Is there a Golden Parachute

in Sannikov’s principal–agent problem?111We are grateful to Yuliy Sannikov for his insightful comments on the first version of this paper. This work benefited from support of the ANR project PACMAN ANR–16–CE05–0027.

Abstract

This paper provides a complete review of the continuous-time optimal contracting problem introduced by Sannikov [52], in the extended context allowing for possibly different discount rates for both parties. The agent’s problem is to seek for optimal effort, given the compensation scheme proposed by the principal over a random horizon. Then, given the optimal agent’s response, the principal determines the best compensation scheme in terms of running payment, retirement, and lump-sum payment at retirement.

A Golden Parachute is a situation where the agent ceases any effort at some positive stopping time, and receives a payment afterwards, possibly under the form of a lump sum payment, or of a continuous stream of payments. We show that a Golden Parachute only exists in certain specific circumstances. This is in contrast with the results claimed by Sannikov [52], where the only requirement is a positive agent’s marginal cost of effort at zero. Namely, we show that there is no Golden Parachute if this parameter is too large. Similarly, in the context of a concave marginal utility, there is no Golden Parachute if the agent’s utility function has a too negative curvature at zero.

In the general case, we prove that an agent with positive reservation utility is either never retired by the principal, or retired above some given threshold (as in Sannikov’s solution). We show that different discount factors induce a face-lifted utility function, which allows to reduce the analysis to a setting similar to the equal–discount rates one. Finally, we also confirm that an agent with small reservation utility does have an informational rent, meaning that the principal optimally offers him a contract with strictly higher utility than his participation value.

Key words: continuous-time principal–agent, optimal control and stopping, face-lifting.

1 Introduction

Principal–agent problems naturally stem from questions of optimal contracting between two parties, a principal (‘she’) and an agent (‘he’), when the agent’s effort cannot be observed or contracted upon. Mathematically, they are formulated as a Stackelberg non–zero sum game, and can also be identified to bi-level optimisation problems in the operations research literature. The number of articles related to this topic is staggering, mainly due to the wide spectrum of concrete problems where this theory is able to provide relevant results, for instance for moral hazard problem in microeconomics with applications to corporate governance, portfolio management, and many other areas of economics and finance.

The first, and seminal, paper on principal–agent problems in continuous-time is by Holmström and Milgrom [30], who show that the optimal contract is linear in the output process, in a finite horizon setting with CARA utility functions for both parties, and when the agent’s effort impacts solely the drift of the output process. This paper is the first to highlight that optimal contracting problems tend to be easier to address in continuous-time, an observation which has been confirmed by the large continuous-time literature in this area. Holmström and Milgrom’s work was extended by Schättler and Sung [54], Sung [64, 65], Müller [41, 42], and Hellwig and Schmidt [28, 27]. While the aforementioned papers use continuous-time extensions of the celebrated first-order approach from the contract theory literature in static cases, see for instance Rogerson [50], the papers by Williams [69, 70, 71] and Cvitanić, Wan, and Zhang [14, 15, 16] use the stochastic maximum principle and forward–backward stochastic differential equations to characterise the optimal compensation for more general utility functions, see also the excellent monograph by Cvitanić and Zhang [13].444Other early continuous-time contract theory models were proposed by Adrian and Westerfield [1], Biais, Mariotti, Plantin, and Rochet [3], Biais, Mariotti, Rochet, and Villeneuve [4], Biais, Mariotti, and Rochet [5], Capponi and Frei [8], DeMarzo and Sannikov [20], DeMarzo, Fishman, He, and Wang [21], Fong [22], He [26], Hoffmann and Pfeil [29], Ju and Wan [32], Keiber [34], Leung [36], Mirrlees and Raimondo [40], Myerson [43], Ou-Yang [44], Pagès [45], Pagès and Possamaï [46], Piskorski and Tchistyi [48], Piskorski and Westerfield [49], Sannikov [51], Schroder, Sinha, and Levental [56], Van Long and Sorger [67], Westerfield [68], Zhang [72], Zhou [73], or Zhu [74].

The seminal work of Sannikov [52], see also [53], represents a genuine breakthrough in this vast literature from various perspectives. First, from the methodological viewpoint, Sannikov introduced the idea to focus on the dynamic continuation value of the agent as a state variable for the principal’s problem. Although this idea was already acknowledged throughout the discrete-time literature on this problem, an illuminating example being Spear and Srivastava [61], its systematic implementation in continuous-time offers an elegant solution approach by means of a representation result of the dynamic value function of the agent. Second, the infinite horizon setting considered by Sannikov revealed remarkable economic implications. Indeed, the main conclusions are that the principal optimally retires the agent, offering him a Golden Parachute, that is to say a lifetime constant continuous stream of consumption, when his continuation utility reaches a sufficiently high level, and that an agent with small reservation utility possesses an informational rent, in the sense that he is offered a contract with strictly higher value.

The main objective of our paper is twofold. First, we revisit Sannikov’s seminal work, though putting a stronger weight on technical rigour, which is unfortunately lacking in some key parts of [52]. We would like to emphasise that this should not be seen in any case as a reason to underestimate the importance of this paper, given the groundbreaking novelties recalled above. In contrast, our first aim is to try and contribute even more to the success of [52] by making it more accessible to a wider community of mathematicians and economists, whose overall understanding of the model may be hindered by the technical gaps in [52]. Notice that we are not the first to try and obtain rigorously the results claimed in [52]. For instance, Strulovici and Szydlowski [63, Section 4.3] offer a more rigorous take on the existence of optimal contracts in the model. However, the authors take for granted the fact that [52] proves that the HJB equation for the principal’s problem has a smooth solution, while we will argue that the proof has important gaps. Similarly, the unpublished PhD thesis of Choi [11] aims at putting the problem on rigorous foundations. Nonetheless, existence of optimal contracts is not addressed there, and the results rely on the assumption that it is never optimal to retire the agent temporarily, while our approach actually proves that this is the case. We also would like to refer to the recent work of Décamps and Villeneuve [19], where the authors study a related, but different, contracting problem, and where again the heart of the analysis is technical clarity: this should be an additional illustration that proving rigorously results in this literature is a challenging task.

Our second goal is to prove that our analysis extends beyond the case where the principal and the agent have the same discount rates. It is an important feature, as most models555Exceptions are the recent work by Hajjej, Hillairet, and Mnif [25], where the agent is risk-averse and more impatient than the principal. However, they do not obtain clear results saying that the hypotheses of their verification result [25, Theorem 4.3] can be verified in practice, as well as the work of Lin, Ren, Touzi, and Yang [37], but there the emphasis is more on obtaining general methods to attack infinite horizon moral hazard problems. in the discrete- or continuous-time literature either allow for risk-averse agents who are as patient as the principal, as in Sannikov [52], Fong [22], Myerson [43], and Hajjej, Hillairet, Mnif, and Pontier [24], or for more impatient, but risk-neutral agents, as in DeMarzo and Sannikov [20], Biais, Mariotti, Plantin, and Rochet [3], Biais, Mariotti, Rochet, and Villeneuve [4], Biais, Mariotti, and Rochet [5], He [26], Piskorski and Tchistyi [48], Piskorski and Westerfield [49], DeMarzo, Fishman, He, and Wang [21], Pagès and Possamaï [46], or Williams [71]. Even more surprisingly, our analysis can also accommodate the case where the principal is actually strictly more impatient than the agent. As far as we know, our paper is the first offering such a comprehensive analysis.

Our main findings are the following. First, in contrast with the overall message from [52], we show that a Golden Parachute may fail to exist in some specific situations. It never happens if the agent’s marginal cost of effort at zero is zero, or is sufficiently large. And it never happens if the agent’s marginal utility is also concave, and his utility function has sufficiently large negative curvature at zero, with a level depending on the marginal cost of effort at zero. We also highlight the fact that there are three regimes, depending on whether the agent is strictly more impatient than the principal or not:

-

when the principal is much more impatient than the agent (the actual bound depends on the level of risk-aversion of the agent), the problem degenerates, optimal contracts cease to exist, and the principal can achieve her first-best value with appropriately defined sequences of incentive-compatible contracts;

-

when the principal is still more impatient than the agent, but above the aforementioned threshold, and the agent’s marginal cost of effort at zero is positive, a Golden Parachute is likely to exist, in the sense that we know that for a large enough continuation utility of the agent, the value of the principal coincides with the value she would obtain by offering a Golden Parachute. Then, the only way a Golden Parachute could fail to exist is when these two functions are equal everywhere, so that the contract does not even start. We also provide sufficient conditions, combining the curvature of the agent’s utility function at zero and his marginal cost of effort at zero, for an informational rent to exist;

-

when the agent is strictly more impatient than the principal, we do not know whether the two functions mentioned in coincide or not, and some numerical evidence seems to indicate that they could fail to do so in general. Besides, we prove that in this case, the value of the principal is non-increasing with respect to the continuation utility of the agent, meaning that an informational rent cannot exist.

We emphasise that our rigorous presentation involves advanced tools from stochastic control theory and partial differential equations. In particular, the justification of the solution claimed by Sannikov in [52] requires an in-depth analysis of the first-best solution, combined with the theory of viscosity solutions, and it is unclear to us how the proof could be significantly simplified.

Finally, from the methodological and theoretical point of view, we have highlighted a novel phenomenon in (properly renormalised) moral hazard problems with risk-aversion and different discount rates, where the principal’s problem has an optimal stopping component, in the sense that she can terminate the contract. Indeed, we prove that the problem could actually be treated as in the case with similar discount rates, provided that the lump sum payment in the principal’s problem be evaluated through an appropriate face-lifted version of the agent’s inverse utility function. The last function is obtained as the value function of the best termination time of the contract when the agent ceases any effort. We believe that this finding in the context of the present contracting problem applies to a wider class of moral hazard problems with early retirement possibilities.666The ’face-lifting’ phenomenon corresponds to the so-called boundary layer effect in singular optimal control problems, and appeared naturally in various pricing problems in finance, either with hedging constraints or market frictions, see for instance Broadie, Cvitanić, and Soner [7], Bouchard and Touzi [6], Chassagneux, Élie, and Kharroubi [9], Guasoni, Rásonyi, and Schachermayer [23], Soner and Touzi [57, 58, 59, 60], Cheridito, Soner, and Touzi [10], and Schmock, Shreve, and Wystup [55], or for utility maximisation problems, see Larsen, Soner, and Žitković [35]. However all these references consider either ‘pure’ optimal control or stochastic target problems, while in our context, the face-lifting phenomenon occurs because of an optimal stopping problem, and is therefore of a different nature.

The paper is organised as follows. Section 2 provides a rigorous formulation of the continuous-time contracting problem, with a clear description of the set of contracts, and introduces the face-lifted utility . Our main results are given in Section 3. As such, Section 3.1 gives all our results on the first- and second-best problems, while Section 3.2 provides some conditions under which no Golden Parachute can exist. Next, Section 3.3 presents our numerical illustrations, and Section 3.4 discusses the gaps in [52]. The subsequent sections are dedicated to the proofs of our main results: Section 4 concentrates on the first-best problem, while Section 5 uses the result of Lin, Ren, Touzi, and Yang [37], itself an extension of earlier results by Cvitanić, Possamaï, and Touzi [17, 18], which justify rigorously Sannikov’s [52] remarkable reduction of the principal’s Stackelberg game problem into a standard control-and-stopping problem. Such a reduction opens the door for the use of standard tools of stochastic control theory. In particular, we treat the case of a very impatient principal in Section 6, which can be addressed directly by exhibiting a sequence of contracts inducing a degenerate situation where both parties achieve as large a payment as possible. The alternative case of reasonably impatient principal is analysed by means of the corresponding dynamic programming equation introduced in Section 7, where we also provide a verification result following the standard theory. In Section 8, we provide a rigorous analysis of the dynamic programming equation, and we isolate a set of conditions which guarantee that the solution is of the form claimed in [52].

2 Sannikov’s contracting problem

2.1 Output process, agent’s effort, and contract

This section reports our understanding of the continuous time contracting model in Sannikov [52]. Let be a probability space carrying a one-dimensional –Brownian motion . For fixed parameters and , the output process is defined by

We denote by the -augmentation of the natural filtration of (or equivalently, of ), which is known to satisfy the usual conditions. We next introduce distributions of the output process under effort , so as to induce the dynamics , for some –Brownian motion . This is naturally accomplished by means of the following argument based on the Girsanov transformation. Let be the collection of all -predictable processes with values in a compact subset of , containing . For all , we may introduce an equivalent probability measure so that the process is a –Brownian motion, and the process can be written in terms of as

Any is called an effort process, and is interpreted as an action exerted in order to affect the distribution of the output process from to . A contract is a triple , where , the set of all –stopping times, is a non-negative -measurable random variable, and , the set of -predictable non-negative processes. Here, represents a retirement time, is a process of continuous payment rate until retirement, and is a lump-sum payment at retirement, which may be interpreted as a Golden Parachute in the terminology of Sannikov [52], see Definition 2.4 below.

We shall introduce later in Section 2.5 the collection of admissible contracts, by imposing some integrability requirements. These contracts allow to formulate the contracting problem which sets the terms of the delegation by the principal (she) of the output process to the agent (he). Namely, the principal seeks to design the optimal contract so as to guarantee that the agent best serves her objectives, while optimising his own interest.

2.2 The agent’s problem

The agent preferences are defined by

-

•

a utility function which is increasing, strictly concave, twice continuously differentiable on , satisfies together with the (one-sided) Inada condition and the growth condition

(2.1) which implies that , and , for any , and for some ;777It should be clear that our specification for is tailored to a power utility function of the form , , for some , though we strictly speaking only require such a behaviour at .

-

•

a cost function , increasing, strictly convex, continuously differentiable, with ;

-

•

a fixed discount rate .

Given a contract and , the utility obtained by the agent is defined by the problem

| (2.2) |

As , and is bounded, notice that is well-defined. Moreover, as the agent is allowed to choose zero effort, inducing , it follows that for any proposed contract . We denote by

the (possibly empty) set of all optimal responses of the agent. The agent only accepts contracts which provide him with a utility above a fixed threshold , where , called participation level. Thus he considers contracts in the subset

Observe that the final lump-sum utility for the agent can be written as , so that it can be equivalently implemented by the payment of the lifetime consumption after retirement at time . We shall comment further on this normalisation in Remark 2.3 below.

2.3 The principal’s problem

The principal is risk-neutral with the objective of maximising her overall revenue induced by the agent’s effort

where we extend [52], allowing the principal to have a possibly different discount rate from that of the agent. Observe that for any , . Then, by standard Itô integration theory, we have for all stopping time , implying that

which is well-defined in , due to the boundedness of and the non-negativity of and . We also notice again that the lump-sum payment at time can be rewritten as , and so it can be implemented by the lifetime payment at rate after , in agreement with the corresponding interpretation in the agent’s problem.

The principal’s problem is defined as follows: anticipating the agent’s optimal response, she chooses the contract which best serves her objective under the participation constraint

| (2.3) |

2.4 Reformulation and face-lifted utility

We next re-write our contracting problem equivalently by using the opposite of the inverse of the agent’s utility

Then, denoting and , the criterion of the agent becomes

| (2.4) |

where we abuse notations and indifferently identify as a contract the triplet , or the triplet . We will use this identification implicitly throughout the paper. As for the principal, we have

Here, the (negative) reward of the principal by stopping at is . Our first result shows that in general, the principal may be able to improve her reward by not ending the contract at some time with a lump-sum payment to the agent, but by instead discouraging the agent from exerting any efforts (which can be understood as an alternative way of ending the contract), and offering him a continuous consumption. The improved (or face-lifted, hereafter) reward is naturally defined by means of the following deterministic control problem

| (2.5) |

where is the set of Borel-measurable maps from to , and for all

and the state process is defined by the controlled first-order ODE

| (2.6) |

To better understand the expression (2.5) for the improved payment, notice that for any , direct integration of this linear ODE leads to

meaning that for a given state of the world , the agent is indifferent between a lump-sum payment at some retirement time , and a continuous payment on the time interval , with zero effort on this time interval, and a retirement deferred to , where the lump-sum payment is now . The restriction on such deferral policies is induced by the fact that the agent is protected by limited liability, and therefore can only receive non-negative payments. The idea is that while the agent is indifferent between these two alternatives, the discrepancy between the discount rates may be such that the principal can actually benefit from postponing retirement.

An immediate consequence is that the value function of the principal can be expressed in its relaxed formulation as

| (2.7) |

where , for some subset defined in Section 2.5 below. The following result states the equivalence of our original contracting problem888As observed by Yuliy Sannikov in private communication, the principal problem may be directly defined by the relaxed formulation (2.7). with , and characterises the face-lifted reward in closed form in terms of the concave conjugate functions

Notice that on , and on . Moreover, our conditions (2.1) on the agent’s utility function is immediately converted for into

| (2.8) |

Proposition 2.1.

We have , and denoting , the face-lifted reward function satisfies

if , we have

if , we have , if , and otherwise, under the additional condition that exists,

| (2.9) |

In particular is decreasing, strictly concave, , and satisfies similar bounds to (2.8), with appropriate positive constants , and , which translate into bounds on similar to those in (2.1), with appropriate positive constants , and . Moreover, the supremum over in (2.5) is attained at , meaning that

| (2.10) |

The equality in Proposition 2.1 is a direct consequence of our definition of admissible contracts in Section 2.5 below. The remaining claims are proved in Appendix A, and provide the following significant results. In the case considered by Sannikov [52], the principal never gains by postponing retirement and allowing the agent to produce zero effort for a while. On the other hand, when , and is not too large, it is always optimal to postpone retirement and is a non-trivial majorant of . Finally, when the principal becomes a lot more impatient than the agent, we actually have , meaning that she can bring back the cost of permanently retiring the agent to .

Example 2.2.

Remark 2.3.

The normalisation of the running rewards of the principal and the agent by their corresponding discount rates in Equation 2.2 and Equation 2.3, is not fundamental, per se. However, the face-lifted principal’s benefit function plays a crucial role to relate equivalent formulations of the problem. Consider for instance the agent’s criterion

which differs from in (2.2) by the form of discount factor instead of . Similarly, change the principal’s criterion to

Then, following the same argument, the corresponding face-lifted utility function is

with controlled state satisfying for any , , and , . The corresponding Hamilton–Jacobi equation is

In particular, in the case of equal discount rates, we see immediately that , , is a solution of this equation. Consequently the decision of retiring the agent should be discussed by comparing the principal’s value function to instead of in this case, see Definition 2.4 below. In this sense, the setting of [52] is the only parametrisation of the problem with for which the face-lifted retirement reward function coincides with .

2.5 Admissible contracts and Golden Parachute

For technical reasons, we introduce further integrability conditions which guarantee that both criteria of the agent and the principal are finite, and more importantly, allow to apply the reduction result of Lin, Ren, Touzi, and Yang [37]. We denote by the collection of all contracts , satisfying in addition the following integrability condition

| (2.11) |

for some . In order to guarantee that the equality of Proposition 2.1 holds, we define the set as the collection of all triples such that

for some , and -measurable with values in , and with values in .

We now introduce the notion of Golden Parachute which has two different meanings in our relaxed formulation (2.7):

-

in Sannikov’s formulation, the retirement time is not explicitly involved in the model formulation. Instead, a Golden Parachute is defined as a stopping time such that the agent exerts no effort while receiving a constant consumption on ;

-

our definition of contracts includes a retirement time , and we may naturally define a situation of Golden Parachute by and , –a.s.

Definition 2.4.

We say that the contracting model exhibits a Golden Parachute, if there exists an optimal contract for the relaxed formulation of the principal’s problem (2.7) such that , and .

In other words, a Golden Parachute corresponds to a situation where there is a high-retirement point for the agent, with either lump-sum payment at retirement or continuous payment after retirement, where retirement means that the agent ceases to exert any effort forever.

2.6 The first-best contracting problem

We conclude this section with the formulation of the first-best version of the contracting problem

where consists of all contracts where is a stopping time with values in , and satisfy the integrability condition of (2.11). By definition of and , we observe that we have

| (2.12) |

The corresponding notion of Golden Parachute is naturally defined in the context of the present first-best contracting problem similar the second-best setting.

3 Main results

3.1 Complete solution of the contracting problems

We first provide a complete solution of the first-best contracting problem which has a different nature depending on the relative value of the agent’s and the principal’s discount rates . Namely, the principal’s first-best contracting problem is degenerate in the case , in the sense that the principal achieves the maximal value by means of a sequence of admissible contracts which offer no intermediate payments, incite the agent to exert maximal effort at all times, and offer him a large lump-sum payment at large retirement time. In the alternative case , the problem does not degenerate any longer, and we shall express its solution in terms of the convex dual of the function

Notice that the expression of in terms of is exactly the same of that of in terms of in Proposition 2.1..

Theorem 3.1.

(First-best contracting)

If , then, , and there is no admissible contract which achieves this value.

If , then

-

-

, with infimum achieved at the unique solution of the first order condition .

-

-

, and if and only if . In this case the first-best optimal contract sets the agent to his participation constraint, and is given by

-

-

Denoting , we have

In particular

if and , we have and therefore a Golden Parachute exists for the first-best contracting problem;

otherwise if or , we have on and there is no first-best Golden Parachute.

Remark 3.2.

Theorem 3.1.- states that when and , the first-best value function coincides with after the finite value . As the value function at the origin is , this shows that a first-best Golden Parachute exists in this case.

By Equation 2.12, we also have in the case and that whenever . However, we shall see that . Therefore, unlike the first-best situation in , we cannot discard the possibility that the second-best contracting principal’s value coincides everywhere with , see Section 3.2.

We next focus on the second-best contracting problem. Recall from Proposition 2.1 that when . Our first result shows that, similar to the first-best situation of Theorem 3.1, the solution of the contracting problem is degenerate in this case. We prove this by exhibiting a sequence of admissible contracts which induces a utility as large as we want for the agent, and reaches the highest possible level for the principal, namely . Roughly speaking, these contracts make small intermediate payments, enforce the highest possible effort for the agent at all times, and promise to pay him an extremely high value after an extremely long time. By exploiting the large discrepancy between the discount rates of the agent and the principal, we show that the continuation utilities of both parties reach their maximum.

The case is more interesting. Similar to Sannikov [52], we denote by the maximal value obtained by the principal when the utility of the agent is held at the level . We provide a characterisation of this function and of the solution of the contracting problem by means of the second-order differential equation

| (3.1) |

where the second-order differential operator is given by

| (3.2) |

and denotes the subgradient of the convex dual of :

| (3.3) |

The following assumption is needed for our main results concerning the second-best contracting problem.

Assumption 3.3.

is concave, and

-

•

if , then , and satisfies

-

•

if , then exists.

Notice that inherits the concavity of . To see this, recall from standard convex duality that the concavity of is equivalent to that of . Then, it follows from the expression of in (2.9) that is concave, which then implies that is concave. We shall provide more comments on these assumptions in Remark 3.6 below.

Theorem 3.4.

(Second-best contracting) Let 3.3 hold.

-

Let . Then , and there is no optimal contract achieving this value.

-

Let , and define the stopping region . Then, under 3.3, we have

-

-

the principal’s value function is the unique viscosity solution of (3.1), in the class of functions such that , , for some

-

-

, is strictly concave, ultimately decreasing, and on , except at at most one point. Moreover , and whenever and , we have .

-

-

if and , then there is always some such that

-

-

more generally, for some

-

-

if for some , then

and the supremum is attained at some . Let be a measurable maximiser of , and a measurable minimiser of , then there exists a unique weak solution to the SDE corresponding to see Equation 5.2 for the definition of this process. In particular, defining

the contract is an optimal contract for the relaxed principal problem (2.7).

-

-

Remark 3.5.

Theorem 3.4.- states that is non-increasing when so that, unlike the findings of Sannikov when , no informational rent exists in this case, i.e. the agent’s value function is never above the requested participation value . An informational rent can only exist when , and it does exist when and is sufficiently small.

In the case , Sannikov [52, pp. 959] mentions that if ?the agent had a higher discount rate than the principal, then with time the principal’s benefit from output outweighs the cost of the agent’s effort,? and that ?it is sensible to avoid permanent retirement by allowing the agent to suspend effort temporarily.?. Our result shows that, under the assumption that is concave, this statement is not correct.

As explained in Remark 3.2., Theorem 3.4.- does not directly imply that when and , a Golden Parachute automatically exists, since even if is then always finite, it could still be that . If indeed, , then the claim made by Sannikov in the case that a Golden Parachute always exists is correct, and can be extended to and . However, in the case , it is unclear in general whether is finite or not, and we do not have sufficient conditions under which it is though we present conditions under which in Section 3.2.

The case is not covered by Theorem 3.4.-–-, due to the fact that in this case, the optimal retirement time may be infinite with positive probability, and therefore cannot satisfy the integrability requirement in Equation 2.11. This is however not a critical issue. Indeed, these integrability conditions on admissible stopping times are taken from the general result in [37]. But a detailed reading of their arguments shows that they only require it in order to be able to treat moral hazard problems where the agent is allowed to control the volatility of the output process, for which they need a theory for second-order backward SDEs with random horizon, which is obtained in Lin, Ren, Touzi, and Yang [38], but does not allow for infinite horizon. In our problem of interest, the agent only controls the drift of , meaning that the classical theory of backward SDEs is sufficient, and these objects are known to be well-posed even with infinite horizon, see for instance Papapantoleon, Possamaï, and Saplaouras [47]. With these results in hand, we can straightforwardly extend the general reduction result of Section 5 to include possibly infinite retirement times, and then obtain a verification result general enough to cover these situations. As this is not central to our message, we refrain to go to this level of generality.

Remark 3.6.

The concavity of means that the risk aversion of the agent is large enough in the power utility setting of Example 2.2, it is equivalent to . Mathematically, this assumption allows to prove that the value function of the principal inherits this property, which in turn is a sufficient condition to ensure that whenever it touches , it coincides with it forever, see Lemma 8.1.. Economically, this means that the principal never retires temporarily the agent.

The raison d’être of this assumption is that it is crucial in our proof of regularity for the value function of the principal. We emphasise that our results could be generalised to accommodate the possibility for the principal to temporarily retire the agent when his continuation utility belongs to finitely many intervals, since our main issue is that without it, we cannot in general rule out the possibility that and could have uncountably many contact points on some compact interval, and the regularity becomes then a very unclear issue, at least to us. We have however refrained from doing this, since we do not have a satisfactory sufficient condition under which we could prove that there are strictly more than one, but finitely many contact points.

The case requires additional conditions in order to ensure that the value function of the principal has a concave first-order derivative, see Step in the proof of Lemma 8.3 . The condition allows to prove using Theorem 3.1.- that outside a compact set, which in turn allows us to prove the required technical comparisons theorems in Appendix B on such a compact set. We believe that the argument can be extended to the general case , but we refrained from doing so for simplicity.

Example 3.7.

The condition on the derivatives of in 3.3 is satisfied if and only

-

•

and , for , ;

-

•

, for .

3.2 Some cases of non-existence of a Golden Parachute

This section specialises the discussion to the economic question of whether a Golden Parachute is optimal in the second-best optimal contracting problem. In particular, our results here contrast with the main findings of Sannikov [52] that a Golden Parachute always exists whenever and . We exploit here the observation that , so that if and only if . As both and are concave in our context, it follows that the map is non-increasing on . Consequently the existence of a Golden Parachute means that solves Equation 3.1 for sufficiently large , but fails to solve it on a right-neighbourhood of . Equivalently, there is No Golden Parachute (NGP) in either one of the following cases

-

, on , so that in this case on

-

, so that in this case on .

We observe that may hold in the context of Theorem 3.4 where it is stated that for values larger than , so that there is no Golden Parachute despite the fact that coincides with , see Example 3.10 below. The following result provides a sufficient conditions for to hold.

Proof.

Since contains an interval, is strictly convex, is concave, and , we have that

Now notice that since , the derivative at of the map inside the supremum above is equal to . Therefore, this map is increasing on a right-neighbourhood of , and thus for any , we have .

∎

Remark 3.9.

Assume for simplicity that , then by Proposition 2.1. Then

so that, as is concave, the existence of a Golden Parachute implies that . In other words, Proposition 3.8 states that holds for sufficiently large .

Example 3.10.

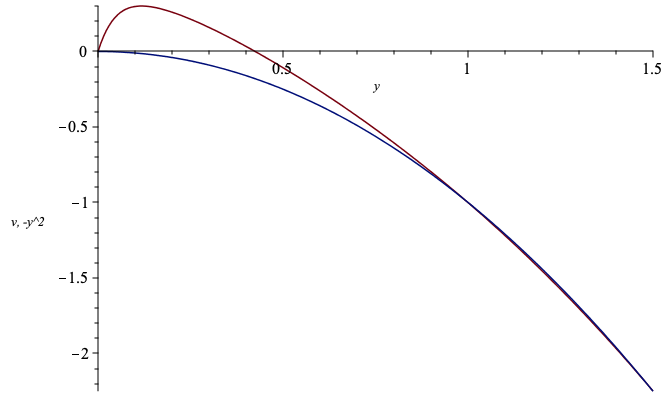

Sannikov [52, Figure 1] considers the situation , so that , and

Notice that, given Sannikov’s conclusion that a Golden Parachute exists, the unboundedness of is not problematic, as the optimal effort remains bounded, so that the problem is unchanged by restricting to the corresponding compact subset of . Under the present specification, we have

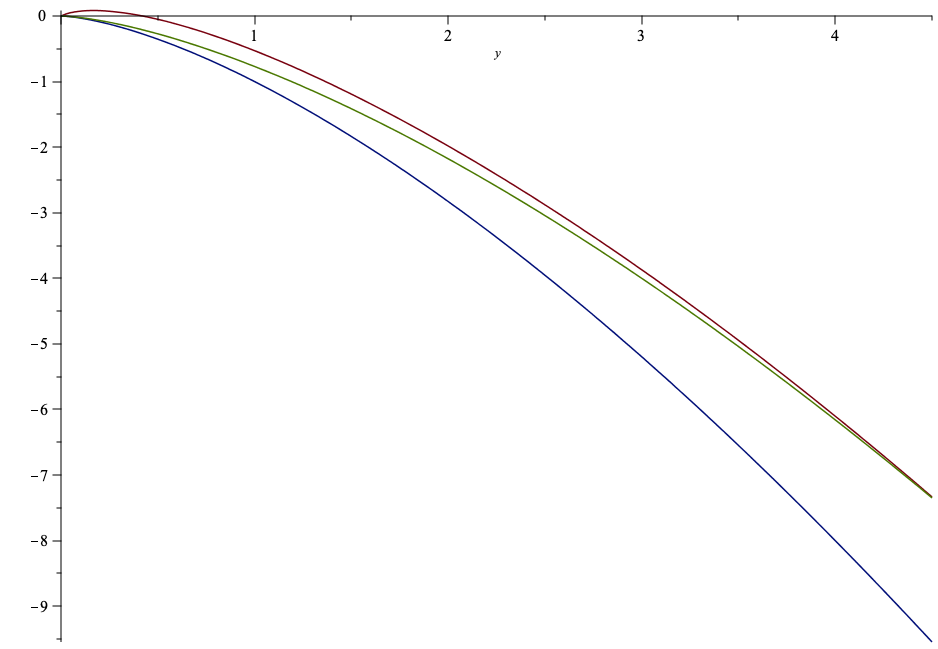

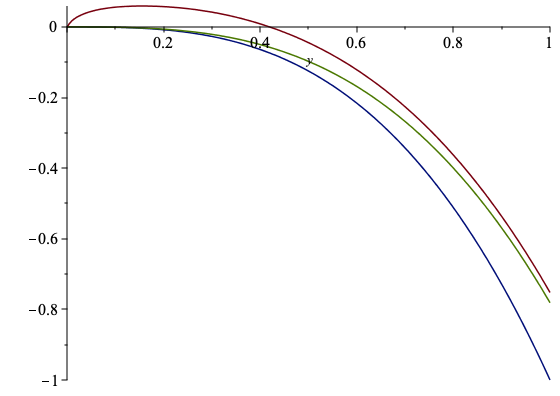

3.3 Numerical illustration

We next provide some numerical results with the cost of effort function from Example 3.10, and utility function . We of course choose the model parameters so that is not satisfied, since in this case the solution is everywhere. Figure 1 takes the parameters in [52] (with , , , , and ), and shows the archetypical case where a Golden Parachute exists.

The next two sets of figures show what happens when . More precisely, Figure 2(a) (with , , , and ) shows a case where becomes equal to after a while and a Golden parachute does exist, while, at least numerically, Figure 2(b) (with , , , and ), seems to show that remains always above , and that no Golden Parachute exists.

3.4 Sannikov’s solution

In this subsection, we specialise the discussion to the case as in [52]. Notice that the HJB equation considered by Sannikov in [52, Equation ] is the same as our Equation 3.1 when restricted to the continuation region

which corresponds to the natural guess that the stopping region is of the form , with some free boundary point to be determined so as to guarantee that the smooth-fit condition holds. Such a guess is more naturally justified by the optimal stopping component of the principal’s problem in our formulation. We shall also see that it is necessary in order to apply the verification argument of Proposition 7.2 below (which in fact requires regularity and except at a zero measure set of points).

A few pages later, namely in [52, Equation ], the author rewrites this ODE with instead of

| (3.4) |

This is motivated by the natural guess that the principal is expected to induce a positive effort for the agent on the continuation region. More importantly, direct manipulations allow to reformulate the last equation equivalently as

| (3.5) |

thus reducing the equation to an explicit non-linear second-order ODE under the additional restriction of a positive marginal cost of effort, that is to say when .

Next, assuming that , the potential explosion of the solution due to the super-linear feature of is bypassed, as the concavity of implies that is bounded in . Theorem 3.4.- shows that this claim is true, modulo the fact that it may happen that . Then, it follows from the standard Cauchy–Lipschitz theorem that the last ODE, with initial data and , has a unique classical solution for any choice of , say . Next, Sannikov argues that it is possible to choose so that this solution indeed solves Equation 3.4. Sannikov’s proof of this claim is not rigorous, and we show in the subsequent analysis that we can circumvent this difficulty by a different approach, under the extra assumption that is concave. Notice also that our main results given in Section 3.1 and Section 3.2, show that

-

•

for , there is no such that the solution of the dynamic programming equation (3.1) agrees with on , see of Proposition 3.8;

-

•

for sufficiently small, we prove under additional conditions that the solution of (3.1) may exhibit the behaviour claimed by Sannikov. In fact, we shall prove that the stopping region is either reduced to , or is of the form for some . This requires some involved technical arguments which are displayed in Section 8 below;

-

•

when the curvature at zero of the agent’s utility is sufficiently large negative, the stopping region is always reduced to for whatever value of . See of Proposition 3.8.

4 Solving the first-best contracting problem

Proof of Theorem 3.1..

We first solve the first best contracting problem when . Notice that in view of (2.12), the result follows directly from Theorem 3.4.. We however provide a simpler proof when .First, the limited liability constraint on the payments made to the agent, and the fact that is bounded by imply immediately that for any , we have Moreover, the only way this can be an equality is to choose , and such that and , which means that either , or . As none of these contracts can satisfy the participation constraint of the agent, there is no admissible contract which achieves this bound .

For any , let us consider the following contract: , , , with the level of effort . Since these contracts are defined by deterministic components, they automatically satisfy the integrability condition of (2.11). Notice also that when goes to , both and converge to . Therefore, we can choose small enough and find a constant , independent of , such that . The utility received by the agent is then

so that the agent’s participation constraint is satisfied for small enough. The principal’s utility is

since , which ends the proof in this case. ∎

Proof of Theorem 3.1..

We start with -–-. By the standard Karush–Kuhn–Tucker method, we rewrite the first-best problem as

As , and is concave, we have

Then, , and therefore

In particular, . Notice that is convex and , where we used the fact that , and the observation that for small enough. Then . The remaining claims follow from the fact that , as has linear growth ( is compact), and grows as at .

For -, by the non-negativity of and convex duality between and , we have for any

which proves the first part of the desired results. To prove the remaining claims, we consider several cases.

- For and . Notice that for , and for In particular, when it follows from the fact that that . As is strictly concave and satisfies similar growth conditions at as , it cannot behave as an affine function for large, and thus . Hence, for , we have , and and coincide as required.

- In the case and , we compute directly for sufficiently negative

which goes to as goes to as claimed.

- For and , the same computations as above lead to

The only unclear term is the first one. As , we may find for all a constant such that for any on . We then have for

Then by arbitrariness of .

- It remains to study the case and . The case is obvious as . For , we can again fix some , and some such that

This implies again have by the arbitrariness of . ∎

5 Reduction to a mixed control-and-stopping problem

In order to solve the second-best contracting problem, we use the general approach of Lin, Ren, Touzi, and Yang [37]999See Footnote 11. The methodology developed in [37] extends the finite maturity setting of Cvitanić, Possamaï, and Touzi [18] and is largely inspired by the method developed in Sannikov [52]. which justifies the remarkable solution approach introduced by Sannikov [52], reducing the Stackelberg game problem of the principal (2.7) to a standard stochastic control one.

To do this, observe that the Hamiltonian of the agent’s problem is given by the convex conjugate function introduced in (3.3), and that the corresponding subgradient contains all possible optimal agent responses

As is closed and is strictly convex101010If is an interval, then the strict convexity of guarantees that is a singleton. However, for a general closed subset , the maximiser may not be unique., notice that

| (5.1) |

because is decreasing whenever . We also abuse notations slightly, and for any -predictable, real-valued process and any , we write whenever , –a.e. Then, the lump-sum payment promised by the principal at takes the form

| (5.2) |

where represents the continuation utility of the agent given a continuous consumption stream and satisfies the integrability condition

| (5.3) |

Remark 5.1.

As observed by Sannikov [52], notice that the non-negativity condition on and implies that the so-called limited liability condition is satisfied. Indeed, as the dynamics of the process are given by , under the agent’s optimal response, we see that is an absorption point for the continuation utility with optimal effort .

By the main reduction result of [37],111111 By the growth condition (2.1) on , the integrability condition (2.11) implies that which is precisely the integrability condition required by Lin, Ren, Touzi, and Yang [37]. we may rewrite the principal’s problem (2.7) as

| (5.4) |

and

| (5.5) |

Here is the collection of all triples such that , and satisfy the integrability conditions (2.11), for some , and therefore also (5.3), together with the limited liability condition of Remark 5.1.

The last control problem only involves the dynamics of under the optimal response of the agent (due to the principal’s criterion which does not involve anymore the state variable )

| (5.6) |

6 Degenerate second-best value for a (very) impatient principal

We now provide the proof of Theorem 3.4. by using the problem reduction from the previous section. Notice first that whenever , then the same argument as in the proof of Theorem 3.1. shows that there cannot exist an optimal contract, and that the first-best and second-best value coincide. Our proof is based on an explicit construction of a sequence of contracts following the idea used in the proof of Theorem 3.1.: we want to have a retirement time going to , associated with a large lump-sum payment. However, because we are now in the second-best case, we need to offer the agent contracts which are incentive-compatible with the level of effort , meaning that these contracts cannot be deterministic. This can however be achieved by choosing a large enough constant control process in Equation 5.6. The price to pay now with such contracts is that the continuation utility of the agent may reach in finite time with positive probability, thus preventing the principal from offering a large lump-sum payment. This thus requires to carefully control the probability of early termination of the contract, and we show that by offering the agent a sufficiently large utility, this probability can be made arbitrarily small.

Proof of Theorem 3.4..

Let us fix some , . It is immediate that in this case . For arbitrary , consider the continuous payment , , where is the corresponding continuation utility of the agent, which is given by

Notice that is an Ornstein–Uhlenbeck process under , whose defining SDE can be solved explicitly

Let now , and consider the contract with retirement time , continuous payments , and terminal payment . We know from the general results in Section 5 that such a contract provides the agent with utility , which he will accept for small enough, regardless of the level of his participation constraint. Indeed, all the integrability requirements are obviously satisfied here, since is deterministic, is bounded, and from the explicit formula for .

We now compute the principal’s utility induced by this contract

Step . For , we have , where , . The law of is well-known (see for instance Karatzas and Shreve [33, Equation (5.13)]), and we have

| (6.1) |

This implies that

Step . Next, we have that there exists some , which may change value from line to line, but is independent of , such that for any

Then, as the last stochastic integral is a Gaussian random variable, and , we see that

| (6.2) |

It can be checked directly that since , the first term on the right-hand side of Section 6 goes to as go to . By (6.1), the second term also goes to as goes to . Finally, for the third one, it follows from the Cauchy–Schwarz’s inequality and Burkholder–Davis–Gundy’s inequality that

Step . It remains to control the continuous payment term

Notice next that we have that for any

Therefore, we have since

Finally, since for any , converges –a.s. to , it is immediate by dominated convergence that

which concludes the proof. ∎

Remark 6.1.

When , we may follow all the steps of the last proof, but take instead . Then, all terms appearing still converge to when goes to , and we may conclude already in Step that .

7 Dynamic programming equation and verification

This section prepares for the proof of the remaining main results of Section 3 by applying the dynamic programming approach to solve the mixed control-and-stopping problem (5.4)–(5.5). 3.3 is in force throughout. Notice that this problem is stationary in time due to the infinite horizon feature, and the time homogeneity of the dynamics of . By standard stochastic control theory, together with Remark 5.1, the corresponding HJB equation is

| (7.1) |

where for any

and the second order differential operator is as introduced in Equation 3.2, and can be rewritten thanks to Equation 5.1 as

| (7.2) |

where Observe by definition that

| (7.3) |

Moreover, inspecting the proof of Proposition 2.1 in Appendix A, the face-lifted reward function of (2.5) satisfies

| (7.4) |

Remark 7.1.

Notice that on , as a direct consequence of (7.4).

Equation 7.1 is equivalent to

| (7.5) |

which agrees exactly with Equation 3.1. Indeed, if is a solution of (7.1), then on , where is the so-called stopping region, and on , which implies that on by part of the present remark. Conversely, assuming that , we see that , and therefore is a super-solution of (7.4). By Lemma A.2, this implies that , and we conclude that solves Equation 7.1.

We next provide a verification argument which is the standard justification of the importance of the dynamic programming equation (7.1), and which guides the subsequent technical analysis to solve the contracting problem.

Proposition 7.2.

Let be on except at a finite number of points.

Assume is a super-solution of (7.1), i.e. , and . Then on .

If and on the continuation region , then under the additional conditions

-

for any , there exists a maximiser of such that the SDE (5.6), with, for any , , , and , has a weak solution;

-

defining , the triplet belongs to .

If in addition is ultimately decreasing, then the principal’s value function is , for some with optimal contract given by

Proof.

We first prove that . For an arbitrary , and with corresponding , we introduce for any integer , , and we directly compute by Itô’s formula that

Since is bounded on and satisfies (5.3), this implies that

where the last convergence follows from the fact that

by the estimate stated in Proposition 2.1, together with the integrability conditions on in (2.11) and on in (5.3). By the arbitrariness of , this shows that .

To prove , we now repeat the previous argument starting from the control introduced in the statement, and denoting the induced controlled state process. As and are maximisers of and , respectively, we see that for any

since on the boundary of .

Finally, is concave by Lemma 8.1 (since the argument for concavity applies to any continuous viscosity solution). As it is assumed to be ultimately decreasing, the existence of a maximiser of on follows, and we obtain that . ∎

We finally prove Theorem 3.4.- by using the verification result provided in Proposition 7.2, and admitting the regularity of stated in the remaining items of Theorem 3.4..

Proof of Theorem 3.4.-, admitting -.

The existence of is immediate by the strict concavity of , and the fact that it is ultimately decreasing. Then, the rest of the proof simply requires to check that the assumptions in Proposition 7.2 are satisfied here. First of all, notice that the map is bounded from above since is compact, and from below by , and it is continuous on because is there. Similarly, the map is bounded on , from below by and from above as well because is a bounded set under our assumptions. The existence of a unique weak solution for is then direct from Stroock and Varadhan [62, Corollary 6.4.4].121212The drift of is not bounded as required in [62, Corollary 6.4.4], because of the term . However, it suffices to apply the result to . Notice in addition that has moments of any order under (and thus under any , , recall that is compact). It remains to verify that satisfies (2.11). However, is a one-dimensional Markov process for which the boundaries and are regular and accessible, it is therefore well-known that is finite with probability . Since is compact, the densities all have moments of any order, uniformly in , from which it is immediate that (2.11) holds. ∎

8 Analysis of the dynamic programming equation

This section provides the proof of Theorem 3.4.-–-. We shall assume throughout that 3.3 is in force. Our first result below identifies the second-best value function as the unique viscosity solution of Equation 7.1 in an appropriate class, and gives relatively direct properties.

Lemma 8.1.

The second-best value function is the unique continuous viscosity solution of Equation 7.1, in the class of maps such that , , for some . Moreover, is strictly concave, ultimately decreasing, and satisfies the following properties

for and for . Moreover, whenever and

if and , then on for some finite

if is concave, then Moreover when .

Proof.

We proceed in several steps.

Step . By standard arguments in control theory, is a (discontinuous) viscosity solution of Equation 7.1, see for instance Touzi [66, Theorem 7.4]. As by (2.12), the bound for is inherited from the similar bound Theorem 3.1.- on the value of the first best contracting problem, and implies that is ultimately decreasing, and for some positive constant . The last bounds allow apply the comparison result of Lemma B.1 to deduce that is the unique viscosity solution of Equation 7.1, and that it is continuous.

Step . We next prove that is strictly concave. To prove concavity, suppose to the contrary that is strictly convex on some non-empty open interval , then we would have that in the viscosity sense on , and thus that on still in the viscosity sense, contradicting the fact that is a continuous viscosity solution of Equation 7.1. The strict concavity follows the same line of argument as in [52]. Suppose to the contrary that for in some interval , then

If , this implies that , and then . In particular . We next argue that this ODE is in addition uniformly elliptic. This is immediate when . For , we have by 3.3, and

As , , for any , we see that for any compact subset of , the supremum in is attained on for some , independent of (but of course depending on the chosen compact set). Hence, the ODE can always be written in explicit form on any compact subset of , and the standard Cauchy–Lipschitz existence and uniqueness theory applies. By uniqueness of the solution of Equation 7.1 with boundary condition and , we deduce that on , contradicting the boundary condition .

If , we also see by the same argument that on , so that implies that , and we get and therefore , which again cannot happen.

Step . We now prove the remaining statements. and are inherited from the similar bounds for stated in Theorem 3.1.. To obtain , notice that the non-negativity of and implies that , meaning that (where exists as the right derivative of a concave function), and that is a viscosity super-solution of

Since is continuous and admits a right-derivative , the last inequality holds Lebesgue–almost everywhere, i.e. . Dividing by and sending to , we deduce the first part of the claim. Next as is non-decreasing in , we deduce that . However, under our assumptions, . Then it follows from the non-decrease of in that . Then, as , and , we have , as required.

It remains to prove . Fix , such that on and on . Since is then a global minimum point of , we can use the viscosity super-solution property of with as a test function to deduce

This implies that , or equivalently

| (8.1) |

Next, there is some such that . Using this time the viscosity sub-solution property of at with as a test function, we deduce

Since , this implies that , and

| (8.2) |

Notice also that we cannot have , nor (this can be seen by arguing exactly as in the proof of Lemma 8.1, depending on whether or not). Using then Equation 8.1 with , we deduce from Equation 8.2 that

Since both and are non-decreasing, and and are positive, the above inequality is impossible.

Finally, let . By Proposition 3.8., never solves the ODE, and we claim that this implies that on . Indeed, notice that any contact point of and is a local minimiser of the difference , so that at such a point. Then, as , it follows from Equation 7.1 that which cannot happen unless . ∎

Remark 8.2.

By the strict concavity of , it is natural to introduce the concave dual function , . Then, if in addition is a solution of the dynamic programming equation, solves the dual equation

| (8.3) |

This follows by evaluating (7.5) at the point and by computing that .131313Such a transformation can also be conducted if the solution is expressed in the sense of viscosity solutions (as it will be needed later), but one has to be careful as strict convexity is not sufficient, see Alvarez, Lasry, and Lions [2, Proposition 5] and the remark after its proof.

Our next task here is to prove that the second-best value function has the required regularity so as to apply the verification argument of Proposition 7.2.

Lemma 8.3.

The second-best value function is on , and on , except at at most one point.

The proof of this regularity result reported separately in the gradually more involved , , and .

Proof of Lemma 8.3 .

Step . Suppose first that . Then is increasing on a right-neighbourhood on , for some . As on , we see that is a viscosity solution of . Notice that , by the strict concavity of . Then is actually a viscosity solution of

Arguing as in the proof of Lemma 8.1 Step , we see that the latter can be reduced to a uniformly elliptic ODE, which admits a unique classical solution with initial conditions and . In particular, this solution must coincide with , which is therefore on . This extends easily to the interval where

| (8.4) |

since we have on that interval. Notice also that we must have that is decreasing on a left-neighbourhood of .

Step . We next consider the alternative case where , see Lemma 8.1 (ii). We shall keep the dependence on as the following argument is valid in the case and will then be needed for the next proof. As , we have by Lemma A.1, and we consider two cases:

-

•

either , then we must also have , so that the ODE at the starting point reduces to the second order part. Since and is non-decreasing with respect to both its variables, we deduce first that that , and as both and are concave . Given that is solves the ODE , this implies that solves Equation 7.1 on . By uniqueness, which is therefore as desired;

-

•

alternatively, if , then the last argument applies when . It remains to consider the case where . As is decreasing, strictly concave, and the map is increasing on a right-neighbourhood of , say , and on . We may now argue as in the proof of Lemma 8.1 Step that our equation, with initial conditions and , reduces to a uniformly elliptic ODE, which admits a unique classical solution on , where is defined exactly as in Equation 8.4 above

Step . By direct calculation, we see that

By concavity of , this implies that a minimum of can only be attained at a point such that , and that the corresponding value is . Then, if we have . Hence, we have at , which by Lemma 8.1 implies that on . As a by-product of the last last argument, we have that is at , and is on . ∎

Proof of Lemma 8.3 .

In this case, it follows from Lemma 8.1. that . Then following Step of the previous proof, we either have and , or and we can then find such that is a classical solution of our nonlinear ODE on , with .

In contrast with the argument in Step of the case , the variations of for seem more difficult to access. Consider instead the dual ODE defined on with :

Arguing as in the proof of Lemma A.1, it is easily seen that this ODE has a unique solution given by

as . Moreover, arguing as in the proof of Lemma A.4 we see that is strictly concave and increasing. By standard convex duality, the corresponding Fenchel transform is the unique strictly concave and decreasing solution of

and we have that .

Next, notice that for any , we have . Indeed, this is true at by definition, and we claim that is concave, which ensures that this remains true for any value of , since is non-increasing in both its variables. Indeed, notice that so that it is equivalent to show that is concave. Now simply notice that for any , we have

since is concave (as is concave), and .

Overall, we have proved that is on , and we have constructed a solution of Equation 7.1 on whose value and derivative at coincide with those of . This defines a solution of Equation 7.1 which is everywhere except maybe at . It is also obvious that since , we have

n particular, we have found a continuous viscosity solution of Equation 7.1 which satisfies the growth condition , so that it must coincide with by the comparison result of Lemma B.1. ∎

Proof of Lemma 8.3 .

Step . By Lemma 8.1. we have since .

First, if , then we also have by Lemma A.1, since . Since , and since is non-decreasing with respect to both its variables, we deduce that so that solves Equation 7.1 on , as both and are concave. By uniqueness, which is therefore as desired, thus completing the proof in this case.

If instead . In this case we argue exactly as in Step in the proof of Lemma 8.3 to deduce that is on the interval , where is expressed in terms of the function of (8.4) as and that is decreasing on a left-neighbourhood of .

Step . We continue with the case . The idea will now be to regularise . Recall from Lemma 8.1 (ii) that must be equal to on , and consider for all the control problem

| (8.5) |

where and is defined as with the extra requirement that the controls take value in . By standard control theory, is a viscosity solution of the equation

where

| (8.6) |

Notice that as . By Lemma B.3, is in fact the unique viscosity solution of this equation.

By the same argument as in the proof of Lemma 8.1, we see that strictly concave on . Moreover, (and uniqueness actually holds in ). This follows from [39, Theorem I.6], using the following remarks: first we can bound the controls and by some arbitrarily large constant, since the optimal one will be bounded as a function of and its derivatives on the compact set ; second, the ODE Equation B.2 is uniformly elliptic for any . By stability of viscosity solutions (see for instance [12, Section 6]), it follows that converges uniformly on , and thus there is some , converging to , above which is non-increasing. By standard convex duality, the Fenchel transform of is on , and it follows from Alvarez, Lasry, and Lions [2, Proposition 5] (or more precisely the generalisation in Imbert [31] which does not require coercitivity conditions), that is a viscosity solution of the ODE

| (8.7) |

Since this is an explicit second-order ODE, the fact that is implies that it is on the above interval, and even .

Notice also that must be above by definition. Since these two maps are also concave and coincide at and , we must have and . Thus, using the Cauchy–Lipschitz theorem, we can uniquely extend to a continuous function on which is on .

Step . Clearly, the function is a classical solution of Equation B.5 for all . Under the conditions of 3.3, we verify in Lemma B.6 and Lemma B.7 that all the conditions of [2, Theorem 1] or more precisely its extension in [31, Theorem 1], are satisfied. Then it follows that is convex, or equivalently, is concave.

Step . We now show that is concave. By the stability of viscosity solutions again and the comparison results in Lemmas B.4 and B.7, we know that and converge uniformly on compact sets respectively to maps and . The uniform convergence ensures that coincides on with , and that . By the concavity of , this shows in particular that is and has a concave derivative. Now, it is obvious that any continuous viscosity solution to the PDE satisfied by has to be strictly concave, and therefore so is . As such, we deduce that is on and that its derivative is concave there, thanks to the concavity of . Thanks to this property, we know that the operator evaluated along the derivatives of can only decrease, and thus that remains forever equal to once it reaches it for the first time at . Arguing as in the proof of Lemma 8.3, we deduce that must coincide with starting from , and that it is at this point and everywhere else, which ends the proof. ∎

Appendix A Face-lifted principal’s reward

A.1 Very impatient principal may reduce her loss to zero

We first consider the case of Proposition 2.1.. Notice that we always have , and that since is non-positive, we have . Besides, by our assumptions on , there exists and , such that for any , . Fix some some and some , and consider then the following control where is the first instant at which reaches the value . We immediately have that In particular, , and for

by the condition . As , the last limit converges to as .

A.2 Non-degenerate face-lifted utility

By standard control theory, and similar to Remark 7.1., we can show that Hamilton–Jacobi equation corresponding to the mixed control-stopping problem reduces to

| (A.1) |

as the last equation implies that . Now, this ODE has as a trivial solution, and when , it has a unique strictly concave solution given by . The following lemma addresses the general case.

Lemma A.1.

Proof.

Notice first that if solves Equation A.1, then, whenever is finite, by letting go to , we get . This implies that , and as we deduce that , an inequality obviously satisfied when , which is the only possible infinite value by concavity of . We consider two cases to verify that

| (A.2) |

-

•

. Assume to the contrary that , then on for some . This in turn implies that on , and equation (A.1) reduces to , on , and we get

(A.3) As and , we see that . Then on , contradicting the strict concavity of .

-

•

. Since , we have again on , for some , and by arguing as in the previous case, we arrive to (A.3), and we see that is necessary in order to avoid explosion of near .

By (A.2), any strictly concave solution of (A.1) is decreasing, and the Fenchel dual function , whose domain is , satisfies the ODE

| (A.4) |

This linear ODE has the generic solution, for any and

| (A.5) |

We next determine and so as to match boundary condition .

Case : . In this case, we may take , thus reducing to the unique solution

In this case, we necessarily have , therefore, by Lemma A.4, is strictly concave, increasing, and . This immediately proves that is unique, strictly concave, decreasing, and above . Besides, the explicit formula we obtained shows by direct integration and using Equation 2.8 that satisfies also Equation 2.8 with appropriate constants, which directly implies the required inequalities for .

Case : and . We can again take to match the boundary condition , as

Moreover, by Lemma A.4, is strictly concave, increasing, and . This immediately proves that is unique, strictly concave, decreasing, and above . We deduce that satisfies the required inequalities as in the previous case.

Case : and . In this case, it can be checked that for any and , we have

We therefore have, a priori, infinitely many possible solutions to the ODE. However, notice that the growth imposed on translates into , and this implies that

| (A.6) |

as . Then, and must be such that where the finiteness of the last integral is satisfied in our setting again by . Consequently, is uniquely determined and given by

| (A.7) |

and we can again use Lemma A.4 to conclude. Finally, it follows from a direct change of variable that the above explicit solution coincides with the expression in Equation 2.9 in all above cases. ∎

The following is the easy inequality in a generic verification theorem for .

Lemma A.2.

Let be a super-solution of on . Then .

Proof.

We first observe that . We next compute for all and that

by the super-solution property of . The arbitrariness of and implies that . ∎

Lemma A.3.

Let and . Assume further that 3.3 holds. Then , where is given explicitly in (2.9), is the unique solution of Equation A.1 in the class of functions satisfying . Moreover, is a strictly concave decreasing majorant of , with .

Proof.

We show by a standard verification argument that where is the solution of (A.1) whose concave dual was derived explicitly in the Lemma A.1. By Lemma A.2, is an upper bound for , i.e. . On the other hand, consider for any the maximiser in the definition of , that is to say as a feedback control where Direct differentiation of (A.1) provides that for any , , so that

Since , we see that is decreasing when , and is therefore well-defined at least until the hitting time of zero . In contrast, when , is increasing until some explosion time , and . Following the same calculation as in the first step of the present proof, we see that under the control , all inequalities are turned into equalities, leading for any to

| (A.8) |

First, by the previous step, when , we have , and we obtain by sending to and using the boundary condition that attains the upper bound , and is therefore an optimal control for the problem . In the alternative case , we have . In the rest of this proof, we show that

| (A.9) |

Then, is defined on , i.e. , and since , we deduce from the growth of that for some , whose value may change from line to line, and any

as . Sending to in (A.8) this provides again that attains the upper bound . In order to verify (A.9), we prove equivalently that the concave dual satisfies

| (A.10) |

Differentiating the ODE (A.4) satisfied by , and using the expression of from Equation A.7, we see that

Notice that , and that is easily shown to be non-negative and non-decreasing. Therefore, if does not go to as goes to , we have that , and Equation A.10 automatically holds. Now if , it follows from l’Hôpital’s rule and our assumptions that

Then, using again l’Hôpital’s rule, we deduce

Then, assuming to the contrary that (A.10) does not hold means that, for fixed , we may find such that , for . Integrating twice and recalling that , this implies that

which in turn leads to the following contradiction by our assumption on the growth of together with the fact that . ∎

We end this section with the result used in the proof of Lemma A.1.

Lemma A.4.

Let , and let be a solution of

| (A.11) |

Then , is strictly concave and increasing.

Proof.

Denote , and notice that Equation A.11 says that for any

by the concavity of . Now define for , , we have We need to distinguish two cases, depending on or . First, if , we have that is non-increasing, and thus

since (recall that is above , which is itself below , since ). Similarly, when , by arguing as in (A.6), we arrive at the conclusion , and thus that , as desired. Next, by direct differentiation of Equation A.11, then substituting the expression of from Equation A.11, and finally using the strict concavity of , we deduce that for any

thus proving the strict concavity of . Finally, since is strictly concave, remains below which is increasing on , and on , then must also be increasing on its domain. ∎

Appendix B Comparison theorems

B.1 The dynamic programming equation and its dual

This section starts by providing the main technical result which was needed to justify the existence of a solution of the dynamic programming equation in Lemma 8.1. Namely, we show that, despite the exploding feature of , the dynamic programming equation satisfies a comparison result.

Lemma B.1.

(Comparison) Let and be respectively an upper-semicontinuous viscosity sub-solution and a lower-semicontinuous viscosity super-solution of (7.1), such that for and for some , Then on .

Remark B.2.

The specific upper bound in the statement of Lemma B.1 with an iterated logarithm is not important per se. Indeed, the proof goes through as long as the upper bound is of the form for some positive, increasing, strictly concave map , null at , growing strictly slower at than .

Proof of Lemma B.1.

We adapt the arguments of Crandall, Ishii, and Lions [12, Section 3] to our context.

Step . Let , for some . Define for any and the map

for some , by the growth assumptions on and . Notice in addition that the supremum is attained on a compact set, then we can find for any a further subsequence, denoted by , converging to some . By standard arguments from viscosity solution theory (see for instance Crandall, Ishii, and Lions [12, Proposition 3.7]), we have

Let us now assume that there is some such that . Then, we have for any and

In particular, for sufficiently large, we have that and are both positive, and we assume for notational simplicity that we took the appropriate subsequence. Using Crandall–Ishii’s lemma (see Crandall, Ishii, and Lions [12, Theorem 3.2]), we can find for each integer , an -valued sequence such that

with the notation for all and , and

where is the two-dimensional identity matrix, and

and where we use the spectral norm for symmetric matrices. Take , and multiply the above inequality by to the left and to the right, this implies in particular that

Step . Denoting , it follows from the sub-solution and super-solution properties of and , that

We deduce that , where

Now notice that since is Lipschitz continuous and non-decreasing with respect to its second variable, and since is non-decreasing, we have for some

We now want to let go to , and will distinguish two cases.

Either is unbounded, then by sending along some subsequence, we get which leads to a contradiction when goes to .

Or is bounded, we take a converging subsequence, and notice that we then have for some , with

-

1.

If is unbounded, we take again a subsequence and get a contradiction by letting go to in

(B.1) -

2.

If otherwise is bounded and has a subsequence converging to some , then taking another subsequence, we obtain a contradiction by letting go to in Equation B.1. Finally, if , then three cases can occur

-

first, if , then and we conclude again by letting go to in Equation B.1;

-

if instead , then and we conclude similarly;

-

finally, if for some , then and we get once more a contradiction.

-

∎

We next provide the comparison result for the approximating PDE. Recall the operator from (8.6).

Lemma B.3.

(Comparison in bounded domain) Fix some and some . Let and be respectively an upper-semicontinuous viscosity sub-solution and a lower-semicontinuous viscosity super-solution of

| (B.2) |

such that and . Then on .

Proof.

We argue exactly as in Step of the proof of Lemma B.1, with , , and with maximisation in the definition of confined to the compact subset . With , the sub-solution and super-solution properties of and induce

Then, whenever there is some , for some , we deduce that

Now notice that since is Lipschitz continuous and non-decreasing with respect to its second variable, and since is non-decreasing, it follows that , contradiction! ∎

We finish this section by proving a comparison result for the convex dual equation of Equation B.2.

Lemma B.4.

(Comparison dual equation) Fix some and some . Let and be respectively an upper semi-continuous viscosity sub-solution and a lower semi-continuous viscosity super-solution of

| (B.3) |

such that and . Then on .

Proof.

We again argue exactly as in Step of the proof of Lemma B.1, with , , and with maximisation in the definition of confined to the compact subset , and . By the sub-solution and super-solution properties of and , we see that

Then, whenever there is some , for some , we deduce that

Now is Lipschitz-continuous and non-decreasing with respect to its second variable, and is Lipschitz continuous on compacts. Then , for . The contradiction follows by letting . ∎

B.2 The differentiated dual dynamic programming equation

This section provides all the technical results needed to prove that the first-order derivative of the solution to the dual equation (8.3) is concave under appropriate assumptions, whenever . Throughout this section, we assume that , so that we can finally write the operator of (8.6) as

Using the envelop theorem, we also see that is differentiable and that for any

where , and is the unique solution of the equation

| (B.4) |

Our first result shows that under appropriate assumptions on , the functions and are monotone with respect to both their arguments, and that is convex with respect to its first argument.

Lemma B.5.

Assume that is and that

Then for any , the maps and are non-decreasing and convex on the domain where they are not constant, while for any , the maps and are non-decreasing.

Proof.

First notice that under our assumptions, the maps and are both increasing and convex. It is therefore enough to prove that for any , is non-decreasing and convex, and that for any , is non-decreasing. Differentiating Equation B.4 with respect to and , we get

from which we deduce immediately that for any , is non-decreasing, and for any , is non-decreasing as well. Next, we compute

which is non-negative for any by assumption. ∎

We now recall, for any , the dual ODEs from Equation B.3