted to the editors DATE.

\fundingJames Watt Scholarship.

Simon J. A. Malham

Maxwell Institute for Mathematical Sciences and School of Mathematical and Computer Sciences, Heriot-Watt University, Edinburgh, EH14 4AS, UK

(, , ).

S.J.A.Malham@hw.ac.ukjs46@hw.ac.ukA.Wiese@hw.ac.ukJiaqi Shen22footnotemark: 2Anke Wiese22footnotemark: 2Simon J. A. Malham

Maxwell Institute for Mathematical Sciences and School of Mathematical and Computer Sciences, Heriot-Watt University, Edinburgh, EH14 4AS, UK (, , ).

S.J.A.Malham@hw.ac.ukjs46@hw.ac.ukA.Wiese@hw.ac.ukJiaqi Shen22footnotemark: 2Anke Wiese22footnotemark: 2

Series Expansions and direct inversion for the Heston model††thanks: Submitted to the editors DATE.

\fundingJames Watt Scholarship.

Simon J. A. Malham

Maxwell Institute for Mathematical Sciences and School of Mathematical and Computer Sciences, Heriot-Watt University, Edinburgh, EH14 4AS, UK

(, , ).

S.J.A.Malham@hw.ac.ukjs46@hw.ac.ukA.Wiese@hw.ac.ukJiaqi Shen22footnotemark: 2Anke Wiese22footnotemark: 2Simon J. A. Malham

Maxwell Institute for Mathematical Sciences and School of Mathematical and Computer Sciences, Heriot-Watt University, Edinburgh, EH14 4AS, UK (, , ).

S.J.A.Malham@hw.ac.ukjs46@hw.ac.ukA.Wiese@hw.ac.ukJiaqi Shen22footnotemark: 2Anke Wiese22footnotemark: 2

Abstract

Efficient sampling for the conditional time integrated variance process in the Heston stochastic volatility model is key to the simulation of the stock price based on its exact distribution. We construct a new series expansion for this integral in terms of double infinite weighted sums of particular independent random variables through a change of measure and the decomposition of squared Bessel bridges. When approximated by series truncations, this representation has exponentially decaying truncation errors. We propose feasible strategies to largely reduce the implementation of the new series to simulations of simple random variables that are independent of any model parameters. We further develop direct inversion algorithms to generate samples for such random variables based on Chebyshev polynomial approximations for their inverse distribution functions. These approximations can be used under any market conditions. Thus, we establish a strong, efficient and almost exact sampling scheme for the Heston model.

keywords:

Series expansion, Direct inversion, Chebyshev approximation, Stochastic volatility

{AMS}

91G60, 41A58, 34E05, 41A10, 60H30

1 Introduction

Stochastic volatility models involving a pair of stochastic differential equations, with the diffusion term of the first one governed by the evolution of the second equation, are immensely popular in the pricing of derivatives. Among the existing stochastic volatility models, the Heston model plays an important role and is used widely. It can be expressed in the form of a two-dimensional system

(1)

(2)

where and are two independent standard Brownian motions, and , , and typically also are positive constants with . The component characterises the dynamics of the stock price while the component specifies the variances of its returns. The introduction of randomness to the volatility has been used to explain the long-observed features of the implied volatility surface in a self-consistent way. The variance process follows a mean-reverting square-root or Cox-Ingersoll-Ross (CIR) process (Cox, Ingersoll and Ross [13]).

Closed form solutions for standard vanilla option prices under the Heston model are available; see Heston [21] and Kahl and Jäckel [25]. However for exotic options, especially path-dependent options, such closed form solutions are not known in general and Monte Carlo simulation is often employed. Typically, continuous stochastic processes are approximated by paths simulated on discrete time grids. It is normally natural to consider the Euler-Maruyama scheme which converges weakly with convergence rate one under certain regularity conditions; see Section in Kloeden and Platen [26], or other standard higher-order discretization approaches such as the Milstein [30] and Itô-Taylor schemes introduced in Chapter and in Kloeden and Platen [26]; see Section in Glasserman [17] as well. However, these conditions do not hold in the Heston model, which will be discussed in detail below.

Discretization schemes such as those have several drawbacks for the Heston model. The first issue is that the probability of the discretised variance process becoming negative is nonzero, which will bring considerable biases to the simulation estimators. Correction techniques such as absorption and reflection are designed to overcome this problem, see Gatheral [15], Bossy and Diop [11] and Higham and Mao [22]. Lord, Koekkoek and Van Dijk [27] unify a large number of traditional correction techniques and design a new scheme, the full truncation method, which seems to perform well in many situations. Taking advantage of the qualitative properties of the true distributions, Andersen [5] proposes two new time-discretization algorithms based on moment-matching strategies, namely the truncated Gaussian scheme and the quadratic-exponential scheme. These positivity-preserving schemes are reported to have substantial improvements in efficiency and robustness over other existing methods; see Andersen [5], Lord, Koekkoek and Van Dijk [27] and Haastrecht and Pelsser [39].

The second issue is related to convergence, which requires the drift and diffusion coefficients to be globally Lipschitz, see Kloeden and Platen [26]. However, the square root functions embedded in the Heston model are not Lipschitz. Thus, convergence of these discretization schemes is difficult to establish; see Glasserman [17] and Andersen [5]. Recently, Altmayer and Neuenkirch [4] have studied the weak convergence rate for a numerical scheme under the Heston model, which typically reaches order one with mild assumptions. Hefter and Jentzen [20] consider the one-dimensional CIR process and show that equidistant discretization methods may have an arbitrary slow convergence rate in the strong sense. See Alfonsi [3] and Berkaoui, Bossy and Diop [7] for more discussions on the convergence of the discretised univariate variance process.

Apart from discretization schemes, there are also (almost) exact simulation methods based on the exact distributions of the stock price and variance processes. The respective transition laws of these follow a conditional lognormal distribution and a conditional scaled noncentral chi-square distribution; see Cox, Ingersoll and Ross [13]. Broadie and Kaya [12] take this approach to generate sample variance and stock price. They apply an acceptance-rejection method to the noncentral chi-square sampling for the variance process. Malham and Wiese [28] propose an exact acceptance-rejection method and a high-accuracy direct inversion method for the simulation of the generalised Gaussian distribution, which are then applied to the noncentral chi-squared sampling. Haastrecht and Pelsser [39] focus on the efficient approximation of the variance. They explore the features of the distribution for the variance process and suggest a cache for its inverse distribution functions, leading to an almost exact simulation scheme.

To realise the stock price, the key task of Broadie and Kaya [12] is to sample from the time integrated variance conditional at the endpoints, i.e. . They build on the results 2.m and 6.d in Pitman and Yor [32] to derive the explicit form for the corresponding characteristic function. Fourier inversion techniques in conjunction with the trapezoidal rule are applied to numerically evaluate the probability distribution function. This is followed by inverse transform sampling to simulate the value of the above integral. Their numerical results imply that the proposed method has a faster convergence rate compared to the Euler scheme with bias-free simulation.

Because of the dependence on and , Broadie and Kaya [12] compute the characteristic function for each step and path in the Monte Carlo simulation. At the expense of a small bias, Smith [37] presents an approximation to the characteristic function, which makes it possible to precalculate and store the values of the characteristic function for all the points required in advance. Glasserman and Kim [18] provide another sampling method

for the time integrated conditional variance, which relies on an explicit representation as infinite sums and mixtures of gamma random variables. When combined with the exact simulation method suggested by Broadie and Kaya [12], their method is highly effective in terms of both accuracy and computational speed for pricing non-path-dependent options across a full range of model parameter values.

Motivated by the decomposition in Glasserman and Kim [18] Theorem , we simplify the variance process to a squared Bessel process by a measure transformation and construct a new series expansion for its conditional integral under the new measure with exponentially decaying truncation errors. We demonstrate that the task of sampling the new series can be largely reduced to simulations of simple random variables, which are independent of any model parameters. We provide highly accurate Chebyshev polynomial approximations to the inverse distribution functions of such random variables and design direct inversion algorithms to generate their samples. Thus, we establish a flexible, efficient and almost exact simulation scheme for the Heston model. To summarise, the advantages of our method are that truncation errors decay exponentially, high-accuracy samples can be generated efficiently by direct inversions and approximations of inverse distribution functions can be used under any market conditions.

The paper is organised as follows. In Section2, we present our new representation under the new probability measure and the acceptance-rejection algorithm for changing back to the original measure. In Section3, we detail the simulation methods for each individual part of the representation. We include the derivation of asymptotic expansions for the corresponding distribution functions and the construction of Chebyshev polynomial approximations for their inverse. We apply our method for pricing purposes and we compare its efficiency and accuracy to Glasserman and Kim [18] with numerical results reported in Section4. Conclusions are drawn in Section5.

2 Main results

The method we propose closely follows the lead of Broadie and Kaya [12] and Glasserman and Kim [18] with the key difference for the simulation of the conditional integral of the variance process. To complete the understanding of the motivation for sampling from the conditional integral, we first quote some properties with regard to the Heston model.

We start with the variance process governed by Eq.2, which is a CIR process (Cox, Ingersoll and Ross [13]) with transition probability given explicitly as a scaled noncentral chi-squared distribution. With the degrees of freedom for this process defined to be , we have

(3)

where is the initial value and denotes a noncentral chi-squared random variable with degrees of freedom and noncentrality parameter . This means that conditional on , is distributed as multiplied by a noncentral chi-squared distribution with degrees of freedom and noncentrality parameter

The above law provides a way of exactly simulating from , see Broadie and Kaya [12], Scott [35] and Malham and Wiese [28] for details.

By employing the explicit solution of the stock price process Eq.1 and Itô’s formula, we obtain

Combining these two results, Broadie and Kaya [12] observe that given , and , the distribution of is Gaussian with known moments since the process is independent of the Brownian motion , i.e.

Hence, an exact simulation for the stock price given the initial conditions and is now reduced to sampling a conditional normal random variable given above provided there is a way to sampling from the joint distribution . As can be simulated using the transition law in Eq.3, the main challenge is now to develop a tractable method for sampling from the time integral of the variance process over given its endpoints and , i.e.

In what follows we focus on developing a new representation for the above integral building upon

the decomposition suggested by Glasserman and Kim [18], which applies the decomposition of the squared Bessel bridges from Pitman and Yor [32].

Before proceeding, we reduce the model to a special case by time-rescaling and a measure transformation. First, define . Then, satisfies the following stochastic differential equation (Glasserman and Kim [18])

where and becomes a standard Brownian motion. In order to consider a new probability measure, we suppose that the original model is established under measure , meaning that our target now is to simulate

under with , and .

Second, we further simplify the model by introducing a new probability measure (Pitman and Yor [32] and Glasserman and Kim [18]) such that

(4)

By the Girsanov theorem, is a standard Brownian motion under . With this replacement, the rescaled process satisfies

(5)

which is a -dimensional squared Bessel process under . Hence, our objective is to sample from the time integral of a squared Bessel process given its values at the endpoints, denoted by , under the new probability measure , i.e.

(6)

and to find a connection between the distributions for the conditional integral under and .

Next, we state our main result which relies on decomposing the conditional integral as introduced by Glasserman and Kim [18].

Theorem 2.1.

Under the new probability measure , the conditional integral of the rescaled variance process is equivalent in distribution to the sum of three infinite series of random variables

where , , , , , are mutually independent, and is a Bessel random variable with parameters and , i.e. . Moreover, , , , , admit the following representations:

a We have

where for , the are independent Poisson random variables with mean and for , the are independent copies of the random variable and are independent exponential random variables for ;

b Further we have

where for , the are independent copies of the random variable and are independent gamma random variables with shape and rate for ;

c And also we have the , , which are independent copies of the random variable such that

where for , the are independent copies of the random variable and are independent gamma random variables with shape and rate for .

Proof 2.2.

We work on the probability measure throughout this proof. We note that for a fixed ,

(7)

where is defined by setting for and . Then using equation Eq.5, the process satisfies

where is a standard Brownian motion. We observe that

is a -dimensional squared Bessel process. Conditional on the end points, the process

is then a squared Bessel bridge, denoted

by . Then the right hand side of Eq.7 has the same distribution as

(8)

We prove the result in three steps.

First, the integral Eq.8 can be decomposed into the sum of three independent parts as follows:

where

and for , are independent copies of

and is an independent Bessel random variable with parameters and , i.e. . This is a direct result from Glasserman and Kim [18], who apply the decomposition of squared Bessel bridges proposed by Pitman and Yor [32] to the transformed variance process.

Second, it follows from Glasserman and Kim [18] that the Laplace transforms of , and for are given by

(9)

(10)

(11)

Third, to verify the random variables , and have the same distribution as the series expansions which define , and respectively, it is sufficient to show that they have identical Laplace transforms. To do this, let us first rewrite , using some important identities regarding the hyperbolic functions and ; see

Malham and Wiese [29]. Specifically, we observe

Iterating times gives us

(12)

(13)

Substituting Eq.12 into Eq.9 and rearranging the terms, we get

where . On the other hand, it follows from that

where as . Thus, for , we have an alternative form for given by

Similarly, for after substitution and rearrangement, we have

where as . As a result, plugging into this expression yields

Next, we derive the Laplace transforms of , and , denoted by , and respectively. For any , we have

where the second equality comes from the interchange of expectation and limit by the Bounded Convergence Theorem and the fourth equality holds due to the fact that for all and (see Biane, Pitman and Yor [8, formula ]).

Following similar arguments, we now determine the Laplace transform for . Indeed, from for any (see Biane, Pitman and Yor [8, formula ], we conclude that

Hence, we can now deduce that as for . In line with the steps explained above, follows since this is a special case when , completing the proof.

Remark 2.3.

We notice that after separating the time parameter , the dependence of on model parameters is only though the Poisson random variable and depends only on one parameter . This feature provides us with a possibility that the task of sampling the conditional integral can be largely reduced to the simulations of simple random variables, whose distributions remain unchanged as we change the values for the model parameters; see section 3.1 and

section

3.5.

We have represented the conditional time integral by double infinite weighted sums and mixtures of simple independent random variables under the new probability measure , which serves as a theoretical basis for the exact simulation from the distribution of Eq.6 under . However, our goal is set up under the probability measure . We now focus on the task of generating a sample from the distribution of the conditional integral under once we have generated a sample under . In particular, we explore the relationship between the probability density functions of the integral under these two probability measures. We specify the details in the following theorem.

Theorem 2.4.

Suppose that and are the probability density functions of under the probability measures and , respectively. Then, we have

where

with denoting the modified Bessel function of the first kind.

Proof 2.5.

We will make use of the shift property of the Laplace transform to justify the theorem. We first establish a connection between their respective Laplace transforms. For any , consider the Laplace transform of at , which is the -expectation of . Thus, we get

The second equality is a result of the change of law formula from Pitman and Yor [32], see the Appendix of Broadie and Kaya [12] as well. Now by the application of the shift property, we can write

Using the formula in Pitman and Yor [32] for the Laplace transform of at given by

and setting establishes the stated result.

The above theorem relates the density of the distribution explicitly given by Theorem2.1 in terms of infinite sums

to the density of the distribution we are interested in. This means we can simulate

the random variable under the measure provided we have an observation from its distribution under the measure . In general, we construct the acceptance-rejection algorithm outlined in Algorithm1 to generate samples from .

On average, the probability of accepting a proposed sample is

where and independently follows the distribution of under . Consequently, we require due to the fact that a probability only takes values between zero and one. In practice, we prefer a value of closer to one as it indicates higher acceptance probability on average, and thus fewer iteration steps needed.

Algorithm 1 Acceptance-Rejection

1: Simulate a realisation of the random variable under using Theorem2.1.

2: Obtain a sample independently from the uniform distribution over unit interval.

3: If , accept as a sample drawn from the distribution of under ; otherwise reject the value of and return to the first step.

Remark 2.6.

The requirement is fulfilled under any market conditions. In fact, because the support for the random variable is , we have

.

Noticing that for and then leads to .

So far, we have described the theories behind the simulation of the time integral conditional variance. It is a matter of sampling infinite series, combined with the acceptance-rejection method. For the next stage, we will address some issues concerning the practical implementation of the theory. In particular, strategies are required to deal with infinite summations of random variables. We propose direct inversion algorithms based on approximating the corresponding inverse distribution functions to tackle this problem. Further, the dependence between the series and the model parameters implies that the recomputation of the inverse distribution functions when using a new set of model coefficients is inevitable. We show that the series can be decomposed as the sum of simple random variables, whose distributions do not depend on any market conditions. We specify the details in the next section.

3 Simulation

In this section, we outline how to generate an exact sample for under by Theorem2.1 introduced earlier. In particular, we discuss the sampling techniques corresponding to and . We note that is a special case of with . In order to apply the decomposition theorem to sample the conditional integral, we need to determine a point at which the infinite summation is terminated. We consider the truncation for the outer summation now, leaving the inner one to be discussed further in the following contexts. Let us denote the truncation level by and the resulting remainder random variables of and by and respectively, i.e.

We evaluate the effect of truncation by summarising the means and variances of the remainder terms in the next lemma; see AppendixA for a detailed proof.

Lemma 3.1.

Given the truncation level , we have

Remark 3.2.

The above lemma implies that the truncation errors decay exponentially. This is an appealing property of the new series in Theorem2.1 as the truncation error will decrease so quickly that the Monte Carlo error will dominate the total error even for small truncation level . Hence, including the terms at lower levels will be enough to produce an accurate approximation. This is supported by our numerical simulations in Section4.

3.1 Simulation of

Recall that by dropping the remainders, we approximate by where

Notice that the are independently and identically distributed as .

To reduce the truncation error further, we simulate the tail sum as well. Glasserman and Kim [18] use the central limit theorem to show the validity of a normal approximation for the remainders. They also point out that a gamma approximation is feasible and better in the sense that its cumulant generating function is closer to that of the remainder random variable compared with that of a normal approximation. Therefore, inspired by this, the approximation to with tail simulation for a given truncation level is

where is a gamma random variable such that its first two moments match those of the remainder from Lemma3.1.

We now detail our sampling strategy for . The series which defines suggests two potential problems. First, the random variables are represented by an infinite weighted sum of independent exponential random variables, which requires an efficient simulation method. Second, given a Poisson sample for a fixed level , sampling the sum of independent random variables becomes increasingly computationally demanding when the sample tends to be larger. Thus, we now incorporate these two tasks with each other and consider simulating the sum of independent random variables directly, denoted by , i.e.

where are independent copies of . Using the Laplace transform for given in Biane, Pitman and Yor [8], has the following Laplace transform:

(14)

for .

We observe that any positive integer can be expressed in the form

Here is the multiples of present in the integer , i.e. , is the multiples of present in the remainder of the division of by , i.e. , and so forth. As the law of is infinitely divisible for any (see Section of Biane, Pitman and Yor [8]), the sum admits the representation

where and for , are independent copies of , i.e. the sum of independent random variables , with . Then, the above representation can be intended as a basis for an efficient sampling scheme for for all if we can realise effectively for .

Indeed, we apply the direct inversion method to simulate with their inverse distribution functions approximated by predetermined Chebyshev polynomials for each .

In general, the direct inversion algorithm for generating the samples of for any is described as follows.

Algorithm 2 Direct inversion for

1: For each , sample independent random variables , from the distribution of using the inverse distribution functions based on the corresponding Chebyshev polynomial approximations.

2: Compute the accumulated sum, i.e. .

The advantage of this algorithm is that we only need to construct the Chebyshev polynomial approximations for the inverse distribution function of for .

With this replacement, the complicated inverse distribution function becomes very easy to compute at arbitrary points. Moreover, since does not depend on any model parameters, the coefficients of the polynomials can be computed and tabulated in advance. As such, when a sample for is needed, we truncate the series representation to include the terms at with the tail approximated by a gamma distribution. For each , we generate Poisson samples and simulate the sums directly by Algorithm2, which requires evaluating some prescribed polynomials with coefficients drawn directly from the cached table; see the supplementary materials. To make the above process fast for implementation, we take advantage of the direct inversion to obtain Poisson samples when the mean is less than . For larger means, the PTRD transformed rejection method suggested by Hörmann [23] will be used.

To obtain the Chebyshev coefficients, it is crucial to determine the values of the inverse distribution functions at several points efficiently and accurately. For large , we derive an asymptotic series expansion for the distribution function of when through the inverse Fourier transform of its characteristic function. While for small , we utilise the explicit expression for the density function given by Biane and Yor [9], which involves the parabolic cylinder functions. To derive the representation for the distribution function, we use a routine consisting of the power series and asymptotic expansions for the parabolic cylinder functions to evaluate the density function followed by term-wise integration. With these expansions computed, we apply root-finding algorithms to calculate the required values.

3.2 Asymptotic expansion for the distribution function of for large

Before proceeding, it is worth noticing that in the limit , the expectation and variance of will diverge. Thus, we standardise the random variable by , so that the new random variable has mean zero and variance one. As is non-negative, the support of is . Then, taking the inverse Fourier transform of the characteristic function, the probability density function of has the form

where denotes the probability density function of and the first equality follows from the classical theorem on transforming density functions. By introducing , the above equation can be written as

(15)

where satisfies

(16)

We apply the standard technique of the steepest descent method to develop the asymptotic approximation for , where all the higher order terms are given in reciprocal powers of , see Bender and Orszag [6], Bleistein and Handelsman [10] and Ablowitz and Fokas [1]. The expansion is then integrated term-wise to generate the asymptotic representation for the distribution function. The general procedure is given below. We first identify the critical points including saddle points of such that . Note that since depends on the parameter , the saddle point will also depend on . Due to the fact that is quite small as , we can establish a useful expression for as a Taylor series in . Afterwards, we demonstrate that the original contour of integration, i.e. the real line, can be deformed onto the steepest descent paths, obtained by considering the contour defined by and , in the domain where the integrand is analytic. In this way, the rapid oscillations of the integrand can be removed when is large, whence the asymptotic behaviour of the integral can be determined locally depending only on a small neighbourhood of the critical points. We present the results in the next theorem, which is proved in AppendixB.

Theorem 3.3.

As for fixed with and sufficiently small, we have

(17)

where and are constants with explicit form derived in the proof and is the gamma function.

Having developed the large asymptotic approximation for the probability density function with all the higher order terms given in reciprocal powers of , the next stage is to derive an asymptotic representation for the corresponding distribution function. Before that, we first consider the asymptotic expansion for the probability for some , with and sufficiently small, which can be accomplished by taking the integration of Eq.17 on the finite interval . We then explain how this expression can be used to approximate the distribution function. The results are summarised in the next theorem with the proof given in AppendixC.

Theorem 3.5.

For , and , sufficiently small, the following asymptotic series expansion holds as . For , we have

For , we have

Here, and are constants explicitly given in Eq.61-Eq.62 and Eq.63-Eq.64 in the proof and is the lower incomplete gamma function.

Remark 3.6.

We have thus established a large asymptotic series expansion for the probability that the random variable takes values in . Notice that this representation is valid when with sufficiently small for . This restriction can be traced back to Theorem3.3, where the saddle point is given in a Taylor series in for small . Hence for practical applications, we truncate the Taylor series to generate an accurate approximation for the saddle point when is sufficiently small. More precisely, there is a region centred around zero with width , throughout which the error of the approximation is below a given threshold. The range of validity can be determined by numerical comparisons using for example Maple in practice. This range of validity turns out to be large enough so that the error in computing the distribution function for large is negligible. More precisely, we take the error below for all the cases considered here and the corresponding values for are , , and for and , respectively.

In summary, we have so far developed a tractable method to evaluate the distribution function . This is approximated by integration of the corresponding density function on some restricted interval with carefully chosen for each . We derive an asymptotic expansion for the integral in reciprocal powers of for all orders following the steepest descent method. In practice, we compute enough terms for the expansion to achieve the desirable accuracy in Maple with digit accuracy for and , along with the root-finding for values at nodal points required by Chebyshev polynomial approximations.

3.3 Series expansion for the distribution function of for small

In this section, we turn to the specifics of the series expansion for the distribution function of for small . Recall from Eq.14 that has the Laplace transform for . Biane and Yor [9, formula ] have given an explicit expression for the probability density function with such a Laplace transform. Namely, for arbitrary , the probability density function is of the form

where is the parabolic cylinder function with order . We use different strategies to calculate these functions according to different ranges of . For small , the power series is preferable while for large an asymptotic expansion will be applied. We summarise these properties here. First, the series expansion for the parabolic cylinder function can be written as

(18)

with the coefficients satisfying some recurrence relations, that can be found in Gil, Segura and Temme [16] or Abramowitz and Stegun [2]. We use Maple for their practical implementation. Second, in the limit , has the following asymptotic behaviour (Gil, Segura and Temme [16, formula ]):

(19)

where denotes the Pochhammer symbol . For comparisons of different computational methods, see Temme [38] and Gil, Segura and Temme [16]. Finally, integrating the density function term-wise yields the series representation for the distribution function of stated below. See AppendixD for a detailed proof.

Theorem 3.7.

For any and , the distribution function can be written as the following convergent series

(20)

where the function for is given by

Further, satisfies

for all that are sufficiently large, where can be expressed as the convergent series

and has the asymptotic expansion

Here, is the upper incomplete gamma function.

The previous theorem provides an effective approach to calculate the distribution function for small across its support with high precision. In practice, we choose to use the asymptotic expansion for the parabolic cylinder function whenever for some positive constant , suggested by Gil, Segura and Temme [16, Section ]. Accordingly, we set when computing the function for fixed . This means only asymptotic series is involved in the computation of for sufficiently large such that . The constant , which may vary depending on the value of , can be determined by numerical trials of comparing the accuracy and efficiency of evaluating both the power series and asymptotic representations at particular points. As in the case for large , we compute the above series representation for and perform the root-finding for in Maple for and . Notice that the series expansion developed here is valid for any , not only for integer . This will be useful in the simulation of later on.

3.4 Chebyshev polynomial approximation for the inverse distribution function of

As presented above, for any positive integer , the simulation of is based on generating a series of random variables for

by direct inversion. This method takes a uniform sample

and returns the quantile function evaluated at as a sample for the associated distribution, which requires computing the inverse of the distribution function. However, it is often the case that the inverting process is computationally inefficient due to many factors such as poor initial guess and the lack of an analytical expression for the corresponding quantile function. Since a large number of samples is needed for the Monte Carlo simulation when the same number of inversions of the distribution will be performed, we now look for a more tractable technique to complete this step.

Indeed, we employ the method of Chebyshev polynomials explained below to approximate the inverse distribution function for .

Despite the fact that the polynomial is just an approximation, we can still obtain highly accurate results by restricting the error, which is controlled by the degrees of the polynomials we construct. In practice, we require the uniform error to be far smaller than the Monte Carlo error, e.g. of order .

Recall that a degree Chebyshev polynomial approximation has the form

where for are the Chebyshev polynomials of degree defined on and for are the Chebyshev coefficients computed in the standard way following Press et al. [33]. Since polynomials often exhibit more rapid changes than the distribution functions, approximations by polynomials might not be able to fully capture the behaviour of the inverse function . Hence, identifying appropriate scaling schemes of the argument is of great importance to allow the application of the Chebyshev polynomial approximation.

The choices of the scales are mainly characterised by the behaviour of the function depending on the range of . We briefly state the scaling and its rationale behind for large and small separately.

Large

Instead of the sum , we take the normalised random variable with zero mean and unit variance into consideration. For the approximation of the inverse distribution function , we focus on the sub-interval of its support first, corresponding to the region where the random variable takes positive values. In the limit of large , the distribution function of resembles that of a standard normal distribution. Thus, we generalise and apply the ideas underlying the Beasley-Springer-Moro direct inversion method for standard normal random variables; see Moro [31], Joy, Boyle and Tan [24] and Malham and Wiese [29]. The normal distribution function has three regions exhibiting different characteristic behaviours on the positive real line. Accordingly, we roughly split the interval into three regimes: the central , the middle and the tail regimes. In general, the central regime roughly represents the area where the decreasing density function has a increasing slope while the middle regime represents the area where the decreasing density function has a declining slope with the tail regime representing the region where the density function is flat taking values close to zero. We neglect the regimes from to .

Remark 3.8.

It should be pointed out here that the above rule is just for reference only. In

reality, we can choose optimal values for the boundaries and by a small number of trials in Maple to ensure that the resulting Chebyshev polynomial approximations have moderate degrees while retaining the accuracy for all three regimes. We may come across the circumstance that the approximations which achieves the desired accuracy have degrees of say for both the central and middle regimes but a higher degree of say for the tail regime for some given and . Such a case should be avoided from the perspective of efficiency as higher degree often comes with higher computational cost. Hence, it is necessary to set the values and again through further investigations so that the degrees of the approximation for all regions are balanced with each other. If both of the degrees of the Chebyshev polynomials constructed for two neighbouring regions are at relative lower level, we may combine those two regimes to one and produce a unified approximation.

In the central regime, we follow Malham and Wiese [29] to scale and shift the variable. Define and , where the parameters and are chosen to make sure and . Then, we approximate the inverse distribution function by

In the middle and tail regimes, we approximate

where and with the parameters and chosen such that at the left endpoint and at the right endpoint. The ansatz for follows from inverting the asymptotic tail approximation for the standard normal, which is equivalent in distribution to when by the central limit theorem; see Moro [31].

The above serves as a general discussion for choosing the scaled variables and approximations in the region of for large . We apply this procedure to the cases and , the inverse distribution functions of which are roughly anti-symmetric.

For the remaining half sub-interval of its support, we can apply similar results to the scaling and approximation following the arguments mentioned above.

Small

In the Chebyshev polynomial approximation for small , the idea remains the same as above. Notice that the random variable takes positive values only. Since the distribution has a heavy right tail, we break down the support of into four regimes: the left , the central , the middle and the right tail regimes. We neglect the regimes at a distance of from its endpoints. In theory, these boundary points are determined in accordance with the behaviour of the distribution function, but again it is better to set them via empirical studies in practice.

The central limit theorem tells us the asymptotic distribution of the sum when P is large. However, for small we have to analyse the limiting behaviour of the distribution function and its inverse in order to help us find the proper scaled variables when we construct Chebyshev polynomial approximations. We build on the series representation for given in Theorem3.7 to derive the results below; see AppendixE for a detailed proof.

Corollary 3.9.

For any , the distribution function has the following asymptotic expansion

(21)

The above expression describes the behaviour of the distribution function as . Now, our goal is to invert this relation to obtain the asymptotic approximation for the inverse distribution function as . Let , then from Eq.21 it is clear

(22)

Introducing the new variable and taking logarithm on both sides, we can rewrite Eq.22 as

After rearrangement, the above expression becomes

Since as , we have in the limit . This relation further gives

Hence, taking advantage of order relations we can write in terms of as

(23)

when . In particular by the fact that as , its leading order behaviour yields

as , i.e. , where the last equation comes from the transformation .

As , i.e. , we adopt a gamma approximation for the tail. This is implied by empirical tests which show that the distribution is positively skewed with a longer right tail. Hence, by matching the mean and variance of with those of a gamma random variable, the shape and rate parameters take the form and . Then, the distribution function is approximated by the distribution function of a gamma random variable with parameters and given as follows:

Making use of the asymptotic relationship given below for the incomplete gamma function (Abramowitz and Stegun [2, formula ])

By a short calculation analogous to Eq.23,

we conclude

On substituting , as , i.e. , its leading order is of the form

The analysis above outlines the asymptotic approximation for as and , and provides the ansatz behind the choices of reasonable scaling variables for Chebyshev polynomial approximations for small , i.e. . Accordingly, we report the routines for approximations of the inverse distribution function through Chebyshev polynomials for the four regimes identified in detail. Note again the parameters and given below restrict the ranges of the transformed variable to the interval .

For all the four regimes, we approximate by a degree Chebyshev polynomial approximation of a scaled and shifted variable as below:

where in the left regime , in the central regime and in the middle regime and right tail regime .

(a)

(b)

Figure 1: We plot the errors in the Chebyshev polynomial approximations to the inverse distribution functions with and with across all regimes, respectively. Note that to highlight the tail we use a log-log10 scale with on the abscissa.

We have summarised the approximation techniques for the inverse distribution function or taking into account the various values that and might take. Following this, we compute the coefficients for the Chebyshev polynomial approximations in the standard fashion (see Press et al. [33]) for the cases , using Maple. With all these accurate and reliable coefficients, quoted in the supplementary materials, then imported to Matlab, subsequent Chebyshev approximations are evaluated by Clenshaw’s recurrence formula, which can be found in Press et al. [33]. Therefore, for any , can be sampled repeatedly with high efficiency using Algorithm2.

We end this section by showing the respective errors in the Chebyshev polynomial approximations to and with when is and in Fig.1. For each , the error of the approximation is , where is obtained by a high precision root-finding procedure applied to the expansions for the distribution functions and is evaluated by the prescribed Chebyshev polynomials. To highlight the tail we plot the errors on a log-log10 scale with on the abscissa. For , we split the interval into two regimes: and , where both of the Chebyshev polynomials have degrees . For , we generate approximations for five regimes as described above where the right tail region is further split into two, the degrees for which are in the left with ,

in the central with ,

in the middle with ,

and in the right tail regimes with and , respectively. Notice the error in all cases is of order . Results for the other values, reported in Shen [36], have similar accuracy as those in Fig.1.

3.5 Simulation of and

Let us first introduce the notation , where is the degrees of freedom. Note that for Heston models calibrated to real market data, the zero boundary of the variance process is typically attainable and strongly reflecting; see Haastrecht and Pelsser [39] and Lord, Koekkoek and Van Dijk [27]. By the Feller condition, this requires , i.e. . Hence, after separating the time parameter, can be written in the form

with depending only on the parameter . The structure of the random variable , along with its dependence on the model parameters, provides us with another possibility to sample and thus , apart from the truncation method. In fact, the Laplace transform of is identical to

that for . We can therefore try to extend the direct inversion of for any developed above for the simulation of .

Recall that has the Laplace transform

which has the same expression as that of given by Eq.14 after replacing by . The only difference is that the parameter now is restricted to rather than positive integers. This suggests the decomposition proposed in section 3.1 for integer and the resulting is no longer reasonable. However, motivated by Malham and Wiese [28], we have the following alternative formula for , which is given to the first three decimal places

where for .

The above decomposition works for the case when is rounded to three decimal digits, but it can be generalised to given to any decimal places in principle. Next, we give the direct inversion algorithm for generating for any given to the first three decimal places.

Algorithm 3 Direct inversion for

1: For each ,

sample independent random variables , from the distribution of by inverse transform sampling based on the corresponding Chebyshev polynomial approximations.

2: Compute the accumulated sum, i.e. .

(a) Figure 2: We plot the errors in the Chebyshev polynomial approximations to the inverse distribution functions with across all regimes. Note as above we use a log-log10 scale with on the abscissa.Figure 3: We plot the errors in the Chebyshev polynomial approximations to the inverse distribution functions with , i.e. across all regimes. Note as above we use a log-log10 scale with on the abscissa.

Given Algorithm3, for a general , the simulation of is reduced to simulating several particular random variables such as , , using their inverse distribution functions, which are approximated by the associated Chebyshev polynomials. To design these Chebyshev polynomial approximations, the approach for with small integer introduced in section 3.3 and section 3.4 can be fully used here. This is because the series expansion and the asymptotic approximation for the distribution function of remain valid for small non-integer . Therefore, we apply the same strategy to calculate the Chebyshev polynomial approximations for the inverse distribution function of with fixed

, ,

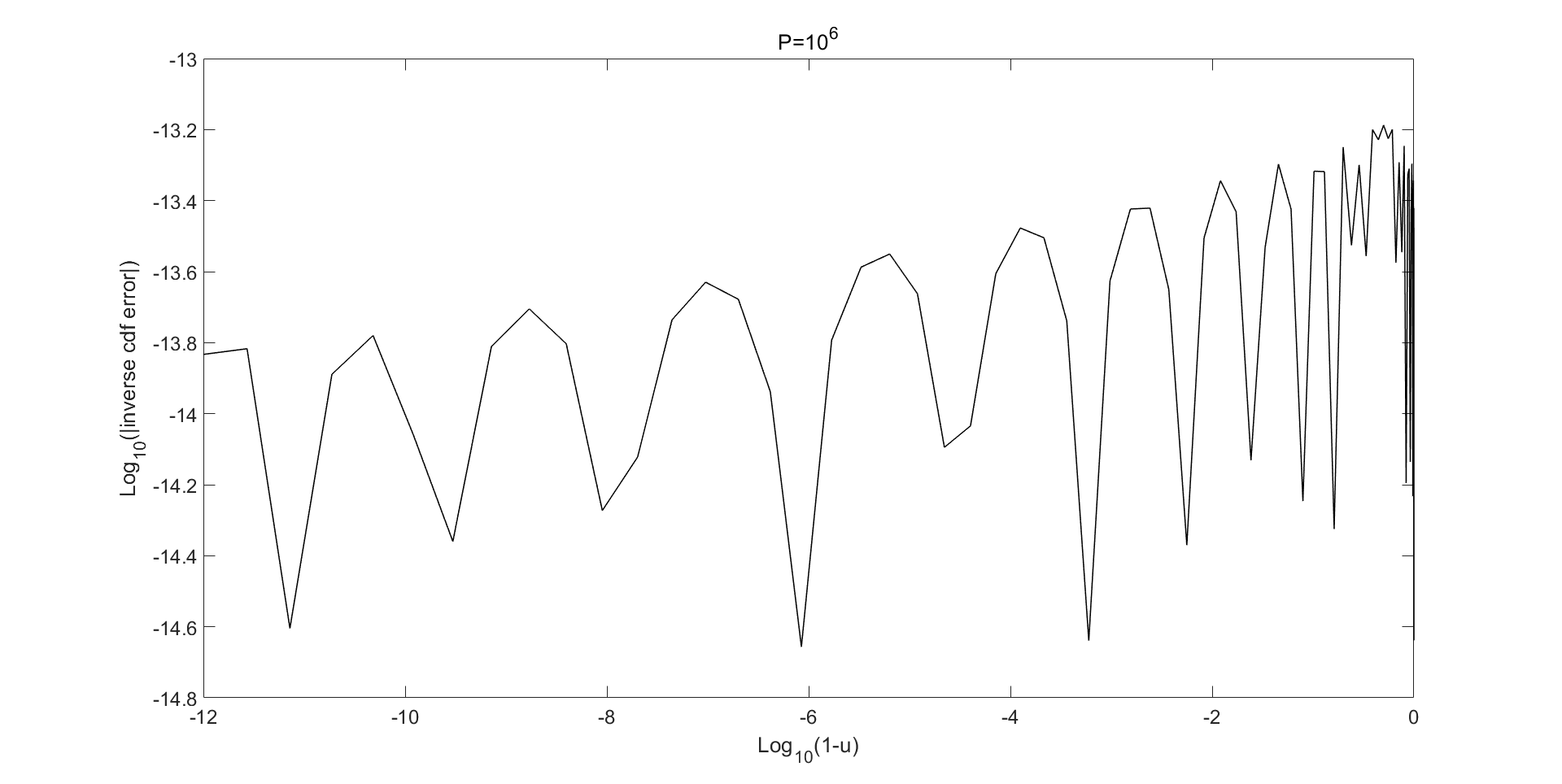

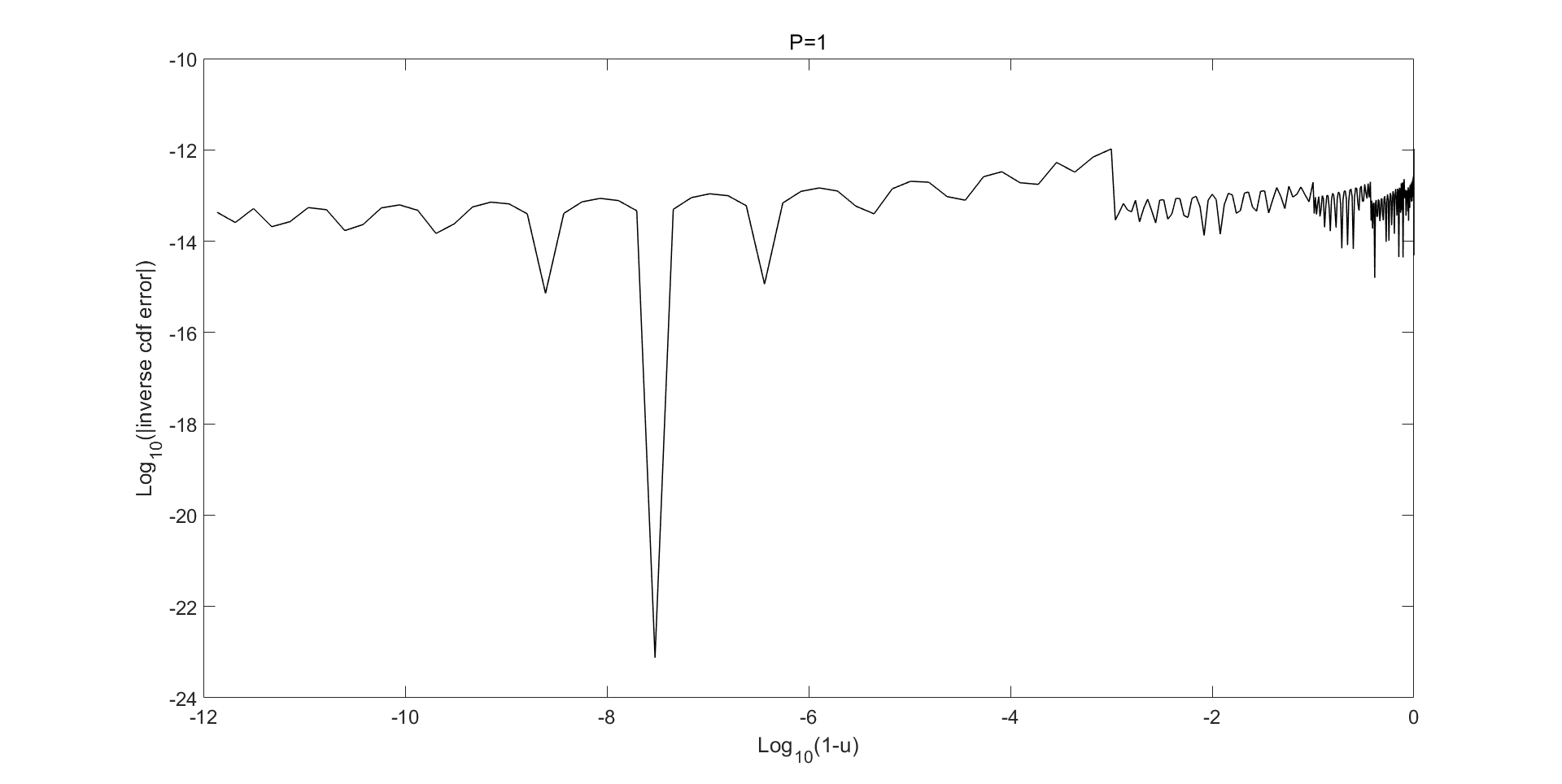

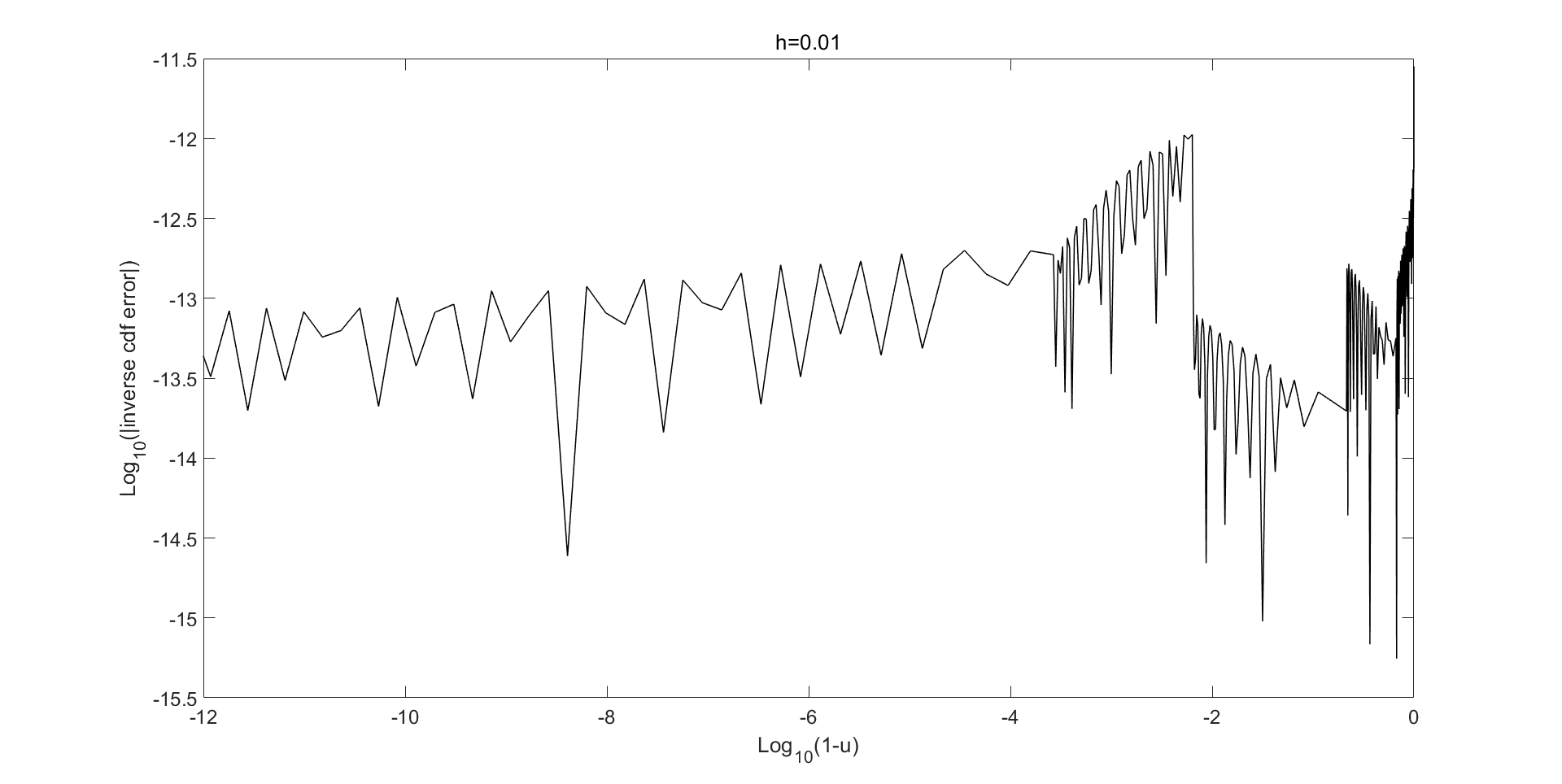

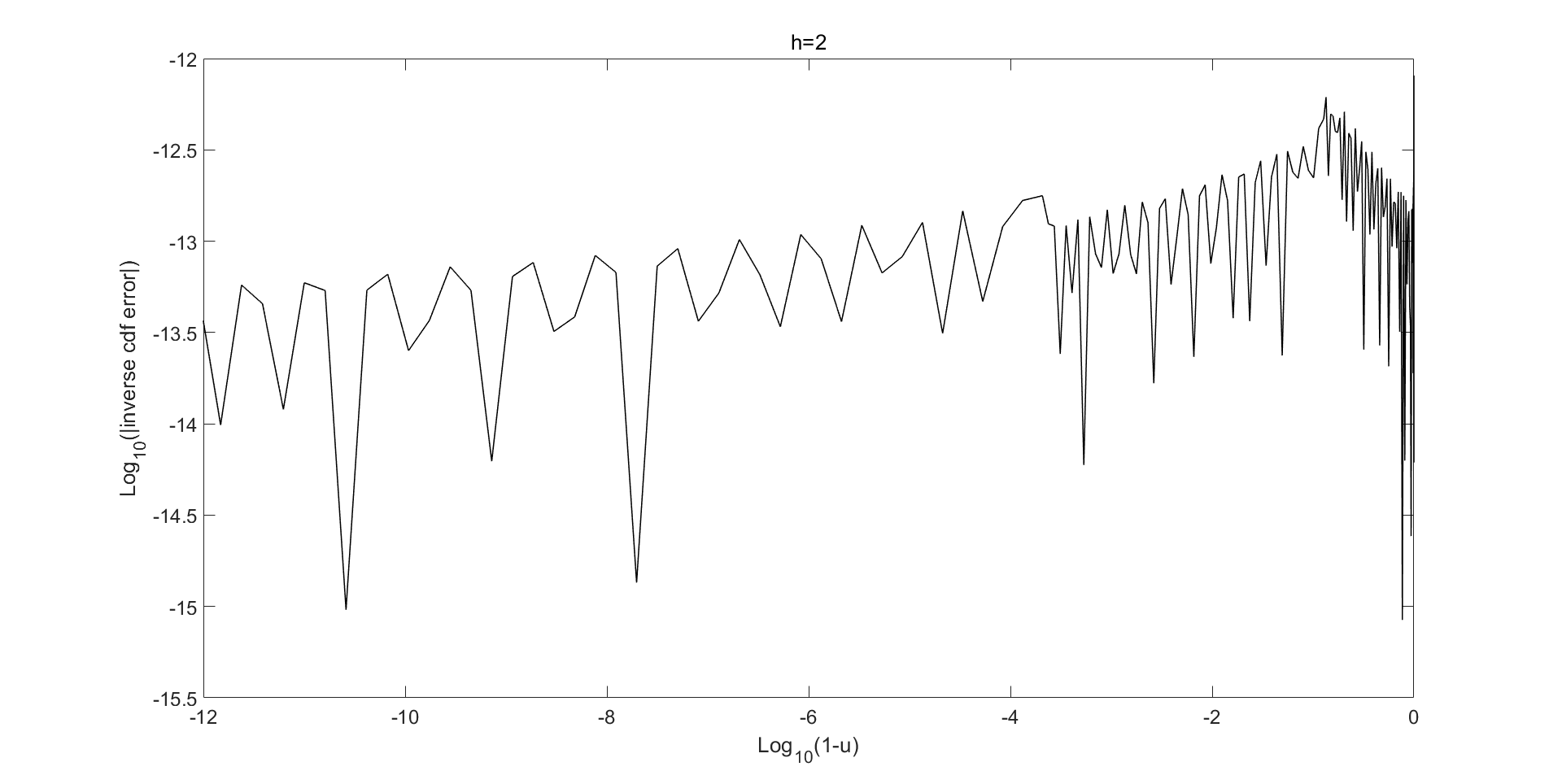

the values for the coefficients of which are presented in the supplementary materials. Fig.2 shows the errors in the approximation for by Chebyshev polynomials across all regimes when . Notice that under such circumstance, because of the heavy tail we further split the right tail region into two smaller regions where different Chebyshev polynomials are developed, making a total of five separate regions: , , , and with degrees , , , and , respectively. All errors are fluctuating at the level of . See Shen [36] for more results of the other cases.

As is a special case of when , the approach to generating samples of discussed above is fully applicable here. In fact, we directly construct the Chebyshev polynomial approximations for the inverse distribution function with since is independent of any parameters. We plot the resulting errors in Fig.3. The polynomials have degrees between and in the four regions with errors of order .

Table 1: Parameters for the Heston model.

Parameters

European

Path-dependent

Case

Case

Case

Case

Asian

Barrier

4 Numerical analysis

In this section, we compare our direct inversion method with the gamma expansion of Glasserman and Kim [18] by pricing four challenging European call options in the Heston model. The sets of parameters considered are given in Table1. These four sets are taken from Glasserman and Kim [18], which are found to be in the typical range of parameter values of the Heston model in practice. Two path-dependent options including an Asian option with yearly fixings (see Smith [37], Haastrecht and Pelsser [39] and Malham and Wiese [28]) and a digital double no touch barrier option (see Lord, Koekkoek and Van Dijk [27] and Malham and Wiese [28]) are also tested with parameter values shown in Table1.

4.1 Time integrated conditional variance

Before giving simulation results for option prices, we first illustrate the performance of the above direct inversion method in terms of accuracy based upon the series expansion given in Theorem2.1. Recall that our objective is to sample from the distribution of the random variable given its endpoints and , denoted by , i.e.

under the probability measure . We have decomposed the integral into the sum of three independent series after measure transformation. Among the realisation of those three series, the first one is truncated with tail approximated by a gamma random variable and the remaining two series are simulated exactly by direct inversion.

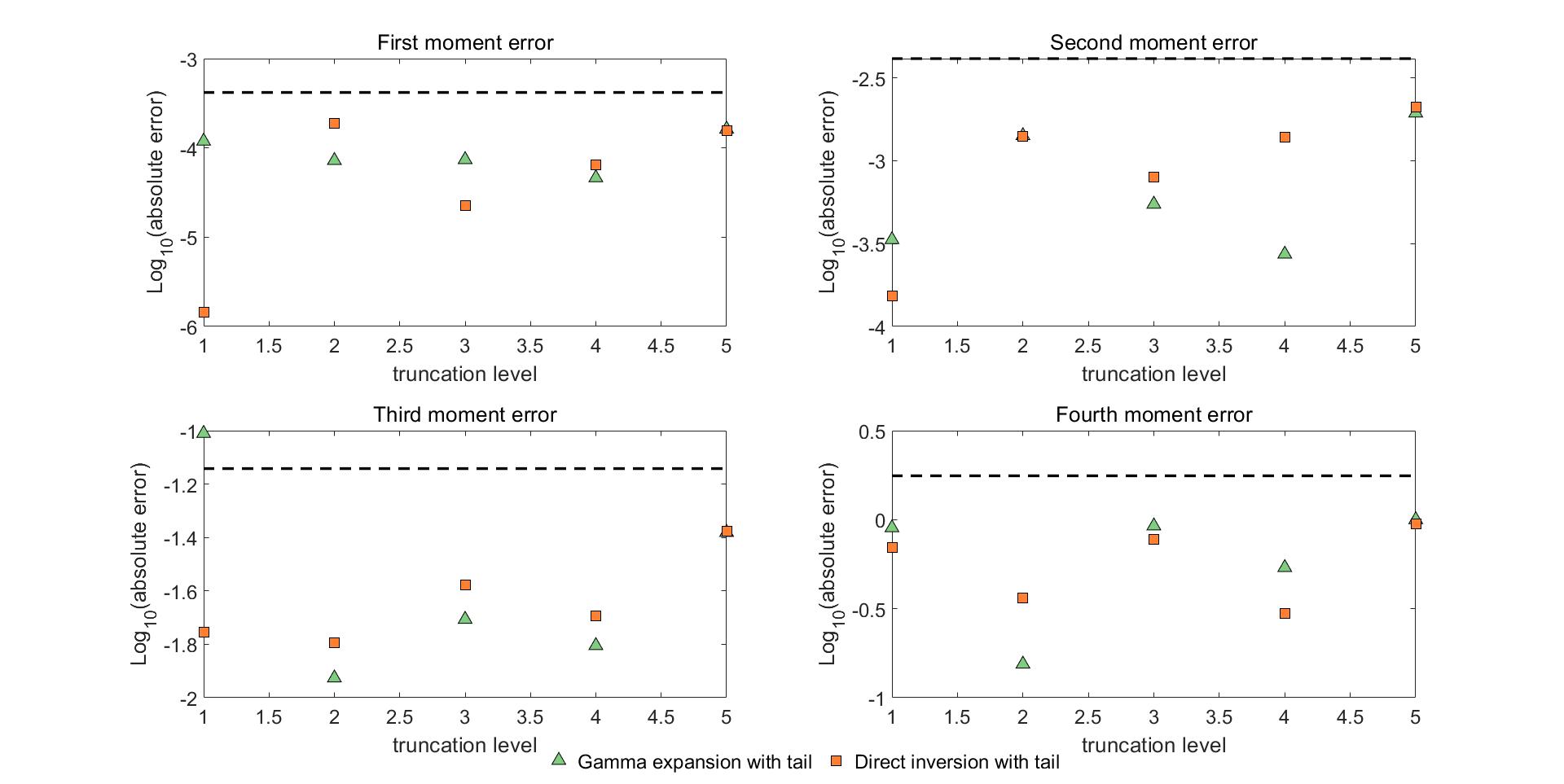

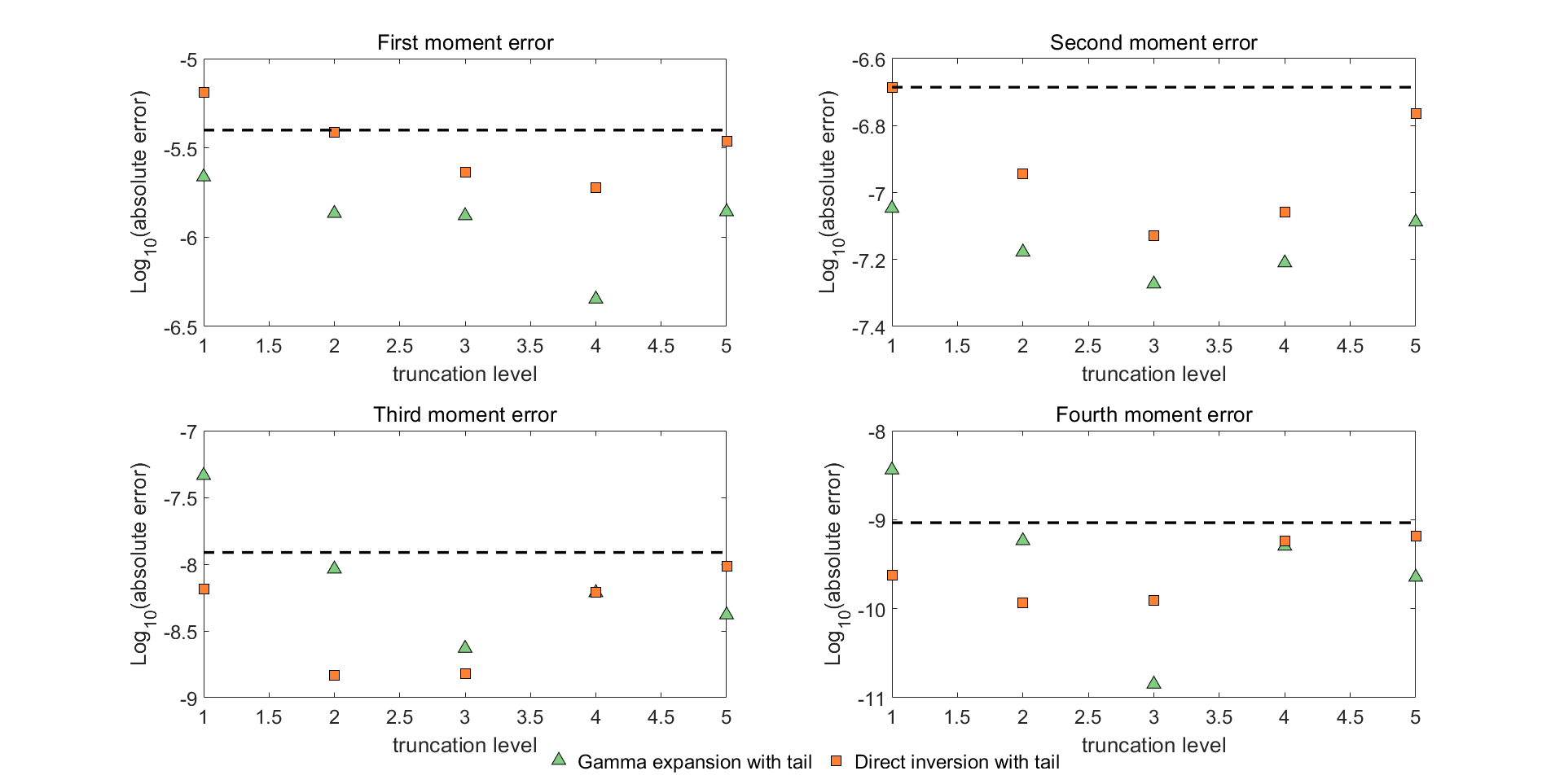

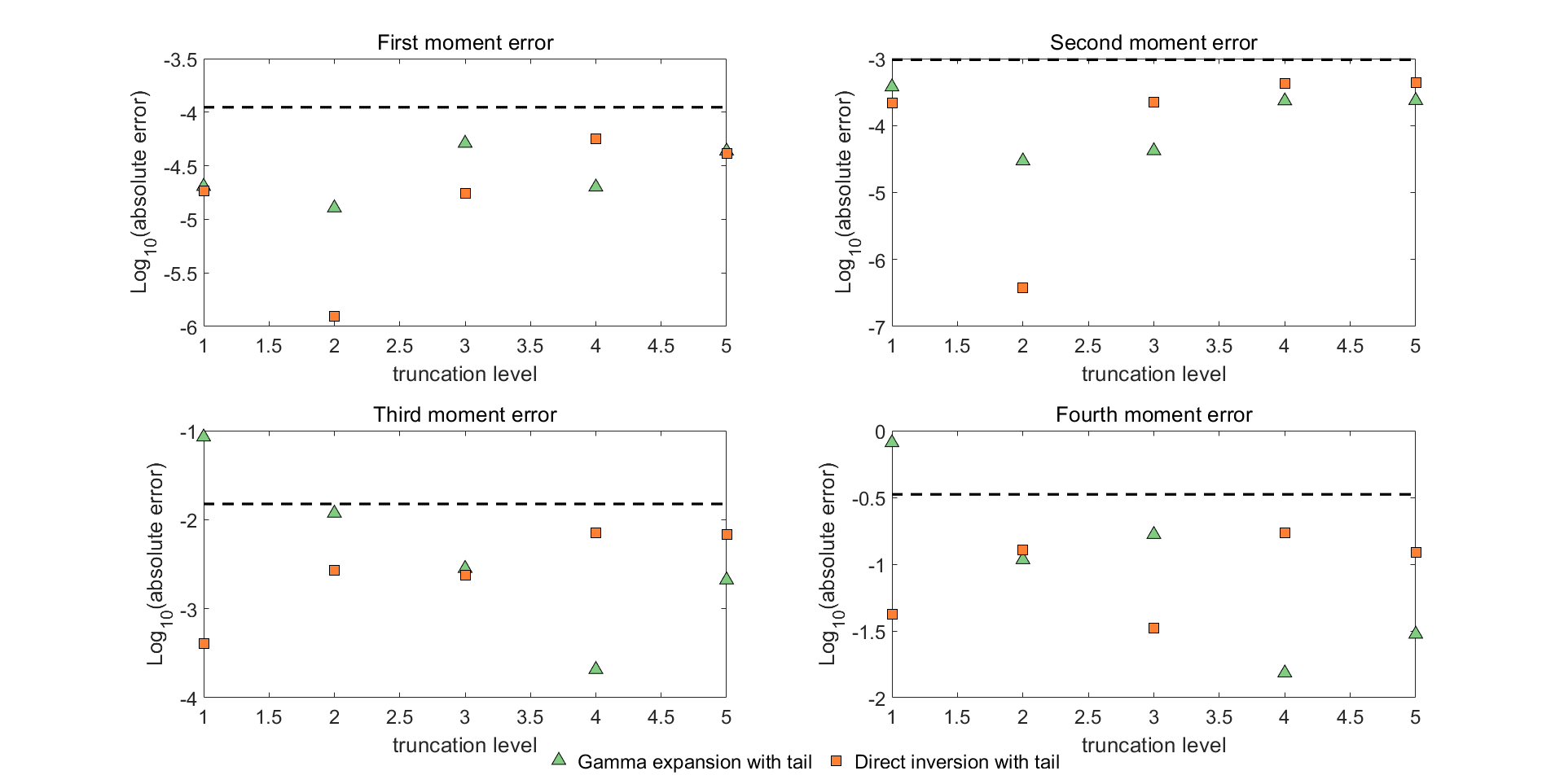

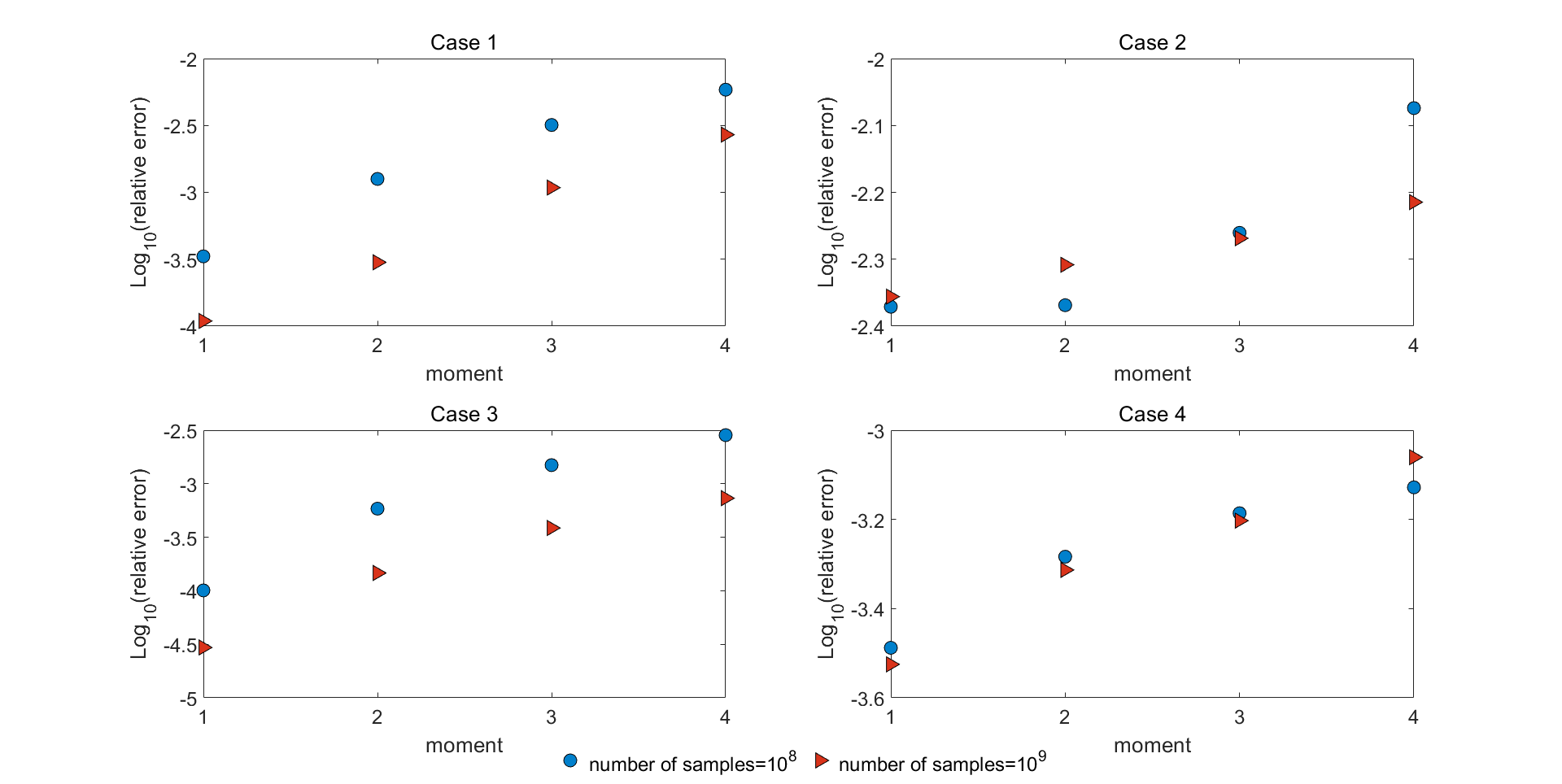

(a) Case : Figure 4: We indicate the absolute errors in the first four moments of the conditional integral simulated by direct inversion and gamma expansion versus the truncation levels for Case with different values for . Both methods are implemented with tail simulation. We perform simulations for each case. Below the dashed line, the errors are not statistically significant at the level of three standard deviations.

In Fig.4 and Fig.5 the absolute errors in the first four moments are displayed for simulating the conditional integral with different values of using our method. For comparison, we include the results by employing the gamma expansion from Glasserman and Kim [18] as well. For both methods, we apply tail approximations with truncation level increasing in integers. The number of samples generated in each case is . The three panels shown in Fig.4 from top to bottom correspond to the three representative values for Case and the panels in Fig.5 correspond to the three fixed values (top to bottom) for Case . Note that the true moments can be computed by evaluating the respective derivatives of the moment generating functions derived by Broadie and Kaya [12] at the origin.

(b) Case :

(c) Case :

Figure 4: (cont.) We indicate the absolute errors in the first four moments of the conditional integral simulated by direct inversion and gamma expansion versus the truncation levels for Case with different values for . Both methods are implemented with tail simulation. We perform simulations for each case. Below the dashed line, the errors are not statistically significant at the level of three standard deviations.

We observe that most errors for the first two moments across different values of and truncation levels for both Case and are not significantly different from zero at the level of three standard deviations, suggesting both methods achieve high accuracy for these two moments as expected. This is consistent with the theory as tail simulation in each method is designed such that the first two moments are matched. In other words, the simulations should lead to the exact first and second moments in principle, whence only Monte Carlo noise with a scaling as the inverse of the square root of the sample size, i.e. , is observed.

For the higher moments, the errors of the direct inversion are fluctuating at some level below the statistical significance for all circumstances considered. These errors are so small that a decreasing trend is not visible when increasing the truncation level. In contrast, with the increment of the truncation levels, the errors of the gamma expansion first exhibit a decaying pattern until the curves become horizontal. For example, the behaviour of the decreasing errors of the third and fourth moments is obvious when the truncation level is increased from one to two. The falling tendency appears to be more significant when we increase the sample size, thus, reduce the Monte Carlo effect, which will be discussed later. This suggests that there exists some bias in the gamma expansion with small truncation levels while the direct inversion with lower truncation levels has the same accuracy as that with higher ones.

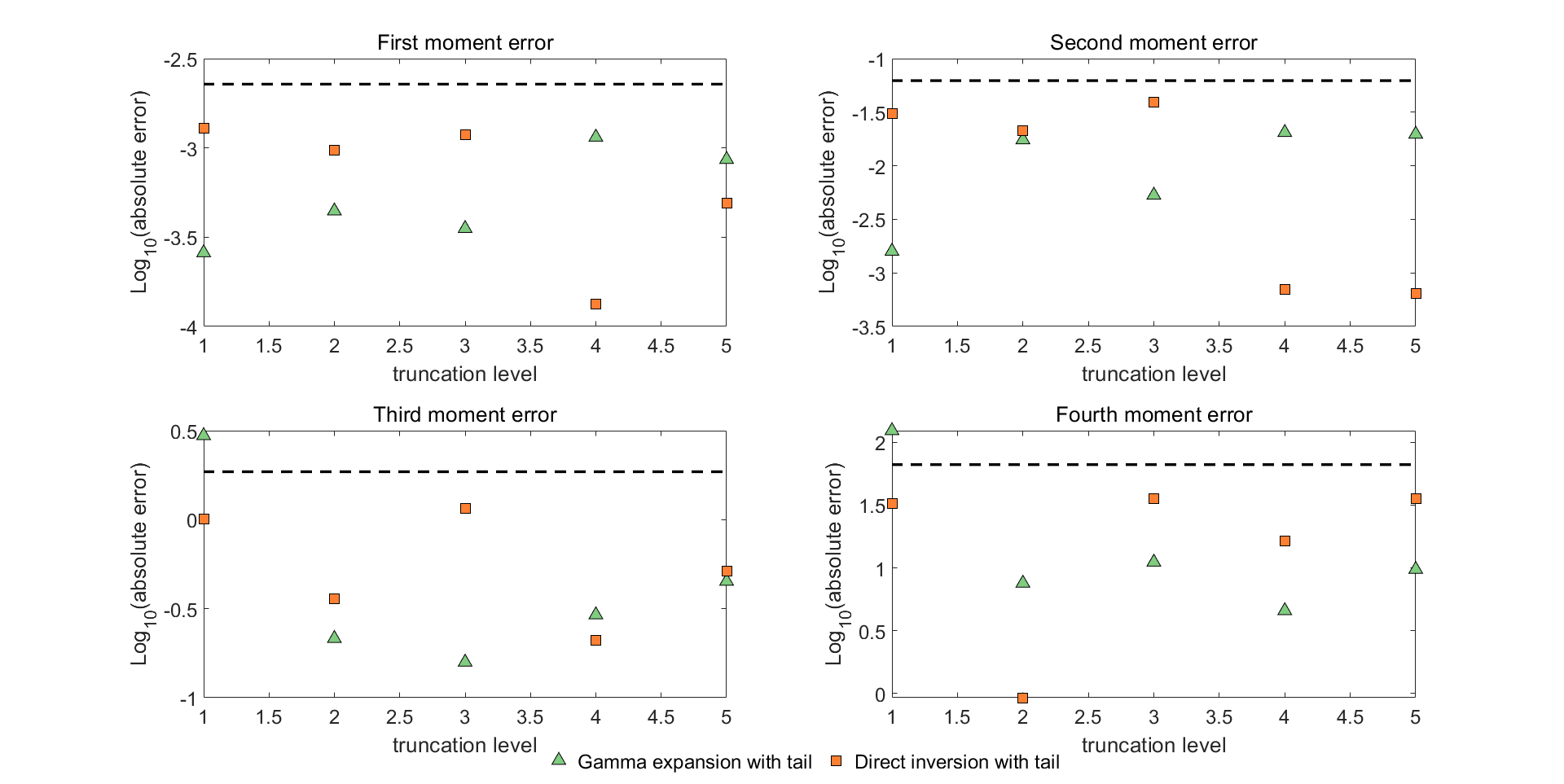

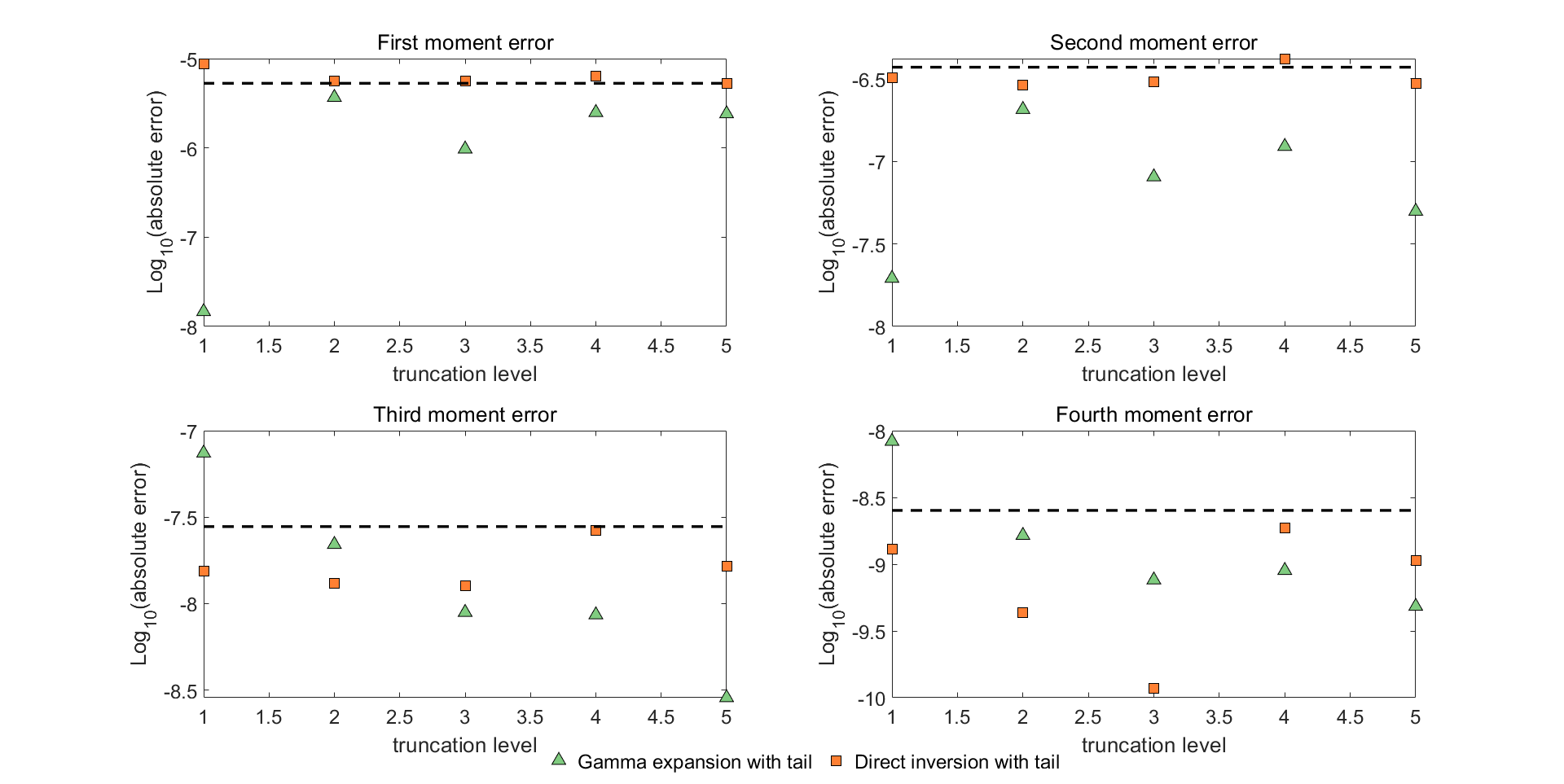

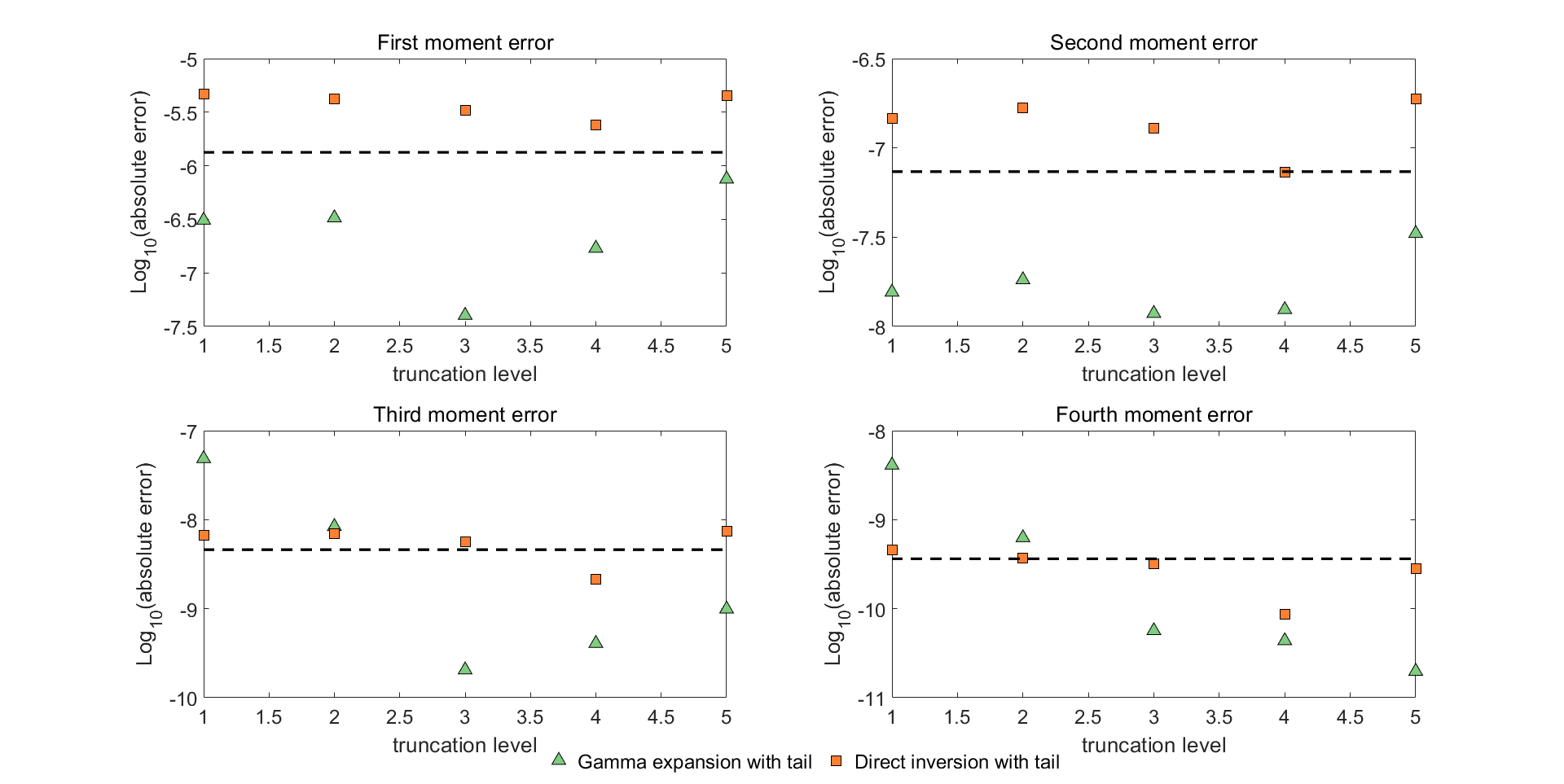

(a) Case : Figure 5: We indicate the absolute errors in the first four moments of the conditional integral simulated by direct inversion and gamma expansion versus the truncation levels for Case with different values for . Both methods are implemented with tail simulation. We perform simulations for each case. Below the dashed line, the errors are not statistically significant at the level of three standard deviations.

(b) Case :

(c) Case :

Figure 5: (cont.) We indicate the absolute errors in the first four moments of the conditional integral simulated by direct inversion and gamma expansion versus the truncation levels for Case with different values for . Both methods are implemented with tail simulation. We perform simulations for each case. Below the dashed line, the errors are not statistically significant at the level of three standard deviations.

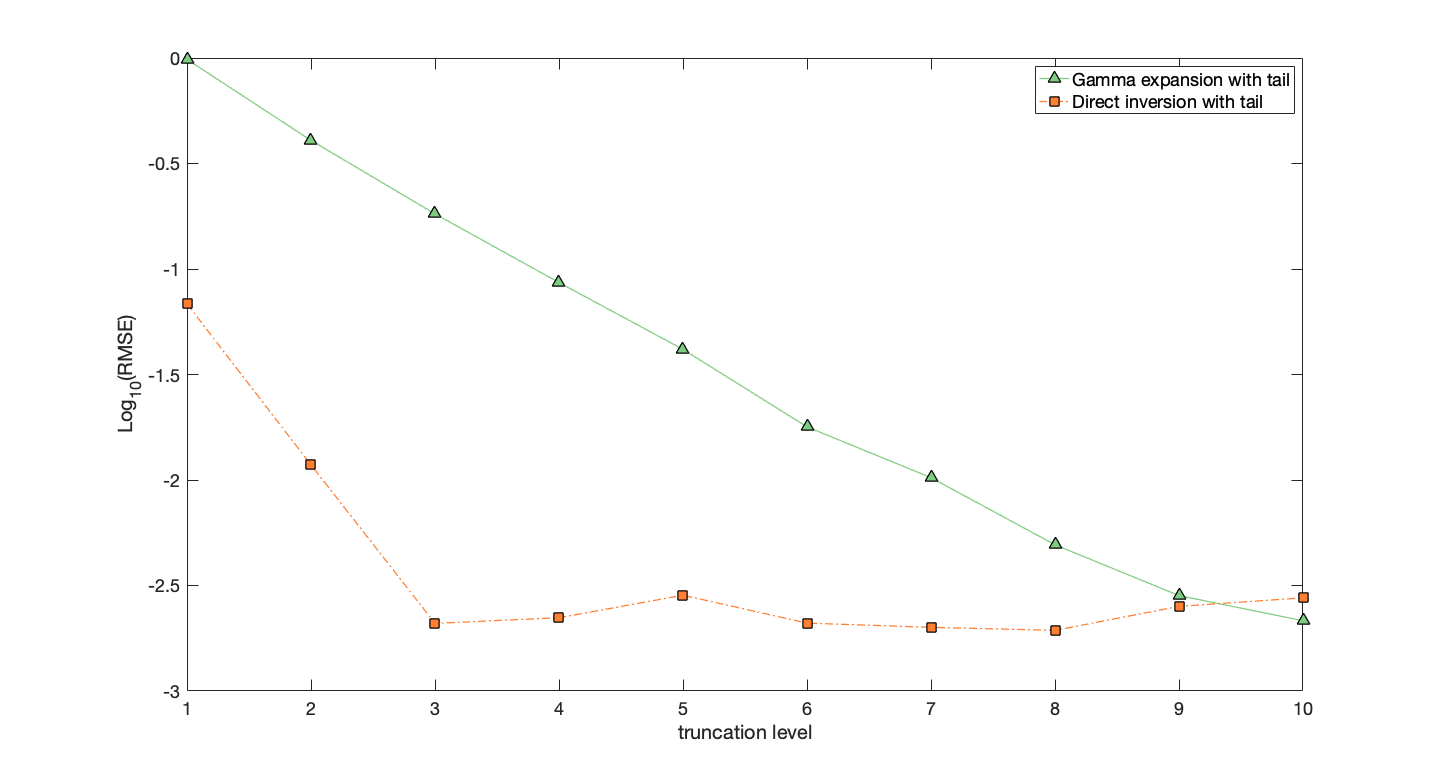

While the figures for Case and have many details in common, they also reveal noteworthy differences in the first two moments. As illustrated in the upper panels in Fig.5a, Fig.5b and Fig.5c for Case , most of the first and second moment errors in the direct inversion are slightly higher compared to those in the gamma expansion at the same truncation level. Errors of the two schemes considered in the first two moments for Case on the other hand seem to be of the same order to some extent with the same truncation level, which can be seen from the upper panels in Fig.4a, Fig.4b and Fig.4c. In order to find a plausible explanation for this difference, we increase the sample size by a factor of and plot the resulting errors versus the truncation levels in Fig.6 and Fig.7.

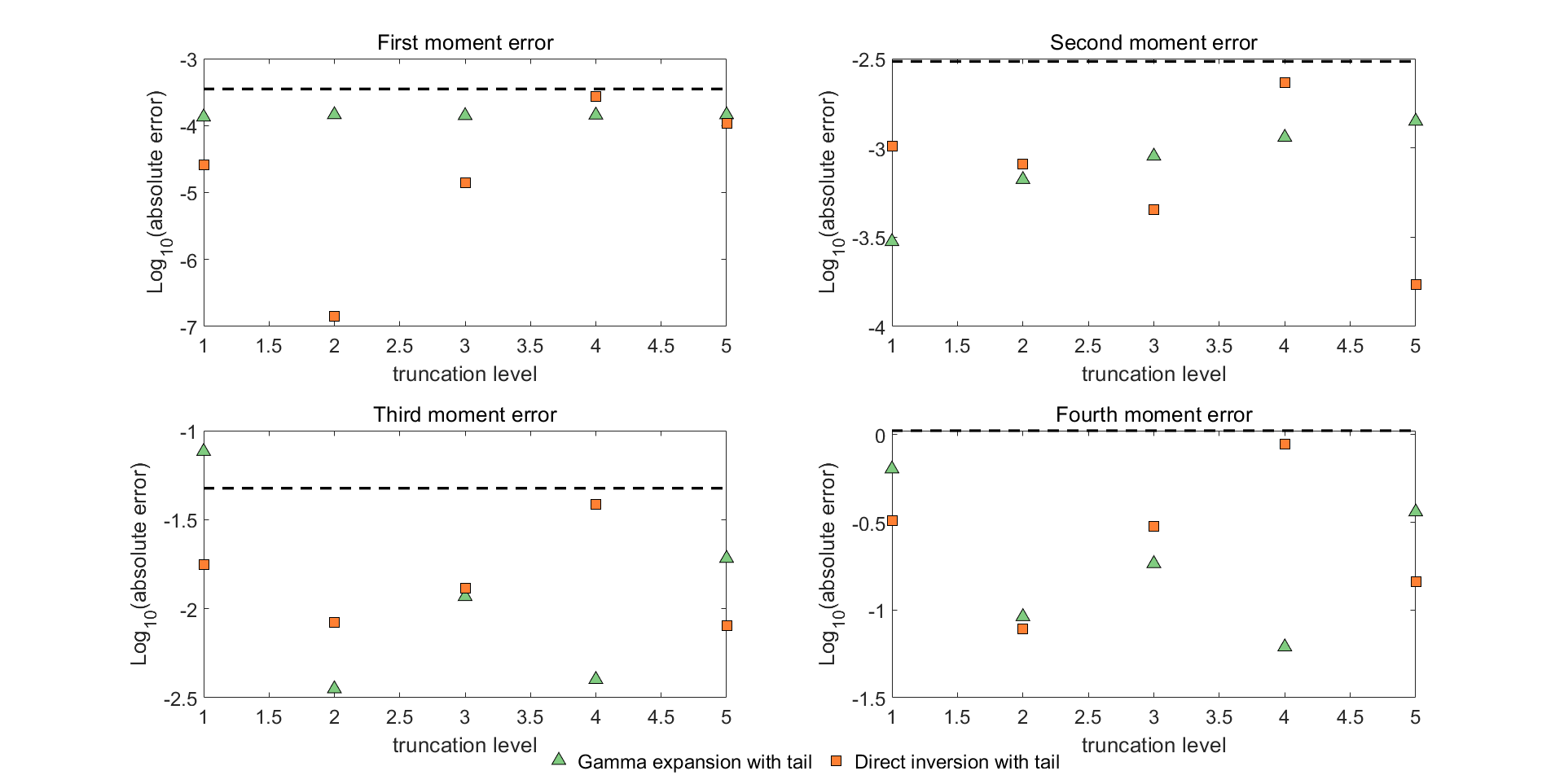

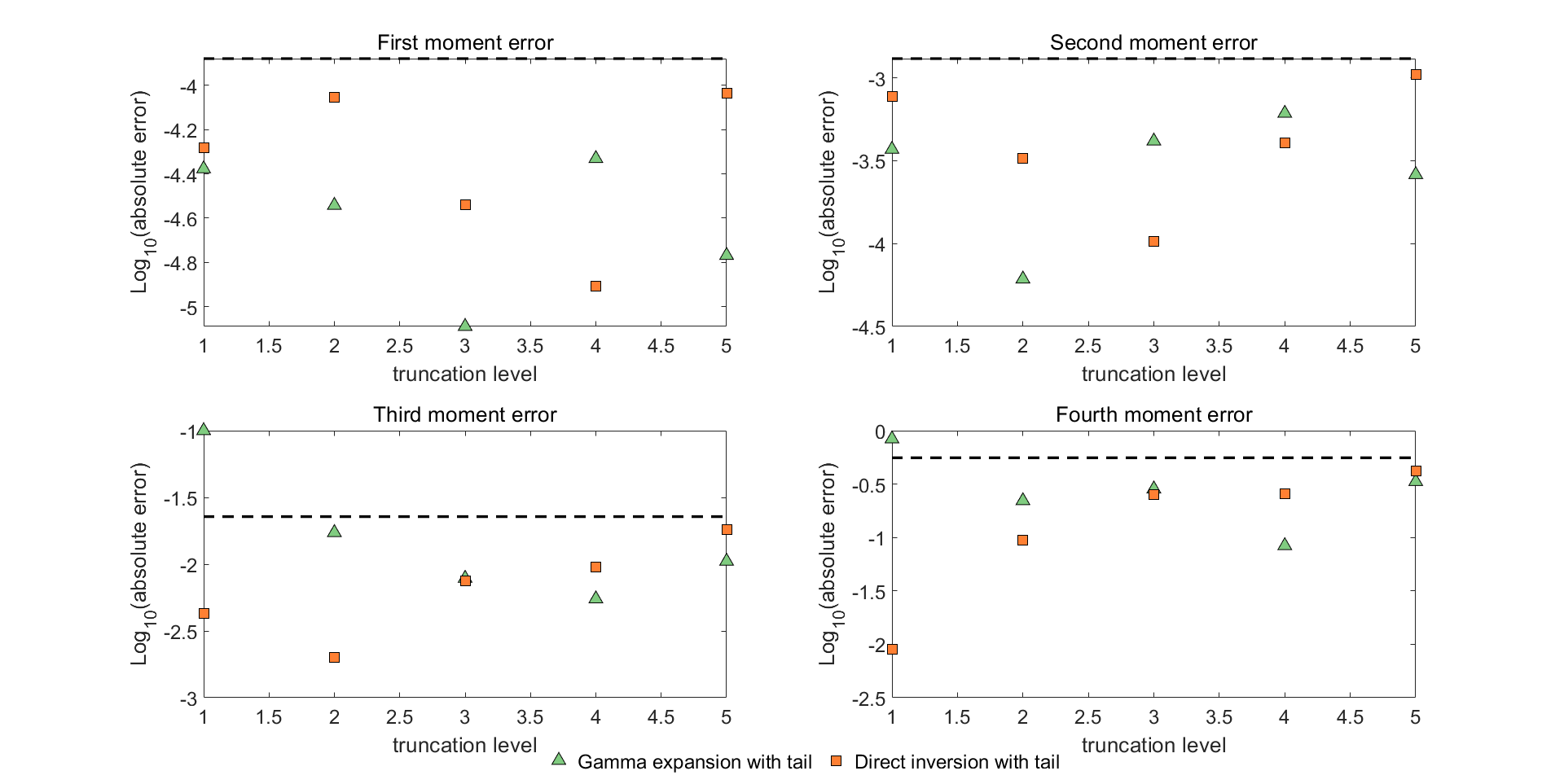

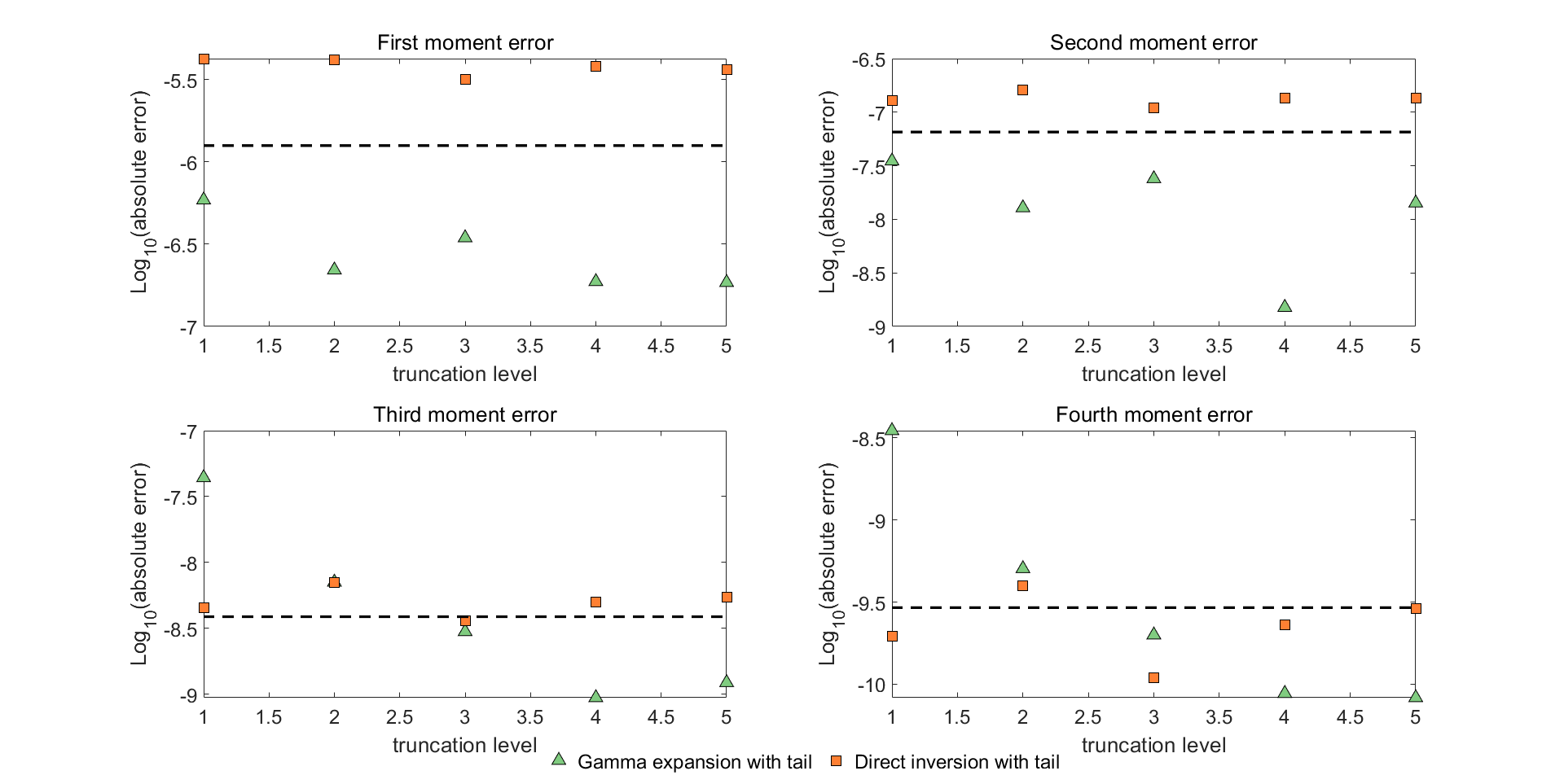

(a) Case :

(b) Case :

Figure 6: We indicate the absolute errors in the first four moments of the conditional integral simulated by direct inversion and gamma expansion versus the truncation levels for Case with different values for . Both methods are implemented with tail simulation. We perform simulations for each case. Below the dashed line, the errors are not statistically significant at the level of three standard deviations.(c) Case : Figure 6: (cont.) We indicate the absolute errors in the first four moments of the conditional integral simulated by direct inversion and gamma expansion versus the truncation levels for Case with different values for . Both methods are implemented with tail simulation. We perform simulations for each case. Below the dashed line, the errors are not statistically significant at the level of three standard deviations.

For Case , Fig.6 demonstrates the errors in all four moments based on the direct inversion are decreased as expected, i.e. proportional to the reciprocal of the square root of the sample size across all the values of and truncation levels. This confirms that the moment errors observed in Fig.4 using the direct inversion are dominated by the Monte Carlo error. On the other hand, for the gamma expansion we note in the upper panels of each subplots that the first two moments of the simulations for all five truncation levels are indeed matched with errors improving roughly according to the expected scaling when increasing the sample size. However, we see in the lower panels that the errors in the third and fourth moments hardly show any changes for lower truncation levels such as one and two while the accuracy for the other truncation levels is improved with the increase of the sample size. In fact, after reducing the Monte Carlo noise, there exists an even more clear decreasing trend for the higher order moment errors with the gamma expansion as the truncation level increases. This seems to corroborate the observations from Fig.4 for Case , indicating that the gamma expansion with small truncation levels exhibits some bias while the direct inversion achieves the same accuracy, restricted by the Monte Carlo error, for all truncation levels.

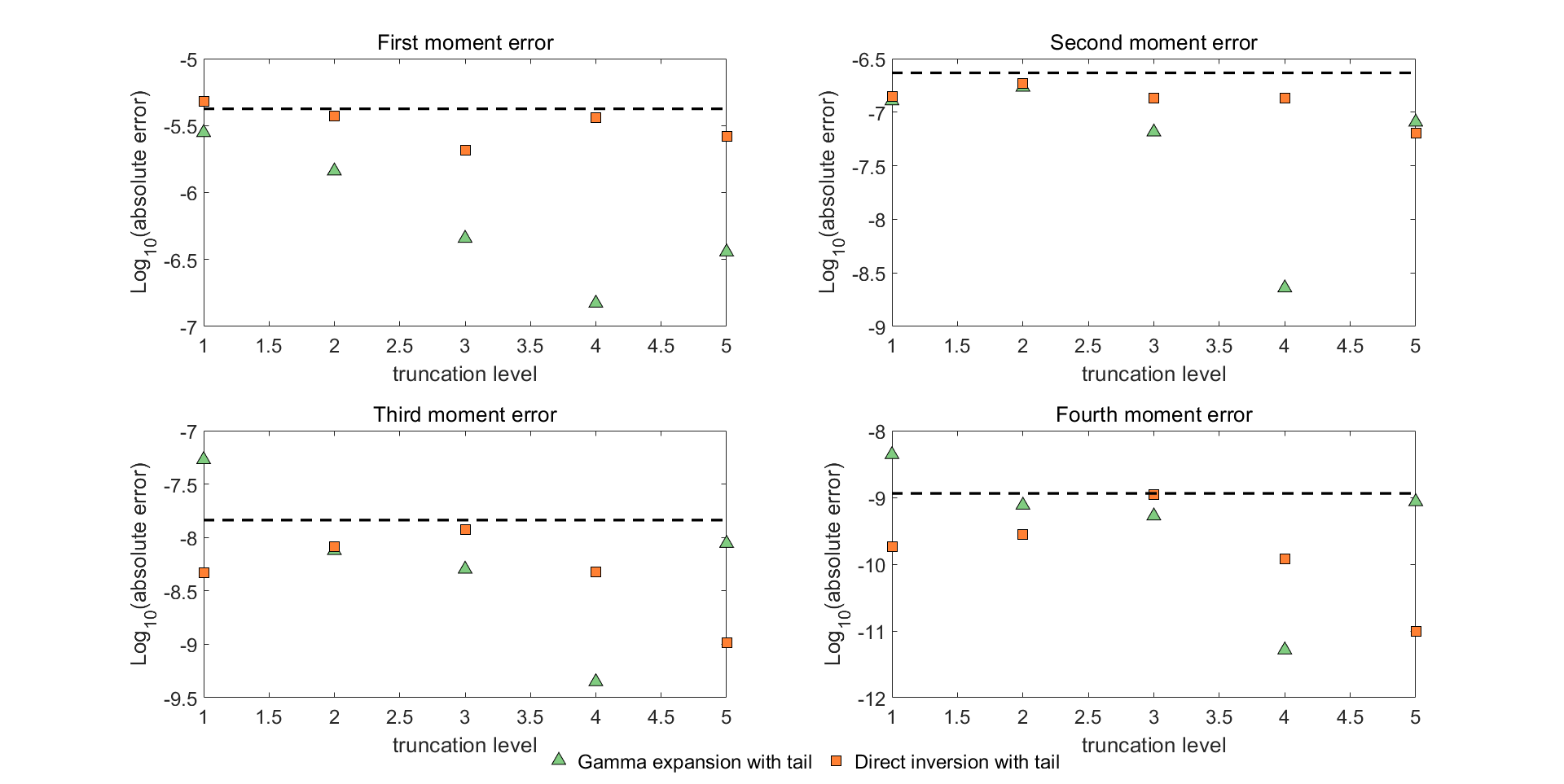

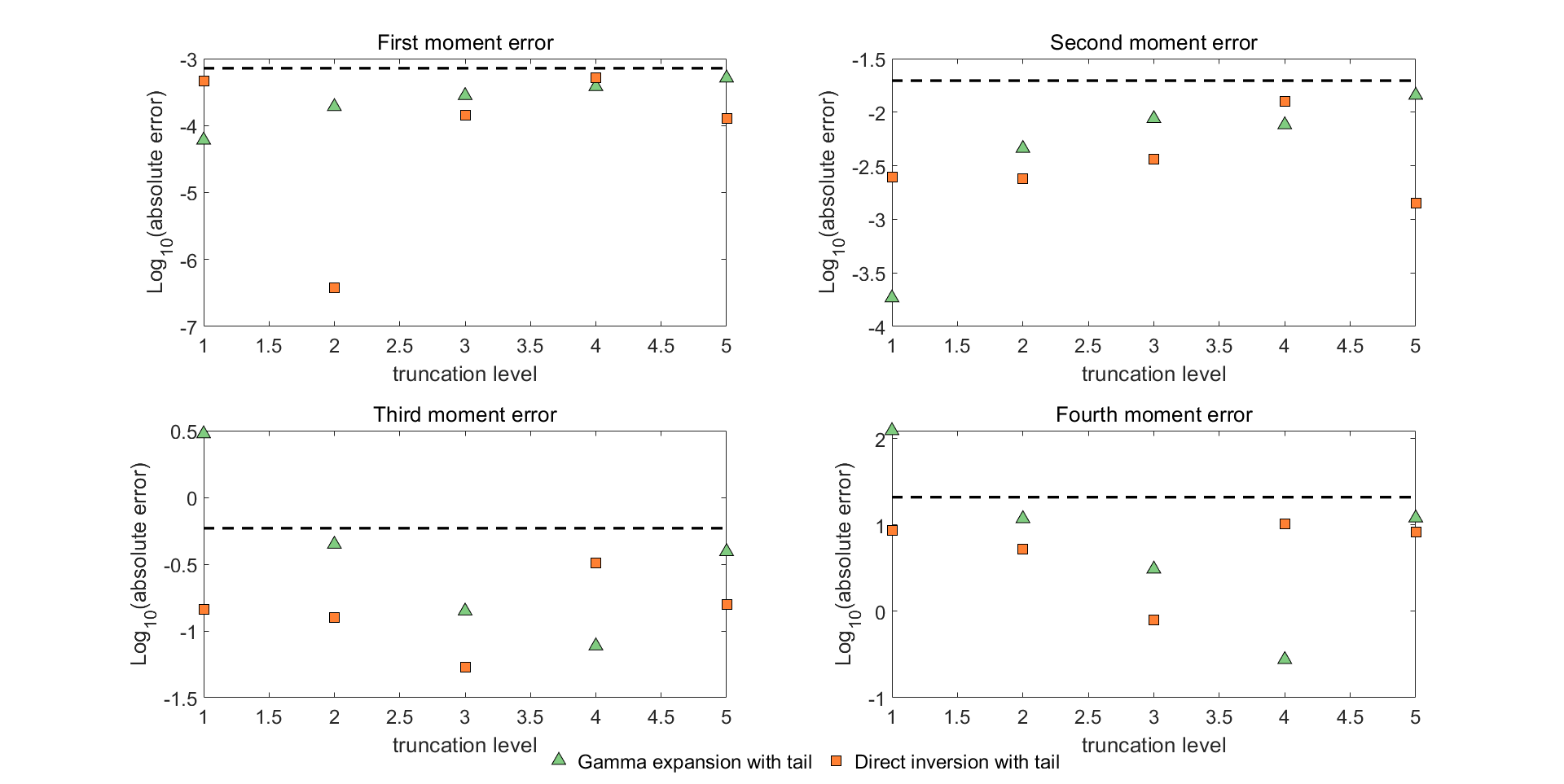

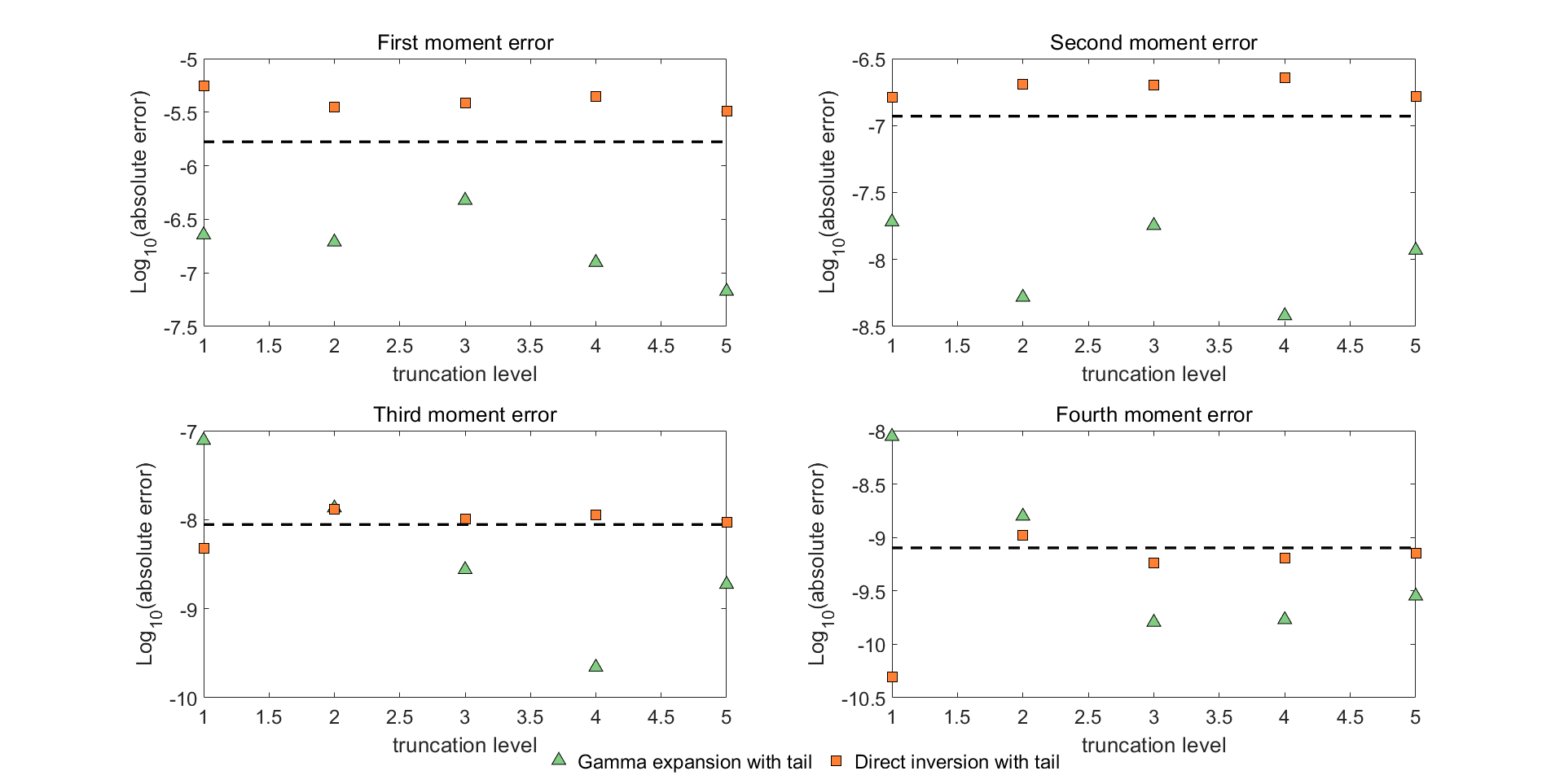

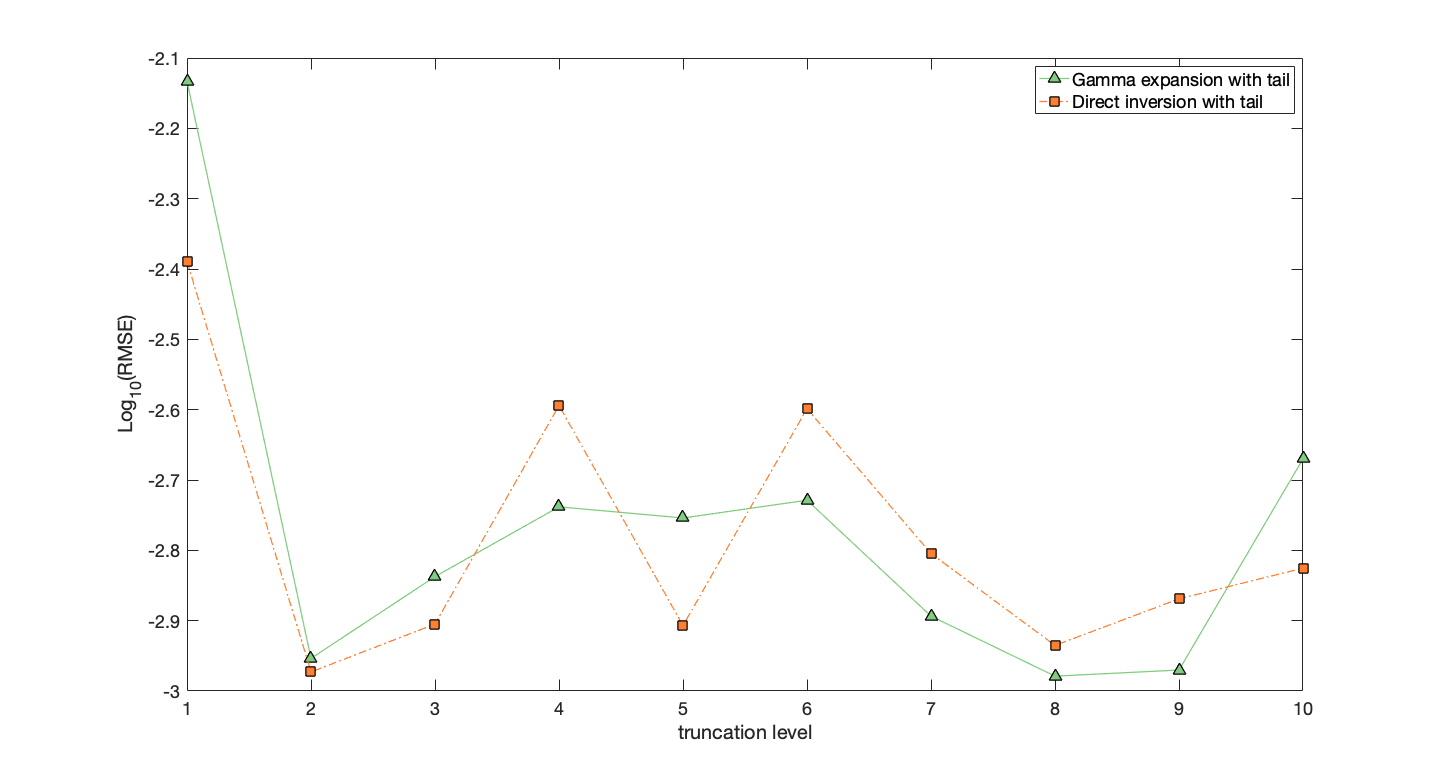

(a) Case : Figure 7: We indicate the absolute errors in the first four moments of the conditional integral simulated by direct inversion and gamma expansion versus the truncation levels for Case with different values for . Both methods are implemented with tail simulation. We perform simulations for each case. Below the dashed line, the errors are not statistically significant at the level of three standard deviations.

(b) Case :

(c) Case :

Figure 7: (cont.) We indicate the absolute errors in the first four moments of the conditional integral simulated by direct inversion and gamma expansion versus the truncation levels for Case with different values for . Both methods are implemented with tail simulation. We perform simulations for each case. Below the dashed line, the errors are not statistically significant at the level of three standard deviations.

In comparison, Fig.7 shows different behaviour for the errors related to the direct inversion for Case while similar conclusion can be reached for the gamma expansion as Case . More specifically, we notice that all moment errors in direct inversion sampling for Case are invariant to increasing the sample size when the truncation levels are fixed. Further we observe that the errors, all remaining steady across a set of different truncation levels, become statistically significant when the number of samples is increased, especially for the first and second moments. Thus, this implies in Case the direct inversion performs equally well for all truncation levels, nevertheless, the accuracy of which is overridden by some bias. We should not fail to mention that the bias is roughly of the same order as the Monte Carlo error with samples, whence it is not reflected in Fig.5. This accounts for the finding for Case that the first and second moment errors for the direct inversion are always slightly larger than those for gamma expansion, where only Monte Carlo error is in presence.

We give a possible explanation for this bias as follows.

The reason for the bias with the direct inversion method for Case lies in the arithmetic precision we use for the parameter , which is related to the random variable . Recall that the proposed decomposition requires the rational parameter is given as a decimal with three significant figures. Let stand for the rounded number and denote the approximation to by replacing with . Next, we give the exact errors in the first and second moments of . Directly computing the first two moments using the series which defines , we can write

Then, the corresponding relative errors are

The above equations shows a linear scaling of the moment errors of in terms of the discrepancy between the true value and the approximated value . Table2 quotes the values for and for all the four European cases. Note that for Case and accurate values of are used while the relative errors for Case and are of order and , respectively. In Fig.8 the panels show the relative errors in the first four moments of for Case to Case using and simulations. For Case and Case , by successively increasing the sample size the high accuracy for the first four moments of sampled by direct inversion Algorithm3 is indeed limited by the Monte Carlo error, which improves roughly according to the expected scale. However, the errors are invariant for Case and Case when increasing the sample size. For these two cases, the systematic Monte Carlo error is lower than the bias caused by replacing the true value with the approximated value . Hence, the errors reflected in Fig.8, dominated by the bias, fail to show improvement when the sample size is increased by a factor of .

Table 2: True value and rounded value .

Case

Case

Case

Case

Figure 8: We plot the relative errors in the first four moments of simulated by direct inversion Algorithm3 for Case to Case . By increasing the sample size by a factor of , we note that the accuracy in the moment errors is improved as expected for Case and Case . The four moment errors are invariant for Case and Case when increasing the sample size, suggesting possible bias in the direct inversion for these two cases.

Based on the above analysis, we conclude that the direct inversion method for exhibits some small bias when approximation of the parameter is adopted. This can conceivably lead to the bias of the general direct inversion scheme for the conditional integral . However, this bias has nothing to do with the development of the method, but is associated with the decomposition technique and the arithmetic precision involved. Without loss of generality, this method can be extended to allow for a finer decomposition

of the parameter given to any number of decimal places. In this sense, we expect that the accuracy available for this method will become more apparent.

4.2 Option price

In this section, we apply the direct inversion method and the gamma expansion to pricing four European call options and two path-dependent options including an Asian option and a barrier option. These two schemes are both based on the known conditional non-central chi-square distribution for the variance process and the conditional lognormal distribution for the asset price. We further compare the above two methods with the full truncation scheme of Lord, Koekkoek and Van Dijk [27], which is a time stepping method with asset price and variance simulated on discrete time grids. This type of equidistant discretization scheme for the one-dimensional CIR process has been shown to have an arbitrarily slow convergence rate in the strong sense in general; see Hefter and Jentzen [20]. Hence, developing other simulation methods becomes essential for practical purposes.

(a) Case

(b) Case

Figure 9: We show the root mean square error in the option price (strike ) versus the truncation level for Case and Case . We use a sample size of with truncation levels increasing in integers from to .

We first demonstrate the tradeoff between the truncation level and accuracy for the direct inversion scheme and the gamma expansion. Fig.9 plots the root mean square error for the price of an at the money European call option against the truncation level for Case and Case . For both methods, we use a sample size of and truncate after terms, increasing in integers from to . For Case , the direct inversion exhibits a faster convergence rate, revealed by the steeper slope in Fig.9a, in contrast with the gamma expansion. Indeed, truncation after three terms already provides a satisfactory estimator with error curve eventually becoming noisy in the larger regime. To obtain the same accuracy, many more terms up to are required for the gamma expansion. For Case , increasing from one to two indeed helps to reduce the error. However, further increase in does not seem to bring improvement to the error for both methods, as seen from the horizontal error curves with small fluctuations in Fig.9b. This implies that approximations with small are sufficient to achieve acceptable accuracy.

Remark 4.1.

Similar conclusions as Case can be reached for Case and Case with numerical results presented in Shen [36]. Simulations with different strikes for in the money and out of the money options for the above four test cases are also included there.

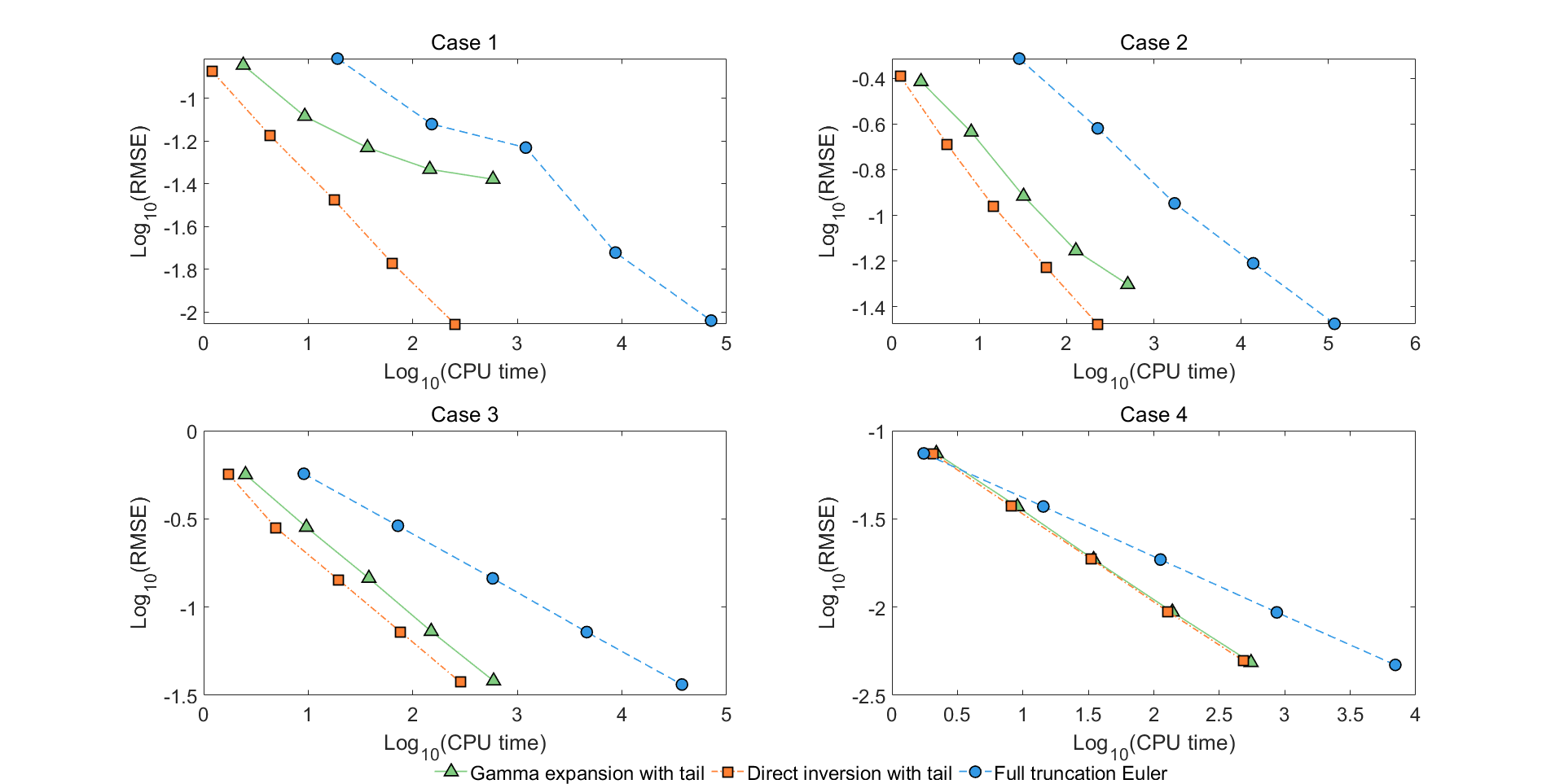

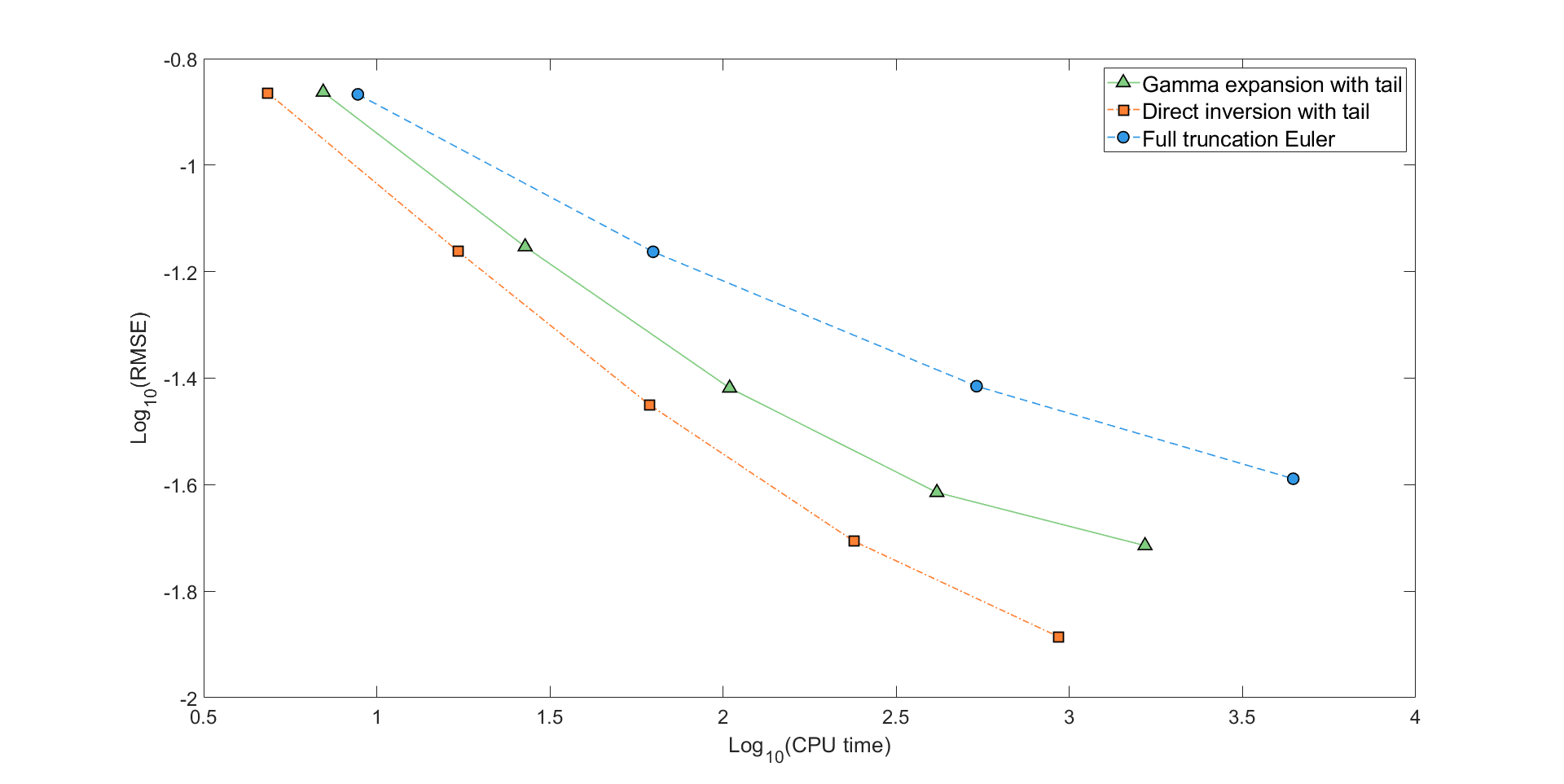

Figure 10: We show the convergence of the root mean square error in the option price (strike ) for Case to Case of gamma expansion and direction inversion, both at a truncation level , and full truncation Euler scheme, with number of time steps equal to the square root of the sample size.

Next, we give the comparisons between the direct inversion method, the gamma expansion and the full truncation Euler scheme. In Fig.10, we plot the root mean square error in the option price as a function of the CPU time required on a log-log10 scale for all schemes. For fair comparisons, we implement these three methods as efficiently as possible and generate the CPU time using compiled Matlab code. For the two non-discretization methods, we choose to use truncation level . For the full truncation Euler method, we set the number of time steps equal to the square root of the sample size. This is motivated by the optimal allocation for the number of time steps from Duffie and Glynn [14], which is proportional to the square root of the number of trials for methods with weak order of convergence being equal to one; see Broadie and Kaya [12] and Lord, Koekkoek and Van Dijk [27].

We can see from the upper panels in Fig.10 that the bias in the gamma expansion with for Case and Case eventually dominates the root mean square error when the number of sample trails increases. By comparison, the root mean square errors for the direct inversion and full truncation Euler scheme are declining monotonically, with the former presenting a more rapid rate with reduced computational cost. For Case and Case , the two non-discretization methods both outperform the full truncation Euler scheme, which has a slower convergence rate reflected by the less steeper slope in the graph.

With regard to the computing time, the gamma expansion is at least two to three times slower than the direct inversion with similar accuracy for Case , Case and Case . For Case , the new method takes much more time compared with Case . This is because more effort is needed for the acceptance-rejection sampling of Case due to the slightly unfavourable values for the model parameters. Although the time needed for the direct inversion is marginally more than the gamma expansion for Case with , as the desired accuracy is increased the new method requires less computational budget. In summary, we conclude that the performance of the direct inversion is the best among the three schemes considered here.

Now we turn to the pricing of options with payoffs depending on sample paths. We first consider an at the money Asian option with yearly fixings, the payoff of which is determined by the average of asset prices at the end of each year. We show in Fig.11 the root mean square error of the price versus the CPU time on a log-log10 scale. For the direct inversion and the gamma expansion, we truncate the series after and simulate the asset prices for each year. Within one year, the terminal value is obtained directly using a single step. For the time discretization scheme, multiple steps are needed for each year. In this test, the number of time steps is taken to be the square root of the sample size in a similar manner to Broadie and Kaya [12] and Smith [37].

Figure 11: We show the convergence of the root mean square error in the option price (strike ) for the Asian option of gamma expansion and direction inversion, both at a truncation level , and full truncation Euler scheme, with number of time steps equal to the square root of the sample size.

Table 3: Estimated prices with standard errors and CPU time for the barrier option.

Stepsize

Direct inversion

Gamma expansion

Estimated price

Standard error

CPU time

Estimated price

Standard error

CPU time

Estimated price

Standard error

CPU time

Estimated price

Standard error

CPU time

Estimated price

Standard error

CPU time

Estimated price

Standard error

CPU time

Estimated price

Standard error

CPU time

Estimated price

Standard error

CPU time

We observe that both the gamma expansion and the direct inversion, even with a lower truncation level, deliver similar accuracy compared to the full truncation scheme for small sample sizes. However when the number of simulations increases, bias of the estimated price starts to dominate the root mean square error for all three methods with the standard deviation decreasing according to the expected scaling, i.e. the inverse of the square root of the sample size. This dominance by the bias eventually decelerates the decrease of the root mean square error. Among the above three methods, the direct inversion produces the smallest bias. In terms of the computing time, very similar conclusions can be drawn as the European option cases. For similar accuracy, the direct inversion is approximately to times faster than the gamma expansion. The time required by the full truncation Euler scheme is by far the largest.

We end this section with a test for pricing a digital double no touch barrier option. The payoff for such an option is either one or zero unit of currency depending on whether the barriers have been crossed. In Table3, we report the estimated price and standard error together with the CPU time of the direct inversion and the gamma expansion at truncation level for a double no touch barrier option with barriers and . We sample a total of paths for each case. We increase the number of time steps per year from to and monitor at each time step if the asset price has hit one of the two barriers.

We see from Table3 that as we decrease the stepsize, the estimated price of both the direct inversion and the gamma expansion is decreasing monotonically. This is in accordance with our expectation since when more dates are being monitored, there are more chances for the asset price to cross the barriers. Because of the nature of these two methods, we expect their estimated price will eventually be almost exact with negligible truncation errors when the asset price is monitored on a more frequent basis, for instance, every trading day. The results here are also consistent with those of the four schemes tested in Malham and Wiese [28, Table ] and the PT, FT and ABR scheme in Lord, Koekkoek and Van Dijk [27, Table ] in terms of accuracy. Similar conclusions can be reached as the cases for European and Asian options in terms of the computational time. The time required for the gamma expansion is to times more than the direct inversion.

5 Conclusion

In this paper, we have designed a new series expansion for the time integrated variance process under the Heston stochastic volatility model. Our expansion is built on a change of measure argument and the decomposition techniques for the integral of squared Bessel bridges by Pitman and Yor [32] and Glasserman and Kim [18]. Acceptance-rejection and direct inversion methods are developed to realise the conditional integral. On combining this result with the method of Broadie and Kaya [12], almost exact simulations of the stock price and variance can be generated on the basis of their exact distributions. We compare our approach with Glasserman and Kim [18] through pricing four practical and challenging options. Apart from that, two path-dependent options including an Asian option and a barrier option are also tested using the above two methods. Further comparisons with a standard time discretization method, i.e. the full truncation Euler scheme, are performed as well. Evidence implies faster computational speed with comparable error in our method.

The series representation and sampling techniques above can also be transferred to the generalised squared Ornstein-Uhlenbeck process with parameters and given by

where denotes a standard Brownian motion. Although in this paper we focus only on the case , the present result can be applied to other cases . In essence we need to find an appropriate decomposition for and hence establish efficient Chebyshev polynomial approximations required for the resulting direct inversion algorithm. The expansions derived in Section3 will be helpful in determining the coefficients.

Lastly, we recommend a direction for future research. Our method entails an acceptance-rejection algorithm with acceptance probability depending on model parameters. Thus, it is difficult to measure its general computational complexity, i.e. the average number of iterations needed. Besides, in the application of risk management and trading, the acceptance-rejection scheme is less favourable as it will introduce considerable Monte Carlo noise in sensitivity analysis. For these reasons, an alternative should be considered. One realistic way to avoid the use of acceptance-rejection is to sample the Radon-Nikodým derivative directly under the new probability measure instead.

For the remainder , as stated in Theorem2.1, the are independent and identically distributed random variables and the are independent Poisson random variables with mean . Taking the expectation of directly, we have

where the last identity holds since

and

. Similarly, we can compute

where we use the formulae and .

For the remainder , similar to the calculations for the moments of , we find

Note that the last step is a direct result of and . Further we can proceed with the computation of the variance:

We use the method of steepest descents to find the limiting behaviour as of the probability density function of the standardised random variable given by

(26)

where and

The complex logarithm is chosen to be the principal branch. Note that the support of is and hence we focus on the case when .

We are interested in the saddle point such that . Before that, let

which gives

We observe and are analytic when after defining and .

Bleistein and Handelsman [10, Chapter ] suggest that we should seek a saddle point near , which will be the dominant one. To obtain an explicit form for the saddle point, we take advantage of the series expansions of and its differentiation . Let us first consider the series expansion of about , which is of the form

(27)

where

(28)

and so forth. Although we can compute the coefficients analytically through Taylor expansion of up to any order, we compute them using Maple in practice. Hence, its differentiation can be expressed as

The above two series converge pointwise in the domain where . It seems that a precise form for the saddle point such that is not obtainable. However, we can get a good approximation by making use of the smallness of . For , i.e. , we solve the above equation by iteration. In fact, after two iterations, we have the following expression for the desired saddle point

We show in AppendixF that the saddle point exists and is unique in the domain of analyticity of , i.e. for any , i.e. . Further since is analytic in this region, we can show the solution is also analytic around by the analytic implicit function theorem and thus has a Taylor series expansion about valid for sufficiently small . Hence we can write

(29)

for sufficiently small , where

(30)

and so on. Again, all these coefficients are calculated via Maple in practice. Notice that the saddle point is near the origin and along the imaginary axis.

Now, we can expand as a Taylor series near the saddle point

(31)

which converges in a neighbourhood of . For preparations, we must evaluate for at . Differentiating the series expansion for in equation Eq.27 leads to

for , where

(32)

for . This series converges in the same domain as the expansion for ; see equation Eq.27. To substitute the Taylor series Eq.29 regarding the saddle point into the above equation, we require to be within its radius of convergence, i.e. . Hence we restrict such that (see RemarkF.4). By noting that

(33)

for , where

(34)

we get that for ,

(35)

for and sufficiently small, where

(36)

for .

With the completion of the foregoing, we are now ready to determine the paths of steepest descent through given by

The condition determining the paths of steepest descent just above, with an error , is given by

(37)

Direct computation reveals that

If we set for , then Eq.37 implies that the paths of steepest descent and ascent from lie along the curves

as is purely imaginary. These paths, close enough to the saddle point , that is when is small, consist of the straight lines and . To distinguish between the ascent and descent paths, we consider along the two lines near . Along , we have

when is near . Along , we have

for close enough to . Thus, the path of steepest descents from is , parallel to the real axis.

As is in the domain of analyticity of , we can deform the original contour of the integration Eq.26 onto the steepest descent paths through the saddle point , denoted by for and for , both pointing a direction away from . It follows from Cauchy’s theorem that

whence the main contributions to the asymptotic expansion of the integral now comes from a small neighbourhood of for large . We use Laplace’s method to evaluate this integral. For some , we have the following asymptotic relation:

(38)

where by replacing the contour of integration with a narrow interval centred around , only exponentially small errors are introduced for large . Now, can be chosen so small that we can replace by its Taylor expansion Eq.31, which converges on the interval . Then, separating the quadratic term from all the higher-order terms of the series expansion Eq.31 in and setting

for any . From this it follows that for any there is an interval for some , in which

Therefore for any , we have

Then as , we can write

which gives

for small . Now the above integrals can be evaluated by change of variables. For arbitrary , the substitution yields

where the last step is a result of the change of variable . Thus as , we have

Similar arguments give us that

as .

Hence, the integration in Eq.40 can be expanded in an asymptotic series for small as follows: