Community Network Auto-Regression for High-Dimensional Time Series

Abstract

Modeling responses on the nodes of a large-scale network is an important task that arises commonly in practice. This paper proposes a community network vector autoregressive (CNAR) model, which utilizes the network structure to characterize the dependence and intra-community homogeneity of the high dimensional time series. The CNAR model greatly increases the flexibility and generality of the network vector autoregressive (Zhu et al., 2017, NAR) model by allowing heterogeneous network effects across different network communities. In addition, the non-community-related latent factors are included to account for unknown cross-sectional dependence. The number of network communities can diverge as the network expands, which leads to estimating a diverging number of model parameters. We obtain a set of stationary conditions and develop an efficient two-step weighted least-squares estimator. The consistency and asymptotic normality properties of the estimators are established. The theoretical results show that the two-step estimator improves the one-step estimator by an order of magnitude when the error admits a factor structure. The advantages of the CNAR model are further illustrated on a variety of synthetic and real datasets.

KEY WORDS: Network autoregression; Community structure; Common latent factors; High dimensional time series; VAR model.

1 Introduction

Consider a large scale network with nodes, which are indexed from . To characterize the network relationship among the nodes, we use an adjacency matrix , where if the -th node is connected the -th node, otherwise . For the -th node at time , we collect a continuous type response . At time , all the responses constitute a high-dimensional vector . We aim to model the temporal dynamics of . A simple VAR(1) model has autoregressive coefficient matrix and the community structure can be used to reduce the dimensionality.

A popular method of modeling the dynamics of with underlying network structure is the network autoregression (NAR, Zhu et al. (2017)) model:

| (1) |

where is the row-normalized adjacency matrix, with and , is a vector of auxiliary covariates, and and are unknown parameters. The model directly embeds the network adjacency matrix and provides easy interpretations. Particularly, the network effect reflects the influence of connected nodes through their averages at time , and the momentum effect quantifies the autoregressive effects from the same node. The NAR model and its variants have been applied to a wide range of fields, such as social behavior studies (Sojourner, 2013; Liu et al., 2017; Zhu et al., 2018), financial risk management (Härdle et al., 2016; Zou et al., 2017), spatial data modeling (Lee and Yu, 2009; Shi and Lee, 2017), among others.

Despite its simple form and easy interpretation, the NAR model (1) has only two parameters and may suffer from the risk of model misspecification. To address this issue, some flexible extensions to the NAR model have been considered in the literature. For instance, Dou et al. (2016) and Zhu et al. (2019) implement node-specific network effect to characterize different inferential powers of different nodes; Sun (2016); Wang et al. (2016); Sun and Malikov (2018) investigate the nonlinear and nonparametric extensions; and Sojourner (2013); Liu et al. (2017); Zhu et al. (2018) consider the multivariate responses. However, previous researches do not fully address two important issues that arise commonly in real applications, namely, heterogeneous network effect and unknown cross-sectional dependence.

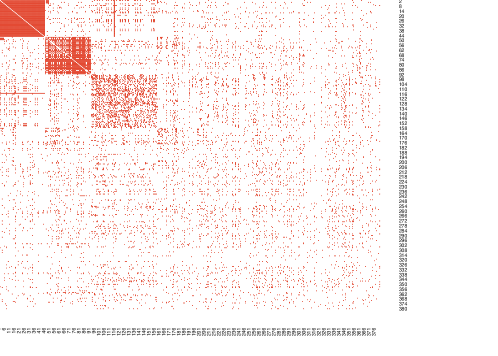

First, to characterize the heterogeneous network effect, we consider a community structure among network nodes. In literature, the community structure is commonly modelled in social networks (Rohe et al., 2011; Zhao et al., 2012). Individuals in different communities tend to behave quite differently. Statistically, although the general dependence structure for responses is widely studied, however, the network structure information is not fully used. Figure 1 shows that, in the Chinese A share stock market, the stocks held by the same shareholders may share denser relationships than other stocks. This motivates us to incorporate the network structure in modeling the dynamics of the individuals. Second, we consider a dynamic factor structure to allow for a more flexible form of cross-sectional dependence structure other than those that can be explained by the network structure or observable covariates. Notably, factor structure (Anderson and Rubin, 1956) arises commonly in a wide range of applications including economics (Stock and Watson, 2011; Bai et al., 2008) and biology (Desai and Storey, 2012). See Chapters 10 and 11 of Fan et al. for the applications of factor models and the references therein. Previous literature related to NAR makes use of only the adjacency matrix , making it difficult to incorporate heterogeneity directly in the model. In addition, the growing dimensionality makes it more challenging to deal with the non-diagonal noise covariance matrix .

In this article, we propose a novel community-augmented network autoregression (CNAR) model that allows for both the heterogeneous network effects across network (i.e., the network coefficient are different across different communities) and the unknown dependences in responses . Specifically, we exploit the network structure deeper through the Stochastic Block Model (SBM), which is widely employed as a canonical model to study clustering and community detection (Lei and Rinaldo, 2015; Abbe et al., 2017) . Heterogeneous network effects are enabled by using different network effects for nodes within different communities. The community structure can be known or unknown as priori. When it is unknown, we devise an equivalent reformulation of our original CNAR model to circumvent an unnecessary clustering step in our setting, which often incurs extra errors when the ultimate goal is instead to recover the community membership matrix.

At the same time, we allow for a latent cross-sectional dependence of by modeling the noise with a linear factor structure. Under such setting, the norm of the error covariance matrix in the genuine presence of the prevasive factors, which renders the ordinary least square estimators converge only at the rate despite of observations. We further propose an efficient two-step estimation procedure and discover surprisingly that it improves the convergence rate to . The convergence rates and the asymptotic normality of the proposed estimators are presented under the generality that the number of communities is also growing with . Furthermore, the convergence of the high dimensional covariance matrix is also established under our modeling framework. Extensive Monte Carlo simulations is carried out to evaluate the finite sample performance of estimators. Numerical performances of CNAR 1st-step, 2nd-step estimators and NAR estimators under different simulation models are compared and evaluated. Lastly, for illustration propose, we analyze the stock return data from Chinese A stock market. Empirical analysis on both synthetic and real data set confirms the advantage of the proposed modeling approach.

1.1 Notation and organization

Let lowercase letter , boldface letter , and capital letter represent scalar, vector, and matrix, respectively. We let denote generic constants, where the uppercase and lowercase letters represent large and small constants, respectively. The actual values of these generic constants may vary in specific scenarios. For any matrix , we use , , and to denote its -th row, -th column, and -th entry, respectively. All vectors are column vectors and row vectors are written as for any vector . Notation represents a vector or a matrix of all ones of proper size. In addition, denotes a unit vector with the th element being 1 and others being 0.

Let be the -th largest singular value of . For an arbitrary square matrix , let be the th eigenvalue of satisfying . Specifically, denote as the spectral radius for a square matrix . For a symmetric , we use and to denote its smallest and largest eigenvalues for convenience. The following matrix norms are used: maximum norm , -norm , -norm , -norm or , -norm , Frobenius norm , -norm . Here we use to denote the trace of a square matrix .

The rest of this paper is organized as follows. In Section 2, we introduce the model and notations. In Section 3, a two step estimation method is presented. In Section 4, we develop the theoretical properties of the estimation. In Section 5, we study the finite sample performance of our estimation via simulation and Section 6 provides an empirical study with a stock return dataset. Section 7 concludes. All proofs and technique lemmas are relegate to the supplementary appendix; see Appendix A, B.

2 Network Autoregression with a Community Structure

2.1 Model and notations

We present the model formulation as follows. First, we assume that the network adjacency matrix is generated by a Stochastic Block Model (SBM) with nodes and communities 111This assumption is made largely for a clear model interpretation and theoretical derivation. As shown by its reformulation (4) and the empirical examples, the CNAR performances well under more general network structures.. The SBM is parameterized by a pair of matrices , where is the membership matrix and is a symmetric connectivity matrix. For each node , let be its community label, such that the -th row of is 1 in column and elsewhere. Given , the adjacency matrix is generated as

To model heterogeneity across nodes in the autoregressive patterns, it is natural to take the above community structure into consideration. We propose the following community augmented network autoregression (CNAR) model,

| (2) |

where , , and are unknown parameters.

The CNAR model (2) characterizes the response by a linear form of the following four components. The first one is the network component, which characterizes the network effects among different communities. It shows how the community total (equivalently, average) responses at time impact on the response . The corresponding parameter is then referred to as community effect. The -th element of represents the effect of -th community to the -th community. It removes the restrictions of the component in the NAR model (1) to much broader linear dependence (see Remark 1 below) and uses the true community profiles rather than the realized links, which are random under the stochastic block model. In addition, the asymmetric community effect is allowed because is not restricted to a symmetric matrix.

Next, the momentum effect quantifies how the local node is driven by its historical behavior. This can be generalized to a diagonal matrix, allowing different nodes to have different momentum parameters. Lastly, includes covariates before time , which is assumed to be independent with . We further characterize the unknown cross-sectional dependence by assuming a latent factor structure on the noise term:

| (3) |

where is the unknown latent factors, is the corresponding loading matrix, and the innovation term follows a multivariate normal distribution . Under such setting, the network nodes are correlated with each other not only through the network relationship, but also through the common driven factors. A strong factor will have impact on most network nodes through the corresponding factor loadings. As a result, the factor structure in (3) characterizes the cross-sectional dependence at a macro level. In the following, we discuss the relationship of the proposed model to the existing literature.

Remark 1. (Relation to the NAR model). Note that the unknown parameter matrix specifies the autoregression network effects of communities. If , then the CNAR model (2) will reduce to the NAR model (1). In general, the above relationship does not hold. From the aspect of model designing, the CNAR model is built based on the population parameter of , while the NAR model is constructed conditional on a realized adjacency matrix .

Remark 2. (Relation to the vector-autoregression and factor models). CNAR model is a parsimoneous augmented vector autoregression (VAR) model with autoregression coefficient matrix modeled as , augmented by the exogeneous variable and cross-sectional dependent errors. The CNAR model (2) could also be comprehended as a special form of factor models. Let be a projection of using the membership projection , which is the vector of the total response in each community Then we have

where . When the true or a consistent estimator is available, can be treated as a known common factor, which embeds the community structure explicitly in the definition. As a complement, consists of unknown factors characterizing other sources of cross-sectional dependence.

Remark 3. (Relation to the community-leveled vector autoregression). By multiplying in both sides of the CNAR model, we have

where is a diagonal matrix, consisting the number of members in each community. Note that is a -dimensional vector. As a result, the CNAR model can be transformed to a community-leveled vector autoregression model, where the autoregression coefficients are specified by and .

2.2 A reformulation of the CNAR model

Different from the NAR model (1), the CNAR model (2) does not directly use the network adjacency matrix or the row-normalized version . Instead, it incorporates the network community structure on a population level. In practice, we only observe a sampled adjacency matrix and the membership matrix is unknown. Estimation of the network autoregressive coefficients necessitates an estimate of at first. A common method to estimate in the SBM is through spectral clustering. This method typically involves an additional step of clustering, for example by -means, after conducting the eigenvalue decomposition of . In the following, we show that this extra clustering step can be circumvented through an alternative formulation of the CNAR model (2).

Recall that, in a SBM, the heuristic of spectral clustering is to relate the eigenvectors of to those of using the fact that . Let be the eigen-decomposition of with and is a diagonal matrix. It is easy to see that and share the same column spaces. Namely, there exists a rotation matrix , such that

Using this fact, we let and reparameterize the CNAR model (2) as

| (4) |

The transformed network effects is equivalent to up to a rotation. But the network autoregressive coefficient stays the same, that is . Matrix is referred to as the spectral representation of . It can be estimated with higher accuracy than the membership matrix , without resorting to the -means algorithm to determine . Consequently, we estimate the pair instead of .

2.3 Model stationarity

In this section, we investigate the stationarity of the time series . Denote by and , we rewrite the CNAR model (4) as

Thus, the CNAR model can be seen as a special case of the vector autoregression (VAR) model with autoregressive matrix given by . In our situation, the autoregressive matrix is structured by embedding the community structure and low-rank common factor configuration. We establish the stationarity condition for the CNAR model (2) as follows.

Theorem 2.1.

Assume that , , , and is strictly stationary. If , then there exists a unique strictly stationary solution with finite first order moment to the CNAR model (2). The solution takes the form,

3 Estimation

According to our analysis in Section 2.2, Model (2) is equivalent to Model (4). It suffices to estimate the spectral representation instead of the membership matrix . To perform the estimation, we firstly estimate by the first eigenvectors of the adjacency matrix corresponding to the largest absolute eigenvalues. The spectral representation is a major step in spectral clustering used in community detection for SBM (Lei and Rinaldo, 2015; Zhao et al., 2012; Rohe et al., 2011). As a result, a knowledge of is sufficient for our purpose of estimation and prediction. For completeness, we include a brief summary of the estimation properties of in Lemma A.6 based on Lei and Rinaldo (2015). Next, we proceed to estimate the autoregression coefficients by a two-step estimator. In the first step, we plug-in the estimated matrix, estimate the unknown autoregression coefficients and the regression residual by the least squares method. In the second step, we estimate the covariance of the noise term by using the POET method (Fan et al., 2013) to the residual , and then use the estimated covariance matrix to further improve the estimation efficiency. The details of the last two steps are presented in the next two sections.

3.1 First step estimation of auto-regression coefficients

First the CNAR Model (2) could be re-written as

Write and let . Then we have the following relationship,

| (5) |

By using a standard least squares estimation, can be estimated by

Note that we assume is uncorrelated over but with cross-sectional dependence. That implies that the above least squares estimation will yield a consistent estimation of . In practice, the true value of is unknown. Instead, we plug-in corresponding estimators into and obtain . Accordingly, we obtain the first step estimator as

| (6) |

3.2 Second-step weighted least squares

Once the first step estimator is given, we are then able to plug-in the estimator to obtain the residuals as follows:

| (7) |

Note that the true noise can be decomposed into a low dimensional factor structure and an independent error in (3). Therefore the covariance matrix of can be expressed as

where and are the covariance matrices of the latent common factor and the idiosyncratic component, respectively.

Estimating a low-rank plus sparse covariance matrix with either observed or unobserved factors has been considered in Fan et al. (2008, 2011, 2013) and Fan and Liao (2019). However, the task here is slightly different from the standard problem: while the is known in previous studies, direct observation of is absent in our setting. We need to use the estimated which are the residuals from the first step regression of the CNAR model. Moreover, we consider a time series setting where the number of communities , and, as a result, the number of coefficients are allowed to grow with .

Specifically, we apply a simplified version of the POET method to the first-step CNAR residual . and are both unknown and are estimated by PCA as in Fan et al. (2013). Let and be the estimated loading matrix and factor, be the estimated idiosyncratic component. The covariance of is given by

| (8) |

where and . Using , we construct a weighted least squares type objective function as follows,

which yields our second step estimator as

| (9) |

One may wonder if (9) is computationally expensive since it requires to compute the inverse of an -dimensional matrix . This issue can be easily solved since takes a special decomposition as in (8). Applying the Sherman-Morrison-Woodbury formula and using the identification condition that we could obtain

| (10) |

The inverse of a sparse matrix can be computed efficiently since it is diagonal.

4 Theoretical Properties

We present the theoretical properties of the CNAR model estimation in this section. First, the asymptotic properties of the first step estimator are presented in Section 4.1. Next, the properties of the covariance estimation as well as the second step estimation are stated in Section 4.2.

4.1 Asymptotic properties of the first-step estimation

To investigate the estimation properties of the first step estimator, we first focus on the case that the number of communities is fixed. As a result, the number of coefficients to be estimated is fixed. In the following theorem we establish the asymptotic result of the first step estimator.

Theorem 4.1.

(First Step Estimator for Fixed )

Assume ,

, and is fixed,

where is a positive constant.

In addition, assume

Assumption B.1

and .

Define .

Then the following conclusion holds.

(a) (Oracle Estimator).

Let

and . We have

,

where

| (17) |

with

,

,

,

,

,

,

.

(b) (First Step Estimator).

Define as smallest absolute nonzero eigenvalue of .

Assume and .

We have .

The proof of Theorem 4.1 is given in Appendix A.2. Related to the results, we have two comments. First, it implies that, both and are -consistent while is -consistent. The slower convergence rates of and are mainly due to the pervasiveness condition (i.e., Assumption B.1) of the factor structure. Under this assumption, the largest eigenvalue of will diverge in the rate of , which reduces the convergence rates of the autoregression related parameters. When there is no pervasive factor, the rate of convergence is .

Remark 4. Note that we require that as a condition to establish the asymptotic results. If it holds , then we could obtain that the and . Under this case, the community structure diminishes the factor effect, which leads to different forms of the asymptotic result. We state the result in the Appendix for completeness.

The above theoretical results are established under the condition that is fixed. However, the fixed assumption can be restrictive in practice. Typically, more groups will emerge as . As a result, the number of parameters to be estimated is also diverging as . The following theorem establishes the theoretical properties of and under this situation. It shows that the properties of Theorem 4.1 continue to hold.

Theorem 4.2.

(First Step Estimator for ) Assume is diagonalizable which holds automatically for symmetric matrices, i.e., with being a diagonal matrix. Assume the same conditions as in Theorem 4.1 and . Let satisfy as , where is a fixed integer and is a non-negative symmetric matrix. It then holds

| (18) |

Further assume and . Then it holds,

| (19) |

The proof of the theorem is given in Appendix A.3. Implied by the above theorem, any finite sub-vector of is -consistent. However, since it ignores the potential cross-sectional dependence structure in , it is sub-optimal in terms of estimation efficiency. We further improve it by a second step estimator and the corresponding theoretical properties are discussed in the next section.

4.2 Asymptotic properties of the second-step estimation

We apply the principal orthogonal complement thresholding method (Fan et al., 2013, POET) to estimate the covariance . However, the task here is slightly different from that in Fan et al. (2013) since direct observations for are not available. Instead, we are able to calculate – the residual from the first step regression of the CNAR model. That is, . The estiamtion properties of and are given in the following theorem.

Theorem 4.3.

The proof of Theorem 4.3 is given in Appendix B.3.4. The result extends the theoretical results of the covariance estimation in Fan et al. (2013) under our CNAR modeling framework. The estimation error of the first step estimator is involved through the extra term . As we could observe, estimating the precision matrix is much easier than under this context. This will lead to the -consistency result of the second step estimator. The details are stated in the following theorem.

Theorem 4.4.

The proof of Theorem 4.4 is given in Appendix A.4. With respect to the convergence result, we have the following comments. First, the assumption involved here requires and , which can be easily satisfied for large scale networks. Second, it should be noted although the largest eigenvalue of diverges in the speed of , the largest eigenvalue of the precision matrix (i.e., ) is bounded by a finite constant (Fan et al., 2013). Hence the noise level is well controlled. As a result, this further enables us to achieve a better convergence rate (i.e., -consistency) of the second step estimator.

5 Numerical Studies

In this section, we use Monte Carlo simulations to assess the adequacy of the asymptotic convergence rates by evaluating the finite sample performance of estimators. For different simulation models and combinations of , , and , we report the relative mean squared errors (ReMSE) for model parameter estimators and the time series predictors. Specifically, for any estimator of the true value , the ReMSE is defined as ReMSE. Since the systematic noise is difficult to predict, we report the prediction error with respect to the signal defined in (25) below. We compare our results with those estimated using NAR (Zhu et al., 2017). All results are based on replications.

The synthetic data are generated according to the following model:

| (25) |

where for CNAR model and with being the row-normalized adjacency matrix. It has different structures in the following three examples, which are specified later. We generate the covariates from multivariate normal distribution with the dimension fixed at . We fix the dimension of latent factor at and generate and from of appropriate dimensions. For true values of the coefficients, we fix and at and . The entries of the loading matrix are also fixed for each pair of but are generated randomly once from .

5.1 Comparison of CNAR and NAR under different network models

In the following three examples, we generate the data by using different mechanisms. The finite sample performances of CNAR and NAR model (Zhu et al., 2017) are compared in terms of estimation and prediction accuracy. Because the covariance of the noise in (25) is not diagonal, we use the 2nd-step weighted least square estimator for both NAR and CNAR estimation for a fair comparison.

-

Example 1

(Stochastic Block Model and CNAR) We construct our network using the stochastic block model with communities

This setting assumes that the edge probability between any pair of nodes depends only on whether they belong to the same community: the edge probability is within community and between community. The quantity reflects the relative difference in connectivity between and within communities. We set , , and . Here is a diagonal matrix, whose diagonal elements are the first numbers of the sequence . We vary , and .

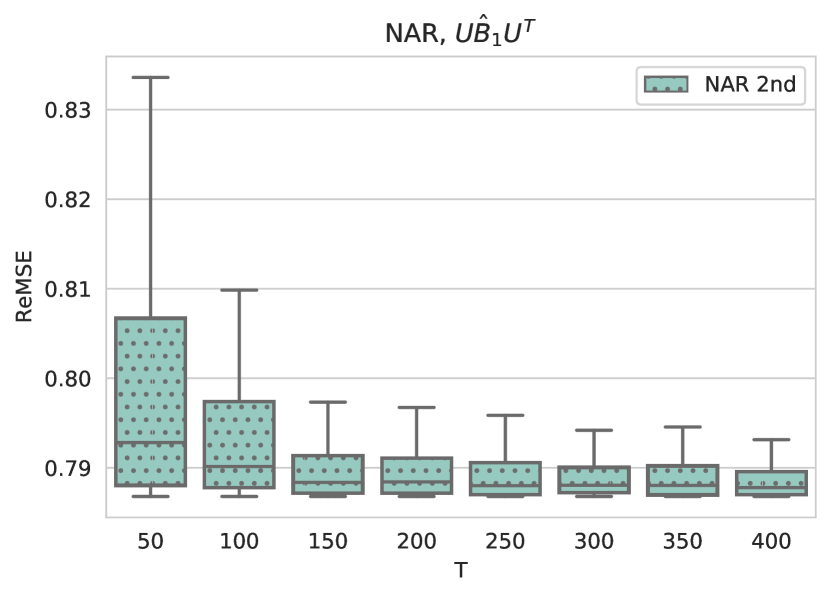

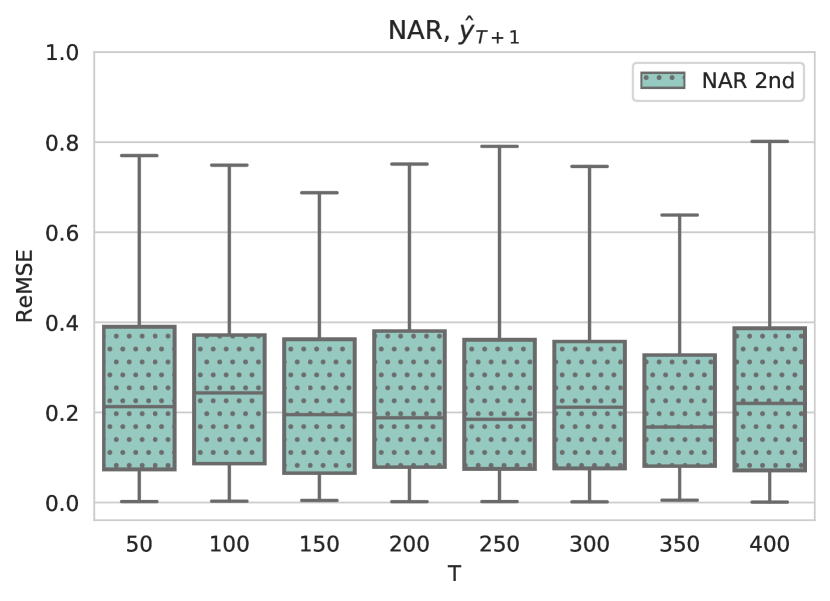

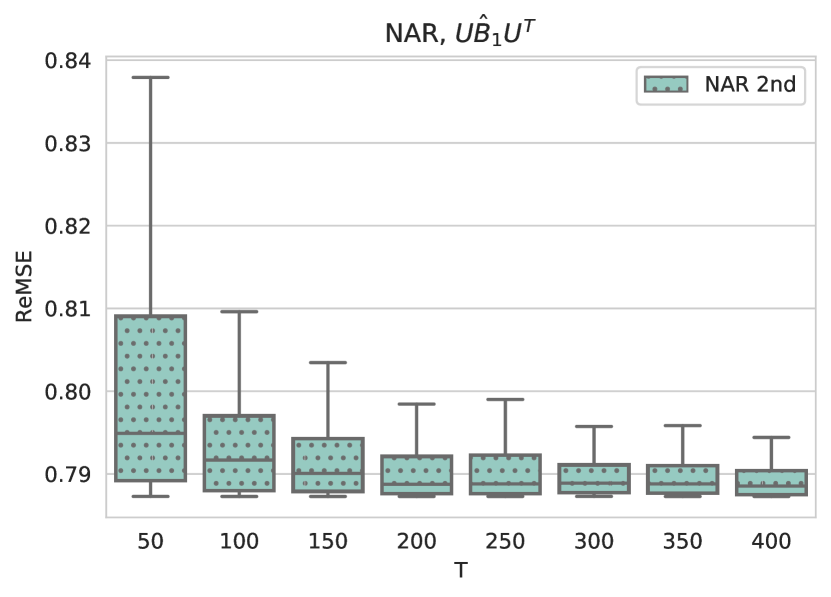

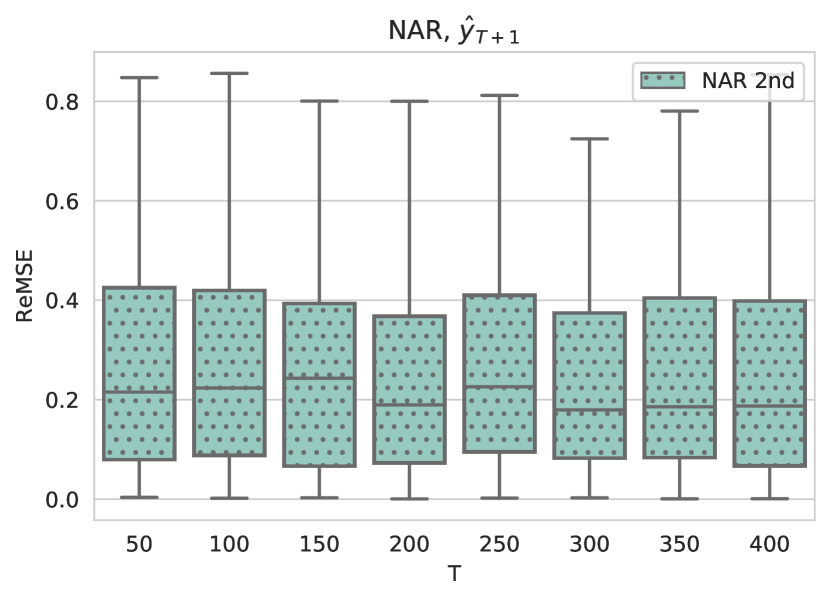

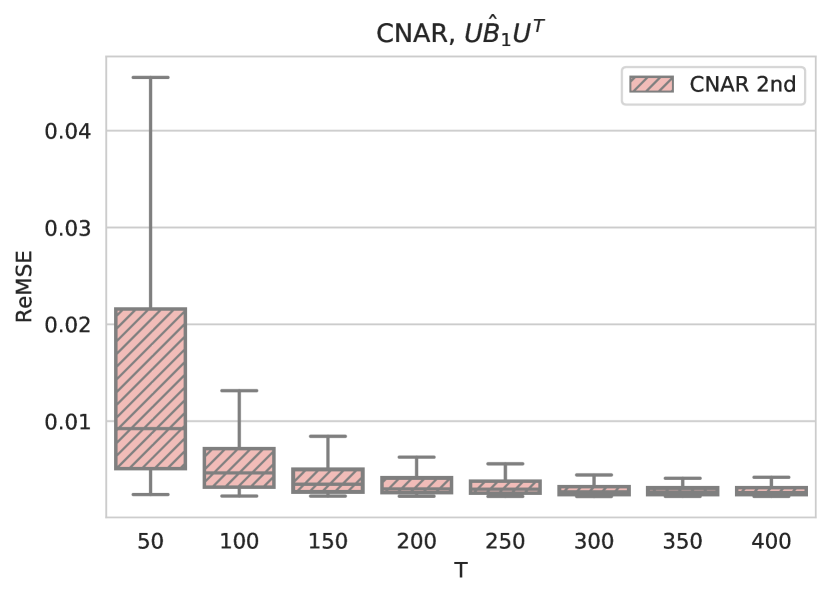

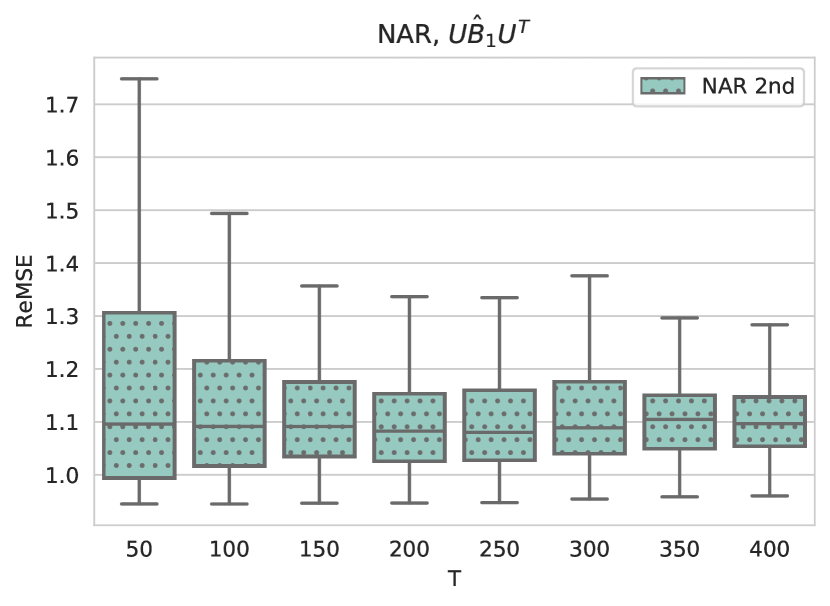

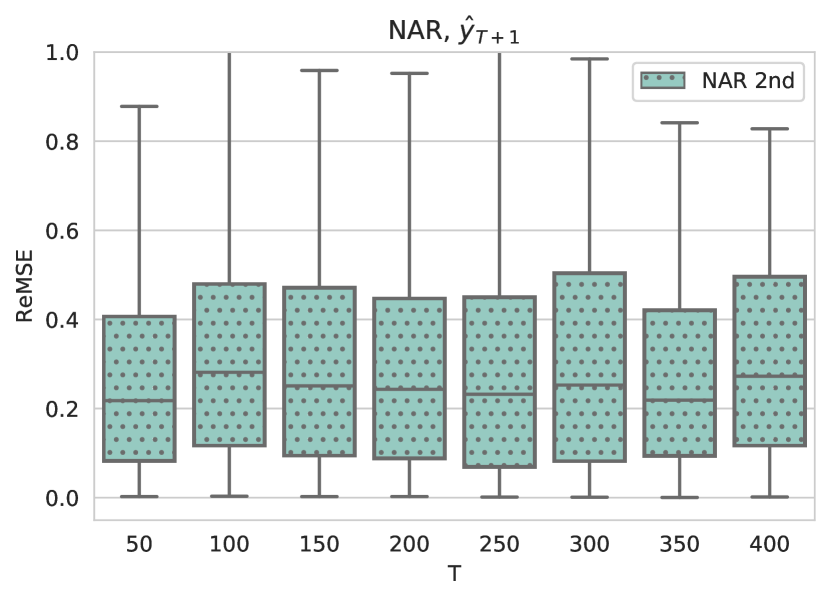

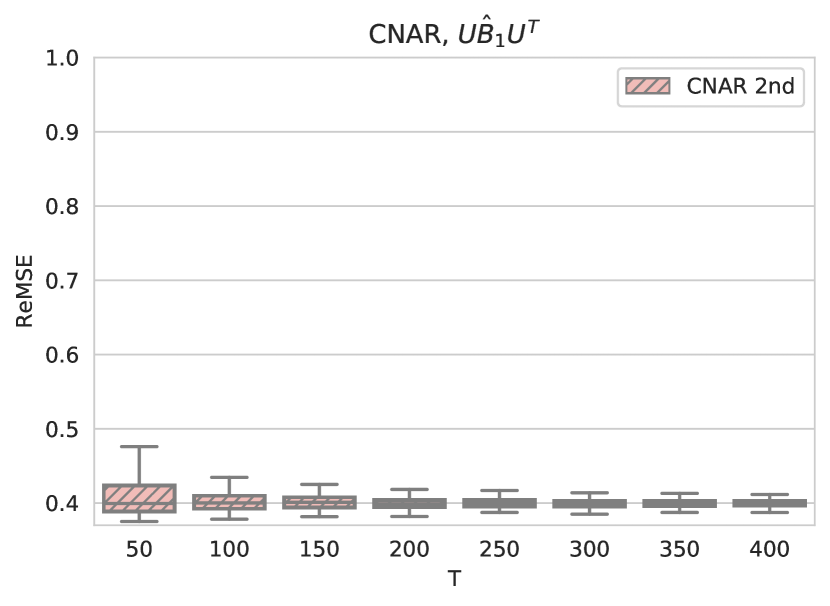

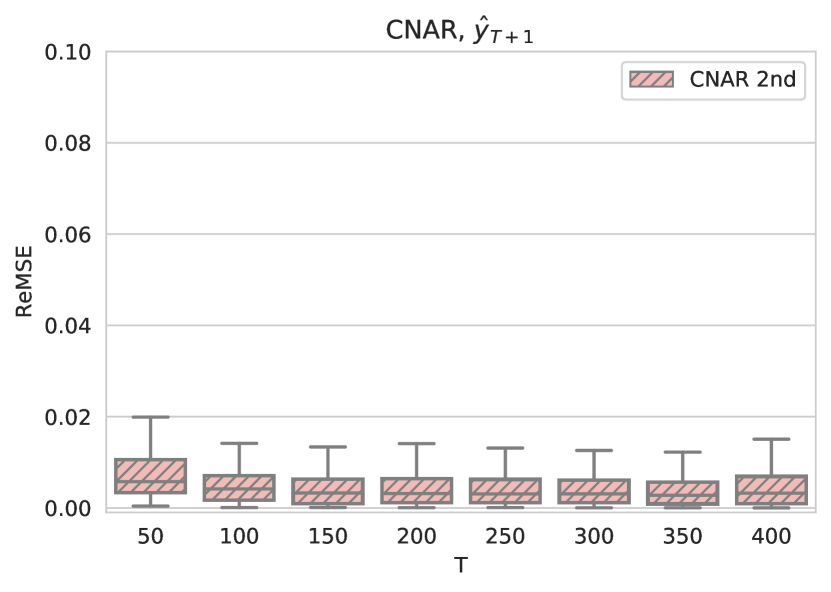

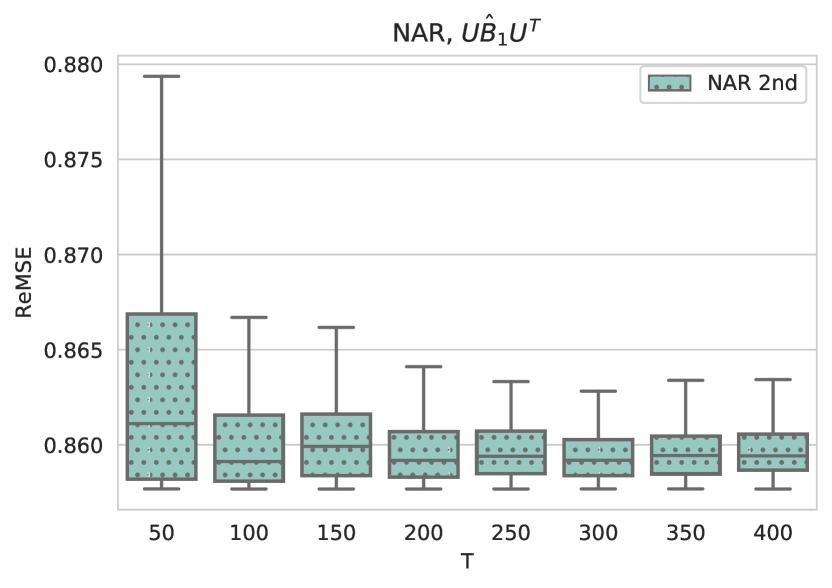

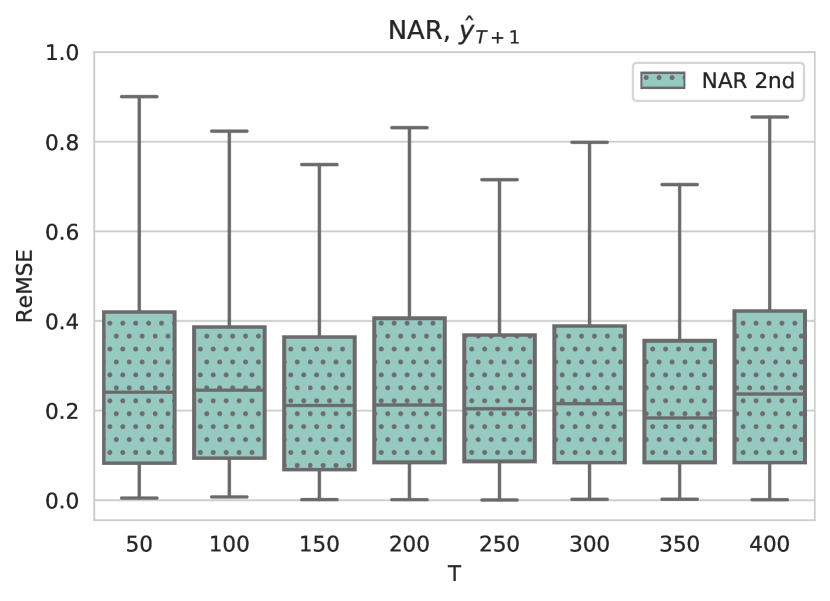

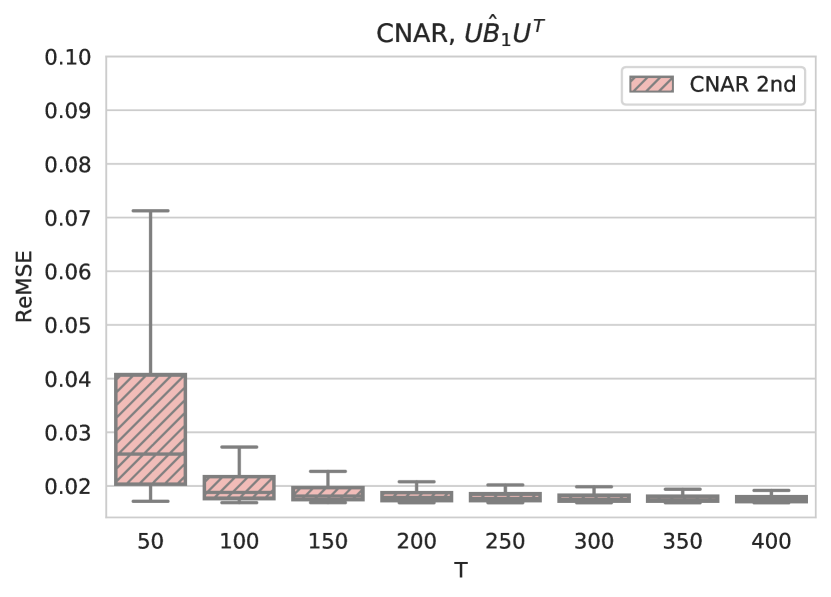

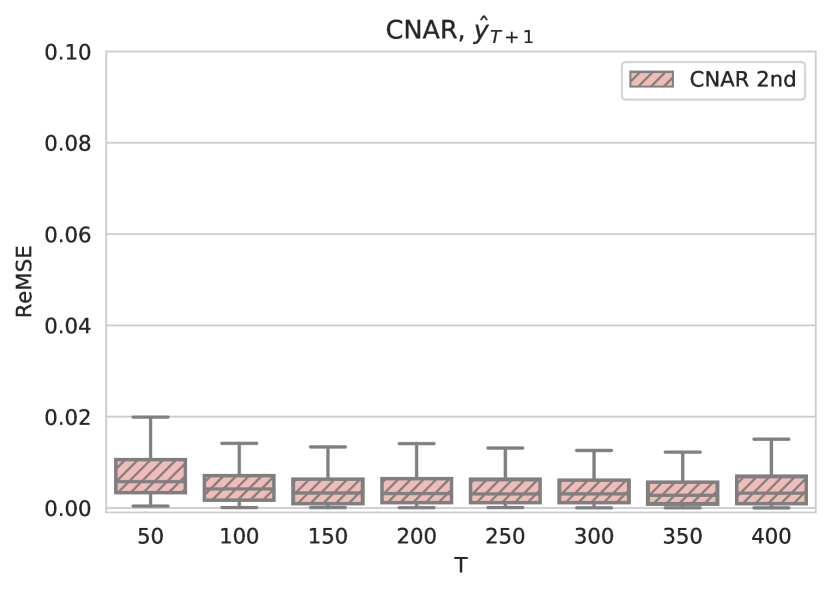

Figure 2 shows, for Example 1, the ReMSE of estimated network AR coefficient and 1-step prediction by NAR (first row) and CNAR (second row), respectively, with and . Note the scales of the y-axes are very different and all . Under all settings, CNAR outperforms NAR with much lower ReMSE, as NAR is not flexible to fully capture the complex community effects. In addition, as increases, the ReMSE of CNAR model decreases, as expected. The CNAR with estimated and two-step weighted LS using covariance estimator (8) becomes closer and closer to the oracle estimator as increases.

Figure 2: Example 1 (SBM and CNAR model with and ). Box plots for the ReMSE for estimated network AR coefficient and 1-step prediction by NAR (first row) and CNAR (second row), respectively. In the supplementary material, we present a table comparing the performance of CNAR and NAR in Example 1 with different numbers of network communities , network sizes and time series length . The performance of CNAR is better than that of NAR under all settings. For the CNAR model, it can be observed that the errors reduce when or with given number of communities , which corroborates with the theoretical findings.

-

Example 2

(Low-rank spectral network and CNAR) In this example, we focus on the sensitivity analysis when the network is not generated from the SBM model. We consider a general network with spectrum resembling that of an SBM. The network is generated by the Python graph function spectral_graph_forge in the NetworkX package (Hagberg et al., 2008), which computes the eigenvectors of a given SBM’s adjacency matrix, filters them and builds a random graph with a similar eigenstructure ( for the second function argument). The membership matrix is generated using community assignments from a spectral clustering. Other model parameters, such as , and , are set in the same way as in Example 1.

Figure 3 shows the ReMSE of estimated network AR coefficient and 1-step prediction by NAR (first row) and CNAR (second row), respectively, with and . Under this setting with a different network generative model, CNAR works similarly to it does in the SBM case in Example 1 and outperforms NAR. In the supplementary material, we compares CNAR and NAR under two additional settings, namely the clusters of power law network and the random partition network. Under all setting, the CNAR model still has much smaller estimation and prediction error compared to the NAR model. Although our theories are based on the SBM generative model, all examples demonstrate empirically that the CNAR applies to a wider group of network models. Therefore, the CNAR model is shown to be more robust than the NAR model.

Figure 3: Example 2 (General low-rank network and CNAR model with and ). Box plots for the ReMSE for estimated network AR coefficient and 1-step prediction by NAR (first row) and CNAR (second row), respectively. -

Example 3

(Stochastic Block Model and NAR) In this setting we consider a situation where the data is generated from the NAR model. Thus the situation is more favorable to NAR in this case. Specifically, the adjacency matrix is generated according to the SBM in Example 1. We set with , where is the row-normalized adjacency matrix. The network size is given as and the time length is specified as . For the CNAR model, we take .

We estimate for NAR, for CNAR (see Remark 1). The ReMSE of the estimates and the 1-step predictions are depicted in Figure 4. While NAR achieves better estimation accuracy with small sample size (e.g., ), CNAR still estimates and predicts with comparable accuracy even under model misspecification. This again demonstrates that the CNAR model is flexible enough to capture the data structure.

Figure 4: Example 3 (SBM and NAR model with and ). Box plots of ReMSE for estimated network AR coefficient and 1-step prediction by NAR (first row) and CNAR (second row), respectively.

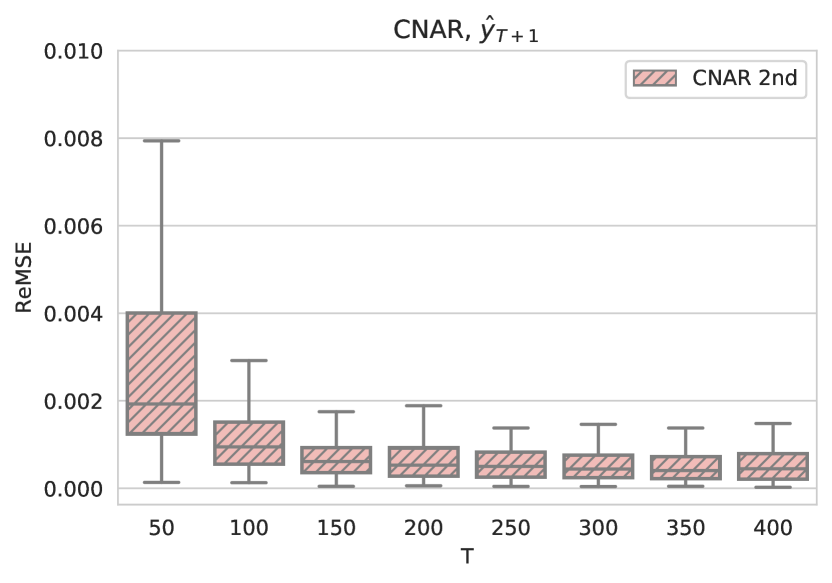

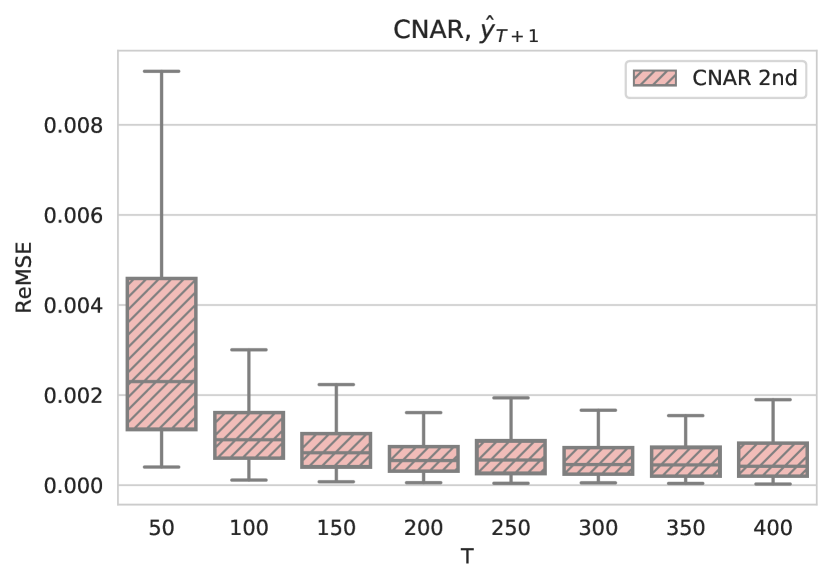

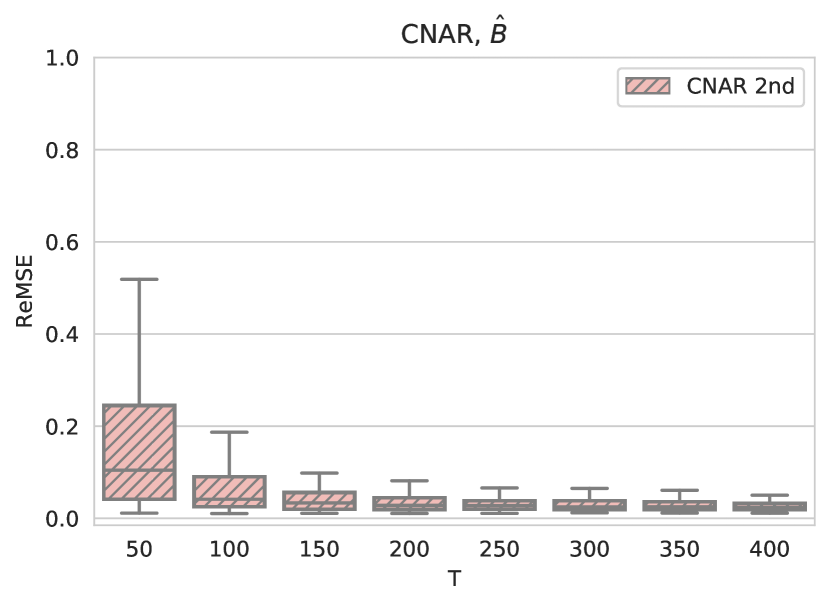

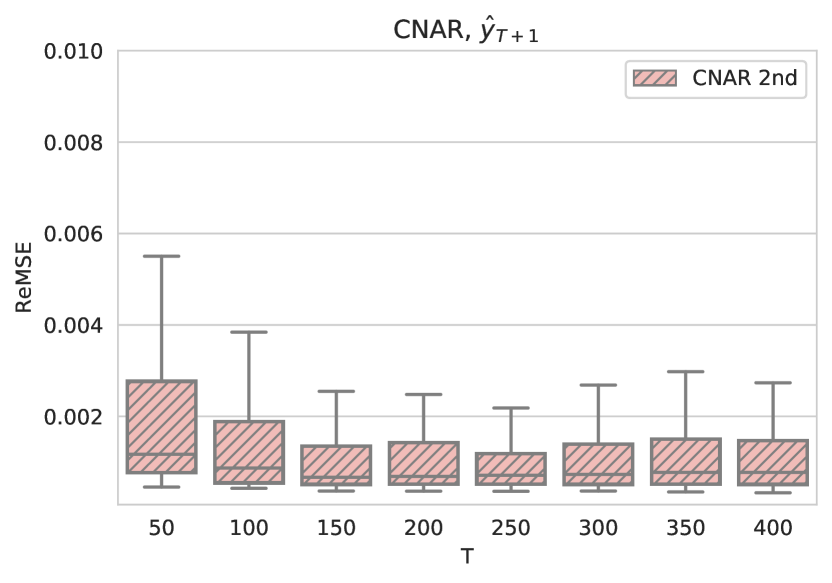

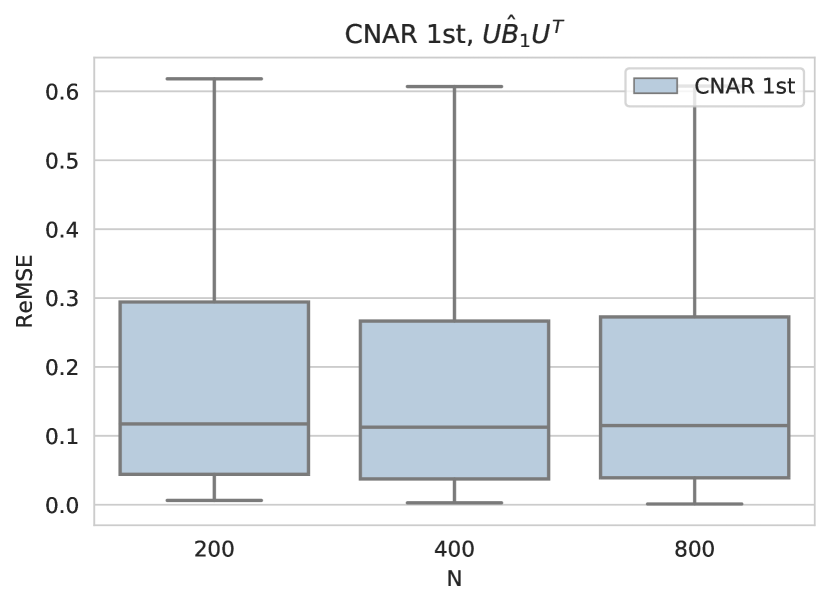

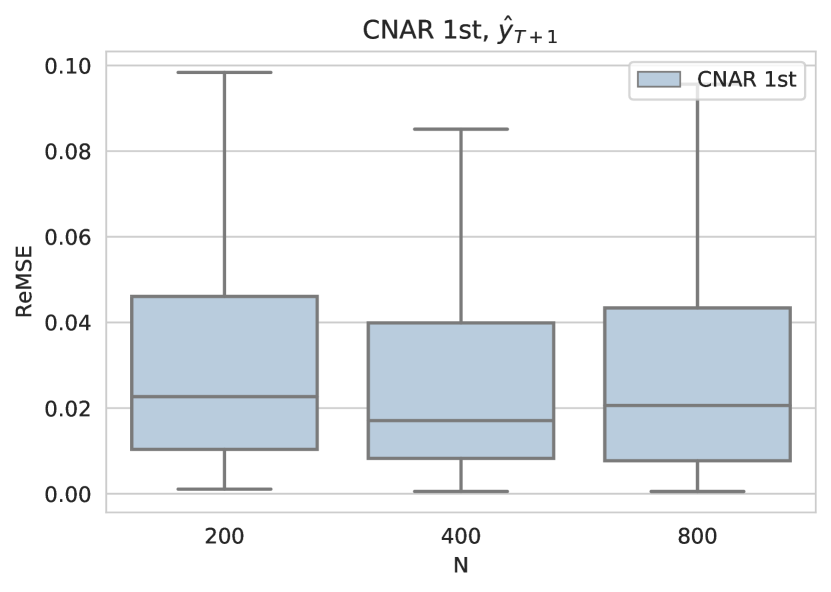

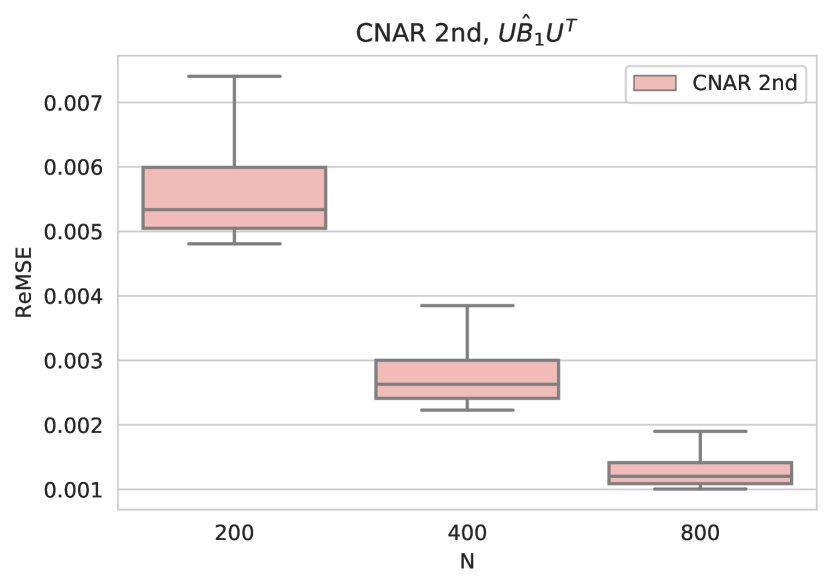

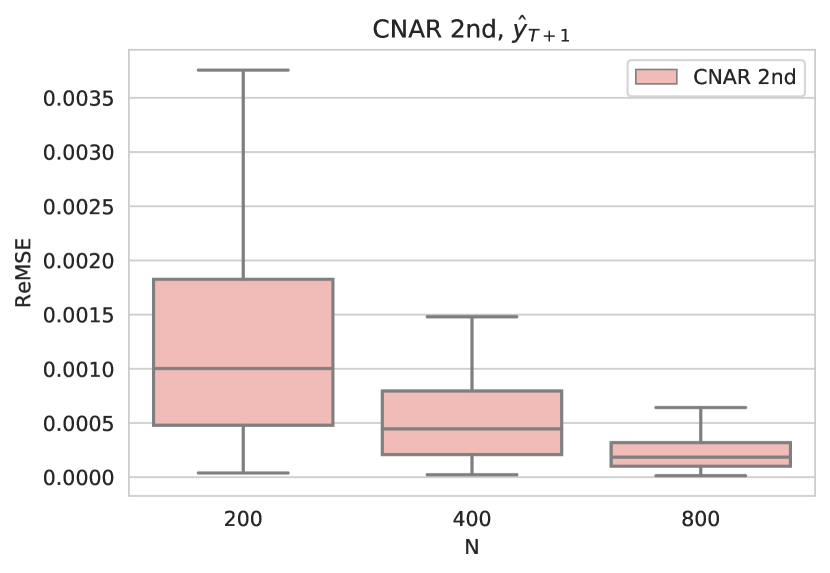

5.2 Comparison of CNAR 1st and 2nd-step estimators

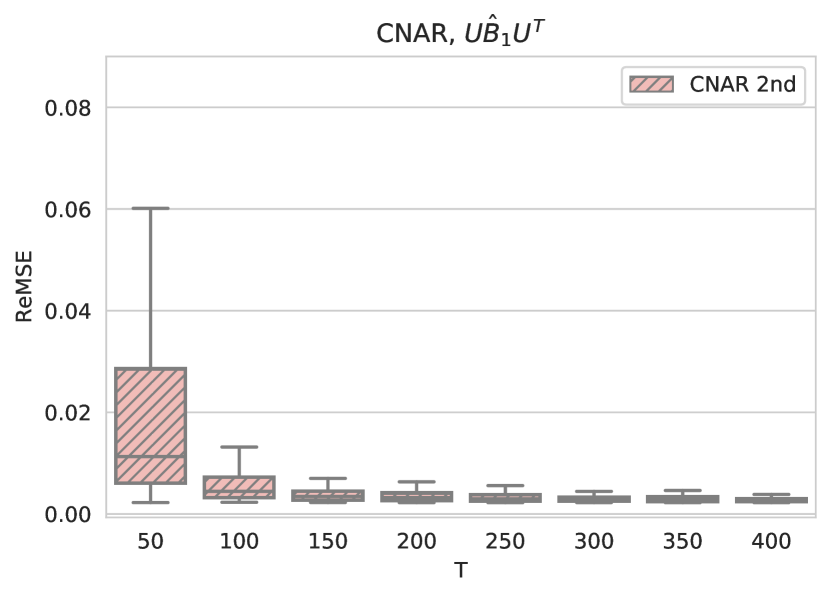

We investigate the different rates of convergence of the CNAR 1st and 2nd-step estimator when we increase . The data are generated following Example 1 with , and varying in . Figure 5 presents the ReMSE of estimated network AR coefficient and 1-step prediction by CNAR 1st (first row) and 2nd-step estimator (second row), respectively. We observe that estimation error of the 1st-step estimator does not change when increases while that of the 2nd-step estimator decreases. This confirms our theoretical results that the 1st-step estimator converges at the rate while the 2nd-step estimator converges at the rate .

6 Real Data Application

In this section, we conduct data analysis using stock return data in Chinese A stock market, which are traded in the Shanghai Stock Exchange and the Shenzhen Stock Exchange. The response is the daily stock return for trading days of stocks in the year of 2014. Motivated by Fama and French (2015), we include the following sixcovariates related to corporations’ fundamentals. They are, SIZE (i.e., the logarithm of market value), BM (i.e., book to market value), PR (i.e., yearly incremental profit ratio), AR (i.e., yearly incremental asset ratio), LEV (i.e., leverage ratio), and CASH (i.e., cash flow).

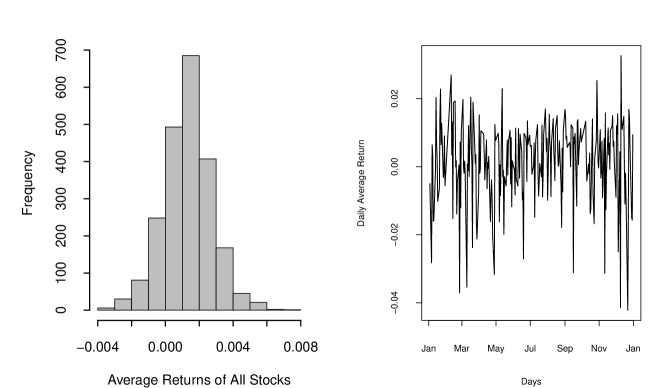

We first conduct a preliminary descriptive analysis of the data. First, for each stock, we calculate the average return during the whole year, i.e., . This leads to the histogram in the left panel of Figure 6. The mean daily return of all stocks is given by 0.13%. Next, for each day, we calculate the average daily returns over all stocks, i.e., . This yields the line chart in the right panel of Figure 6. A higher volatility level can be captured during January to March and November to December.

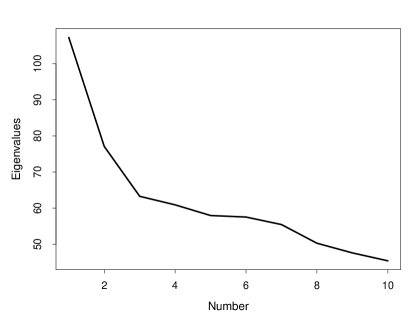

We construct the network relationship by using the top ten shareholder information of stocks. Specifically, if the th and th stock shares at least one of the top ten shareholders (Zhu et al., 2019), otherwise . We next conduct spectral clustering algorithm using the adjacency matrix following (Lei and Rinaldo, 2015). By the screeplot of the eigenvalues (shown in Figure 7), we set the number of groups to be . The group sizes are given as 78, 461, 1648 respectively.

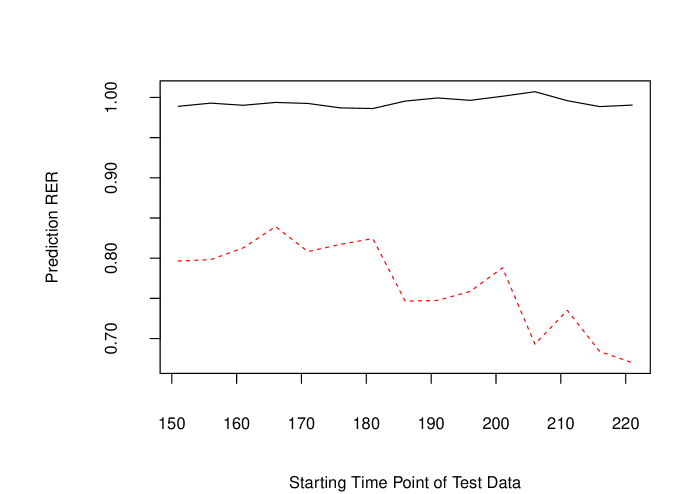

We next estimate the parameters in the CNAR model using the data. To evaluate the model performance, a sliding window approach is used. The number of factors is selected to be by using the screeplot approach. The time window for model training is set to be days. Then, the subsequent days are employed for model testing. The mean square prediction error is calculated as , where is the predicted response and is the first time point of the testing data. Further define a baseline MSPE as , where is the mean responses of the th node within the training period. A relative prediction error is then defined as . For model comparison, the CNAR model is compared with the NAR model (Zhu et al., 2017) in terms of the prediction accuracy. Specifically, the ReMSPE are given in Figure 8. As one could observe, the prediction accuracy of the CNAR model is about 20%–30% higher than the NAR model, which illustrates the prediction power of the proposed methodology.

7 Summary

Modeling a high-dimensional time series with network dependence is a difficult yet commonly encountered problem in real-world applications. The CNAR model mitigates the problem by incorporating the community structure in a network, yet provides more flexibility than the NAR model by allowing network coefficients to vary across different communities. In addition, it takes account of possible non-network-related factors and thus corrects the unrealistic assumption of the NAR model that the noises are cross-sectional uncorrelated. Both theoretical and empirical results confirm the advantage of CNAR model.

There are several interesting future research topics under the general framework of the CNAR model. First, the theoretical analysis of the CNAR is based on the assumption of a underlying stochastic block model. Generally speaking, any community structure will work if can be estimated consistently. This is illustrated empirically by a simulation study here. Therefore, it is of great interest to investigate this problem formally under different network structures. Second, the network structure discussed here is assumed to be static. However, in reality the network structure typically evolve slowly with time. Incorporating in the proposed CNAR model with a time-varying network structure is another interesting problem worth pursuing. Last, in this work we allow for estimating network effects for a diverging number of communities. In future study one could further consider high dimensional covariates and discuss variable screening and selection procedures under the model framework.

References

- Abbe et al. (2017) Abbe, E., J. Fan, K. Wang, and Y. Zhong (2017). Entrywise eigenvector analysis of random matrices with low expected rank. arXiv preprint arXiv:1709.09565.

- Anderson and Rubin (1956) Anderson, T. W. and H. Rubin (1956). Statistical inference in factor analysis. In Proceedings of the third Berkeley symposium on mathematical statistics and probability, Volume 5, pp. 111–150.

- Bai (2003) Bai, J. (2003). Inferential theory for factor models of large dimensions. Econometrica 71(1), 135–171.

- Bai et al. (2008) Bai, J., S. Ng, et al. (2008). Large dimensional factor analysis. Foundations and Trends® in Econometrics 3(2), 89–163.

- Barabási and Albert (1999) Barabási, A.-L. and R. Albert (1999). Emergence of scaling in random networks. science 286(5439), 509–512.

- Basu et al. (2015) Basu, S., G. Michailidis, et al. (2015). Regularized estimation in sparse high-dimensional time series models. The Annals of Statistics 43(4), 1535–1567.

- Bickel et al. (2008) Bickel, P. J., E. Levina, et al. (2008). Covariance regularization by thresholding. The Annals of Statistics 36(6), 2577–2604.

- Cai and Liu (2011) Cai, T. and W. Liu (2011). Adaptive thresholding for sparse covariance matrix estimation. Journal of the American Statistical Association 106(494), 672–684.

- Clauset et al. (2009) Clauset, A., C. R. Shalizi, and M. E. Newman (2009). Power-law distributions in empirical data. SIAM review 51, 661–703.

- Desai and Storey (2012) Desai, K. H. and J. D. Storey (2012). Cross-dimensional inference of dependent high-dimensional data. Journal of the American Statistical Association 107(497), 135–151.

- Dou et al. (2016) Dou, B., M. L. Parrella, and Q. Yao (2016). Generalized yule–walker estimation for spatio-temporal models with unknown diagonal coefficients. Journal of Econometrics 194(2), 369–382.

- Fama and French (2015) Fama, E. F. and K. R. French (2015). A five-factor asset pricing model. Journal of Financial Economics 116(1), 1–22.

- Fan et al. (2008) Fan, J., Y. Fan, and J. Lv (2008). High dimensional covariance matrix estimation using a factor model. Journal of Econometrics 147(1), 186–197.

- (14) Fan, J., R. Li, C.-H. Zhang, and H. Zou. Statistical Foundations of Data Science. Chapman & Hall/CRC.

- Fan and Liao (2019) Fan, J. and Y. Liao (2019). Learning latent factors from diversified projections and its applications to over-estimated and weak factors. under review.

- Fan et al. (2011) Fan, J., Y. Liao, and M. Mincheva (2011). High dimensional covariance matrix estimation in approximate factor models. Annals of statistics 39(6), 3320.

- Fan et al. (2013) Fan, J., Y. Liao, and M. Mincheva (2013). Large covariance estimation by thresholding principal orthogonal complements. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 75(4), 603–680.

- Fortunato (2010) Fortunato, S. (2010). Community detection in graphs. Physics reports 486(3-5), 75–174.

- Hagberg et al. (2008) Hagberg, A., D. A. Schult, and P. J. Swart (2008). Exploring network structure, dynamics, and function using networkx. In T. V. Gäel Varoquaux and J. Millman (Eds.), Proceedings of the 7th Python in Science Conference (SciPy2008), pp. 11–15.

- Hall and Heyde (2014) Hall, P. and C. C. Heyde (2014). Martingale limit theory and its application. Academic press.

- Härdle et al. (2016) Härdle, W. K., W. Wang, and L. Yu (2016). TENET: Tail-event driven network risk. Journal of Econometrics 192(2), 499–513.

- Holme and Kim (2002) Holme, P. and B. J. Kim (2002). Growing scale-free networks with tunable clustering. Physical review E 65(2), 026107.

- Lee and Yu (2009) Lee, L.-f. and J. Yu (2009). Spatial nonstationarity and spurious regression: the case with a row-normalized spatial weights matrix. Spatial Economic Analysis 4(3), 301–327.

- Lei and Rinaldo (2015) Lei, J. and A. Rinaldo (2015). Consistency of spectral clustering in stochastic block models. The Annals of Statistics 43(1), 215–237.

- Liu et al. (2017) Liu, X., E. Patacchini, and E. Rainone (2017). Peer effects in bedtime decisions among adolescents: a social network model with sampled data. The Econometrics Journal 20(3), S103–S125.

- Rohe et al. (2011) Rohe, K., S. Chatterjee, B. Yu, et al. (2011). Spectral clustering and the high-dimensional stochastic blockmodel. The Annals of Statistics 39(4), 1878–1915.

- Rudelson et al. (2013) Rudelson, M., R. Vershynin, et al. (2013). Hanson-wright inequality and sub-gaussian concentration. Electronic Communications in Probability 18.

- Shi and Lee (2017) Shi, W. and L.-f. Lee (2017). Spatial dynamic panel data models with interactive fixed effects. Journal of Econometrics 197(2), 323–347.

- Sojourner (2013) Sojourner, A. (2013). Identification of peer effects with missing peer data: Evidence from project star. The Economic Journal 123(569), 574–605.

- Stock and Watson (2011) Stock, J. H. and M. Watson (2011). Dynamic factor models. Oxford Handbooks Online.

- Sun (2016) Sun, Y. (2016). Functional-coefficient spatial autoregressive models with nonparametric spatial weights. Journal of econometrics 195(1), 134–153.

- Sun and Malikov (2018) Sun, Y. and E. Malikov (2018). Estimation and inference in functional-coefficient spatial autoregressive panel data models with fixed effects. Journal of Econometrics 203(2), 359–378.

- Vershynin (2011) Vershynin, R. (2011). Lectures in geometric functional analysis. Preprint, University of Michigan.

- Wang et al. (2016) Wang, H., J. Lin, and J. Wang (2016). Nonparametric spatial regression with spatial autoregressive error structure. Statistics 50(1), 60–75.

- Zhao et al. (2012) Zhao, Y., E. Levina, J. Zhu, et al. (2012). Consistency of community detection in networks under degree-corrected stochastic block models. The Annals of Statistics 40(4), 2266–2292.

- Zhu et al. (2019) Zhu, X., X. Chang, R. Li, and H. Wang (2019). Portal nodes screening for large scale social networks. Journal of Econometrics 209(2), 145–157.

- Zhu et al. (2018) Zhu, X., D. Huang, R. Pan, and H. Wang (2018). Multivariate spatial autoregression for large scale social networks. Journal of Econometrics To appear.

- Zhu et al. (2019) Zhu, X., D. Huang, R. Pan, and H. Wang (2019). Multivariate spatial autoregressive model for large scale social networks. Journal of Econometrics.

- Zhu et al. (2017) Zhu, X., R. Pan, G. Li, Y. Liu, and H. Wang (2017). Network vector autoregression. Annals of Statistics 45(3), 1096–1123.

- Zhu et al. (2019) Zhu, X., W. Wang, H. Wang, and W. K. Härdle (2019). Network quantile autoregression. Journal of econometrics 212(1), 345–358.

- Zou et al. (2017) Zou, T., W. Lan, H. Wang, and C.-L. Tsai (2017). Covariance regression analysis. Journal of the American Statistical Association 112(517), 266–281.

Appendix A Proofs of Parameter Estimation

A.1 Proof of Theorem 2.1

Note that the solution given by Theorem 2.1 satisfies the CNAR model. We then verify that the solution satisfies strict stationarity. Note that

Specifically we have . It yields that

| (26) |

by the condition in Theorem 2.1. It then holds that exists and is a strictly stationary process.

We next verify that the uniqueness of the stationary solution. Assume is another stationary solution to the CNAR model (2) with . Then we have for any integer . Consequently, by (26) one can conclude , where is a finite constant. Here is chosen arbitrarily. Hence we have , which implies with probability 1. This completes the proof.

A.2 Proof of Theorem 4.1

In the following we first prove that the asymptotic normality holds for . Then the result could also be obtained for by following the similar procedure.

Step 1. (Proof of ) Recall that we have

It suffices to deal with and separately. Then we have . Note that and take the form as

| (30) | |||

| (34) |

Let . Note that . Without loss of generality, we assume in the following.

(2) . It suffices to show that for any we have . Write . Hence we have . Accordingly, denote and , where . Then constitutes a martingale array. Then we employ the central limit theorem (Corollary 3.1 of Hall and Heyde (2014)) to obtain the result.

First we have

Note that . According to (48) of Lemma A.4, we have , where is a finite constant. To verify the asymptotic normality, we prove the following two results.

(a) .

Due to the similarity, we verify that . It suffices to verify that and . Note that follows . For the first one we have . Then by using (61). Hence . Then the result holds. The second could be similarly proved by noticing .

(b) .

Denote . Following the same procedure of proving (57), we could show that

Hence the conclusion (b) holds.

Step 2. (Proof of ).

A.3 Proof of Theorem 4.2

1. Proof of (18). First we have

where is defined in (30). To prove the result, it suffices to show that for any with , we have and , where is defined in (17) and . For the first conclusion, it suffices to verify that Note by (64) of Lemma A.8 and specifying , can be obtained by the assumption that . We then show

| (35) |

in the following.

Note here is finite, therefore it suffices to show that for any with that Denote and . Then constitutes a martingale array. The rest of the proof can be obtained by following the Step 1 (2) in the proof of Theorem 4.1 to employ the central limit theorem (Corollary 3.1 of Hall and Heyde (2014)) and (64) of Lemma A.8.

A.4 Proof of Theorem 4.4

Define . Let be the estimated precision matrix after the first step estimation. Correspondingly, let . We have the following expression,

It suffices to show for any with , that

| (36) | |||

| (37) |

(36) can be obtained by using by (68) of Lemma A.8. Next, (37) can be subsequently proved by using the central limit theorem (Corollary 3.1 of Hall and Heyde (2014)) of the martingale sequence by following the proof of (35) in the proof of Theorem 4.2.

A.5 Theoretical Properties under

In this scenario, we present the theoretical properties in the following theorem.

Theorem A.1.

Under , the convergence rate of is still the same but is asymptotically uncorrelated with . The proof is given as follows.

Proof.

Under the case , we replace by with , and with . In addition, define as the estimator for . Denote and as in (30) except replacing with . In addition, define .

A.6 Technical Lemmas

In this section we present several technical Lemmas, which will be used in the proof of the main Theorems. Specifically, Lemma A.2 to A.5 establish convergence conditions for the high dimensional time series . Lemma A.6 provides Frobenius or bounds of the leading eigenvectors of the adjacency matrix under SBM. Lemma A.7 to A.8 establish nonasymptotic bounds related to , which are critical for proving main theoretical results of the estimators.

Lemma A.2.

Let , where s are independent and identically distributed

random variables with mean zero, variance and finite fourth order moment.

Let , where

and independently follows multivariate normal distribution with .

Define .

In addition, assume the independence between and .

Let be an arbitrary square matrix.

Then the following conclusion holds.

(a) if the limit exists

and

| (38) |

as .

(b)

if

| (39) |

as .

(c) if the limit exists

and as .

Proof.

Let . Then we have . Using the conclusion (d) of Lemma 1 in Zhu et al. (2017), the result can be obtained. ∎

Lemma A.3.

Let and . Assume and , where and are finite constants. Assume and . Then it holds for any integer that

| (40) |

for any vector satisfying , and is a finite positive constant. In addition, we have

| (41) | |||

| (42) |

where and are finite constants.

Proof.

Note that . Hence it suffices to deal with the upper bounds respectively for and .

Note that . Then we have

| (43) | |||

| (44) |

Proof of (40). It suffices to deal with the upper bounds respectively for and .

(1) Upper Bound for . First note . Then it suffices to derive upper bounds for directly. By (44) we have

| (45) |

where the inequality is due to the Cauchy’s inequality that .

(2) Upper bound for . Note that by and (45) we have .

Proof of (41) and (42). Due to the similarity of the proof, we only show the proof of (42) in the following. Recall that . Then it suffices to derive the upper bound for and respectively. By (44), we have

.

Note that . By Cauchy’s inequality, we have

Hence we have

| (46) |

Next, note that by Cauchy’s inequality

where is a finite constant. Then by (46) the result can be obtained.

∎

Lemma A.4.

Let be a set of identically distributed random variables. Assume that (a) for ; (b) for any ; (c) for any ; (d) and , where is a finite positive constant. Let , , and , where and are dimensional matrices, are -dimensional vectors. We then have

| (47) | |||

| (48) |

where is a finite constant.

Proof.

Lemma A.5.

Assume is diagonalizable, i.e., , where is a diagonal matrix. Let as defined in Section 2.3. Then

where .

Proof.

Let collect the complement orthogonal vector of . Further denote , thus we have . Further denote , , and . Therefore we have , where is a diagonal matrix. This leads to . First by definition we have we have

Further by the decomposition of we have , where is diagonal with entries . By the condition we have . Therefore is invertible for all and the eigenvalues of are for all and . Hence we have

∎

Lemma A.6.

Let be an adjacency matrix generated from a stochastic block model . Assume that is of rank , with smallest absolute nonzero eigenvalue at least and for some . Let be the leading eigen-vectors of and , respectively. Then, there exist a orthonormal matrix and a constant such that

| (49) |

with probability at least .

Proof.

Combining Lemma 5.1 and Theorem 5.2 of Lei and Rinaldo (2015), we obtain that, for some orthonormal matrix ,

with probability at least . The constant is the absolute constant invovled in Theorem 5.2. The maximum degree in Theorem 5.2 becomes in the current setting. ∎

Lemma A.7.

Assume the same conditions as in Theorem 4.2. Define if and otherwise. For any vector , , with and , it holds

| (50) | |||

| (51) | |||

| (52) | |||

| (53) | |||

| (54) |

In addition, let , , . Then we have

| (55) | |||

| (56) |

If and , then define and . Otherwise define by replacing (or ) with (or ). Let and . Accordingly, define as in (17). It holds that for any

| (57) |

Furthermore by assuming we have

| (58) | |||

| (59) |

Proof.

We prove the results one by one in the following. Recall that and takes the form in (43). Hence if , we could drop in and the proof procedure is the same. In this case we could verify that . Assume (thus ) and for convenience in the following. This leads to for any .

Proof of (50): Note that . Let and denote and . Hence we have , where . By the Hanson-Wright inequality of Rudelson et al. (2013), we have

| (60) |

where . Note that . For any satisfying we have

Recall that . According to Basu et al. (2015) (Proposition 2.3 and (2.6)) and Lemma A.5 we have

| (61) |

where , and is assumed to be diagonalizable. Furthermore, note that . Therefore we have . Hence by the conditions in Theorem 4.2 and (61), we have , which leads to the final result.

Proof of (51): Note that we have . Let . It can be derived that

Using (60) and follow the same technique in proving (50), we can show for any

| (62) |

Then by the maximum inequality property, (51) can be proved.

Proof of (52)–(54): The proofs of (52) and (53) are similar to (51). Note that for (52) . Hence and omitted here.

Proof of (58) and (59): The result of (58) can be obtained by replacing by in (50)–(52). Due to the similarity we only show the first one. Note that we have we have decomposition as follows

We then bound the above two parts respectively.

(a) Bound on .

Note that

| (63) |

Hence we have

By letting and noting and by (61), the conclusion can be obtained by using Lemma A.6.

(b) Bound on .

Let . Note that we have . Then we have by (57). By using the technique in deriving (63), we have . It can be verified that . Consider the events . Then by Chebyshev’s Inequality,

as long as . Letting , the result can be obtained.

By using the same technique in (50), we can firstly show that

Proof of (55) and (56): Let and let , . Then we have . Hence we have for any . It can be easily verified that and . Similar to (50), by using the Hanson-Wright inequality given in Rudelson et al. (2013), it can concluded that

which proves (55).

Similarly, note that . Then it can be verified that and . Therefore by the Hanson-Wright inequality (56) can be proved.

∎

Lemma A.8.

Proof.

Proof of (64): We consider the set . Choose as a -net of , where the definition of covering net is given in Vershynin (2011). By Lemma 3.5 of Vershynin (2011), we have . It holds that for every , there exists some such that , where . Define . Then we have

Note that . Therefore the third term is bounded by . Next by Cauchy’s inequality we have . Hence one could derive that . Combining the result of Lemma A.7, it implies,

This completes the proof.

Proof of (67) and (68): Note that

can be decomposed into two parts. Therefore we deal with each part separately. First note that by Theorem 4.3. Hence we have

due to by (64).

Next, by the same argument to (64), we could establish that

where the details are omitted here. We have . This leads to (67). Lastly, (68) can be obtained by following the same technique by using (65).

∎

Appendix B Property of the covariance estimator of

In this section, we establish the convergence rate of the covariance estimator from – the residual from the first-step regression residual of the CNAR model. Recall that the oracle estimators and are the first-step estimators when the rotated community membership matrix is known and the feasible estimator and are those when is estimated from the adjacency matrix . Here we only show results for the oracle estimators and . Since is assume to be uncorrelated with and , so is . Lemma A.6 establishes that is a consistent estimator of . Thus, the proof of the non-oracle case where a consistent estimator is plugged in is a trivial extension whose technique is the same as that in Theorem 4.1 (ii).

We make use of some results in Fan et al. (2013). However, there are several differences: first, even with oracle , the task here is slightly different from that in Fan et al. (2013) since direct observations for is not available. Instead, we observe – the residual from the first step regression of the CNAR model. That is, ; second, the dimension of is , where the number of communities is allow to grow with the number of network nodes . Thus, shows up in our results; third, we are considering a time series here, thus is correlated with . Recall that the first-step estimator

where

| (69) |

Plugging in the formula of in , we have

| (70) |

We denote and use in general. In our first CNAR case, we have by Theorem 4.1.

B.1 Assumptions

The following Assumptions B.1 – B.4 are the same as Assumptions 1-4 from Fan et al. (2013). They are included here for completeness. See Fan et al. (2013) for more discussions on these assumptions. Assumption B.5 is special for our setting. It puts regularity condition on the CNAR covariates. Sub-Gaussian covariates satisfy Assumption B.5.

Assumption B.1 (Pervasiveness).

All eigenvalues of the matrix are bounded away from both 0 and as .

Assumption B.1 requires the factors to be pervasive. Because of the fast diverging eigenvalues, it is hard to achieve a good rate of convergence for estimating under whether the spectral norm or Frobenius norm when . However, the quantity of interest in our case is , which can be consistently estimated with good rate.

Assumption B.2 (Factor and idiosyncratic components).

-

(a)

is strictly stationary. In addition, , for all , and .

-

(b)

There are constants such that , and

-

(c)

There are and such that, for any , and ,

Assumption B.3 (Strong mixing).

Let and denote the -algebras that are generated by and respectively. Define the mixing coefficient

There exists such that , and satisfying, for all ,

Note that Assumption B.3 is weaker than the assumption that are uncorrelated overtime. Thus it is automatically satisfied under Assumptions in Appendix A.

Assumption B.4 (Regularity conditions).

There exists such that, for all , , and ,

-

(a)

where is the -th row of .

-

(b)

.

-

(c)

.

Assumption B.5 (Regularity condition on CNAR covariates).

Re call that . Let ,

-

(a)

For all , , , ,

-

(b)

For all , , .

-

(c)

For all , , .

-

(d)

For all and , define random variable

we assume .

B.2 Technical lemmas

Lemma B.6.

Consider a stationary auto-regressive model of order 1 AR(1): , where , then for any ,

-

(i)

.

-

(ii)

.

-

(iii)

.

Proof.

-

(i)

We have . Then, by stationary condition . For any , we have .

Proofs of (ii) and (iii) are the same. ∎

Lemma B.7.

Suppose that the random variables and both satisfy the exponential-type tail condition: There exist and , such that, ,

Then for some and , and any ,

Proof.

Lemma A.2 in Fan et al. (2011). ∎

Lemma B.8.

Suppose that the random variable , , has bounded fourth moments, that is, where and is a positive constant. Then .

Proof.

Applying the Markov’s inequality to the fourth moments, we have , . By Bonferroni’s method, we have

For any , this probability can be driven below by choosing . Thus, .

∎

Lemma B.9.

Proof.

Lemma B.10.

B.3 Covariance estimation of

B.3.1 Loading and factor estimators

The common factors need to be estimated uniformly in . When we do not observe , in addition to the factor loadings, there are factors to estimate. Intuitively, the condition requires the number of parameters that are introduced by the unknown factors to be ‘not too many’, so we can estimate them uniformly. Technically, as demonstrated by Bickel et al. (2008), Cai and Liu (2011) among many others, achieving uniform accuracy is essential for large covariance estimation.

Recall that is defined in (70). Let , . In addition, let be the diagonal matrix of the first largest eigenvalues of in decreasing order, and is -times the corresponding eigenvector (i.e., the estimated factors). By the definition of eigenvectors and eigenvalues, we have (or ) and . Let with defined in (70),

Let , we have a similar decomposition of factor estimation errors as expression (A.1) in Bai (2003):

| (72) | ||||

To bound , we need the following lemmas, along with Lemma 8 and 9 in Fan et al. (2013).

Proof.

- (a)

-

(b)

where the last equation is derived the same as that in (a).

-

(c)

Same as that of (b).

∎

Proof.

-

(a)

Recall that be the diagonal matrix of the first largest eigenvalues of in decreasing order. Similar to Lemma 5 in Fan et al. (2013), it is straightforward to prove that all the eigenvalues of are bounded away from 0. Using inequality and identity (72), we have, for some constant ,

The first four terms on the right-hand side are bounded in in Lemma 8 in Fan et al. (2013), while the last three terms are bounded in Lemma B.11which produce an additional term with order .

-

(b)

Part (b) follows inequality and part (a).

∎

Lemma B.13.

-

(a)

.

-

(b)

.

Proof.

Corollary B.14.

Proof.

-

(a)

Using the fact that and that , we have

We bound each term on the right-hand side. It follows from Lemma 4 (iii) in Fan et al. (2013) and Lemma B.13 that

For the second term, . Therefore, . The Cauchy-Schwarz inequality and (a) imply

For the third term, and imply that the third term is .

For the last term, we have

where we use the result that derived in Lemma B.10 (c). The result follows by adding all term together.

∎

B.3.2 Idiosyncratic covariance bound

Lemma B.15.

Proof.

Corollary B.16.

B.3.3 Covariance bound of the CNAR residual

Lemma B.17.

Denote , we have the following results:

-

(i)

and .

-

(ii)

.

-

(iii)

.

Proof.

Lemma B.18.

Denote , we have

Proof.

Lemma B.19.

Denote . If , then with probability approaching 1, for some ,

-

(i)

.

-

(ii)

-

(iii)

-

(iv)

Proof.

Our result corresponds to the special case where and is a constant in Lemma 15 in Fan et al. (2013). The proof is the same and thus omitted here. ∎

B.3.4 Proof of Theorem 4.3

Proof.

Denote ,

- (i)

-

(ii)

Define . Note that and . The triangular inequality gives

Step 1. Firstly, we bound .

Let and .

By Sherman-Morrison-Woodbury formula, we have and . Hence it leads to , where

We bound each of the six terms. First, is bounded in Corollary B.16 (ii): . Then,

which used the results that and by Lemma B.19. Similarly, we have . Since Then,

Similarly, . Finally, by Lemma B.19, . Then, by Lemma B.18,

Consequently, . Adding up to gives,

Step 2. Now we turn to . Again, using the Sherman-Morrison-Woodbury formula, we have

where the first equation is due to that and , by Lemma B.19.

∎

Appendix C Additional simulation results

C.1 Different network models

-

Example 4

(Clusters of Powerlaw graphs and CNAR) In this section, we consider a network generated by Holme and Kim algorithm (Holme and Kim, 2002) for growing graphs with powerlaw degree distribution. Specifically, in this type of network, communities are generated the degrees of the nodes follow a powerlaw distribution. As a result, it assumes that the majority of nodes have few connections but a small proportion have a large amount of connections (Barabási and Albert, 1999; Clauset et al., 2009). Numerically, the graph can be generated by the Holme and Kim algorithm implemented using the power law graph function powerlaw_cluster_graph in the Python NetworkX. For each node of the -th community, we set the expected degree as , where is the number of nodes in the -th community. Subsequently, we randomly add edges between the -th and -th communities for all with . The membership matrix is generated according to the original disjoint community assignment. Other model parameters, such as , and , are set in the same way as in Example 1. Under this setting we focus on the sensitivity analysis when the network is not generated from the SBM model. We set and vary . For CNAR, we set .

Figure 9: Example 4 (Power law and CNAR model with and ) box plots of estimated network AR coefficient and 1-step prediction by NAR (first row) and CNAR (second row), respectively. Figure 10 shows, for Example 4, the box plots of estimated network AR coefficient and 1-step prediction by NAR (first row) and CNAR (second row), respectively. Under this setting with a different network generative model, CNAR still has much smaller estimation and prediction error compared to the NAR model.

-

Example 5

(Random Partition Graph and CNAR) In this example, we consider a network generated by a random partition graph. A random partition graph is a graph of communities with different sizes. The nodes within the same group are connected with probability and nodes of different groups are connected with probability . The network is a generalization of the planted-l-partition described in Fortunato (2010). Under this setting we focus on the sensitivity analysis when the network is not generated from the SBM model. We fix , , set and vary . For CNAR, we set .

Figure 10: Example 3 ( and ) box plots of estimated network AR coefficient and 1-step prediction by NAR (first row) and CNAR (second row), respectively. Figure 10 shows, for Example 3, the box plots of estimated network AR coefficient and 1-step prediction by NAR (first row) and CNAR (second row), respectively. Under this setting with a different network generative model, CNAR still has much smaller estimation and prediction error compared to the NAR model.

C.2 More Tables

Table 1 compares the performance of CNAR and NAR in Example 1 with different numbers of network communities , network sizes and time series length . The performance of CNAR is better than that of NAR under all settings. For the CNAR model, it can be observed that the errors reduce when or with given number of communities , which corroborates with the theoretical findings.

| N | 200 | 400 | 800 | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| T | 100 | 200 | 400 | 100 | 200 | 400 | 100 | 200 | 400 | |

| CNAR | 1.028(0.826) | 0.692(0.235) | 0.573(0.109) | 0.671(0.64) | 0.378(0.175) | 0.282(0.064) | 0.423(0.574) | 0.188(0.111) | 0.132(0.038) | |

| 0.087(0.115) | 0.047(0.066) | 0.028(0.037) | 0.062(0.086) | 0.022(0.028) | 0.011(0.016) | 0.028(0.039) | 0.012(0.019) | 0.005(0.008) | ||

| 0.075(0.049) | 0.033(0.019) | 0.017(0.011) | 0.039(0.027) | 0.02(0.013) | 0.008(0.005) | 0.023(0.019) | 0.009(0.006) | 0.004(0.003) | ||

| 0.393(0.186) | 0.16(0.051) | 0.067(0.013) | 0.436(0.183) | 0.168(0.042) | 0.073(0.012) | 0.436(0.233) | 0.168(0.052) | 0.075(0.013) | ||

| 0.222(0.199) | 0.158(0.125) | 0.123(0.093) | 0.133(0.143) | 0.068(0.054) | 0.055(0.042) | 0.068(0.065) | 0.036(0.033) | 0.024(0.018) | ||

| NAR | 79.304(0.95) | 78.978(0.442) | 78.84(0.267) | 79.44(1.129) | 78.988(0.391) | 78.858(0.206) | 79.263(0.945) | 78.901(0.358) | 78.768(0.17) | |

| 1.18(1.617) | 0.609(0.87) | 0.323(0.417) | 1.012(1.341) | 0.408(0.534) | 0.197(0.238) | 0.84(1.137) | 0.427(0.562) | 0.29(0.392) | ||

| 0.128(0.09) | 0.063(0.039) | 0.034(0.024) | 0.062(0.045) | 0.029(0.019) | 0.013(0.008) | 0.049(0.043) | 0.026(0.019) | 0.016(0.01) | ||

| 131.969(33.141) | 135.776(32.599) | 132.931(29.923) | 147.165(47.26) | 162.518(46.868) | 149.743(47.375) | 148.61(43.089) | 152.632(43.682) | 148.676(42.989) | ||

| 29.393(22.326) | 29.081(22.5) | 26.765(20.776) | 25.45(18.84) | 24.625(19.555) | 24.977(19.662) | 23.822(19.763) | 26.169(19.523) | 22.901(18.158) | ||

| N | 200 | 400 | 800 | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| T | 100 | 200 | 400 | 100 | 200 | 400 | 100 | 200 | 400 | |

| CNAR | 6.438(4.782) | 3.699(1.463) | 2.781(0.67) | 12.215(13.866) | 3.751(3.269) | 2.287(1.191) | 6.715(7.052) | 2.808(3.018) | 1.44(0.751) | |

| 0.501(0.527) | 0.459(0.348) | 0.458(0.276) | 0.242(0.286) | 0.166(0.153) | 0.148(0.099) | 0.058(0.066) | 0.036(0.042) | 0.033(0.029) | ||

| 0.083(0.053) | 0.034(0.021) | 0.018(0.012) | 0.047(0.037) | 0.021(0.013) | 0.009(0.006) | 0.027(0.024) | 0.01(0.006) | 0.004(0.003) | ||

| 0.579(0.299) | 0.221(0.093) | 0.087(0.022) | 0.584(0.274) | 0.203(0.073) | 0.081(0.019) | 0.547(0.296) | 0.204(0.087) | 0.086(0.022) | ||

| 0.55(0.321) | 0.466(0.205) | 0.435(0.194) | 0.328(0.363) | 0.24(0.088) | 0.225(0.089) | 0.146(0.118) | 0.11(0.037) | 0.098(0.038)) | ||

| NAR | 118.235(11.852) | 120.618(7.064) | 120.764(5.263) | 117.957(10.267) | 118.787(6.804) | 118.434(3.579) | 117.439(11.364) | 118.106(7.028) | 119.381(4.248) | |

| 125.762(62.419) | 163.337(48.24) | 177.707(36.655) | 146.252(69.925) | 167.32(48.436) | 182.017(35.401) | 133.572(62.174) | 152.431(44.752) | 168.377(33.508) | ||

| 0.626(0.529) | 0.672(0.366) | 0.7(0.342) | 0.743(0.687) | 0.75(0.462) | 0.77(0.32) | 0.476(0.493) | 0.498(0.413) | 0.549(0.288) | ||

| 154.012(44.686) | 165.392(40.281) | 173.069(37.539) | 140.849(44.641) | 141.83(42.436) | 147.844(43.091) | 149.635(45.276) | 148.763(41.65) | 146.915(42.255) | ||

| 70.517(79.946) | 78.527(77.728) | 81.192(93.785) | 74.014(82.83) | 76.315(80.286) | 96.753(105.348) | 61.656(61.865) | 64.156(62.587) | 80.163(84.228) | ||

| N | 200 | 400 | 800 | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| T | 100 | 200 | 400 | 100 | 200 | 400 | 100 | 200 | 400 | |

| CNAR | 34.058(12.94) | 20.223(4.597) | 14.838(1.848) | 47.738(52.773) | 16.928(5.854) | 10.103(1.622) | 67.223(72.426) | 16.054(8.291) | 7.117(1.736) | |

| 7.882(5.952) | 8.632(4.437) | 8.414(3.188) | 1.624(1.528) | 1.314(0.876) | 1.27(0.564) | 0.569(0.526) | 0.522(0.368) | 0.549(0.243) | ||

| 0.096(0.068) | 0.042(0.025) | 0.021(0.013) | 0.052(0.042) | 0.023(0.014) | 0.009(0.006) | 0.033(0.029) | 0.011(0.007) | 0.005(0.003) | ||

| 0.97(0.55) | 0.338(0.16) | 0.119(0.039) | 1.032(0.587) | 0.315(0.14) | 0.108(0.039) | 0.998(0.543) | 0.307(0.152) | 0.113(0.039) | ||

| 3.302(2.062) | 3.285(1.791) | 3.086(1.99) | 1.432(1.539) | 1.102(0.525) | 1.131(0.625) | 0.679(0.355) | 0.531(0.198) | 0.513(0.206) | ||

| NAR | 112.158(6.815) | 115.272(5.37) | 115.143(3.672) | 111.769(7.856) | 113.367(5.904) | 113.878(3.362) | 112.965(9.235) | 113.947(5.687) | 114.929(3.282) | |

| 162.078(78.495) | 194.58(60.394) | 213.942(47.352) | 128.507(84.004) | 170.411(73.947) | 194.52(49.671) | 148.284(89.314) | 185.514(68.186) | 228.376(49.852) | ||

| 0.571(0.471) | 0.576(0.335) | 0.614(0.314) | 0.386(0.376) | 0.329(0.264) | 0.328(0.178) | 0.443(0.447) | 0.49(0.361) | 0.637(0.301) | ||

| 173.495(39.55) | 183.232(29.815) | 186.471(25.941) | 159.843(41.978) | 163.451(41.729) | 165.72(40.3) | 158.264(41.08) | 157.368(44.235) | 153.193(44.345) | ||

| 78.506(80.632) | 89.195(88.442) | 85.424(90.699) | 79.499(81.137) | 86.888(89.941) | 113.873(114.174) | 63.753(64.996) | 73.894(74.438) | 95.918(101.764) | ||