Weak convergence of the intersection point process of Poisson hyperplanes

Abstract

This paper deals with the intersection point process of a stationary and isotropic Poisson hyperplane process in of intensity , where only hyperplanes that intersect a centred ball of radius are considered. Taking it is shown that this point process converges in distribution, as , to a Poisson point process on whose intensity measure has power-law density proportional to with respect to the Lebesgue measure. A bound on the speed of convergence in terms of the Kantorovich-Rubinstein distance is provided as well. In the background is a general functional Poisson approximation theorem on abstract Poisson spaces. Implications on the weak convergence of the convex hull of the intersection point process and the convergence of its -vector are also discussed, disproving and correcting thereby a conjecture of Devroye and Toussaint [J. Algorithms 14.3 (1993), 381–394] in computational geometry.

Keywords. Convex hull, integral geometry, intersection point process, Poisson hyperplane process, Poisson point process approximation, rate of convergence, weak convergence.

MSC. Primary 60D05, 60F05; Secondary 52A22, 53C65.

1 Introduction

The mathematical analysis of Poisson point processes of hyperplanes in () and the resulting random tessellations has a long tradition in stochastic geometry, see, for example, [25, 29, 30] and the many references given therein. A large number of mean value formulas and relations are known explicitly and in the last decade also a comprehensive second-order and central limit theory for a variety of geometric functionals associated with such Poisson hyperplane tessellations has been developed, see [24, 10, 12, 11, 27] and also Remark 5.8 below.

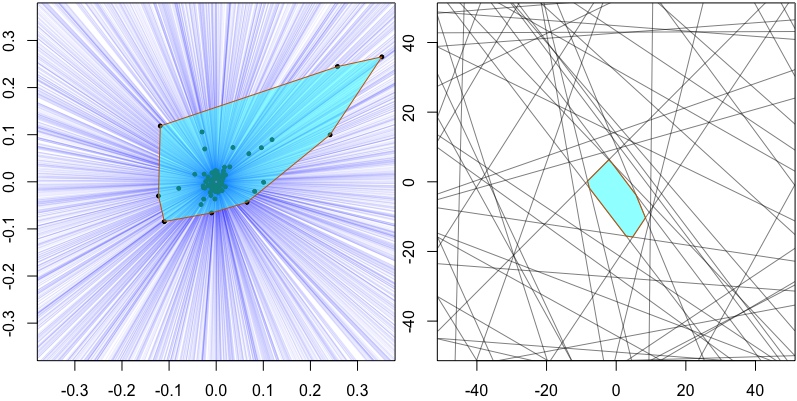

The problem we are dealing with in this paper is motivated by an observation known in the area of computational geometry: An arrangement of lines chosen at random from has a vertex set whose convex hull has an absolutely bounded expected vertex number, see [3, 8, 9]. We refer the reader to the introduction of [3] for an explanation on how this fact improves the average algorithmic complexity for the computation of the convex hull of such vertex sets. In [8] it is conjectured that the expected vertex number tends to , as the number of random lines goes to infinity. Our results can be considered as a variation and extension of this theme in a number of different directions. To describe them, we start by considering for an arbitrary space dimension an arrangement of random hyperplanes in driven by a stationary and isotropic Poisson point process on the space of hyperplanes having intensity . This gives rise to an infinite collection of random hyperplanes and the convex hull of the associated random set of intersection points almost surely coincides with . Therefore, in a next step, we apply a thinning procedure to the Poisson process and we only keep those hyperplanes which intersect a ball of radius centred at the origin. This leaves us with an almost surely finite collection of random hyperplanes in in general position. In particular, any -tuple of the remaining distinct hyperplanes intersects in a randomly located point in . By we denote the random point process of all such intersection points, see Figure 1 for illustrations and simulations. The convex hull of is a random polytope in whose description is in the focus of our attention and whose analysis is motivated by [3, 8, 9, 1, 6]. Our main result is a quantitative limit theorem for the point process itself, as and where is a suitable function of . As it turns out, if we choose then converges in distribution to a non-trivial limiting point process, namely a Poisson point process in whose intensity measure has the power-law density with respect to the Lebesgue measure and where is a constant only depending on the dimension (for example, ). Formally, our main result reads as follows.

Main Theorem (Theorem 5.3).

Let be the intersection point process and be the Poisson point process as introduced above. Then, taking , we have that converges to in distribution (on the space of point process in supplied with the vague topology), as .

As a particular feature, we will derive an upper bound on the speed of convergence in this limit theorem, which is measured in terms of the famous Kantorovich-Rubinstein optimal transportation distance. Moreover, this convergence together with a continuous-mapping-type result implies that the convex hull of converges in distribution to the convex hull of on the space of convex bodies in supplied with the Hausdorff distance. We will also conclude from this the convergence in distribution of the number of -dimensional faces for any . We argue that in dimension , for example, the expected number of vertices cannot converge to a constant smaller than , disproving and correcting thereby the aforementioned conjecture from [8].

We would like to emphasize that Poisson point processes in with a power-law density function, such as the one appearing in the definition of , and their convex hulls have recently been intensively investigated and are closely connected with (asymptotic) geometric and probabilistic description of several well known objects in stochastic geometry. As concrete examples we mention the Poisson zero polytope, the typical Poisson-Voronoi cell, random convex hulls of independent random points in convex bodies with smooth boundary, spherical random polytopes on half-spheres or Poisson-Voronoi tessellations in spherical spaces. Our paper adds another item to this list and underlines once again the outstanding role in stochastic geometry of Poisson point processes with a power-law density function and their convex hulls, see [19, 21, 17, 18, 20].

In order to prove the results outlined above, we have to bring together a number of different technical tools and devices. To show the convergence of the intersection point process to the Poisson point process we make use of an abstract functional Poisson limit theorem which has been developed in [7] in the framework of the Malliavin-Stein technique on abstract Poisson spaces. It is this device, which delivers the rate of convergence measured in the Kantorovich-Rubinstein for point processes. Beside the convergence of the intensity measures of the involved point processes, this approach also requires control over a number of auxiliary integral expressions. Their analysis constitutes the most technical part of this paper and requires an extensive use of integral-geometric transformation formulas of Blaschke-Petkantschin type in combination with asymptotic expansions of integrals having a geometric flavour. This also results in a higher-dimensional asymptotic version of Huygen’s principle

The remaining parts of this paper are structured as follows. In Section 2 we recall some preliminaries, mainly related to Grassmannians and integral geometry. We also formally introduce there the Poisson hyperplane process and its intersection point process, which are the main objects we deal with in this paper. Section 3 contains a number of preparatory lemmas, which are of more technical nature, but which are essential in the proof of our main result. The convergence of the intensity measure of the intersection point process is derived in Section 4 on the basis of the material developed in the previous section. In Section 5 we prove our quantitative limit theorem for the intersection point process and discuss implications to the convergence of its convex hull. Also, we elaborate there on the implication of our results to the conjecture of Devroye and Toussaint from [8].

2 Notation and preliminaries

2.1 General notation, linear and affine Grassmanians

In this article we work in the -dimensional Euclidean space , . It is equipped with the usual topology and Lebesgue measure. We consider the standard scalar product and norm , and denote by and the orthogonal spaces of a vector and a flat .

The unit ball and sphere (centred at the origin) are denoted by and , respectively. A ball centred at the origin and of radius is denoted by . The (Lebesgue) volume of and surface area of are given by

The spherical Lebesgue measure on is denoted by . We use the convention to add the dimension of the sphere as an index when we consider the spherical Lebesgue measure on a lower dimensional unit sphere. For example we denote by the spherical Lebesgue measure on the -dimensional sphere , where is a -dimensional linear subspace. We use the notation to indicate the restriction of a measure to a (measurable) set .

For , the linear (resp. affine) Grassmanian (resp. ) is the space of all -dimensional linear (resp. affine) subspaces of . These spaces are endowed with their usual topologies and Haar measures (resp. ), normalised as in [29]. Let be integers, and . We introduce the following notation for spaces of linear or affine spaces which contain or are contained in or :

These spaces are again equipped with the usual topologies and relative Haar measures , , and , see [29, Chapter 7.1].

For real-valued functions and , we use the standard Landau notation which means that there exists a positive constant such that for all .

The constants in this paper might depend on the space dimension , but on nothing else. Their value may change from occurrence to occurrence.

2.2 An integral-geometric transformation formula

In the present article we often have to deal with multivariate integrals over the Grassmannians or relative Grassmannians we introduced in the previous section. Such integrals can usually be evaluated or simplified by applying suitable integral-geometric transformation formulas, which can be found in [29], for example.

A special case of the affine Blaschke-Petkantschin formula [29, Theorem 7.2.8] says that for any and any non-negative measurable function , we have

| (2.1) |

where

is a constant depending only on and , and is the so-called subspace determinant, which can be defined as the -dimensional Lebesgue volume of the parallelepiped spanned by , where for each , is one of the two unit normal vectors of (arbitrarily chosen).

As the definition of the subspace determinant above suggests, it is sometime more convenient to work with the normal vectors of hyperplances rather than the hyperplanes themselves. In this spirit, the following formula is quite useful. For any non-negative measurable function ,

| (2.2) |

2.3 Poisson hyperplane processes and derived point processes

We denote by , , a stationary and isotropic Poisson hyperplane process of intensity , i.e., a Poisson point process on with intensity measure , see [23, 29] for formal definitions. Furthermore, we denote by the restriction of to the set of hyperplanes that intersect the ball of radius . Almost surely the hyperplanes of this process are in general position, meaning that the intersection of any of them has codimension , for any . In this paper, and in particular in the next definition, we assume that all realisations of the underlying hyperplane process satisfy this condition. We are interested in the intersection point process induced by , which is defined by

| (2.3) |

where is the set of all -tuple of distinct hyperplanes of . Note that almost surely the intersections in (2.3) are single points. Applying the multivariate Mecke formula [23, Theorem 4.4] we see that the intensity measure of the intersection point process is

| (2.4) |

where

is a shorthand notation for the set of hyperplanes intersecting the ball .

3 Preparatory lemmas

3.1 Intersection of a fixed affine flat with a random linear subspace

The Cauchy distribution on with density

is known to arise as the distribution of the intersection point in the plane between the -axis and a random line passing through the point with coordinates and with direction uniformly distributed (Huygen’s principle). In this paper some computations involve a very similar quantity, namely the norm of the intersection point between a random -dimensional linear space and a fixed affine flat of complementary dimension . The next lemma provides its distribution. In this lemma we represent random linear subspaces (resp. flats) as fixed linear subspaces (resp. flats) on which we apply a random rotation.

Lemma 3.1.

Let , and be fixed. Denote by the distance between the origin and the flat . Let be a uniformly distributed random rotation, i.e., a rotation distributed according to the Haar probability measure on the compact topological group . Then, denoting by equality in distribution, we have that

and the density of both random variables is given by

| (3.1) |

In particular, for ,

| (3.2) |

Proof.

The first statement is trivial since

and has the same distribution as .

Let us denote by the -dimensional linear space spanned by . Now, we make two observations which will be used for a ‘dimension reduction argument’. First

and second, for any non-negative measurable function , one has that

The first equality is a simple consequence of the rotation invariance of the Haar measures on and on , and the fact that the intersection of linear spaces of dimensions and has dimension one, whenever the two spaces are in general position. The second equality is a parametrisation of . Therefore we can ‘reduce the ambient space’ in the following way:

Decompose the affine flat into a sum , where is translated by a vector . An elementary geometric analysis in the right-angled triangle with vertices the origin, and leads to

and therefore we obtain

This is the normalised -dimensional volume of a certain neighborhood of the great subsphere of the sphere . If , this neighborhood is the full sphere and thus the probability is in that case. Otherwise, it is some kind of ‘slightly bent’ cylinder of height . With the slice integration formula [2, Corollary A.5] this is

Taking the derivative with respect to of the last expression provides the density (3.1) and bounding by proves the estimate (3.2). ∎

3.2 Another preparation

The next lemma is a significant ingredient for computation in the next section.

Lemma 3.2.

Let , , . Consider the function defined by

Then, if we denote by the distance between the origin a flat , we have that

-

1.

the value is a function of the ratio ,

-

2.

and

where the constants , , depend only on the dimension difference and , and the constant involved in bounding the big term depends only on , and .

Remark 3.3.

Proof.

In this proof we will drop the indices , and appearing in and write only instead. Also we define and to be, respectively, the -dimensional linear subspace parallel to and the orthogonal projection of the origin onto . In particular and .

Let be an arbitrary rotation and . By considering the substitutions , , we see that . In particular, by taking , we see that the first claim of the lemma holds.

The rest of the proof is dedicated to show the second claim. First, we represent the affine hyperplanes , , as sums , where the ’s are the linear hyperplanes parallel to the ’s. Note that through this rewriting we can replace the subspace determinant in the definition of by , since it is invariant under translations of its components. Also we recall that, by definition, . We get

| (3.3) | ||||

Next, we parametrise the hyperplanes by their unit orthonormal vectors . By duality these vectors belong to . Indeed, for any of the ’s, the corresponding orthogonal hyperplanes contain . More precisely, we use the transformation

which holds for any non-negative measurable function and follows from the invariance and uniqueness of the Haar measure on similarly to (2.2). Iterating this formula over the -fold integral in (3.3) and using the fact that

we get

Now, we will simplify the indicator functions. For this we observe that a hyperplane of the form can be written as . Indeed, these two expressions represent the same hyperplane characterised by being parallel to and containing the point . It makes clear that such a hyperplane intersects the ball if and only if the scalar product is between and . Therefore,

| (3.4) | ||||

At this point, we split the proof by considering whether (easy part) or (more intricate part).

Case where :

Thanks to the Cauchy-Schwarz inequality we see that, in this case, the conditions in the indicator functions in (3.4) are always satisfied and therefore

| (3.5) |

The later expression is a constant which depends only on and , and therefore the lemma is proved for the case where .

Case where :

Now we will adapt the slice integration formula [2, Corollary A.5] to transform integrals over the -dimensional unit sphere of the space into integrals over the -dimensional slices obtained by cutting that sphere by hyperplanes parallel to . In this set-up, the slice integration formula can be written as

for any non-negative measurable function . Iterating this formula over the -fold integral in (3.4), we get

We will now simplify the condition in the indicator functions. Using that, for any , the vectors and are orthogonal, we see that

and thus we get the simplification

Since we are in the case where , we have that the interval is a subset of and therefore we can pass the lately discussed conditions into the domain of the outer integral as follows:

In the next step we apply for each the linear substitution which have the effect of bringing the integration domain of the outer integral back to the unit cube , i.e.,

Using that the vectors ’s are orthogonal to and multilinearity we can take out of the subspace determinant the factor , which appears in front of each term . This gives the equality

In the final part of this proof we will approximate the product and subspace determinant above by terms independent from and , and bound the approximation error in terms of the ratio . This will eventually allow us to conclude the proof.

Since in the last integral the variables all belong to the bounded interval , we have that the product is arbitrarily close to as long as the ratio is small enough. More precisely one can check that

where the constant in the big term is a bounded positive number depending only on and .

Similarly as above we have that, for ,

In particular, for any given ’s and ’s the subspace determinant in the last integral tends to , as the ratio goes to . We still need to bound the error involved in this approximation. To do this we observe that the (subspace) determinant is a locally Lipschitz function and that each of the involved vectors belong to the bounded cylinder . Therefore,

Putting these approximations together and remembering that the constants in the big terms depend only on and , we can take these error terms out of the integral of investigation, which gives

where the constants involved in bounding the big term depend now on (and also and as before), and is the constant, which depends only on and and is defined by

| (3.6) |

This concludes the proof. ∎

4 Convergence of the intensity measure

4.1 Pointwise convergence of the density function

In this section we consider the convergence of the intensity measure of the intersection point process , as . We start with a lemma dealing with the convergence of the density function of .

Lemma 4.1.

The density of the intensity measure , with respect to the Lebesgue measure on , satisfies

| (4.1) |

where the constants , , are the same constants as in Lemma 3.2 applied with and . In particular, if , it follows immediately that for any fixed ,

with

| (4.2) |

4.2 Convergence in total variation of the (restricted) intensity measure

Recall that is the intensity measure of the intersection point process where and is the intensity measure of the limiting Poisson point process which has density , where is the constant defined in (4.2). Also, for , we denote by , the restrictions of these measures to the complement of the ball . The total variation distance between the two (restricted) measures is defined as

where the supremum is taken over all Borel set . As a simple corollary of Lemma 4.1 we find that for any fixed this distance goes to zero as the intensity goes to infinity.

Corollary 4.2.

Let . Assume that . Then there is a constant depending only on such that

In particular,

Proof.

Let be a Borel set. From Lemma 4.1 we have that

Thus

Since this bound is independent from the choice of the set , by taking the supremum over all we bound the total variation distance by a big of , which goes to zero. The proof is thus complete. ∎

5 Convergence of the point process and its convex hull

5.1 Convergence in Kantorovich–Rubinstein distance of the (restricted) intersection process

In this section we show that the restriction of the intersection process to the complement of a ball with radius converges in Kantorovich–Rubinstein distance to the restriction of the Poisson point process . Let us first introduce, with a geometric point of view, the Kantorovich–Rubinstein distance between simple point processes in . For a definition applying to a more general setting we refer the reader to Section 2.5 of [7] where this distance is introduced with a functional point of view. For two discrete point sets and in we say that the total variation distance between them is the quantity

where denotes the number of points of which does not belong to , possibly infininity. Note that this definition corresponds to the one used in the previous section when the sets and are considered as counting measures. Now, consider two simple point processes and in . Here, as in the rest of the article, we identify a simple point process with its support, which is a random discrete subset of . The Kantorovich–Rubinstein distance between and is defined as

where denotes the set of couplings of and , i.e., the set of pairs such that and have the same distribution, . Informally speaking, the Kantorovich–Rubinstein distance measures by how many points and differ on average, if we couple them optimally.

We want to use this distance to compare the intersection point process with the Poisson point process . The first consists almost surely of finitely many points, while the second is almost surely infinite. Therefore their Kantorovich–Rubinstein distance is always infinite for any . Thus, in order to obtain a meaningful result we will consider the restriction of both point processes to the complement of a ball with positive radius. Doing so, we ensure that both point processes are almost surely finite.

Theorem 5.1.

Assume that . Then, we have that

where is a positive constant which depends only on . In particular

| (5.1) |

Proof.

Theorem 3.1 of [7] applied to our setting says that

where is defined (and bounded) in the Lemma 5.2 below. Corollary 4.2 and Lemma 5.2 provide bounds for each of the two summands of the right hand side, and thus we get the bound

from which Theorem 5.1 follows. Note that the assumptions of Corollary 4.2 and of Lemma 5.2 are both satisfied. Therefore the proof is complete. ∎

In the next lemma we deal with the error term , which appeared in (5.1) in the proof of the previous theorem.

Lemma 5.2.

For , , , and , set

| (5.2) |

where denotes the integral

Then, for and , we have that

where is a positive constant depending only on .

Proof.

Let and be fixed. We want to show that tends to , as and . The constant appearing below depends on and , and is independent of everything else. Its specific value varies from line to line and is irrelevant for the proof.

First part of the proof: Make use of Lemma 3.2.

In this first part we use integral geometric formulas in order to rewrite the integral in term of integrals studied in Lemma 3.2.

Let (resp. ) denotes the intersection of the affine hyperplanes involved in the inner (resp. outer) integral, that is

Applying twice the Blaschke-Petkantschin formula (2.1) permits us to rewrite our integral by ‘pivoting’ the hyperplanes ’s around and . It gives that equals

Note that we also took out of the integral the factors and . We will now make more apparent the structure of this expression by using the following notation, which is similar to the one used in Lemma 3.2:

and

With this notation and using Fubini’s theorem the investigated integral takes the form

Lemma 3.2 gives us precise approximations of and in terms of the distances between the origin and the flats and , respectively. In order to have a hand on these distances we decompose the affine flat (resp. ) into a sum a linear flat (resp. ) and a translation vector (resp. ) in the orthogonal complement of that flat. The aforementioned distances are simply the Euclidean norms of the vectors and . The quantity of interest thus becomes

It is easy to see that if and if . For the other cases we use Lemma 3.2 which provides us for with

and for with

Here, we only need to consider upper bounds, so we will keep from these two approximations the following statements which hold for all :

where is some large enough constant depending only on and . Plugging these bounds in the integral above yields

| (5.3) |

where

Second part of the proof: Bound .

We will now focus on bounding the newly introduced term . One difficulty in estimating this term comes from the fact that it is hard to get a good hand on the norm of the intersection of the affine flats and . In order to overcome this problem, we will reduce it to intersections involving one linear flat and one affine flat. As we will see, the norm of such intersections are much more easily handled. Observe that the origin and the points , and are the vertices of a parallelogram. Thus we have that

Therefore, using the triangle inequality and the fact that if a sum of two positive real numbers is bigger than then at least one of the two is bigger than , we obtain the following bound of the indicator function which appears in the term :

Thus we have that , where

and

Let us consider . By using spherical coordinates in the -dimensional space and then Fubini’s theorem, we get that , with

and

The integral is the probability that the random linear space intersects the fixed flat at a distance from the origin greater than . Such a probability is estimated in Lemma 3.1, from which we get that

We evaluate also the integral , namely

Note that for the last equality to hold one needs that both exponents and are distinct from . This is insured by the condition . Putting the pieces together we get the bound

| (5.4) |

Next, we deal with and recall that

In this integral we consider the intersection of a fixed linear space with a ‘moving’ affine space . If we compare with the definition of we see some similarities but also that the roles of which space is fixed and which one is moving are interchanged. As above we will use Lemma 3.1 to bound this integral, but first we need to rewrite it in a more convenient form. Using spherical coordinates in the -dimensional space , Fubini’s theorem and ‘parametrising’ the space by we can rewrite the integral as

where denotes an arbitrarily chosen -dimensional flat at distance from the origin, . The inner integral is the probability that a random flat and a fixed linear space have their intersection point with a norm at least . Lemma 3.1 tells us that, for a fixed , this is of order at most . Therefore

Recall that by assumption. Thus, without loss of generality, we may assume that is large enough to ensure that , and therefore

The two first integrals give a term of order and the third a term of order . Since this yields

| (5.5) |

Combining the bounds (5.4) and (5.5) for the terms and , we finally get

Third (and final) part of the proof.

We now plug the last bound into (5.3) to conclude that

| (5.6) |

where

We use spherical coordinates in the -dimensional subspace to see that

Recall that without loss of generality . We split the integral into three parts:

Since we use the inequalities

to get the bound

Note that each of the monomials , and is distinct from , except for if . In order to avoid distinguishing cases we will use the bound

which is valid for all . Thus, we get

We notice that this bound is independent from , so when we plug it into (5.6) we can ignore the integral over . Also recall that . This gives

For and , the last quantity is maximised for . This proves Lemma 5.2. ∎

5.2 Convergence in distribution of the intersection process

Using Theorem 5.1 we are now in a position to state our main theorem. We prove that under the assumption that the intersection point process converges in distribution to a Poisson point process with power law density function in . To explain the meaning of this convergence we supply the space of counting measures on with the vague topology induced by the mappings , where is a non-negative continuous function with compact support. With this topology becomes a Polish space and convergence in distribution of point processes refers to weak convergence induced by the vague topology, see [22, Chapter 16 and Appendix A2]. Since all point processes we deal with are simple (that is, have no multiple points or atoms) the convergence of a sequence of (simple) point processes to a simple point process is equivalent to the convergence in distribution of the real-valued random variables to for all relatively compact sets satisfying , where we write for the boundary of , see [22, Theorem 16.16].

Theorem 5.3.

Let and be a Poisson point process in whose intensity measure has density function , where is the same as in the previous section and given by (4.2). Then, we have that

in

Proof.

Theorem 16.16 of [22] implies that in the following list of statements, (1) is equivalent to (2) and (3) is equivalent to (4):

-

(1)

;

-

(2)

for all Borel sets , relatively compact (in the space ) and with boundary of zero Lebesgue measure.

-

(3)

;

-

(4)

for all Borel sets , relatively compact (in the space ) and with boundary of zero Lebesgue measure.

We are going to show that (1) holds and that (4) is equivalent to (2) (for all ).

Let be any fixed real number. Using Theorem 5.1 we have that

This implies (1) by Proposition 2.1 of [7].

Now, consider a set as in (4). Since it is relatively compact in its boundary does not contain the origin and therefore there exists a small radius such that . From this we conclude that since (2) holds for all , (4) holds as well. As mentioned above, (4) is equivalent to (3) and therefore the theorem follows. ∎

Remark 5.4.

The constant appearing in the statement of Theorem 5.3 is defined in (4.2). In other words, is times the expected volume of a random parallelotope spanned by independent random vectors which are uniformly distributed on (i.e., according to the normalised -dimensional Hausdorff measure on that set). In dimension the integral in the definition of can be computed explicitly:

In higher dimensions such a computation seems no longer tractable.

Remark 5.5.

The result of Theorem 5.3 remains true if one constructs the point process as the intersections of independent and identically distributed random hyperplanes uniformly distributed in the set of hyperplanes intersecting the ball , that is, if we replace the role of the Poisson hyperplane process by a binomial hyperplane process of same intensity measure. The proof would follow exactly the same lines and relies on the fact that the bound from [7] on the Kantarovich-Rubinstein distance applies as well when the underlying process is a binomial point process. We restricted ourselves to the Poisson case for simplicity and because the Poisson hyperplane process and its induced tessellation are the more classical objects in stochastic geometry.

5.3 Convergence of the convex hull

In the previous section we have established that the intersection point process converges in distribution to the Poisson point process with density function , as and . Now we will consider the weak convergence of the convex hull together with its -vector. For a polytope and we write for the number of -dimensional faces of . The vector is called the -vector of . Moreover, we recall the Hausdorff distance

on the space of non-empty compact subsets of . Endowing with the topology generated by the Hausdorff distance and the induced Borel -field, a random non-empty compact set is a measurable mapping from an underlying probability space to the measurable space , and convergence in distribution of a sequence of random compact sets to a random compact set refers to weak convergence with respect to this topology, see [22, Chapter 16] and [29, Chapter 12.3].

Theorem 5.6.

Let . It holds that converges, as , to in distribution. Moreover, converges to in distribution for all , as .

Proof.

First, it follows from [29, Lemma 3.1.4] and [29, Theorem 12.3.5] that (for any and ) and are almost surely random non-empty compact sets in . Now, let and consider the asymptotics as . We have already seen that . Applying the Skorokhod representation theorem [22, Therorem 4.30] we can find a probability space and random elements and such that and and and have the same distribution (for any ), and such that almost surely. For almost all we have that

-

1.

for every open half-space such that ,

-

2.

is in general position, that is, no atoms of belong to the same -dimensional flat, .

These are precisely the assumptions of Lemma 4.1 in [19] which implies that, as and for almost all ,

with respect to the Hausdorff distance and, for any ,

Going back to the original probability space we get the two convergences claimed in the theorem. ∎

We would like to rephrase the result of Theorem 5.6 in a different way. For this consider the tessellation induced by a stationary and isotropic Poisson hyperplane process in of intensity . This is a random collection of pairwise non-overlapping random polytopes covering the whole space. With probability one precisely one of these polytopes contains the origin of in its interior. This random polytope is denoted by and called the zero cell of the Poisson hyperplane tessellation of intensity . Let us also recall that for a convex set we denote by the convex dual of . In particular, if is a polytope containing the origin in its interior,

| (5.7) |

for all , see [31, Corollary 2.13].

Corollary 5.7.

Let and put , where is defined by (4.2). Then converges, as , in distribution to . Moreover, converges in distribution to for all , as .

Proof.

Remark 5.8.

By means of the last corollary, properties on the asymptotic distribution of can be derived by duality from statements on the distribution of the zero cell . This random polytope, as well as its volume-debiased version – known as typical cell –, has been intensively investigated since the pioneering work of Miles and Matheron in the 1960’ies and 1970’ies, see [29, Chapter 10.4] and the many references cited therein. More recent results include formulas for the expected face numbers of the zero cell in any dimension [18, 21], a description of ‘large’ [5, 16, 15] or ‘small’ [4, 28] typical and zero cells, super-exponential bounds on the probability of having facets for large [5] and a probabilistic analysis of zero cell in high dimensions [26, 13, 14].

Based Theorem 5.6 we are now in the position to disprove the conjecture from [8] we discussed in the introduction. In fact, Corollary 5.9 yields a lower bound on limit of all expected face number for any space dimension .

Corollary 5.9.

Let and fix . Then

In particular, if ,

Proof.

The first claim is a direct consequence of Fatou’s lemma together with the fact that all the random variables , , and are non-negative. In dimension , we have that for any polygon and so the identity follows from [19, Corollary 2.13] by taking there. ∎

We would like to emphasize that the expected face numbers of the convex hull of the Poisson point process have been computed explicitly for any and in [17, Theorem 2.1] and are given by

where is the imaginary unit. For example, for this leads to

as in Corollary 5.9 and for one has the values

Remark 5.10.

In analogy with [19, Theorem 2.4], which deals with the convergence of the expected face numbers (and higher moments) of random cones generated by an i.i.d. sample, we conjecture that Corollary 5.9 can be strengthened to the statement that , as , for any and . However, it should be noted that, although this is tempting, this does formally not follow from Theorem 5.3. To prove the missing uniform integrability of the family of random variables seems a challenging task in view of the intricate correlation structure of the intersection point process .

Acknowledgement

AB and GB were supported by the German Research Foundation (DFG) via GRK 2131 “High-Dimensional Phenomena in Probability – Fluctuations and Discontinuity”.

References

- [1] Mikhail J. Atallah “Computing the convex hull of line intersections” In J. Algorithms 7.2, 1986, pp. 285–288 DOI: 10.1016/0196-6774(86)90010-6

- [2] Sheldon Axler, Paul Bourdon and Wade Ramey “Harmonic Function Theory” 137, Graduate Texts in Mathematics Springer-Verlag, New York, 1992 DOI: 10.1007/b97238

- [3] Daniel Berend and Vladimir Braverman “Convex hull for intersections of random lines” In 2005 International Conference on Analysis of Algorithms, Discrete Math. Theor. Comput. Sci. Proc., AD Assoc. Discrete Math. Theor. Comput. Sci., Nancy, 2005, pp. 39–47

- [4] Gilles Bonnet “Small cells in a Poisson hyperplane tessellation” In Adv. in Appl. Math. 95, 2018, pp. 31–52 DOI: 10.1016/j.aam.2017.11.002

- [5] Gilles Bonnet, Pierre Calka and Matthias Reitzner “Cells with many facets in a Poisson hyperplane tessellation” In Adv. Math. 324, 2018, pp. 203–240 DOI: 10.1016/j.aim.2017.11.016

- [6] Yutai T. Ching and Der-Tsai Lee “Finding the diameter of a set of lines” In Pattern Recognition 18.3-4, 1985, pp. 249–255 DOI: 10.1016/0031-3203(85)90050-0

- [7] Laurent Decreusefond, Matthias Schulte and Christoph Thäle “Functional Poisson approximation in Kantorovich-Rubinstein distance with applications to U-statistics and stochastic geometry” In Ann. Probab. 44.3, 2016, pp. 2147–2197 DOI: 10.1214/15-AOP1020

- [8] Luc Devroye and Godfried Toussaint “Convex hulls for random lines” In J. Algorithms 14.3, 1993, pp. 381–394 DOI: 10.1006/jagm.1993.1020

- [9] Mordecai Golin, Stefan Langerman and William Steiger “The convex hull for random lines in the plane” In Discrete and Computational Geometry 2866, Lecture Notes in Comput. Sci. Springer, Berlin, 2003, pp. 172–175 DOI: 10.1007/978-3-540-44400-8_17

- [10] Lothar Heinrich “Central limit theorems for motion-invariant Poisson hyperplanes in expanding convex bodies” In Rend. Circ. Mat. Palermo (2) Suppl., 2009, pp. 187–212

- [11] Lothar Heinrich, Hendrik Schmidt and Volker Schmidt “Central limit theorems for Poisson hyperplane tessellations” In Ann. Appl. Probab. 16.2, 2006, pp. 919–950 DOI: 10.1214/105051606000000033

- [12] Lothar Heinrich, Hendrik Schmidt and Volker Schmidt “Limit theorems for functionals on the facets of stationary random tessellations” In Bernoulli 13.3, 2007, pp. 868–891 DOI: 10.3150/07-BEJ6131

- [13] Julia Hörrmann and Daniel Hug “On the volume of the zero cell of a class of isotropic Poisson hyperplane tessellations” In Adv. in Appl. Probab. 46.3, 2014, pp. 622–642 DOI: 10.1239/aap/1409319552

- [14] Julia Hörrmann, Daniel Hug, Matthias Reitzner and Christoph Thäle “Poisson polyhedra in high dimensions” In Adv. Math. 281, 2015, pp. 1–39 DOI: 10.1016/j.aim.2015.03.025

- [15] Daniel Hug, Matthias Reitzner and Rolf Schneider “The limit shape of the zero cell in a stationary Poisson hyperplane tessellation” In Ann. Probab. 32.1B, 2004, pp. 1140–1167 DOI: 10.1214/aop/1079021474

- [16] Daniel Hug and Rolf Schneider “Typical cells in Poisson hyperplane tessellations” In Discrete Comput. Geom. 38.2, 2007, pp. 305–319 DOI: 10.1007/s00454-007-1340-9

- [17] Zakhar Kabluchko “Angles of random simplices and face numbers of random polytopes”, 2019 arXiv:1909.13335

- [18] Zakhar Kabluchko “Expected -vector of the Poisson zero polytope and random convex hulls in the half-sphere”, 2019 arXiv:1901.10528

- [19] Zakhar Kabluchko, Alexander Marynych, Daniel Temesvari and Christoph Thäle “Cones generated by random points on half-spheres and convex hulls of Poisson point processes” In Probab. Theory Related Fields 175.3-4, 2019, pp. 1021–1061 DOI: 10.1007/s00440-019-00907-3

- [20] Zakhar Kabluchko and Christoph Thäle “The typical cell of a Voronoi tessellation on the sphere”, 2019 arXiv:1911.07221

- [21] Zakhar Kabluchko, Christoph Thäle and Dmitry Zaporozhets “Beta polytopes and Poisson polyhedra: -vectors and angles”, 2018 arXiv:1805.01338

- [22] Olav Kallenberg “Foundations of Modern Probability”, Probability and its Applications (New York) Springer-Verlag, New York, 2002 DOI: 10.1007/978-1-4757-4015-8

- [23] Günter Last and Mathew D. Penrose “Lectures on the Poisson Process” 7, Institute of Mathematical Statistics Textbooks Cambridge University Press, Cambridge, 2018 DOI: 10.1017/9781316104477

- [24] Günter Last, Mathew D. Penrose, Matthias Schulte and Christoph Thäle “Moments and central limit theorems for some multivariate Poisson functionals” In Adv. in Appl. Probab. 46.2, 2014, pp. 348–364 DOI: 10.1239/aap/1401369698

- [25] Georges Matheron “Random Sets and Integral Geometry” With a foreword by Geoffrey S. Watson, Wiley Series in Probability and Mathematical Statistics John Wiley & Sons, New York-London-Sydney, 1975

- [26] Eliza O’Reilly “Thin-shell concentration for zero cells of stationary Poisson mosaics” In Adv. in Appl. Math. 117, 2020, pp. 102017\bibrangessep24 DOI: 10.1016/j.aam.2020.102017

- [27] Matthias Reitzner and Matthias Schulte “Central limit theorems for -statistics of Poisson point processes” In Ann. Probab. 41.6, 2013, pp. 3879–3909 DOI: 10.1214/12-AOP817

- [28] Rolf Schneider “Small faces in stationary Poisson hyperplane tessellations” In Math. Nachr. 292.8, 2019, pp. 1811–1822 DOI: 10.1002/mana.201800366

- [29] Rolf Schneider and Wolfgang Weil “Stochastic and Integral Geometry”, Probability and its Applications (New York) Springer-Verlag, Berlin, 2008 DOI: 10.1007/978-3-540-78859-1

- [30] Dietrich Stoyan, Wilfrid S. Kendall and Joseph Mecke “Stochastic Geometry and its Applications.” In Wiley Ser. Probab. Math. Stat. Chichester: John Wiley & Sons Ltd., 1995

- [31] Günter M. Ziegler “Lectures on Polytopes” 152, Graduate Texts in Mathematics Springer-Verlag, New York, 1995, pp. x+370 DOI: 10.1007/978-1-4613-8431-1