On -Convergence of Schur-Hadamard Products of Independent Nonsymmetric Random Matrices

Abstract.

Let and be two independent collections of zero mean, unit variance random variables with uniformly bounded moments of all orders. Consider a nonsymmetric Toeplitz matrix and a Hankel matrix , and let be their elementwise/Schur-Hadamard product. In this article, we show that almost surely, , as an element of the -probability space , converges in -distribution to a circular variable. With i.i.d. Rademacher entries, this construction gives a matrix model for circular variables with only bits of randomness. We also consider a dependent setup where and are independent strongly multiplicative systems (à la Gaposhkin [7]) satisfying an additional admissibility condition, and have uniformly bounded moments of all orders—a nontrivial example of such a system being , where . In this case, we show in-expectation and in-probability convergence of the -moments of to those of a circular variable. Finally, we generalise our results to Schur-Hadamard products of structured random matrices of the form and , under certain assumptions on the link-functions and , most notably the injectivity of the map . Based on numerical evidence, we conjecture that the circular law , i.e. the uniform measure on the unit disk of , which is also the Brown measure of a circular variable, is in fact the limiting spectral measure (LSM) of . If true, this would furnish an interesting example where a random matrix with only bits of randomness has the circular law as its LSM.

Key words and phrases:

Free probability; -distribution; circular variable; non-crossing partitions; circular law; limiting spectral measure; Brown measure2020 Mathematics Subject Classification:

46L54, 60B201. Introduction

Let be an complex matrix with eigenvalues . The empirical spectral measure (ESM) of is the probability measure given by

| (1) |

where is the Dirac measure at . The circular law is the uniform measure on the unit disk of . Consider IID matrices , where are i.i.d. zero mean unit variance complex random variables. The famous circular law theorem [14] states that the ESMs converge weakly almost surely to . Weak limits of ESMs are called limiting spectral measures (LSMs).

A patterned/structured random matrix is a matrix whose -th entry is given by , where is a link-function which dictates the pattern, and is a collection of random variables with zero mean, unit variance. The random variables are typically assumed to be i.i.d. for showing almost sure weak convergence of ESMs. A few notable examples of patterned matrices are given in Table 1.

| Matrix | Link function | |

|---|---|---|

| IID | ||

| Wigner | ||

| nonsymmetric Toeplitz | ||

| Hankel |

Existence of almost sure weak limits of the ESMs of various self-adjoint patterned random matrices is known. For example, the Wigner matrix has the semi-circular law as its LSM, which is a probability measure on with density

| (2) |

Symmetric Toeplitz () and Hankel matrices also have LSMs [6, 9]; however, their densities are not known explicitly. For a unified treatment of symmetric patterned random matrices, see [4].

On the other hand, it is not known if nonsymmetric Toeplitz matrices have LSMs. In fact, besides IID matrices and their variants which only require independence of the entries but not identical distribution, weak limits are known for only a handful of models in the nonsymmetric/non-self-adjoint case (see, e.g., [10, 8, 12, 3]).

In this article, we consider elementwise/Schur-Hadamard products (denoted by the symbol ) of independent nonsymmetric patterned random matrices. Let and be two different link-functions and and two independent collections of random variables with zero mean and unit variance. Let

Consider the Schur-Hadamard product of and :

| (3) |

Note that by our assumptions on and , the entries of remain zero mean, unit variance.

Schur-Hadamard products of symmetric patterned random matrices were considered in [5] and a main result of that paper says that if is symmetric Toeplitz and is Hankel, then the LSM of exists and is in fact the semi-circular law .

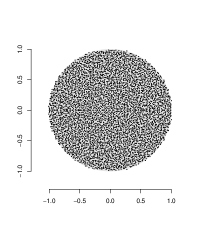

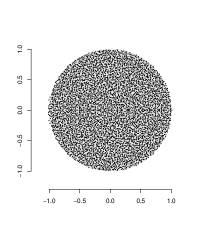

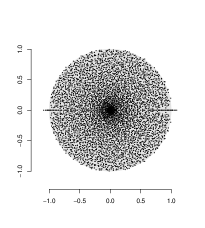

In this article, we consider the Schur-Hadamard product of nonsymmetric Toeplitz and Hankel matrices, i.e. we take and . Simulations shown in Figure 1 prompt us to make the following conjecture.

Conjecture 1.1.

Let and . Suppose that and are independent collections of i.i.d. random variables with zero mean and unit variance. Then the ESM of converges weakly almost surely to the circular law .

In fact, one of our main motivations for studying the Schur-Hadamard product model is that Conjecture 1.1, if true, would provide an interesting example of a random matrix model with only bits of randomness with as the LSM. More elaborately, one can take the entries to be independent Rademacher variables, i.e. random signs, as in Figure 1-(b). All the standard models with as LSM possess bits of randomness (an exception is the recent paper [3], where the authors require bits of randomness).

In this article, we consider the problem from a free-probabilistic perspective. We show in Theorem 3.2 that , as an element of the -probability space converges in -distribution to a circular variable. We originally showed this for input random variables which are independent with zero mean, unit variance, and have uniformly bounded moments of all orders. One of the anonymous referees pointed out that the classical central limit theorem holds for a strongly multiplicative system (SMS)111Multiplicative systems of random variables were first studied by [1]. For a central limit theorem for SMSs, see, e.g., [7]. of random variables (see Definition 3.3), and raised the question if we can allow such entries.

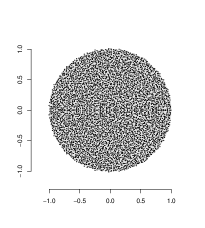

In Theorem 3.2, we allow the input random variables and to be independent SMSs satisfying a certain admissibility condition (see Definition 3.4) and having uniformly bounded moments of all orders. Independent random variables with zero mean, unit variance, and uniformly bounded moments of all orders are trivial examples of such systems. A nontrivial example is the collection , where . Simulations suggest that the circular law limit is possibly true even under such dependence. See Figure 1-(c).

When the entries are independent random variables with zero mean, unit variance, and uniformly bounded moments of all orders, we further show that almost surely, , as an element of the -probability space , converges in -distribution to a circular variable (see Theorem 3.4-(a)). When the entries form admissible SMSs with uniformly bounded moments of all orders, we are only able to establish an in-probability version (see Theorem 3.4-(b)).

As a direct corollary to our results, we recover the aforementioned result of [5] that the LSM of the -scaled Schur-Hadamard product of symmetric Toeplitz and Hankel matrices is the semi-circular law (see Corollary 3.2).

It is well-known that circular variables are -diagonal, and they have as their Brown measure (see, e.g., Chapter 11 of [11]). In this context, let us recall that Voiculescu [15] showed that matrices from the Ginibre ensemble (which are essentially IID matrices with Gaussian entries) converge in -distribution to a circular variable, thus constructing the first matrix model for circular variables. The Schur-Hadamard product construction also gives a matrix model for circular variables, albeit with only bits of randomness.

|

|

|

| (a) | (b) | (c) |

Another main result of [5] is that if and determine the Wigner link-function in the sense that

| (4) |

and some other regularity conditions hold on , then the LSM of is the semi-circular law . Note that (4) is equivalent to saying that for some map , where is the map . The symmetric Toeplitz and Hankel link-functions satisfy this property.

A similar result holds in the nonsymmetric case. We establish in Theorem 3.3 that if the map

is injective, plus some regularity assumptions on and hold, then converges in -distribution to a circular variable. This motivates us to make the following generalisation of Conjecture 1.1.

Conjecture 1.2.

Remark 1.1.

The condition that the map is injective implies that the entries of are uncorrelated. Indeed, because of our assumptions on the input random variables, we have

| (5) |

Now if , then either , or . Thus one of the covariances in (1.1) must vanish.

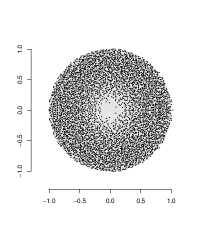

However, just being uncorrelated is not enough as the simulations of Figure 2 suggest. There we take and which makes the map injective. We will impose a regularity condition that would disallow link-functions like which make an input random variable appear too many times in a column or row (see Assumption 3.2).

|

|

|

| (a) | (b) | (c) |

Remark 1.2.

In two special cases, Conjecture 1.2 can be proved easily:

-

(i)

.

-

(ii)

, the common distribution of the ’s is symmetric about , and is an i.i.d. Rademacher sequence.

In both cases, it is easy to see that is an IID matrix, and hence the LSM of is the circular law.

The rest of the paper is organised as follows. In Section 2, we provide a review of the free-probabilistic concepts needed for our main results. In Section 3, we present our main results: In Sections 3.1 and 3.2, we state our assumptions on the input random variables and prove some general results. In Section 3.3, we state and prove the -convergence result for the Schur-Hadamard product of nonsymmetric Toeplitz and Hankel matrices. Then, in Section 3.4, we show how the proof technique for the Toeplitz and Hankel case extends to more general link-functions. Finally, in Section 3.5, we prove in-probability and almost sure versions of our -convergence results.

2. A quick review of some free-probabilistic concepts

A non-commutative probability space is a pair , where is a unital algebra over , and is a state, i.e. a linear functional on such that (here is the unit of ).

A -probability space is a non-commutative probability space , where is a unital -algebra, and the state is positive, i.e.

The state plays the same role in non-commutative probability as the expectation operator does in classical probability.

A natural example comes from the unital -algebra of matrices over (the identity matrix serves as the unit while the -operation is given by taking conjugate transpose). This becomes a -probability space when endowed with the state .

To deal with random matrices, given a probability space , one may consider the unital -algebra of random matrices whose entries are in , the space of random variables with all moments finite. Equipped with the state , where denotes expectation with respect to , this becomes a -probability space.

Definition 2.1.

(Free independence) Let be a non-commutative probability space and let be a collection of unital subalgebras of , indexed by a fixed set . The subalgebras are called freely independent, or just free, if

for every , where

-

(a)

for some ;

-

(b)

for every ; and

-

(c)

neighbouring elements are from different subalgebras, i.e. .

Elements from are called freely independent, or just free, if the unital subalgebras generated by each of them are free.

From now on, will denote a -probability space unless stated otherwise. For , , the number is called a -moment of . If is self-adjoint, i.e. if , then -moments reduce to moments .

Definition 2.2.

A semi-circular variable in a -probability space is a self-adjoint element whose moments are given by

where is the -th Catalan number. It turns out that is the moment sequence of the semi-circular law .

Definition 2.3.

A circular variable in a -probability space is an element of the form

where and are freely independent semi-circular elements.

Definition 2.4.

The -distribution of an element is the linear functional such that

This is equivalent to specifying all the -moments

The -moments (and hence the -distribution) of a circular variable are easy to calculate due to the fact that circular variables are the simplest examples of the so-called -diagonal variables (see, e.g., Chapter 15 of [13]).

To describe these -moments, we first need to talk about non-crossing partitions. Given a totally ordered finite set , we denote by the set of all partitions of . This is in fact a lattice with respect to the reverse refinement partial order: given , if each block of is contained in some block of .

Given a partition , let be its blocks, ordered by their smallest elements. is called the size of and is denoted by . The smallest element of each block will be called a primary element, and the rest of the elements secondary. The smallest element of is the first primary element, that of the second primary element, and so on.

To give an example, let . Consider the partition . In this case, we have three blocks: , and . The elements are the primary elements in that order, the rest are secondary elements.

A partition is crossing if there are elements in such that and for two different blocks of . The partition in the above example is crossing.

Let denote the set of all non-crossing partitions of . This is a sub-lattice of . A partition is called a pair-partition if all its blocks are doubletons. The set of all pair-partitions of will be denoted by . Similarly, the set of all non-crossing pair-partitions of will be denoted by .

We will typically take for some integer . We will write , and instead of , etc. The Catalan numbers introduced earlier count non-crossing partitions: .

We are now ready to describe the -moments of a circular variable.

Proposition 2.1.

Let be a circular variable. Then

Circular variables have as their Brown measure, which is a generalisation of spectral measures of self-adjoint operators to non-normal operators. We will not define Brown measures here and, instead, refer the interested reader to Chapter 11 of [11].

Now we discuss the notion of convergence in -distribution (also called convergence in -moments). We will sometimes abbreviate this to just -convergence.

Definition 2.5.

Let be a sequence of -probability spaces. We say that converges in -distribution to if for all , one has

This is equivalent to the requirement that for any and symbols , one has convergence of the corresponding -moments:

3. Main results

We will first work out some general results when our matrices have entries that are independent random variables with zero mean, unit variance, and uniformly bounded moments of all orders. Then, in Section 3.2, we will allow the entries to form SMSs. Our experience from Section 3.1 will lead us naturally to an admissibility condition on the SMSs, which will be used as a substitute for independence in killing certain joint moments of the entries.

3.1. Some general results

Assumption 3.1.

The input random variables are independent with zero mean, unit variance, and uniformly bounded moments of all orders, i.e. for any ,

Note that this is true if is an i.i.d. collection with zero mean, unit variance, and all moments finite. We make the same assumptions on . Moreover, we assume that and are independent.

We note that these assumptions do imply that .

For , let

If is a patterned matrix, then we may write, using the above notation, .

We now expand the -moments of . Below denotes a multi-index and , are fixed symbols.

| (6) |

where and are convenient shorthands for and , respectively.

To any , associated is a partition of induced by the values of for fixed : belong to the same block if , where . For a partition , we denote by the set of all multi-indices , for which the associated partition is . To give an example, let , , , , and be the Toeplitz link-function. Then the multi-index is associated with the partition of , since and . We will sometimes refer to as an -value at location . Thus, in the above example, and are -values in , both of which are repeated twice ( at locations and , and at locations and ). Finally, note that is a partition of .

Let . and for every primary element of are called generating indices (here ). As there are many primary elements, the total number of generating indices in is if is a primary element of (i.e. is a block of ), and otherwise.

The following assumption is crucial for analysing symmetric patterned random matrices (see, e.g., [4]). We will also need it here.

Assumption 3.2.

For a link-function , let

Thus means that the total number of times a particular input variable can appear in a row or column is uniformly bounded. We assume that .

Note that for both the nonsymmetric Toeplitz and the Hankel link-functions, . An important consequence of having is that any non-generating index can be determined, up to a bounded number of choices, from its predecessor generating indices. We record this in the following lemma, which will be used repeatedly later.

Lemma 3.1.

Suppose . Let . Then one can determine any non-generating , up to a bounded number of choices, from all previous generating .

Proof.

Let be a non-generating index. Then . Further, is a primary element, so that is generating. Thus we must have . Also, must be a secondary element. Thus there exists some such that belong to the same block of . Now we have the relation

| (8) |

As , can be determined from (8), up to a bounded number of choices, for any fixed .

We now use an inductive argument. Taking to be the first non-generating index, we see that can be determined from the choices of the preceding indices all of which are generating. Assume that the first -many non-generating indices can be determined from their predecessor generating indices. By the argument given in the previous paragraph, the -th non-generating index can be determined by previously occurring indices. But since all previously occurring non-generating indices can be determined by their predecessor generating indices, we conclude that is determined by its predecessor generating indices. ∎

The proof of the following lemma is standard. We include it here for completeness.

Lemma 3.2.

Let and . If , then for some constant , depending only on the link-function and .

Proof.

implies that if belong to the same block of , then we have the constraint

Therefore, if , then once the generating indices of have been chosen in one of at most many ways, the non-generating indices can be chosen in at most ways. We can thus take . ∎

Proof.

If or have any singleton blocks, then, by the centredness and independence of the input variables, for any , and hence the left-hand side of (9) is trivially zero.

So we assume that all the blocks of and are of size at least . Since not both are pair-partitions, one of them, say , has a block of size at least . Since the input random variables have uniformly bounded moments of all orders, by Hölder’s inequality. Thus it suffices to show that

This follows from Lemma 3.2 because

where we have used the bound which is true since each block of has size at least and there is at least one block of size at least . ∎

From Lemma 3.3, we immediately get that for odd ,

| (10) |

From now on, we shall work with even and write instead of in the forthcoming expressions.

Note that for pair-partitions , if , then . It follows that

| (11) |

Motivated by the respective definitions in [5], we make the following definitions.

Definition 3.1.

Two link-functions and are said to be compatible if for any , we have

Definition 3.2.

Two link-functions and are said to be jointly circular if

Theorem 3.1.

Proof.

3.2. Entries that form SMSs

Definition 3.3.

A collection of random variables is called an SMS if for all distinct and , , , one has

A trivial example of an SMS would be a collection of independent random variables with zero mean and unit variance. More generally, any martingale difference sequence is an SMS, provided that , and for all 222Examples of such systems are simple to construct. For instance, set with , , and for , take where and is some positive measurable function of .. Another nontrivial example, which is not a martingale difference sequence, is the collection , where .

If is an SMS, is a link-function, and , where is a pair-partition, then it is clear that . To deal with other partitions, we need further assumptions.

Definition 3.4.

Say that an SMS , with having all moments finite for any , is admissible if for all distinct and , , , one has

if there is at least one such that .

A trivial example of an admissible SMS would be a collection of independent random variables with zero mean, unit variance, and all moments finite. Of course, SMSs arising from more general martingale difference sequences do not necessarily satisfy the admissibility condition. Finally, one can verify that the SMS , where , is also admissible.

If is an admissible SMS, is a link-function, and , where is a partition containing a singleton block, then it is clear that .

We tackled partitions that contain no singleton blocks and at least one block of size using Lemma 3.2 and the assumption of uniformly bounded moments of all orders. Note that the collection , where , satisfies this by virtue of being uniformly bounded.

The discussions above show that Assumption 3.1 in Lemma 3.3 and Theorem 3.1 can be replaced by the following weaker assumption.

Assumption 3.1′.

We assume that is an admissible SMS with uniformly bounded moments of all orders, i.e. for any , one has

We make the same assumptions on . Moreover, we assume that and are independent.

3.3. Toeplitz and Hankel

In what follows, we will often find constraints between generating indices. Such constraints will be referred to as killing constraints, because existence of such a constraint will make , thus killing its asymptotic contribution to the relevant -moment.

Also, in non-crossing pair-partitions, there will always exist a block of adjacent elements. Such blocks will be referred to as good. Once we remove a good block, there will be a new good block in the remaining partition (of the reduced set). For example, in the case , consider the non-crossing pair-partition . Here is a good block. After we remove , we get a new good block of adjacent elements in the reduced set .

We first prove a general result regarding joint-circularity.

Lemma 3.4.

Suppose the map is injective and Assumption 3.2 holds. Then and are jointly circular.

Proof.

Suppose that . Then implies that for all , we have

We have two possibilities:

-

(a)

. In this case, we conclude by injectivity that and .

-

(b)

. In this case, we conclude that and .

Since is a non-crossing pair-partition, it has a good block of the form . In the case , we get the constraint . In the case , we get the constraint . In the former case, we cannot choose the generating index freely, i.e. we have a killing constraint; this means that the asymptotic contribution from is zero. On the other hand, in the second case, is a free variable. If we remove the block from , then in the remaining partition of there is another good block of adjacent elements. Apply the above argument again to that block. It is clear that we can have a potentially nonzero contribution only if for all . In the latter case, we get exactly free variables, which shows that . This means that

if is a non-crossing pair-partition.

Now suppose that is a crossing pair-partition. Pick with the property that is the smallest secondary element. Then, as before, we have the contingencies (a) and (b). By the definition of , we must have that is primary and so is generating. Similarly, is also generating, because either or is primary (as ). Thus, in the case , the constraint is a killing constraint. So we assume on the contrary. Then, since both and are generating, we have a killing constraint unless . If the latter is the case, we remove the good block from and apply the above argument again. As is non-crossing, sooner or later we will end up with a partition having no good blocks and hence a nontrivial killing constraint. This means that

if is a crossing pair-partition. ∎

Corollary 3.1.

The nonsymmetric Toeplitz and the Hankel link-functions are jointly circular.

Proof.

Clearly, the map is injective. ∎

Lemma 3.5.

The nonsymmetric Toeplitz and the Hankel link-functions are compatible.

Proof.

Let us take and . Suppose that are pair-partitions. Then the link-functions give us constraints in total. We will show that under these constraints, there can be at most elements that can be chosen freely.

Consider the primary elements in and . Suppose these are not the same for the two partitions. Consider the first element that is primary in but secondary in . Then is generating according to but non-generating according to . Hence, choosing the previous generating indices according to fixes . Since the previous generating indices agree for and , can be determined up to boundedly many choices in terms of previous generating indices. This gives a nontrivial killing constraint.

Now suppose that the primary elements are the same in both and . Then, since , there is an element that is secondary in both and such that there are primary elements with and . Let be the smallest element of this type. Without loss of generality, let us assume that . Then we have

Adding the above two equations, we get

| (12) |

Case I (): Using (12), we get that

which is a killing constraint. Case II (): If is a primary element, then is generating, and we have from (12) a killing constraint. So we assume that is secondary. Therefore there exists a primary element such that is a block of both and . This gives, via injectivity of ,

In the former case, , which, via (12), leads to the relation

This is a killing constraint. In the latter case, , which, via (12), leads to

If , this gives a killing constraint for . If and is primary, then we again have a killing constraint. Finally, if is secondary, we apply the same argument as above with replacing the role of to get a primary element such that is a block of both and , and so on. It is clear that by continuing this procedure we will eventually end up with some primary element , such that is a block of both and and . Then, no matter whether and are equal or not, we have some nontrivial killing constraint. ∎

Together, Corollary 3.1 and Lemma 3.5 give us our main result on nonsymmetric Toeplitz and Hankel matrices.

Theorem 3.2.

Under Assumption 3.1′, if and , then converges in -distribution to a circular variable in expected normalised trace.

3.4. General link-functions

In the proof of Lemma 3.5, we have used three facts about the nonsymmetric Toeplitz and the Hankel link-functions:

- (i)

-

(ii)

The map is injective.

-

(iii)

Equation (12) gives rise to killing constraints.

In order to prove compatibility of two general link-functions and along the lines of Lemma 3.5, we need appropriate assumptions on them so as to have analogues of items (i) - (iii). Assumption 3.2 will give us (i). For (ii), we will assume the injectivity of the map , which we anyway need for joint circularity. Let us now look at the analogue of (12) in the general case.

As in the proof of Lemma 3.5, consider the situation where and have the same primary elements, and the elements encountered there, with and . We then have the simultaneous equations

| (13) |

Denote that map by . Let denote the inverse of . Write . Then from (13), we get that

| (14) |

which is the general version of (12). As in the proof of Lemma 3.5, this gives rise to various types of constraints for different combinations of and . We need to make sure that these are killing constraints.

Lemma 3.6.

Suppose that Assumption 3.2 holds. Let . Then the equation

| (15) |

has an at most bounded number of solutions in (resp. ) when (resp. ) are fixed.

Proof.

Lemma 3.7.

Let . Consider the equation

| (16) |

Then fixing any four variables among constrains the remaining variable to take an at most bounded number of values.

Proof.

Lemma 3.7 will help us get killing constraints from (14) for most values of and . However, in certain degenerate cases we need to make extra assumptions.

Assumption 3.4.

Assume that the link-functions and are such that the map taking is injective. Let denote the inverse of . Write . Let . Consider the following equations obtained from (16) by equating some of the variables.

| (17) |

| (18) |

| (19) |

| (20) |

| (21) |

| (22) |

| (23) |

| (24) |

| (25) |

| (26) |

| (27) |

| (28) |

Assume that Equations (17) and (18) (resp. Equations (24) and (25)) constrain (resp. ) to take an at most bounded number of values when the rest of variables are kept fixed. Assume also that each one among Equations (19)-(23) and (26)-(28) constrain each one among the variables , and to take an at most bounded number of values when the rest of variables are kept fixed.

Lemma 3.8 (Compatibility of general link-functions).

Proof.

We proceed as in the proof of Lemma 3.5. When the primary elements are not the same in and , one can use the same argument as in the proof of Lemma 3.5. Otherwise, we begin with (14). As before, let us consider the case . The other case can be tackled similarly. In Case I, i.e. when , (14) leads to the relation

| (29) |

which gives a killing constraint by Assumption 3.4 (more specifically, via (17) in general, and via (18) in the degenerate case ). Similarly, in Case II, i.e. when , we are led to relations of the form

| (30) |

or

| (31) |

where is a primary element with . Consider (30) first. When all the indices involved are distinct, we get killing constraints by Lemma 3.7. The degenerate cases where some of the indices are equal are covered by Assumption 3.4: the case is covered by (19), the case is covered by (20), the case is covered by (21), and the case is covered by (22).

Now consider (31). If all the indices involved are distinct then we get killing constraints by Lemma 3.7. As for the degenerate cases, Assumption 3.4 again comes to our aid. The case gives us (29) which is a killing constraint as seen earlier. On the other hand, the case is covered by (23).

Thus we end up with killing constraints in all possible scenarios and hence the proof is complete. ∎

Theorem 3.3 (General link-functions).

The following are a couple of examples where one can verify Assumptions 3.2 and 3.4:

-

(1)

, .

-

(2)

, .

An example of a pair of link-functions which do not satisfy Assumption 3.4 is . One can check that in this case . For , the constraint (17) becomes

As vanishes from the constraint altogether, fixing the other variables does not impose any constraints on , thus violating Assumption 3.4. This creates troubles in the proof of Lemma 3.8. For instance, in the case , the relation (29) gives us

i.e.

| (32) |

For , unless is generating, we do not necessarily have a killing constraint here, and additional work is required to find one. In this case, one may argue as follows: by Lemma 3.1, considering the constraints coming from only, one can determine a non-generating up to a bounded number of choices from its predecessor generating indices (in fact, due to the linear nature of the constraints, one can explicitly solve for in terms of the previous generating indices). On the other hand, (32) gives a different linear constraint on . Together these two separate constraints on create a killing constraint between the predecessor generating indices of .

We believe that the line of argument given above works for all pairs of linear link-functions , where are integers with nonzero and , even if these link-functions do not satisfy some parts of Assumption 3.4, and the arguments given in the proof of Lemma 3.8 do not yield killing constraints in all of the cases considered. However, since writing down the constraints explicitly for general is rather cumbersome, we remain content with an informal discussion.

3.5. Almost sure convergence

Earlier we have shown convergence of the -moments in expected normalised trace. However, a stronger result can be established under Assumption 3.1—the -moments in normalised trace converge almost surely to the -moments of a circular variable. The proof of this is essentially the same as the proof of Lemma B.1 of [5], modulo some minor details. On the other hand, under Assumption 3.1′, we are only able to show in-probability convergence. This requires some new combinatorial arguments.

Theorem 3.4.

Suppose that Assumption 3.2 holds and the link-functions and are compatible and jointly circular. Let be a circular variable in some -probability space .

Note that in order to prove almost sure/in-probability convergence of to , where , it is enough to show convergence for monomials. Now, since we have already shown that

for any and , in order to prove almost sure/in-probability convergence, it is enough to control centred moments of suitably. For example, in case of in-probability convergence, it is enough to show that

| (33) |

On the other hand, for almost sure convergence, it is sufficient to show that

for any and , which can be established by showing that

for some .

To this end, we will establish bounds on the fourth centred moment of under Assumptions 3.1 and 3.1′.

Lemma 3.9.

Remark 3.1.

Before we prove Lemma 3.9, we need to discuss the concept of matching of multiple multi-indices. Let denote the multi-index . Fix . We say that the multi-indices are jointly -matched if every -value occurs at least twice across all the multi-indices. If every -value occurs exactly twice across all the multi-indices, then we say that the multi-indices are jointly -matched in pairs. We say that are across -matched, if every multi-index has at least one -value that appears in at least one of the other multi-indices.

Proof of Lemma 3.9.

As in (3.1), we can use multi-indices to write

Therefore

| (34) |

The strategy now is to split the sum into a bounded number of sub-sums according to the matching properties of the multi-indices , and show that each of these sub-sums are , where (we show that under Assumption 3.1, one can take for all of these sub-sums, whereas under Assumption 3.1′, for certain sub-sums). This is done by showing that (i) the summands are exactly for certain sub-sums, rendering those sub-sums exactly , and (ii) for the remaining sub-sums, the summands are bounded by some constant that depends only on , and the number of such summands is .

We first carry out the above programme under Assumption 3.1′ to prove part (a).

Case 1 ( is neither jointly -matched, nor jointly -matched). Note that if is not jointly -matched, then one of the ’s, say , will have a single occurrence of an input random variable making (by the admissibility of the SMS ). This would mean that

Here we are using the admissibility , and the independence of and . The same conclusion can be made if is not jointly -matched.

Case 2 ( is both jointly -matched and jointly -matched, but neither across -matched, nor across -matched). In this case, some multi-index, say , is only self--matched, i.e. none of its -values appear among the -values of any of the other multi-indices. Similarly, some multi-index, say is only self--matched. The case can be tackled in the exact same manner as in the proof of Lemma B.1 of [5]. The idea is that by Assumption 3.1′, the entry variables have uniformly bounded moments of all orders, so by an application of Hölder’s inequality, is bounded by some constant that depends only on , and not . Thus it is enough to bound the possible number of quadruples of multi-indices obeying the condition . In [5], an bound for some is established via a case-by-case counting argument.

Now consider the case . Without loss of generality, we assume that . Then can be chosen in ways. The remaining multi-indices are jointly -matched as well as jointly -matched. We now employ a case-by-case analysis.

-

(1)

Consider the case where is either across -matched or across -matched. In this case, Lemma A.1 of [5] tells us that can be chosen in ways. Thus the total number of choices for is which is when is even. In fact, by considering the case where the multi-indices are jointly -matched in pairs as well as jointly -matched in pairs, it is not hard to see that the number of choices is exactly of order . Thus, in this case, we cannot get a bound for some .

-

(2)

Now consider the case where is neither across -matched nor across -matched. Then some is only self--matched, and some is only self--matched. Again, we may have two contingencies: or . If , then we can proceed like the case and ultimately prove an bound. So let us consider the case . Assume, without loss of generality, that . Then can be chosen in ways.

-

i.

If is either across -matched or across -matched, then by Lemma A.1 of [5], can be chosen in ways. Thus, in this case, the total number of choices for is

Again, the upper bound can be attained by considering multi-indices that are jointly -matched in pairs as well as jointly -matched in pairs.

-

ii.

Otherwise, is neither across -matched nor across -matched. In this case, all the multi-indices are self--matched as well as self--matched. If any one of these multi-indices has an -value or -value repeated at least thrice, then that multi-index can be chosen in at most ways (this bound can also be attained). In that case, the total number of choices for is

However, if each of the multi-indices is self-matched in pairs with respect to both and , then the total number of choices is . This would have led to a bound on (34), were it not for the fact that we can do an exact computation in this case. As each of the multi-indices is self-matched in pairs with respect to both and , we get by strong multiplicativity that for any . This means that

It is easy to see using strong multiplicativity and the independence of the ’s and ’s that the product on the right-hand side vanishes when we expand it.

-

i.

We thus see that under Assumption 3.1′, we only have an upper bound on the number of multi-indices in the case.

Case 3 ( is both jointly -matched and jointly -matched, and also either across -matched or across -matched). In this case, by Equation (B.1) of [5], we get that can be chosen in ways.

We now turn to part (b). In Cases 1 and 3, and in the sub-case of Case 2, we have already established bounds, for some , under Assumption 3.1′, which therefore continue to hold under the special case of Assumption 3.1. In the sub-case of Case 2, for which we only have an bound under Assumption 3.1′, we can do much better under Assumption 3.1. Indeed, when and Assumption 3.1 is true, is independent of , and is independent of . Also, since the ’s and the ’s are independent, we can write

Thus the contribution of the relevant sub-sum is exactly . This leads us to an overall bound on under Assumption 3.1, and completes the proof of part (b). ∎

Proof of Theorem 3.4.

As we have discussed earlier, in-probability (resp. almost sure) convergence of under Assumption 3.1′ (resp. Assumption 3.1) to , where , follows from Lemma 3.9.

Further, as the collection of monomials is countable, after one shows almost sure convergence for monomials, one can club all the relevant null sets into a single null set outside which pointwise convergence holds for monomials and hence for all polynomials. This proves that almost surely, converges in -distribution, as an element of the -probability space , to a circular variable under Assumption 3.1. ∎

From Theorem 3.4-(a), we can obtain as a direct corollary one of the main results of [5], namely the almost sure weak convergence of the ESM of the -scaled Schur-Hadamard product of symmetric Toeplitz and Hankel matrices to the semi-circular law, under Assumption 3.1.

Corollary 3.2.

Suppose that Assumption 3.1 holds. If and , then the ESM of converges weakly almost surely to the semi-circular law.

Proof.

If is as in Theorem 3.2, then is the Schur-Hadamard product of a symmetric Toeplitz matrix and a Hankel matrix, whose entries satisfy Assumption 3.1, except that the diagonal entries of the symmetric Toeplitz matrix has variance —but this does not matter since changing the diagonal entries does not affect the LSM (see, e.g., Theorem 2.5 of [2]). Now, using Theorem 3.4, we conclude that almost surely for all ,

This implies the desired result by moment method because is a semi-circular variable if is circular. ∎

Acknowledgements

We thank the anonymous referees for their many helpful comments and suggestions that significantly improved the paper.

References

- [1] G. Alexits. Convergence Problems of Orthogonal Series. Pergamon Press, New York-Oxford-Paris, 1961.

- [2] Z. Bai and J. W. Silverstein. Spectral Analysis of Large Dimensional Random Matrices. Springer, New York, 2nd edition, 2010.

- [3] A. Basak, N. Cook, and O. Zeitouni. Circular law for the sum of random permutation matrices. Electronic Journal of Probability, 23(33):1–51, 2018.

- [4] A. Bose. Patterned Random Matrices. CRC Press, Boca Raton, FL, 2018.

- [5] A. Bose and S. S. Mukherjee. Bulk behavior of Schur–Hadamard products of symmetric random matrices. Random Matrices: Theory and Applications, 3(02):1450007, 2014.

- [6] W. Bryc, A. Dembo, and T. Jiang. Spectral measure of large random Hankel, Markov and Toeplitz matrices. The Annals of Probability, 34(1):1–38, 2006.

- [7] V. F. Gaposhkin. A central limit theorem for strongly multiplicative systems of functions. Mathematical notes of the Academy of Sciences of the USSR, 6(4):720–724, 1969.

- [8] A. Guionnet, M. Krishnapur, and O. Zeitouni. The single ring theorem. Ann. of Math. (2), 174(2):1189–1217, 2011.

- [9] C. Hammond and S. J. Miller. Distribution of eigenvalues for the ensemble of real symmetric Toeplitz matrices. Journal of Theoretical Probability, 18(3):537–566, jul 2005.

- [10] M. W. Meckes. Some Results on Random Circulant Matrices. In High dimensional probability V: the Luminy volume, pages 213–223. Institute of Mathematical Statistics, Beachwood, OH, 2009.

- [11] J. A. Mingo and R. Speicher. Free Probability and Random Matrices. Springer, New York, 2017.

- [12] H. H. Nguyen and S. O’Rourke. The elliptic law. Int. Math. Res. Not. IMRN, (17):7620–7689, 2015.

- [13] A. Nica and R. Speicher. Lectures on the Combinatorics of Free Probability. Cambridge University Press, Cambridge, 2006.

- [14] T. Tao, V. Vu, and M. Krishnapur. Random matrices: Universality of ESDs and the circular law. The Annals of Probability, 38(5):2023–2065, 2010.

- [15] D. Voiculescu. Limit laws for random matrices and free products. Inventiones mathematicae, 104(1):201–220, 1991.