Distributionally Robust Losses

for Latent Covariate Mixtures

John C. Duchi1 Tatsunori Hashimoto2 Hongseok Namkoong3

Departments of 1Statistics, Electrical Engineering, and 2Computer Science, Stanford University

3Decision, Risk, and Operations Division, Columbia Business School

{jduchi,thashim}@stanford.edu, namkoong@gsb.columbia.edu

Abstract

While modern large-scale datasets often consist of heterogeneous subpopulations—for example, multiple demographic groups or multiple text corpora—the standard practice of minimizing average loss fails to guarantee uniformly low losses across all subpopulations. We propose a convex procedure that controls the worst-case performance over all subpopulations of a given size. Our procedure comes with finite-sample (nonparametric) convergence guarantees on the worst-off subpopulation. Empirically, we observe on lexical similarity, wine quality, and recidivism prediction tasks that our worst-case procedure learns models that do well against unseen subpopulations.

1 Introduction

When we train models over heterogeneous data, a basic goal is to train models that perform uniformly well across all subpopulations instead of just on average. For example, in natural language processing (NLP), large-scale corpora often consist of data from multiple domains, each domain varying in difficulty and frequently containing large proportions of easy examples [21]. Standard approaches optimize average performance, however, and yield models that accurately predict easy examples but sacrifice predictive performance on hard subpopulations [62].

The growing use of machine learning systems in socioeconomic decision-making problems, such as loan-servicing and recidivism prediction, highlights the importance of models that perform well over different demographic groups [6]. In the face of this need, a number of authors observe that optimizing average performance often yields models that perform poorly on minority subpopulations [3, 36, 41, 17, 66, 76]. When datasets contain demographic information, a natural approach is to optimize worst-case group loss or equalize losses over groups. But in many tasks—such as language identification or video analysis [76, 17]—privacy concerns preclude recording demographic or other sensitive information, limiting the applicability of methods that require knowledge of demographic identities. For example, lenders in the United States are prohibited from asking loan applicants for racial information unless it is to demonstrate compliance with anti-discrimination regulation [20, 22].

To address these challenges, we seek models that perform well on each subpopulation rather than those that achieve good (average) performance by focusing on the easy examples and domains. Thus, in this paper we develop procedures that control performance over all large enough subpopulations, agnostic to the distribution of each subpopulation. We study a worst-case formulation over large enough subpopulations in the data, providing procedures that automatically focus on the difficult subsets of the dataset. Our procedure guarantees a uniform level of performance across subpopulations by hedging against unseen covariate shifts, potentially even in the presence of confounding.

In classical statistical learning and prediction problems, we wish to predict a target from a covariate vector drawn from an underlying population , measuring performance of a predictor via the loss . The standard approach is to minimize the population expectation . In contrast, we consider an elaborated setting in which the observed data comes from a mixture model, and we evaluate model losses on a component (subpopulation) from this mixture. More precisely, we assume that for some mixing proportion , the data are marginally distributed as , while the subpopulations and are unknown. The classical formulation does little to ensure equitable performance for data from both and , especially for small . Thus for a fixed conditional distribution , we instead seek that minimizes the expected loss under the latent subpopulation

| (1) |

We call this loss minimization under mixture covariate shifts.

As the latent mixture weight and components are unknown, it is impossible to compute the loss (1) from observed data. Thus, we postulate a lower bound on the subpopulation proportion and consider the set of potential minority subpopulations

Concretely, our goal is to minimize worst-case subpopulation risk ,

| (2) |

The worst-case formulation (2) is a distributionally robust optimization (DRO) problem [9, 70] where we consider the worst-case loss over mixture covariate shifts , and we term the methodology we develop around this formulation marginal distributionally robust optimization, as we seek robustness only to shifts in the marginals over the covariates . For datasets with heterogeneous subpopulations (e.g. natural language processing corpora), the worst-case subpopulation corresponds to a group that is “hard” under the current model . As we detail in the related work section, the approach (2) has connections with covariate shift problems, distributional robustness, fairness, and causal inference. In particular, the dual form of (2) corresponds to the conditional-value-at-risk (CVaR) of the conditional risk .

In some instances, the worst-case subpopulation (2) may be too conservative; the distribution of may shift only on some components, or we may only care to achieve uniform performance across one variable. As an example, popular computer-vision datasets draw images mostly from western Europe and the United States [68], but one may wish for models that perform uniformly well over different geographic locations. In such cases, when one wishes to consider distributional shifts only on a subset of variables (e.g. geographic location) of the covariate vector , we may simply redefine as , and as in the problem (2). All of our subsequent discussion generalizes to such scenarios.

On the other hand, because of confounding, the assumption that the conditional distribution does not change across groups may be too optimistic. While the assumption is appropriate for machine learning tasks where human annotators use to generate the label , many problems include unmeasured confounding variables that affect the label and vary across subpopulations. For example, in a recidivism prediction task, the feature may be the type of crime, the label represents re-offending, and the subgroup may be race; without measuring unobserved variables, such as income or location, is likely to differ between groups. To address this issue, in Section B we generalize our proposed worst-case loss (2) to incorporate worst-case confounding shifts, providing finite-sample upper bounds on worst-case loss whose tightness depends on the effect of the unmeasured confounders on the conditional risk .

1.1 Overview of results

In the rest of the paper, we construct a tractable finite sample approximation to the worst-case problem (2), and show that it allows learning models that perform uniformly well over subpopulations. Our starting point is the duality result (see Section 2.1)

For convex losses, the dual form yields a single convex loss minimization in the variables for minimizing . When we (approximately) know the conditional risk —for example, when we have access to replicate observations for each —it is reasonably straightforward to develop estimators for the risk (2) (see Section 2.2).

Estimating the conditional risk via replication is infeasible in scenarios in which corresponds to a unique individual (similar to issues in estimation of conditional treatment effects [44]). Alternative procedures that depend on parametric assumptions on the family of conditional risks for all are restrictive, as we study learning problems over a flexible class of machine learning models (e.g., random forests, gradient boosted decision trees, kernel methods, neural networks). In this work, we instead consider a scalable nonparametric approach involving the variational representation

| (3) |

As the space is too large to effectively estimate the quantity (3), we consider approximations via easier-to-control function spaces and study the problem

| (4) |

By choosing appropriately—e.g. as a reproducing kernel Hilbert space [11, 25] or a collection of bounded Hölder continuous functions—we can develop analytically and computationally tractable approaches to minimizing Eq. (4) to approximate Eq. (2).

Since the variational approximation to the dual objective is a lower bound on the worst-case subpopulation risk , it does not (in general) provide uniform control over subpopulations . Motivated by empirical observations that confirm the limitations of this approach, we propose and study a more “robust” formulation than the problem (2) that provides a natural upper bound on the worst-case subpopulation risk . Our proposed formulation variational form analogous to Eq. (4) and is estimable. If we consider a broader class of distributional shifts, we arrive at a more conservative formulation than the problem (2). Define the Rényi divergence-ball [78] of order

Then for and , Lemma 2.1 and Duchi and Namkoong [27, Section 3.2] show

Abstracting the particular choice of uncertainty in , for , the dual reformulation [69, 27]

| (5) |

always upper bounds the worst-case subpopulation performance (2). As we show in Section 4, for Lipschitz conditional risks , Eq. (5) is equal to a variant of the problem (4) where we take to be a particular collection of Hölder-continuous functions allowing estimation from data. Because our robustness approach in this paper is new, there is limited analysis—either empirical or theoretical—of similar problems. Consequently, we perform some initial empirical evaluation on simulations to suggest the appropriate approximation spaces in the dual form (4) (see Section 3). Our empirical analysis shows that the upper bound (5) provides good performance compared to other variational procedures based on (4), which informs our theoretical development and more detailed empirical evaluation to follow.

We develop an empirical surrogate to the risk (5) in Section 4. A key advantage of our finite-sample procedure is that it does not depend on unrealistic parametric assumptions on the conditional risk . Our main theoretical result—Theorem 1—shows that the model minimizing this empirical surrogate achieves

with high probability whenever is suitably smooth. In a rough sense, then, we expect that trades between approximation error—via the gap between and —and estimation error.

While our convergence guarantee gives the nonparametric rate , we empirically observe that our procedure achieves low worst-case losses even when the dimension is large. We conjecture that this follows because our empirical approximation to the norm bound (5) is an upper bound with error only , but a lower bound at the conservative rate . Such results—which we present at the end of Section 4—seem to point to the conservative nature of our convergence guarantee in practical scenarios. In our careful empirical evaluation on semantic similarity assessment and recidivism prediction tasks (Section 6), we observe that our procedure learns models that perform uniformly well across unseen minority subpopulations and difficult examples. Nevertheless, the pessimistic dependence on the dimension is unavoidable under nonparametric assumptions on the conditional risk , as we show in Section 5. In light of these fundamental hardness results, identifying a realistic yet restricted class of conditional risks that allow faster statistical convergence is an interesting topic of future work.

1.2 Related work

Several important issues within statistics and machine learning closely relate to our goals of uniform performance across subpopulations. We briefly touch on a few of these connections here and hope that further linking them may yield alternative approaches and deeper insights.

Covariate shifts.

A number of authors study the case where a target distribution of interest is different from the data-generating distribution—known as covariate shift or sample selection bias [71, 8, 75]. Much of the work focuses on the domain adaptation setting where the majority of the observations come from a source population (and corresponding domain) . These methods require (often unsupervised) samples from an a priori fixed target domain, and apply importance weight methods to reweight the observations when training a model for the target [74, 13, 35, 43]. For multiple domains, representation based methods can identify sufficient statistics not affected by covariate shifts [40, 34].

On the other hand, our worst-case formulation assumes no knowledge of the latent group distribution (unknown target) and controls performance on the worst subpopulation of size larger than . Kernel-based adversarial losses [79, 53, 54] minimize the worst-case loss over importance weighted distributions, where the importance weights lie within a reproducing kernel Hilbert space. These methods are similar in that they consider a worst-case loss, but these worst-case weights provide no guarantees (even asymptotically) for latent subpopulations.

Distributionally robust optimization.

A large body of work on distributionally robust optimization (DRO) methods [10, 12, 49, 58, 28, 59, 30, 67, 16, 72, 51, 32, 15, 33, 48, 73, 47] solves a worst-case problem over the joint distribution on . On the other hand, our marginal DRO formulation (2) studies shifts in the marginal covariate distribution . Concretely, we can formulate an analogue of our marginal formulation (2)

| (6) |

where is the set of joint distributions over such that for some and probability on . The joint DRO objective (6) upper bounds the marginal worst-case formulation (2), and is frequently too conservative (see Section 2). By providing a tighter bound on the worst-case loss (2) under mixture covariate shifts, our proposed finite-sample procedure (16) achieves better performance on unseen subpopulations (see Sections 4 and 6). For example, the joint DRO bound (6) applied to zero-one loss for classification may result in a degenerate non-robust estimator that upweights all misclassified examples [42], but our marginal DRO formulation mitigates these issues by using the underlying metric structure.

Similar to our formulation (2), distributionally robust methods defined with appropriate Wasserstein distances—those associated with cost functions that are infinity when values of differ—also consider distributional shifts in the marginal covariate distribution . Such formulations allow incorporating the geometry of , and consider local perturbations in the covariate vector (with respect to some metric on ). Our worst-case subpopulation formulation (2) departs from these methods by considering all large enough mixture components (subpopulations) of , giving strong fairness and tail-performance guarantees for learning problems.

Fairness.

A growing literature recognizes the challenges of fairness within statistical learning [29, 37, 46, 45, 38, 22], which motivates our approach as well. Among the many approaches to this problem, researchers have proposed that models with similar behavior across demographic subgroups are fair [29, 45]. The closest approach to our work is the use of Lipschitz constraints as a way to constrain the labels predicted by a model [29]. Rather than directly constraining the prediction space, we use the Lipschitz continuity of the conditional risk to derive upper bounds on model performance. The gap between joint DRO and marginal DRO relates to “gerrymandering” [45]: fair models can be unreasonably pessimistic by guaranteeing good performance against minority subpopulations with high observed loss—which can be a result of random noise—rather than high expected loss [29, 45, 39]. Our marginal DRO approach mitigates such gerrymandering behavior relative to the joint DRO formulation (6); see Section 4 for a more detailed discussion.

Causal inference.

A common goal in causal inference is to learn models that perform well under interventions, and one formulation of causality is as a type of invariance across environmental changes [61]. In this context, our formulation seeking models with low loss across marginal distributions on is an analogue of observational studies in causal inference. Bühlmann, Meinshausen, and colleagues have proposed a number of procedures similar in spirit to our marginal DRO formulation (2), though the key difference in their approaches is that they assume that underlying environmental changes or groups are known. Their maximin effect methods find linear models that perform well over heterogeneous data relative to a fixed baseline with known or constrained population structure [56, 64, 19], while anchor regression [65] fits regression models that perform well under small perturbations to feature values. Heinze-Deml and Meinshausen [40] consider worst-case covariate shifts, but assume a decomposition between causal and nuisance variables, with replicate observations sharing identical causal variables. Peters et al. [61] use heterogeneous environments to discover putative causal relationships in data, identifying robust models and suggesting causal links. Our work, in contrast, studies models that are robust to mixture covariate shifts, a new type of restricted intervention over all large enough subpopulations.

2 Performance Under Mixture Covariate Shift

We begin by reformulating the worst-case loss over mixture covariate shifts (2) via its dual (Section 2.1). We first consider a simpler setting in which we can collect replicate labels for individual feature vectors —essentially, the analogue of a randomized study in causal inference problems—showing that in this case appropriate sample averages converge quickly to the worst-case loss (2) (Section 2.2). Although this procedure provides a natural gold standard when is estimable, it is impossible to implement when large sets of replicate labels are unavailable. This motivates the empirical fitting procedure we propose in Eq. (16) to come, which builds out of the tractable upper bounds we present in Section 4.

2.1 Upper bounds for mixture covariate shift

Taking the dual of the inner maximization problem over covariate shifts (2) gives the below result.

Lemma 2.1.

If , then

| (7) |

If additionally w.p. 1, the infimizing lies in .

See Section D.1 for the proof. The dual form (7) is the conditional-value-at-risk (CVaR) of the conditional risk ; CVaR is a common measure of risk in the portfolio and robust optimization literatures [63, 70], but there it applies to an unconditional loss, making it (as we discuss below) conservative for the problems we consider.

The joint DRO (6) problem is more conservative than its marginal counterpart (7) where the adversary selects over distributions with a fixed ; the joint DRO dual objective is greater than the marginal DRO (7) unless is a deterministic function of . In Section 4, we provide an approximation to the marginal DRO dual form (7), and one of our contributions is to show that our procedure has better theoretical and empirical performance than conservative estimators using the joint DRO objective (6). Furthermore, we expect the joint DRO problem to exhibit particular sensitivity to outliers in unlike its marginal counterpart. Both joint and marginal DRO are sensitive to outliers in —addressing this is an important topic of future research.

To illustrate the advantages of the marginal distributionally robust approach, consider a misspecified linear regression problem, where we predict and use absolute the loss . Letting , the following mixture model generates the data

| (8) |

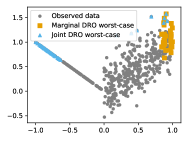

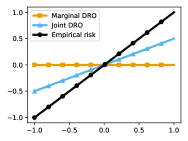

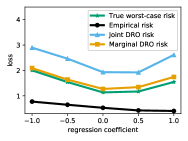

so that the subpopulation has minority proportion . We plot observations from this model in Figure 1(a), where 85% of the points are on the right, and have high noise. The model with the best uniform performance is near , which incurs similar losses between left and right groups. In contrast, the empirical risk minimizer () incurs a high loss of on the left group and on the right one.

Empirical risk minimization tends to ignore the (left) minority group, resulting in high loss on the minority group (Figure 1(b)). The joint DRO solution (6) minimizes losses over a worst-case distribution consisting of examples that receive high loss (blue triangles), which tend to be samples on due to noise. This results in a loose upper bound on the true worst-case risk as seen in Figure 1(c). Our proposed estimator selects a worst-case distribution consisting of examples with high conditional risk (Figure 1(a), orange squares). This worst-case distribution is not affected by the noise level, and results in a close approximation to the true loss (Figure 1(c)).

2.2 Estimation via replicates

A natural approach to estimating the dual form (7) is a two phase strategy, where we draw and then—for each in the sample—draw a secondary sample of size i.i.d. from the conditional . We then use these empirical samples to estimate . While it is not always possible to collect replicate labels for a single , human annotated data—which is common in machine learning applications [55, 5]—allows replicate measurement, where we may ask multiple annotators to label the same .

We show this procedure can yield explicit finite sample bounds with error at most for the population marginal robust risk (2) when the losses are bounded.

Assumption A1.

For , we have for all .

Since we often want to show uniform concentration guarantees over , we make the following standard assumption to control the size of the model class.

Assumption A2.

is -Lipschitz a.s., and .

The following estimate approximates the worst-case loss (2) for a fixed value of .

Proposition 1.

See Section D.2 for the proof. The estimator in Proposition 1 approximates the worst-case loss (2) well for large enough and . However—similar to the challenges of making causal inferences from observational data and estimating conditional treatment effects—it is frequently challenging or impossible to collect replicates for individual observations , as each represents an unrepeatable unique measurement. Consequently, the quantity in Proposition 1 is a type of gold standard, but achieving it can be practically challenging.

3 Variational Approximation to Worst-Case Loss

The difficulty of collecting replicate data, coupled with the conservativeness of the joint DRO objective (6) for approximating the worst-case loss , impel us to study tighter approximations that do not depend on replicates. Recalling the variational representation (3), our goal is to minimize

As we note in the introduction, this quantity is challenging to work with, so we restrict to subsets . The advantage of this formulation and its related relaxations (4) is that it replaces the dependence on the conditional risk with an expectation over the joint distribution on , which we may estimate using the empirical distribution, as we describe in the next section.

Each choice of a collection of functions to approximate the variational form (3) in the formulation (4) yields a new optimization problem. The lack of a “standard” choice motivates us to perform experiments to direct our development. In Section A, we develop several candidate approximations that are computationally feasible. A priori it is unclear whether different formulations should yield better performance; at least at this point, our theoretical understanding provides similarly limited guidance. To this end, we perform a small simulation study in Section A.2 to direct our coming deeper theoretical and empirical evaluation, discussing the benefits and drawbacks of various choices of through the example we introduce in Figure 1(a), Section 2.1. For ease of exposition, we initially defer these comparisons to Section A and focus on developing the approximation method that exhibits the best empirical performance.

We consider the upper bound (5) on as—as we shall see—it provides the best empirical performance. Recall that a function is -Hölder continuous for and if for all . We consider the function class consisting of bounded Hölder functions, which we motivate via an -norm bound (5) on the dual objective (7). For any and we have

| (9) |

If is Hölder continuous, then the function

| (10) |

attaining the supremum in the variational form (9) is Hölder continuous with constant dependent on the magnitude of the denominator. As we show shortly, carefully selecting the smoothness constant and norm radius allows us to ensure and to derive guarantees for the resulting estimator.

Minimizing the upper bound rather than the original variational objective (alternatively, seeking higher-order robustness than the CVaR of the conditional risk as in our discussion of the quantity (5)) incurs approximation error. In practice, our experience is that this gap has limited effect, and the following lemma—whose proof we defer to Section D.4—quantifies the approximation error in inequality (9).

Lemma 3.1.

Let Assumption A1 hold and . For

We now formally show that the variational form provides a tractable upper bound to the worst-case loss for Lipschitzian conditional risks.

Assumption A3.

For , the mappings and are -Lipschitz.

To ease notation let denote the space of Hölder continuous functions

| (11) |

If Assumption A3 holds and the denominator in the expression (10) has lower bound , then , and we can approximate the variational form (9) by solving an analogous problem over smooth functions. Otherwise, we can bound the -norm (9) by , which is small for small values of . Hence, if we define a variational objective over smooth functions

| (12) |

we arrive at a tight approximation to the variational form (9), which we prove in Section D.5.

4 Tractable Risk Bounds for Variational Problem

In this section, we develop an empirical approximation to the norm bounded Hölder class, and formally develop and analyze a marginal DRO estimator . We derive this estimator by solving an empirical approximation of the upper bound (12) and provide a number of generalization guarantees for this procedure. We complement these results in Section 5 and quantify the fundamental hardness of optimizing over subpopulations using finite samples.

4.1 The empirical estimator

Since the variational approximation does not use the unknown conditional risk , its empirical plug-in is a natural finite-sample estimator. Defining

| (13) |

we consider the estimator

| (14) |

The following lemma shows that the plug-in is the infimum of a convex objective.

Lemma 4.1.

For a sample and , define the empirical loss

| (15) |

Then for all .

See Section D.6 for proof. We can interpret dual variables as a transport plan for transferring the loss from example to in exchange for a distance dependent cost represented by the last term in the preceding display. The objective thus consists of transport costs and any losses larger than after smoothing according to the transport plan .

Noting that is jointly convex in —and jointly convex in if the loss is convex—we consider the empirical minimizer

| (16) |

as an approximation to the worst-case mixture covariate shift problem (2). We note that interpolates between the marginal and joint DRO solution; as , in the infimum over and , an existing empirical approximation to the joint DRO problem [27].

4.2 Generalization and uniform convergence

We now turn to uniform convergence guarantees based on concentration of Wasserstein distances, which show that the empirical minimizer in expression (16) is an approximately optimal solution to the population bound (5). First, we prove that the empirical plug-in (14) converges to its population counterpart at the rate . For , define the Wasserstein distance between two probability distributions on a metric space by

The following result—whose proof we defer to Section D.7—shows that the empirical plug-in (14) is at most -away from its population version.

Our final bound follows from the fact that the Wasserstein distance between empirical and population distributions converges at rate . (See Section D.8 for proof.) In the next subsection, we show that the exponential dependence on the dimension is unavoidable even under more restrictive assumptions on the conditional risk .

Theorem 1.

Our concentration bounds exhibit tradeoffs for the worst case loss (2) under mixture covariate shifts; in Theorem 1, the power trades between approximation and estimation error. As , the value defined by the infimum of the expression (5) over approaches the optimal value so that approximation error goes down, but estimation becomes more difficult.

Upper bounds at faster rates

Theorem 1 shows the empirical estimator is approximately optimal with respect to the -bound (5), but with a conservative -rate of convergence. On the other hand, we can still show that provides an upper bound to the worst-case loss under mixture covariate shifts (2) at the faster rate . This provides a conservative estimate on the performance under the worst-case subpopulation. See Section D.9 for the proof.

5 Fundamental hardness of marginal DRO

So far in our development, we only required flexible nonparametric assumptions on the conditional risk for all . We view this as a practically important aspect of our approach; a learning procedure should not depend on unrealistic modeling assumptions. In this section, we show that the pessimistic scaling with the problem dimension we saw in the previous section is unavoidable when considering a nonparametric class of conditional risks. Optimization of both the original worst-case subpopulation risk (2) and the -norm the upper bound are governed by similar pessimistic dependence on the dimension.

We study the fundamental hardness of optimizing the worst-case subpopulation risk , where we now make explicit the dependence on the data-generating distribution in the notation. We show that the fundamental statistical difficulty of solving marginal DRO problems follow a standard nonparametric rate when only requiring the conditional risk to be a Hölder-smooth function. Recall that the Hölder class of -smooth functions for and is

| (19) |

where denotes the space of -times continuously differentiable functions on , and , for any -tuple of nonnegative integers . Let be the set of data-generating distributions with Hölder smooth conditional risk uniformly over

We study the finite sample minimax risk for a sample of size

| (20) |

where the outer infimum is over all measurable functions of the data . In the definition (20), the inner supremum is not to be confused with the worst-case over subpopulations in defining our distributionally robust formulation. With this, in Appendix D.10 we prove the following.

Theorem 2.

Let , , . There are constants depending on , such that for all , where for odd and for even .

Our minimax lower bound shows that the exponential sample complexity in the dimension is unavoidable in the nonparametric minimax sense (20), so that while the bounds Theorem 1 guarantees may not be completely sharp, the worst-case exponential dependence on dimension is real. As is typical in nonparametric estimation, we recover parametric rates as . More carefully identifying the (problem-dependent) constants remains a goal of future work.

A similar argument shows it is equally difficult to optimize the -upper bound (5) on the worst-case subpopulation risk. We again study the finite sample minimax risk for a sample of size

where the outer infimum is over all measurable functions of the data . In Appendix D.11, we prove the following result via a trivial adaptation of the proof of Theorem 2.

Corollary 1.

Let the conditions of Theorem 2 hold. There are constants depending on such that for , where for odd and for even .

6 Experiments

We now present empirical investigations of the procedure (16), focusing on two main aspects of our results. First, our theoretical results exhibit nonparametric rates of convergence, so it is important to understand whether these upper bounds on convergence rates govern empirical performance and the extent to which the procedure is effective. Second, on examples with high conditional risk , we expect our procedure to improve performance on minority groups and hard subpopulations when compared against joint DRO and empirical risk minimization (ERM). The code for all experiments can be found in https://github.com/hsnamkoong/marginal-dro.

To investigate both of these issues, we begin by studying simulated data (Section 6.1) so that we can evaluate true convergence precisely. We see that in moderately high dimensions, our procedure outperforms both ERM and joint DRO on worst-off subpopulations; we perform a parallel simulation study in Section B.1 for the confounded case (minimizing of Lemma B.2). After our simulation study, we continue to assess the efficacy of our procedure on real data, using our method to predict semantic similarity (Section 6.2), wine quality (Section 6.3) and crime recidivism (Section 6.4). In all of these experiments, our results are consistent with our expectation that our procedure (16) typically improves performance over unseen subpopulations.

Hyperparameter choice is important in our procedures. We must choose a Lipschitz constant , worst-case group size , risk level , and moment parameter . In our experiments, we see that cross-validation is attractive and effective. We treat the value as a single hyperparameter to estimate via a hold-out set or, in effort to demonstrate sensitivity to the parameter, plot results across a range of . As the objective (16) is convex standard methods apply; we use (sub)gradient descent to optimize the problem parameters over . In each experiment, we compare our marginal DRO method against two baselines: empirical risk minimization (ERM) and joint DRO (6). ERM minimizes the empirical risk , and provides very weak guarantees on subpopulation performance. The joint DRO formulation (6) is the only existing method that provides an upper bound to the worst-case risk. We evaluate empirical plug-ins of the dual formulation ()

| (21) |

which is the joint DRO counterpart of our marginal DRO procedure (16) for the same value of . Joint DRO formulations over other uncertainty sets (e.g. Wasserstein balls [47]) do not provide guarantees on subpopulation performance as they protect against different distributional shifts, including adversarial attacks [72].

6.1 Simulation study: the unconfounded case

Our first simulation study focuses on the unconfounded procedure (16), where the data follows the distribution (28), and the known ground truth allows us to carefully measure the effects of the problem parameters and sensitivity to the smoothness assumption . We focus on the regression example from Sec. A.2 with loss , so the procedure (16) is an empirical approximation to minimizing the worst-case objective .

The simulation distribution (28) captures several aspects of loss minimization in the presence of heterogeneous subpopulations. The subpopulations and constitute a majority and minority group, and minimizing the risk of the majority group comes at the expense of risk for the minority group. The two subpopulations also define an oracle model that minimizes the maximum loss over the two groups. As the uniform distribution exhibits the slowest convergence of empirical distributions for Wasserstein distance [31]—and as Wasserstein convergence underpins our rates in Lemma 4.2—we use the uniform distribution over covariates . We train all DRO models with worst-case group size and choose the estimated Lipschitz parameter by cross-validation on a replicate-based estimate of the worst-case loss (22) (below) using a held-out set of 1000 examples and 100 repeated measurements of . We do not regularize as .

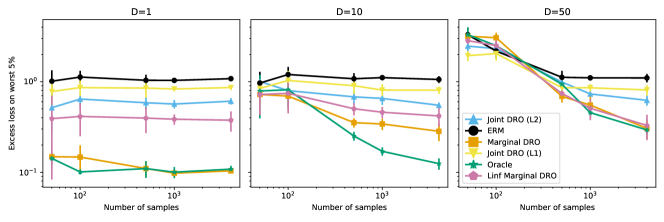

Effect of the -norm bound

We evaluate the difference in model quality as a function of , which controls the tightness of the -norm upper bound. Our convergence guarantees in Theorem 1 are looser for near , though such values achieve smaller asymptotic bias to the true sub-population risk, while values of near 2 suggest a more favorable sample size dependence in the theorem.

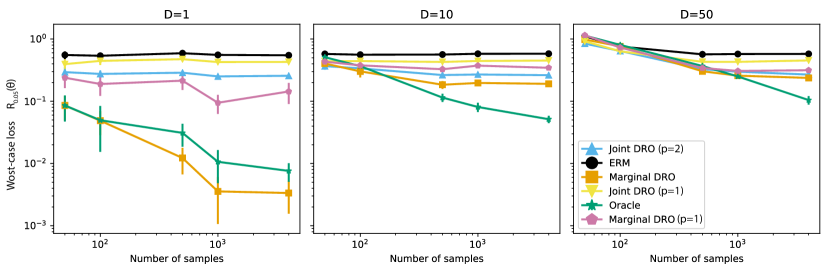

In Figure 2, we plot the results of experiments for each suggested procedure, where the horizontal axes index sample size and the vertical axes an empirical approximation to the worst-case loss

| (22) |

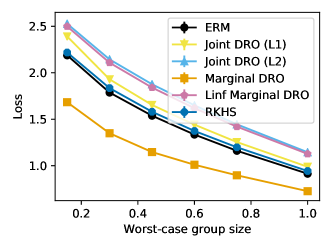

over the worst 5% of the population (test-time ); the plots index dimensions . . We evaluate a worst-case error smaller than the true mixture proportion to measure our procedure’s robustness within the minority subgroup. The plots suggest that the choice (Marginal DRO) outperforms (Linf Marginal DRO), and performance generally seems to degrade as . We consequently focus on the case for the remainder of this section.

Sample size and dimension dependence

We use the same experiment to also examine the pessimistic convergence rate of our estimator (16); this is substantially worse than that for ERM and joint DRO (6), both of which have convergence rates scaling at worst as [27]. In low dimensions ( to ) convergence to the optimal function value—which we can compute exactly—is relatively fast, and marginal DRO becomes substantially better with as few as 500 samples (Figure 2). In higher dimensions (), marginal DRO convergence is slower, but it is only worse than the joint DRO solution when . At large sample sizes , marginal DRO begins to strictly outperform the two baselines as measured by the worst-case 5% loss (22).

Sensitivity to robustness level

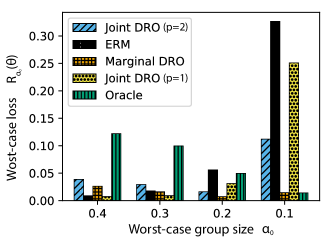

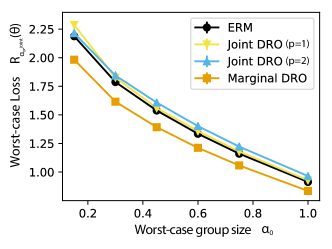

We rarely know the precise minority proportion , so that in practice one usually provides a postulated lower bound ; we investigate sensitivity to its specification. We fix the data generating distribution and train DRO models with , while evaluating them using varying test-time worst case group size in Eq. 22. We show the results of varying the test-time worst-case group size in Figure 3(a). Marginal DRO obtains a loss within times the oracle model regardless of the test-time worst-case group size, while both ERM and joint DRO incur substantially higher losses on the tails.

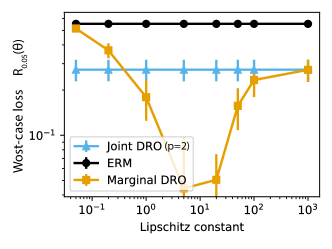

Sensitivity to Lipschitz constant

Finally, the empirical bound (18) requires an estimate of the Lipschitz constant of the conditional risk. We vary the estimate in Figure 3) for , , and , showing that the marginal robustness formulation has some sensitivity to the parameter, though there is a range of several orders of magnitude through which it outperforms the joint DRO procedures. The behavior that it exhibits is expected, however: the choice reduces the marginal DRO procedure to ERM in the bound (18), while the choice results in the joint DRO approach. In higher dimensions, marginal DRO will increasingly behave like joint DRO, leading to a smaller range of Lipschitz constants where marginal DRO performs well.

6.2 Semantic similarity prediction

We now present the first of our real-world evaluations of the marginal DRO procedure (16), focusing on a setting where we have multiple measured outcome labels for each covariate , so it is possible to accurately estimate the worst-case loss over covariate shifts. We consider the WS353 lexical semantic similarity prediction dataset [2] where the features are pairs of words, and labels are a set of human annotations rating the word similarity on a – scale. In this task, our goal is to use noisy human annotations of word similarities to learn a robust model that accurately predicts word similarities over a large set of word pairs.

We represent each word pair as the difference of the word vectors and associated to each word in GloVe [60] and cast this as a standard metric learning task of predicting a scalar similarity with a word-pair vector via the quadratic model , , . We use the absolute deviation loss . The training set consists of individual annotations of word similarities (ignoring any replicate structure), and we fit the marginal DRO model with , joint DRO models (21) with , and an ERM model. All methods use the same ridge regularizer tuned for the ERM model. We train all DRO procedures using and tune the Lipschitz constant via a held out set using the empirical estimate to the worst-case loss based on replicate annotations (as in Proposition 1).

To evaluate each model , we take an empirical approximation to the worst-case loss over the word pairs with respect to the averaged human annotation

| (23) |

This is a worst-case version of the standard word similarity evaluation [60], where we also use averaged replicate human annotations as the ground truth in our evaluations, and consider test-time worst-case group sizes ranging from 0.01 to 1.0.

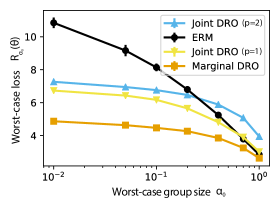

All methods achieve low average error over the entire dataset, but ERM, joint DRO and marginal DRO exhibit disparate behaviors for small subgroups. ERM incurs large errors at of the test set, resulting in near random prediction. Applying the joint DRO estimator reduces error by nearly half and marginal DRO reduces this even further (Figure 4).

6.3 Distribution shifts in wine quality prediction

Next, we show that marginal DRO () can yield improvements outside of the worst-case subgroup assumptions we have studied thus far. The UCI wine dataset [24] is a regression task with 4898 examples and 12 features, where each example is a wine with measured chemical properties and the label is a subjective quality assessment; the data naturally splits into subgroups of white and red wines. We consider a distribution shift problem where the regression model is trained on red wines but tested on (subsets of) white wines. Unlike the earlier examples, the test set here does not correspond to subpopulations of the training distribution, and the chemical features of red wine are likely distinct from those for white wines, violating naive covariate shift assumptions.

We minimize the absolute deviation loss for linear predictions, tuning baseline parameters (e.g. ridge regularization) on a held-out set that is i.i.d. with the training distribution. Our training distribution is 1500 samples of red wines and the test distribution is all white wines. We evaluate models via their loss over worst-case subgroups of the white wines, though in distinction from earlier experiments, we have no replicate labels. Thus we measure the joint DRO loss (6), i.e.

so that the worst-case loss measures the subgroup losses under the white wine distribution.

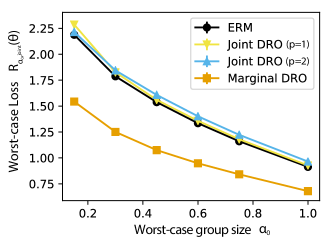

Figure 8 shows the worst-case loss over the test set as a function of . Here, Marginal DRO with Lipschitz constants varying over to and provides improvements over both joint DRO and ERM baselines across the entire range of test-time . Marginal DRO improves losses both for the pure distribution shift from red to white wines (test-time group size ) as well as for the more pessimistic groups with small test-time proportion . Distribution shift from red to white wines appears difficult to capture for the pessimistic joint DRO methods.

6.4 Recidivism prediction

Finally, we show that marginal DRO can control the loss over a minority group on a recidivism prediction task. The COMPAS recidivism dataset [23] is a classification task where examples are individual convicts, features consist of binary demographic labels (such as African American or not) and description of their crimes, and the label is whether they commit another crime after release (recidivism). We use the fairML toolkit version of this dataset [1]. Classification algorithms for recidivism have systematically discriminated against minority groups, and this dataset illustrates such discrimination [6]. We consider this dataset from the perspective of achieving uniform performance across various groups. There are binary variables in data, each indicating a potential split of the data into minority and majority group (e.g. young vs. not young, or Black vs. non-Black), of which have enough () observations in each split to make reasonable error estimates. We train a model over the full population (using all the features), and for each of the demographic indicator variables and evaluate the held-out 0-1 loss over both the associated majority group and minority group.

Our goal is to ensure that the classification accuracy remains high without explicitly splitting the data on particular demographic labels (though we include them in our models as they have predictive power). We use the binary logistic loss with linear models and a train/test split. We set for all DRO methods (approximately matching demographic statistics in the United States, with 60% white and 40% other races), and apply ridge regularization to all models with regularization parameter tuned for the ERM model.

| Method | Old | Young | Black | Hispanic | Other race | Female | Misdemeanor |

|---|---|---|---|---|---|---|---|

| ERM | 37.7 0.8 | 44.6 1.0 | 37.7 0.8 | 37.5 0.9 | 37.9 1.1 | 37.5 0.9 | 37.6 0.8 |

| Joint () - ERM | 10.0 2.0 | 4.0 1.7 | 9.7 1.7 | 9.6 1.8 | 10.9 2.3 | 9.2 1.8 | 9.0 1.6 |

| Joint () - ERM | 5.8 1.7 | 1.2 1.7 | 5.2 1.5 | 7.4 1.9 | 6.6 2.1 | 5.9 1.7 | 5.1 1.5 |

| Marginal L=0.01 - ERM | -0.7 0.7 | 1.4 1.1 | -1.0 0.7 | -1.7 0.9 | -2.4 1.1 | -1.5 0.8 | -1.5 0.7 |

| Marginal L=0.001 - ERM | -1.1 0.7 | 0.4 1.1 | -1.4 0.7 | -2.1 0.9 | -2.6 1.1 | -1.9 0.8 | -1.8 0.7 |

Table 6.4 presents the 0-1 loss on the seven demographic splits over 100 random train/test splits. For each attribute (table column) we split the test set into examples for which the attribute is true and false and report the average 0-1 loss on the worst of the two groups. The first row gives the average worst-case error and associated 95% standard error for the ERM model. For the DRO based models (remaining rows), we report the average differences with respect to the baseline ERM model and standard error intervals. Unlike our earlier regression tasks, joint DRO (both and ) performs worse than ERM on almost all demographic splits. On the other hand, we find that marginal DRO with the appropriate smoothness constant reduces classification errors between – on the worst-case group across various demographics, with the largest error reduction of 3% occurring in the young vs. old demographic split.

References

- Adebayo [2016] J. A. Adebayo. Fairml : Toolbox for diagnosing bias in predictive modeling. Master’s thesis, Massachusetts Institute of Technology, 2016.

- Agirre et al. [2009] E. Agirre, E. Alfonseca, K. Hall, J. Kravalova, M. Pasca, and A. Soroa. A study on similarity and relatedness using distributional and wordnet-based approaches. In Proceedings of the North American Chapter of the Association for Computational Linguistics (NAACL-HLT), 2009.

- Amodei et al. [2016] D. Amodei, S. Ananthanarayanan, R. Anubhai, J. Bai, E. Battenberg, C. Case, J. Casper, B. Catanzaro, Q. Cheng, and G. Chen. Deep speech 2: end-to-end speech recognition in English and Mandarin. In Proceedings of the 33rd International Conference on Machine Learning, pages 173–182, 2016.

- Aronszajn [1950] N. Aronszajn. Theory of reproducing kernels. Transactions of the American Mathematical Society, 68(3):337–404, May 1950.

- Asuncion and Newman [2007] A. Asuncion and D. J. Newman. UCI machine learning repository, 2007. URL http://www.ics.uci.edu/~mlearn/MLRepository.html.

- Barocas and Selbst [2016] S. Barocas and A. D. Selbst. Big data’s disparate impact. 104 California Law Review, 3:671–732, 2016.

- Bartlett and Mendelson [2002] P. L. Bartlett and S. Mendelson. Rademacher and Gaussian complexities: Risk bounds and structural results. Journal of Machine Learning Research, 3:463–482, 2002.

- Ben-David et al. [2007] S. Ben-David, J. Blitzer, K. Crammer, and F. Pereira. Analysis of representations for domain adaptation. In Advances in Neural Information Processing Systems 20, pages 137–144, 2007.

- Ben-Tal et al. [2009] A. Ben-Tal, L. E. Ghaoui, and A. Nemirovski. Robust Optimization. Princeton University Press, 2009.

- Ben-Tal et al. [2013] A. Ben-Tal, D. den Hertog, A. D. Waegenaere, B. Melenberg, and G. Rennen. Robust solutions of optimization problems affected by uncertain probabilities. Management Science, 59(2):341–357, 2013.

- Berlinet and Thomas-Agnan [2004] A. Berlinet and C. Thomas-Agnan. Reproducing Kernel Hilbert Spaces in Probability and Statistics. Kluwer Academic Publishers, 2004.

- Bertsimas et al. [2018] D. Bertsimas, V. Gupta, and N. Kallus. Data-driven robust optimization. Mathematical Programming, Series A, 167(2):235–292, 2018.

- Bickel et al. [2007] S. Bickel, M. Brückner, and T. Scheffer. Discriminative learning for differing training and test distributions. In Proceedings of the 24th International Conference on Machine Learning, 2007.

- Birgé and Massart [1995] L. Birgé and P. Massart. Estimation of integral functionals of a density. The Annals of Statistics, pages 11–29, 1995.

- Blanchet et al. [2017] J. Blanchet, Y. Kang, F. Zhang, and K. Murthy. Data-driven optimal transport cost selection for distributionally robust optimizatio. arXiv:1705.07152 [stat.ML], 2017.

- Blanchet et al. [2019] J. Blanchet, Y. Kang, and K. Murthy. Robust Wasserstein profile inference and applications to machine learning. Journal of Applied Probability, 56(3):830–857, 2019.

- Blodgett et al. [2016] S. L. Blodgett, L. Green, and B. O’Connor. Demographic dialectal variation in social media: A case study of African-American English. In Proceedings of Empirical Methods for Natural Language Processing, pages 1119–1130, 2016.

- Boucheron et al. [2013] S. Boucheron, G. Lugosi, and P. Massart. Concentration Inequalities: a Nonasymptotic Theory of Independence. Oxford University Press, 2013.

- Bühlmann and Meinshausen [2016] P. Bühlmann and N. Meinshausen. Magging: maximin aggregation for inhomogeneous large-scale data. Proceedings of the IEEE, 104(1):126–135, 2016.

- Bureau [2014] C. F. P. Bureau. Using publicly available information to proxy for unidentified race and ethnicity: a methodology and assessment, 2014. Available at https://www.consumerfinance.gov/data-research/research-reports/usingpublicly-available-information-to-proxy-for-unidentified-race-and-ethnicity/.

- Cer et al. [2017] D. Cer, M. Diab, E. Agirre, I. Lopez-Gazpio, and L. Specia. Semeval-2017 task 1: Semantic textual similarity multilingual and cross-lingual focused evaluation. In Proceedings of the 10th International Workshop on Semantic Evaluation (SemEval 2017), 2017.

- Chen et al. [2019] J. Chen, N. Kallus, X. Mao, G. Svacha, and M. Udell. Fairness under unawareness: Assessing disparity when protected class is unobserved. In Proceedings of the Conference on Fairness, Accountability, and Transparency, pages 339–348. ACM, 2019.

- Chouldechova [2017] A. Chouldechova. A study of bias in recidivism prediciton instruments. Big Data, pages 153–163, 2017.

- Cortez et al. [2009] P. Cortez, A. Cerdeira, F. Almeida, T. Matos, and J. Reis. Modeling wine preferences by data mining from physicochemical properties. Decision Support Systems, 47(4):547–553, 2009.

- Cristianini and Shawe-Taylor [2004] N. Cristianini and J. Shawe-Taylor. Kernel Methods for Pattern Analysis. Cambridge University Press, 2004.

- Duchi [2018] J. C. Duchi. Introductory lectures on stochastic convex optimization. In The Mathematics of Data, IAS/Park City Mathematics Series. American Mathematical Society, 2018.

- Duchi and Namkoong [2021] J. C. Duchi and H. Namkoong. Learning models with uniform performance via distributionally robust optimization. Annals of Statistics, 49(3):1378–1406, 2021.

- Duchi et al. [2021] J. C. Duchi, P. W. Glynn, and H. Namkoong. Statistics of robust optimization: A generalized empirical likelihood approach. Mathematics of Operations Research, 46:946–969, 2021.

- Dwork et al. [2012] C. Dwork, M. Hardt, T. Pitassi, O. Reingold, and R. Zemel. Fairness through awareness. In Innovations in Theoretical Computer Science (ITCS), pages 214–226, 2012.

- Esfahani and Kuhn [2018] P. M. Esfahani and D. Kuhn. Data-driven distributionally robust optimization using the wasserstein metric: Performance guarantees and tractable reformulations. Mathematical Programming, Series A, 171(1–2):115–166, 2018.

- Fournier and Guillin [2015] N. Fournier and A. Guillin. On the rate of convergence in Wasserstein distance of the empirical measure. Probability Theory and Related Fields, 162(3-4):707–738, 2015.

- Gao and Kleywegt [2016] R. Gao and A. J. Kleywegt. Distributionally robust stochastic optimization with wasserstein distance. arXiv:1604.02199 [math.OC], 2016.

- Gao et al. [2017] R. Gao, X. Chen, and A. Kleywegt. Wasserstein distributional robustness and regularization in statistical learning. arXiv:1712.06050 [cs.LG], 2017.

- Gong et al. [2016] M. Gong, K. Zhang, T. Liu, D. Tao, C. Glymour, and B. Schölkopf. Domain adaptation with conditional transferable components. In Proceedings of the 33rd International Conference on Machine Learning, pages 2839–2848, 2016.

- Gretton et al. [2009] A. Gretton, A. Smola, J. Huang, M. Schmittfull, K. Borgwardt, and B. Schölkopf. Covariate shift by kernel mean matching. In J. Q. nonero Candela, M. Sugiyama, A. Schwaighofer, and N. D. Lawrence, editors, Dataset Shift in Machine Learning, chapter 8, pages 131–160. MIT Press, 2009.

- Grother et al. [2010] P. J. Grother, G. W. Quinn, and P. J. Phillips. Report on the evaluation of 2d still-image face recognition algorithms. NIST Interagency/Internal Reports (NISTIR), 7709, 2010.

- Hardt et al. [2016] M. Hardt, E. Price, and N. Srebro. Equality of opportunity in supervised learning. In Advances in Neural Information Processing Systems 29, 2016.

- Hashimoto et al. [2018] T. Hashimoto, M. Srivastava, H. Namkoong, and P. Liang. Fairness without demographics in repeated loss minimization. In Proceedings of the 35th International Conference on Machine Learning, 2018.

- Hébert-Johnson et al. [2017] Ú. Hébert-Johnson, M. P. Kim, O. Reingold, and G. N. Rothblum. Calibration for the (computationally-identifiable) masses. arXiv:1711.08513 [cs.LG], 2017.

- Heinze-Deml and Meinshausen [2017] C. Heinze-Deml and N. Meinshausen. Grouping-by-id: Guarding against adversarial domain shifts, 2017.

- Hovy and Søgaard [2015] D. Hovy and A. Søgaard. Tagging performance correlates with author age. In Proceedings of the 53rd Annual Meeting of the Association for Computational Linguistics (Short Papers), volume 2, pages 483–488, 2015.

- Hu et al. [2018] W. Hu, G. Niu, I. Sato, and M. Sugiayma. Does distributionally robust supervised learning give robust classifiers? arXiv:1611.02041v4 [stat.ML], 2018. URL https://arxiv.org/abs/1611.02041v4.

- Huang et al. [2007] J. Huang, A. Gretton, K. M. Borgwardt, B. Schölkopf, and A. J. Smola. Correcting sample selection bias by unlabeled data. In Advances in Neural Information Processing Systems 20, pages 601–608, 2007.

- Imbens and Rubin [2015] G. Imbens and D. Rubin. Causal Inference for Statistics, Social, and Biomedical Sciences. Cambridge University Press, 2015.

- Kearns et al. [2018] M. Kearns, S. Neel, A. Roth, and Z. S. Wu. Preventing fairness gerrymandering: Auditing and learning for subgroup fairness. arXiv:1711.05144 [cs.LG], 2018.

- Kilbertus et al. [2017] N. Kilbertus, M. R. Carulla, G. Parascandolo, M. Hardt, D. Janzing, and B. Schölkopf. Avoiding discrimination through causal reasoning. In Advances in Neural Information Processing Systems 30, 2017.

- Kuhn et al. [2019] D. Kuhn, P. M. Esfahani, V. A. Nguyen, and S. Shafieezadeh-Abadeh. Wasserstein distributionally robust optimization: Theory and applications in machine learning. In Operations Research & Management Science in the Age of Analytics, pages 130–166. INFORMS, 2019.

- Lam and Qian [2019] H. Lam and H. Qian. Combating conservativeness in data-driven optimization under uncertainty: A solution path approach. arXiv:1909.06477 [math.OC], 2019.

- Lam and Zhou [2015] H. Lam and E. Zhou. Quantifying input uncertainty in stochastic optimization. In Proceedings of the 2015 Winter Simulation Conference. IEEE, 2015.

- Le Cam [1973] L. Le Cam. Convergence of estimates under dimensionality restrictions. Annals of Statistics, 1(1):38–53, 1973.

- Lee and Raginsky [2017] J. Lee and M. Raginsky. Minimax statistical learning and domain adaptation with Wasserstein distances. arXiv:1705.07815 [cs.LG], 2017.

- Lei [2018] J. Lei. Convergence and concentration of empirical measures under Wasserstein distance in unbounded functional spaces. arXiv:1804.10556 [math.ST], 2018.

- Liu and Ziebart [2014] A. Liu and B. Ziebart. Robust classification under sample selection bias. In Advances in Neural Information Processing Systems 27, pages 37–45, 2014.

- Liu and Ziebart [2017] A. Liu and B. Ziebart. Robust covariate shift prediction with general losses and feature views. arXiv:1712.10043 [cs.LG], 2017. URL https://arxiv.org/abs/1712.10043.

- Marcus et al. [1994] M. Marcus, B. Santorini, and M. Marcinkiewicz. Building a large annotated corpus of English: the Penn Treebank. Computational Linguistics, 19:313–330, 1994.

- Meinshausen and Bühlmann [2015] N. Meinshausen and P. Bühlmann. Maximin effects in inhomogeneous large-scale data. The Annals of Statistics, 43(4):1801–1830, 2015.

- Minty [1970] G. J. Minty. On the extension of lipschitz, lipschitz-hölder continuous, and monotone functions. Bulletin of the American Mathematical Society, 76(2):334–339, 1970.

- Miyato et al. [2015] T. Miyato, S.-i. Maeda, M. Koyama, K. Nakae, and S. Ishii. Distributional smoothing with virtual adversarial training. arXiv:1507.00677 [stat.ML], 2015.

- Namkoong and Duchi [2017] H. Namkoong and J. C. Duchi. Variance regularization with convex objectives. In Advances in Neural Information Processing Systems 30, 2017.

- Pennington et al. [2014] J. Pennington, R. Socher, and C. D. Manning. Glove: Global vectors for word representation. In Proceedings of Empirical Methods for Natural Language Processing, 2014.

- Peters et al. [2016] J. Peters, P. Bühlmann, and N. Meinshausen. Causal inference by using invariant prediction: identification and confidence intervals. Journal of the Royal Statistical Society, Series B, 78(5):947–1012, 2016.

- Rajpurkar et al. [2018] P. Rajpurkar, R. Jia, and P. Liang. Know what you don’t know: Unanswerable questions for squad. In Proceedings of the Annual Meeting of the Association for Computational Linguistics, 2018.

- Rockafellar and Uryasev [2000] R. T. Rockafellar and S. Uryasev. Optimization of conditional value-at-risk. Journal of Risk, 2:21–42, 2000.

- Rothenhäusler et al. [2016] D. Rothenhäusler, N. Meinshausen, and P. Bühlmann. Confidence intervals for maximin effects in inhomogeneous large-scale data. In Statistical Analysis for High-Dimensional Data, pages 255–277. Springer, 2016.

- Rothenhäusler et al. [2018] D. Rothenhäusler, P. Bühlmann, N. Meinshausen, and J. Peters. Anchor regression: heterogeneous data meets causality. arXiv:1801.06229 [stat.ME], 2018.

- Sapiezynski et al. [2017] P. Sapiezynski, V. Kassarnig, and C. Wilson. Academic performance prediction in a gender-imbalanced environment. In Proceedings of the Eleventh ACM Conference on Recommender Systems, volume 1, pages 48–51, 2017.

- Shafieezadeh-Abadeh et al. [2015] S. Shafieezadeh-Abadeh, P. M. Esfahani, and D. Kuhn. Distributionally robust logistic regression. In Advances in Neural Information Processing Systems 28, pages 1576–1584, 2015.

- Shankar et al. [2017] S. Shankar, Y. Halpern, E. Breck, J. Atwood, J. Wilson, and D. Sculley. No classification without representation: Assessing geodiversity issues in open data sets for the developing world. arXiv:1711.08536 [stat.ML], 2017.

- Shapiro [2017] A. Shapiro. Distributionally robust stochastic programming. SIAM Journal on Optimization, 27(4):2258–2275, 2017.

- Shapiro et al. [2009] A. Shapiro, D. Dentcheva, and A. Ruszczyński. Lectures on Stochastic Programming: Modeling and Theory. SIAM and Mathematical Programming Society, 2009.

- Shimodaira [2000] H. Shimodaira. Improving predictive inference under covariate shift by weighting the log-likelihood function. Journal of Statistical Planning and Inference, 90(2):227–244, 2000.

- Sinha et al. [2018] A. Sinha, H. Namkoong, and J. Duchi. Certifying some distributional robustness with principled adversarial training. In Proceedings of the Sixth International Conference on Learning Representations, 2018.

- Staib and Jegelka [2019] M. Staib and S. Jegelka. Distributionally robust optimization and generalization in kernel methods. In Advances in Neural Information Processing Systems, pages 9131–9141, 2019.

- Storkey and Sugiyama [2006] A. J. Storkey and M. Sugiyama. Mixture regression for covariate shift. In Advances in Neural Information Processing Systems 19, pages 1337–1344, 2006.

- Sugiyama et al. [2007] M. Sugiyama, M. Krauledat, and K.-R. Müller. Covariate shift adaptation by importance weighted cross validation. Journal of Machine Learning Research, 8:985–1005, 2007.

- Tatman [2017] R. Tatman. Gender and dialect bias in YouTube’s automatic captions. In First Workshop on Ethics in Natural Langauge Processing, volume 1, pages 53–59, 2017.

- van der Vaart and Wellner [1996] A. W. van der Vaart and J. A. Wellner. Weak Convergence and Empirical Processes: With Applications to Statistics. Springer, New York, 1996.

- van Erven and Harremoës [2014] T. van Erven and P. Harremoës. Rényi divergence and Kullback-Leibler divergence. IEEE Transactions on Information Theory, 60(7):3797–3820, 2014.

- Wen et al. [2014] J. Wen, C.-N. Yu, and R. Greiner. Robust learning under uncertain test distributions: Relating covariate shift to model misspecification. In Proceedings of the 31st International Conference on Machine Learning, pages 631–639, 2014.

- Yu [1997] B. Yu. Assouad, Fano, and Le Cam. In Festschrift for Lucien Le Cam, pages 423–435. Springer-Verlag, 1997.

Appendix A Alternative variational approximations

Recalling the variational representation (3), we wish to minimize the variational approximation

For each choice of we propose below, we consider an empirical approximation , the subset of restricted to mapping instead of , solving the empirical alternative

| (24) |

We design our proposals so the dual of the inner supremum (24) is computable. When the conditional risk is smooth, we can provide generalization bounds for our procedures. We omit detailed development for our first two procedures—which we believe are natural proposals, justifying a bit of discussion—as neither is as effective as the last procedure in our empirical evaluations, which controls the upper bound (5) on .

A.1 Example approximations and empirical variants

Reproducing Hilbert kernel spaces (RKHS)

Let be a reproducing kernel [11, 4] generating the reproducing kernel Hilbert space with associated norm . For any , we can define a norm ball

and consider the variational approximation (4) with . To approximate the population variational problem , we consider a restriction of the same kernel to the sample space . Let be the Gram matrix evaluated on samples , and define the empirical approximation

(Recall that if , then .) To compute the empirical problem (24) with , we take the dual of the inner supremum. Simplifying the dual form—whose derivation is a standard exercise in convex optimization—we get

| (25) |

For convex losses , this is a convex optimization problem in .

Hölder continuous functions (bounded Hölder)

Instead of the space of bounded functions, we restrict attention to Hölder continuous functions

| (26) |

where the particular scaling with respect to and is for notational convenience in Section 4. The empirical plug-in of is

the empirical plug-in of the variational problem (4) with is given by the procedure (24) with . Taking the dual of the inner supremum problem, we have the following equivalent dual formulation of the empirical variational problem

| (27) |

For convex losses , this is again a convex optimization problem in , and is always smaller than the empirical joint DRO formulation (6).

By definition, the population Hölder continuous variational approximation provides the lower bound on the worst-case loss

As a consequence, cannot upper bound the subpopulation loss uniformly over . Nonetheless, for any subpopulation with Lipschitz density , then does provide a valid upper bound on :

Lemma A.1.

Let be any distribution with -Lipschitz density . Then

See Section D.3 for a proof. For example, if and both have Lipschitz log densities, then is also Lipschitz, as the following example shows.

Example 1: Let be absolutely continuous with respect to some -finite measure , denote and and assume and are -Lipschitz. Let , and consider any fixed . If we assume that without loss of generality that > , then

where the final inequality follows because and . Consequently, then is -Lipschitz.

A.2 Empirical Comparison of Variational Procedures

We consider an elaborated version of the data mechanism (8) to incorporate higher dimensionality, with the data generating distribution

| (28) |

Our goal is to predict via , and we use the absolute loss . We provide details of the experimental setup, such as the estimators and optimizers, in Section 6. In brief, we perform a grid search over all hyperparameters (Lipschitz estimates and kernel scales) for each method over 4 orders of magnitude; for the RKHS-based estimators, we test Gaussian, Laplacian, and Matern kernels, none of which have qualitative differences from one another, so we present results only for the Gaussian kernel .

Dimension dependence

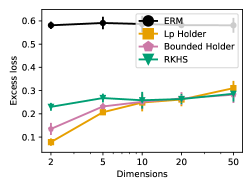

We first investigate the dimension dependence of the estimators, increasing in the model (28) from to with a fixed sample size .

Under model (28), we consider marginal distributionally robust objective (2) and evaluate the excess risk for the choice , the hardest 15% of the data. As grows, we expect estimation over Hölder continuous functions to become more difficult, and for the RKHS-based estimator to outperform the others. Figure 6 bears out this intuition (plotting the excess risk): high dimensionality induces less degradation in the RKHS approach than the others. Yet the absolute performance of the Hölder-based methods is better, which is unsurprising, as we are approximating a discontinuous indicator function.

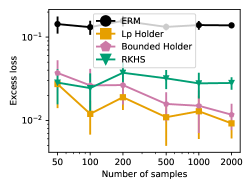

Sample size dependence

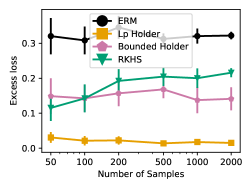

We also consider the sample dependence of the estimators, fitting models using losses with robustness level set to , then evaluating their excess risk using , so that we can see the effects of misspecification, as it is unlikely in practice that we know the precise minority population size against which to evaluate. Unlike the -Hölder class (Eq. (9)), the bounded -Hölder continuous function class (26) can approximate the population optimum of the original variational problem (3) as and . Because of this, we expect that as the sample size grows, and is set optimally, the bounded Hölder class will perform well.

On example (8) with , we observe in Figure 6(a) that both Hölder continuous class estimators with constants set via a hold-out set perform well as grows, achieving negligible excess error. In contrast, the RKHS approach incurs high loss even with large sample sizes. Although both Hölder class approaches perform similarly when the robustness level is set properly, we find that the -Hölder class is substantially better when the test time robustness level changes. The -Hölder based estimator is the only one which provides reasonable estimators when training with and testing with (Figure 6(b)). Motivated by these practical benefits, we study finite sample properties of the -bound estimator in this paper.

Real dataset

Finally, we expand the scope of empirical evaluations by studying the wine quality estimation experiment (Section 6.3). We observe that our proposed marginal DRO approach continues to be more accurate compared to alternative variational approximations.

Appendix B Risk bounds under confounding

Our assumption that is fixed for each of our marginal populations over is analogous to the frequent assumptions in causal inference that there are no unmeasured confounders [44]. When this is true—for example, in machine learning tasks where the label is a human annotation of the covariate —minimizing worst-case loss over covariate shifts is natural, but the assumption may fail in other real-world problems. For example, in predicting crime recidivism based on the type of crime committed and race of the individual, unobserved confounders (e.g. income, location, education) likely vary with race. Consequently, we provide a parallel to our earlier development that provides a sensitivity analysis to unmeasured (hidden) confounding.

Let us formalize. Let be a random variable, and in analogy to (2) we define

| (29) |

Our goal is then to minimize the worst-case loss under mixture covariate shifts

| (30) |

Since the confounding variable is unobserved, we extend our robustness approach assuming a bounded effect of confounding, and derive conservative upper bounds on the worst-case loss.

We make the following boundedness definition and assumption on the effects of .

Definition 1.

The triple is at most -confounded for the loss if

Assumption A4.

The triple is at most -confounded for the loss .

Paralleling earlier developments, we derive a variational bound on the worst-case confounded risk (30). If , our worst-case formulation approaches the joint DRO problem as .

Confounded variational problem

Under confounding, a development completely parallel to Lemma 2.1 and Hölder’s inequality yields the dual

for all . Taking the variational form of the -norm for yields

| (31) |

Instead of the somewhat challenging variational problem over , we reparameterize problem (31) as , where is smooth and is a bounded residual term, which—by taking the worst case over bounded —allows us to provide an upper bound on the worst-case problem (29). Let be the space of Hölder functions (11) and be the space of bounded functions

Then defining the analogue of the unconfounded variational objective (12)

the risk is -close to the variational objective (31). See Appendix D.12 for proof.

Confounded estimator

By replacing with the empirical version (the set of Hölder functions on the empirical distribution) and with the empirical counterpart , we get the obvious empirical plug-in of the population quantity . In this case, a duality argument provides the following analogue of Lemma 4.1, which follows because the class simply corresponds to an constraint on a vector in .

Lemma B.2.

For any and , we have

Upper bound on confounded objective

In analogy with Proposition 2, the empirical plug-in is an upper bound on the population objective under confounding. Although our estimator only provides an upper bound, it provides practical procedures for controlling the worst-case loss (29) when Assumption A4 holds, as we observe in the next section. The next proposition, whose proof we provide in Section D.13, shows the upper bound.

B.1 Simulation study: the confounded case

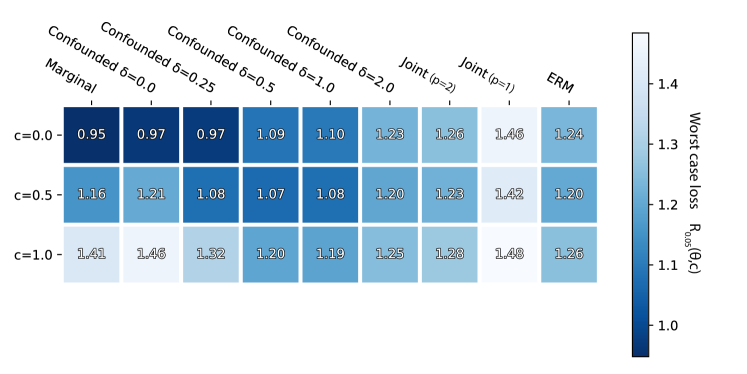

To complement our results in the unconfounded case, we extend our simulation experiment by adding unmeasured confounders, investigating the risk upper bounds of Lemma B.2 and Proposition 3. We generate data nearly identically to model (28), introducing a confounder :

To evaluate a putative parameter , we approximate the worst-case risk

| (33) |

via the plug-in replicate estimate in Proposition 1, using a sample of size , replicates, and test-time worst-case group size . The gap in the conditional risk from -confounding (i.e. ) in Definition 1 varies monotonically with . To construct estimates , we minimize the dual representation of the empirical confounded risk in Lemma B.2, varying the postulated level of confounding while fixing the training time worst-case group size . We present results in Fig. 9, which compares the worst-case loss (33) as varies (vertical axis) for different methods to select (horizontal axis). We compare marginal DRO (16) (which assumes no confounding ), the procedure minimizing empirical confounded risk as we vary , and the joint DRO procedure (21) (full confounding) with , and empirical risk minimization (ERM). The figure shows the (roughly) expected result that the confounding-aware risks achieve lower worst-case loss (33) as the postulated confounding level increases with the actual amount of confounding, with joint DRO and ERM achieving worse performance.

Appendix C Additional validation experiments

In this section, we provide additional experiments quantifying the computational overhead associated with marginal DRO, and analyze the robustness of previous results with respect to the choice of the loss function. Finally, we compare different smoothness assumptions on the conditional risk on real-world data.

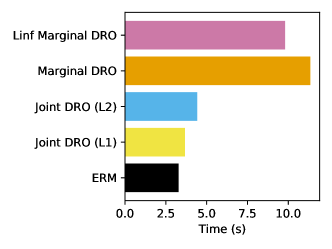

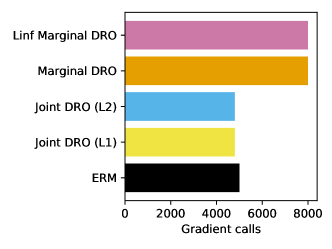

C.1 Computational overhead

To analyze the computational overhead of marginal DRO, we benchmark both the number of gradient oracle calls (defined as the number of times we take the gradient of the objective with respect to or ) and overall runtime. We focus on the simulation experiments in Section 6.1 with and . The results in Figure 10 show that marginal DRO incurs a 2-3x overhead, but the overall runtime costs of all algorithms are still low. The gradient call comparisons show that the increased runtimes are primarily due to the increased cost of individual gradient calls (as each gradient computation for marginal DRO involves gradients over both the model parameters as well as the transport matrix ) rather then increases in the number of overall gradient steps.

All DRO methods including joint and marginal DRO use bisection search to optimize the dual parameter , but this additional cost does not substantially affect the number of gradient calls or runtime, as we re-use initializations for gradient descent across different steps of the bisection search. The added number of gradient calls to marginal DRO methods arise from the fact that we must tune one additional hyperparameter which involves additional grid search on top of the bisection search.

There is an added gradient call overhead for the marginal DRO variants, which must additionally perform hyperparameter search over on a held out set. Even with re-using initializations, this results in a higher number of gradient oracle calls. Finally, there is an additional runtime overhead for both marginal DRO variants in terms of runtime due to the larger number of parameters.

C.2 Effect of loss function choice

We also quantify the impact of the loss function by re-running the large scale simulation in Figure 2 using the squared loss rather than the absolute deviation loss, keeping the same experimental settings such as validation methods and hyperparameters. We find in Figure 11 that the results in the simulation remain qualitatively same as before. The main difference is that marginal DRO performs slightly better, but none of the ERM or joint DRO baselines perform well even in this setting. Together with the classification results discussed in previous sections, these squared loss results suggest that the performance gains of marginal DRO are not limited to minimizing the absolute deviation loss.

Appendix D Proofs

D.1 Proof of Lemma 2.1

We begin by deriving a likelihood ratio reformulation, where we use to ease notation

| (34) |

To see that inequality “” holds, let be a probability over . Note that induces a distribution over , which we denote by the same notation for simplicity. Since for some probability and , we have . Letting , it belongs to the constraint set in the right hand side and we conclude holds. To see the reverse inequality “”, for any likelihood ratio , let so that for all . Noting defines a probability measure and , we conclude that inequality holds.

Next, the following lemma gives a variational form for conditional value-at-risk, which corresponds to the worst-case loss (2) under mixture covariate shifts.

Lemma D.1 ([70, Example 6.19]).

For any random variable with ,

We now show that when ,

| (35) |

Noting that is strictly increasing on since for , we may assume w.l.o.g. that . Further, for , we have

We conclude that the equality (35) holds.

D.2 Proof of Proposition 1

Using the dual of Lemma 2.1, we first show that with probability at least ,

| (36) |

As the above gives a uniform approximation to the dual objective , the proposition will then follow.

To show the result (36), we begin by noting that

| (37) |

To bound the first term in the bound (37), note that since is -Lipschitz, a standard symmetrization and Rademacher contraction argument [18, 7] yields

with probability at least . To bound the second term in the bound (37), we first note that

since . The preceding quantity has bound , and using that its expectation is at most the bounded differences inequality implies the uniform concentration result (36).

The second result follows from a nearly identical argument by noting that we still have the Lipschitz relation

D.3 Proof of Lemma A.1

Let . Since is a likelihood ratio and , we have the upper bound

Then we use the sequence of inequalities, starting from our dual representation on , that

This gives the result.

D.4 Proof of Lemma 3.1

Since , we have

which gives the first bound. To get the second bound, note that for a -Lipschitz function , we have . Since is -Lipschitz on , we get

Taking -power on both sides, we obtain the second bound.

D.5 Proof of Lemma 3.2

First, we argue that

| (38) |

and for any . We consider an arbitrary but fixed and .

Suppose that , then

and we have the upper bound. On the other hand, assume . The inner supremum in Eq. (9) is attained at defined in expression (10), and from Assumption A3, for any ,

where we used in the first inequality. Thus, we conclude that is in , and obtain the equality

where we did a change of variables to in the last equality. This yields the bound (38).

Now, for , the bound (38) is actually an equality. This proves the first claim. To show the second claim, it remains to show that