Solving Bayesian Risk Optimization via Nested

Stochastic Gradient Estimation

Abstract

In this paper, we aim to solve Bayesian Risk Optimization (BRO), which is a recently proposed framework that formulates simulation optimization under input uncertainty. In order to efficiently solve the BRO problem, we derive nested stochastic gradient estimators and propose corresponding stochastic approximation algorithms. We show that our gradient estimators are asymptotically unbiased and consistent, and that the algorithms converge asymptotically. We demonstrate the empirical performance of the algorithms on a two-sided market model. Our estimators are of independent interest in extending the literature of stochastic gradient estimation to the case of nested risk functions.

1 Introduction

We consider the following optimization problem:

| (1) |

where is the solution space, is a random vector representing the randomness in simulation, and is a function that is evaluated through simulation. The expectation is taken with respect to (w.r.t.) , the correct distribution of . In a typical simulation optimization setting, the true distribution is unknown and estimated from a finite set of input data, and the following approximate problem is solved, where the estimated distribution is denoted by .

| (2) |

Due to the use of a finite dataset, even when the approximate problem (2) is solved to optimality, the optimal solution can perform poorly under true distribution. This issue is referred to as input uncertainty in simulation optimization.

Recently, Zhou \BBA Xie (\APACyear2015) and Wu \BOthers. (\APACyear2018) proposed the Bayesian Risk Optimization (BRO) framework which formulates the simulation optimization problem under input uncertainty. In BRO, assuming that belongs to a known parameterized family of distributions with unknown parameter , instead of solving (1) we solve the following:

| (3) |

where is a risk function mapping the random variable (induced by ) to a real number, and is the Bayesian posterior distribution of given a chosen prior and input data . The risk function can be chosen according to the risk preferences of the practitioner, and includes the risk neutral expectation and the minimax formulation of distributionally robust optimization (DRO, see e.g. Rahimian \BBA Mehrotra, \APACyear2019) as extreme cases under certain conditions. In this paper, we consider the following four cases of : Expectation, Mean-Variance, Value-at-Risk (VaR), and Conditional Value-at-risk (CVaR). A formal introduction and a thorough review of BRO, along with a discussion on alternative approaches, is provided in Section 2.

We aim to solve the BRO problem (3). To do so, we will use a Stochastic Approximation (SA, see Kushner \BBA Yin, \APACyear2003) approach, which requires gradient information. Historically, most work on stochastic gradient estimation focused on finding the gradient of expectation (see Fu, \APACyear2006, \APACyear2008). Some more recent research studies the Monte-Carlo estimation of gradients of VaR and CVaR; e.g. Hong (\APACyear2009) for VaR, and Hong \BBA Liu (\APACyear2009) for CVaR, where each derives a closed form expression of the corresponding gradient, and provides an asymptotically unbiased and consistent infinitesimal perturbation analysis (IPA) based estimator. Other work in this field includes Liu \BBA Hong (\APACyear2009), Fu \BOthers. (\APACyear2009), Jiang \BBA Fu (\APACyear2015), Tamar \BOthers. (\APACyear2015) and Peng \BOthers. (\APACyear2017), to name a few. A review of Monte-Carlo methods for estimation of VaR, CVaR and their gradients can be found in Hong \BOthers. (\APACyear2014).

Other related works include the literature on nested simulation, e.g. Lan \BOthers. (\APACyear2010), Gordy \BBA Juneja (\APACyear2010), Broadie \BOthers. (\APACyear2015), H. Zhu \BOthers. (\APACyear2020); Jaiswal \BOthers. (\APACyear2019), which studies the data-driven risk averse optimization problem under a parameterized Bayesian setting using the log-exponential risk measure; and H. Wang \BOthers. (\APACyear2020), which uses Bayesian Optimization (see Frazier, \APACyear2018) methods to optimize the expectation case of BRO with black-box expensive-to-evaluate objective functions.

Our work differs from the aforementioned works in the sense that the literature on nested simulation does not consider gradients or optimization, and the literature on gradient estimation does not consider nested risk functions. The literature on gradient estimation requires access to (and its gradients), while we only have access to (and its gradients), where , and (and its gradients) has to be estimated via sampling. The need to estimate the function adds another level of uncertainty to gradient estimation. To the best of our knowledge, this work is the first to study stochastic gradient estimation of nested risk functions.

The contributions of this paper can be summarized as follows: (i) We propose sample path gradient estimators for the four risk functions mentioned earlier, extending the literature in stochastic gradient estimation to the case of nested risk functions; (ii) We propose stochastic approximation algorithms with local convergence guarantees for optimization of the BRO framework; (iii) We provide a numerical study on a two-sided market model that demonstrates the value of risk averse solution approaches in the presence of input uncertainty. Although the exposition in this paper is focused on the BRO framework, it is worth noting that our estimators can be applied more broadly, e.g., for estimating the sensitivities of quantiles of financial portfolios.

2 An Overview of BRO Framework

As mentioned in the introduction, in a typical simulation optimization framework, one aims to solve the following problem:

| (4) |

where the solution space is a non-empty, compact subset of , is a random vector representing the stochastic noise in the system, and is a function mapping to . The expectation is taken w.r.t , the true distribution of . In practice, is not known and is typically replaced with an estimate which is obtained from a finite set of input data. The estimation error of due to the use of finite data is often referred to as the input model uncertainty, or simply as input uncertainty. There is a large literature dedicated to studying the impact of input uncertainty in estimating system performance; see Barton (\APACyear2012) and Song \BOthers. (\APACyear2014) for a review.

Due to input uncertainty, even when the estimated problem is solved to optimality, the optimal solution can perform poorly under the true distribution. Hence, a natural question is, “how do we make decisions that account for input uncertainty?”. We are interested in finding good solutions that hedge against input uncertainty. One common approach is to construct an ambiguity set that includes with high probability, and optimize w.r.t. the worst-case outcome within this set. This approach is referred to as Distributionally Robust Optimization (DRO) framework and has a large literature dedicated to it; see Rahimian \BBA Mehrotra (\APACyear2019) for a review. In DRO, constructing the ambiguity set is a non-trivial task and has a large impact on the solution performance and tractability of the resulting problem. A large ambiguity set can lead to overly conservative solutions, whereas, a small uncertainty set might fail to include the true distribution. An alternative approach is to optimize with respect to a risk neutral expectation of the objective function over the set of all possible input distributions. As argued in Zhou \BBA Xie (\APACyear2015), these two approaches can be seen as two extreme cases. The risk neutral expectation might fail to put enough weight over extreme (tail) scenarios, whereas, the DRO approach might be overly conservative due to hedging against worst-case scenarios.

Moreover, to the best of our knowledge, in a simulation optimization setting, the existing literature lacks tractable reformulations of the DRO problems. Although one can use the minimax formulation to formulate the distributionally robust simulation optimization problem, efficient optimization of this problem remains an open question due to the lack of structure in the function. In the robust optimization literature, Bertsimas \BOthers. (\APACyear2010) study a simulation optimization problem that is jointly robust to both implementation errors and parameter uncertainty, however, their method does not work when one is only concerned about the parameter uncertainty. Besides these popular approaches, the robust simulation optimization problem found interest in the kriging literature, e.g. Dellino \BOthers. (\APACyear2015); Kleijnen (\APACyear2017), where a response surface is fitted over , and robustness is typically facilitated by optimizing the mean performance subject to constraints on the standard deviation.

In this paper, we focus on the Bayesian Risk Optimization (BRO) framework, which was proposed by Zhou \BBA Xie (\APACyear2015) and Wu \BOthers. (\APACyear2018) as an alternative approach to simulation optimization under input parameter uncertainty. Suppose that the true distribution belongs to a parameterized family of distributions such that for some , where is the unknown true parameter and is the parameter space. Assuming that the form of is known, we take a Bayesian approach and calculate the posterior likelihood of for a given dataset of independent and identically distributed (i.i.d.) input data drawn from the true distribution. Let denote the prior distribution of . Then, using Bayesian updating we can calculate the posterior distribution

where () is the likelihood of obtaining () given parameter , and denotes equivalence up to a normalization constant.

Define as the objective value under parameter , where denotes the expectation w.r.t. . If we view as a random variable with distribution , we can treat as a random variable induced by . Define as a risk function over which maps the random variable to . Instead of solving (4), we solve

| (5) |

which is referred to as the BRO problem. The risk function can be chosen to reflect the risk preference of the practitioner. In this paper, we focus on the following four cases of :

-

1.

Expectation: ;

-

2.

Mean - Variance: ;

-

3.

Value-at-Risk: ;

-

4.

Conditional Value-at-Risk: ;

where () denote that the expectation (variance) is taken w.r.t. , and denote the level Value-at-Risk and Conditional Value-at-Risk respectively. We will define VaR and CVaR formally in corresponding subsections.

For the four cases of considered here, Wu \BOthers. (\APACyear2018) study the asymptotic properties of the objective functions and optimal solutions. We briefly summarize their results here. As the intuition would suggest, they show that as the data size , the posterior distribution converges in distribution to a degenerate distribution on . Furthermore, under mild regularity conditions, it is shown that for every fixed as , almost surely (a.s.), and a.s. for all four cases of considered here. Similarly, for the consistency of optimal solutions, it is shown that a.s. as where and are the sets of optimal solutions to (5) and (4) respectively, and is the distance between two sets with and being an arbitrary norm.

Moreover, the analysis of Wu \BOthers. (\APACyear2018) reveals the following asymptotic normality results which can be used to construct confidence intervals for the true objective value. Let denote the normal distribution, and let and denote the probability density function (PDF) and cumulative density function (CDF) of respectively. Then, for every , as ,

-

•

for Expectation and Mean-Variance objectives,

-

•

for the Value-at-Risk objective,

-

•

and for the Conditional Value-at-Risk objective,

where denotes convergence in distribution. The variance is defined as where is the Fisher information matrix, denotes the transpose, and is the gradient w.r.t. . The point-wise convergence results presented here can be extended to convergence results in the function space of . Similar normality results also hold for the optimal values.

To summarize, Wu \BOthers. (\APACyear2018) establish the consistency and asymptotic normality of objective functions and optimal solutions for the four cases of considered here. They also show that the objectives of BRO can be approximated as a weighted sum of posterior mean objective and half-width of the true-objective’s confidence interval. In this paper, our aim is to optimize the BRO problem (5) for a given choice of and a given posterior distribution of . We refer the interested reader to Zhou \BBA Xie (\APACyear2015), Zhou \BBA Wu (\APACyear2017), and Wu \BOthers. (\APACyear2018) for further discussion on BRO formulation.

3 Solving the BRO Problem

In this section, we introduce our approach to solving the BRO problem. We take an SA approach, develop the stochastic gradient estimators needed, and conclude with convergence results for the algorithms. Throughout the paper, we use and to denote the gradients and respectively. We use as shorthand for , the expectation over the posterior distribution of , and as a shorthand for . The nested expectation is also shortened as . The proofs are provided in the online supplement.

3.1 Stochastic Approximation Algorithm

The BRO problem in its essence is a typical simulation optimization problem where the objective function is costly to estimate. Due to the nested structure of the objective function, one needs many more samples to estimate the BRO objective compared to a typical expectation or CVaR objective. If one were to use samples to estimate the inner expectation and samples to estimate the outer risk function, it would take a total of samples to estimate the BRO objective. This high cost of estimation motivates us to concentrate on algorithms that take advantage of the structure of the problem and require fewer function evaluations per iteration. With this motivation, the class of gradient based methods known as Stochastic Approximation emerges as an obvious candidate. To solve the BRO problem (5), we propose to use the SA algorithm of the following form (see Kushner \BBA Yin, \APACyear2003):

| (6) |

where is a non-empty, compact solution space, is the step size sequence, is the descent direction, is the projection operator that projects the iterate back to the feasible set . A typical candidate for is an estimate of the negative gradient of the objective function, which leads to the well known Stochastic Gradient Descent algorithm. Given a good estimator of the gradient, the stochastic approximation algorithm has nice convergence properties. We proceed in next subsection with the derivation of stochastic gradient estimators of the BRO problem (5) for the four cases of mentioned above.

3.2 Derivation of Stochastic Gradient Estimators

In this section, we derive the stochastic gradient estimators for the BRO problem. The results are derived only for one-dimensional . Multidimensional case can be handled by treating each dimension as a one-dimensional parameter while fixing the rest. We start by providing the estimators for Expectation and Mean - Variance cases without going into details, then derive the estimators for the more technically challenging cases of VaR and CVaR. The following lemma from Broadie \BBA Glasserman (\APACyear1996) is key to the consistency of IPA estimators and is used without mention throughout the paper.

Lemma 3.1.

Proposition 1, Broadie \BBA Glasserman (\APACyear1996) - Let denote a Lipschitz continuous function that is differentiable on a set of points . Suppose that there exists a random variable with such that for all and exists w.p. (with probability) 1 for all , with an open set. If for all , then for all .

3.2.1 Expectation and Mean-Variance Cases

Suppose that the interchange of gradient and expectation is justified (see Assumption 3.3). Then, we have the following for the gradients of expectation and variance respectively:

| (7) |

and

| (8) | ||||

The equations (7) and (8) can be used to provide gradient estimators for Expectation and Mean-Variance cases. For the Expectation case, it is seen that is a single run unbiased gradient estimator and the sample average (where are independent with distribution with ) is a strongly consistent estimator of the gradient. Similarly, for Mean-Variance case, we have

| (9) |

as an unbiased gradient estimator with independent and i.i.d. samples. One could use the same sample for and the same sample for at the expense of increased variance, and reduce the number of simulation runs to . However, using any fewer simulation runs would make the estimation of second and third terms biased. We do not study the trade off here since our main focus is on the estimation of VaR and CVaR gradients. This subsection is concluded by noting that sample averaging yields a strongly consistent estimator for the Mean-Variance case.

3.2.2 Value-at-Risk Case

In this subsection, we introduce the nested estimator of VaR gradients, and establish the asymptotical properties of the proposed estimator. Value-at-Risk, defined as , is the quantile of the loss function. We are interested in estimating the gradient using samples of and corresponding sample path gradients. Throughout the paper, and are used as shorthand notations for VaR and respectively.

If one has access to samples of , then can be estimated by the sample quantile (see Serfling, \APACyear2008) where is the ceiling function, denotes order statistic corresponding to the ordering , and is treated as a random variable induced by . However, in our case, we only have access to samples from . Let denote the Monte-Carlo estimator of generated using samples. Note that the ordering of based on does not necessarily correspond to the ordering of , i.e. does not hold in general. Therefore, we define a new ordering, denoted by , such that . This ordering is not uniquely defined by and depends on the realization of s. Under a mild set of assumptions, H. Zhu \BOthers. (\APACyear2020) shows that is a strongly consistent estimator of . Motivated by the consistency of , we propose

| (10) |

as the nested estimator of VaR gradients where is the IPA gradient estimator corresponding to . In the remainder of this subsection, we proceed to show that the estimator is asymptotically unbiased, and the batch-mean estimator , where is the number of batches of equal size and is the estimator corresponding to batch , is consistent and asymptotically normally distributed.

Notice that has the same form as , the single-layer estimator of quantile gradients of Hong (\APACyear2009). Both estimators stem from the observation that, under a mild set of assumptions, the quantile gradients can be expressed as .

We now introduce the technical conditions that lead to the consistency of these estimators. The assumptions we introduce here can be viewed in three categories. First, we have a set of assumptions due to H. Zhu \BOthers. (\APACyear2020) that are needed to justify consistency of by providing the necessary smoothness of . A second set of assumptions are needed to justify the interchange of gradient and expectation, and thus the validity of IPA gradient estimators. An additional assumption by Hong (\APACyear2009) is needed to validate the interchange for the case of VaR. A final set of assumptions are needed to mitigate the difficulties arising from conditioning on measure zero sets, and ensure that the pathwise gradient estimator is sufficiently smooth.

Let denote the estimation error and denote the normalized error. Then, . Under following set of assumptions, H. Zhu \BOthers. (\APACyear2020) prove that is a strongly consistent estimator of .

Assumption 3.2.

(H. Zhu \BOthers., \APACyear2020)

-

1.

For all , the response has finite conditional second moment, i.e., w.p. 1 and .

-

2.

The joint density of and , and its partial gradients and exist for each , all pairs of and for all .

-

3.

For all , there exists non-negative functions and such that , , for all . Furthermore, for , and .

The first part of the assumption ensures the validity of Central Limit Theorem (CLT). Second and third parts first appear in Gordy \BBA Juneja (\APACyear2010) and provide sufficient smoothness to ensure that the PDF of convergences to the PDF of sufficiently fast. For our purposes, they provide uniform bounds on the moments of the estimation error. See Gordy \BBA Juneja (\APACyear2010) for further discussion on these assumptions.

Assumption 3.3.

There exists a random variable such that , and the following holds in a probability 1 subset of .

-

1.

w.p.1 for all .

-

2.

The sample path gradient exists w.p.1 .

Assumption 3.3 ensures that exists (w.p.1), , and that these relations can be extended to . Let denote the distribution function of and define . We have the following assumption due to Hong (\APACyear2009).

Assumption 3.4.

(Hong, \APACyear2009) For any , has a continuous density in a neighborhood of , and exists and is continuous w.r.t. both and at .

This assumption ensures that is a continuous random variable in a neighborhood of , and that its gradient exists and is continuous in the same neighborhood. It is shown in Jiang \BBA Fu (\APACyear2015) that Assumptions 3.3 & 3.4 are sufficient to justify the expression , and that the continuity (in ) of follows from these two assumptions. Under these assumptions, Hong (\APACyear2009) and Jiang \BBA Fu (\APACyear2015) show that as , and the batch-mean estimator (with as the number of batches) is consistent.

We would like to show that as . Let us introduce some more notations that will come in handy in proving this convergence. Given that , we define

-

•

,

-

•

,

as the probability measures corresponding to the given conditional distributions. These measures will be useful for characterizing and respectively where . In what follows, we let denote a ball centered at with radius .

Assumption 3.5.

Assume that there exists a family of measures and a number such that for all and for all ,

Assumption 3.6.

.

Assumptions 3.5 and 3.6 impose technical conditions to ensure that the estimation errors for both the function value and its gradients are well behaved. Assumption 3.5 is seemingly abstract and deserves further explanation. It essentially requires that the distribution of the gradient estimate conditioned on the function value converges to its true counterpart. One would notice that conditioned on the value of the function estimate, the gradient estimator is no longer unbiased and in general, as the observations ( and ) rely on the same set of ’s. Intuition suggests that as and the estimation error , the corresponding errors in gradient estimation should also cancel out. Assumption 3.5 is a technical condition that we impose to mitigate the difficulties arising from conditioning on measure zero sets in proving this behavior. In fact, if the condition (and its noisy counterpart) is relaxed from a point to a neighborhood, i.e. , it can be shown that Assumption 3.5 follows from Assumptions 3.2 & 3.6. We provide a detailed discussion on the assumptions in the online supplement, where it is also shown that Assumption 3.5 is satisfied in a general class of problems.

Now that we have established the necessary regularity conditions, we have the following proposition on the asymptotic bias of . In the following means , means , and means and .

Proposition 3.7.

Moreover, if in addition the integral in Assumption 3.5 is , is differentiable w.r.t. at , and the budget sequence is such that , then the bias is .

Even though is asymptotically unbiased, it is not consistent in general when is multidimensional, particularly when the set is not a singleton. See Hong (\APACyear2009) for a discussion on consistency of , and Jiang \BBA Fu (\APACyear2015) for an additional assumption under which is consistent along with some examples. The same argument carries on to our case. A common approach is to use batching to address this difficulty. We have the following theorem which provides the consistency of the batch-mean estimator , where are i.i.d. copies and k is the number of batches.

Theorem 3.8.

In addition to the asymptotic unbiasedness and consistency, we have the following result that characterizes the asymptotic distribution of . The proof is a direct application of Lyapunov’s Central Limit Theorem combined with Proposition 3.7. It is identical to the proof of Theorem 5 of Hong (\APACyear2009), and is omitted here.

Theorem 3.9.

Suppose that the (stronger) assumptions of Proposition 3.7 hold, , and for some . Then,

where is the asymptotic variance of .

3.2.3 Conditional Value-at-Risk Case

Conditional Value-at-Risk, defined as , is the expectation of large losses. We are interested in estimating the gradient using samples of (and ). We use and as shorthand notations for CVaR and respectively.

Under a mild set of assumptions, Hong \BBA Liu (\APACyear2009) show that CVaR gradients can be written in the form of a conditional expectation as

| (11) |

We propose the following estimator of CVaR gradients that mimics a Monte-Carlo estimator of (11) with the available information.

| (12) |

In the remainder of this subsection, we show that is a strongly consistent and asymptotically unbiased estimator of .

The analysis of relies on a weaker set of assumptions than that of . Assumption 3.5 is no longer needed, and Assumption 3.4 is replaced with the following weaker assumption due to Hong \BBA Liu (\APACyear2009). Assumption 3.10, along with Assumption 3.3, is needed to ensure validity of (11).

Assumption 3.10.

(Hong \BBA Liu, \APACyear2009)

-

1.

The VaR function is differentiable for any .

-

2.

For any , .

We note that Assumption 3.10 and is implied by 3.4 and the differentiability of . It is presented separately here, as it replaces Assumption 3.4 with a weaker set of conditions. The following proposition is needed in proving the consistency of .

Proposition 3.11.

Suppose Assumption 3.2 holds and . Then

Note that (11) can be rewritten as , which admits as a Monte-Carlo estimator. Proposition 3.11 shows that the bias introduced by replacing with its noisy version, , disappears in the limit. The following proposition extends this result to show that is asymptotically unbiased and the bias is of the order .

Proposition 3.12.

We conclude this subsection with the following theorem that provides strong consistency of .

Remark 1.

Even though the results here are derived using the IPA estimator for the inner expectation, one should notice that our proofs only require a consistent estimator of the inner expectation. Therefore, where IPA is not applicable or it is not preferred for any other reason, one could replace with any consistent estimator such as the generalized likelihood ratio estimator of Peng \BOthers. (\APACyear2018), support independent unified likelihood ratio and infinitesimal perturbation analysis estimator of Y. Wang \BOthers. (\APACyear2012) etc. as long as the corresponding regularity conditions hold.

3.3 Convergence Analysis of the Algorithms

In this subsection, we start with a brief discussion on implementation and computational cost of the SA algorithm, and show that the use of and results in consistent algorithms for solving the corresponding BRO problems.

The SA algorithm is briefly summarized in Algorithm 1. When a closed form of the posterior distribution is not available, one may use numerical methods, such as Markov Chain Monte Carlo (MCMC) (Lange, \APACyear2010), variational Bayes (Fox \BBA Roberts, \APACyear2012) etc., to approximate the posterior distribution. We emphasize that it is only necessary to draw an empirical approximation to the posterior before the optimization starts (see Section 4.2 for more details). This avoids a repeated use of e.g. MCMC, which is not necessary since the posterior distribution does not change, and facilitates cost effective sampling of from the generated empirical distribution. Thus, the computational cost of Algorithm 1 is dominated by the simulations of , which has a total computational cost of .

The remainder of the subsection is dedicated to proving the convergence of the algorithms. The main result is summarized in the following theorem.

Theorem 3.14.

Theorem 3.14 is a direct application of Theorem 2.1 of Kushner \BBA Yin (\APACyear2003). Following their analysis, is deconstructed as , where is the negative gradient at , is martingale difference error term, and is the bias term. Kushner \BBA Yin (\APACyear2003) imposes the following set of assumptions to ensure the convergence of the SA algorithm.

Assumption 3.15.

Chapter 5.2, Kushner \BBA Yin (\APACyear2003)

-

1.

;

-

2.

There is a measurable function of and random variables such that

-

3.

is continuous;

-

4.

, ;

-

5.

w.p.1.

Let for the VaR estimator with , , and . For the CVaR, apply the same decomposition with replacing . To see that Assumption 3.15 is satisfied, note the following. Assumption 3.15.1 immediately follows from Assumption 3.6. Assumption 3.15.2 is satisfied by the given deconstruction. For Assumption 3.15.3, we assume that and are continuously differentiable. Assumption 3.15.4 is a common requirement for the step size sequences and is imposed here. As shown by Theorem 2.3 of Kushner \BBA Yin (\APACyear2003) and Theorem 2 of Kushner (\APACyear2010), Assumption 3.15.5 can be replaced with w.p.1 which is given by Propositions 3.7 and 3.12 for VaR and CVaR cases respectively. Therefore, Assumption 3.15 is satisfied and Theorem 3.14 follows immediately from Theorem 2.1 of Kushner \BBA Yin (\APACyear2003).

Remark 2.

4 Numerical Examples

In this section, we present an empirical study of the proposed algorithm. We start with a simple quadratic example, where we compare the numerical efficiency of two gradient-based algorithms that use the estimators developed in this paper with two gradient-free approaches from the existing literature. We follow that with a more realistic example of a two-sided market model, where we demonstrate the convergence of the SA algorithm on several BRO objectives. The section is concluded with a discussion on the objective choice, where the robustness of various objective choices are demonstrated.

4.1 A simple quadratic example

In this section, we study a simple quadratic example, where we compare the numerical efficiency of optimization algorithms using the gradient estimators developed in this paper with the gradient-free methods from the literature that can be used to solve the BRO problem. For gradient-based methods, we consider a quasi-newton method, the LBFGS algorithm (C. Zhu \BOthers., \APACyear1997), which only requires access to the gradients of the function, as well as the SA algorithm described above. For gradient-free alternatives, we consider the Nelder-Mead simplex method (Nelder \BBA Mead, \APACyear1965), and the Expected Improvement algorithm (Jones \BOthers., \APACyear1998), both of which are known for their superior empirical performance.

The example in consideration is modified from Hong (\APACyear2009), and is given by with the simulation oracle , where . It follows that , and .

In the online supplement, we discuss the details of the experiment, verify the assumptions, and obtain the analytical solution to the BRO optimization problem. Table 1 presents the average optimality gap obtained from replications using the BRO CVaR objective with risk level . The algorithms use the same simulation budget, where the BRO objective and its gradient is estimated using and . Since the benchmark algorithms are developed for deterministic optimization, we consider both stochastic evaluations of the objective and the Sample Average Approximation (SAA, Kim \BOthers., \APACyear2015) counterpart, which converts it into an approximate deterministic optimization problem by fixing the random variables and .

| # of evaluations | SAA? | SA | LBFGS | Nelder-Mead | EI |

|---|---|---|---|---|---|

| 10 | No | ||||

| Yes | |||||

| 20 | No | ||||

| Yes | |||||

| 50 | No | ||||

| Yes | |||||

| 100 | No | ||||

| Yes |

The results show a clear advantage of using the SA algorithm over all the benchmarks considered. Using the stochastic gradient estimators, our proposed Algorithm 1 (results highlighted in Table 1) achieves almost 2 orders of magnitude better performance than the closest competitor. We observe that the benchmark algorithms (LBFGS, Nelder-Mead and EI) have difficulty in solving the optimization problem using the stochastic estimators, while the results improve a little when solving the SAA counterpart. This shows that the methods developed in this paper provide a clear improvement over the existing alternatives for optimizing the BRO problem.

4.2 A Two-Sided Market Model

In a two-sided market model, the customers and providers arrive to the system according to two independent arrival processes. Upon arrival, a customer is served immediately if there is an available provider, otherwise the customer queues up to be served by future provider arrivals. Similarly, arriving providers leave the queue immediately if there is a customer waiting, otherwise they wait for the future customer arrivals. With some slight variation, such models can be used to mimic system dynamics of various real life scenarios such as sharing or gig economies. In this example, it is assumed that a provider can only serve one customer, and the system operates without abandonment. Customer arrivals are assumed to follow a Poisson process with rate , and provider arrivals follow a Poisson process with rate , where denotes the price set by the platform, with () decreasing (increasing) in . The rate functions are given by where are the (known) potential numbers of customers and providers, and are the (unknown) sensitivities of customers and providers respectively. These rate functions result in and , which agrees with the intuition that no providers (customers) should be willing to participate when the price is () and vice versa.

In our setting, the platform aims to minimize customer wait time to improve customer satisfaction. However, one could easily see that a naive objective of minimizing the expected wait time would drive price to infinity, leading to excess number of providers and no customers, thus no service or revenue. To avoid this pitfall, the objective is modified to be a weighted combination of customer waiting time and expected revenue. We estimate the customer waiting time by , the average waiting time of first customers, where denotes the waiting time of the customer, and expected revenue is estimated as . The resulting objective takes the form

where is a predetermined weight. If the rate functions and (i.e. ) are known, one can use sampling to estimate and optimize the objective. Since is unknown and is estimated from a finite set of real world data, the objective is replaced by to account for input uncertainty.

In order to estimate the gradient of the objective, we need to sample from and its gradient . Note that , where and denote the arrival time of provider and customer respectively, and where and . The gradient can be calculated as .

Before we can run the experiments, we need to estimate the objective function (and its gradient) which requires sampling from . One should notice that regardless of the choice of prior, does not admit a simple closed form solution. However, we can use an MCMC method, the Metropolis-Hastings algorithm (see Lange, \APACyear2010), to sample from . Suppose that the true parameters are , and we are given a dataset of size (each) of inter-arrival times drawn at .

Since the likelihood functions of and are separable, we estimate the posteriors using two independent MCMC runs. For the MCMC, we use a Gaussian proposal distribution, and the candidate is generated as with . We use as an uninformative prior. With the given choice of proposal and prior distributions, the acceptance probability simplifies to

where the likelihood of is calculated as with as the probability density given the parameter . We use a (post burn-in) run length of iterations with the starting point of and a burn-in period of iterations. An empirical analysis of the output using the Wasserstein distance, described in the online supplement, suggests that the samples are drawn from a stationary distribution. Let denote the list of samples generated from the MCMC run. is sampled as follows: we generate a random variable as the index and set . Since the MCMC converges to the posterior distribution and the are samples from the approximate steady state distribution of the MCMC, the generated this way are approximately distributed as . The resulting samples from MCMC have a sample average of and sample standard deviation of for , and a sample average of and sample standard deviation of for . The corresponding maximum likelihood estimators (MLE) are given by and , which suggests that the input data for the customers is not representative of the true distribution.

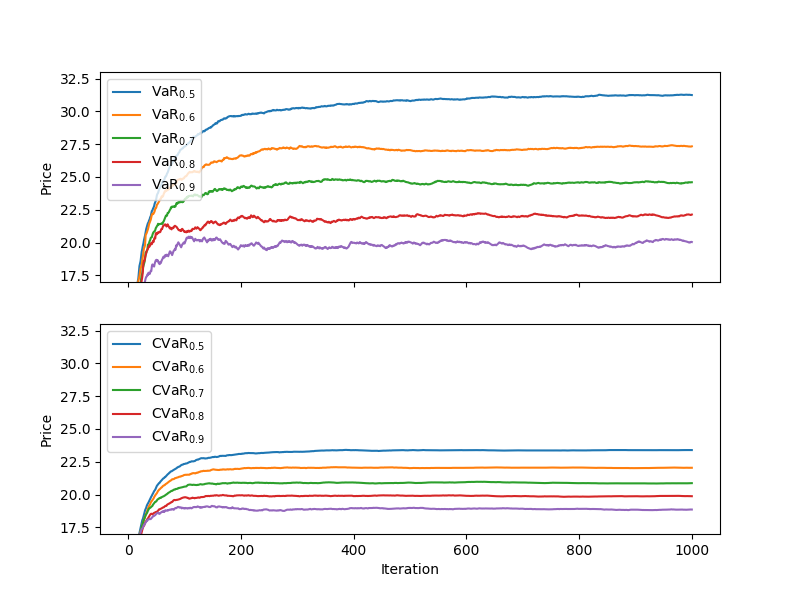

The problem parameters are set as . Before going into the optimization, we need to pick the budget and step size sequences. The choice of step size is problem specific, as both too large and too small step size sequences harm the convergence of the algorithm. We recommend using simple pilot experiments to guide the selection. For the budget sequences, Propositions 3.7 & 3.12 suggest that and should be of the same order, however the relative magnitudes are again problem dependent. We recommend checking the relative magnitudes of stochastic and input uncertainties, estimated by the standard deviation of for a fixed and w.r.t. with respectively, and modifying and until a balance is achieved. As a result of pilot experiments, we pick for this example. In light of Remark 2, we use the non-batching estimator for VaR.

For the algorithm runs, the step size sequence is chosen as and the budget sequence is . For each choice of below, we run replications of the algorithms, each for iterations with . The results are reported in Table 2. For each , we report the average solution obtained from replications (as ), the estimate of the solution standard deviations (as std()), the approximate optimal solution to the corresponding BRO problem (as ), and the performance of the obtained solution under the true distribution (as ). was evaluated using Monte Carlo simulation with samples. The reported is computed via brute-force Monte Carlo simulation with simulation intervals of using common random numbers (CRN) and a budget of . One would notice that for certain choices of there is a discrepancy of about between the algorithm solutions and the estimated optimal solutions. We note that the difference between the solution performances was below in each case, and the difference can be attributed to the estimator bias. For comparison, the true optimal solution and its performance is estimated as and , using Monte Carlo simulation with simulation intervals of using CRN and samples. The MLE solution is estimated in a similar manner to be with , which points to the value of robustness in this particular example.

| 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | ||

|---|---|---|---|---|---|---|

| VaR | ||||||

| std() | ||||||

| CVaR | ||||||

| std() | ||||||

In Figure 1, we plot a typical algorithm run for each . It is seen that the algorithm solutions quickly move into a neighborhood of the optimal solution and proceed to refine the solution further in the following iterations. There is a striking difference between the variability of the solution paths corresponding to VaR and CVaR objectives, which can be attributed to our decision to forgo batching in favor of computational efficiency. Without batching, the value of the VaR estimator is calculated using a single realization of , whereas, the value of the CVaR estimator is calculated by averaging over a number of ’s.

The results reported in Table 2 demonstrate the convergence of the algorithms to a the optimal solution as given in Theorem 3.14. Moreover, it is seen that different choices of correspond to a wide spread of solutions, which in turn has a significant effect on the resulting objective values. The true performance (i.e., under the true input parameter) of the solutions will be shown in the next section, while we discuss the choice of .

4.3 Discussion on objective choice

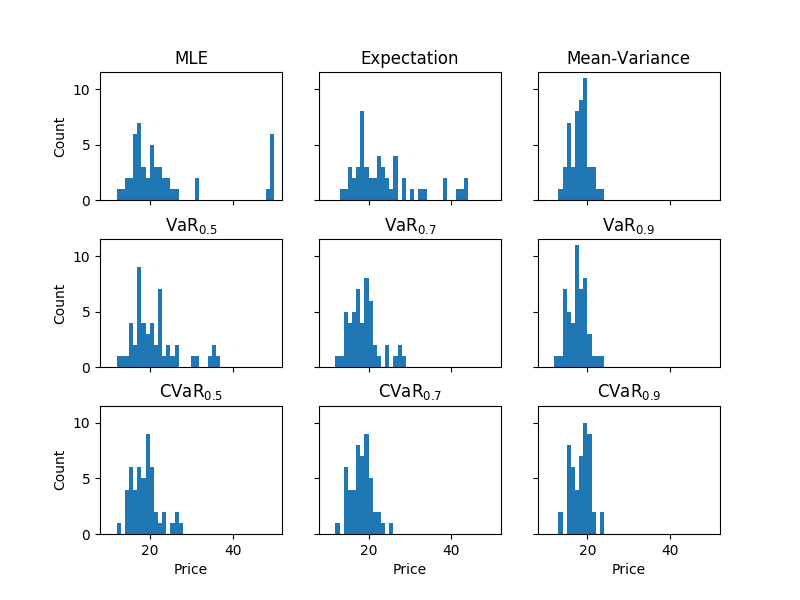

So far, our work focuses on solving the BRO problem given a risk function. However, the choice of the risk function (or the objective) is not a trivial task by itself. In this subsection, we will empirically compare several objectives and try to highlight the effect each has on the resulting decision. We draw independent input data sets of size each. For each set of input data, we estimate the posterior distribution and optimize the corresponding objective functions using the same parameters as the original problem. For VaR and CVaR objectives, we use risk levels . In addition, we compare with the Expectation, Mean-Variance (with variance weight of ) and MLE objectives.

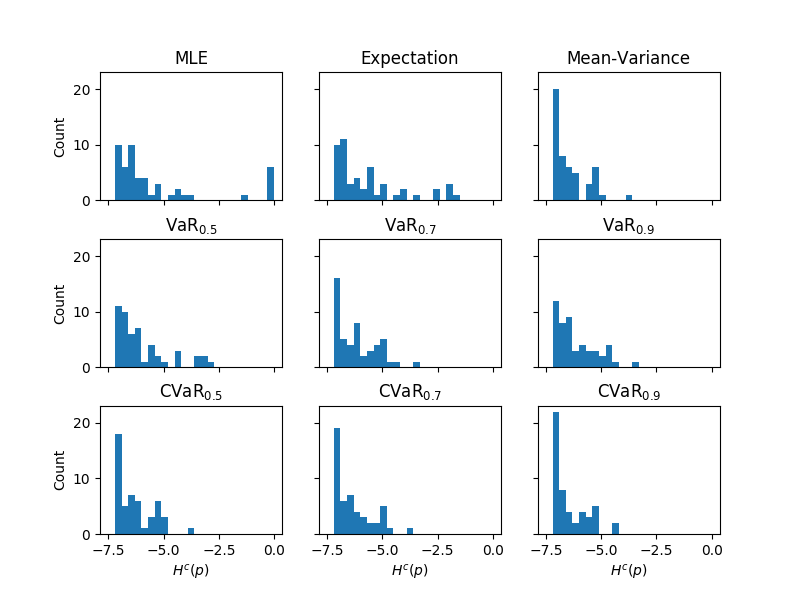

The performance of the solutions obtained from algorithm runs are estimated via Monte Carlo simulation using CRN and samples. The histograms of the solutions and the solution performances are then plotted in Figures 2 and 3 for each choice of . In order to highlight the important areas, we restrict the histograms to a range of in Figure 2. This was only an issue for the case of MLE, where the solutions ranged up to . Any solution value that exceeded is plotted as a point at .

A quick look at Figures 2 & 3 reveals the importance of objective choice. Figure 2 demonstrates the robustness of the BRO objectives, in the sense that the solutions are robust to the particular realization of the input data, and are more concentrated compared to MLE objectives. Although not explicitly shown, observation of just a few outliers in the input data affects the resulting MLE solutions drastically, whereas, the risk averse BRO solutions are much less sensitive to such observations. The choice of a small input size of further highlights the importance of the objective choice here. As expected, the robustness increases with and the CVaR objectives are more robust than VaR objectives by definition. In this example, the BRO solutions tend to concentrate around the true optimal solution, which leads to superior overall performance compared to MLE objective, as seen in Figure 3. We would like to emphasize that, although preferred, the superior solution performance is not something that a robust objective aims to provide, and the true aim of a robust objective is to provide a consistent solution performance across a wide range of input data. We refer an interested reader to Zhou \BBA Wu (\APACyear2017) for a similar numerical study on an M/M/1 queue problem and a News-vendor problem. We end our discussion by noting that it is possible to combine several objectives studied here and solve them using the tools developed in this paper. For example, if one wishes to balance between the robustness of VaR & CVaR and the average solution performance, Mean-VaR and Mean-CVaR objectives are obvious choices. In addition to choosing , one can adjust the relative weights of the Mean and VaR/CVaR objectives to balance between robustness and expected solution performance.

5 Conclusion

In this paper, with the aim of developing efficient methods for solving the Bayesian Risk Optimization framework, we derive stochastic gradient estimators and propose associated stochastic approximation algorithms. Our estimators extend the literature of stochastic gradient estimation to the case of nested risk functions. An example of a two-sided market model is studied to demonstrate the numerical performance of the algorithms, and provide insight into the choice of BRO objectives. Although the exposition of the paper focuses on the BRO framework, the gradient estimators we develop can be used in other settings where nested simulation is used, such as estimating the sensitivities of complex financial portfolios.

Acknowledgements

The authors gratefully acknowledge the support by the National Science Foundation under Grant CAREER CMMI-1453934 and the Air Force Office of Scientific Research under Grant FA9550-19-1-0283.

References

- Barton (\APACyear2012) \APACinsertmetastarBarton2012Input-uncertainty{APACrefauthors}Barton, R\BPBIR. \APACrefYearMonthDay2012. \BBOQ\APACrefatitleInput Uncertainty in Outout Analysis Input uncertainty in outout analysis.\BBCQ \BIn \APACrefbtitleProceedings of the Winter Simulation Conference Proceedings of the winter simulation conference (\BPGS 6:1–6:12). \APACaddressPublisherWinter Simulation Conference. \PrintBackRefs\CurrentBib

- Bertsimas \BOthers. (\APACyear2010) \APACinsertmetastarBertsimas2010RobustSim{APACrefauthors}Bertsimas, D., Nohadani, O.\BCBL \BBA Teo, K\BPBIM. \APACrefYearMonthDay2010. \BBOQ\APACrefatitleRobust Optimization for Unconstrained Simulation-Based Problems Robust optimization for unconstrained simulation-based problems.\BBCQ \APACjournalVolNumPagesOperations Research581161-178. {APACrefDOI} \doi10.1287/opre.1090.0715 \PrintBackRefs\CurrentBib

- Broadie \BOthers. (\APACyear2015) \APACinsertmetastarBroadie2015Regression{APACrefauthors}Broadie, M., Du, Y.\BCBL \BBA Moallemi, C\BPBIC. \APACrefYearMonthDay2015. \BBOQ\APACrefatitleRisk Estimation via Regression Risk estimation via regression.\BBCQ \APACjournalVolNumPagesOperations Research6351077-1097. {APACrefDOI} \doi10.1287/opre.2015.1419 \PrintBackRefs\CurrentBib

- Broadie \BBA Glasserman (\APACyear1996) \APACinsertmetastarBroadie1996IPA{APACrefauthors}Broadie, M.\BCBT \BBA Glasserman, P. \APACrefYearMonthDay1996. \BBOQ\APACrefatitleEstimating Security Price Derivatives Using Simulation Estimating security price derivatives using simulation.\BBCQ \APACjournalVolNumPagesManagement Science422269-285. {APACrefDOI} \doi10.1287/mnsc.42.2.269 \PrintBackRefs\CurrentBib

- Dellino \BOthers. (\APACyear2015) \APACinsertmetastarDellino2015Metamodel{APACrefauthors}Dellino, G., Kleijnen, J\BPBIP\BPBIC.\BCBL \BBA Meloni, C. \APACrefYearMonthDay2015. \BBOQ\APACrefatitleMetamodel-Based Robust Simulation-Optimization: An Overview Metamodel-based robust simulation-optimization: An overview.\BBCQ \BIn G. Dellino \BBA C. Meloni (\BEDS), \APACrefbtitleUncertainty Management in Simulation-Optimization of Complex Systems. Uncertainty management in simulation-optimization of complex systems. \APACaddressPublisherSpringer, Boston, MA. \PrintBackRefs\CurrentBib

- Fox \BBA Roberts (\APACyear2012) \APACinsertmetastarFox2012VariationalBayes{APACrefauthors}Fox, C\BPBIW.\BCBT \BBA Roberts, S\BPBIJ. \APACrefYearMonthDay2012. \BBOQ\APACrefatitleA tutorial on variational Bayesian inference A tutorial on variational bayesian inference.\BBCQ \APACjournalVolNumPagesArtificial Intelligence Review. \PrintBackRefs\CurrentBib

- Frazier (\APACyear2018) \APACinsertmetastarfrazier2018tutorial{APACrefauthors}Frazier, P\BPBII. \APACrefYearMonthDay2018. \APACrefbtitleA Tutorial on Bayesian Optimization. A tutorial on bayesian optimization. \PrintBackRefs\CurrentBib

- Fu (\APACyear2006) \APACinsertmetastarFU2006Gradient{APACrefauthors}Fu, M\BPBIC. \APACrefYearMonthDay2006. \BBOQ\APACrefatitleChapter 19 Gradient Estimation Chapter 19 gradient estimation.\BBCQ \BIn S\BPBIG. Henderson \BBA B\BPBIL. Nelson (\BEDS), \APACrefbtitleSimulation Simulation (\BVOL 13, \BPG 575 - 616). \APACaddressPublisherElsevier. {APACrefDOI} \doihttps://doi.org/10.1016/S0927-0507(06)13019-4 \PrintBackRefs\CurrentBib

- Fu (\APACyear2008) \APACinsertmetastarFU2008SA-Summary{APACrefauthors}Fu, M\BPBIC. \APACrefYearMonthDay2008. \BBOQ\APACrefatitleWhat you should know about simulation and derivatives What you should know about simulation and derivatives.\BBCQ \APACjournalVolNumPagesNaval Research Logistics558723-736. {APACrefDOI} \doi10.1002/nav.20313 \PrintBackRefs\CurrentBib

- Fu \BOthers. (\APACyear2009) \APACinsertmetastarFu2009Quantile-Sens{APACrefauthors}Fu, M\BPBIC., Hong, L\BPBIJ.\BCBL \BBA Hu, J\BHBIQ. \APACrefYearMonthDay2009. \BBOQ\APACrefatitleConditional Monte Carlo Estimation of Quantile Sensitivities Conditional monte carlo estimation of quantile sensitivities.\BBCQ \APACjournalVolNumPagesManagement Science55122019-2027. {APACrefDOI} \doi10.1287/mnsc.1090.1090 \PrintBackRefs\CurrentBib

- Gordy \BBA Juneja (\APACyear2010) \APACinsertmetastarGordy2010Nested{APACrefauthors}Gordy, M\BPBIB.\BCBT \BBA Juneja, S. \APACrefYearMonthDay2010. \BBOQ\APACrefatitleNested Simulation in Portfolio Risk Measurement Nested simulation in portfolio risk measurement.\BBCQ \APACjournalVolNumPagesManagement Science56101833-1848. {APACrefDOI} \doi10.1287/mnsc.1100.1213 \PrintBackRefs\CurrentBib

- Hong (\APACyear2009) \APACinsertmetastarHong2009VaR{APACrefauthors}Hong, L\BPBIJ. \APACrefYearMonthDay2009. \BBOQ\APACrefatitleEstimating Quantile Sensitivities Estimating quantile sensitivities.\BBCQ \APACjournalVolNumPagesOperations Research571118-130. {APACrefDOI} \doi10.1287/opre.1080.0531 \PrintBackRefs\CurrentBib

- Hong \BOthers. (\APACyear2014) \APACinsertmetastarHong2014VaR-CVaR-Rev{APACrefauthors}Hong, L\BPBIJ., Hu, Z.\BCBL \BBA Liu, G. \APACrefYearMonthDay2014. \BBOQ\APACrefatitleMonte Carlo Methods for Value-at-Risk and Conditional Value-at-Risk: A Review Monte carlo methods for value-at-risk and conditional value-at-risk: A review.\BBCQ \APACjournalVolNumPagesACM Trans. Model. Comput. Simul.24422:1–22:37. {APACrefDOI} \doi10.1145/2661631 \PrintBackRefs\CurrentBib

- Hong \BBA Liu (\APACyear2009) \APACinsertmetastarHong2009CVaR{APACrefauthors}Hong, L\BPBIJ.\BCBT \BBA Liu, G. \APACrefYearMonthDay2009. \BBOQ\APACrefatitleSimulating Sensitivities of Conditional Value at Risk Simulating sensitivities of conditional value at risk.\BBCQ \APACjournalVolNumPagesManagement Science552281-293. {APACrefDOI} \doi10.1287/mnsc.1080.0901 \PrintBackRefs\CurrentBib

- Jaiswal \BOthers. (\APACyear2019) \APACinsertmetastarJaiswal2019{APACrefauthors}Jaiswal, P., Honnappa, H.\BCBL \BBA Rao, V\BPBIA. \APACrefYearMonthDay2019. \BBOQ\APACrefatitleRisk-Sensitive Variational Bayes: Formulations and Bounds Risk-Sensitive Variational Bayes: Formulations and Bounds.\BBCQ \APACjournalVolNumPagesarXiv e-printsarXiv:1903.05220. \PrintBackRefs\CurrentBib

- Jiang \BBA Fu (\APACyear2015) \APACinsertmetastarJiang2015Quantile{APACrefauthors}Jiang, G.\BCBT \BBA Fu, M\BPBIC. \APACrefYearMonthDay2015. \BBOQ\APACrefatitleTechnical Note—On Estimating Quantile Sensitivities via Infinitesimal Perturbation Analysis Technical note—on estimating quantile sensitivities via infinitesimal perturbation analysis.\BBCQ \APACjournalVolNumPagesOperations Research632435-441. \PrintBackRefs\CurrentBib

- Jones \BOthers. (\APACyear1998) \APACinsertmetastarJones1998EI{APACrefauthors}Jones, D\BPBIR., Schonlau, M.\BCBL \BBA Welch, W\BPBIJ. \APACrefYearMonthDay1998\APACmonth12. \BBOQ\APACrefatitleEfficient Global Optimization of Expensive Black-Box Functions Efficient global optimization of expensive black-box functions.\BBCQ \APACjournalVolNumPagesJ. of Global Optimization134455–492. \PrintBackRefs\CurrentBib

- Kim \BOthers. (\APACyear2015) \APACinsertmetastarKim2015SAA{APACrefauthors}Kim, S., Pasupathy, R.\BCBL \BBA Henderson, S\BPBIG. \APACrefYearMonthDay2015. \BBOQ\APACrefatitleA Guide to Sample Average Approximation A guide to sample average approximation.\BBCQ \BIn M\BPBIC. Fu (\BED), \APACrefbtitleHandbook of Simulation Optimization Handbook of simulation optimization (\BPGS 207–243). \APACaddressPublisherNew York, NYSpringer New York. {APACrefDOI} \doi10.1007/978-1-4939-1384-8_8 \PrintBackRefs\CurrentBib

- Kleijnen (\APACyear2017) \APACinsertmetastarKLEIJNEN2017Kriging{APACrefauthors}Kleijnen, J\BPBIP. \APACrefYearMonthDay2017. \BBOQ\APACrefatitleRegression and Kriging metamodels with their experimental designs in simulation: A review Regression and kriging metamodels with their experimental designs in simulation: A review.\BBCQ \APACjournalVolNumPagesEuropean Journal of Operational Research25611 - 16. {APACrefDOI} \doihttps://doi.org/10.1016/j.ejor.2016.06.041 \PrintBackRefs\CurrentBib

- Kushner (\APACyear2010) \APACinsertmetastarKushner2010SA-Survey{APACrefauthors}Kushner, H. \APACrefYearMonthDay2010. \BBOQ\APACrefatitleStochastic approximation: a survey Stochastic approximation: a survey.\BBCQ \APACjournalVolNumPagesWiley Interdisciplinary Reviews: Computational Statistics2187-96. \PrintBackRefs\CurrentBib

- Kushner \BBA Yin (\APACyear2003) \APACinsertmetastarKushner&Yin2003SA{APACrefauthors}Kushner, H.\BCBT \BBA Yin, G. \APACrefYear2003. \APACrefbtitleStochastic Approximation and Recursive Algorithms and Applications Stochastic approximation and recursive algorithms and applications (\BVOL 35). \APACaddressPublisherSpringer-Verlag New York. \PrintBackRefs\CurrentBib

- Lan \BOthers. (\APACyear2010) \APACinsertmetastarLan2010CVaR{APACrefauthors}Lan, H., Nelson, B\BPBIL.\BCBL \BBA Staum, J. \APACrefYearMonthDay2010. \BBOQ\APACrefatitleA Confidence Interval Procedure for Expected Shortfall Risk Measurement via Two-Level Simulation A confidence interval procedure for expected shortfall risk measurement via two-level simulation.\BBCQ \APACjournalVolNumPagesOperations Research5851481-1490. {APACrefDOI} \doi10.1287/opre.1090.0792 \PrintBackRefs\CurrentBib

- Lange (\APACyear2010) \APACinsertmetastarLange2010{APACrefauthors}Lange, K. \APACrefYear2010. \APACrefbtitleNumerical Analysis for Statisticians Numerical analysis for statisticians (\PrintOrdinal2nd \BEd). \APACaddressPublisherSpringer, New York, NY. {APACrefDOI} \doi10.1007/978-1-4419-5945-4 \PrintBackRefs\CurrentBib

- Liu \BBA Hong (\APACyear2009) \APACinsertmetastarLiu&Hong2009Quantile-Kernel{APACrefauthors}Liu, G.\BCBT \BBA Hong, L\BPBIJ. \APACrefYearMonthDay2009. \BBOQ\APACrefatitleKernel estimation of quantile sensitivities Kernel estimation of quantile sensitivities.\BBCQ \APACjournalVolNumPagesNaval Research Logistics566511-525. {APACrefDOI} \doi10.1002/nav.20358 \PrintBackRefs\CurrentBib

- Nelder \BBA Mead (\APACyear1965) \APACinsertmetastarNelderMead1965{APACrefauthors}Nelder, J\BPBIA.\BCBT \BBA Mead, R. \APACrefYearMonthDay196501. \BBOQ\APACrefatitleA Simplex Method for Function Minimization A Simplex Method for Function Minimization.\BBCQ \APACjournalVolNumPagesThe Computer Journal74308-313. {APACrefDOI} \doi10.1093/comjnl/7.4.308 \PrintBackRefs\CurrentBib

- Peng \BOthers. (\APACyear2017) \APACinsertmetastarPeng2017Quantile{APACrefauthors}Peng, Y., Fu, M\BPBIC., Glynn, P\BPBIW.\BCBL \BBA Hu, J. \APACrefYearMonthDay2017. \BBOQ\APACrefatitleOn the asymptotic analysis of quantile sensitivity estimation by Monte Carlo simulation On the asymptotic analysis of quantile sensitivity estimation by monte carlo simulation.\BBCQ \BIn \APACrefbtitle2017 Winter Simulation Conference (WSC) 2017 winter simulation conference (wsc) (\BPG 2336-2347). \PrintBackRefs\CurrentBib

- Peng \BOthers. (\APACyear2018) \APACinsertmetastarPeng2018GLR{APACrefauthors}Peng, Y., Fu, M\BPBIC., Hu, J\BHBIQ.\BCBL \BBA Heidergott, B. \APACrefYearMonthDay2018. \BBOQ\APACrefatitleA New Unbiased Stochastic Derivative Estimator for Discontinuous Sample Performances with Structural Parameters A new unbiased stochastic derivative estimator for discontinuous sample performances with structural parameters.\BBCQ \APACjournalVolNumPagesOperations Research662487-499. {APACrefDOI} \doi10.1287/opre.2017.1674 \PrintBackRefs\CurrentBib

- Rahimian \BBA Mehrotra (\APACyear2019) \APACinsertmetastarrahimian2019dro-review{APACrefauthors}Rahimian, H.\BCBT \BBA Mehrotra, S. \APACrefYearMonthDay2019. \APACrefbtitleDistributionally Robust Optimization: A Review. Distributionally robust optimization: A review. \PrintBackRefs\CurrentBib

- Serfling (\APACyear2008) \APACinsertmetastarSerfling1980{APACrefauthors}Serfling, R\BPBIJ. \APACrefYear2008. \APACrefbtitleApproximation Theorems of Mathematical Statistics Approximation theorems of mathematical statistics. \APACaddressPublisherWiley-Blackwell. {APACrefDOI} \doi10.1002/9780470316481 \PrintBackRefs\CurrentBib

- Song \BOthers. (\APACyear2014) \APACinsertmetastarSong2014Input-uncertainty{APACrefauthors}Song, E., Nelson, B\BPBIL.\BCBL \BBA Pegden, C\BPBID. \APACrefYearMonthDay2014. \BBOQ\APACrefatitleAdvanced tutorial: Input uncertainty quantification Advanced tutorial: Input uncertainty quantification.\BBCQ \BIn \APACrefbtitleProceedings of the Winter Simulation Conference 2014 Proceedings of the winter simulation conference 2014 (\BPG 162-176). {APACrefDOI} \doi10.1109/WSC.2014.7019886 \PrintBackRefs\CurrentBib

- Tamar \BOthers. (\APACyear2015) \APACinsertmetastarTamar2015CVaR{APACrefauthors}Tamar, A., Glassner, Y.\BCBL \BBA Mannor, S. \APACrefYearMonthDay2015. \BBOQ\APACrefatitleOptimizing the CVaR via Sampling Optimizing the cvar via sampling.\BBCQ \BIn \APACrefbtitleProceedings of the Twenty-Ninth AAAI Conference on Artificial Intelligence Proceedings of the twenty-ninth aaai conference on artificial intelligence (\BPGS 2993–2999). \APACaddressPublisherAAAI Press. \PrintBackRefs\CurrentBib

- H. Wang \BOthers. (\APACyear2020) \APACinsertmetastarWang2020BOBRO{APACrefauthors}Wang, H., Yuan, J.\BCBL \BBA Ng, S\BPBIH. \APACrefYearMonthDay2020. \BBOQ\APACrefatitleGaussian process based optimization algorithms with input uncertainty Gaussian process based optimization algorithms with input uncertainty.\BBCQ \APACjournalVolNumPagesIISE Transactions524377-393. {APACrefDOI} \doi10.1080/24725854.2019.1639859 \PrintBackRefs\CurrentBib

- Y. Wang \BOthers. (\APACyear2012) \APACinsertmetastarWang2012SLRIPA{APACrefauthors}Wang, Y., Fu, M\BPBIC.\BCBL \BBA Marcus, S\BPBII. \APACrefYearMonthDay2012. \BBOQ\APACrefatitleA New Stochastic Derivative Estimator for Discontinuous Payoff Functions with Application to Financial Derivatives A new stochastic derivative estimator for discontinuous payoff functions with application to financial derivatives.\BBCQ \APACjournalVolNumPagesOperations Research602447-460. {APACrefDOI} \doi10.1287/opre.1110.1018 \PrintBackRefs\CurrentBib

- Wu \BOthers. (\APACyear2018) \APACinsertmetastarwu2018BRO{APACrefauthors}Wu, D., Zhu, H.\BCBL \BBA Zhou, E. \APACrefYearMonthDay2018. \BBOQ\APACrefatitleA Bayesian Risk Approach to Data-driven Stochastic Optimization: Formulations and Asymptotics A bayesian risk approach to data-driven stochastic optimization: Formulations and asymptotics.\BBCQ \APACjournalVolNumPagesSIAM Journal on Optimization2821588-1612. {APACrefDOI} \doi10.1137/16M1101933 \PrintBackRefs\CurrentBib

- Zhou \BBA Wu (\APACyear2017) \APACinsertmetastarZhou2017book-chapter{APACrefauthors}Zhou, E.\BCBT \BBA Wu, D. \APACrefYearMonthDay2017. \BBOQ\APACrefatitleSimulation Optimization Under Input Model Uncertainty Simulation optimization under input model uncertainty.\BBCQ \BIn A. Tolk, J. Fowler, G. Shao\BCBL \BBA E. Yücesan (\BEDS), \APACrefbtitleAdvances in Modeling and Simulation: Seminal Research from 50 Years of Winter Simulation Conferences Advances in modeling and simulation: Seminal research from 50 years of winter simulation conferences (\BPGS 219–247). \APACaddressPublisherSpringer International Publishing. {APACrefDOI} \doi10.1007/978-3-319-64182-9_11 \PrintBackRefs\CurrentBib

- Zhou \BBA Xie (\APACyear2015) \APACinsertmetastarzhou2015BRO{APACrefauthors}Zhou, E.\BCBT \BBA Xie, W. \APACrefYearMonthDay2015. \BBOQ\APACrefatitleSimulation Optimization when Facing Input Uncertainty Simulation optimization when facing input uncertainty.\BBCQ \BIn \APACrefbtitleProceedings of the 2015 Winter Simulation Conference Proceedings of the 2015 winter simulation conference (\BPGS 3714–3724). \APACaddressPublisherIEEE Press. \PrintBackRefs\CurrentBib

- C. Zhu \BOthers. (\APACyear1997) \APACinsertmetastarZhu1997LBFGS{APACrefauthors}Zhu, C., Byrd, R\BPBIH., Lu, P.\BCBL \BBA Nocedal, J. \APACrefYearMonthDay1997\APACmonth12. \BBOQ\APACrefatitleAlgorithm 778: L-BFGS-B: Fortran Subroutines for Large-Scale Bound-Constrained Optimization Algorithm 778: L-bfgs-b: Fortran subroutines for large-scale bound-constrained optimization.\BBCQ \APACjournalVolNumPagesACM Trans. Math. Softw.234550–560. {APACrefDOI} \doi10.1145/279232.279236 \PrintBackRefs\CurrentBib

- H. Zhu \BOthers. (\APACyear2020) \APACinsertmetastarZhu2017input-uncertainty{APACrefauthors}Zhu, H., Liu, T.\BCBL \BBA Zhou, E. \APACrefYearMonthDay2020. \BBOQ\APACrefatitleRisk Quantification in Stochastic Simulation under Input Uncertainty Risk quantification in stochastic simulation under input uncertainty.\BBCQ \APACjournalVolNumPagesACM Trans. Model. Comput. Simul.301. {APACrefDOI} \doi10.1145/3329117 \PrintBackRefs\CurrentBib