Empirical likelihood ratio test on quantiles under a density ratio model

Abstract

Population quantiles are important parameters in many applications. Enthusiasm for the development of effective statistical inference procedures for quantiles and their functions has been high for the past decade. In this article, we study inference methods for quantiles when multiple samples from linked populations are available. The research problems we consider have a wide range of applications. For example, to study the evolution of the economic status of a country, economists monitor changes in the quantiles of annual household incomes, based on multiple survey datasets collected annually. Even with multiple samples, a routine approach would estimate the quantiles of different populations separately. Such approaches ignore the fact that these populations are linked and share some intrinsic latent structure. Recently, many researchers have advocated the use of the density ratio model (DRM) to account for this latent structure and have developed more efficient procedures based on pooled data. The nonparametric empirical likelihood (EL) is subsequently employed. Interestingly, there has been no discussion in this context of the EL-based likelihood ratio test (ELRT) for population quantiles. We explore the use of the ELRT for hypotheses concerning quantiles and confidence regions under the DRM. We show that the ELRT statistic has a chi-square limiting distribution under the null hypothesis. Simulation experiments show that the chi-square distributions approximate the finite-sample distributions well and lead to accurate tests and confidence regions. The DRM helps to improve statistical efficiency. We also give a real-data example to illustrate the efficiency of the proposed method.

keywords:

[class=MSC]keywords:

, and

1 Introduction

Suppose we have independent random samples from population distributions . Let their respective density functions with respect to some -finite measure be . If there exist a vector-valued function and unknown vector-valued parameters of dimension such that

| (1) |

then they define a density ratio model (DRM) as introduced by Anderson [1]. By convention, we call the base distribution and the basis function. There is a symmetry in the DRM: any one of may serve as the base distribution. We require the first element of to be 1 so that the corresponding coefficient is a normalization constant, and the elements of must be linearly independent. The linear independence is a natural requirement: otherwise, some elements of are redundant.

When data are collected from a DRM, the whole data set can be utilized to estimate , which lead to efficiency gain. The nonparametric assumption in the DRM is nonrestrictive. Combined with a moderate-sized , a single DRM contains a broad range of parametric distribution families. Thus, the DRM has a low risk of model misspecification. There is a growing interest in the DRM in statistics [28, 15, 13, 42] as well as in the machine learning community [34]. In this paper, we study the inference problem for population quantiles under the DRM. Population quantiles and their functions are important parameters in many applications. For example, government agents gauge the overall economic status of a country based on annual surveys of household income distribution. The trend in the quantiles of the income distribution is indicative [2, 24]. In forestry, the lower quantiles of the mechanical strength of wood products are vital design values [39]. Other examples include Chen and Hall [7], Yang and He [41], Chen and Liu [8], Chen et al. [11], Koenker et al. [22], Gonçalves, Migon and Bastos [17], Chen and Liu [9].

The data from DRMs are a special type of biased sample [37, 38, 28, 29]. The empirical likelihood (EL) of Owen [26] is an ideal platform for statistical inference under the DRM. The EL retains the effectiveness of likelihood methods and does not impose a restrictive parametric assumption. The ELRT statistic has a neat chi-square limiting distribution, much like the parametric likelihood ratio test given independent and identically distributed (i.i.d.) observations [25, 30]. The EL has already been widely used for data analysis under the DRM [27, 31, 8, 5]. However, there has been limited discussion of the ELRT in the biased sampling context. Both Qin [27] and Cai, Chen and Zidek [5] permit no additional equations. Although the classical Wald method remains effective for both hypothesis tests and confidence regions [28, 8, 11], it must be aided by a consistent and stable variance estimate. In addition, its confidence regions are oval-shaped regardless of the shape of the data cloud. Thus, an ELRT has the potential to push the boundary of the DRM much further.

This paper establishes the limiting chi-square distribution of the ELRT for quantiles under the DRM. We prove that the ELRT statistic has a chi-square limiting distribution under certain conditions. The resulting confidence regions have data-driven shapes, more accurate coverage probabilities, and smaller volumes. In Section 2, we state the problem of interest and the proposed ELRT under the DRM. In Section 3, we study the limiting distribution of the ELRT statistic and some other useful asymptotic results. We illustrate the superiority of the ELRT and the associated confidence regions through simulated data in Section 4 and for real-world data in Section 5. We illustrate the power property of the ELRT in Section 6. Technical details and the proofs of the main theorems are given in Appendices A and B.

2 Research problem and proposed approach

Let be independent i.i.d. samples from a DRM defined by (1). Let be the total sample size. Denote by the quantile of the th population for some and . Let be the quantiles at some levels of populations in an index set of size . We study the ELRT under the DRM for the following hypothesis:

| (2) |

for some given of dimension .

The hypothesis formulated in (2) has many applications. In socio-economic studies, when studying the distributions of household disposable incomes, economists and social scientists often divide the collected survey data into five groups. These groups are famously known as quintile groups. The first group consists of the lowest of the data, the second group consists of the next 20%, and so on. Many studies have shown that the quintiles are important for explaining the economy and consumer behaviour [6, 40, 21, 12]. In statistics, the cut-off points of these quintile groups are the quantiles of the populations: for example, the th percentile separates the first and second quintile groups. Governments may, therefore, consider this th percentile as key for determining which families should receive a special subsidy to help society’s less fortunate. Moreover, when new policies are implemented, the evolution of the quantiles of household income over time may reflect the impact of the policies. As a consequence, these quantiles are of particular interest to social scientists and politicians as a way to measure the effects of policy changes. In statistical inference, these types of tasks can most appropriately be carried out using a hypothesis testing procedure, which can be naturally extended to the construction of confidence regions. Hence, the research problem we study here is of scientific significance in many applications. In the real-data analysis, we study confidence regions for quantiles of household incomes based on US Consumer Expenditure Surveys.

We use an ELRT to test the hypothesis in (2). Let for all applicable . The EL function is the probability of observing the data. Under the DRM, it is given by

| (3) |

For notational convenience, we have dropped the ranges of the indices in the expressions. Observe that the EL in (3) is 0 if is a continuous distribution. Surprisingly, this seemingly devastating property does little harm to the usefulness of the EL. Since the EL in (3) can also be regarded as a function of the parameters and the base distribution , we may write its logarithm as

where we define by convention.

Let be the expectation operation under , and let

be the density of with respect to for . Clearly, . This also implies that

| (4) |

The population quantile of satisfies or is defined to be a solution of

| (5) |

Let

Following Owen [26] and Qin and Lawless [30], we introduce the profile log-EL of the population quantiles :

| (6) |

and

An ELRT statistic for the hypothesis in (2) is defined as

We call the ELRT statistic hereafter. Clearly, the larger the value of , the stronger the evidence for departure from the null hypothesis in the direction of the alternative hypothesis. We reject when exceeds some critical value that is decided based on the distributional information of under . The limiting distribution of and other related properties are given in the next section.

We observe that the approach needs no change for a set of quantiles from the same population. For notational simplicity, the presentation is given for quantiles from different populations.

3 Asymptotic properties of and other quantities

The distributional information of is vital to the implementation of the ELRT in applications. In this section, we show that it is asymptotically chi-square distributed. We also present some secondary but useful asymptotic results.

3.1 A dual function

The profile log-EL function is defined to be the solution of an optimization problem that can be solved by the Lagrange multiplier method. Let and be Lagrange multipliers. Define a Lagrangian as

In Appendix B, we will show that under mild conditions that are easy to verify, there aways exists some such that a solution in to (4) and (5) exists. With this promise, according to the Karush–Kuhn–Tucker theorem [3], the solution to the constrained optimization problem in (2) satisfies

Let be the solution. Some simple algebra gives and

where .

We now introduce another set of notation:

To aid our memory, we note that is a mixture density with mixing proportions ; is a vector of density functions with respect to the mixture combined with the mixing proportions; and is a vector of normalized . With the help of this notation, we define a dual function

| (7) |

The dual function has some easily verified mathematical properties. We can show that

| (8) |

and that is a saddle point of satisfying

| (9) |

In the following section, we study some of the properties of through the dual function .

3.2 Asymptotic properties

We discuss the asymptotic properties under the following nonrestrictive conditions on the sampling plan and the DRM.

Conditions:

-

(i)

The sample proportions have limits in as ;

-

(ii)

The matrix is positive definite;

-

(iii)

For each and in a neighbourhood of the true parameter value , we have

Here are some implications of the above conditions.

-

1.

Under Condition (iii), the moment generating function of with respect to exists in a neighbourhood of . Hence, all finite-order moments of are finite.

-

2.

When is large enough and is in a small neighbourhood of , the derivatives of the dual function are all bounded by some polynomials of . Hence, they are all integrable.

-

3.

Under Condition (ii), the sample version of is also positive definite when is very large.

We now state the main results; the proofs are given in Appendix A.

Lemma 3.1.

The second derivative of the dual function is not negative definite in comparison to a usual likelihood function. This is understandable because is not a model parameter. However, it has full rank and plays an important role in localizing .

The next result implies that the dual function resembles the log-likelihood function under regularity conditions in an important way: its first derivative is an unbiased estimating function.

Lemma 3.2.

Under Conditions (i) to (iii), we have

where the expectation is calculated by regarding as a random variable with distribution .

Furthermore, as , we have

where is a square matrix of dimension .

A key step in the asymptotic study of and the ELRT statistic is localization. That is, is in a small neighbourhood of the true value as the sample size goes to infinity. The following lemma asserts that is almost surely located in the -neighbourhood of .

Lemma 3.3.

Under Conditions (i) to (iii), as , the saddle point of the dual function is in the -neighbourhood of with probability .

In addition, is asymptotically multivariate normal.

The results in the previous lemma shed light on the asymptotic properties of the EL under the DRM. At the same time, they pave the way for the following celebrated conclusion in the EL literature.

Theorem 3.4 enables us to determine an approximate rejection region for the ELRT. We reject the null hypothesis at the significance level when the observed value of is larger than the upper quantile of the chi-square distribution . This also provides a foundation for the construction of confidence regions of . Let

An ELRT-based approximate confidence region for is

| (10) |

where is the quantile of .

4 Simulation studies

In this section, we report some simulation results. We conclude that the chi-square approximation to the sample distribution of is very accurate. The corresponding confidence regions have a data-driven shape and accurate coverage probabilities. In almost all cases considered, the -based confidence regions outperform those based on the Wald method in terms of the average areas and coverage probabilities. The DRM markedly improves the statistical efficiency, and the details are as follows.

4.1 Numerical implementation and methods included

Recall that the ELRT statistic is defined to be

In data analysis, we must solve the optimization problem . As Cai, Chen and Zidek [5] suggest, it can be transformed into an optimization problem of a convex function, and it has a simple solution. We further turn this optimization problem into the problem of solving a system of equations that are formed by equating the derivatives of the induced convex function to . The numerical implementation can be efficiently carried out by a root solver in the R [35] package nleqslv [20] for nonlinear equations. It uses either the Newton or Broyden iterative algorithms.

To compute , we can solve (9), as (8) suggests. This leads to a system of nonlinear equations in , with being the dimension of the vector-valued basis function and the number of population quantiles of interest specified in . In most applications, a with dimension 4 or less is suitable. For a system of this size, the R package nleqslv for roots is very effective even when is as large as . The existence of the solution to (4) and (5) is proved in Appendix B. Guided by this proof, our choice of the initial and guarantees numerical success.

As is typical for DRM examples, we simulate data from the normal and

gamma distributions and examine the ELRT-based hypothesis tests and

confidence regions for the population quantiles.

For comparison, we include Wald-based and nonparametric inference on the same quantiles.

To make the article self-contained, we now briefly review the Wald

and nonparametric methods.

Wald method. The Wald method for confidence region construction of was given in Chen and Liu [8]. Let be the argument maximizer of , and also let

for , where . The maximum EL estimator (MELE) of the quantile of is then given by

Let . We have, as ,

for some matrix that is a function of and . A plug-in estimate of was suggested by Chen and Liu [8], and an R package drmdel [4] by the authors of Cai, Chen and Zidek [5] includes the MELE and in its output. A level approximate confidence region for based on the Wald method is then given by

| (11) |

The Wald method can also be used for hypothesis tests on quantiles. We refer to the confidence region in (11) as the one based on the Wald method.

Nonparametric method. Suppose is the empirical distribution based on a sample from the distribution , and is the sample quantile. The sample quantile is asymptotically normal [32] with asymptotic variance as and . In view of this, the Wald method remains applicable with the help of a nonparametric consistent density estimator. We follow the literature and let

for some kernel function and bandwidth . Under mild conditions on and proper choices of and , is consistent [33]. We set to the density function of the standard normal distribution, and we use a rule-of-thumb bandwidth suggested by Silverman [33]:

where is the standard deviation of and is the interquartile range. With these, we obtain a plug-in estimate

and subsequently a approximate confidence region for :

| (12) |

where . This nonparametric Wald method can also be employed for hypothesis tests on quantiles. We refer to the confidence region in (12) as the one based on the nonparametric method.

When constructing the confidence region in (12), density estimation is required as an intermediate step to obtain a variance estimate . One may also use bootstrap method as an alternative nonparametric method to construct confidence regions for quantiles. We do not think these two nonparametric methods will lead to significantly different results, and hence we use (12) as a nonparametric competitor in this article.

The proposed ELRT method apparently has the highest computational cost, yet it takes a negligible second for each simulation repetition. This renders recording the computational times unnecessary in simulation.

4.2 Data generated from normal distributions

Normality is routinely assumed but unlikely strictly valid in real-world applications. When multiple samples are available, we include all normal distributions without a normality assumption via a DRM coupled with . In this simulation, we generate data from normal distributions with sample sizes . Their means and standard deviations are chosen to be and . In the simulation experiment, we generate 1000 sets of samples of size and compute the values for the hypothesis on the medians of and :

where are the true values. Note that although we simulate data from normal distributions, the parametric information does not play any role in the data analysis.

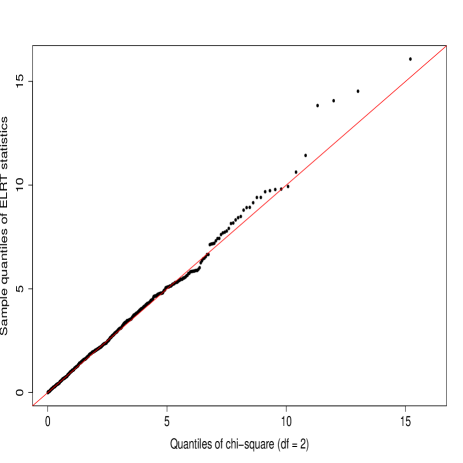

Because is true, has a limiting distribution. Figure 1 gives a quantile-quantile (Q-Q) plot of the 1000 simulated values against the distribution. Over the range from 0 to 6 that matters in most applications, the points are close to the red 45-degree line. Clearly, the chi-square distribution is a good approximation of the sampling distribution of , demonstrating good agreement with Theorem 3.4.

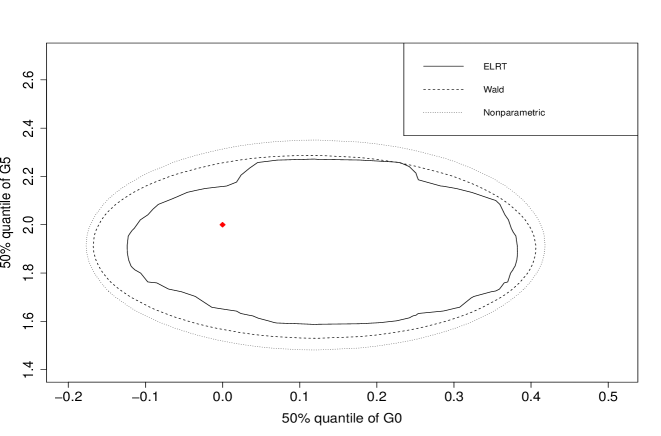

In Figure 2, we depict the confidence regions of based on the ELRT in (10), the Wald method in (11), and the nonparametric method in (12) based on a typical simulated data set with the true marked as a red diamond. The ELRT contour is not smooth because is not smooth at data points. Clearly, the ELRT confidence region has the smallest area and is therefore the most efficient. In Table 1, we make direct quantitative comparisons between the three methods in terms of the coverage probabilities and areas of the and confidence regions. We remark that the ELRT confidence region can be approximated by triangles all pointing to the MELE. We add up the areas of these triangles to get the total area. Both the LRT and Wald methods under the DRM have empirical coverage probabilities close to the nominal levels; the nonparametric method has overcoverage. In general, the ELRT outperforms.

| Method | 90% | 95% | |||

|---|---|---|---|---|---|

| Coverage probability | Area | Coverage probability | Area | ||

| ELRT | |||||

| Wald | |||||

| Nonparametric | |||||

| ELRT | |||||

| Wald | |||||

| Nonparametric | |||||

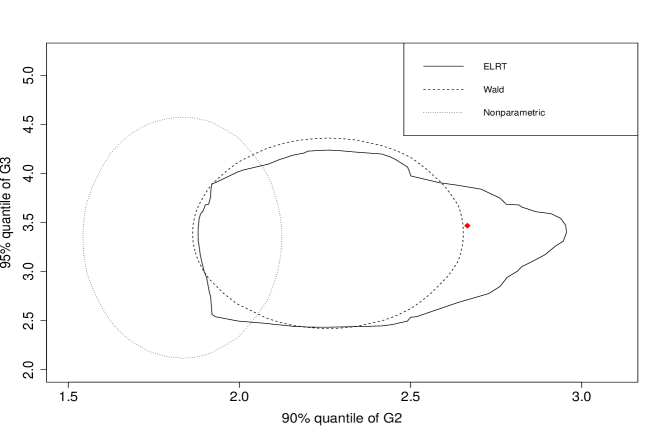

In applications, the sample sizes from different populations are unlikely to be equal. Does the superiority of the ELRT require equal sample sizes from these populations? We also simulated data from the same distributions with unequal sample sizes. We set the sizes of populations to 100 and 200, and the sizes of populations to 50 and 100, respectively. We constructed confidence regions for the th percentile of and the th percentile of , where both populations have the smaller sample sizes. Figure 3 shows the three confidence regions based on a simulated data set; we see that the ELRT is superior. Admittedly, this is one of the more extreme cases. Table 2 gives the average areas and empirical coverage probabilities of the three confidence regions, based on 1000 repetitions. The ELRT confidence regions have the most accurate coverage probabilities, while the other two methods have low coverage. The ELRT confidence regions have larger average areas that are not excessive.

| Method | 90% | 95% | |||

|---|---|---|---|---|---|

| Coverage probability | Area | Coverage probability | Area | ||

| ELRT | |||||

| Wald | |||||

| Nonparametric | |||||

| ELRT | |||||

| Wald | |||||

| Nonparametric | |||||

4.3 Data generated from gamma distributions

In applications, income, lifetime, expenditure, and strength data are positive and skewed. Gamma or Weibull distributions are often used for statistical inference in such applications. In the presence of multiple samples, replacing the parametric model by a DRM with is an attractive option to reduce the risk of model mis-specification. We generate 1000 sets of independent samples of sizes from gamma distributions with shape parameters and scale parameters . We test the hypothesis on the medians of and :

where are the true medians of and , respectively. Note that although we simulate data from gamma distributions, the parametric information does not play any role in the data analysis.

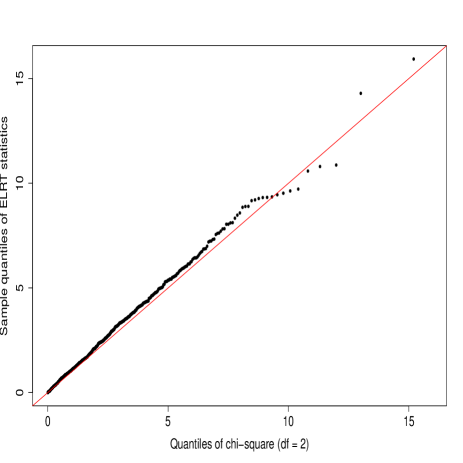

Figure 4 shows the Q-Q plot based on 1000 values against the theoretical limiting distribution . The points in the Q-Q plot are close to (but slightly above) the 45-degree line in the range from 0 to 6. This implies that the corresponding tests will have close to nominal levels. Overall, the chi-square approximation is satisfactory.

In Figure 5, we depict the confidence regions of using the ELRT in (10), the Wald method in (11), and the nonparametric method in (12), based on a typical simulated data set with marked as a red diamond. Clearly, the ELRT-based confidence region has a smaller area and is therefore more efficient. In Table 3 we make direct quantitative comparisons of the coverage probabilities and areas. Both the ELRT and Wald methods under the DRM have empirical coverage probabilities very close to the nominal levels. The nonparametric confidence regions have overcoverage and inflated sizes. We again conclude that the ELRT is superior to the nonparametric method.

| Method | 90% | 95% | |||

|---|---|---|---|---|---|

| Coverage probability | Area | Coverage probability | Area | ||

| ELRT | |||||

| Wald | |||||

| Nonparametric | |||||

| ELRT | |||||

| Wald | |||||

| Nonparametric | |||||

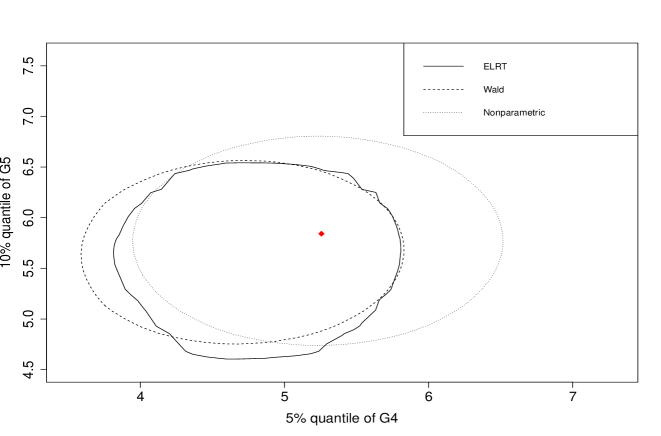

We also study the confidence regions for a pair of lower quantiles: the th percentile of and the th percentile of . Figure 6 shows the three confidence regions based on a simulated data set. Table 4 gives the average areas and coverage probabilities of the three confidence regions, based on 1000 repetitions. The ELRT method is still the most efficient. Maintaining the accurate coverage probabilities, the ELRT confidence regions still have satisfactory areas that are comparable to the Wald confidence regions.

| Method | 90% | 95% | |||

|---|---|---|---|---|---|

| Coverage probability | Area | Coverage probability | Area | ||

| ELRT | |||||

| Wald | |||||

| Nonparametric | |||||

| ELRT | |||||

| Wald | |||||

| Nonparametric | |||||

5 Real-data analysis

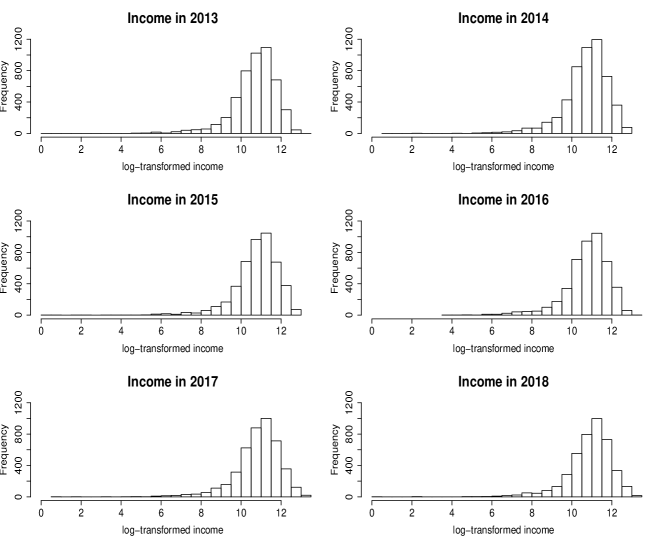

In the previous simulations, we chose the most suitable basis function in each case because the population distributions were known to us. This is not possible in real-world applications. In this section, we create a simulation population based on the US Consumer Expenditure Surveys data concerning US expenditure, income, and demographics. The data set is available on the US Bureau of Labor Statistics website (https://www.bls.gov/cex/pumd.htm). The data are collected by the Census Bureau in the form of panel surveys, in which approximately 5000 households are contacted each quarter. After a household has been surveyed it is dropped from subsequent surveys and replaced by a new household. The response variable is the annual sum of the wages or salary income received by all household members before any deductions. Household income is a good reflection of economic well-being. The data files include some imputed values to replace missing values due to non-response.

We study a six-year period from 2013 to 2018, and we log-transform the response values to make the scale more suitable for numerical computation. Note that the quantiles are transformation equivariant. We exclude households that have no recorded income even after imputation, and there remain 4919, 5304, 4641, 4606, 4475, and 4222 households from 2013 to 2018. The histograms shown in Figure 7 indicate that it is difficult to determine a suitable parametric model for these data sets, but a DRM may work well enough. We take the basis function ; it may not be the best choice, but as a result the simulation results for the DRM analysis are more convincing.

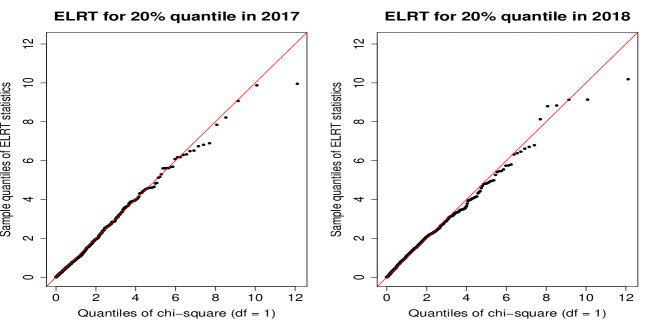

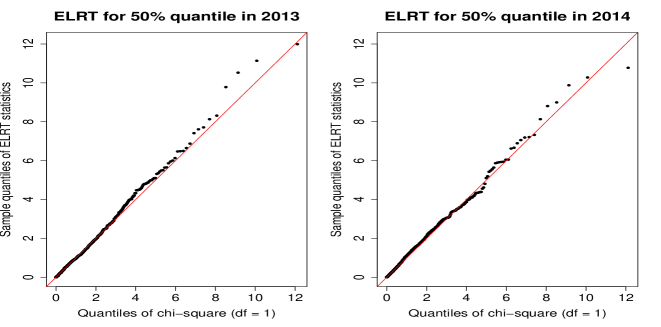

In this simulation, we form 6 populations based on the yearly data sets. We test hypotheses on the th and th percentiles based on independent samples of size 100, which are obtained by sampling with replacement from the respective populations. To test the size of a single quantile of a single population, the limiting distribution of is . Figures 8 and 9 contain a few Q-Q plots of versus for with or . In all the plots, the points of are close to the 45-degree line. Thus, the precision of the chi-square approximation is satisfactory. The plots for other levels or populations are similar and not presented.

The Wald method (11) may be regarded as being derived from an asymptotic distributed statistic:

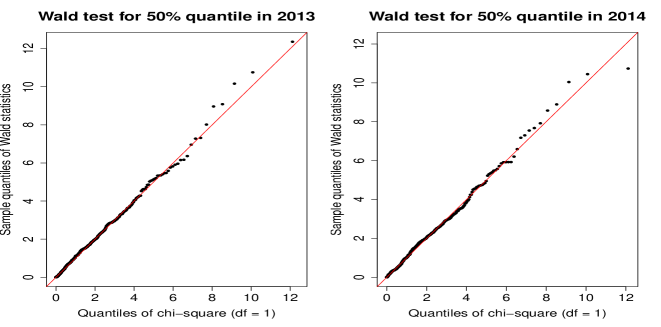

We also obtain values and construct Q-Q plots, and a selected few are given in Figures 10 and 11. These plots show that the chi-square approximation is not as satisfactory. There are many possible explanations, but a major factor could be the unstable variance estimator that the Wald method must rely on, especially for lower quantiles. One of the most valued properties of the likelihood ratio test approach is that there is no need to estimate a scale factor.

A direct consequence of the poor chi-square approximation could be undercoverage of the confidence intervals. Table 5 gives the coverage probabilities and average lengths of the confidence intervals based on three methods: ELRT in (10), Wald in (11), and nonparametric in (12). The improved efficiency of the DRM is best reflected in the average lengths of the confidence intervals. It can be seen that the DRM-based methods achieve on average about and improvement over the nonparametric method for the th and th percentiles respectively. Comparing the ELRT and Wald methods, both done under DRM, we find that the ELRT is comparable to the Wald method for the th percentile and clearly more efficient for the th percentile.

| Year | ELRT | Wald | Nonparametric | ||||

|---|---|---|---|---|---|---|---|

| Average lengths | |||||||

| quantile levels all | |||||||

| 2013 | |||||||

| 2014 | |||||||

| 2015 | |||||||

| 2016 | |||||||

| 2017 | |||||||

| 2018 | |||||||

| average | |||||||

| quantile levels all | |||||||

| 2013 | |||||||

| 2014 | |||||||

| 2015 | |||||||

| 2016 | |||||||

| 2017 | |||||||

| 2018 | |||||||

| average | |||||||

| Empirical coverage probabilities | |||||||

| quantile levels all | |||||||

| 2013 | |||||||

| 2014 | |||||||

| 2015 | |||||||

| 2016 | |||||||

| 2017 | |||||||

| 2018 | |||||||

| average | |||||||

| quantile levels all | |||||||

| 2013 | |||||||

| 2014 | |||||||

| 2015 | |||||||

| 2016 | |||||||

| 2017 | |||||||

| 2018 | |||||||

| average | |||||||

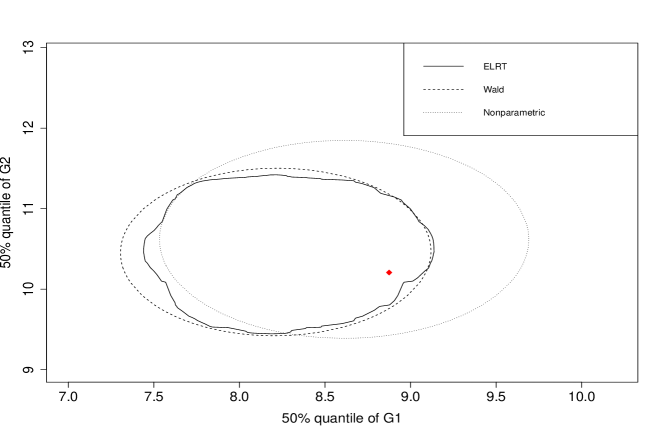

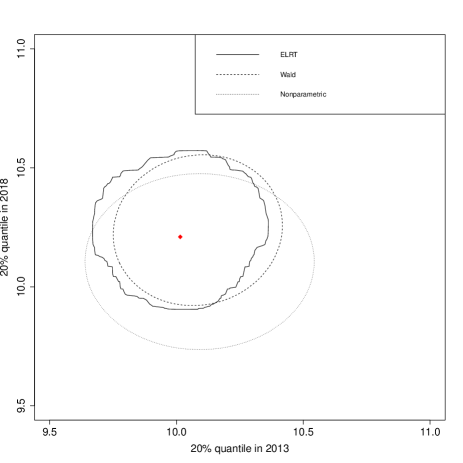

In the next simulation, we focus on the confidence region of the first quantiles of the household incomes in the years 2013 and 2018, namely the th percentiles for these two years. Figure 12 shows the confidence regions using the three methods based on simulated real data of size . Table 6 gives the average coverages and areas of the three confidence regions, based on 1000 repetitions. The ELRT produces the most satisfactory confidence regions. The ELRT confidence regions improve the Wald confidence regions by rightfully increased area to achieve more accurate coverage probabilities. They are much more efficient than the nonparametric confidence regions.

| Method | 90% | 95% | |||

|---|---|---|---|---|---|

| Coverage probability | Area | Coverage probability | Area | ||

| ELRT | |||||

| Wald | |||||

| Nonparametric | |||||

| ELRT | |||||

| Wald | |||||

| Nonparametric | |||||

6 Power property and comparison

Due to the linkage between the confidence region and the hypothesis test, we are certain that the ELRT has superior power property based on the simulation studies already done. At the same time, different tests have different higher power regions in the space of the alternative hypotheses. A generally inferior test can outperform other tests in specific regions. We now use simulation to examine the power properties of the three tests. We find the power properties do not vary much across different data types. To save space, we only present the simulation results based on real data.

Consider the null hypothesis on values of the th percentiles of years 2013 and 2018 with true values being . We examine the power of the three tests against a range of false null hypotheses. One of them, for instance, is

We either inflate to deflate the true value by 1% or 2% leading to 8 false null hypotheses. We report the powers against these false in Table 7 when the nominal levels are 5% and 10% and the sample sizes are and .

We observe that the rejection probabilities of all three tests are above the corresponding nominal levels. They increase when the sample size increases from to . These observations suggest the unbiasedness and consistency of the three tests. We restrain from reading too much into some small differences as the sample size is not sufficiently large. The power of ELRT is around 50% when the assumed quantiles are 2% off from the truth and the sample size is at level 5%.

Direct power comparison is most meaningful when tests under consideration have the same size. Because we use the asymptotic distributions for all three methods, there are non-ignorable differences in their null rejection rates (see Table 6). For each test, level, and sample size combination, we calculate the average rejection rate. The nonparametric test has lower power in general. Yet the nonparametric test has higher rejection rates than ELRT 2 out of 8 times when at 5% level. However, the type I errors are 5.8% and 8.4% for ELRT and nonparametric in this case. If this 44.8% inflation factor in type I error is applied to their powers, then ELRT would have higher powers in all 8 cases. This general comment is applicable to all the other 3 combinations.

The Wald test seems to have higher power than the ELRT on average in all 4 sample size and level combinations. However, its gain in lower type II error is at the cost of higher type I error. When and at level 10%, Table 6 shows the ratio of their type I errors is . Once we adjust the power of ELRT by this factor, the conclusion will be reversed. This is the same for the other sample size and level combinations.

Although the three tests have different high power regions, the ELRT is overall a better one. The similar observations extend to unreported simulation results based on data generated from normal and gamma distributions.

True value of the percentiles: .

| ELRT | Wald | Nonparametric | |||||

| Level of the test | |||||||

| Change in scale | value in | Rejection rates | |||||

| ()% | |||||||

| ()% | |||||||

| ()% | |||||||

| ()% | |||||||

| ()% | |||||||

| ()% | |||||||

| ()% | |||||||

| ()% | |||||||

| average | |||||||

| ()% | |||||||

| ()% | |||||||

| ()% | |||||||

| ()% | |||||||

| ()% | |||||||

| ()% | |||||||

| ()% | |||||||

| ()% | |||||||

| average | |||||||

Appendix A Proofs of the main results

This Appendix provides the proofs of the technical results. In the following proofs, without loss of generality, we proceed as if the sample proportions do not depend on and equal their limits . Our results are applicable as long as none of the populations have comparatively very small sample sizes. Also, for the sake of convenience, with a generic function we use

Moreover, the DRM parameters are arranged in the order

where is the th component of the vector-valued parameter . This order is needed for the expressions of the second derivative of in the proof of Lemma 3.1 and for the covariance matrix of the first derivative in the proof of Lemma 3.2.

A.1 Proof of Lemma 3.1

This lemma asserts that the second derivative matrix of has a finite and full-rank matrix as a limit.

Proof.

We first recognize that can be written as a sum of sets of i.i.d. random variables:

| (13) |

with

Therefore, we may write

By the law of large numbers [14], as ,

for some block matrix given by

Here we remark again that we assume that the sample proportions do not change with and always equal their limits .

Next, we show that has full rank. We first give the following expressions:

where is the Kronecker product, is a vector of length that has 1 in the th entry and 0 elsewhere (we define by convention), and is the population index of the th quantile of interest.

Based on the above expressions, we first note that

which is clearly negative semidefinite. We now strengthen the conclusion to negative definite. By Condition (ii), is positive definite. Since , we have that

is positive definite. Simple algebra leads to the negative definiteness of . For the same reason, is positive definite if does not degenerate, which is assured because

From

we conclude that has full rank if does. Because is positive definite and is negative definite, must be positive definite, and so it has full rank. This completes the proof that has full rank.

∎

A.2 Proof of Lemma 3.2

Proof.

The first conclusion of this lemma is that the first derivative of in (7) has zero expectation when evaluated at . Recall that

For any , the partial derivative of with respect to is given by

At and , this reduces to

Hence, we have

| (14) |

For each , and at and , we have

For the first term, it can be seen that

At the same time, for the second term, we have

Therefore, we find that

| (15) |

The second conclusion of this lemma is the asymptotic normality of the first derivative. Despite its complex expression, we can see that is a sum of sets of i.i.d. random variables of sizes with mean zero and finite second moment in the matrix sense. Recall (13) from the proof of Lemma 3.1 that

where

We may write

For each , as ,

has a limiting distribution of normal with mean zero and finite second moment in the matrix sense, by the multivariate central limit theorem for triangular arrays [14]. Because are independent of each other, the targeted quantity

is asymptotically normal with mean zero.

We now give the expression for the covariance matrix in the limiting distribution. Let be the asymptotic covariance matrix of , then we have

The expression for is given by

After some algebra, we find that

where is a unit vector with the th element being 1 ( by convention). We have

Let

where is an -dimensional vector of ones; we then also have

Finally, we get

This completes the proof that is asymptotically normal.

∎

A.3 Proof of Lemma 3.3

Proof.

Given , let be the solution to

We first prove that uniformly for any in the -neighbourhood of , is . For notational convenience, in this section we omit in if this does not cause any confusion.

Following the typical proof in Owen [26], the claim is true if uniformly for such that we have

-

(i)

;

-

(ii)

has a positive definite limit.

We omit other details but prove the above results. Note that little and big without in the subscript are orders in the sense of almost surely.

Recall that as shown in Lemma 3.2. We have

| (16) |

applying the law of the iterated logarithm to each .

For in a small neighbourhood of , there is a generic nonrandom constant such that

| (17) |

with the order in the last step derived from the finite moment assumption on . Applying (A.3) and (17), with being a value between and , we get

This proves (i).

Recall that and observe

By focusing on in an -neighbourhood of , we have

As we have remarked, the validity of (i) and (ii) implies that uniformly for ,

| (18) |

Following the same line of the proof, we also have a stronger order for when :

| (19) |

The next stage of the proof is dedicated to showing that . We consider a function of :

It can easily be seen that is a maximizer of . Since is a smooth function, there must be a maximizer of in the compact set . We prove that this maximizer is attained in the interior of the compact set by showing that uniformly for on the boundary of the compact set. For any unit vector and , expanding at yields (see Folland [16])

| (20) |

where is the Lagrange remainder term in obvious notation:

for some between and . By the uniform boundedness of the third-order derivatives of , we have uniformly over .

For the first term in the expansion, we note that as given in (19), and this implies

with the order of implied by Lemma 3.2. Therefore,

For the second term in the expansion, we proceed as follows. With as given in (19) and Lemma 3.1, we first note that

Taking derivatives with respect to on both sides of the identity

and then setting , we further have

Hence,

Therefore, the expansion of in (20) becomes

The matrix in the quadratic form is negative definite, following the line of an argument in the proof of Lemma 3.1. Hence, as , with probability 1,

uniformly over all unit vector . This proves

and together with (18) further implies that

We are now ready to prove the asymptotic normality of . Expanding at , we get

∎

A.4 Proof of Theorem 3.4

Proof.

We notice that, as shown in Cai, Chen and Zidek [5],

From (8) we also have

These relations lead to

| (22) |

Cai, Chen and Zidek [5] show in the proof of their Theorem 1 that

for the same given in the proof of Lemma 3.1.

Let

with and the identity matrix with proper sizes. We then get

where the middle step can be obtained via some typical matrix algebra or Theorem 8.5.11 in Harville [19].

As given in the proof of Lemma 3.2, the asymptotic variance of is . We also have

Hence,

By the result on quadratic forms of the multivariate normal (section 3.5, Serfling [32]), the limiting distribution of is chi-square with the degrees of freedom being the trace of , which is as claimed in this theorem. This completes the proof.

∎

Appendix B Definability of the profile log-EL

Discussions of the properties of the ELRT statistic are not meaningful if the profile log-EL is not well defined. In fact, in some situations, the constrained maximization has no solution [18]. Such an “empty-set” problem can be an issue, but there are methods in the literature to overcome this obstacle [10, 23, 36]. In this Appendix, we show that our does not suffer from the “empty-set” problem under two additional mild conditions. The first condition restricts our attention to quantile values in the range

The second requires one of the components of to be monotone in , in addition to a component being . All of our examples satisfy these conditions.

To define the profile log-EL , we must have some such that

We work on the most general case where contains all populations, and without loss of generality let . The above expressions are equivalent to (including and allowing )

Let and where and is monotone in . We can rewrite the equations as

with . For notational simplicity, we retain the notation instead of in what follows.

Let be any set of non-negative values such that . Define

Since is a monotone increasing function in , is decreasing in and is increasing in . Thus, we have

These imply that the ratio is decreasing in and that

By the intermediate value theorem, there must exist a value such that

Let . We note that and form a solution to the system. Hence, a solution to the system always exists.

We may shift the solution to set if required. Validity in the general case of is implied by setting the other entries of to the value . Therefore, we have shown that our profile log-EL does not suffer from the “empty-set” problem under mild conditions.

Acknowledgments

The authors are grateful to the referees and the Editor for their helpful comments and suggestions.

References

- Anderson [1979] {barticle}[author] \bauthor\bsnmAnderson, \bfnmJA\binitsJ. (\byear1979). \btitleMultivariate logistic compounds. \bjournalBiometrika \bvolume66 \bpages17–26. \endbibitem

- Berger and Skinner [2003] {barticle}[author] \bauthor\bsnmBerger, \bfnmYves G\binitsY. G. and \bauthor\bsnmSkinner, \bfnmChris J\binitsC. J. (\byear2003). \btitleVariance estimation for a low income proportion. \bjournalJournal of the Royal Statistical Society: Series C (Applied Statistics) \bvolume52 \bpages457–468. \endbibitem

- Boyd and Vandenberghe [2004] {bbook}[author] \bauthor\bsnmBoyd, \bfnmStephen\binitsS. and \bauthor\bsnmVandenberghe, \bfnmLieven\binitsL. (\byear2004). \btitleConvex Optimization. \bpublisherCambridge University Press. \endbibitem

- Cai [2015] {bmanual}[author] \bauthor\bsnmCai, \bfnmSong\binitsS. (\byear2015). \btitledrmdel: Dual Empirical Likelihood Inference under Density Ratio Models in the Presence of Multiple Samples \bnoteR package version 1.3.1. \endbibitem

- Cai, Chen and Zidek [2017] {barticle}[author] \bauthor\bsnmCai, \bfnmSong\binitsS., \bauthor\bsnmChen, \bfnmJiahua\binitsJ. and \bauthor\bsnmZidek, \bfnmJames V\binitsJ. V. (\byear2017). \btitleHypothesis testing in the presence of multiple samples under density ratio models. \bjournalStatistica Sinica \bvolume27 \bpages761–783. \endbibitem

- Castelló and Doménech [2002] {barticle}[author] \bauthor\bsnmCastelló, \bfnmAmparo\binitsA. and \bauthor\bsnmDoménech, \bfnmRafael\binitsR. (\byear2002). \btitleHuman capital inequality and economic growth: Some new evidence. \bjournalThe Economic Journal \bvolume112 \bpagesC187–C200. \endbibitem

- Chen and Hall [1993] {barticle}[author] \bauthor\bsnmChen, \bfnmSong Xi\binitsS. X. and \bauthor\bsnmHall, \bfnmPeter\binitsP. (\byear1993). \btitleSmoothed empirical likelihood confidence intervals for quantiles. \bjournalThe Annals of Statistics \bvolume21 \bpages1166–1181. \endbibitem

- Chen and Liu [2013] {barticle}[author] \bauthor\bsnmChen, \bfnmJiahua\binitsJ. and \bauthor\bsnmLiu, \bfnmYukun\binitsY. (\byear2013). \btitleQuantile and quantile-function estimations under density ratio model. \bjournalThe Annals of Statistics \bvolume41 \bpages1669–1692. \endbibitem

- Chen and Liu [2019] {barticle}[author] \bauthor\bsnmChen, \bfnmJiahua\binitsJ. and \bauthor\bsnmLiu, \bfnmYukun\binitsY. (\byear2019). \btitleSmall area quantile estimation. \bjournalInternational Statistical Review \bvolume87 \bpagesS219–S238. \endbibitem

- Chen, Variyath and Abraham [2008] {barticle}[author] \bauthor\bsnmChen, \bfnmJiahua\binitsJ., \bauthor\bsnmVariyath, \bfnmAsokan Mulayath\binitsA. M. and \bauthor\bsnmAbraham, \bfnmBovas\binitsB. (\byear2008). \btitleAdjusted empirical likelihood and its properties. \bjournalJournal of Computational and Graphical Statistics \bvolume17 \bpages426–443. \endbibitem

- Chen et al. [2016] {barticle}[author] \bauthor\bsnmChen, \bfnmJiahua\binitsJ., \bauthor\bsnmLi, \bfnmPengfei\binitsP., \bauthor\bsnmLiu, \bfnmYukun\binitsY. and \bauthor\bsnmZidek, \bfnmJames V\binitsJ. V. (\byear2016). \btitleMonitoring test under nonparametric random effects model. \bjournalarXiv preprint arXiv:1610.05809. \endbibitem

- Corak [2019] {barticle}[author] \bauthor\bsnmCorak, \bfnmMiles\binitsM. (\byear2019). \btitleThe Canadian geography of intergenerational income mobility. \bjournalThe Economic Journal. \endbibitem

- De Oliveira and Kedem [2017] {barticle}[author] \bauthor\bsnmDe Oliveira, \bfnmVictor\binitsV. and \bauthor\bsnmKedem, \bfnmBenjamin\binitsB. (\byear2017). \btitleBayesian analysis of a density ratio model. \bjournalCanadian Journal of Statistics \bvolume45 \bpages274–289. \endbibitem

- Durrett [2010] {bbook}[author] \bauthor\bsnmDurrett, \bfnmRick\binitsR. (\byear2010). \btitleProbability: Theory and Examples. \bpublisherCambridge University Press. \endbibitem

- Fokianos et al. [2001] {barticle}[author] \bauthor\bsnmFokianos, \bfnmKonstantinos\binitsK., \bauthor\bsnmKedem, \bfnmBenjamin\binitsB., \bauthor\bsnmQin, \bfnmJing\binitsJ. and \bauthor\bsnmShort, \bfnmDavid A\binitsD. A. (\byear2001). \btitleA semiparametric approach to the one-way layout. \bjournalTechnometrics \bvolume43 \bpages56–65. \endbibitem

- Folland [2002] {bbook}[author] \bauthor\bsnmFolland, \bfnmG. B.\binitsG. B. (\byear2002). \btitleAdvanced Calculus. \bseriesFeatured Titles for Advanced Calculus Series. \bpublisherPrentice Hall. \endbibitem

- Gonçalves, Migon and Bastos [2020] {barticle}[author] \bauthor\bsnmGonçalves, \bfnmKelly CM\binitsK. C., \bauthor\bsnmMigon, \bfnmHelio S\binitsH. S. and \bauthor\bsnmBastos, \bfnmLeonardo S\binitsL. S. (\byear2020). \btitleDynamic quantile linear models: A Bayesian approach. \bjournalBayesian Analysis \bvolume15 \bpages335-262. \endbibitem

- Grendár and Judge [2009] {barticle}[author] \bauthor\bsnmGrendár, \bfnmMarian\binitsM. and \bauthor\bsnmJudge, \bfnmGeorge\binitsG. (\byear2009). \btitleEmpty set problem of maximum empirical likelihood methods. \bjournalElectronic Journal of Statistics \bvolume3 \bpages1542–1555. \endbibitem

- Harville [1997] {bbook}[author] \bauthor\bsnmHarville, \bfnmDavid A\binitsD. A. (\byear1997). \btitleMatrix Algebra from a Statistician’s Perspective \bvolume1. \bpublisherSpringer. \endbibitem

- Hasselman [2018] {bmanual}[author] \bauthor\bsnmHasselman, \bfnmBerend\binitsB. (\byear2018). \btitlenleqslv: Solve Systems of Nonlinear Equations \bnoteR package version 3.3.2. \endbibitem

- Humphries et al. [2014] {barticle}[author] \bauthor\bsnmHumphries, \bfnmDebbie L\binitsD. L., \bauthor\bsnmBehrman, \bfnmJere R\binitsJ. R., \bauthor\bsnmCrookston, \bfnmBenjamin T\binitsB. T., \bauthor\bsnmDearden, \bfnmKirk A\binitsK. A., \bauthor\bsnmSchott, \bfnmWhitney\binitsW. and \bauthor\bsnmPenny, \bfnmMary E\binitsM. E. (\byear2014). \btitleHouseholds across all income quintiles, especially the poorest, increased animal source food expenditures substantially during recent Peruvian economic growth. \bjournalPloS one \bvolume9 \bpagese110961. \endbibitem

- Koenker et al. [2017] {bbook}[author] \bauthor\bsnmKoenker, \bfnmRoger\binitsR., \bauthor\bsnmChernozhukov, \bfnmVictor\binitsV., \bauthor\bsnmHe, \bfnmXuming\binitsX. and \bauthor\bsnmPeng, \bfnmLimin\binitsL. (\byear2017). \btitleHandbook of Quantile Regression. \bpublisherCRC Press. \endbibitem

- Liu and Chen [2010] {barticle}[author] \bauthor\bsnmLiu, \bfnmYukun\binitsY. and \bauthor\bsnmChen, \bfnmJiahua\binitsJ. (\byear2010). \btitleAdjusted empirical likelihood with high-order precision. \bjournalThe Annals of Statistics \bvolume38 \bpages1341–1362. \endbibitem

- Muller [2008] {barticle}[author] \bauthor\bsnmMuller, \bfnmChristophe\binitsC. (\byear2008). \btitleThe measurement of poverty with geographical and intertemporal price dispersion: Evidence from Rwanda. \bjournalReview of Income and Wealth \bvolume54 \bpages27–49. \endbibitem

- Owen [1988] {barticle}[author] \bauthor\bsnmOwen, \bfnmArt B\binitsA. B. (\byear1988). \btitleEmpirical likelihood ratio confidence intervals for a single functional. \bjournalBiometrika \bvolume75 \bpages237–249. \endbibitem

- Owen [2001] {bbook}[author] \bauthor\bsnmOwen, \bfnmA. B.\binitsA. B. (\byear2001). \btitleEmpirical Likelihood. \bpublisherChapman & Hall/CRC, New York. \endbibitem

- Qin [1993] {barticle}[author] \bauthor\bsnmQin, \bfnmJing\binitsJ. (\byear1993). \btitleEmpirical likelihood in biased sample problems. \bjournalThe Annals of Statistics \bvolume21 \bpages1182–1196. \endbibitem

- Qin [1998] {barticle}[author] \bauthor\bsnmQin, \bfnmJing\binitsJ. (\byear1998). \btitleInferences for case-control and semiparametric two-sample density ratio models. \bjournalBiometrika \bvolume85 \bpages619–630. \endbibitem

- Qin [2017] {bbook}[author] \bauthor\bsnmQin, \bfnmJing\binitsJ. (\byear2017). \btitleBiased Sampling, Over-identified Parameter Problems and Beyond. \bpublisherSpringer. \endbibitem

- Qin and Lawless [1994] {barticle}[author] \bauthor\bsnmQin, \bfnmJin\binitsJ. and \bauthor\bsnmLawless, \bfnmJerry\binitsJ. (\byear1994). \btitleEmpirical likelihood and general estimating equations. \bjournalThe Annals of Statistics \bvolume22 \bpages300–325. \endbibitem

- Qin and Zhang [1997] {barticle}[author] \bauthor\bsnmQin, \bfnmJing\binitsJ. and \bauthor\bsnmZhang, \bfnmBiao\binitsB. (\byear1997). \btitleA goodness-of-fit test for logistic regression models based on case-control data. \bjournalBiometrika \bvolume84 \bpages609–618. \endbibitem

- Serfling [1980] {bbook}[author] \bauthor\bsnmSerfling, \bfnmRobert J\binitsR. J. (\byear1980). \btitleApproximation Theorems of Mathematical Statistics. \bpublisherWiley, New York. \endbibitem

- Silverman [1986] {bbook}[author] \bauthor\bsnmSilverman, \bfnmBernard W\binitsB. W. (\byear1986). \btitleDensity Estimation for Statistics and Data Analysis \bvolume26. \bpublisherCRC Press. \endbibitem

- Sugiyama, Suzuki and Kanamori [2012] {bbook}[author] \bauthor\bsnmSugiyama, \bfnmMasashi\binitsM., \bauthor\bsnmSuzuki, \bfnmTaiji\binitsT. and \bauthor\bsnmKanamori, \bfnmTakafumi\binitsT. (\byear2012). \btitleDensity Ratio Estimation in Machine Learning. \bpublisherCambridge University Press. \endbibitem

- R Core Team [2018] {bmanual}[author] \bauthor\bsnmR Core Team (\byear2018). \btitleR: A Language and Environment for Statistical Computing \bpublisherR Foundation for Statistical Computing, \baddressVienna, Austria. \endbibitem

- Tsao and Wu [2014] {barticle}[author] \bauthor\bsnmTsao, \bfnmMin\binitsM. and \bauthor\bsnmWu, \bfnmFan\binitsF. (\byear2014). \btitleExtended empirical likelihood for estimating equations. \bjournalBiometrika \bvolume101 \bpages703–710. \endbibitem

- Vardi [1982] {barticle}[author] \bauthor\bsnmVardi, \bfnmYehuda\binitsY. (\byear1982). \btitleNonparametric estimation in the presence of length bias. \bjournalThe Annals of Statistics \bvolume10 \bpages616–620. \endbibitem

- Vardi [1985] {barticle}[author] \bauthor\bsnmVardi, \bfnmYehuda\binitsY. (\byear1985). \btitleEmpirical distributions in selection bias models. \bjournalThe Annals of Statistics \bvolume13 \bpages178–203. \endbibitem

- Verrill, Kretschmann and Evans [2015] {bunpublished}[author] \bauthor\bsnmVerrill, \bfnmS.\binitsS., \bauthor\bsnmKretschmann, \bfnmD. E.\binitsD. E. and \bauthor\bsnmEvans, \bfnmJ. W.\binitsJ. W. (\byear2015). \btitleSimulations of strength property monitoring tests. \bnoteUnpublished manuscript. Forest Products Laboratory, Madison, Wisconsin. Available at http://www1.fpl.fs.fed.us/monit.pdf. \endbibitem

- Wunder [2012] {barticle}[author] \bauthor\bsnmWunder, \bfnmTimothy A\binitsT. A. (\byear2012). \btitleIncome distribution and consumption driven growth: How consumption behaviors of the top two income quintiles help to explain the economy. \bjournalJournal of Economic Issues \bvolume46 \bpages173–192. \endbibitem

- Yang and He [2012] {barticle}[author] \bauthor\bsnmYang, \bfnmYunwen\binitsY. and \bauthor\bsnmHe, \bfnmXuming\binitsX. (\byear2012). \btitleBayesian empirical likelihood for quantile regression. \bjournalThe Annals of Statistics \bvolume40 \bpages1102–1131. \endbibitem

- Zhuang, Hu and Chen [2019] {barticle}[author] \bauthor\bsnmZhuang, \bfnmWW\binitsW., \bauthor\bsnmHu, \bfnmBY\binitsB. and \bauthor\bsnmChen, \bfnmJ\binitsJ. (\byear2019). \btitleSemiparametric inference for the dominance index under the density ratio model. \bjournalBiometrika \bvolume106 \bpages229–241. \endbibitem