Prediction under latent factor regression: adaptive PCR, interpolating predictors and beyond

Abstract

This work is devoted to the finite sample prediction risk analysis of a class of linear predictors of a response from a high-dimensional random vector when follows a latent factor regression model generated by a unobservable latent vector of dimension less than . Our primary contribution is in establishing finite sample risk bounds for prediction with the ubiquitous Principal Component Regression (PCR) method, under the factor regression model, with the number of principal components adaptively selected from the data – a form of theoretical guarantee that is surprisingly lacking from the PCR literature. To accomplish this, we prove a master theorem that establishes a risk bound for a large class of predictors, including the PCR predictor as a special case. This approach has the benefit of providing a unified framework for the analysis of a wide range of linear prediction methods, under the factor regression setting. In particular, we use our main theorem to recover known risk bounds for the minimum-norm interpolating predictor, which has received renewed attention in the past two years, and a prediction method tailored to a subclass of factor regression models with identifiable parameters. This model-tailored method can be interpreted as prediction via clusters with latent centers.

To address the problem of selecting among a set of candidate predictors, we analyze a simple model selection procedure based on data-splitting, providing an oracle inequality under the factor model to prove that the performance of the selected predictor is close to the optimal candidate. We conclude with a detailed simulation study to support and complement our theoretical results.

Keywords: High-dimensional regression, latent factor model, identifiability, principal component regression, interpolating predictor, prediction with latent-state clusters, model selection

1 Introduction

This work is devoted to the derivation and analysis of finite sample prediction risk bounds for a class of linear predictors of a random response from a high-dimensional, and possibly highly correlated random vector , when the vector follows a latent factor regression model, generated by a latent vector of dimension lower than . We assume that there exist a random, unobservable, latent vector , a deterministic matrix , and a coefficient vector such that

| (1) | ||||

with some unknown . The random noise and have mean zero and second moments and , respectively. The random variable and random vectors and are mutually independent. Throughout the paper, both and have rank equal to .

Independently of this model formulation, but based on the belief that depends chiefly on a lower-dimensional approximation of , prediction of via principal components (PCR) is perhaps the most utilized scheme, with a history dating back many decades (Kendall, 1957; Hotelling, 1957). Given the data and consisting of independent copies of , PCR- predicts after observing a new data point by

| (2) | |||||

where is the matrix of the top eigenvectors of the sample covariance matrix , relative to the largest eigenvalues, where is ideally determined in a data-dependent fashion and denotes the Moore-Penrose inverse of a matrix .

Model (1) provides a natural context for the theoretical analysis of PCR- prediction. It is perhaps surprising that its theoretical study so far is limited to asymptotic analyses of the out-of-sample prediction risk for PCR- as (Stock and Watson, 2002; Bai and Ng, 2006), and finite sample / asymptotic risk bounds on the in-sample prediction accuracy of PCR- (Bai, 2003; Bair et al., 2006; Fan et al., 2013; Kelly and Pruitt, 2015; Fan et al., 2017) in identifiable factor models with known and fixed .

To the best of our knowledge, finite sample prediction risk bounds for , corresponding to data-dependent choices of , are lacking in the literature, and their study under factor models of unknown , possibly varying with , provides motivation for this work.

To obtain risk bounds for PCR, we prove a master theorem, Theorem 2, that establishes a finite sample prediction risk bound for linear predictors of the general form

| (3) |

where is an appropriate matrix that may be deterministic or depend on the data , with dimension allowed to be random.

This approach has the benefit of not only covering the special case of PCR, corresponding to choice , but of offering a unifying analysis of other prediction schemes of the form (3). One important example corresponds to , which leads to another model agnostic predictor, the generalized least squares estimator (also known as the minimum norm interpolating predictor), which has enjoyed revamped popularity in the last two years (Montanari et al., 2019; Bunea et al., 2020; Muthukumar et al., 2019, 2020; Hastie et al., 2019; Feldman, 2019; Belkin et al., 2019a, b, 2018a, 2018b, 2018c; Bartlett et al., 2019; Liang and Rakhlin, 2018). Using the full data matrix for prediction – instead of just the first principal components as in PCR – leads to additional bias compared to PCR prediction. However, in the high-dimensional regime , this bias can become small and choosing can become a viable alternative to PCR that requires no tuning parameters.

In addition to these two model-agnostic prediction methods, Theorem 2 can be used to analyze predictors directly tailored to model (1), which are shown formally to be of type (3) in Section 4.2. We give a particular expression of , as well as the corresponding prediction analysis, under further modelling restrictions that render parameters , and identifiable. The model specifications given in Section 4.2 allow us to view as a cluster membership matrix, making it possible to address a third, understudied, class of examples pertaining to prediction from low-dimensional feature representation, that of prediction of via latent cluster centers, for features that exhibit an overlapping clustering structure corresponding to .

1.1 Our contributions and organization of the paper

Our main theoretical goal is to offer sufficient conditions on under which the prediction risk , defined as

| (4) |

provably approaches an optimal risk benchmark, as and grow, with particular attention given to the case . The expectation in (4) is taken with respect to the new data point .

Our main applications will be to the finite sample risk bounds of the three classes of predictors discussed in the previous section.

1. General finite sample risk bounds for linear predictors, under factor regression models. To meet our main theoretical goal, in Section 2, we state the risk benchmark in Lemma 1 and prove a master theorem, and our main theoretical result, Theorem 2. It provides a finite sample bound on , for generic , when follow a factor regression model (1) that is fully introduced in Section 2.1.

The risk bound (14) of Theorem 2 depends on random quantities , , and , where we use to denote the th largest singular value for any matrix . To interpret these, note that (see Lemma 11 in Appendix A for the proof), where is the projection onto the range of . We then see that is the rank of the projected data matrix used for constructing , captures the size of the signal that is retained in after projection onto the range of , and captures the bias introduced by using only the component of in the range of for prediction.

The utility of Theorem 2, as a general result, is in reducing the difficult task of bounding to the relatively easier one of controlling , , and corresponding to any matrix of interest.

2. Finite sample risk bounds for PCR-, with data-adaptive principal components. We use Theorem 2 to analyze the prediction risk of PCR- under the factor regression model, for two choices of the number of principal components . We first consider the theoretical elbow method, which selects corresponding to the smallest eigenvalue of above the noise level of order , for an absolute constant . Corollary 4 provides the rate

| (5) |

The first term on the right hand side is the standard variance term of linear regression in dimensions. The second term is a bias term that arises from the fact that we predict using instead of ; we show that such a term is unavoidable in Lemma 1 of Section 2.2 below.

We termed this procedure theoretical as depends on unknown quantities of the data distribution. We address this by introducing a novel method in Section 3.1, which we show in Corollary 6 achieves the same rate as PCR with the theoretical elbow method, under mild additional assumptions, and is fully data-adaptive, only requiring the choice of one scale-free tuning parameter.

3. Minimum-norm interpolating predictors. In Section 4.1 we use the master theorem to recover risk bounds for the Generalized Least Squares predictor (GLS), independently derived in Bunea et al. (2020). This predictor is also known as the minimum-norm interpolating predictor when .

4. Prediction under identifiable factor regression models: Essential regression. In Section 4.2 we consider a particular identifiable factor regression model, the Essential Regression model introduced in Bing et al. (2019). The identifiability assumptions employ a type of errors-in-variables parametrization of , described in Section 4.2, that allows the components of to be respectively matched with distinct groups of components of . The latter property, combined with a further sparsity assumption on , can be used to define overlapping clusters of with latent centers , (Bing et al., 2020). Thus, of independent interest, prediction in Essential Regression is prediction via latent cluster centers. We show formally in Section 4.2 that this model specification leads to predictors of type (3), with , for an appropriate estimator of . We provide a finite sample prediction bound in Theorem 9, as an application of Theorem 2. We use the derived bound as an example that illustrates the possible benefits of sparsity in the predictor’s coefficient matrix, as our matrix is allowed to be sparse.

5. Data-splitting under factor regression models.

To allow for model selection among the diverse set of prediction methods in this setting, we offer a simple model selection approach in Section 5 based on data splitting. We provide an oracle inequality showing that the selected predictor performs nearly as well as the predictor with the lowest risk.

A preview of the results in Sections 3 – 4 is given in Table 1 below, which focuses on the high-dimensional regime where for a large enough constant , and is stated under the simplifying assumptions and , where is the reduced effective rank of , the covariance matrix of from model (1). The bound for Essential Regression contains the quantity , which is the sparsity level of the sub-matrix of corresponding to non-pure variables in the Essential Regression model, namely the variables associated with more than one latent factor (see Section 4.2 for a formal definition). The full set of conditions under which these bounds hold, as well as their general form is given, respectively, in each of the sections in which these methods are analyzed. For now we mention that we do not make specific distributional assumption on the data, but we do derive the rates given in the table below under the assumption that , , and are sub-Gaussian.

The term is common to all three risk bounds, and shows that all methods have the potential to adapt to the unknown, latent, -dimensional model structure, provided that the remaining terms are small. Relative to PCR and ER, the GLS method has an additional variance term , that arises from the fact that GLS uses the full data matrix , as opposed to a lower-dimensional projection of it; this demonstrates that GLS has competitive performance only when . The relative performance of the PCR and ER methods depends on the sparsity of the matrix : when , for example, the ER method can outperform PCR.

We further discuss the relative merits of these predictors, in terms of their respective risk bounds and assumptions under which they hold, in Section 4.3.

| Prediction Method | Excess risk bound | |

| PCR | ||

| GLS | ||

| ER |

We conclude the paper with Section 6, in which we present a detailed simulation study of the PCR-type predictors, the minimum-norm interpolating predictor, and predictors under Essential Regression, as well as the proposed model selection method. All proofs are deferred to the Appendix.

Notation

We use the following notation throughout the paper. For any vector , we use denote its norm for . We write . For an arbitrary real-valued matrix , we use to denote the Moore-Penrose inverse of , and to denote the singular values of in non-increasing order. We define the operator norm , the Frobenius norm , the elementwise sup-norm and the cardinality of non-zero entries . For a symmetric positive semi-definite matrix , we use to denote the eigenvalues of in non-increasing order, and to denote its condition number.

For any two sequences and , we write if there exists some constant such that . The notation stands for and .

We use to denote the identity matrix. For , we let . Lastly, we use to denote positive and finite absolute constants that unless otherwise indicated can change from line to line.

2 Bounding the risk

In this section we derive and discuss bounds on the risk defined in (4), corresponding to the predictor . Our results are valid for any that can be either random depending on or fixed, where but is allowed to be random.

2.1 Preliminaries

As the risk is defined relative to the first two moments of , which are further linked to quantities under model (1), our risk bounds are written in terms of the components of . We thus start by formally defining model (1) with respect to .

Definition 1 ((Sub-Gaussian) Factor Regression Model).

We say the pair follows the model FRM with , and write or , when

-

(1)

Equation (1) holds with matrix , vector , and random quantities that are mutually independent;

-

(2)

and are mean zero with and , and is also mean zero without loss of generality, with .

-

(3)

Both and have rank equal to .

We further say if the following holds in addition to (1) – (3)

-

(4)

There exist finite, absolute positive constants and such that

-

(a)

is sub-Gaussian111A mean zero random variable is called sub-Gaussian if for all .;

-

(b)

where is sub-Gaussian222A mean zero random vector is called sub-Gaussian if is sub-Gaussian for any unit vector . with ;

-

(c)

where is sub-Gaussian with .

-

(a)

Since there exist multiple parameters for which has the same joint distribution, the model is not identifiable without further restrictions on the parameter space. As this work is devoted to the prediction of , and not to the estimation of , this is not problematic. We thus allow for this lack of identifiability and our subsequent analysis of is valid for any such that sG-FRM(). In particular, the analysis is applicable to any identifiable sG-FRM, whenever further structure on is added to Definition 1. We note that depends on , but we suppress this dependence in the notation for simplicity.

2.2 Benchmark of

To provide a benchmark for , we let

| (6) |

denote the coefficient of the best linear predictor (BLP) of from , where is the Moore-Penrose pseudoinverse of . For any such that with corresponding latent vector , we have the following chain of simple equalities from our independence assumptions

We interpret the term as an oracle risk value because it is the minimal risk of predicting from , had been observable. We thus focus on bounding the difference and refer to it as excess risk, with the tacit understanding that the excess is relative to oracle prediction.

We further note that the term in (2.2) is the minimal risk incurred by predicting by , with an observable . Display (2.2) shows that it is a population level cost that is incurred in any risk analysis of a predictor of type (3) performed under FRM. Lemma 1 below quantifies its size, and makes use of the signal-to-noise ratio given by

| (8) |

Its proof can be found in Appendix A.1.

Lemma 1.

For any with invertible such that ,

| (9) |

The inequalities above become asymptotically tight when the signal retained in dimensions by dominates the ambient noise, that is, when as . In general, as soon as , for some and is well conditioned such that , we further obtain, using (2.2), for any , that

| (10) |

Therefore a risk analysis of linear predictors under factor regression models, which consists in upper bounding , will necessarily include terms larger than in the risk bounds, irrespective of the construction of the linear predictor. If, in addition, is well-conditioned with , then

and Lemma 1 in turn implies

This demonstrates that the signal-to-noise ratio must necessarily dominate for

the excess risk to vanish as .

2.3 Upper bound of the risk

To motivate our main result, we first introduce some key quantities that appear in the risk bound derivation for any generic leading to the predictors of type (3).

The prediction risk bound depends on in Definition 1, specifically on the noise level of . To quantify this noise level, we use the following deviation bound from Lemma 18 in Appendix B. For any such that , one has

| (11) |

where is defined as

| (12) |

with being some positive constant. The quantity will play a role in the risk bound and it could take any non-negative value in general. When for some constant , one has When for some constant , we have . In particular, if , we have . This holds for instance when is diagonal with entries bounded away from 0 and , independent of .

We write the projection onto the column space of as

its complement as and . Since , as proved in Lemma 11 in Appendix A, we find that making clear that the component of the data matrix orthogonal to the range of , , is not used for prediction. It is natural therefore that the size of this component, as measured by its largest singular value, , will affect the risk bound, and needs to be contrasted with the size of the retained signal, , as measured by its smallest non-zero singular value . These two quantities appear in the risk bound below.

We now state our main theorem; its proof is deferred to Appendix A. Recall that is the risk defined in (4). Write .

Theorem 2.

Let for some , and set

| (13) |

For any with for some positive constant such that , there exists some absolute constant such that

| (14) | ||||

Here the symbol means the inequality holds up to a multiplicative constant possibly depending on the sub-Gaussian constants , and .

Since we aim to provide a unified analysis of the risk for a general , the bound (14) itself depends on the random quantities , and . To make it informative, one needs to further control these random quantities for specific choices of . The main usage of Theorem 2 is thus to reduce the task of bounding to the relatively easier one of controlling , and . We will demonstrate this for several choices of in the following sections.

Theorem 2 holds for any estimator that is constructed from with any . We now explain the various terms in the bound (14). Recall that and . To aid intuition, by adding and subtracting terms, we have

| (15) |

We discuss the four terms above one by one.

-

•

The first term leads to the following variance term in (14):

We see that the random variable quantifies the retained signal in by noting that . The two factors and come from bounding the second moments of and from , respectively, relative to the retained signal . The dimension reflects the complexity of and the integer is the intrinsic dimension of the latent factor, thus only appearing in the term containing .

-

•

The second and third terms in (15) lead to the following term in (14), which can be interpreted as arising from the fact that and are not observed:

With slight abuse of terminology, we refer to this as a bias term. The factor is irreducible, as argued in (10), the term has been explained in the first term, and the inflation factor is due to the inflated noise level of compared to .

-

•

The fourth term in (15) quantifies the error of estimating the best linear predictor under the factor regression model. In this model, we note that with . Also noting that is a projection matrix, the fourth term in (15) represents the error of estimating the range space of , which is exactly zero if the range of contains the range of . In general, the bound in (14) corresponding to this term is

where the first part is the error of estimating the range space of while the second part is that of estimating the range space of , controlled by .

Remark 1.

In light of the above discussion, we make two important remarks. First, to maintain a fast rate of the risk bound in (14), we should retain enough signal in relative to the noise such that with high probability. Second, if this is the case, the bound (14) simplifies to

As increases, meaning that the predictor can be interpreted as more complex, the variance term increases, while the term is not affected.

If decreases as increases (as seen with the PCR predictor studied in the next section), the term , corresponding to the error of estimating the range space of , gets smaller.

Therefore, the tradeoff of using a more complex predictor lies between the increasing variance and the decreasing error of estimating the range space of , provided that enough signal is retained in . A more transparent tradeoff can be seen for the PCR predictor analyzed in the next section. More generally, for each of our examples, we will see the mechanism by which , , and are controlled.

3 Analysis of Principal Component Regression under the factor regression model

In this section we use the general result, Theorem 2, to derive risk bounds for the popular Principal Component Regression (PCR) method. For any integer , the PCR-predictor PCR- corresponds to taking , the matrix with columns equal to the first right singular vectors of corresponding to the non-increasing singular values . We start by giving risk bounds for PCR- for any in the corollary below. For simplicity, we write

with the convention that and for all . All the proofs of this section can be found in Appendix A.2.

Corollary 3.

For any with and some positive constant such that follows sG-FRM, there exists some absolute constant such that, for any (possibly random),

| (16) |

where and

| (17) | ||||

| (18) |

Corollary 3 follows immediately from the identities and , and an application of Theorem 2 with

The bound in (16) depends on and , which may be further controlled by and , respectively, in order to make the bound more informative (see, for example, the proof of Remark 2 in Appendix A.2). Nevertheless, (16) illustrates the effect of and hints at the choice with

| (19) |

Here is defined in (12) and is some positive constant. The quantity corresponds to what is known as the elbow method, and is a ubiquitous approach for selecting the number of top principal components of the data matrix . The quality of as an estimator of the effective rank of has been analyzed in Bunea and Xiao (2015), but its role in PCR has received little attention. By definition, , which implies

Furthermore, Weyl’s inequality implies and, in conjunction with (11), and by choosing , we obtain with high probability. We summarize this discussion in the following result pertaining to prediction via the first principal components selected via the elbow method.

Corollary 4.

For any with such that follows sG-FRM, we have for defined in (19) for any ,

| (20) |

Remark 2.

-

1.

We refer to the method analyzed in Corollary 4 as the theoretical elbow method, as it involves the theoretically optimal threshold level . The next section analyzes the performance of a data-adaptive elbow method.

-

2.

For any , we show in Appendix A.2 that, if for some sufficiently large constant , then holds for some with high probability. The event implies which, in conjunction with the high probability event , guarantees with high probability. Corollary 4 thus covers the risk of PCR-, that is, the risk of the PCR predictor corresponding to the true of this .

3.1 Selection of the number of retained principal components via penalized least squares

A practical issue of PCR- is that the selection of according to (19) relies on a theoretical order in (12), which depends on the unknown quantities and . To overcome this difficulty, we

provide an alternative, data dependent procedure, which shares the risk bound derived for PCR-.

Our procedure of selecting the number of retained principal components is adopted from Bing and Wegkamp (2019), originally proposed for selecting the rank of the coefficient of a multivariate response regression model . The factor model is a particular case with and , and, following Bing and Wegkamp (2019), we define

| (21) |

for a given sequence . Here is some absolute constant introduced to avoid division by zero. We write as the best rank approximation of . More specifically, let the SVD of as with non-increasing and we have .

The denominator of the ratio defining can be viewed as a penalty on the numerator, with tuning sequence . From Bing and Wegkamp (2019, Equation 2.7), the minimizer conveniently has a closed form

counting the number of singular values of above a variable threshold. This is in contrast to the elbow method in (19), which counts the number of singular values of above the fixed threshold , as

We note that when , for any . Hence there are multiple minima (zeroes in this case) in , and if we adopt the convention to choose the first index with

, we find , almost surely. The risk of PCR- has already been discussed in Remark 2 above.

The theoretical guarantees proved in Bing and Wegkamp (2019) are based on the assumption that has i.i.d. entries with zero mean and bounded fourth moments. Proposition 5 extends this to models in which the rows of are allowed to have dependent entries, when they follow a sub-Gaussian distribution. We show that the choice , for some absolute numerical constant , leads to desirable results. The induced size of , for this , is of order . We found the choice worked well for all our simulations, as presented in Section 6.

Let denote the effective rank of . The following proposition shows that finds, adaptively, the theoretical elbow.

Proposition 5.

Let be defined in (21) with for some absolute constant . For any such that follows sG-FRM, , and

| (22) |

for some positive constants and , we have

| (23) |

Condition holds, for instance, if with . We explain the connection between restriction (22) and the proposed choice of . Using elementary algebra, Bing and Wegkamp (2019, Theorem 6 and Proposition 7) proves the deterministic result

| (24) |

which shows that if is appropriately large, then the selected is less than or equal to dimension of the factor regression model generating the data. On the other hand, by concentration inequalities of and around and , respectively (see the proof of Proposition 5 in Appendix A.2), the bound

| (25) |

holds with probability larger than . Thus, in view of (24) and (25), the event holds with high probability as soon as . Under (22), we arrive at the choice and, in turn, .

We note that (22) holds, for instance, in the commonly considered setting

| (26) |

while being more general. One can alternatively consider other error structures, for instance, with , in which case the above reasoning leads to the choice . However, this would limit the range of , up to in (21), while our interest is in factor regression models with dimensions allowed to grow with .

3.2 Existing results on PCR

Due to the popularity and simplicity of PCR, its prediction properties under the factor regression model have been studied for nearly two decades. Most existing theoretical results, discussed below, are asymptotic in and and, to the best of our knowledge, have been established for a model of known dimension , or when is identifiable under additional restrictions on the parameter space, and can be consistently estimated.

The fact that PCR prediction, under the factor regression model with known or identifiable , has asymptotically vanishing excess risk only when both and grow to is a well known result. This can already be seen from our derivation (10) above, which shows that a necessary condition for prediction with vanishing excess risk, under factor regression models with well conditioned , is , which can be met when , as explained below.

This phenomenon was first quantified in Stock and Watson (2002), where it is shown that

This result is the most closely related to ours, and we discuss it in detail below. We also mention that several later works, for instance Bai (2003) and Fan et al. (2013), provided explicit convergence rates and inferential theory for the in-sample prediction error , whereas in this work we study out-of-sample performance. For completeness, we comment on these related, but not directly comparable, results in Appendix D.

In addition to being asymptotic in nature, the results in Stock and Watson (2002), and also those regarding the in-sample prediction accuracy, are established under the following set of conditions: , , , as , and

| (28) |

These conditions serve as identifiability conditions for (Stock and Watson, 2002). Condition (28) further implies that, for some constants ,

| (29) |

In contrast, our Corollaries 3, 4 and 6 are non-asymptotic statements, which hold for any finite , and , where is allowed to depend on , with . Consequently, and are also allowed to grow with . Furthermore, our conditions on the signal are much weaker than (29) to derive the risk bound of PCR-. To see this, and for a transparent comparison, suppose and . Then from Remark 2 we only require a condition much weaker than of (Stock and Watson, 2002) given in (29) above, namely

Finally, the results in Stock and Watson (2002) are established for the unique under additional restrictions of the parameter space discussed above, whereas our results are established for any with such that satisfying sG-FRM, without requiring to be identifiable. In particular, our results hold for any identifiable that further satisfies (28).

4 Analysis of alternative prediction methods

In this section we illustrate the usage of the main Theorem 2 to derive risk bounds under a factor regression model for two other prediction methods: Generalized Least Squares (Bunea et al., 2020), as an example of another model agnostic predictor construction, and model-tailored prediction, in an instance of an identifiable factor regression model provided by the Essential Regression framework introduced in Bing et al. (2019). All proofs for this section are contained in Appendix A.3.

4.1 Prediction risks of minimum norm interpolating predictors under factor regression models

In the recent paper Bunea et al. (2020), risk bounds were established under the factor regression model for the Generalized Least Squares (GLS) predictor, which corresponds to taking :

| (30) |

We recover as these results in Corollary 7 and Corollary 8 below, as further illustration of the application of our main theorem. Since and , the application of Theorem 2 with amounts to obtaining a lower bound on the smallest non-zero singular value of to bound .

We consider the low ()- and high ()-dimensional settings separately. In the former case, GLS reduces to the ordinary least squares (OLS) method. The following corollary states the prediction risk of the OLS under the factor regression model. The proof uses a standard random matrix theory result (see Vershynin, 2012, Theorem 5.39) to show , which implies . Recall that .

Corollary 7 (GLS: low-dimensional setting).

Suppose for an absolute constant . For any with and such that , one has

When is much larger than , the GLS becomes the minimum norm interpolator (Bunea et al., 2020), one method studied in the recent wave of literature on the generalization of overparameterized models with zero or near-zero training error (Montanari et al., 2019; Bunea et al., 2020; Muthukumar et al., 2019, 2020; Hastie et al., 2019; Feldman, 2019; Belkin et al., 2019a, b, 2018a, 2018b, 2018c; Bartlett et al., 2019; Liang and Rakhlin, 2018). Theorem 2 can also be applied to recover a slightly modified form of the prediction risk bound from Bunea et al. (2020) in this case, which we state in the following corollary. Recall that is the effective rank of .

Corollary 8 (GLS: high-dimensional setting. Interpolating predictors.).

For any with such that , suppose defined in Definition 1 has independent entries and for some sufficiently large constant . Then there exists such that

4.2 Prediction under Essential Regression

Both Principal Component Regression and Generalized Least Squares are model-agnostic methods, in that they do not use explicit estimates of the model parameters to perform prediction. In contrast, further assumptions can be placed on the factor model to make identifiable, in which case a direct estimate of can be meaningfully constructed and used for prediction. The Essential Regression (ER) framework introduced in Bing et al. (2019) provides an approach to do this.

Essential Regression is a particular factor regression model under which the latent factor becomes interpretable under additional model assumptions. Specifically, under model (1), one further assumes the following model specifications.

Assumption 1.

-

(A0)

for all .

-

(A1)

For every , there exists at least two , such that .

-

(A2)

There exists a constant such that

-

(A3)

The covariance of is diagonal with bounded diagonal entries.

The indices satisfying are called pure variables and collected in the set . We use to denote all the variables that are non-pure.

Within the Essential Regression framework, the matrix becomes identifiable up to a signed permutation (Bing et al., 2020). In fact, can be further shown to be identifiable (Bing et al., 2019).

We explain how to construct predictors of tailored to a factor model, and elaborate on the predictor tailored to Essential Regression. Under any factor model (1), the best predictor of from is . However, since is not observable, this expression does not lend itself to sample level prediction. A practically usable expression for a predictor under the factor regression model can be obtained by the following reasoning. Using the Moore-Penrose inverse of the matrix , we observe that model (1) implies

The best linear predictor (BLP) of from is given by

| (31) |

The simple observation that

justifies predicting by . Inserting the identity simplifies to

motivating prediction based on a new data point by

which has the general form (3) with , with being an estimator of tailored to the ER model, developed in Bing et al. (2020). We summarize the construction of in Appendix C for completeness.

To analyze the prediction risk of we will also need the following assumption on the covariance matrix , which plays the same role as the Gram matrix in classical linear regression with random design.

Assumption 2.

Assume for some constants and bounded away from and .

The prediction risk of can be obtained via an application of Theorem 2, with the choice . Since is identifiable under the Essential Regression framework, the estimator can be compared directly with and, as shown in Bing et al. (2020),

| (32) |

with high probability. The rows of the submatrix of correspond to all the index set of non-pure variables. The estimation bound (32) can be leveraged to obtain a small improvement in the risk bound by slightly adjusting the proof of Theorem 2. Using this approach, we obtain the following result by establishing, with high probability, that

Theorem 9 (Prediction in Essential Regression).

Remark 3.

-

1.

We note that the bound (33) depends on , which in turn depends on the number of non-pure variables, and the sparsity of the rows of corresponding to these non-pure variables. The rate indicates that prediction based on will perform best when the number of pure variables is large, and any non-pure variable , the th component of , only depends on a small number of latent variables. We give, in the following section, a simplified form of this bound, and compare this prediction scheme with the other methods discussed in this work.

-

2.

The identifiable factor model , with satisfying Assumption 1, has been used in Bing et al. (2020) to construct overlapping clusters of the components on . The latent factors can be viewed as random cluster centers, while a sparse matrix gives the cluster membership. From this perspective, and in light of the discussion leading up to the predictor construction, one can view as the risk of predicting from predicted cluster centers, on the basis of data that exhibits a latent cluster structure with overlap.

4.3 Comparison of simplified prediction risks

In this section we offer a comparison of the prediction risk of the predictors analyzed above. For a transparent comparison, we compare them under an identifiable factor regression model. To this end, we consider the Essential Regression framework as a data generating mechanism under which we compare PCR-, with known , the GLS predictor (), and the Essential Regression predictor (), based on Corollary 4, Remark 2, Corollary 8 and Theorem 9, respectively. The notation stands for up to a multiplicative logarithmic factor in or .

For ease of comparison, we consider the simplified setting in which ,333This is met for instance when all ’s are pure variables and the numbers of pure variables for all groups are balanced in the sense that . Another instance such that holds with high probability is that and the rows of are i.i.d. realizations of a sub-Gaussian random vector whose second moment has operator norm bounded by . The factor takes in Assumption 1 into account. and , and focus on the high-dimensional regime where for a large enough constant . We have

| (34) | ||||

Since the Essential Regression predictor is an instance of model based prediction, we comment on when the two model agnostic predictors are competitive, under this particular model specification.

We begin with a comparison between and , and note that the difference in their respective errors bounds depends on the sparsity of . The risk bound on is valid for any such that , and is in particular valid for satisfying the additional Essential Regression constraints. Our results show that while PCR- prediction is certainly a valid choice under this particular model set-up, it could be outperformed by the model tailored predictor. If each row of is sparse such that , then has a faster rate. This advantage becomes considerable if , that is, in the presence of a growing number of pure variables. However, if is not sparse such that , and , then has a slower rate than . Nevertheless, from a practical perspective, conditions on the sparsity of () simply mean that not all variables in the vector contribute to explaining a particular , for each , which is the main premise of Essential Regression. Furthermore, in this risk bound comparison, corresponds to , for an appropriate, fully data dependent, estimator of the identifiable dimension . In order to employ a fully data driven PCR prediction, corresponding to an estimated , we would also need the delicate step of estimating it described in Section 3 above. The risk bound above will then hold under conditions discussed in Remark 2.

Finally, the much simpler GLS interpolating predictor has a bound that compares favorably to the other agnostic predictor, PCR-, only when is small enough, for instance, . This extra term in the bound for compared to the bound for PCR-, is due to the additional variance induced by the usage the full data matrix , as opposed to the first principal components, which may already capture the majority of the signal.

5 Predictor selection via data splitting

Whenever a factor regression model can be assumed to generate a given data set, but it is unclear what further model specifications are in place, one can, in principle, construct several predictors, some model agnostic and some tailored to prior beliefs. In this section we address the problem of choosing among a set of candidate predictors for a given data set that is assumed to be generated by a factor regression model. Suppose we have linear predictors with respective coefficients that we want to choose from. For ease of presentation, in this section assume is divisible by . Let be a subset of with , and let . Define

| (35) |

where for each , is trained on the data set and is thus independent of . We then use as our predictor, for which we establish the following oracle inequality, which is an adaptation of Theorem 2.1 from Wegkamp (2003) to factor regression models and unbounded linear predictors. Moreover, we provide a high-probability statement, as opposed to a bound on the expected risk as in Wegkamp (2003). The proof is deferred to Appendix A.4.

Theorem 10.

Let , where is defined in (35). Then for any such that , there exist absolute constants and a constant such that when and for any ,

| (36) |

where .

In the bound above, the worst excess risk appears in the remainder term, which may appear unusual. Most model-selection oracle inequalities either are formulated as a bound on the empirical risk, or assume that the predictors are uniformly bounded, or both, and as a result do not contain a term of this form. The bound we give is for the prediction risk on new data, and for unbounded loss and predictors, since . For the bound to be useful, it thus must be the case that none of the predictors has risk that grows too fast. In particular, if the risks of all predictors are bounded above in high probability, then the second term in (10) will be and thus typically subdominant.

As an illustration, we can use this data-splitting procedure with and the three prediction methods discussed in Section 4.3. If the three excess risks in (34) are all , which is met under the conditions discussed in detail in Section 4.3, then the bound (10) becomes

We further confirm the ability of the data-splitting approach to adapt to the best-case risk via simulations in Section 6 below.

On a practical note, we remark that the splitting procedure can be repeated several times with random splits to obtain estimates that can be used to construct the average . This aggregate coefficient vector satisfies the same risk bound (10) by convexity of the loss, while this approach in practice could alleviate some of the bias induced by the choice of split for the data.

6 Simulations

In this section, we complement and support our theoretical findings with simulations, focusing on the prediction performance of candidate predictors under both the generic factor regression model and the Essential Regression framework.

Candidate predictors:

We consider the following list of predictors:

-

•

PCR- with obtained from (21) with ;

-

•

PCR-: the principal component regression (PCR) predictor using the true ;

- •

-

•

GLS: the Generalized Least Squares predictor defined in (30);

-

•

ER-A: the Essential Regression predictor with in (3);

-

•

Lasso: implemented in glmnet with the tuning parameter chosen via cross-validation;

-

•

Ridge: implemented in glmnet with the tuning parameter chosen via cross-validation;

- •

Both Lasso and Ridge are included for comparison. The Lasso is developed for predicting from when we expect that the best predictor of is well approximated by a sparse linear combination of the components of . Under our model specifications, the best linear predictor of from is given by

where the last step follows from the factor model (1) and an application of the Woodbury matrix identity. Although is not sparse in general, we observe that . Hence its -norm may be small if is small. Our simulation design allows for these possibilities.

Data generating mechanism:

We first describe how we generate , , and . To generate , we set to a -length sequence from 2.5 to 3 with equal increments. The off-diagonal elements of are then chosen as for all . Finally, is chosen as a diagonal matrix with diagonal elements sampled from , and is generated with entries sampled from Unif.

Generating depends on the modeling assumption. Under the factor regression model, we sample each entry of independently from . Under the Essential Regression setting, recall that can be partitioned into and which satisfy Assumption 1. To generate , we set for each and choose , where denotes the kronecker product. Each row of is generated by first randomly selecting its support with cardinality drawn from and then by sampling its non-zero entries from with random signs. In the end, we rescale such that the norm of each row is no greater than 1.

Finally, we generate the matrix and the noise matrix whose rows are i.i.d. from and , respectively. We then set and where the components of are i.i.d. .

For each setting, we generating 100 repetitions of and record their corresponding results. The performance metric is based on the new data prediction risk. To calculate it, we independently generate a new dataset containing i.i.d. samples drawn according to our data generating mechanism. The prediction risk of the predictor is calculated as .

6.1 Prediction under the factor regression model

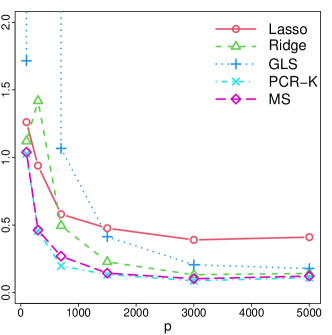

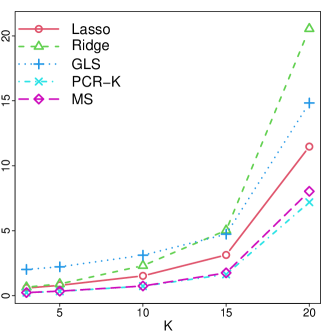

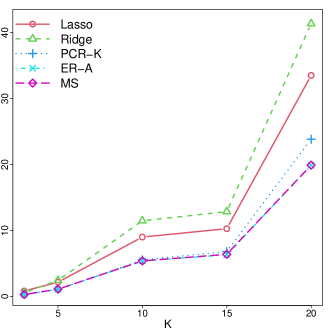

We compare the performance of PCR-, PCR-, PCR-ratio, GLS, Lasso, Ridge and MS by varying , and the signal-to-noise ratio (SNR) defined in (8), one at a time. The MS predictor is based on (35) over all the aforementioned methods.

We first set , and vary from , then choose , and vary from . The prediction risks of different predictors for these two settings are shown in Figure 1. Since both PCR- and PCR-ratio consistently select the true , we only present the result for PCR-.

|

|

Results:

Overall, it is clear that the MS predictor selects the best predictor in almost all settings, corroborating Theorem 10. Meanwhile, PCR- has the best performance in all settings as it is tailored to the factor regression model.

From the first panel, all methods perform better as increases (with exceptions given to GLS and Ridge when ). This contradicts the classical understanding that having more features increases the degrees of freedom of the model, hence inducing larger variance. By contrast, in our setting, increasing the number of features provides information that can be used to predict . This can be seen from the minimal excess risk in Lemma 1 by noting that increases as increases. This phenomenon has been observed in the classical factor (regression) model, see, for instance, Stock and Watson (2002); Bai (2003); Bai and Ng (2008, 2006); Fan et al. (2013) and the references therein.

Perhaps more interestingly, when is much larger than , GLS and Ridge have performance similar to PCR-. This demonstrates our conclusions in Section 4.3 that GLS and PCR- are comparable when . We also note from our simulation that Ridge tends to select near-zero regularization parameter when , whence Ridge essentially reduces to GLS (Hastie et al., 2019). In contrast to GLS and Ridge, the performance of Lasso stops improving after . When is moderately large (say ), GLS and Ridge have larger errors than PCR- and Lasso. In particular, if is close to , the error of GLS diverges, a phenomenon observed in Hastie et al. (2019), for example, under the linear model.

From the second panel, the prediction error for all methods deteriorates as increases. This indicates that prediction becomes more difficult for large , supporting our results in Sections 3 and 4. We also note that the performance of Ridge deteriorates faster than the other methods when grows.

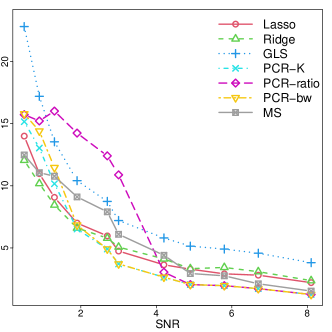

To further demonstrate how different predictors behave as the signal-to-noise ratio (SNR) changes, we multiply by a scalar chosen within . We set , and . For each , we calculate the SNR and plot the prediction risks of each predictor in Figure 2.

Results:

As expected, all methods perform worse as the SNR decreases. MS has consistently selected the (near) best predictor. When the SNR is small (less than 2), Ridge has the best performance. As soon as the SNR exceeds , PCR-K and PCR- start to outperform the other methods. In terms of selecting , when the SNR is larger than , PCR- starts estimating consistently whereas PCR-ratio fails until the SNR is greater than . Both PCR- and PCR-ratio tend to under-estimate in the presence of a small SNR. However, PCR- selects closer to than PCR-ratio, leading to better performance. Moreover, the loss due to using by PCR- is not significant, in line with Corollary 6 and Remark 2.

6.2 Prediction under the Essential Regression model

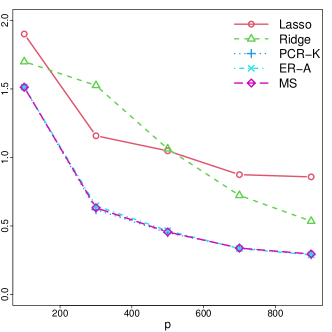

We compare all the predictors when data is generated from an Essential Regression model. To vary and individually, we first set , , and choose from , then fix , , and vary in . The prediction risks of different predictors are shown in Figure 3. PCR- and PCR-ratio are not included as they have almost the same performance as PCR-. As it was demonstrated under the factor regression setting that GLS is outperformed by the other predictors when is not large enough, we also excluded its performance from the plot.

Summary:

We observe the same phenomenon as before, that is: (1) all predictors benefit from large ; (2) as increases, the performance of all predictors deteriorate. Furthermore, the model-based ER predictor has similar performance as the model-free PCR predictor when is small. The advantage of ER over PCR enlarges as grows. This is aligned with our theoretical findings in Section 4.3 that ER benefits from the sparsity of , because our data generating mechanism ensures that the larger is, the sparser becomes.

|

|

Acknowledgements

Bunea and Wegkamp are supported in part by NSF grants DMS-1712709 and DMS-2015195.

References

- Ahn and Horenstein [2013] Seung C. Ahn and Alex R. Horenstein. Eigenvalue ratio test for the number of factors. Econometrica, 81(3):1203–1227, 2013.

- Bai [2003] Jushan Bai. Inferential theory for factor models of large dimensions. Econometrica, 71(1):135–171, 2003.

- Bai and Ng [2002] Jushan Bai and Serena Ng. Determining the number of factors in approximate factor models. Econometrica, 70(1):191–221, 2002.

- Bai and Ng [2006] Jushan Bai and Serena Ng. Confidence intervals for diffusion index forecasts and inference for factor-augmented regressions. Econometrica, 74(4):1133–1150, 2006. doi: 10.1111/j.1468-0262.2006.00696.x.

- Bai and Ng [2008] Jushan Bai and Serena Ng. Forecasting economic time series using targeted predictors. Journal of Econometrics, 146(2):304 – 317, 2008. Honoring the research contributions of Charles R. Nelson.

- Bair et al. [2006] Eric Bair, Trevor Hastie, Debashis Paul, and Robert Tibshirani. Prediction by supervised principal components. Journal of the American Statistical Association, 101(473):119–137, 2006.

- Bartlett et al. [2019] Peter L. Bartlett, Philip M. Long, Gábor Lugosi, and Alexander Tsigler. Benign overfitting in linear regression. In arXiv:1906.11300, 2019.

- Belkin et al. [2018a] Mikhail Belkin, Daniel Hsu, and Partha Mitra. Overfitting or perfect fitting? risk bounds for classification and regression rules that interpolate. In arXiv:1806.05161, 2018a.

- Belkin et al. [2018b] Mikhail Belkin, Siyuan Ma, and Soumik Mandal. To understand deep learning we need to understand kernel learning. In arXiv:1802.01396, 2018b.

- Belkin et al. [2018c] Mikhail Belkin, Alexander Rakhlin, and Alexandre B. Tsybakov. Does data interpolation contradict statistical optimality? In arXiv:1806.09471, 2018c.

- Belkin et al. [2019a] Mikhail Belkin, Daniel Hsu, Siyuan Ma, and Soumik Mandal. Reconciling modern machine-learning practice and the classical bias–variance trade-off. Proceedings of the National Academy of Sciences, 116(32):15849–15854, 2019a. doi: 10.1073/pnas.1903070116.

- Belkin et al. [2019b] Mikhail Belkin, Daniel Hsu, and Ji Xu. Two models of double descent for weak features. In arXiv:1903.07571, 2019b.

- Bing and Wegkamp [2019] Xin Bing and Marten H. Wegkamp. Adaptive estimation of the rank of the coefficient matrix in high-dimensional multivariate response regression models. Ann. Statist., 47(6):3157–3184, 12 2019. doi: 10.1214/18-AOS1774. URL https://doi.org/10.1214/18-AOS1774.

- Bing et al. [2019] Xin Bing, Florentina Bunea, and Marten Wegkamp. Inference in interpretable latent factor regression models. In arXiv:1905.12696, 2019.

- Bing et al. [2020] Xin Bing, Florentina Bunea, Ning Yang, and Marten Wegkamp. Adaptive estimation in structured factor models with applications to overlapping clustering. To appear in the Annals of Statistics, 2020.

- Bunea and Xiao [2015] Florentina Bunea and Luo Xiao. On the sample covariance matrix estimator of reduced effective rank population matrices, with applications to fpca. Bernoulli, 21(2):1200–1230, 05 2015. doi: 10.3150/14-BEJ602. URL https://doi.org/10.3150/14-BEJ602.

- Bunea et al. [2020] Florentina Bunea, Seth Strimas-Mackey, and Marten Wegkamp. Interpolation under latent factor regression models. In arXiv:2002.02525, 2020.

- Fan et al. [2013] Jianqing Fan, Yuan Liao, and Martina Mincheva. Large covariance estimation by thresholding principal orthogonal complements. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 75(4):603–680, 2013.

- Fan et al. [2017] Jianqing Fan, Lingzhou Xue, and Jiawei Yao. Sufficient forecasting using factor models. Journal of Econometrics, 201(2):292 – 306, 2017.

- Feldman [2019] Vitaly Feldman. Does learning require memorization? A short tale about a long tail. arXiv:1906.05271, 2019.

- Hastie et al. [2019] Trevor Hastie, Andrea Montanari, Saharon Rosset, and Ryan J. Tibshirani. Surprises in high-dimensional ridgeless least squares interpolation. In arXiv:1903.08560, 2019.

- Hotelling [1957] Harold Hotelling. The relations of the newer multivariate statistical methods to factor analysis. British Journal of Statistical Psychology, 10(2):69–79, 1957.

- Hsu et al. [2014] Daniel Hsu, Sham M. Kakade, and Tong Zhang. Random design analysis of ridge regression. Found. Comput. Math., 14(3):569–600, June 2014. ISSN 1615-3375. doi: 10.1007/s10208-014-9192-1.

- Kelly and Pruitt [2015] Bryan Kelly and Seth Pruitt. The three-pass regression filter: A new approach to forecasting using many predictors. Journal of Econometrics, 186(2):294 – 316, 2015. ISSN 0304-4076. High Dimensional Problems in Econometrics.

- Kendall [1957] Maurice G. Kendall. A course in multivariate analysis. Hafner Pub. Co., 1957.

- Lam and Yao [2012] Clifford Lam and Qiwei Yao. Factor modeling for high-dimensional time series: Inference for the number of factors. Ann. Statist., 40(2):694–726, 04 2012.

- Liang and Rakhlin [2018] Tengyuan Liang and Alexander Rakhlin. Just interpolate: Kernel ”ridgeless” regression can generalize. In arXiv:1808.00387, 2018.

- Montanari et al. [2019] Andrea Montanari, Feng Ruan, Youngtak Sohn, and Jun Yan. The generalization error of max-margin linear classifiers: High-dimensional asymptotics in the overparametrized regime. In arXiv:1911.01544, 2019.

- Muthukumar et al. [2019] Vidya Muthukumar, Kailas Vodrahalli, Vignesh Subramanian, and Anant Sahai. Harmless interpolation of noisy data in regression. In arXiv:1903.09139, 2019.

- Muthukumar et al. [2020] Vidya Muthukumar, Adhyyan Narang, Vignesh Subramanian, Mikhail Belkin, Daniel Hsu, and Anant Sahai. Classification vs regression in overparameterized regimes: Does the loss function matter? In arXiv:2005.08054, 2020.

- Stock and Watson [2002] James H. Stock and Mark W. Watson. Forecasting using principal components from a large number of predictors. Journal of the American Statistical Association, 97(460):1167–1179, 2002. ISSN 01621459.

- Vershynin [2012] Roman Vershynin. Introduction to the non-asymptotic analysis of random matrices, pages 210 – 268. Cambridge University Press, 2012.

- Wegkamp [2003] Marten Wegkamp. Model selection in nonparametric regression. Ann. Statist., 31(1):252–273, 2003.

Appendix

We provide section-by-section proofs for the main results in Appendices A.1 – A.4. Auxiliary lemmas are collected in Appendix B. Appendix C contains the procedure of estimating under the Essential Regression framework while comparison with more existing literature on factor models is stated in Appendix D.

Appendix A Main proofs

We start by giving an elementary lemma that proves for any . Recall that, for any matrix , denotes its Moore-Penrose inverse and denotes the projection onto the column space of .

Lemma 11.

Let be any matrix. Then

Proof.

Write the SVD of as where and are orthonormal matrices with . We then have

The result then follows by noting that . Step (i) uses the fact that

which can be verified by the definition of Moore-Penrose inverse. Indeed, let , and . We need to verify

Straightforwardly,

and similar arguments hold for . Step (ii) uses step (i) with and ∎

A.1 Proofs for Section 2

Proof of Lemma 1

Let , . Since is invertible, so is invertible. Thus, letting ,

| (37) |

Using this expression, and the factor model structure , , the proof of Lemma 4 in Bunea et al. [2020] uses the Woodbury matrix identity to simplify (37), arriving at

Letting , we then have

To obtain the upper bound on we use

where we used in the last step.

To find the lower bound we first observe that

Furthermore,

so using this in the previous display,

as claimed. ∎

Proof of Theorem 2

Define and recall that from (3). Pick any with such that follows FRM() where is some positive constant. By and , and the independence of , , and , one has

| (38) | ||||

| (39) |

We define an event in (40) below, on which we bound the risk. Invoking Lemmas 13, 14 and using , we find that the stated bound holds on the event . Then, by Lemma 12, , which completes the proof. ∎

We state and prove three lemmas which are used in the proof of Theorem 2. Recall that

Lemma 12.

For any with and some positive constant such that follows FRM(), we have for some absolute constant , where we define the event

| (40) |

Here, for some constants and depending on and , respectively,

with , defined in (12), and

Proof.

By an application of Theorem 5.39 of Vershynin [2012] and , we find . From Lemma 18 with , , and , we find .

We note that has independent sub-Gaussian entries, so is a sub-Gaussian random vector. Applying Lemma 17 with , , and choosing yield

| (41) |

We prove in Lemma 15. By the independence of and both and , the matrix is independent of . Thus, by an application of Lemma 17 with , , and gives . Taking the expectation over then gives . The same argument with gives .

Combining results, we find

∎

Proof.

Starting with the identity

| (43) |

with , we have

To bound the first term, notice that

where the last step holds on (in particular, on ). Observe that, on ,

Write the SVD of as where and are orthogonal matrices with . Recalling that , the following holds, on the event ,

| (44) |

where we used for any matrix in , in and

in . This concludes, on the event ,

| (45) |

Proof.

Proof.

By , one has

for any matrix . Choose

to obtain

Then by the basic inequality ,

| (55) | ||||

where we invoked the definition of in the last line. Invoke from (40) to finish the proof. ∎

A.2 Proofs for Section 3

Proof of Corollary 3

The corollary is an application of Theorem 2 with . Given any realization of and (possibly random) , we may write the SVD of as

The diagonal matrix contains the non-increasing singular values and contains the corresponding right-singular vectors. Consequently,

Invoke Theorem 2 with , , and to conclude the proof.∎

Proof of Corollary 4 & Remark 2

Proof of Proposition 5

We work on the event

with defined in (12) and some constants , depending on . We have on the event ,

by choosing any . From Theorem 6 and Proposition 7 of Bing and Wegkamp [2019] with , and , we deduce

on the event .

To prove the lower bound , we notice that, on the event ,

| (56) |

The first inequality uses (2.7) in Bing and Wegkamp [2019], while the second inequality uses . Further invoking (3.8) in Proposition 7 of Bing and Wegkamp [2019] yields

Next, on the event , choosing in , we find

| by | ||||

Hence, combining all three previous displays, we derive

Next, we prove . By (2.7) in Bing and Wegkamp [2019] once again, we have

From (2.3) in Proposition 1 of Bing and Wegkamp [2019], this inequality is equivalent to

Since on , we have

| by (3.8) of Proposition 7 in Bing and Wegkamp [2019] | ||||

| by (21) | ||||

| by and | ||||

It remains to prove . First note that

By invoking Lemma 20 for fixed and some absolute constant , the inequality

holds with probability at least Apply the union bound over , invoke for sufficiently large , and conclude

Finally, Lemma 18 shows that , taking in large enough. ∎

A.3 Proofs for Section 4

Proof of Corollary 7

By Theorem 5.39 of Vershynin [2012], with probability at least , where we use that has independent sub-Gaussian rows with sub-Gaussian constant bounded by an absolute constant, which is implied by the sub-Gaussianity of and , and that . Thus, with the same probability,

Proof of Corollary 8

Proof of Theorem 9

Instead of directly applying Theorem 2, we slightly modify the proofs of Theorem 2 to obtain a sharp result for .

From the proof of Theorem 2, display (A) gives

We then point out the modifications of the proof of Lemmas 13 and 14. Recall . We work on the event defined in the proof of Theorem 2 intersected with the event that and

The last two events holds with probability at least for some constant [Bing et al., 2020]. In display (47) of Lemma 13 for bounding , we use

We change the way to bound the second term on the right hand side. Specifically, set and use twice to obtain

By , and Lemma 16, after a bit algebra, we conclude

| (57) |

with probability at least . In the last step, we used the fact that is bounded and . Together with the proofs of Lemma 13, one can deduce that

where

To bound , we modify two places in the proof of Lemma 14. Display (A) is bounded by

where we will invoke Lemma 16. For the first term of the right hand side, by (55), we have

which can be further bounded by using (A.3) and invoking the event . Collecting all these ingredients, we conclude

It then remains to lower bound by bounding from below. By Weyl’s inequality, , we have

by writing . To lower bound , using Weyl’s inequality again and invoking Lemma 19 yield

with probability at least . On the other hand, by ,

By and Lemmas 16 and 18, we have

with probability at least . Provided that

for sufficiently small constant , we then conclude that

from noting This concludes . The result then follows by collecting terms. ∎

The following lemma provides upper bounds for the operator norm of . Recall that .

Lemma 16.

Under conditions of Theorem 9, with probability at least , one has

Proof.

A.4 Proof of Theorem 10 in Section 5

For any , let

so that for all , by the definition of , . Also let

Finally, for any fixed or random define

where the expectation is over that are independent of .

We have

Using in the first term of the above, we have for any ,

| (58) |

The first term in the above can be further re-written as

Using this result in (58), we find that for any ,

| (59) |

Below we prove that

| (60) |

and

| (61) |

where and depend only on from Definition 1, and are absolute constants. The final result follows from taking a minimum over in (59) and combining (60) and (61) with a union bound.

Bounding and

Since are independent of , we will prove (60) for the case when are non-random without loss of generality.

We first consider . For all , the following holds:

| (62) |

where we write and . To prove this, suppose the left hand side holds true and consider the cases , which implies , and , which implies and thus . Thus,

| (63) | |||||

where we let in the last step. Recalling that for any random variable , , and using the assumption that is a fixed vector, we find

where . Thus,

so by Bernstein’s inequality [Vershynin, 2012],

| (64) |

Choosing , and combining with (63), for ,

| (65) |

We next consider . For , we have

To prove this, suppose the left hand side holds and consider the cases , which implies , and , which implies . Multiplying the right hand inequality by , and choosing , we find

| (66) |

Recalling

an application of (66) gives

Choosing and applying (64) with , we conclude

| (67) |

Combining (65) and (67) with a union bound and some algebra proves (60).

Bounding and

Appendix B Auxiliary lemmas

The following lemma is used in our analysis. The tail inequality is for a quadratic form of sub-Gaussian random vectors. It is a slightly simplified version of Lemma 30 in Hsu et al. [2014].

Lemma 17.

Let be a sub-Gaussian random vector. For all symmetric positive semi-definite matrices , and all ,

Proof.

The following lemma provides an upper bound on the operator norm of where is a random matrix and its rows are independent sub-Gaussian random vectors. It differs from Bunea et al. [2020, Theorem 10] in the sense that independence across columns of is not required.

Lemma 18.

Let be by matrix whose rows are independent sub-Gaussian random vectors with identity covariance matrix. Then for all symmetric positive semi-definite matrices ,

Proof.

Another useful concentration inequality of the operator norm of the random matrices with i.i.d. sub-Gaussian rows is stated in the following lemma. This is an immediate result of Vershynin [2012, Remark 5.40].

Lemma 19.

Let be by matrix whose rows are i.i.d. sub-Gaussian random vectors with covariance matrix . Then for every , with probability at least ,

with where and are positive constants depending on .

The deviation inequalities of the inner product of two random vectors with independent sub-Gaussian elements are well-known; we state the one in Bing et al. [2019] for completeness.

Lemma 20.

[Bing et al., 2019, Lemma 10] Let and be any two sequences, each with zero mean independent sub-Gaussian and sub-Gaussian elements. Then, for some absolute constant , we have

In particular, when , one has

where and are some positive constants.

Appendix C The LOVE algorithm

For the reader’s convenience, we give the specifics of estimating in the Essential Regression model, as developed in Bing et al. [2020]. The first step is estimation of the number of latent factors, , and the partition of pure variables, , which is achieved by Algorithm 1 below.

Given estimates and as outputs of Algorithm 1, we compute, for each and ,

| (68) |

to form the estimator of .

The submatrix is then constructed as follows. For each and the estimated pure variable set ,

| Pick an element at random, and set ; | (69) | |||

| For the remaining , set . | (70) |

Letting , to construct the remaining submatrix , we use the Dantzig-type estimator proposed in Bing et al. [2020] given by

| (71) |

for any , with tuning parameter .

The estimator enjoys the optimal convergence rate of for any [Bing et al., 2020, Theorem 5].

Appendix D More existing literature on factor models

We discuss in this section some related work on factor models which might be used to establish results of the excess risk of PCR.

By treating and jointly from model 1 as an augmented factor model

the fit is constructed by regressing onto where is the matrix of the first right singular vectors of . Bai [2003] shows that

| (72) |

for a variance term . The uniform convergence rate of over is further derived in Fan et al. [2013]. These element-wise results for in-sample prediction could, in principle, be extended to out-of-sample prediction, via additional arguments, but is not treated in the aforementioned works.

We now comment on the main differences between our Corollary 4 and the aforementioned results. The existing results are all established under conditions including , , , and (29), The uniform consistency in Fan et al. [2013] additionally requires . As a result, all previous results are asymptotic statements as .

By contrast, our Corollaries 3, 4 and 6 are non-asymptotic statements which hold for any finite , and . Moreover, they only requires the sub-Gaussian tail assumptions in Definition 1 and . As detailed in Section 3.2, our conditions on the signal are much weaker than (29) to derive the risk of PCR-.

Under condition (29), as assumed in the aforementioned literature, the prediction risk in our Corollary 4 reduces to

This rate coincides with that of , introduced in (72). Under conditions in Fan et al. [2013], their results (see, for instance, Corollary 3.1) imply

for some constant , which is slower than our rate.