Real-time detection of a change-point in a linear expectile model

Gabriela CIUPERCA

Institut Camille Jordan, UMR 5208, Université Claude Bernard Lyon 1, France

Abstract:

In the present paper we address the real-time detection problem of a change-point in the coefficients of a linear model with the possibility that the model errors are asymmetrical and that the explanatory variables number is large. We build test statistics based on the cumulative sum (CUSUM) of the expectile function derivatives calculated on the residuals obtained by the expectile and adaptive LASSO expectile estimation methods. The asymptotic distribution of these statistics are obtained under the hypothesis that the model does not change. Moreover, we prove that they diverge when the model changes at an unknown observation. The asymptotic study of the test statistics under these two hypotheses allows us to find the asymptotic critical region and the stopping time, that is the observation where the model will change. The empirical performance is investigated by a comparative simulation study with other statistics of CUSUM type. Two examples on real data are also presented to demonstrate its interest in practice.

Keywords: real-time change-point detection; asymmetric model error; expectile; adaptive LASSO; stopping time.

Subject Classifications: 62F05; 62J07; 62L10

1. Introduction

In many applications (medicine, finance, engineering, ecology, meteorology) it is necessary to solve the problem of testing in real-time of a change in a model which does not satisfy classical conditions. Moreover, with the recent technological advancements that allow the collection of a vast amounts of data, the studied model can contain a large number of explanatory variables. These involve the need to automatically select the relevant variables simultaneously with the change detection, whence the practical interest of the results obtained in this paper.

Therefore, we consider the real-time detection of a change-point in a linear model when the model errors can be asymmetrical and when the number of explanatory variables can be large.

There are two types of change-point detection: a posteriori and in real-time (sequential). The a posteriori detection is done once the experiment has ended, after which we ask whether there have been changes in the model and if so, find their number and their location. Real-time detection is done with each observation: we have a model based on historical data and we know that the change did not occur. At each new observation we test whether the model has changed or not. The test is based on a statistic built on the residuals corresponding to the estimators obtained on the historical data model. If the model errors satisfy the classical conditions, that is zero mean and bounded variance, Horváth et al. (2004) introduced the test statistic based on the cumulative sum (CUSUM) of the residuals obtained by the least squared (LS) estimation method. However, if the law of errors is asymmetrical, then the LS estimation method is not appropriate to estimate the model parameters because it produces non accurate estimators. Then, Newey and Powell (1987) introduced the expectile estimation method which is more appropriate when the first four moments of the model errors exist and the distribution of is asymmetrical. Another possible estimation method when does not satisfy the classical conditions on the moments is the quantile one (see Koenker (2005)). The expectile method has the advantage over the quantile method that it is differentiable, therefore theoretical studies and numerical computation are easier. Another advantage is that the asymptotic variance of the expectile estimator can be calculated without going via the density of the model error.

If the number of explanatory variables of the model is large and only a part is relevant (with non-zero coefficients) then the automatic selection of these variables can be carried out using the adaptive LASSO penalty introduced by Zou (2006) for the LS loss function. If the loss function is quantile or expectile, then, corresponding adaptive LASSO estimators have been proposed and studied by Ciuperca (2016) and Liao et al. (2019), respectively.

Let us give some recent paper references where the CUSUM method or variations have been used for detection in linear models of a change-point in real-time. Zhou et al. (2015) propose and study a test statistic as a CUSUM of the subgradient of the quantile process in order to detect in real-time a change in a linear quantile model. Kirch and Weber (2018) propose different statistics with respect to the number of observations included in the partial sum: modified moving-sum-statistic, Page’s cumulative-sum-statistic and the standard moving-sum-statistic.

Zhang and Li (2017a) consider a model for which the effect of a covariate on the response

variable is linear but varies below and above an unknown threshold in a continuous way. Therefore, Zhang and Li (2017a) study a different model from that of the present paper because they consider that the change occurs when one of the regressors exceeds a certain value which is seen as the change sought and estimated. Based on a weighted CUSUM type statistic, they develop a testing procedure for the existence of structural change at a given expectile. The same model where the change occurs with respect to an unknown value of a covariable is considered by Zhang and Li (2017b) which develop a score-like test based on a weighted CUSUM process. Jiang and Kurozumi (2020) applied the CUSUM test based on LS residuals to sequentially detect structural change in a linear model with a trend. For the proposed test statistic, they get the limiting null distribution and the divergence under the alternative. In addition, the asymptotic distributions of the corresponding stopping times is derived. On the other hand, Jiang and Kurozumi (2019) investigated two modified versions of the CUSUM test to avoid losing power when the mean of the regressor is orthogonal to the shift. In Qi et al. (2016), a new class of fluctuation sequential tests based on recursive estimates is proposed, for which asymptotic behaviour is studied. For the change-point detection on the parameter of a certain discrete-time stochastic processes, Nedényi (2018) presents a statistic based on the CUSUM of the estimates of certain martingale difference sequences.

In order to locate the change-point in a multivariate data with heavy-tailed distribution, Liu et al. (2019) propose a tail adaptive approach. Moreover, in order to detect in real-time an abrupt change in linear regression models, Geng et al. (2019) propose a novel algorithm, in Bayesian and non-Bayesian formulation. Even if it is not the CUSUM method that is used, we consider it important to cite Horváth and Rice (2019)’s paper where a linear factor model is considered and where the dimension of the factors and the sample size tend jointly to

infinity. For testing the structural stability of the model, it is proved that, under the null hypothesis, if the effect of the factors is sufficiently strong then the processes of partial

sample estimates of the largest eigenvalues of the sample covariance matrix have Gaussian limits. Works which simultaneously consider the relevant variables detection and also the real-time detection of a change in the model by a CUSUM type technique are Ciuperca (2015) and Ciuperca (2018) where the loss function is LS and quantile, respectively, with an adaptive LASSO type penalty.

To the best of the author’s knowledge, there is no work in the literature regarding the real-time detection of a change in the coefficients of a linear model using the expectile method and when the coefficient number is large. In this last case, the adaptive LASSO expectile method will be used to select the relevant variables on the historical data.

Finally, but not lastly, we would like to remind that the CUSUM-type methods are used to detect a change in the parameters of a time series. Here are some references from the recent literature: Song and Kang (2020), Gronneberg and Holcblat (2019), Prášková (2018), Chen and Hu (2017).

The remainder of the paper is organized as follows. In Section 2 we introduce the model, the assumptions, the null and alternative hypothesis for the model and we state two auxiliary results. In order to detect the change in the model in real-time, two test statistics are proposed and asymptotically studied under the null hypothesis (no change) and under the alternative hypothesis (there exist a change in the model coefficients after the historical data) in Section 3. In Section 4, we study and compare by a numerical study the proposed statistics with other test statistics. The two test statistics are also applied on two real data. The proofs of the results are postponed to Section 5.

2. Preliminaries and models

In this section we present the model, the considered assumptions and some preliminary theoretical results.

First of all, give some general notations that will be used throughout the paper. We make the convention that all vectors and matrices are in bold and that all vectors are column. For a vector v, we denote by its transposed, by , and , the , , norms, respectively. For , the -vector has all components . We denote by a positive generic constant independent from , which value may differ from one formula to another. The value of is not of interest. For a set , let us denote by the cardinality of and by its complementary set. The notations , represent respectively the convergence in distribution and in probability, as .

We consider a model on observations:

| (2.1) |

The observations are called historical observations and historical data. After these observations, other incoming observations sequentially are measured for the response variable and for the vector which contains the explanatory variables. The considered model on these observations is:

| (2.2) |

For models (2.1) and (2.2), the -vector of the explanatory variables is deterministic, with the components , for and . Furthermore, the values of are known for any .

For model (2.1), the parameter vector is of dimension fixed and its true value (unknown) is which does not depend on . Regarding the -vector of parameters of model (2.2), details will be given later.

Through the paper, the following assumptions are considered for the design :

-

(A1) , for some constant .

-

(A2) For , , and the -square matrix , there exists a positive definite matrix , such that, .

We emphasize that Assumption (A1) was also considered for expectile models for example by Zhao et al. (2018) and Ciuperca (2020), while Assumption (A2) is standard for linear models to ensure the identifiability of the coefficients (see for example Zou (2006), Geng et al. (2019), Liao et al. (2019)).

Moreover, the errors of models (2.1) and (2.2) will be assumed to be of the same distribution, not necessarily symmetrical. In order to introduce the suppositions on , with a generic term of , and to perform the statistical inference proposed in this paper, we introduce the expectile function. For a fixed expectile index , the expectile function of order is defined by:

The derivative of in is and the second derivative is .

Thereby, for the errors , we suppose the following assumption:

-

(A3) are i.i.d. continuous, such that and .

Note that assumption (A3) is standard for the expectile models (see Liao et al. (2019), Zhao et al. (2018), Gu and Zou (2016), Ciuperca (2020)).

We introduce the following notations:

The mean depends on the index but, in order to relieve the notation, we drop .

Since the errors satisfy assumption (A3) and not the classical assumptions of zero mean and bounded variance, Newey and Powell (1987) introduced the expectile estimator for the coefficients of a linear model. Thus, the parameter vector of model (2.1) is estimated by the expectile estimator which is defined by:

| (2.3) |

Under assumptions (A1)-(A3), the expectile estimator converges to the true value with a convergence rate of order (see Ciuperca (2020)). We denote the components of the vector by .

The following proposition states a more precise result on the asymptotic behavior of .

Proposition 2.1.

Under assumptions (A1)-(A3), we have:

We are now focusing on model (2.2), for which two hypotheses are considered, the observations constituting the monitoring period.

For this model, we test the null hypothesis that after the historical observations, the coefficients of model (2.2) coincide with those of model (2.1):

, for all ,

against the alternative hypothesis, that there is an unknown observation from which there is a change in the coefficients of the model:

: there exists , such that

with and unknown. Unlike , the value of can depend on .

For the monitoring period, there are two possible cases depending on the values of the number of observations after the historical data. These cases are referred as the following procedures:

-

•

open-end procedure, when or when (, );

-

•

closed-end procedure, when .

For the open-end procedure the monitoring is carried out to infinity if no change occurs in the model, while for the closed-end procedure, the monitoring is stopped after a fixed number of observations even if no change occurs.

Under hypothesis , the unknown change-point can depend on . If depends on , thus, it is not very far from the last observation of the historical data. thus, we consider that satisfies the following assumption:

-

(A4) , with the constant such that for the open-end procedure and for the closed-end procedure.

This is a typical condition on in a real-time detection problem of a change-point (see Hušková and Kirch (2012), Ciuperca (2018), Jiang and Kurozumi (2020)).

Moreover, assumption (A4) is in accordance with the definition of the two procedures.

Taking into account the convergence rate of towards , we consider the following random processes:

with , .

By the following lemma we study the difference between and its expectation, result which will be used to show the convergence in law under hypothesis of the two test statistics proposed in the following section.

Lemma 2.1.

For any constants , and integer , we have that there exists a constant such that, for sufficiently large and :

With these preliminary elements we are now ready to introduce the test statistics and to state the main results of the present paper.

3. Test statistics

In this section we propose two test statistics, based on the expecile and on the adaptive LASSO expectile residuals. For these statistics, we give the asymptotic distribution under hypothesis , for the two procedures (open-end and closed-end) and we show that they diverge under hypothesis . These results will allow us to find the stopping time when hypothesis starts to be rejected.

The proofs of all results presented in this section are given in Section 5.

3.1. Test statistic based on the expectile residuals

In order to test hypothesis against , we first build a test statistic based on the residuals obtained by considering the expectile estimator given by (2.3) for , with . For this purpose, we first calculate the residuals on all data:

After which, we introduce:

-

•

the -squared matrix: ;

-

•

for a fixed constant and , the following normalization function

-

•

the statistic .

Then, we consider as statistic for testing against :

which is a CUSUM (cumulative sum) test statistic calculated on the basis of the sum of weighted by the design and divided by the normalization function. By the following theorem, we state the asymptotic distribution of this test statistic under hypothesis for the open-end and closed-end procedures. Recall that for the closed-end procedure and for the open-end procedure we have .

Theorem 3.1.

Under assumptions (A1)-(A3), if hypothesis holds, then:

with a Wiener process of dimension , for the open-end procedure case and for the closed end procedure case.

As stated in Section 1 of Introduction, Zhang and Li (2017a) also used the expectile method to estimate the parameters of the model, except that the change does not occur in the coefficients but when one of the continuous explanatory variables exceeds an unknown threshold. The test statistic is different from ours and its asymptotic distribution under hypothesis is also different from that obtained in Theorem 3.1.

We now study the asymptotic behavior of the test statistic under alternative hypothesis , by proving that in this case it diverges.

By the following theorem we prove that the test statistic built on the expectile residuals converges to infinity under the alternative hypothesis.

Theorem 3.2.

Under assumptions (A1)-(A4), if for any constant such that for , the condition is satisfied, then, when hypothesis is true such that , we have:

The condition indicates that the jump in the coefficients must be much greater than the convergence rate of the expectile estimator towards . Intuitively, if the jump is of the same order as the convergence rate then it will be difficult to identifying the change. The same condition was considered by Zhou et al. (2015), Ciuperca (2017) for real-time change-point detection by quantile frameworks. Obviously, the parameters , may not depend on .

Theorems 3.1 and 3.2 allow us to detect the observation, called stopping time, where the change will occur when hypothesis is rejected, for a fixed size :

| (3.1) |

with the -th quantile of the distribution of .

From Theorems 3.1 and 3.2 we also deduce that the asymptotic critical region is: . Moreover, for a size fixed, the test statistic has the asymptotic type I error probability equal to and the asymptotic power equal to 1, when . This implies that and , that is, that the asymptotic probability of a false alarm is and that the change-point is detected with probability converging to one.

3.2. Test statistics based on the adaptive LASSO expectile residuals

Now consider for model (2.1) the possibility that the number of regressors is large and that among the components of a certain number are 0. Then, the automatic selection of the relevant explanatory variables (that is with non-nul coefficients) is essential and therefore the test statistic will take into account the automatic selection results. We then use as an estimation method, the adaptative LASSO expectile method, proposed and studied by Liao et al. (2019) for fixed and generalized by Ciuperca (2020) when depends on . In the present paper we suppose that does not depend on and that . The condition is necessary to have the identifiability of the expectile estimator calculated on the historical data.

The adaptative LASSO expectile estimator calculated on the historical observations is defined by:

| (3.2) |

with the adaptive weight , where is the -th component of the expectile estimator , a known constant and a positive deterministic sequence of tuning which converges to infinity as . The components of the adaptive LASSO expectile estimator are .

The tuning parameter and the constant satisfy the following assumption:

- (A5)

-

and , for .

Assumption (A5) is the classical supposition on the tuning parameter and on the power for the adaptive LASSO estimators: see Zou (2006) for the LS loss function, Ciuperca (2016) for the quantile loss function, Liao et al. (2019) for the expectile loss function.

Let us consider the set which contains the index of the non-zero coefficients of model (2.1). Since is unknown, the set is unknown as well. Taking into account definition (3.2) of the adaptive LASSO expectile estimator , we deduce that the set is an estimator for .

For a -vector of parameters, let us denote by the sub-vector of which contains the components , with and we denote by . We also define the -squared matrix by taking the lines and columns of the matrix . Thus, we have: . Similarly, we define the vectors , and the matrix .

The interest of the estimator is that it satisfies oracle properties, that is, under assumptions (A1)-(A3), (A5), it satisfies the following two properties (see Theorem 3 of Liao et al. (2019)):

-

•

sparsity property: .

-

•

asymptotic normality property: converges in distribution to a zero-mean Gaussian vector with the variance .

The convergence rate of towards is of order , under assumptions (A1)-(A3) and the sequence such that (see Theorem 2.1 of Ciuperca (2020)).

Let us now give a similar result to Proposition 2.1 for the adaptive LASSO expectile estimators of the non-zero coefficients.

Proposition 3.1.

Under assumptions (A1)-(A3), (A5), we have:

After this presentation of the necessary tools, we return to the test of against . For a fixed known constant and , we propose in the case of a model with large number of explanatory variables the following statistic:

with

the residuals corresponding to the adaptive LASSO expectile estimator and . Thus, in order to test against when is large we will consider the following test statistic:

For simplification of the calculations, taking into account the sparsity property of the estimator , without reducing the generality of our approach, let us assume bellow that , other cases are similarly proved. Then, we can write:

| (3.3) |

with , , the dimension of the vector being random.

For studying the test statistic under hypothesis we will first consider and study the following statistic:

The following theorem gives the asymptotic distribution of the test statistic , under hypothesis .

Theorem 3.3.

Under assumptions (A1)-(A3), (A5), if hypothesis holds, then:

with for the open-end procedure, for the closed-end procedure and a Wiener process of dimension .

Then, we now state the asymptotic behaviour of the test statistic under hypothesis .

Corollary 3.1.

Under the same conditions as in Theorem 3.3, if hypothesis holds, we have:

with a Wiener process of dimension .

Note that under hypothesis , the asymptotic behaviour of the statistic is the similar as that of the test statistic considered by Ciuperca (2018) for an adaptive LASSO quantile model. The simulations presented in Section 4 will show that in the case large, the test statistic based on the adaptive LASSO expectile estimator gives better results than that based on the adaptive LASSO quantile estimators.

We now consider that hypothesis is true and that the unknown parameter vector after observation can contain non-zero coefficients for indices other than those of . Let be then the corresponding index set which is also unknown. Without loss the generality, we rewrite: , . In order to study the test statistics and , under hypothesis , let us consider the index set , the parameters , and with .

Theorem 3.4.

If assumptions (A1)-(A5) are satisfied and if for any constant such that for the following inequality takes place , when hypothesis holds such that , then

This theorem allows us to deduce the divergence under hypothesis of the test statistic . This test statistic will be used in applications because the set is unknown, being estimated by .

Corollary 3.2.

Under the same conditions as in Theorem 3.4, we have

Similar to definition (3.1), we can find the stopping time from which hypothesis will be rejected when the test statistic is . Thus, for a fixed size , the stopping time is:

| (3.4) |

with the -th quantile of the distribution of . The quantile depends on by the dimension of the Wiener process . Then, the asymptotic critical region is: . Similarly to the test statistic constructed on the basis of the expectile estimation method, the test statistic has asymptotic size and the asymptotic power equal to 1, when . Thus, we have also that and .

We conclude this subsection by pointing out that when the model contains irrelevant variables, then the use of the test statistic is preferable to , especially when is large. This choice will be confirmed by the simulations presented in the following section.

4. Simulation study and applications

In this section we first perform a numerical study to illustrate our theoretical results and to compare our test statistics with those built on the adaptive LASSO quantile (Ciuperca (2018)) and the adaptive LASSO LS (Ciuperca (2015)) residuals. Afterwards, we present two applications on real data.

4.1. Simulation study

For the simulation study presented in this section, we use the following R language packages: package SALES with function ernet for the expectile regression, the package quantreg with function rq for quantile regression, the package ”lqa” with the function lqa for LS model with adaptive LASSO penalty.

In all simulations we consider that the number of non-zero coefficients on the historical data is three. More precisely , with , , . Under hypothesis , the change occurs in and only the first coefficient changes: , , . Then as well. Regarding design we consider two possibilities, for :

- D1

-

: , for any ,

- D2

-

: , for any ,

and , , , , for D1 and D2.

In all simulations, for adaptive LASSO expectile estimator (3.2), we consider the following value for the tuning parameter and, based on the simulation conclusions of Ciuperca (2020), we choose the power in the adaptive weights . For the model errors , two distributions are considered: one symmetric, more precisely the reduced centered normal distribution and one asymmetric of exponential distribution , that is with the density function . In order to estimate the expectile index such that in assumption (A3), we use the following relation:

Then, we calculate the empirical estimation of by:

The same type of penalties are considered for the adaptive LASSO quantile and LS methods, with the same tuning parameter and the powers in the weights and , respectively. We consider the quantile method for the index 0.5, that is the least absolute deviations loss.

For all studies, the theoretical test size is set .

4.1.1. Study and comparison of empirical sizes and powers

In Tables 1 and 2 we present the empirical test sizes () for the open-end and closed-end procedures using the test statistics: built on the residuals obtained by the expectile estimation method, built on the adaptive LASSO expectile residuals and a modified adaptive LASSO expectile statistic. The modified method consists of first selecting the relevant variables (with the non-null coefficient estimations) and reconsidering an expectile model only with these explanatory variables. The number of historical observations is . The number of the Monte Carlo replications is 10000 when , 5000 when and 2000 when . The results presented in Table 1 are obtained when the design is D1, while in Table 2 the design is of type D2. The number of explanatory variables is set either three, so there are no non-zero coefficients, or ten, so there are seven zero coefficients. From Tableau 1 we observe that the results clearly improve for when . On the other hand, for when , , we get that the empirical test sizes are strictly greater than 0.05 for closed-end procedure by the three expectile estimation methods. For , if , then we obtain using the test statistics constructed on the residuals obtained by the adaptive LASSO and modified methods (except the case for the closed-end procedure). For , if then and generally, for the results are better than for the other two values of . The results of Tableau 2 are significantly better than in Table 1. For , the smaller is the less the results obtained by the expectile method are good compared to those obtained by the adaptive LASSO expectile method. Conversely, when , that is when we have a small number of regressors and without irrelevant variables, the two test statistics corresponding to the two estimation methods give similar results. Whether in Table 1 or 2, we always obtain in all cases the empirical powers equal to 1.

In view of these results, because in the following we consider models with certain zero coefficients we only consider the test statistic on the adaptive LASSO expectile residuals.

In Tables 3 and 4 we compare the results obtained by:

-

•

the test statistic constructed on adaptive LASSO expectile residuals,

-

•

the statistic proposed by Ciuperca (2018) using adaptive LASSO quantile residuals,

-

•

the CUSUM statistic, in the case of the open-end procedure, proposed by Ciuperca (2015) constructed on the adaptive LASSO LS residuals,

for design of type D1 in Table 3 and of type D2 in Table 4. Since the test statistic on the adaptive LASSO LS residuals systematically makes false change-point detections, in order to improve results, Ciuperca (2015) proposed a modified procedure. So, we did the same for adaptive LASSO expectile and quantile frameworks, for comparing. We present the empirical test sizes () and powers () when the number of the explanatory variables is large: either 100 or 250. From Tables 3 and 4 we deduce that by the open-end procedure we obtain when and when , by the adaptive LASSO expectile and modified methods, for . For open-end procedure, if , then the values of obtained by the test statistic on the adaptive LASSO expectile residuals are similar to those obtained by the test statistic on the adaptive LASSO quantile residuals, except in the case when the test statistic on the adaptive LASSO expectile residuals give better results. We have the same observation for the two modified procedures. Note that for the test statistics by the quantile frameworks, when , we obtain that the values of are very far from 1, so, the tests do not detect the change in the model. The modified adaptive LASSO LS test gives very good results (). When hypothesis is true, our tests show their superiority in the detection of , since we obtain . For the two possible values of , the tests by the quantile frameworks don’t always detect change when . When , , if is large, then the modified adaptive LASSO LS test don’t detect the change also in a proportion of maximum .

We observe that, when is large, the tests which give better results in terms of the change-point detection or of less false alarm, by each framework, are: adaptive LASSO expectile, adaptive LASSO quantile and modified adaptive LASSO LS, for the open-end procedure. We then make a comparison between these three methods, for open-end procedure, when and , so when there are zero and non-zero coefficients and the value of is small compared to . The results are presented in Table 5. We observe that for the empirical test sizes are all smaller than theoretical test size . Otherwise, when the design is D1, the corresponding test statistic to the modified adaptive LASSO LS method does not detect the change-point, especially when the errors are exponential, therefore they have an asymmetric distribution. When the design is D2 and the model errors are exponential, it is the test statistic on the adaptive LASSO quantile residuals which does not detect the change. Moreover, from Table 5 we deduce that the test statistic on the adaptive LASSO expectile residuals gives very good results when the model error distribution is asymmetric.

| estimation | |||||||||

| method | procedure | 0 | 0.15 | 0.45 | |||||

| 500 | adaptive LASSO expectile | open-end | 0 | 0.005 | 0 | 0.01 | 0.04 | 0.21 | |

| 0.002 | 0.001 | 0.005 | 0.03 | 0.11 | 0.27 | ||||

| closed-end | 0 | 0.01 | 0.004 | 0.04 | 0.04 | 0.22 | |||

| 0.005 | 0.03 | 0.01 | 0.07 | 0.11 | 0.29 | ||||

| modif adaptive LASSO expectile | open-end | 0 | 0.001 | 0 | 0.006 | 0.04 | 0.16 | ||

| 0.002 | 0.004 | 0.005 | 0.01 | 0.11 | 0.22 | ||||

| closed-end | 0 | 0.007 | 0.004 | 0.02 | 0.04 | 0.18 | |||

| 0.005 | 0.01 | 0.01 | 0.03 | 0.11 | 0.23 | ||||

| expectile | open-end | 0 | 0.002 | 0 | 0.01 | 0.04 | 0.37 | ||

| 0.002 | 0.008 | 0.005 | 0.02 | 0.11 | 0.35 | ||||

| closed-end | 0 | 0.01 | 0.004 | 0.05 | 0.04 | 0.40 | |||

| 0.005 | 0.02 | 0.01 | 0.06 | 0.11 | 0.38 | ||||

| 300 | adaptive LASSO expectile | open-end | 0.01 | 0.02 | 0.03 | 0.05 | 0.07 | 0.14 | |

| 0.03 | 0.04 | 0.05 | 0.07 | 0.14 | 0.22 | ||||

| closed-end | 0.05 | 0.08 | 0.07 | 0.11 | 0.08 | 0.15 | |||

| 0.08 | 0.10 | 0.10 | 0.13 | 0.15 | 0.23 | ||||

| modif adaptive LASSO expectile | open-end | 0.002 | 0.004 | 0.01 | 0.01 | 0.03 | 0.07 | ||

| 0.007 | 0.01 | 0.02 | 0.02 | 0.09 | 0.14 | ||||

| closed-end | 0.02 | 0.02 | 0.02 | 0.03 | 0.04 | 0.08 | |||

| 0.03 | 0.03 | 0.04 | 0.05 | 0.10 | 0.14 | ||||

| expectile | open-end | 0.002 | 0.02 | 0.01 | 0.05 | 0.03 | 0.32 | ||

| 0.007 | 0.04 | 0.02 | 0.10 | 0.09 | 0.40 | ||||

| closed-end | 0.02 | 0.08 | 0.02 | 0.14 | 0.03 | 0.36 | |||

| 0.03 | 0.13 | 0.04 | 0.19 | 0.10 | 0.42 | ||||

| 200 | adaptive LASSO expectile | open-end | 0.05 | 0.05 | 0.08 | 0.08 | 0.15 | 0.17 | |

| 0.08 | 0.08 | 0.12 | 0.13 | 0.25 | 0.27 | ||||

| closed-end | 0.13 | 0.15 | 0.14 | 0.17 | 0.16 | 0.19 | |||

| 0.17 | 0.19 | 0.20 | 0.22 | 0.26 | 0.28 | ||||

| modif adaptive LASSO expectile | open-end | 0.01 | 0.02 | 0.02 | 0.05 | 0.08 | 0.13 | ||

| 0.02 | 0.05 | 0.04 | 0.08 | 0.16 | 0.21 | ||||

| closed-end | 0.04 | 0.09 | 0.06 | 0.10 | 0.09 | 0.14 | |||

| 0.06 | 0.12 | 0.08 | 0.14 | 0.17 | 0.22 | ||||

| expectile | open-end | 0.01 | 0.08 | 0.02 | 0.14 | 0.08 | 0.33 | ||

| 0.02 | 0.12 | 0.04 | 0.20 | 0.16 | 0.44 | ||||

| closed-end | 0.04 | 0.24 | 0.06 | 0.28 | 0.09 | 0.37 | |||

| 0.06 | 0.29 | 0.08 | 0.34 | 0.17 | 0.46 | ||||

| 100 | adaptive LASSO expectile | open-end | 0.07 | 0.14 | 0.09 | 0.16 | 0.10 | 0.17 | |

| 0.16 | 0.20 | 0.19 | 0.24 | 0.23 | 0.31 | ||||

| closed-end | 0.19 | 0.27 | 0.18 | 0.26 | 0.11 | 0.19 | |||

| 0.27 | 0.33 | 0.22 | 0.33 | 0.24 | 0.32 | ||||

| modif adaptive LASSO expectile | open-end | 0.03 | 0.05 | 0.04 | 0.07 | 0.05 | 0.08 | ||

| 0.06 | 0.09 | 0.08 | 0.12 | 0.15 | 0.20 | ||||

| closed-end | 0.09 | 0.14 | 0.09 | 0.13 | 0.06 | 0.09 | |||

| 0.13 | 0.19 | 0.14 | 0.19 | 0.16 | 0.21 | ||||

| expectile | open-end | 0.03 | 0.25 | 0.04 | 0.31 | 0.05 | 0.47 | ||

| 0.06 | 0.31 | 0.08 | 0.37 | 0.15 | 0.51 | ||||

| closed-end | 0.09 | 0.49 | 0.09 | 0.48 | 0.06 | 0.50 | |||

| 0.13 | 0.52 | 0.14 | 0.52 | 0.16 | 0.53 | ||||

| estimation | |||||||||

| method | procedure | 0 | 0.15 | 0.45 | |||||

| 500 | adaptive LASSO expectile | open-end | 0.005 | 0.001 | 0.01 | 0.003 | 0.24 | 0.16 | |

| 0.02 | 0.003 | 0.06 | 0.02 | 0.30 | 0.20 | ||||

| closed-end | 0.02 | 0.005 | 0.04 | 0.01 | 0.26 | 0.17 | |||

| 0.05 | 0.02 | 0.10 | 0.04 | 0.31 | 0.20 | ||||

| modif adaptive LASSO expectile | open-end | 0.004 | 0.001 | 0.01 | 0.003 | 0.22 | 0.16 | ||

| 0.01 | 0.003 | 0.03 | 0.02 | 0.25 | 0.20 | ||||

| closed-end | 0.009 | 0.005 | 0.02 | 0.01 | 0.24 | 0.17 | |||

| 0.02 | 0.02 | 0.06 | 0.04 | 0.26 | 0.20 | ||||

| expectile | open-end | 0.004 | 0.03 | 0.01 | 0.08 | 0.22 | 0.32 | ||

| 0.01 | 0.05 | 0.03 | 0.13 | 0.25 | 0.51 | ||||

| closed-end | 0.009 | 0.09 | 0.02 | 0.13 | 0.24 | 0.54 | |||

| 0.02 | 0.12 | 0.06 | 0.20 | 0.26 | 0.52 | ||||

| 300 | adaptive LASSO expectile | open-end | 0.008 | 0.007 | 0.02 | 0.02 | 0.19 | 0.18 | |

| 0.04 | 0.04 | 0.08 | 0.08 | 0.30 | 0.27 | ||||

| closed-end | 0.03 | 0.03 | 0.05 | 0.04 | 0.20 | 0.19 | |||

| 0.09 | 0.09 | 0.13 | 0.12 | 0.31 | 0.28 | ||||

| modif adaptive LASSO expectile | open-end | 0.004 | 0.004 | 0.01 | 0.001 | 0.17 | 0.17 | ||

| 0.01 | 0.02 | 0.04 | 0.04 | 0.23 | 0.21 | ||||

| closed-end | 0.02 | 0.02 | 0.04 | 0.02 | 0.18 | 0.18 | |||

| 0.04 | 0.05 | 0.07 | 0.07 | 0.24 | 0.22 | ||||

| expectile | open-end | 0.004 | 0.02 | 0.01 | 0.07 | 0.17 | 0.14 | ||

| 0.01 | 0.07 | 0.04 | 0.16 | 0.23 | 0.48 | ||||

| closed-end | 0.02 | 0.10 | 0.04 | 0.16 | 0.18 | 0.47 | |||

| 0.04 | 0.17 | 0.07 | 0.25 | 0.24 | 0.50 | ||||

| 200 | adaptive LASSO expectile | open-end | 0.03 | 0.01 | 0.06 | 0.01 | 0.28 | 0.18 | |

| 0.10 | 0.05 | 0.17 | 0.08 | 0.39 | 0.27 | ||||

| closed-end | 0.10 | 0.04 | 0.13 | 0.04 | 0.30 | 0.19 | |||

| 0.19 | 0.10 | 0.25 | 0.12 | 0.40 | 0.28 | ||||

| modif adaptive LASSO expectile | open-end | 0.02 | 0.004 | 0.05 | 0.009 | 0.26 | 0.17 | ||

| 0.05 | 0.02 | 0.11 | 0.05 | 0.31 | 0.22 | ||||

| closed-end | 0.07 | 0.02 | 0.11 | 0.02 | 0.27 | 0.18 | |||

| 0.11 | 0.05 | 0.16 | 0.07 | 0.32 | 0.22 | ||||

| expectile | open-end | 0.02 | 0.09 | 0.05 | 0.15 | 0.26 | 0.48 | ||

| 0.05 | 0.16 | 0.11 | 0.25 | 0.31 | 0.53 | ||||

| closed-end | 0.07 | 0.23 | 0.11 | 0.27 | 0.27 | 0.51 | |||

| 0.11 | 0.30 | 0.16 | 0.36 | 0.32 | 0.54 | ||||

| 100 | adaptive LASSO expectile | open-end | 0.12 | 0.11 | 0.21 | 0.14 | 0.48 | 0.23 | |

| 0.23 | 0.22 | 0.30 | 0.27 | 0.44 | 0.38 | ||||

| closed-end | 0.22 | 0.23 | 0.29 | 0.23 | 0.49 | 0.25 | |||

| 0.27 | 0.35 | 0.28 | 0.36 | 0.31 | 0.40 | ||||

| modif adaptive LASSO expectile | open-end | 0.09 | 0.08 | 0.18 | 0.10 | 0.45 | 0.19 | ||

| 0.13 | 0.13 | 0.19 | 0.18 | 0.41 | 0.29 | ||||

| closed-end | 0.18 | 0.18 | 0.25 | 0.18 | 0.46 | 0.21 | |||

| 0.20 | 0.24 | 0.26 | 0.25 | 0.42 | 0.31 | ||||

| expectile | open-end | 0.09 | 0.38 | 0.18 | 0.44 | 0.45 | 0.59 | ||

| 0.13 | 0.44 | 0.19 | 0.50 | 0.41 | 0.61 | ||||

| closed-end | 0.18 | 0.60 | 0.25 | 0.60 | 0.46 | 0.62 | |||

| 0.20 | 0.62 | 0.26 | 0.63 | 0.42 | 0.63 | ||||

| or | estimation | ||||||||

| procedure | method | 0 | 0.15 | 0.45 | |||||

| open-end | ad.LASSO expectile | 0.01 | 0.005 | 0.02 | 0.01 | 0.115 | 0.05 | ||

| modif ad.LASSO expect | 0.002 | 0.03 | 0.01 | 0.04 | 0.10 | 0.10 | |||

| ad.LASSO quantile | 0.003 | 0.005 | 0.01 | 0.005 | 0.05 | 0.09 | |||

| modif ad.LASSO quant | 0.003 | 0.07 | 0.01 | 0.12 | 0.05 | 0.20 | |||

| ad.LASSO LS | 1 | 1 | 1 | 1 | 1 | 1 | |||

| modif ad.LASSO LS | 0.002 | 0 | 0.005 | 0.01 | 0.02 | 0.04 | |||

| ad.LASSO expectile | 0.04 | 0.01 | 0.07 | 0.03 | 0.24 | 0.12 | |||

| ad.LASSO expect modif | 0.02 | 0.01 | 0.04 | 0.04 | 0.19 | 0.16 | |||

| ad.LASSO quantile | 0.009 | 0 | 0.02 | 0.03 | 0.14 | 0.10 | |||

| ad.LASSO quant modif | 0.01 | 0.20 | 0.02 | 0.25 | 0.13 | 0.33 | |||

| ad.LASSO LS | 1 | 1 | 1 | 1 | 1 | 1 | |||

| modif ad.LASSO LS | 0.008 | 0.03 | 0.01 | 0.03 | 0.06 | 0.09 | |||

| closed-end | ad.LASSO expectile | 0.15 | 0.05 | 0.15 | 0.05 | 0.15 | 0.07 | ||

| modif ad.LASSO expect | 0.08 | 0.11 | 0.09 | 0.11 | 0.14 | 0.12 | |||

| ad.LASSO quantile | 0.09 | 0.08 | 0.09 | 0.08 | 0.08 | 0.12 | |||

| modif ad.LASSO quant | 0.09 | 0.24 | 0.09 | 0.25 | 0.07 | 0.23 | |||

| ad.LASSO expectile | 0.22 | 0.14 | 0.23 | 0.15 | 0.27 | 0.13 | |||

| modif ad.LASSO expect | 0.11 | 0.16 | 0.13 | 0.17 | 0.20 | 0.18 | |||

| ad.LASSO quantile | 0.12 | 0.10 | 0.13 | 0.09 | 0.18 | 0.11 | |||

| modif ad.LASSO quant | 0.12 | 0.41 | 0.13 | 0.40 | 0.18 | 0.33 | |||

| open-end | ad.LASSO expectile | 1 | 1 | 1 | 1 | 1 | 1 | ||

| modif ad.LASSO expect | 1 | 1 | 1 | 1 | 1 | 1 | |||

| ad.LASSO quantile | 1 | 1 | 1 | 1 | 1 | 1 | |||

| modif ad.LASSO quant | 1 | 1 | 1 | 1 | 1 | 1 | |||

| ad.LASSO LS | 1 | 1 | 1 | 1 | 1 | 1 | |||

| modif ad.LASSO LS | 0.86 | 0.85 | 0.93 | 0.92 | 0.97 | 0.97 | |||

| ad.LASSO expectile | 1 | 1 | 1 | 1 | 1 | 1 | |||

| modif ad.LASSO expect | 1 | 1 | 1 | 1 | 1 | 1 | |||

| ad.LASSO quantile | 1 | 1 | 1 | 1 | 1 | 1 | |||

| modif ad.LASSO quant | 1 | 1 | 1 | 1 | 1 | 1 | |||

| ad.LASSO LS | 0.97 | 0.99 | 0.98 | 0.99 | 0.98 | 0.99 | |||

| modif ad.LASSO LS | 0.98 | 0.45 | 0.99 | 0.59 | 0.99 | 0.73 | |||

| closed-end | ad.LASSO expectile | 1 | 1 | 1 | 1 | 1 | 1 | ||

| modif ad.LASSO expect | 1 | 1 | 1 | 1 | 1 | 1 | |||

| ad.LASSO quantile | 1 | 1 | 1 | 1 | 1 | 1 | |||

| modif ad.LASSO quant | 1 | 1 | 1 | 1 | 1 | 1 | |||

| ad.LASSO expectile | 1 | 1 | 1 | 1 | 1 | 1 | |||

| modif ad.LASSO expect | 1 | 1 | 1 | 1 | 1 | 1 | |||

| ad.LASSO quantile | 1 | 1 | 1 | 1 | 1 | 1 | |||

| modif ad.LASSO quant | 1 | 1 | 1 | 1 | 1 | 1 | |||

| or | estimation | ||||||||

| procedure | method | 0 | 0.15 | 0.45 | |||||

| open-end | ad.LASSO expectile | 0.02 | 0.01 | 0.03 | 0.03 | 0.25 | 0.07 | ||

| modif ad.LASSO expect | 0.03 | 0.04 | 0.05 | 0.06 | 0.28 | 0.11 | |||

| ad.LASSO quantile | 0.001 | 0.002 | 0.01 | 0.007 | 0.06 | 0.09 | |||

| modif ad.LASSO quant | 0.03 | 0.09 | 0.06 | 0.13 | 0.12 | 0.24 | |||

| ad.LASSO LS | 1 | 1 | 1 | 1 | 1 | 1 | |||

| modif ad.LASSO LS | 0.004 | 0.001 | 0.005 | 0.004 | 0.02 | 0.02 | |||

| ad.LASSO expectile | 0.06 | 0.06 | 0.12 | 0.09 | 0.36 | 0.21 | |||

| modif ad.LASSO expect | 0.08 | 0.09 | 0.13 | 0.12 | 0.36 | 0.23 | |||

| ad.LASSO quantile | 0.02 | 0.01 | 0.05 | 0.03 | 0.35 | 0.10 | |||

| modif ad.LASSO quant | 0.17 | 0.22 | 0.22 | 0.27 | 0.33 | 0.37 | |||

| ad.LASSO LS | 1 | 1 | 1 | 1 | 1 | 1 | |||

| modif ad.LASSO LS | 0.007 | 0.006 | 0.01 | 0.01 | 0.06 | 0.05 | |||

| closed-end | ad.LASSO expectile | 0.16 | 0.13 | 0.16 | 0.14 | 0.29 | 0.09 | ||

| modif ad.LASSO expect | 0.26 | 0.18 | 0.28 | 0.18 | 0.38 | 0.13 | |||

| ad.LASSO quantile | 0.12 | 0.11 | 0.12 | 0.11 | 0.09 | 0.10 | |||

| modif ad.LASSO quant | 0.21 | 0.33 | 0.21 | 0.32 | 0.16 | 0.27 | |||

| ad.LASSO expectile | 0.23 | 0.21 | 0.24 | 0.21 | 0.28 | 0.23 | |||

| modif ad.LASSO expect | 0.26 | 0.25 | 0.29 | 0.26 | 0.38 | 0.26 | |||

| ad.LASSO quantile | 0.20 | 0.17 | 0.21 | 0.17 | 0.37 | 0.12 | |||

| modif ad.LASSO quant | 0.40 | 0.46 | 0.40 | 0.46 | 0.52 | 0.41 | |||

| open-end | ad.LASSO expectile | 1 | 1 | 1 | 1 | 1 | 1 | ||

| modif ad.LASSO expect | 1 | 1 | 1 | 1 | 1 | 1 | |||

| ad.LASSO quantile | 0.99 | 0.99 | 0.99 | 1 | 1 | 1 | |||

| modif ad.LASSO quant | 0.99 | 0.98 | 0.99 | 0.99 | 1 | 1 | |||

| ad.LASSO LS | 1 | 1 | 1 | 1 | 1 | 1 | |||

| modif ad.LASSO LS | 1 | 1 | 1 | 1 | 1 | 1 | |||

| ad.LASSO expectile | 1 | 1 | 1 | 1 | 1 | 1 | |||

| modif ad.LASSO expect | 1 | 1 | 1 | 1 | 1 | 1 | |||

| ad.LASSO quantile | 0.42 | 0.51 | 0.55 | 0.65 | 0.73 | 0.79 | |||

| modif ad.LASSO quant | 0.30 | 0.33 | 0.43 | 0.49 | 0.63 | 0.75 | |||

| ad.LASSO LS | 1 | 1 | 1 | 1 | 1 | 1 | |||

| modif ad.LASSO LS | 1 | 1 | 1 | 1 | 1 | 1 | |||

| closed-end | ad.LASSO expectile | 1 | 1 | 1 | 1 | 1 | 1 | ||

| modif ad.LASSO expect | 1 | 1 | 1 | 1 | 1 | 1 | |||

| ad.LASSO quantile | 1 | 1 | 1 | 1 | 1 | 1 | |||

| modif ad.LASSO quant | 1 | 1 | 1 | 1 | 1 | 1 | |||

| ad.LASSO expectile | 1 | 1 | 1 | 1 | 1 | 1 | |||

| modif ad.LASSO expect | 1 | 1 | 1 | 1 | 1 | 1 | |||

| ad.LASSO quantile | 0.87 | 0.93 | 0.86 | 0.93 | 0.72 | 0.84 | |||

| modif ad.LASSO quant | 0.79 | 0.82 | 0.79 | 0.84 | 0.69 | 0.81 | |||

| or | estimation | |||||

| method | 0 | 0.15 | 0.45 | |||

| D1 | ad.LASSO expectile | 0.007 | 0.02 | 0.07 | ||

| ad.LASSO quantile | 0.004 | 0.008 | 0.02 | |||

| modif ad.LASSO LS | 0.002 | 0.004 | 0.02 | |||

| ad.LASSO expectile | 0.002 | 0.04 | 0.18 | |||

| ad.LASSO quantile | 0.007 | 0.02 | 0.11 | |||

| modif ad.LASSO LS | 0.01 | 0.02 | 0.08 | |||

| ad.LASSO expectile | 1 | 1 | 1 | |||

| ad.LASSO quantile | 1 | 1 | 1 | |||

| modif ad.LASSO LS | 0.48 | 0.62 | 0.73 | |||

| ad.LASSO expectile | 1 | 1 | 1 | |||

| ad.LASSO quantile | 1 | 1 | 1 | |||

| modif ad.LASSO LS | 0.08 | 0.16 | 0.30 | |||

| D2 | ad.LASSO expectile | 0.002 | 0.008 | 0.14 | ||

| ad.LASSO quantile | 0.001 | 0.004 | 0.06 | |||

| modif ad.LASSO LS | 0.003 | 0.006 | 0.03 | |||

| ad.LASSO expectile | 0.02 | 0.04 | 0.22 | |||

| ad.LASSO quantile | 0.007 | 0.02 | 0.18 | |||

| modif ad.LASSO LS | 0.01 | 0.02 | 0.07 | |||

| ad.LASSO expectile | 1 | 1 | 1 | |||

| ad.LASSO quantile | 0.99 | 0.99 | 0.99 | |||

| modif ad.LASSO LS | 1 | 1 | 1 | |||

| ad.LASSO expectile | 1 | 1 | 1 | |||

| ad.LASSO quantile | 0.08 | 0.17 | 0.43 | |||

| modif ad.LASSO LS | 1 | 1 | 1 | |||

4.1.2. Automatic variable selection comparison

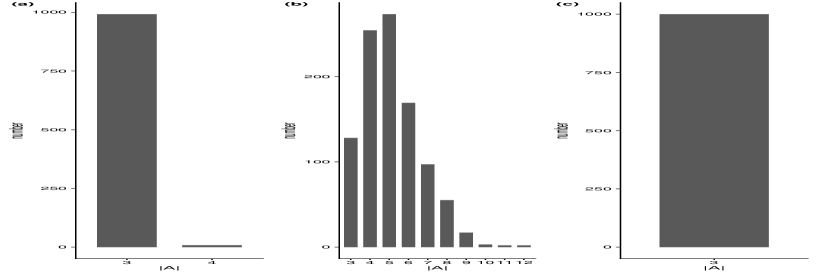

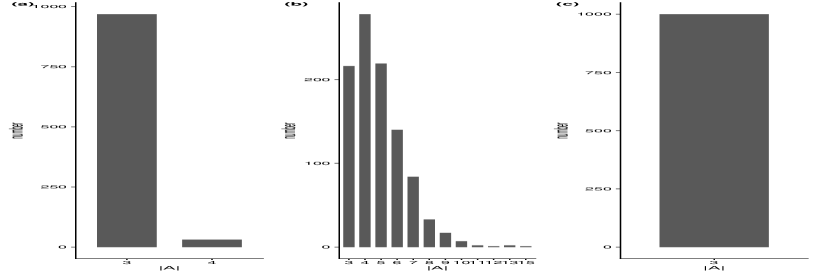

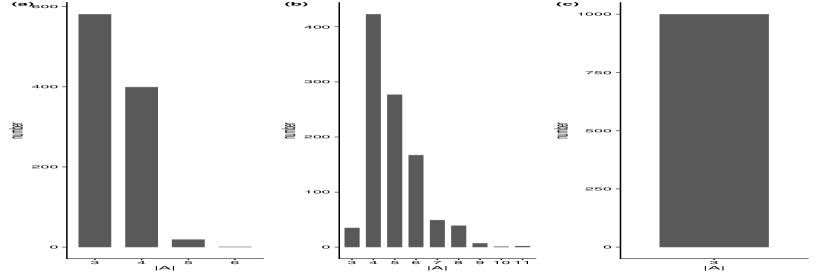

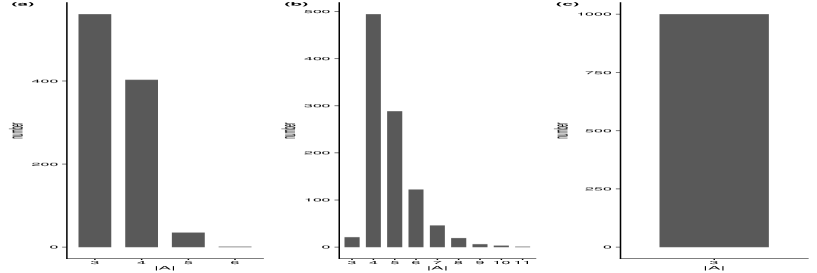

To complete the comparison of the three automatic variable selection methods, in Figures 1 and 2, we represent for expectile, quantile and LS methods with adaptive LASSO penalties, for , , design D1 and 1000 Monte Carlo replications. The errors are Normal in the Figure 1 and of distribution in Figure 2. Similarly we have the histograms of Figures 3 and 4 when the design is D2. We observe that by adaptive LASSO LS method estimation, we obtain , for each Monte Carlo replication. By the adaptive LASSO expectile method, we identify the exact number of non-zero coefficients in most cases, while by the adaptive LASSO quantile method, the exact number of three non-zero coefficients is very rarely found, being overestimated, takes values from 3 to 15. We deduce that the penalized expectile estimation method is superior to that quantile from the point of view of the identification of the true non-zero coefficients when is very close to .

4.1.3. Stopping time estimation

In Table 6 we give some summary statistics (min, median, max) of the stopping times obtained by 2000 Monte Carlo replications for the test statistics constructed on:

-

•

adaptive LASSO expectile residuals;

-

•

expectile residuals (only for );

-

•

adaptive LASSO quantile residuals;

-

•

modified adaptive LASSO LS residuals.

Two possible values for are considered , two model errors , and the two designs D1 and D2. We get the same median of the stopping times by the statistics and when . The results obtained by the statistic built on modified adaptive LASSO LS residuals are in correlation with those of Table 3 because it does not identify the change for each Monte Carlo replication. Consequently, the median and the maximum of the stopping times are (the change was not detected before observation ). The test statistic built on the adaptive LASSO quantile residuals identifies the change much later than the two test statistics proposed in this paper. In general, our two statistics detect earlier the change in a model with asymmetric errors compared to the statistics on the adaptive LASSO quantile and modified adaptive LASSO LS residuals.

| estimation | ||||||

| method | min | median | max | |||

| 100 | D2 | ad. LASSO expectile | 19 | 29 | 43 | |

| modif ad. LASSO LS | 19 | 25 | 29 | |||

| ad. LASSO quantile | 48 | 77 | 147 | |||

| ad. LASSO expectile | 22 | 24 | 32 | |||

| modif ad. LASSO LS | 16 | 22 | 23 | |||

| ad. LASSO quantile | 100 | 159 | 210 | |||

| D1 | ad. LASSO expectile | 26 | 26 | 27 | ||

| modif ad. LASSO LS | 74 | |||||

| ad. LASSO quantile | 67 | 96 | 117 | |||

| ad. LASSO expectile | 24 | 27 | 28 | |||

| modif ad. LASSO LS | 52 | |||||

| ad. LASSO quantile | 52 | 74 | 103 | |||

| 10 | D2 | ad. LASSO expectile | 12 | 12 | 20 | |

| expectile | 12 | 12 | 20 | |||

| modif ad. LASSO LS | 15 | 18 | 20 | |||

| ad. LASSO quantile | 63 | 98 | 166 | |||

| ad. LASSO expectile | 24 | 24 | 41 | |||

| expectile | 12 | 24 | 42 | |||

| modif ad. LASSO LS | 15 | 17 | 21 | |||

| ad. LASSO quantile | 141 | 193 | 209 | |||

| D1 | ad. LASSO expectile | 16 | 24 | 31 | ||

| expectile | 16 | 24 | 31 | |||

| modif ad. LASSO LS | 18 | 75 | 84 | |||

| ad. LASSO quantile | 77 | 96 | 128 | |||

| ad. LASSO expectile | 21 | 31 | 34 | |||

| expectile | 22 | 29 | 34 | |||

| modif ad. LASSO LS | 21 | 78 | 95 | |||

| ad. LASSO quantile | 43 | 69 | 89 | |||

4.1.4. Conclusions of the simulations

The best performing values of that give best results for the test statistics and are of to , the value of the empirical sizes increasing with . If there are no zero model coefficients then, the test statistic built on the expectile residuals make fewer false point-change detections than . Conversely, if the model has irrelevant variables then the statistic gives better results, in terms of , than , especially when is large and close to . Under hypothesis , the obtained values for the empirical size by the open-end procedure are lower than those obtained by the closed-end procedure. For a model with a small or large number of explanatory variables, some of which are irrelevant, the test statistics constructed on the adaptive LASSO expectile residuals, adaptive LASSO quantile residuals and modified adaptive LASSO LS residuals, when the hypothesis is true, that is no change after historical data, give similar results for symmetrical or asymmetrical model errors. Indeed, by the three methods we obtained when . In exchange, if the model changes after the historical data, the test statistics on the adaptive LASSO quantile residuals and on the modified adaptive LASSO LS residuals do not detect the change every time, especially when the model errors have an asymmetric distribution.

On the other hand, the adaptive LASSO expectile estimation method is superior to that of adaptive LASSO quantile estimation method from the point of view of the identification of true non zero coefficients when the number of explanatory variables is very close to the number of historical observations.

The detection delays of the change under hypothesis in a model with asymmetric errors is shorter for our two test statistics than those given by the two comparison test statistics.

All of these, show that our proposed test statistic gives very good results for real-time detection of a change-point and above all it is superior to the statistics constructed on the residuals of the adaptive LASSO quantile and modified adaptive LASSO LS methods, especially when the model error distribution is asymmetrical.

4.2. Applications on real data

This subsection presents two applications on the real data of the test statistics and by the open-end procedure.

4.2.1. Aquatic toxicity towards the fishes

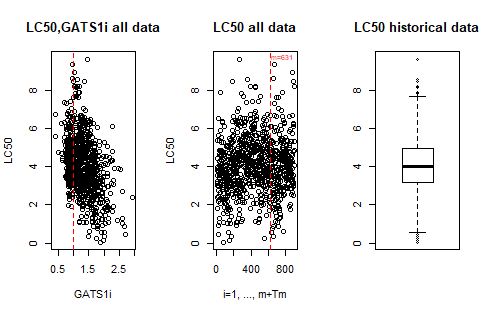

In the first example, the aquatic acute toxicity towards the fish Pimephales promelas is studied. The data proposed by Cassotti et al. (2015) can be downloaded from the Machine Learning Repository site https://archive.ics.uci.edu/ml/datasets/QSAR+fish+toxicity#. The response variable is the aquatic acute toxicity concentration, denoted by LC50. There are six explanatory variables on the molecular descriptors: MLOGP (molecular properties), CIC0 (information indices), GATS1i (2D autocorrelations), NdssC (atom-type counts), NdsCH ((atom-type counts), SM1_Dz (2D matrix-based descriptors). The number of observations in the database is 908. In the left sub-figure of Figure 5 we represent LC50 in respect to GATS1i on the all 908 observations. Taking into account this sub-figure, we reorder the database with respect to the decreasing values of GATS1i and we take as historical observations those for which GATS1i¿1. The number of historical observations is and those from (see the middle sub-figure of Figure 5, where the dotted line is for ). In the right sub-figure of Figure 5 we have the boxplot of LC50 on the historical observations. We observe that the values of LC50 are asymmetrical around the empirical average, the estimated value of the expectile index being 0.469. For , the explanatory variable vector is . We obtain that the expectile estimation of the model coefficients on the historical observations is , while the adaptive LASSO expectile estimation is . Since the coefficient of NdssC in is zero we deduce that this number of atoms does not influence the concentration of LC50 and then . By the two test statistics and we get that there is a change in the model after the historical data. The stopping times are estimated as 30 and 22 by expectile and adaptive LASSO expectile test statistics, respectively. This means that by the test statistic based on the expectile residuals, the model will change as soon as the value of GATS1i is smaller than 0.963 and by the test statistic based on the adaptive LASSO expectile residuals, the model changes as soon as .

4.2.2. NO2 pollution data

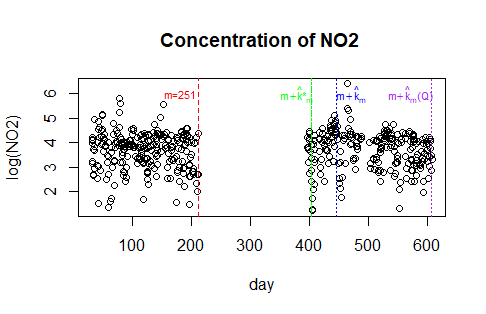

In this second example we take the one presented in Ciuperca (2018) where a test statistic built on the adaptive LASSO quantile estimator was used to detect a change in a linear model of NO2 pollution with respect to six explanatory variables: logarithm of the number of cars per hour, temperature 2 m above ground, wind speed, temperature difference between 25 and 2 m above ground, wind direction, hour of day when the data were measured. Note that there may be days with several measures and days without measures. Historical data measured between November 1, 2001 and April 30, 2002, contains 251 observations for 212 days. From May 1, 2002 there are no data until October 31 (inclusive), 2002 and therefore there is a gap in Figure 6. From November 1, 2002 other were made for 211 days, until August 2003. The all values of NO2 are represented in Figure 6 where with the red dotted vertical line we represented the observation . The data come from the Dept. of Statistics, Carnegie Mellon University and can be uploaded to http://lib.stat.cmu.edu/datasets/NO2.dat. By the adaptive LASSO quantile estimation method, Ciuperca (2018) got that the number of cars per hour and the temperature difference between 25 and 2 m are relevant variables for NO2. The associated test statistic detects a change to observation 248 after the historical data. For the estimated expectile index equal to 0.62, we obtain that only adaptive LASSO estimation of the coefficient of the number of cars is different from zero. The test statistics detects a change to observation 70 after the historical data and to observation 14. In Figure 6 we have drawn with dotted lines in green and blue the observations where the change is detected by and , respectively. Then, the two test statistics proposed in the present paper detect earlier the change in the model compared to the change found by the statistic based on the adaptive LASSO quantile estimator proposed by Ciuperca (2018), drawn with a vertical purple dotted line in Figure 6. The results are summarized in Table 7. In Table 7 and Figure 6, is the stopping time of relation (3.4) obtained by , of (3.1) by and by test statistic built on the adaptive LASSO quantile residuals of Ciuperca (2018).

| April 30, 2002 | November 8, 2002 | December 20, 2002 | July 30, 2003 |

5. Proofs

Proof of Proposition 2.1. The expectile estimator is the solution of the system of equations: . Then:

| (5.1) |

On the other hand, by elementary calculations, for , we have:

| (5.2) |

Taking into account assumption (A1) and since , we have for , :

Then, we can write relation (5.1):

| (5.3) |

By assumptions (A2) and (A3) and since , we have by the law of large numbers (LLN):

| (5.4) |

On the other hand, since , together with assumption (A1), by the Bienaymé-Tchebychev inequality, we have:

| (5.5) |

Combining relations (5.3), (5.4), (5.5) and assumptions (A1), (A3), we obtain:

The proposition is proved.

Recall the Hoeffding’s inequality which will be used in the proof of Lemma 2.1.

Hoeffding’s inequality (Hoeffding (1963)): If are independent random variables, and two real sequences with and , for any , then for all :

Proof of Lemma 2.1. For all , we can write the function as: .Then, for , with and a positive constant, we have for ,

Hence, for , the -th component of the random process is:

In order to study , let us consider the random variable: .

Using the identity that, for all : , then we can write: . Thus, we have: . Furthermore, using assumption (A1) we have that the component is bounded with probability 1, by , with a constant. Let’s take in Hoeffding inequality , for and . Then, for all we have:

| (5.6) |

We take , for any positive constant . Then, relation (5.6) becomes, for all :

| (5.7) |

Thus, relation (5.7) implies that for all such that , for all , there exists a constant such that:

and Lemma follows.

Proof of Theorem 3.1.

We first show that the supremum of cannot be reached for small. Effectively, if is small then . On the other hand, since , taking into account assumptions (A1) and (A3), the fact that is a continuous Borel function, then we have that: . Thus, taking into account assumption (A1), we have: and therefore . Hence, for small we have, .

We therefore consider that and we study first in two cases.

-

a) if , then, taking into account that , we have:

-

b) If , then , from where, with the notation , we get:

But and . Moreover , from where . These last two relations imply .

Thus, we showed in cases a) and b) that . On the other hand, by Lemma 2.1 we have, for , , that:

| (5.8) |

For the expectation in the right-hand side of (5.8), since hypothesis is true, using relation (5.2), together with the supposition that of (A3) and assumption (A1), we have:

We replace this last relation in (5.8) and we obtain:

| (5.9) |

On the other hand, by Proposition 2.1, we have:

We take then and relation (5.9) becomes:

| (5.10) |

But, by assumption (A2), since is large, we have: . Thus, relation (5.10) becomes:

This relation implies, taking into account the definition of :

| (5.11) |

According to the K-M-T approximation, there exists two independent -dimensional Wiener processes and such that, for and (see Komlós et al. (1975) and Komlós et al. (1976)):

| (5.12) |

and

| (5.13) |

Then, taking into account relations (5.11), (5.12) and (5.13), we obtain:

| (5.14) |

On the other hand, as in the proof of Theorem 2.1 of Horváth et al. (2004) we have that:

| (5.15) |

with a Wiener process of dimension . It remains to study the two remainders in relation (5.11). By Lemma 2 of Zhou et al. (2015) we have:

| (5.16) |

For the second remainder, we have:

| (5.17) |

-

If , then and also:

-

a) ,

-

b) ,

-

c) .

From a), b), c) we obtain that in the case , relation (5.17) is for .

-

-

If , using Lemma 2 of Zhou et al. (2015), we have:

In conclusion we obtain that relation (5.17) is . Combining this with relations (5.16), (5.15), (5.14) and (5.11), the theorem follows.

Proof of Theorem 3.2. We prove the theorem for the open-end procedure. The proof for the closed-end procedure is similar. Without reducing the generality, we suppose that , with and we will show that there is an observation for which the test statistic diverges. We consider and we study the following random vector:

| (5.18) |

Similarly to the proof of Theorem 3.1, we have that there exists a constant such that,

with probability converging to 1 as .

Since the function is increasing in , we have:

| (5.19) |

with probability converging to 1 as .

For the random vector given by (5.18) it remains to study . For this, taking into account the convergence rate of towards , let us consider the following sum, for , with :

| (5.20) |

For the mean of the random process , using Lemma 2 of Gu and Zou (2016) and relation (5.20), we have that:

with a constant such that .

Using the supposition that: and since , we get:

| (5.21) |

If , then, relation (5.21) implies that

and using the LLN we obtain:

| (5.22) |

If such that then,

| (5.23) |

On the other hand, by the Central Limit Theorem, we have:

| (5.24) |

Therefore, combining (5.20), (5.22), (5.23), (5.24), we obtain:

| (5.25) |

(see also relation (4.25) of Ciuperca (2017)). Because the convergence rate of to is of order , relation (5.25) implies:

| (5.26) |

The theorem follows by combining relations (5.19) and (5.26).

Proof of Proposition 3.1. The Karush-Kuhn-Tucker optimality conditions for the adaptive LASSO expectile estimator are:

| (5.27) |

| (5.28) |

with the sign of : for and .

Taking into account the convergence rate of the expectile estimator towards and the supposition of assumption (A5), we have for all :

| (5.29) |

From relation (5.27) we get from all :

| (5.30) |

Using relation (5.2) and the convergence in probability of to , we have:

Taking into account this last relation in (5.30), we obtain for all :

| (5.31) |

Taking into account (5.28), (5.29) and (5.31) we obtain by the same arguments as in the proof of Proposition 2.1 that:

i.e. the claim of the proposition.

Proof of Theorem 3.3. Taking inspiration from the approach used for the test statistic built on the expectile residuals, let us consider

If small, using Lemma 2 of Gu and Zou (2016) and since , we have:

If large. By Lemma 2.1 we have:

| (5.32) |

with . For the expectation in the right-hand side of (5.32) we have, combining relation (5.2), together with the supposition that of (A3), with assumption (A1), that:

| (5.33) |

Since and , then we can take in the definition of . Thus, we obtain:

| (5.34) |

On the other hand, combining relations (5.32) and (5.33) we have:

| (5.35) |

By Proposition 3.1 we have that

Then, relation (5.35) becomes:

Thus, taking also into account relation (5.34) combined with given by relation (5.5), with assumption (A2), we obtain:

from where

| (5.36) |

On the other hand, for the two remainders of relation (5.36), as , we have:

The end of the proof is similar to that of Theorem 3.1.

Proof of Corollary 3.1.

The proof is similar to that of Corollary 1 in Ciuperca (2018) and it is omitted.

Proof of Theorem 3.4 In order to expose the major points of the argument, the proof is presented for only, the other cases being similar. Consider the observation . For the denominator of the statistic we make the decomposition:

By the proof of Theorem 3.3 we have with the probability converging to 1 as , that:

Taking into account the convergence rate of towards (see Theorem 2.1 of Ciuperca (2020)) and the sparsity property of , let the random process:

with , . Taking into account relation (3.3), we have:

with , .

We start with the study of .

For , let be the probability . Since , together with the fact that is a continuous Borel function, we get that: for any .

For , let be the independent random variables which takes the value 0 with probability .

The variance of exists and is bounded.

Then, by the Bienaymé-Tchebychev inequality, taking into account also assumption (A1), we obtain that for all :

Thus,

which implies .

We now study . As in the proof of Theorem 3.2 we have:

and the end of the proof is similar to that of Theorem 3.2.

References

- Cassotti et al. (2015) Cassotti M, Ballabio D, Todeschini R, Consonni V (2015) A similarity-based QSAR model for predicting acute toxicity towards the fathead minnow (Pimephales promelas). SAR and QSAR in Environmental Research 26:217–243.

- Chen and Hu (2017) Chen Z, Hu Y (2017) Cumulative sum estimator for change-point in panel data. Statist Papers 58(3):707–728.

- Ciuperca (2015) Ciuperca G (2015) Real time change-point detection in a model by adaptive LASSO and CUSUM. J SFdS 156(4):113–132.

- Ciuperca (2016) Ciuperca G (2016) Adaptive LASSO model selection in a multiphase quantile regression. Statistics 50(5):1100–1131.

- Ciuperca (2017) Ciuperca G (2017) Real Time Change-point Detection in a Nonlinear Quantile Model. Sequential Anal 36(1):1–23.

- Ciuperca (2018) Ciuperca G (2018) Test by adaptive LASSO quantile method for real-time detection of a change-point. Metrika 81:689–720.

- Ciuperca (2020) Ciuperca G (2020) Variable selection in high-dimensional linear model with possibly asymmetric errors. In revision to Comput Statist Data Anal, https://arxiv.org/abs/1812.03121

- Geng et al. (2019) Geng J, Zhang B, Huie LM, Lai L (2019) Online change-point detection of linear regression models. IEEE Trans Signal Process 67(12):3316–3329.

- Gronneberg and Holcblat (2019) Gronneberg S, Holcblat B (2019) On partial-sum processes of ARMAX residuals. Ann Statist 47(6):3216–3243.

- Gu and Zou (2016) Gu Y, Zou H (2016) High-dimensional generalizations of asymmetric least squares regression and their applications. Ann Statist 44(6):2661–2694.

- Hoeffding (1963) Hoeffding W (1963) Probability inequalities for sums of bounded random variables. J Amer Statist Assoc 58: 13–30.

- Horváth and Rice (2019) Horváth L, Rice G (2016) Asymptotics for empirical eigenvalue processes in high-dimensional linear factor models. J Multivariate Anal 169:138–165.

- Horváth et al. (2004) Horváth L, Hušková M, Kokoszka P, Steinebach J (2004) Monitoring changes in linear models. J Statist Plann Inference 126(1):225–251.

- Hušková and Kirch (2012) Hušková M, Kirch C (2012) Bootstrapping sequential change-point tests for linear regression. Metrika 75(5):673–708.

- Jiang and Kurozumi (2019) Jiang P, Kurozumi E (2019) Power properties of the modified CUSUM tests. Comm Statist Theory Methods 48(12):2962–2981.

- Jiang and Kurozumi (2020) Jiang P, Kurozumi E (2020) Monitoring parameter changes in models with a trend. J Statist Plann Inference 207:288–319.

- Kirch and Weber (2018) Kirch C, Weber S (2018) Modified sequential change point procedures based on estimating functions. Electron J Statist 12(1):1579–1613.

- Koenker (2005) Koenker R (2005) Quantile Regression Econometric Society Monographs. 38, Cambridge University Press, Cambridge.

- Komlós et al. (1975) Komlós J, Major P, Tusnády G (1975) An approximation of partial sums of independent RV’s, and the sample DF. I. Z Wahrsch Verw Gebiete 32:111–131.

- Komlós et al. (1976) Komlós J, Major P, Tusnády G (1976) An approximation of partial sums of independent RV’s, and the sample DF. II. Z Wahrsch Verw Gebiete 34:33–58.

- Liao et al. (2019) Liao L, Park C, Choi H (2019) Penalized expectile regression: an alternative to penalized quantile regression. Ann Inst Statist Math 71(2):409–438.

- Liu et al. (2019) Liu B, Zhou C, Zhang X (2019) A tail adaptive approach for change point detection. J Multivariate Anal 169:33–48.

- Nedényi (2018) Nedényi FK (2018) An online change detection test for parametric discrete-time stochastic processes. Sequential Anal 37(2):246–267.

- Newey and Powell (1987) Newey WK, Powell JL (1987) Asymmetric least squares estimation and testing. Econometrica 55(4):818–847.

- Oh and Lee (2019) Oh H, Lee S (2019) Modified residual CUSUM test for location-scale time series models with heteroscedasticity. Ann Inst Statist Math 71(5):1059–1091.

- Prášková (2018) Prášková Z (2018) Change point detection in vector autoregression. Kybernetika 54(6):1122–1137.

- Qi et al. (2016) Qi P, Duan X, Tian Z, Li F (2016) Sequential monitoring for changes in models with a polynomial trend. Comm Statist Simulation Comput 45(1):222–239.

- Song and Kang (2020) Song J, Kang J (2020) Sequential change point detection in ARMA-GARCH models. J Stat Comput Simul 90(8):1520–1538.

- Zhang and Li (2017a) Zhang F, Li Q (2017a) A continuous threshold expectile model. Comput Statist Data Anal 116:49–66.

- Zhang and Li (2017b) Zhang F, Li Q (2017b) Robust bent line regression. J Statist Plann Inference 185:41–55.

- Zhao et al. (2018) Zhao J, Chen Y, Zhang Y (2018) Expectile regression for analyzing heteroscedasticity in high dimension. Statist Probab Lett 137:304–311.

- Zhou et al. (2015) Zhou M, Wang HJ, Tang Y (2015) Sequential change point detection in linear quantile regression models. Statist Probab Lett 100:98–103.

- Zou (2006) Zou H (2006) The adaptive Lasso and its oracle properties. J Amer Statist Assoc 101(476):1418–1428.