A 22 random switching model and its dual risk model

Abstract

In this article a special case of two coupled M/G/1-queues is considered, where two servers are exposed to two types of jobs that are distributed among the servers via a random switch. In this model the asymptotic behavior of the workload buffer exceedance probabilities for the two single servers/ both servers together/ one (unspecified) server is determined. Hereby one has to distinguish between jobs that are either heavy-tailed or light-tailed. The results are derived via the dual risk model of the studied coupled M/G/1-queues for which the asymptotic behavior of different ruin probabilities is determined.

2020 Mathematics subject classification. 60K25, 94C11 (primary), 60G10, 91G05 (secondary)

Keywords: bipartite network, bivariate compound Poisson process, hitting probability, coupled M/G/1-queues, random switch, regular variation, ruin theory, queueing theory

1 Introduction

A general switch is modelled by a two-server queueing system with two arrival streams. A well-studied special cases of such a switch is given by the clocked buffered switch, where in a unit time interval each arrival stream can generate only one arrival and each server can serve only one customer; see e.g. [1, 11, 19] and others. This switch is commonly used to model a device used in data-processing networks for routing messages from one node to another.

In this paper we study a switch that operates in continuous time, i.e. the arrivals are modelled by two independent compound Poisson processes. Every incoming job is of random size and it is then distributed to the two servers by a random procedure. This leads to a pair of coupled M/G/1-queues. In this model we study the equilibrium probabilities of the resulting workload processes. In particular we determine the asymptotic behavior of the probabilities that the workloads exceed a prespecified buffer. Hereby we will distinguish between workload exceedance of a specific single server, both servers, or one unspecified server. As we will see, the behavior of these workload exceedance probabilities strongly depends on whether jobs are heavy-tailed or light-tailed and we will therefore consider both cases separately.

A related model to the one we study has been introduced in [10] where a pair of coupled queues driven by independent spectrally-positive Lévy processes is introduced. The coupling procedure however is completely different to the switch we shall use. For this model, in [10], the joint transform of the stationary workload distribution in terms of Wiener-Hopf factors is determined. Two parallel queues are also considered e.g. in [23] for an M/M/2-queue where arriving customers simultaneously place two demands handled independently by two servers. We refer to [2] and [22] and references therein for more general information on Lévy-driven queueing systems.

As it is well known, there are several connections between queueing and risk models. In particular the workload (or waiting time) in an M/G/1 queue with compound Poisson input is related to the ruin probability in the prominent Cramér-Lundberg risk model, in which the arrival process of claims is defined to be just the same compound Poisson process; see e.g. [2] or [31]. To be more precise, let

be a Cramér-Lundberg risk process with initial capital , premium rate , i.i.d. claims with cdf such that a.s. and , and a claim number process which is a Poisson process with rate . Then it is well known that the ruin probability

tends to as , as long as the net-profit condition holds, while otherwise . In particular, if the claims sizes are light-tailed in the sense that an adjustment coefficient exists, i.e.

where is the tail-function of the claim sizes, then the ruin probability satisfies the famous Cramér-Lundberg inequality (cf. [2, Eq. XIII (5.2)], [3, Eq. I.(4.7)])

Furthermore in this case the Cramér-Lundberg approximation states that (cf. [2, Thm. XIII.5.2], [3, Eq. I.(4.3)])

for some known constant depending on the chosen parameters of the model. On the contrary, for heavy-tailed claims with a subexponential integrated tail function it is known that (cf. [3, Thm. X.2.1])

and in the special case of tail-functions that are regularly varying this directly implies that the ruin probability decreases polynomially.

Via the mentioned duality these results can easily be translated into corresponding results on the workload exceedance probability of an M/G/1-queue.

In this paper we shall use an analogue duality between queueing and risk models in a multi-dimensional setting as it was introduced in [7]. This allows us to obtain results on the workload exceedance probabilities of the switch by studying the corresponding ruin probabilities in the two-dimensional dual risk model.

Bivariate risk models are a well-studied field of research. A prominent model in the literature, that can be interpreted as a special case of the dual risk model in this paper, has been introduced by Avram et. al. [5]. In this so-called degenerate model a single claim process is shared via prespecified proportions between two insurers (see e.g. [4, 5, 6, 24, 26]). The model allows for a rescaling of the bivariate process that reduces the complexity to a one-dimensional ruin problem. Exact results and sharp asymptotics for this model have been obtained in [4], where also the asymptotic behavior of ruin probabilities of a general two-dimensional Lévy model under light-tail assumptions is derived. In [24] the degenerate model is studied in the presence of heavy tails; specifically asymptotic formulae for the finite time as well as the infinite time ruin probabilities under the assumption of subexponential claims are provided. In [26] the degenerate model is extended by a constant interest rate. In [6] another generalization of the degenerate model is studied that introduces a second source of claims only affecting one insurer. Our risk model defined in Section 2.2 can be seen as a further generalization of the model in [6] because of the random sharing of every single claim, compare also with Section 5.2 below.

There exist plenty of other papers concerning bivariate risk models of all types and several approaches to tackle the problem. E.g. [14, 21] consider bivariate risk models of Cramér-Lundberg-type with correlated claim-counting processes and derive partial integro-differential equations for infinite-time ruin and survival probabilities in these models. Various authors focus on finite time ruin probabilities under different assumptions, see e.g. [15, 16, 17, 29, 32, 37, 38]. E.g. in [38] the finite time survival probability is approximated using a so-called bivariate compound binomial model and bounds for the infinite-time ruin probability are obtained using the concept of association.

In general dimensions, multivariate ruin is studied e.g. in [9, 12, 13, 25, 30, 34]. In particular, in [9] a bipartite network induces the dependence between the risk processes and this model is in some sense similar to the dual risk model in this paper. Further, in [20], multivariate risk processes with heavy-tailed claims are treated and so-called ruin regions are studied, that is,

sets in which are hit by the risk process with small probability. Multivariate regularly varying claims are also

assumed e.g. in [27] and [30], where in [27] several lines of business are considered that can balance out ruin, while [30] focuses exclusively on simultaneous ruin of all business lines/agents. Further, [36] introduces a notion of multivariate subexponentiality and applies this on a multivariate risk process. Note that [27] and [36] both consider rather general regions of ruin and some of the results from these papers will be applied on our dual risk model.

The paper is outlined as follows. In Section 2 we specify the random switch model that we are interested in and introduce the corresponding dual risk model. Section 3 is devoted to study both models under the assumption that jobs/claims are heavy-tailed and it is divided into two parts. First, in Section 3.1 we focus on subexponentiality. As we shall rely on results from [36] we first concentrate on the risk model in Section 3.1.1 and then transfer our findings to the switch model in Section 3.1.2. Second, we treat the special case of regular variation in Section 3.2, where we start with results for the risk model in Section 3.2.1, taking advantage of results given in [27], before we transfer our findings to the switch model in Section 3.2.2. In Section 4 we assume all jobs/claims to be light-tailed and again first consider the risk model in Section 4.1 before converting the results to the switch context in Section 4.2. Two particular examples of the switch will then be outlined in Section 5 where we also compare the behavior of the exceedance probabilities for different specifications of the random switch via a short simulation study in Section 5.3. The final Section 6 collects the proofs of all our findings.

2 The switching model and its dual

2.1 The random switching model

Let be servers (or workers) with work speeds and let be two job generating objects. We assume that both objects generate jobs independently with Poisson rates , respectively, and that the workloads generated by one object are i.i.d. positive random variables. More specifically, we identify the objects , , with two independent compound Poisson processes

with jumps being i.i.d. copies of two random variables such that and , .

The jobs shall be distributed to the two servers by a random switch that is modeled by a random -matrix , independent of all other randomness and satisfying the following conditions:

-

(i)

for all , meaning that a job can not be assigned more than totally or less than not at all to a certain server,

-

(ii)

for all , i.e. every job must be assigned entirely to the servers.

The switch matrix is triggered independently at every arrival of a job.

We are interested in the coupled -queues defined by the resulting storage processes of the two servers, i.e.

| (2.1) |

where are i.i.d. copies of and

In particular we aim to study the stationary distribution of the multivariate storage process , that is the distributional limit of as whenever it exists. In this case we write

| (2.2) |

for a generic random vector with this steady-state distribution. Note that here and in the following denotes the transpose of a vector or matrix.

Let be some fixed buffer barrier for the system and with . Set , i.e. . Then we are interested in the probabilities that the single servers exceed their barriers

| (2.3) |

the probability that at least one of the workloads exceeds the barrier

| (2.4) |

and the probability that both of the workloads exceed the barrier

| (2.5) |

2.2 The dual risk model

In the one-dimensional case it is well known that there exists a duality between risk- and queueing models, see e.g. [2]. The multivariate analogue shown in [7] allows us to formulate the dual risk model to the above introduced random switching model as follows.

Let such that is a Poisson process with rate . Define the multivariate risk process

| (2.6) |

where are i.i.d. random matrices, independent of all other randomness, such that

Note that the components of satisfy the net-profit condition, if

| (2.7) |

We will therefore assume (2.7) throughout the paper. Note that as mentioned in [7], (2.7) implies existence of the stationary distribution of , i.e. in (2.2) is well-defined. For a proof of this fact in the univariate setting, see e.g. [31, Thm. 4.10].

For the buffer , in the risk model, we define the ruin probabilities of the single components

| (2.8) |

the ruin probability for at least one component

| (2.9) |

and the ruin probability for all components

| (2.10) |

where as before for with .

The following Lemma allows us to gather information about the bivariate storage process in the switching model by performing calculations on our dual risk model.

Lemma 2.1.

Proof.

Note that in the ruin context it is common (see e.g. [4] or [9]) to consider also the simultaneous ruin probability for all components

| (2.11) |

As we will see, results on can sometimes be shown in analogy to those on and we shall do so whenever it seems suitable. However, has no counterpart in the switching model.

2.3 Further notations

To keep notation short, we write , and for the positive/negative half line of the real numbers, respectively, and likewise use the notations , and such that in particular . Further . For any set we write for its closure, and for its boundary, i.e. .

We write for asymptotic equivalence at infinity, i.e. if and only if , while indicates that such a convergence does not hold. Moreover we use the standard Landau symbols, i.e. if and only if as .

Lastly, throughout the paper we set and , which yields in particular for any tail function .

3 The heavy-tailed case

In this section we will assume that the distribution of the arriving jobs is heavy-tailed. A very general class of heavy-tailed distributions is given by the subexponential distributions, and we will consider this case in Section 3.1 below. However, as we will see, the asymptotics we obtain in this case are not very explicit, in the sense that in a multivariate setting they do not allow for a direct statement about the speed of decay of the exceedance probabilities. We will therefore proceed and treat the more special case of regularly varying distributions in Section 3.2, where speeds of decay can be derived more easily.

3.1 The subexponential case

Recall first that a random variable in with distribution function is called subexponential if

where is the second convolution power of , i.e. the distribution of , where and are i.i.d. copies of . In this case, we write or .

As we are considering a multivariate setting in this paper, our proofs use a concept of multivariate subexponentiality. Several approaches for this exist and we shall rely here on the definition and results as given in [36], which also provides a comprehensive overview of previous notions of multivariate subexponentiality as given in [18, 33].

3.1.1 Results in the risk context

We start by presenting our main theorem in the subexponential setting, which we state in terms of the risk process defined in Section 2.2. Its proof relies on the theory developed in [36] and is given in Section 6.1 below.

Theorem 3.1.

For all set

| (3.1) |

and assume that

| (3.2) |

Further, define a cdf by

| (3.3) |

and assume that , then

| (3.4) |

The asymptotic behavior of the ruin probabilities for single components in the subexponential setting as presented in the next lemma can be shown by classic results. Again a proof is given in Section 6.1.

Lemma 3.2.

Assume that

is subexponential. Then the ruin probability for a single component (2.8) fulfills

| (3.5) |

Lastly we consider the joint ruin probability in the following proposition.

3.1.2 Results in the switch context

With the help of Lemma 2.1 we may now directly summarize our findings from the last section to provide a rather explicit insight into the asymptotic behavior of the workload barrier exceedance probabilities in the switching model defined in Section 2.1.

Corollary 3.4 (Asymptotics of the exceedance probabilities under subexponentiality).

3.2 The regularly varying case

In this section we will restrict the class of considered heavy-tailed distributions and assume that the tail functions of the arriving jobs are regularly varying. As we will see, this restriction leads to a much more explicit description of the asymptotic behavior of ruin and exceedance probabilities.

Let be a measurable function and recall that is regularly varying (at infinity) with index if for all it holds that

with the case typically being referred to as slowly varying. In this case we write . A real-valued random variable is called regularly varying with index , i.e. , if its tail function is regularly varying with index . It is well-known that for all , cf. [3, Prop. X.1.4].

Further we follow [27] and call a random vector on multivariate regularly varying if there exists a non-null measure on such that

-

(i)

,

-

(ii)

for all Borel sets bounded away from ,

-

(iii)

for all Borel sets satisfying it holds that

(3.10)

The norm will typically be chosen to be the -norm in this article. If is multivariate regularly varying, necessarily there exists satifsfying that for all as in (3.10) and it holds that

Thus we write .

Note that in the one-dimensional case the above definitions coincide. We refer to [8] and [35] for references of the above and more detailed information on multivariate regular variation.

3.2.1 Results in the risk context

We will now present our first main result in the regularly varying context. Note that this is not obtained by an application of our above results in the special case of regular variation, but instead we give an independent proof of Theorem 3.5 in Section 6.2 that relies on results from [28]. This approach also allows to consider the simultaneous ruin probability, which had not been possible with the methods used in Section 3.1 due to stronger assumptions on the involved ruin sets.

Theorem 3.5.

Assume the claim size variables are regularly varying, i.e. , and for . Then with , from Section 2 and it follows that there exists a measure such that

Further

| (3.11) |

and

| (3.12) |

with , and .

Note that by conditioning on we have

| (3.13) |

Using the limiting-measure property of it is further possible to explicitely compute the constants , and in Theorem 3.5 above. This then yields the following proposition whose proof is also postponed to Section 6.2.

Proposition 3.6.

Assume , and for and set

such that clearly implies . Then

| (3.14) | ||||

| (3.15) | ||||

and

| (3.16) | ||||

where we interpret .

We continue our study of the asymptotics of the risk model by determining the asymptotic behavior of . It is clear from Equations (2.12) and (3.14) that in order to do this, we first have to determine the asymptotic behavior of the ruin probabilities for single components (2.8), which will be given by the following lemma.

Lemma 3.7.

With this the following proposition is straightforward. Again, the proof can be found in Section 6.2.

3.2.2 Results in the switch context

Again we may now summarize our findings in the context of the switching model defined in Section 2.1 as follows.

Corollary 3.9 (Asymptotics of the exceedance probabilities for regularly varying jobs).

Assume the workload variables are regularly varying, i.e. , and for . Set

such that implies . Recall from (3.15) and the integrated tail functions for servers from (3.8). Then the workload exceedance probabilities (2.3) and (2.4) fulfil

Assuming additionally (3.9) the workload exceedance probability (2.5) fulfills

If (3.9) fails, then

Remark 3.10.

At first sight the structure of the asymptotic formulae for and in the regularly varying and the subexponential case looks pretty similar, as both formulae rely on a minimum inside an integral. However, in the case of regularly varying claims the formulae immediately provide the principal behavior of the tail, only the constant needs more computation. On the contrary, in the subexponential case the initial capital is involved strongly inside the integral and even to obtain the asymptotics up to a constant, one has to calculate the integral explicitely.

Example 3.11.

In the setting of Corollary 3.9 assume that . Then in all asymptotics given in Corollary 3.9 the terms including that are regularly varying with index are dominated by the terms involving which are regularly varying with index . This yields that in this case

as long as . Similarly, since , we obtain

With these observations at hand we may conclude that (3.9) holds if and only if

| (3.19) |

Thus, given (3.19), we get

while otherwise

Remark 3.12.

The above example can be generalized in the sense that a regularly varying tail dominates any lighter tail, no matter whether this is regularly varying as well or not.

Indeed, assuming that w.l.o.g. for and is such that

| (3.20) |

one can prove in complete analogy to the results from the last subsection, that the workload exceedance probabilities (2.3), (2.4), and (2.5) fulfil

and, assuming additionally that (3.9) holds,

while otherwise

4 The light-tailed case

In this section we will study the asymptotic behavior of ruin/workload exceedance probabilities for claims/jobs that are typically small, i.e. we will assume throughout this section that the moment generating functions , , are such that

| (4.1) |

4.1 Results in the risk context

As in the heavy-tailed setting we start by studying the dual risk model. Again, the ruin probabilities for the single components are particularly easy to treat. The following lemma is obtained by a direct application of Lundberg’s well-known inequality and the Cramér-Lundberg approximation, see e.g. [3, Thms. IV.5.2 and IV.5.3]. In Section 6.3 a short proof is provided.

Lemma 4.1.

Assume the claim size variables fulfill(4.1) and assume there exist (unique) solutions to

| (4.2) |

Then the ruin probabilities of the single components fulfil

where

| (4.3) |

Using (2.12) in the form we easily derive the following Lundberg-type bound for from the above Lemma.

Corollary 4.2.

Remark 4.3.

Similarly to what has been done in [9, Thm. 6.1] it is also possible to derive a Lundberg bound for via classical martingale techniques. Indeed one can show that for any such that

it holds that

As this has no implications for the considered queueing model we will not go into further details here.

To derive the asymptotics of , and we rely on results from [4], which lead to the following Theorem.

4.2 Results in the switch context

Again, using Lemma 2.1 we summarize our findings from the last subsection to obtain the following corollary on the asymptotic behavior of the workload barrier exceedance probabilities in the switching model defined in Section 2.1.

Corollary 4.5 (Asymptotics and bounds of the exceedance probabilities for light-tailed jobs).

Assume the workload variables are light-tailed such that (4.1) holds and assume there exist (unique) solutions to (4.2). Then the workload exceedance probabilities (2.3), (2.4), and (2.5) fulfil

Further, with as in (4.3), it holds

| (4.4) |

while the probability that both workloads exceed their barrier fulfills

Remark 4.6.

Note that the light-tail assumption (4.1) does not necessarily imply existence of solving (4.2). Assuming for the slightly stronger condition

Either

or there exists such that

however is sufficient for existence of .

In case that the above condition fails, i.e. for some there exists such that for all and for all , then existence of depends on the chosen parameters of the model; see e.g. [3, Chapter IV.6a] for a more thorough discussion of this.

Remark 4.7.

If then the summand of lower order on the right hand side of (4.4) can be omitted in the asymptotic equivalence. Thus, in contrast to the regularly varying case, the vector here is crucial for the exact asymptotic behavior and contributes more than just inside the constant.

On the other hand we immediately see that, given two job distributions and hence given , we can choose in order to minimize the joint exceedance probabilities. The optimal then solves

which leads to

5 Examples and simulation study

In this section we consider two special choices of the random switch for which we will evaluate the above results and compare to simulated data. The first part is dedicated to the special case of the Bernoulli switch, where the queueing processes become independent of each other. In the second part we discuss the special case of a non-random switch, where every job is shared between the servers with some predefined deterministic proportions. We finish in Section 5.3 with a short comparison to study the influence of the chosen type of randomness on the exceedance probabilities.

5.1 The Bernoulli switch

The Bernoulli switch does not split any jobs, but assigns the arriving jobs randomly to one of the two servers. More precisely we set

independent of each other with . This yields independence of the components of the process which can now be represented as

where and are independent copies of , , , and the counting processes , , , and are independent Poisson processes with rates , , , and , respectively. In particular from (2.5) and (2.13) we obtain in the Bernoulli switch

| (5.1) |

and hence and can be expressed in terms of , and . Thus, although the Bernoulli switch is not covered by Theorem 3.1 in the subexponential setting, as (3.2) is not fulfilled, via (5.1) one can still calculate the asymptotics using Lemma 3.2.

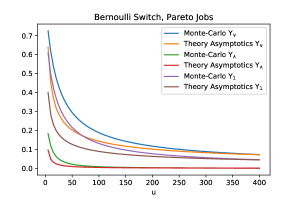

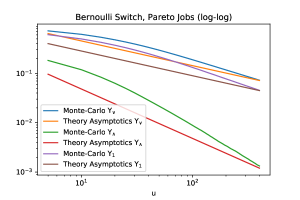

Here job sizes are Pareto distributed with , , and , . Further , , , and . The Bernoulli switch is characterized by and . For these parameters from (5.2) we derive and such that and via (5.1).

Note that a direct evaluation of the asymptotics of as given in Corollary 3.9 yields the same result.

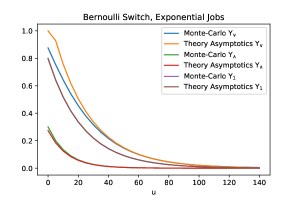

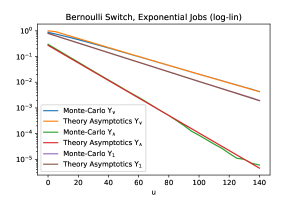

Here jobs are exponentially distributed with , , and , . Further , , , and . The Bernoulli switch is characterized by and . For these parameters from (5.4) we derive and and (5.3) yields and from which and via (5.1). Note that in the latter case we keep both summands, since the exponents are close together.

Indeed we obtain by direct application of Corollary 3.4 that if (which holds in particular if , , )

| (5.2) | ||||

In the light-tailed case an application of Corollary 4.5 yields

| (5.3) | ||||

as long as there exist such that (4.2) holds, which in the Bernoulli switch simplifies to

| (5.4) | ||||

The asymptotic behavior of and can now be described via (5.1).

5.2 The deterministic switch

The deterministic switch is characterized by setting

for some predefined constants .

Note that for , meaning that we have only one source of claims, the corresponding dual risk model coincides with the degenerate model considered in [4, 5, 24]. Allowing two sources of claims, but setting , reduces our model to the setting treated in [6].

Clearly, for any choice of in the deterministic switch one can easily evaluate the asymptotics of the exceedance probabilities as given in Corollaries 3.4 , 3.9, and 4.5 since all appearing expectations disappear.

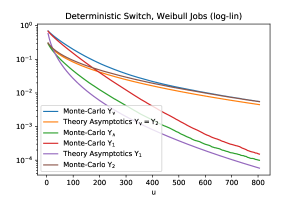

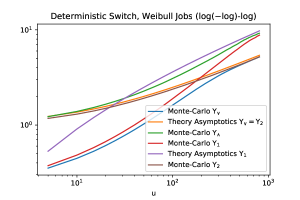

Job sizes are Weibull distributed with , , and , . Further , , , and . The deterministic switch is characterized by and . For these parameters from Corollary 3.4 we derive , and , while for no asymptotics are given as (3.9) fails.

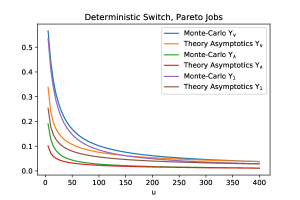

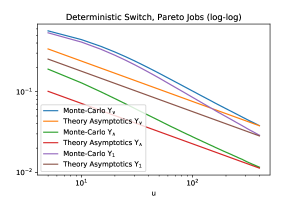

Here - as in Figure 2 - job sizes are Pareto distributed with , , and , . Further , , , and . The deterministic switch is characterized by and . For these parameters from Corollary 3.9 we derive , and , while , and .

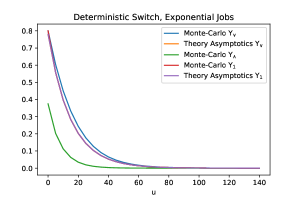

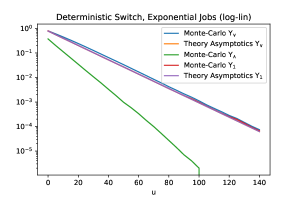

Here jobs are - as in Figure 3 - exponentially distributed with , , and , . Further , , , and . The deterministic switch is characterized by and . For these parameters from (4.2) we obtain and , which yield and , while and by Corollary 3.9.

In Figures 4, 5, and 6 we compare the asymptotics and bounds in the deterministic switch obtained in this way with data that has been simulated using standard Monte-Carlo techniques. Again simulations and theoretical asymptotics fit well in all cases. Note that in contrast to the cases with lighter tails, in the purely subexponential case depicted in Figure 4 we observe that is close to for small , but close to for large . This can be interpreted as follows. While for small the net working speed determines the exceedance probabilities, for large this becomes less relevant and the workload exceedance is mainly influenced by the heavyness of the tails.

Example 5.1.

Consider a deterministic switch with and , i.e. there is only one source of jobs and the jobs are distributed deterministically to the two servers with proportions and , and assume that , such that the resulting dual risk model properly rescaled coincides with the degenerate model studied in [4, 5, 24]. Then, applying Theorem 3.1 in this setting reproduces the tail behavior of the probability of ruin of at least one component stated in [24, Cor. 2.2]. Interestingly, also the ruin probability of both insurance companies one derives in this case from Proposition 3.3 coincides with the asymptotics provided in [24, Eq. (2.9)], although the latter corresponds to simultaneous ruin. This suggests that in this special setting the ruin probability of both components and the simultaneous ruin probability of both components are asymptotically equivalent.

5.3 A comparison of different switches

In this section we aim to compare the two above special cases of the Bernoulli switch and the deterministic switch with a non-trivial random switch, which we chose to be a Beta switch characterized by setting

for some constants , where is the Beta distribution with density , .

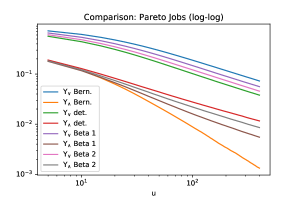

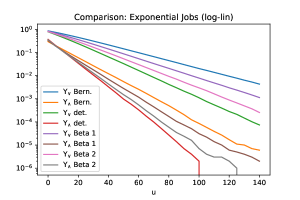

To keep all examples comparable, we fix , , , , and such that the scenarios only differ in the behavior of the switch and the job sizes. Figure 7 shows the approximate exceedance probabilities obtained by Monte Carlo simulation for the Bernoulli switch, the deterministic switch und two different Beta switches.

Throughout , , , and . On the left - as in Figures 2 and 5 - job sizes are Pareto distributed with , , and , . On the right jobs are - as in Figures 3 and 6 - exponentially distributed with , , and , . The Bernoulli switch is characterized by and , the deterministic switch is characterized by and , the Beta switch 1 is characterized by and , and the Beta switch 2 is characterized by and .

As we can see, in the regularly varying case the probability that at least one of the workloads exceeds the barrier tends to zero with the same index of regular variation for all choices of the random switch. In case of the probability that both components exceed their barrier , the Bernoulli switch yields a faster decay due to the independence of the two workload processes in this model.

Further, the figure indicates the intuitive behavior: The more correlated the co-ordinates of the workload process are, the closer together are and . This leads to a trade-off between the two probabilities: Changing the switch towards reducing one probability raises the other and the Beta switches may serve here as a compromise to control both probabilities.

In the light-tailed case the trade-off between and can not be observed. Quite the contrary, the more correlated the co-ordinates of the workload process are, the lower tend to be the exceedance probabilities. Hence in this case the Bernoulli switch yields the highest exceedance probabilities, while the deterministic switch obtains the best results.

Thus, for keeping small, in general the simple deterministic switch yields good results. On the contrary, if one is interested to keep small, the tail-behavior of the appearing jobs is crucial for the choice of the optimal switch. Here again Beta switches or other non-trivial random switches may serve as a compromise in situations where the tail-behavior of the appearing jobs is unknown.

6 Proofs

6.1 Proofs for Section 3.1

To prove the asymptotic result for the ruin probability as given in Theorem 3.1 we need some preliminary definitions and results.

Let

be a family of open sets, where increasing means, that for each and we have . Let be a probability measure on . For we define a cdf on by setting

Then, following [36, Def. 4.6], if we say that . Furthermore is multivariate subexponential, if .

Throughout this section we consider the specific sets

| (6.1) |

Then clearly and by [36, Rem. 4.1] also for all .

Moreover, we specify to be the probability measure of the claims in the dual risk model described in Section 2.2. Then we can prove some basic relationships in the upcoming lemma.

Lemma 6.1.

Proof.

By definition of , and and conditioning on

where for

which proves the first equation. The second equation follows by an analogue computation.

Lastly, using the obtained expression for we may compute using Tonelli’s theorem

where for

This proves . Moreover we note that the finite mean of the claim sizes implies finiteness of . ∎

Proof of Theorem 3.1.

Recall the definition of the set in (6.1) and note that obviously satisfies [36, Assumption 5.1]. Furthermore note that if and only if , which immediately implies that

Thus, by [36, Thm. 5.2] we obtain

| (6.2) |

as soon as we can guarantee that the probability measure on defined by

and , is in . This however is by definition equivalent to the assumption that the cdf , , is in . Since by Lemma 6.1 with as given in (3.3), this is assumed in the theorem. Lastly, observe that the right hand side of (6.2) equals as shown in Lemma 6.1. ∎

Remark 6.2.

Naively one could guess that subexponentiality of the claims and should be enough to obtain subexponentiality of at least . However, as noted in [36, Remark 4.9] this is not true in general, because random mixing of two subexponential distributions (as done by our matrix ) leads to a subexponential distribution if and only if the sum of the mixed distributions is subexponential. This again is not true in general.

Proof of Lemma 3.2.

Fix and assume that Otherwise is monotonely decreasing, , and the statement is proven. Note that by definition

where the random variables are i.i.d. copies of two generic random variables , . The corresponding integrated tail function is defined as

From [3, Thm. X.2.1] we obtain that if

| (6.3) |

where

| (6.4) |

such that

Further

and since by Tonelli’s theorem for all

this proves . Inserting everything in (6.3) we obtain

which immediately yields the result by (2.7) via substitution with . ∎

6.2 Proofs for Section 3.2

Proposition 6.3.

Let be a random vector in and let be a random -matrix independent of . Let

where denotes the preimage under . If for some and then with

where denotes the complement of the unit sphere in .

Proof.

Lemma 6.4.

Proof.

Obviously for some non-null measure concentrated on the axes, and since the random variables are independent and both regularly varying with indices . To prove the Lemma it is thus enough to check the prerequisites of Proposition 6.3. Clearly, using the properties of and we compute for any . Further for measurable and bounded away from

Thus for and recalling property (ii) of the matrix we obtain

where we have used that, due to positivity of , is zero on . This finishes the proof. ∎

To prove the remainder of Theorem 3.5 we will use a result from [28]. To do so, first recall the bivariate compound Poisson process from our dual risk model from Section 2.2. Let be the independent identically -distributed interarrival times of the Poisson process , i.e.

We define the random walk

| (6.5) |

and directly observe that is compensated, i.e. for all

| (6.6) |

The following Lemma explains the relationship between the risk process and the random walk .

Lemma 6.5.

Let be a ruin set, i.e. assume that

-

(i)

, i.e., , and

-

(ii)

for all .

Then

Proof.

Recall from (2.6) that where . Thus by assumption (i) may enter only by a jump and since a.s. we get

which yields the claim. ∎

We proceed with a Lemma that specifies the ruin sets that we are interested in.

Lemma 6.6.

Let

then

Proof.

Clearly

which is . The second equality follows analogously. ∎

Proposition 6.7.

Proof.

The following Lemma justifies the usage of Proposition 6.7 for our problem.

Lemma 6.8.

Proof.

Properties (i), (ii) and (iv) are obvious. Consider (iii). Fix an arbitrary . It holds that

and we have

Set

such that . Now consider the set . Let , then

Thus for we have . Further the set is obviously bounded away from zero, since . We thus obtain

Since the last sum is infinite, must be zero. The same argument applied to thus yields the result for . The proof for is analogue. ∎

Proof of Theorem 3.5.

For the proof of Proposition 3.6 we will use the following lemma.

Lemma 6.9.

Let be regularly varying with indices and set

for , such that clearly implies . Then for any constants

where we interpret .

Proof.

Obviously it holds that

Proof of Proposition 3.6.

We concentrate first on the -case and start by determining the constant . Using the limiting-measure property of , (3.13) and the properties of and we obtain

Now recall that which yields

Hence

A similar computation for thus leads to

where denotes the probability measure induced by and denotes the set of all possible realisation of . Hereby the second equality has been obtained by conditioning on while the last equality follows from Lebesgue’s theorem of dominated convergence. Note that Lebesgue’s theorem is applicable since

and thus there exists independent of the realisation such that for all the integrand is smaller than

which, as a constant (with respect to ), is clearly -integrable.

By Tonelli’s theorem we thus obtain

Applying Lemma 6.9 now yields (3.14).

The proof of (3.16) can be carried out in complete analogy.

∎

Proof of Lemma 3.7.

It is enough to prove that under the present assumptions also the assumption of Lemma 3.2 is fulfilled. Hence, we need to show that for implies that . Recall and from the proof of Lemma 3.2 and assume for the moment, that neither a.s., nor a.s. Then, using Proposition 6.3 and the same argumentation as in the proof of Lemma 6.4 we obtain that . Thus the corresponding tail functions of the integrated tail functions are regularly varying as well, with index , which implies . If a.s. then and clearly which again implies . ∎

Proof of Proposition 3.8.

Assume (3.6) holds true. From Lemma 3.7 and its proof we obtain directly as

where the first two terms on the right hand side are regularly varying with index , while the latter two terms are regularly varying with index .

Together with (3.11), (3.13) we thus obtain that as

where (3.6) ensures that terms with the same index of regular variation do not cancel out asymptotically. Using Tonelli’s theorem as in the proof of Lemma 3.7 this yields

and hence (3.17) by substituting . If (3.6) fails, then the statement follows in analogy to the proof of Proposition 3.3. ∎

6.3 Proofs for Section 4

Proof of Lemma 4.1.

We take up the notation used in the proof of Lemma 3.7 and denote the jumps of the resulting one-dimensional risk processes by , . Then the given bound for follows from [3, Thm. IV.5.2] with such that . (Note that in [3] the constants and are combined as .) But since by conditioning

this is equivalent to (4.2).

Further by [3, Thm. IV.5.3] it holds

with as given in (6.4) and

where, again by conditioning,

which yields the given asymptotics. ∎

Proof of Theorem 4.4.

Recall from Section 2.2 that

such that the joint cumulant exponent of the two-dimensional Lévy process can be determined via conditioning first on , then on the components of , as

which is by assumption (4.1) well defined on some set . The first two statements thus follow from [4, Thm. 3], as long as there exist , such that and , the interior of . But since

we observe that which exists and is such that by assumption. Likewise we obtain with .

The last equation now follows directly from the fact that .

∎

References

- [1] I. Adan, O. J. Boxma, and J. Resing. Queueing models with multiple waiting lines. Queueing Systems, 37:65–98, 2001.

- [2] S. Asmussen. Applied Probability and Queues. Springer, 2nd edition, 2003.

- [3] S. Asmussen and H. Albrecher. Ruin probabilities. World Scientific, 2nd edition, 2010.

- [4] F. Avram, Z. Palmowski, and M. Pistorius. Exit problem of a two-dimensional risk process from the quadrant: Exact and asymptotic results. Ann. Appl. Probab., 18:2421–2449, 2008.

- [5] F. Avram, Z. Palmowski, and M. Pistorius. A two-dimensional ruin problem on the positive quadrant. Insurance Math. Econom., 42:227–234, 2008.

- [6] A.L. Badescu, E. C. K. Cheung, and L. Rabehasaina. A two-dimensional risk model with proportional reinsurance. J. Appl. Probab., 48(3):749–765, September 2011.

- [7] E. S. Badila, O. J. Boxma, J. A. C. Resing, and E. M. M. Winands. Queues and risk models with simultaneous arrivals. Adv. in Appl. Probab., 46(3):812–831, 2014.

- [8] B. Basrak. The sample autocorrelation function of non-linear time series. PhD thesis, University of Groningen, 2000. available on https://www.rug.nl/research/portal/files/3142993/thesis.pdf.

- [9] A. Behme, C. Klüppelberg, and G. Reinert. Ruin probabilities for risk processes in a bipartite network. Stoch. Models, 36:548–573, 2020.

- [10] O. Boxma and J. Ivanovs. Two coupled Levy queues with independent input. Stochastic Systems, 3(2):574–590, 2013.

- [11] O. J. Boxma and G. J. van Houtum. The compensation approach applied to a 2 2 switch. Probability in the Engineering and Informational Sciences, 7(4):471–493, 1993.

- [12] Y. Bregman and C. Klüppelberg. Ruin estimation in multivariate models with Clayton dependence structure. Scand. Act. Journal, 2005(6):462–480, 2005.

- [13] J. Cai and H. Li. Multivariate risk model of phase type. Insurance Math. Econom., 36(2):137–152, 2005.

- [14] W. Chan, H. Yang, and L. Zhang. Some results on ruin probabilities in a two-dimensional risk model. Insurance Math. Econom., 32(3):345–358, 2003.

- [15] Y. Chen, L. Wang, and Y. Wang. Uniform asymptotics for the finite-time ruin probabilities of two kinds of nonstandard bidimensional risk models. J. Math. Anal. Appl., 401(1):114–129, 2013.

- [16] Y. Chen, Y. Wang, and K. Wang. Asymptotic results for ruin probability of a two-dimensional renewal risk model. Stoch. Anal. Appl., 31(1):80–91, 2013.

- [17] Y. Chen, K.C. Yuen, and K.W. Ng. Asymptotics for the ruin probabilities of a two-dimensional renewal risk model with heavy-tailed claims. Applied Stochastic Models in Business and Industry, 27(3):290–300, 2010.

- [18] D. Cline and S. Resnick. Multivariate subexponential distributions. Stochastic Process. Appl., 42:49–72, 1992.

- [19] J. W. Cohen. On the asymmetric clocked buffered switch. Queueing Systems, 30(3/4):385–404, 1998.

- [20] J.F. Collamore. First passage times of general sequences of random vectors: A large deviations approach. Stochastic Process. Appl., 78(1):97–130, 1998.

- [21] L. Dang, N. Zhu, and H. Zhang. Survival probability for a two-dimensional risk model. Insurance Math. Econom., 44(3):491–496, 2009.

- [22] K. Debicki and M. Mandjes. Queues and Lévy Fluctuation Theory. Springer, 2015.

- [23] L. Flatto and S. Hahn. Two parallel queues created by arrivals with two demands I. SIAM Journal on Applied Mathematics, 44(5):1041–1053, 1984.

- [24] S.G. Foss, D. Korshunov, Z. Palmowski, and T. Rolski. Two-dimensional ruin probability for subexponential claim size. Probab. Math. Statist., 37, 2017.

- [25] L. Gong, A.L. Badescu, and E.C.K. Cheung. Recursive methods for a multi-dimensional risk process with common shocks. Insurance Math. Econom., 50(1):109–120, 2012.

- [26] Z. Hu and B. Jiang. On joint ruin probabilities of a two-dimensional risk model with constant interest rate. J. Appl. Probab., 50(2):309–322, 2013.

- [27] H. Hult and F. Lindskog. Heavy-tailed insurance portfolios: buffer capital and ruin probabilities. Technical Report 1441, School of ORIE, Cornell University, 2006.

- [28] H. Hult, F. Lindskog, T. Mikosch, and G. Samorodnitsky. Functional large deviations for multivariate regularly varying random walks. Ann. Appl. Probab., 15:2651–2680, 2005.

- [29] T. Jiang, Y. Wang, Y. Chen, and H. Xu. Uniform asymptotic estimate for finite-time ruin probabilities of a time-dependent bidimensional renewal model. Insurance Math. Econom., 64:45–53, 2015.

- [30] D.G. Konstantinides and J. Li. Asymptotic ruin probabilities for a multidimensional renewal risk model with multivariate regularly varying claims. Insurance Math. Econom., 69:38–44, 2016.

- [31] A. E. Kyprianou. Fluctuations of Lévy processes with Applications. Springer, 2nd edition, 2014.

- [32] J. Li, Z. Liu, and Q. Tang. On the ruin probabilities of a bidimensional perturbed risk model. Insurance Math. Econom., 41(1):185–195, 2007.

- [33] E. Omey. Subexponential distribution functions in . J. Math. Sci., 138:5434–5449, 2006.

- [34] S. Ramasubramanian. A multidimensional ruin problem. Commun. Stoch. Anal., 6(1):33–47, 2012.

- [35] S. Resnick. Heavy-Tail Phenomena. Springer, 2007.

- [36] G. Samorodnitsky and J. Sun. Multivariate subexponential distributions and their applications. Extremes, 19(2):171–196, 2016.

- [37] H. Yang and J. Li. Asymptotic finite-time ruin probability for a bidimensional renewal risk model with constant interest force and dependent subexponential claims. Insurance Math. Econom., 58:185–192, 2014.

- [38] K.C. Yuen, J. Guo, and X. Wu. On the first time of ruin in the bivariate compound poisson model. Insurance Math. Econom., 38(2):298–308, 2006.