Predicting the Number of Future Events

This paper describes prediction methods for the number of future events from a population of units associated with an on-going time-to-event process. Examples include the prediction of warranty returns and the prediction of the number of future product failures that could cause serious threats to property or life. Important decisions such as whether a product recall should be mandated are often based on such predictions. Data, generally right-censored (and sometimes left truncated and right-censored), are used to estimate the parameters of a time-to-event distribution. This distribution can then be used to predict the number of events over future periods of time. Such predictions are sometimes called within-sample predictions and differ from other prediction problems considered in most of the prediction literature. This paper shows that the plug-in (also known as estimative or naive) prediction method is not asymptotically correct (i.e., for large amounts of data, the coverage probability always fails to converge to the nominal confidence level). However, a commonly used prediction calibration method is shown to be asymptotically correct for within-sample predictions, and two alternative predictive-distribution-based methods that perform better than the calibration method are presented and justified.

Keywords: Binomial predictand; Bootstrap; Calibration; Censored data; Predictive distribution

1 Introduction

There are many applications where it is necessary to predict the number of future events from a population of units associated with an on-going time-to-event process. Such applications also require a prediction interval to quantify statistical prediction uncertainty arising from the combination of process variability and parameter uncertainty. Some motivating applications are given below.

Product-A Data: This example is from Escobar and Meeker, (1999), where, during a particular month, =10000 units of Product-A were put into service. Over the next 48 months, 80 failures occurred and the failure times were recorded. A prediction interval on the number of failures among the remaining 9920 units during the next 12 months was requested by the management.

Heat Exchanger Tube Data: This example is based on data described in Nelson, (2000). Nuclear power plants have steam generators that contain many stainless steel heat-exchanger tubes. Cracks initiate and grow in the tubes due to a stress-corrosion mechanism over time. Periodic inspections of the tubes are used to detect cracks. Consider a fleet of steam generators having a total of =20,000 tubes. One crack was detected after the first year of operation, which was followed by another crack during the second year and six more cracks during the third year. The data are interval-censored as the exact initiation times are unknown. A prediction interval was needed for the number of tubes that would crack from the end of the third year to the end of the tenth year.

Bearing-Cage Data: The bearing-cage failure-time data are from Abernethy et al., (1983) and are provided in the online supplementary material. Groups of aircraft engines employing this bearing cage were put into service over time (staggered entry). At the data freeze date, 6 bearing-cage failures had occurred while the remaining 1697 units with various service times were still in service (multiple right-censored data). To assure that a sufficient number of spare parts would be available to repair the aircraft engine in a timely manner, management requested a prediction interval for the number of bearing-cages that would fail in the next year, assuming 300 hours of service for each aircraft.

The purpose of this paper is to show how to construct prediction intervals for the number of future events from an on-going time-to-event process, investigate the properties of different prediction methods, and give recommendations on which methods to use.

This paper is organized as follows. Section 2 provides concepts and background for prediction inference. Section 3 describes the single-cohort within-sample prediction problem. Section 4 defines how the within-sample prediction is irregular and demonstrates that the plug-in method fails to provide an asymptotically correct prediction interval. Section 5 describes the calibration method for prediction intervals and establishes its asymptotic correctness. Section 6 presents two other prediction interval methods based on predictive distributions. The first one is a general method using parametric bootstrap samples, while the second method is inspired by generalized pivotal quantities and applies to a log-location-scale family of distributions. Section 7 extends the single-cohort within-sample prediction to the multiple-cohort problem. Section 8 compares different prediction methods, through simulation, while Section 9 applies the prediction methods to the motivating examples. Section 10 discusses the choice of distribution for the time-to-event process and addresses the issue of distribution misspecification. Section 11 gives recommendations and describes potential areas for future research.

2 Background

In a general prediction problem, denote the observable data by and the future random variable by ; while generic for now, later this paper will focus on the within-sample prediction where is a count. The conditional cdf for given is denoted by , where is a vector of parameters. The goal is to make inference for through a prediction interval, as a useful tool for quantifying uncertainty in prediction.

2.1 Prediction Intervals

When parameters in are known, the one-sided upper prediction bound is defined as the quantile of the conditional cdf for , which is

| (1) |

and the one-sided lower prediction bound may be defined as

| (2) |

where this modification of the usual quantile of ensures that is at least when is a discrete random variable. We may obtain an equal-tail prediction interval (approximate when is a discrete random variable) by combining these two prediction bounds.

In most applications, equal-tail prediction intervals are preferred over unequal ones, even though it is sometimes possible to find a narrower prediction interval with unequal tail probabilities. This is because the equal-tail prediction interval can be naturally decomposed into a practical one-sided upper prediction bound and a lower prediction bound where the separate consideration of one-sided bounds is needed when the cost of being outside the prediction bound is much higher on one side than the other.

When the parameters in are unknown, an estimation of from the observed data is required. The plug-in method, also known as the naive or estimative method (cf. Section 2.3), is to replace with a consistent estimator in the prediction bounds (1) and (2). The plug-in upper prediction bound is then while the plug-in lower prediction bound is .

2.2 Coverage Probability

Besides the plug-in method, other methods for computing prediction bounds or intervals are available. Let generically denote a prediction interval (or bound) of a nominal coverage level , where researchers would like the probability of falling within the interval to be (or close to) (i.e., ).

To be clear, there are two possible types of coverage probability: conditional coverage probability and unconditional (overall) coverage probability. The conditional coverage probability of a particular method is defined as

where denotes the conditional probability of given the observable data . The conditional coverage probability is a random variable because it is a function of the data . The unconditional coverage probability of a prediction interval method can be obtained by taking an expectation with respect to the data and it is defined as

The unconditional coverage probability is a fixed property of a prediction method and, as such, can be most readily studied and used to compare alternative prediction interval methods. We focus on unconditional coverage probability in this paper and use the term coverage probability to refer to the unconditional probability, unless stated otherwise.

We say a prediction method is exact if holds. If converges to as the sample size increases, we say the corresponding prediction method is asymptotically correct. When is a discrete random variable, however, asymptotic correctness and exactness may not generally hold or be possible for a prediction interval method, due to the discreteness in the distribution of .

2.3 Related Literature

Extensive research exists regarding some methods for computing prediction intervals. While the plug-in method has been criticized for ignoring the uncertainty in , this method is often widely viewed as being asymptotically correct (related to “regular predictions” described in Section 4.1). For example, Cox, (1975), Beran, (1990), and Hall et al., (1999) showed that the coverage probability of the plug-in method has an accuracy of for a continuous predictand under certain conditions. In Section 4 we show, however, that the plug-in method is not asymptotically correct in the context of within-sample prediction.

Section 5 presents a calibration method for within-sample prediction intervals. Cox, (1975) originally proposed the calibration idea to improve on the plug-in method and also provided analytical forms for prediction intervals based on general asymptotic expansions. Atwood, (1984) used a similar method. Beran, (1990) employed bootstrap in the calibration method, avoiding the complicated analytical expressions. Escobar and Meeker, (1999) described similar methods for constructing prediction intervals for failure times and the number of future failures, based on censored life data.

This paper does not specifically address Bayesian prediction methods, but the classic idea of a Bayesian predictive distribution can be extended to non-Bayesian methods and two such methods are considered in Section 6. Several authors have considered similar notions of a non-Bayesian predictive distribution (e.g., Aitchison, (1975), Davison, (1986), Barndorff-Nielsen and Cox, (1996)). Lawless and Fredette, (2005) demonstrated a relationship between predictive distributions and (approximate) pivotal-based prediction intervals, including the calibration method described in Beran, (1990). Fonseca et al., (2012) further elaborated on the relationship between predictive distributions and the calibration method. Shen et al., (2018) proposed a general framework to construct a predictive distribution by replacing the posterior distribution in the definition of a Bayesian predictive distribution with a confidence distribution.

3 Single Cohort Within-Sample Prediction

3.1 Within-Sample Prediction and New Sample Prediction

The term “within-sample” prediction has been used to distinguish from the more widely known “new sample” prediction. In new-sample prediction, past data are used, for example, to compute a prediction interval for the lifetime of a single unit from a new and completely independent sample. For within-sample prediction, however, the sample has not changed; the future random variable that researchers wish to predict (i.e., a count) relates to the same sample that provided the original (censored) data.

3.2 Single-Cohort Within-Sample Prediction and Plug-in Method

Let be an unordered random sample from a parametric distribution having support on the positive real line and . Under Type \Romannum1 censoring at , the available data may then be expressed by , where is a variable indicating whether is observed before the censoring time , so that the actual observed variables are given as . The observed number of events (uncensored units) in the sample will be denoted by . For a future time , let denote the (future) number of values from , that occur in the interval . The conditional distribution of is then given the observed data , where is the conditional probability that given that . As a function of , we may define by

| (3) |

The goal is to construct a prediction interval for based on the observed data when is unknown. This is referred to as single-cohort within-sample prediction because all the units enter the system at the same time and are homogeneous; and both the data and the predictand are functions of the uncensored random sample .

Let denote an estimator of based on , then a plug-in estimator of the conditional probability follows from (3). Analogous to the bounds in Section 2.1, a plug-in lower prediction bound is defined as

where and are, respectively, the binomial cdf and quantile function. Similarly, the plug-in upper prediction bound for is defined as

Section 2.2 mentioned that asymptotically correct coverage may not generally be possible for prediction intervals involving a discrete predictand. However, for within-sample prediction here, prediction interval methods can be sensibly examined for properties of asymptotic correctness, which we consider in the following section. This is because discreteness in the (conditionally) binomial predictand essentially disappears in large sample sizes , due to normal approximations.

4 The Irregularity of the Within-Sample Prediction

4.1 A Regular Prediction Problem

Under the general prediction framework described in Section 2, the conditional cdf of a predictand given the observed data is often estimated by the plug-in method as (also known as a predictive distribution), where is a consistent estimator of based on . To frame much of the literature related to the plug-in method (Section 2.3), we may define the prediction problem most often commonly related to the plug-in method as “regular” according to the following definition.

Definition 1.

In the notation of Section 2, a prediction problem is called regular if

holds as for any consistent estimator of (i.e., ).

Unlike coverage probability (where exactness may again not be possible for discrete predictands), the above definition reflects the underlying sense of how the plug-in method for prediction intervals is often asymptotically valid for both discrete and continuous predictands. By the nature of many prediction problems (e.g., new sample prediction), the conditional form of cdf may also not necessarily vary with (e.g., ). Hence, in a regular prediction problem, the plug-in predictive distribution (estimated cdf) asymptotically captures the true conditional cdf of the predictand, so that differences are expected to vanish between quantiles of the true predictand and the associated plug-in prediction bounds. Further, when the predictand has a continuous and asymptotically tight conditional distribution (with probability 1), such as when the conditional cdf of the predictand does not vary with , then the plug-in method will be asymptotically correct.

4.2 Failure of the Plug-in Method

This section shows that the within-sample prediction problem described in Section 3 is not regular and that the plug-in method is not asymptotically valid for within-sample prediction. To avoid redundancy, the presentation of results will focus on the plug-in upper prediction bound; the lower bound is analogous by Remark 1 below. In the context of within-sample prediction (cf. Section 3.2), recall that the plug-in upper prediction bound for the future count is defined as

The following theorem shows that the coverage probability of will not correctly converge to as increases.

Theorem 1.

Let denote a random sample from a parametric distribution with cdf (at the true value of ), which is observed under Type I censoring at . Suppose also that , in (3), is continuous at , and that the conditional probability (parametric function) is continuously differentiable in a neighborhood of with non-zero gradient . Based on the censored sample, suppose is an estimator of satisfying , as , for a multivariate normal distribution with mean vector and positive definite variance matrix . Then,

-

1.

The within-sample prediction of fails to be a regular prediction problem: denoting as the conditional cdf of and as its plug-in estimator, then

where is a standard normal variable with cdf , , and

-

2.

The plug-in upper prediction bound generally fails to have asymptotically correct coverage:

where is the sign function and . Furthermore, is a decreasing function of for a given , while is increasing in for , and holds for any .

Remark 1. The lower plug-in bound behaves similarly with in Theorem 1.

The proof of Theorem 1 is in the online supplementary material.

This counter-intuitive result reveals that the plug-in method should not

be used to construct prediction intervals in the within-sample prediction

problem, even if the sample size is large.

The first part of Theorem 1 entails that plug-in estimation

fails to capture the distribution of the predictand here, to the

extent that the supremum difference between estimated and true distributions

has a random limit, rather than converging to zero as in a regular

prediction (cf. Definition 1). As a consequence, the limiting

coverage probability of the plug-in bound turns out to be “off” by an

amount determined by a magnitude of in Theorem 1 (part 2).

For increasing values of , the coverage probability approaches 0.5,

regardless of the nominal coverage level intended.

An intuitive explanation for the failure of plug-in method is that, although converges consistently to , the growing number of Bernoulli trials in offsets the improvements that larger samples may offer in estimation by .

In other words, when standardizing the true quantile,

say , of the (conditionally binomial) predictand ,

one obtains a standard normal quantile

by normal approximation;

however, the same standardization applied to the plug-in bound gives , which differs by a substantial and random amount (having a normal limit itself).

Hence, validity of the plug-in method for within-sample prediction would

require an estimator such that ,

which demands more than what is available from standard -consistency.

5 Prediction Intervals Based on Calibration

5.1 Calibrating Plug-in Prediction Bounds

Cox, (1975) suggested an approximation for improving the plug-in method, which will be described next. Considering the general prediction problem (cf. Section 2.1), suppose a future random variable has a conditional cdf given random sample and is a consistent estimator of from . The coverage probability of the % plug-in upper prediction bound is denoted by , where is generally different from due to the estimation uncertainty in . The basic idea of the calibration method is to find a level so that the coverage probability is equal to (or closer to) . The resulting upper plug-in prediction bound is called the upper calibrated prediction bound. However, determination of relies on both the distribution of and the sampling distribution of , each of which depends on the unknown parameter . So instead, is obtained by solving the equation , where denotes bootstrap probability induced by and by as a bootstrap version of ; for example, may be based on a bootstrap sample found by a parametric bootstrap applied using in the role of the unknown parameter vector . Beran, (1990) showed, that under certain conditions, instead of having a coverage error of , the coverage probability of the calibrated upper prediction bound improves upon the plug-in methods, e.g., . However, such results for the validity of the calibration method cannot be applied directly to within-sample prediction because conditions in Beran, (1990) entail that the prediction problem be regular (cf. Section 4.1), which is not true for the within-sample prediction problem (Theorem 1). Consequently, the issue of asymptotic correctness for the calibration method needs to be determined for within-sample prediction, as next considered.

5.2 The Calibration-Bootstrap Method for the Within-Sample Prediction

The general method in Beran, (1990) is modified to construct a calibrated prediction interval for within-sample prediction and it is called the calibration-bootstrap method in the rest of this paper. For a bootstrap sample with observed events (e.g., from a parametric bootstrap using ), we define a random variable set where is the bootstrap version of and , conditional on .

For the lower prediction bound, the calibrated confidence level is

where is the bootstrap probability induced by , and then the calibrated lower prediction bound is given by . For the upper prediction bound, the calibrated confidence level is

so that the calibrated upper prediction bound is . Here and represent lower and upper plug-in prediction bounds, respectively, as defined in Section 3.2.

The calibration-bootstrap method involves approximating the distribution of with the bootstrap distribution of . The bootstrap distribution of is used to calibrate the plug-in method. The procedure of using the calibration-bootstrap method to construct a prediction interval is described below:

-

1.

Compute the maximum likelihood (ML) estimate using data and the ML estimate .

-

2.

Generate a bootstrap sample and the number of events is denoted by .

-

3.

Compute and using the bootstrap sample .

-

4.

Generate from the distribution and compute .

-

5.

Repeat step 2-4 for times and get realizations of as .

-

6.

Find the and quantiles of , and denote these by and , respectively. The calibrated lower and upper prediction bounds are and .

The pseudo-code for this algorithm is in the online supplementary material.

Next, the calibration-bootstrap method is shown to be asymptotically correct. This requires a mild assumption on the bootstrap involved, namely that the parameter estimators in the bootstrap world provide valid approximations for the sampling distribution of the original data estimators , in large samples. More formally, let denote the probability law of the bootstrap quantity (conditional on the data ) and let denote the probability law of . Let denote the distance between these distributions under any metric that metricizes the topology of weak convergence (e.g., the Prokhorov Metric). Also, in the bootstrap re-creation, the probability that a bootstrap observation is observed before the censoring time should be a consistent estimator of (e.g., would hold as a natural estimator under a parametric bootstrap).

Theorem 2.

Under the conditions of Theorem 1, suppose that and as . Then, the calibrated upper and lower prediction bounds, respectively and have asymptotically correct coverage, that is

The proof is in the online supplementary material. Theorem 2 and its extension in Section 7 guarantee, for example, that the calibration prediction method employed in Escobar and Meeker, (1999), Hong et al., (2009), Hong and Meeker, (2010), and Hong and Meeker, (2013) to construct the prediction intervals for the cumulative number of events is asymptotically correct.

6 Prediction Intervals Based on Predictive Distributions

6.1 Predictive Distributions

Under the general prediction setting in Section 2, recall that the predictive distribution under the plug-in method, given by , provides an estimator of the conditional cdf , of the predictand . Quantiles of this predictive distribution can be associated with prediction bounds for . Generally speaking, any method that leads to a prediction bound for can be translated to a predictive distribution by defining the upper prediction bound as the quantile of the predictive distribution (and vice versa). In this section, the strategy is to construct predictive distributions that lead to prediction bound (or interval) methods having asymptotically correct coverage for within-sample prediction.

For this purpose, it is helpful to consider a Bayesian predictive distribution, defined by

| (4) |

where is a joint posterior distribution for . The quantile of the Bayesian predictive distribution provides the upper Bayesian prediction bound. While this paper does not pursue the Bayesian method, the idea of the Bayesian predictive distribution can nevertheless be used by replacing the posterior in (4) with an alternative distribution over parameters to similarly define non-Bayesian predictive distributions. Harris, (1989) replaced the posterior distribution in (4) with the bootstrap distribution of the parameters to construct a predictive distribution while Wang et al., (2012) replaced the posterior distribution with a fiducial distribution. Shen et al., (2018) proposed a framework for predictive inference by replacing the posterior distribution in (4) with a confidence distribution (CD) and provided theoretical results for this CD-based predictive distribution for the case of a scalar parameter. A CD is a probability distribution that can quantify the uncertainty of an unknown parameter, where both the bootstrap distribution in Harris, (1989) and the fiducial distribution in Wang et al., (2012) can be viewed as CDs; see Xie and Singh, (2013) for a review of these ideas.

To summarize, a predictive distribution can be constructed by using a data-based distribution on the parameter space to replace the posterior distribution in (4). Following this idea, we aim to use draws from a joint probability distribution for the parameters such that the resulting predictive distribution can be used to construct asymptotically correct prediction bounds and intervals for within-sample prediction. In particular, we propose two ways of constructing predictive distributions, extending the framework proposed by Shen et al., (2018) to the within-sample prediction case. In Section 6.2, we describe a prediction method that is based on the bootstrap distribution of the parameters and it is called the direct-bootstrap method in this paper. In Section 6.3, we describe another method that works specifically with the (log)-location-scale family of distributions. This method is inspired by generalized pivotal quantities (GPQ) and involves generating bootstrap samples and it is called the GPQ-bootstrap method.

6.2 The Direct-Bootstrap Method

For within-sample prediction, recall that number of events between the censoring time and a future time , given the Type \Romannum1 censored data , is , where is the number of events observed in and is the conditional probability in (3). The direct-bootstrap method uses the distribution of a bootstrap version of , which is induced by the distribution of estimates from a bootstrap sample , to construct a predictive distribution. Letting denote bootstrap probability (probability induced by a bootstrap sample ), the predictive distribution constructed using direct-bootstrap method is

| (5) |

where are realized bootstrap versions of from independently generated bootstrap samples , and is the number of bootstrap samples. The lower and upper prediction bounds using the direct-bootstrap method are then

| (6) |

6.3 The GPQ-Bootstrap Method

This section focuses on the log-location-scale distribution family and develops another method to construct a predictive distribution through approximate GPQs. Suppose is an i.i.d. random sample from a log-location-scale distribution

| (7) |

where is a known cdf that is free of parameters. For example, if is the standard normal cdf , then has the log-normal distribution.

Hannig et al., (2006) described methods for constructing GPQs and outlined the relationship between GPQs and fiducial inference. Applying these ideas, GPQs can be defined for the parameters in the log-location-scale model as follows. If is a complete or Type II censored independent sample from a log-location-scale distribution, a set of GPQs for under is given by

| (8) |

where denotes an independent copy of the sample , and and denote the ML estimators of computed from and , respectively. These GPQs induce a distribution over the parameter space based on data estimates and, due to the fact that are pivotal quantities based on a complete or Type II censored sample from the log-location-family, the distribution of in (8) can be directly approximated by simulation.

GPQs can also, in some applications, be used to construct confidence intervals when an exact pivot is unavailable. Notice that, while the quantities in (8) are GPQs for log-location-scale family based on complete or Type II censored data, these are no longer GPQs with Type \Romannum1 censored data, where exact GPQs technically fail to exist. This is because the distribution of depends on the unknown event probability before the censoring time under Type \Romannum1 censoring, which applies also to .

However, the formula in (8) can be used to provide a joint approximate GPQ distribution under Type I censoring. Letting denote a bootstrap version of , (8) is extended to define a joint approximate GPQ distribution as the bootstrap distribution of , where

| (9) |

The above definition of also follows by using the bootstrap distribution of to approximate the sampling distribution of and linearly solving for . Then using instead of , a predictive distribution can be defined by using the same procedure that defined the predictive distribution in (5). Namely, by defining a random variable from (3) with a bootstrap distribution induced by , the predictive distribution for using the GPQ-bootstrap method is given by

where are computed from realized bootstrap samples. The lower and upper prediction bounds using GPQ-bootstrap method can be obtained by replacing the predictive distribution with in (6).

6.4 Coverage Probability of the Proposed Methods

This section shows that both the direct-bootstrap method (Section 6.2) and the GPQ-bootstrap method (Section 6.3) produce asymptotically correct prediction bounds/intervals for the future count . Hence, these two methods yield asymptotically valid inference for within-sample prediction of , as does the calibration-bootstrap method (Theorem 2, Section 5), but not by the standard plug-in method (Theorem 1, Section 4).

Theorem 3.

Under the same conditions as Theorem 2,

-

1.

The upper and lower prediction bounds using the direct-bootstrap method, respectively and , have asymptotically correct coverage. That is,

-

2.

If the parametric distribution belongs to the log-location-scale distribution family (7), with standard cdf differentiable on , the upper and lower prediction bounds using the GPQ-bootstrap method, respectively and , have asymptotically correct coverage. That is,

The proof of Theorem 3 is in the online supplementary material.

7 Multiple Cohort Within-Sample Prediction

7.1 Multiple Cohort Data

So far, the focus has been on the within-sample prediction for single-cohort data. Multiple cohort data, however, are more common in applications. In this section, the results from single-cohort data are extended to multiple-cohort data.

In multiple-cohort data (e.g. the bearing cage data of Section 1), units from different cohorts are placed into service at different times. The multiple-cohort data can be seen as a collection of several single-cohort datasets as , where is the number of cohorts and is the number of units in the cohort (sometimes, with no grouping, many cohorts have size 1). Within each cohort , we may express an observation involved as , for , where is a random variable from a parametric distribution , is the censoring time for cohort , and is a random variable indicating whether a unit’s value (e.g., failure time) is less than the censoring time . Given the multiple-cohort data , the number of observed events (e.g., failures) within cohort is defined as , where the total number of units is . The predictand in the multiple-cohort data is the total number of events that will occur in a future time window of length and it is denoted by , where for .

Within each cohort , the number of future events has a binomial distribution. As in Section 3, the conditional distribution of is , where is defined as

Consequently, the predictand has a Poisson-binomial distribution with probability vector and weight vector . We denote this Poisson-binomial distribution by , where the cdf of the Poisson-binomial distribution is denoted by and the quantile function is denoted by ; these functions are available in the poibin R package (described in Hong, (2013)).

If is a consistent estimator of based on the multiple-cohort data , an estimator of conditional probabilities follows by substitution , , similar to the single-cohort case. Then, the plug-in lower and upper prediction bounds for are

Similar to the single-cohort case (Theorem 1), the plug-in method also fails to provide an asymptotically correct coverage probability under multiple-cohort data; see the online supplementary material.

7.2 The Calibration-Bootstrap Method for Multiple Cohort Data

Formulating prediction bounds using the calibration-bootstrap method first requires simulation of bootstrap samples, where each bootstrap sample matches the original data in terms of the number of cohorts as well as their respective sizes and censoring times , . The bootstrap version of the estimator is from each bootstrap sample . Additionally, the number of events (e.g., failures) in the bootstrap sample, grouped by cohort, is , from which we denote a bootstrap future count by based on a weight vector from the bootstrap sample as . The bootstrap variable set is then applied into a Poisson-binomial cdf and then leads to a transformed random variable for deriving calibrated confidence levels and in the same way as in the single-cohort situation. Then, the calibrated lower prediction bound is and the similar upper prediction bound version is .

The calibration-bootstrap method remains asymptotically correct for multiple-cohort within-sample prediction. The multiple-cohort extensions of Theorem 2 and the algorithm are in the online supplementary material.

7.3 The Direct- and GPQ-Bootstrap Methods for Multiple Cohort Data

For multiple-cohort data, constructing prediction bounds for based on the predictive-distribution-based methods also requires bootstrap data and, in particular, the distribution of a bootstrap version of as in Section 7.2. The predictive distribution from the direct-bootstrap method is

| (10) |

where are realized bootstrap versions of across independently generated bootstrap versions of multiple-cohort data (e.g., ). The direct-bootstrap lower and upper prediction bounds for are defined as the modified quantile and quantile of this predictive distribution, respectively, and given by

If belongs to the log-location-scale family as in (7), we use to compute approximate GPQs using (9), and compute where . Then the GPQ-bootstrap method can be implemented to obtain prediction bounds for by replacing with in the definition of the direct-bootstrap predictive distribution (10) and analogously determining prediction bounds from the quantiles of this predictive distribution. The direct- and GPQ-bootstrap methods produce asymptotically correct prediction bounds from multiple-cohort data, and the extension of Theorem 3 is provided in the online supplementary material.

8 A Simulation Study

The purpose of this simulation study is to illustrate agreement for finite sample sizes with the theorems established in the previous sections and to provide insights into the performance of different methods in the case of finite samples. The details and results in this section are for Type \Romannum1 censored single-cohort data. Let the event of interest be the failure of a unit. We simulated Type \Romannum1 censored data using the two-parameter Weibull distribution and compared the coverage probabilities of the prediction bounds based on the plug-in, calibration-bootstrap, direct-bootstrap, and GPQ-bootstrap methods. The Weibull cdf is

with positive scale and shape parameters, and can also be parameterized as

where is the cdf of the standard smallest extreme value distribution with and . The conditions in Theorems 1-3 can be verified for Type I censored Weibull data, so that the Weibull distribution can be used to illustrate all of the aforementioned methods for within-sample prediction (e.g., the ML estimators of the Weibull parameters have sampling distributions with normal limits and can be validly approximated by parametric bootstrap as described in Scholz, (2001)).

8.1 Simulation Setup

The factors for the simulation experiment are (i) , the probability that a unit fails before the censoring time ; (ii) , the expected number of failures at the censoring time , where is the total sample size (i.e., including both the censored and the uncensored observations); (iii) , the probability that a unit fails in a future time interval where ; (iv) , the Weibull shape parameter. Because is a scale parameter, without loss of generality, was used in the simulation. A simulation with all combinations of the following factors levels was conducted: (i) ; (ii) ; (iii) ; (iv) .

For each combination of the these four factors, 90% and 95% upper prediction bounds and 90% and 95% lower prediction bounds were constructed.

The procedure for the simulation is as follows:

-

1.

Simulate =5000 Type \Romannum1 censored samples for each of the factors-level combinations of the four factors.

-

2.

Use ML to estimate parameters in each censored sample.

-

3.

Compute prediction bounds using the different methods for each sample.

-

4.

Compute the conditional (i.e., binomial) coverage probability for each of the prediction bounds.

-

5.

Determine the unconditional coverage probability for each method by averaging the conditional coverage probabilities.

Within each of the =5000 simulated Type I censored samples, =5000 bootstrap samples were generated by parametric bootstrap (i.e., as a random sample from the fitted Weibull distribution with Type I censoring at ) and these samples were used for the calibration-bootstrap method and the two predictive-distribution-based methods. In the simulation, we excluded those samples having fewer than 2 failures to avoid estimability problems, so that all =5000 original samples and all the =25,000,000 bootstrap samples in the simulation have at least 2 failures. The probability of a data sample with fewer than 2 failures for each factor-level combination is given in Table 1.

| E()=5 | E()=15 | E()=25 | E()=35 | E()=45 | |

|---|---|---|---|---|---|

| 0.037 | 0.000 | 0.000 | 0.000 | 0.000 | |

| 0.034 | 0.000 | 0.000 | 0.000 | 0.000 | |

| 0.027 | 0.000 | 0.000 | 0.000 | 0.000 |

8.2 Simulation Results

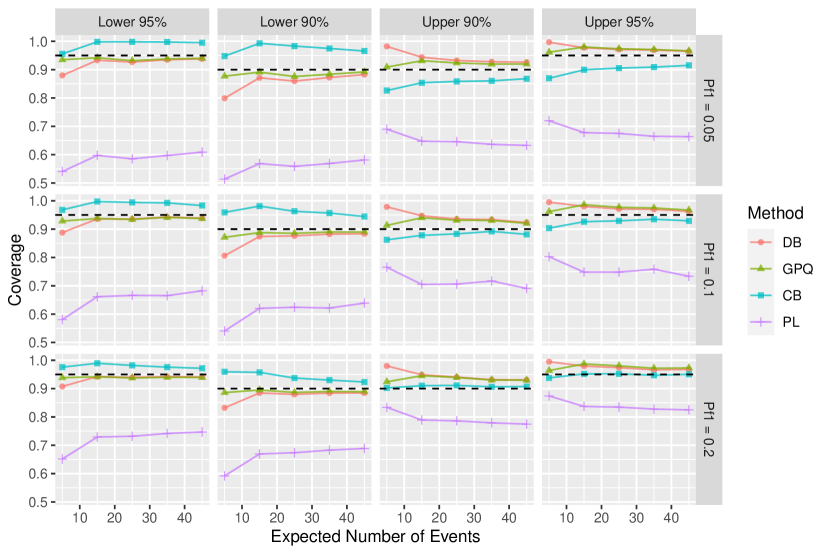

A small subset of the plots displaying the complete simulation results are given here, as the results are generally consistent across the different factor-level combinations. Figure 1 shows the coverage probabilities from plug-in, calibration-bootstrap, direct-bootstrap, and GPQ-bootstrap methods when and . The horizontal dashed line in each subplot represents the nominal confidence level. Plots for the other factor-level combinations are given in the online supplementary material.

Some observations from the simulation results are:

-

1.

The plug-in method fails to have asymptotically correct coverage probability. As decreases, which entails less information or fewer events observed before the censoring time , the coverage probability deviates more from the nominal level.

-

2.

The direct- and GPQ-bootstrap methods are close to each other in terms of coverage probabilities except when . The calibration-bootstrap method differs considerably from the direct- and GPQ-bootstrap methods. The calibration-bootstrap method tends to be more conservative than the other bootstrap-based methods for constructing lower prediction bounds, and also is less conservative for constructing upper prediction bounds.

-

3.

For the lower bounds, the direct- and GPQ-bootstrap methods dominate the calibration-bootstrap method. For the upper bounds, the coverage probabilities of the former two bootstrap-based methods are slightly conservative but still close to the nominal level. The calibration-bootstrap method is better than the direct- and GPQ-bootstrap methods in just a few of these upper bounds.

-

4.

Compared with the calibration-bootstrap method, whose performance is highly related to the level of , the coverage probabilities of the direct- and GPQ-bootstrap methods are insensitive to the level of . As decreases, the lower prediction bound using the calibration-bootstrap method has over-coverage while the upper prediction bound has under-coverage. This implies that under heavy censoring (small ), extremely large sample sizes (or correspondingly large expected number of failing ) are required to attain coverage probabilities close to the nominal confidence level.

From these observations, we can see that the direct- and GPQ-bootstrap methods (i.e., predictive-distribution-based methods) tend to dominate the calibration-bootstrap method in terms of the performance of the prediction bounds, even though all three methods are asymptotically valid. This is because the predictive-distribution-based methods target the one source of parameter uncertainty in the conditional distribution of the predictand (i.e., as addressed by applying bootstrap versions or to “smooth” estimation uncertainty for ), while the number of Bernoulli trials used in these predictive distributions matches that of the predictand. Due to its definition, however, the calibration-bootstrap method involves bootstrap approximation steps (i.e., ) for both the number of failures as well as the binomial probability . The calibration-bootstrap method essentially imposes an approximation for the known number of trials prescribing the predictand . As a consequence, coverages from the calibration-bootstrap method are generally less accurate than those from the predictive-distribution-based methods for within-sample prediction.

9 Application of the Methods

9.1 Examples

Product-A Data: The ML estimates of the Weibull shape and scale parameters are and , respectively, based on 80 failure times among 10,000 units before 48 months. Then, for the 9920 surviving units, the ML estimate of the probability that a unit will fail between 48 and 60 months of age is Using the ML estimates of the Weibull parameters , we simulate 10,000 bootstrap samples that are censored at 48 months and obtain ML estimates of from each bootstrap sample. Based on applying these with each interval method, Table 2 gives prediction bounds for the number of failures in the next 12 months. As indicated by our results, even with a large number of failures, the plug-in method intervals can be expected to be off and are too narrow compared to the other bounds.

| Confidence Level | Bound Type | Plug-in | Direct | GPQ | Calibration |

|---|---|---|---|---|---|

| 95% | Lower | 23 | 20 | 20 | 20 |

| 90% | Lower | 25 | 23 | 23 | 23 |

| 90% | Upper | 39 | 43 | 43 | 43 |

| 95% | Upper | 42 | 47 | 47 | 46 |

Heat Exchanger Data: In this example, there are no exact failure times in the data. That is, the data here contain limited information as there were only 8 failures among 20,000 exchanger tubes that were inspected (in censored data analysis, the informational content of data is closely related to the number of failures) and these failure times are interval-censored (not exact). The likelihood function under a Weibull model for the heat exchanger data is

resulting in ML estimates and . The conditional probability of a tube failing between the third and tenth year, given that tube has not failed at the end of the third year, is then estimated as .

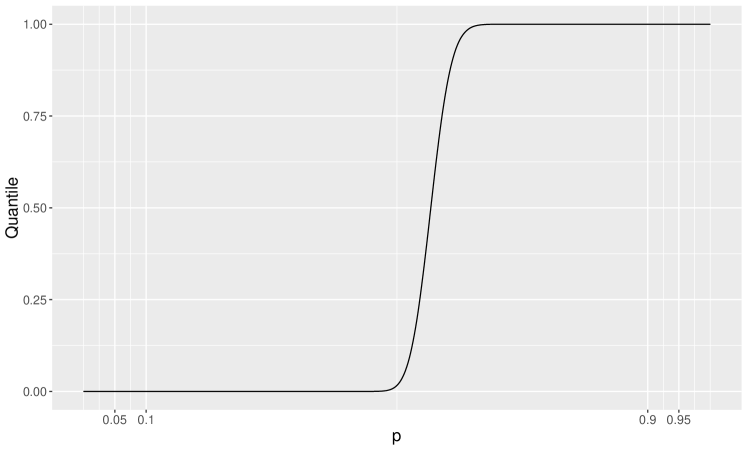

The ML estimates from 10,000 bootstrap samples (parametric bootstrap with censoring at 3 years) are used in the calibration-bootstrap and two predictive-distribution-based methods. However, the calibration-bootstrap method exhibits numerical instabilities with these data due to the small number of failures. To illustrate, Figure 2 shows the approximate quantile function of used in the calibration-bootstrap method, involving the evaluation of a random variable in its cdf , given the number of failures and the estimate from a bootstrap sample. This quantile function is also the calibration curve, where the x-axis gives the desired confidence level , while the y-axis gives the corresponding calibrated confidence level ( or ) to be used for determining plug-in prediction bounds (or quantiles from a distribution). From Figure 2, we can see that the and quantiles nearly equal while the and quantiles nearly equal 1. This creates complications in computing the prediction bounds, for example, as there is numerical instability near the 100% quantile of the distribution. Consequently, 90% and 95% bounds from the calibration-bootstrap method are computationally not available (NA).

| Confidence Level | Bound Type | Plug-in | Direct | GPQ | Calibration |

|---|---|---|---|---|---|

| 95% | Lower | 138 | 28 | 23 | NA |

| 90% | Lower | 142 | 43 | 34 | NA |

| 90% | Upper | 176 | 1627 | 888 | NA |

| 95% | Upper | 180 | 4343 | 1890 | NA |

Table 3 instead provides prediction bounds from the plug-in and direct- and GPQ-bootstrap methods. The plug-in prediction bounds differ substantially from the two bootstrap-based methods. Unlike the previous example (Product A data), the direct- and GPQ-bootstrap methods also differ appreciably based on the limited failure information with the heat exchanger data; we return to explore such differences in Section 9.2. The upper bounds involve a large amount of extrapolation and may not be practically meaningful other than to warn that there is a huge amount of uncertainty in the 10-year predictions.

Bearing Cage Data: In this example, staggered entry data containing multiple cohorts are considered. Table 4 gives the prediction bounds for the bearing cage dataset using 10,000 bootstrap samples. While similar in spirit to the Product-A example, the predictand here differs by having a Poisson-binomial distribution. The latter can be computed with the R package poibin, which is applied to construct prediction bounds using methods described in Section 7.2. Table 4 gives the resulting prediction bounds for the bearing cage dataset.

| Confidence Level | Bound Type | Plug-in | Direct | GPQ | Calibration |

|---|---|---|---|---|---|

| 95% | Lower | 2 | 1 | 1 | 1 |

| 90% | Lower | 2 | 2 | 2 | 2 |

| 90% | Upper | 8 | 10 | 13 | 10 |

| 95% | Upper | 9 | 12 | 20 | 12 |

9.2 Comparing the Direct- and GPQ-Bootstrap Methods

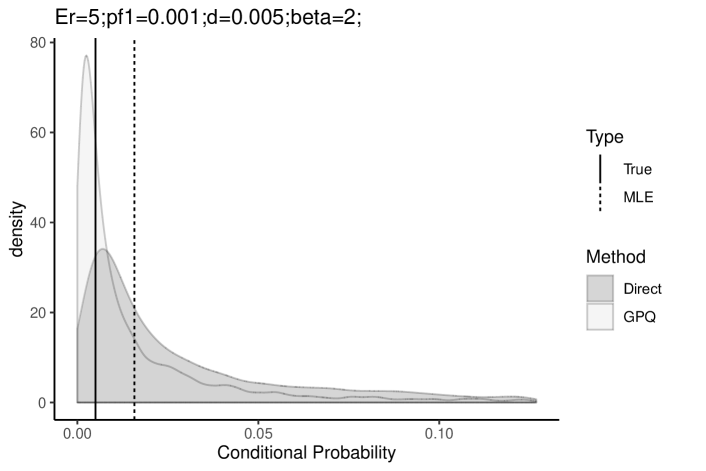

In the heat exchanger example, the prediction bounds obtained from the direct- and GPQ-bootstrap methods appear very different. This motivates us to investigate the cause of such differences in similar prediction applications involving limited information.

A general simulation setting is first described for mimicking the heat exchanger data. The heat exchanger data has two important features in that the number of events is small (i.e., 8) and so is the proportion of observed events (i.e., 0.004). Hence, in the simulation, the expected number of events is set to 5 while the proportion failing is 0.001, with a Weibull shape parameter and scale parameter . Different levels of are used for the probability of events in the forecast window. The simulation results (available in the online supplementary material) reveal that, overall, the GPQ-bootstrap method has better coverage probability than the direct-bootstrap method in this simulation setting. For the upper prediction bound, the direct-bootstrap method is generally more conservative than the GPQ-bootstrap method in terms of coverage probability, indicating that upper prediction bounds from the direct-bootstrap method are larger than the GPQ counterparts. On the other hand, the lower bound based on the direct-bootstrap method generally tends to have under-coverage compared to the GPQ-bootstrap method, suggesting also larger lower bounds from the direct-bootstrap method relative to the GPQ-bootstrap method. These patterns in the prediction bounds (i.e., with larger direct-bootstrap bounds compared to those from the GPQ-bootstrap in a setting of a limited number of events) are consistent with the prediction bounds found from the heat exchanger example.

To further illustrate, Figure 3 shows the bootstrap distributions of and from a single Monte Carlo sample that represents the typical behavior found in this simulation setting: values of used in the predictive distribution of GPQ-bootstrap method tend to be smaller and more concentrated than the values used in the direct-bootstrap predictive distribution. Note that direct- and GPQ-bootstrap predictive distributions are approximated by and , respectively, and that direct- and GPQ-bootstrap prediction bounds correspond to quantiles from these predictive distributions. Consequently, because and are small (e.g., less than 0.25) while is generally larger than in Figure 3, then is generally smaller than , implying quantiles from can be expected to exceed those from in data cases with a limited number of events. However, asymptotically, both and are similarly normally distributed and symmetric around (shown in online supplementary material), so that the direct- and GPQ-bootstrap prediction bounds may be expected to behave alike in data situations with a larger number of events and larger sample sizes, as seen in Figure 1 (and in the Product A application).

10 Choice of a Distribution

Extrapolation is usually required when predicting the number of future events based on an on-going time-to-event process. For example, it may be necessary to predict the number of returns in a three-year warranty period based on field data for the first year of operation of a product. An exception arises when life can be modeled in terms of use (as opposed to time in service) and there is much variability in use rates among units in the population. The high-use units will fail early and provide good information about the upper tail of the amount-of-use return-time distribution (e.g., Hong and Meeker, (2010)).

When extrapolation is required, predictions can be strongly dependent on the distribution choice. In most applications, especially with heavy censoring, there is little or no useful information in the data to help choose a distribution. Then, for example, it is best to choose a failure-time distribution based on knowledge of the failure mechanism and the related physics/chemistry of failure. In important applications, this would be typically be done by consulting with experts who have such knowledge.

For example, the lognormal distribution could be justified for failure times that arise from the product of a large number of small, approximately independent positive random quantities. Examples include failure from crack initiation and growth due to cyclic stressing of metal components (e.g., in aircraft engines) and chemical degradation like corrosion (e.g., in microelectronics). These are two common applications where the lognormal distribution is often used. Gnedenko et al., (1969, pages 36-37) provide mathematical justification for this physical/chemical motivation.

|

|

|

|

|

|

Based on extreme value theory, the Weibull distribution can be used to model the distribution of the minimum of a large number of approximately iid positive random variables from certain classes of distributions. For example, the Weibull distribution may provide a suitable model for the time to first failure of a large number of similar components in a system. Consider a chain with many nominally identical links and suppose that the chain is subjected cyclic stresses over time. As suggested in the previous paragraph, the number of cycles to failure for each link could be described adequately with a lognormal distribution. The chain, however, fails when the first link fails. The limiting distribution of (properly standardized) minima of iid lognormal random variables is a type 1 smallest extreme value (or Gumbel) distribution. For all practical purposes, however, the Weibull distribution provides a better approximation. For further information on this result from the penultimate theory of extreme values, see Green, (1976), Castillo, (1988, Section 3.11), and Gomes and de Haan, (1999). Similarly, if failures are driven by the maximum of a large number of approximately iid positive random variables, a Fréchet distribution would be suggested. The reciprocal of a Weibull random variable has a Fréchet distribution.

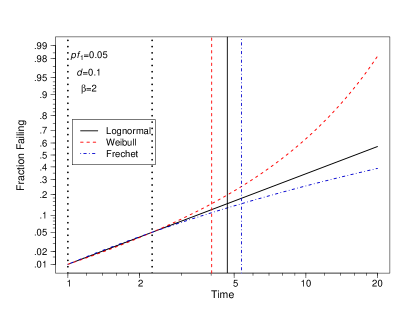

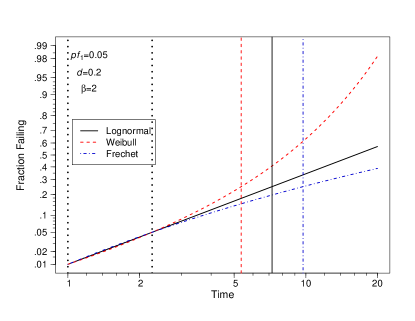

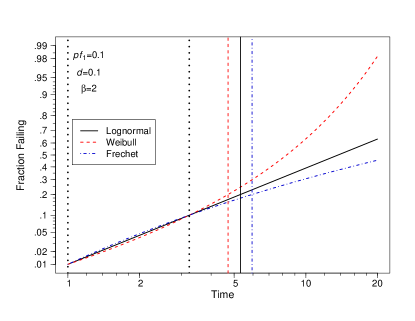

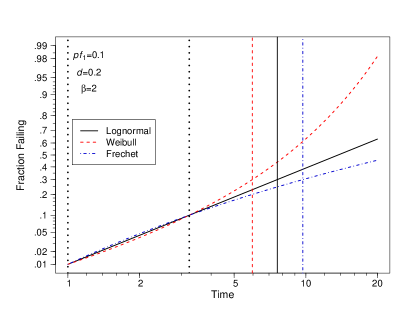

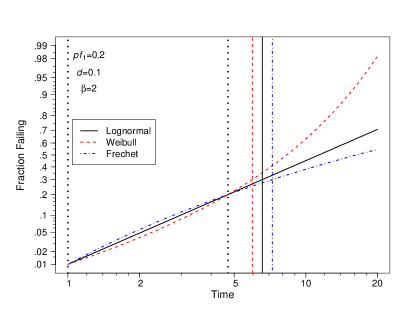

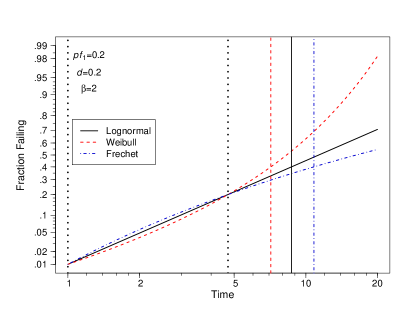

Of course, choosing a distribution based on failure-mechanism knowledge is not always possible. The alternative is to do sensitivity analyses, using different distributions. Figure 4 provides a comparison of the Weibull, lognormal, and Fréchet cdfs where the Weibull distribution was chosen with a shape parameter and the other factor level combinations of and used in the Section 8 simulation. The scale parameter is determined by letting the 0.01 Weibull quantile be 1. The cdfs are plotted on lognormal probability scales where the lognormal cdf is a straight line. The particular parameters for the lognormal and Fréchet distributions were chosen such that the distributions cross at the 0.01 and quantiles, simulating the range of the data where the agreement among distributions will be good. Similar plots for and are provided in the online supplementary material. The Weibull distribution is always more pessimistic (conservative) than the lognormal and the Fréchet is always more optimistic than the lognormal. For example, if the true distribution is Weibull but lognormal distribution is used to fit the data, the prediction intervals, regardless of the method, will underpredict the number of events. When in doubt, the Weibull distribution is often used because it is the conservative choice.

11 Concluding Remarks

This paper studies the problem of predicting the future number of events based on censored time-to-event data (e.g., failure times). This type of prediction is known as within-sample prediction. A regular prediction problem is defined for which standard plug-in estimation commonly applies, and it is shown that the within-sample prediction is not regular and that the plug-in method fails to produce asymptotically valid prediction bounds. The irregularity of within-sample prediction and the failure of the plug-in method motivated the study of the calibration method as an alternative approach for prediction bounds, though the previously established theory for calibration bounds does not apply to within-sample prediction. The calibration method is implemented via bootstrap and called calibration-bootstrap method, which is proved to be asymptotically correct (i.e., producing prediction bounds with asymptotically correct coverage). Then, turning to formulations of a predictive distribution, we study and validate two other methods to obtain prediction bounds, namely the direct-bootstrap and GPQ-bootstrap methods. All prediction methods considered can be applied to both single-cohort and multiple-cohort data.

While theoretical results show that the calibration-bootstrap method and the two predictive-distribution-based methods are all asymptotically correct, the simulation study shows that the direct-bootstrap and GPQ-bootstrap methods outperform the calibration-bootstrap method in terms of coverage probability accuracy relative to a nominal coverage level. The two predictive-distribution-based methods are also easier to implement compared to the calibration-bootstrap method, and can also be computationally more stable (e.g., heat exchanger data example). Thus, we recommend predictive distribution methods, especially the direct-bootstrap method for general applications involving within-sample prediction.

In this paper, all of the units in the population were assumed to have the same time-to-event distributions. In many applications, however, units are exposed to different operating or environmental conditions, resulting in different time-to-event distributions. For example, during 1996-2000, the Firestone tires installed on Ford Explorer SUVs experienced unusually high rates of failure, where problems first arose in Saudi Arabia, Qatar, and Kuwait because of the high temperatures in those countries (see National Highway Traffic Safety Administration, (2001)). Having prediction intervals that use covariate information (like temperature and moisture) could be useful for manufacturers and regulators in making decisions about a possible product recall, for example. Similarly, there can be seasonality effects in time-to-event processes and within-sample predictions.

The methods described in this paper can be extended to handle either constant covariates or time-varying covariates. Using calibration-bootstrap methods, Hong et al., (2009) used constant covariates to predict power-transformer failures. Despite the complicated nature of their data (random right censoring and truncation and combinations of categorical covariates with small counts in some cells), Hong et al., (2009) were able to use the fractional random-weight method (e.g., Xu et al.,, 2020) to generate bootstrap estimates. Shan et al., (2020) used time-varying covariates to account for seasonality in two different warranty prediction applications. As mentioned by one of the referees, if there is seasonality and data from only part of one year is available, there is a difficulty. In such cases, it would be necessary to use past data on a similar process to provide information about the seasonality.

Covariate information in reliability field data has not been common, but that is changing, due to a reduction in costs and advances and in sensor, communications, and storage technology. In the future, much more covariate information on various system operating/environmental variables will be available to make better predictions, as described in Meeker and Hong, (2014).

Acknowledgments

We would like to thanks Luis A. Escobar for helpful comments on this paper. We are also grateful to the editorial staff, including two reviewers, for helpful comments that improved the manuscript. Research was partially supported by NSF DMS-2015390.

References

- Abernethy et al., (1983) Abernethy, R., Breneman, J., Medlin, C., and Reinman, G. (1983). Weibull Analysis Handbook. Wright-Patterson AFB, Ohio 45433. Available at https://apps.dtic.mil/dtic/tr/fulltext/u2/a143100.pdf. Last accessed on March 3, 2020.

- Aitchison, (1975) Aitchison, J. (1975). Goodness of prediction fit. Biometrika, 62:547–554.

- Atwood, (1984) Atwood, C. L. (1984). Approximate tolerance intervals, based on maximum likelihood estimates. Journal of the American Statistical Association, 79:459–465.

- Barndorff-Nielsen and Cox, (1996) Barndorff-Nielsen, O. E. and Cox, D. R. (1996). Prediction and asymptotics. Bernoulli, 2:319–340.

- Beran, (1990) Beran, R. (1990). Calibrating prediction regions. Journal of the American Statistical Association, 85:715–723.

- Castillo, (1988) Castillo, E. (1988). Extreme Value Theory in Engineering (Statistical Modeling and Decision Science). Academic Press.

- Cox, (1975) Cox, D. R. (1975). Prediction intervals and empirical Bayes confidence intervals. Journal of Applied Probability, 12:47–55.

- Davison, (1986) Davison, A. C. (1986). Approximate predictive likelihood. Biometrika, 73:323–332.

- Escobar and Meeker, (1999) Escobar, L. A. and Meeker, W. Q. (1999). Statistical prediction based on censored life data. Technometrics, 41:113–124.

- Fonseca et al., (2012) Fonseca, G., Giummolè, F., and Vidoni, P. (2012). Calibrating predictive distributions. Journal of Statistical Computation and Simulation, 84:373–383.

- Gnedenko et al., (1969) Gnedenko, B. V., Belyayev, Y. K., and Solovyev, A. D. (1969). Mathematical methods of reliability theory. Academic Press.

- Gomes and de Haan, (1999) Gomes, M. I. and de Haan, L. (1999). Approximation by penultimate extreme value distributions. Extremes, 2:71–85.

- Green, (1976) Green, R. F. (1976). Partial attraction of maxima. Journal of Applied Probability, 13:159–163.

- Hall et al., (1999) Hall, P., Peng, L., and Tajvidi, N. (1999). On prediction intervals based on predictive likelihood or bootstrap methods. Biometrika, 86:871–880.

- Hannig et al., (2006) Hannig, J., Iyer, H., and Patterson, P. (2006). Fiducial generalized confidence intervals. Journal of the American Statistical Association, 101:254–269.

- Harris, (1989) Harris, I. R. (1989). Predictive fit for natural exponential families. Biometrika, 76:675–684.

- Hong, (2013) Hong, Y. (2013). On computing the distribution function for the Poisson-binomial distribution. Computational Statistics and Data Analysis, 59:41–51.

- Hong and Meeker, (2010) Hong, Y. and Meeker, W. Q. (2010). Field-failure and warranty prediction based on auxiliary use-rate information. Technometrics, 52:148–159.

- Hong and Meeker, (2013) Hong, Y. and Meeker, W. Q. (2013). Field-failure predictions based on failure-time data with dynamic covariate information. Technometrics, 55:135–149.

- Hong et al., (2009) Hong, Y., Meeker, W. Q., and McCalley, J. D. (2009). Prediction of remaining life of power transformers based on left truncated and right censored lifetime data. The Annals of Applied Statistics, 3:857–879.

- Lawless and Fredette, (2005) Lawless, J. F. and Fredette, M. (2005). Frequentist prediction intervals and predictive distributions. Biometrika, 92:529–542.

- Meeker and Hong, (2014) Meeker, W. Q. and Hong, Y. (2014). Reliability meets big data: opportunities and challenges. Quality Engineering, 26:102–116.

- National Highway Traffic Safety Administration, (2001) National Highway Traffic Safety Administration (2001). Engineering analysis report and initial decision regarding EA00-023: Firestone Wilderness AT Tires. Washington, DC: US Department of Transportation. Available at https://icsw.nhtsa.gov/nhtsa/announce/press/Firestone/firestonesummary.html. Last accessed on March 3, 2020.

- Nelson, (2000) Nelson, W. (2000). Weibull prediction of a future number of failures. Quality and Reliability Engineering International, 16:23–26.

- Scholz, (2001) Scholz, F. (2001). Maximum likelihood estimation for Type I censored Weibull data including covariates. In ISSTECH-96-022, Boeing Information & Support Services, PO Box 24346, MS-7L-22. Available at http://faculty.washington.edu/fscholz/DATAFILES498B2008/ISSTECH-96-022.pdf. Last accessed on August 3, 2020.

- Shan et al., (2020) Shan, Q., Hong, Y., and Meeker, W. Q. (2020). Seasonal warranty prediction based on recurrent event data. Annals of Applied Statistics, 14:929–955.

- Shen et al., (2018) Shen, J., Liu, R. Y., and Xie, M.-G. (2018). Prediction with confidence—a general framework for predictive inference. Journal of Statistical Planning and Inference, 195:126–140.

- Wang et al., (2012) Wang, C., Hannig, J., and Iyer, H. K. (2012). Fiducial prediction intervals. Journal of Statistical Planning and Inference, 142:1980–1990.

- Xie and Singh, (2013) Xie, M.-G. and Singh, K. (2013). Confidence distribution, the frequentist distribution estimator of a parameter: A review. International Statistical Review, 81:3–39.

- Xu et al., (2020) Xu, L., Gotwalt, C., Hong, Y., King, C. B., and Meeker, W. Q. (2020). Applications of the fractional-random-weight bootstrap. The American Statistician. https://doi.org/10.1080/00031305.2020.1731599.