Markovian approximation of the rough Bergomi model for Monte Carlo option pricing

Abstract

The recently developed rough Bergomi (rBergomi) model is a rough fractional stochastic volatility (RFSV) model which can generate more realistic term structure of at-the-money volatility skews compared with other RFSV models. However, its non-Markovianity brings mathematical and computational challenges for model calibration and simulation. To overcome these difficulties, we show that the rBergomi model can be approximated by the Bergomi model, which has the Markovian property. Our main theoretical result is to establish and describe the affine structure of the rBergomi model. We demonstrate the efficiency and accuracy of our method by implementing a Markovian approximation algorithm based on a hybrid scheme.

Keywords: rough fractional stochastic volatility, forward variance model, Markovian representation, volatility skew, Volterra integral, rough Heston, hybrid scheme simulation

MSC codes: 60H35; 65C30; 91G20; 91G60; 65C05; 62P05;

JEL codes: C63; C15; C52; G13; G12; C02

ACM codes: G.3; I.6.1; F.2.1; G.1.2; I.6.3; G.1.10;

1 Introduction

The rough Bergomi (rBergomi) model introduced by Bayer et al., (2016) has gained acceptance for stochastic volatility modelling due to its power-law at-the-money volatility skew which is consistent with empirical studies (see Forde and Zhang, 2017, Fukasawa, 2017, Gatheral et al., 2018) and the market impact function under the no-arbitrage assumption (see Jusselin and Rosenbaum, 2018). However, the stochastic process which characterizes this volatility model is rougher than that of a Brownian motion; in particular, the lack of Markovianity makes classical pricing methods infeasible.

In order to price options under an rBergomi model and calibrate such a model, Bayer et al., (2018) propose hierarchical adaptive sparse grids for option pricing, Bayer et al., (2019) propose a deep learning method for rBergomi model calibration, Jacquier et al., (2018) develop pricing algorithms for VIX futures and options, and McCrickerd and Pakkanen, (2018) develop a ‘turbocharged’ Monte Carlo pricing method. In spite of these efforts, the inherent challenges brought by the rBergomi model still prevent its widespread adoption in industry.

Inspired by the technique from Abi Jaber and El Euch, (2019), Gatheral and Keller-Ressel, (2019) and Harms and Stefanovits, (2019), in which the authors design a multi-factor stochastic volatility model with Markovian structure to approximate the rough Heston model, we establish an analogous multi-factor affine structure for the rBergomi model. In the affine structure, the Volterra kernel corresponds to a superposition of infinitely many Ornstein-Uhlenbeck (O-U) processes with different speeds of mean reversion. Truncating this infinite sum into a finite sum of O-U processes yields an approximation of the rBergomi model which is a Markovian approximated Bergomi (aBergomi) model. We then prove the existence and uniqueness of solutions to this affine aBergomi model, and show that its affine structure converges to the one of the rBergomi model.

To numerically simulate the rBergomi model in practice, we adopt the hybrid scheme proposed in Bennedsen et al., (2017) for the stochastic Volterra-type integrals (). The hybrid scheme consists in approximating the power-law kernel by a combination of a power function near zero and a step function elsewhere, with a lower complexity, where is the number of time steps, as opposed to the complexity of the Cholesky method in Bayer et al., (2016). Here, the rBergomi power-law kernel can be approximated by the exponential kernel after truncating before . Our numerical tests demonstrate that using exponential terms in (i.e. a 25-term O-U process), we can obtain an accurate (low root mean squared error), yet tractable and computationally efficient approximation of the fractional rBergomi model.

The paper is organized as follows. In Section 2, we introduce the Bergomi and rBergomi models and discuss their respective ATM volatility skews. In particular we provide for the first time a proof that the ATM volatility skew of the rBergomi model is equivalent to the power while this does not hold for the Bergomi model (equation (8)). In Section 3, we establish the affine structure of the rough Bergomi model. Section 4 is dedicated to the approximation of the rough Bergomi model by a multi-factor Bergomi model. Finally, Section 5 compares numerical simulations of the rBergomi model with our approximated Bergomi (aBergomi) model with a finite number of terms, showing the effectiveness of our approximation.

2 Bergomi and rough Bergomi models

This section introduces the Bergomi and rough Bergomi stochastic volatility models (Definitions 2 and 1), along with the corresponding notations used throughout the paper.

We consider a filtered probability space , which supports two dimensional correlated Brownian motions and . A log price process is assumed to follow the dynamics

| (1) |

where is the instantaneous spot variance process. Let be the instantaneous forward variance for date observed at time ; in particular corresponds to the spot variance.

Bayer et al., (2016) proposed the so-called rough Bergomi model where the forward variance follows

| (2) |

where and have correlation , is a negative exponent depending on the Hurst exponent of the underlying fractional Brownian motion, and is a positive parameter depending on . The definition of the rBergomi model is summarized below:

Definition 1.

The rBergomi stochastic volatility model takes the form

| (3) |

where , and .

By contrast, the two-factor Bergomi model is defined as follows.

Definition 2.

Assumption 1.

Without loss of generality, we assume throughout the paper that the initial forward variance curve is flat. This simplification is common in the rBergomi literature, see for example Bayer et al., (2016), Bayer et al., (2018) and Bayer et al., (2019). We use the notation for the constant initial forward variance curve.

2.1 ATM volatility skew

This subsection derives the ATM volatility skew of the rBergomi and Bergomi models, as the more realistic ATM volatility skew of the rBergomi model over the Bergomi model is one of the motivations behind the introduction of the rBergomi model.

From Bergomi and Guyon, (2012), we can define the price and the volatility dynamics of a generic stochastic volatility model as follows:

| (5) |

where in particular note that is the log-spot, is the instantaneous spot variance, is the instantaneous forward variance for date observed at time , and is the volatility of forward instantaneous variances which takes values in where is the dimension of the Brownian motion . Note that in this formulation, the covariance between spot and variance is modelled through the first component of , see Bergomi and Guyon, (2012) for more details.

One can derive the following second-order expression (w.r.t. volatility of volatility) for the Black-Scholes implied volatility:

| (6) |

where , is the strike and is a dimensionless scaling factor for the volatility of variances. The ATM volatility and the two coefficients and are given by

where is the total variance to expiration , is the effective volatility, and are autocorrelations (Bergomi and Guyon,, 2012):

-

•

is the doubly integrated spot-variance covariance function

-

•

-

•

is the triply integrated variance/variance covariance function

-

•

.

-

•

is the double time-integral of the instance spot variance covariance function times the sensitivity of with respect to instantaneous forward variances

-

•

.

2.1.1 ATM volatility skew in the rBergomi model

Theorem 1.

In the rBergomi model (3), the ATM volatility skew satisfies

| (7) |

Proof.

We first explicit the autocorrelation functional in the rBergomi model. Using the fact that , the autocorrelation functionals and are given by

Then, using the fact that

we obtain

Therefore, using Assumption 1, we obtain the following explicit first-order approximation:

where is a constant depending on . We are then able to compute the first-order approximations of the three correlation values explicitly. The first-order approximation of can be written as follows:

Thus, the ATM volatility skew generated by the rBergomi model satisfies Equation 7, which is consistent with empirical evidence (see for example, Gatheral et al., (2018)). ∎

2.1.2 ATM volatility skew in the two-factor Bergomi model

We now compare this result to the volatility skew in the classical two-factor Bergomi model.

Theorem 2.

In the two-factor Bergomi model , the ATM volatility skew satisfies

| (8) |

Proof.

The Brownian motions can be decomposed as:

where are three independent Brownian motions and . Thus the volatilities of variance in the general formulation (5) can be written as:

or equivalently:

where

The corresponding covariances can be expressed similarly as:

Using once again Assumption 1, we obtain

where

and

Similarly, we have , where the coefficients

and

Since and are constants, we can derive the term structure of the ATM volatility skew as in equation (8) with first order in . ∎

However, this result derived for the Bergomi model by the Bergomi-Guyon expansion (Bergomi and Guyon,, 2012) is inconsistent with empirical evidence, see for example Bayer et al., (2016). This suggests that the power-law kernel of the forward variance curve in the rBergomi model will lead to more realistic and accurate pricing and hedging results than the exponential kernel of the forward variance curve in the Bergomi model.

3 Markovian representation of the rough Bergomi model

The purpose of this section is to establish the infinite-dimensional affine nature and Markovianity of the rBergomi model.

Definition 3.

An Ornstein-Uhlenbeck (O-U) process is the solution of the following stochastic differential equation (SDE):

| (9) |

where is the mean-reversion speed, is the mean-reversion level, and is a standard Brownian motion. Its strong solution is explicitly given by

| (10) |

Assumption 2.

Definition 4.

Without loss of generality, we define the sigma-finite measure on as .

3.1 Volterra-type integral as a functional of a Markov process

Theorem 3.

Proof.

the Laplace transform of the measure in Definition 4 is

which can be recognised as the power-law kernel in the Volterra type integral. Consequently, we have , and using Fubini’s stochastic theorem (Protter,, 2005), we obtain . From Definition 3, where , we obtain the Markovian representation given by equation 13. ∎

Theorem 4.

The O-U process (10) has the affine structure

Proof.

From Fubini’s stochastic theorem, is Gaussian under the filtration for , with mean

Furthermore, using Itō’s isometry, we have the conditional variance:

Thus

∎

3.2 Affine structure in the rBergomi model

From Definition 1 and Theorem 3, the rBergomi model can be rewritten in the following form:

where is the log stock price, is the initial flat forward variance curve, and are two Brownian motions with correlation and .

Our aim is now to write the log stock price in affine form as the first coordinate of an infinite-dimensional affine process. To do so, we introduce the following symmetric nonnegative tensor:

Let . The relation holds.

Therefore, the log stock price dynamics can be written as

where is the Doléans-Dade stochastic exponential.

Theorem 5.

The process satisfies the affine structure

| (14) |

where

| (15) | ||||

| (16) |

Proof.

From Fubini’s stochastic theorem, is Gaussian under the filtration for , with conditional mean

and conditional variance

Then, the random variable defined as

is a noncentral distribution with one degree of freedom and noncentrality parameter

Corollary 1.

The rBergomi model is an infinite-dimensional Markovian process.

Proof.

This corollary follows from Theorem 5 which exhibits that the rBergomi model has an exponential-affine dependence on , hence the model is Markovian in each dimension. ∎

4 Approximation of the rough Bergomi model by the aBergomi model

In this Section, we first introduce the aBergomi model which is used to approximate the rBergomi model (3). After that, we will demonstrate the existence and uniqueness of the solution of this aBergomi model. We also prove that the aBergomi model is well-defined and the solution of the aBergomi model converges to that of the rBergomi model when the number of terms in the aBergomi model goes to infinity. At the same time, we show that the rBergomi model inherits the affine structure of the Bergomi model.

Since the rBergomi model can be represented by

and the -term Bergomi model with the same Brownian motion in the variance process can be represented by

| (17) |

we can view the rBergomi model as a continuous infinite-term Bergomi model under the measure , in which the mean-reversion speed has been integrated from to , with the Brownian motion . We can therefore approximate the rBergomi model by a -term exponential kernel instead of the power kernel of the Volterra process in the rBergomi model.

Following equation (17), after approximating the exponential kernel by the kernel , we can rewrite the aBergomi model (17) as follows:

| (18) |

where are positive weights, are mean-reverting speeds, and , with initial conditions and .

4.1 Existence and uniqueness of

We rewrite in (18) as the following stochastic equation

| (19) |

Theorem 6.

Proof.

Then the strong existence and uniqueness of follows, along with its Markovianity w.r.t. the spot price and the factors for .

4.2 Convergence of to

To prove that the solution of the aBergomi model converges to the solution of the rBergomi model , we need to choose a suitable to approximate . When , (see Carmona et al., 2000, Muravlev, 2011, Harms and Stefanovits, 2019).

Theorem 7.

There exist weights and mean reversion speeds , such that , where is the norm.

The proof of this theorem is in the Appendix.

Applying the previous computations and the Kolmogorov tightness criterion, we can get that the sequence is tight for the uniform topology and the limit satisfies the model (18).

4.3 Affine structure of the aBergomi model

In this section, we detail the affine property of the aBergomi model.

Theorem 8.

The process (equation (19)) has the following affine structure

5 Numerical method

In this section, we first introduce the hybrid scheme and algorithm to approximate an rBergomi model by an aBergomi model. And then, we compare the simulated volatilities of both models. To demonstrate the approximation accuracy and efficiency, we investigate the RMSE of simulated results for different number of terms and number of time steps in numerical tests. By some improved algorithms, we observe that 25-term O-U process and 100 time steps can produce a good output, with reliable outcomes and fast calculation speed under 20000 Monte Carlo paths.

5.1 Hybrid scheme for simulation

Recalling equation (3), the rough Bergomi model with time horizon under an equivalent martingale measure identified with can be written as:

| (20) |

where are two standard Brownian motions with correlation . We recall Assumption 1 that the forward variance curve is flat for all : Thus, the spot variance in Equation (20) is given by

To simulate the Volterra-type integral , we apply the hybrid scheme proposed in Bennedsen et al., (2017), which approximates the kernel function of the Brownian semi-stationary processes by a Wiener integrals of the power function at and a Riemann sum elsewhere.

Let be a filtered probability space which supports a standard Brownian motion . We consider a Brownian semi-stationary process (Bss):

| (21) |

where is an -predictable process which captures the stochastic volatility of and is a Borel-measurable kernel function. We assume that for all and the process is covariance-stationary, namely

These assumptions imply that is covariance-stationary. However, the process need not be strictly stationary.

Assumption 3.

The assumptions concerning the kernel function are as follows:

- (A1)

-

For some ,

where is continuously differentiable, slowly varying at 0 and bounded away from 0. Moreover, there exists a constant such that the derivative of satisfies

- (A2)

-

The function is continuously differentiable on , with derivative that is ultimately monotonic and also satisfies .

- (A3)

-

For some ,

In order to implement the hybrid scheme to the rBergomi model, we need to introduce a particular class of non-stationary processes, namely truncated Brownian semi-stationary (tBss) processes,

| (22) |

where the kernel function , the volatility process and the driving Brownian motion are as defined in the definition of Bss processes. can also be seen as the truncated stochastic integral at of the Bss process . Equation (22) is integrable since is differentiable on .

5.2 Algorithm for hybrid scheme

Now, we can discretise equation (22) in time. Let be the total number of time steps, be the time step size, and be a time grid on the interval .

According to Bennedsen et al., (2017), the observations can be computed via ( case)

| (23) |

using the random vectors the random variables where , and the random vectors (see Proposition 2.8 in Bennedsen et al., 2017).

To simulate the Volterra process , we use:

then,

The related matrix representation takes the form of

| (24) |

In the rBergomi model, is a constant for

defined in equation (18). When simulating

, we need to perform a matrix multiplication, the

computational complexity of which is of order

when using the conventional matrix multiplication algorithm. However,

multiplying a lower triangular Toeplitz matrix can be regarded as

a discrete convolution which can be evaluated efficiently by fast

Fourier transform. Therefore the computational complexity can be reduced

to . The algorithm to simulate the

Volterra process is described in Algorithm 1.

Then we can use a standard Euler scheme to simulate the price .

Below we give a simulation of the stock price in the rBergomi model in Fig.LABEL:fig:compre (see Algorithm 2). The parameters are listed in Table 1.

| 0.026 | |

| 1.9 | |

| -0.43 |

5.3 Approximation of the kernel

For sake of simplicity, we start with deriving the approximation of the rBergomi model with 2 terms. It works in the same way when terms number is bigger than 2. The 2-term Bergomi model (4) that we used to approximate the rBergomi model is given as follows.

| (25) |

where . Here, we introduce the process defined as

| (26) |

where are from the exponential kernel , and and are two O-U processes. Hence the process can be written as a driftless Gaussian process as follows:

and its quadratic variation is where . The forward variation process can be written as . Thus, the solution of the forward variation process is where and

| (27) | |||||

Recall that and when under the condition that the factor number is large enough (this formula is more applicable than (27) when , provided is large enough).

Using the approximation by Bergomi model, we consider the parameters in the exponential kernel on . Note that when , the power kernel while is finite. To compute the approximation numerically, we need to truncate the kernel . To do so we can use the scipy.optimize module in Python or the nlinfit function in MATLAB for the nonlinear regression of the parameters and the simulated price . We exemplify the truncation of by letting , the truncated parameter and let .

We define the integral on the truncated region and apply the scaling property of Brownian motion as follows:

After scaling , the process demands change to be driftless Gaussian and satisfy where . Then the process can be written as . Thus, the kernel in the rBergomi model on can be approximated by .

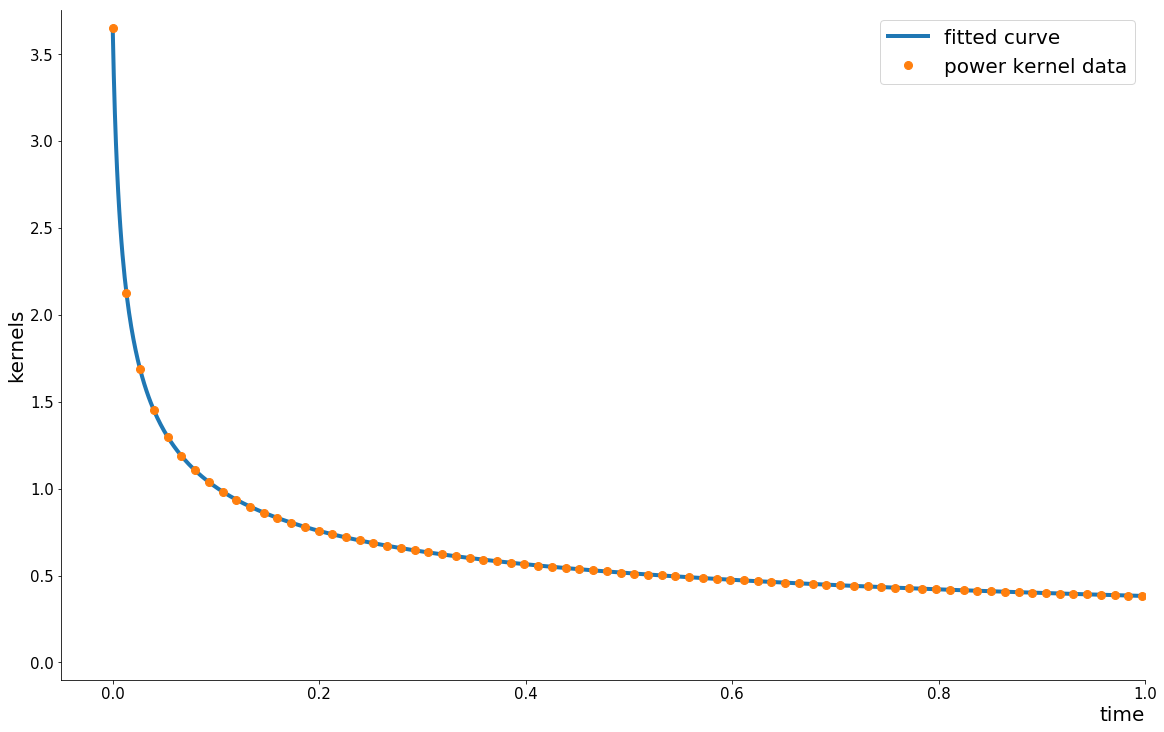

Figure 1 displays the power kernel in the rBergomi model and the in the 25-term aBergomi model when and . This figure suggests that is sufficiently accurate for nonlinear regression, with a Root-mean-square error (RMSE) of .

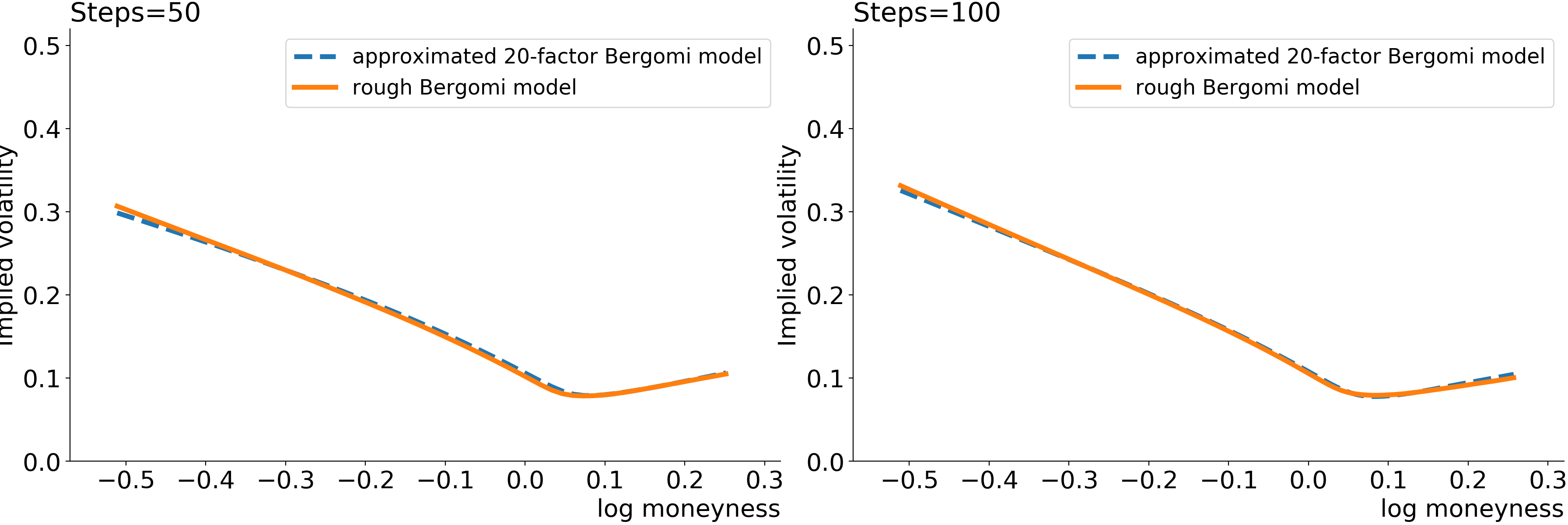

The method for simulating the variance in the aBergomi model is described in Section 5.2, which leads directly to the volatility smiles in Figure 2 (see Algorithm 3). From Figure 2, we note that the at-the-money calibration is better with 50 time steps at the cost of a worse out-of-the-money calibration. Meanwhile, 100 time steps can approximate the rBergomi model visually well. However, we multiply the aBergomi smile by a constant for different time steps since the Riemann-sum scheme is able to capture the shape of the implied volatility smile, but not its level (see Bennedsen et al., 2017). To generate realistic implied volatility smiles, we determine the square of multiplication factors for different time steps in Table 2.

| time steps | square of multiplication factors |

|---|---|

| 50 | 0.750323909 |

| 100 | 0.550447453 |

| 150 | 0.485093611 |

| 200 | 0.450392126 |

| Time steps | rBergomi | 10-term aBergomi | 15-term aBergomi | 20-term aBergomi | 25-term aBergomi |

|---|---|---|---|---|---|

| 50 | 0.408105 | 0.099360 | 0.139226 | 0.172056 | 0.216408 |

| 100 | 0.500114 | 0.236882 | 0.313049 | 0.402372 | 0.454303 |

| 150 | 0.560219 | 0.365012 | 0.449856 | 0.558937 | 0.686911 |

| 200 | 0.586050 | 0.425685 | 0.590825 | 0.725772 | 0.872691 |

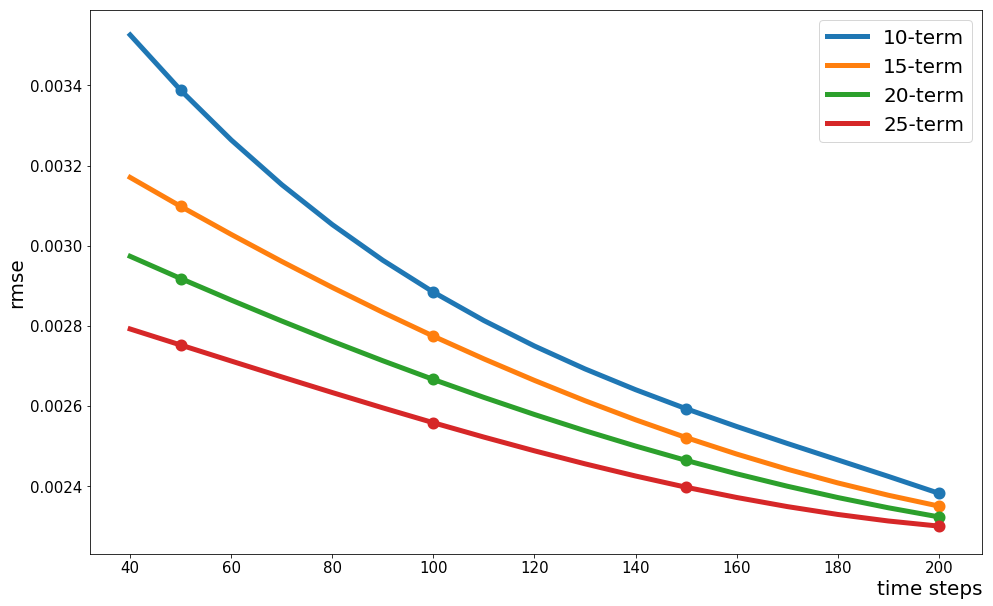

We compute the RMSE of the implied volatility approximation with different numbers of terms in the aBergomi model and different time steps in Figure 3 and compare the pricing speed in Table 3. The numerical results suggest that the RMSE of different term numbers reduces to the same low level as the number of time steps increases. Therefore, we may conclude that choosing the 25-term O-U process and 100 time steps can produce a good output, with reliable outcomes and fast calculation speed with 20000 Monte Carlo paths.

6 Conclusion

In this paper, we prove the power-law behavior of the ATM volatility skew as time to maturity goes to zero of the rBergomi model and we also propose an aBergomi model with finite terms to approximate the rBergomi model. The approximation enables the adoption of classical pricing methods while keeping the fractional feature of the model. When the terms number in the aBergomi model is large enough, we can prove its convergence to the rBergomi model. We not only give the theoretical proofs, but also give its numerical results. A hybrid scheme for the rBergomi model with the computational complexity is developed for the aBergomi model. Numerically simulated results by the hybrid scheme demonstrate the accuracy and efficiency of the approximation.

The model parameters used in the numerical test are calibrated from the regression of the power-law kernel of the rBergomi model. Other efficient calibration methods are worth investigation for future research.

Appendix A Appendix

A.1 Proof of Theorem 7

In this subsection, we give the proof of the theoretical results in Theorem 7.

Proof.

Let be auxiliary mean reversion speeds such that for and . Recall that . We have

| (28) | ||||

The first term on the RHS of the inequality (28) can be estimated as below:

For the second term, applying a second-order Taylor expansion of the exponential function for , choosing and , we can obtain that

since

Hence,

Thus, the convergence of depends on the weights and mean reversions . Let for each and . We have

We can also proceed to get the explicit expressions of and as follows:

Since , we have as when ,

| (29) | |||||

Let , RHS and , solving for , we have , where and

When , the RHS of equation (29) attains its minimum and where is a constant. ∎

References

- Abi Jaber and El Euch, (2019) Abi Jaber, E. and El Euch, O. (2019). Multifactor approximation of rough volatility models. SIAM Journal on Financial Mathematics, 10(2):309–349.

- Bayer et al., (2016) Bayer, C., Friz, P., and Gatheral, J. (2016). Pricing under rough volatility. Quantitative Finance, 16(6):887–904.

- Bayer et al., (2018) Bayer, C., Hammouda, C. B., and Tempone, R. (2018). Hierarchical adaptive sparse grids for option pricing under the rough Bergomi model. arXiv preprint arXiv:1812.08533.

- Bayer et al., (2019) Bayer, C., Horvath, B., Muguruza, A., Stemper, B., and Tomas, M. (2019). On deep calibration of (rough) stochastic volatility models. arXiv preprint arXiv:1908.08806.

- Bennedsen et al., (2017) Bennedsen, M., Lunde, A., and Pakkanen, M. S. (2017). Hybrid scheme for Brownian semistationary processes. Finance and Stochastics, 21(4):931–965.

- Bergomi, (2005) Bergomi, L. (2005). Smile dynamics II. Risk magazine, 18(10).

- Bergomi, (2009) Bergomi, L. (2009). Smile dynamics IV. Risk magazine, 22(12).

- Bergomi and Guyon, (2012) Bergomi, L. and Guyon, J. (2012). Stochastic volatility’s orderly smiles. Risk, 25(5):60.

- Carmona et al., (2000) Carmona, P., Coutin, L., and Montseny, G. (2000). Approximation of some Gaussian processes. Statistical inference for stochastic processes, 3(1-2):161–171.

- Forde and Zhang, (2017) Forde, M. and Zhang, H. (2017). Asymptotics for rough stochastic volatility models. SIAM Journal on Financial Mathematics, 8(1):114–145.

- Fukasawa, (2017) Fukasawa, M. (2017). Short-time at-the-money skew and rough fractional volatility. Quantitative Finance, 17(2):189–198.

- Gatheral et al., (2018) Gatheral, J., Jaisson, T., and Rosenbaum, M. (2018). Volatility is rough. Quantitative Finance, 18(6):933–949.

- Gatheral and Keller-Ressel, (2019) Gatheral, J. and Keller-Ressel, M. (2019). Affine forward variance models. Finance and Stochastics, pages 1–33.

- Harms and Stefanovits, (2019) Harms, P. and Stefanovits, D. (2019). Affine representations of fractional processes with applications in mathematical finance. Stochastic Processes and their Applications, 129(4):1185–1228.

- Jacquier et al., (2018) Jacquier, A., Martini, C., and Muguruza, A. (2018). On VIX futures in the rough Bergomi model. Quantitative Finance, 18(1):45–61.

- James et al., (2013) James, G., Witten, D., Hastie, T., and Tibshirani, R. (2013). An introduction to statistical learning, volume 112. Springer.

- Jusselin and Rosenbaum, (2018) Jusselin, P. and Rosenbaum, M. (2018). No-arbitrage implies power-law market impact and rough volatility. Available at SSRN 3180582.

- McCrickerd and Pakkanen, (2018) McCrickerd, R. and Pakkanen, M. S. (2018). Turbocharging Monte Carlo pricing for the rough Bergomi model. Quantitative Finance, 18(11):1877–1886.

- Muravlev, (2011) Muravlev, A. A. (2011). Representation of a fractional Brownian motion in terms of an infinite-dimensional Ornstein-Uhlenbeck process. Russian Mathematical Surveys, 66(2):439–441.

- Øksendal and Zhang, (1993) Øksendal, B. and Zhang, T.-S. (1993). The stochastic Volterra equation. In Barcelona Seminar on Stochastic Analysis, pages 168–202. Springer.

- Protter, (2005) Protter, P. E. (2005). Stochastic differential equations. In Stochastic integration and differential equations, pages 249–361. Springer.