The Spectral Approach to Linear Rational Expectations Models

Abstract

This paper considers linear rational expectations models in the frequency domain under general conditions. The paper develops necessary and sufficient conditions for existence and uniqueness of particular and generic systems and characterizes the space of all solutions as an affine space in the frequency domain. It is demonstrated that solutions are not generally continuous with respect to the parameters of the models, invalidating mainstream frequentist and Bayesian methods. The ill-posedness of the problem motivates regularized solutions with theoretically guaranteed uniqueness, continuity, and even differentiability properties. Regularization is illustrated in an analysis of the limiting Gaussian likelihood functions of two analytically tractable models.

JEL Classification: C10, C32, C62, E32.

Keywords: Linear rational expectations models, frequency domain, spectral representation, Wiener-Hopf factorization, regularization, Gaussian likelihood function.

1 Introduction

Spectral analysis of stationary processes is a cornerstone of time series analysis (Brockwell & Davis, 1991; Pourahmadi, 2001; Lindquist & Picci, 2015). Since its beginnings in the late 1930s, it has benefited from being at the intersection of a number of fundamental mathematical subjects including probability, functional analysis, and complex analysis (Rozanov, 1967; Nikolski, 2002; Bingham, 2012a, b). The purpose of this paper is to attempt to bring some of this rich tradition into the linear rational expectations model (LREM) literature in the form of useful theoretical results but also with applications to statistical inference.

Using the spectral representation of stationary processes due to Kolmogorov (1939, 1941b, 1941a) and Cramér (1940, 1942), this paper recasts the LREM problem in the classical Hilbert space of the frequency domain literature. This is demonstrated concretely on simple scalar models before generalizing to multivariate models. Like the structural VARMA problem, the LREM problem is equivalent to a linear system in Hilbert space. Using the factorization method of Wiener & Hopf (1931), the paper then characterizes existence and uniqueness of solutions to particular as well as generic systems, generalizing results by Onatski (2006). The set of all solutions to a given LREM is shown to be a finite dimensional affine space in the frequency domain. The dimension of this space is expressed much more simply than in Funovits (2017, 2020). It is important to note that the underlying assumptions of existence and uniqueness in this paper are weaker than in all of the previous literature on frequency domain solutions of LREMs (Whiteman, 1983; Onatski, 2006; Tan & Walker, 2015; Tan, 2019) as these works require the exogenous process to have a purely non deterministic Wold (1938) representation, an assumption that is demonstrated to be unnecessary. The weaker assumptions of this paper also permit a clear answer for why unit roots must be excluded, an aspect of the theory absent from the previous literature.

The main results of the paper concern the ill-posdeness of the LREM problem in macroeconometrics. Hadamard (1902) defines a problem to be well-posed if its solutions satisfy the conditions of existence, uniqueness, and continuous dependence on its parameters. The LREM problem is ill-posed because it violates not just the second condition but also the third. Indeed, it has long been accepted that non-uniqueness is a feature of the LREM problem and many techniques have been developed to deal with it (e.g. Taylor (1977), McCallum (1983), Lubik & Schorfheide (2003), Farmer et al. (2015), Bianchi & Nicolò (2019)). This paper highlights the fact that non-unique solutions that have been proposed in the literature are not guaranteed to be continuous. This problem seems to be either not well understood or not fully appreciated so far; to the author’s knowledge, Sims (2007) is the only acknowledgement of this problem. The problem of discontinuity is quite serious because it invalidates mainstream econometric methodology as reviewed, for example, in Canova (2011), DeJong & Dave (2011), or Herbst & Schorfheide (2016). These methods utilize floating point arithmetic to either optimize objective functions or sample from posterior distributions; they cannot find the isolated extrema or explore the posterior probabilities with atoms generated by discontinuity of LREM solutions.

Fortunately, the literature on ill-posed problems offers an immediate solution to the problem: regularization. The idea here is that when theory is insufficient to pin down a unique solution, other information can be brought to bear. The method can be interpreted in at least two ways: (i) penalizing economically unreasonable solutions or shrinking towards economically reasonable ones or (ii) imposing prior beliefs on the frequencies of fluctuations that solutions ought to exhibit. For example, we may like to avoid solutions where certain variables vary too wildly or impose the prior that solutions to a business cycle model should exhibit fluctuations of period between 4 and 32 quarters in quarterly data. The paper provides conditions for existence and uniqueness of regularized solutions and proves that they are continuously (even differentiably) dependent on their parameters. Thus, regularized solutions can be applied in any mainstream econometric method, frequentist or Bayesian.

As an application, the paper considers two models whose limiting Gaussian likelihood functions can be derived analytically. The exercise illustrates concretely the problems of ill-posedness alluded to earlier and the ability of regularization to restore regularity and allow for both frequentist and Bayesian analyses. Thus, the recommendation for empirical analysis is to either restrict attention to unique solutions or to use regularization.

This work is related to several recent strands in the literature. Komunjer & Ng (2011), Qu & Tkachenko (2017), Kociecki & Kolasa (2018), and Al-Sadoon & Zwiernik (2019) study the identification of LREMs based on the spectral density of observables. Christiano & Vigfusson (2003), Qu & Tkachenko (2012), Sala (2015) utilize spectral domain methods for estimating LREMs using ideas that go back to Hansen & Sargent (1980). Jurado & Chahrour (2018) study the problem of subordination (what they call “recoverability”) in the context of macroeconometric models. Al-Sadoon (2018) utilizes a generalization of Wiener-Hopf factorization in order to study unstable and non-stationary solutions ot LREMs. Ephremidze, Shargorodsky & Spitkovsky (2020) provide recent results on the continuity of spectral factorization. Finally, Al-Sadoon (2020) provides numerical algorithms for computing regularized solutions.

This paper is organized as follows. Section 2 sets up the notation and reviews the fundamental concepts of spectral analysis of time series. Section 3 provides a list of examples of simple LREMs and their solutions in the frequency domain. Section 4 introduces Wiener-Hopf factorization. Section 5 sets up the LREM problem, its existence and uniqueness properties, and establishes its ill-posedness. Section 6 introduces regularized solutions. Section 7 applies mainstream methodology to simple examples and illustrates the benefits of regularization. Section 8 concludes. Sections A-D comprise the appendix. Finally, the code for reproducing the symbolic computations and graphs is available in the Mathematica notebook accompanying this paper, spectral.nb.

2 Notation and Review

We will denote by , , and the sets of integers, real numbers, and complex numbers respectively. By we will denote the set of matrices of complex numbers. We will use to denote the identity matrix. For , . For , is the conjugate transpose of , and .

All random variables in this paper are defined over a single probability space . For a complex random variable , the expectation operator is denoted by . The space is defined as the Hilbert space of complex valued random variables , modulo -almost sure equality, such that with inner product and norm

Similar to other Hilbert spaces we will consider in this paper, is a set of equivalence classes of functions and not a set of functions. However, mathematical convention “relegate[s] this distinction to the status of a tacit understanding” (Rudin, 1986, p. 67). Thus, we will write “” instead of “ for -almost all ” and similarly for elements of all of the other Hilbert spaces we consider in this paper. The space is defined as the Hilbert space of -dimensional vectors of complex valued random variables , , , with the inner product and norm

Let the stochastic process

have the property that is constant and depends on and only through . Such a process is known as a covariance stationary process. Given , we may define a number of useful objects.

First, we may define , the closure in of the set of all finite complex linear combinations of the set . We define to be the Hilbert space of all with for .

Traditionally, spectral analysis utilizes the forward (rather than backward) shift operator,

It is well known that extends uniquely to a bijective linear map satisfying for all (Lindquist & Picci, 2015, Theorem B.2.7).

We may next define the unique spectral measure on the unit circle, , which satisfies

(Lindquist & Picci, 2015, p. 80). Many books express the integral as ; the notation here is substantially more compact. When is absolutely continuous with respect to normalized Lebesgue measure on , defined by

then the Radon-Nikodým derivative is the spectral density matrix of . Note that the spectral density of -dimensional standardized white noise is . Another important example of a spectral measure, is the Dirac measure at defined as

for Borel subsets . Note that is the spectral measure of a process of the form for , with .

We may also define the Hilbert space of all Borel-measurable mappings , modulo -almost everywhere equality such that with inner product and norm

We define to be the Hilbert space of all with for endowed with the inner product and norm

The spectral representation theorem states that

for a vector of random measures with and for Borel subsets (Lindquist & Picci, 2015, Theorem 3.4.1). Many books express the integral above equivalently as , where for ; again, the notation here is substantially more compact. The spectral representation theorem establishes a unitary mapping defined by (Lindquist & Picci, 2015, Theorem 3.1.3). We call the spectral characteristic of . Thus,

In particular,

Denote by the -th standard basis row vector of . The spectral representation theorem implies that , the closure in of the set of all finite complex linear combinations of , is in correspondence with the closure of the set of all finite complex linear combinations of in , denoted . and are defined analogously. This implies that the orthogonal projection of onto in is

where is the orthogonal projection of onto in . Thus, the best linear prediction of in terms of is given by

It is easily established that and for all (Lindquist & Picci, 2015, p. 44). It follows that for all and likewise for all (Lindquist & Picci, 2015, Lemma 2.2.9). Thus

If is a stochastic process such that is covariance stationary, we will say that is causal in if . Finally, if is causal in and satisfies for all , we call an innovation process.

3 Examples

Armed with the basic machinery above, we now make a first attempt at solving LREMs in the frequency domain. We will see that solving simple univariate LREMs involves only elementary spectral domain techniques as discussed in textbook treatments of spectral analysis such as Brockwell & Davis (1991) or Pourahmadi (2001). The methods also provide strong hints to the general approach to solving LREMs. In this section, is a scalar covariance stationary process with , , , , and defined as in the previous section.

3.1 The Autoregressive Model

We begin on familiar territory.

| (1) |

with . The frequency-domain analysis of this model is available in many textbooks. For completeness, we provide a treatment here that is geared towards understanding the more general cases to come.

We require a stationary solution causal in (further motivation of this restriction can be found in Section 5). Thus, we require

for some spectral characteristic .

Notice that we may restrict attention to the equation

If a solution to exists, then the rest of process can be generated as

and clearly satisfies (1).

Thus, we must solve

In the frequency domain, we have

| (2) |

Since the linear mapping on is bounded in norm by , we see that the mapping is invertible so that

is the unique solution to (2), where the summation is understood to converge in the sense (Gohberg et al., 2003, Theorem 2.8.1). Thus, we arrive at the unique solution to ,

The interchange of the summation and the stochastic integral is admissible because the stochastic integral is a bounded linear operator mapping from to and the inner summation converges in . It follows that the unique stationary solution is

The operator is interchangeable with the summation because it is a bounded linear operator on and the summation converges in .

3.2 The Cagan Model

The Cagan model is given as,

| (3) |

with . Again, we look for a stationary solution causal in and we restrict attention to the equation

and, following a similar argument to that used above, we arrive at the underlying frequency domain problem,

| (4) |

Since the linear mapping on is bounded in norm by , we see that the mapping is invertible so that

is the unique solution to (4), where the summation is understood to converge in the sense (Gohberg et al., 2003, Theorem 2.8.1). Thus, we arrive at the unique solution to ,

The interchange of the summation and the stochastic integral is admissible because the stochastic integral is a bounded linear operator mapping to and the inner summation converges in . It follows that the unique stationary solution is

The operator is interchangeable with the summation because it is a bounded linear operator on and the summation converges in .

3.3 The Mixed Model

Now suppose we have the more general model

| (5) |

where and . This leads to the frequency-domain equation

| (6) |

As noted by Sargent (1979), the solution to this system depends on the factorization of

We assume, without loss of generality, that . There are four cases to consider.

Suppose . We can then write and express the system as

The first equation can be solved as in the Cagan model (since ), while the second can be solved as in the autoregressive model (since ). This procedure leads us to the unique solution

In the time domain, we obtain the following solution

which then gives us the general solution,

Next, suppose that . Then we may write and express our system as

The first equation does not have a unique solution in general. For example, when , then solves the equation for any . More generally, every solution is of the form

where with orthogonal to . We can then solve for as

In the time domain, this leads to the general solution

where for is an arbitrary innovation process. Indeed, for all because and is orthogonal to for all because as is orthogonal to .

Now suppose . Then we may write and

Clearly can be solved as in the Cagan model to produce

This implies that

However, the right hand side is not generally an element of . To see this, let , then is an orthonormal set and the equation above reduces to , which is orthogonal to .

Finally, suppose either or so that for some . Then there is no solution in general, in the sense that there exist processes for which no stationary solution can be found. To see this, let , the Dirac measure at . If a solution to (6) exists, then it must satisfy

This then implies that in , which implies that , contradicting the fact that .

4 Wiener-Hopf Factorization

The approach we have taken in the last section is well understood in the theory of convolution equations (Gohberg & Fel’dman, 1974). The requisite factorization of into two parts, a part to solve like the Cagan model and a part to solve like the autoregressive model, is known as a Wiener-Hopf factorization (Wiener & Hopf, 1931). In this section, we state the basic concepts and properties of Wiener-Hopf factorization that we will need.

Definition 1.

Let be the class of functions defined by

| (7) |

where for and . Define to be the class of functions (7) with for . The sets , are defined as the sets of matrices of size populated by elements of and respectively.

The class of functions is known as the Wiener algebra in the functional analysis literature (Gohberg et al., 1993, Section XXIX.2). Note that every function analytic in a neighbourhood of defines an element of but the opposite inclusion does not hold (e.g. diverges outside ). For , we also have that

where is the –essential supremum of .

Definition 2.

A Wiener-Hopf factorization of is a factorization

| (8) |

where , , , , and is a diagonal matrix with diagonal elements , where are integers, called partial indices.

We remark that the factorization given in Definition 2 is termed a left factorization in the Wiener-Hopf factorization literature (Gohberg & Fel’dman, 1974, p. 185). It differs from the right factorization utilized in Onatski (2006) and Al-Sadoon (2018), where the roles of are reversed. The difference is due to the fact that the present analysis works with the forward shift operator, whereas Onatski (2006) and Al-Sadoon (2018) work with the backward shift operator. A left factorization of is obtained from a right factorization of .

Theorem 1.

Let and suppose for all . Then has a Wiener-Hopf factorization and its partial indices are unique.

Proof.

The condition in Theorem 1 is minimal for existence a Wiener-Hopf factorization and uniqueness of the part. The parts are not unique but their general form is well understood (Gohberg & Fel’dman, 1974, Theorem VIII.1.2). The non-uniqueness of has no bearing on any of our results. Wiener-Hopf factorizations can be computed in a variety of ways (see Rogosin & Mishuris (2016) for a recent survey).

The partial indices allow us to identify an important subset of .

Definition 3.

Let be the subset of such that for all and .

When , so that is the set of such that for all . Notice that for every element of , the partial indices are either all non-negative, all non-positive, or all zero. This implies that for every element of ,

where is equal to 1, , or 0 according to whether the argument is positive, negative, or zero respectively. Since is the winding number of as traverses the unit circle counter-clockwise (Gohberg & Fel’dman, 1974, Theorem VIII.3.1 (c)), we can easily determine the sign of the partial indices of elements of by looking at the winding number. The importance of this fact will become clear in the next section when we combine it with the following fact.

Theorem 2.

If is endowed with the –essential supremem norm then is open and dense in .

Proof.

See the proof of Theorems 1.20 and 1.21 of Gohberg et al. (2003). ∎

Theorem 2 implies that the generic or typical element of that admits a Wiener-Hopf factorization is an element of . Said differently, the elements of are non-generic or exceptional in the space of Wiener-Hopf factorizable elements of .

To see the role played by Wiener-Hopf factorization, consider system (6) again. In the first case, factorized as

| In the second case, factorized as | ||||||||

| In the third case, factorized as | ||||||||

In the fourth case, for some and there does not exist a solution in general. Notice that the case of existence and uniqueness is associated with a partial index of zero, the case of existence and non-uniqueness is associated with a positive partial index, and the cases of non-existence in general is associated with a negative partial index and/or a zero of . These associations are not accidental as we will see in the next section.

5 Existence and Uniqueness

Given the Wiener-Hopf factorization techniques, we can now address the general LREM problem in the frequency domain. Our first task is to define existence and uniqueness of solutions to the LREM problem in the time domain.

Definition 4.

An LREM is a pair , expressed formally as

| (9) |

where is exogenous and is endogenous.

The model in (9) is understood as a set of structural equations relating current, expected, and lagged values of the endogenous process to current, expected, and lagged values of exogenous economic forces . typically consists of economic variables of interest, such as output, inflation, and the interest rate, that we seek to explain in terms of underlying economic forces , such as shocks to technological growth or economic policy. Occasionally, researchers also consider solutions driven by sunspots, economic forces that do not appear explicitly in the system (their associated columns of are equal to zero) but are nevertheless considered to influence the behaviour of the solution; we discuss these solutions further in Section 6. The dimension of may be larger or, as is typically the case in modern LREMs, smaller than the dimension of .

The class of models considered in Definition 5 includes the class of structural equation models ( and are constant), the class of structural VARMA models ( and are matrix polynomials in ), and all LREMs considered in Canova (2011), DeJong & Dave (2011), and Herbst & Schorfheide (2016). For example, the model of Smets & Wouters (2007), studied in Section 6.2 of Herbst & Schorfheide (2016), consists of endogenous variables and exogenous shocks.

Now in order to endow (9) with mathematical meaning, we must first note that LREMs are distinguished among mathematical systems in that they take as inputs not only realizations of exogenous inputs but also a spectral measure .

That is because the output of an LREM solves a system of equations in past, present, as well as expected values of . In the time domain perspective on LREMs, the role of is played by a filtration with respect to which conditional expectations can be computed (Al-Sadoon, 2018, Definition 4.2). Here, conditional expectations are substituted by linear projections, the natural analogue to expectations in the frequency domain and, in order to compute projections, needs to be specified as well. We will see that the transfer function of solutions requires the triple , while the realizations of the output require, additionally, the realizations of the inputs. In following this system-theoretic approach to LREMs, therefore, we will often use phrases such as “for every spectral measure ” or “for every stationary process ”.

Definition 5.

Let be a zero-mean, -dimensional, covariance stationary process with spectral measure and let be an LREM. A solution to is an -dimensional covariance stationary process , causal in , and satisfying

| (10) |

where the series converge in . We say that has no solution in general if it is possible to find a such that no solution to exists. A solution is unique if whenever is also a solution, then for all .

By Definition 5, an LREM is a mathematical system that transforms arbitrary covariance stationary inputs into covariance stationary outputs (Kalman et al., 1969; Kailath, 1980; Sontag, 1998; Caines, 2018). The restriction to stationarity involves no loss of generality of the LREMs considered in practice as and typically describe deviations away from a steady state (Canova, 2011; DeJong & Dave, 2011; Herbst & Schorfheide, 2016). The mathematics of non-stationary LREMs is developed in Al-Sadoon (2018).

Definition 5 also restricts attention to causal solutions. This is because the purpose of an LREM, similarly to structural VARMA, is to explain the behaviour of economic variables in terms of past and present economic shocks and to obtain impulse responses. It makes little sense to consider models where current inflation is determined by a future shock to technology, for example. Note, however, that we do not impose invertibity of in terms of as it is not necessary for our purposes, although it does become necessary for estimation purposes (see Al-Sadoon & Zwiernik (2019)).

As in the previous section, it suffices to solve the equation

For if is a covariance stationary process causal in and satisfies this system, applying the forward shift operator times to each equation we obtain (10). Of course, the forward shift operator commutes with the summation because the sum converges in . Let have the spectral characteristics . Then the frequency domain equivalent is

| (11) |

Classical frequency domain theory is built on the backwards shift operator . In order to analysis (11), we will need an additional, closely related, operator.

Definition 6.

Define to be the operators

We write for the operator (resp. ) composed with itself (resp. ) times and we define , the identity mapping.

The following lemma (proof omitted) lists the most important properties of and .

Lemma 1.

The operators and have the following properties:

-

(i)

.

-

(ii)

for all .

-

(iii)

for all .

-

(iv)

is a right inverse of .

-

(v)

.

-

(vi)

.

-

(vii)

For all and , .

-

(viii)

For , .

Lemma 1 (i) states that the backwards shift operator is the adjoint of . Lemma 1 (ii) implies that the operator norm of is bounded above by 1. Lemma 1 (iii) implies that is an isometry (Gohberg et al., 2003, Theorem X.3.1). This implies that the operator norm of is equal to 1. Lemma 1 (iv) establishes that is right-invertible. Lemma 1 (v) clarifies the obstruction to left-invertible of as may be non-trivial. For example, when and , then . Since is the set of spectral characteristics associated with innovations to , if and only if is purely deterministic (Lindquist & Picci, 2015, Definition 4.5.1). Lemma 1 (vi) expresses the intuitive fact that the dimension of the innovation space of a stationary process is bounded above by the dimension of the process. Lemma 1 (vii) is a convenient expression for iterates of the operator. Finally, Lemma 1 (viii) decomposes the kernel of into a direct sum generated by the kernel of . It follows, since is an isometry, that . The time-domain analogue of the decomposition in Lemma 1 (viii) is the familiar one from Broze et al. (1985, 1995), where a process causal in satisfies

if and only if

That is, if and only if is representable as the sum of the prediction revisions between and for all .

The fact that the operators are uniformly bounded in the operator norm by 1 (Lemma 1 (i) and (ii)) ensures that is a bounded linear operator on whenever (Gohberg et al., 1990, Theorem I.3.2). More generally, we have the following definition, adopted from Gohberg & Fel’dman (1974).

Definition 7.

For with -th element , define as

where the series converges in the operator norm, and as

Since , the operator norm of is bounded above by . Note that by Lemma 1 (i), .

Definition 7 allows us to express (11) more compactly as,

| (12) |

Recall that the spectral characteristic of is . Thus, we have arrived at a linear equation in the Hilbert space . Equations (2), (4), and (6) are special cases of (12).

As we saw in Section 3, the first step towards inverting is to obtain a Wiener-Hopf factorization of ,

By Theorem 1, this factorization exists if for all . Then , , and can be defined as in Definition 7 and it is easily checked that

a fact that at first seems trivial until one recalls that is not generally equal to when (Lemma 1 (iv) and (v)). Then (12) can be broken up into a system of three equations,

The first system involves only the operator and is solved as in the Cagan model; the third system involves only the operator and is solved as in the autoregressive model; and the second system may involve either of the operators or and is where non-existence and non-uniqueness may arise. To see this, note that implies that

are well defined bounded linear operators on and

where is the identity mapping on . Finally, if all of the partial indices of are zero, then is invertible (it is equal to ). However, since is generally invertible only on the right (see Lemma 1), the best we can hope for is right invertibility of and therefore . Clearly, is right invertible if and only if all the partial indices of are non-negative; in that case, a right inverse of is given as

| (17) |

However, there are generally infinitely many other right inverses of . Every right inverse of is of the form for some right inverse of .

The theoretical foundations for existence and uniqueness are now complete and all that remains is to apply well-known cookie-cutter results from functional analysis along with the simple techniques we employed in Section 3.

Lemma 2.

If is an LREM, for all , and has a Wiener-Hopf factorization (8), then for every spectral measure there exists a satisfying (12) if and only if the partial indices of are non-negative. The general form of the solution is then

| (18) |

where

| (19) |

and . The solution is unique for every spectral measure if and only if the partial indices of are all equal to zero.

Proof.

Lemma 2 provides necessary and sufficient conditions for existence and uniqueness of solutions irrespective of the exogenous inputs. This is in following with our system-theoretic approach to LREMs. Of course, restricting attention to a particular and , we can say slightly more. For example, if the partial indices are non-negative and has the property that then by Lemma 1 (viii), and there is a unique solution to (12). That is to say, there can be no multiplicity of solutions for a perfectly predictable . This point is made in a different context in Al-Sadoon (2018), p. 641.

In the special case of a structural VARMA model, Lemma 2 reduces to the classical result that if for all , there exists a unique causal stationary solution for every spectral measure (Hannan & Deistler, 2012, Sections 1.1-1.2). This is due to the fact that in that case and is a Wiener-Hopf factorization of . Note that the problem of uniqueness does not arise in the case of structural VARMA.

Lemma 2 states that is made up of spectral characteristics corresponding to arbitrary innovation processes (see Appendix A for a detailed analysis of ). The time-domain analogue of this result is the fact that non-unique solutions are driven by arbitrary innovation processes (Al-Sadoon, 2018, Theorem 4.1). The dimension of is the dimension of the innovation space of multiplied by the winding number of . This number is obtained in Funovits (2017, 2020) based on the Sims (2002) framework (see also Sorge (2019)).

Lemma 2 begs the question of what happens if zeros are present on the unit circle. This is addressed in the next result.

Lemma 3.

If is an LREM, for some , and , there exists a spectral measure such that (12) has no solution.

Proof.

Let satisfy and choose . If a solution to (12) exists, it must satisfy . Since for –a.e. , it follows that . This implies that . Since for –a.e. and , . This implies that , a contradiction. ∎

The basic idea behind Lemma 3 is that when for some , the system has a form of instability akin to that of a resonance frequency in a mechanical system. When such a system is subjected to an input oscillating at frequency , its output cannot be stationary. In particular, a mechanical system will oscillate with increasing amplitude until failure (Arnold, 1973, p. 183). In the parlance of system theory, the system is said to have an unstable mode (Sontag, 1998, Chapter 5).

The rank condition on in Lemma 3 permits inputs at frequency to excite the instability in the system. In the VARMA literature it is typically assumed that for all (Hannan & Deistler, 2012, Chapter 2). In the systems theory literature, similar conditions characterize controllability of the output in terms of the input (Kailath, 1980, Chapter 6). Without a condition of this sort, there may be no input that can excite the system’s instability. For example, the LREM has a solution for any . Note that this condition permits oscillatory inputs to excite instability but not necessarily white noise inputs. For example, the LREM has and so that the conditions of Lemma 3 are satisfied but the instability of the system cannot be excited by a white noise input because, as is easily checked, is a solution to (12) when . It is possible to formulate a different condition on that will permit white noise inputs to excite instability in the system and, indeed, much more can be said about stability in LREMs. However, a general analysis of stability of LREMs is outside the scope of this paper and is left for future research.

To summarize.

Theorem 3.

Let be an LREM.

-

(i)

If for all , then for every covariance stationary process there exists a solution to if and only if the partial indices of are non-negative. The general form of the solution is

where is given in (19), , and the dimension of the solution space is the dimension of the innovation space of times the winding number of . The solution is unique for every if and only if the partial indices of are all equal to zero.

-

(ii)

If for some and , then there exists no solution to in general.

The relationship between the partial indices and existence and uniqueness of solutions to LREMs was first discovered by Onatski (2006). The general expression of solutions is similar to the one obtained in Theorem 4.1 (ii) of Al-Sadoon (2018). Lubik & Schorfheide (2003), Farmer et al. (2015), Bianchi & Nicolò (2019), and Al-Sadoon (2020) provide computational methods for obtaining the solution in Theorem 3.

We can also state the following result for generic systems (i.e. systems in ), a more specialized version of which is also due to Onatski (2006).

Theorem 4.

For generic with for all , there exists possibly infinitely many solutions, a unique solution, or no solution in general according to whether winds around the origin a positive, zero, or a negative number of times as traverses counter-clockwise.

In closing, it is important to note that the assumptions underlying existence and uniqueness in this paper are weaker than in all of the previous literature on frequency domain solutions of LREMs, namely the work of Whiteman (1983), Onatski (2006), Tan & Walker (2015), and Tan (2019). These works require the exogenous process to have a purely non deterministic Wold (1938) representation, an assumption that is demonstrated to be unnecessary. The weaker assumptions of this paper have also facilitated discussion of zeros of , an aspect of the theory absent from the previous literature. The advantage of these stronger assumptions, however, is that they do permit very explicit expressions of solutions. See Appendix B for a more detailed discussion.

6 Ill-Posedness and Regularization

Current macroeconometric methodology obtains LREMs from theoretical consideration (e.g. inter-temporal optimization of firms and households) and imposes only the first of Hadamard’s conditions of well-posedness, existence. In this section, we show that the other two conditions, uniqueness and continuity, are violated and discuss the consequences of these violations. This leads to the development of a new regularized solution to LREMs with important regularity properties.

6.1 Non-Uniqueness

Non-uniqueness has long been a feature of the LREM problem in macroeconometrics. The first approach to non-uniqueness, proposed by Taylor (1977), chooses the solution that minimizes the variance of the price variable in the model if one exists. Taylor motivates this solution by asserting that collective rationality of the economic agents in the model will naturally lead them to coordinate their activities to achieve this solution. Unfortunately, this provides no guidance for models in which indeterminacy afflicts non-price variables.

The second approach to non-uniqueness obtains a particular solution and sets in (18). This is the “minimum state variable” approach of McCallum (1983). It ought to be emphasized, however, that there are generally infinitely many ways to obtain particular solutions, one for every right inverse of . For example, in the Cagan model of Section 3 with , is a right inverse of for every . Thus, the concept of minimum state variable solution is not well-defined without specifying the particular right inverse to be used for the solution. Geometrically, a minimum state variable solution picks a point on by committing to a particular choice of right inverse to and ignoring all other solutions (see Figure 1). From a practical perspective, solving the LREM by one algorithm may lead to one minimum state variable but a different algorithm might lead to a completely different minimum state variable solution.

Finally, the modern approach to non-uniqueness, as exemplified by Lubik & Schorfheide (2003), Farmer et al. (2015), and Bianchi & Nicolò (2019) uses the general expression in Theorem 3. Here, every solution is represented as , where . That is, every solutions is represented as a particular solution plus a part generated by arbitrary innovation processes, also known as sunspots (Farmer, 1999). Both the particular solution and the sunspot are parametrized and the parameters are then estimated from data. The geometry of the spectral approach allows us to see very clearly a serious conceptual problem with this approach. Various papers in the literature claim to present evidence of the importance of sunspots as drivers of macroeconomic activity by showing that the contribution of sunspots, as measured by the size of the estimated , is not insignificant empirically. However, it is clear from Figure 2 that the size of very much depends on the particular solution; by one representation, the solution is and sunspots play a large role, by another representation sunspots play a small role. Without a sound economic reason for the choice of particular solution, it is unclear that the contribution of sunspots is being measured correctly. Thus, the modern approach suffers from a similar difficulty as the minimum state variable approach.

It emerges, therefore, that the problem of non-uniqueness was never fully resolved in the macroeconometrics literature. Although sunspots have played an important role in macroeconomic theory, conceptualized as “self-fulfilling expectations” and “animal spirits,” the empirical methodology employed for measuring the contribution of sunspots rests upon an arbitrary choice of the particular solution without any economic foundations.

6.2 Discontinuity

Even if one remains unconvinced of the importance of selecting the particular solution based on sound economic reasoning, there remains the problem of discontinuity. It is an unfortunate fact that particular solutions to an LREM can be discontinuous in its parameters; this occurs when is non-generic, i.e. an element of . This is compounded by the fact that LREMs are typically parametrized purely on theoretical considerations, without any regard to statistical properties, so that elements of are not expressly excluded (Onatski, 2006; Sims, 2007). We will illustrate this discontinuity with the simplest possible example. It is, of course, possible to illustrate discontinuity using a more realistic example based on an LREM that is used in practice but doing so comes at the cost of analytic tractability, as solving even the simplest multivariate LREMs can be quite cumbersome.

Consider the following example,

| (24) |

with . Thus, is a standardized white noise process.

In order to compute solutions we will need to obtain a Wiener-Hopf factorization,

Thus, there exists a non-unique solution for every . Define as in Definition 7, . We will restrict attention to minimum state variable solutions (i.e. in (18)),

The solution is clearly discontinuous at . In particular,

tends to infinity as . Thus, discontinuities can arise in the process of solving an LREM.

While this discontinuity may be quite jarring to readers acquainted with the LREM literature, from the Wiener-Hopf factorization literature point of view there is nothing surprising about this discontinuity. Indeed, (24) is a minor modification of the example given in Section 1.5 of Gohberg et al. (2003). The fact that only multivariate systems with non-unique solutions can exhibit this discontinuity may explain why discontinuity has not received sufficient attention in the LREM literature. The heart of the problem is that, when , there are points in at which partial indices are discontinuous, these are precisely the non-generic set (Gohberg et al., 2003, Corollary 1.22). That is, if has partial indices satisfying , then there are small (in the –essential supremum norm) changes in that lead to a jump in and since has undergone only a small change, must also jump. If we then choose a fixed left inverse in the solution (18) (e.g. choosing as in (17)), then the discontinuity can affect the solution. This is, unfortunately, what is done in all existing solution algorithms (Al-Sadoon, 2018, 2020). In our example, the partial indices of are for and for ; and for . The discontinuity in the partial indices is what generates the discontinuity of the Wiener-Hopf factors, which in turn generates a discontinuity in the solution.

It bears emphasising that this discontinuity is a feature of the mathematical problem, it is not a feature of the particular algorithm used to solve the problem; Al-Sadoon (2020) shows how it arises in the Sims (2002) framework, Al-Sadoon (2018) shows how it arises in a linear systems framework, and Appendix C shows how it arises when solving the system by hand. It is also important to note that the discontinuity of Wiener-Hopf factorization implies that there can exist no numerically stable way to compute it generally. While the elements of can be factorized using finite precision arithmetic, the elements of cannot be factorized without infinite precision. Thus, it is a non-starter to verify numerically whether a given system is generic or not in the process of estimation and inference. Note that an analogous problem arises for Jordan canonical factorization, which is discontinuous at a non-generic set of matrices in when (Horn & Johnson, 1985, pp. 127-128); there, the recommendation is to compute the Schur canonical form instead; and in the next section we will propose, similarly, to compute a different solution to the LREMs than the one provided in Theorem 3.

The continuous dependence of a model on its parameters is a necessary ingredient of all estimation and inference techniques. In Section 7 it is demonstrated that mainstream frequentist and Bayesian methods break down completely in the context of the model above.

6.3 Regularization

Having established that the LREM problem in macroeconometrics is ill-posed, we now consider how to obtain economically meaningful solutions amenable to mainstream econometric techniques.

Perhpas the most natural solution to the ill-posedness problem is to restrict attention to systems with unique solutions (i.e. LREMs , where the partial indices of are equal to zero). Al-Sadoon & Zwiernik (2019) have shown that unique solutions are not only continuous in the parameters of an LREM but also analytic (see the proof of Theorem 6.2). A less restrictive solution is to allow for non-uniqueness but restrict attention to generic systems (i.e. ). However, genericity cannot be taken for granted as both Onatski (2006) and Sims (2007) have warned and some models may be parametrized to always fall inside (interestingly, Sims (2007) is widely but erroneously considered to be a critique of Onatski (2006), see Al-Sadoon (2019)). Moreover, we need differentiability, not just continuity, in order to ensure asymptotic normality of extremum estimators (Pötscher & Prucha, 1997; Hannan & Deistler, 2012). Therefore, we opt for a more straightforward solution, regularization.

With the geometry of the spectral approach in view, one is led inexorably to consider the Tykhonov-regularized solution to (12), which minimizes the total variance, among all solutions to (10),

It can be shown that , where is the Moore-Penrose inverse of (Groetsch, 1977, p. 41). This takes a particularly simple form in our context.

Lemma 4.

If , for all , and the partial indices of are non-negative then,

Proof.

Lemma 4 implies a very simple technique for computing the Tykhonov-regularized solution. Whenever a solution to (12) exists, the Tykhonov-regularized solution is obtained as the unique solution to the auxiliary block triangular frequency domain system,

This implies that whenever a solution exists, the regularized solution is obtained uniquely by solving an auxiliary LREM. For example, in the mixed model from Section 3, the Tykhonov-regularized solution is the solution to the auxiliary LREM,

This regularized solution exists and is unique whenever the original system satisfies the conditions for existence.

Note that when the partial indices of are all equal to zero, . In other words, Tykhonov-regularization has no effect if the solution is unique.

More generally, we may consider

where is a bounded linear operator chosen by the researcher. Next, we consider economic motivation for a number of choices of .

If the researcher wishes to shrink the variance of the -th component of , they can set

Note that when the -th component is the price variable, we obtain the Taylor (1977) solution.

One can also also shrink expected values of . For example, if certain solutions obtained by the methods reviewed above yield expectations of output that are too variable relative to what one expects empirically, then one can impose this prior by using

where is the coordinate corresponding to output in .

Linear combinations of lagged, current, and expected values of coordinates of can also be shrunk similarly. The operator

shrinks the second difference of all variables, imposing smoothness on solutions, similar to the idea of the Hodrick & Prescott (1997) filter.

Note that the operators above belong to the class of operators defined in Definition 7. Thus, we can, more generally use any to construct the weight

More importantly, regularization can allow the researcher to shrink across frequencies. For example, the researcher may wish to shrink the spectrum of the solution towards frequencies of between and corresponding to business cycle fluctuations of period 4-32 quarters in quarterly data, i.e. using

Finally, we can consider solutions that minimize a finite weighted sum of individual criteria as reviewed above,

where and for . This would allow the researcher to impose different criteria according to the weights . This can be achieved by using

The argument for regularization is the same as employed throughout the inverse and ill-posed problems literatures: if theory is insufficient to pin down a unique continuous solution, other information can be employed. In our case, regularization allows economically meaningful shrinkage criteria to choose the best among all possible solutions or, what amounts to the same, it allows the researcher’s priors about economic behaviour to select the most appropriate solution. Regularization resolves the problem of selecting an economically grounded particular solution and, as we will soon see, also ameliorates the discontinuity problem.

Existence of regularized solutions is guaranteed whenever the given LREM satisfies the already minimal conditions for existence of solutions. That is because, according to Lemma 2, the set of all solutions is finite dimensional and so the problem of minimizing subject to reduces to a problem of minimizing a non-negative quadratic form (see Figure 3). Uniqueness of regularized solutions, on the other hand, is the subject of the next result.

Lemma 5.

If is an LREM, for all , the partial indices of are non-negative, and is a bounded linear operator, then for every spectral measure ,

where is the restriction of to , is a regularized solution to (12). This solution is unique for every spectral measure if and only if .

Proof.

See Appendix D. ∎

Lemma 5 finds a representative regularized solution and proves that it is unique if and only if . Geometrically, this condition requires the operator to put weight on all directions of indeterminacy of the LREM. If , it will be possible to perturb in any direction in to arrive at another regularized solution and uniqueness will fail. A host of other representations of are obtained in Appendix D.

Some special cases of Lemma 5 are particularly instructive. When , the regularized solution is unique regardless of . That is, when puts weight on all directions in the solution space, the regularized solution is unique. An example of this is , which produces the Tykhonov-regularized solution . When (i.e. the solution to the LREM is unique), the regularized solution is the unique solution regardless of . This is due to the fact that is the zero operator (because is the zero operator) and so that , the unique solution.

Theorem 5.

If is an LREM, for all , the partial indices of are non-negative, and is a bounded linear operator, then for every covariance stationary process there exists a solution minimizing given by

The solution is unique for every if and and only if .

Proof.

Follows from Lemma 5 and the spectral representation theorem. ∎

The expression for regularized solutions in Theorem 5 is primarily of theoretical interest. It will allow us to study continuity and differentiability with respect to underlying parameters. For estimation and inference, on the other hand, Al-Sadoon (2020) provides a numerical algorithm for computing regularized solutions in the Sims (2002) framework, which leads to equivalent algebraic rather than geometric criteria for existence and uniqueness.

We have shown that, with an appropriate choice of , the regularized solution can overcome the non-uniqueness problem. Our next result shows that regularized solutions also overcome the discontinuity problem. The continuity guarantee that we require for mainstream econometric methodology is not with respect to the norm but with respect to the –essential supremum norm; see e.g. the continuity results for bounded spectral densities and the Gaussian likelihood functions in (Hannan, 1973; Deistler & Pötscher, 1984; Anderson, 1985). If we parametrize and as and , then it is clear that we need and to be jointly continuous in and . However, Green & Anderson (1987) note that this is not sufficient to ensure continuity of the Wiener-Hopf factors in the –essential supremum norm. Thus, we use Green and Anderson’s idea of imposing control over and .

Theorem 6.

Let and . Under the conditions

-

(i)

.

-

(ii)

is an open set and .

-

(iii)

and are analytic in a neighbourhood of for every .

-

(iv)

, , , and are jointly continuous at every .

-

(v)

for all .

-

(vi)

for all , and the partial indices of are all non-negative.

Then , is continuous at in the –essential supremum norm.

Proof.

See Appendix D. ∎

The assumptions of Theorem 6 are quite strong relative to the discussion so far. However, the relevant case for most macroeconometric applications is the case where , while and are Laurent matrix polynomials of uniformly bounded degree. Indeed, all of the LREMs in Canova (2011), DeJong & Dave (2011), or Herbst & Schorfheide (2016) are of this form. In this case, the continuity of the coefficients of and is sufficient to ensure conditions (iii) and (iv) of Theorem 6.

For the purpose of establishing asymptotic normality, we typically need not just continuity in the essential supremum norm but also differentiability in the essential supremum norm (i.e. the finite differential in converges to the infinitesimal differential in the essential supremum norm over ). This stronger form of differentiability allows us to differentiate under integrals, which appear in the asymptotics of maximum likelihood and generalized method of moments estimators. The following result provides exactly what we need.

Theorem 7.

Let be a positive integer. Under assumptions (i) – (vi) of Theorem 6 and,

-

(vii)

, , , and are jointly continuously differentiable with respect to of all orders up to .

Then , is continuously differentiable of order with respect to at in the –essential supremum norm.

Proof.

See Appendix D. ∎

Condition (vii) of Theorem 7 is a direct strengthening of condition (iv) of Theorem 6. When and are Laurent matrix polynomials of uniformly bounded degree, as is usually the case in macroeconomic models, the -th order continuous differentiability of the coefficients of and is sufficient to ensure this condition is satisfied.

To see Theorem 7 in action, consider the regularized solution to the example from the previous subsection. This can be obtained analytically in just a handful of steps.

To invert the operator in the expression above, we note that it is of the form defined in Definition 7, with underlying element, . This matrix has the Wiener-Hopf factorization . Thus,

where the last equality follows from the fact that when . As guaranteed by Theorems 6 and 7, this solution is not just continuous as a function of but also smooth. Note that the implicit right inverse of in is

Thus, it is only by using a special right inverse of that we can absorb the effect of discontinuity in the partial indices at on the solution.

To summarize, the LREM problem in macroeconometrics is ill-posed. However, regularization produces solutions that are unique, continuous, and even smooth under very general regularity conditions.

7 The Limiting Gaussian Likelihood Function

As an application of the spectral approach to LREMs, we consider the limiting Gaussian likelihood function of solutions. We will follow mainstream methodology in disregarding uniqueness, identifiability, and invertibility in parametrizing the models we consider (see Al-Sadoon & Zwiernik (2019) for a careful parametrization that addresses all of these considerations). We will see that the limiting Gaussian likelihood function can display very irregular behaviour in the region of non-uniqueness, invalidating underlying assumptions of mainstream frequentist and Bayesian analysis. In turn, regularized solutions can avoid some of these anomalies. Of course, empirical analysis is conducted on the likelihood function or similar objective function and not its limit; however, it is easily checked that, in the examples below, all of our qualitative observations hold just as well for the empirical analogues. For the purposes of this section, we will assume that is purely non-deterministic with a rational spectral density of full rank; and are also rational; and . See Appendix B for further discussion of these assumptions.

Our assumptions imply that any solution to the LREM is representable as

where is an -dimensional standardized white noise (not necessarily Gaussian) and the transfer function is rational with no poles on or outside .

Now suppose that, instead of , the process were thought to have a different rational transfer function, with not identically zero. Then the -th auto-covariance matrix according to is . If we define and let be the covariance matrix of according to , then the Gaussian likelihood function evaluated at is given as

Up to a monotonic transformation, the Gaussian likelihood function is given by

The limit of this object is well known when is the transfer function of a Wold representation. However, this may not always be the case. For example, the Cagan model solution of Section 3 with and has a first impulse response of zero, which means that the transfer function of the solution is not invertible and so cannot correspond to a Wold representation. However, there always exists a which satisfies the conditions for a Wold representation such that (Lindquist & Picci, 2015, Theorem 4.6.7). Under certain regularity conditions (Theorem 4.1.1 and Lemmas 4.2.2 and 4.2.3 of Hannan & Deistler (2012)), converges almost surely as to

We will focus primarily on as it is a good approximation of and it can be computed analytically for simple LREMs. The computations and graphs of the subsequent subsections can be found in the Mathematica notebook accompanying this paper, spectral.nb.

7.1 The Cagan Model

Consider the limiting Gaussian likelihood function of the Cagan model from Section 3 when , restricting attention to real parameters (Lubik & Schorfheide (2004) study the Gaussian likelihood of this model for a single sample). Then has the Weiner-Hopf factorization

Thus, the true model can be expressed as

where we have used the fact that for and . The spectral density of the true model is then given as

Consider the limiting Gaussian likelihood function when is specified correctly with parameters and as

We may choose the following Wold representation of ,

This implies that the limiting Gaussian likelihood function when is given by

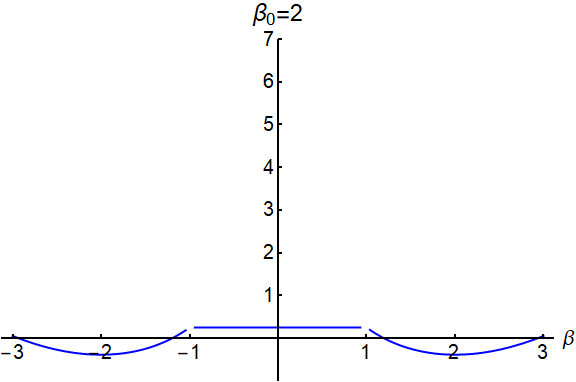

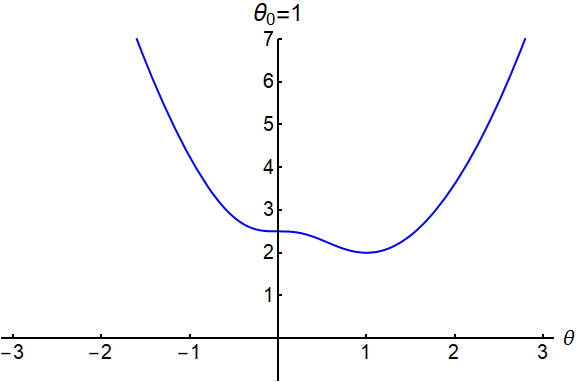

The contours of this function are plotted in Figure 4. The limiting Gaussian likelihood function diverges as the parameters approach the boundary of non-invertiblity, (Hannan & Deistler, 2012, p. 114); hence the white regions in the figure. The most important feature to note is the extent of non-identifiability in this model. is minimized at the set , where ; indeed, for , is an all-pass function. Compounding this non-identifiability, any algorithm tasked with either optimizing or exploring is guaranteed to fail to converge if not initiated in the region ; it is easily checked that such algorithms will tend to either or , none of which are in the parameter space.

If, on the other hand, , then

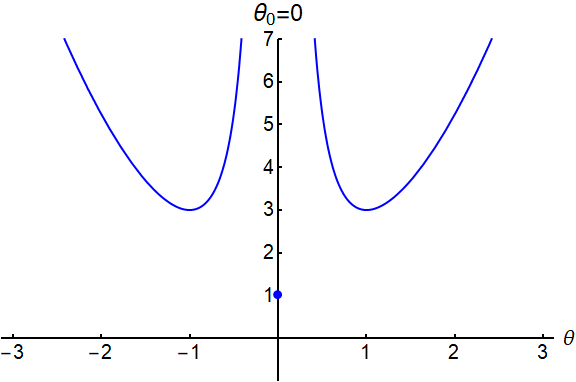

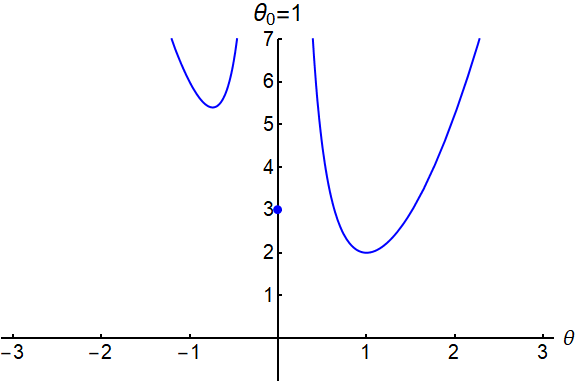

Irregularity is still a feature of when . This function is plotted in Figure 6 for . Since the gradient of this function is rational in and , we can obtain all of its critical points exactly (Cox et al., 2015, Section 3.1); these are the dots highlighted in the figure. In addition to the global minimizer at , there are two local minima. Just as in the case , if one should be so unfortunate as to initialize their algorithm in the wrong region, they will be guaranteed to fail to either optimize or explore the limiting Gaussian likelihood function. Things are made worse if . Figure 6 plots for and (this choice will become clear shortly). In this case, has two global minimizers at .

Consider now, the regularized solution of the Cagan model. It is easily checked that this corresponds to setting (hence the choice of earlier). We have,

This transfer function produces a white noise process with variance . Indeed, the ratio is an all-pass function. Therefore, if we specify correctly, then its Wold representation is

Now if , the limiting Gaussian likelihood function is given as

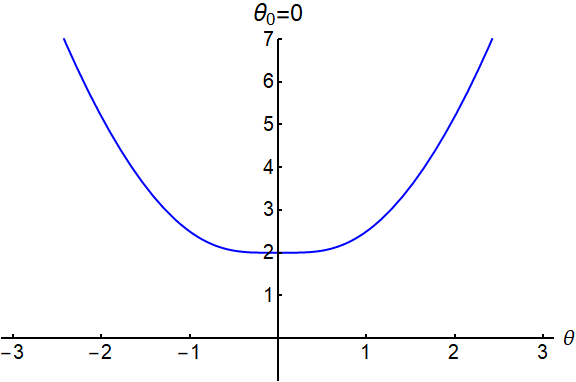

is minimized at the interval . See the left plot of Figure 7. Even though is still not identified, it suffers less identification failure than in the non-regularized solution.

If on the other hand, ,

Here the likelihood function is multi-modal. See the right plot of Figure 7. Thus, while regularization reduces identification problems substantially, it does not fully eliminate them.

In summary, we have found that even for the simplest of LREMs, the Cagan model, the Gaussian likelihood function exhibits some serious irregularities if the parameter space is not restricted to the region of uniqueness or the solution is not regularized. We have found that regularization helps circumvent some of these irregularities.

7.2 Non-Generic Systems

Consider now the non-generic system we studied in Section 6. The non-regularized solution is given by

If is correctly specified, then it has a Wold representation,

The limiting Gaussian likelihood function when is easily computed as

This function is minimized at the correct value of . However, it displays some very serious irregularities as seen in the left plot of Figure 9. The limiting Gaussian likelihood function is not continuous at . Indeed . Due to the local minima at , numerical optimization algorithms will not be able to find the global minimizer and will instead converge to one of the local minimizers.

The discontinuity of the limiting Gaussian likelihood function also affects any Bayesian analysis. Mainstream Markov Chain Monte Carlo methods, as surveyed in Herbst & Schorfheide (2016) for example, require the likelihood function to be continuous. Applied to the problem at hand, these algorithms will explore the posterior around the local minimizers and fail to explore the posterior at .

As these discontinuities occur at non-generic points, even plotting the empirical likelihood function or posterior will likely fail to detect them. We emphasise again that determining whether a given point is a point of discontinuity requires infinite precision, so it will not be feasible to check this numerically in the process of estimation and inference.

The limiting Gaussian likelihood function when is also easily computed as

This function is minimized at the correct value of . It continues to exhibit irregularities as seen in the right plot of Figure 9. Although the function is now continuous at its global minimizer, it is still discontinuous and has a local minimum both of which can potentially lead to incorrect estimation and inference.

Consider next the regularized solution to this system.

If is correctly specified, then by using elementary linear system methods (e.g. Theorem 1 of Lippi & Reichlin (1994)) it is easily shown that it has a Wold representation,

The limiting Gaussian likelihood function for this model can be computed exactly and is plotted in Figure 9 for and . Clearly regularization restores not just continuity but also smoothness. This is a direct corollary of Theorems 6 and 7.

In conclusion, the simple example above indicates serious problems with mainstream methodology. The assumption that a solution depends continuously on the parameters of a model is crucial for all mainstream methods of estimating LREMs as reviewed in Canova (2011), DeJong & Dave (2011), and Herbst & Schorfheide (2016). Mainstream frequentist analyses cannot allow for objective functions discontinuous at the population parameter and mainstream Bayesian analyses cannot accommodate posterior distributions with discontinuities at unknown locations. The solution is quite simple, either the parameter space should be restricted to the region of existence and uniqueness, as in Al-Sadoon & Zwiernik (2019), or regularization should be employed.

8 Conclusion

This paper has extended the LREM literature in the direction of spectral analysis. It has done so by relaxing common assumptions and developing a new regularized solution. The spectral approach has allowed us to study examples of limiting Gaussian likelihood functions of simple LREMs, which demonstrate the advantages of the new regularized solution as well as highlighting weaknesses in mainstream methodology. For the remainder, we consider some implications for future work.

The regularized solution proposed in this paper is the natural one to consider for the frequency domain. However, its motivation has been entirely econometric in nature and this begs the question of whether it can be derived from decision-theoretic foundations as proposed by Taylor (1977). Regularization has already made inroads into decision theory (Gabaix, 2014). This line of inquiry may yield other forms of regularization which may have more interesting dynamic or statistical properties.

The analysis of the Cagan model shows that the parameter space is disconnected and it can matter a great deal where one initializes their optimization routine to find the maximum likelihood estimator or their exploration routine for sampling from the posterior distribution. Therefore, it would be useful to develop simple preliminary estimators of LREMs analogous to the results for VARMA (e.g. Sections 8.4 and 11.5 of Brockwell & Davis (1991)) that can provide good initial conditions for frequentist and Bayesian algorithms.

Wiener-Hopf factorization theory has been demonstrated here and in previous work (Onatski (2006), Al-Sadoon (2018), Al-Sadoon & Zwiernik (2019)) to be the appropriate mathematical framework for analysing LREM. This begs the question of what is the appropriate framework for non-linear rational expectations models. The hope is that the mathematical insights from LREM theory will allow for important advances in non-linear modelling and inference.

Finally, researchers often rely on high-level assumptions as tentative placeholders when a result seems plausible but a proof from first principles is not apparent. Continuity of solutions to LREMs with respect to parameters has for a long time been one such high-level assumption in the LREM literature. The fact that it is generally false, should give us pause to reflect on the prevalence of this technique. At the same time, the author hopes to have conveyed a sense of optimism that theoretical progress from first principles is possible.

Appendix A Parametrizing the Set of Solutions

By Lemma 2, the set of solutions to (12) when is the affine space , where

it suffices to parametrize

The problem then reduces to the parametrization of for and, by Lemma 1 (viii), the problem reduces even further to the parametrization of . Now if , then for all and so . If , we may find an orthonormal basis for it,

Note that by Lemma 1 (vi). Lemma 1 (viii) then implies that

is an orothonormal basis for for . Thus,

where

Therefore, is the space of complex matrix polynomials in , with -th row degrees bounded by , multiplied by . Notice that if has partial indices at zero, then the last rows of are identically zero. The dimension of is obtained by counting the coefficients above, .

Appendix B Relation to Previous Literature

This section provides a review of the approaches of Whiteman (1983), Onatski (2006), Tan & Walker (2015), and Tan (2019) (henceforth, the previous literature). We will see that the previous literature makes significantly stronger assumptions about that also make it cumbersome to address the topic of zeros of . On the other hand, the stronger assumptions do allow for very explicit expressions of solutions.

The previous literature takes as its starting point the existence of a Wold decomposition for with no purely deterministic part. Thus, it imposes that be absolutely continuous with respect to and that the spectral density matrix has an analytic spectral factorization with spectral factors of fixed rank –a.e. (Lindquist & Picci, 2015, Theorems 4.4.1 and 4.6.8). Formally, the conditions are

| (25) | |||

Theorem II.8.1 of Rozanov (1967) provides equivalent analytical conditions. This paper has demonstrated that a complete spectral theory of LREMs is possible without imposing any such restrictions.

Clearly, the spectral factorization in (25) is not unique. However, there always exists a spectral factor unique up to right multiplication by a unitary matrix such that there is an satisfying

(Lindquist & Picci, 2015, Theorem 4.6.5). This choice of spectral factor yields a Wold representation. To see this, let

Then

Thus, is an -dimensional standardized white noise process causal in . It follows easily that so that . Since is a left inverse of ,

and so

is a Wold representation with

The previous literature imposes a priori the representation

before attempting to solve for the coefficients by complex analytic methods (Whiteman, 1983; Tan & Walker, 2015; Tan, 2019) or by Wiener-Hopf factorization (Onatski, 2006). This method cannot yield the correct solution if has a non-trivial purely deterministic part. In fact, the representation above need not be assumed a priori and can be derived as a consequence of Theorem 3 under conditions (25).

where

Thus we have obtained the spectral characteristic of relative to the random measure associated with . It follows that is indeed representable as a moving average in with coefficients,

It is important to note, however, that the stronger assumptions of the previous literature lead to a more explicit expression for spectral characteristics of solutions. In particular,

where whenever . This follows from the fact that is orthogonal to . It then follows that

because . Finally, using the results of Appendix A, , where is a matrix polynomial in . Thus,

and so

An interesting special case is when , , and are rational. If is rational, any Wiener-Hopf factors are rational as well (Clancey & Gohberg, 1981, Theorem I.2.1). If is rational, the associated can also be chosen to be rational (Baggio & Ferrante, 2016, Theorem 1). Thus, and are also rational.

Finally, we note that the previous literature has avoided any mention of zeros of . Indeed, it is substantially more difficult to deal with zeros of without the general theory of this paper because one no longer has access to degenerate spectral measures (e.g. the Dirac measure) that can straightforwardly excite the instability of the system.

Appendix C Solving the Non-Generic System

Consider solving the system (24) by hand when . In the time domain, this is given by

| (26) | ||||

| (27) |

where is a standard white noise process. Macroeconomic textbooks (e.g. Sargent (1979)) implicitly assume the admissibility of the following elementary operations for solving LREMs.

-

(i)

Multiply both sides of equation by a non-zero constant.

-

(ii)

Apply the mapping, , to both sides of equation and add the resultant to equation .

-

(iii)

Permute equations and .

These elementary operations are a direct generalization of the familiar row-reduction elementary operations in linear algebra () as well as the elementary operations for VARMA manipulation (). See p. 39 of Hannan & Deistler (2012).

We seek a process causal in that solves (26) and (27). The most immediate solution does not require any of the elementary operations above. It can be obtained by noting that, since , we can set

then substitute into equation (27) and, noting that , we obtain

We therefore obtain the solution

which is clearly causal in . However, this is not the only way of solving the problem. If we multiply both sides of equation (26) by (operation (i)), we obtain

Now apply to both sides of equation (27) and add the resultant to equation (26) (operation (ii)) to obtain

Thus, we can set

Plugging this into (27), we obtain

which allows us to set (using operation (i)),

Finally, permuting the two equations we have obtained (operation (iii)), we obtain the alternative solution

This is precisely the solution obtained in Section 6.

Appendix D Proofs

Define for and , and, for , . Set to be the limit of as whenever it exists. Clearly is a unitary operator on , is a bounded operator on , and is not generally bounded on .

We will need the following inequality, inspired by similar inequalities of Anderson (1985) and Green & Anderson (1987), to prove our main results.

Lemma 6.

If and , then

Proof.

Let be the counter-clockwise segment of from to and let be the indicator function for that segment. By a change of variables

Since , is –integrable so the right hand side converges to for – a.e. and , the Lebesgue points of (Rudin, 1986, Theorem 7.10). On the other hand, since converges in , the continuity of the inner product implies that the left hand side converges to . Therefore,

It follows by the triangle and Jensen’s inequality that

Now among all Lebesgue points of , choose a such that . Thus,

Since we have

Now simply take the essential supremum on the left hand side (Rudin, 1986, p. 66). ∎

We will also need a notion of differentiation of operators that interacts well with . For an arbitrary , define to be the operator limit of as if it exists. Note that is the operator derivative of at . Also, for and ,

If is analytic in neighbourhood of , takes a particularly simple form.

Lemma 7.

Let be analytic in neighbourhood of and let be its derivative, then .

Proof.

Since is also analytic in a neighbourhood of (Rudin, 1986, Corollary 10.16), its restriction to is in and is well defined on . Next, since is a unitary operator on , Lemma 2.2.9 of Lindquist & Picci (2015) implies that

where we have used the fact that and the fact that for all . Since restricted to is in , the discussion following Definition 7 implies that is bounded in the operator norm by

This converges to zero as by the uniform continuity of on . ∎

The final lemma consists of technical results, more general versions of which are due to Locker & Prenter (1980) and Callon & Groetsch (1987). Our proofs are specialized and modified so that they follow from first principles.

Lemma 8.

Let , let for all , and suppose the partial indices of are non-negative. Let be a bounded linear operator, let , and let . Then the following holds:

-

(i)

For , the inner product

defines a Hilbert space and we write .

-

(ii)

and have equivalent norms.

-

(iii)

If , then its adjoint is given by

-

(iv)

The Moore-Penrose inverse of in is,

Proof.

(i) Clearly, is an inner product and it remains to show that is complete. Let be an Cauchy sequence. Then both and are Cauchy in and respectively. They must therefore have limits and respectively. Now write

where and , the orthogonal complement to in . Then

We have already established in Lemma 4 that is a bounded linear operator. Since is the orthogonal projection onto in (Groetsch, 1977, p. 47),

It follows, since is a bounded linear operator, that

Therefore,

It has already been established in Lemma 2 that , thus is of finite rank and its image is closed. Thus exists and is a bounded linear operator (Groetsch, 1977, Corollary 2.1.3). Moreover, implies that is injective, thus the image of is . By Theorem 2.1.2 of Groetsch (1977), the image of is the image of . Thus, is the orthogonal projection onto in and so,

Therefore converges in to a point, call it . Finally,

and the boundedness of and imply that converges to in as well.

(ii) Since and are bounded linear operators, there exists an upper bound on their operator norms and

The equivalence of and on then follows from Corollary XII.4.2 of Gohberg et al. (2003).

(iii) For ,

This implies that

Since the last term is equal to and and are arbitrary,

If , then . This implies that is injective. Next, if is orthogonal to the image of , then for all . Since is self-adjoint as an operator on , we have that for all , in particular . Thus, is surjective. It follows that is invertible (Gohberg et al., 2003, p. 283) and the expression for follows.

(iv) By the arguments used in Lemma 4, we have the following representation

The second equality follows from (iii), the third follows from Lemma 4, and the fourth follows from Theorem V.6.1 of Gohberg et al. (1990). Next, notice that the operator

is a self-adjoint projection acting on . By Theorem II.13.1 of Gohberg et al. (2003), it is the orthogonal projection onto its image and it is easily seen that this is the image of . Let

Then is the orthogonal projection onto , the orthogonal complement to the image of in . Since is the image of , is the orthogonal projection onto the image of . We then have that

where we have used basic properties of the Moore-Penrose inverse (Groetsch, 1977, Sections 2.1-2.2) as well as the fact that and map into . It follows that

Lemma 8 (i) introduces a Hilbert space that plays an important role in our regularization theory; and have the same elements but different inner products. Lemma 8 (ii) implies that convergence of points in (operators on) is equivalent to convergence of points in (operators on) . In particular, , whether acting on points or operators, takes the same value in both spaces. On the other hand, adjoints and orthogonal projections are not the same in both spaces due to the different inner products. This is what is proven in Lemma 8 (iii) and (iv).

Proof of Lemma 5.

The proof that solves the regularization problem is due to Callon & Groetsch (1987). We provide an alternative direct derivation. By Lemmas 2 and 4,

By Lemma 2, is of finite dimension, therefore the image of is finite dimensional and closed. Thus exists and is a bounded linear operator (Groetsch, 1977, Corollary 2.1.3). The minimum above is therefore attained for (Groetsch, 1977, p. 41). The uniqueness result then follows from the fact that . ∎

Proof of Theorem 6.

Conditions (i) and (ii) together with Lemma 6 imply that

provided and exist, where . We will prove that both terms on the right hand side converge to zero as . In this proof, all limits, Moore-Penrose inverses, and adjoints are understood to be with respect to . The Hilbert space is only needed in step 2.

STEP 1. .

By the discussion following Definition 1 and condition (iii), the operators and are well defined. By the discussion following Definition 7, the operator norm of is bounded above by . By condition (iv), is jointly continuous and so is continuous at (Sundaram, 1996, Theorem 9.14). It follows that and so converges to in the operator norm as . The same argument applied to proves that converges to in the operator norm as .

Condition (vi) implies that is Fredholm (Gohberg & Fel’dman, 1974, Theorem VIII.4.1) and we have already seen in the proof of Lemma 4 that is onto as well. Thus, any small enough perturbation of in the operator norm will lead to an operator that is also onto (Gohberg et al., 2003, Theorem XV.3.1). Since converges to in the operator norm and , Theorem 1.6 of Koliha (2001) implies that converges in the operator norm to .