Optimization by moving ridge functions:

Derivative-free optimization for computationally intensive functions

Abstract

A novel derivative-free algorithm, optimization by moving ridge functions (OMoRF), for unconstrained and bound-constrained optimization is presented. This algorithm couples trust region methodologies with output-based dimension reduction to accelerate convergence of model-based optimization strategies. The dimension-reducing subspace is updated as the trust region moves through the function domain, allowing OMoRF to be applied to functions with no known global low-dimensional structure. Furthermore, its low computational requirement allows it to make rapid progress when optimizing high-dimensional functions. Its performance is examined on a set of test problems of moderate to high dimension and a high-dimensional design optimization problem. The results show that OMoRF compares favourably to other common derivative-free optimization methods, even for functions in which no underlying global low-dimensional structure is known.

keywords:

derivative-free optimization; nonlinear optimization; trust region methods; dimension reduction; ridge functions; active subspaces1 Introduction

Derivative-free optimization (DFO) methods seek to solve optimization problems using only function evaluations — that is, without the use of derivative information. These methods are particularly suited for cases where the objective function is a ‘black-box’ or computationally intensive (Conn, Scheinberg, and Vicente 2009b). In these cases, computing gradients analytically or through algorithmic differentiation may be infeasible and approximating gradients using finite differences may be intractable. Common applications of DFO methods include engineering design optimization (Kipouros et al. 2008), hyper-parameter optimization in machine learning (Ghanbari and Scheinberg 2017), and more (Levina et al. 2009). Derivative-free trust region (DFTR) methods are an important class of DFO which iteratively create and optimize a local surrogate model of the objective in a small region of the function domain, called the trust region. Unlike standard trust region methods, DFTR methods use interpolation or regression to construct a surrogate model, thereby avoiding the use of derivative information.

However, acquiring enough samples for surrogate model construction may be computationally prohibitive for problems of moderate to high dimension. This issue is magnified when considering computationally intensive functions, such as computational fluid dynamics (CFD) or finite element method (FEM) simulations, where a single function evaluation may require minutes, hours, or even days (Gu 2001). For these functions, the cost of optimization is dominated by the cost of function evaluation rather than by the optimization algorithm itself. Algorithms which can achieve an acceptable level of convergence in relatively few function evaluations are highly desirable in such cases. Shan and Wang (2010) provide a comprehensive survey of the unique challenges faced when optimizing high-dimensional, computationally intensive functions.

Fortunately, it has been shown that many functions of interest vary primarily along a low-dimensional linear subspace of the input space. For example, efficiency and pressure ratio of turbomachinery models (Seshadri et al. 2018), merit functions of hyper-parameters of neural networks (Bergstra and Bengio 2012), and drag and lift coefficients of aerospace vehicles (Lukaczyk et al. 2014) have all been shown to have low-dimensional structure. Functions that have this structure are known as ridge functions (Pinkus 2015), and may be written

| (1) |

where , , , denotes the -dimensional projection of domain onto the subspace , and . If , then exploiting low-dimensional structure may lead to significant reductions in computational requirement.

In this article, a novel DFTR method for unconstrained and bound-constrained nonlinear optimization of computationally intensive functions is presented. This algorithm is called optimization by moving ridge functions (OMoRF), as it leverages local ridge function approximations which move through the function domain. Although numerous optimization algorithms have used subspaces to reduce the problem dimension (Wang et al. 2016; Zhao, Alimo, and Bewley 2018; Kozak et al. 2019), OMoRF differs from these approaches in a few key aspects. First, it is completely derivative-free. This differs from the variance reduced stochastic subspace descent (VRSSD) algorithm presented by Kozak et al. (2019). Although the VRSSD algorithm does not require full gradient calculations, it still requires the computing of directional derivatives. Similarly, the Delaunay-based derivative-free optimization via global surrogates with active subspace method (-DOGS with ASM) proposed by Zhao, Alimo, and Bewley (2018) requires an initial sample of gradient evaluations to determine the dimension-reducing subspace. Second, the subspaces computed by OMoRF correspond to the directions of strongest variability of the objective function. In contrast, the random embeddings approach used by Wang et al. (2016) and Cartis and Otemissov (2020) randomly generates a dimension-reducing subspace which, in general, does not correspond to directions of high variability of the function. Finally, OMoRF does not assume a single global dimension-reducing subspace. Many similar algorithms which use ridge functions for optimization purposes (Lukaczyk et al. 2014; Zhao, Alimo, and Bewley 2018; Gross, Seshadri, and Parks 2020) assume the function domain can be sufficiently described using a constant, global subspace. That is, it is assumed that the function varies primarily along a constant linear subspace throughout the whole domain . This assumption may limit the application of ridge function modeling to a few special cases. Although adaptive sampling approaches have been previously applied for stochastic optimization with active subspaces (Choromanski et al. 2019), to the best of the authors’ knowledge, OMoRF is the first model-based optimization algorithm to propose the use of locally defined ridge function models.

This article has four main contributions. First, a novel strategy for dynamically updating the subspace of a locally defined ridge during model-based optimization is proposed. Moreover, using theoretical results from interpolation and ridge approximation theory, the benefits of this approach are demonstrated. Second, the novel DFTR algorithm, OMoRF, is presented. An open source Python implementation of this algorithm has been made available for public use. Third, a novel sampling method for ridge function models which maintains two separate interpolation sets, one for ensuring accurate local subspaces and one for ensuring accurate quadratic models over those subspaces, is presented. Finally, OMoRF is applied to a variety of test problems, including a high-dimensional aerodynamic design optimization problem.

The rest of this article is organized as follows. A brief introduction to trust region methods is provided in Section 2. In Section 3, algorithms for constructing ridge function approximations are explored. This section also includes a discussion on the full linearity of ridge function models, with this discussion motivating the use of moving ridge function models. The OMoRF algorithm and some key features of the algorithm are presented in Section 4. In Section 5, the algorithm is tested against other common DFO methods on a variety of test problems. Finally, a few concluding remarks are provided in Section 6.

2 Trust region methods

Trust region methods replace the unconstrained optimization problem

| (2) |

with a sequence of trust region subproblems

| (3) |

where is the current iterate, is the trust region radius, and is a simple model which approximates in the trust region

| (4) |

The solution to the trust region subproblem (3) gives a step , with a candidate for the next iterate . The ratio

| (5) |

is used to determine if the candidate is accepted or rejected and the trust region radius increased or reduced.

2.1 Derivative-free trust region methods

For standard trust region methods, a common choice of model is the Taylor series expansion centred around

| (6) |

where is a symmetric matrix approximating the Hessian . Constructing this Taylor quadratic clearly requires knowledge of the function derivatives. Alternatively, DFTR methods may use interpolation or regression to construct . That is, using a set of samples and basis functions , the model is defined as

| (7) |

where for are the coefficients of the model. In the case of fully-determined interpolation, the number of samples is equal to the number of coefficients, i.e. , so the coefficients may be determined by solving the linear system

| (8) |

where

| (9) |

Note that the current iterate is generally included in the interpolation set, so .

Global convergence of trust region methods which use the Taylor quadratic (6) has been proven (Conn, Gould, and Toint 2000). These convergence properties rely heavily on the well-understood error bounds for Taylor series. For these same guarantees to hold for DFTR methods, one must ensure the surrogate models satisfy Taylor-like error bounds

| (10) | ||||

for all , where are independent of and . Models which satisfy these conditions are known as fully linear. A similar definition exists for fully quadratic models, i.e. models which have similar convergence properties as a second-order Taylor series.

Satisfying certain geometric conditions on the sample set (Conn, Scheinberg, and Vicente 2008) allows one to ensure fully linear/quadratic models. In the case of polynomial surrogates, Conn, Scheinberg, and Vicente (2009b) proved that these conditions on were equivalent to bounding the condition number of the matrix

| (11) |

where

In particular, it was shown that, if the condition number of is sufficiently bounded, then polynomial models constructed from are fully linear/quadratic. Numerous algorithms for improving the geometry of for polynomial interpolation are presented by Conn, Scheinberg, and Vicente (2009b) (see Chapter 6).

2.2 Limitations of derivative-free trust region methods

Fully-determined polynomial interpolation of degree in dimensions requires function evaluations. In the case of quadratic interpolation, this would require sample points. When is small, this requirement may be easily met; however, as increases, this requirement may become prohibitive, particularly in the case of functions which are expensive to evaluate. Many DFTR methods account for this computational burden by avoiding the use of fully-determined quadratic models. For instance, the optimization algorithm COBYLA (Powell 1994) uses linear models, requiring only samples. Although this greatly reduces the effect of increased dimensionality, linear models generally do not capture the curvature of the true function, so convergence may be slow (Wendor, Botero, and Alonso 2016).

Some algorithms reduce the required number of samples by constructing under-determined quadratic interpolation models. This requires more samples than is necessary for linear models, but fewer than fully-determined quadratic models. For example, the algorithms NEWUOA (Powell 2006) and BOBYQA (Powell 2009) use minimum Frobenius norm interpolating quadratics, which require a constant number of more than points, but less than points. Generally, a default of is used. Many other optimization algorithms (Zhang, Conn, and Scheinberg 2010; Cartis et al. 2019) have used a similar approach, and it has proven to be quite effective in practice. Nevertheless, this initial requirement may limit the efficacy of these approaches when the objective is both high-dimensional and computationally expensive.

Alternatively, other DFTR algorithms seek to reduce the initial start-up cost by using very few points initially, but increasing the number of points as more become available. For example, the DFO-TR algorithm proposed by Bandeira, Scheinberg, and Vicente (2012) builds quadratic models using significantly fewer than points, possibly as few as points. Although this was done using minimum Frobenius norm models, as in NEWUOA and BOBYQA, they also showed that, by assuming approximate Hessian sparsity, one could also use sparsity recovery techniques, such as compressed sensing (Eldar and Kutyniok 2012). Furthermore, it was proven that such models are probabilistically fully quadratic. That is, these models satisfy second-order Taylor-like error bounds with a probability bounded below by a term dependent on the number of sample points used. Moreover, the convergence of DFTR methods which employ probabilistically fully linear/quadratic models was proved by Bandeira, Scheinberg, and Vicente (2014), provided the models satisfied the Taylor-like error bounds with probability greater than or equal to .

3 Ridge function approximations

Ridge function approximations allow one to reduce the effective dimensionality of a function by determining a low-dimensional representation which is a function of a few linear combinations of the high-dimensional input. These approximations can be determined using a number of methods (Constantine 2015; Diez, Campana, and Stern 2015; Hokanson and Constantine 2017). This article will focus on two approaches: 1) derivative-free active subspaces, and 2) polynomial ridge approximation.

3.1 Active subspaces

The active subspace of a given function has been defined by Constantine, Dow, and Wang (2014) as the -dimensional subspace of the inputs which corresponds to the directions of strongest variability of . To see how one may discover , consider a probability density function which is strictly positive on the domain of interest and assume that

| (12) |

where is the identity matrix. Provided is full rank, these assumptions are easily satisfied by a change of variables (Constantine and Doostan 2017). Typically, is taken to be Gaussian for unbounded inputs , with each coordinate scaled and shifted to be of mean 0 and standard deviation 1. When is bounded below and above, is generally taken to be the uniform distribution with scaled and shifted to lie between .

Given and its partial derivatives are square integrable with respect to , the active subspace of can be found using the covariance matrix

| (13) |

In practice, this covariance matrix is approximated by

| (14) |

where are drawn randomly from . This matrix is symmetric, positive semidefinite, so its real eigendecomposition is given by

| (15) |

where and . Partitioning and as

| (16) |

results in the active subspace and the inactive subspace . The reduced coordinates and are known as the active and inactive variables, respectively. The following lemma quantifies the variation of along these coordinates.

Lemma 3.1.

The mean-squared gradients of with respect to the coordinates and satisfy

| (17) | ||||

Proof.

See the proof of Lemma 2.2 by Constantine (2015). ∎

From Lemma 3.1 it is clear that on average shows greater variability along than . Moreover, the sum of the partitioned eigenvalues and quantifies this variation. This motivates the well-known heuristic of choosing the reduced dimension as the index with the greatest log decay of eigenvalues (Constantine 2015).

In the derivative-free context, the approximate covariance matrix

| (18) |

where is a surrogate model of , may be used as a surrogate for . The efficacy of this approach is clearly dependent on the accuracy of the inferred gradients. To provide a theoretical guarantee of this statement, assume that

| (19) |

for all for some domain with independent of and

where is a surrogate model for and is some controllable parameter. Note, if is fully linear, then by definition,

implying that fully linear models inherently satisfy this assumption as , i.e. as the trust region radius shrinks. Given this assumption, the following lemma (modified from Lemma 3.11 in Constantine (2015)) provides an error bound between the approximate covariance matrix (18) and the true covariance matrix (13).

Lemma 3.2.

Assume is Lipschitz continuous with Lipschitz constant . The norm of the difference between and is bounded by

| (20) |

Proof.

See Appendix A. ∎

Provided is easily computed, one may be able to compute an analytic form for . Two model-based heuristics for approximating active subspaces using , one with a quadratic model and one a linear model, were proposed by Constantine and Doostan (2017) (see Algorithms 1 and 2). In the case of a quadratic model

| (21) |

using the assumptions on from (12), the approximate covariance matrix (18) becomes

| (22) |

The active subspace can then be approximated by partitioning the eigenvectors of by the log decay of its eigenvalues, as before. In the case of a linear model

| (23) |

the approximate covariance matrix (18) becomes

| (24) |

so the active subspace may be approximated by the 1-dimensional vector

| (25) |

These model-based heuristics have been successfully applied to a number of real-life applications. For instance, active subspaces for models of lithium ion batteries (Constantine and Doostan 2017) and turbomachinery models (Seshadri et al. 2018) have been approximated in this way. Moreover, this approach offers significant benefits over other subspace-based dimension reduction strategies. First, it is completely derivative-free. This allows it to be easily incorporated with other DFTR methods to reduce the computational overhead of surrogate modeling. Second, provided the inferred gradients satisfy the assumption (19), the error between the approximate covariance matrix (18) and the true covariance matrix (13) may be bounded using Lemma 3.2. Finally, calculating the approximate 1-dimensional subspace (25) is very inexpensive compared to other methods, requiring only samples to approximate the active subspace. However, one major limitation of this approach is that (25) can only be used to approximate a 1-dimensional active subspace. When the function of interest is not sufficiently described using a single direction, this approach may fail. Although the global quadratic covariance matrix (22) has been effectively used to calculate higher dimensional subspaces (Seshadri et al. 2018), it also requires a significant overhead in function evaluations. This limitation motivates the use of an alternative method of ridge function approximation in the case where higher dimensional subspaces are desired.

3.2 Polynomial ridge approximation

Unlike the active subspaces approach, ridge function recovery allows one to find the subspace and the coefficients (7) of a ridge function simultaneously. Hokanson and Constantine (2017) developed a method of doing this for the case in which is a polynomial of dimension and degree . Their approach was to use variable projection to solve the minimization problem

| (26) |

where denotes the set of polynomials on of degree , denotes the Grassmann manifold of -dimensional subspaces of , and is a set of samples. Writing as

(as seen in (8)), where , allows one to formulate (26) as a nonlinear least squares problem in terms of the coefficients and the subspace

| (27) |

with such that and . Using the fact that may be easily discovered using the Moore-Penrose pseudoinverse, one may write (27) as the Grassmann manifold optimization problem

| (28) |

over strictly . To solve this problem, Hokanson and Constantine (2017) developed a novel Grassmann Gauss-Newton method for iteratively solving (28).

3.3 Fully linear ridge function models

Global convergence of DFTR methods relies on models which are fully linear, i.e. models which satisfy the bounds (10). Demonstrating full linearity of ridge function models requires

| (29) | ||||

for all (4), where are constants which are independent of and . For standard polynomial interpolation models, one may use well poisedness of the interpolation set to prove full linearity (as shown in Conn, Scheinberg, and Vicente (2008)). However, in the case of polynomial ridge functions, there is an extra level of complexity involved as the models are constructed over a projected input space. Unless has an exact ridge function representation with known effective dimension, projection of its domain onto the subspace will have some inherent information loss associated with it. This is because, for each value of the reduced coordinate , there exist many (possibly infinitely many) coordinates in the full space which map to it. Variations in the function values associated with each full space coordinate may show up as ‘noise’ in the -dimensional projection of the function domain. This observation leads to two forms of error: 1) information loss from dimension reduction, and 2) response surface error which arises from polynomial interpolation with samples which are corrupted by noise.

To formalize these two forms of error, consider the conditional expectation of given .

Definition 3.3.

Let be square-integrable with respect to a probability density function , be a subspace with orthogonal columns and be an orthogonal basis for the complement of the span of the columns of . The conditional expectation of given is defined as

| (30) |

where and is the conditional density

That is, the conditional expectation of given is the average value of for all possible values for a given reduced coordinate . The function is the unique, optimal ridge function approximation in the norm for a given subspace (see the proof of Theorem 8.3 in Pinkus (2015)).

The error functions

| (31) |

represent the information loss from reducing onto the subspace . If one can appropriately bound and for all , one can show full linearity of the conditional expectation (30). Although the mean-squared error of with respect to is known to be bounded in expectation (see Theorem 3.1 by Constantine, Dow, and Wang (2014)), there exists no formal error analysis for bounding the error functions (31) for any and . However, in the special case where has no dependence on , these error bounds are satisfied. Such functions are known as -invariant. Using the following proposition proposed by Constantine (2015), full linearity of is trivially shown in the case where is -invariant.

Proposition 3.4.

Let be -invariant. Then, for any two points which lie in the domain of and satisfy ,

Proof.

See the proof of Proposition 2.3 by Constantine (2015). ∎

Unfortunately, using as a surrogate model is not practical, as it requires high-dimensional integration along the coordinate. Instead, a ridge function approximation which acts as a surrogate to is used. This introduces the error functions

| (32) |

which represent the response surface error. Although may be smooth and differentiable with respect to reduced coordinates , the -dimensional samples used to construct will be noisy as they will be obtained from the -dimensional function . Kannan and Wild (2012) provide theoretical guarantees for quadratic models constructed from noisy functions (see Theorem 2.2). Using similar logic, the following theorem provides error bounds for and .

Theorem 3.5.

Suppose is continuously differentiable, is Lipschitz continuous with Lipschitz constant in the trust region (where denotes ), and that contains at least points (including the current iterate ) which when projected onto the subspace results in a set

(where ) of affinely independent points such that the matrix

is invertible. Then, if the quadratic ridge function

interpolates at all points in such that, for any ,

the following inequalities hold for any with :

| (33) | ||||

with

| (34) |

Proof.

See Appendix B. ∎

3.4 Motivating moving ridge functions

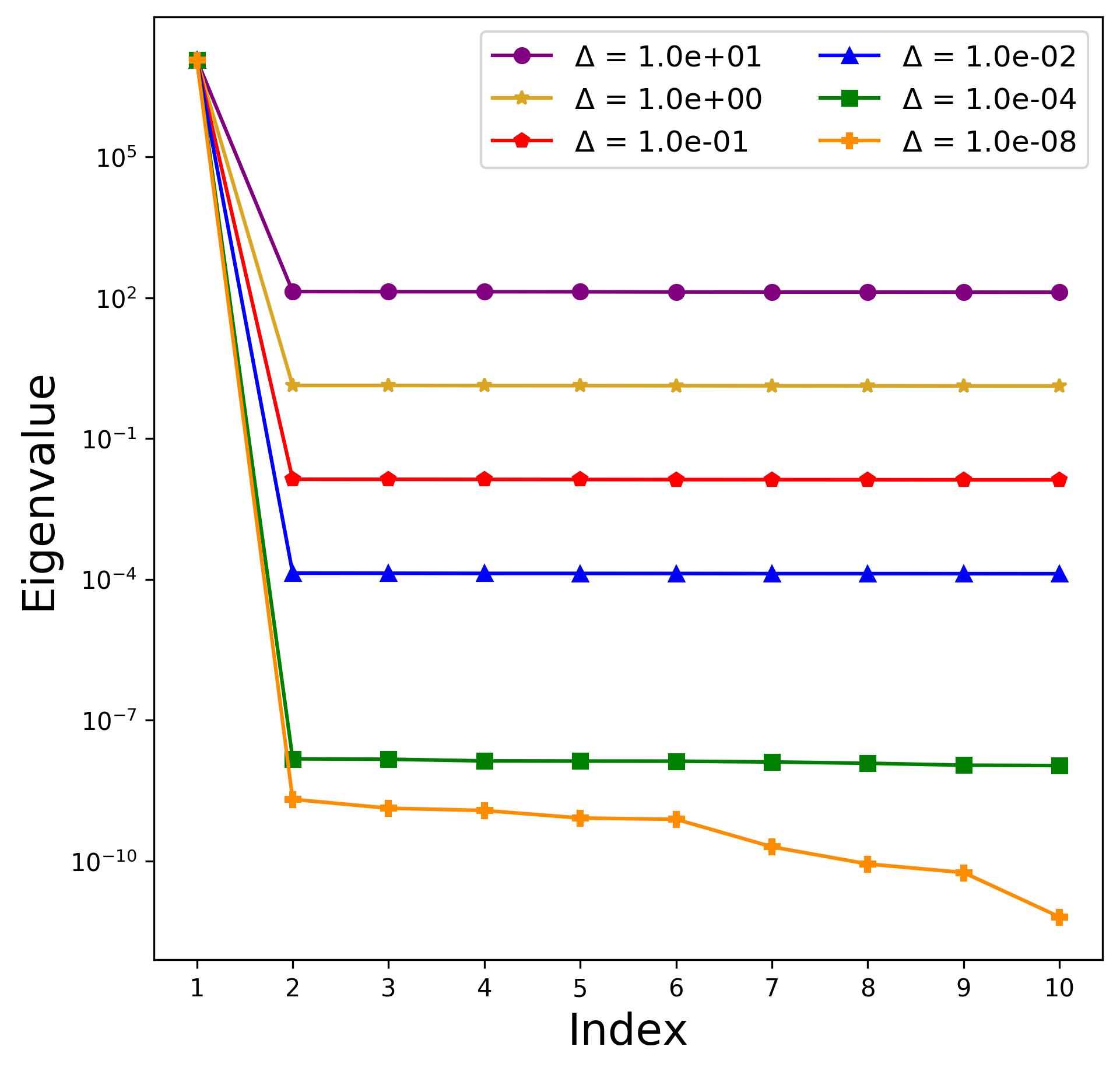

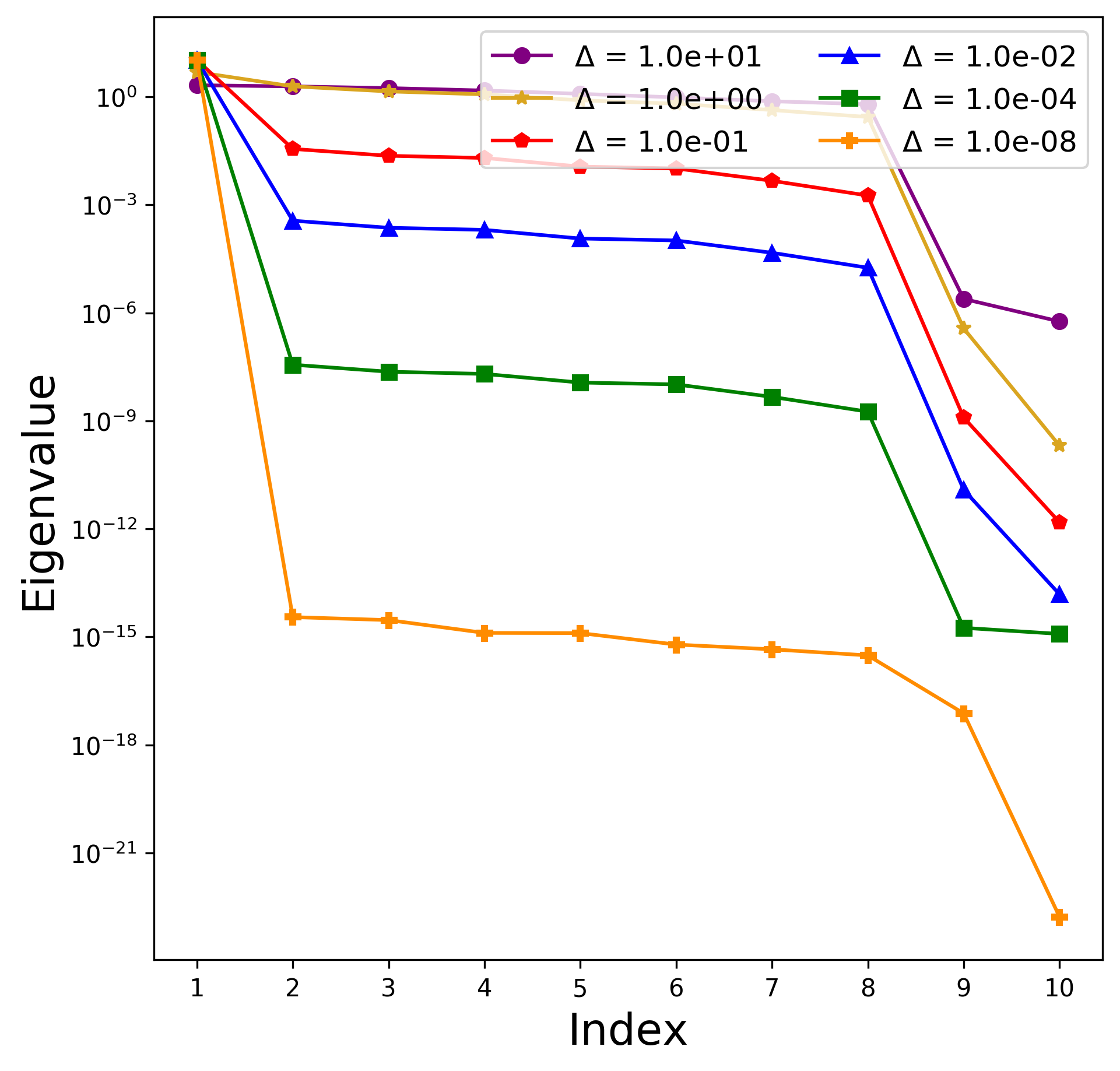

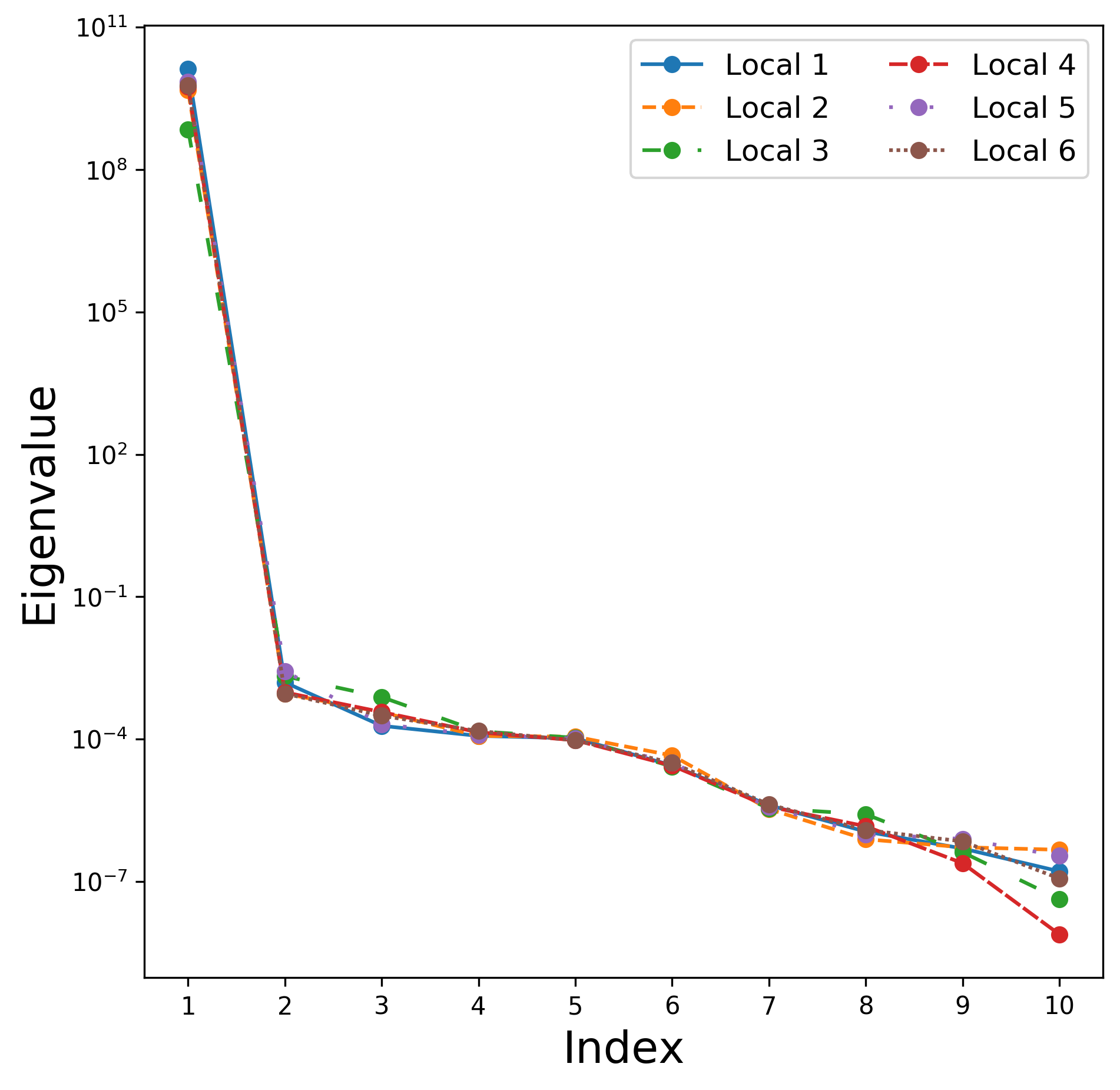

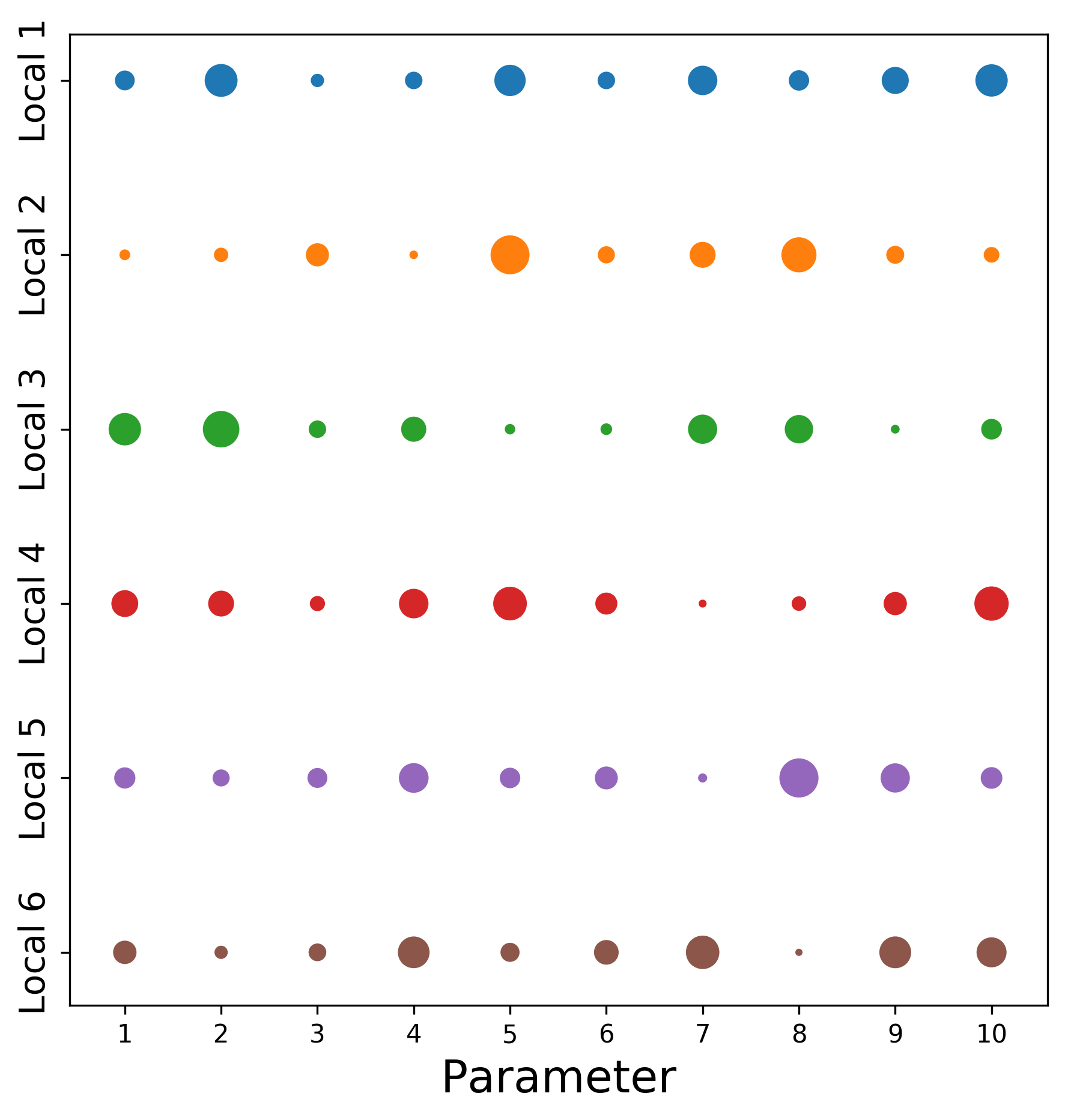

The majority of research into ridge function approximations has assumed that the function of interest varies along a global subspace (Glaws et al. 2017; Wong et al. 2019; Gross, Seshadri, and Parks 2020). Unless the function is an exact ridge function, i.e. is -invariant, this assumption may lead to a significant amount of information loss when projecting onto the subspace. However, using local subspaces , with each corresponding to a small region of interest in the function domain, may allow to be accurately modeled as a -invariant function. To motivate this approach, six 10-dimensional functions from the CUTEst (Gould, Orban, and Toint 2015) problem set have been considered (ARGLINA, MCCORMCK, NCVXBQP1, PENALTY1, SCHMVETT, VARDIM). For each of these functions, active subspaces have been approximated using the Monte-Carlo gradient sampling method (14) with 100,000 samples taken at uniformly distributed random locations. The active subspaces for six regions of interest defined by hypercubes of variable radius , all centred at the same randomly chosen location in the function domain were calculated. The eigenvalues for each of these functions are shown in Figure 1.

3

From inspection of Figure 1, it is apparent that, as decreases, the gap between the first eigenvalue and the remaining eigenvalues generally increases for these functions. This suggests that, as the region of interest becomes smaller, these functions become inherently 1-dimensional. Moreover, for many of these functions the remaining eigenvalues seem to tend to zero as decreases. By Lemma 3.1, this implies very little to no average variability along the inactive variables , meaning these functions can be treated as nearly -invariant for small . Note, there clearly exist functions which seemingly do not have eigenvalues which tend to zero. For instance, although VARDIM has seemingly very strong 1-dimensional structure at this particular location in the function domain, the remaining eigenvalues are still . This suggests that at this particular region of the domain, although VARDIM has strong 1-dimensional structure, this structure does not get more prominent as the size of function domain decreases.

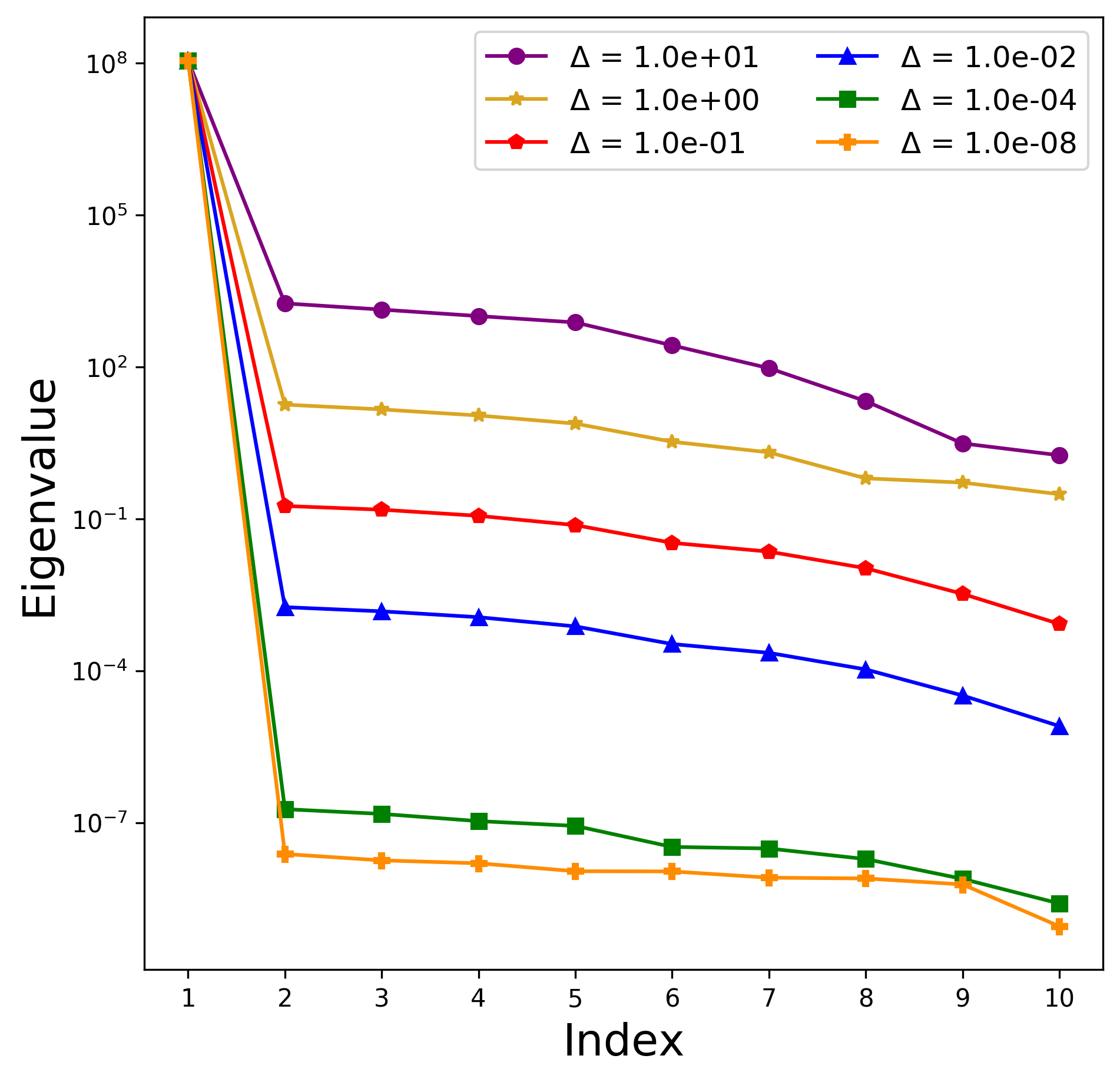

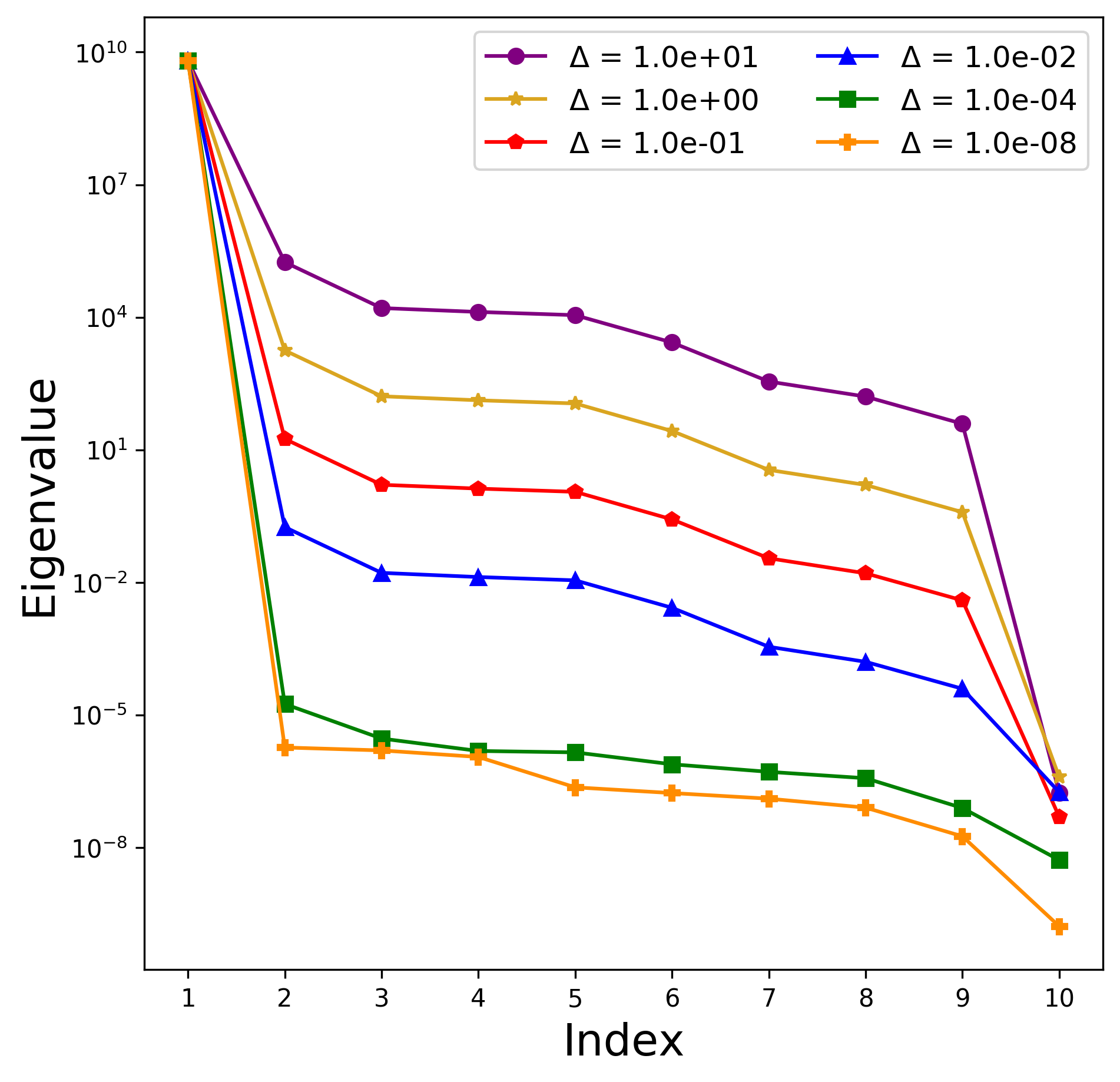

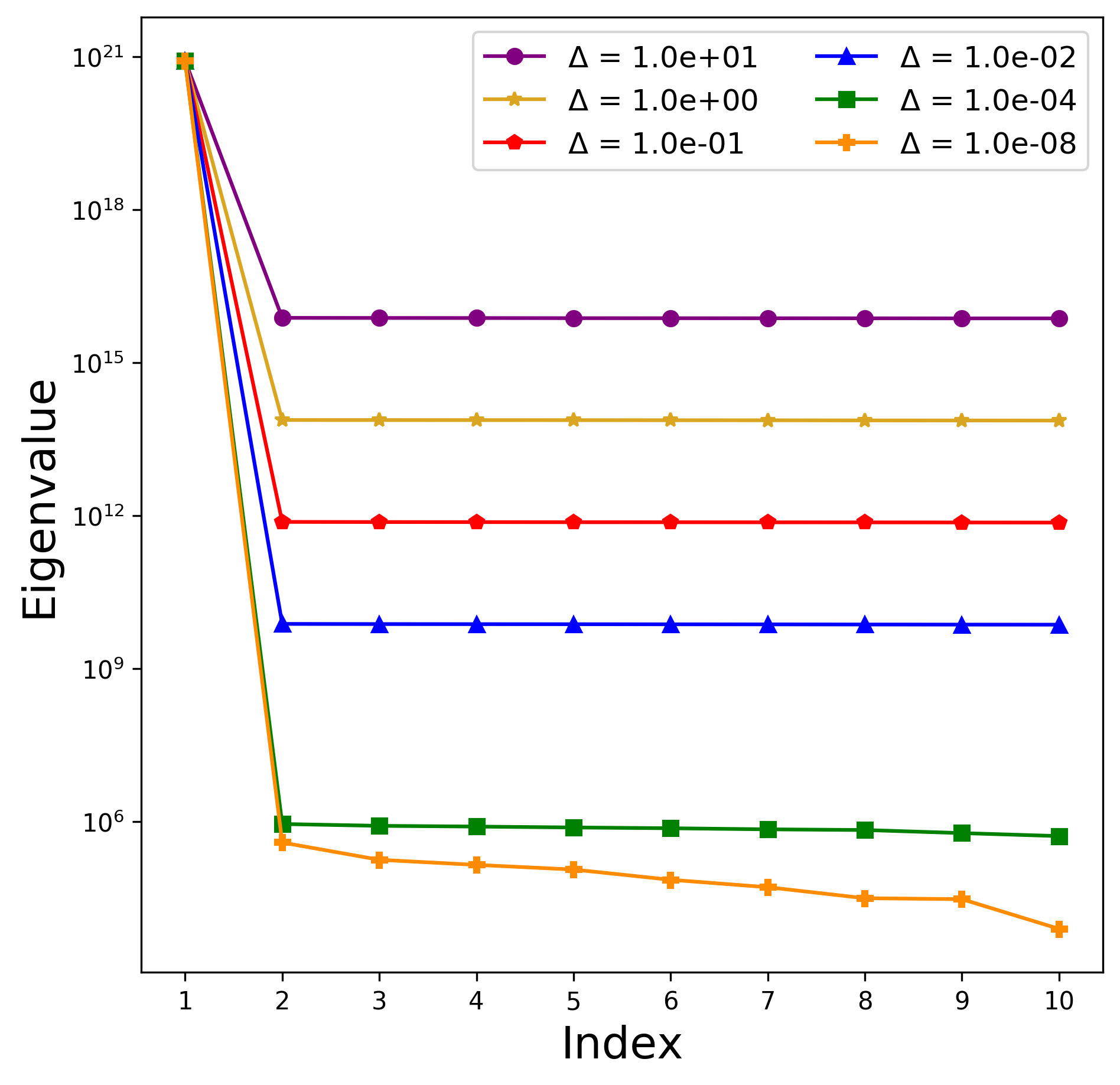

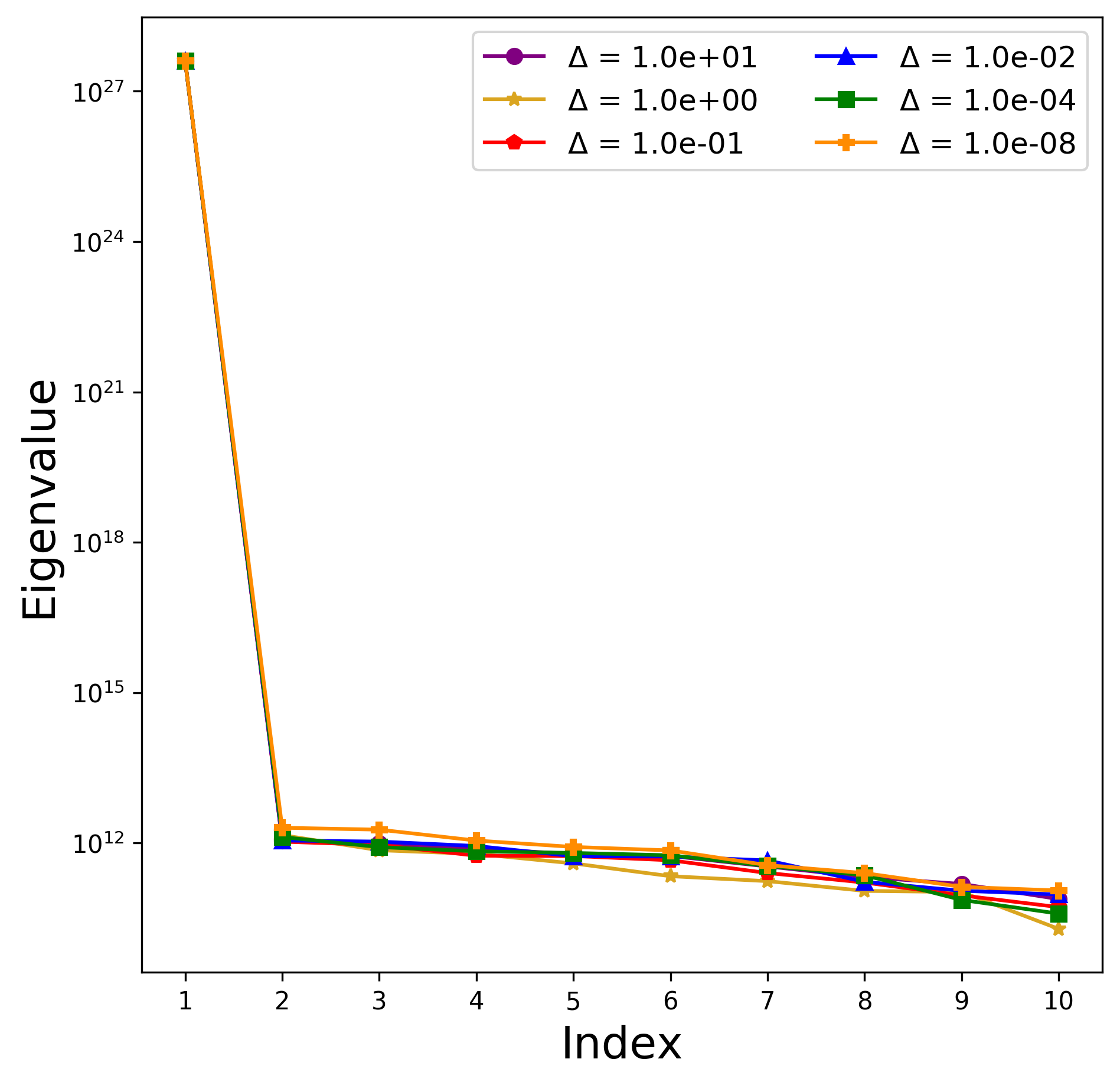

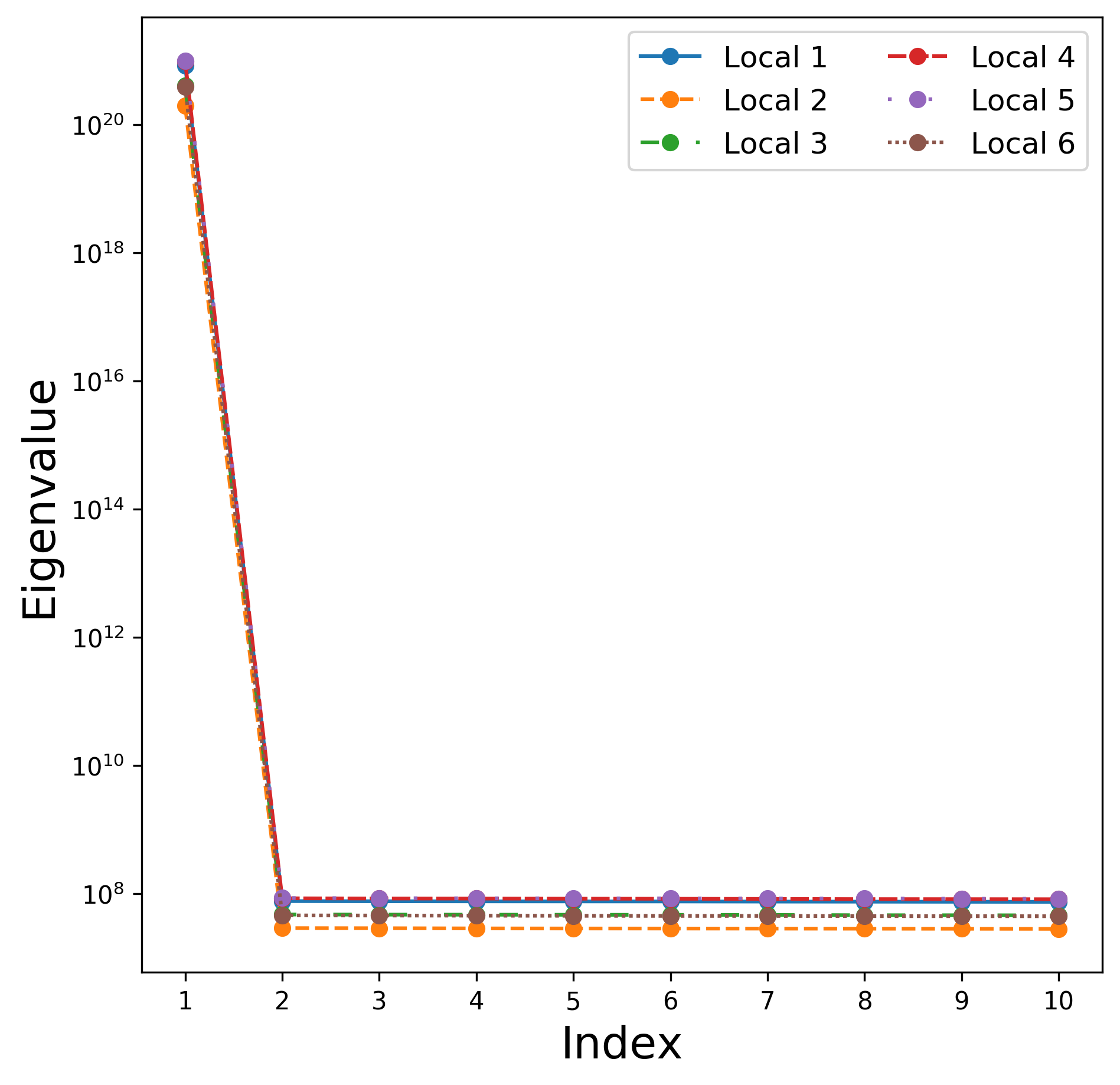

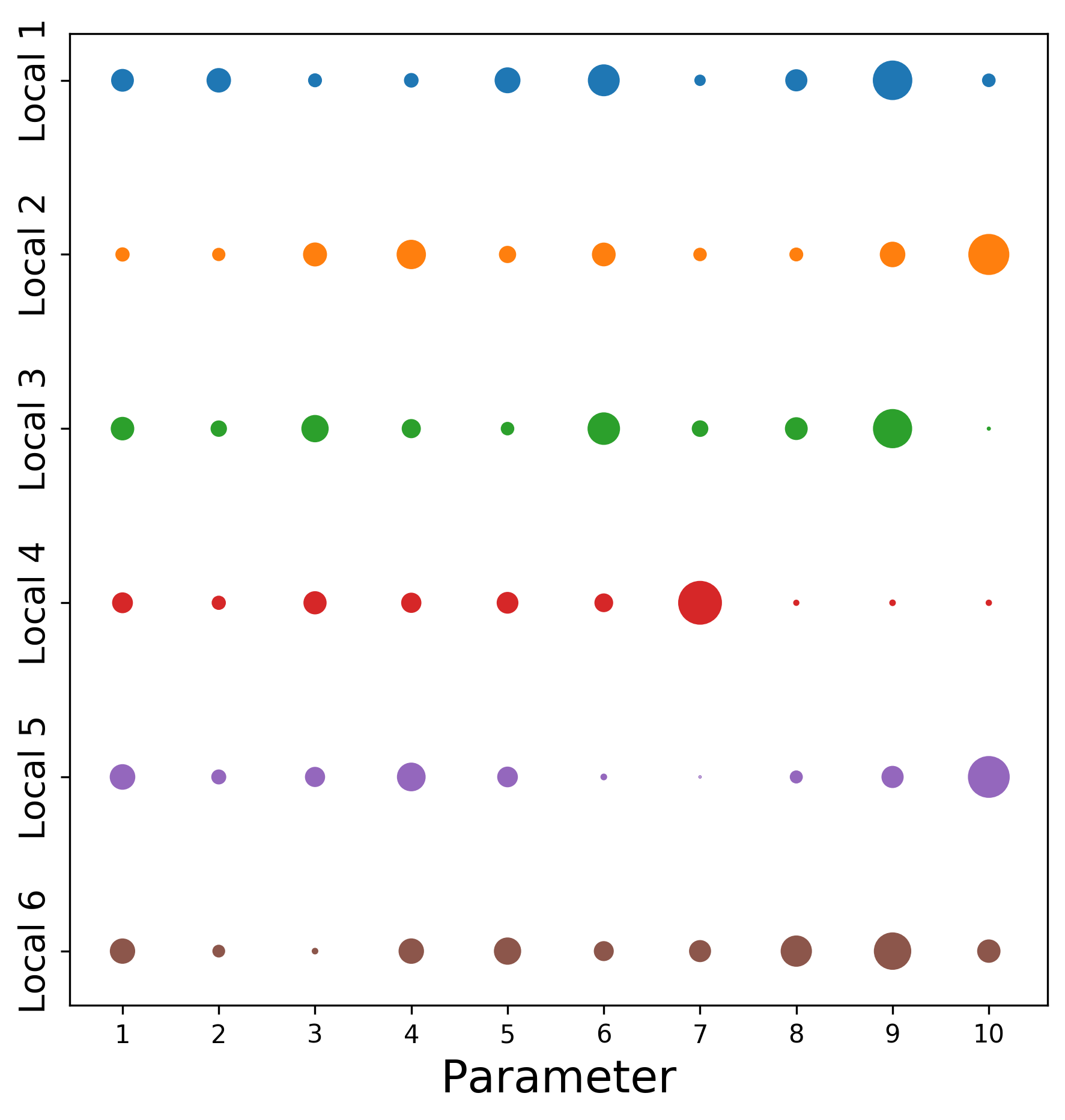

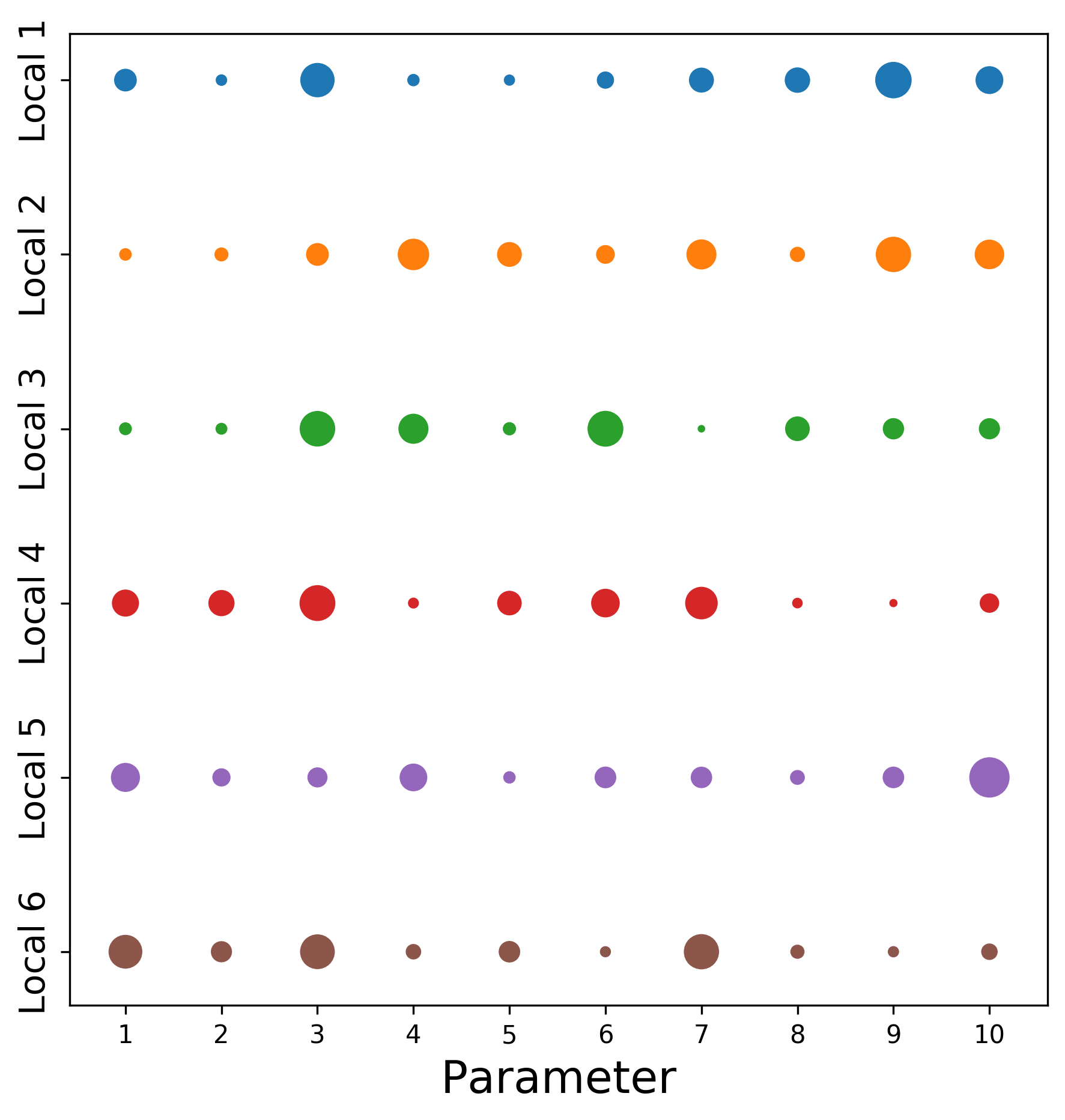

In order to use dimension-reducing subspaces in a DFTR algorithm, it is hypothesized that the subspaces should be periodically updated as one moves through the function domain. To motivate this hypothesis, local active subspaces for six regions have been defined by hypercubes of radius for each function. The centroids of the hypercubes were chosen using Latin hypercube sampling such that each local region was sufficiently distant from the others. The eigenvalues of these subspaces are shown in Figure 2.

3

For each of these functions, one can see a significant log decay in the eigenvalues after the first index for all of the local subspaces. This suggests that, for each of these regions of interest, the direction defined by the first eigenvector of (14) captures a significant amount of the variation of the function. Note, the observation that, in small regions of interest, multivariate functions can be approximated by 1-dimensional ridge functions is not surprising. In particular, the first-order Taylor expansion

| (35) |

can be considered a 1-dimensional ridge function with the subspace . However, this observation clearly breaks down when considering subspaces of higher dimension. Nevertheless, using subspaces of higher dimension may still be advantageous for some problems, as will be seen later.

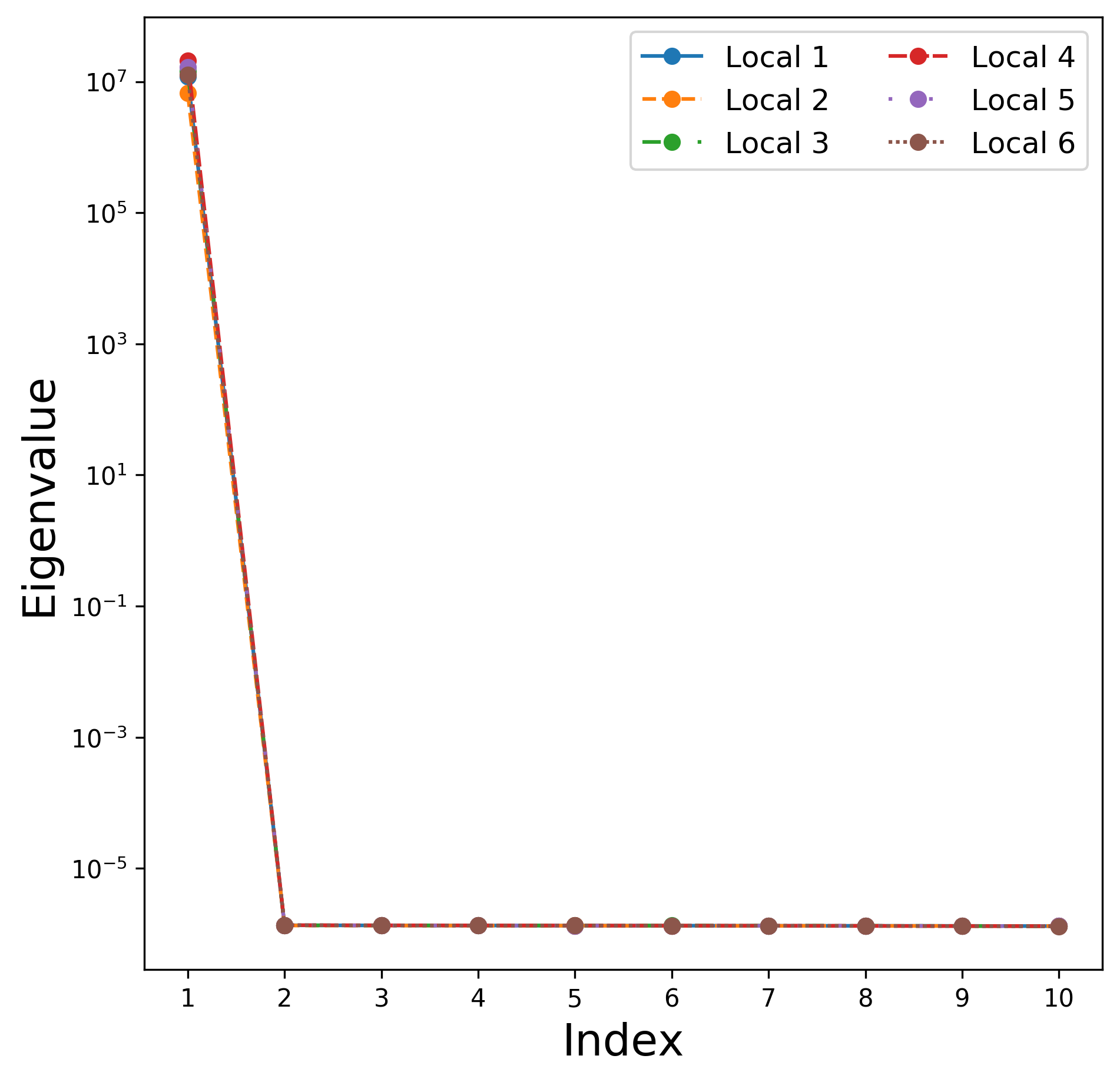

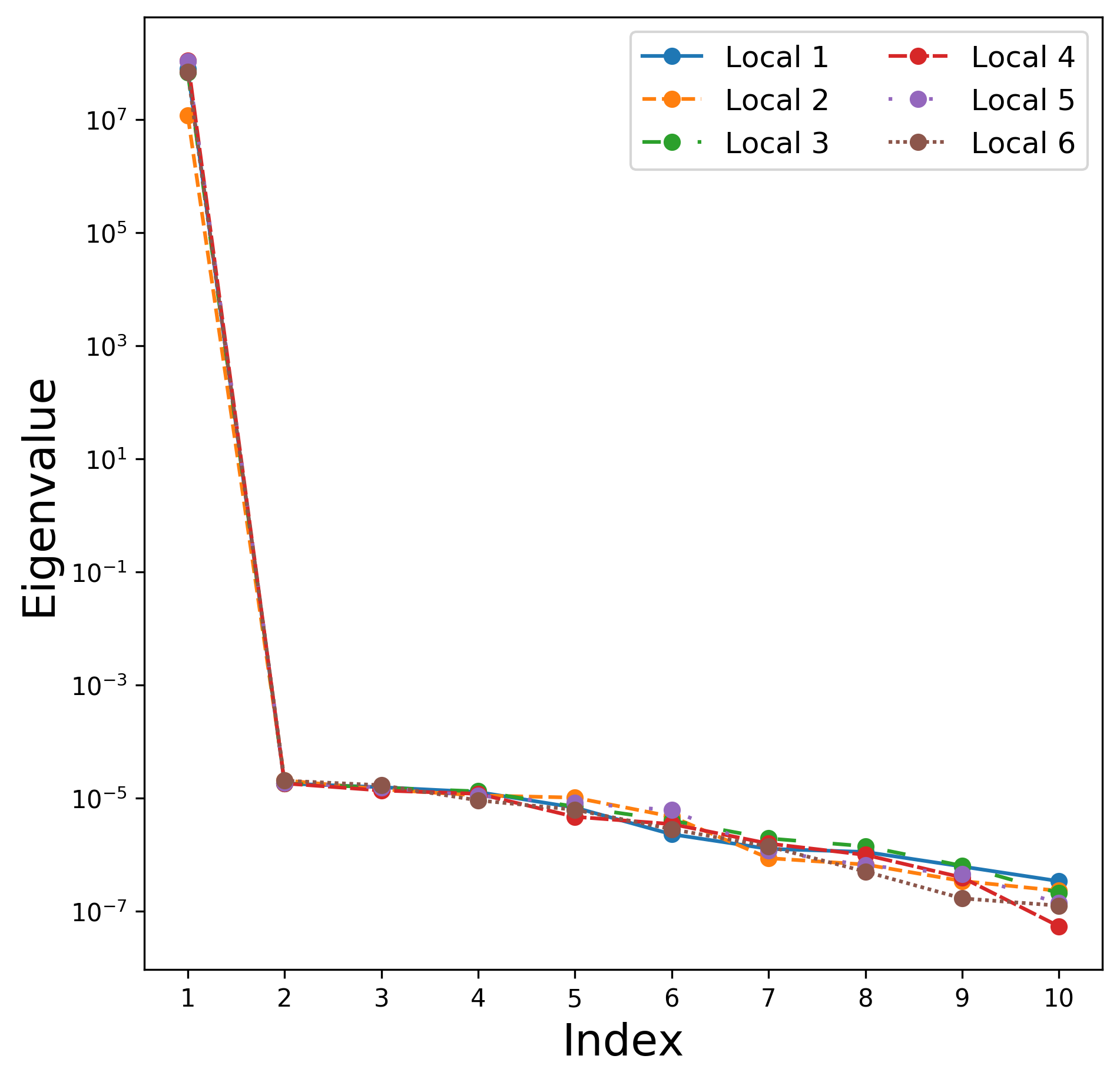

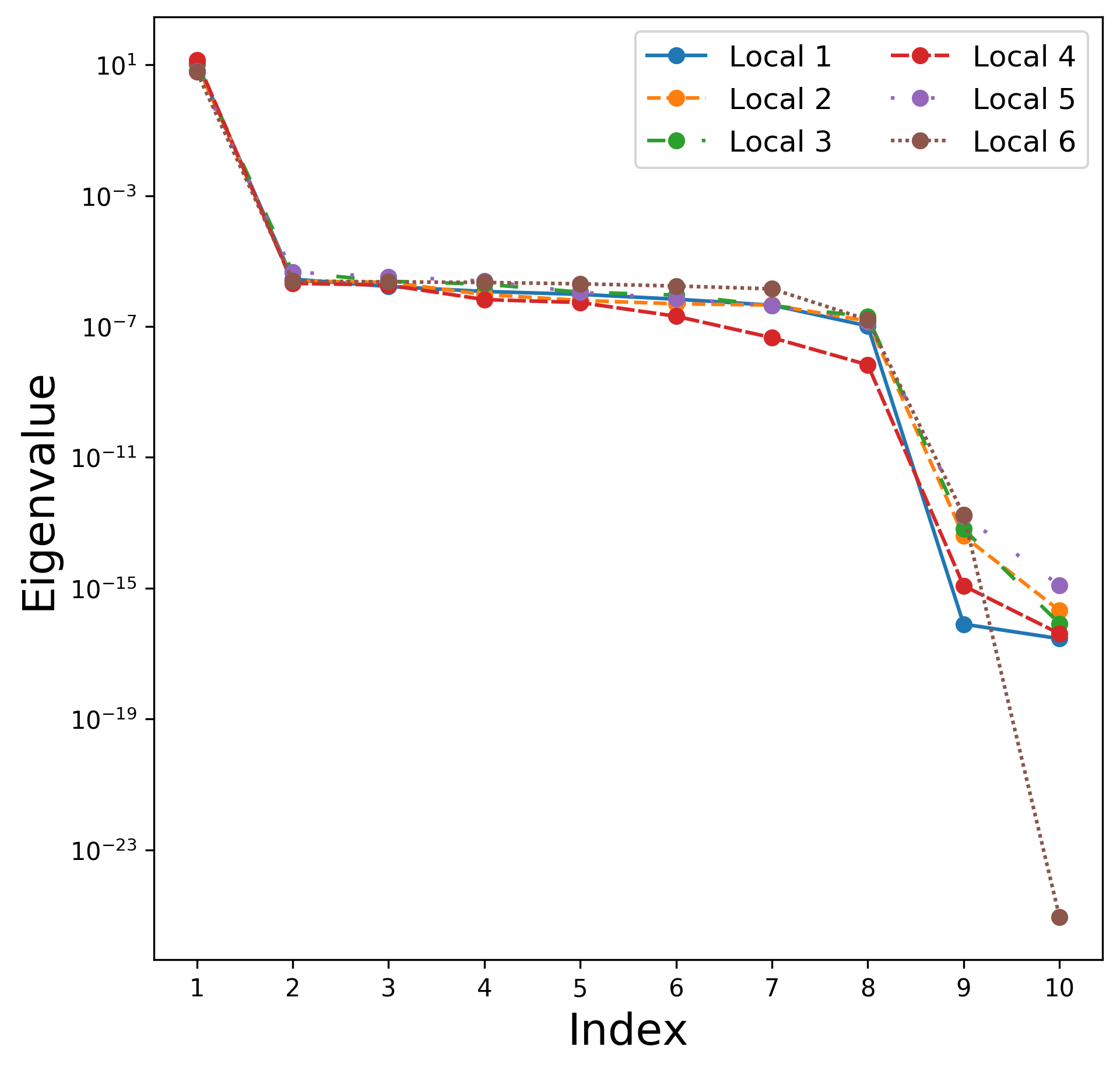

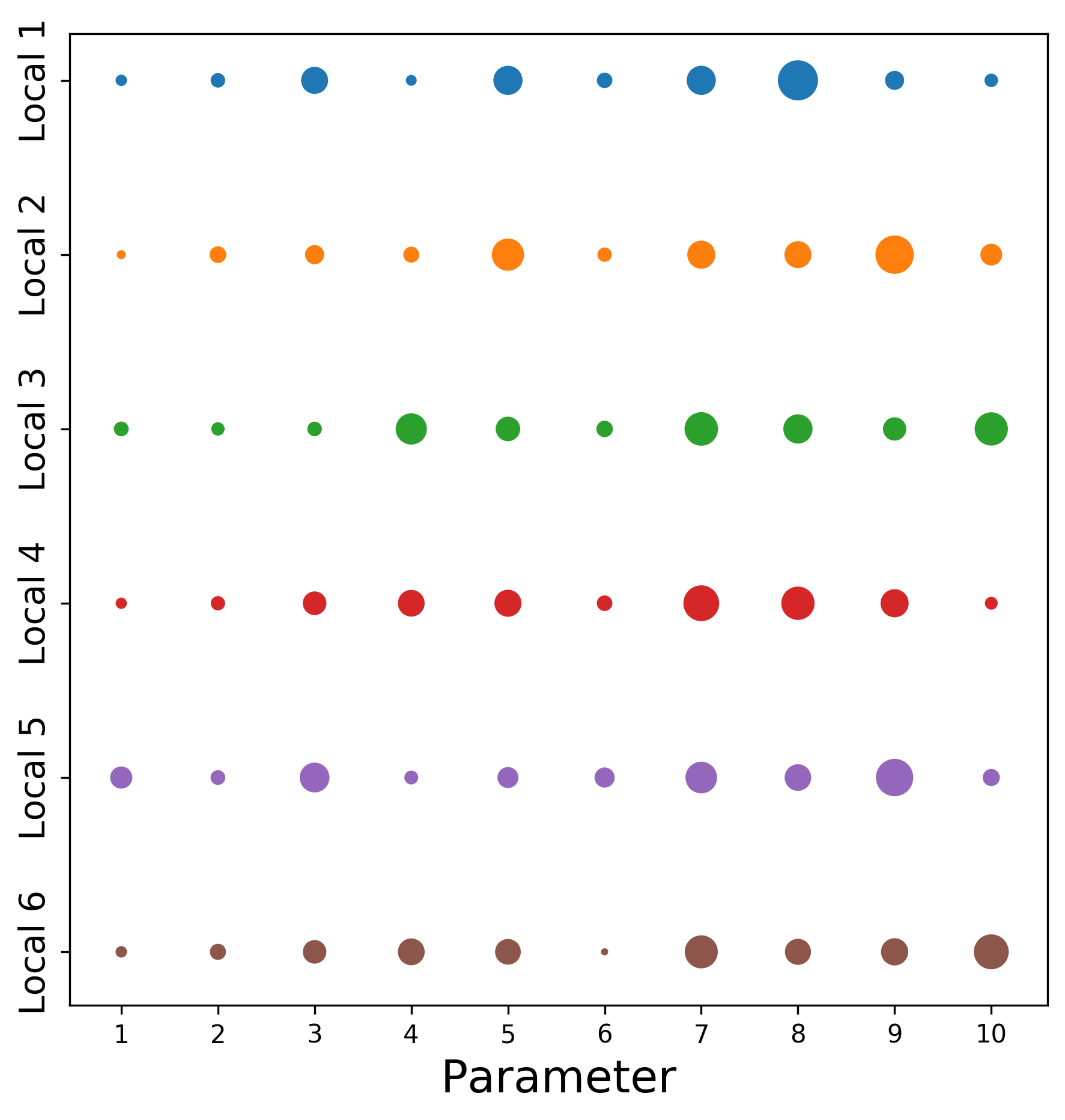

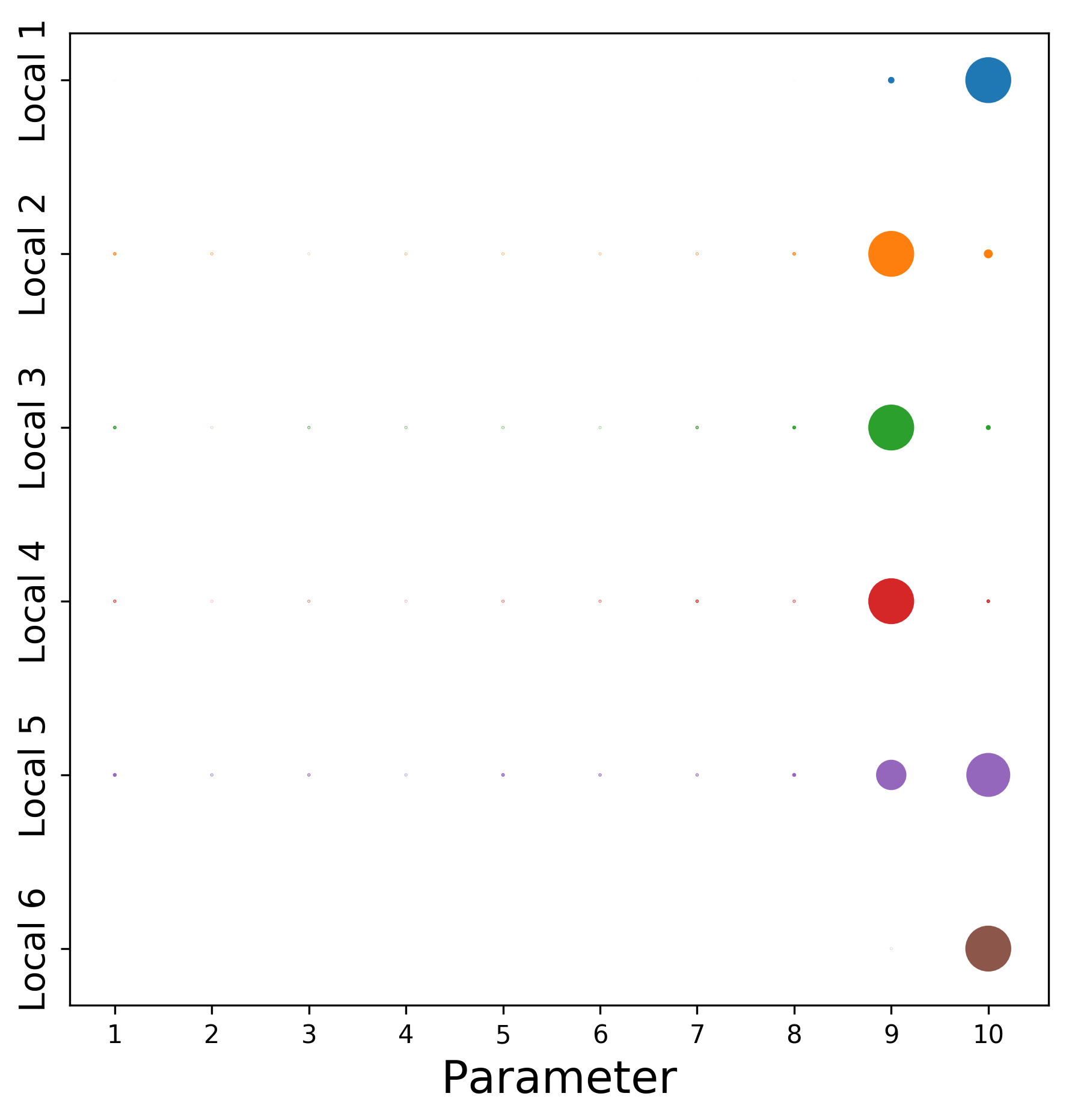

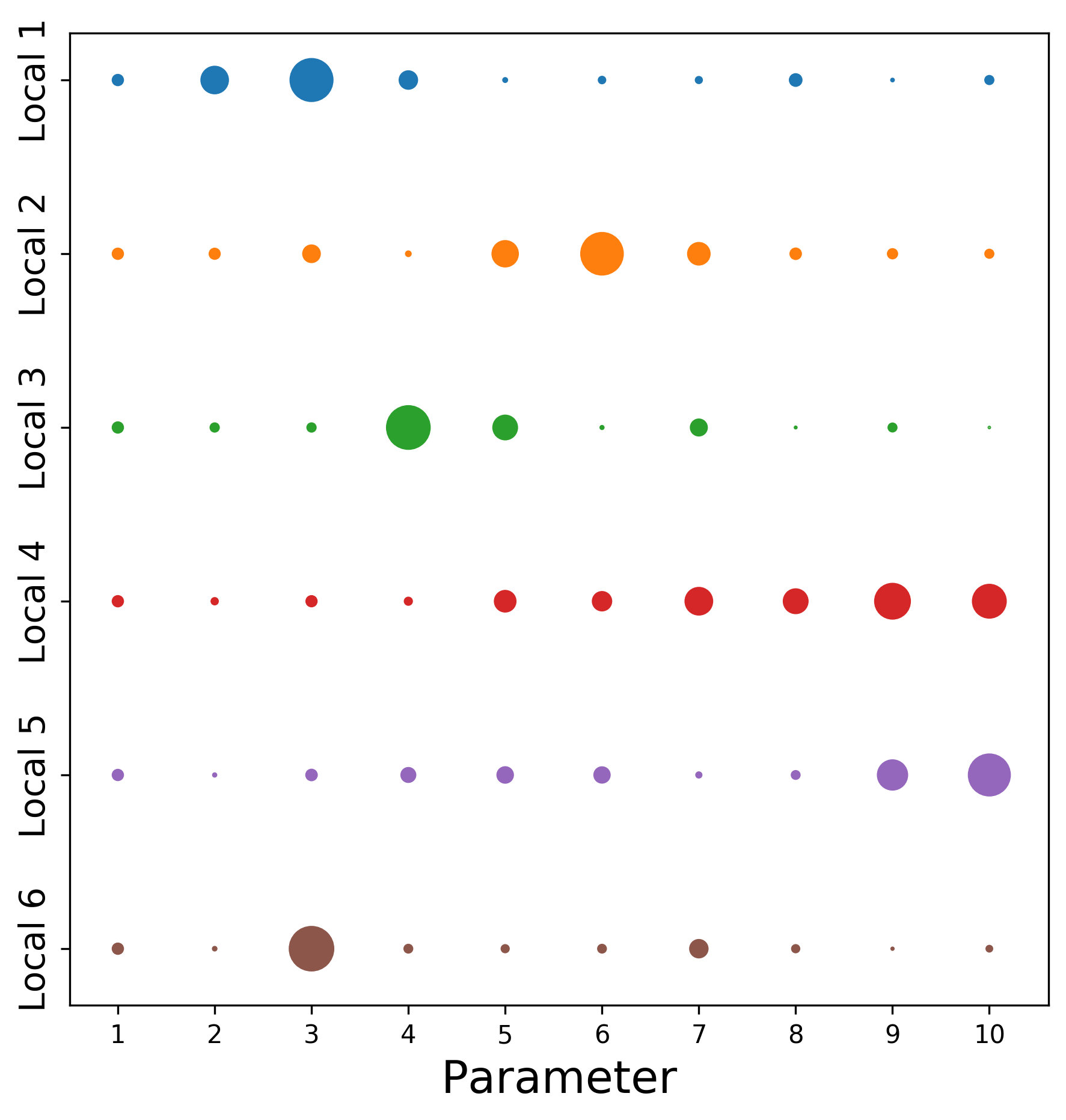

The weights from each of these 1-dimensional subspaces are shown in Figure 3, with the size of the markers indicating the relative size of the weights. Not surprisingly, the weight vectors generally vary significantly between each region of interest. Clearly, it would be nearly impossible to accurately describe these functions with constant subspaces, as there are regions which have a weight vector which is linearly independent of the weight vectors associated with other regions of the function domain. Interestingly, some functions seem to have multiple regions of the function domain which can be defined using a single subspace. For instance, it looks to be possible to define these six regions of interest for the SCHMVETT function by 3 low-dimensional subspaces, one using strictly the 9th parameter, another using the 10th parameter, and one with a mixture of the two. This observation may motivate the use of subspace clustering techniques (Parsons, Haque, and Liu 2004) in further studies.

3

4 OMoRF algorithm

The OMoRF algorithm is detailed in Algorithm 1. At each iteration, a local subspace is determined and a quadratic ridge function is constructed. To ensure the accuracy of this model, two separate interpolation sets are maintained: the set is used to construct the local subspace , while is used to determine the coefficients of the interpolation model . Next, the trust region subproblem

| (36) |

is solved to obtain a candidate solution . The ratio

| (37) |

is used to determine whether or not this candidate solution is accepted and if the trust region radius is decreased. Before decreasing the trust region, checks on the quality of and are performed, and if necessary, their geometries are improved by calculating new sample points.

Remark 1.

An open source Python implementation of OMoRF is available for public use from the Effective Quadratures package (Seshadri and Parks 2017).

Remark 2.

Remark 3.

Just as in UOBYQA, NEWUOA and BOBYQA, two trust region radii and are maintained. However, unlike those algorithms, is not explicitly used to detach control of the sampling region from . Rather, is used as a lower bound when decreasing , preventing the trust region from shrinking too quickly before the model is sufficiently ‘good’. This is the same approach as used in other similar algorithms (Cartis et al. 2019; Cartis and Roberts 2019).

Remark 4.

Convergence of many DFTR algorithms is generally dependent on a so-called criticality step (Conn, Scheinberg, and Vicente 2009a). During this step, the accuracy of the model is ensured whenever its gradient is sufficiently small. In Algorithm 1, this has been replaced by a safety step (Lines 9–11), as is done in Powell’s algorithms. During this safety step, a check is performed on the step to ensure it is sufficiently large before evaluating the candidate solution . If it is not, then the accuracy of is improved. This check can be seen as an analogue of the criticality step, as discussed in Conn, Scheinberg, and Vicente (2009b) (see Section 11.3).

4.1 Interpolation set management

In Section 3.3, it was shown that the accuracy of a ridge function model is dependent on two sources of error: information loss by projecting onto a subspace and the response surface error of . Ideally, a single interpolation set could be maintained which could be improved to reduce both sources of error. Unfortunately, such an approach would require a priori knowledge of the subspace . Therefore, OMoRF maintains two separate interpolation sets: of samples for calculating , and of samples for calculating the coefficients of .

The set is used to construct the subspace using either derivative-free active subspaces or polynomial ridge approximation. In either case, the first step is to build a fully linear -dimensional linear interpolator (23). In the case of derivative-free active subspaces, is simply the 1-dimensional active subspace (25). If a greater dimensionality is required, is used to solve the Grassmann manifold optimization problem (28). Note, solving (28) requires an initial guess for . In OMoRF, the approximate 1-dimensional subspace (25), appended with its orthogonal complement, is used as the initial point for the manifold optimization problem (28). Note, although the solution to problem (28) could also be used in the case of , it was found that the 1-dimensional active subspace (25) generally gave superior algorithmic performance. Therefore, this method is only employed in the case where higher dimensions are desired, e.g. when it is believed that a 1-dimensional subspace insufficiently describes the underlying problem dimension.

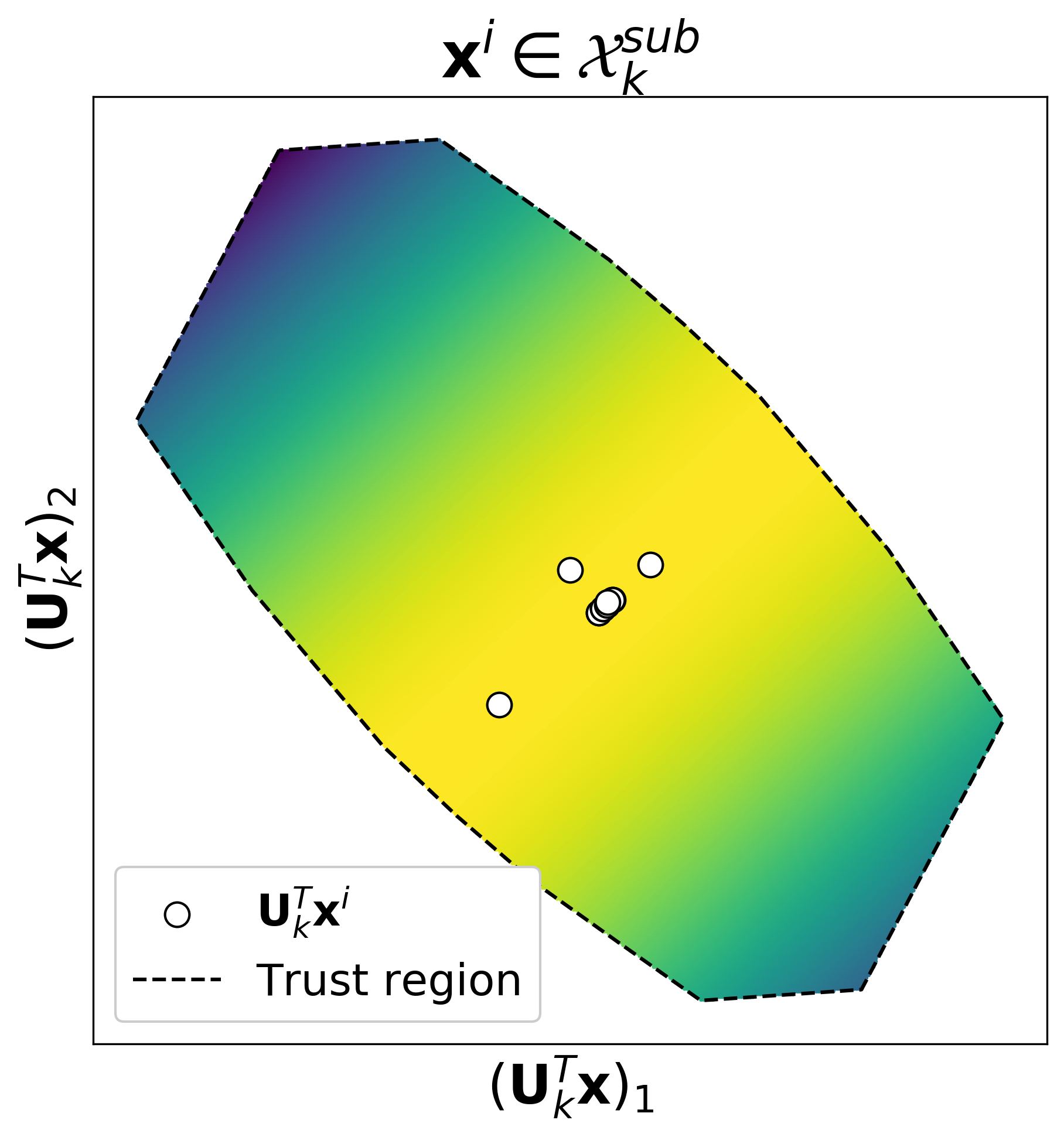

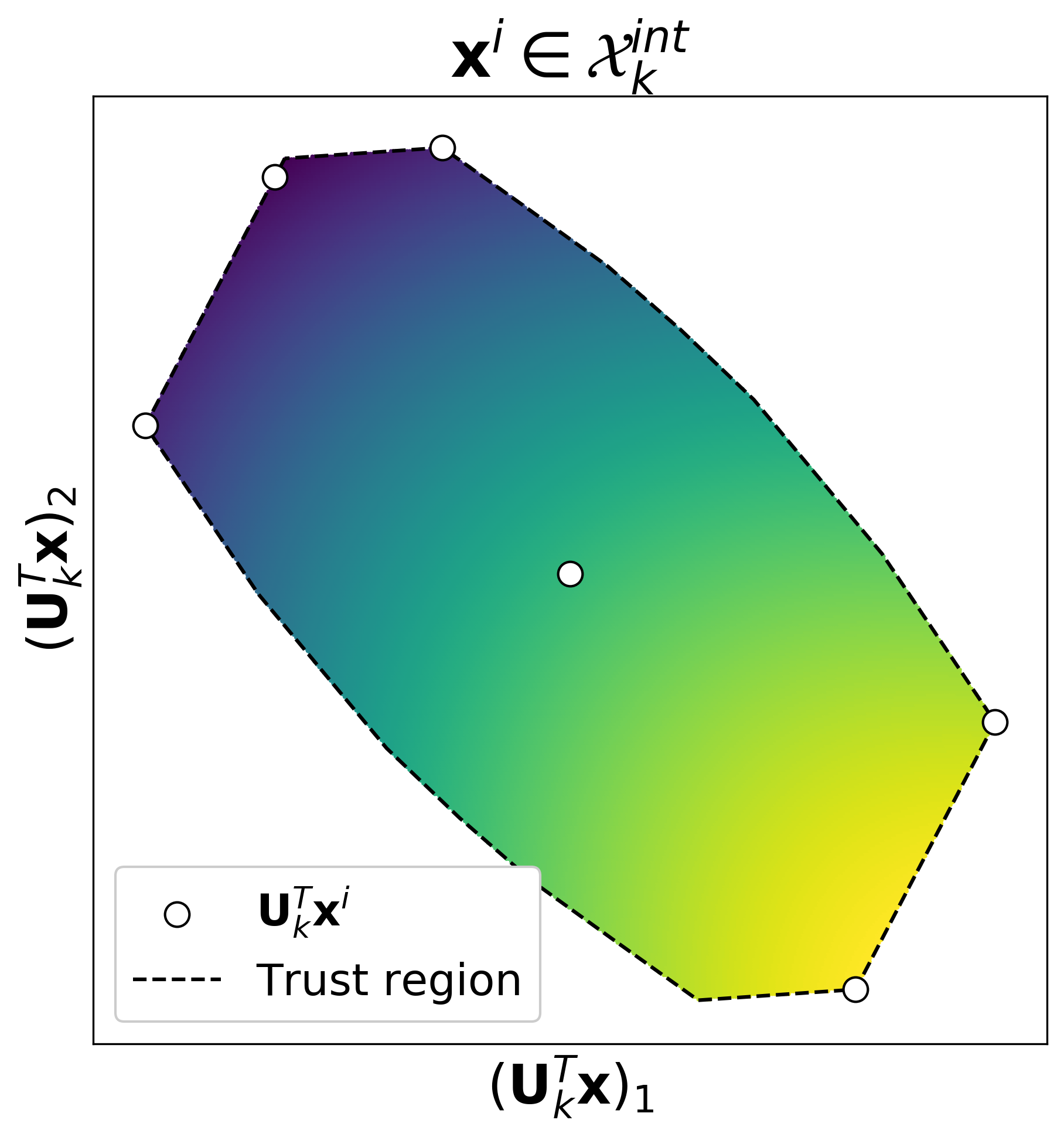

Once the subspace is known, one may be tempted to use the points to calculate the coefficients of . However, these projected samples generally insufficiently span the -dimensional projected space, leading to poor surrogate models. Provided , determining a more suitable set of samples is not only relatively cheap, but can also dramatically improve the quality of the ridge function surrogate. Figure 4 provides an example of the 10-dimensional Styblinski-Tang function

| (39) |

projected onto a 2-dimensional subspace. From this figure it is clear that, although the set may be well suited for linear interpolation in 10 dimensions, the projected set does not span the 2-dimensional space very well. In contrast, the projected set effectively spans this space, which in turn gives a much more accurate ridge function model. To demonstrate this increase in accuracy, samples were drawn at random from a uniform distribution bounded by the trust region domain. From these samples, the coefficient of determination

| (40) |

where

and , was calculated for both of these models. The values for the ridge function models constructed from and can be seen in Figure 4.

1

4.2 Interpolation set updates

Algorithm 1 always includes new sample points as they become available by appending to the interpolation sets and . When the iterate is successful, i.e. , Algorithm 3 is invoked for both sample sets to choose a point to be replaced for each set before continuing the iteration. Note, new sample points are not calculated during this call of Algorithm 3. When the iterate is not successful, it is necessary to ensure the accuracy of the model before reducing the trust region radius . In this case, not only is the previously calculated sample added, but another new geometry-improving point is determined and subsequently added. Determining whether or not these sets need to be improved is done by checking the maximum distance of the samples to the current iterate. If this distance is too large, it indicates the interpolation set has not been updated recently, so it may need improvement. The full details of this process are provided in Algorithm 2.

There are a few points to note about Algorithm 2. First, although other conditions may be used as a measure of the quality of an interpolation set, the maximum distance of the samples to the current iterate gives a quick and simple means of determining whether or not to improve the interpolation set. Similar approaches have been successfully applied in other DFTR methods (Fasano, Morales, and Nocedal 2009; Bandeira, Scheinberg, and Vicente 2012; Cartis and Roberts 2019). Second, a pivotal algorithm, which has been modified from Algorithm 6.6 in Conn, Scheinberg, and Vicente (2009b), has been used both to choose points to be replaced and calculate new geometry-improving points. The details of this modified algorithm are given in Algorithm 3 in Appendix C. Third, to reduce the computational burden of each iteration, only a single geometry-improving sample point is calculated during calls of Algorithm 3. The point which is replaced by this new sample point is also determined using Algorithm 3. Fourth, improvements to are prioritized over . This is because generally has significantly fewer samples than , so can be updated more rapidly than . If all of the points in are sufficiently close to the current iterate , this indicates that has been recently improved. In these cases, if the model needs improving, it may be because the subspace needs to be updated. Finally, a new subspace is calculated whenever the geometry of is improved. This is because improving the geometry of improves the quality of the linear interpolator (23), which, by Lemma 3.2, leads to a more accurate covariance matrix (18). Therefore, improving before calculating potentially allows the algorithm to find a more suitable dimension-reducing subspace.

4.3 Choice of norm and extending for bound constraints

Unlike most trust region algorithms, the infinity norm is used in this implementation of OMoRF. Although the more common choice of the Euclidean norm would also be suitable, this choice was made in order to simplify the extension of OMoRF to the bound-constrained optimization problem

| (41) |

To see how this choice simplifies matters, note that is equivalent to

where is an -dimensional vector of ones multiplied by . The feasible region at iteration is then simply the intersection of

To simplify, one may write this feasible region as , where

for .

In the case of a Euclidean norm trust region, the feasible region is the intersection of

The shape of this region does not lend itself to a simple formulation, so working with the Euclidean norm may be more cumbersome in the case of bound-constrained optimization problems. Note, some methods, such as BOBYQA (Powell 2009), handle the awkward shape of the feasible region by projecting the step obtained from a Euclidean trust region onto the hyperrectangle.

5 Numerical results

The performance of OMoRF has been tested against three well-known DFO algorithms: COBYLA, BOBYQA, and Nelder-Mead (Nelder and Mead 1965). The Effective Quadratures (Seshadri and Parks 2017) implementation was used for OMoRF, SciPy (Virtanen et al. 2020) was used for COBYLA, Py-BOBYQA (Cartis et al. 2019) was used for BOBYQA, and NLopt (Johnson 2018) was used for Nelder-Mead. For BOBYQA, two variants, one with the minimum of interpolation points and another with the default of , were tested. All of the tested algorithms were provided the same initial starting point and arbitrarily chosen characteristic length . In the case of unconstrained problems, a value of was used, while was used for bound-constrained problems. To force the solvers to use all of the available computational budget, the convergence criterion was set to a value of such that it was generally not reached. For OMoRF, the following parameter values were used: , , , , , , , , , and .

5.1 Testing methodology

Performance and data profiles (Moré and Wild 2009) have been used for comparing these algorithms on many of the following test problems. These profiles are defined in terms of three characteristics: the set of test problems , the set of algorithms tested , and a convergence test . Given the convergence test, a problem and a solver , the number of function evaluations necessary to pass the convergence test was used as a performance metric . Moreover, the convergence test

| (42) |

where is some tolerance, is the starting point, and is the minimum attained value of for all solvers within a given computational budget for problem , was used.

The performance profile is defined as

| (43) |

In other words, is the proportion of problems in in which solver attains a performance ratio of at most . In particular, is the proportion of problems for which the solver performs the best for that particular convergence criterion , and as , represents the proportion of problems which can be solved within the computational budget. Data profiles are defined as

| (44) |

where is the dimension of problem . This represents the proportion of problems that can be solved — measured by convergence criterion — by a solver within function evaluations (or simplex gradients).

5.2 CUTEst problems

The CUTEst (Gould, Orban, and Toint 2015) test problem set was used to examine solver performance. From the set of unconstrained and bound-constrained optimization problems, two subsets were defined: 1) 40 problems of moderate dimension (), and 2) 40 problems of high dimension (). A full list of these problems may be found in Appendix D. The focus of this article is on derivative-free optimization of computationally intensive functions where a strict computational budget may limit the number of function evaluations available to a solver. In order to simulate such an environment, a computational budget of simplex gradients (i.e. function evaluations) was specified. These solvers were tested with a low accuracy requirement of and a high accuracy requirement of . In these studies, two comparisons are made. Initially, four variants of OMoRF, with , are compared. From this comparison, the best of these solvers is chosen for comparison with the other solvers. In this second comparison, the best solution per problem from the first comparison is retained, even if the solver has been eliminated. This approach has been taken in order to avoid performance profile crowding (see Gould and Scott (2016)). Note, to further reduce the crowding effect, the results from BOBYQA with points have been omitted from the plots below. This is because this solver was generally significantly inferior to BOBYQA with points.

5.2.1 Moderate dimension problems

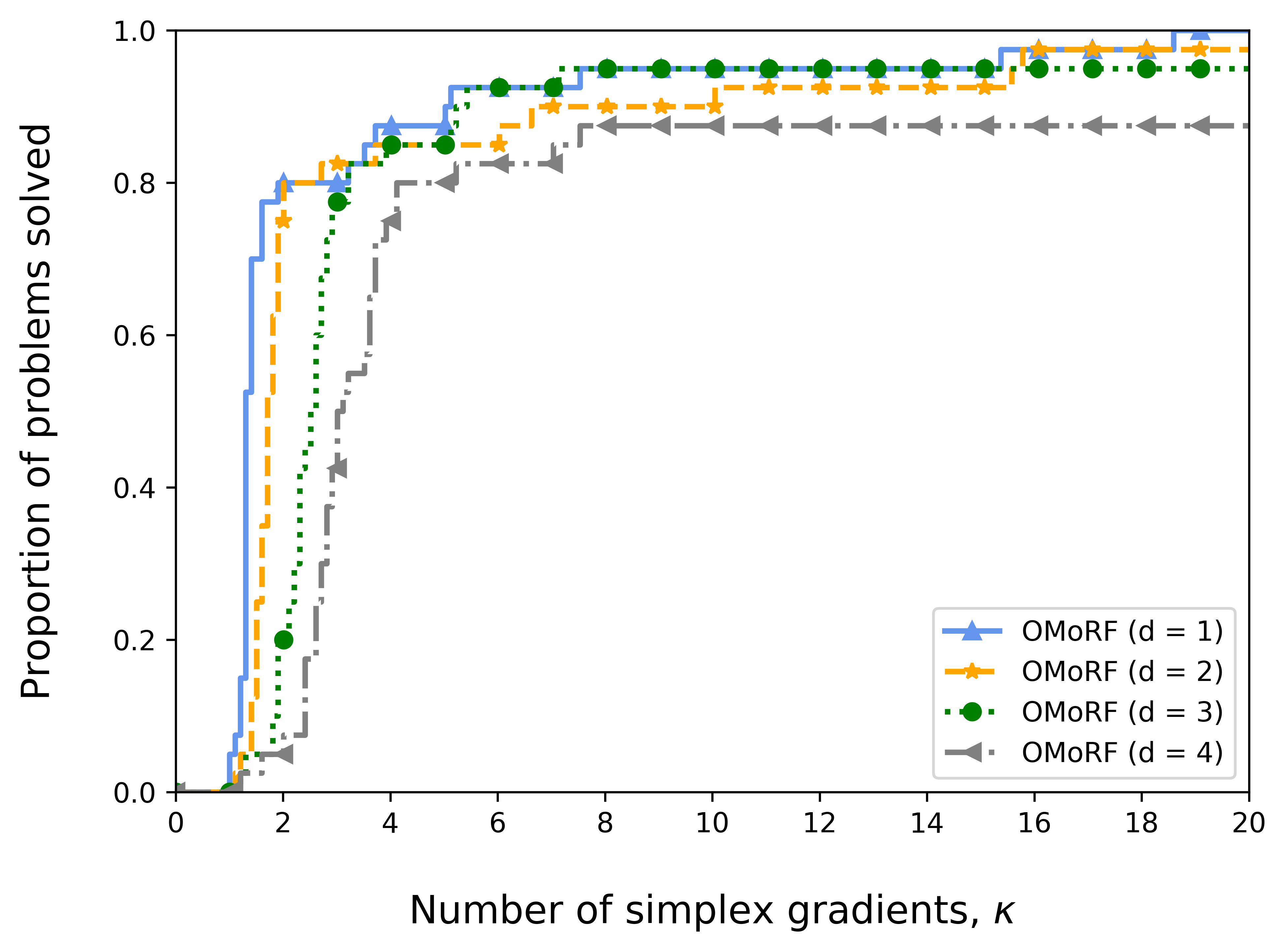

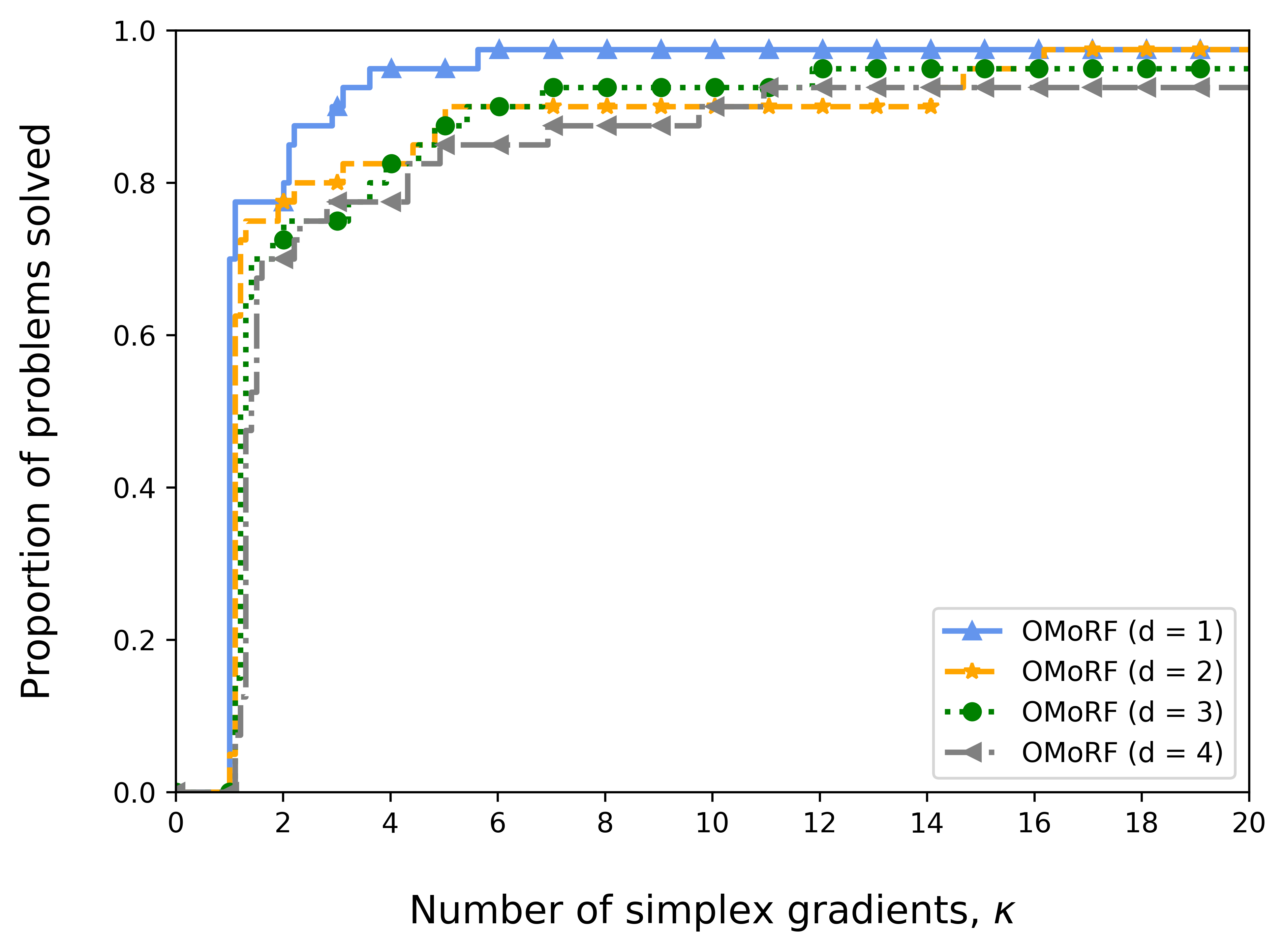

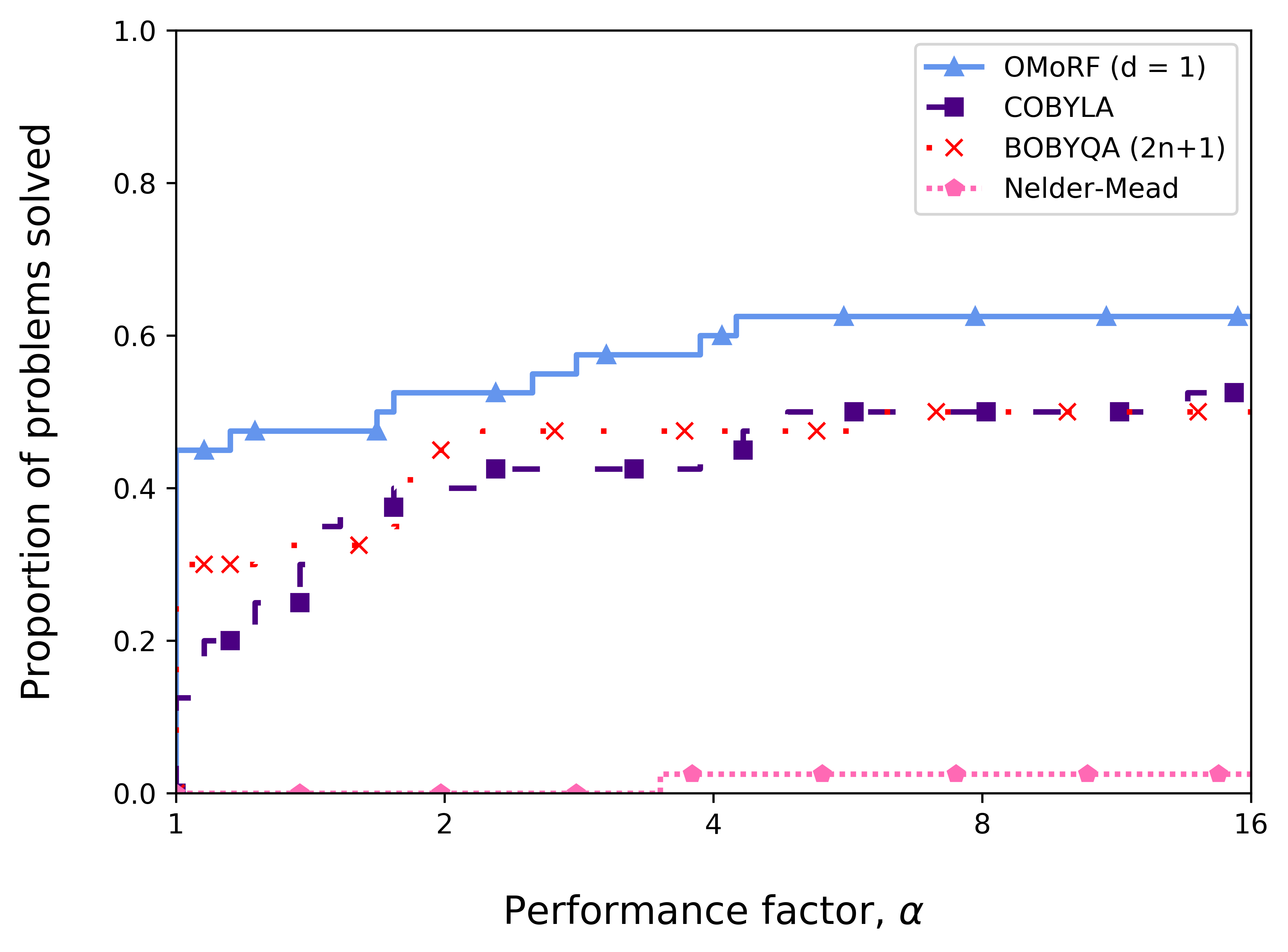

The data and performance profiles for all tested variants of OMoRF for the test set of moderate dimension problems are shown in Figure 5. It is clear that OMoRF significantly outperformed the other solvers. In fact, for the low accuracy requirement cases, this variant of OMoRF was the best solver for more than 90% of the test problems. Although this dropped to 80% in the high accuracy requirement, this was still significantly better than the other solvers. The solver with the next best performance, OMoRF , was the quickest solver to reach convergence for only around 10% of the problems for both the low and high accuracy requirements. Furthermore, it is clear that, for problems of moderate dimension, increasing can have a negative effect on the algorithmic performance. This is because, given a subspace , the number of points required to construct a quadratic ridge function is . If is not significantly less than , this requirement can be prohibitive. For example, when , 15 samples are required to approximate the coefficients of , provided the subspace is known. This means that if , 26 points (11 points to construct ) will be required to construct . In comparison, only 14 points are required when .

2

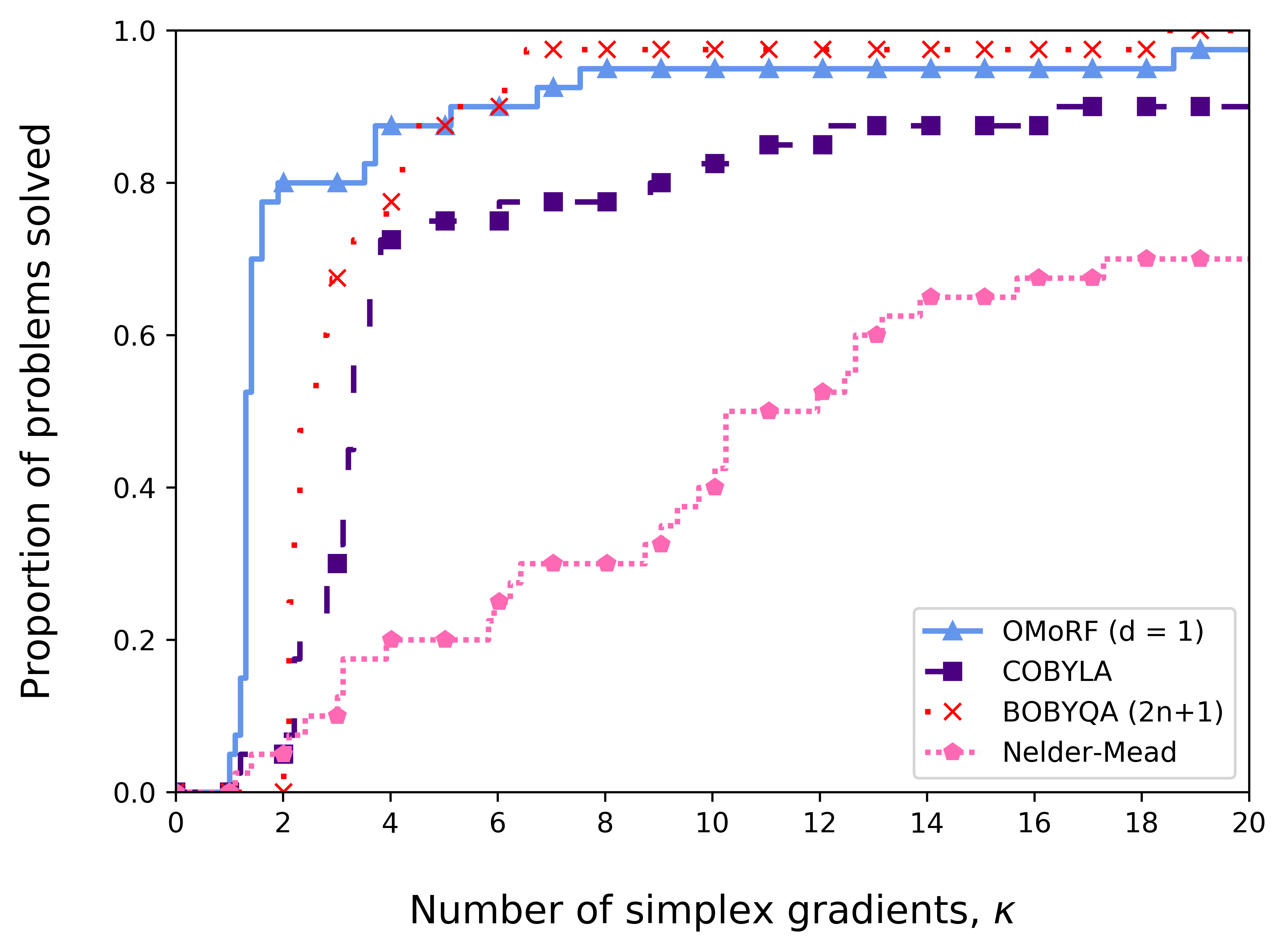

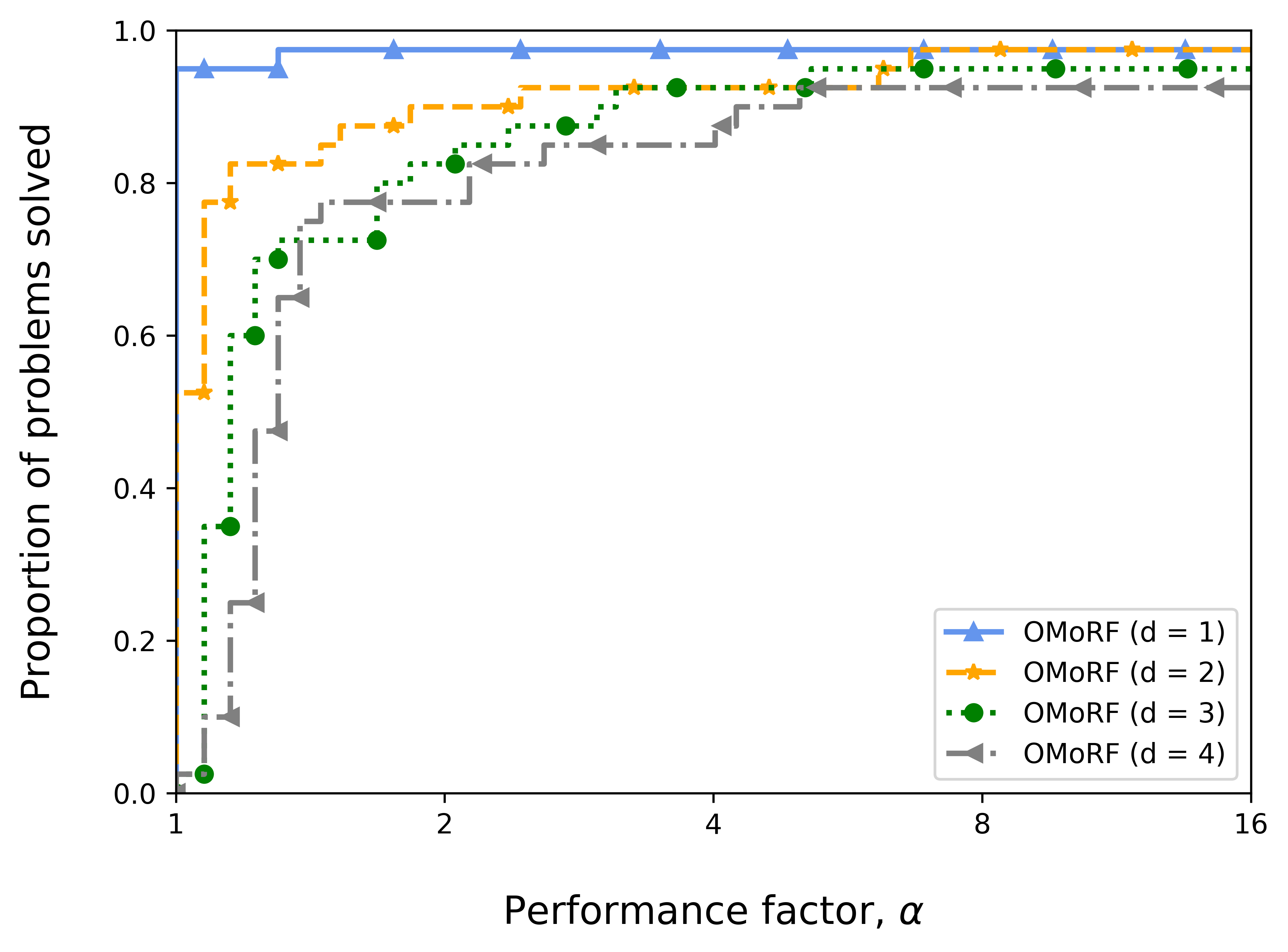

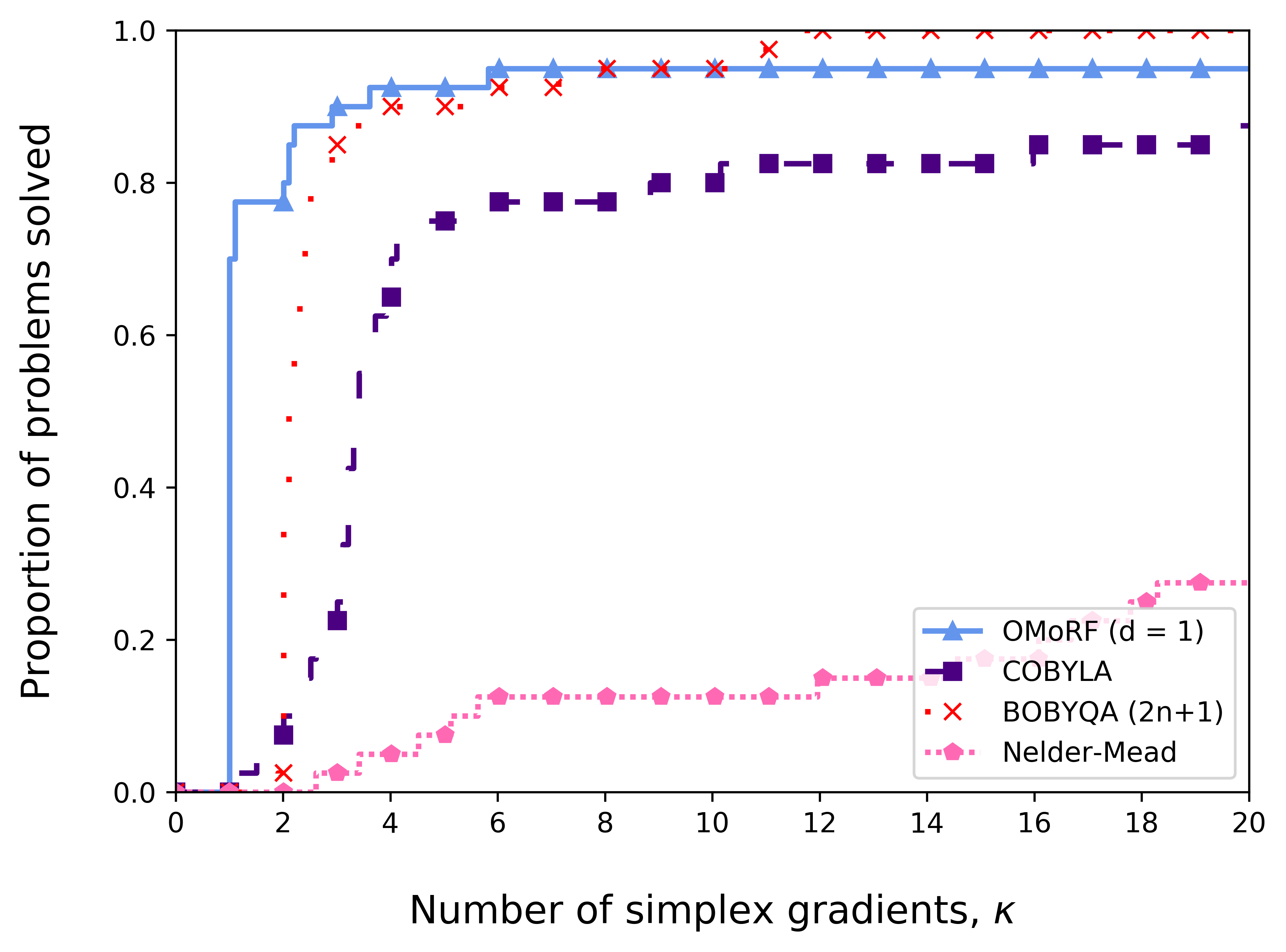

Due to the clear advantages in performance, OMoRF has been used for comparison with the other solvers. The data and performance profiles for OMoRF , COBYLA, BOBYQA and Nelder-Mead for the test set of moderate dimension problems are shown in Figure 6. As previously mentioned, the data and performance profiles shown in Figure 6 used the minimum attained value from all solvers. On the other hand, Figure 5 only included the minimum attained value from the four variants of OMoRF. This explains the relative decrease in performance for OMoRF in Figure 6. Nevertheless, for the problems in this test set, OMoRF was generally the quickest solver to achieve convergence at both the low and high accuracy requirement. From the performance profile, one can see that it was the first solver to converge for over 80% of the problems for the low accuracy requirement and nearly 40% for the high accuracy requirement. Additionally, OMoRF was able to make much quicker initial progress than the other methods, as demonstrated in the data profiles. In the case of the low accuracy requirement, nearly 80% of the problems could be solved to convergence within 2 simplex gradients, compared to 5% for COBYLA and 0% for BOBYQA. This quick convergence is likely due to its ability to model functions with low-dimensional quadratics, allowing it to capture function curvature with significantly fewer samples. However, one point to note is that, as the number of function evaluations increased, BOBYQA was able to solve a larger proportion of the problems at the low accuracy requirement. This suggests that BOBYQA may be a slightly superior general-purpose solver when seeking low accuracy solutions.

2

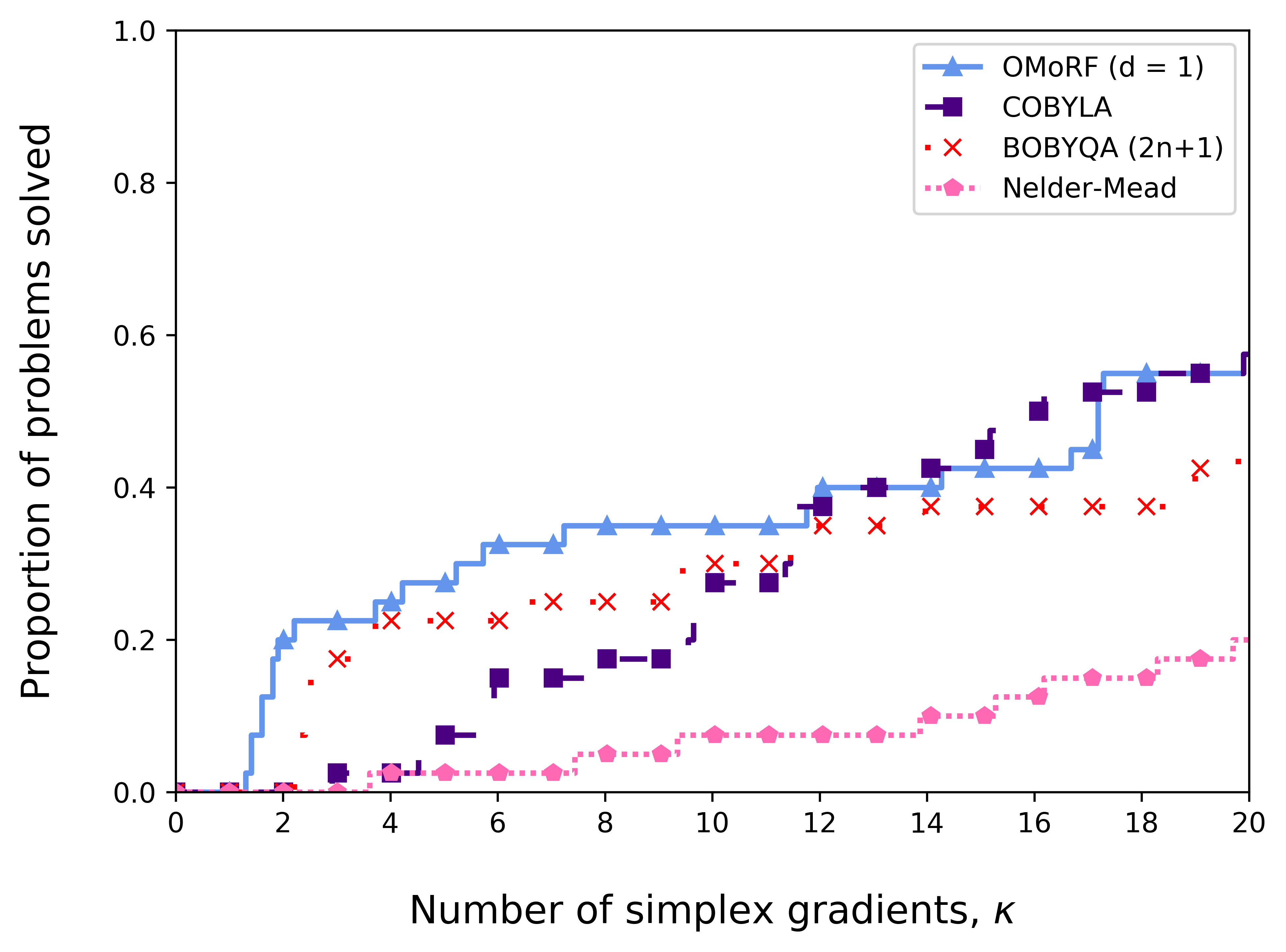

5.2.2 High dimension problems

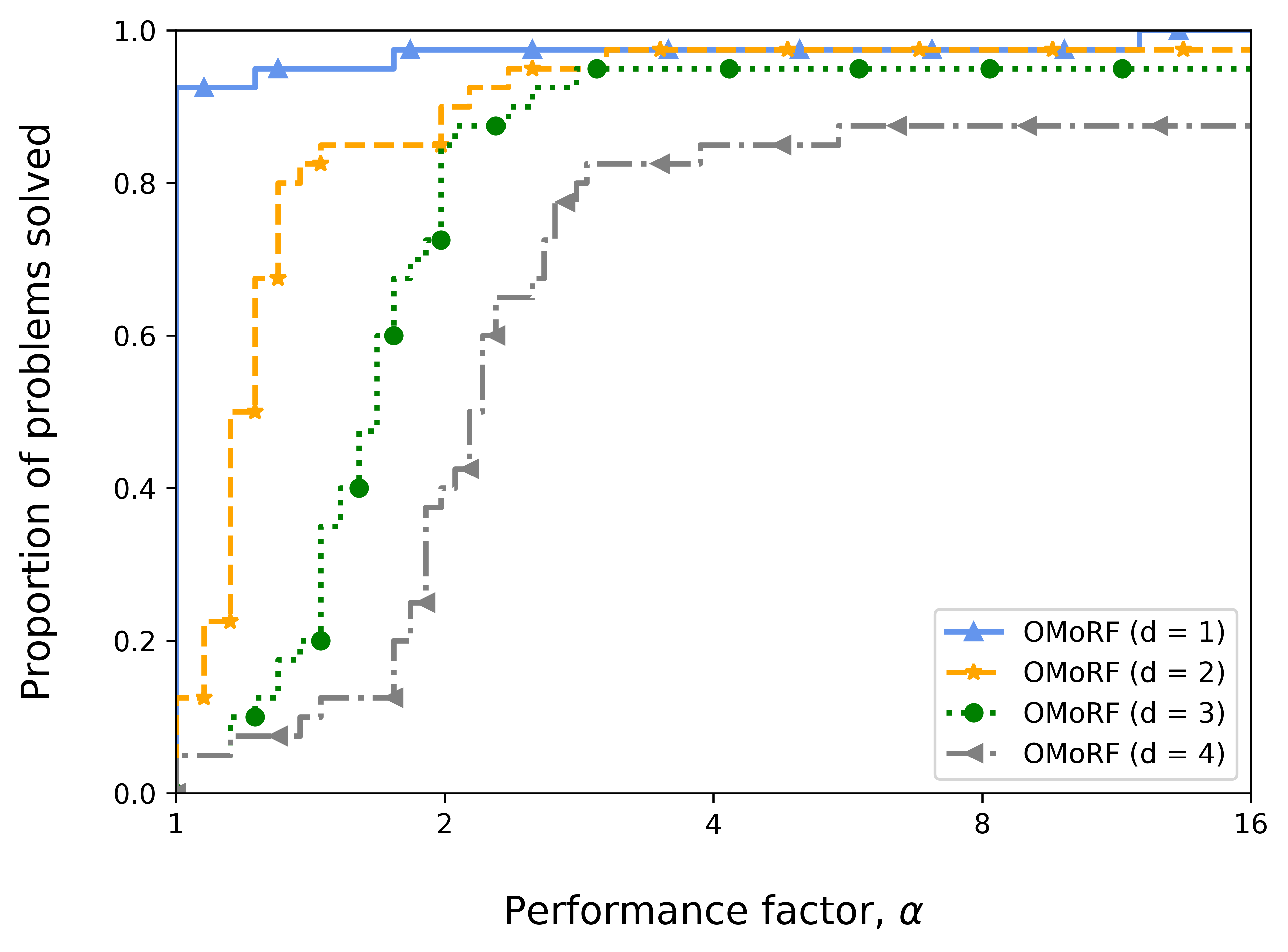

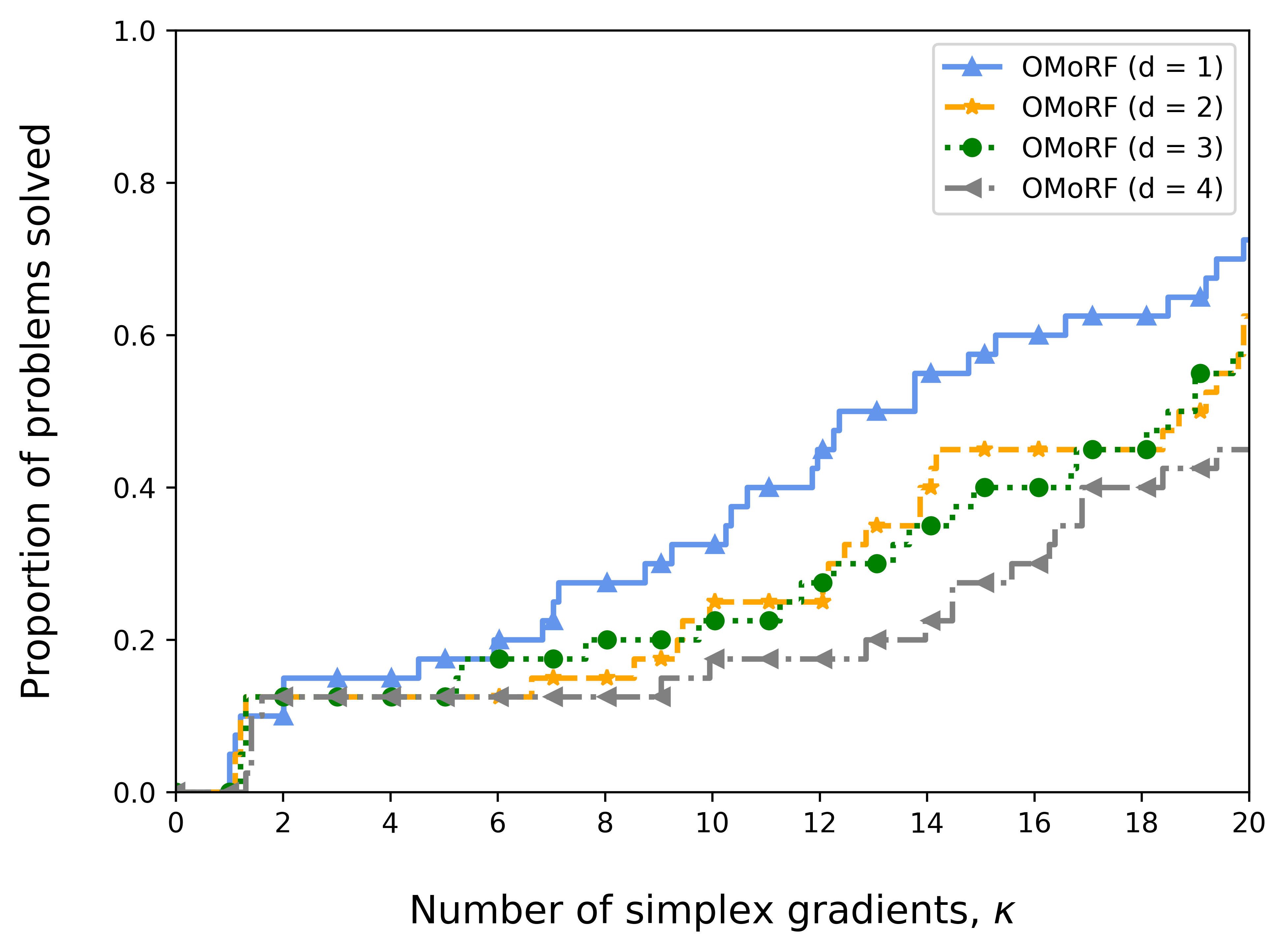

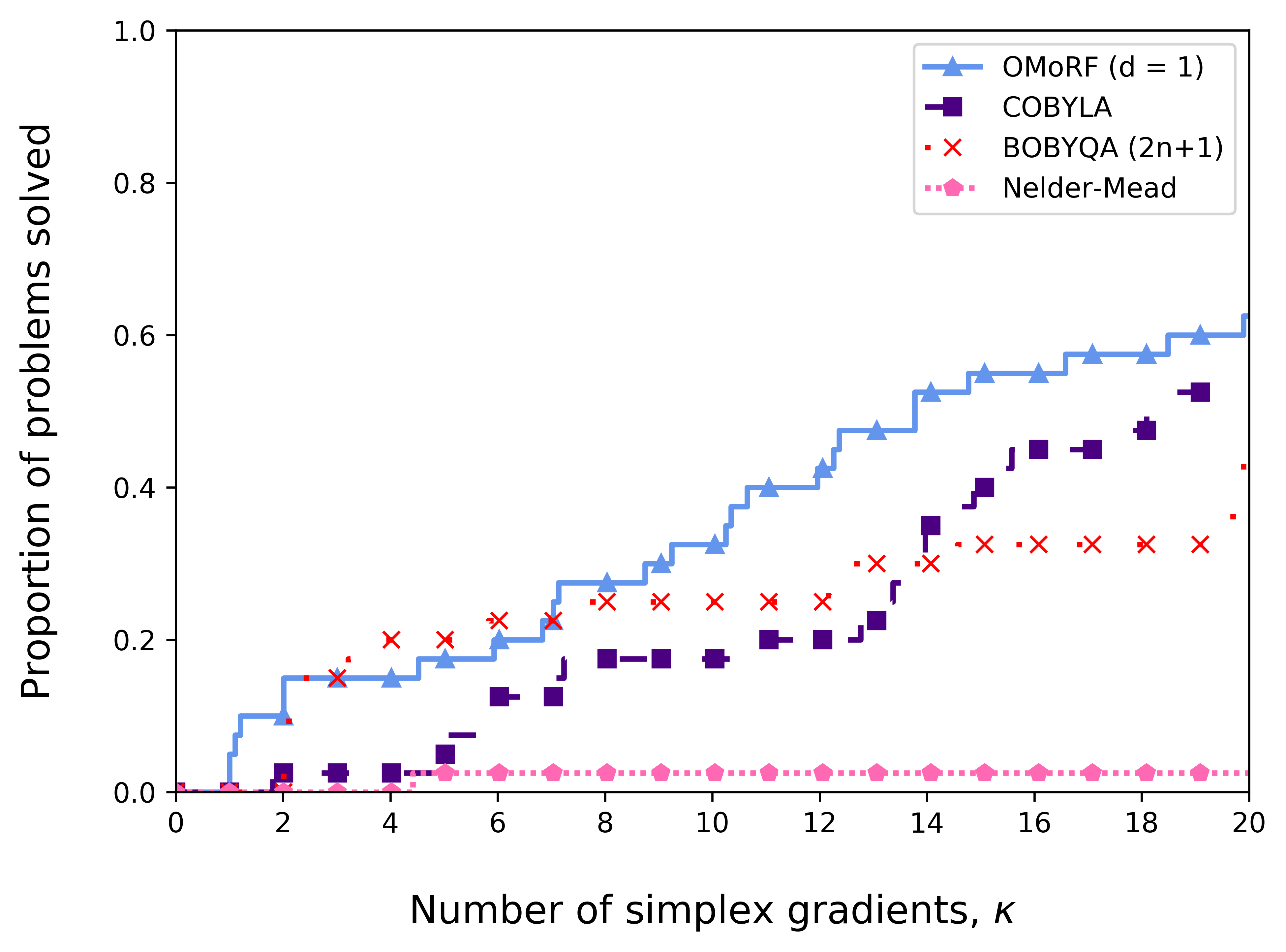

The data and performance profiles for all tested variants of OMoRF for the test set of high dimension problems are shown in Figure 7. Just as in the case problems of moderate dimension, OMoRF was generally the superior solver for this test set. In particular, it was the fastest solver to reach convergence at both the low and high accuracy requirements. Additionally, OMoRF achieved convergence to the high accuracy requirement more than any other solver tested, with it solving about 70% of the problems using the full computational budget. Interestingly, the other variants of OMoRF were more competitive for the high-dimensional problems than the problems of moderate dimension, with all the solvers achieving convergence to the low accuracy requirement for more than 90% of the problems. In particular, OMoRF was able to achieve convergence to the low accuracy requirement for approximately the same proportion of problems as OMoRF . This relative performance increase is likely due to the fact that, as the dimension of the problem increases, the required samples needed to construct a quadratic ridge function becomes less restrictive.

2

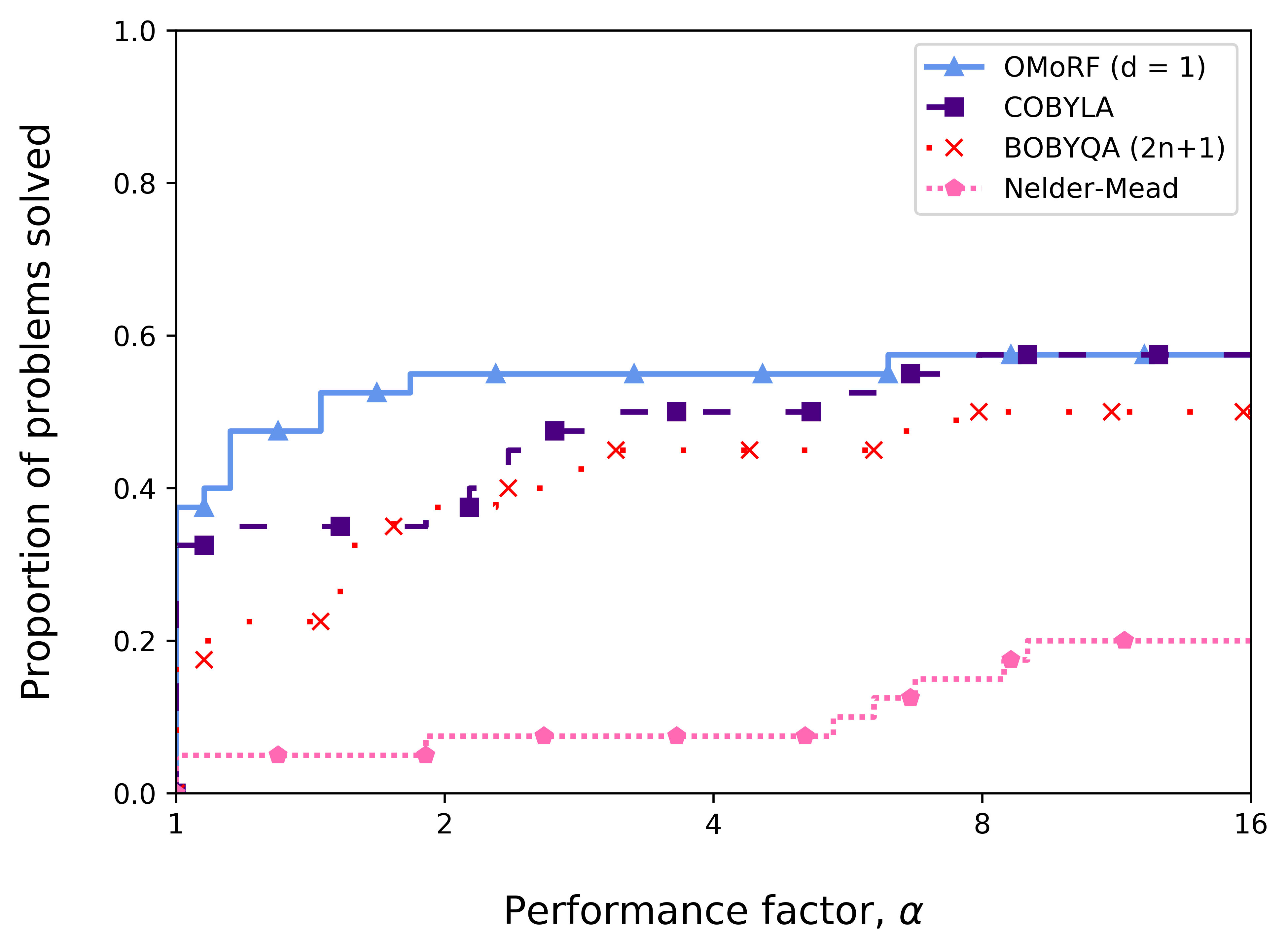

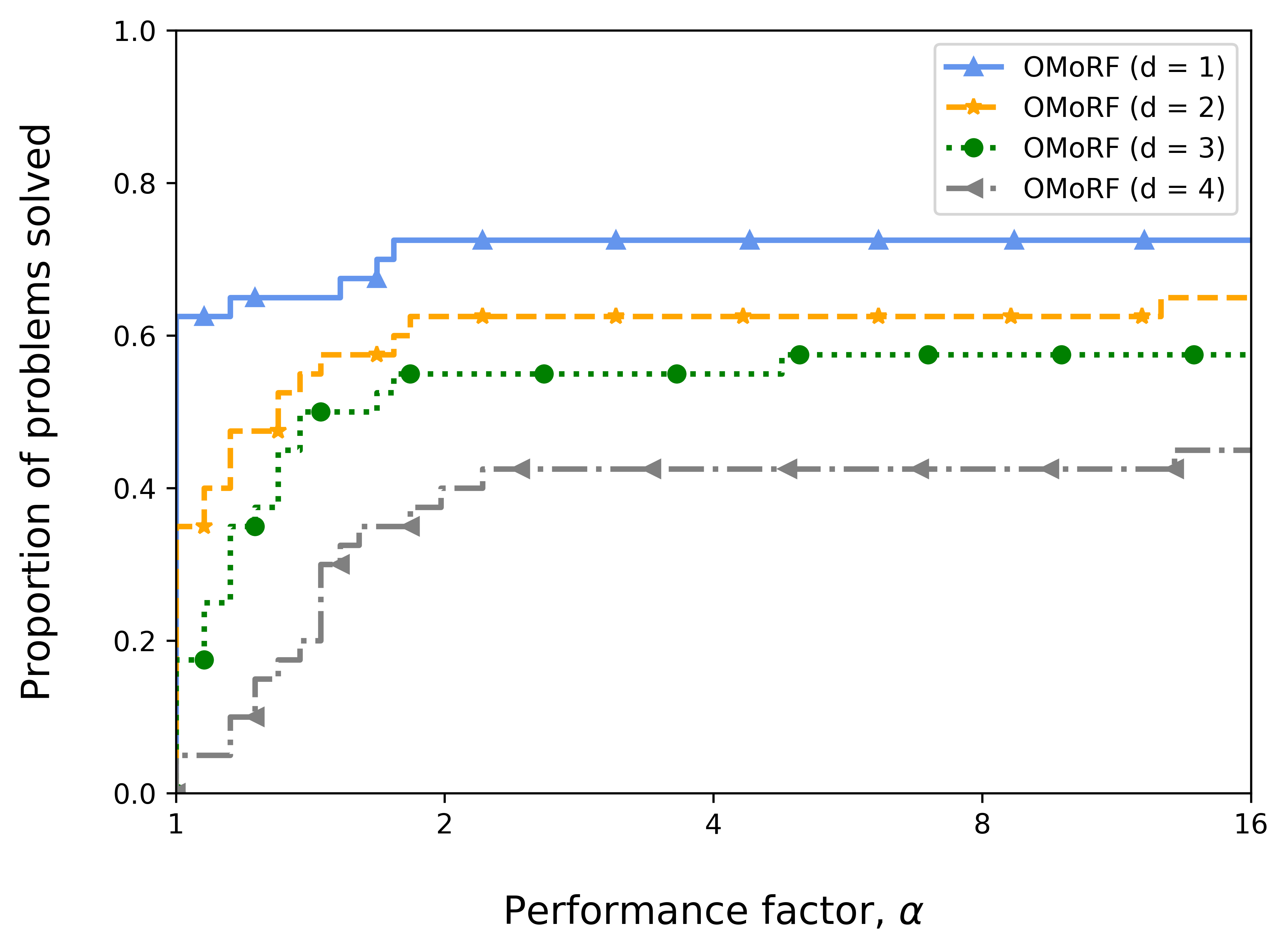

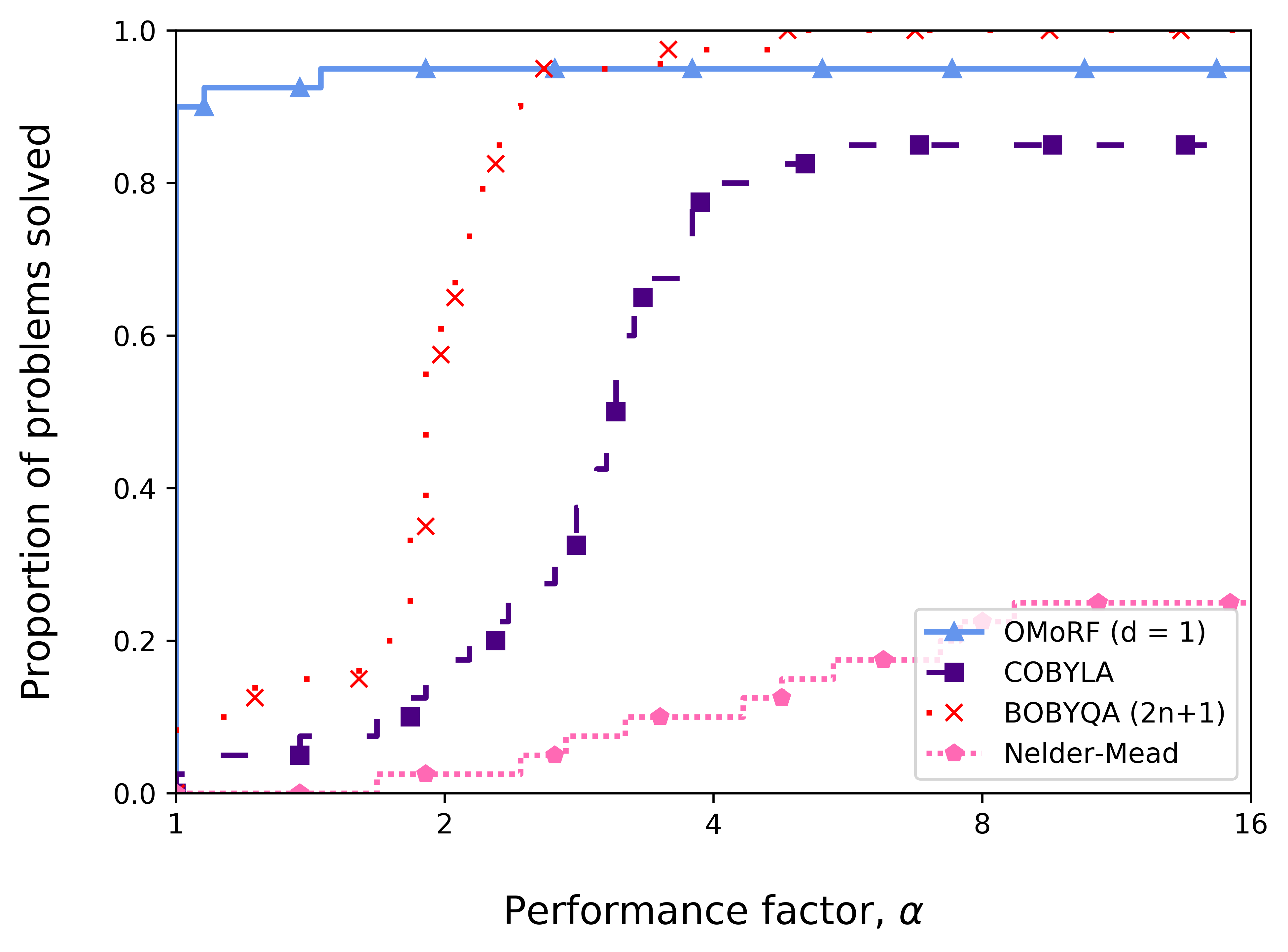

Although the other variants of OMoRF were more competitive, OMoRF was still generally the best performing solver, so this variant was again used for comparison with the other solvers. The data and performance profiles for OMoRF , COBYLA, BOBYQA and Nelder-Mead for the test set of high dimension problems are shown in Figure 8. For this set, the superiority of the OMoRF solver over the other algorithms is even more apparent, with it being the fastest solver to achieve convergence for around 90% of the problems at the low accuracy requirement and approximately 45% for the high accuracy requirement. Although BOBYQA still achieved convergence for a slightly larger proportion of the problems at the low accuracy requirement, OMoRF achieved convergence at the high accuracy requirement for a greater proportion of these problems than any other solver. In particular, at the high accuracy requirement, OMoRF was able to achieve convergence for approximately 60% of these problems. COBYLA, the next best solver, managed to achieve convergence for only approximately 50% of these problems.

2

5.3 Aerodynamic design problem

To demonstrate the efficacy of OMoRF when optimizing high-dimensional functions which are computationally intensive, design optimization of the ONERA-M6 transonic wing, parameterized by 100 free-form deformation (FFD) design points, has been used as a test problem. The objective is to minimize inviscid drag subject to bound constraints on the FFD parameters. This problem has been adapted from an open source tutorial (Palacios and Kline 2017). Furthermore, it has been used for testing design optimization algorithms and approaches in multiple studies (Lukaczyk et al. 2014; Qiu et al. 2018). In this study, this problem has been formulated as

| (45) |

with denoting the FFD parameters and the drag coefficient. The flight conditions are of steady flight at a free-stream Mach number of 0.8395 and an angle of attack of 3.06∘. The Euler solver provided by the open source computational fluid dynamics (CFD) simulation package SU2 (Palacios et al. 2013) was used to evaluate each design. A single CFD simulation required approximately 5 minutes on 8 CPU cores of a 3.7 GHz Ryzen 2700X desktop. Given this computational burden, a strict limit of 500 function evaluations was specified when optimizing this problem. It is noted that, although derivatives of this objective function may be obtained using algorithmic differentiation, this problem still provides a useful test problem for high-dimensional, computationally intensive design optimization.

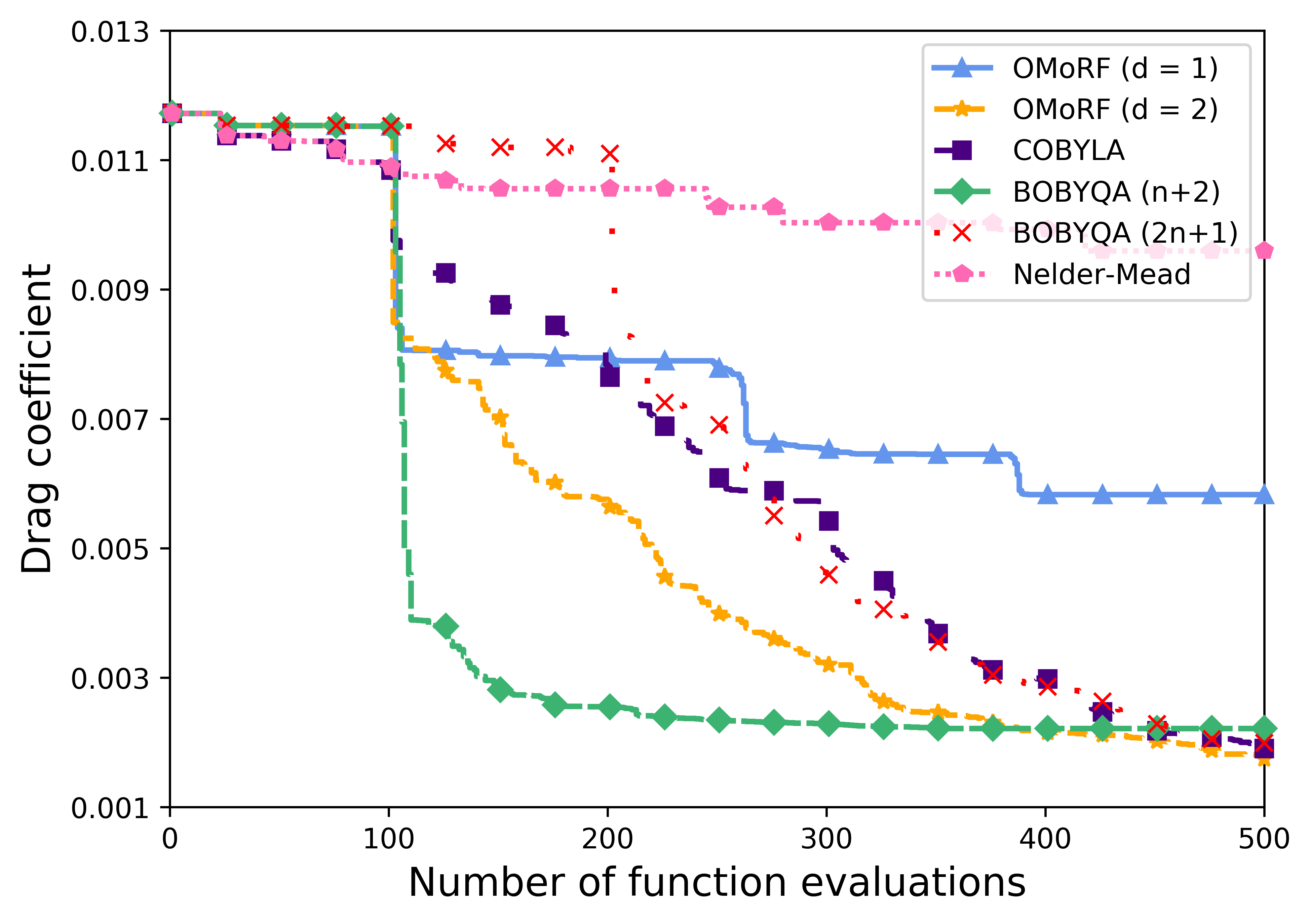

For this problem, both OMoRF and OMoRF were included in the solver comparison. Additionally, both BOBYQA with and points have been included. Figure 9 shows the convergence plot and Table 1 shows the final attained drag coefficients for this design optimization problem. Although BOBYQA shows very quick initial progress, achieving a drag coefficient of less than within 200 function evaluations, its progress afterwards stalls. In fact, OMoRF outperforms it from 400 function evaluations onward, and from 450 function evaluations onward so do COBYLA and BOBYQA . Moreover, not only does OMoRF show very rapid progress, it ultimately outperforms all of the other solvers by achieving the smallest drag coefficient within the computational budget. Interestingly, although OMoRF generally performed quite well in the previous test problems, its performance was significantly worse for this problem. It is hypothesized that, in this case, the underlying problem dimension is best described using more than one dimension. This is in agreement with the findings from previous studies (Lukaczyk et al. 2014; Qiu et al. 2018). In particular, Lukaczyk et al. (2014) discovered that the drag coefficient response of the ONERA-M6 wing was best described using at least a 2-dimensional subspace. Moreover, as discussed for the previous tests, the cost of constructing 2-dimensional ridge function surrogates is considerably less noticeable for high-dimensional problems, making OMoRF generally a more competitive algorithm as the problem dimension increases. In this case, the benefits of capturing the underlying 2-dimensional behaviour clearly outweighed the disadvantages of requiring more sample points to update the ridge function surrogate models.

| Solver | |

|---|---|

| OMoRF () | |

| OMoRF () | |

| COBYLA | |

| BOBYQA | |

| BOBYQA | |

| Nelder-Mead |

6 Conclusion

A novel DFTR method, which leverages output-based dimension reduction in a trust region framework, has been presented. This approach is based upon the idea that, by reducing the effective problem dimension, functions of moderate to high dimension may be modeled using fewer samples. Using these reduced dimension surrogate models for model-based optimization may then lead to accelerated convergence. Although many functions cannot be modeled to sufficient accuracy by globally defined ridge functions, the use of local subspaces allows for greater flexibility, while also maintaining the computational benefits of dimension reduction. Although not proven, the full linearity of ridge function models has been discussed and using this discussion, a motivation for using moving ridge functions has been presented. The efficacy of this algorithm was demonstrated on a number of test problems, including high-dimensional aerodynamic design optimization. Future work will focus on providing further theoretical statements on the convergence properties of this algorithm, extending this method to the case of general nonlinear constraints, and applying this approach to other optimization problems.

Acknowledgements

The authors would like to sincerely thank Dr Pranay Seshadri for his invaluable assistance and advice when developing this algorithm. The first author would also like to thank Dr Hui Feng for her useful suggestions and complete support. The authors also thank three anonymous referees for their valuable comments and suggestions.

Disclosure statement

No potential conflict of interest was reported by the authors.

Funding

This work was supported by the Weir Advanced Research Centre (WARC) through an Engineering and Physical Sciences Research Council (EPSRC) Industrial Cooperative Awards in Science & Technology (CASE) Studentship under Grant Number RG94532.

References

- Bandeira, Scheinberg, and Vicente (2012) Bandeira, Afonso, Katya Scheinberg, and Luís Vicente. 2012. “Computation of sparse low degree interpolating polynomials and their application to derivative-free optimization.” In Mathematical Programming, Vol. 134, 223–257.

- Bandeira, Scheinberg, and Vicente (2014) Bandeira, Afonso, Katya Scheinberg, and Luís Vicente. 2014. “Convergence of trust-region methods based on probabilistic models.” SIAM Journal on Optimization 24 (3): 1238–1264.

- Bergstra and Bengio (2012) Bergstra, James, and Yoshua Bengio. 2012. “Random search for hyper-parameter optimization.” Journal of Machine Learning Research 13: 281–305.

- Cartis et al. (2019) Cartis, Coralia, Jan Fiala, Benjamin Marteau, and Lindon Roberts. 2019. “Improving the flexibility and robustness of model-based derivative-free optimization solvers.” ACM Transactions on Mathematical Software 45 (3): 1–41.

- Cartis and Otemissov (2020) Cartis, Coralia, and Adilet Otemissov. 2020. “A dimensionality reduction technique for unconstrained global optimization of functions with low effective dimensionality.” (Preprint).

- Cartis and Roberts (2019) Cartis, Coralia, and Lindon Roberts. 2019. “A derivative-free Gauss-Newton method.” Mathematical Programming Computation 11 (4): 631–674.

- Choromanski et al. (2019) Choromanski, Krzysztof, Aldo Pacchiano, Jack Parker-Holder, Yunhao Tang, and Vikas Sindhwani. 2019. “From complexity to simplicity: Adaptive ES-active subspaces for blackbox optimization.” In Advances in Neural Information Processing Systems, 10299–10309.

- Conn, Gould, and Toint (2000) Conn, Andrew, Nicholas Gould, and Philippe Toint. 2000. Trust-region methods. Philadelphia, Pa.: Society for Industrial and Applied Mathematics: Mathematical Programming Society.

- Conn, Scheinberg, and Vicente (2008) Conn, Andrew, Katya Scheinberg, and Luís Vicente. 2008. “Geometry of interpolation sets in derivative free optimization.” Mathematical Programming 111 (1): 141–172.

- Conn, Scheinberg, and Vicente (2009a) Conn, Andrew, Katya Scheinberg, and Luís Vicente. 2009a. “Global convergence of general derivative-free trust-region algorithms to first- and second-order critical points.” SIAM Journal on Optimization 20 (1): 387–415.

- Conn, Scheinberg, and Vicente (2009b) Conn, Andrew, Katya Scheinberg, and Luís Vicente. 2009b. Introduction to derivative-free optimization. Philadelphia, Pa.: Society for Industrial and Applied Mathematics: Mathematical Programming Society.

- Constantine and Doostan (2017) Constantine, Paul, and Alireza Doostan. 2017. “Time-dependent global sensitivity analysis with active subspaces for a lithium ion battery model.” Statistical Analysis and Data Mining 10 (5): 243–262.

- Constantine, Dow, and Wang (2014) Constantine, Paul, Eric Dow, and Qiqi Wang. 2014. “Active subspace methods in theory and practice: Applications to kriging surfaces.” SIAM Journal on Scientific Computing 36 (4): A1500–A1524.

- Constantine (2015) Constantine, Paul G. 2015. Active subspaces: Emerging ideas for dimension reduction in parameter studies. Philadelphia, Pa.: SIAM Spotlights.

- Diez, Campana, and Stern (2015) Diez, Matteo, Emilio Campana, and Frederick Stern. 2015. “Design-space dimensionality reduction in shape optimization by Karhunen-Loève expansion.” Computer Methods in Applied Mechanics and Engineering 283 (1): 1525–1544.

- Eldar and Kutyniok (2012) Eldar, Yonina, and Gitta Kutyniok. 2012. Compressed sensing: Theory and applications. Cambridge, UK: Cambridge University Press.

- Fasano, Morales, and Nocedal (2009) Fasano, Giovanni, José Luis Morales, and Jorge Nocedal. 2009. “On the geometry phase in model-based algorithms for derivative-free optimization.” Optimization Methods and Software 24 (1): 145–154.

- Ghanbari and Scheinberg (2017) Ghanbari, Hiva, and Katya Scheinberg. 2017. “Black-box optimization in machine learning with trust region based derivative free algorithm.” (Preprint).

- Glaws et al. (2017) Glaws, Andrew, Paul Constantine, John N. Shadid, and Tim Wildey. 2017. “Dimension reduction in MHD power generation models: Dimensional analysis and active subspaces.” Statistical Analysis and Data Mining: The ASA Data Science Journal 10: 312–325.

- Gould, Orban, and Toint (2015) Gould, Nicholas, Dominique Orban, and Philippe Toint. 2015. “CUTEst: a Constrained and Unconstrained Testing Environment with safe threads for mathematical optimization.” Computational Optimization and Applications 60 (3): 545–557.

- Gould and Scott (2016) Gould, Nicholas, and Jennifer Scott. 2016. “A note on performance profiles for benchmarking software.” ACM Transactions on Mathematical Software 43 (2): 1–5.

- Gross, Seshadri, and Parks (2020) Gross, James, Pranay Seshadri, and Geoffrey Parks. 2020. “Optimisation with intrinsic dimension reduction: A ridge informed trust-region method.” In Proceedings of AIAA SciTech Forum and Exposition, Orlando, USA.

- Gu (2001) Gu, Lei. 2001. “A comparison of polynomial based regression models in vehicle safety analysis.” In Proceedings of the ASME Design Engineering Technical Conference, Vol. 2.

- Hokanson and Constantine (2017) Hokanson, Jeffrey, and Paul Constantine. 2017. “Data-driven polynomial ridge approximation using variable projection.” SIAM Journal on Scientific Computing 40 (3): 1566–1589.

- Johnson (2018) Johnson, Steven. 2018. “The NLopt nonlinear-optimization package.” http://github.com/stevengj/nlopt.

- Kannan and Wild (2012) Kannan, Aswin, and Stefan Wild. 2012. Obtaining quadratic models of noisy functions. Technical Report. 9700 South Cass Avenue, Argonne, Illinois, USA: Argonne National Labratory.

- Kipouros et al. (2008) Kipouros, Timoleon, Daniel Jaeggi, William Dawes, Geoffrey Parks, Mark Savill, and John Clarkson. 2008. “Biobjective design optimization for axial compressors using tabu search.” AIAA Journal 46 (3): 701–711.

- Kozak et al. (2019) Kozak, David, Stephen Becker, Alireza Doostan, and Luis Tenorio. 2019. “Stochastic subspace descent.” (Preprint).

- Levina et al. (2009) Levina, Tatsiana, Yuri Levin, Jeff McGill, and Mikhail Nediak. 2009. “Dynamic pricing with online learning and strategic consumers: An application of the aggregating algorithm.” Operations Research 57 (2): 327–341.

- Lukaczyk et al. (2014) Lukaczyk, Trent, Paul Constantine, Francisco Palacios, and Juan Alonso. 2014. “Active Subspaces for Shape Optimization.” In 10th AIAA Multidisciplinary Design Optimization Specialist Conference, .

- Moré and Wild (2009) Moré, Jorge, and Stefan Wild. 2009. “Benchmarking derivative-free optimization algorithms.” SIAM Journal on Optimization 20 (1): 172–191.

- Nelder and Mead (1965) Nelder, John, and Roger Mead. 1965. “A simplex method for function minimization.” The Computer Journal 7 (4): 308–313.

- Palacios et al. (2013) Palacios, Francisco, Michael Colonno, Aniket Aranake, Alejandro Campos, Sean Copeland, Thomas Economon, Amrita Lonkar, Trent Lukaczyk, Thomas Taylor, and Juan Alonso. 2013. “Stanford University Unstructured (SU2): An open-source integrated computational environment for multi-physics simulation and design.” In 51st AIAA Aerospace Sciences Meeting including the New Horizons Forum and Aerospace Exposition 2013, .

- Palacios and Kline (2017) Palacios, Francisco, and Heather Kline. 2017. “Constrained shape design of a transonic inviscid wing.” Accessed 2019-08-12. https://su2code.github.io/tutorials/Inviscid_3D_Constrained_ONERAM6/.

- Parsons, Haque, and Liu (2004) Parsons, Lance, Ehtesham Haque, and Huan Liu. 2004. “Subspace Clustering for High Dimensional Data: A Review.” SIGKDD Explorations, Newsletter of the ACM Special Interest Group on Knowledge Discovery and Data Mining 6 (1): 90–105.

- Pinkus (2015) Pinkus, Allan. 2015. Ridge functions. Cambridge, UK: Cambridge University Press.

- Powell (1994) Powell, Michael. 1994. “A direct search optimization method that models the objective and constraint functions by linear interpolation.” In Advances in Optimization and Numerical Analysis, 51–67. Springer Netherlands.

- Powell (2006) Powell, Michael. 2006. “The NEWUOA software for unconstrained optimization without derivatives.” In Large-Scale Nonlinear Optimization, 255–297.

- Powell (2009) Powell, Michael. 2009. The BOBYQA algorithm for bound constrained optimization without derivatives. Technical Report. Cambridge, UK: Department of Applied Mathematics and Theoretical Physics, University of Cambridge.

- Qiu et al. (2018) Qiu, Yasong, Junqiang Bai, Nan Liu, and Chen Wang. 2018. “Global aerodynamic design optimization based on data dimensionality reduction.” Chinese Journal of Aeronautics 31 (4): 643–659.

- Scheinberg and Toint (2010) Scheinberg, Katya, and Philippe Toint. 2010. “Self-correcting geometry in model-based algorithms for derivative-free unconstrained optimization.” SIAM Journal on Optimization 20 (6): 3512–3532.

- Seshadri and Parks (2017) Seshadri, Pranay, and Geoffrey Parks. 2017. “Effective-Quadratures (EQ): Polynomials for computational engineering studies.” The Journal of Open Source Software 2 (11).

- Seshadri et al. (2018) Seshadri, Pranay, Shahrokh Shahpar, Paul Constantine, Geoffrey Parks, and Mike Adams. 2018. “Turbomachinery active subspace performance maps.” Journal of Turbomachinery 140 (4): 041003–1–041003–11.

- Shan and Wang (2010) Shan, Songqing, and G. Gary Wang. 2010. “Survey of modeling and optimization strategies to solve high-dimensional design problems with computationally-expensive black-box functions.” Structural and Multidisciplinary Optimization 41 (2): 219–241.

- Virtanen et al. (2020) Virtanen, Pauli, Ralf Gommers, Travis Oliphant, Matt Haberland, Tyler Reddy, David Cournapeau, Evgeni Burovski, et al. 2020. “SciPy 1.0: Fundamental algorithms for scientific computing in Python.” Nature Methods 17: 261–272.

- Wang et al. (2016) Wang, Ziyu, Frank Hutter, Masrour Zoghi, David Matheson, and Nando De Freitas. 2016. “Bayesian optimization in a billion dimensions via random embeddings.” Journal of Artificial Intelligence Research 55: 361–367.

- Wendor, Botero, and Alonso (2016) Wendor, Andrew, Emilio Botero, and Juan Alonso. 2016. “Comparing different off-the-shelf optimizers’ performance in conceptual aircraft design.” In 17th AIAA/ISSMO Multidisciplinary Analysis and Optimization Conference, .

- Wong et al. (2019) Wong, Chun Yui, Pranay Seshadri, Geoffrey Parks, and Mark Girolami. 2019. “Embedded ridge approximations: constructing ridge approximations over localized scalar fields for improved simulation-centric dimension reduction.” (Preprint).

- Zhang, Conn, and Scheinberg (2010) Zhang, Hongchao, Andrew Conn, and Katya Scheinberg. 2010. “A derivative-free algorithm for least-squares minimization.” SIAM Journal on Optimization 20 (6): 3555–3576.

- Zhao, Alimo, and Bewley (2018) Zhao, Muhan, Shahrouz Ryan Alimo, and Thomas Bewley. 2018. “An active subspace method for accelerating convergence in Delaunay-based optimization via dimension reduction.” In Proceedings of the IEEE Conference on Decision and Control, Miami Beach, Florida, USA, 2765–2770.

7 Appendices

Appendix A Proof of Lemma 3.2

Proof.

Let denote and denote . First, observe that

where is the Lipschitz constant of . Next,

Finally,

∎

Appendix B Proof of Theorem 3.5

Proof.

Let

be a quadratic ridge function with and note

Subtracting from gives

Taking the first-order Taylor expansion of around and rearranging gives

| (46) |

To remove , subtract the above equation evaluated at from the equations to give

| (47) |

Equation (47) is true for any such that and any .

Bounding the absolute value of each term of the right-hand side of (47) provides a bound on . First, note that since is Lipschitz continuous with constant , the absolute values of the first two terms may be bounded as follows:

Similarly, the absolute values of the third and fourth expressions can be bounded by using

Finally, the absolute values of the last two terms may be bounded by using the fact that interpolates at the sample points

As , it is known that and . Therefore,

| (48) |

As (48) is true for every , it is also true for . So using , one may write

Finally, taking to the right-hand side and using the fact that

the result

| (49) |

is obtained.

To obtain a similar bound on , note from (46) that

Rearranging and collecting like terms gives

| (50) |

as required. ∎

Appendix C Modified pivotal algorithm for updating interpolation sets

In Algorithm 2, a mechanism for choosing samples to be replaced and improving the geometry of interpolation sets was alluded to. This mechanism is presented in Algorithm 3 for clarity. This algorithm has been adapted from Algorithm 5.1 in Conn, Scheinberg, and Vicente (2008). It applies Gaussian elimination with row pivoting to to place an upper bound on , in turn bounding the condition number of . The pivot polynomial basis for is related to the rows of the upper triangular matrix in the LU factorization of . Rows which have pivot values of small absolute value make large contributions to . Samples in correspond to rows of , so by replacing these samples with ones which have higher pivot values, the geometry of can be improved. The aim of the search (52) is to find and prioritize samples which have high pivot values over those which have low pivot values. Finally, if the geometry needs to be improved, the optimization problem (51) is solved, returning the point in the trust region of maximal absolute pivot value.

| (51) |

| (52) |

There are a few points to note about Algorithm 3. First, when choosing a point to be replaced, lines 5–6 in Algorithm 3 are omitted. Second, if during the search for points with low pivot values , no consideration is given to the distance the point is from the current iterate, then situations occur where points which are within the trust region are replaced before points which are not. Therefore, an idea from Powell (2009) has been borrowed which gives preference to points within the trust region. In particular, the term is divided by in the search (52). Although alternative methods which seek a balance between preserving the quality of the interpolation set and the close proximity of sample points are available (see Scheinberg and Toint (2010)), this method of dividing the pivot value by the relative distance of point to the power of four (i.e. ) when lies outside the trust region seems to work quite well in practice. Third, when performing geometry-improving steps, the conditional in line 5 is not activated until the last iteration (i.e. ). This means that, at each iteration, only a single new geometry-improving sample point will be calculated, leading to incremental improvements in the quality of the interpolation set. Fourth, although the points which improve are different than for , Algorithm 3 may be applied to both of these sets by a suitable choice of dimension , degree and polynomial basis . In the case of , the dimension , degree and the natural polynomial basis

| (53) |

are used, whereas, in the case of , the dimension , degree 2 and , i.e. the natural polynomial basis defined on the subspace , are used. Finally, although this algorithm can be applied to any set , Conn, Scheinberg, and Vicente (2008) found it to be most effective when applied to the shifted and scaled set

| (54) |

where

This is the same approach that is used in OMoRF when updating the sample sets.

Appendix D CUTEst problems

The tables below provide lists of the problems which were used in the optimization studies. Table 2 contains the problems of moderate dimension and Table 3 contains the problems of high dimension . In the tables below is the minimum attained value from all the tested solvers within the computational budget of 20 simplex gradients. Values of and have been rounded to the nearest 7 significant figures.

| # | Problem | |||

|---|---|---|---|---|

| 1 | ARGLINA | 10 | 430 | 389.9999 |

| 2 | ARGLINB | 10 | 6.476671 | 99.62547 |

| 3 | ARGLINC | 10 | 4.083138 | 101.1255 |

| 4 | ARGTRIGLS | 10 | 2.966540 | 0 |

| 5 | BOX | 10 | 0 | -0.1725693 |

| 6 | BOXPOWER | 10 | 72.36521 | 4.845789 |

| 7 | BROWNAL | 10 | 273.248 | 6.64347 |

| 8 | DIXMAANA | 15 | 143.5 | 1 |

| 9 | DIXMAANB | 15 | 228.25 | 1 |

| 10 | DIXMAANC | 15 | 395.5 | 1.000002 |

| 11 | DIXMAAND | 15 | 756.76 | 1 |

| 12 | DIXMAANE | 15 | 113.5 | 1.000535 |

| 13 | DIXMAANF | 15 | 199.25 | 1.000235 |

| 14 | DIXMAANG | 15 | 365.5 | 1.000454 |

| 15 | DIXMAANH | 15 | 724.6 | 1.000555 |

| 16 | DIXMAANI | 15 | 103.1667 | 1.001657 |

| 17 | DIXMAANJ∗ | 15 | 189.1056 | 1.004441 |

| 18 | DQDRTIC | 10 | 14472 | 0 |

| 19 | HATFLDGLS | 25 | 27 | 2.991629 |

| 20 | HILBERTA | 10 | 60.18943 | 7.493782 |

| 21 | HILBERTB | 10 | 510.1894 | 0 |

| 22 | HYDCAR6LS | 29 | 704.1073 | 3.274127 |

| 23 | MCCORMCK | 10 | 9 | -9.646185 |

| 24 | METHANL8LS | 31 | 4345.1 | 13.042193 |

| 25 | MOREBV | 10 | 0.01598655 | 1.020147 |

| 26 | NCVXBQP1 | 10 | -55.125 | -22050 |

| 27 | NCVXBQP2∗ | 10 | -28.125 | -14381.865 |

| 28 | NCVXBQP3 | 10 | -14.625 | -11957.805 |

| 29 | NONDIA | 10 | 3604.0 | 1.070407 |

| 30 | PENALTY1 | 10 | 148032.5 | 1.119897 |

| 31 | PENALTY2 | 10 | 162.6528 | 2.975281 |

| 32 | POWER | 10 | 3025 | 1.347023 |

| 33 | POWERSUM | 10 | 2.851305 | 1.604428 |

| 34 | PROBPENL | 10 | 1600 | 0 |

| 35 | SANTALS | 21 | 1.430615 | 0.04634251 |

| 36 | SCHMVETT | 10 | -22.88052 | -23.99999 |

| 37 | TQUARTIC | 10 | 0.81 | 2.051379 |

| 38 | TRIGON1 | 10 | 2.96654 | 0 |

| 39 | TRIGON2 | 10 | 51.08556 | 2.80259 |

| 40 | VARDIM | 10 | 2.198551 | 0.04920879 |

| # | Problem | |||

|---|---|---|---|---|

| 1 | ARGLINA∗ | 50 | 550 | 350 |

| 2 | ARGLINB | 50 | 3.480995 | 99.62547 |

| 3 | ARGLINC | 50 | 3.160263 | 101.1255 |

| 4 | ARGTRIGLS | 50 | 16.32621 | 2.997498 |

| 5 | BA-L1LS | 57 | 127387.8 | 1.134976 |

| 6 | BA-L1SPLS | 57 | 127387.8 | 0 |

| 7 | DIXMAANA | 90 | 856 | 1.000167 |

| 8 | DIXMAANB | 90 | 1409.5 | 1.002449 |

| 9 | DIXMAANC | 90 | 2458 | 1.000219 |

| 10 | DIXMAAND | 90 | 4722.76 | 1.000204 |

| 11 | DIXMAANE | 90 | 665.5833 | 1.026302 |

| 12 | DIXMAANF | 90 | 1225.292 | 1.003309 |

| 13 | DIXMAANG∗ | 90 | 2267.583 | 1.004975 |

| 14 | DIXMAANH | 90 | 4518.933 | 1.004104 |

| 15 | DIXMAANI | 90 | 603.591 | 1.043307 |

| 16 | DIXMAANJ | 90 | 1164.3 | 1.004421 |

| 17 | DQRTIC | 50 | 86832 | 0 |

| 18 | ENGVAL1 | 50 | 2891 | 53.58364 |

| 19 | HYDC20LS | 99 | 1341.663 | 17.23815 |

| 20 | LUKSAN12LS | 98 | 32160 | 4119.833 |

| 21 | LUKSAN13LS | 98 | 64352 | 25550.51 |

| 22 | LUKSAN14LS∗ | 98 | 26880 | 164.4811 |

| 23 | LUKSAN15LS | 100 | 27015.85 | 3.569885 |

| 24 | LUKSAN16LS | 100 | 13068.48 | 3.569714 |

| 25 | LUKSAN17LS | 100 | 1.68737 | 25.26664 |

| 26 | LUKSAN22LS | 100 | 24876.86 | 871.1351 |

| 27 | MCCORMCK | 50 | 49 | -46.12886 |

| 28 | MOREBV | 50 | 1.321345 | 1.42846 |

| 29 | NCVXBQP1 | 50 | -1258.875 | -507223.9 |

| 30 | NCVXBQP2 | 50 | -703.125 | -338857.6 |

| 31 | NCVXBQP3 | 50 | 64.125 | -183479.1 |

| 32 | NONDIA | 50 | 19604 | 0.432696 |

| 33 | PENALTY1 | 50 | 1.842534 | 4.898239 |

| 34 | PENALTY2 | 50 | 100969.4 | 4.300743 |

| 35 | POWER∗ | 50 | 1.625625 | 0.175913 |

| 36 | PROBPENL | 50 | 57600 | 0 |

| 37 | SPARSQUR | 50 | 358.5938 | 0 |

| 38 | TQUARTIC | 50 | 0.81 | 0.04204344 |

| 39 | TRIDIA | 50 | 1274 | 6.544255 |

| 40 | VARDIM | 50 | 5.432025 | 0.3873602 |