No COVID-19 Climate Silver Lining in the US Power Sector

Abstract

Recent studies conclude that the global coronavirus (COVID-19) pandemic decreased power sector CO2 emissions globally and in the United States. In this paper, we analyze the statistical significance of CO2 emissions reductions in the U.S. power sector from March through December 2020. We use Gaussian process (GP) regression to assess whether CO2 emissions reductions would have occurred with reasonable probability in the absence of COVID-19 considering uncertainty due to factors unrelated to the pandemic and adjusting for weather, seasonality, and recent emissions trends. We find that monthly CO2 emissions reductions are only statistically significant in April and May 2020 considering hypothesis tests at 5% significance levels. Separately, we consider the potential impact of COVID-19 on coal-fired power plant retirements through 2022. We find that only a small percentage of U.S. coal power plants are at risk of retirement due to a possible COVID-19-related sustained reduction in electricity demand and prices. We observe and anticipate a return to pre-COVID-19 CO2 emissions in the U.S. power sector.

keywords:

COVID-19 , electric power sector , decarbonization , climate change , United States , counterfactual analysis , Gaussian processes , machine learning , statistical significance , economic modeling , coal , capacity markets , price duration curveIntroduction

Despite its disruptive impacts on economic and social activities, the global coronavirus (COVID-19) pandemic could have a climate-related silver lining: a sustained reduction in carbon dioxide (CO2) emissions [1, 2, 3, 4]. Several studies attribute COVID-19-related decreases in energy demand to decreases in CO2 emissions [1, 2, 5, 6, 7, 8, 9, 10]. Other studies report the impacts of COVID-19 on factors that affect power sector CO2 emissions, such as electricity demand [11, 12, 13] and changes to the electricity supply mix [14, 15].

We focus on the impacts of COVID-19 on power sector CO2 emissions in the contiguous United States. The power sector in the contiguous U.S. accounts for 33% of total U.S. CO2 emissions [16]. The power sector is the focus of U.S. decarbonization efforts: since January 1, 2018, nine U.S. states, the District of Columbia, and Puerto Rico enacted legislation that requires reductions in power sector CO2 emissions of 90% or greater in those jurisdictions by 2050 or earlier; while 23 electric utilities pledged to reduce their CO2 emissions by 80-100% by 2050 or earlier [17]. Altogether, those state legislative actions and utility pledges amount to an intended reduction in power sector CO2 emissions of more than 50% by mid-century.

We estimate the statistical significance of U.S. power sector CO2 emissions reductions from March through December 2020 while accounting for typical variability in emissions and adjusting for weather, seasonality, and recent emissions trends. Additionally, we estimate the expected impact of COVID-19 on the retirement of coal-fired power plants through 2022. The paper is structured as follows.

In Section 2, we employ a simple probabilistic model that accounts for weather and seasonality and captures historical variability in factors unrelated to COVID-19, to estimate the impact of COVID-19 on power sector CO2 emissions () in the United States. We use the model to evaluate COVID-19-related CO2 emissions reductions and the statistical significance of such reductions relative to typical variance in emissions.

In Section 3, we use the probabilistic model to determine the relative impacts of changes in electricity generation () and carbon intensity of electricity supply (C/E) on CO2 emissions, and the relative impacts on C of changes in the electricity supplies of the three principal power generation fossil fuel sources in the U.S.: coal, natural gas, and oil.

In Section 4, we employ economic modeling to evaluate the expected impact of COVID-19 on U.S. coal plant retirements. We analyze the expected profitability through 2022 of the 845 coal-fired power plant units operating in U.S. wholesale electricity and capacity markets. Those 845 coal units represent 74% of coal units, 67% of coal capacity, and 42% of power sector CO2 emissions in the contiguous U.S. [18]. To estimate the expected profitability of coal-fired power plant units, we use hourly historical electricity market price data, monthly electricity market price forecasts, annual and bi-annual capacity market price data, and data related to the locations, operating capacities, and costs of coal-fired generation units.

Are COVID-19-Related Reductions in Power Sector CO2 Emissions Statistically Significant?

Data

Our analysis of U.S. power sector CO2 emissions requires three types of data: net generation by fuel, emissions factors by fuel, and heating and cooling degree days. We obtain net generation by fuel from the Energy Information Administration (EIA) Form EIA-923 [19], which reports monthly generation and fuel consumption for every power plant. We obtain Form EIA-923 data for the period between January 2016 and December 2020. Monthly plant-level emissions are computed by multiplying fuel consumption for each plant by fuel code-specific emissions factors published by the EIA and U.S. Environmental Protection Agency (EPA) [20, 21, 22]. Total CO2 emissions for the contiguous U.S. are evaluated by aggregating plant-level emissions. We obtain population-weighted heating degree day (HDD) and cooling degree day (CDD) data from the EIA [23].

Methods

We employ a Gaussian process (GP) regression model to forecast CO2 emissions in the contiguous United States. GP regression models are a class of Bayesian nonparametric models. They assume that every finite collection of random variables has a multivariate normal distribution. GP regressions can be used, as in our case, to forecast the likely ranges of variables corresponding to future periods based on observed historical data. GP regressions are appropriate for testing the statistical significance and estimating the uncertainty of outcomes impacted by seasons and other periodic variables [24, 25]. GP regressions have been used to forecast electricity demand and prices, wind and solar power generation, CO2 emissions, battery state-of-charge, and optimal grid management strategies, among other related applications [26, 27, 28, 29, 30, 31, 32, 33, 34].

We develop a GP regression that represents a counterfactual scenario in which the COVID-19 pandemic had not occurred. It is developed using the Python GPy library [25]. The GP regression is fit on vector time series data that describes CO2 emissions, HDDs, and CDDs in the contiguous U.S. To forecast CO2 emissions, we fit a constant term (bias kernel), a trend term (linear kernel), and a combination of sinusoidal terms (a standard periodic kernel) to historical CO2 emissions data. The constant and trend terms capture average year-over-year trends while the periodic term, which is constrained to model one-year periods, describes repeating seasonal patterns in the time series. Bias and linear kernels are used to model the impacts of population-weighted HDDs and CDDs on CO2 emissions. The GP model is fit using a SciPy implementation of the L-BFGS-B algorithm with five random restarts [35]. The L-BFGS-B algorithm is a standard optimization technique [36, 37]; L-BFGS-B and multiple random restarts are commonly used to fit GPs. Our optimization settings yield model runs that are highly stable and reproducible. The GP model explicitly captures weather, medium-term CO2 emissions trends, and seasonality. We attribute the remaining Gaussian noise to factors that are not modeled explicitly, such as short-term macroeconomic changes, discrete or non-linear changes to the power-system, and outlier events.

The GP regression is fit to historical emissions data for the period January 2016 through February 2020, the last month before COVID-19-related shelter-in-place orders took effect. This historical period is long enough to obtain a strong model fit but not so long as to necessitate additional nonlinear approximations or more complicated multiyear regression methods. The regression model is used to forecast emissions from March through December 2020. Such a forecast is a probabilistic representation of what emissions would have been in a counterfactual scenario in which COVID-19 had not occurred.

We compare observed to forecasted data and evaluate deviations between the two. The GP methodology allows us to estimate the statistical significance of these deviations. The model generates Gaussian distributions of values in each forecasted month in the counterfactual scenario. Given these Gaussian distributions, statistical hypothesis testing amounts to determinations of 95% confidence intervals (CIs) and a simple decision rule: if the observed CO2 emissions level is outside of the 95% CI, we reject the null hypothesis that the observation could have occurred with reasonable probability in the absence of COVID-19. In other words, if the observed CO2 emissions level is outside of the 95% CI, we infer statistically significant impacts of COVID-19 on CO2 emissions. If the observed value is within the 95% CI, we accept or fail to reject the null hypothesis and conclude that deviations are not statistically significant under our decision rule.

Results

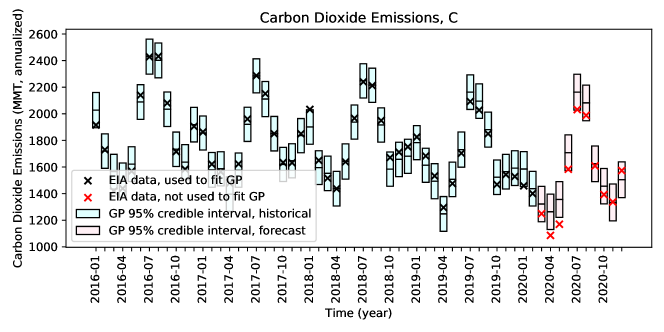

We show in Figure 1 deviations from the predictive distributions of power sector CO2 emissions generated by the GP regression. CO2 emissions are reported in million metric tonnes (MMT) of CO2 on an annualized basis. The black points show historical CO2 emissions values computed using Form EIA-923 and used to fit the GP regression model, and the red points show observed CO2 emissions values for COVID-19-concurrent months. The red points are not fitted to the GP regression model. The 95% CIs are shown by the shaded bars. Blue bars show historical variability in CO2 emissions and red bars show forecasted variability in the counterfactual scenario. The horizontal line within each 95% CI bar shows each GP regression mean (expected) value.

We report the numerical results of the GP regression in Table 1. Column “” shows the percent deviations from GP regression mean values and 95% CI bounds, in units of percent deviation, for each month March through December 2020. CO2 emissions values were lower than GP mean values from March through October 2020 and higher in November and December 2020. However, those deviations are outside of predicted 95% CIs in just two months immediately after shelter-in-place orders took effect, April and May 2020. Deviations are not statistically significant for any of the other ten months in the period.

Figure 1 shows that one monthly historical deviation from the GP regression mean, in January 2018, is outside of the 95% confidence interval. In January 2018, the “bomb cyclone” weather event in the Northeast and Mid-Atlantic caused electricity demand to increase and for relatively high-cost oil- and dual-fired generation resources to help meet that demand [38, 39].

Assessment of the Impacts of E and C/E on COVID-19-Related CO2 Emissions

We extend upon the statistical hypothesis tests that we present in Section 2 to determine the relative impacts of changes in electricity generation () and carbon intensity of electricity supply (C/E) on reductions in power sector CO2 emissions. We describe the data sources and methods that are used to estimate the impacts of changes in E and C/E on COVID-19-related reductions in CO2 emissions. The results of counterfactual analyses based on GP regression predictive distributions are presented.

Data

The steps we perform to obtain CO2 emissions time series are described in Section 2. We follow analogous steps to derive time series for E and C/E. Additionally, we use the same data sources that are described in Section 2 for data related to CO2 emissions, electricity generation, electricity generation by fuel type, and CO2 emissions by fuel type.

C E C/E March 2020 percent deviation (95% confidence interval bounds) -5.5% (+/- 10.0%) -3.3% (+/- 2.5%) -2.8% (+/- 7.0%) April 2020 percent deviation (95% confidence interval bounds) -14.0% (+/- 10.5%) -8.8% (+/- 2.5%) -8.6% (+/- 7.1%) May 2020 percent deviation (95% confidence interval bounds) -13.7% (+/- 9.9%) -5.7% (+/- 2.5%) -9.4% (+/- 7.1) June 2020 percent deviation (95% confidence interval bounds) -7.3% (+/- 7.9%) -2.4% (+- 2.1%) -5.5% (+/- 6.4) July 2020 percent deviation (95% confidence interval bounds) -6.1% (+/- 6.2%) -1.7% (+/- 1.9%) -2.8% (+/- 5.9%) August 2020 percent deviation (95% confidence interval bounds) -4.5% (+/- 6.4%) -2.7% (+/- 1.9%) -0.6% (+/- 6.0%) September 2020 percent deviation (95% confidence interval bounds) -1.0% (+/- 8.2%) -1.4% (+/- 2.3%) 0.9% (+/- 6.4%) October 2020 percent deviation (95% confidence interval bounds) -4.3% (+/- 9.1%) -3.8% (+/- 2.4%) -0.7% (+/- 6.7%) November 2020 percent deviation (95% confidence interval bounds) 0.3% (+/- 10.4%) -0.6% (+/- 2.6%) -1.3% (+/- 7.1%) December 2020 percent deviation (95% confidence interval bounds) 4.6% (+/- 8.9%) 1.6% (+/- 2.3%) 2.8% (+/- 6.6%) Average deviation, March through December 2020 -5.1% -2.9% -2.8%

Methods

We assess counterfactual and observed values of electricity generation () and carbon intensity of electricity supply (C/E). The counterfactual scenario assumes the continuation of historical power sector CO2 emissions in the absence of COVID-19. The same probabilistic modeling framework that is described in Section 2 is used to estimate counterfactual values for E and C/E.

As in our counterfactual analysis of CO2 emissions, we include a linear kernel, a bias kernel, and a constrained standard periodic kernel in the GP regressions to capture both short-term and medium-term trends in E and C/E over a period from January 2016 to February 2020. Linear and bias kernels are also used for HDD and CDD data. The GP regression-defined counterfactual data is compared to observed data from March to December 2020.

E and C/E are modeled independently and the joint relationships between those terms are not modeled. As such, the product of the E and C/E values in a given month is not necessarily equal to , the CO2 emissions that are computed in that month.

from Coal from Natural Gas from Oil Counterfactual Average Emissions, March-December 2020 (MMT, annualized) 853.5 674.7 9.8 Observed Average Emissions, March-December 2020 (MMT, annualized) 780.1 664.6 10.7 Average Percent Deviation, March-December 2020 -8.6% -2.0% 12.7%

Results

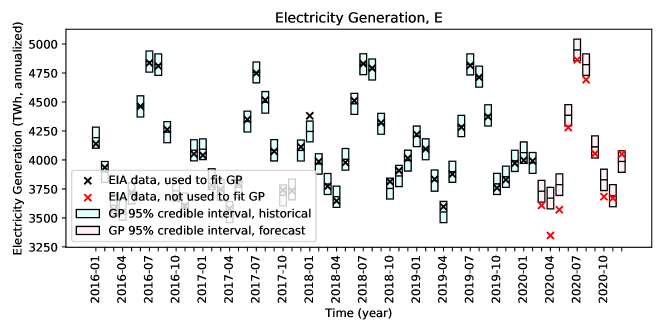

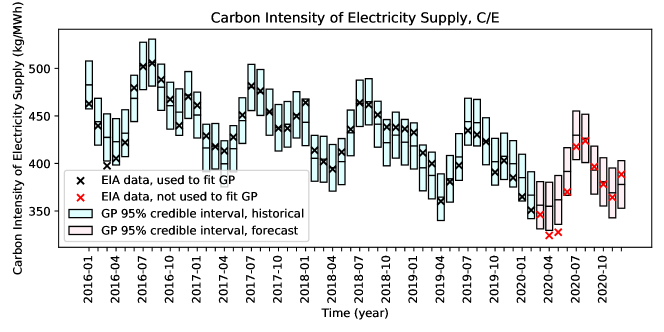

Columns “” and “C/E” in Table 1 show the percent deviations from GP regression mean values and 95% CI bounds for and C/E, respectively, relative to what we would expect in the counterfactual scenario in each month March through December 2020. Fig. 2 and Fig. 3 show the observed values, GP regressions, and counterfactual values for E and C/E, respectively. Fig. 2 shows that the observed values of E are outside of (lower than) the 95% CIs in six months: March, April, May, June, August, and October 2020. The observed values of C/E are outside of (lower than) the 95% CIs in only the two months that followed COVID-19 shelter-in-place orders: April and May 2020 (Fig. 3).

Additional GP regressions are performed to estimate the relative impacts on C/E associated with changes in coal-, natural gas-, and oil-fired electricity generation. The results of those GP regressions are shown in Table 2. The fuel-specific GP regressions exhibit more uncertainty than the regressions of C, E, and C/E. For example, the forecasted 95% CI for coal generation-related CO2 emissions in April 2020 accounts for +/- 24.9% of the mean forecasted value. This implies that that historical fuel-specific CO2 emissions, HDD, and CDD data are less predictive of future fuel-specific CO2 emissions using GP regressions than the same for total (fuel-agnostic) CO2 emissions, E, or C/E. Nevertheless, we find that the average reductions in CO2 emissions from coal- and natural gas-fired electricity generation are 8.6% and 2.0%, compared to an average increase in oil-fired generation of 12.7%. In the next section, we assess whether COVID-19 could accelerate coal-fired power plant retirements relative to a counterfactual scenario in which COVID-19 had not occurred.

Will COVID-19 Accelerate U.S. Coal Plant Retirements?

Coal generation capacity and utilization in the U.S. decreased every year after a peak in 2008 [40]. Such decreases persisted in recent years despite policy interventions by the Trump administration intended to support the coal industry [41]. Decreases in coal generation were driven by reductions in natural gas prices, flat or negative growth in electricity demand, and increasing state-level support for renewable generation technologies [42, 43, 44]. Additionally, some financial institutions are reluctant to support new coal power plants and refurbishments [45, 46].

In this section, we assess whether COVID-19 could accelerate coal plant retirements in the contiguous U.S. To evaluate potential retirements, we estimate the expected profitability through 2022 of each of the 845 coal-fired power plant units in the seven unbundled power market regions in the U.S. Those coal-fired power plant units comprise 74% of coal units, 67% of coal capacity, and 42% of power sector CO2 emissions in the contiguous U.S. [18].

Profitability is estimated in two scenarios: a counterfactual scenario in which we employ an electricity market price forecast developed prior to COVID-19-related shelter-in-place orders; and a scenario that reflects current expectations in which we use observed electricity market prices from March to December 2020 and an electricity market price forecast developed after shelter-in-place orders took effect. Both energy and capacity market revenues are taken into account. We identify coal plants that were expected to be profitable prior to COVID-19-related shelter-in-place orders but are no longer expected to be profitable due to expected reductions in electricity demand and prices. Those plants are considered to be at risk of retirement due to COVID-19.

Data

Estimates of coal-fired power plant profitability rely on data related to electricity market prices and capacity auction clearing prices. We also rely on data related to the locations, installed generating capacities, variable costs, and fixed costs of coal-fired electricity generation units.

Historical hourly zonal electricity market prices are obtained from S&P Global Market Intelligence (S&P) [47]. We obtain hourly historical price data for 57 electricity market zones for the period between January 1, 2018 and December 31, 2020.

Forecasts of monthly average regional electricity market prices are obtained from the EIA [48, 49]. The EIA publishes monthly average wholesale electricity market prices in a single zone in each electricity market region. Two market price forecasts published by the EIA are obtained: a forecast published in January 2020 prior to COVID-19-related shelter-in-place orders, and another forecast published in January 2021, after shelter-in-place orders took effect.

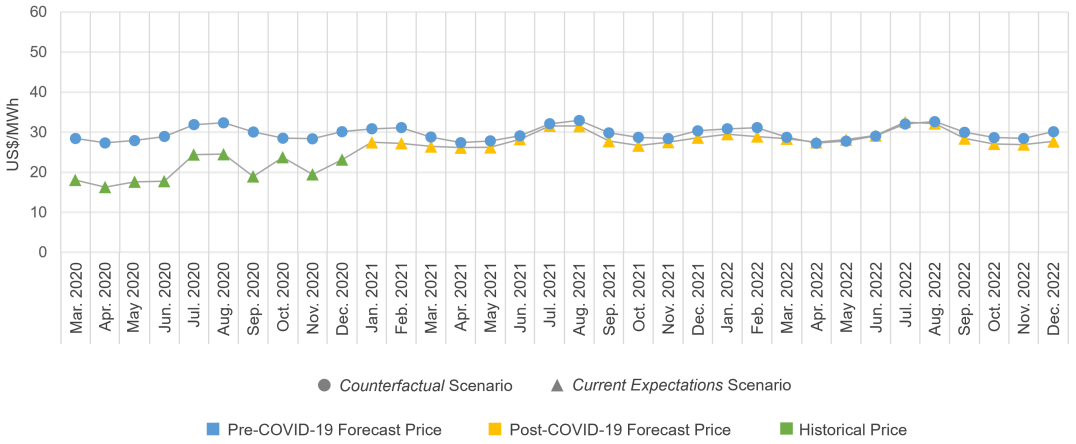

Two electricity market price scenarios are constructed, hourly for each zone, from the monthly EIA forecasts. A counterfactual hourly price scenario reflects the electricity market price forecasts from March 2020 through December 2022 published by the EIA in January 2020. The other hourly scenario reflects our current expectations of electricity market prices. The current expectations scenario reflects actual historical market prices from March through December 2020 and electricity market price forecasts from January 2021 through December 2022. Fig. 4 shows the capacity-weighted monthly average electricity prices in our counterfactual and current expectations scenarios.

Capacity auction clearing prices are obtained from S&P for the four electricity market regions that run forward capacity auctions: MISO, New England, New York, and PJM [50]. In these four regions, generators submit offers to electricity system operators to provide generation capacity in a future “capacity commitment period,” in exchange for payment from electricity system operators. MISO, New England, and PJM run annual capacity auctions for forward capacity commitment periods beginning June 1 and ending May 31. New York runs biannual capacity auctions that correspond to a winter capacity commitment period between November 1 and April 30, and a summer capacity commitment period between May 1 and October 31. Capacity auction clearing prices are established on a zonal basis.

We obtain actual zonal capacity auction clearing prices through May 31, 2023 for New England. For PJM, price data are available through May 31, 2022. We assume that prices for the subsequent annual commitment period, ending May 31, 2023, are the averages of the prices in the previous five periods. For MISO, price data are available through May 31, 2021. We assume that prices for the subsequent annual commitment periods, ending May 31, 2022 and 2023, are the averages of the prices in the previous four periods. For New York, price data is available through April 30, 2021. We assume that prices for the two subsequent summer commitment periods and the two subsequent winter periods are the averages of the prices in the previous three summer and winter periods, respectively.

The locations, installed generation capacities, and variable costs of each coal-fired electricity generation unit in the seven U.S. electricity market regions are obtained from S&P [18]. Such data is obtained for 2019, the latest year in which data is available. Those data report the regional and zonal locations of each generation unit, the month and year that each unit entered into service, the operating capacity of each unit, and the variable and fixed costs of each unit. Coal-fired cogeneration facilities that produce both electricity and heat are excluded. Such facilities typically supply electricity directly to industrial and commercial facilities. It is difficult to estimate the profitability of such units because they do not earn electricity market revenues for the electricity they supply directly to those facilities.

Finally, an estimate of the weighted average cost of capital (WACC) of coal-fired electricity generation units is obtained from the National Renewable Energy Laboratory Annual Technology Baseline 2019 (NREL ATB) [51]. We adopt an annual WACC of 4.61%.

Methods

The profitability of coal-fired power plant units is estimated. The profitability (P) for a given month (m) and generation unit (u) is calculated as that unit’s electricity and capacity market revenues ( and , respectively) net of variable operating costs and fixed operating and maintenance (O&M) costs ( and respectively):

| (1) |

We describe below the methods we use to estimate expected zonal hourly electricity market prices, monthly electricity market revenues and variable costs, monthly capacity market revenues, and overall profitability for the period between March 1, 2020 and December 31, 2022.

Zonal Hourly Electricity Market Prices

Profitability is estimated across two sets of electricity market prices: one set based on an electricity market price forecast published by the EIA in January 2020, prior to COVID-19-related shelter-in-place orders, and another set based on actual historical prices between March and December 2020 and an electricity market price forecast published by the EIA in January 2021.

Each of the seven electricity market regions has multiple electricity market zones. The EIA publishes average monthly market price forecasts for each of the seven electricity market regions. Those monthly regional market price forecasts are converted to hourly zonal market price forecasts. Such a step is necessary to accurately model expected electricity market revenues, variable costs, and capacity market revenues, which are allocated on a zonal basis. The following procedure is performed to determine the forecasted hourly prices in a given month and electricity market zone:

-

1.

For a given month and electricity market zone and region (e.g., June, AEP zone, PJM region), average prices in that month (e.g., June) are determined for each of the three years prior to 2021 for which we obtain historical data, 2018, 2019, and 2020.

-

2.

We compute the differences of those historical average prices with the corresponding monthly price forecast in the appropriate electricity market region (e.g., June 2020, PJM region) published by the EIA.

-

3.

The hourly prices from the historical month associated with the smallest difference that we compute in Step 2 are adopted as our hourly zonal forecast price profile.

-

4.

We shift the hourly zonal forecast price profile up or down by a constant value such that the average monthly zonal price (e.g., June 2020, AEP zone) is equal to the average monthly regional price (e.g., June 2020, PJM region) published by the EIA.

That series of steps is applied to each forecast month and each zone in each electricity market region. Two sets of hourly price forecasts are developed for each zone: one set based on monthly price forecasts published by the EIA in January 2020, prior to COVID-19-related shelter-in-place orders, and another set based on actual historical prices between March and December 2020, and monthly price forecasts published by the EIA in January 2021.

Monthly Electricity Market Profits and Variable Costs

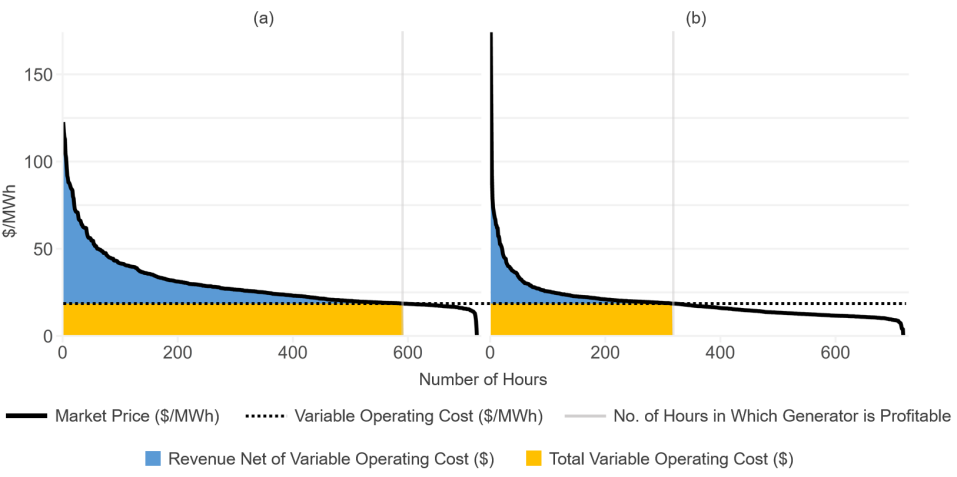

The electricity market revenue and variable operating costs for a given generation unit are estimated by determining the number of hours in a month in which that unit is online. We assume a generation unit is online for the hours in which the electricity market price is greater than or equal to the unit’s variable cost of operation. For each month, we generate a price duration curve (PDC) in which we order hourly electricity prices from highest to lowest. The PDC is used to estimate total variable operating costs and electricity market revenues.

The use of PDCs is illustrated in Fig. 5. In Fig. 5, we show two PDCs that correspond to hourly electricity prices in June 2020 in the AEP zone in the PJM region. The prices in Fig. 5 (a) reflect an electricity price forecast published by the EIA in January 2020, prior to shelter-in-place orders, and the prices in Fig. 5 (b) reflect actual prices in June 2020. The horizontal dashed lines reflect the variable operating cost ($/MWh) of a coal unit in the AEP zone, “Rockport ST1.” Monthly electricity market profits are shown in blue and monthly total variable operating costs ($) in yellow. The vertical grey lines indicate the numbers of hours in which it is profitable for Rockport ST1 to operate in each of the two scenarios.

Electricity market profits and variable operating costs are calculated for each of the 845 coal-fired generation units in the seven electricity market regions in the U.S.

Monthly Capacity Market Revenues

Four of the seven electricity market regions, MISO, New England, New York, and PJM, run annual or bi-annual generation capacity auctions in which those regional operators solicit bids from generation units to be available to provide capacity in a future capacity commitment period [50].

We assume that a generation unit bids into a capacity auction such that the unit can expect to be profitable if its bid clears in a given capacity commitment period. For a generation unit (u) that does not otherwise expect to be profitable in a given capacity commitment period (cp), that unit submits a capacity bid such that the present value of cash flows associated with its bid () would cover the present value of the sum of its variable costs and fixed O&M costs ( and respectively) net of the present value of electricity market revenues (). For a generation unit that does expect to be profitable in a given capacity commitment period, that unit bids zero dollars into the capacity auction for that period. Eq. 2 shows the bidding behavior for generation units that do not expect to be profitable in electricity markets alone, in a given capacity commitment period.

| (2) |

Capacity auction clearing prices are obtained or estimated for each capacity commitment period through 2022 for each of the four regions that run forward capacity auctions. Those clearing prices are established on a zonal basis. A generation unit that submits a bid that is equal to or lower than the auction clearing price receives capacity market revenues. A generation unit () that clears in a given commitment period () in a given zone () receives capacity market revenue () in a given month () equal to the zonal auction clearing price (), in units of $/MW-day, multiplied by the operating capacity of the unit () and the number of days in the month ():

| (3) |

Capacity market revenues are calculated for every coal-fired electricity generation unit in New England, New York, MISO, and PJM, and for every month in the period from March 1, 2020 to December 31, 2022.

Overall Profitability for the Period Between March 1, 2020 and December 31, 2022

The overall profitability of each coal-fired generation unit is estimated for the period between March 1, 2020 and December 31, 2022. The overall profitability () for each unit () is estimated as the sum of discounted cash flows in each month, where ranges from 1 to 34, the number of months in the period. is the monthly nominal net cash flow, and is the weighted average cost of capital (WACC) (Eq. 4). We apply a monthly WACC of 0.38% that we derive from an annual WACC of 4.61%, consistent with the NREL ATB.

| (4) |

The monthly nominal net cash flow () is the sum of monthly nominal electricity and capacity market revenues net of the sum of monthly nominal variable costs and fixed O&M costs. The profitability of every coal generation unit is calculated in two scenarios: a counterfactual scenario that relies on an electricity market price forecast published by the EIA in January 2020 prior to shelter-in-place orders, and a scenario that reflects our current expectations and is based on actual prices in March through December, and a price forecast published by the EIA in January 2021.

Results

We analyze the expected profitability from March 2020 to December 2022 of the 845 coal-fired electricity generation units operating in the seven unbundled power market regions in the United States. 90 of the 845 coal-fired generation units, representing only 2.8 GW or 1.9% of coal generation capacity in the seven power market regions, were expected to be profitable prior to COVID-19 but are no longer expected to be profitable due to COVID-19-related reductions in electricity prices. We consider those 90 units to be at risk of early retirement due to COVID-19. The mean age and operating capacity of those 90 units are 59.1 years and 31.1 MW, respectively. The newest units were operational in November 2012 and the oldest unit was operational in July 1954. A single at-risk unit resides in SPP, while the remaining units reside in MISO: 79 units in MISO Zone 6, nine units in MISO Zone 4, and one unit in MISO Zone 9.

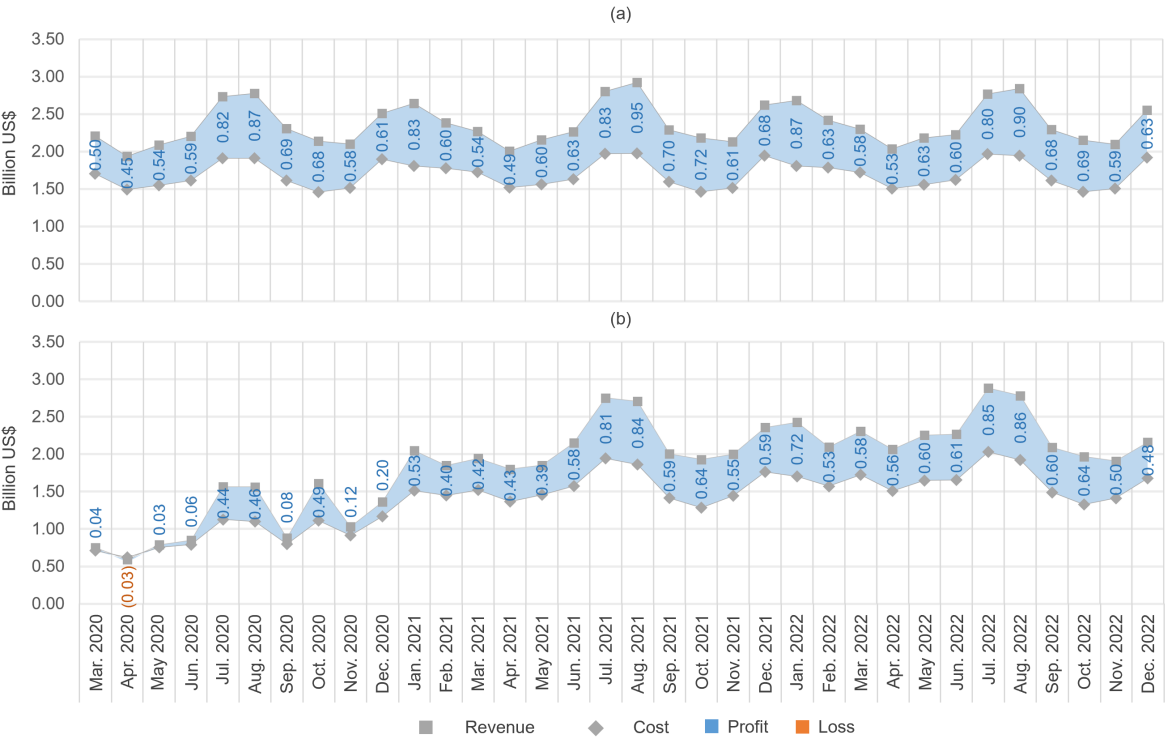

Estimates of the impacts of COVID-19 on the monthly profitability of coal-fired electricity generation units in aggregate are illustrated in Fig. 6. Fig. 6 (a) shows estimates in the counterfactual scenario, and Fig. 6 (b) shows estimates in the current expectations scenario. Squares represent monthly revenues, diamonds represent monthly costs, and the shaded areas represent monthly profits or losses. Coal generation units in total are $6.5 billion less profitable in the current expectations scenario relative to the counterfactual scenario over the entire period, in present value terms. Of that amount, coal generation units earn $4.5 billion less profit in the current expectations scenario in March through December 2020.

Discussion

Multiple studies conclude that COVID-19 is responsible for reductions in U.S. power sector CO2 emissions [2, 5, 9, 10] and others conclude that the reduction in CO2 emissions or electricity demand is permanent [3, 4, 13, 52]. For example, researchers conclude in a recent report [13] that COVID-19-related shelter-in-place orders could trigger a sustained long-term reduction in U.S. electricity demand of 65-160 terawatt-hours, or 1.6-4.0% of annual electricity demand. In their central scenario, the authors estimate a transition of about 11% of U.S. office workers to permanent work-from-home positions, permanent decreases in office and retail-related electricity consumption, and a permanent increase in residential electricity consumption.

We find little evidence of permanent reductions in our analysis of observed changes in U.S. power sector CO2 emissions in the context of normal historical variability. We report statistically significant reductions in CO2 emissions () in only April and May 2020, and thereafter a return to the levels of CO2 emissions that we would expect in the absence of COVID-19 (Section 2 and Fig. 1).

With respect to electricity generation () and carbon intensity of electricity supply ()—two factors that bear on power sector CO2 emissions—we report returns to levels that we would have expected in the absence of COVID-19.

For , we observe statistically significant reductions in March, April, May, June, August, and October 2020 compared to what we would have expected in absence of COVID-19, but observe values within typical ranges in November and December 2020 (Fig. 2 and Table 1).

Qualitatively, we expect to remain in typical ranges as economic activity in the U.S. returns to pre-COVID-19 levels. While the U.S. Bureau of Economic Analysis estimates that U.S. real gross domestic product (GDP) declined 9.0% in the second quarter of 2020 relative to real GDP in those quarters in 2019 [53], GDP in the third and fourth quarters were only down 2.8%, and 2.5%. A first COVID-19 economic relief bill was signed into law by President Trump on March 27, 2020 and a second by President Biden on March 11, 2021. Owing to these developments and to the expected continued distribution of effective COVID-19 vaccinations, the Board of Governors of the Federal Reserve System, the U.S. Congressional Budget Office, the Organization for Economic Co-Operation and Development, and other authorities anticipate a return to pre-COVID-19 economic growth rates in 2021 [54, 55, 56, 57, 58].

With respect to C/E, we observe statistically significant reductions in April and May 2020 and a subsequent return to levels that we would expect in the absence of COVID-19 (Fig. 3 and Table 1). Nonetheless, we show an average reduction in CO2 emissions associated with coal-fired electricity generation of 8.6% compared to an average reduction in natural gas-fired CO2 emissions of only 2.0% (Table 2). We explore the possibility of COVID-19-related coal power plant retirements and find that COVID-19 is likely to put at risk of retirement less than 2% of coal generation capacity in the contiguous U.S. through 2022 (Section 4).

Much of the literature on the impacts of COVID-19 on CO2 emissions assumes a causal relationship between the two. Ours is one of the first studies to explore whether such a relationship exists. We do not find evidence that COVID-19 is linked to a reduction in U.S. power sector CO2 emissions except in the two months immediately following shelter-in-place orders. Nor do we find evidence that COVID-19 is likely to drive out of business more than a small percentage of U.S. coal generation facilities. We observe returns to pre-COVID-19 levels of CO2 emissions, electricity generation, and carbon intensity of electricity supply.

Author Contributions

The authors worked collectively to design the study. SL, PS, and DS performed the GP regression data analysis with guidance from ML. ML and PS developed the energy and capacity market profitability model with guidance from SL. ML, TC, DS, and SL drafted and edited the manuscript. All authors approved the submitted version.

Competing Interests

The authors declare no competing interests.

Acknowledgements

The authors would like to thank Dr. Jesse D. Jenkins and Dr. David Harrison for reviewing a draft of this work. They would also like to thank Dr. Edward S. Rubin, Doug Houseman, Bruce Nilles, Laura Martin, Ted Nace, Dr. Christopher Greig, Dr. Christian Hauenstein, and Dr. Audun Botterud for providing expertise with respect to coal power plant investment decisions and capacity market bidding behavior.

Data availability

All of the data that support the findings of this study are publicly available via the sources and web links provided in the References section of this paper. The exception is data furnished by S&P, which was made available to Max Luke, an employee of NERA Economic Consulting (NERA), via NERA’s paid subscription to S&P Global Market Intelligence service.

Code availability

Full open source Python code and Excel calculations to replicate the results presented in this paper are available via GitHub at the following URL: https://github.com/highlandenergy/no-covid-19-climate-silver-lining-in-the-us-power-sector [59].

References

- [1] International Energy Agency, “Global Energy Review 2020: The Impacts of the COVID-19 Crisis on Global Energy Demand and CO2 Emissions,” tech. rep., 2020.

- [2] C. Le Quéré, R. B. Jackson, M. W. Jones, A. J. Smith, S. Abernethy, R. M. Andrew, A. J. De-Gol, D. R. Willis, Y. Shan, J. G. Canadell, P. Friedlingstein, F. Creutzig, and G. P. Peters, “Temporary reduction in daily global CO2 emissions during the COVID-19 forced confinement,” Nature Climate Change, 2020.

- [3] Y. Shan, J. Ou, D. Wang, Z. Zeng, S. Zhang, D. Guan, and K. Hubacek, “Impacts of COVID-19 and fiscal stimuli on global emissions and the Paris Agreement,” Nature Climate Change, 2020.

- [4] C. Le Quéré, G. P. Peters, P. Friedlingstein, R. M. Andrew, J. G. Canadell, S. J. Davis, R. B. Jackson, and M. W. Jones, “Fossil CO2 emissions in the post-COVID-19 era,” Nature Climate Change, 2021.

- [5] Z. Liu, Z. Deng, P. Ciais, R. Lei, S. J. Davis, S. Feng, B. Zheng, D. Cui, X. Dou, P. He, B. Zhu, C. Lu, P. Ke, T. Sun, Y. Wang, X. Yue, Y. Wang, Y. Lei, H. Zhou, Z. Cai, Y. Wu, R. Guo, T. Han, J. Xue, O. Boucher, F. Chevallier, E. Boucher, Y. Wei, Q. Zhang, D. Guan, P. Gong, D. M. Kammen, K. He, and H. J. Schellnhuber, “COVID-19 causes record decline in global CO2 emissions,” 2020.

- [6] L. Myllyvirta, “Coronavirus temporarily reduced China’s CO2 emissions by a quarter.” https://www.carbonbrief.org/analysis-coronavirus-has-temporarily-reduced-chinas-co2-emissions-by-a-quarter, February 2020. Accessed: 2020-05-25.

- [7] S. Evans, “Analysis: Coronavirus set to cause largest ever annual fall in CO2 emissions.” https://www.carbonbrief.org/analysis-coronavirus-set-to-cause-largest-ever-annual-fall-in-co2-emissions, April 2020. Accessed: 2020-04-25.

- [8] Z. Hausfather, “COVID-19 Could Result in Much Larger CO2 Drop in 2020.” https://thebreakthrough.org/issues/energy/covid-co2-drop, April 2020.

- [9] K. T. Gillingham, C. R. Knittel, J. Li, M. Ovaere, and M. Reguant, “The Short-run and Long-run Effects of Covid-19 on Energy and the Environment,” Joule, 2020.

- [10] C. Bertram, G. Luderer, F. Creutzig, N. Bauer, F. Ueckerdt, A. Malik, and O. Edenhofer, “COVID-19-induced low power demand and market forces starkly reduce CO2 emissions,” Nature Climate Change, 2021.

- [11] J. López Prol and O. Sungmin, “Impact of COVID-19 Measures on Short-Term Electricity Consumption in the Most Affected EU Countries and USA States,” iScience, 2020.

- [12] D. Agdas and P. Barooah, “Impact of the COVID-19 Pandemic on the U.S. Electricity Demand and Supply: An Early View From Data,” IEEE Access, 2020.

- [13] Center on Global Energy Policy, Columbia University, “Potential Implications of the COVID-19 Crisis on Long-Term Electricity Demand in the United States,” tech. rep., 2020.

- [14] S&P Global, “The Energy Transition And COVID-19: A Pivotal Moment For Climate Policies And Energy Companies,” tech. rep., 2020.

- [15] S&P Global, “COVID-19 Could Make 2020 Crucial for Renewables.” https://www.spglobal.com/en/research-insights/featured/covid-19-could-make-2020-crucial-for-renewables. Accessed: 2021-02-22.

- [16] U.S. Energy Information Administration, “2018 State energy-related carbon dioxide emissions by sector.” https://www.eia.gov/environment/emissions/state/excel/table4.xlsx, March 2021. Accessed: 2021-03-26.

- [17] Clean Air Task Force, “Factsheet: State and utility climate change targets shift to carbon reductions, technology diversity,” tech. rep., November 2019.

- [18] S&P Global Market Intelligence, “Asset Data, Power Plant Units.” Paid subscription service.

- [19] U.S. Energy Information Administration, “Form EIA-923 detailed data with previous form data (EIA-906/920).” https://www.eia.gov/electricity/data/eia923, April 2020. Accessed: 2020-05-13.

- [20] U.S. Energy Information Administration, “Carbon Dioxide Emissions Coefficients.” http://www.eia.gov/environment/emissions/co2_vol_mass.cfm, February 2016. Accessed: 2020-05-05.

- [21] U.S. Energy Information Administration, “Table A.3. Carbon Dioxide Uncontrolled Emission Factors.” https://www.eia.gov/electricity/annual/html/epa_a_03.html, February 2016. Accessed: 2021-03-05.

- [22] U.S. Environmental Protection Agency, “Emission Factors for Greenhouse Gas Inventories.” https://www.epa.gov/sites/production/files/2015-07/documents/emission-factors_2014.pdf, April 2014. Accessed: 2021-03-05.

- [23] U.S. Energy Information Administration, “Short-Term Energy Outlook Data Browser.” https://www.eia.gov/outlooks/steo/data/browser/, February 2021. Accessed: 2021-01-15.

- [24] C. E. Rasmussen and C. K. Williams, Gaussian Processes for Machine Learning, vol. 1. MIT press Cambridge, 2006.

- [25] GPy, “GPy: A gaussian process framework in python.” http://github.com/SheffieldML/GPy, since 2012.

- [26] A. Zeng, H. Ho, and Y. Yu, “Prediction of building electricity usage using Gaussian Process Regression,” Journal of Building Engineering, vol. 28, p. 101054, 2020.

- [27] P. Kou, D. Liang, L. Gao, and J. Lou, “Probabilistic electricity price forecasting with variational heteroscedastic Gaussian process and active learning,” Energy Conversion and Management, vol. 89, pp. 298–308, 2015.

- [28] H. Sheng, J. Xiao, Y. Cheng, Q. Ni, and S. Wang, “Short-term solar power forecasting based on weighted Gaussian process regression,” IEEE Transactions on Industrial Electronics, vol. 65, no. 1, pp. 300–308, 2017.

- [29] N. Chen, Z. Qian, I. T. Nabney, and X. Meng, “Wind power forecasts using Gaussian processes and numerical weather prediction,” IEEE Transactions on Power Systems, vol. 29, no. 2, pp. 656–665, 2013.

- [30] M. Sharifzadeh, A. Sikinioti-Lock, and N. Shah, “Machine-learning methods for integrated renewable power generation: A comparative study of artificial neural networks, support vector regression, and Gaussian Process Regression,” Renewable and Sustainable Energy Reviews, vol. 108, pp. 513–538, 2019.

- [31] J. Lee, P. Zhang, L. K. Gan, D. A. Howey, M. A. Osborne, A. Tosi, and S. Duncan, “Optimal operation of an energy management system using model predictive control and Gaussian process time-series modeling,” IEEE Journal of Emerging and Selected Topics in Power Electronics, vol. 6, no. 4, pp. 1783–1795, 2018.

- [32] G. O. Sahinoglu, M. Pajovic, Z. Sahinoglu, Y. Wang, P. V. Orlik, and T. Wada, “Battery state-of-charge estimation based on regular/recurrent Gaussian process regression,” IEEE Transactions on Industrial Electronics, vol. 65, no. 5, pp. 4311–4321, 2017.

- [33] D. Fang, X. Zhang, Q. Yu, T. C. Jin, and L. Tian, “A novel method for carbon dioxide emission forecasting based on improved Gaussian processes regression,” Journal of cleaner production, vol. 173, pp. 143–150, 2018.

- [34] S. J. Lee, Adaptive electricity access planning. Massachusetts Institute of Technology, 2018.

- [35] P. Virtanen, R. Gommers, T. E. Oliphant, M. Haberland, T. Reddy, D. Cournapeau, E. Burovski, P. Peterson, W. Weckesser, J. Bright, S. J. van der Walt, M. Brett, J. Wilson, K. Jarrod Millman, N. Mayorov, A. R. J. Nelson, E. Jones, R. Kern, E. Larson, C. Carey, İ. Polat, Y. Feng, E. W. Moore, J. Vand erPlas, D. Laxalde, J. Perktold, R. Cimrman, I. Henriksen, E. A. Quintero, C. R. Harris, A. M. Archibald, A. H. Ribeiro, F. Pedregosa, P. van Mulbregt, and S. . . Contributors, “SciPy 1.0: Fundamental Algorithms for Scientific Computing in Python,” Nature Methods, vol. 17, pp. 261–272, 2020.

- [36] R. H. Byrd, P. Lu, J. Nocedal, and C. Zhu, “A limited memory algorithm for bound constrained optimization,” SIAM Journal on scientific computing, vol. 16, no. 5, pp. 1190–1208, 1995.

- [37] C. Zhu, R. H. Byrd, P. Lu, and J. Nocedal, “Algorithm 778: L-bfgs-b: Fortran subroutines for large-scale bound-constrained optimization,” ACM Transactions on Mathematical Software (TOMS), vol. 23, no. 4, pp. 550–560, 1997.

- [38] A. Lee, “January’s cold weather affects electricity generation mix in Northeast, Mid-Atlantic,” 2018. Accessed: 2020-07-18.

- [39] U. E. I. Administration, “Northeastern Winter Energy Alert.” https://www.eia.gov/special/alert/east_coast/, January 2018. Accessed: 2021-03-21.

- [40] W. J. Culver and M. Hong, “Coal’s decline: Driven by policy or technology?,” The Electricity Journal, vol. 29, no. 7, pp. 50–61, 2016.

- [41] R. Mendelevitch, C. Hauenstein, and F. Holz, “The death spiral of coal in the US: will changes in US Policy turn the tide?,” Climate Policy, vol. 19, no. 10, pp. 1310–1324, 2019.

- [42] J. Coglianese, T. D. Gerarden, and J. H. Stock, “The effects of fuel prices, environmental regulations, and other factors on US Coal Production, 2008-2016,” The Energy Journal, vol. 41, no. 1, 2020.

- [43] A. Benn, P. Bodnar, J. Mitchell, and J. Waller, Managing the Coal Capital Transition: Collaborative Opportunities for Asset Owners, Policymakers, and Environmental Advocates. Rocky Mountain Institute, 2018.

- [44] U.S. Energy Information Administration, “Most coal plants in the United States were built before 1990.” https://www.eia.gov/todayinenergy/detail.php?id=30812, April 2017. Accessed: 2020-06-25.

- [45] J. Smyth, “Major banks announce new policies to help push utilities away from coal.” https://www.energyandpolicy.org/major-banks-announce-new-policies-to-help-push-utilities-away-from-coal, May 2020. Accessed: 2020-06-25.

- [46] G. Readfearn, “Adani mine: three major insurers to have no further involvement in coal project.” https://www.theguardian.com/environment/2020/jun/12/adani-mine-three-major-insurers-to-have-no-further-involvement-in-coal-project, June 2020. Accessed: 2020-06-25.

- [47] S&P Global Market Intelligence, “ISO Real-Time Prices.” Paid subscription service.

- [48] U.S. Energy Information Administration, “Short-Term Energy Outlook, January 2020.” https://www.eia.gov/outlooks/steo/archives/jan20_base.xlsx. Accessed: 2020-08-06.

- [49] U.S. Energy Information Administration, “Short-Term Energy Outlook, January 2021.” https://www.eia.gov/outlooks/steo/archives/jan21_base.xlsx. Accessed: 2020-08-06.

- [50] S&P Global Market Intelligence, “ISO Capacity Auction Results.” Paid subscription service.

- [51] U.S. National Renewable Energy Laboratory, “Annual Technology Baseline 2019.” https://data.nrel.gov/system/files/115/2019-ATB-data.xlsm. Accessed: 2020-08-06.

- [52] J. Mendez, M. Meyer, J. Leaton, B. Nelson, and J. Hempstead, “Coronavirus-related power demand reductions drive lower carbon emissions,” tech. rep., Moody’s, 2020.

- [53] U.S. Bureau of Economic Analysis, “National Income and Product Accounts, 2020, Q4, Advance Release.” https://apps.bea.gov/histdata/Releases/GDP_and_PI/2019/Q4/Third_March-27-2020/Section1all_xls.xlsx. Accessed: 2021-02-21.

- [54] Board of Governors of the Federal Reserve System, “December 16, 2020: FOMC Projections materials, accessible version.” https://www.federalreserve.gov/monetarypolicy/fomcprojtabl20201216.htm. Accessed: 2021-02-21.

- [55] Congressional Budget Office, “An Overview of the Economic Outlook: 2021 to 2031,” tech. rep., February 2021.

- [56] Organization for Economic Co-Operation and Development, “Real GDP forecast: DEC 2020 forecast, Annual growth rate (%), Q4 2019 – Q4 2022.” https://data.oecd.org/gdp/real-gdp-forecast.htm. Accessed: 2021-02-21.

- [57] Deloitte, “United States Economic Forecast 4th Quarter 2020.” https://www2.deloitte.com/us/en/insights/economy/us-economic-forecast/united-states-outlook-analysis.html. Accessed: 2021-02-21.

- [58] Toronto Dominion, “U.S. Quarterly Economic Forecast COVID-19, Vaccines, Knowns & Unknowns.” https://economics.td.com/us-quarterly-economic-forecast. Accessed: 2021-02-21.

- [59] S. J. Lee and M. Luke, “No covid-19 climate silver lining in the us power sector.” https://github.com/highlandenergy/no-covid-19-climate-silver-lining-in-the-us-power-sector, 2021.