Marginalization of Regression-Adjusted Treatment Effects in Indirect Comparisons with Limited Patient-Level Data

Abstract

Population adjustment methods such as matching-adjusted indirect comparison (MAIC) are increasingly used to compare marginal treatment effects when there are cross-trial differences in effect modifiers and limited patient-level data. MAIC is based on propensity score weighting, which is sensitive to poor covariate overlap and cannot extrapolate beyond the observed covariate space. Current outcome regression-based alternatives can extrapolate but target a conditional treatment effect that is incompatible in the indirect comparison. When adjusting for covariates, one must integrate or average the conditional estimate over the population of interest to recover a compatible marginal treatment effect. We propose a marginalization method based on parametric G-computation that can be easily applied where the outcome regression is a generalized linear model or a Cox model. In addition, we introduce a novel general-purpose method based on the ideas underlying multiple imputation, which we term multiple imputation marginalization (MIM) and is applicable to a wide range of models, including parametric survival models. The approaches view the covariate adjustment regression as a nuisance model and separate its estimation from the evaluation of the marginal treatment effect of interest. Both methods can accommodate a Bayesian statistical framework, which naturally integrates the analysis into a probabilistic framework. A simulation study provides proof-of-principle for the methods and benchmarks their performance against MAIC and the conventional outcome regression. The simulations are based on scenarios with binary outcomes and continuous covariates, with the log-odds ratio as the measure of effect. The marginalized outcome regression approaches achieve more precise and more accurate estimates than MAIC, particularly when covariate overlap is poor, and yield unbiased marginal treatment effect estimates under no failures of assumptions. Furthermore, the marginalized regression-adjusted estimates provide greater precision and accuracy than the conditional estimates produced by the conventional outcome regression, which are systematically biased because the log-odds ratio is a non-collapsible measure of effect. Keywords: Health technology assessment; indirect treatment comparison; causal inference; marginal treatment effect; outcome regression; standardization

1 Introduction

The development of novel pharmaceuticals requires several stages, which include regulatory evaluation and, in several jurisdictions, health technology assessment (HTA).[1] To obtain regulatory approval, a new technology must demonstrate efficacy and randomized controlled trials (RCTs) are the gold standard for this purpose, due to their potential in limiting bias.[2] Evidence supporting regulatory approval is often provided by a two-arm RCT, typically comparing the new technology to placebo or standard of care. Then, in certain jurisdictions, HTA addresses whether the health care technology should be publicly funded by the health care system. For HTA, manufacturers must convince payers that their product offers the best “value for money” of all available options in the market. This demands more than a demonstration of efficacy[3] and will often require the comparison of treatments that have not been trialed against each other.[4]

In the absence of head-to-head trials, indirect treatment comparisons (ITCs) are at the top of the hierarchy of evidence to inform treatment and reimbursement decisions, and are very prevalent in HTA.[5] Standard ITCs use indirect evidence obtained from RCTs through a common comparator arm.[5, 6] These techniques are compatible with both individual patient data (IPD) and aggregate-level data (ALD). However, they are biased when the distribution of effect measure modifiers differs across trial populations, meaning that relative treatment effects are not constant.[7]

Often in HTA, there are: (1) no head-to-head trials comparing the interventions of interest; (2) IPD available from the manufacturer’s own trial but only published ALD for the comparator(s); and (3) imbalances in effect measure modifiers across studies. Several “pairwise” methods, labeled population-adjusted indirect comparisons, have been introduced to estimate relative treatment effects in this scenario. These include matching-adjusted indirect comparison (MAIC),[8] based on inverse propensity score weighting, and simulated treatment comparison (STC),[9] based on outcome modeling/regression. There is a simpler alternative, crude direct post-stratification (also known as non-parametric standardization, subclassification or direct adjustment)[10], but this fails if any of the covariates are continuous or where there are several covariates for which one must account,[11] in which case it is also inefficient. Very recently, a relevant outcome modeling-based approach called multilevel network meta-regression (ML-NMR) has been developed.[12, 13] This incorporates larger networks of treatments and studies. The focus of this article is on the pairwise approaches but ML-NMR is considered in the discussion.

Recommendations on the use of MAIC and STC in HTA have been provided, defining the relevant terminology and evaluating the theoretical validity of these methods.[7, 14] However, this guidance is only provisional as further research must: (1) examine these methods through comprehensive simulation studies; and (2) develop novel methods for population adjustment.[7, 14] In addition, recommendations have highlighted the importance of embedding the methods within a Bayesian framework, which allows for the principled propagation of uncertainty to the wider health economic model,[15] and is particularly appealing for “probabilistic sensitivity analysis”.[16] This is a required component in the normative framework of HTA bodies such as NICE,[15, 16] used to characterize the impact of the uncertainty in the model inputs on decision-making.

Recently, several simulation studies have been conducted to assess population-adjusted indirect comparisons.[17, 18, 19, 20] Remiro-Azócar et al. perform a simulation study benchmarking the performance of the typical use of MAIC and STC against the standard ITC for the Cox model and survival outcomes.[17] In this study, MAIC yields unbiased and relatively accurate treatment effect estimates under no failures of assumptions, but the robust sandwich variance may underestimate standard errors where effective sample sizes are small. In the simulation scenarios, there is some degree of overlap between the studies’ covariate distributions. Nevertheless, it is well known that weighting methods like MAIC are highly sensitive to poor overlap, are not asymptotically efficient, and incapable of extrapolation.[20, 21, 22, 23] With poor overlap, extreme weights may produce unstable treatment effect estimates with high variance. A related problem in finite samples is that feasible weighting solutions may not exist[24] due to separation problems where samples sizes are small and the number of covariates is large.[25, 26]

Outcome regression approaches such as STC are appealing as these tend to be more efficient than weighting, providing more stable estimators and allowing for model extrapolation.[27] We view extrapolation as an advantage because poor overlap, with small effective sample sizes and large percentage reductions in effective sample size, is a pervasive issue in HTA.[28] While extrapolation can also be viewed as a disadvantage if it is not valid, in our case it expands the range of scenarios in which population adjustment can be used.

The aforementioned simulation study[17] demonstrates that the typical usage of STC, as described by HTA guidance and recommendations,[14] produces systematically biased estimates of the marginal treatment effect, with inappropriate coverage rates, because it targets a conditional estimand instead. With the Cox model and survival outcomes, there is bias because the conditional (log) hazard ratio is non-collapsible. In addition, the conditional estimand cannot be combined in any indirect treatment comparison or compared between studies because non-collapsible conditional estimands vary across different covariate adjustment sets. This is a recurring problem in meta-analysis.[29, 30]

The crucial element that has been missing from the typical usage of STC is the marginalization of treatment effect estimates. When adjusting for covariates, one must integrate or average the conditional estimate over the joint covariate distribution to recover a marginal treatment effect that is compatible in the indirect comparison. We propose a simple marginalization method based on parametric G-computation[31, 32] or model-based standardization,[33, 34, 35, 36] often applied in observational studies in epidemiology and medical research where treatment assignment is non-random. In meta-analysis, Vo et al.[37, 38] have used parametric G-computation to transport RCT results to a specific target population. We extend these approaches to population-adjusted indirect comparisons with limited patient-level data. In addition, we introduce a novel general-purpose method based on the ideas underlying multiple imputation,[39] which we term multiple imputation marginalization (MIM) and is applicable to a wide range of models, including parametric survival models.

Both parametric G-computation and multiple imputation marginalization can be viewed as extensions to the conventional STC, with all methods making use of effectively the same outcome model. The novel methodologies are outcome regression approaches, thereby capable of extrapolation, that target marginal treatment effects. They do so by separating the covariate adjustment regression model from the evaluation of the marginal treatment effect of interest. The conditional parameters of the regression are viewed as nuisance parameters, not directly relevant to the research question. The methods can be implemented in a Bayesian statistical framework, which explicitly accounts for relevant sources of uncertainty, allows for the incorporation of prior evidence (e.g. expert opinion), and naturally integrates the analysis into a probabilistic framework, typically required for HTA.[15]

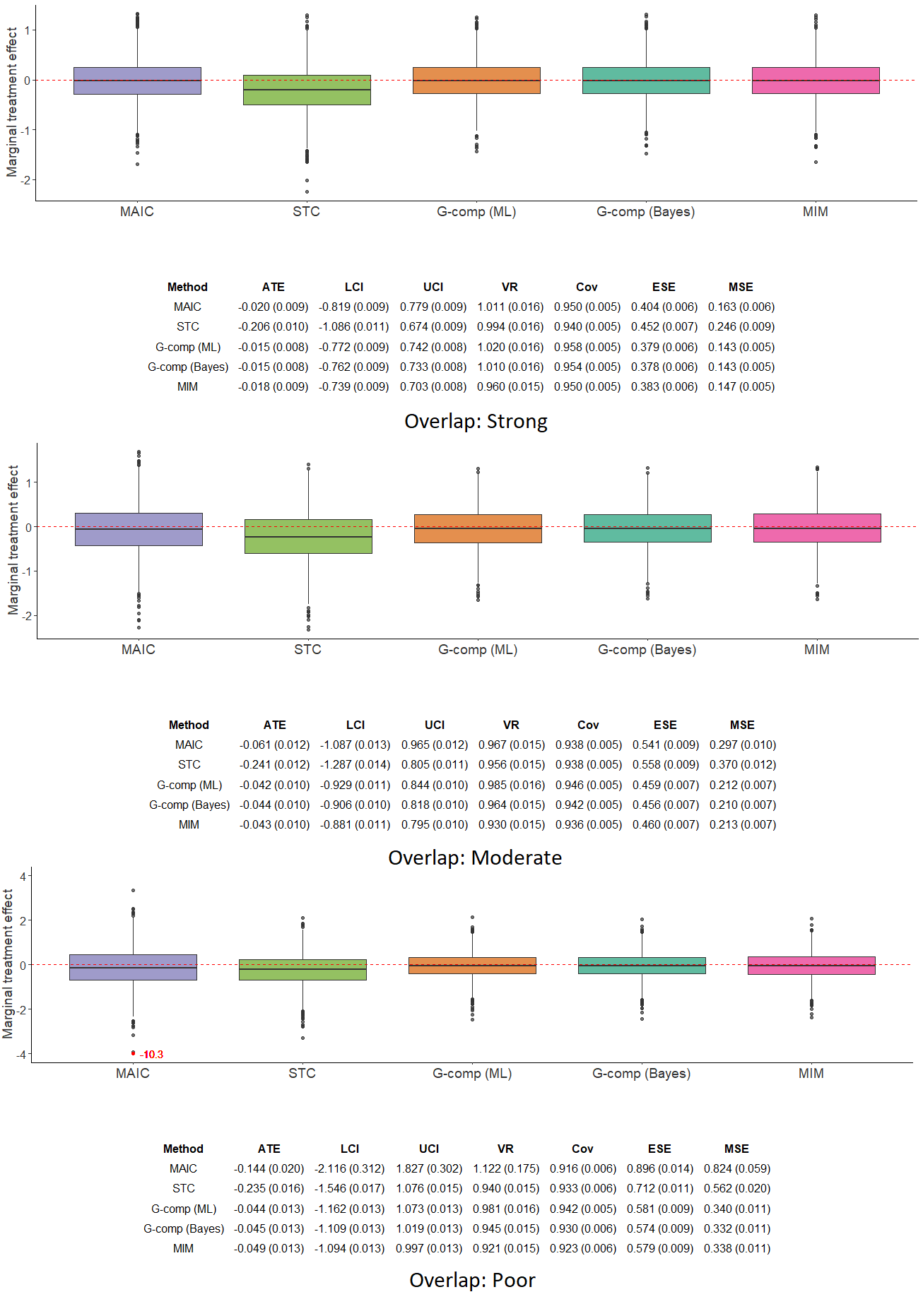

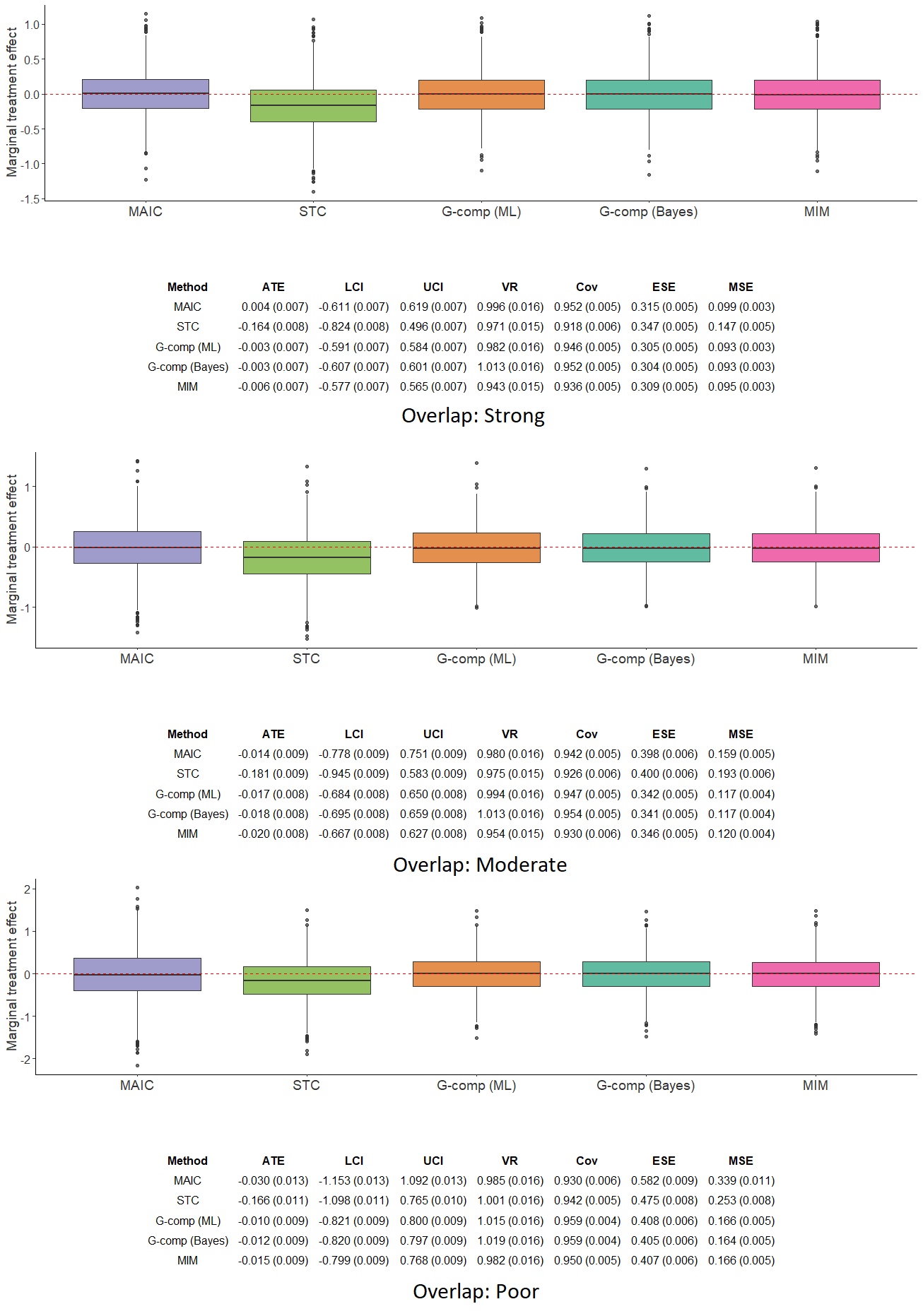

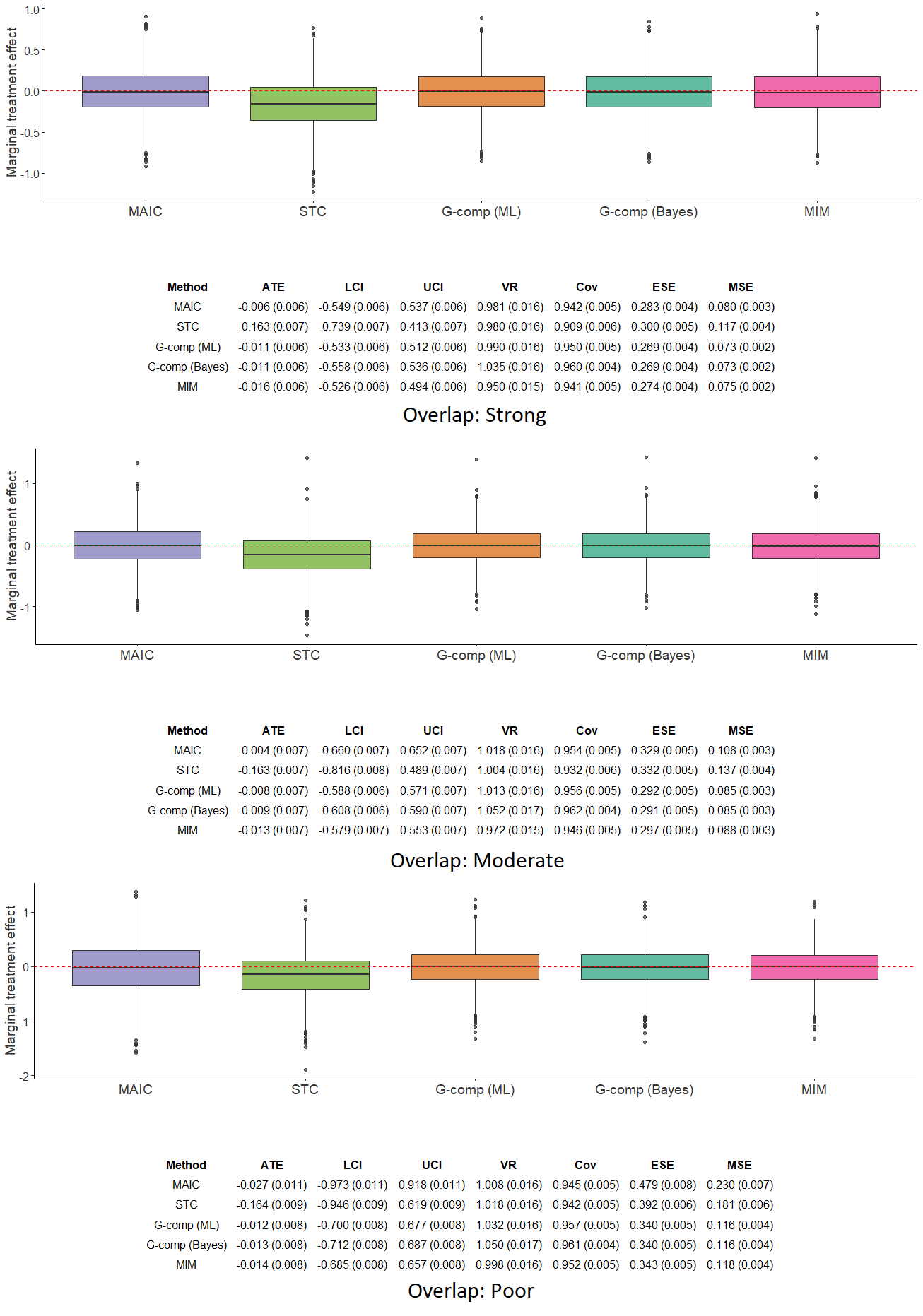

In this paper, we carry out a simulation study to benchmark the performance of the novel methods against MAIC and the conventional STC. The simulations provide proof-of-principle and are based on scenarios with binary outcomes and continuous covariates, with the log-odds ratio as the measure of effect. The marginalized outcome regression approaches achieve greater precision and accuracy than MAIC and are unbiased under no failures of assumptions. Furthermore, the marginalized regression-adjusted estimates provide greater precision than the conditional estimates produced by the conventional version of STC. While this precision comparison is irrelevant, because it is made for estimators of different estimands, it supports previous research on non-collapsible measures of effect.[33, 30]

In Section 2, we present the context and data requirements for population-adjusted indirect comparisons. Section 3 provides a detailed description of the outcome regression methodologies. Section 4 outlines a simulation study, which evaluates the statistical properties of different approaches to outcome regression with respect to MAIC. Section 5 describes the results from the simulation study. An extended discussion of our findings is presented in Section 6.

2 Context

Consider an active treatment , which needs to be compared to another active treatment for the purposes of reimbursement. Treatment is new and being tested for cost-effectiveness, while treatment is typically an established intervention, already on the market. Both treatments have been evaluated in a RCT against a common comparator , e.g. standard of care or placebo, but not against each other. Indirect comparisons are performed to estimate the relative treatment effect for a specific outcome. The objective is to perform the analysis that would be conducted in a hypothetical head-to-head RCT between and , which indirect treatment comparisons seek to emulate.

The RCT is widely considered the gold standard design to evaluate treatments[40] due to its internal validity.[2] Appropriate randomization guarantees covariate balance on expectation, so that the treatment groups are comparable and confounding is limited. Therefore, assuming no structural issues (e.g. no dropout, measurement error, etc.), RCTs allow for unbiased estimation of the relative treatment effect within the study.

RCTs have different types of potential target average estimands of interest: marginal or population-average effects, calibrated at the population level, and conditional effects, calibrated at the individual level. The former are typically, but not necessarily, estimated by an “unadjusted” analysis. This may be a simple comparison of the expected outcomes for each group or a univariable regression including only the main treatment effect. Conditional treatment effects are typically estimated by an “adjusted” analysis (e.g. a multivariable regression of outcome on treatment and covariates), accounting for prognostic variables that are pre-specified in the protocol or analysis plan, such as prior medical/treatment history, demographics and physiological status. A recurring theme throughout this article is that the terms “conditional and adjusted (likewise marginal and unadjusted) should not be used interchangeably” because marginal need not mean unadjusted and covariate-adjusted analyses may also target marginal estimands.[30, 41]

The marginal effect would be the average effect, at the population level (conditional on the entire population distribution of covariates), of moving all individuals in the trial population between two hypothetical worlds: from one where everyone receives treatment to one where everyone receives treatment .[42, 43, 44] The conditional effect corresponds to the average treatment effect at the unit level, conditional on the effects of the covariates that have also been included in the model. This would be the average effect of switching the treatment of an individual in the trial population from to , fully conditioned on the average combination of subject-level covariates, or the average effect across sub-populations of subjects who share the same covariates. Population-adjusted indirect comparisons are used to inform reimbursement decisions in HTA at the population level. Therefore, marginal treatment effect estimates are required.[45]

The indirect comparison between treatments and is typically carried out in the “linear predictor” scale;[5, 6] namely, using additive effects for a given linear predictor, e.g. log-odds ratio for binary outcomes or log hazard ratio for survival outcomes. Indirect treatment comparisons can be “anchored” or “unanchored”. Anchored comparisons make use of a connected treatment network. In this case, this is available through a common comparator . Unanchored comparisons use disconnected treatment networks or single-arm trials and require much stronger assumptions than their anchored counterparts.[7] The use of unanchored comparisons where there is connected evidence is discouraged and often labeled as problematic.[7, 14] This is because it does not respect within-study randomization and is not protected from imbalances in any covariates that are prognostic of outcome (almost invariably, a larger set of covariates than the set of effect measure modifiers). Hence, our focus is on anchored comparisons.

In the standard anchored scenario, a manufacturer submitting evidence to HTA bodies has access to IPD from its own trial that compares its treatment against the standard health technology . The disclosure of proprietary, confidential IPD from industry-sponsored clinical trials is rare. Hence, individual-level data on baseline covariates, treatment and outcomes for the competitor’s trial, evaluating the relative efficacy or effectiveness of intervention vs. , are regularly unavailable, for both the submitting company and the national HTA agency assessing the evidence. For this study, only summary outcome measures and marginal moments of the covariates, e.g. means with standard deviations for continuous variables or proportions for binary and categorical variables, as found in so-called “Table 1” of clinical trial publications, are available. We consider, without loss of generality, that IPD are available for a study comparing treatments and (denoted ) and published ALD are available for a study comparing interventions and ().

Standard ITCs such as the Bucher method[6] assume that there are no differences across trials in effect measure modifiers. A variable is an effect measure modifier, effect modifier for short, if the relative effect of a particular intervention, as measured on a specific scale, varies at different levels of the variable. For instance, if women react differently to a drug therapy than men on the log-odds ratio scale, then gender modifies the effect of the drug on such scale. Within the biostatistics literature, effect modification is usually referred to as heterogeneity or interaction, because effect modifiers are considered to alter the effect of treatment by interacting with it on a specific scale,[46] and are typically detected by examining statistical interactions.[47]

Consider that denotes a treatment indicator. Active treatment is denoted , active treatment is denoted , and the common comparator is denoted . In addition, denotes a specific study. The study, comparing treatments and is denoted . The study is denoted . The true relative treatment effect between and in study population is indicated by and is estimated by .

In standard ITCs, one assumes that the vs. treatment effect in the population is equal to , the effect that would have have occurred in the population. Note that the Bucher method and most conventional network meta-analysis methods do not explicitly specify a target population of policy interest (whether this is , or otherwise).[48] Hence, they cannot account for differences in covariates across study populations. The Bucher method is only valid when either: (1) the vs. treatment effect is homogeneous, such that there is no effect modification; or (2) the distributions of the effect modifiers are the same in both studies.

If the vs. treatment effect is heterogeneous and the effect modifiers are not equidistributed across trials, relative treatment effects are no longer constant across the trial populations, except in the pathological case where the bias induced by different effect modifiers is in opposite directions and cancels out. Hence, the assumptions of the Bucher method are broken. In this scenario, standard ITC methods are liable to produce biased and overprecise estimates of the treatment effect.[49] These features are undesirable, particularly from the economic modeling point of view, as they impact negatively on the probabilistic sensitivity analysis.

Conversely, MAIC and STC target the vs. treatment effect that would be observed in the population, thereby performing an adjusted indirect comparison in such population. MAIC and STC implicitly assume that the target population is the population. The estimate of the adjusted vs. treatment effect is:

| (1) |

where is the estimated relative treatment effect of vs (mapped to the population), and is the estimated marginal treatment effect of vs. (in the population). The estimate and an estimate of its variance may be directly published or derived non-parametrically from crude aggregate outcomes made available in the literature. The majority of RCT publications will report an estimate targeting a marginal treatment effect, derived from a simple regression of outcome on a single independent variable, treatment assignment. In addition, the estimate should target a marginal treatment effect for reimbursement decisions at the population level. Therefore, should target a marginal treatment effect that is compatible with .[50]

As the relative effects, and , are specific to separate studies, the within-trial randomization of the originally assigned patient groups is preserved. Because the estimates are based on different study samples (IPD are unavailable for ), the within-trial relative effects are assumed statistically independent of each other. Hence, their variances are simply summed to estimate the variance of the vs. treatment effect. One can also take a Bayesian approach to estimating the indirect treatment comparison, in which case variances would be derived empirically from draws of the posterior density. We believe that a Bayesian analysis is helpful because simulation from the posterior distribution provides a framework for probabilistic decision-making, directly allowing for both statistical estimation and inference, and for principled uncertainty propagation.[5]

A reference intervention is required to define the effect modifiers. In the methods considered in this article, we are selecting the effect modifiers of treatment with respect to (as opposed to the treatment effect modifiers of vs. ). This is because we have to adjust for these in order to perform the indirect comparison in the population, implicitly assumed to be the target population. If one had access to IPD for the study and only published ALD for the study, one would have to adjust for the factors modifying the effect of treatment with respect to , in order to perform the comparison in the population.

In some contexts, a distinction is made between sample-average and population-average marginal effects.[11, 51, 52, 53] Typically, another implicit assumption made by population-adjusted indirect comparisons is that the marginal treatment effects estimated in the trial sample (as described by its published covariate summaries for ), match those that would be estimated in the study’s target population. This implies that either: (1) the sample on which inferences are made is the trial’s target population; or (2) it is a simple random sample representative of such population, ignoring sampling variability.

2.1 The need for outcome regression approaches

At present, matching-adjusted indirect comparison (MAIC)[8] is the most commonly used population-adjusted indirect comparison method.[28] “Matching-adjusted” is a misnomer, as the indirect comparison is actually “weighting-adjusted”, with the population adjustment based on propensity score weighting.[54] A logistic regression is used to model the trial assignment odds conditional on a selected set of baseline covariates. The weights estimated by the model represent the “trial selection” odds, namely, the odds of being enrolled in the trial. These are balancing scores that, when applied to the IPD, form a pseudo-population that has balanced covariate moments with respect to the population. The weights are often applied to a weighted simple regression to estimate the marginal treatment effect for vs. in the population. However, MAIC does not explicitly require an outcome model. The development of outcome regression methods, which estimate an outcome-generating mechanism given treatment and the baseline covariates, is appealing for several reasons:

(1) Statistical precision and efficiency. Outcome regression tends to give more precise estimates than weighting. Weighting is particularly inefficient and unstable where covariate overlap is poor and effective sample sizes are small,[26, 55, 56, 57, 58] as it is sensitive to inordinate influence by extreme weights. Outcome regression can extrapolate the association between outcome and covariates where overlap is insufficient, while weighting methods cannot extrapolate beyond the observed covariate space in the IPD. Valid extrapolation, using the linearity assumption or other appropriate assumptions about the input space, requires accurately capturing the true covariate-outcome relationships.

(2) Different modeling assumptions. While MAIC relies on a correctly specified model for the conditional odds of trial assignment given the covariates, outcome regression methods rely on a correctly specified model for the conditional expectation of the outcome given treatment and the covariates. In my experience, identifying the variables that affect outcome is more straightforward than identifying the factors that drive trial assignment in the context of population-adjusted indirect comparisons. This is not typically the case in the standard use of propensity score weighting in observational studies, where one identifies the factors that drive treatment (as opposed to trial) assignment. Nevertheless, in our scenario, the factors driving selection into different RCTs are often arbitrary.[59, 60] Researchers may benefit from the use of distinct modeling approaches with different assumptions, as these can yield different results, especially if there is a violation of assumptions.

(3) Flexibility. Researchers could use augmented or doubly robust methods[44, 61, 62, 63] that combine the model for the expectation of the outcome with the trial assignment odds model. These are attractive due to their increased robustness to model misspecification: consistent estimation only requires the correct specification of either of the two models, not necessarily both.[61, 64] Even with the reduced misspecification risk, they tend to have improved precision and efficiency with respect to the standard weighting estimators.[65]

2.2 Some assumptions

Besides the differences in (typically parametric) model specification, weighting methods such as MAIC and outcome regression methods such as those discussed in this article mostly require the same set of assumptions. An in-depth non-technical description of these is detailed in Supplementary Appendix A and a short discussion is presented in subsection 6.2. The assumptions include:

-

1.

Internal validity of the and trials, e.g. appropriate randomization and sufficient sample sizes so that the treatment groups are comparable, no interference, negligible measurement error or missing data, the absence of non-compliance, etc.

-

2.

Consistency under parallel studies such that both trials have identical control treatments, sufficiently similar study designs and outcome measure definitions, and have been conducted in care settings with a high degree of similarity.

-

3.

Accounting for all effect modifiers of treatment vs. in the adjustment. This assumption is called the conditional constancy of the vs. marginal treatment effect,[14] and requires that a sufficiently rich set of baseline covariates has been measured for the study and is available in the study publication.aaaIn the anchored scenario, we are interested in a comparison of relative outcomes or effects, not absolute outcomes. Hence, an anchored comparison only requires conditioning on the effect modifiers of the vs. treatment effect. This assumption is named the conditional constancy of relative effects,[7, 14] i.e., given the selected effect-modifying covariates, the marginal vs. treatment effect is constant across the and populations. There are other formulations of this assumption,[11, 51, 52, 66, 53] such as trial assignment/selection being conditionally ignorable, unconfounded or exchangeable for such treatment effect, i.e., conditionally independent of the treatment effect, given the selected effect modifiers. One can consider that being in population or population does not carry over any information about the marginal vs treatment effect, once we condition on the treatment effect modifiers. This means that after adjusting for these effect modifiers, treatment effect heterogeneity and trial assignment are conditionally independent. Another advantage of outcome regression with respect to weighting is that, by being less sensitive to overlap issues, it allows for the inclusion of larger numbers of effect modifiers. This makes it easier to satisfy the conditional constancy of relative effects.

-

4.

Overlap between the covariate distributions in and . More specifically, that the ranges of the selected covariates in the trial cover their respective moments in the population. The overlap assumption (often referred to as “positivity”) can be overcome in outcome regression if one is willing to rely on model extrapolation, assuming correct model specification.[44]

-

5.

Correct specification of the population. Namely, that it is appropriately represented by the information available to the analyst, that does not have access to patient-level data from the study.

Most assumptions are causal and untestable, with their justification typically requiring prior substantive knowledge.[67] Nevertheless, we shall assume that they hold throughout the article. We discuss potential failures of assumptions and their consequences in subsection 6.2, in the context of the simulation study, and in Supplementary Appendix A.

3 Methodology

3.1 Data structure

For the trial IPD, let . Here, is a matrix of baseline characteristics (covariates), e.g. age, gender, comorbidities, baseline severity, of size , where is the number of subjects in the trial and is the number of available covariates. For each subject , a row vector of covariates is recorded. Each baseline characteristic can be classed as a prognostic variable (a covariate that affects outcome), an effect modifier, both or none. For simplicity in the notation, it is assumed that all available baseline characteristics are prognostic of the outcome and that a subset of these, , is selected as effect modifiers on the linear predictor scale, with a row vector recorded for each subject. We let represent a vector of outcomes, e.g. a time-to-event or binary indicator for some clinical measurement; and is a treatment indicator ( if subject is under treatment and if under ). For simplicity, we shall assume that there are no missing values in . As outlined in the Discussion, the outcome regression methodologies can be readily adapted to address this issue, particularly under a Bayesian implementation, but this is an area for future research.

We let denote the information available for the study. No individual-level information on covariates, treatment or outcomes is available. Here, represents a vector of published covariate summaries, e.g. proportions or means. For ease of exposition, we shall assume that these are available for all covariates (otherwise, one would take the intersection of the available covariates), and that the selected effect modifiers are also available such that . An estimate of the vs. treatment effect in the population, and an estimate of its variance , either published directly or derived from crude aggregate outcomes in the literature, are also available. Note that these are not used in the adjustment mechanism but are ultimately required to perform inference for the indirect comparison in the population.

Finally, we let the symbol stand for the dependence structure of the covariates. Under certain assumptions about representativeness, this can be retrieved from the trial, e.g. through the observed pairwise correlations, or from external data sources such as registries. This information, together with the published covariate summary statistics, is required to characterize the joint covariate distribution of the population. A pseudo-population of subjects is simulated from this joint distribution, such that denotes a matrix of baseline covariates of dimensions , with a row vector of covariates simulated for each subject . Notice that the value of does not necessarily have to correspond to the actual sample size of the study; however, the simulated cohort must be sufficiently large so that the sampling distribution is stabilized, minimizing sampling variability. Again, a subset of the simulated covariates, , makes up the treatment effect modifiers on the linear predictor scale, with a row vector for each subject . In this article, the asterisk superscript represents unobserved quantities that have been constructed in the population.

The outcome regression approaches discussed in this article estimate treatment effects with respect to a hypothetical pseudo-population for the study. Before outlining the specific outcome regression methods, we explain how to generate values for the individual-level covariates for the population using Monte Carlo simulation.

3.2 Individual-level covariate simulation

Ideally, the population should be characterized by the full joint distribution of covariates. However, the restriction of limited IPD makes it unlikely that the joint distribution of the covariates is available. Where there are not many covariates and these are binary, this is sometimes available as a cross-tabulation. However, most of the time we need to approximate the joint distribution appropriately. This is important to avoid bias arising from the incomplete specification of the population. The published summary values and the correlation structure are combined, making certain parametric assumptions about the marginal distributional forms, to infer the joint distribution of the covariates and construct an appropriate pseudo-population for inferences. The proposed approaches allow the analyst to bring in some prior knowledge or evidence to inform the potential distributions of the covariates. However, it is worth noting that we cannot give a general recipe for this step, which requires context-specific knowledge that is likely not available from the observed data in the trials.

Firstly, the marginal distributions for each covariate are specified. The mean and, if applicable, the standard deviation of the marginals are sourced from the report to match the published summary statistics. As the true marginal distributional forms are not known, some parametric assumptions are required. For instance, if it is reasonable to assume that sampling variability for a continuous covariate can be described using a normal distribution, and the covariate’s mean and standard deviation are published in the report, we can assume that it is marginally normally distributed. Hence, we can also select the family for the marginal distribution using the theoretical validity of the candidate distributions alongside the IPD. For example, the marginal distribution of duration of prior treatment at baseline could be modeled as a log-normal or Gamma distribution as these distributions are right-skewed and bounded to the left by zero. Truncated distributions can be used to resemble the inclusion/exclusion criteria for continuous covariates in the trial, e.g. age limits, and avoid deterministic overlap violations.

Secondly, the correlations between covariates are specified. We suggest two possible data-generating model structures for this purpose: (1) simulating the covariates from a multivariate Gaussian copula;[12, 68] or (2) factorizing the joint distribution of the covariates into the product of marginal and conditional distributions. The former approach is perhaps more general-purpose. The latter is more flexible, defining separate models for each variable, but its specification can be daunting where there are many covariates and interdependencies are complex.

Any multivariate joint distribution can be decomposed in terms of univariate marginal distribution functions and a dependence structure.[69] A Gaussian copula “couples” the marginal distribution functions for each covariate to a multivariate Gaussian distribution function. The main appeal of a copula is that the correlation structure of the covariates and the marginal distribution for each covariate can be modeled separately. We may use the pairwise correlation structure observed in the patient-level data as the dependence structure, while keeping the marginal distributions inferred from the summary values and the IPD. Note that the term “Gaussian” does not refer to the marginal distributions of the covariates but to the correlation structure. While the Gaussian copula is sufficiently flexible for most modeling purposes, more complex copula types (e.g. Clayton, Gumbel, Frank) may provide different and more customizable correlation structures.[68]

Alternatively, we can account for the correlations by factorizing the joint distribution of covariates in terms of marginal and conditional densities. This strategy is common in implementations of sequential conditional algorithms for parametric multiple imputation.[70, 71] For instance, consider two baseline characteristics: , which is a continuous variable, and the presence of a comorbidity , which is dichotomous. We can factorize the joint distribution of the covariates such that .

In this scenario, we draw for subject from a suitable marginal distribution, e.g. a normal, with the mean and standard deviation sourced from the published summaries or official life tables. The mean of (the conditional proportion of the comorbidity) given the age, can be modeled through a regression: , with where is an appropriate link function. Here, the coefficients and represent respectively the overall proportion of comorbidity in the population (marginalizing out the age), and the correlation level between comorbidity and (the centered version of) age. The former coefficient can be directly sourced from the published summaries, whereas the latter could be derived from pairwise correlations observed in the IPD or from external sources, e.g. clinical expert opinion, registries or administrative data, applying the selection criteria of the trial to subset the data. Figure 1 provides an example of a similar probabilistic structure with three covariates: and the presence of two comorbidities, and . In this example, the distribution of the covariates is factorized such that .

It is important to acknowledge that this “covariate simulation” step arises due to a suboptimal scenario, where patient-level data on covariates are unavailable for the study. Ideally, this should be freely available or, at least, disclosed by the sponsor company. Raw patient-level data are always the preferred input for statistical inference, allowing for the testing of assumptions.[73] The underlying reasons for unavailable IPD are diverse and span across a range of issues. Perhaps the most sensitive of these is privacy, with the General Data Protection Regulation[74] ratified by the European Union in 2018 recognizing data concerning health as a special category of data with specific protection safeguards and disclosure regulations.

We note that, if the main hindrance to the availability of IPD is privacy, the manufacturer itself could facilitate statistical inference by using the IPD to create fully artificial covariate datasets.[75] The release of such datasets would not involve a violation of privacy or confidentiality and would avoid the need for the “covariate simulation” step. Alternatively, Bonofiglio et al.[76] have recently proposed a framework where access to covariate correlation summaries is made possible through distributed computing. It is unclear whether access to such framework would be granted to a competitor submitting evidence for reimbursement to HTA bodies, albeit the summaries could be reported in clinical trial publications.

3.3 Conventional outcome regression

In simulated treatment comparison (STC), IPD from the trial are used to fit a regression model describing the observed outcomes in terms of the relevant baseline characteristics and the treatment variable .

STC has different formulations.[7, 9, 14, 77] In the conventional version described by the NICE Decision Support Unit Technical Support Document 18,[7, 14] the individual-level covariate simulation step described in subsection 3.2 is not performed. The covariates are centered at the published mean values from the population. Under a generalized linear modeling framework, the following regression model is fitted to the observed IPD:

| (2) |

where, for a generic subject , is the expected outcome on the natural scale, e.g. the probability scale for binary outcomes, is an invertible canonical link function, is the intercept, is a vector of regression coefficients for the prognostic variables, is a vector of interaction coefficients for the effect modifiers (modifying the vs. treatment effect) and is the vs. treatment coefficient. For binary outcomes in logistic regression, one uses the link function, but other choices are possible in practice, e.g. the identity link for standard linear regression with continuous-valued outcomes, or the log link for Poisson regression with count outcomes. In the population adjustment literature, covariates are sometimes centered separately for active treatment and common comparator arms.[78, 79, 80] We do not recommend this approach because it may break randomization, distorting the balance between treatment arms and on covariates that are not accounted for. If these covariates are prognostic of outcome, this would compromise the internal validity of the within-study treatment effect estimate for vs. .

The regression in Equation 2 models the conditional outcome mean given treatment and the centered baseline covariates. Because the IPD prognostic variables and the effect modifiers are centered at the published mean values from the population, the estimated is directly interpreted as the vs. treatment effect in the population or, more specifically, in a pseudopopulation with the covariate means and the correlation structure. Typically, analysts set in Equation 1, inputting this coefficient into the health economic decision model.[81, 82] For uncertainty quantification purposes, the variance of said treatment effect is obtained from the standard error estimate of the treatment coefficient in the fitted model.[7, 14]

An important issue with this approach is that the treatment parameter , extracted from the fitted model, has a conditional interpretation at the individual level, because it is conditional on the baseline covariates included as predictors in the multivariable regression.[42, 17] However, we require that estimates a marginal treatment effect, for reimbursement decisions at the population level. In addition, we require that is compatible with the published marginal effect for vs. , , for comparability in the indirect treatment comparison in Equation 1. Even if the published estimate targets a conditional estimand, this cannot be combined in the indirect treatment comparison because it likely has been adjusted using a different covariate set and model specification than .[30] An indirect comparison of conditional treatment effects cannot be performed because we do not have access to the study patient-level data and cannot derive a compatible conditional estimate for vs. , using the same outcome regression specification. In any case, a comparison of conditional treatment effects is not of interest when making decisions at the population level in HTA.[50] Therefore, the treatment coefficient does not target the estimand of interest.

With non-collapsible effect measures such as the odds ratio in logistic regression, marginal and conditional estimands for non-null effects do not coincide,[83] even with covariate balance and in the absence of confounding.[84, 85] Targeting the wrong estimand may induce systematic bias, as observed in a recent simulation study.[17] Most applications of population-adjusted indirect comparisons are in oncology[17, 28] and are concerned with non-collapsible measures of treatment effect such as (log) hazard ratios[42, 86, 84] or (log) odds ratios.[42, 86, 84, 85] With both collapsible and non-collapsible measures of effect, maximum-likelihood estimators targeting distinct estimands will have different standard errors. Therefore, marginal and conditional estimates quantify parametric uncertainty differently, and conflating these will lead to the incorrect propagation of uncertainty to the wider health economic decision model, which will be problematic for probabilistic sensitivity analyses.

3.4 Marginalization via parametric G-computation

The crucial element that has been missing from the typical application of outcome regression is the marginalization of the vs. treatment effect estimate. When adjusting for covariates, one must integrate or average the conditional estimate over the joint covariate distribution to recover a marginal treatment effect that is compatible in the indirect comparison. Parametric G-computation[31, 32, 87, 88, 89] is an established method for marginalizing regression-adjusted conditional estimates. The literature on population-adjusted indirect comparisons has been developed separately to G-computation, despite the close relationships between the methodologies. We build a new link between the two in the next paragraphs.

G-computation in this context consists of: (1) predicting the conditional outcome expectations under treatments and for each subject in the population; (2) averaging the predictions to produce marginal outcome means on the natural scale; and (3) back-transforming the averages to the linear predictor scale, contrasting the linear predictions to estimate the marginal vs. treatment effect in the population. This marginal effect is compatible in the indirect treatment comparison. This procedure is a form of standardization, a technique which has been performed for decades in epidemiology, e.g. when computing standardized mortality ratios.[62] Parametric G-computation is often called model-based standardization[33, 34, 35] because a parametric model is used to predict the conditional outcome expectations under each treatment. When the covariates and outcome are discrete, the estimation of the conditional expectations could be non-parametric, in which case G-computation is numerically identical to crude direct post-stratification.[10]

G-computation marginalizes the conditional estimates by separating the regression modeling outlined in subsection 3.3 from the estimation of the marginal treatment effect for vs. . Firstly, a regression model of the observed outcome on the covariates and treatment is fitted to the IPD:

| (3) |

In the context of G-computation, this regression model is often called the “Q-model”. Contrary to Equation 2, it is not centered on the mean covariates for reasons we shall explain shortly.

Having fitted the Q-model, the regression coefficients are treated as nuisance parameters. The parameters are applied to the simulated covariates to predict hypothetical outcomes for each subject under both possible treatments. Namely, a pair of predicted outcomes, also called potential outcomes,[90] under and under , is generated for each subject.

Parametric G-computation typically relies on maximum-likelihood estimation to fit the regression model in Equation 3. In this case, the methodology proceeds as follows. We denote the maximum-likelihood estimate of the regression parameters as . Leaving the simulated covariates at their set values, we fix the treatment values, indicated by a vector , for all . By plugging treatment into the maximum-likelihood regression fit for each simulated individual, we predict the marginal outcome mean, on the natural scale, when all subjects are under treatment :

| (4) | ||||

| (5) |

Equation 4 follows from the law of total expectation, such that the (marginal) expected outcome is equal to the expected value of the conditional expected outcome, given the predictors. The joint probability density function for the covariates is denoted . This could be replaced by a probability mass function if the covariates are discrete or by a mixture density if there is a combination of discrete and continuous covariates. Replacing the integral by the summation in Equation 5 follows from using the empirical joint distribution of the simulated covariates as a non-parametric estimator of the density .[30]

Similar to above, by plugging treatment into the regression fit for every simulated observation, we predict the marginal outcome mean in the hypothetical scenario in which all units are under treatment :

| (6) | ||||

| (7) |

To estimate the marginal or population-average treatment effect for vs. in the linear predictor scale, one back-transforms to this scale the average predictions, taken over all subjects on the natural outcome scale, and calculates the difference between the average linear predictions:

| (8) |

where we have removed the dependence on for simplicity in the notation. If the outcome model in Equation 3 is correctly specified, the estimators of the marginal outcome means on the natural scale and , i.e., are consistent with respect to convergence to their true value, and so is the marginal treatment effect estimate .

For illustrative purposes, consider a logistic regression for binary outcomes. In this case, is the average of the individual probabilities predicted by the regression when all participants are assigned to treatment . Similarly, is the average probability when everyone is assigned to treatment . The inverse link function would be the inverse logit function , and the average predictions in the probability scale could be substituted into Equation 8 and transformed to the log-odds ratio scale, using the logit link function. More interpretable summary measures of the marginal contrast, e.g. odds ratios, relative risks or risk differences, can also be produced by manipulating the average natural outcome means differently than in Equation 8, mapping these to other scales. For instance, a marginal odds ratio can be estimated as , where denotes the logit link function. The standard scale commonly used for performing indirect treatment comparisons is the log-odds ratio scale[5, 6, 7] and this linear predictor scale is used to define effect modification, which is scale-specific.[14] Hence, we assume that the marginal log-odds ratio is the relative effect measure of interest.

Note that the estimated absolute outcomes and , e.g. the average outcome probabilities under each treatment in the case of logistic regression, are sometimes desirable in health economic models without any further processing.[91] In addition, these could be useful in unanchored comparisons, where there is no common comparator group included in the analysis, e.g. if the competitor trial is an RCT without a common control or a single-arm trial evaluating the effect of treatment alone. In the unanchored case, absolute outcome means are compared across studies as opposed to relative effects. However, unanchored comparisons make very strong assumptions which are largely considered impossible to meet (absolute effects are conditionally constant as opposed to relative effects being conditionally constant).[7, 14]

3.4.1 Cox proportional hazards regression

The most popular outcome types in applications of population-adjusted indirect comparisons are survival or time-to-event outcomes (e.g. overall or progression-free survival), and the most prevalent measure of effect is the (log) hazard ratio.[28] Therefore, developing G-computation approaches where the nuisance model is a Cox proportional hazards regression is important and useful to practitioners. In this setting, and should target marginal log hazard ratios for indirect treatment comparisons in the linear predictor scale. Something to bear in mind is that, even if Cox models are very frequently used in evidence synthesis for time-to-event data, health economic modelers typically use parametric survival models for extrapolation purposes. In subsection 3.6, we develop a novel general-purpose methodology that can be used in scenarios where the outcome regression of interest is a parametric survival model.

The G-computation formulae for the Cox regression are provided by Stitelman et al.[92] Consider that a Cox proportional hazards model has first been fitted, conditional on covariates which follow the functional form in the linear predictor of Equation 3. For the generalized linear model, we were interested in the average outcome predictions in the natural scale. With Cox regression, the average survival probabilities are of interest.

We proceed similarly as in Equations 4-8. Leaving the simulated covariates at their set values, we fix the value of treatment at for all . By plugging treatment into the Cox regression fit for each simulated unit, we compute the expected marginal survival probability when all subjects are under treatment :

| (9) | ||||

| (10) |

Above, denotes a particular time point and denotes a potential event time under treatment , such that is the mean treatment-specific probability of surviving beyond . In Equation 9, denotes an estimate of the survival probability under treatment at time for simulated subject with covariates . Equation 10 follows from expressing the survival function in terms of , an estimate of the baseline cumulative hazard function at time , exponentiated and raised to the power of the exponentiated linear predictor term. Estimates of the baseline cumulative hazard are easily obtained from Cox regressions fitted with the standard survival analysis software packages.

Similarly, the expected marginal survival probability when all simulated subjects are under treatment is given by:

| (11) | ||||

| (12) |

where denotes a potential event time under treatment , and denotes the estimated survival probability under treatment at time for subject with simulated covariates . The marginal hazard at time for treatment can be expressed as the negative logarithm of the survival probability, . Therefore, the estimate of the marginal log hazard ratio for vs. in the population at time is:

| (13) |

where and are obtained using Equations 9-10 and Equations 11-12, respectively.

The Cox regression assumes that the true marginal log hazard ratio is independent of time due to the proportional hazards assumption. However, as pointed out by Varadhan et al.,[93] the estimate in Equation 13 may vary across different values of . We have to set to a specific time point, or alternatively, to estimate the marginal hazard ratio over a set of time points and display the estimates graphically. When selecting a value of , bear in mind that, in Equation 13, the marginal log hazard ratio estimate is undefined at for which for treatment .[92] A simulation procedure for marginalizing estimates of conditional hazard ratios has recently been proposed by Daniel et al.[30] This approach should avoid these issues by averaging the marginal log hazard ratio over a set time frame, but adapting the methodology to the current setting is beyond the scope of this article.

One can manipulate the expected marginal survival probabilities differently than in Equation 13 to produce estimates of the marginal risk difference (the additive difference in survival probabilities) or the marginal log relative risk at a particular time point.[92] These effect measures are more easily interpreted. However, indirect treatment comparisons with survival outcomes are typically performed in the log hazard ratio scale,[5] and this linear predictor scale is used to define effect modification, which is scale-specific.[14] Therefore, the marginal log hazard ratio is the relative effect measure of interest.

3.4.2 Model fitting and selection

Because the regression in Equation 3 will be our working model from now onward, we briefly discuss some good practices for model fitting and model selection. Time and care should be taken to perform these exercises and fit an appropriate regression.

The inclusion of all imbalanced effect modifiers in Equation 3 is required for unbiased estimation of both the marginal and conditional vs. treatment effects in the population.[94] A strong fit of the regression model, evaluated by model checking criteria such as the residual deviance and information criteria, may increase precision. Hence, we could select the model with the lowest information criterion conditional on including all effect modifiers.[94] Model checking criteria should not guide causal decisions on effect modifier status, which should be defined prior to fitting the outcome model. As effect-modifying covariates are likely to be good predictors of outcome, the inclusion of appropriate effect modifiers should provide an acceptable fit. In addition, note that any model comparison criteria will only provide information about the observed data and therefore tell just part of the story.[95] We have no information on the fit of the selected model to the patient-level data.

At this point, the readers may be wondering why the outcome regressions fitted in subsections 3.3 and 3.4 are different. In the conventional outcome regression described in 3.3 and by the NICE technical support document,[14] the IPD covariates are centered by plugging in the mean covariate values. In the Q-model required for G-computation, outlined in 3.4, the covariates are not centered and the regression fit is used to make predictions for the simulated covariates. The underlying reason for this has been described for generalized linear models with non-linear link functions, such as logistic or Poisson regression.[96, 97, 98] On the natural scale, averaging the individual outcome predictions made at the centered covariates of the sample does not consistently estimate the marginal mean response for the centered sample. In the words of Bartlett,[96] “prediction at the mean” value of the baseline covariates for a treatment group does not result in the “marginal mean” under such treatment. Similarly, in the words of Qu and Luo,[97] the “mean at mean covariates” of the study sample is generally not equivalent to the marginal response over the subjects in the sample. The former results in a conditional estimate whereas the latter produces a marginal population-level estimate, of interest in our scenario.

We have postulated a single outcome model for all subjects in the IPD, which includes the necessary treatment-covariate interaction terms to capture effect modification over the covariates. Nevertheless, another possible strategy is to fit two outcome models separately for each treatment group in the randomized trial, i.e., to fit one regression to the patients under treatment and then another regression among the patients under , then predicting the conditional outcome expectations and averaging these out on the entire simulated pseudo-population. This is perhaps a more “objective” approach to covariate adjustment, as the model-fitting is performed independently of reference to a conditional treatment effect (in this case, the fitted regressions do not have a treatment coefficient), but obviates the estimation of treatment-by-covariate interactions.[58, 99] Throughout the article, we consider the nuisance model in Equation 3 to be a parametric regression. Alternatively, non-parametric estimators of the conditional expectation may be less susceptible to model misspecification. We discuss the potential application of these methods in subsection 6.2.

3.4.3 Variance estimation

From a frequentist perspective, it is not easy to derive analytically a closed-form expression for the standard error of the marginal vs. treatment effect. Deriving the asymptotic distribution is not straightforward because, typically, the estimate is a non-linear function of each of the components of . When using maximum-likelihood estimation to fit the outcome model, standard errors and interval estimates can be obtained using resampling-based methods such as the traditional non-parametric bootstrap[100] or the m-out-of-n bootstrap.[93] In our bootstrap implementation, we only resample the IPD of the trial due to patient-level data limitations for the study. The standard error would be estimated as the sample standard deviation of the resampled marginal treatment effect estimates. Assuming that the sample size is reasonably large, we can appeal to the asymptotic normality of the marginal treatment effect and construct Wald-type normal distribution-based confidence intervals. Alternatively, one can construct interval estimates using the relevant quantiles of the bootstrapped treatment effect estimates, without necessarily assuming normality. This avoids relying on the adequacy of the asymptotic normal approximation, an approximation which will be inappropriate where the true model likelihood is distinctly non-normal,[101] and may allow for the more principled propagation of uncertainty.

An alternative to bootstrapping for statistical inference is to simulate the parameters of the multivariable regression in Equation 3 from the asymptotic multivariate normal distribution with means set to the maximum-likelihood estimator and with the corresponding variance-covariance matrix, iterate over Equations 4-8 and compute the sample variance. This parametric simulation approach is less computationally intensive than bootstrap resampling. It has the same reliance on random numbers and may offer similar performance.[102] It is equivalent to approximating the posterior distribution of the regression parameters, assuming constant non-informative priors and a large enough sample size. Again, this large-sample formulation relies on the adequacy of the asymptotic normal approximation.

3.5 Bayesian parametric G-computation

A Bayesian approach to parametric G-computation may be beneficial for several reasons. Firstly, the maximum-likelihood estimates of the outcome regression coefficients may be unstable where the sample size of the IPD is small, the data are sparse or the covariates are highly correlated, e.g. due to finite-sample bias or variance inflation. This leads to poor frequentist properties in terms of precision. A Bayesian approach with default shrinkage priors, i.e., priors specifying a low likelihood of a very large effect, can reduce variance, stabilize the estimates and improve their accuracy in these cases.[87]

Secondly, we can use external data and/or contextual information on the prognostic effect and effect-modifying strength of covariates, e.g. from covariate model parameters reported in the literature, to construct informative prior distributions for and , respectively, and skeptical priors (i.e., priors with mean zero, where the variance is chosen so that the probability of a large effect is relatively low) for the conditional treatment effect , if necessary. Where meaningful prior knowledge cannot be leveraged, one can specify generic default priors instead. For instance, it is unlikely in practice that conditional odds ratios are outside the range . Therefore, we could use a null-centered normal prior with standard deviation 1.15, which is equivalent to just over 95% of the prior mass being between 0.1 and 10. As mentioned earlier, this “weakly informative” contextual knowledge may result in shrinkage that improves accuracy with respect to maximum-likelihood estimators.[87] Finally, it is simpler to account naturally for issues in the IPD such as missing data and measurement error within a Bayesian formulation.[103, 104]

In the generalized linear modeling context, consider that we use Bayesian methods to fit the outcome regression model in Equation 3. The difference between Bayesian G-computation and its maximum-likelihood counterpart is in the estimated distribution of the predicted outcomes. The Bayesian approach also marginalizes, integrates or standardizes over the joint posterior distribution of the conditional nuisance parameters of the outcome regression, as well as the joint covariate distribution . Following Keil et al.,[87] Rubin[105] and Saarela et al.,[106] we draw a vector of size of predicted outcomes under each set intervention from its posterior predictive distribution under the specific treatment. This is defined as , where is the posterior distribution of the outcome regression coefficients , which encode the predictor-outcome relationships observed in the trial IPD. This[87] is given by:

| (14) | ||||

| (15) |

As noted by Keil et al.,[87] the posterior predictive distribution is a function only of the observed data , the joint probability density function of the simulated pseudo-population, which is independent of , the set treatment values , and the prior distribution of the regression coefficients.

In practice, the integrals in Equations 14 and 15 can be approximated numerically, using full Bayesian estimation via Markov chain Monte Carlo (MCMC) sampling. This is carried out as follows. As per the maximum-likelihood procedure, we leave the simulated covariates at their set values and fix the value of treatment to create two datasets: one where all simulated subjects are under treatment and another where all simulated subjects are under treatment . The outcome regression model in Equation 3 is fitted to the original IPD with the treatment actually received. From this model, conditional parameter estimates are drawn from their posterior distribution , given the observed patient-level data and some suitably defined prior .

It is relatively straightforward to integrate the model-fitting and outcome prediction within a single Bayesian computation module using efficient simulation-based sampling methods such as MCMC. Assuming convergence of the MCMC algorithm, we form realizations of the parameters , where is the number of MCMC draws after convergence and indexes each specific draw. Again, these conditional coefficients are nuisance parameters, not of direct interest in our scenario. Nevertheless, the samples are used to extract draws of the conditional expectations for each simulated subject (the posterior draws of the linear predictor transformed by the inverse link function) from their posterior distribution. The -th draw of the conditional expectation for simulated subject set to treatment is:

| (16) |

Similarly, the -th draw of the conditional expectation for simulated subject under treatment is:

| (17) |

The conditional expectations drawn from Equations 16 and 17 are used to impute the individual-level outcomes under treatment and under treatment , as independent draws from their posterior predictive distribution at each iteration of the MCMC chain. For instance, if the outcome model is a normal linear regression with a Gaussian likelihood, one multiplies the simulated covariates and the set treatment for each subject by the -th random draw of the posterior distribution of the regression coefficients, given the observed IPD and some suitably defined prior, to form draws of the conditional expectation (which is equivalent to the linear predictor because the link function is the identity link in linear regression). Then each predicted outcome would be drawn from a normal distribution with mean equal to and standard deviation equal to the corresponding posterior draw of the error standard deviation. With a logistic regression as the outcome model, one would impute values of a binary response by random sampling from a Bernoulli distribution with mean equal to the expected conditional probability .

Producing draws from the posterior predictive distribution of outcomes is fairly simple using dedicated Bayesian software such as BUGS,[107] JAGS[108] or Stan,[109] where the outcome regression and prediction can be implemented simultaneously in the same module. Over the MCMC draws, these programs typically return a matrix of simulations from the posterior predictive distribution of outcomes. The -th row of this matrix is a vector of outcome predictions of size using the corresponding draw of the regression coefficients from their posterior distribution. We can estimate the marginal treatment effect for vs. in the population by: (1) averaging out the imputed outcome predictions in each draw over the simulated subjects, i.e., over the columns, to produce the marginal outcome means on the natural scale; and (2) taking the difference in the sample means under each treatment in a suitably transformed scale. Namely, for the -th draw, the vs. marginal treatment effect is:

| (18) |

The average, variance and interval estimates of the marginal treatment effect can be derived empirically from draws of the posterior density, i.e., by taking the sample mean, variance and the relevant percentiles over the draws, which approximate the posterior distribution of the marginal treatment effect. The computational expense of the Bayesian approach to G-computation is expected to be similar to that of the maximum-likelihood version, given that the latter typically requires bootstrapping for uncertainty quantification. Computational cost can be reduced by adopting approximate Bayesian inference methods such as integrated nested Laplace approximation (INLA)[110] instead of MCMC sampling to draw from the posterior predictive distribution of outcomes.

Note that Equation 18 is the Bayesian version of Equation 8. Other parameters of interest can be obtained, e.g. the risk difference by using the identity link function in this equation, but these are typically not of direct relevance in our scenario. Again, where the contrast between two different interventions is not of primary interest, the absolute outcome draws from their posterior predictive distribution under each treatment may be relevant. The average, variance and interval estimates of the absolute outcomes can be derived empirically over the draws. An argument in favor of a Bayesian approach is that, once the simulations have been conducted, one can obtain a full characterization of uncertainty on any scale of interest.

In the Cox regression scenario, parametric Bayesian G-computation would follow a similar approach, and would involve drawing the marginal survival probabilities under each treatment from their posterior predictive distribution. Implementing Bayesian parametric G-computation in the Cox regression scenario is a research priority.

3.6 Multiple imputation marginalization

We now develop a general-purpose marginalization procedure labeled multiple imputation marginalization (MIM) because it contains many similarities to multiple imputation. This procedure might be useful where the effect measure of interest cannot be readily summarized in terms of predicted outcomes and G-computation cannot be easily applied. An example scenario where this is the case is when the outcome model is a parametric survival regression. Parametric survival distributions, e.g. exponential, Weibull, Gompertz, log-logistic, log-normal and generalized gamma, are commonly used in health economic evaluations to extrapolate published Kaplan-Meier survival curves from the clinical trial follow-up period to a lifetime horizon.[111, 112, 113, 114, 115] As well as permitting survival extrapolation, these may allow for non-proportional and time-varying hazards. The area under the extrapolation is used to estimate the mean survival benefit of an intervention in cost-effectiveness analyses, typically in terms of life years or quality-adjusted life years. Parametric survival models are particularly of interest in oncology health technology appraisals.

Consider that the outcome model of interest is a parametric survival model. In this scenario, an anchored regression-adjusted indirect comparison would be conducted as follows: (1) a univariable parametric survival regression of outcome on treatment group is fitted to the trial data (the subject-level data is typically reconstructed from digitized Kaplan-Meier curves, e.g. using the algorithm by Guyot et al.[116]); (2) a multivariable covariate-adjusted parametric survival model (of the same family as the model in Step 1) is fitted to the trial data with treatment group as a covariate; (3) the coefficients of the covariate-adjusted regression are marginalized to derive a marginal treatment effect for vs. in the population (with the location or rate coefficient and, potentially, ancillary coefficients such as shapes being treated as nuisance parameters); and (4) this relative treatment effect is applied to the survival curve of common comparator in the study to yield a survival curve for treatment in the population. To our knowledge, the marginalization procedure in Step 3 cannot be easily conducted in this scenario (and in many others) using parametric G-computation. This motivates the development of a general-purpose framework such as MIM.

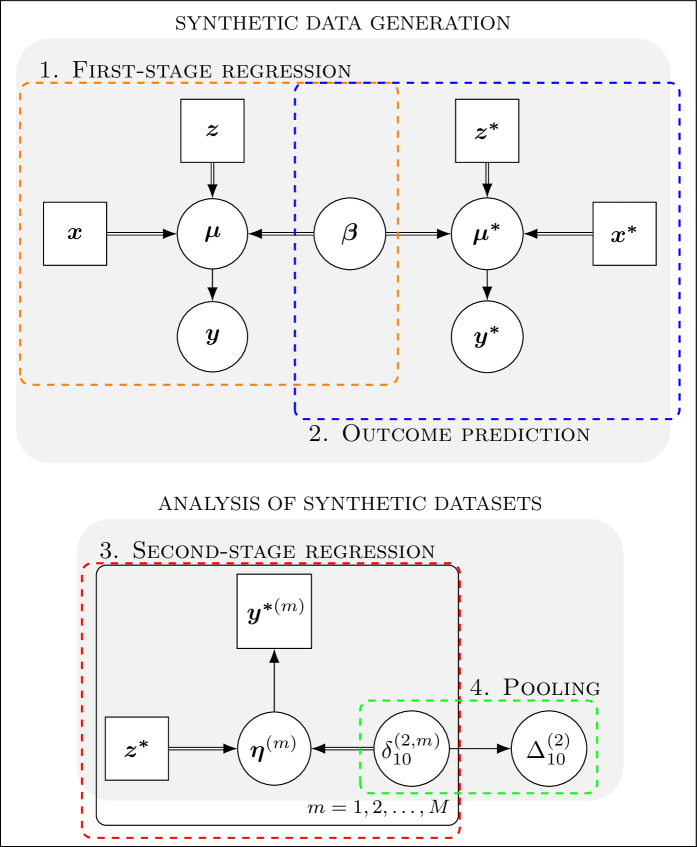

Conceptually, MIM splits the population adjustment into two separate stages: (1) the generation (synthesis) of synthetic datasets; and (2) the analysis of the generated datasets. The synthesis is completely separated from the analysis — only after the synthesis has been completed is the marginal effect of treatment on the outcome estimated. This is analogous to the separation between design and analysis in propensity score methods, between imputation and analysis in multiple imputation, or between fitting (and predicting outcomes with) the Q-model and estimating the marginal treatment effect in G-computation.

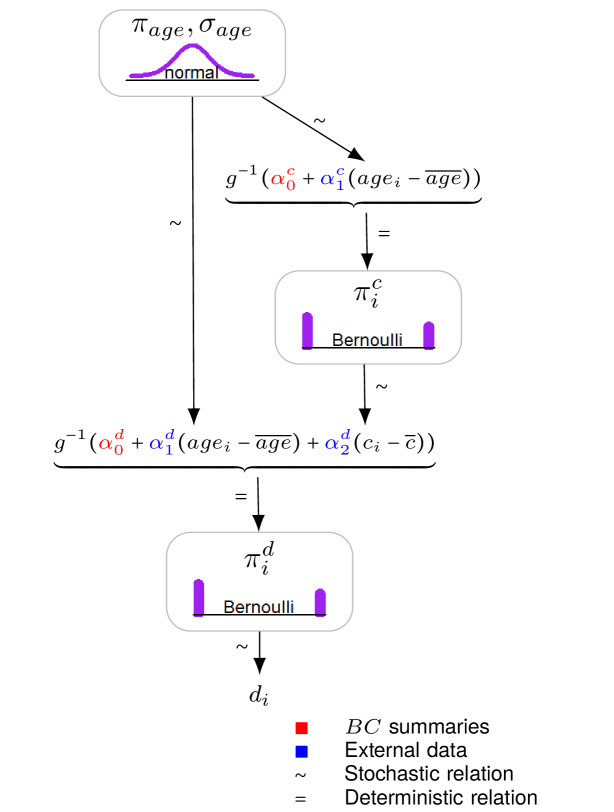

Similarly to Bayesian G-computation, MIM sits naturally within a Bayesian framework in integrating different sources of evidence to fully characterize probabilistic relationships among a set of relevant variables, using a simulation approach. A more detailed explanation of each module is provided below. Figure 2 displays a Bayesian directed acyclic graph (DAG) summarizing the general MIM structure and the links between the modules. In this graphical representation, the nodes represent the variables of the model (constants are denoted as squares and stochastic nodes are circular); single arrows indicate probabilistic relationships and double arrows indicate logical functions. The plate notation indicates repeated analyses. We return to Figure 2 and provide further explanations for the notation throughout this section. For consistency with the rest of the article, MIM is presented within a generalized linear modeling formulation. Nevertheless, its formal integration in a unified survival analysis framework for HTA, which contains many particularities, is a necessary and important piece of currently ongoing research.

3.6.1 Generation of synthetic datasets: a missing data problem

The first stage, synthetic data generation, consists of two steps. Initially, the first-stage regression builds a model to capture the relationship between the outcome and the covariates and treatment in the observed IPD. In the outcome prediction step, we generate predicted outcomes for and in the population by drawing from the posterior predictive distribution of outcomes, given the observed predictor-outcome relationships in the trial IPD, the simulated covariates and the set treatment.

These steps are identical to those described for the Bayesian G-computation procedure in subsection 3.5. Interestingly, Bayesian G-computation follows closely the basic principles of multiple imputation.[39] This is a simulation technique where missing data points are replaced with a set of plausible values conditional on some pre-specified imputation mechanism. Multiple imputation can be regarded as a fundamentally Bayesian operation,[39, 117, 95] as the imputed outcomes are drawn from the posterior predictive distribution of observed outcomes. In addition, our problem can be conceptualized as a missing data problem, where the individual-level outcomes for treatments and in the population are treated as systematically missing data under a complete case analysis.[118] Namely, we only observe the outcomes for the subjects in the trial, with the outcomes experienced in the population “missing”. The imputation mechanism would be the statistical model in Equation 3 relating the outcomes to the predictors . This dependence structure is estimated using the original IPD and used to construct the posterior predictive distribution of outcomes.

Practically, we may frame Bayesian G-computation as conducting hypothetical trials comparing vs. in the population. Extending the parallel with the missing data literature, the outcome-generation process in these trials is based on the assumption of a missing-at-random mechanism. Namely, the missing relative outcomes for vs. in the population are conditionally exchangeable with those observed in the population (conditioning on the predictors that have been adjusted for). Therefore, this missing-at-random assumption is analogous to the conditional constancy of relative effects mentioned in subsection 2.2, which is untestable using the available data alone.

There is one conceptual difference between the synthesis stage of MIM and parametric G-computation, which arises in order to facilitate the presentation of MIM. Instead of considering two datasets with subjects each (one under treatment and the other under treatment ), each synthesis considers a single dataset with individuals that maintains the original treatment allocation ratio of the trial. Treatment in all synthetic datasets will be fixed to , a vector of size . In practice, this different conceptualization will not make a difference provided that is reasonably large. This is because, in the synthetic samples, we “enforce” the randomization of individuals into and by simulating the covariates for active treatment and control arms combined.

As per Bayesian G-computation, the synthesis stage can be performed using MCMC. Iterating over the converged draws of the MCMC algorithm, one generates synthetic datasets, , where . Here, is a matrix of individual-level covariates, drawn from their approximate joint distribution as per subsection 3.2, and is the assigned treatment in the syntheses, as previously described. Each is a vector of predicted outcomes of size . We fill in by drawing from its posterior predictive distribution. In line with the multiple imputation framework, these draws are repeated independently times to create completed syntheses, with the posterior samples making up the imputed datasets. In standard multiple imputation, it is not uncommon to release as little as 5 imputed datasets.[39, 119] However, MIM is likely to require a larger value of as it imputes an entire dataset as opposed to a relatively small proportion of missing values, i.e., the “fraction of missing information” is 1.

Within a survival analysis framework, the fitted first-stage regression would be used to predict survival times in the simulated pseudo-population for the study. One would assume that censoring is non-informative, which is an assumption made, in any case, by the Cox proportional hazards regression and the standard parametric survival models. Namely, one would not attempt to simulate censoring according to any given distribution, or to mimic any particular censoring pattern (essentially, assuming that all times are uncensored in the simulated data structure).

3.6.2 Analysis of synthetic datasets