Estimating the logarithm of characteristic function and stability parameter for symmetric stable laws

Abstract

Let be an i.i.d. sample from symmetric stable distribution with stability parameter and scale parameter . Let be the empirical characteristic function. We prove an uniform large deviation inequality: given preciseness and probability , there exists universal (depending on and but not depending on and ) constant so that

where and . As an applications of the result, we show how it can be used in estimation unknown stability parameter .

Keywords: Stable laws, large deviation inequalities, parameter estimation;

MSC codes: Stable laws 60E07; Confidence regions 62F25

1 Introduction and preliminaries

Let be an i.i.d. sample from stable law with characteristic function , where for and for , and , , , are (unknown) stability, skewness, scale and shift parameters, respectively. Basic properties of stable distributions can be found in [15, 13, 9]. Let be the empirical distribution function, and the empirical characteristic function, i.e.

| (1.1) |

Let and . Estimating the parameters of stable law is a notoriously hard problem (see, e.g., [8, Section 2], [15, Chapter 4]). Simple empirical characteristic function based closed form estimates were proposed in [11]. In particular, the stability parameter estimator is

| (1.2) |

where are fixed arguments and . Since for any , , a.s., we see that any choice of gives consistent estimator. The same points can be used to give consistent closed form estimators also to other parameters , , of stable law (see [5, Theorem 1]). Despite the asymptotic consistency holds for any pair , in practice the right choice of and is crucial and the universal selection of these values has remained unsolved (e.g., [10, 1, 3]). Recently, [6] suggests that the choice of and should be fixed based on the preciseness of , that is, on the preciseness of . Clearly, the preciseness of depends on how well and estimates for .

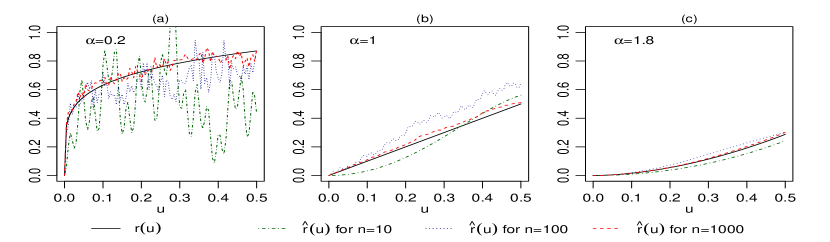

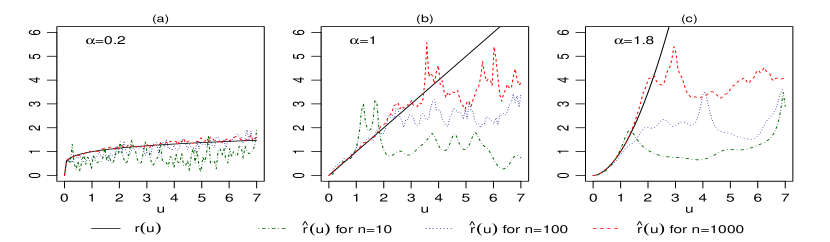

Figure 1 and Figure 2 show that is relatively accurate estimate of only in a small interval , where obviously depends on sample size , but unfortunately also on – the smaller , the smaller also . So, there seems not to exist an universal (that applies for any ) upper bound so that were small for any even when is known. It is clearly evident from Figure 1 and Figure 2, that too big makes the estimate of very imprecise. Observe that cannot also be very small, because then is also very small and that affects the preciseness of even when , . On the other hand, Figure 1 and Figure 2 as well as simulations in [6] suggest that despite the possible non-existence of universal , there might exists an universal (not depending on and ) so that is relatively small.

Our main theoretical result states that for symmetric 111For mathematical tractability in formulas, in particular in tail estimation in (1.7) and (2.3), we provide our results for symmetric stable laws. Similar construction of proof can be applied for general stable laws. stable laws such universal exists.

Theorem 1.1.

Let be an i.i.d. sample from symmetric stable law. Fix , . Then there exists such that for every and

| (1.3) |

where is independent of and .

Theorem is proved in Subsection 2. From Theorem 1.1 it follows that with probability , , given is big enough and is cosen such that , . Therefore, in order to apply (1.2), it makes sense not to fix arguments and , but the values and instead. The obtained estimate is then

| (1.4) |

where, , and are carefully chosen constants and

| (1.5) |

The estimates of parameters at and based on and were proposed and studied in [6]. The current article thus provides theoretical justification to the such method of argument selection.

Note that estimating the parameters via two points and as in (1.2) deserves more attention in the recent literature and specifying and via function as in (1.5) is not the only option. In [1], and is taken such that the distance between Cauchy () and Gaussian () characteristic functions at were maximal. The idea of maximizing the distance between characteristic functions is further developed in [3], where an iterative 8-step algorithm for specifying and is proposed. Although the idea of maximizing discrepancy between characteristic functions (or rather between -functions) is quite natural, and the simulations in [3] show good behaviour of that choice in practice, the proposed algorithm in [3] is still ad hoc in nature and lacks theoretical justification. In particular, it is not clear that it allows to choose and so that the inequality (1.6) below holds.

The proof of the Theorem 1.1 is constructive, but the goal of it is to show that universal exists, not to optimize the constant, i.e. to find the biggest possible and smallest possible . It means that the constructed in the proof is probably too small for practical use. Although, for every , and , , a.s. as grows, our upper bound satisfies , where is a constant depending on . Thus is always bounded away from 1 and does not increase to the infinity as grows. This need not necessarily be the deficiency of the proof, rather than necessary property. To see that, assume the inequality (1.3) holds with some . Then it follows that

where , so that the universal upper bound (that applies for any )

would exists. However, there is no evidence at all that such an

exists, suggesting that the a.s. convergence is not uniform over small – for every and

there exists small enough so that the difference

is still big. If so, then must

always remain smaller than 1.

The situation is different, when we bound the unknown stability

parameters below from zero, i.e. we assume the existence of

(which can be arbitrary small) such that the unknown parameter belongs to .

In this case the upper bound satisfies (Corollary 2.1), and in this case also

the upper bound exists. The existence of is common

assumption in practice (e.g., [7, 4, 8] suggest ) and we keep this additional

assumption in Theorem 2.1, that provides a uniform bound

similar to (1.3) to the difference of logarithms . Theorem 2.1 is actually a simple

corollary of Theorem 1.1, but the additional assumption about

the existence of is necessary, because if is very small,

then can be rather big even when is very

close to .

Section 3 is devoted to the applications of Theorem

2.1 in the light of large deviation inequalities for

. We show how the upper bound from

Theorem 2.1 can be used to solve the two basic questions

related with estimate in (1.4):

-

•

Given precision , probability and lower bound , find (needed to construct in (1.4)) and possibly small sample size so that

(1.6) -

•

Given sample size and , find and possibly small so that (1.6) holds. In other words, find exact i.e. non-asymptotic confidence interval to .

The solutions of these questions are formulated as Theorem

3.1 and Theorem 3.2.

The bound in Theorem 2.1 is constructed using the basic bound

provided by Theorem 1.1. Thus the

and required sample size in the inequality (1.6) depend

heavily on the function . Unfortunately, the function constructed in Section 2 is not explicitly given and, hence, difficult to work with. Although the main goal of the

present paper is just to show that the function exists, in Section 4, we discuss another possibility to

construct . The new construction gives analytically more tractable bound, the price for it is bigger minimal required

sample size and lower bound. Also the upper bound constructed in Section 4 is also strictly smaller than 1 for every . So we have two different constructions

with the same property, and this allows us to conjecture that even the best bound is always smaller than 1 and we also conjecture that the universal upper bound does not exist.

Preliminaries.

For every stable distribution has tail(s) that are asymptomatically power laws with heavy tails (e.g., [9, Theorem 1.12], [13, Property 1.2.15],

where , , and For symmetric stable laws () these results imply the existence of constants222For general stable laws it implies for the exitsence of constants and with and . so that

| (1.7) |

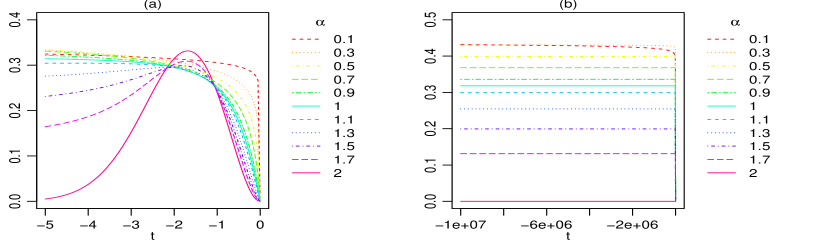

Figure 3 plots the function for different -values and in the range and . Increasing the interval shows similar pattern, hence it is clear that there exists so that . Throughout the paper, we keep undetermined, although one can take it as . It is also obvious that is independent of .

In what follows, we shall use the following elementary inequalities: for any ,

we obtain that implies . Thus, for any and

| (1.8) |

Observe that (1.8) holds for any estimate .

2 Main results

2.1 Proof of Theorem 1.1

Bounding the difference of characteristic functions.

Recall is the standard empirical estimate given by (1.1). To bound we use the approach in [2] as follows. For every ,

Since for every and , the first term can be bounded

where . The last inequality holds, because . Similarly, the third term can be estimated above by . To estimate the second term, we use the integration by parts

Therefore, for any

| (2.1) |

For any , let be so big that . Then also and (2.1) implies

| (2.2) |

By (1.7), we can take

| (2.3) |

and so with , by (2.2) and (2.3)

| (2.4) |

Bounding .

Recall . Fix and define . We now use Dworetzky-Kiefer-Wolfowitz inequality [14, p. 268]):

to estimate

Define

From (1.8), we obtain

which is equivalent to , and so the desired upper bound for any , denoted by is the solution of the following equality

| (2.5) |

Observe that

Hence the following condition gives a lower bound for minimal sample size so that :

| (2.6) |

The existence of .

The following lemma shows that , hence the universal (not depending on and ) bound exists. Since , without loss of generality, in the lemma we consider . The lemma finishes the proof of Theorem 1.1.

Lemma 2.1.

Fix and such that . Let be the solution of the equality . Then is continuous strictly positive function on and . In particular, .

Proof.

For every and , define function

Let us fix and denote . Let

Since is continuous and strictly decreasing function, the maximizer exists and is unique. It is not difficult to see that must satisfy the following equalities:

The inequality in the left implies that

| (2.7) |

The equality in the right implies and is equivalent to . Hence we obtain

| (2.8) |

Define function

| (2.9) |

Thus is the solution of the equality .

Suppose now . Let and be as with and instead of , respectively

and let and be the solutions of the equalities and . Clearly, for any , it holds . However, since , by (2.8) we see that there exists so that eventually since obviously

, we obtain that and by (2.7), thus . Now observe that for any and ,

and . Moreover is strictly decreasing function. For such functions, pointwise convergence implies uniform convergence, so that as grows

| (2.10) |

The uniform convergence implies that the solutions of the equalities converge as well, i.e. , provided so that the solutions exists.

We have proven that the function is continuous on the set . Let us now consider the case . From the equalities , it follows that

where . Therefore, for every fixed ,

with

where stands for Lambert -function. Observe that is strictly decreasing function with limits and . Hence (2.10) holds with . This, in turn, implies that , where is the solution of the equality . Since , and by assumption , we see that . Hence is continuous strictly positive function on , thus . ∎

2.2 Bounding

We are now interested in finding the probabilistic bounds on difference , where, as previously, is iid sample from symmetric stable law, and . For that an additional assumption has to be made. In the present subsection, we assume that there exists a known lower bound such that the parameter space is instead of . The crucial benefit of knowing the lower bound of is the fact that the bound from Theorem 1.1 increases to infinity as grows. Recall that the bound in lacks this property: although increases with , it always satisfies and, as argued in Introduction, such a property might be unavoidable. Bounding the parameter space away from zero, we have a new bound that tends to infinity as increases. Let us formulate it as a corollary.

Corollary 2.1.

Assume to be given. Fix , and let be as in Theorem 1.1. Then for every there exists independent of and such that and

for every and .

Proof.

Fix and take so big that . Then for every and for every , the function

is increasing in . Therefore

| (2.11) |

Now observe that when , then for every , it holds , thus . Since , it follows that . Therefore, there exists so big that . From (2.11), it follows that when , it holds , . Hence The inequality in the statement now follows from Theorem 1.1. ∎

Theorem 2.1.

3 Applications of Theorem 2.1

Recall the estimate in (1.4). The construction of requires fixing the constants and . The following simple lemma shows how Theorem 2.1 can be used to prove a large deviation inequality for .

Lemma 3.1.

Proof.

Since is continuous, we have by (1.4) that and . Let

| (3.3) |

On the event , it holds for and so and . Therefore, on the set , for any the following implications hold

We have thus shown that

Exact confidence intervals.

In what follows, we shall briefly discuss how to choose such that (3.2) holds. In particular, we shall address the following classical problems of parameter estimation:

- Q1:

- Q2:

To solve Q1, define for any , and

| (3.4) |

where is as in Corollary 2.1. The function depends also on and , but these parameters are fixed and left out from notation. Define

where is as in Theorem 1.1. Now take minimal such that . Observe that is increasing, so that when , then for any . The estimation procedure is now the following.

EstimationProcedure1:

Theorem 3.1.

Let , and be given. Let be the sample size satisfying . Then the estimate obtained via EstimationProcedure1 satisfies the inequality (3.2), provided the true parameter satisfies the inequality .

Proof.

According to definition of , the parameters and as specified by EstimationProcedure1 are such that and . With , we see that

so that the equation (3.1) holds. This equation also implies that . Since , we have . Thus both inequalities in (2.12) hold and therefore , where is as in Theorem 2.1. Hence all assumptions of Theorem 2.1 are fulfilled and so (2.13) holds. Both assumptions of Lemma 3.1 are fulfilled and so the inequality (3.2) holds as well.∎

To solve Q2, we need to assume some minimal requirements about the given sample size . In what follows, we assume that there exists such that , where is as in Theorem 1.1. Now we define

The function also depends on and , but these are fixed. As previously, define

Now find (as small as possible) such that .

EstimationProcedure2:

Theorem 3.2.

Let , the sample size , where and be given. Let satisfy . Then the estimate obtained via EstimationProcedure2 satisfies the inequality (3.2), provided the true parameter satisfies the inequality .

Proof.

According to definition of , the parameters and as specified by EstimationProcedure2 are such that . Since is decreasing, it holds that . With , we see that equation (3.1) holds. This equation also implies that and hence both inequalities in (2.12) hold and therefore , where is as in Theorem 2.1. Hence all assumptions of Theorem 2.1 are fulfilled and so (2.13) holds. Then Lemma 3.1 implies that (3.2) holds as well.∎

4 An alternative construction

Recall the construction of the in the proof of Theorem 1.1: the key of the construction is the large deviation inequality

| (4.1) |

where and . Then was defined as the solution of the equality

| (4.2) |

and so the the desired bound was obtained. In order (4.2) to have positive solution, the sample size must satisfy .

The large deviation bound (4.2) constructed in Section 2.1 is not the one possible option. We now sketch another possible construction yielding to a different inequality, and therefore, also to the different function and different bound .

Unlike the obtained in Section 2.1, the new has more explicit form. The price for it is much bigger required sample sice .

Observe that by (2.2) and (2.3) the inequality

implies that

Hence for every ,

Recall and . Hence, we obtain

| (4.3) |

Choose

Thus plugging into (4.3), we obtain with ,

where

The inequality (4.2) holds with an equality, when

and , are solutions of the following equalities:

| (4.4) | ||||

| (4.5) |

Thus

and holds when

| (4.6) |

From (4.6), we obtain necessary sample size

| (4.7) |

The solution of equality (4.5) is

where is Lambert’s W-function and is defined as follows

Observe that and It can be shown that

| (4.8) |

where while only if and , where is given by (4.7), and is the solution of the equality

Since , it holds that for any , and so the alternative construction satisfies our conjecture. However, it is possible to show the for any ,

So we have another construction that confirms our conjecture that the universal bound satisfies the inequality and the universal bound does not exists.

5 Comparison of and

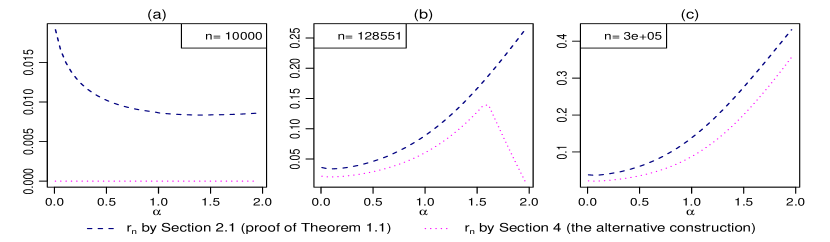

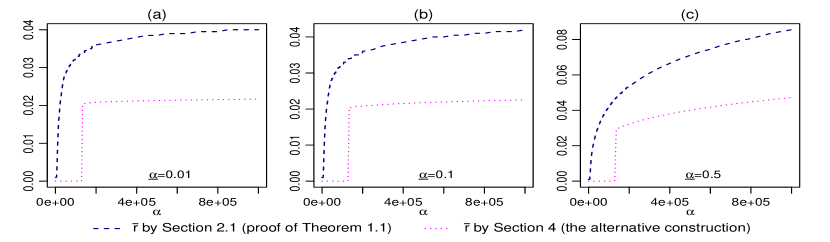

Fix , and . We find the values of obtained in Section 2.1 as follows: first we numerically find as the solution of the equality , where is given by (2.9), then we calculate given by (2.7) and then can be found as solution of (2.5). We compare the obtained values of with the ones obtained in Section 4: , where is the solution of equality (4.4) and is the solution of equality (4.5). Note that by (4.7) we have only if . Figure 4 plots both constructions of versus for different sample sizes .

Obviously, in Figure 4 (a) the obtained by the alternative construction in Section 4 is because . However, the values of obtained by Section 2.1 are small but positive.

In Figure 4 (b) both constructions give positive results (because ) while alternative construction gives smaller (more conservative) values, with drop after (and minimum over is at ). In Figure 4 (c) the large sample size such as is used and both behave in concordance while the alternative construction yields smaller values for all values of . Next we compare the values of obtained by Section 2.1 and Section 4. Figure 5 plots versus for different lower limits . It is clearly evident from Figure 5 that is increasing in (while alternative construction requires ). Setting lower limit from to increases the values of approximately twice. All in all, in our example the construction given by Section 2.1 yields much bigger (less conservative) values of than the more explicit form construction given by Section 4.

References

- Bibalan et al. [2017] Bibalan, M. H., H. Amindavar, and M. Amirmazlaghani (2017). Characteristic function based parameter estimation of skewed alpha-stable distribution: An analytical approach. Signal Process. 130, 323–336.

- Csörgo [1981] Csörgo, S. (1981). Limit behaviour of the empirical characteristic function. The Annals of Probability 9(1), 130–144.

- Kakinaka and Umeno [2020] Kakinaka, S. and K. Umeno (2020). Flexible two-point selection approach for characteristic function-based parameter estimation of stable laws. Online at https://arxiv.org/abs/2005.11499.

- Kogon and Williams [1998] Kogon, S. M. and D. B. Williams (1998). Characteristic function based estimation of stable distribution parameters. In R. J. Adler, R. E. Feldman, and M. S. Taqqu (Eds.), A Practical Guide to Heavy Tails, pp. 311–335. Boston: Birkhäuser.

- Krutto [2016] Krutto, A. (2016). Parameter estimation in stable law. Risks 4(4), 43.

- Krutto [2018] Krutto, A. (2018). Empirical cumulant function based parameter estimation in stable laws. Acta et Commentationes Universitatis Tartuensis de Mathematica 22(2), 311–338.

- McCulloch [1996] McCulloch, J. H. (1996). Financial applications of stable distributions. In G. Maddala and C. Rao (Eds.), Statistical Methods in Finance, Volume 14 of Handbook of Statistics, pp. 393 – 425. Elsevier.

- Nolan [2001] Nolan, J. P. (2001). Maximum likelihood estimation and diagnostics for stable distributions. In O. Barndorff-Nielsen, S. Resnick, and T. Mikosch (Eds.), Lévy Processes, pp. 379–400. Boston: Birkhäuser.

- Nolan [2018] Nolan, J. P. (2018). Stable Distributions - Models for Heavy Tailed Data. Boston: Birkhäuser. In progress, Chapter 1 online at http://fs2.american.edu/jpnolan/www/stable/stable.html.

- Paulson et al. [1975] Paulson, A. S., E. W. Holcomb, and R. A. Leitch (1975). The estimation of the parameters of the stable laws. Biometrika 62(1), 163–170.

- Press [1972] Press, J. S. (1972). Estimation in univariate and multivariate stable distributions. J. Amer. Statist. Assoc. 67(340), 842–846.

- Robust Analysis Inc. [2017] Robust Analysis Inc. (2017). STABLE 5.3 R Version for Windows. Washington, DC, USA: Robust Analysis Inc. http://www.robustanalysis.com/.

- Samorodnitsky and Taqqu [1994] Samorodnitsky, G. and M. S. Taqqu (1994). Stable Non-Gaussian Random Processes: Stochastic Models with Infinite Variance. New York: Chapman & Hall.

- van der Vaart [1998] van der Vaart, A. (1998). Asymptotic Statistics. Cambridge: Cambridge University Press.

- Zolotarev [1986] Zolotarev, V. (1986). One-dimensional Stable Distributions, Volume 65 of Translations of mathematical monographs. American Mathematical Society.