Instrument variable detection with graph learning : an application to high dimensional GIS-census data for house pricing

Abstract

Endogeneity bias and instrument variable validation have always been important topics in statistics and econometrics. In the era of big data, such issues typically combine with dimensionality issues and, hence, require even more attention. In this paper, we merge two well-known tools from machine learning and biostatistics—variable selection algorithms and probablistic graphs—to estimate house prices and the corresponding causal structure using 2010 data on Sydney. The estimation uses a 200-gigabyte ultrahigh dimensional database consisting of local school data, GIS information, census data, house characteristics and other socio-economic records. Using ”big data”, we show that it is possible to perform a data-driven instrument selection efficiently and purge out the invalid instruments. Our approach improves the sparsity of variable selection, stability and robustness in the presence of high dimensionality, complicated causal structures and the consequent multicollinearity, and recovers a sparse and intuitive causal structure. The approach also reveals an efficiency and effectiveness in endogeneity detection, instrument validation, weak instrument pruning and the selection of valid instruments. From the perspective of machine learning, the estimation results both align with and confirms the facts of Sydney house market, the classical economic theories and the previous findings of simultaneous equations modeling. Moreover, the estimation results are consistent with and supported by classical econometric tools such as two-stage least square regression and different instrument tests. All the code may be found at https://github.com/isaac2math/solar_graph_learning.

keywords:

T1Xu would like to thank Google Australia and NICTA for hardware and programming assistance in package optimization and development. Xu also would like to thank Dr. Peter Exterkate, Uni Sydney and Prof. A. Colin Cameron, UC Davis for their valuable advice.Fisher would like to acknowledge the financial support of the Australian Research Council grant DP0663477.

and

1 Introduction

Endogeneity bias has long been a problem in causal analysis and has for decades been a focus of research by statisticians, econometricians and biostatisticians. With the ongoing increases in dimensionality, the topic requires more attention than ever. On the one hand, we seem to have more information, which raises the potential to observe and rectify endogeneity bias by finding a valid instrumental variable (referred to as instrument for short); on the other hand, the problem is complicated by the curse of high dimensionality and the consequent complication of dependence structures. Thus, it is important to investigate how best to utilise high-dimensional data for endogeneity detection and instrument selection while minimizing the curse of dimensionality. In this paper, we combine two theoretically well-founded machine learning and biostatistical tools—variable selection and random graph estimation—and demonstrate that the combination performs admirably in endogeneity detection and instrument selection in the presence of ultrahigh dimensional data.

In causal analysis, Pearl (2009, 246) shows that there are three definitions of a valid instrument: graphical criteria, error-based criteria and counterfactual criteria, where the graphical criteria implies the error-based criteria. Classical regression analysis relies mostly on the error-based criteria. In econometrics, the instrument is typically defined by the data-generating process

| (1.1) |

where are noise terms, cause , cause and is endogenous.111Unfortunately the causation assumption cannot be dropped; otherwise, endogeneity will inevitably arise. See Appendix LABEL:App:IV_def. For the validity of an instrument , we typically require

-

C1

, and

-

C2

in the population.

C1 implies that changes in cannot affect , further implying that changes in cannot affect via . C2 implies that changes in can affect , further implying that changes in can affect via . C1 and C2 together mean that can only impact via .

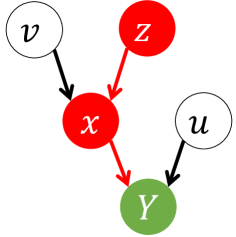

The idea of an instrument can be generalized using probabilistic graph models (also called Bayes nets or causal networks). In probabilistic graph models, the causal structure in (1.1) can be expressed equivalently by a directed acyclic graph (graph for short) as in Figure 1.222There are several notation systems for graphs. Throughout the paper we follow the notation in Koller and Friedman (2009). In much research on causal inference (e.g., Spirtes et al. (2000b, p44)), causal structure is directly defined using graphs that visually represent the causal relationships between variables.

A useful analog to a graph is a family tree, where family members (variables) are connected by arrows representing parentage (causation). In Figure 1, the arrows from to mean that and directly cause , further implying that . Analogously, we say that are the parents of , is the child of and is a spouse of . In Figure 1, directly causes and, hence, indirectly causes . The variables that directly or indirectly cause are the ancestors of . Hence, and are the descendants of . Lastly, two variables are siblings if they share the same parents.333See Koller and Friedman (2009, Section 2.2) for further detail on the terminology.

In statistics and biostatistics, causal inference is typically conducted via two stages. The first stage is to estimate the causal structure of the key variable (such as finding all its parents, children and spouses). Based on the estimated causal structure, we estimate the magnitude of the causal effects from or to . As one of the most popular tool for structure estimation, graph learning provides unparalleled clarity on the causal structure specification. As a result, graph learning is typically considered critical for the accuracy and stability of the causal inference result. Failure to learn an accurate graph may result in different kind of estimation biases and cause a number of consequential problems, such as endogeneity, multicollinearity and misinterpretation. We illustrate this point using the following three examples.

Motivating examples

Field knowledge and experience are frequently relied on when constructing the causal structure in empirical researches. However, if field knowledge is incomplete, unclear or partially misspecified, it may cause a series of problems for causal inference. In the following examples, we demonstrate that even a very small problem on causal structure specification can cause severe problems. Specifically, example 1 shows that correct causal inference relies on the temporal order of variable, e.g., when the value of a variable is determined.

Example 1. In both numerical and theoretical analysis of linear regression, typically — the parent of — is on the right-hand side of the equation and is on the left. Such variable allocation is consistent with the order of time stamps — the ancestor(s) on the right and its descendant on the left; moreover, it reflects the fact that, during the data generating procedure, has to be generated first to determine the value of the child variable . However, in empirical analysis, field knowledge may fail to provide the detailed temporal order of variables. For example, suppose the true causal structure appears as in Figure 2,

reflecting the data-generating process

| (1.2) |

where , and are vectors; both and cause ; is independent from . Clearly, (1.2) implies that, in order to determin the value of , the values of ’s parents — and — must be determined first. Suppose that (i) the field knowledge confirms that and does have a causal relation; (ii) the field knowledge is not clear on which variable is generated first. Due to the fact that is the variable of interests, will typically be chosen as the response variable. Hence, the empirical model is

| (1.3) |

with , and . Thus, and (1.3) suffers from endogeneity. Worse, by mistaking the parent () to be a child, the causal structure in (1.3) is completely wrong. In this case, it would be very difficult to find an instrument to solve the problem. As a result, either the model is set up correctly by the temporal order, or it will be contaminated by endogeneity; there is hardly any middle ground. ∎

Example 1 illustrates the importance of specifying the correct parent-child relation in a graph. Such problem referred to as Markov equivalence in graph learning, which will be detailedly discussed in latter sections. Statistical tools (like information criteria and tests) can verify whether there is likely to be a non-zero population correction between and ; however, without further information, they cannot identify whether causes or the other way around. To avoid such misspecification, one method is to collect the ‘time stamp’ of each variable (when the value of a variable is determined) and order variables temporally. This requires that we should collect all the details about each variable. However, the time stamp issue is only part of the possible problems for inaccurate causal structure estimation. In Example 2, we demonstrate that, without an accurate graph, the causal inference procedure may be misled into a wrong track and never returns the true result.

Example 2. In regression analysis, it is well-known that regression coefficient estimates will be biased and inconsistent if an important covariate is omitted. To avoid omitted variable bias, it is often recommended (for example, Pratt and Schlaifer (1988)) that investigators enlarge the set of potential covariates and control more variables. In this example, we demonstrate that this may also cause problems in causal inference.

Assume that the data are generated by the causal structure in Figure 1 and that the data generating process is (1.1). Suppose that we want to investigate the causal effect from to . Unfortunately, if we include in the regression equation to avoid omission variable bias and set the equation as

| (1.4) |

we may never have an accurate inference on the causal effect from to . As shown in Figure 1, , implying there is an indirect causal relation from to via . However, if we include in our regression, the value of will be controlled when you investigate the relation between to . This implies that cannot affect the value of and, hence, . As a result, will not be significant in the regression equation and we may wrongly conclude that has no causal effect on .

Worse, in empirical analysis, the culprit is likely to be mistaken from the persepctive of multicollinearity rather than a wrong causal structure. Noticing the high correlation between and , some may wonder whether there is an omitted confounder for and , resulting in an even larger control variable set; some may be misled and focus on improving the robustness of the regression instead of reconsidering the causal structure that the regression equation implies. Essentially, an increase in sample size or regression with robust standard errors may address multicollinearity issue only if the underlying causal structure of the regression equation is correct. By contrast, the source of the problem here is that ‘we control a variable that we should not’. In this case, if we want to use single-equation OLS to correctly measure the magnitude of the causal effect from to , the only solution is that we remove from the equation.∎

Example 2 clearly reveals that, similar to variable omission, redundant variables may also be a severe problem for the causal effect estimation. Put it another way, ”control a wrong variable” and ”control too few” are both problematic. To avoid the latter and the consequential omission variable bias, we typically focus on enlarging the set of control variables; however, such strategy is meaningful only if we know the correct causal structure in advance, which will prevent controlling a ‘wrong’ variable like example 2. As a result, a systematic causal structure estimation needs to be done before measuring the magnitude of the causal effect in OLS, implying that a careful selection of variables is necessary.

Moreover, different sets of control variables are required under different scenarios. In example 2, you only need to include the parents of if you are interested in the direct (causal) effect to ; by contrast, you need to drop all the parents of from the regression equation if you aim to measure the indirect effect from ’s grandparents. This implies that, to well serve causal inference, an accurate graph is highly recommended. If learning the graph globally is impossible, at least we need variable selection algorithms to identify ’s parents, spouses and children (whom directly causes or is directly caused by). As a result, careful use of the selection algorithm is required well, especially for high dimensional data with complicated causal structure. Otherwise, variable selection algorithm may be misled and produce wrong causal structures, which may render the estimated structure unusable. Using the popular lasso algorithm in example 3, we demonstrate numerically the difficulty of correctly identifying the parents of in the presence of a strong confounding effect and demonstrate how it causes problems on causal structure estimation. For precision and conciseness, we follow Zhao and Yu (2006); Tibshirani et al. (2012) and quantify the difficulty of correctly identifying parents with the well-known irrepresentable condition (IRC).

Example 3.(Zhao and Yu, 2006) Assume the data-generating process is

| (1.5) |

where all variables are Gaussian; , , , , and are standardized vectors; and are independent from . The causal structure shows that are the common parents of , which are siblings. In this example, we try to use lasso to find the parents of .

The IRC states that, for variable selection accuracy in lasso (i.e., selecting and dropping in this case), . Otherwise, with a large probability, lasso-type estimators will take the sibling of to be a parent (see the last simulation in Xu et al. (2019) for detail). Worse, if a group of variables are highly correlated with one another, Zou and Hastie (2005) shows that lasso may randomly drop variables from the group (referred to as the grouping effect), making the variable selection process extremely sensitive to sampling randomness. As a result, lasso may wrongly include the sibling as a parent or dump the true parent and .

The consequnce of a wrong selection result is well beyond the variable redundancy in regression equations. There will be carried-on erros that can render the whole structure misspecified. In this example, if the variable selection algorithm mistake the sibling of as its parent, all the children of the — the true nephews of — are consequently mistaken as ’s siblings; if the variable selection algorithm mistake a parent of (say ) redundant, all the ancestors of the — the true ancestors of and the variables indirectly causing — are consequently mistaken as redundant as well.

The ultimate consequnce is that, if a causal structure is misspecified, the succeeding statistical decisions regarding will all be biased, such as selecting instrument variables, estimating the magnitude of a causal effect, prediction and forecast. Moreover, this also leads to difficulties with model interpretation and understanding. ∎

As shown in example 3, we need to mitigate the caveats of traditional lasso estimator in empirical applications with severe multicollinearity or a complicated causal structure. To improve variable selection accuracy and robustness, we follow Xu et al. (2019) and apply the novel subsample-ordered least-angle regression algorithm (solar) instead. Solar is derived from least-angle regression (Efron et al., 2004) and significantly outperforms lasso in terms of sparsity and variable-selection accuracy on data with severe multicollinearity and complicated causal structures. In particular, Xu et al. (2019) shows that, unlike lasso, solar maintains variable selection robustness when IRC fails.

All previous examples shows that causal inference requires well thoughts, detailed ‘big data’ with enough variables and time stamps, an accurate causal structure and a robust variables selection result that tolerates high dimensionality and multicollinearity caused by complicated causal structures. In this paper, we carefully pick all the tools that satisfy the requirements above and assemble them as a data-driven method to select and validate instrument variables in high dimensional data.

1.1 Literature review on graphical causal inference, graph learning and variable selection

Causal inference based on probabilistic graphs learning

Implementing a data-driven causal inference has been a central topic in machine learning and biostatistics for decades. Verma and Pearl (1990) pioneered the use of graphs to analyze causal structure in the 1980s and summarize all the corresponding researches in Pearl (2009). Building on that, Spirtes et al. (2000b, p197) consider causal inference from the joint perspectives of graph learning and regression analysis. Both Pearl (2009) and Spirtes et al. (2000b) investigate the definition of instrument variables from the perspective of graph and show that it is implies that classical definition based on regression error. They illustrates that, as a special case of causal analysis, (i) the classical linear regression model typically assumes an oversimplified causal structure; (ii) regression can be easily misled by the complexity of causal structures in real-world data. As a result, it may not be reliable to estimate the magnitude of the causal effect using linear regression without verifying the causal structures. Overall, to correctly estimate the causal effect magnitude, these researches recommend graphs for learning causal structure data-driven in advance. Building on that, classical machine learning and biostatistics researches (for example, (Brito and Pearl, 2002; Kuroki and Cai, 2005; Chu et al., 2013; Silva and Shimizu, 2017)) show that joint distributions alone are insufficient to determine whether an observable variable is a valid instrument, which is affected by a phenomenon called Markov equivalence and can be solved by finding the time stamps of each variable. Also, without specifying the time stamps, the researches still show that instrument variable assumptions can nevertheless be falsified by exploiting constraints in the joint distribution of multiple observable variables. The relevant algorithms are combinatorial and consequently requires huge computation loads even though the dimensionality of the data is not large. As a result, graphically causal inference would benefit deeply from a quick and accurate graph learning algorithm.

Graph learning are typically based on two methods : constraint-based learning and score-based learning (see, e.g., (Scutari and Denis, 2014)). To find a correct graph, constraint-based learning assumes a distribution on the joint distribution of all variables and carries out all conditional and marginal dependence tests among every possible pairs of variables. When testing the dependence between two variables, the constraint-based learning is senstive to the variables conditioned on. Also, this methods is combinatorially exhaustive and typically cost great computation loads when the dimensionality is large. By constrast, score-based learning computes an information criterion score (such as AIC, BIC, BGE score) for a given graph, selecting the graph with the minimal information criterion score. Score-based learning can be carried out using different packages (e.g., the R package bnlearn or the Python package pgmpy). Based on score-based and constraint-based learning, different algorithms are created. Typical constraint-based algorithms include Peter-Clark (PC) and Fast Causal Inference (FCI) (Spirtes et al., 2000a). PC assumes that there is no confounder (unobserved direct common cause of two variables), and its discovered causal information is asymptotically correct. FCI gives asymptotically correct results even in the presence of confounders. Such approaches are widely applicable because they can handle various types of data distributions and causal relations, given reliable conditional independence testing methods. However, they do not necessarily provide complete causal information because they output Markov equivalence classes, i.e., a set of causal structures satisfying the same conditional independences. The PC and FCI algorithms produce graphical representations of these equivalence classes. In cases without confounders, there also exist score-based algorithms that aim to find the causal structure by optimizing a properly defined score function. Among them, Greedy Equivalence Search (GES) (Chickering, 2002) is a well-known two-phase procedure that directly searches over the space of equivalence classes. To reduce the computation load of score-based learning, researchers in machine learning and biostatistics typically assume the jointly distribution is Gaussian and the dependence among variables are all linear, which implies a linear Gaussian graph (e.g., Bollen (1989); Geiger and Heckerman (1994); Spirtes et al. (2000b)) and later on is generalized as a linear non-Gaussian graph (e.g., Shimizu et al. (2006)) and a nonlinear non-Gaussian graph (e.g., Hoyer et al. (2008)).

Variable selection and corresponding issues in linear graph learning

In empirical researches, a graph learning task typically starts from linear graph learning (e.g., Bollen (1989); Geiger and Heckerman (1994); Spirtes et al. (2000b); Friedman et al. (2008)). Compared with nonlinear graphs on the same dataset, linear graphs requires much less computation load and is easier for inference. Also, linear graph is deeply related to linear modelling methods like linear regression, best subset variable selection, shrinkage and lasso. Only if linearity cannot approximate the dependency in the data, researchers apply nonlinear dependence measure like Hilbert Schmidt independence criterion (Gretton et al., 2005) and mutual information.

As a major issue in linear graph learning, multicollinearity is frequently observed among variables with complicated causal structures, which will cause several problems for the parameter estimation in both linear modelling and linear graph learning. First, since linear model estimation is based on error minimization, multicollinearity will reduce the magnitude of the minimal eigenvalue in the linear space, causing numerical convergence problems (e.g., Cholesky decomposition or gradient descent) when applying maximum liklihood or maximum a posteriori. Second, severe multicollinearity amplifies parameter estimate instability across samples, making it difficult to interpret the coefficients reliably and accurately. Third, multicollinearity causes problems for statistical tests that rely on the sample covariance (e.g., the post-OLS t-test or the lasso covariance test (Lockhart et al., 2014). The conditional correlation tests of in constraint-based learning (Farrar and Glauber, 1967)). Last but not least, multicollinearity may also reduce the algorithmic stability of the model (Elisseeff et al., 2003), which reduces the generalization ability and the out-of-sample prediction of the estimated model.

Moreover, multicollinearity also affects the reliability of variable selection algorithms in linear modelling and linear graph learning. Zou and Hastie (2005); Jia and Yu (2010) find that, if a group of variables are highly correlated with one another, lasso-type estimators may randomly select one variable from the group and drop the others out of the regression, referred to as the grouping effect. Since all linear modelling techniques make the variable selection decision based on the conditional correlation between and , the grouping effect may well apply to all variable selection methods in linear models. Multicollinearity also affect linear graph learning. Heckerman et al. (1995); Chickering et al. (2004) shows that learning a linear graph is NP-hard on data with large . As a result, graph learning algorithms typically work well on data with large and very sparse . In many graph learning applications, variable selection algorithms (e.g., SCAD (Fan and Li, 2001), ISIS (Fan and Lv, 2008) or different lasso-type estimators (Fan et al., 2009)) are used to filter out redundant variables before graph learning. As a result, with grouping effect, variable selection methods may randomly drop some of the highly correlated variables, resulting in omissions of important variables in the linear graph learning.

Many attempts have been made to reduce the effects of multicollinearity. For more stable regression coefficient estimates, Hoerl and Kennard (1970) apply Tikhonov regularization to OLS, resulting in the ridge regression. However, it complicates statistical tests and post-estimation inference. To reduce the grouping effect and obtain stable variable-selection results, cross-validated group lasso and cross-validated elastic net (CV-en) have been introduced (Zou and Hastie, 2005; Friedman et al., 2010). However, group lasso relies on manual grouping of variables, which depends heavily on accurate field knowledge. On the other hand, while Zou and Hastie (2005) and Jia and Yu (2010) show that CV-en may improve the stability of variable selection, Jia and Yu (2010) counter that the improvement is marginal and that “when the lasso does not select the true model, it is more likely that the elastic net does not select the true model either.”

1.2 Main results

In this paper we combine two well-known tools from machine learning and biostatistics—variable selection algorithms and graph learning—and apply them to estimate the causal structure of the housing market and the follow-up socio-economic effects using data for 2010 from Sydney, Australia. It is an ultrahigh dimensional database consisting of local education data, GIS information, census data, house characteristics and other socio-economic records. We show that, with ”big data”, it is possible to perform a data-driven instrument selection efficiently and purge out the invalid instruments. The estimated graph of the causal structure of the housing market provides an intuitive interpretation and matches the facts of the Sydney house market, economic theories and the previous empirical findings on house pricing. The estimated graph also returns an accurate and sparse house pricing model, outmatching other methods in terms of the bias-variance trade-off.

The estimated graph visually depicts the causal structure of house pricing dynamics. Using the graph, we detect endogeneity in house prices, which is confirmed by simultaneous equations modelling. The graph estimation method therefore represents a data-driven, as opposed to ad hoc, approach to detecting endogeneity. Furthermore, we are able to use the graph effectively and efficiently for instrument selection and validation, which are confirmed by traditional instrument tests from Durbin, Wooldridge and Hausman. Moreover, using the graph-recommended instrument, we significantly resolve endogeneity bias in the house price regression, which is confirmed by two-stage least squares. Last but not least, the graph estimation method also helps to identify a weak instrument, which is consistent with economic intuition.

The paper is organized as follows. In section 2, we introduce variable and instrument selection from the perspective of the random graph. In section 3, we introduce the 2010 Sydney house data and demonstrate in detail the procedure of variable selection and graph estimation using the data. In section 5, we use the estimation results for endogeneity detection and instrument selection. We also show that our graph-based results are consistent with received empirical knowledge on the housing market.

2 Graph and instrument variable selection

Before applying graphs for instrument variable selection and causal inference, it is important to introduce graphs and the graphical definition of instrument variables properly. Graph learning terminologies are defined differently across different areas. To consistent with the literature in machine learning, the following definitions and explanations on graph and instrument variables are based on Spirtes et al. (2000b), Pearl (2009) and Koller and Friedman (2009).

2.1 Graphical criteria for instrument variables

To properly define an instrument variable using graphs, we need first to define how the change in one variable can affect another in a graph. This is represented by the concept of a trail.444This is also referred to as “path” in some graph learning literature

Definition 2.1 (Trail of a graph).

-

•

for any pair of variables in a graph, we say that they are connected () if either or ( and have a parent-child relation).

-

•

for variables in a graph, we say that they form a trail if, , .

Intuitively, a trail is a sequence of variables that are sequentially connected by arrows. A change in can affect only if there is a trail between the two variables. Put it from the perspective of joint distribution, if there exists a trail between and , either the unconditional or some conditional correlation between and is not zero in population. In Figure 1, for example, is a trail, meaning a change in can be passed to if is not conditioned on; or, equivalently, the correlation between and is not zero if we do not condition on . In Figure 1 and (1.1), is also a trail, meaning a change in can pass to only if (i) is held constant and (ii) is not fixed; from the perspective of correlation, and are correlated when is held constant and is not.

In the examples above, plays a key role in the trails. If is held constant, the population correlation between and will be zero. As a result, any change in a variable at one end of the trail cannot affect the variable on the other end, which is the mistake that we make in example 2. To describe the role of variables like , we say the variables at both ends of the trail are d-separated by .555This is also referred to as “the variables at both ends of the trail are blocked by ” in some graph learning literature

Definition 2.2 (d-separation).

Let be a trail from the variable to the variable . We define and to be d-separated by a set of variables (denoted by ) if and are independent after conditioning on all variables in .

For example, by in the following cases.

-

•

contains a directed chain ( or ) such that the middle variable ;

-

•

contains a fork () such that the middle variable ;

-

•

contains a collider () such that the middle variable and no descendant of is in .

We also introduce two useful remarks for d-separation. Firstly, if directly causes (i.e., ) with no intermediate variables, and will never be independent regardless of the variable conditioned on (except and ). In this case, we say that no variable can d-separate and (sometimes denoted ). Secondly, as illustrated in Figure 4, if and have no causal relation whatsoever, we say any variable (for example, variable ) can d-separate and (sometimes denoted ). Using the concept of d-separation, the graphical definition of an instrument can be precisely defined, following Brito and Pearl (2002), Pearl (2009) and Silva and Shimizu (2017), and illustrated in Figure 5.666As shown by Brito and Pearl (2002) and Pearl (2009, pp. 247-248), the complete set of graphical criteria for an instrument is more complicated than our definition as it incorporates the idea of conditional instruments in a graph. To avoid being sidetracked, we leave further discussion to Appendix LABEL:App:IV_def.

Definition 2.3 (Graphical criteria of instruments).

Let and be variables in graph and directly causes . is an instrument for if

-

G1

and can be d-separated by any variable in , where is the graph in which the effect from to is cut off (sometimes denoted ).

-

G2

and cannot be d-separated by any variable in (sometimes denoted ).

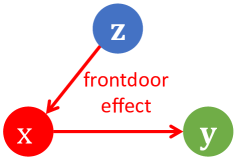

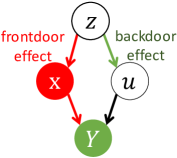

Graphically, G1 means that, if we remove all the causal effects from to , cannot affect any more.777Sometimes, G1 is modified to , where is obtained by removing all the arrows entering from the graph , but Definition 2.3 is the more common definition of instrument. Nonetheless, both versions mean that the effect from to must go only through . Similarly, G2 means that the effect from to cannot be broken by holding any variable constant. Both G1 and G2 mean that the effect from to must go only through . Put another way, holding constant, cannot affect by any means. In graph learning, the effect from to via the (endogenous) variable is also referred to as the frontdoor effect (FE) (Figure 5a). Moreover, Definition 2.3 is a generalized version of the usual definition of an instrument in regression analysis. Assuming that causes in (1.1), implies the existence of an FE. Likewise, implies there does not exist any effect from to that does not go through (also referred to as no backdoor effect (BE)).888In other graph learning literature (Pearl (2009), for example), this is also referred to as “ satistfies the ‘no backdoor criterion’ for the causal effect between and ”

The classical machine learning and biostatistics researches (for example, Spirtes et al. (2000b) and Pearl (2009)) show that definition 2.3 (aka the graphical criteria of instrument variables) implies the classical definition based on regression error, which is also referred to as the error-based criteria of instrument variables. For more detailed analysis and examples, see Appendix LABEL:App:IV_def.

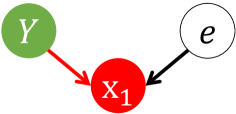

As Spirtes et al. (2000b) and Pearl (2009) show, Definition 2.3 can be used to identify instruments variables in a graph. Take Figure 6 as an example. A classical case in econometrics, Figure 6 contains an arrow from to . As a result, in (1.1), implying is not a valid instrument. Equivalently, the arrow from to allows to affect separately from the endogenous variable , which is a BE. As a result, Figure 6 violates G1 since and are not independent even though is held constant.

2.2 Variable selection for graph learning

Figure 5 and Appendix LABEL:App:IV_def reveals the unparalleled advantage of the graph on instrument variable selection. If we can accurately estimate the graph (or at least estimate the role of each variable relative to ), choosing an appropriate instrumental variable is straightforward. Hence, an accurate graph estimation is the core of data-drive causal inference. As example 2 and 3 illustrate, variable omission and variable redundancy can both mislead the graph learning and, consequently, causal inference. To avoid variable omission, it is always safe to start graph learning from ”big data” — a dataset that contains as many relevant variables as possible. Unfortunately, minimizing the chance of variable omission may bring a large number of potential variables in your graph, raising the issues of dimensionality and computation. Dimensionality and computation aside, including redundant variables may cause problems in example 2 and 3 and return misleading and counterintuitive results. Hence, it is necessary to accompany graph learning with variable selection (aka variable elimination).

To build the connection between variable selection and regression-based causal inference, in this paper we follow the common linearity assumptions (e.g., Bollen (1989); Geiger and Heckerman (1994); Spirtes et al. (2000b)) as follows,

-

A1

the data generating process of each variable can be represented as a linear regression equation;

-

A2

the dependencies among variables can be represented by correlation (e.g., (1.1)).

Both A1 and A2 imply that the causal structure is linear or, equivalently, we have a linear graph in population. It is worth noting that we do not assume that the linear equation is a perfect representation of the data generating process. In fact, it is quite common for linear models to suffer misspecification, especially if we are not sure about the linearity of the data-generating process. Hence, in this paper, we start graph learning from linear graph and always check the appropriateness of linearity assumption when we get the result. If linearity is not appropriate in some case, we will add nonlinearity pattern (e.g., neural network, kernel regression in reproducing kernel Hilbert spaces) into the graph learning.

With A1 and A2, all graphs in this paper are linear graphs and graph learning can be comprehended from the perspective of high-dimensional regression analysis. In classical regression analysis, significance test and variable selection algorithms are applied to find the variables with non-zero population coefficients. A regression coefficient represents the conditional correlation between the corresponding covariate and the response variable, holding other covariates constant. As a result, variable selection algorithms aim to find the variables that are conditionally correlated to in the population, holding all other variables constant.999After standardizing the response variable and all covariates, the regression coefficient of is the conditional correlation between and , holding all other covariates constant. In graph learning, the set of such variable is called Markov blanket of (denoted MB()), which includes the parent(s), children and spouse(s) of . Hence, in linear graphs, recovering the MB() is equivalent to finding true variables in the linear regression of on all other variables, illustrated graphically in Figure 7 and analysed with example 4.101010For a more general explanation and examples, see Pearl (2009), Koller and Friedman (2009) or Scutari and Denis (2014).

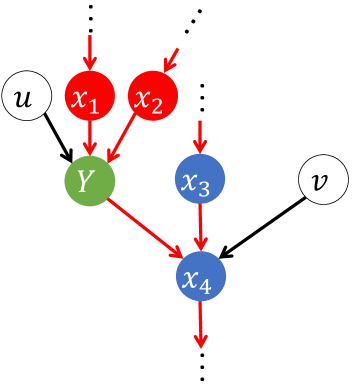

Example 4. In Figure 7, and are independent latent noise terms; are the parents of ; are the spouses of ; together cause . Together with A1 and A2, the data-generating process in Figure 7 is the following linear regression system,

| (2.1) |

Holding constant, (2.1) shows that all the variation in is caused only by (mathematically, ). Put another way, after partialing out from , the variation in can be explained by the children of . As a result, the independence between and and the second equation of (2.1) imply that

| (2.2) |

After replacing in (2.1) with the right-hand side of (2.2), the data generating process of — first equation in (2.1) — reduces to the following population regression equation of on its MB members,

| (2.3) |

where is a linear function of . Hence, Equation (2.3) is the population reduced form of the linear system (2.1), where only MB variables are informative (or true) variables.∎

Example 4 means that, when we apply the variable selection algorithm on Equation (2.3) with enough sample size, a consistent variable selector (for example, lasso-type estimators and SCAD) should keep only and purge out all other variables. Zhao and Yu (2006) show that the irrepresentable condition almost surely guarantees the variable selection consistency of lasso. This implies that, with irrepresentable condition, it is very likely that lasso only select the true variables in Equation (2.3) — the MB members of — with small enough . As a result, in linear graphs, variable selection for the regression of is equivalent to finding the MB of . Having said that, due to the complicated causal structure, variables in the graph may be heavily correlated. As a result, when applying lasso-type estimators in a graph, we need to always check correlation between the selected variables and dropped variables in order to detect potential violation of the irrepresentable condition.

Finding the correct Markov Blanket of a variable is important for graph learning. In graph learning, both score-based and constraint-based learning works combinatorially, which require huge computation load. As a result, the classical graph learning algorithm do not work well when dimensionality is high. However, after purging as many redundant variables as possible from the Markov blanket, the possible combination number of causal effects from and to will be reduced exponentially. As a result, accurate Markov Blanket estimation makes graph learning easy and quick, which further faciliates causal inference and instrument variable selection on .

3 Graph estimation on Sydney house market data

In this section, we prepare the Sydney real estate database for graph learning and causal inference. In the classical applied econometrics, the house price is typically explained by easily-measured attributes (e.g., the number of bedrooms, bathrooms, land size, distance to amenities, etc.) using a linear regression equation. To avoid the possible variable omission bias, our database includes as much objective information that is relevant to the market value of particular a house, much of which, of course, is determined by the location of the property, its unique features, and the characteristics of the neighbourhood. With a ”big data” database, we apply the variable selection algorihtm to the database and try to find as many Markove blanket memebers of house price as possible.

3.1 Description and sources of databases and primitive variable elimination

The house market database is assembled from more than 10 different datasets, including 2010 Sydney house transaction data (including every 2010 sale of a house in City, Mid, North, South and East Sydney as well as all house features), 2010 and 2011 Sydney crime data by suburb, 2010 GIS data (extracted and complied from Sydney geospatial topological database, climate database, pollution database and Google Maps database), 2011 census data by Statistical Area Level 1 (SA1, the smallest census area in Australia, which have an average population size of approximately 200 people or, equivalently, 60 households), 2009 local school quality and catchment data, 2010 Sydney traffic data, data on public transport (train stations, ferry docks and bus routes), and so on. To speed up computation and data manipulation, we synthesize all databases using Aparche Spark on the Google Cloud. Altogether, the total variable number is above 10 thousands, the observations number is above 10 thousands and the size of the database is above 200GB. Due to the size of the synthesized database, we do not attach it in this paper.

The variables in the databases are collected from different sources. Some house features are reported in real-estate advertising and others are scraped from Google searches using a Python internet scraper; the distance of each house to nearest key locations is computed in QGIS—a open-source Python-based geographical information system—using the GPS location of each house and geodata collected from Google Maps and Department of Land and Natural Resources, New South Wales. The 2009 Index of Community Socio-Educational Advantage (ICSEA) score—an measure of the socio-educational background of students at each school—is collected from the Australian Curriculum, Assessment and Reporting Authority (ACARA). The variables on local school quality (average National Assessment Program – Literacy and Numeracy (NAPLAN) examination results) are also collected from ACARA. The 2009 and 2010 crime data are collected from the Australian Bureau of Statistics and Department of Justice, New South Wales. The 2011 census data, traffic data, climate data, geospatial topological database and pollution database are acquired from the Australian Bureau of Statistics. It is also worth noting that all the socio-economic data are observed by SA1, the smallest statistic area in 2011 census. Each SA1 in our data contains typically around 200 local residents. Most important, to avoid Simpson’s paradox, in QGIS we only incorporate the SA1 that only covers houses, which rule out other types of real estate like apartments.111111In other graph learning literature, Simpson’s paradoxis also referred to as Simpson’s reversal or reversal paradox. For example, see Simpson (1951) and Blyth (1972). The detailed variable list is attached at Appedix 2 as a csv file.

As explained in literature review, graph learning and MB selection typically work well on datasets with small . However, our dataset has and both larger than 10000. Not only is that well above the computation limit of graph learning but, with such high dimensionality, there are likely to be many variables irrelevant to the MB of house price. As a result, following Fan and Lv (2008), we conduct variable selection in two stages to reduce dimensionality from high to a moderate scale that is below the sample size. As the primitive stage, we use iterative sure independence screening (ISIS, Fan and Lv (2008)) and rule out variables whose conditional correlation to house prices are, ceteris paribus, approximately . Using the variables that survive ISIS, we execute detailed variable selection and use the corresponding results for MB selection and graph learning.

To control the effect of high dimnesionality and sampling randomness, we embed ISIS into the framework of boostrap. The detailed step of ISIS is explained as follows. Firstly, we generate 2000 bootstrap samples. On each bootstrap sample, we run ISIS directly to select the variables that are highly correlated to house price. The ISIS is stopped based on BIC minimization. After obtaining 2000 ISIS results, we average them and select the variables that is at least selected in 70% of 2000 results. The last step is, considering the huge multicollinearity among variables that may render the selection result unstable, we also include the variables that are moderately correlated with the variable selected in last step. For example, only the year 3 mean reading score and year 5 numeracy score are selected by ISIS. Considering the possible grouping effect among mean scores of local school, we include them all. After conducting the ISIS variable elimination directly on Google Cloud, the variables that survive ISIS are returned as the first column of Table 1. As shown in the table, the 57 variables that survive SIS fall into 5 categories: features of the house, distances to key locations (public transport, shopping, etc.), neighbourhood socio-economic data, localized administrative and crime data, and local school quality. Pairwise correlations among all 57 covariates indicate that, not surprisingly, multicollinearity and the grouping effect are present in the data.121212Due to the large number of covariates, we report the correlations in supplementary files. Thus, we proceed to variable selection with the upmost caution.

| CV-en | CV-lasso | solar | |||||

| (lar, cd) | |||||||

| Variable | Description | linear | log | linear | log | linear | log |

| Bedrooms | property, number of bedrooms | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ |

| Baths | property, number of bathrooms | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ |

| Parking | property, number of parking spaces | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ |

| AreaSize | property, land size | ✓ | ✓ | ✓ | ✓ | ||

| Airport | distance, nearest airport | ✓ | ✓ | ✓ | ✓ | ||

| Beach | distance, nearest beach | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ |

| Boundary | distance, nearest suburb boundary | ✓ | ✓ | ✓ | ✓ | ||

| Cemetery | distance, nearest cemetery | ✓ | ✓ | ✓ | |||

| Child care | distance, nearest child-care centre | ✓ | ✓ | ✓ | ✓ | ✓ | |

| Club | distance, nearest club | ✓ | ✓ | ✓ | ✓ | ||

| Community facility | distance, nearest community facility | ✓ | ✓ | ||||

| Gaol | distance, nearest gaol | ✓ | ✓ | ✓ | ✓ | ||

| Golf course | distance, nearest golf course | ✓ | ✓ | ✓ | ✓ | ||

| High | distance, nearest high school | ✓ | ✓ | ✓ | ✓ | ||

| Hospital | distance, nearest general hospital | ✓ | ✓ | ✓ | |||

| Library | distance, nearest library | ✓ | ✓ | ||||

| Medical | distance, nearest medical centre | ✓ | ✓ | ✓ | |||

| Museum | distance, nearest museum | ✓ | ✓ | ✓ | ✓ | ||

| Park | distance, nearest park | ✓ | ✓ | ✓ | |||

| PO | distance, nearest post office | ✓ | ✓ | ✓ | |||

| Police | distance, nearest police station | ✓ | ✓ | ✓ | ✓ | ||

| Pre-school | distance, nearest preschool | ✓ | ✓ | ✓ | ✓ | ||

| Primary | distance, nearest primary school | ✓ | ✓ | ✓ | ✓ | ||

| Primary High | distance, nearest primary-high school | ✓ | ✓ | ✓ | ✓ | ||

| Rubbish | distance, nearest rubbish incinerator | ✓ | ✓ | ✓ | |||

| Sewage | distance, nearest sewage treatment | ✓ | |||||

| SportsCenter | distance, nearest sports centre | ✓ | ✓ | ✓ | ✓ | ||

| SportsCourtField | distance, nearest sports court/field | ✓ | ✓ | ✓ | ✓ | ||

| Station | distance, nearest train station | ✓ | ✓ | ✓ | |||

| Swimming | distance, nearest swimming pool | ✓ | ✓ | ✓ | ✓ | ||

| Tertiary | distance, nearest tertiary school | ✓ | ✓ | ✓ | ✓ | ||

| Mortgage | SA1, mean mortgage repayment (log) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ |

| Rent | SA1, mean rent (log) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ |

| Income | SA1, mean family income (log) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ |

| Income (personal) | SA1, mean personal income (log) | ✓ | |||||

| Household size | SA1, mean household size | ✓ | ✓ | ✓ | ✓ | ||

| Household density | SA1, mean persons to bedroom ratio | ✓ | ✓ | ✓ | ✓ | ||

| Age | SA1, mean age | ✓ | ✓ | ✓ | ✓ | ✓ | |

| English spoken | SA1, percent English at home | ✓ | ✓ | ✓ | |||

| Australian born | SA1, percent Australian-born | ✓ | ✓ | ✓ | |||

| Suburb area | suburb, area | ✓ | ✓ | ✓ | |||

| Population | suburb, population | ✓ | ✓ | ✓ | |||

| TVO2010 | suburb, total violent offences, 2010 | ✓ | ✓ | ||||

| TPO2010 | suburb, total property offences, 2010 | ✓ | ✓ | ✓ | |||

| TVO2009 | suburb, total violent offences, 2009 | ✓ | ✓ | ✓ | |||

| TPO2009 | suburb, total property offences, 2009 | ✓ | ✓ | ||||

| ICSEA | local school, ICSEA | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ |

| ReadingY3 | local school, year 3 mean reading score | ✓ | ✓ | ✓ | ✓ | ||

| WritingY3 | local school, year 3 mean writing score | ✓ | ✓ | ✓ | ✓ | ||

| SpellingY3 | local school, year 3 mean spelling score | ✓ | ✓ | ✓ | |||

| GrammarY3 | local school, year 3 mean grammar score | ✓ | ✓ | ✓ | |||

| NumeracyY3 | local school, year 3 mean numeracy score | ✓ | ✓ | ✓ | ✓ | ||

| ReadingY5 | local school, year 5 mean reading score | ✓ | |||||

| WritingY5 | local school, year 5 mean writing score | ✓ | ✓ | ✓ | |||

| SpellingY5 | local school, year 5 mean spelling score | ✓ | ✓ | ✓ | |||

| GrammarY5 | local school, year 5 mean grammar score | ✓ | ✓ | ✓ | |||

| NumeracyY5 | local school, year 5 mean numeracy score | ✓ | ✓ | ||||

| Number of variables selected | 57 | 53 | 44 | 36 | 9 | 11 | |

The database is particularly well suited to demonstrate the linear graph learning technique. Firstly, we have over 200GB of data on tens of thousands of variables and more than ten thousands observations. The size of such ‘big data’ reduces the possibility of variable omission. Even though some factors in the house market are not observable, their proxies are likely to be included in the synthesized database, further reducing the issue of variable omission. Secondly, as shown below, the regression on the selected variables are high (e.g., for a typical regression with only 11 variables, ; slightly tuning the functional forms, the regression can easily reach approximately ), indicating that the majority of the patterns in the data are linear. As a result, for this application, the nonlinearity issue does not concern us too much. By constrast, in other applications of linear graph learning it would be prudent to carry out similar checks for variable omission and linearity.

3.2 Second stage variable selection, its sparsity and prediction accuracy under different functional forms

Pearl (2009) points out that dependence and causation relations should not be affected by the functional forms of variables. For example, if is a parent of , must be also true, and vice versa. Nonetheless, to avoid being misled by variable form, we conduct second stage variable selection in both linear and log terms, only selecting variables that are simultaneously selected in both scenarios. To avoid the possibility that some variable selection algorithm loses sparsity or accuracy, we implement solar, lasso and cross-validated elastic net (CV-en) for comparison. We optimize lasso using both cross-validated coordinate descent (CV-cd) and cross-validated least-angle regression (CV-lars), both of which return the same variable selection result due to .

With all variables in linear form, Table 1 shows the selection results from solar, lasso and CV-en. Consistent with Jia and Yu (2010), both lasso solvers and CV-en simultaneously lose sparsity of variable selection due to the complicated causal structures and severe multicollinearity in the data. Lasso only manages to drop 7 variables and CV-en selects all 57 variables. It is not recommended to heuristically increase the value of in lasso-type estimators (e.g., the one-sd rule or the ‘elbow’ rule) since it may trigger further grouping effects and consequently lead to the random dropping of variables. On the other hand, CV-en is designed to tolerate multicollinearity and the grouping effect and is expected to return a sparse and stable regression result. However, CV-en fails to accomplish any variable selection, suggesting sensitivity to the complicated causal structure in the house price dataset. By contrast, solar returns a sparse regression model, with only variables selected from .

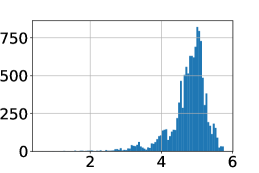

Table 1 also shows the selection results when all variables measured in dollars (e.g., rent, family income, etc.) are transformed by logarithms and the response variable is . The decision to use a log transform only on dollar-measured variables is for both statistical and empirical reasons. Statistically, it is because that the other variables in the data are distributed almost symmetrically without heavy tails. As illustrated with Gaol and Beach in Figure 8, log transforms induce pronounced left skewness. As shown in Figures 8f and 8c, left skewness is not resolved by changing variables units before the log transform. Empirically, log transforms may cause interpretation difficulties. For example, we are typically interested in the price response to unit as opposed to a percentage increase in the number of bedrooms or bathrooms. As a result, we do not use log transforms on the other variables.

In log regression, due to variable form changes, lasso selects 35 variables and CV-en selects 54. Some of the lasso and CV-en selections seem odd. For example, lasso drops all Year 5 test scores, Year 3 Spelling and Grammar but selects all the other Year 3 examination scores. CV-en selects all other scores, dropping only Year 5 Reading. These selections seem to suggest that only some primary school examination scores particularly matter in house pricing. By contrast, solar returns a very sparse regression model, with only variables selected in the log regression and of them are also selected in the linear regression. Since causal relations should not be affected by variable forms, we select variables chosen by solar simultaneously in Tables 1: {bedrooms, baths, Parking, Beach, ChildCare, Gaol, ICSEA, logMortgage, logRent, logFamInc}.

| Variable | elas net | lasso | rec solar | solar |

|---|---|---|---|---|

| constant | ||||

| Bedrooms | ||||

| Baths | ||||

| Parking | ||||

| Airport | ||||

| Beach | ||||

| Child care | ||||

| Gaol | ||||

| Rubbish | ||||

| log(Mortgage) | ||||

| log(Rent) | ||||

| log(Income) | ||||

| Age | ||||

| ICSEA | ||||

| Variable | elas net | lasso | rec solar | solar |

|---|---|---|---|---|

| constant | ||||

| Bedrooms | ||||

| Baths | ||||

| Parking | ||||

| Airport | ||||

| Beach | ||||

| Child care | ||||

| Gaol | ||||

| Rubbish | ||||

| Mortgage | ||||

| Rent | ||||

| Income | ||||

| Age | ||||

| ICSEA | ||||

Lastly, solar variable selection outperforms lasso-type estimators in terms of the balance between sparsity and prediction accuracy, as shown in Tables 2 and 3. Table 3 details the post-selection OLS results on CV-en, lasso and solar selection from the log models, showing solar selects only 9 variables compared with lasso (44) and CV-en (57). Surprisingly, pruning 35 to 48 variables from the 1 list only reduces the by 5%. This confirms that, from the perspective of prediction, solar successfully identifies the most important variables in the database. A very similar result is also found in Table 2 where solar only selects 11 out of 57 variables, which explains 73% of the variation of log(price). The extra variables selected by lasso or CV-en only improve the by around 2%. It is known that more covariates, redundant or not, always increase in finite. In this datset, 25 more variables (from solar to lasso) only increases by 3%. This suggests that either the 3% gain is pure overfitting; or they are conditionally correlated to in a very weak level. As those with direct causal relations from/to , the Markov Blanket variables of are always strongly correlated to , holding all other variables constant. A weak conditional correlation suggest that these variables may be the remote ancesters/descendants of . This does not suggest that they have no causal relations to ; it just implies that they are not in the MB of and do not have a direct causal effect.

While the log and linear models should represent the same causal structure, the linear model performs relatively poorly. Also, with log transform, the dollar measured variables are less skewed and possibly with a lighter tail. Hence, we focus on the log regression. As explained previously, the MB includes all the variables that are conditionally correlated to price in the population, implying that the MB variables should be able to explain all non-noise variation in price. Since we do not know the population variance of noise, we cannot know with absolute certainty the magnitude of noise variation. However, with %, we are confident that the majority of price variation is linear and explained by the MB variables. The remaining 27% may be due to noise, functional form error (e.g., to capture nonlinear patterns, we should use a polynomial equation, a trigonometric equations or a nerual network instead of a first-order linear equation), or spatial clustering in the geographical data. While we cannot rule out nonlinearity, the severity of those problems appears to be under control. The high explanatory power of the variables selected by solar under the log transform is reassuring on the reliability of MB selection. In Appendix 3, we try using other machine learning methods to capture the nonlinearity among and the selected variables. It turns out that, with cross validation controlling the overfitting, the selected variable can easily explain around 90% of the variation of , confirming that there does exist a nonlinear pattern between the selected variables and , which accounts for another 17% of and is not the major pattern in our dataset.

3.3 Grouping effects in variable selection

Before moving on to graph learning, we need to check whether grouping effects cause solar to mistakenly exclude variables from the price MB. As noted above, the accuracy and robustness of variable selection may be reduced when grouping effects are embedded in the data, especially when the dependence and causation structures are complicated. As shown in the supplementary correlation table, the distances of houses to different locations are highly spatially correlated with one another. To investigate whether solar variable selection is affected by such multicollinearity, Table 4 focuses on the group of variables highly correlated to gaol, including airport, rubbish and childcare, all of which have pairwise unconditional correlations above 0.5.

| ChildCare | Airport | Rubbish | Beach | |

| 0.756 | 0.715 | 0.671 | 0.528 |

Based on the results in Table 4, we standardize all variables and estimate the regression

| (3.1) |

| coefficient | ||||

|---|---|---|---|---|

| constant | ||||

| Airport | ||||

| ChildCare | ||||

| Rubbish | ||||

| Beach |

| degrees of freedom |

Table 5 shows that almost 90% of the variation in Gaol can be explained by {ChildCare, Airport, Rubbish, Beach} and in (3.1), indicating severe multicollinearity between Gaol and the other 4 variables. The empirical reason why {Gaol, ChildCare, Airport, Rubbish, Beach} are highly correlated is easy to see. The house market data cover a roughly 10km square area in eastern Sydney. The gaol (Long Bay correctional complex), several childcare centers (e.g., Blue Gum Cottage Child Care, Alouette Child Care, etc.), the airport (Kingsford-Smith Airport) and waste treatment facilities (e.g., Banksmeadow Transfer Terminal, Malabar Wastewater Treatment Plant, Cronulla Wastewater Treatment Plant) are all located in the southeast corner of the 10km square area, explaining the collinearity among the variables.

The multicollinearity very likely breaches the irrepresentable condition (IRC) and indicates the presence of grouping effects, casting doubt on the variable selection process. The implication is that, even though we know that at least one of the variables in {ChildCare, Airport, Rubbish, Beach, Gaol} is in the MB of price, it may be difficult to pinpointing precisely which one statistically. To avoid being misled by any grouping effect, we consider enlarge the subset {Gaol, ChildCare, Beach} into the gaol group {ChildCare, Airport, Rubbish, Beach, Gaol} in the variable selection results. We refer to the union of the solar variables and {ChildCare, Airport, Rubbish, Beach, Gaol} as the rectified solar selection. Thus, for completeness, we compare the OLS results in both linear and log forms with the selection results from lasso, CV-en, solar ((3.2) and (3.4)) and rectified solar selection ((3.3) and (3.5)).

| (3.2) | ||||

| (3.3) | ||||

| (3.4) | ||||

| (3.5) | ||||

The comparisons are also summarized in Tables 2 and 3. The most interesting thing is the from rectified solar. The difference between the solar and CV-en values tells us that the 48 variables dropped by solar explain a mere 5% of price variation while the difference between the solar and rectified solar shows that the gaol group dropped by solar explains 2% of price variation. A very similar result can be found in the comparison of log models. Thus, among all the 48 dropped variables, {Airport, Rubbish} seem to be the most important. This is additional evidence to justify previous doubts about the grouping effect.

4 Score-based graph learning based on solar variable selection

In last section, we select MB members of house prices using rectified solar. Ceteris paribus, each variable selected by rectified solar is highly likely to be conditionally correlated to price in the population, implying that they are highly likely to be the MB of price. However, it is possible that these variables have different roles: some may serve as the parents of price while others may serve as children or spouses. In order to accomplish endogeneity detection and instrument variable selection, we need to estimate the role of each MB member and all the complete pattern of causations in the MB. For this step, we implement the score-based graph learning method.

4.1 Temporal ordering of MB variables and Markov equivalence

A common problem in graph learning and causal inference is the Markov equivalence. In a nutshell, Markov equivalence says that, without an exact time stamp (i.e., when a variable is generated or, equivalentlym, when the value of a variable is determined), we cannot learn the exact population graph from the data. Instead, we can only learn the skeleton of the population graph (i.e., a graph without arrows or an undirected graph). Figure 9 illustrates these concepts in a simple example.

Figure 9a shows the population graph to be . However, without knowing the time stamp of each variable (which variable is born first), it is impossible to find the correct parent-child relations. We can only find a skeleton graph (Figure 9b), where we know that , , and . Any graphs that fit these conditions are included in the Markov equivalence class. Thus, Figure 9a (population graph), Figure 9c and Figure 9d (the confounding or fork structure) are included in the Markov equivalence class. Figure 9e (the collider structure) is not included since the correlation between and is zero unless is conditioned on. Put another way, without specific time stamps in this example, graph learning can only identify whether or not the population graph follows a collider structure, which is not particularly useful. However, with the corresponding time stamps and a large number of variables, we can eliminate Markov equivalence and narrow the list of candidates in the population graph. For example, if we know that , and were generated at respectively year 1990, 1991 and 1992, we can rule out Figure 9c and 9d from the Markov Equivalence, implying that Figure 9a is the correct graph.

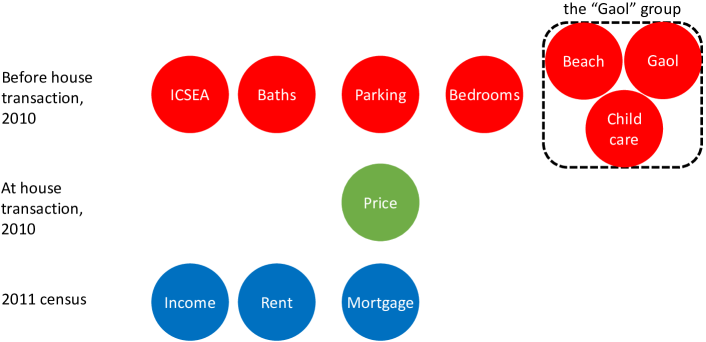

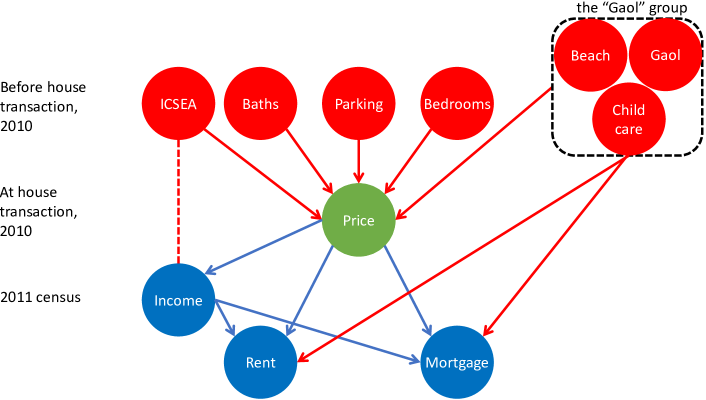

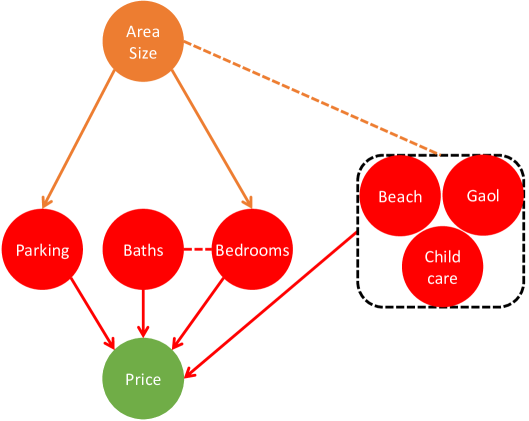

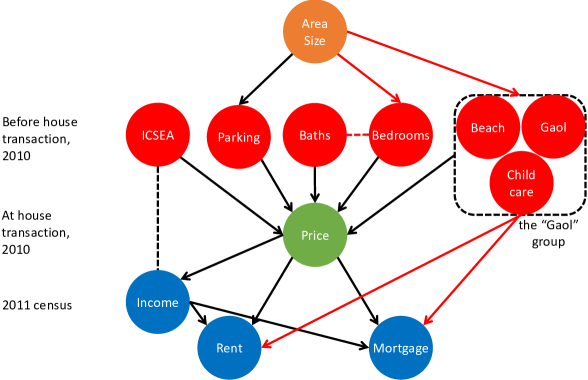

Based on the temporal order of variable generation in the house data, the selected variables can be ordered vertically. In Figure 10, the red nodes (house features, distances and ICSEA) are determined before the house transaction in 2010; the green nodes are generated at the time of the 2010 house transaction; and the blue nodes (demographic variables) are generated at the 2011 census, after 2010 house transactions.131313Multiple green nodes are included in our database, including the house transaction method (e.g., auction, private sale, and so on), the listing history and 30 other variables. We focus on price in this graph estimation. Due to the probable IRC violation discussed above, {Gaol, ChildCare, Beach} are grouped manually and represent the the ‘Gaol group’ {Gaol, ChildCare, Beach, Airport, Rubbish}. The temporal order helps to identify the role of each variable in the MB: variables generated in 2011 cannot cause any change in those generated in or before 2010, implying that the red nodes cannot be the descendants of green and blue nodes; likewise, the green nodes cannot be the children of blue nodes as well. Since all selected variables are in the MB of price, the red nodes have to be the parents of price while rent and mortgage are the children of price. Since parents cause their children, who further cause the grandchildren, the time stamps and MB variable yield the estimated graph and the causation realtions as Figure 11.

The role of income in Figure 11 is worthy of discussion. 2009 ICSEA is computed partially based on household income at 2009 while the income variable is household income in 2011. Since there exists strong temporal correlation in household income and since we do not have a high-dimensional database on household income, we cannot determine whether the correlation between ICSEA and income is purely autocorrelation or contains some kind of causation. Assuming there exists causation, we cannot identify it statistically without detailed earnings data linked to house transactions. Detailed earnings data are beyond our scope. Moreover, linking detailed earnings data to the house addresses in the transactions data would likely run afoul of data privacy regulations. Hence, we connect ICSEA and income with an undirected dash, meaning graphically that there may be some kind of relation that we cannot identify in detail. Since solar variable selection confirms that income and the gaol group belong to both the MB of rent and MB of mortgage (details can be found in the supplementary files), we connect them to rent and mortgage directly, which completes the graph learning as Figure 11.

4.2 Backdoor effect estimation

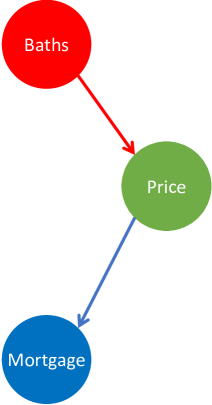

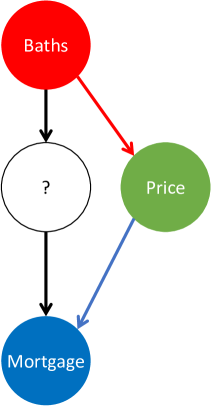

Figure 11 shows that a parent of price can indirectly cause a change in rent or mortgage through price (e.g., ), confirming the existence of the frontdoor effect(FE). The last step of graph learning is to determine whether the parents of price can cause a change in rent or mortgage without going through price. Such a causal effect is a backdoor effect (BE) and illustrated as black arrows in Figure 12. BE can be constructed either as Figure 12b or Figure 12c. The difference between Figures 12b and 12c is that, in Figure 12b, Baths can cause a change in Mortgage even after controlling for any possible variables. BEs of such kind cannot be cut off even though you control all the other variables in the world. By contrast, after controlling the variable(s) ‘?’ and Price in Figure 12c, Baths can no longer cause any change in Mortgage, meaning that BEs of such kind are controllable. We can estimate which causal structure fits the data better as follows. First, we find out which of Figures 12a and 12b fits data better without controlling for any other variables. If Figure 12a is chosen, it implies that there is no BE. If Figure 12b is chosen, there exists a BE and we need to combinatorially determine whether there exists a variable(s) ‘?’ in the BE from Baths to Mortgage.

We use the score-based learning method to find the optimal causal structure. Specifically, we estimate the AIC, BIC and BGE scores of Figure 12a (column ‘no BE’ in Table 6) and Figure 12b (column ‘BE’ in Table 6) on the house pricing data and choose the one with the lower score. If bath only causes mortgage via price, the conditional correlation between baths and mortgage will be very close to zero after holding price constant. Hence, due to the overfitting of the causal structure in Figure 12b, its AIC, BIC or BGE scores will be higher than for Figure 12a, implying that the no-BE graph fits the data better. By replacing baths with parking or bedrooms in Figure 12, we can instead check whether a BE exists between mortgage and other parents of price. In a similar vein, by replacing mortgage with rent, we can also check whether a BE exists between rent and any parent of price. Table 6 shows the results from BE estimation.

(optimal AIC, BIC, and BGE scores in red)

| logRent | logMortgage | ||||

|---|---|---|---|---|---|

| BE | No BE | BE | No BE | ||

| AIC | 23726.55 | 23731.28 | 19437.42 | 19482.37 | |

| Baths | BIC | 23759.74 | 23760.78 | 19470.61 | 19511.87 |

| BGE | 23758.70 | 23760.01 | 19470.54 | 19512.35 | |

| AIC | 27197.09 | 27500.08 | 23060.65 | 23251.17 | |

| Bedrooms | BIC | 27230.27 | 27529.58 | 23093.84 | 23280.67 |

| BGE | 27230.75 | 27529.87 | 23095.31 | 23282.22 | |

| AIC | 25002.25 | 25064.54 | 20762.16 | 20815.63 | |

| Parking | BIC | 25035.44 | 25094.04 | 20795.35 | 20845.13 |

| BGE | 25034.62 | 25093.35 | 20795.46 | 20845.70 | |

We use logRent and logMortgage for the BE estimation in Table 6 because, although the score-based learning method works well on many subgaussian variables for small , Rent and mortgage are typically right-skewed distributions. The log transform can significantly reduce right skewness and improve the accuracy of the AIC, BIC, and BGE scores. Table 6 clearly shows that the graph without BEs consistently have lower scores in terms of AIC, BIC and BGE, which confirms the validity of no BE. As a result, Figure 11 is the final estimated graph as the MB of price; we don’t need to add in any BE.

It is worth noting that we ignore ICSEA, income and the gaol group in Table 6 for statistical reasons. Due to IRC violation in the gaol group, it is difficult to estimate accurately the BE of variables in the group to the children of price.141414Statistically, the minimal eigenvalue of the covariance matrix may be very close to , resulting in unreliable AIC, BIC, or BGE scores. ICSEA is synthesized from a number of variables such as household income, family wealth and other factors representing the socio-economic status of the household. As a result, there may exists a complicated causal relation among each part of ICSEA and price, which we cannot investigate due to the unknown form of the synthesis.

4.3 Graph interpretations and remarks on AreaSize

Figure 11 shows that the graph estimation and MB selection offers interpretations consistent with economic intuition about the dynamics of the house market. First, houses with more desirable features and better locations are purchased by higher-income households at higher prices. Second, higher house prices causes higher mortgage repayments and higher rental payments. Third, higher-rent houses are leased to higher-income households (households with high ICSEA scores). From a demographic perspective, after higher-income home owners or tenants move into the newly purchased or leased houses, the average income and family income in the local SA1 also increases, reflected on the graph as price causing income.

It is worth noting that AreaSize is not selected into the MB of price, which seems counterintuitive. However, this can be explained using Figure 13. Firstly, area size of houses at different locations are not comparable. A downtown terrace house with small area size can be much more expensive than a house on a large plot 10km from downtown. Hence, ceteris paribus, AreaSize has much more explanatory power on price if we compare houses within a local area or spatial neighbourhood, which requires a spatial statistics technique151515For example, lasso variable selection within a spatial Gaussian kernel. as opposed to simply controlling for distance to various locations. Secondly, AreaSize measure the area of the land and is originally determined when the land is purchased, which is even earlier than the house construction. This implies that AreaSize is one of the constraints for the construction of parking, baths rooms and bedrooms. Thus, AreaSize is likely a parent of parking and bedrooms and may also be simultaneously determined with location when the land is purchased. Thus, AreaSize does not belong to the MB of price. It is also interesting to note that, unlike parking and bedrooms, the number of baths is not a child of AreaSize and that there is a undirected edge between baths and bedrooms. This finding is data-driven because while is significantly nonzero in the data. This phenomenon is not unexpected. During house design and construction, the number of bathrooms is typically a function of the number of bedrooms (essentially, of expected household size). Given household size and number of bedrooms, there seems to be little incentive to build more bathrooms with more AreaSize. At the end of the day, due to a lack of data on the first-hand house market and new construction, we are unable to infer a graph incorporating construction and land purchase and will not pursue the topic further.

5 Application of graph estimation: endogeneity detection and instrument selection

With the estimated graph in hand, we can begin the instrument selection procedure using Definition 2.3. The first step to selecting a valid instrument is to ensure there is endogeneity in the graph, otherwise we only waste degrees of freedom.

5.1 Endogeneity detection using graphs

Price is endogenous statistically and empirically. Figure 11 depicts a graph that reflects a statistically dynamic system. The input of the system is the gaol group, house features and ICSEA, rent and mortgage are two outputs, and price is internally determined by the statistical system. As a result, price is highly likely to be endogenous. The endogeneity of price is also supported statistically by variable selection results. For example, by estimating linear and log solar regressions of rent on all the other variables, we have the following estimated regression models,

| (5.1) | ||||

| (5.2) |

Since the ratio is almost , the solar variable selection results are statistically robust and accurate. Solar includes log(price) and price in (5.1) and (5.2), respectively, implying that price is an very important covariate in the rent regressions and that it is highly likely that rent and price are simultaneously determined. Thus, along with the solar variable selection results in (3.2) and (3.4), we can establish the simultaneous equations models in log terms

| (5.3) |

or in linear terms

| (5.4) |

The simultaneous determination of rent, price and mortgage is also empirically intuitive. Before bidding on a house, the buyer needs to estimate the upper bound of mortgage that a bank will offer and, if the purchase is for investment purposes, how much rent the property will return. Before a bank decides on a mortgage application, it typically first gets a valuation of the house price and the expected rent. Similarly, rent is typically related to the price of house and monthly mortgage amount.161616In a competitive market with zero transactions costs, of course, rent would exactly cover the mortgage, which itself would be equal to the price of the house.

5.2 Instrument selection using graphs

Given price is endogenous, we need to find a valid instrument in the rent regression. We focus on the regression analysis of rent in this paper, but the mortgage analysis proceeds along the same lines. A valid instrument must satisfy Definition 2.3 and non-existence of a BE (Figures 5 and 6). Using Figure 11, we directly uncover 3 instrumental variables: baths, bedrooms and parking, all of which satisfy Definition 2.3 only if we control the Gaol group variables. As shown in Figure 14, if we fail to control the Gaol group variables, a backdoor effect will be constructed between Rent and any of{baths, bedrooms, parking} as follows :due to the existence of the confounder AreaSize, Baths, for example, will be unconditionally correlated to Bedrooms, which is further unconditionally correlated to the Gaol group variables due to the confounder AreaSize. Since the Gaol group variables — variables to represent the house location — causes the change of the rent, a BE is constructed. This violates Definition 2.3 by allowing the change of Baths to affect the change Rent even though you control the house price. Under such circumstance, Baths cannot be an instrument for the causal effect from Price to Rent since it represent two effects: the causal effect from Price to Rent and the backdoor effect mentioned above.Hence, the Gaol group variables must be controlled, meaning that they have to be included into the instrument variable regression of rent.