Invariant states of hydrodynamic limits of randomized load balancing networks

Abstract

Randomized load-balancing algorithms play an important role in improving performance in large-scale networks at relatively low computational cost. A common model of such a system is a network of parallel queues in which incoming jobs with independent and identically distributed service times are routed on arrival using the join-the-shortest-of--queues routing algorithm. Under fairly general conditions, it was shown by Aghajani and Ramanan that as , the state dynamics converges to the unique solution of a countable system of coupled deterministic measure-valued equations called the hydrodynamic equations. In this article, a characterization of invariant states of these hydrodynamic equations is obtained and, when , used to construct a numerical algorithm to compute the queue length distribution and mean virtual waiting time in the invariant state. Additionally, it is also shown that under a suitable tail condition on the service distribution, the queue length distribution of the invariant state exhibits a doubly exponential tail decay, thus demonstrating a vast improvement in performance over the case , which corresponds to random routing, when the tail decay could even be polynomial. Furthermore, numerical evidence is provided to support the conjecture that the invariant state is the limit of the steady-state distributions of the -server models. The proof methodology, which entails analysis of a coupled system of measure-valued equations, can potentially be applied to other many-server systems with general service distributions, where measure-valued representations are useful.

Key Words. load balancing; power of two choices; stochastic network; many-server queue; fluid limit; hydrodynamic limit; measure-valued processes; randomized algorithms; invariant state; equilibrium distribution; cloud computing

1 Introduction

1.1 Background and Motivation

Randomized load balancing is an effective method that is used to improve performance in large scale networks while incurring relatively low communication overhead and computation costs. The model considered here consists of a parallel network of servers, to which jobs with independent and identically distributed (i.i.d.) service times arrive according to a renewal process with rate . Upon arrival of a job, out of the servers are chosen independently and uniformly at random, and the job is routed to the server with the shortest queue, with ties broken uniformly at random. Each server processes jobs from its queue in a first-come first-serve (FCFS) manner and jobs leave the system on completion of service. A server never idles when there is a job in its queue. The arrival process and service times are assumed to be mutually independent, and service times of jobs have finite mean which, without loss of generality, is taken to be one. The system described above will be referred to as the model.

This model was first introduced and analyzed in the case of Poisson arrivals and exponential service distributions by Vvedenskaya et al. [23] and Mitzenmacher [18]. They introduced a countable state representation of the process consisting of the fraction of queues with length greater than for each integer and showed that as , the state converges to a fluid limit, characterized as the unique solution to a countable system of coupled ordinary differential equations (ODEs). Under the stability condition , for they also obtained an analytical expression for the the unique invariant state of the fluid limit, and showed that it exhibits a doubly exponential decay. It was also shown in [23] that the stationary distributions of the -server systems converge to this invariant state, in the limit as . On the other hand, when , the stationary queue length distribution is the same as that for an M/M/1 queue, which is well known to exhibit just an exponential tail decay. Thus, the works [23, 18] uncovered the remarkable property that a dramatic improvement in performance can be achieved by introducing just a little bit of randomness into the system (i.e., even when ), a phenomenon that has been dubbed “the power of two choices.” A variant of this model that has received much attention recently is when the grows with , but in this article we focus on the case when is fixed and does not grow with . This involves a very different analysis, entailing a comparison with a system subject to join the shortest queue (JSQ) routing. In this article we focus on the case when is fixed and does not grow with , which is particularly relevant in many models where the cost of polling multiple servers is very high.

Until recently, most work on this model and its variants had focused on exponential service times. An extension to phase-type service distributions was first considered by Li and Lui [16], who analyzed the invariant states of a formal fluid limit. More general service distributions were then considered in a series of works by Bramson, Lu and Prabhakar [5, 6, 7, 8]. Under very broad assumptions and more general routing schemes, it was first shown in [5] that under the subcriticality condition , each -server system is ergodic with a unique stationary distribution. The works [6, 7, 8] specialize to the SQ() model with Poisson arrivals and service distributions with decreasing hazard rate, and directly establish convergence of the -server steady-state distributions without first establishing a fluid limit. In particular, when , it is shown in [7, Theorem 2.2] that the -server stationary queue length distribution converges to the unique solution of a fixed point equation, and this equation is analyzed to show that for power law distributions with exponent , the limiting stationary distribution has a doubly exponential tail if and a power law tail if . However, many realistic service distributions are neither exponential nor phase-type, and may not have a decreasing hazard rate. For example, statistical analyses suggest that service times follow a log-normal distribution in [9], a Gamma distribution in Automatic Teller Machines [15], or a shifted exponential distribution in [10, 17]. While an analogous result iis conjectured to hold for a larger class of service diistributions, this precise class has not been identified and, moreover, according to the authors of [7], it would be challenging to extend their approach beyond service distributions with decreasing hazard rate (see [7, Paragraph 9, Section 1]).

This motivates taking a different approach to analyzing the equilibrium behavior of randomized load balancing with general service distributions than that adopted in [6, 7, 8]. In this article, we consider the approach of first establishing a fluid limit that characterizes the limiting dynamics of the -server system, as , and then showing that the -server stationary distributions converge to the unique invariant state of the fluid limit. This approach has proved fruitful for many network models that admit simple Markovian representations, including (as mentioned above), the SQ() model with exponential service distributions (see [23]). However, in the case of general service distributions, each of the steps are significantly more challenging due to the fact that the dynamics are more compliciated, and there is no common finite or countable-dimensional Markovian representation for all -server systems. However, for a broad class of service distributions, recent work of [3] used a convenient state representation in terms of a coupled system of stochastic measure-valued processes and showed that the dynamics converges to the unique solution of a countable system of deterministic measure-valued equations, which we referred to as the hydrodynamic equations, in accordance with the parlance of interacting particle systems. Moreover, the works [3, 2, 1] which (under additional conditions on the service distributions) provide a reformulation of the hydrodynamic equations in terms of a countable system of coupled partial differential equations. While these papers focused on transient behavior of this network, in our work study equilibrium properties of the hydrodynamic limit. Our first main result, Theorem 3.3, provides a convenient characterization of the invariant state of the hydrodynamic equations in terms of fixed points of certain maps (see Remark 3.4). The methodology, which entails analysis of a system of coupled measure-valued equations, can potentially be applied to other many-server systems with general service distributions for which measure-valued representations are useful. This characterization is sufficiently tractable to construct a numerical algorithm to compute the queue length distribution and virtual waiting time in the invariant state, which is described (for simplicity, in the case ) in Section 4. Additionally, we show in Theorem 3.7 that, under a tail (or, equivalently, moment) condition on the service distribution, the invariant queue length distribution exhibits a doubly exponential decay rate. Our numerics show that while the decay rate of the invariant queue distribution is of interest, it may not manifest itself till far into the tail, and thus it is important to be able to compute and characterize finite queue length exceedance probabilities as well, which is feasible with our algorithm.

Our work also takes a small step towards understanding equilibrium behavior in large systems. Using our numerical algorithm, we provide provide numerical evidence that appears to support the conjecture that for a large class of service distributions, the invariant state is the limit of the stationary distributions of -server systems. Since the -server stationary distributions are known to be tight (due to the results in [5]), to provide a rigorous proof of this convergence it would suffice to show that the solution to the hydrodynamic equations converges to the invariant state characterized here for a large class of initial conditions. Whereas this is a non-trivial problem that is relegated to future work, it is encouraging that analogous results have been recently established for a related problem. Specifically, the framework used in [3] to obtain the hydrodynamic limit builds upon simpler measure-valued representations introduced in [14] and [12] to analyze many-server systems with a common queue and their fluid limits in the absence and presence of abandonments (so-called GI/G/N and GI/G/N+G queues). Invariant states of the associated fluid limits were characterized in Section 6 of [14] and [13], and more recent work has established convergence to equilibrium for a large class of general service distributions beyond those with decreasing hazard rate [4]. Thus, while a more sophisticated analysis will no doubt be needed to consider the more complicated system of measure-valued equations that comprise the hydrodynamic equations, these recent results do offer some hope that this approach is tractable.

We close by mentioning a related model considered in [21, 22] of a parallel server network with routing, general service distributions and Poisson arrivals. Specifically, the work [21] considers the case when each server has a queue and uses head-of-the-line processor sharing (instead of first-in-first-out, as considered here) to process jobs in the queue, whereas the article [22] considers a loss network. Both works employ a measure-valued representation like that in [3], establish a hydrodynamic limit, as the number of servers goes to infinity. They also characterize the invariant state and establish insensitivity to the distribution by showing that the solution to the fixed point for all service distributions coincides with the one in the exponential case.

1.2 Organization of the Paper and Common Notation

This article is organized as follows. Section 2 introduces the basic assumptions and the equations that characterize the hydrodynamic limit of the model. Section 3 states the main results. Section 4 presents numerical approximations of the invariant state performance measures for various distributions, and also provides evidence to support convergence of equilibrium measures to the invariant state. The proofs of Theorems 3.3 and 3.7 are given in Sections 5 and Section 6, respectively. Proofs of certain technical results are relegated to Appendices B–C.

Throughout, we will use the following notation. Let and denote the set of natural numbers and integers respectively. For every , let denote the space of continuous bounded functions on , and denote the Borel -algebra on . Also, for a metric space , let denote the set of -valued functions on that are right continuous and have finite left limits on , and let be the subset of -valued continuous functions on . Let denote the space of sub-probability measures on for some . Given an interval , let denote the space of Borel subsets of . For any , a measure on and an integrable function , we use the notation

and omit the subscripts when . Also, let represent for .

2 Hydrodynamic Equations

In this section, we introduce the equations that characterize the hydrodynamic limit of our load balancing model, as established in [3]. Throughout, we make the following assumptions on the service distribution.

Assumption I.

The service distribution whose cumulative distribution function (cdf) is denoted by , has density and finite mean, which can (and will) be set to .

Define and let be the right-end of the support of the distribution. Also, let denote the hazard rate function:

In [3] the state of an -server randomized load balancing system is represented by the Markov process , where for each , is a (random) finite measure on that has a unit delta mass at the age (that is, the time spent in service by time ) of each job that, at time , is in service at a queue of length no less than . For every , the scaled state takes values in , where

| (2.1) |

where recall is the space of sub-probability measures on .

For every , define

| (2.2) |

Note that , and for ,

| (2.3) |

We recall the definition of the hydrodynamic equations given in [3, Section 2.3].

Definition 2.1.

(Hydrodynamic Equations) Given and , in is said to solve the hydrodynamic equations associated with if and only if for every ,

| (2.4) |

and the following equations are satisfied:

| (2.5) |

and, for every ,

| (2.6) | ||||

where

| (2.7) |

and

| (2.8) |

We now briefly provide some intuition behind the form of the hydrodynamic equations. The term

represents the limiting mean conditional scaled departure rate from queues of length at least at time , and thus given by (2.7) represents the limiting cumulative scaled departure rate from queues of length at least at time .

The term represents the limiting fraction of queues of length at least at time . Note that the scaled arrival rate of jobs to the network is given by , and for , the probability that an arriving job is routed to a queue of length at time is equal to , with the convention . Thus, , where is defined by (2.8), represents the scaled arrival rate at time of jobs to queues of length . Hence, is the total increase in the fraction of queues of length greater than or equal to due to arrivals in the interval . On the other hand, represents the cumulative decrease in the fraction of queues of length at least due to service completions. The mass balance equation, (2.5) is a result of these observations.

Lastly, the right-hand side of equation (2.6) describes the three terms that contribute to the measure . The first term accounts for jobs that were already in service at time . The second term represents the contribution due to departures from queues of length greater than or equal to in the interval . The third term represents the contribution to due to jobs that entered service at a queue of length at least at some time and are still in service at time .

Along with Assumption I, we also make the following assumption throughout.

Assumption II.

There exists a unique solution to the hydrodynamic equations.

3 Main Results

To state our main results, we will require the following basic definition.

Definition 3.1 (Invariant State).

Given , is said to be an invariant state of the hydrodynamic equations with arrival rate if for every , defined by

solves the hydrodynamic equations associated with .

When is clear from the context, we will just say it is an invariant state of the hydrodynamic equations. Given an invariant state of the hydrodynamic equations, we define

| (3.1) |

which captures the corresponding invariant queue length distribution. We will only be interested in invariant states for which the invariant queue length distribution satisfies

| (3.2) |

Note that this is a necessary condition for the mean of the invariant queue length distribution to be finite. Moreover, as shown in Lemma 5.5, the condition (3.2) turns out to be equivalent to requiring , which will be satisfied by any “physically relevant” invariant state, including one that arises as the limit of stationary -server systems.

Remark 3.2.

In the sequel, we will refer to a physical invariant state as any invariant state that additionally satisfies (3.2). The latter condition is necessary for uniqueness even in the case of an exponential service distribution since, for example, as it is easy to verify, for any service distribution , (and, consequently, ) for every , is always an invariant state of the hydrodynamic equations.

We now state our first main result on existence and characterization of physical invariant states. Its proof is given in Section 5.4.

Theorem 3.3.

Suppose Assumptions I and II hold and fix , . Then there exists a physical invariant state of the hydrodynamic equations with arrival rate if and only if there exist a sequence of measurable functions on that are continuously differentiable on such that for , and for , and for ,

| (3.3) |

where for ,

| (3.4) |

In this case,

| (3.5) |

Furthermore, a physical invariant state of the hydrodynamic equations with arrival rate always exists, and also satisfies

| (3.6) |

Remark 3.4.

As an immediate consequence of Theorem 3.3, we recover the following well-known result for the exponential service distribution (see [23, Theorem 1] and [18, Lemma 2]).

Remark 3.5.

Our next result, which concerns the tail behavior of a physical invariant state, requires an additional condition:

Assumption III.

Fix . Suppose there exist , , and such that

| (3.8) |

Remark 3.6.

This tail condition is almost equivalent to a moment condition. Specifically, a sufficient condition for the tail condition is that service distribution have finite moment for some , whereas a necessary condition is that the service distribution has a finite moment. Thus, it is immediate that any distribution with all moments finite, such as the Gamma, shifted exponential and lognormal, as well as the Pareto, the latter with tail parameter greater than ), all satisfy the conditions in Assumption III.

We prove the following result in Section 6.1.

Theorem 3.7.

The result in Theorem 3.7 significantly extends previous results on the power of two choices for specific classes of service distributions such as exponential [18, 23], phase-type [16] and Pareto with parameter [8]. Besides applying to more general distributions like lognormal and shifted exponential distributions that are relevant in practice, it provides a unified approach for obtaining all these results as special cases. The most significant contribution of Theorem 3.7 is in identifying the tail decay condition on the service distribution in Assumption III as the precise property that leads to a doubly exponential tail decay. Indeed, the results for power-law distributions obtained in [8] provide a counterexample that shows that when this tail decay condition is not satisfied, then the asymptotic tails of the invariant queue lengths need not be doubly exponential, and in fact, could be power law. In this sense, the result of Theorem 3.7 is tight.

While the tail decay property is an interesting property, the decay property may not manifest itself till rather far into the tails and so finite (invariant) queue length exceedance probabilities are often of more practical interest. In Section 4, we illustrate how for , the characterization of the invariant states of the measure-valued hydrodynamic equations obtained in Theorem 3.3 allows us to compute more general invariant quantities of relevance besides the queue length, such as the virtual waiting time, which appears not to have been considered in the literature before (except in the case of exponential service times).

4 Numerical Results when

We now present numerical results, for simplicity restricting to the case .

4.1 Properties of the physical invariant state

We first obtain an alternative representation for that is more amenable to computation than the one given in (3.3)-(3.4). Recall the definition of a physical invariant state from Remark 3.2.

Lemma 4.1.

Suppose is a physical invariant state of the hydrodynamic equations, with an associated sequence of measurable functions as in Theorem 3.3. Then on and for ,

| (4.1) |

where , and for , are recursively defined as follows:

| (4.2) |

Proof.

The identity on follows from Theorem 3.3. Substituting in (3.3) with , we see that

which verifies (4.1) for . Now, suppose (4.1) holds for some . Substituting in (3.3) and using (4.1) and (4.2), we have

which shows that (4.1) also holds when is replaced with . Thus, by the principle of mathematical induction, we are done. ∎

4.2 An algorithm for computing the invariant state

The following result, whose proof is deferred to Appendix C, is the key result that allows numerical computation of the invariant states.

Proposition 4.2.

Now, fix , and a service distribution that satisfies Assumptions I and II. Let be the invariant queue length distribution, which is uniquely defined by Proposition 4.2. For , given and , and as in (3.4), we compute as the zero of the function on the interval using the bisection method with an error tolerance of . We then use the recursion (4.1) using the adaptive quadrature method with a tolerance of to numerically approximate the integrals therein.

The resulting numerical estimates for and a variety of distributions (see Appendix A for details) are tabulated in Table 1, where is set to zero if the numerical estimate for is below the precision error, i.e., . Continuing the numerical computation for for the above distributions, the only non-zero values are , and for the Weibull distribution with , and , and for the Pareto distribution with . Even for small values of the decay of appears to be faster for lighter-tailed as opposed to heavier-tailed distributions (such as Weibull with , and Pareto with ). In Section 4.3, we show that these approximations to the invariant state agree well with the approximations to the limiting stationary distribution obtained via simulations.

| Exponential | ||||

|---|---|---|---|---|

| Gamma | ||||

| () | ||||

| Weibull | ||||

| () | ||||

| Weibull | ||||

| () | ||||

| Lognormal | ||||

| () | ||||

| Pareto | ||||

| () | ||||

| Pareto | ||||

| () | ||||

| Burr | ||||

| (, | ||||

| ) |

To understand the rate of decay of the invariant queue length with respect to , Table 2 tabulates the function for the above distributions, where the entry NaN denotes that could not be computed due to loss of precision while estimating . For service distributions exhibiting a doubly exponential tail decay, by Theorem 3.7 should converge to (or be lower bounded by) a constant as . For example, it is easy to check that for the exponential service distribution converges to 1 as . This assertion cannot be inferred from Table 2, thus showing that the decay rate does not manifest itself till far into the tail. Thus, from a practical point of view, this underscores the importance of being able to compute for finite , as our approach allows.

| Exponential | ||||

| Gamma | ||||

| () | ||||

| Weibull | NaN | |||

| () | ||||

| Weibull | ||||

| () | ||||

| Lognormal | ||||

| () | ||||

| Pareto | NaN | |||

| () | ||||

| Pareto | ||||

| () | ||||

| Burr | ||||

| (, | ||||

| ) |

Due to the measure-valued representation, it is also possible to calculate the invariant states of other important performance measures in addition to the queue length. For example, consider the virtual waiting time at any time , defined to be the amount of time that a virtual job hypothetically arriving at time would have to wait before entering service. Using [2, Theorem 4.5], it can be easily deduced that when , the invariant mean virtual waiting time, is given by

| (4.3) |

where We now compute the invariant mean virtual waiting time by using the following approximation to (4.3).

where , , and , with a tolerance of

| Exponential | Pareto | Pareto | Pareto | Pareto | Pareto | |

| () | () | () | () | () | ||

| Weibull | Weibull | Weibull | Weibull | Gamma | |

| () | () | () | () | () | |

The numerics show that for a given distribution, the invariant mean virtual waiting time increases with increase in the heaviness of the tail of the distribution. While this may appear intuitive, it is not completely obvious, since it is in contrast to transient time results obtained in [2, Section 5.2.2], where the relaxation time (defined to be the time it takes for the network backlog to decrease to the extent that the mean virtual waiting time reaches half of its initial value) is smaller in the heavy-tailed case when compared to the light-tailed case.

4.3 Potential convergence of the -server equilibria to the invariant state

As mentioned in Section 1.1, for service distributions with decreasing hazard rate function, it was shown in [7] that the sequence of stationary distributions of -server systems subject to our load balancing algorithm converges to a limit and that in the case of power law distributions with tail parameter , this limit has a doubly exponential tail if and only if . They use a different approach not involving the study of dynamic behavior (or the hydrodynamic limit).

An alternative approach is to characterize the hydrodynamic limit and show that the unique invariant state of the hydrodynamic equations coincides with the limiting stationary distribution. The results of this paper, along with that of [3] and [7] can be combined to show that this is true in the case of service distributions with decreasing hazard rate. We conjecture that the unique physical invariant state coincides with the limiting stationary distribution even for more general service distributions. Below, we provide numerical evidence to support this conjecture.

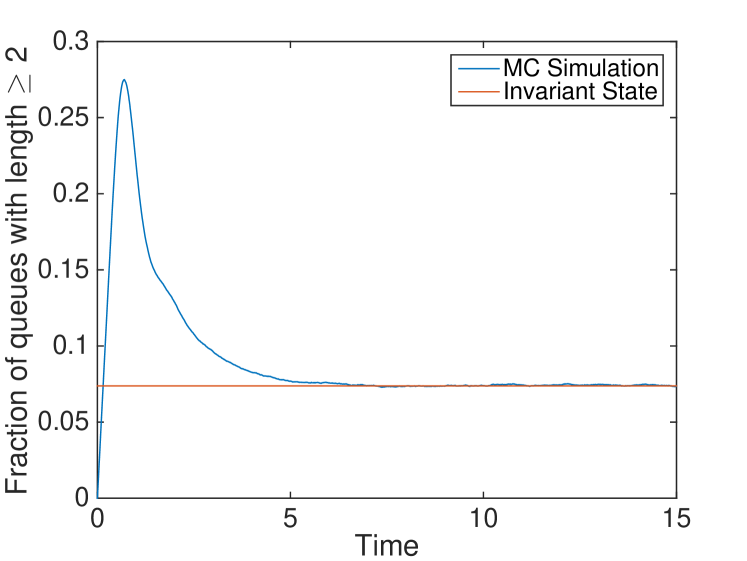

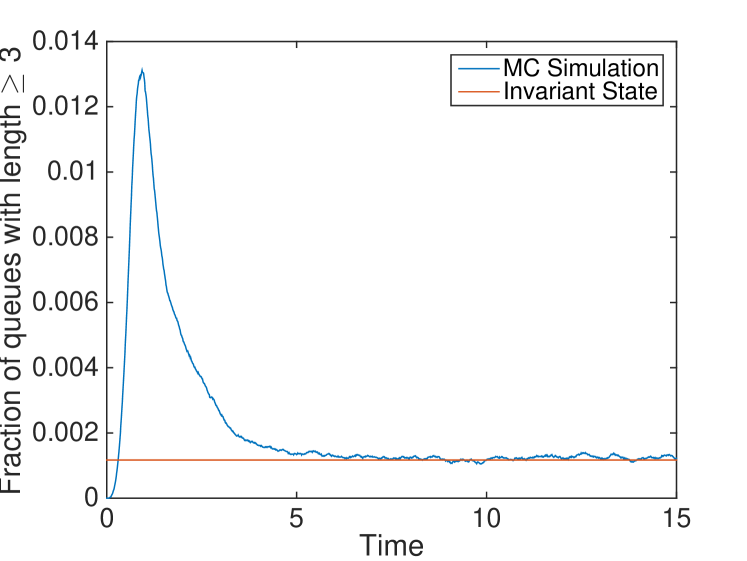

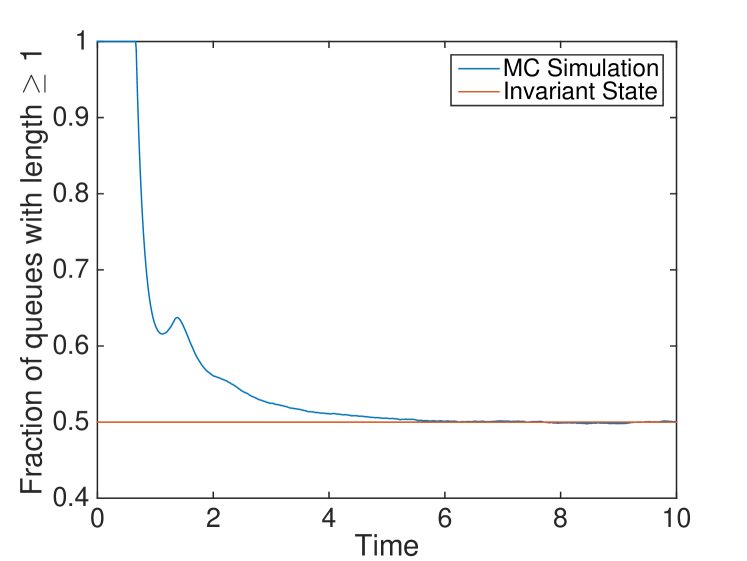

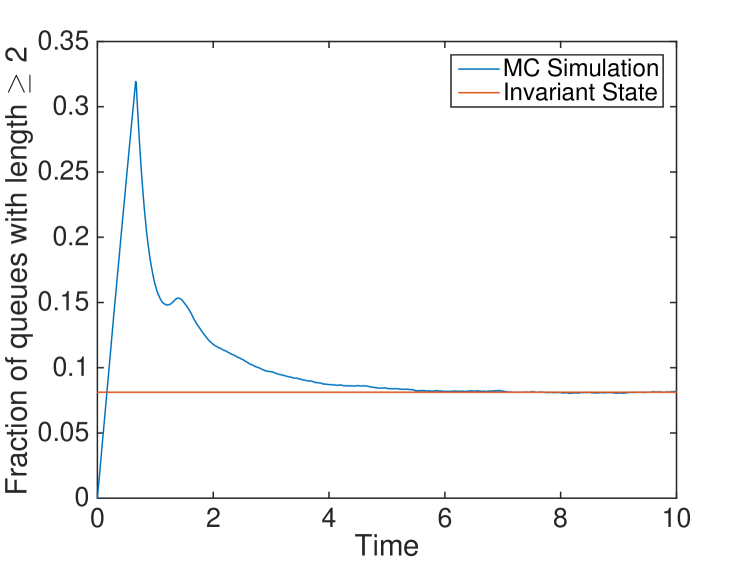

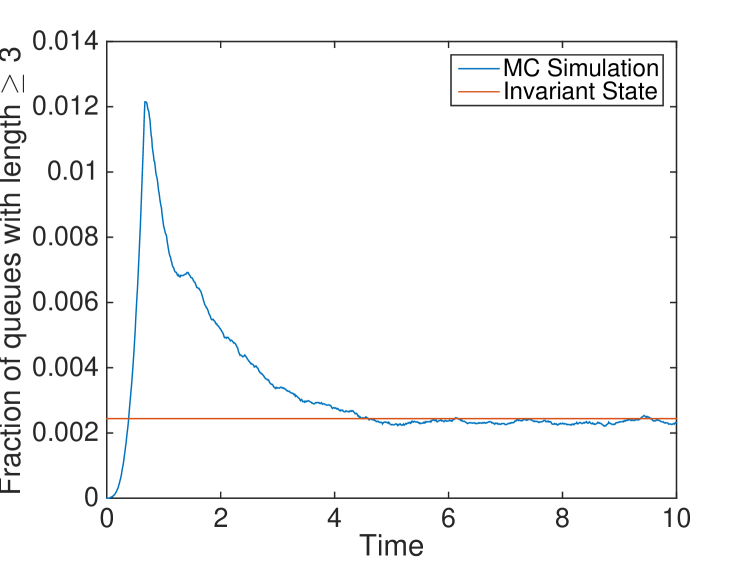

We only present results for the lognormal and Pareto distributions. Note that, while the Pareto distribution has a decreasing hazard rate function, and so one expects agreement of the two quantities due to [3, 7], it is significant that the lognormal distribution still shows agreement despite not having a monotonic hazard rate function. Similar trends are observed for a variety of other service distributions and arrival rates. Figures 1 and 2 below present a comparison, for , of with estimates of the probability that a typical queue has length no less than at time , using Monte Carlo simulations of an -server network with and for the time interval for the Lognormal distribution, and for the Pareto distribution, using 600 realizations, with the initial condition that at time , every server has exactly one job with age . We then compute the probability that a typical queue has length at time , and compare this quantity with the invariant state obtained in Table 1. For large (e.g., ) it becomes harder to use simulations to get accurate estimates of the equilibrium probability of the queue exceeding ; whereas, the recursions can still be used to get an approximation to . Figure 1 confirms the results for the Lognormal distribution and Figure 2 for the Pareto distribution and provides support for the conjecture (similar trends are observed for a variety of initial conditions and service distributions.)

5 Proof of Theorem 3.3

Let be a physical invariant state of the hydrodynamic equations in the sense of Remark 3.2. Then (by definition) , , is a solution to the hydrodynamic equations with initial condition , and condition (3.2) holds with defined as in (3.1). Define the associated invariant quantities

| (5.1) |

From (2.7), it follows that for every , the departure process with initial state satisfies

| (5.2) |

and using (2.8), the measure-valued routing process is given by for all .

The proof of Theorem 3.3, which is presented in Section 5.4, relies on several preliminary results. First, in Section 5.1, we obtain a bound on the departure rate in an invariant state, in Section 5.2 we obtain a useful characterization of an invariant state (see Proposition 5.3), and in Section 5.3 we establish existence of a physical invariant state.

5.1 The departure rate in an invariant state

Lemma 5.1.

Suppose is an invariant state of the corresponding hydrodynamic equations, and let be the corresponding queue length distribution. Then, for every ,

| (5.3) |

Moreover if (3.2) holds, that is, as , then

| (5.4) |

Proof.

Let be an invariant state of the hydrodynamic equations. Then, for every , (2.4) implies , and (2.5), (5.1) and (5.2) imply that

| (5.5) |

and for ,

| (5.6) |

where the last equality invokes (2.2). Thus, defining , we see that for ,

| (5.7) |

which proves (5.3). Furthermore, since for all , and , (5.1) implies (5.4). ∎

5.2 Characterization of invariant states

We begin by stating a result establishing absolute continuity of the invariant state. Its proof is relegated to Appendix B.

Lemma 5.2.

Let be an invariant state of the hydrodynamic equations. Then for every , is absolutely continuous with respect to Lebesgue measure on .

Proposition 5.3.

Proof.

Since each is absolutely continuous with respect to Lebesgue measure by Lemma 5.2, and for , there exists , a sequence of measurable functions on such that . Hence, clearly satisfies (3.5), and since , this immediately implies (3.4). Now using in (2.6), and for , combining (5.1), (5.2), and (5.5), we have for every and ,

Recalling that , this implies that

A standard monotone class argument shows that this holds for every bounded measurable function . Hence, the above equation holds if and only if for a.e. ,

It is easy to see that this implies that is a.s. equal to the constant , and with some abuse of notation, we denote this constant again by . In turn, since both and , this implies that

| (5.10) |

which proves (5.8).

Similarly, for , setting in (2.6), and using the identity for any along with (3.5), (5.1) and (5.2), we have for every , and ,

| (5.11) |

Since is integrable with respect to by definition, we can use Fubini’s theorem to change the order of integration in the last term on the right-hand side of (5.2), and apply the identity for , to obtain

where we use the notation to denote the minimum of and . Thus, we can rewrite (5.2) as

| (5.12) |

where, for ,

Now, (5.12) clearly holds if and only if for every , for a.e. , which in turn holds if and only if for every ,

| (5.13) |

and

| (5.14) |

We will first consider the implications of the equality in (5.14). Define

and

| (5.15) |

Note that is continuous on , and using the definition of and (5.6), we can rewrite (5.14) as

| (5.16) |

with boundary condition . Solving this linear ordinary differential equation, we see that

Combining this with (5.16) and recalling that , we obtain

| (5.17) |

which in particular shows that is continuous. Also, to further simplify the right-hand side, note that (5.15) shows that is differentiable with continuous derivative . An integration by parts then yields

Substituting this back into (5.17), and using (5.15), (2.2), (5.3) and (5.10) we obtain

which coincides with the identity in (5.9).

To complete the proof, it only remains to check that with this definition of , (5.13) is also satisfied, and that each is continuously differentiable. First, note that for any and , we have

When combined with (5.16) both as is and with replaced by , and the relation , this yields

and when combined with (5.15), this implies

Together, the last two displays imply that

which, given the definition of , proves that (5.13) is also satisfied.

Since is a constant function, it is clearly continuously differentiable and for all . Given that is continuously differentiable on , the continuous differentiability of on is an immediate consequence of (5.9).

The continuously differentiable property of on then follows from the principle of mathematical induction.

∎

5.3 Existence of a physical invariant state

In this section, we use the characterization obtained in Proposition 5.3 to show that an invariant state always exists (see Proposition 5.6). The proof of existence relies on a few preliminary results. The first is a monotonicity property of the sequence of functions that satisfy (5.9).

Lemma 5.4.

Given an invariant state , let be the associated measurable functions on that are continuously differentiable on , as described in Proposition 5.3. Then, for any ,

Proof.

We now consider physical invariant states, namely those that satisfy condition (3.2).

Lemma 5.5.

Let be a physical invariant state of the hydrodynamic equations, that is, for which the associated satisfies , with as in (3.1). Then .

Proof.

Fix an invariant state, and let be the associated sequence of functions described in Proposition 5.3. By Lemma 5.4 for every , is monotonically decreasing in , and is bounded below by . Together with (5.8), this shows , for all , , and the limit exists for all . Since is integrable, the dominated convergence theorem implies On the other hand, (3.4) and the tail condition of (3.2) show that When combined, these limits imply Since and for , this implies a.e.. Likewise, using , (3.5), the integrability of , and the dominated convergence theorem, one has

Thus, taking the limit in equation (5.3) as , and using the fact that , we see that

Comparing the last two equations, we conclude that Since (3.5) and (5.8) imply , this completes the proof of the lemma. ∎

Let denote the space of bounded functions on that are continuously differentiable on . Fix , and consider the associated map defined as follows: for define

| (5.18) |

where is defined by

| (5.19) |

Then the following criterion for existence of a physical invariant state is an immediate consequence of Proposition 5.3 and Lemma 5.5.

Proposition 5.6.

Suppose that whenever either or when is non-constant and

| (5.20) |

then has at least one fixed point on . Then there exists a physical invariant state for the hydrodynamic equations with arrival rate .

Proof.

Assume the supposition of the proposition holds. By Proposition 5.3 and Lemma 5.5, any physical invariant state must satisfy and . On the other hand, (5.3) and Lemma 5.5 imply that . When substituted into (5.9) and (3.5), this implies (3.3) and (3.6) must hold. Thus, to show existence of an invariant state it suffices to find sequences of continuously differentiable functions and positive constants that satisfy (3.3) and (3.4). For , define , with , and let be a fixed point of in , which exists by the claim, and let be as defined in terms of via (3.3). Then clearly satisfies (3.4) due to (5.19), and there is a unique satisfying (3.4) with satisfying (3.3) if and only if the fixed point of is unique. Now, suppose that for some , there exist continuously differentiable functions and constants that satisfy (3.3) and (3.4) for . Then (3.3) and (3.4) imply that satisfies (5.20). Therefore, setting , the claim above shows that has a fixed point that we denote by , and let be as defined in (3.3), and note that then (3.4) holds on account of (5.19). Thus, we have constructed and that satisfy (3.3) and (3.4) for all , and the first assertion of the proposition follows by induction. ∎

5.4 Proof of Theorem 3.3

Proof of Theorem 3.3.

To establish Theorem 3.3 it suffices to verify the supposition of Proposition 5.6. To see why the latter is true, fix that satisfies the stated conditions, and define . Note that then we need to show that has at least one zero on . Note that by (2.2), for all whenever . Since is not identically zero and is strictly positive on , (5.18) implies that and hence, . Since is continuous, by the intermediate value theorem, to show has a zero on , it suffices to show that . Note that a simple integration by parts yields

| (5.21) |

If , then by (5.19), and (5.21) shows that . Thus, (with equality holding only if ) and so has a zero on if and at if . On the other hand, if satisfies (5.20), then (5.21) and (5.19) show that

where the last inequality also uses the fact that is non-constant. This proves the first assertion of Theorem 3.3. Also, in view of (3.5), the right-hand side of (3.6) is equal to . Therefore, (3.5) follows from Proposition 5.3 and Lemma 5.5. This completes the proof of Theorem 3.3. ∎

6 Tail Decay for the Invariant State

Throughout this section recall that we fix , , suppose Assumptions I-III hold and let , and be as in Assumption III. Also, let be the queue length distribution associated with a physical invariant state of the hydrodynamic equations. Note that the analysis here does not explicitly require uniqueness of the physical invariant state, and only relies on the characterization stated in Theorem 3.3 (and proved in Section 5).

6.1 A reduction

In this section we show that the proof of Theorem 3.7 can be reduced to establishing certain key estimates stated in Proposition 6.1 below. We first introduce some relevant notation. Define

| (6.1) |

where denotes the largest integer less than or equal to . Throughout this section, given , and for all , we will use the convention that

Proposition 6.1.

The proof of Proposition 6.1, which involves a careful analysis of the equations characterizing the invariant state, is lengthy and deferred to Section 6.3. We now use this result to prove Theorem 3.7 in two steps. First, in Lemma 6.2, we show that Proposition 6.1 directly implies that the sequence has at least an exponentially fast decay rate. We then combine this a priori estimate with a result on inhomogeneous recursions (Lemma 6.3 below) to show that the decay rate is at least doubly exponential.

Lemma 6.2.

Suppose Assumptions I – III hold. Let be the queue length distribution associated with a physical invariant state of the hydrodynamic equations and let and be as in Proposition 6.1. If is not an integer, then there exists such that for all ,

| (6.4) |

If is an integer, then there exists such that for all ,

| (6.5) |

Proof.

First note that Proposition 6.1 implies that for some , and ,

| (6.8) |

We consider two cases:

Case 1: is not an integer. In this case, define

| (6.9) |

and

| (6.10) |

Note that and imply and . Let

| (6.11) |

where denotes the smallest integer greater than or equal to . Now, define . Since and for all ,

As the inductive hypothesis, assume that there exists such that

| (6.12) |

for all . Applying (6.8) with for the case , using (6.9), (6.10) and the induction hypothesis (6.12), we see that is bounded above by

where the last inequality uses , and (6.11). Thus, by the inductive hypothesis, (6.12) holds for all . Together with the fact that is non-decreasing, (6.9) and (6.10), this implies

Since , there exists such that (6.4) holds for all .

Case 2: is an integer. In this case the proof of (6.5) follows the same argument as in the non-integral case but with , and

where note that (since and ) and imply and . ∎

Lemma 6.3.

Given strictly positive numbers , and , for every and such that , there exists such that if

| (6.13) |

then

Proof.

Subtracting from and using (6.13), we see that for ,

Subtracting from again, using the above equation, and rearranging, we have for ,

Define by

| (6.14) |

Noting that is not a root of , let be the distinct roots of , with , and let denotes the multiplicity of the root . Then Since and , by Theorem 4.1.1 of [20],

| (6.15) |

where is a polynomial in of degree no less than .

A direct inspection of (6.14) shows that , the root has degree , and , where

By Descartes’ rule of signs, there exists exactly one positive root of . Let us denote it by . Note that and since by assumption. Thus, or equivalently . Using Rouche’s theorem (see [19, Exercise 237, page 321]) it is easy to show that has no roots other than in the disc . Hence, for . In view of the representation for in (6.15), this implies

Setting proves the claim. ∎

Proof of Theorem 3.7.

Fix a physical invariant state of the hydrodynamic equations, and let be the associated queue length distribution.

We consider two cases:

Case 1: is not an integer. Let be as in Proposition 6.1. In this case, using the monotonicity of the logarithm function along with (6.2), we see that for

By Lemma 6.2, there exists such that

Set for , and recursively define

Then, applying Lemma 6.3 with , (noting that ), , and for , we conclude there exists such that

Since for all , this proves (3.9), in this case.

Case 2: is an integer. Let and be as in Proposition 6.1. Then (6.3) implies that for every ,

By Lemma 6.2, there exists such that

Now, set for and recursively define

Since is an integer, implies . Since , , , we have . Thus, applying Lemma 6.3 with , and for , we conclude there exists such that

Since for all , this proves (3.9), for Case 2 as well. ∎

Remark 6.4.

The estimates for in (6.2) and (6.3) are analogous to the estimates for corresponding probabilities obtained in (3.5) and (3.6) of Proposition 3.2 in [8]. One may expect that the proof of the tail decay property in Theorem 3.7 could therefore be deduced from Proposition 6.1 by simply referring to the argument used in [8] to deduce their tail decay result (in Theorem 1.1 of [8]) from Proposition 3.2 therein, which only involves comparison with a homogeneous linear recursion (see Proposition 3.3 of [8]). However, we could not quite resolve the argument in [8], and instead provide a self-contained proof that entails a two-step argument presented above, that involves comparison with the slightly more complicated inhomogeneous recursion analyzed in Lemma 6.3.

6.2 Preliminary Estimates on the Density of the Physical Invariant State

In this section we obtain preliminary estimates that are used to prove Proposition 6.1 in Section 6.3.

Lemma 6.5.

Proof.

Since is the queue length distribution associated with a physical invariant state of the hydrodynamic equations, by Theorem 3.3, , and by convention . Hence, (6.16) follows from (3.3) with , and the inequality , which holds by (2.3). For the proof of (6.17) we will make repeated use of the fact that the function is increasing for any . Using (3.3) again, but now with , and using the inequality (6.16), we obtain

Together with the inequality from (2.3), this implies,

which proves (6.17) for .

Now, suppose (6.17) holds for some . Then using (3.3) with replaced by and (6.17), we have

Therefore,

Using the inequality from (2.3), we then obtain

which shows that (6.17) holds with replaced by . Thus, by the principle of mathematical induction, (6.17) holds for all .

∎

We now state a result that is an immediate consequence of Lemma 6.5 and the elementary inequalities and for .

Corollary 6.6.

We now make an observation that will be used repeatedly in the next section. Recalling that, , and are constants from Assumption III, now define

| (6.20) |

Note that . Fix to be a non-decreasing measurable function . Then clearly

Using the above inequality and (3.8), and rescaling, we see that

| (6.21) |

Define as follows:

| (6.22) |

Using the convention for all , also define

| (6.23) |

Fix , and let , be as in Assumption III, and let be as defined in (6.22). Then, recalling from (3.4), integrating the inequality (6.19) with respect to and using the identity , it follows that for

Applying (6.2) with for , and using (6.23), this implies

| (6.24) |

where

| (6.25) |

The proof of Proposition 6.1 will proceed by bounding the right-hand side of (6.24) by (6.2) or (6.3), depending on whether is or is not an integer, using an inductive argument and the estimates in the following lemma. In what follows, recall the convention that for all .

Lemma 6.7.

Fix and . If , we have

| (6.28) |

whereas if , then there exists such that

| (6.31) |

Moreover, we also have

| (6.34) |

6.3 Proof of Proposition 6.1

First note that the convention for and the assumption imply by Theorem 3.3. Suppose is not an integer. Using (3.4), (6.18) of Corollary 6.6 and the fact that , we have

where the second inequality uses (6.2) with , where is defined in (6.23). Applying (6.34) of Lemma 6.7, with , and using and for all , we obtain

| (6.35) |

which shows that (6.2) holds for .

Similarly, using (3.4) and (6.19) of Corollary 6.6, with , and (6.2), with , we have

| (6.36) |

We now claim that for any and ,

| (6.37) |

Indeed, this follows from the fact that

and the fact that and . Together, (6.35), (6.36) and (6.37), with and , yield

| (6.38) |

We now use induction to obtain estimates for all . Define , , and

| (6.39) |

Moreover, suppose for some ,

| (6.40) |

To upper bound the first term on the right-hand side of (6.24), we combine (6.40), with , and (6.37), with and , to conclude that

| (6.41) |

Next, to estimate the last term on the right-hand side of (6.24), combine (6.25) with (6.34) of Lemma 6.7, to obtain

| (6.42) |

We now identify respective upper bounds for each of the summand in the middle term on the right-hand side of (6.24). First, note that when , (6.28) and the inequalities for all , and imply

| (6.43) |

On the other hand, if , using the fact that and for all , as well as (6.40) and (6.37), with and , one obtains

| (6.44) |

We now observe that . Since , and for , by definition

which implies for all . Combining this with (6.41)-(6.44), the definition (6.39) and the inequality , we conclude that

6.4 Proof of Key Estimates

To complete the proof of Proposition 6.1, in this section we present the proof of Lemma 6.7. We start with a preliminary result in Lemma 6.8 that will be used in the proof. Recall the definition of from (6.23) and note that and the sequence is non-decreasing. Define

| (6.45) |

and note that since as ; see (3.2). As always, .

Lemma 6.8.

Fix . Let . Then for any ,

| (6.46) |

Moreover, if and , then

| (6.47) |

If and , then

| (6.48) |

Proof.

Proof of Lemma 6.7.

Fix , and . We first show that (6.28) and (6.31) imply (6.34). First, suppose . Recalling the definition of from (6.25), we now claim (and justify below) that

| (6.49) |

Indeed, note that if , then since , and for . This immediately implies (6.49) when . On the other hand, if , then the trivial inequality and (6.25) imply (6.49). Noting that implies is bounded above by the constant defined in (6.22), the last two displays imply (6.34). If , (6.31) can be shown to imply (6.34) using the same argument, but with replaced by .

Case 1: Suppose and . Then, using the definition of in (6.25) and (since ) applying (6.46) with and , as well as (6.22), this implies

Combining this with the observation that for all due to (6.45) and the case assumption, we have, for any ,

| (6.50) |

Since , choosing , we obtain

This immediately implies (6.28) when and , and (6.31) when and and also, noting that implies for any , when . When , since implies , (6.50) also proves (6.28) in that case. The remaining case when and can be deduced similarly from (6.50) by setting therein.

Case 2: Suppose and . We now look at the partition of the interval . Note that

| (6.51) |

Since , using (6.46) with and , we have

| (6.52) |

Next, since implies , we have for , and . Since and , we use (6.47) with to obtain

| (6.53) |

where

| (6.54) |

Now, for any the case assumption, which in particular implies , the inequality , and the fact that is increasing imply that and , and hence, that

| (6.55) |

Case 2A: Suppose . Restricting so that , and using (6.48) with , we have for any ,

| (6.56) |

Since and , choosing , we obtain

| (6.57) |

Combining (6.51) – (6.54), (6.57) and (6.55) with the fact that

| (6.58) |

and the definitions of and in (6.22) and (6.25), respectively, we obtain (6.28) whenever .

Setting and in (6.56), we obtain

| (6.59) |

Now, noting that and is non-increasing, we conclude that

| (6.60) |

Combining (6.51) – (6.54), (6.58) – (6.60) and the definitions of and in (6.22) and (6.25), respectively, we obtain

(6.28) when .

Case 2B: Suppose

. Note that and the fact that is increasing implies for all and for all . Then, substituting the expression for in (6.23), and , we obtain

| (6.61) |

Combining (6.51) – (6.55) and (6.61) with the fact that

| (6.62) |

the observation that for any and the definitions of and in (6.22) and (6.25), respectively, we obtain (6.31).

Case 3: Suppose , and . Using (6.45), this implies for all . We now look at the partition of the interval . Note that

| (6.63) |

Since , using (6.46) with and , we have

| (6.64) |

For the interval note that and the fact that is increasing in implies for all . Hence, we have

| (6.65) |

Additionally, if , note that for , . Since , we use (6.47) with and the definition of in (6.54) to obtain

| (6.66) |

Case 3A: Suppose . First, let . Since by (6.1), (6.65) simplifies to

| (6.67) |

Note that for , . Since and, we use (6.47), with and the definition of in (6.54) to obtain

| (6.68) |

Also, note that and the fact that is increasing implies for all and for all . Hence, using (6.23), we obtain

| (6.69) |

Combining (6.63), (6.64), (6.4) – (6.4), (6.60), (6.58) (since ) and the definitions of and in (6.22) and (6.25), respectively, we obtain (6.28) when .

Now, let . Using (6.23), (6.65) simplifies to

| (6.70) |

Combining (6.63), (6.64), (6.66), (6.4), (6.58), (6.55) (since ) and the definitions of and in (6.22) and (6.25), respectively, we obtain (6.28) when .

Case 3B: Suppose . First, let . Using (6.23) and the fact that there exists such that for all , (6.65) simplifies to

| (6.71) |

Now, noting that , , and is non-increasing, we conclude that

| (6.72) |

Combining (6.63), (6.64), (6.66), (6.4), (6.72), (6.62) (since ) and the definitions of and in (6.22) and (6.25), respectively, we obtain (6.31) when .

Acknowledgements: The authors were partially supported by NSF grants DMS-1713032 and DMS-1407504 and ARO grant W911NF2010133.

Appendix A Types of Distributions

In this section, we will look at the distribution functions of the various distributions that we considered in Section 4.

-

•

Gamma distribution: The Gamma distribution with unit mean is parameterized by , and

where denotes the Gamma function

and denotes the lower incomplete gamma function,

-

•

Weibull distribution: The Weibull distribution with unit mean is parameterized by , and

where .

-

•

Lognormal distribution: The Lognormal distribution with unit mean is parameterized by , and

where , and denotes the error function

-

•

Pareto distribution: The Pareto distribution with unit mean is parameterized by , and

where .

-

•

Burr distribution: The Burr distribution with unit mean is parameterized by and , and

where , and denotes the beta function, i.e.,

Appendix B Absolute Continuity of the Invariant State

We start by making a simple observation.

Lemma B.1.

If is a solution to the hydrodynamic equations with initial condition , then for all Lebesgue integrable functions on , and all ,

| (B.1) | ||||

Proof.

We show below that (B.1) holds for indicator functions. Indeed, fix consider a sequence with for each and . For each , consider defined by

Then pointwise as . Using (2.6) with and the Dominated Convergence theorem, we have

By linearity, it then follows that (B.1) holds for all simple functions. Since any Lebesgue integrable function can be represented as a monotone limit of simple functions, another application of the DCT shows that (B.1) is satisfied whenever is a Lebesgue integrable function. ∎

In what follows, is an invariant state of the hydrodynamic equations.

Proof of Lemma 5.2.

For , substituting and in (B.1), and using (5.2), we have for each ,

| (B.3) |

The relation (5.1) implies that for ,

| (B.4) |

Claim: Given ,

| (B.5) |

where

| (B.6) |

The claim for follows on using (B.4) and (B), with , and sending .

Now, suppose (B.5) holds for some with . For , using (5.1), the inequality , and (B.5), with replaced by , we have

When combined with (B) and(B.6), and sending , the above equation yields (B.5). Given , define . Let be a Lebesgue measurable set with , where denotes Lebesgue measure. Since (by, e.g., [11, Lemma 1.17])

there exists such that and . Since by Lemma 5.1, using (B.5) and (B.6) with , we obtain for all ,

Appendix C Uniqueness of the Invariant State when

In this section we prove Proposition 4.2. The proof will rely on the following elementary lemma.

Lemma C.1.

Let and let be a function on such that is continuously differentiable on , for , has at least one root in and the derivative of at every root in is negative, i.e.,

Then there exists a unique such that .

Proof.

First note that since is negative at all its roots, there does not exist any interval such that on . Let be two distinct roots of . Since , and has a continuous derivative, there exist , and such that and . By the intermediate value theorem there exists at least one such that and . This contradicts our assumption, and hence, has a unique root. ∎

Proof of Proposition 4.2.

Fix . By definition we know and we set and note that (3.4) holds. Now, suppose for any , and satisfy (3.3) and (3.4) for . Then by Remark 3.4, it suffices to show that has a unique fixed point in , which then must be . Define , . Then, setting in the expression for in (2.2) and using (3.7),

| (C.1) |

Note that

Also, integrating the right-hand side of (C.1) by parts, and using the fact that (3.3) and (3.4), with , imply and , we conclude that

Since by Lemma 5.4, we have . Thus, for . On differentiating (C.1), we obtain

Using (3.7) with and we see that

Now, since and satisfies (3.3) and therefore (5.9), Lemmas 5.4 and 5.5 imply the monotonicity of , we have for all , . Thus,

Combining the last three displays and rearranging, we obtain

Using Hölder’s inequality, we have

and

Combining the last three displays and evaluating at any fixed point of in ,

| (C.2) |

where for ,

Differentiating we obtain

To show that for , it suffices to show the numerator of the first term is positive. Since implies when , this follows from

Hence, is increasing on . When combined with (C.2), this implies

Hence using the definition of in (C.1), continuous differentiability of from Proposition 5.3 and substituting and in Lemma C.1, we conclude that has a unique fixed point in . ∎

References

- [1] Aghajani, R., Li, X., and Ramanan, K. Mean-field dynamics of load-balancing networks with general service distributions. Arxiv preprint, https://arxiv.org/abs/1512.05056, 2015.

- [2] Aghajani, R., Li, X., and Ramanan, K. The pde method for the analysis of randomized load balancing networks. Proc. ACM Meas. Anal. Comput. Syst. 1, 2 (Dec. 2017), 38:1–38:28.

- [3] Aghajani, R., and Ramanan, K. The hydrodynamic limit of a randomized load balancing network. Ann. Appl. Probab. 29, 4 (2019), 2114–2174.

- [4] Atar, R., Kang, W., Kaspi, H., and Ramanan, K. Large-time limit of many-server queues with reneging. In Preparation.

- [5] Bramson, M. Stability of join the shortest queue networks. Ann. Appl. Probab. 21, 4 (2011), 1568–1625.

- [6] Bramson, M., Lu, Y., and Prabhakar, B. Randomized load balancing with general service time distributions. SIGMETRICS Perform. Eval. Rev. 38, 1 (June 2010), 275–286.

- [7] Bramson, M., Lu, Y., and Prabhakar, B. Asymptotic independence of queues under randomized load balancing. Queueing Syst. 71, 3 (2012), 247–292.

- [8] Bramson, M., Lu, Y., and Prabhakar, B. Decay of tails at equilibrium for FIFO join the shortest queue networks. Ann. Appl. Probab. 23, 5 (2013), 1841–1878.

- [9] Brown, L., Gans, N., Mandelbaum, A., Sakov, A., Shen, H., Zeltyn, S., and Zhao, L. Statistical analysis of a telephone call center: a queueing-science perspective. J. Amer. Statist. Assoc. 100, 469 (2005), 36–50.

- [10] Chen, S., Sun, Y., Kozat, U. C., Huang, L., Sinha, P., Liang, G., Liu, X., and Shroff, N. B. When queueing meets coding: Optimal-latency data retrieving scheme in storage clouds. arXiv preprint arXiv:1404.6687 (2014).

- [11] Folland, G. B. Real analysis, second ed. Pure and Applied Mathematics (New York). John Wiley & Sons, Inc., New York, 1999. Modern techniques and their applications, A Wiley-Interscience Publication.

- [12] Kang, W., and Ramanan, K. Fluid limits of many-server queues with reneging. Ann. Appl. Probab. 20, 6 (2010), 2204–2260.

- [13] Kang, W., and Ramanan, K. Asymptotic approximations for stationary distributions of many-server queues with abandonment. Ann. Appl. Probab. 22, 2 (2012), 477–521.

- [14] Kaspi, H., and Ramanan, K. Law of large numbers limits for many-server queues. Ann. Appl. Probab. 21, 1 (2011), 33–114.

- [15] Kolesar, P. Stalking the endangered cat: A queueing analysis of congestion at automatic teller machines. Interfaces 14, 6 (1984), 16–26.

- [16] Li, Q.-L., Lui, J. C., and Wang, Y. A matrix-analytic solution for randomized load balancing models with ph service times. In International Workshop on Performance Evaluation of Computer and Communication Systems (2010), Springer, pp. 240–253.

- [17] Liang, G., and Kozat, U. C. Tofec: Achieving optimal throughput-delay trade-off of cloud storage using erasure codes. In INFOCOM, 2014 Proceedings IEEE (2014), IEEE, pp. 826–834.

- [18] Mitzenmacher, M. The power of two choices in randomized load balancing. IEEE Transactions on Parallel and Distributed Systems 12, 10 (2001), 1094–1104.

- [19] Narasimhan, R., and Nievergelt, Y. Complex analysis in one variable, second ed. Birkhäuser Boston, Inc., Boston, MA, 2001.

- [20] Stanley, R. P. Enumerative combinatorics. Vol. I. The Wadsworth & Brooks/Cole Mathematics Series. Wadsworth & Brooks/Cole Advanced Books & Software, Monterey, CA, 1986. With a foreword by Gian-Carlo Rota.

- [21] Vasantam, T., Mukhopadhyay, A., and Mazumdar, R. R. The mean-field behavior of processor sharing systems with general job lengths under the sq (d) policy. Performance Evaluation 127 (2018), 120–153.

- [22] Vasantam, T., Mukhopadhyay, A., and Mazumdar, R. R. Insensitivity of the mean field limit of loss systems under routeing. Adv. in Appl. Probab. 51, 4 (2019), 1027–1066.

- [23] Vvedenskaya, N. D., Dobrushin, R. L., and Karpelevich, F. I. A queueing system with a choice of the shorter of two queues—an asymptotic approach. Problemy Peredachi Informatsii 32, 1 (1996), 20–34.