Rank-based Estimation under Asymptotic Dependence and Independence, with Applications to Spatial Extremes

Abstract

Multivariate extreme value theory is concerned with modeling the joint tail behavior of several random variables. Existing work mostly focuses on asymptotic dependence, where the probability of observing a large value in one of the variables is of the same order as observing a large value in all variables simultaneously. However, there is growing evidence that asymptotic independence is equally important in real world applications. Available statistical methodology in the latter setting is scarce and not well understood theoretically. We revisit non-parametric estimation and introduce rank-based M-estimators for parametric models that simultaneously work under asymptotic dependence and asymptotic independence, without requiring prior knowledge on which of the two regimes applies. Asymptotic normality of the proposed estimators is established under weak regularity conditions. We further show how bivariate estimators can be leveraged to obtain parametric estimators in spatial tail models, and again provide a thorough theoretical justification for our approach.

keywords:

[class=MSC2020]keywords:

, and

1 Introduction

Assessing the frequency of extreme events is crucial in many different fields such as environmental sciences, finance and insurance. The most severe risks are often associated to a combination of extreme values of several different variables or the joint occurrence of an extreme phenomenon across different spatial locations. Statistical methods for accurate modeling of such multivariate or spatial dependencies between rare events is provided by extreme value theory. Applications include the analysis of extreme flooding (Keef, Tawn and Svensson, 2009; Asadi, Davison and Engelke, 2015; Engelke and Hitz, 2020), risk diversification between stock returns (Poon, Rockinger and Tawn, 2004; Zhou, 2010) and climate extremes (Westra and Sisson, 2011; Zscheischler and Seneviratne, 2017).

Extremal dependence between largest observations of two random variables and with distribution functions and , respectively, can take many different forms. A classical assumption to measure and model this dependence is multivariate regular variation (cf., Resnick, 1987), which is equivalent to the existence of the stable tail dependence function

| (1.1) |

see Huang (1992) and de Haan and Ferreira (2006). This condition allows a first broad classification regarding extremal dependence of bivariate random vectors into two different regimes. If , and are said to be asymptotically independent; in this case the joint exceedance probability is negligible compared to the marginal exceedance probabilities. Otherwise, a stronger form of extremal dependence, called asymptotic dependence, holds and the joint exceedance probability is of the same order as the probability of one of the components exceeding a high threshold.

Most of the existing probabilistic and statistical theory deals with asymptotic dependence. A variety of methods exists, including non-parametric estimation (Huang, 1992; Einmahl and Segers, 2009; Guillotte, Perron and Segers, 2011), bootstrap procedures (Peng and Qi, 2008; Bücher and Dette, 2013), parametric approaches including likelihood estimation (Ledford and Tawn, 1996; de Haan, Neves and Peng, 2008; Padoan, Ribatet and Sisson, 2010; Dombry, Engelke and Oesting, 2017) and M-estimation (Einmahl, Krajina and Segers, 2008; Engelke et al., 2015). See also Einmahl, Krajina and Segers (2012, 2016) for inference in the -dimensional and spatial setting. There is a rich literature on multivariate tail models (see for instance Gumbel, 1960; Tawn, 1988; Hüsler and Reiss, 1989, among many others) and generalizations to spatial domains (Brown and Resnick, 1977; Smith, 1990; Schlather, 2002).

Recent studies have shown that in many applications such as spatial precipitation (Le et al., 2018) and significant wave height (Wadsworth and Tawn, 2012), dependence tends to become weaker for the largest observations and asymptotic independence is therefore the more appropriate regime. In this case, the stable tail dependence function in (1.1) does not contain information on the degree of asymptotic independence and is therefore not suitable for statistical modeling. A remedy to this problem was proposed by Ledford and Tawn (1996, 1997) who introduced a more flexible condition on the joint exceedance probabilities. Their setting implies the existence of

| (1.2) |

where is a suitable measurable function that makes the limit nontrivial. Necessarily, is regularly varying at zero with index . The residual tail dependence coefficient describes the strength of residual dependence in the tail and implies asymptotic independence. One speaks about positive and negative association between extremes if and , respectively. Early works focus on estimating the degree of asymptotic independence and various estimators have been proposed and studied (Ledford and Tawn, 1997; Peng, 1999; Draisma et al., 2004). A more complete description of the residual extremal dependence structure is given by the function in Equation 1.2; in fact, the value of can be deduced from (see Section 2 below). Several parametric families exist for multivariate (e.g., Weller and Cooley, 2014) and spatial applications (e.g., Wadsworth and Tawn, 2012). Other statistical approaches for modeling asymptotic independence are also related to this function, including hidden regular variation (Resnick, 2002; Heffernan and Resnick, 2007) and the conditional extreme value model (Heffernan and Tawn, 2004). Note that Equation 1.2 includes the asymptotic dependence case if , and the function then contains the same information as .

Since it is typically not known a priori whether asymptotic dependence or independence is present in a data set, recent parametric models are able to capture both regimes as different sub-sets of the parameter space (e.g., Ramos and Ledford, 2009; Wadsworth et al., 2017; Huser, Opitz and Thibaud, 2017; Engelke, Opitz and Wadsworth, 2019; Huser and Wadsworth, 2019). Most of the literature in this domain is concerned with constructing parametric models, and estimation is usually based on censored likelihood and discussed informally while no theoretical treatment of the corresponding estimators is provided. Moreover, it is typically assumed that extreme observations used to construct estimators already follow a limiting model, and the bias which results from this type of approximation is ignored.

The present paper is motivated by a lack of generic estimation methods that work under both asymptotic dependence and independence and have a thorough theoretical justification. We first revisit a non-parametric, rank-based estimator of the function in Equation 1.2 which appeared in (Draisma et al., 2004) and provide a new fundamental result on its asymptotic properties, which completely removes any smoothness assumptions on . This result is the crucial building block for the second major contribution of this paper: a new M-estimation framework that is applicable across dependence classes.

M-estimators for the stable tail dependence function have been proposed by Einmahl, Krajina and Segers (2008, 2012, 2016). Under asymptotic dependence, can be recovered from and thus any method for estimating also yields an estimator for . However, this is no longer true under asymptotic independence. Estimators of can therefore not be used to fit statistical models with asymptotic independence or models bridging both dependence classes. We define a new class of M-estimators based on for parametric extreme value models that can be applied regardless of the dependence class. A major challenge under asymptotic independence is due to the fact that the scaling function is unknown. Additionally, loses some of the regularity (such as concavity) that it enjoys under asymptotic dependence. Nevertheless, we are able to prove asymptotic normality of our estimators under weak regularity conditions, which are shown to be satisfied for popular models such as the class of inverted max-stable distributions (see Wadsworth and Tawn, 2012).

The challenges described above become even greater for spatial data. Even at the level of pairwise distributions, real data can exhibit asymptotic dependence at locations that are close but asymptotic independence at locations that are far apart. This necessitates models that can incorporate both, asymptotic dependence and independence at the same time. Estimation in such models calls for methods that can deal with both regimes simultaneously, and we show that our findings in the bivariate case can be leveraged to construct estimators in this setting.

In Section 2, we provide the necessary background on asymptotic dependence and independence for bivariate distributions, discuss an extension to the spatial setting, and provide several examples. The estimation methodology is introduced in Section 3, while theoretical results are collected in Section 4. The methodology is illustrated via simulation studies in Section 5, while an application to extreme rainfall data is given in Section 6. All proofs are deferred to Sections S1, S2, S3 and S4 in the Supplementary Material.

2 Multivariate extreme value theory

2.1 Bivariate models

Let be a bivariate random vector with joint distribution function and marginal distribution functions and , respectively. There is a variety of approaches to describe the joint tail behavior of .

The assumption of multivariate regular variation (cf., Resnick, 1987) is classical in extreme value theory and the stable tail dependence function in (1.1) has been extensively studied. Its margins are normalized, , and it satisfies for all . Moreover, it is a convex and homogeneous function of order one, the latter meaning that for all . The importance of stable tail dependence functions stems from their connection to max-stable distributions. A bivariate random vector has max-stable dependence with standard uniform margins iff its distribution function is given by

| (2.1) |

where is the stable tail dependence function pertaining to . Note that any max-stable distribution associated with satisfies Equation 1.1 with that same , this follows after a simple Taylor expansion. Two examples of max-stable distributions (equivalently, stable tail dependence functions) that will repeatedly appear in the present paper are as follows.

- (i)

- (ii)

While multivariate regular variation and max-stability have been very popular due to their nice theoretical properties, they are not informative under asymptotic independence which limits their use in many applications.

Assumption (1.2) allows for more flexible tail models since the limiting function is non-trivial even under asymptotic independence and contains information on the structure of residual extremal dependence in the vector . For the sake of identifiability, we scale such that . We will refer to and as the survival tail function and the scaling function associated to . It turns out that has to be regularly varying of order and that is a homogenous funcion of order , that is,

see for example Draisma et al. (2004) or Lemma S2 in the supplement. Note that the extremal dependence coefficient (see Coles, Heffernan and Tawn, 1999) can be defined as . Asymptotic independence is then equivalent to , or , whereas asymptotic dependence corresponds to .

Furthermore, the homogeneity property of implies a spectral representation. More precisely, there exists a finite measure on such that

see Theorem 1 in Ramos and Ledford (2009) or Lemma S6 in the supplement.

We provide several examples that illustrate the concepts discussed above without going too deeply into technical details. A more thorough discussion of the corresponding theory is given throughout Section 4.

Example 1 (Domain of attraction of max-stable distributions).

Suppose that satisfies Equation 1.1 for a stable tail dependence function which is not everywhere equal to . Then Equation 1.2 holds with and , where the extremal dependence coefficient is positive. We further note that Equation 1.1 holds whenever is in the max domain of attraction of a max-stable random vector satisfying Equation 2.1, see de Haan and Ferreira (2006) for a definition and additional details.

Example 2 (Inverted max-stable distributions).

The family of inverted max-stable distributions (e.g., Wadsworth and Tawn, 2012, Definition 2) is parametrized by all stable tail dependence functions. More precisely, let be the distribution function of a bivariate distribution with max-stable dependence, uniform margins and stable tail dependence function . A random vector with uniform marginal distributions is said to have an inverted max-stable distribution with stable tail dependence if . Assuming that satisfies a quadratic expansion (see Example 8), the law of satisfies Equation 1.2 with

where denotes the -th directional partial derivative of from the right, . Any such stable tail dependence function satisfies , and therefore this is an asymptotically independent model with .

Any existing parametric class of stable tail dependence functions can be used to define a parametric class of inverted max-stable distributions. In particular we consider the two families discussed earlier

-

(i)

Provided that , the inverted Hüsler–Reiss distribution has

(2.2) where .

-

(ii)

The inverted asymmetric logistic distribution has

(2.3) where and . Note that by suitable choices of the parameters any value of such that can be obtained.

Example 3 (A random scale construction).

Bivariate random scale constructions are a popular way of creating distributions with rich extremal dependence structures; see Engelke, Opitz and Wadsworth (2019) and references therein for an overview. They are random vectors of the form where the radial variable is assumed independent of the angular variables , . This motivates the following model with parameters :

| (2.4) |

where are independent and a distribution has distribution function for . By Example 9 below, satisfies Equation 1.2 with functions and depending only on the value of the ratio . In particular, we obtain asymptotic dependence if and asymptotic independence otherwise. Detailed expressions for and are provided in Example 9.

2.2 Spatial models

Spatial extreme value theory is an extension of multivariate extremes to continuous index sets. It is particularly useful for modeling extremes of natural phenomena over spatial domains and examples include heavy rainfall, high wind speeds and heatwaves (e.g., Davison and Gholamrezaee, 2012; Le et al., 2018).

Let be a spatial domain (typically a subset of ) and be a stochastic process whose extremal behavior we are interested in. We impose the condition in Equation 1.2 on all bivariate margins of so that for each pair of locations, and all the limit

| (2.5) |

exists and is non-trivial; here is the distribution function of . Similarly to the bivariate case, must be regularly varying with index and is homogeneous of order .

In applications, spatial extreme value theory can be linked to multivariate extreme value theory through the fact that spatial processes are usually measured at a finite set of locations. However, generic multivariate models do not take into account the additional structure arising from spatial features of the domain. Statistical models for processes, in contrast, make use of geographical information to construct structured, low-dimensional parametric models (see, e.g., Engelke and Ivanovs, 2021).

Similarly to max-stable distributions in Equation 2.1, max-stable processes play an important role in modeling spatial extremes. The stochastic process is called max-stable if all its finite dimensional distributions are max-stable, which implies in particular that for each pair , the bivariate margin satisfies Equation 2.1 with stable tail dependence function . Hence Equation 2.5 follows for any max-stable process for which are not independent for all .

Brown–Resnick processes (Brown and Resnick, 1977) provide an important subclass of max–stable processes. A Brown–Resnick process is parametrized by a variogram function , and any pair is a bivariate Hüsler–Reiss distribution with parameter (Hüsler and Reiss, 1989). Parametric models can be constructed by imposing a parametric form for . An example when is the fractal family of variograms given by , where , is the Euclidean norm and , are the model parameters (Kabluchko et al., 2009). We next discuss two classes of processes for which Equation 2.5 holds.

Example 4 (Domain of attraction of max-stable processes).

A process is in the max-domain of attraction of the max-stable process if there exist sequences of continuous functions such that

| (2.6) |

for i.i.d. copies of the process where weak convergence takes place in the space of continuous functions on equipped with the supremum norm; see de Haan et al. (2001) and Chapter 9 of de Haan and Ferreira (2006) for the special case .

Equation 2.6 implies that any pair with is in the max-domain of attraction of the pair . If every such pair is not independent, Equation 2.5 holds for all by the discussion in Example 1.

While max-stable processes allow for flexible spatial dependence structures, they can only be used as models for asymptotic dependence. This often violates the characteristics observed in real data, especially for locations that are far apart. To model data in such cases, asymptotically independent spatial models have been constructed that satisfy Equation 2.5 and where the residual tail dependence coefficients vary with the distance between the pair of locations. Most of the models are identifiable from the bivariate margins so that statistical methods for will provide estimators for spatial tail dependence parameters; see Section 3.3 for the methodology. A broad class of asymptotically independent stochastic processes are the inverted max-stable processes (Wadsworth and Tawn, 2012).

Example 5 (Inverted max-stable processes).

Let be a process with max-stable dependence, uniform margins and bivariate tail dependence functions . The process is called inverted max-stable. For a pair , assuming that satisfies the smoothness condition mentioned in Example 2, satisfies Equation 2.5 with

so that is a (usually non-constant) function on . In particular, if a Brown–Resnick process is parametrized by a variogram function then the corresponding inverted Brown–Resnick process has .

3 Estimation

In this section we present the proposed estimators. First, we recall the non-parametric estimator of a survival tail function from Draisma et al. (2004) in Section 3.1. Using this as building block, we construct M-estimators for bivariate survival tail functions (Section 3.2) and leverage those estimators to introduce methodology for spatial tail estimation (Section 3.3).

3.1 Non-parametric estimators of survival tail functions

Recall that is a random vector with joint distribution function that satisfies Equation 1.2, and assume that its marginal distribution functions and are continuous. Denoting by the joint distribution function of , we can rephrase Equation 1.2 as

| (3.1) |

for some function as . Suppose that are independent samples from . Since are unknown, the observations are not available and can not be used to construct a feasible estimator of . A typical solution to this problem is to replace by its empirical counterpart , which leads to the estimator

| (3.2) |

see Huang (1992); Drees and Huang (1998); Einmahl, Krajina and Segers (2008, 2012) among others for related approaches in the estimation of stable tail dependence functions.

Given and the expansion in Equation 3.1, an intuitive plug-in estimator of the function is given by

| (3.3) |

where we set in Equation 3.1 for an intermediate sequence such that , . Note, however, that this estimator is infeasible under asymptotic independence since the function is in general unknown. A simple remedy is to recall that we considered the normalization and construct a ratio type estimator

| (3.4) |

to cancel out the unknown scaling factor . This leads to a fully non-parametric estimator of , which is interesting in its own right. Some comments on the asymptotic properties of this estimator will be provided in Section 4.1.1.

Remark 1.

In practice, and especially in a spatial context, it is sometimes appropriate to select directly the effective number of observations used for estimating (Wadsworth and Tawn, 2012). This can be achieved by selecting such that for a given value . This leads to a data-dependent parameter which will also be covered by our theory.

3.2 M-estimation in (bivariate) parametric model classes

While the non-parametric estimators from the previous section possess attractive theoretical properties, they have certain practical drawbacks. For any finite sample size they are neither continuous nor homogeneous, hence they are not admissible survival tail functions. Additionally, it is difficult to use purely non-parametric estimators in spatial settings. A solution to this problem, which also yields easily interpretable estimators, is to fit parametric models.

In what follows, assume that belongs to a family , where and the true parameter is unknown. Our aim is to leverage the non-parametric estimators from Section 3.1 to construct an estimator for . For stable tail dependence functions which are only informative under asymptotic dependence such a program was carried out in Einmahl, Krajina and Segers (2008, 2012). A direct application of the corresponding ideas in our setting would be to estimate through

for an integrable vector-valued weight function , where denotes the Euclidean norm. However, as we will discuss in Remark 5, the use of would place unnecessarily strong assumptions on the function in the case of asymptotic dependence. Hence we propose to consider the following alternative approach. Define

| (3.5) |

and let

| (3.6) |

To understand the rationale of this approach, note that is proportional to but the proportionality constant involves and is thus unknown. We thus essentially propose to add this unknown normalization factor as an additional scale parameter . More precisely, write for the Lebesgue measure on , let

and note that and are linked through . Thus minimizes if and only if minimizes . Furthermore, under suitable assumptions on and we have if and only if and . Hence, if is close to , it is expected that will be close to and that will be approximately .

Note that Equation 3.5 only involves an integral of while also involves point-wise evaluation of this function. Since integration acts as smoothing, it can be expected that studying will require less regularity conditions than working with ; see Remark 5 for additional details.

3.3 Parametric estimation for spatial tail models

In this section, we show how the bivariate estimation procedures discussed earlier can be leveraged to obtain two different estimators for parametric spatial models, which can include both asymptotic dependence and independence. Assume that we observe independent copies of a spatial process at a finite set of locations . Denote the corresponding observations by where are independent copies of the random vector ; see Einmahl, Krajina and Segers (2016) for a similar framework.

Let denote the set of all subsets of of size 2 interpreted as ordered pairs, so that elements of will take the form with . In what follows, we will need to repeatedly make use of vectors that are indexed by all pairs . For such vectors we will assume that the pairs in are ordered in a pre-specified order and will write for the entry of the vector that corresponds to pair .

Assume that for each pair the random vector satisfies Equation 3.1 with scale function and survival tail function . Following the ideas laid out in Section 3.1, define as in Equation 3.2 but based on the bivariate observations . We now discuss two parametric estimators for the functions .

Assume that we start with a parametric model , , for bivariate survival tail functions and that each falls in this class. This implies that can be linked to a spatial parameter space through the relations , where for each pair . To make this idea more concrete, consider the following example, which we will revisit in Sections 5.2 and 6.

Example 6.

If the process is an inverted Brown–Resnick process on (see Example 5) then has an inverted Hüsler–Reiss distribution and the bivariate survival tail functions are of the form , for some . This determines the parametric class . A more specific model of Brown–Resnick processes corresponds to the sub-family of fractal variograms (Kabluchko et al., 2009; Engelke et al., 2015), where

| (3.7) |

where is the coordinate of the location ; see Section 6 for more motivation of this particular parametrization. The global parameter thus takes the form and .

Given the setting above, we can thus compute parametric estimators , by the methods for bivariate estimation discussed in Section 3.2, i.e., is the minimizer of , where is defined as in (3.5) with and an intermediate sequence replacing and . We obtain an estimator of the spatial parameter by least squares minimization,

| (3.8) |

As an alternative, one may use the relations between the spatial and bivariate parameters and minimize all the objective functions simultaneously, leading to the estimator

| (3.9) |

A theoretical analysis of the estimators and is provided in Theorem 5. We further remark that the computational complexity of the proposed estimators is much lower than that of methods based on full likelihood and it compares favorably to pairwise likelihood. Additional details regarding the latter point can be found in Section S5 of the supplement.

Remark 2.

At first glance the minimization problem in Equation 3.9 seems to be computationally intractable since it contains parameters and since can be very large even for moderate dimension . However, a closer inspection reveals that for given , partially minimizing the objective function in (3.9) over has the exact solution

whenever the right-hand side is positive for all . This is satisfied if for instance is positive everywhere and each is based on at least one data point. Thus only numerical optimization over , which is usually low-dimensional, is required.

4 Theoretical results

We now present our main results on the asymptotic distributions of the various estimators introduced in Section 3. First, functional central limit theorems are stated for , followed by our main result on the bivariate M-estimator. Finally, asymptotic normality of the processes and of the two parametric estimators in the spatial setting is established. The proofs of all main results are deferred to Section S1 in the supplement.

4.1 The bivariate setting

All results in this section will be derived under the following fundamental assumption.

Condition 1.

-

(i)

Equation 3.1 holds uniformly on with a function and the function is such that exists.

-

(ii)

As , and .

We note that in the proofs, Equation 3.1 is required to hold locally uniformly on , but by Lemma S2 uniformity on implies uniformity over compact subsets of . Condition 1(ii) is a standard assumption that makes certain bias terms negligible. It is not a model assumption; under Condition 1(i), there always exists a sequence such that Condition 1(ii) is satisfied and thus all of the following discussion will focus on Condition 1(i). Notably and in contrast to most of the existing literature involving non-parametric estimation, Condition 1 does not assume any differentiability of the function . In fact, our proofs show that all the regularity required on can be derived from Equation 3.1. Considering Remark 1, it is possible to use a data-dependent value . In following results, when this is done, we will assume that there is an unknown sequence that satisfies Condition 1(ii), that is defined as therein, and that is chosen so that .

We next discuss this condition in the examples introduced in Section 2.1. Proofs for the claims in the examples below can be found in Sections S3 and S4 of the supplement.

Example 7 (Example 1, continued).

Most of the literature on asymptotic analysis of estimators of the stable tail dependence function or related quantities under domain of attraction conditions makes some version of the following assumption

| (4.1) |

for a non-vanishing function on where , see for instance condition (C2) in Einmahl, Krajina and Segers (2008) or the discussion in Bücher, Volgushev and Zou (2019). A simple computation involving the inclusion-exclsion formula further shows that this is equivalent to assuming that convergence in Equation 1.1 takes place with rate and that . Clearly Equation 4.1 implies Condition 1(i) with , and .

Example 8 (Example 2, continued).

Let be a bivariate inverted max-stable distribution and assume that there exists a constant such that for all ,

where represent the directional partial derivatives of from the right. In particular, it suffices for to be twice differentiable. Then the random vector satisfies Condition 1(i) with , and . Moreover, and .

Example 9 (Example 3, continued).

Let be a random scale construction as defined in Equation 2.4 and set . Then satisfies Condition 1(i) with functions , and determined by as in Table 1 below.

4.1.1 Asymptotic theory for non-parametric estimators

In this section we consider the estimator from Equation 3.3. Since the process convergence results differ under asymptotic dependence and independence, we discuss these settings separately. Our first result deals with asymptotic independence.

Theorem 1 (Asymptotic normality of under asymptotic independence).

Assume Condition 1. Then under asymptotic independence, i.e., when ,

in , for any . Here, is a centered Gaussian process with covariance structure given by . The same remains true if is replaced by as described after Condition 1.

Note that process convergence of the estimator from Equation 3.4 can be obtained from the above result through a straightforward application of the functional delta method. This will not be needed in the theory for M-estimators in the next section and details are omitted for the sake of brevity.

Asymptotic properties of were considered in Draisma et al. (2004). However, the proof of the corresponding result (Lemma 6.1) in the latter reference makes the additional assumption that the partial derivatives of exist and are continuous on (cf. Peng, 1999, Theorem 2.2). In contrast, we are able to show that no condition on existence or continuity of partial derivatives is required. This is a considerable strengthening of the result which further allows to handle many interesting examples that were not covered by the results of Draisma et al. (2004). Indeed, both the popular class of inverted max-stable distributions in Example 2 and the random scale construction in Example 3 lead to functions that fail to have continuous or even bounded partial derivatives. Before moving on to discussing results under asymptotic dependence, we briefly comment on some of the main ideas of the proof.

Remark 3 (Main ideas of the proof of Theorem 1).

The proof relies on the decomposition

where

and and denote the th order statistics of and , respectively with . The core difficulty is to show that the difference is negligible. Under the assumption of the existence and continuity of partial derivatives of on made in Draisma et al. (2004) this is a direct consequence of the fact that under asymptotic independence . Dropping this assumption considerably complicates the theoretical analysis. The proof strategy is to derive bounds on increments of for close to where the partial derivatives of can become unbounded (see Lemmas S7 and S2.7) and to combine those bounds with subtle results on weighted weak convergence of as a process in ; see Lemma S3 where we essentially leverage the findings of Csörgő and Horváth (1987).

We next turn to the case of asymptotic dependence. Results on convergence of in the space are well known under this regime; they are equivalent to similar results about estimated stable tail dependence functions (cf. Huang, 1992). However, they require the existence and continuity of partial derivatives of or, equivalently, . As shown in Einmahl, Krajina and Segers (2008, 2012), the latter condition is restrictive and in fact not necessary to derive asymptotic normality of M-estimators.

The treatment of M-estimators in Einmahl, Krajina and Segers (2008, 2012) involves a direct analysis of certain integrals without using process convergence in . While this approach could be transferred to our setting, we will instead follow a strategy put forward in Bücher, Segers and Volgushev (2014) and prove weak convergence of with respect to the hypi-metric introduced therein. This approach will turn out to generalize much more easily when we deal with spatial estimation problems. Convergence with respect to this metric holds without any assumptions on the existence of partial derivatives and is sufficiently strong to guarantee convergence of integrals which is needed for the analysis of M-estimators.

Let denote the partial derivative of with respect to from the left and denote its partial derivative with respect to from the right. Under asymptotic dependence, is concave since is convex (de Haan and Ferreira, 2006, Proposition 6.1.21), hence those directional partial derivatives exist everywhere on , by Theorem 23.1 of Rockafellar (1970). The definition can be extended to be setting to be the derivative from the right instead of from the left.

To describe the limiting distribution, recall that is positive only in the case of asymptotic dependence. For , define

| (4.2) |

and let be an -valued, zero mean Gaussian process on with covariance function . Note that is the limiting process in Theorem 1, that is constant in and that is constant in .

Theorem 2 (Asymptotic normality of under asymptotic dependence).

Assume Condition 1. Then under asymptotic dependence, i.e., when ,

in , for any . Here, is defined as in Theorem 1. The same remains true if is replaced by as described after Condition 1.

Note that weak convergence in the above theorem takes place in where corresponds to equivalence classes of functions in with respect to the hypi-(semi-)metric , see Bücher, Segers and Volgushev (2014) for additional details.

The proof of Theorem 2 follows by adapting the arguments given in Bücher, Segers and Volgushev (2014) for the function and builds on the fact that under asymptotic dependence the function is differentiable almost everywhere. Note however that, in contrast to similar results in Bücher, Segers and Volgushev (2014), our limiting process is stated without appealing to lower semi-continuous extensions. This type of statement is inspired by the representation of certain integrals in Einmahl, Krajina and Segers (2012) and is possible in the bivariate setting due to concavity of under asymptotic dependence. Additional comments on the representation of the limiting process are given in Remark 4 below.

Remark 4.

In order to obtain asymptotic results for our M-estimator, weak convergence of to is sufficient. Under asymptotic dependence, this is seen to follow from Theorem 2 (see the proof of Theorem 3). However, this process convergence result is not necessary. An approach that is used in Einmahl, Krajina and Segers (2012) is to write an expression for the random vector and directly work out its weak limit. With this strategy, may be defined as left or right derivatives without problem as will be unchanged. In contrast, proving weak hypi-convergence of to makes our results more general and more easily generalized to the spatial framework. The cost of doing so is that the directional derivatives must be chosen in a specific way; see Lemma S9.

Remark 5.

Recall that under asymptotic independence, process convergence of could be obtained from Theorem 1 by a simple application of the delta method. This is no longer the case in the general setting of Theorem 2 because weak convergence with respect to the hypi-metric does not imply convergence of , unless the limiting process has sample paths which are a.s. continuous in . The latter happens only if the partial derivatives of exist and are continuous in . Under this additional assumption convergence of with respect to the hypi-metric can be obtained.

4.1.2 Asymptotic theory for bivariate M-estimators

Equipped with the process convergence tools from the previous section, we proceed to analyze the M-estimator introduced in Section 3.2. Consistency is established by standard arguments, and for the sake of brevity we do not state the corresponding results here. In the present section, we focus on the asymptotic distribution. Define the objective function by

| (4.3) |

Clearly, . In addition, assume that is a unique, well separated zero of and let denote the Jacobian matrix of for points where it exists.

Define under asymptotic independence and otherwise

where is defined in Equation 4.2. Recall from the previous section that these directional derivatives always exist when since in this case is concave. In fact, is the covariance between and (under asymptotic independence) or between and (under asymptotic dependence). Hence in those two regimes,

is the covariance matrix of the random vector or , respectively. We are now ready to state the main result of this section: asymptotic normality of , which holds under both asymptotic dependence and independence.

Theorem 3 (Asymptotic normality of ).

Assume that has a unique, well separated zero at and is differentiable at that point with Jacobian of full rank , . Further assume Condition 1. Then the estimators defined in Equation 3.6 satisfy

where . The same remains true if is replaced by as described after Condition 1.

While for simplicity the estimator is defined as an exact minimizer, the same result can be obtained for an approximate minimizer. Precisely, it is obvious from the proof of Theorem 3 that as long as , the conclusion still holds. Finally, recall that the coefficient of tail dependence can be recovered from the function since the latter is homogeneous of order , and this relation always holds. Therefore, inside the assumed parametric model, can be represented as a function . The asymptotic distribution of the resulting estimator can be obtained by a direct application of the delta method and details are omitted for the sake of brevity.

4.2 The spatial setting

In this section we assume the framework of Section 3.3 and establish asymptotic properties of the estimators therein. For each pair , let be an intermediate sequence and define

From Section 4.1.1, the asymptotic distribution of is known under suitable conditions. However, as the spatial estimators and are based on all pairs, a joint convergence statement about all processes is necessary. This will require an additional assumption which we present and discuss next.

Let denote the marginal distribution functions of the random vector , which itself consists of the spatial process evaluated at different locations. In order to obtain the asymptotic covariance between different processes , we need to ensure that certain multivariate tail probabilities converge. Partition the set into and , consisting of the asymptotically independent and asymptotically dependent pairs, respectively. In the formulation of the following assumption, and are used to denote pairs. For brevity, is also used to denote a point in .

Condition 2.

For every , satisfies Condition 1(i) with functions and exists. Intermediate sequences are chosen so that and . For pairs , points and sets of two-dimensional vectors with entries in , let

We assume that the sequences are chosen such that the limits

exist for all , and that the convergence is locally uniform over .

We next discuss the above condition in three special cases of particular interest. The first two are processes in the domain of attraction of max-stable processes and inverted max-stable processes. The third one is a mixture process appearing in Wadsworth and Tawn (2012), which can have asymptotically dependent and independent pairs simultaneously.

Example 10 (Example 4, continued).

If is in the max-domain of attraction of a max-stable process, then is in the max-domain of attraction of a max-stable distribution on with stable tail dependence function

see Equation 1.1. If moreover the convergence is locally uniform over and if every pair is asymptotically dependent, then Condition 2 holds. Note that this is automatically satisfied if itself is max-stable. The sequences can be chosen all equal to , say, and for every pair , . The sequences can also be chosen all asymptotically equivalent to , say, by choosing . The limiting covariance terms can all be deduced from by straightforward calculations.

Example 11 (Example 5, continued).

If is an inverted max-stable process, then has an inverted max-stable distribution, and we assume that the associated stable tail dependence function is component-wise strictly increasing. The latter is trivially satisfied if has a positive density. Then if all the pairwise functions satisfy the quadratic expansion introduced in Example 8, Condition 2 is satisfied and the sequences can be chosen so that the are all equal, that is, for every pair , for some intermediate sequence . Here, is empty so the only required covariance terms are (see Section S3)

For instance, any inverted Brown–Resnick process (or rather the implied inverted -dimensional Hüsler–Reiss distribution corresponding to the observed locations) satisfies Condition 2 as long as the aforementioned -variate distribution has a density. The latter can easily be checked (e.g., Engelke and Hitz, 2020, Corollary 2).

Example 12 (Wadsworth and Tawn (2012), Section 4).

Let be a max-stable process and be an inverted max-stable process, both with unit Fréchet margins. Suppose that satisfies the monotonicity condition stated in Example 11, and additionally that none of its pairwise distributions is perfectly independent. Let and define the process by

Then also has unit Fréchet margins. If becomes independent at a certain spatial distance, the process transitions between asymptotic dependence and independence at that distance. An instance of such a max-stable process is found in the second example after Theorem 1 of Schlather (2002), assuming that the Radius of the random disks is bounded (see also Davison, Padoan and Ribatet, 2012, eq. (23) and the discussion that precedes).

The process can be shown to satisfy Condition 2 if the sequences are chosen so that the are all equal. The terms , and are mostly determined by the process , as in Example 10; see Section S3 in the supplement for details.

4.2.1 Joint distribution of non-parametric estimators

The joint limiting behavior of the processes relies on , a collection of centered Gaussian processes on . The covariance between and is given by , the covariance between and takes the form , and the covariance between and is equal to . For , let and for , let

where are defined similarly to in Section 4.1.1.

Theorem 4 (Asymptotic normality of ).

Assume Condition 2. Then

in the product space , for any . The same remains true if each is replaced by the data-dependent sequence as described after Condition 1.

The preceding result can be applied in all generality as long as the four-dimensional tails of the spatial process of interest are sufficiently smooth. The admissible settings include, but are far from limited to, Examples 10, 11 and 12.

According to Bücher, Segers and Volgushev (2014), convergence in the hypi-metric is equivalent to uniform convergence when the limit is a continuous function. The process clearly has almost surely continuous sample paths under asymptotic independence, as well as under asymptotic dependence if the partial derivatives of exist everywhere and are continuous. It follows that in those cases converges in . In fact, one may replace the product space in the result above by , where represents either equipped with the supremum distance (if or has continuous partial derivatives) or equipped with the hypi-metric (otherwise). In particular, for processes where every pair is asymptotically independent such as inverted max-stable processes, the hypi-metric can be replaced by the supremum distance everywhere.

4.2.2 Asymptotics for parametric estimators

We now show how Theorem 4 leads to asymptotic results for the parametric estimators and introduced in Equations 3.9 and 3.8. Recall the setting of Section 3.3, and in particular the functions and the relation . Similarly to the bivariate setting, define

In the bivariate setting, we required to be differentiable and have a unique well-separated zero. In the spatial setting we need a comparable assumption.

Condition 3.

For every pair , the functions and are continuously differentiable at the points and , respectively, with Jacobian matrices and of full ranks and . Additionally (i) or (ii) holds.

-

(i)

The functions and have a unique, well separated zero at the points and , respectively.

-

(ii)

The function as a function on has a unique, well separated zero at the point .

Assuming both parts of Condition 3, we now introduce the notation that is needed to define the limiting covariance matrices of the two estimators. In the following, elements of a vector are ordered by pair first, and then by dimension . The same convention is used when ordering the rows or columns of a matrix.

Letting denote the limiting Gaussian processes appearing in Theorem 4, consider the matrix with blocks of the form

Let be a block-diagonal matrix with blocks given by

| (4.4) |

where and indicates the sub-matrix consisting of rows 1 to and columns 1 to of the matrix . Define by stacking the matrices , , on top of each other. Denote by the unit vector in with a one in the position corresponding to the pair and let be obtained by stacking the matrices

on top of each other. Finally, define

Theorem 5 (Asymptotic normality of the estimators of ).

Assume Condition 2 and suppose that the sequences are all asymptotically equivalent to , say. Then under Condition 3(i), the estimator defined in Equation 3.8 satisfies

and under Condition 3(ii), the estimators defined in Equation 3.9 satisfy

where and are as above. The same remains true if each is replaced by the data-dependent sequence , based on the same sequence , as described after Condition 1.

The assumption of asymptotic equivalence of all can be substantially relaxed. Otherwise, a simple way to satisfy it is to select one and use data-driven sequences .

5 Simulations

5.1 Bivariate distributions

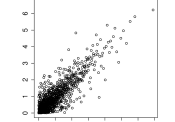

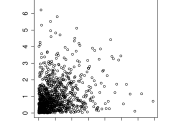

In this section we study the finite sample behavior of the estimator introduced in the paper. We simulate samples from the bivariate vector , where is the signal and is and independent noise vector. We consider three different models for the bivariate distributions .

-

(M1)

The inverted Hüsler–Reiss model from Example 2(i) with unit Fréchet margins, whose corresponding class of functions takes the form where .

- (M2)

- (M3)

Figures S1, S2 and S3 in the supplement show realizations of models M1–M3 corresponding to different parameter values and rescaled to unit exponential margins for illustration.

As a noise vector we simulate samples of , where and are independent with Pareto distribution function , . Note that this tail is lighter than that of the marginal distributions in all three models; it can be shown that this additive noise does not affect the functions and of .

All of the results that follow are based on simulation repetitions and samples of size . In all the simulations, we use the same weight function (represented by in Equation 3.5), which we now describe. Consider the following rectangles: , , , and . The function is given by

| (5.1) |

where and is simply a reference point in the parameter space that ensures that all components of have comparable magnitude. In the three models above, the reference points are , and , respectively. The rectangles are chosen in order to capture various aspects of the function : contains information about the unknown scale (recall that we scale so that ). The rectangles are geared towards determining homogeneity properties of since and are especially useful for estimating . The rectangles are informative about asymmetry of the function with respect to its arguments. Different choices of the weight function would be possible, and the best choice will be different for each model under consideration and even for each specific parameter value within a given model class. Nevertheless, the aforementioned choice seems close to optimal for all the models considered here. In Section S6 of the supplement, a sensitivity analysis is carried out where we repeat the simulation study with different weight functions that are constructed by considering only some of the rectangles instead of all five. See also Einmahl, Krajina and Segers (2008, 2012) for a related discussion in the estimation of stable tail dependence functions.

5.1.1 The inverted Hüsler–Reiss model (M1)

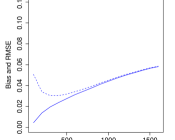

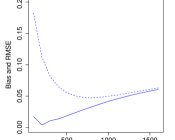

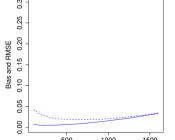

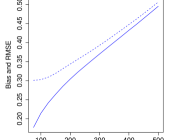

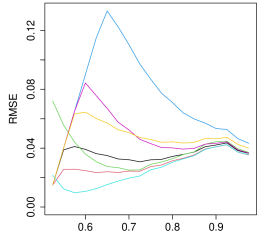

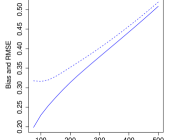

Figure 1 shows the effect of on the estimation performance of from Equation 3.6 in terms of absolute bias and root MSE for the three parameter values , , and . We observe that for larger values of (or smaller values of , corresponding to more independence in the extremes) larger values of lead to the best RMSE. This is in line with our theory as, for fixed , smaller corresponds to smaller values of and hence larger asymptotic variance.

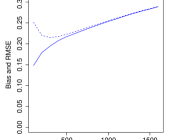

An analysis of for a finer range of parameter values is provided in Figure 2. Motivated by the findings in Figure 1 we fix ; this choice leads to reasonable performance across all parameter values. Overall the results are satisfactory, with a more pronounced negative bias for smaller values of and more variance for increasing .

5.1.2 The inverted asymmetric logistic model (M2)

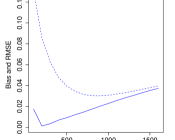

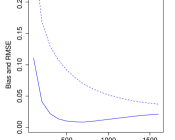

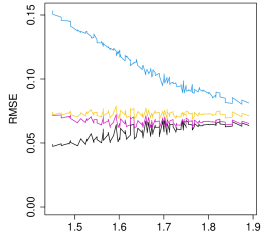

Figure 3 shows the impact of on estimated parameter values for three different choices of . Since here the parameter is two-dimensional, we consider (and estimate) the Euclidean bias and RMSE of the estimator , defined as and , respectively.

Similarly to the pattern observed in Figure 1 we see that smaller values of necessitate larger values of in order to achieve a good balance between bias and variance.

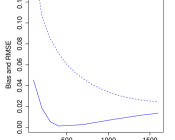

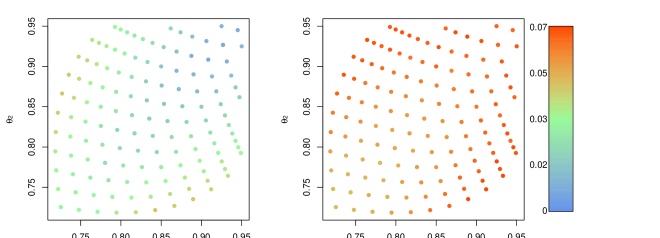

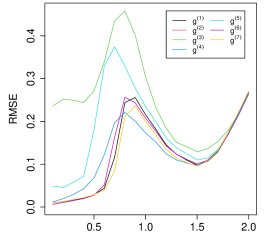

Figure 4 shows the performance of the proposed M-estimator for a range of different parameters with Euclidean bias in the left panel and RMSE in the right panel; the value is fixed throughout. Since the relation is not easily invertible, we selected a grid of values of , calculated all the corresponding points and kept the values for which , .

We observe that the estimators perform better for parameter values close to the diagonal, with larger bias and variance for more asymmetric parameter values. The overall estimation accuracy is reasonably good, with worst case RMSE values around 0.07.

5.1.3 The Pareto random scale model (M3)

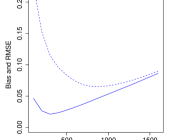

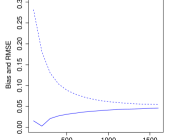

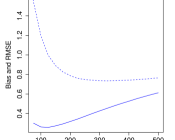

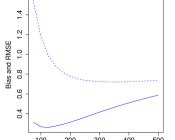

Figure 5 shows the effect of on the performance of our M-estimator in terms of absolute bias and root MSE for the three parameter values , , and . We notice that the estimator is considerably more biased at than at other parameter values. This is expected as, according to Table 1, the bias function vanishes only at a logarithmic rate when , compared to a polynomial rate elsewhere. Moreover, like in the other models, we observe that for more independent data (characterized by larger ), larger values of are required to drive down the variance of the estimator.

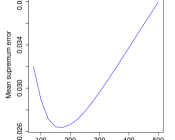

An analysis of for a finer range of parameter values is provided in Figure 6. Motivated by Figure 5 we fix , which approximately minimizes the maximal RMSE. Overall the estimator is very precise for small values of , but incurs a bias around where it struggles to distinguish between values slightly smaller and slightly larger than 1. This phenomenon is not completely unexpected; a close look at Table 1 reveals that has almost (but not quite) a symmetry around the point , e.g. is very similar in shape to . This point also corresponds to the transition between asymptotic dependence and independence, which makes estimation challenging.

5.2 Spatial models

In this section we illustrate the performance of the proposed methodology for spatial data. The candidate class for results from inverted Brown–Resnick processes with fractal variograms (see Example 6) and takes the form

| (5.2) |

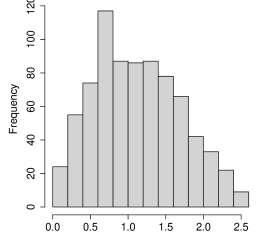

where and is the Euclidean distance between the two locations in pair (measured in units of latitude). Motivated by the data application in the following section, the true parameter values are set as and the values for are obtained from randomly sampled pairs of locations in that data set; see Figure S5 in the supplement for a histogram of the distances in this sample.

To evaluate the performance of our estimators we simulate independent data sets, each of size , of an inverted Brown–Resnick process with unit Fréchet margins and fractal variogram from Equation 3.7 with . Following the bivariate simulations, to each of the 40 components of the data we add an independent random variable with Pareto distribution function , . Using the same weight function as in the bivariate simulations (see Equation 5.1), we compute the two estimators introduced in Equations 3.8 and 3.9. Since the performance of both estimators turns out to be very similar, we only report results for the least squares estimator from Equation 3.8 here and defer all simulations for the estimator (3.9) to Section S6 in the supplement.

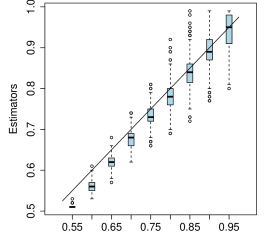

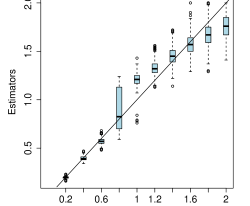

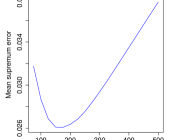

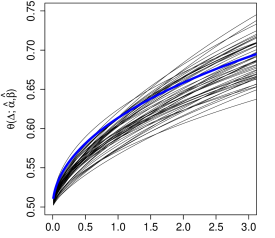

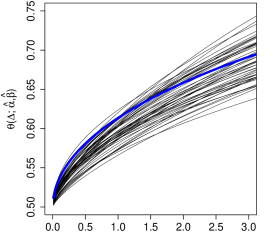

Following the discussion in Remark 1, we fix a value and select each such that . The first two panels of Figure 7 show the absolute bias and RMSE of the estimators and , respectively, as functions of . We observe that the RMSE for both estimators is relatively large across all values of . Interestingly, this does not result in a bad performance in estimating the function . Indeed, the last panel of Figure 7 shows averaged (over simulation runs) values for and indicates a good overall performance; note that the observed values of are all smaller than 3 (see Figure S5 in the supplement). This can be explained by the fact that different values of can lead to somewhat similar curves in the range of interest. This is further illustrated in the left panel of Figure 8 where a random sample of 50 estimated functions is displayed.

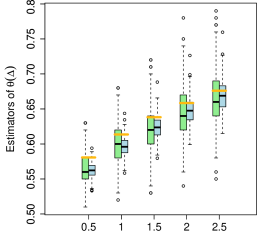

We conclude this section by fixing and comparing the performance of estimators for based on a bivariate sample at a given distance and the spatial estimator discussed above. Boxplots corresponding to five pairs of stations with distances are shown in the left panel of Figure 8. As expected from the theory, using the spatial estimator is advantageous as it allows to combine information from different distances and leads to a reduced variance.

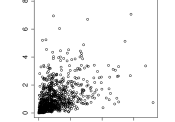

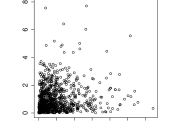

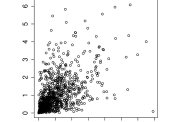

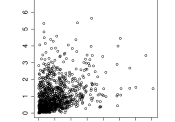

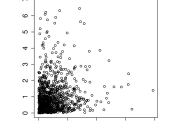

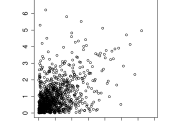

6 Application to rainfall data

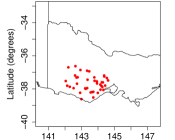

In a data set introduced in Le et al. (2018), rainfall was measured daily from 1960 to 2009 at a set of 92 different locations in the state of Victoria, southeastern Australia, for a total of measurements. The conclusions in that paper are that an asymptotically independent model is suitable. A subset of 40 locations, for a total of 780 pairs, was randomly sampled; see the right panel of Figure 9. To the data at those selected locations we fit the same tail model as in Section 5.2, given in Equation 5.2. The weight function that we use is the same as before and as in Section 5.2, we make use of Remark 1 by fixing a value and choosing each accordingly.

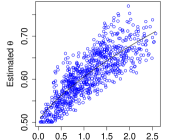

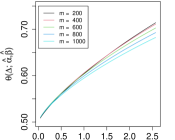

We set . The left panel of Figure 9 shows the 780 pairwise estimators plotted against the distances . Despite some estimates at the boundary of the parameter space, the results do not provide much evidence for asymptotic dependence, whereas all estimates are away from the boundary for distances of at least 0.3 units of latitude, strongly suggesting asymptotic independence at these distances. Our two estimators (3.8) and (3.9) of yield estimates of (1.55, 2.24) and (1.56, 2.24), respectively. They are extremely similar, as hinted by the simulation study from Section 5.2. The curve corresponding to the least squares estimator is also shown in the left panel of Figure 9. The middle panel of Figure 9 displays similar curves for the least squares estimator when varies from 200 to 1 000. It shows that the estimated curve is robust with respect to the choice of .

Acknowledgments

We are grateful to two reviewers for their valuable input. Their constructive comments and suggestions resulted in a substantial improvement of this paper. Michaël Lalancette was supported by the Fonds de recherche du Québec – Nature et technologies and by an Ontario Graduate Scholarship. Sebastian Engelke was supported by the Swiss National Science Foundation and the Fields Institute for Research in Mathematical Sciences. Stanislav Volgushev was supported in part by a discovery grant from NSERC of Canada and a Connaught new researcher award.

SUPPLEMENTARY MATERIAL

This Supplementary Material is divided in six sections. Section S1 contains the proofs of all main results, with a number of necessary technical results deferred to Section S2. Sections S3 and S4 present proofs of several claims from different Examples. A brief discussion of computational complexity in spatial estimation is given in Section S5 and additional simulation results appear in Section S6.

S1 Proofs of main results

In this section are collected the proofs of Theorems 1, 2, 3, 4 and 5. A number of more technical results, which are instrumental in the following, are collected in Section S2.

S1.1 Bivariate estimation

For the proofs concerning the bivariate estimators, we assume the framework of Sections 3.1 and 3.2, we define the transformed random variables , and note that is the distribution function of the random vector . Define the transformed observations , and denote by and the ordered versions thereof. Additionally define . For an intermediate sequence , define the random functions and by

for . Recalling that , it allows us to write

where

denotes the empirical distribution function of . We begin by discussing technical results that will be used in the proof of both Theorem 1 and Theorem 2. Consider the decomposition

For the second term in the above decomposition, note that

uniformly over all ; here the last equation follows from Condition 1(ii). By Corollary S1 we have , and thus

Next define for all

| (S1.1) |

By Lemma S4 this process converges, in , to the process from Theorem 1 and by Corollary S1 and converge uniformly in probability to the identity function . Therefore, the triple converges jointly in distribution to . This implies

| (S1.2) |

Indeed, consider the map

where and assume that the product space is equipped with the norm . Observe that is continuous at points where is a continuous function and that the sample paths of are almost surely continuous. Thus, by the continuous mapping theorem, with probability converging to 1,

Since the limit is constant a.s. Equation S1.2 follows. Combining the equations above, we find

| (S1.3) |

where the term is uniform on , and we recall that in .

S1.1.1 Proof of Theorem 1

Define

In light of Equation S1.3 it suffices to prove that uniformly on . From here on it is more convenient to study component-wise increments. That is, we write

and we will show that both and converge to 0 in probability, starting with .

By assumption, since with probability converging to 1 we have for every , we can write

| (S1.4) | ||||

| (S1.5) |

uniformly on , since the sequence was chosen so that . We will use both Equations S1.4 and S1.5 as representations of throughout the proof.

Let . From there, partition in , and (if , is empty). These sets represent the “small”, “intermediate” and “large” values of , respectively. We will prove that the suprema of on , and all converge to 0 in probability. Equation S1.5 yields

where we have once again used the facts that whenever and that , in addition to the fact that . This proves that in probability.

Using Equation S1.5 again, the supremum of on can be expressed as

where we have used Lipschitz continuity of and Lemma S3. The last bound holds for any function that satisfies the conditions in Lemma S3, but from now on we use on and on , where is chosen small enough so that is well defined and non-decreasing. By monotonicity, the supremum is attained at . We then have

because since , eventually , so eventually . The last display converges in probability to 0 since

as , which proves that in probability.

Finally, when considering large values of , Lemma S3 and a combination of Equations S2.7 and S7 imply that

where . By monotonicity of , the inside of the can be upper bounded by

and since with probability converging to 1, for every , , this can in turn be upper bounded (with probability converging to 1) by

It can easily be checked (e.g. by differentiation) that the function is decreasing. Thus, the above supremum is attained at . Finally, elementary computations yield

Overall, we have shown that uniformly over . Note that all the bounds we derived are uniform over all values of , although it was removed from the notation for parsimony. In order to deal with , we recall once again that with probability converging to 1, we have for every . Therefore, with probability converging to 1,

This can be shown to converge in probability to 0 using the exact same proof as for . We finally conclude that in , and the proof for deterministic is complete. It remains to show that the result continues to hold if we replace the deterministic sequence by data-dependent as outlined in Remark 1. This is established in Section S1.1.3.

S1.1.2 Proof of Theorem 2

In view of Equation S1.3, we require the joint asymptotic behavior of , and . Define, for ,

a rescaled version of the marginal empirical distribution functions of and . We now show that the -valued process

| (S1.6) |

converges in distribution to the Gaussian process defined in Section 4.1.1 with covariance matrix from Equation 4.2, where .

Again, let denote the identity map on . The three processes , and are individually tight (see Lemma S4) and hence it suffices to prove convergence of the marginal distributions. This in turn follows from convergence of the covariance function, by the multivariate Lindeberg-Feller theorem (see van der Vaart (2000), Theorem 2.27); verification of the Lindeberg condition is similar to condition (B) in the proof of Lemma S4. The convergence of to is already shown in Lemma S4. Using similar arguments and recalling that , one easily deals with the other covariance terms and concludes that the processes in Equation S1.6 weakly converge to in .

Note that the random functions and are the generalized inverses of and , respectively. Because , the term is negligible. Upon applying Vervaat’s lemma (Vervaat (1972)), which states that the generalized inverse mapping is Hadamard differentiable around the identity function, we deduce that the processes , defined by

weakly converge to in . For , define the sets

| (S1.7) |

Let be the subset of functions such that is constant in , is constant in and the functions and are elements of . Let be the space of equivalence classes equipped with the topology of hypi-convergence. Define the functionals by

Equation S1.3 can be rephrased as , assuming that , which is true with probability

Let be the subset of continuous functions such that . As soon as converges uniformly to , by Lemma S9, hypi-converges to , where satisfies

Note that concentrates on . Therefore, by the extended continuous mapping theorem (van der Vaart and Wellner, 1996, Theorem 1.11.1),

in . It remains to show that the result continues to hold if we replace the deterministic sequence by data-dependent as outlined in Remark 1. This is established in Section S1.1.3.

S1.1.3 Proof that Theorems 1 and 2 continue to hold with

Let be the estimator computed with the random quantity instead of . We shall prove that in probability uniformly over (under asymptotic independence) or in the hypi semimetric (under asymptotic dependence).

Note that the definition of implies that . By assumption, converges to in probability uniformly in a neighborhood of . Jointly with the fact that , this readily implies that in probability. Further note that

We first discuss the case of asymptotic independence. By Theorem 1 and by Skorokhod’s almost sure representation, we may assume that almost surely, and . The object of interest is then equal, with probability one, to

| (S1.8) |

where we have used homogeneity of , regular variation of and the fact that almost surely, the sample paths of are continuous, hence uniformly continuous on compact sets. The terms are uniform over . Finally, it is shown in Lemma S2 that uniformly over in a neighborhood of 1, . Recalling that almost surely, the first term in Equation S1.8 is then uniformly of the order of , which vanishes by Condition 1(ii).

In the case of asymptotic dependence, Theorem 2 ensures that in the hypi semimetric. We may apply the reasoning above except that, from the definition of the process , we get the additional term

| (S1.9) |

this follows from the fact that under asymptotic dependence, is homogeneous of order 1 and the directional partial derivatives of such a function, when they exist, are constant along rays from the origin. The above term vanishes uniformly since has to be locally bounded (only under asymptotic dependence) and since the sample paths of are almost surely continuous. We therefore obtain Equation S1.8, except that this time the term is understood in the hypi semimetric. From here on the proof is completed in the same way as under asymptotic independence.

S1.1.4 Proof of Theorem 3

Recall the definition of from Section 3.2. Letting , the assumption that minimizes the norm of becomes equivalent to minimizing the norm of . The key is to note that for any ,

| (S1.10) |

with defined as in Theorems 1 and 2. By the dominated convergence theorem, and because is integrable, one easily sees that the functional is continuous in . By Lemma S10, this is also true in the topology of hypi-convergence on at points that are continuous Lebesgue-almost everywhere on . It is the case of both limiting Gaussian processes appearing in Theorems 1 and 2: , and have almost surely continuous sample paths and under asymptotic dependence, the directional derivatives are almost everywhere continuous. Those two results and the continuous mapping theorem then imply that

We may therefore apply Lemma S11 with , , and , and as required we obtain

S1.2 Spatial estimation

For the proofs in the spatial setting, we assume the framework of Section 3.3, we define the transformed random variables and for a pair , let be the distribution function of the random vector . Define the transformed observations and denote by the ordered versions thereof and define . For intermediate sequences , we define the (weighted) empirical tail quantile functions , , by

Recalling that , it allows us to write

where denotes the empirical distribution function of . Following the discussion before the proof of Theorem 1, we may define

and similarly obtain

| (S1.11) |

where is defined as in Theorem 4 and the term is uniform over compact sets.

S1.2.1 Proof of Theorem 4

For asymptotically independent pairs, the second term of Equation S1.11 vanishes uniformly, by the proof of Theorem 1. Define the -valued processes by

where . The proof now proceeds similarly to that of Theorem 2; we show that converges in distribution, that the processes of interest can be approximately represented as a transformation of , and we conclude by applying a continuous mapping theorem.

For , , let

Recall that denotes the identity mapping on . By standard arguments (see, e.g., the proofs of Theorems 1 and 2), we see that each of the processes and converge in distribution in , hence they are tight random elements in that space. It follows that the sequence of processes

| (S1.12) |

is tight in the product space . A Lindeberg-type condition (van der Vaart, 2000, Theorem 2.27) can easily be checked, so weak convergence of the process in Equation S1.12 follows from convergence of to a suitable covariance matrix. This is simply a consequence of Condition 2; indeed, for suitable pairs , and , this condition implies that

We deduce that in , the processes in Equation S1.12 weakly converge to the Gaussian process

as defined in Section 4.2. Noting that is the generalized inverse function of and that , we apply Vervaat’s lemma (Vervaat, 1972) to obtain that

| (S1.13) |

in .

Recall the definition of the sets in Equation S1.7 and let be the subset of functions of the form such that is constant in , is constant in and such that the functions and are elements of .

Defining as the product space , with equipped with the topology of hypi-convergence, consider the following functionals . For an element , is a function such that if , and

if . Referring to Equation S1.11 and recalling that the second term thereof vanishes if , we notice that for every pair , . This representation, of course, holds only if ; this is satisfied with probability at least

where the last convergence follows by Corollary S1 applied for each . Define , where is the subset of continuous functions such that , as

For a sequence that converges uniformly to a function , in . This can be seen by considering each pair separately; the result is obvious for asymptotically independent pairs, and for asymptotically dependent ones it follows from Lemma S9.

Finally, notice that the process concentrates on . Therefore, by Equation S1.13 and the extended continuous mapping theorem (van der Vaart and Wellner, 1996, Theorem 1.11.1),

in .

S1.2.2 Proof of Theorem 5

Similarly to the bivariate case, let

As in the proof of Theorem 3, we may deduce that for every pair , and ,

with as defined in Theorem 4. By a similar argument to the bivariate case (involving the dominated convergence theorem and Lemma S10 to establish continuity of the mapping , see the proof of Theorem 3 for the applicability of Lemma S10), Theorem 4 and the continuous mapping theorem yield

| (S1.14) |

The remaining proof consists of a number of successive applications of Lemma S11. We deal with each of the two estimators separately.

-

(i)

For each pair , applying Lemma S11 with , , and yields

(S1.15) where is the block corresponding to the pair in the matrix defined in Equation 4.4; its existence, as well as the required smoothness of , are guaranteed by Condition 3. Now redefining as , we see that is in fact a minimizer of the norm of , where is redefined as . Applying Lemma S11 again with and as above, and , we obtain

where the last equality follows from Equation S1.15 and is defined as in Section 4.2 in the paragraph below Equation 4.4. The conclusion that follows from this and Equation S1.14.

-

(ii)

Let . Once more, we redefine

The estimator can be seen to minimize the norm of . Therefore, applying Lemma S11 with and , we obtain

which, combined with Equation S1.14, implies .

S2 Technical results used in Section S1

Throughout the paper, particularly the proof of Lemma S2 below, we use (without reference when obvious) the following results on regularly varying functions at 0.

Lemma S1.

Suppose the functions and are regularly varying at 0 with indices and , respectively.

-

(i)

If (respectively ), (respectively ).

-

(ii)

For any , is –RV at 0.

-

(iii)

The product is –RV at 0.

-

(iv)

If , then is –RV at 0.

-

(v)

If , then is –RV at 0, where we define the generalized inverse of as

Proof.

The assertions (ii) and (iii) are trivial consequences of the definition of regular variation. As for (i), (iv) and (v), analogue versions for regularly varying functions at are proved in Proposition 0.8 of Resnick (1987). The proof can readily be adapted, using the fact that is –RV at 0 if and only if is –RV at .

∎

Lemma S2.

-

(i)

Assume Equation 3.1. Then there exists such that is a regularly varying (RV) function at 0 with index and is -homogeneous.

-

(ii)

Assume Condition 1(i) and suppose that is non-decreasing and that there exists such that as . Then Equation 3.1 holds locally uniformly on .

Remark S1.

In part (ii) of the previous result, the monotonicity condition on is artificial; it can be removed at the cost of replacing by the non-decreasing function . Indeed, if Condition 1 is satisfied with , it is trivially satisfied with . Moreover, if , also satisfies the same property.

Because is positive non-decreasing, that required property implies that holds for every (Bingham, Goldie and Teugels, 1987, Corollary 2.0.6). The function is then said to be -regularly varying at 0.

Proof.

-

(i)

Recall that we assume . For any , Equation 3.1 implies that and . This can be manipulated into

By Karamata’s characterization theorem (Bingham, Goldie and Teugels, 1987, Theorem 1.4.1), has to be –RV and , for some . However, since , we must have . Moreover, for any ,

Defining , this proves (i).

-

(ii)

For arbitrary , we write . We will prove that Equation 3.1 holds uniformly over all and over , for an arbitrary .

We have

(S2.1) First, the term is equal to uniformly in . In order to control the term , we note that since is -RV, there exists a slowly varying function such that for any ,

where we have used the fact that , which can be reversed into . The function is thus slowly varying with remainder (Bingham, Goldie and Teugels, 1987, Section 3.12). By theorem 3.12.1 of that book, the previous relation holds uniformly over all , so we henceforth focus on values . Using Theorem 3.12.2 of the same book (which we adapt for slow variation at 0), we obtain that for some constants and for small enough,

where the functions are real-valued, measurable and satisfy for some constant . The ratio becomes

As , we can use the monotonicity of to control the integral in the previous display:

Because , is lower bounded, so can be chosen large enough so that also upper bounds the absolute value of . Therefore, using the fact that for every , , we obtain

What we are interested in is bounding . This can be done by recalling that

(S2.2) By simple differentiation, it is straightforward to see that for a fixed value of small enough so that , the function is differentiable in its first argument and that

This suggests that the function attains its unique maximum at the point . Considering Equation S2.2, we obtain that for all ,

as , since and since the function is continuously differentiable at 0. Finally, this allows us to rewrite Equation S2.1 as

and the last equation holds uniformly over and . The proof is over since .

∎

Lemma S3.

Let be a non-decreasing function such that as and assume there exists such that

Then under the assumptions of Theorem 1, for every we have

where is defined as in Section S1.1. In particular, note that , as well as any function that satisfies in a neighborhood of 0, are valid choices.

Proof.

This is essentially proved in Csörgő and Horváth (1987), up to a slight difference between their definition of the quantiles and ours. We prove here that this difference does not change the result. More precisely, their Theorem 2.6 (ii) states that

| (S2.3) |

where we denote what they call (to avoid confusion with our definitions). From their definitions, one easily sees that

Then, by the reverse triangle inequality,

Using this and the inequality , we have

| (S2.4) |

In the first term, since and , we must have . Therefore, we end up studying , for some . It is a well known fact that those differences, regardless of the value of , have a Beta distribution with parameters 1 and . In particular, they are both . It follows that the first supremum on the right hand side of Equation S2.4 is asymptotically bounded in probability by

by assumption on . As for the second term in Equation S2.4, it is equal to

after shifting to the right by . Using Equation S2.3, this is in turn equal to

once again by the properties of . We have shown that the difference between the quantity we are interested in and the term appearing in Equation S2.3 is . We may thus conclude, by Equation S2.3, that

∎

Corollary S1.

Proof.

Note that by definition, whenever . It follows that

This is by the preceding Lemma S3 with the function . The same proof holds with replaced by .

∎

Lemma S4.

Under Condition 1 the process as defined in Equation S1.1 converges to the process from Theorem 1 in .

Proof.

Denoting , we see that can be written as

Therefore, convergence of the process to a Gaussian process in is equivalent to checking that the sequence of function classes

are Donsker classes for the distribution of . This is guaranteed by Theorem 11.20 of Kosorok (2008), provided that we can check the six conditions. Note that admits the envelope function .

-

(0)

First, the AMS condition is trivially satisfied; by right continuity of indicator functions, for any , and ,

It follows that Equation (11.7) of Kosorok (2008) is satisfied with , which is countable. Hence the classes are AMS.

-

(A)

For every , it is easily checked that is a VC class with VC-index 2. Therefore, condition (A) is a direct consequence of Lemma 11.21 of Kosorok (2008).

-

(B)

For arbitrary, it follows from the definition of that