Convergence of Deep Fictitious Play for Stochastic Differential Games

Abstract

Stochastic differential games have been used extensively to model agents’ competitions in Finance, for instance, in P2P lending platforms from the Fintech industry, the banking system for systemic risk, and insurance markets. The recently proposed machine learning algorithm, deep fictitious play, provides a novel efficient tool for finding Markovian Nash equilibrium of large -player asymmetric stochastic differential games [J. Han and R. Hu, Mathematical and Scientific Machine Learning Conference, pages 221-245, PMLR, 2020]. By incorporating the idea of fictitious play, the algorithm decouples the game into sub-optimization problems, and identifies each player’s optimal strategy with the deep backward stochastic differential equation (BSDE) method parallelly and repeatedly. In this paper, we prove the convergence of deep fictitious play (DFP) to the true Nash equilibrium. We can also show that the strategy based on DFP forms an -Nash equilibrium. We generalize the algorithm by proposing a new approach to decouple the games, and present numerical results of large population games showing the empirical convergence of the algorithm beyond the technical assumptions in the theorems.

Keywords: Deep fictitious play, convergence analysis, stochastic differential games, Markovian Nash equilibrium, backward stochastic differential equations.

1 Introduction

Deep neural network has become a popular and powerful tool in scientific computing, for its remarkable performance in approximating high-dimensional functions. Its success has brought natural applications in stochastic differential games, where high-dimensional optimization problems and/or stochastic differential equations are solved to provide the modeling and analysis of tactical interactions among multiple decision-makers in the context of a random dynamical system. These decision-makers, usually referred to as players or agents, can interact in a manner ranging from completely non-cooperative to completely cooperative. The nature of uncertainty makes stochastic differential games appropriate to be used for the study of competitions in Finance, e.g., in P2P lending platforms [63, 46] from the Fintech industry and insurance markets [65, 6, 18].

For non-cooperative stochastic differential games, a core problem is to compute the associated Nash equilibrium, which refers to a set of strategies so that when applied, no player will profit from unilaterally changing her own choice. When the games involve heterogeneous agents of moderate size, e.g., , computing the Nash equilibrium becomes numerically challenging since conventional numerical algorithms lose their efficiency for beyond , and the mean-field framework has not started to work well with asymmetric players.

To address the challenge, the authors have recently proposed the deep fictitious play (DFP) algorithms [30], providing a novel efficient tool for finding Markovian Nash equilibrium of large -player asymmetric stochastic differential games. However, despite the efficient performance in simulation, the algorithm’s theoretical foundation is still lacking, which will be the focus of this paper. In addition, we generalize the previous algorithms, and propose a general two-step scheme: The first step aims to recast the game into sub-problems that will be repeatedly solved. The desired algorithm requires that, after the recast, the sub-problems are decoupled among different players given the previous stage’s solutions, and that their solutions converge to the true Nash equilibrium. Specifically, we propose two options for the first step:

-

I.

Fictitious play. This approach was used in [30], assuming that players are myopic and will choose their best responses against others’ previous stage action at every subsequent stage. Therefore each player still faces a nonlinear optimization problem.

-

II.

Policy update. This approach calculates the game values using all responses from the previous stage, and the current stage responses are determined as if they are the optimizers of the calculated game values.

The second step of the DFP algorithm aims to solve the sub-problems efficiently and accurately. Remark that, due to the large number of players and the high dimensionality of the controlled state process, each sub-problem may still be high-dimensional after the decoupling step. In [30], the Deep BSDE method was employed for each sub-problem, which presents excellent performance. It relies on the BSDE representations of semi-linear partial differential equations (PDEs) and deep learning approximations after discretizing the BSDE by an Euler scheme. It parametrizes the initial position of the backward process and the adjoint process by DNNs, then simulates both processes in a forward manner, aiming to minimize the discrepancy between the terminal value of the backward process and its network approximation. The analysis for the second step shall focus on this method. Meanwhile, we remark that other deep neural networks (DNNs) based algorithms, such as deep learning backward dynamic programming (DBDP) method [39] and deep Galerkin method [62], are also promising choices for solving sub-problems.

Related literature. The theoretical study of differential games was initiated by R. Isaacs in the early 1960s [41]. Later on, to better describe read world’s uncertainties, noises are added to the state of the system, and stochastic differential games now have been intensively used across many disciplines. Domains of applications include management science (e.g., operations management, marketing, finance, systemic risk), economics (e.g., industrial organization, environmental and macroeconomics, production of exhaustible resources), social science (e.g., networks, crowd behavior, congestion), biology (e.g., flocking), and military (e.g., cyber-attacks).

Fictitious play is well documented in the economics literature, as a learning process for finding Nash equilibria. It was firstly proposed by [10, 11] for normal-form games. Since then, there have been extensive studies on the convergence of fictitious play or its variation under different setting, for instance, see [50, 51, 45, 35, 7]. For stochastic differential games, besides [30], the most related work is [37], where fictitious play is used to design numerical algorithms for finding open-loop Nash equilibria. We remark that, the idea of fictitious play is not limited to study the games with a moderate number of heterogeneous players [37, 30], but has also been applied in mean-field games, e.g., see [12, 9, 22].

The proposed policy update for the first step of the DFP algorithm closely follows policy iteration (PI) in spirit, which was initially introduced by Howard [36] for discounted Markovian decision problems (MDP). It consists of two steps: policy evaluation (obtaining the expected reward for a given policy) and policy improvement (updating the policy using the rewards for successor states). PI was later generalized to modified PI in [61], and has remained as the method of choice in designing reinforcement learning algorithms, e.g., see [27, 59] and the references therein.

The literature of using DNNs for learning high-dimensional function is rich, including methods for solving high-dimensional parabolic PDEs and BSDEs (e.g., the deep BSDE method [20, 31], the DBDP [39, 24], and many others [62, 4, 5, 58, 64, 42]). It also yields algorithms for solving the Schrödinger equation [34, 57, 33], stochastic control problems [29, 52], mean field games [17, 1] and nonlinear optimal stopping problems [38].

Main contribution. The contribution of this paper consists of the following: 1. We propose a general two-step scheme that extends the original deep fictitious play algorithm [30], and provide two options for solving the first step. The proposed algorithm can efficiently solve stochastic differential games with heterogeneous agents of large size (e.g., ), and the presence of common noise. 2. We provide the theoretical foundation for the proposed algorithms. In specific, with small time duration, we prove that the solutions to the decoupled sub-problems, if solved repeatedly and exactly at each stage, converge to the true Nash equilibrium; that the numerical solutions to each sub-problem tend to be exact as we refine the time step in the Euler scheme; and that the strategy based on numerical solutions forms an -Nash equilibrium, after running sufficiently many stages and using sufficiently fine time step. 3. We present numerical results showing empirical convergence even beyond the technical assumptions used in the theorems.

The rest of this paper is organized as follows. In Section 2, we give the mathematical formulation of general -player asymmetric stochastic games in continuous time. The algorithms consisting of the decoupling step and sub-problem-solving step via deep learning are detailed in Section 3. Section 4 provides convergence analysis for the proposed algorithms, followed by numerical examples presented in Section 5. We make conclusive remarks in Section 6.

2 Mathematical Formulation

Throughout the paper, we shall use the following notations:

-

•

A boldface character refers to a collection of objects from all players;

-

•

A regular character with a superscript refers to an objective from player (no matter a scalar or a vector) or the column of a vector;

-

•

A boldface character with a superscript refers to a collection of objects from all players except ;

-

•

The state process introduced below is a common process to all players, and will always be in boldface.

We consider a general -player non-zero-sum stochastic differential games. An -valued common state process is controlled by a Markovian strategy/policy111Hereafter, we shall use strategy and policy interchangeably. :

| (1) |

where is the collection of all players’ -valued strategies. For simplicity, we assume for . If not (e.g., some boundedness constraints are put on ), we can assume there exist Lipschitz mappings from to so that , and all the statements below hold easily with the help of the Lipschitz mappings. The drift and diffusion coefficients and are deterministic functions of the common state, , , where is the space for the joint control , and is a -dimensional standard Brownian motion on a filtered probability space .

Player aims at minimizing her expected total cost:

| (2) |

by choosing among all admissible strategies :

| (3) |

where the running cost and the terminal cost are deterministic measurable functions. Obviously, the quantity in (2) is also affected by other players’ strategies . To emphasis this dependence, we introduce the notation for the cost of player starting at when players choose their strategies :

| (4) |

In the following sections, we shall present the algorithms for solving the above game and prove its theoretical convergence. In particular, we are interested in finding a Markovian Nash equilibrium (or the Markovian -Nash equilibrium).

Definition 2.1.

A Markovian -Nash equilibrium is a tuple , such that, for non-negative ,

| (5) |

A Markovian Nash equilibrium, denoted by , is equivalent to an -Nash equilibrium where . Here is the product space of , and is the set of all players.

As discussed in [30], the formulation (1)–(2) is less restrictive than the usual case where player can only control her private state. Here, a common state is controlled by all agents, which is a common feature in economics literature (see e.g., [19, 60, 47]). Therefore, it is important to include it in our framework, although this will increase the coupling and make the problem harder to solve, both theoretically and numerically. Remark that the difficulty still persists in the limiting problem as with indistinguishable players, when allowing entering into others’ states. This is called the extended mean-field game and it has attracted certain attention recently (e.g., [25, 26, 13]). On the other hand, by choosing and in (1) properly, one can reduce the formulation (1) to the simpler case where each player controls her private state through . For instance, if each player’s private state is -dimensional, we can let , with for , then the problem (1)–(2) is the standard modeling in literature in many disciplines including social science, management science and engineering, with the player’s -dimensional private state controlled by only.

In the Markovian setting, the value function of player reads as:

| (6) |

Then, to compute the Markovian Nash equilibrium, we apply the dynamic programming principle and obtain a system of Hamilton-Jacobi-Bellman (HJB) equations:

| (7) |

where , denote the derivative of with respect to , the gradient and the Hessian of function with respect to , and Tr denotes the trace of a matrix. Note that the HJB system (7) is coupled, as each minimizer depends on and the function and in (7) depend on all minimizers .

Under appropriate conditions, the solution to (7) is related to BSDEs, using nonlinear Feynman-Kac formula (cf. [54, 21, 55]). To ease our notations of the BSDEs, we prescribe the following the relation on and .

Assumption 1.

There exists a measurable function : , so that for any .

Consequently, we can define the Hamiltonian function by:

| (8) |

where denotes the column of , and thus is an vector. Using this notation, the HJB system can be rewritten as:

| (9) |

To better describe the optimal game policies, we define by:

| (10) |

In other words, is the minimizer of the Hamiltonian, with an emphasis of the dependence on the player’s game value and others’ strategies . Then, we define a function as the fixed point of

| (11) |

Note that, with the above notations and , we have assumed the minimizer in (10) exists and is unique, and (11) has a unique fixed point. Later in Assumption 2, we will detail explicit conditions on the model parameters, such that these assumptions are satisfied.

We now state the corresponding BSDE formulation of (7), which is the key component of the algorithm design in Section 3 and the convergence analysis in Section 4. Let be the solution to the following BSDE:

| (12) |

where is the minimized Hamiltonian vector, and is the vector form of all terminal costs. Then we have the relation:

| (13) | |||

| (14) |

and the optimal game policy is expressed by

| (15) |

Using the relation (14), we notice 222We use as an matrix., and sometimes write .

Remark 1.

Note that the process in (12) does not allude to in the controlled dynamics defined in (1). Indeed, it is an auxiliary forward stochastic process derived from the HJB system (6) using the nonlinear Feyman-Kac formula, which is an object different from the controlled process in equation (1). One, of course, has the flexibility to choose a different forward process with nonzero drift:

| (16) |

and to express the solution to (9) via (14) with all replaced by . This is essentially rewriting equation (9) to

| (17) |

and take as the driver. Note that due to the coupling in (9), needs to be identical across all . Nevertheless, we think the choice in (12) is the most natural one, without additional knowledge of .

In the next section, after we introduce the decoupling step, each sub-problem is also interpreted via a BSDE system (cf. (22) and (24)). There, though one can freely choose different for each backward process thanks to the decoupling, we still choose the forward process without a drift term as we did in (12) for multiple reasons. We defer this explanation to Remark 2.

If solving directly, no matter which system ((7) or (12)), one will encounter computational difficulties due to the high dimensionality of or the large number of agents. To overcome this, we propose a two-step scheme in Section 3, where we generalize the idea in [30] and offer two options for the first step. The convergence analysis with appropriate assumptions will be presented in Section 4.

3 Algorithm

The two-step scheme for solving Markovian Nash equilibrium works as follows. We first decouple the problem (1)–(2) into independent sub-problems, for which we need to solve repeatedly and can solve in a parallel manner. Since each sub-problem may still be high-dimensional, we then solve them using deep neural networks with a reformulation in backward stochastic differential equations (BSDEs). Next, we describe the algorithms for each step in detail.

3.1 Step I: Decoupling

This step aims to decentralize the game, converting it into single-agent problems to be solved repeatedly. The algorithms start with an initial guess of the Nash equilibrium and produce a sequence of strategies afterward, which we denote by . The following two options at this step differ in how the sequence is determined. Notationwise, refers to the collection of all players’ policies at stage , and its component refers to player ’s choice.

-

1.

Fictitious Play. In this option of Step I, at each stage, each player faces an optimization problem (2) while assuming that others are using their strategies from the previous stage as fixed strategies. In other words, at stage , is known to all players, and player ’s decision problem is

(18) where is defined in (4), and the state process follows (1) with being replaced by . Here represents the strategies of all players but player at stage , and is a short notation of , which emphasis the parameter role of .

Under the Markovian framework, we denote by the problem value of player at stage . Following the idea of fictitious play, it is the solution of the following HJB system

(19) -

2.

Policy Update. This is slightly different from fictitious play, where every player follows her strategy from the previous stage to update the problem value. In this case, it is no longer an optimization, but a linear problem for the value function induced by the fix strategy :

(20)

After solving out the decoupled PDE (19) or (20), at the end of stage , a policy is determined by

| (21) |

and policies from all players together form .

Note that for fictitious play algorithms, is indeed the optimal strategy of problem (18); while for policy update algorithms, the problem is linear, but we pretend that is the value of an optimization problem, and is determined as if it is an optimizer. In short, the two algorithms differ at how is update from . When interpreting via BSDEs, the different update rules result in slightly different drivers of the backward components, see equations (22) and (24) below. Nevertheless, the analysis based on the two algorithms presented in Theorems 2 and 3 follows similarly.

3.2 Step II: Solving Each Sub-problem via BSDE

For each sub-problem, described by (19) or (20), we write down their BSDE counterpart:

| (22) |

where is defined by

| (23) |

or

| (24) |

Here is a random variable whose range covers the states of interest.

Remark 2.

Note that, in both BSDEs above, we choose the forward process without a drift term for three reasons: (a) it avoids the involvement of , and thus keeps the forward process the same from stage to stage; (b) the BSDEs can be vectorized (cf. (39)) with a single forward process which coincides with forward component of (12) (corresponding to the true solution), both will facilitate our analysis (c) numerically, this means only one forward process needs to be simulated for all sub-problems, which makes one iteration of step I–II more efficient.

For both sub-problems, the connection between the associated BSDEs and PDEs are the same:

| (25) |

and according to (21), both optimal policy processes at stage are expressed by

| (26) |

Therefore, it suffices to solve these two possibly high-dimensional BSDE systems by an efficient algorithm, which we shall describe and call deep BSDE in the sequel. To avoid repetition and cumbersome notation, the algorithms will be presented on a generic BSDE with possibly non-zero drift term:

| (27) |

The algorithm applied to the exact system (22) and (24) will be presented in Section 4.2.

The deep BSDE is firstly introduced in [20], for solving high-dimensional parabolic PDEs. The idea is to solve a single variational form of (27) after a temporal discretization version using deep neural networks. For a partition of size on the time interval , and are short notations for the time and Brownian motion increments respectively, and we denote by the mesh of this partition:

| (28) |

We also define a step function , and a set for later use:

| (29) |

The deep BSDE method solves the minimization problem:

| (30) | |||

| (31) | |||

| (32) |

where and are hypothesis spaces related to deep neural networks, and for brevity, we use the notation for , for , etc. The goal is to find optimal deterministic maps such that the loss function in (30) is minimized. Intuitively, the smaller of (30) provides the better approximation to the original problem (27). In practice, the expected value is replaced by the loss of a very deep neural network, which is formed by stacking all the subnetworks in sequence according to (32). The loss is computed by generating sample paths of and producing (31)–(32). At each stage, there are losses corresponding to sub-problems solved by the deep BSDE method.

Here we recall a convergence theorem for the deep BSDE method from [32].

Theorem 1.

For the generic BSDE (27), we assume:

-

1.

The functions , , and satisfy the following Lipschitz condition:

for a constant ;

-

2.

The functions , and are all 1/2-Hölder continuous with respect to . For simplicity, we use for this Hölder constant.

-

3.

We also use to denote the upper bound of , , and .

Then, we have the following two estimates:

| (33) | |||

| (34) |

where and are the hypothesis spaces for neural network architectures to approximate and , and are given in (28)–(29), , and is a constant only depending on , , and .

Remark 3.

Theorem 1 is a brief summary of Theorems 1 and 2 in [32]. The first inequality (33) shows that the distance between the true solution of BSDE (27) and the output of the deep BSDE method can be controlled by its loss function. In other words, in practice, the accuracy of the numerical solution is effectively indicated by the value of loss function. The second inequality (34) states that a small loss function of the deep BSDE method is attainable if the hypothesis spaces ( and ) can approximate specific functions well. Beyond Theorems 1 and 2 in [32], there are still some theoretical issues remaining unresolved regarding the deep BSDE method, which are common in almost all the algorithms involving deep neural networks: First, it is unclear yet that what types of hypothesis spaces can approximate the specific functions in the deep BSDE method without the curse of dimensionality (i.e., the number of parameters of neural networks grows at most polynomially both in dimension and the reciprocal of the approximation error). Second, even with suitable function spaces, it is hard to guarantee the optimization algorithm can find approximately the minimizer of the highly nonconvex loss function. We refer the interested readers to [20, 31, 32] for more detailed descriptions and theoretical justifications of the deep BSDE method. Details on the implementation in this paper are presented in Section 5.

4 Convergence Analysis

This section will provide the theoretical foundation for the deep fictitious play algorithm. Section 4.1 focuses on the decoupling step. Theorem 2 proves the convergence to the true Nash equilibrium, if the decoupled sub-problems are solved exactly and repeatedly. Section 4.2 focuses on the numerical error on the deep BSDE algorithm for solving each sub-problem. Theorem 3 presents a game version of Theorem 1. Section 4.3 combines the previous results, identifies the -Nash equilibrium produced by deep fictitious play, and analyzes its numerical performance on the original game.

4.1 Convergence Analysis of the Decoupling Step

In this section, we will focus on the convergence of the decoupling step, i.e., how the systems defined by PDEs (19) (fictitious play) or (20) (policy update) converge to the system defined by PDEs (7), or equivalently, how the corresponding BSDE systems (22) (fictitious play) or (24) (policy update) converge to the BSDE system (12).

Throughout this paper, we shall use the following assumptions.

Assumption 2.

We shall use , and to denote the Euclidean norm, Frobenius norm and spectral norm, respectively.

-

(1)

The functions , , and are Lipschitz with respect to and :

Here is a positive constant.

- (2)

-

(3)

The functions and are uniformly bounded:

Here denotes the i-th component of and is a positive constant.

-

(4)

The functions , , , and are all 1/2-Hölder continuous with respect to . We shall use as the upper bound of all the Hölder constants.

-

(5)

The constant is also the upper bound of constants , , , and .

Assumption 3.

We remark that Assumption 2 is quite standard in the analysis of stochastic differential games and Assumption 3 can be satisfied in several cases. For instance, Assumption 3 holds true under Assumptions 1 and 2 with small time duration. We provide a detailed proof of this point (Proposition 6) in the appendix. Note that the small time duration assumption is commonly seen in games, for instance in solving mean-field games [15] and in the convergence of numerical schemes for mean-field games [3]. Besides, through the nonlinear Feynman-Kac formula and the boundedness of in Assumption 2, Assumption 3 is also satisfied if the solution to the HJB system (7) is uniformly Lipschitz with respect to . Specifically, with additional assumptions:

| (36) |

is indeed continuous and differentiable with bounded and continuous gradients on (cf. [14, Proposition 2.13]). Therefore, using small time duration result (Proposition 6) on for small , one has the uniformly Lipschitz on and Assumption 3 is fulfilled under (36). We also point out that Assumption 3 implies that the BSDE system (12) has a unique adapted -integrable solution, which will be shown in Proposition 7 in the appendix.

Recalling that is the index of the stage in the decoupling step, now we present the main result in this section regarding its convergence.

Theorem 2.

Proof.

Theorem 2 states the convergence of both fictitious play (according to (22)) and policy update (according to (24)). The proofs of these two are very similar, and we shall focus on the fictitious play method for brevity.

To perform convergence analysis, we first rewrite the BSDE systems to show the explicit dependence on the players’ strategies. For (12), it reads as

| (38) |

where are defined in (8) and (10). The rewritten system of (22) is

| (39) |

where , and stands for the column of . Note that this is slightly an abuse of notation with (23), to show the driver’s explicit dependence on . Also note that the rewritten system (39) is simply a condensed form of (22), concatenating all into , without changing its decoupled nature. This will also ease the notation in the following proof.

We now define . Noticing that

| (40) |

Therefore, with Assumptions 2 and 3,

| (41) |

where are two positive constants only depending on , and .

Next, we define , , . With equations (38) and (39), we have

| (42) |

For any , by Ito’s formula, taking expectation on both sides and integrating from to , we have

| (43) | ||||

| (44) |

where the inequality holds because . Then, taking the supremum with respect to , we deduce

| (45) |

Choosing , we can obtain

| (46) |

For , using inequality (4.1) again, we have

| (47) |

The Lipschitz condition of the function and estimate (47) give that

| (48) |

which is equivalent to (further assuming

| (49) |

For a given , we can choose large enough such that

| (50) |

Then, there exists a constant that only depends on , , , and such that

| (51) |

Combining the last inequality with inequalities (46) and (47), we obtain our result. ∎

Remark 4.

We remark that the convergence in Theorem 2 holds for games with any size of instead of the focus in the numerical algorithm which is between 5 and 100, and is independent of any numerical scheme.

4.2 Numerical Error Analysis

This section is dedicated to analyzing the numerical error introduced by the deep BSDE method when solving each sub-problem. Specifically, we aim to control the distance between defined in (12) and the discrete system satisfying:

| (52) |

where is either with when decoupled through fictitious play, or when decoupled through policy update. As stated in Section 3.2, and are paramterized by neural networks,

where and are the optimal deterministic maps determined at stage that belongs to the hypothesis spaces (cf. Section 3.2). Afterwards, the -stage policies defined on are updated by:

| (53) |

where . Note that the above notation is simply a vector form of the deep BSDE method applied to system (22) or (24). It does not change the decoupling nature of the deep fictitious play algorithm, i.e., each entry in still solves its own problem.

Initially, we hope to apply Theorem 1 to the BSDE system and . By the game feature and the decoupling scheme, stage ’s estimates rely on the regularity of stage ’s policy (see definition in (21)). Specifically, it requires the following condition, in addition to Assumption 2:

| (54) |

However, in general, this property is not inherited from stage to stage. To circumvent this issue, we introduce a projection operator, which needs to be applied at the end of each stage. Along this line, we need the following assumption.

Assumption 4.

The optimal policy as a function on is Lipschitz with respect to and 1/2-Hölder continuous with respect to , i.e.,

| (55) |

We also assume that for any .

Recall the set containing all endpoints of the partition on from (29), for any we define a Hilbert space on :

| (56) |

with norm , and a subset

with a constant . We claim that is a closed convex subset of , so the projection from to exists and does not increase distance (cf., [8, Chapter 5]):

| (57) |

The convexity of is straightforward. To see the closedness, let be a convergent sequence in , then there exists a subsequence of , denoted by , that converges to a.s.. Since

and let , we obtain

Noticing that the functions in and are identical if they agree almost everywhere, we can conclude and is closed.

Therefore, we are able to apply the projection operator at the end of each stage, i.e., we change equation (53) to

| (58) | |||

| (59) |

By this definition, the numerical solution in fact implicitly depends on the value of . We suppress this dependence for brevity of notation. The main theorem in this section is as follows.

Theorem 3.

Under Assumptions 1–4, let be a measurable function satisfying:

| (60) |

Then, for any , assuming that in (56), where is a constant depending on , , , and , we have

| (61) |

where is defined in (52), for , and is a constant depending only on , , , , , , , and . Here represents either the discrete BSDE system using fictitious play or policy update in the decoupling step, depending on the definition of in (52).

Next, with a slight abuse of notation (see Remark 5 (2) for details), we define as

with from the BSDE systems (22) in the setting of fictitious play or (24) in the setting of policy update, in which the previous stage policy is given by the extension of the numerical approximation in time

| (62) |

Then we have the following inequality

| (63) |

where and are hypothesis spaces for neural network architectures to approximate and , and is a constant only depending on , , , , , and . We still refer and as the hypothesis spaces for , , without introducing superscript to indicate the stage.

Remark 5.

We have the following remarks regarding Theorem 3:

-

(1)

The interpretation of Theorem 3 is similar to that of Theorem 1. The first inequality (3) shows that the distance between the true solution of BSDE (12) and the output of the deep BSDE method at stage can be controlled together by the mesh size, the error of the initial policy and the loss functions achieved at all the previous stages. The second inequality (3) states that the loss function of deep BSDE method at each stage is small if the approximation capability of the parametric function spaces ( ( and ) is high. The overall message conveyed in Theorem 3 is that, if the deep BSDE method can solve each sub-problem accurately enough, the deep fictitious play method will produce a strategy close to the Nash equilibrium.

-

(2)

Note that there is a slight abuse of notation in the statement of Theorem 3, since and have already been introduced in Sections 4.1 and 3.1, as the theoretical solution from the decoupling step at stage . In this section, to avoid introducing further complicated notations, we still refer as the theoretical solution depending on , but is the interpolation (62) of the deep BSDE solution at stage . Nevertheless, the relation between and the interpolated strategy in theorem 3 remains the same as the relation between and the exact strategy in Theorem 2, thus some estimates follow using the same derivations as in the proof of Theorem 2. In particular, we can obtain that there exists positive constants and only depending on , , and such that for any ,

(64) (65) where follows (62) and is the interpolation of strategies computed numerically at stage .

Proof.

Throughout this proof, we will use to denote a positive constant depending only on , , , , , and and use to denote a positive constant depending on all the above constants and the arguments represented by . Both and may vary from line to line.

We next prove the inequality (3). As before, we will focus on proving the case of fictitious play in the sequel, and we claim that the statements also hold for policy update using a similar argument.

Recalling the in (52), we then define the Euler-type scheme for BSDE system (12) as follow:

| (67) |

With Assumptions 1 and 2, classical estimations of the discretization error gives

| (68) |

For the -part error, we decompose it into two terms by the Cauchy-Schwartz inequality:

| (69) |

A similar inequality can be written on the -part error. For both of them, the second term is taken care by applying Theorem 1 to . More precisely, under Assumptions 2–4 and (66), one has:

| (70) |

where is defined in (52). For the first term in (69), we recall the inequality (65) (choosing ) and deduce

| (71) |

where we have used

| (72) |

as a consequence of (66) and (68). Combining (69)–(4.2), we claim that

| (73) |

Using equations (64), (70) and (72), we can similarly obtain that

| (74) |

We next derive an estimate that is useful in controlling the -part error. We first require , then we have

| (75) |

where we have used the Cauchy-Schwart inequality, inequalities (65), (68), (70) and (72).

For the -part error, it suffices to control and we plan to

-

(1)

express in terms of ;

-

(2)

obtain the estimate of by the property (57) of ;

-

(3)

take care the difference between the -part error and II by III which is defined by:

(76)

Step (2) follows from the fact that is defined as the projection of into , and that if viewed as a function on . Step (3) is a consequence of Assumption 4 and (68). So it remains to address step (1).

To this end, we define , then , and , then . Thus, for any , using the AM-GM inequality

| I | ||||

| (77) |

For term , using (4.2) and the Lipschitz condition of in (58), we obtain

| (78) |

where we remove ’s dependence on using and we have also used

| (79) |

Combining the last inequality with (76) yields the estimate for term :

| (80) |

Now plugging the estimates of and into (77) and following step (1)–(3), we obtain:

| (81) | |||

| (82) | |||

| (83) |

where we have used that

| (84) |

Let and be large enough such that

| (85) |

then for we deduce

| (86) |

Combining the above inequality with inequality (73) and (74), we obtain our result. ∎

Here are some remarks regarding Theorem 3 on its implication for numerical algorithms. The primary concern is how we can implement the projection mapping in practice if wished. Note that we choose 1/2-Hölder continuity in time in Assumption 4 for the generality of the result, although numerically it is challenging to guarantee the Hölder continuity. If we replace that with the Lipschitz continuity in time, as a more restrictive condition, and instead consider the projection onto the space with the Lipschitz continuity, the estimates still hold. Accordingly, there are some practical approaches in the literature on ensuring the Lipschitz continuity of deep neural networks that can be introduced in our algorithms. For instance, [23] gives an efficient and accurate estimation of Lipschitz constants for deep Neural networks, and [56] further extends it for robust training with regularization to keep the Lipschitz constant of neural networks small. In practice, Wasserstein GAN [2, 28] has shown remarkable performance when using weight clipping as a loose but efficient way to impose the Lipschitz constraint. Therefore we can leverage similar techniques to keep the Lipschitz regularity during the training of the deep fictitious play. Also, notice that in the above, we define a single projection from the space of all players’ strategies , in consideration of the simplicity of the statement. One can also use the projection of for each player with possibly easier numerical implementation and the same theoretical guarantee.

4.3 On the -Nash Equilibrium

This section combines the previous analysis, identifies the -Nash equilibrium produced by the deep fictitious play, and evaluates its performance on the original game.

Theorem 4.

Under Assumptions 1–4, if is a policy function on and Lipschitz in , and

| (87) |

where is the forward component of (12), then

-

(1)

Given , the game values produced by are near the Nash equilibrium, i.e.,

(88) where with , with defined in (4). Thus, there exists such that and

(89) Here is a constant depending on , , and which may vary from line to line in the proof.

-

(2)

The generated game paths are close to the paths associated with the Nash equilibrium:

(90) where and follow (1) with the true Nash equilibrium strategy and . Here is an arbitrary constant in , and is a constant depending on , , , and .

Immediately, we have the following corollary.

Corollary 1.

Under Assumptions 1–4, assuming the sub-problems (52) are solved accurate enough at all stages, i.e.,

| (91) |

here C is a constant depending only on , , , , , and . Then, for sufficiently large and small mesh size , the strategy defined in (62), as an interpolated policy based on the deep fictitious play, forms an -Nash equilibrium.

Proof.

Remark 6.

As mentioned in Remark 3, there are still some theoretical issues unsolved regarding the approximation error and optimization of the deep BSDE method. The analysis of the deep fictitious play method has similar issues that remain open. To circumvent these issues and have a rigorous statement for -Nash equilibrium, we introduce assumption (91). In practice, an observable proxy of (91) is the training loss of the deep BSDE method evaluated by its Monte Carlo counterpart.

Proof of Theorem 4.

The proof of item (1) relies on the estimates of BSDEs presented previously. Let solve (22) with replaced by . By the nonlinear Feynman-Kac formula (cf. [54, 21, 55]) and the associated HJB equation, we have . Therefore, we have

| (92) |

To bound the above term, we claim a stronger result:

| (93) |

where solves (12), , and , as a consequence of (64), (65) and (87).

If we let solve (24) with replaced by , an argument similar to (92) and (93) can give the second inequality in (88). Then (89) is obtained by observing

| (94) |

and

We now prove item (2). Under the standing assumptions, we first observe that and are Lipschitz in . Thus is well-defined, and the standard estimates in SDE gives (cf. [67, Theorem 3.2.4])

| (95) |

To bound the right-hand side above with the condition (87), let us define a new probability measure , and denote by the Radon-Nikodym derivative:

| (96) |

where . By Assumptions 2, the Novikov’s condition is fulfilled. Thus , and is a standard Brownian motion under . In particular, the process can be rewritten as , and immediately from (87) we have

| (97) |

where we denote by the expectation under measure . We next compute a bound for under , for :

| (98) |

where denote , and we have used the Cauchy-Schwartz inequality and the boundedness of in Assumptions 2. Therefore, we have

where we have consecutively used Hölder’s inequality, the estimate of , the Lipschitz property of , the boundedness of and , and the estimate (97). Here is a constant depending on the , , , and , which may vary from line to line. With (95) and noticing we conclude. ∎

In practice, the game is play on , but not . Therefore, we will define a discrete version of the stochastic differential game (1)–(2) and evaluate the performance of in section 4.2 on the discrete game. To be precise, given a policy function on , we define the discrete state process and discrete individual cost functional as follows

| (99) | ||||

| (100) |

Note that when there are both and in the superscript of , it refers to the (discrete) process of the original state (1), and when there is only in the superscript, it refers to the (discrete) process We then state a discrete version of Theorem 4.

Theorem 5.

Under Assumptions 1–4, if is a policy function on , Lipschitz in and Hölder continuous with t:

| (101) |

and

| (102) |

then

-

(1)

The value of the discrete game produced by is close to the one associated with the Nash equilibrium of the continuous game, i.e.,

(103) where . Moreover, there exists such that and

(104) Here is a constant depending on , , , , , and , which may vary from line to line in the proof.

- (2)

Proof.

Let , then with an argument similar to that in Theorem 3, satisfies:

| (106) |

By (68), (102) and (106), we have

| (107) |

By the regularity of (c.f. (106)) and the standard estimates of the Euler Scheme of SDE (c.f. [44]), we can obtain

| (108) |

Observing that

| (109) |

with (106), (108) and Assumption 2, one has

| (110) |

Finally, with (4.3), (108), (110) and Theorem 4, we reach all the conclusions of this theorem. ∎

5 Numerical Examples

We supplement our theoretical analysis by numerical examples. We shall mainly focus on how deep BSDE performs when combined with policy update strategy in the decoupling step, i.e., when solving (24). We refer readers to [30] for the numerical performance when the deep BSDE method is used to solve the sub-problems derived from fictitious play, whose results are similar to those presented here from policy update. The example we present here is an inter-bank game concerning the systemic risk [16]. Assume an inter-bank market with banks, and denote by the log-monetary reserves of bank at time . Its dynamics are modeled as the following diffusion processes,

| (111) |

Here represents the rate at which bank borrows from or lends to other banks in the lending market, while denotes its control rate of cash flows to a central bank. The standard Brownian motions are independent, in which stands for the idiosyncratic noises and denotes the systemic shock, or so-called common noise in the general context. To describe the model in the form of (1), we concatenate the log-monetary reserves of banks to form . The associated drift term and diffusion term are defined as

| (112) |

| (113) |

and is -dimensional. The cost functional (4) that player wishes to minimize has the form

| (114) |

Under such specifications, the solution of this game admits a quadratic form whose coefficient functions can be solved from a Riccati equation. We direct the interested readers to [CaFovosSu:15, 30] for the detailed interpretation of this model and the explicit characterization of the solution.

In our numerical computation, we choose , , and

| (115) |

We discretize the time into intervals and specify the hypothesis spaces and for each player as follows. We parametrize (the superscript is dropped again for simplicity) with a neural network, denoted by , as the space of . We also parametrize with another network, denoted by , as the space of , in which the timestamp is provided as another dimension of the input. This choice is in consistence with our theoretical analysis in Theorem 3 involving the linear interpolation of the strategy in time.

In this numerical example, we use fully-connected feedforward networks to instantiate both and . Since the problem is homogeneous among all the players, we let two networks share the same parameters among all the players and only solve player 1’s problem for updating the parameters. Both networks consist of three hidden layers with a width of . The activation function is hyperbolic tangent, and the technique of batch normalization [40] is adopted right after each linear transformation and before activation. For simplicity, we do not impose the projection procedure discussed in Section 4.2.

Regarding the optimization, the loss function in Deep BSDE is differentiable with respect to the network parameters. We can use backpropagation to derive the gradient of the loss function with respect to all the parameters in the neural networks and employ stochastic gradient descent (SGD) to optimize all the parameters. In this work, we use Adam optimizer [43] to optimize network parameters with constant learning rate 5e-4 and batch size . The parameters are updated by 30000 steps in total.

To implement the algorithm, we also need to specify the distribution of the initial state in (22) or (24). We follow the same way as in [30]. Each component of , as the initial state of each player, is sampled independently from the uniform distribution on . is chosen such that in the following process driven by the optimal policy

the standard deviation of is approximately . In other words, is determined as a fixed-point. The rationale for such a procedure is to make sure the data generated for the learning is representative enough in the whole state space.

Note that our technical assumptions are not strictly satisfied in this example, since are not Lipschitz continuous, is not uniform bounded, and is not sufficiently small. Nevertheless, our numerical results show that the deep BSDE method can solve this game when combined with policy update. In particular, we compute the relative error of controls (proportional to the gradient of value function):

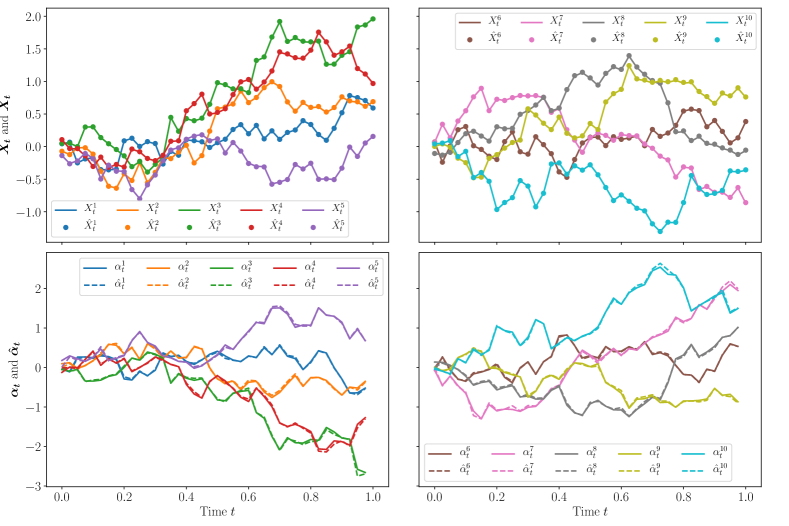

where is the true solution (of player 1), is the prediction from the neural networks, and is the average of evaluated at all the indices . To compute the relative error, we generate ground truth sample paths using Euler scheme based on (24) and the true optimal strategy. Note that the superscript here does not mean the player index, but the path for all players. The final RSE for the Deep BSDE method is 0.27%. Figures 1 presents one sample path for each player of the optimal state process and the optimal control vs. their approximations , with good agreement.

6 Conclusion

In this paper, we established the theoretical foundation for the deep fictitious play algorithm for finding Markovian Nash equilibrium proposed in [30]. Specifically, we proved the following three things: 1. The solutions of the decoupled sub-problems, if solved exactly and repeatedly, converge to the true Nash equilibrium; 2. The numerical error of each sub-problem, if solved by deep BSDE individually and repeatedly, converges to zero subject to the universal approximation capacity of neural networks; 3. The interpolated strategy based on the deep fictitious play algorithm forms a -Nash equilibrium, after sufficiently many stages and with sufficiently small mesh . We also generalize the algorithm by proposing a new approach to decouple the games, and present a numerical example in the end to show the empirical convergence beyond the technical assumptions used in the theorems. In the future, with this solidly established theory of deep fictitious play, we aim to study the competitions in Finance, including P2P lending platforms from the Fintech industry and insurance markets. We also plan to generalize the theory and algorithm to stochastic differential games with delays.

Data availability statement

Data sharing not applicable to this article as no new data were created or analysed during the this study.

References

- [1] A. Angiuli, J.-P. Fouque, and M. Laurière. Unified reinforcement Q-learning for mean field game and control problems. arXiv preprint arXiv:2006.13912, 2020.

- [2] M. Arjovsky, S. Chintala, and L. Bottou. Wasserstein generative adversarial networks. In Proceedings of the 34th International Conference on Machine Learning, volume 70 of Proceedings of Machine Learning Research, pages 214–223, 2017.

- [3] E. Bayraktar, A. Budhiraja, and A. Cohen. A numerical scheme for a mean field game in some queueing systems based on markov chain approximation method. SIAM Journal on Control and Optimization, 56(6):4017–4044, 2018.

- [4] C. Beck, S. Becker, P. Cheridito, A. Jentzen, and A. Neufeld. Deep splitting method for parabolic PDEs. arXiv preprint arXiv:1907.03452, 2019.

- [5] C. Beck, W. E, and A. Jentzen. Machine learning approximation algorithms for high-dimensional fully nonlinear partial differential equations and second-order backward stochastic differential equations. Journal of Nonlinear Science, 29(4):1563–1619, 2019.

- [6] A. Bensoussan, C. C. Siu, S. C. P. Yam, and H. Yang. A class of non-zero-sum stochastic differential investment and reinsurance games. Automatica, 50(8):2025–2037, 2014.

- [7] U. Berger. Fictitious play in 2n games. Journal of Economic Theory, 120(2):139–154, 2005.

- [8] H. Brezis. Functional analysis, Sobolev spaces and partial differential equations. Springer Science & Business Media, 2010.

- [9] A. Briani and P. Cardaliaguet. Stable solutions in potential mean field game systems. Nonlinear Differential Equations and Applications, 25(1):1, 2018.

- [10] G. W. Brown. Some notes on computation of games solutions. Technical report, Rand Corp Santa Monica CA, 1949.

- [11] G. W. Brown. Iterative solution of games by fictitious play. Activity Analysis of Production and Allocation, 13(1):374–376, 1951.

- [12] P. Cardaliaguet and S. Hadikhanloo. Learning in mean field games: the fictitious play. ESAIM: Control, Optimisation and Calculus of Variations, 23(2):569–591, 2017.

- [13] P. Cardaliaguet and C.-A. Lehalle. Mean field game of controls and an application to trade crowding. Mathematics and Financial Economics, 12(3):335–363, 2018.

- [14] R. Carmona and F. Delarue. Probabilistic Theory of Mean Field Games with Applications I. Springer, 2017.

- [15] R. Carmona and F. Delarue. Probabilistic Theory of Mean Field Games with Applications II. Springer, 2017.

- [16] R. Carmona, J.-P. Fouque, and L.-H. Sun. Mean field games and systemic risk. Communications in Mathematical Sciences, 13(4):911–933, 2015.

- [17] P. Casgrain, B. Ning, and S. Jaimungal. Deep Q-learning for Nash equilibria: Nash-DQN. arXiv preprint arXiv:1904.10554, 2019.

- [18] S. Chen, H. Yang, and Y. Zeng. Stochastic differential games between two insurers with generalized mean-variance premium principle. Astin Bulletin: The Journal of the IAA, 48(1):413–434, 2018.

- [19] E. J. Dockner, S. Jorgensen, N. Van Long, and G. Sorger. Differential Games in Economics and Management Science. Cambridge University Press, 2000.

- [20] W. E, J. Han, and A. Jentzen. Deep learning-based numerical methods for high-dimensional parabolic partial differential equations and backward stochastic differential equations. Communications in Mathematics and Statistics, 5(4):349–380, 2017.

- [21] N. El Karoui, S. Peng, and M. C. Quenez. Backward stochastic differential equations in finance. Mathematical Finance, 7(1):1–71, 1997.

- [22] R. Elie, J. Pérolat, M. Laurière, M. Geist, and O. Pietquin. On the convergence of model free learning in mean field games. arXiv preprint arXiv:1907.02633, 2019.

- [23] M. Fazlyab, A. Robey, H. Hassani, M. Morari, and G. Pappas. Efficient and accurate estimation of Lipschitz constants for deep neural networks. In Advances in Neural Information Processing Systems, pages 11427–11438, 2019.

- [24] M. Germain, H. Pham, and X. Warin. Deep backward multistep schemes for nonlinear PDEs and approximation error analysis. arXiv preprint arXiv:2006.01496, 2020.

- [25] D. A. Gomes, S. Patrizi, and V. Voskanyan. On the existence of classical solutions for stationary extended mean field games. Nonlinear Analysis: Theory, Methods & Applications, 99:49–79, 2014.

- [26] D. A. Gomes and V. K. Voskanyan. Extended deterministic mean-field games. SIAM Journal on Control and Optimization, 54(2):1030–1055, 2016.

- [27] A. Gosavi. A reinforcement learning algorithm based on policy iteration for average reward: Empirical results with yield management and convergence analysis. Machine Learning, 55(1):5–29, 2004.

- [28] I. Gulrajani, F. Ahmed, M. Arjovsky, V. Dumoulin, and A. C. Courville. Improved training of wasserstein gans. In Advances in neural information processing systems, pages 5767–5777, 2017.

- [29] J. Han and W. E. Deep learning approximation for stochastic control problems. arXiv preprint arXiv:1611.07422, 2016.

- [30] J. Han and R. Hu. Deep fictitious play for finding Markovian Nash equilibrium in multi-agent games. In Proceedings of The First Mathematical and Scientific Machine Learning Conference (MSML), volume 107, pages 221–245, 2020.

- [31] J. Han, A. Jentzen, and W. E. Solving high-dimensional partial differential equations using deep learning. Proceedings of the National Academy of Sciences, 115(34):8505–8510, 2018.

- [32] J. Han and J. Long. Convergence of the deep BSDE method for coupled FBSDEs. Probability, Uncertainty and Quantitative Risk, 5(1):1–33, 2020.

- [33] J. Han, J. Lu, and M. Zhou. Solving high-dimensional eigenvalue problems using deep neural networks: A diffusion Monte Carlo like approach. Journal of Computational Physics, 2020.

- [34] J. Han, L. Zhang, and W. E. Solving many-electron Schrödinger equation using deep neural networks. Journal of Computational Physics, page 108929, 2019.

- [35] J. Hofbauer and W. H. Sandholm. On the global convergence of stochastic fictitious play. Econometrica, 70(6):2265–2294, 2002.

- [36] R. A. Howard. Dynamic programming and markov processes. John Wiley, 1960.

- [37] R. Hu. Deep fictitious play for stochastic differential games. arXiv preprint arXiv:1903.09376, 2019.

- [38] R. Hu. Deep learning for ranking response surfaces with applications to optimal stopping problems. Quantitative Finance, 2020. to appear.

- [39] C. Huré, H. Pham, and X. Warin. Deep backward schemes for high-dimensional nonlinear PDEs. Mathematics of Computation, 89(324):1547–1579, 2020.

- [40] S. Ioffe and C. Szegedy. Batch normalization: Accelerating deep network training by reducing internal covariate shift. In International Conference on Machine Learning, pages 448–456, 2015.

- [41] R. Isaacs. Differential games: a mathematical theory with applications to warfare and pursuit, control and optimization. Courier Corporation, 1999.

- [42] S. Ji, S. Peng, Y. Peng, and X. Zhang. Three algorithms for solving high-dimensional fully-coupled FBSDEs through deep learning. IEEE Intelligent Systems, 2020.

- [43] D. Kingma and J. Ba. Adam: a method for stochastic optimization. In Proceedings of the International Conference on Learning Representations, 2015.

- [44] P. E. Kloeden and E. Platen. Numerical solution of stochastic differential equations, volume 23. Springer Science & Business Media, 2013.

- [45] V. Krishna and T. Sjöström. On the convergence of fictitious play. Mathematics of Operations Research, 23(2):479–511, 1998.

- [46] H. Liu, H. Qiao, S. Wang, and Y. Li. Platform competition in peer-to-peer lending considering risk control ability. European Journal of Operational Research, 274(1):280–290, 2019.

- [47] N. V. Long. Dynamic games in the economics of natural resources: a survey. Dynamic Games and Applications, 1(1):115–148, 2011.

- [48] J. Ma and J. Zhang. Representation theorems for backward stochastic differential equations. The annals of applied probability, 12(4):1390–1418, 2002.

- [49] E. J. McShane. Extension of range of functions. Bulletin of the American Mathematical Society, 40(12):837–842, 1934.

- [50] P. Milgrom and J. Roberts. Adaptive and sophisticated learning in normal form games. Games and Economic Behavior, 3(1):82–100, 1991.

- [51] D. Monderer and L. S. Shapley. Fictitious play property for games with identical interests. Journal of Economic Theory, 68(1):258–265, 1996.

- [52] T. Nakamura-Zimmerer, Q. Gong, and W. Kang. Adaptive deep learning for high dimensional Hamilton-Jacobi-Bellman equations. arXiv preprint arXiv:1907.05317, 2019.

- [53] E. Pardoux and S. Peng. Adapted solution of a backward stochastic differential equation. Systems & Control Letters, 14(1):55–61, 1990.

- [54] E. Pardoux and S. Peng. Backward stochastic differential equations and quasilinear parabolic partial differential equations. In Stochastic Partial Differential Equations and Their Applications, pages 200–217. Springer, 1992.

- [55] E. Pardoux and S. Tang. Forward-backward stochastic differential equations and quasilinear parabolic PDEs. Probability Theory and Related Fields, 114(2):123–150, 1999.

- [56] P. Pauli, A. Koch, J. Berberich, and F. Allgöwer. Training robust neural networks using Lipschitz bounds. arXiv preprint arXiv:2005.02929, 2020.

- [57] D. Pfau, J. S. Spencer, A. G. D. G. Matthews, and W. M. C. Foulkes. Ab-initio solution of the many-electron Schrödinger equation with deep neural networks. arXiv preprint arXiv:1909.02487, 2019.

- [58] H. Pham, X. Warin, and M. Germain. Neural networks-based backward scheme for fully nonlinear PDEs. arXiv preprint arXiv:1908.00412, 2019.

- [59] W. B. Powell and J. Ma. A review of stochastic algorithms with continuous value function approximation and some new approximate policy iteration algorithms for multidimensional continuous applications. Journal of Control Theory and Applications, 9(3):336–352, 2011.

- [60] A. Prasad and S. P. Sethi. Competitive advertising under uncertainty: A stochastic differential game approach. Journal of Optimization Theory and Applications, 123(1):163–185, 2004.

- [61] M. L. Puterman. Markov Decision Processes: Discrete Stochastic Dynamic Programming. John Wiley & Sons, 1994.

- [62] J. Sirignano and K. Spiliopoulos. DGM: A deep learning algorithm for solving partial differential equations. Journal of computational physics, 375:1339–1364, 2018.

- [63] Z. Wei and M. Lin. Market mechanisms in online peer-to-peer lending. Management Science, 63(12):4236–4257, 2017.

- [64] B. Yu, X. Xing, and A. Sudjianto. Deep-learning based numerical BSDE method for barrier options. arXiv preprint arXiv:1904.05921, 2019.

- [65] X. Zeng. A stochastic differential reinsurance game. Journal of Applied Probability, 47(2):335–349, 2010.

- [66] J. Zhang. Backward stochastic differential equations. In Backward Stochastic Differential Equations, pages 79–99. Springer, 2017.

- [67] J. Zhang. Backward Stochastic Differential Equations: From Linear to Fully Nonlinear Theory. Springer, 2017.

Appendix A Supporting Propositions for Assumption 3

We prove the following propositions in this section.

Proposition 6.

Proposition 7.

First, we need the following classical estimation (cf. [66, Theorem 5.2.2]), which give a uniform bound of the -component of BSDEs. We state and provide the proof of this lemma here to compute an exact upper bound for the convenience of later analysis.

Lemma 1.

Let , the adapted process taking value in , be the solution of the following BSDE system:

| (117) |

where the coefficients , and satisfy the following condition:

Then:

| (118) |

where is the Lebesgue measure on .

Proof.

Denote by the solution of the following BSDE:

| (119) |

for any . Then, for any and , let be the short notation444The notation here is slightly inconsistent with the statement in Section 2: A boldface character with a superscript denotes a solution with the initial condition . for , . The wellposedness of BSDEs (117) and (119) is classical in literature; see, e.g., [53].

We define , , , and as follows:

Then, we have

| (120) | ||||

| (121) |

and Itô’s lemma gives

| (122) | ||||

| (123) |

Taking the expectation on both sides yields

| (124) |

and by Grönwall’s inequality, we have . Similarly, we deduce that

| (125) |

and by Grönwall’s inequality, we have

| (126) |

Following the argument in [48, Theorem 3.1], we define and deduce from (126). Therefore, we claim

Also noticing that -a.s. (cf. [48, Theorem 3.1]),

and the law of is absolute continuous with respect to the Lebesgue measure on , we can get

Finally, since is measurable with respect to , where denotes the collection of Lebesgue measurable sets on , we obtain our conclusion. ∎

Using the above lemma, we can prove that the solution to the BSDE system (12) has a bounded -component, for sufficiently small . Note that the standard estimate can not be applied directly here, as the driver defined in (12) is not global Lipschitz in .

Proof of Proposition 6.

We first prove the existence. Fix , we use to denote the projection from to , and use for its column. Let with , then its Lipschitz constants with respect to and are computed by

| (127) |

Now define and consider the solution to the following BSDE system

| (128) |

Following Lemma 1, Assumption 2 and inequality (A) with , and , we have:

| (129) | ||||

| (130) |

Therefore, if , is the desired solution to the BSDE system (12) with , which can be fulfilled if is small enough. ∎

Proof of Proposition 7.

Let be another adapted solution of the BSDE system (12) such that

| (131) |

Define , and and we can write

| (132) |

Itô’s lemma gives

| (133) |

Taking expectation on both side and using , we deduce that

| (134) |

for any . By

| (135) |

we have with . Taking in (134), we deduce that and therefore by Grönwall’s inequality. We then have from the first equality in (134), which implies . ∎