figuresection

A fully data-driven approach to minimizing CVaR for portfolio of assets via SGLD with discontinuous updating ††thanks: This work was supported by The Alan Turing Institute for Data Science and AI under EPSRC grant EP/N510129/1. Y. Z. was supported by The Maxwell Institute Graduate School in Analysis and its Applications, a Centre for Doctoral Training funded by the UK Engineering and Physical Sciences Research Council (grant EP/L016508/01), the Scottish Funding Council, Heriot-Watt University and the University of Edinburgh.

Abstract

A new approach in stochastic optimization via the use of stochastic gradient Langevin dynamics (SGLD) algorithms, which is a variant of stochastic gradient decent (SGD) methods, allows us to efficiently approximate global minimizers of possibly complicated, high-dimensional landscapes. With this in mind, we extend here the non-asymptotic analysis of SGLD to the case of discontinuous stochastic gradients. We are thus able to provide theoretical guarantees for the algorithm’s convergence in (standard) Wasserstein distances for both convex and non-convex objective functions. We also provide explicit upper estimates of the expected excess risk associated with the approximation of global minimizers of these objective functions.

All these findings allow us to devise and present a fully data-driven approach for the optimal allocation of weights for the minimization of CVaR of portfolio of assets with complete theoretical guarantees for its performance. Numerical results illustrate our main findings.

1 Introduction

We are concerned in this article with the study of stochastic optimization problems of the form

| (1) |

where the gradient of is discontinuous in and is a random element with a smooth density. Within this framework, we highlight and solve the problem of minimizing CVaR (expected shortfall) of a portfolio of assets in terms of optimal selection of weights for individual assets as explained in Section 5.2.2. We offer theoretical guarantees for the approximate solution of the optimization problem (1) by generating a such that the expected excess risk

is minimized. To achieve this, we analyse the convergence properties of the stochastic gradient Langevin dynamics (SGLD) algorithm with discontinuous updating , which is given by

| (2) |

where is an -valued random variable, is the stepsize, is the so-called inverse temperature parameter, is a measurable function satisfying with being an i.i.d. sequence, and is an independent sequence of standard -dimensional Gaussian random variables. One recalls heere that the SGLD algorithm (2) can be viewed as a discretization of the Langevin SDE:

| (3) |

where and represents the standard Brownian motion. Moreover, it is well-known that, under appropriate conditions, the Langevin SDE (3) admits a unique invariant measure which concentrates around the minimizers of when is sufficiently large, , see [16] for more details.

Theoretical guarantees of the SGLD algorithm (2) to the target distribution have been established in Wasserstein-2 distance under the assumptions that is convex and (locally) Lipschitz continuous, see [1], [2], [10] and references therein. Recently, these results are considered under more generalised conditions aiming to include a wider range of practical applications. To relax the convexity condition, a dissipativity condition is proposed in [19], and the convergence result is obtained in Wasserstein-2 distance with the rate . This is the first such result in non-convex optimization, which is then improved in the work [23] and [8]. Compared to [19], a higher rate of convergence with dependence on is achieved in [23] following a direct analysis of the ergodicity of the overdamped Langevin Monte Carlo (LMC) algorithms, while a rate 1/2 in Wasserstein-1 distance is obtained in [8] by using the contraction results developed in [14].

As for the generalisation of the smoothness of , to the best of the author’s knowledge, there are no theoretical guarantees established in the literature for the SGLD algorithm (2) with discontinuous gradient. We present here the first such results. We are inspired by similar studies for stochastic gradient descent (SGD) algorithms, see [15] and [7] and references therein. In particular, [15] provides an almost sure convergence result, while [7] provides a strong convergence result with rate 1/2.

In this paper, we establish non-asymptotic error bounds for the SGLD algorithm (2) with discontinuous gradient . More precisely, non-asymptotic results in Wasserstein-1 and Wasserstein-2 distances between the law of the -th iterate of the SGLD algorithm (2) and the target distribution are obtained under convexity and dissipativity conditions for . This allows us to then provide full analytic results concerning the expected excess risk of the associated optimization problem (1). All this is achieved by assuming that is decomposed in to two parts and , where is locally Lipschitz continuous and is bounded. Furthermore, is assumed to satisfy a conditional Lipschitz-continuity (CLC) property proposed in [7], which is given explicitly in Assumption 3 below.

We illustrate the applicability of our findings by presenting examples from quantile and VaR, CVaR estimations in Section 5. In particular, we solve the problem of optimal allocation of weights for the minimization of CVaR of a portfolio of assets. This is also the first such result in the literature to the best of the author’s knowledge. Numerical experiments are implemented and their results support our theoretical findings.

The paper is organised as follows. Section 2 presents the assumptions and main results. In Section 3, the proofs for the main theorems in the non-convex case are provided, which are followed by the proofs for the results in the convex case in Section 4. Practical examples along with the minimization algorithm of CVaR for a portfolio of assets are presented in Section 5 while auxiliary results are provided in Section A.

We conclude this section by introducing some notation. Let be a probability space. We denote by the expectation of a random variable . For any , denote by the -th entry of the vector. Fix an integer . For an -valued random variable , its law on (the Borel sigma-algebra of ) is denoted by . Scalar product is denoted by , with standing for the corresponding norm (where the dimension of the space may vary depending on the context). For and for a non-negative measurable , the notation is used. Given a Markov kernel on and a function integrable under , for any , denote by . For any integer , let denote the set of probability measures on . For , let denote the set of probability measures on such that its respective marginals are . For two probability measures and , the Wasserstein distance of order is defined as

| (4) |

2 Main results

Denote by , for any . is an -valued, -adapted process. It is assumed throughout the paper that , and are independent. Moreover, the following assumptions are considered:

Assumption 1.

Let take the form

where and satisfy the following:

-

(i)

is jointly Lipschitz continuous in both variables, i.e. there exist , such that for any , ,

-

(ii)

is bounded in , i.e. there exist such that for any , ,

Assumption 2.

We assume the inital value satisfies . The process is i.i.d. with and . Moreover, it satisfies

Remark 1.

Assumption 3.

There exists a positive constant such that, for all ,

Remark 3.

Assumption 3 is satisfied for a wide class of , see Section 5 for the examples. Here, for the illustrative purpose, one considers the following simple example. Suppose is a lower semi-continuous function, where , are bounded and jointly Lipschitz continuous functions, i.e. there exist such that for any , ,

the intervals take the form , or , and are Lipschitz continuous functions. In this case, it is enough to require the marginal density function of is continuous and bounded for any . Then, the property stated in Assumption 3 holds.

Proof.

See Appendix A.1. ∎

2.1 Nonconvex case

Further to the assumptions above, we consider the following conditions on , which can be viewed as a generalization of the convexity assumption.

Assumption 4.

There exist , such that for any ,

and for all and ,

The smallest eigenvalue of is a positive real number and .

Theorem 1.

Theorem 1 provides the rate of convergence between the law of the SGLD algorithm (2) and the target distribution in distance. An analogous result in Wasserstein-2 distance can be obtained.

Corollary 1.

By using the convergence result in Wasserstein-2 distance as presented in Corollary 1, one can obtain an upper bound for the expected excess risk .

2.2 Convex case

Recall Assumption 1, where it is assumed . In this section, we present (improved) convergence results of the SGLD algorithm (2) under the convexity condition of and .

In the case that satisfies a convexity condition but not , the result in Theorem 1 can be recovered.

Assumption 5.

There exist such that for any ,

and for each , ,

The smallest eigenvalue of is a positive real number with .

Proof.

See Appendix A.2. ∎

Corollary 3.

If is assumed to be convex in addition to Assumption 5, then it can be shown that the rate of convergence is 1/2 in Wasserstein-2 distance between the law of the SGLD algorithm (2) and the target distribution , which appeared to be optimal, see [1, Example 3.4].

Assumption 6.

There exist such that for any ,

and for each , ,

The smallest eigenvalue of is a positive real number .

Define

| (10) |

with given in Remark 5. Under the convexity condition of , the non-asymptotic bound for is obtained with the optimal convergence rate 1/2. The explicit statement is given below.

Theorem 2.

By using Theorem 2, one can obtain an upper bound for the expected excess risk in the convex case.

3 Proofs of the main results: nonconvex case

Denote by the natural filtration of , . It is a classic result that SDE (3) has a unique solution adapted to , since is Lipschitz-continuous by (6). In order to obtain the convergence results in Theorem 1 and Corollary 1, we first introduce some auxiliary processes.

3.1 Further notation and introduction of auxiliary processes

Define the Lyapunov function for each by

and similarly , for any real . Notice that these functions are twice continuously differentiable and

Let denote the set of satisfying .

Consider the following auxiliary processes. For each ,

Notice that , is also a Brownian motion and

Then, , is the natural filtration of , . One notice that is independent of . Then, define the continuous-time interpolation of the SGLD algorithm (2) as

| (11) |

with initial condition . In addition, due to the homogeneous nature of the coefficients of equation (11), the law of the interpolated process coincides with the law of the SGLD algorithm (2) at grid-points, i.e. , for each . Hence, crucial estimates for the SGLD can be derived by studying equation (11).

Furthermore, consider a continuous-time process , , which denotes the solution of the SDE

with initial condition , .

Definition 1.

Fix and define

where .

Intuitively, is a process started from the value of the SGLD process (11) at time and made run until time with the continuous-time Langevin dynamics.

3.2 Preliminary estimates

We proceed by establishing the moment bounds of the processes and .

Lemma 1.

Proof.

For any and , define . By using (11), it is easily seen that for

Then, by using Assumptions 1, 2, 4 and Remark 1, one obtains

where the last inequality is obtained by using , for twice. For with given in (7),

For , one obtains

which implies

For , we have

Combining the two cases yields

where . Therefore, one obtains

where and the result follows by induction. To calculate a higher moment, denote by , for , one calculates

| (14) |

where the last inequality holds due to , for and with . Then, one continues with calculating

By Remark 1, for , one observes

| (15) |

Then, by using Assumption 4 and by taking in (15), one obtains

which implies, by using

For , one obtains

similarly, for , we have

moreover, for

Denote by

| (16) | ||||

For , one obtains

As for , we have

Combining the two cases yields

| (17) |

where

| (18) |

with given in (16). Substituting (17) into (3.2), one obtains

where . The proof completes by induction. ∎

Remark 7.

Next, we present a drift condition associated with the SDE (3), which will be used to obtain the moment bounds of the process .

Proof.

The following Lemma provides the second and the fourth moment of the process .

Lemma 3.

Proof.

For any , application of Ito’s lemma and taking expectation yields

Differentiating both sides and using Lemma 2, we arrive at

which yields

Now for , by using Corollary 5,one obtains

where the last inequality holds due to for and . Similarly, for , one obtains

where the last inequality holds due to for and . ∎

3.3 Proof of the main theorems

We introduce a functional which is crucial to obtain the convergence rate in . For any , ,

| (20) |

and it satisfies trivially

| (21) |

The case , i.e. , is used throughout the section. The result below states a contraction property of .

Proposition 1.

Proof.

See Proposition 3.14 of [8]. ∎

By using the contraction property provided in Proposition 1, one can construct the non-asymptotic bound between and , , in distance by decomposing the error using the auxiliary process :

| (22) |

One notices that when , the result holds trivially. Thus, we consider the case , which implies .

An upper bound for the first term in (22) is obtained in the Lemma below.

Proof.

To handle the first term in (22), we start by establishing an upper bound in Wasserstein-2 distance and the statement follows by noticing . By employing synchronous coupling, using (11) and the definition of in Definition 1, one obtains

Then, the triangle inequality leads

Taking squares on both sides and the application of Remark 2 yield

By taking expectations on both sides and by using , for , one obtains

which implies due to and Lemma 13

| (23) |

where and are provided in (52). Next, we bound the last term in (3.3) by partitioning the integral. Assume that where . Thus we can write

where

Taking squares of both sides

Finally, we take expectations of both sides. Define the filtration . We first note that for any , ,

By the same argument for all . Therefore, the last term of (3.3) is bounded as

where the last inequality holds due to Lemma 12 and and are provided in (51). Therefore, the bound (3.3) becomes

Using Grönwall’s inequality yields

which implies by ,

| (24) |

where

| (25) |

Then, the following Lemma provides the bound for the second term in (22).

Proof.

By using similar arguments as in Lemma 5, an analogous result can be obtained in distance, which is given in the following corollary.

Proof.

Finally, by using the inequality (22) and the results from previous lemmas, one can obtain the non-asymptotic bound between and , , in distance.

Before proceeding to the proofs of the main results, we provide explicitly the constants and in Proposition 1.

Lemma 7.

The contraction constant in Proposition 1 is given by

where the explicit expressions for and can be found in Lemma 2 and is given by

Furthermore, any can be chosen which satisfies the following inequality

where and . The constant is given as the ratio , where are given explicitly in [8, Lemma 3.26].

Proof.

See [8, Lemma 3.26]. ∎

Proof of Theorem 1 One notes that, by Lemma 6 and Proposition 1, for

which implies, for any

where

| (29) |

with given in 28.

Proof of Corollary 1 By using (24) in Lemma 4, Corollary 6 and Proposition 1, one obtains

where and it can be further calculated as

Finally, one obtains

where

| (30) |

Proof of Corollary 2 To obtain an upper bound for the expected excess risk , one considers the following splitting

| (31) |

where and with for all . By using [19, Lemma 3.5], Lemma 1, 14 and Corollary 1, the first term on the RHS of (31) can be bounded by

where

| (32) | ||||

with given in (30) and given in (12). Moreover, the second term on the RHS of (31) can be estimated by using [19, Proposition 3.4], which gives,

where

| (33) |

Finally, one obtains

4 Proof of the main results: convex case

The analysis of the convergence results in the convex case, i.e. Theorem 2, relies on the properties of the LMC algorithm, known also as the unadjusted Langevin algorithm (ULA). The LMC algorithm associated with SDE (3) is given explicitly by, for any ,

| (34) |

For , the Markov kernel associated with (34) is given by, for all and ,

In this section, the moment estimates of the SDE (3), the LMC algorithm (34) and the SGLD algorithm (2) are presented which contribute to the analysis of the convergence resuts.

4.1 Preliminary estimates

Under Assumptions 5 and 6, has a unique minimizer . Denote by the semigroup associated with SDE (3). The statements below provide a moment bound and a convergence result for SDE (3).

Lemma 8 (Proposition 1 in [12]).

The following lemma provides moment estimates for and it states that admits an invariant measure which may differ from .

Lemma 9.

The lemma below presents a second moment bound for in the convex case.

Lemma 10.

Proof.

By using (2), one writes, for any ,

Taking conditional expectation on both sides and by using Remark 1 and Assumption 1, 5 yield

| (36) | ||||

which implies, for ,

Then, for , one notices that

and this indicates

Similarly, for , one obtains

Combining the two cases yields

where . The result follows by induction.

Moreover, one observes that when in Assumption 1, is co-coercive, i.e. for any and for every

| (37) |

Then, by substituting (37) into (4.1), one obtains

which implies for

By using the same arguments as above, consider the case , one notices that

and this indicates

Similarly, for , one obtains

Combining the two cases yields

where . ∎

4.2 Convergence results

We aim to establish the non-asymptotic bound in Wasserstein-2 distance between and . To achieve this, we consider the following decomposition:

| (38) |

The lemma presented below provides the non-asymptotic estimates for the last two terms in (38).

Theorem 3.

The non-asymptotic estimate for the first term in (38) is provided in the following lemma.

Proof.

Proof of Theorem 2 One observes that by using Theorem 3 and Lemma 11

where

| (41) |

with , given in Lemma 3, and given in (39) and (40) respectively.

Proof of Corollary 4 The proof follows the same lines as the proof of Corollary 2. To obtain an upper bound for the expected excess risk , one considers

| (42) |

where and with for all . By using [19, Lemma 3.5], Lemma 8, 10 and Theorem 2, the first term on the RHS of (42) can be bounded by

where is the minimizer of , and

| (43) | ||||

with given in (41) and given in (35). Moreover, the second term on the RHS of (42) can be estimated by using [19, Proposition 3.4], which gives,

where

| (44) |

Finally, one obtains

5 Applications

5.1 Quantile estimation with regularization

We consider the problem of quantile estimation for AR(1) processes, which has been discussed in [7], [17] and [22] amongst others, with regularization. It assumed therefore that the data , , follows an AR(1) process given by

where is a constant with and are i.i.d. standard Normal random variables. The above expression can be further rewritten as

One notes that has a stationary distribution which is normally distributed with mean 0 and variance . Our task is to identify the -th quantile of the stationary distribution using the SGLD algorithm (2), in other words, we aim to solve the following problem:

where and

The stochastic gradient is given by

| (45) |

where is a positive constant. To check Assumption 1, denote by , . It can be easily seen that Assumption 1 holds with , , and . Then, by Remark 3 and its proof in A.1, Assumption 3 holds with . Moreover, Assumption 4 holds with and , which implies and .

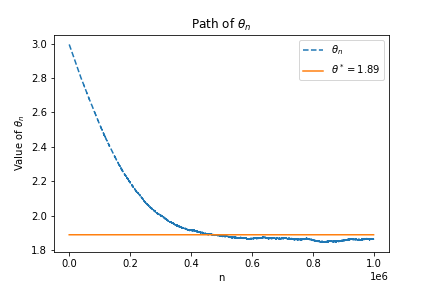

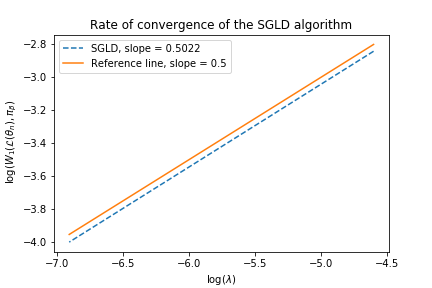

One notes that the value of the -th quantile of is given by where is the cumulative distribution function of the standard normal distribution. For the simulation, set , , and thus, . Moreover, let , , and . Note that we use the step restriction given in Remark 7 for all the examples in this section. In Figure 1, the left graph is obtained by using the SGLD algorithm (2) with and the number of iterations . It shows the path of with the first iterations being discarded, and the path stabilises at around the true value . The right graph of Figure 1 illustrates the rate of convergence of the SGLD algorithm in Wasserstein-1 distance based on 5000 samples. The slope of the results in obtained using numerical experiments is 0.5022, which supports our theoretical finding in Theorem 1 with rate .

5.2 VaR-CVaR algorithm

In this section, we consider the problem of computing Value-at-Risk (VaR) and Conditional-Value-at-Risk (CVaR), which are two commonly used risk measures in financial risk management. In order to obtain the two quantities, one considers the following optimization problem:

| (46) |

where , is continuous and is integrable with respect to the probability measure. As noted in [4], can represent more complicated payoff structures than simple vanilla instruments while can accommodate a large family of asset distributions including those generated by stochastic/local volatility models, see e.g. [11], [20] and [21] references therein. Then, by [4, Proposition 2.1], and . To compute VaR, the stochastic gradient of the SGLD algorithm (2) is given by

5.2.1 Single asset

Let , one notices that the above expression has a similar form as (45). Then, one can check that Assumption 1 - 4 are satisfied. More precisely, denote by , , Assumption 1 holds with , , and . Let be a one-dimensional random variable with finite fourth moment, then Assumption 2 is satisfied. Denote by the upper bound of the density of , Assumption 3 holds with . Furthermore, Assumption 4 holds with and , which implies and .

| VaR* | CVaR* | VaR* | CVaR* | |||||

|---|---|---|---|---|---|---|---|---|

| 1.645 | 2.062 | 1.642 | 2.062 | 2.326 | 2.677 | 2.329 | 2.662 | |

| (0.02) | (0.0006) | (0.04) | (0.0038) | |||||

| 4.290 | 5.124 | 4.294 | 5.126 | 5.653 | 6.335 | 5.640 | 6.336 | |

| (0.03) | (0.0006) | (0.06) | (0.0032) | |||||

| 11.224 | 13.311 | 11.230 | 13.305 | 14.632 | 16.337 | 14.643 | 16.313 | |

| (0.05) | (0.0006) | (0.11) | (0.006) | |||||

| VaR* | CVaR* | VaR* | CVaR* | |||||

|---|---|---|---|---|---|---|---|---|

| 1.812 | 2.416 | 1.808 | 2.407 | 2.764 | 3.357 | 2.767 | 3.350 | |

| (0.02) | (0.0005) | (0.05) | (0.003) | |||||

| 1.895 | 2.595 | 1.895 | 2.594 | 2.998 | 3.757 | 3.001 | 3.782 | |

| (0.03) | (0.0008) | (0.05) | (0.0024) | |||||

| 2.353 | 3.876 | 2.358 | 3.873 | 4.541 | 6.968 | 4.542 | 6.967 | |

| (0.03) | (0.0008) | (0.08) | (0.0028) | |||||

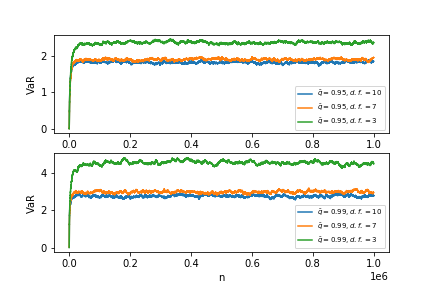

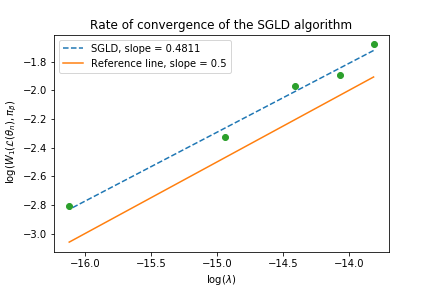

For the numerical experiments, we set , , , and the number of iterations . Table 1 and 2 present VaR and CVaR for the normal distribution and Student’s t-distribution. VaR* and CVaR* in the tables denote the theoretical values, while and denote the numerical approximations from the SGLD algorithm (2). Each approximation in the table is obtained based on 10000 samples, which is followed by its sample standard deviation shown in brackets. In addition, in Figure 2, the left graph illustrates the path of for the -distribution, whereas the right graph shows that the rate of convergence of the SGLD algorithm (2) is 0.4811. One notes that the samples from is generated by running the SGLD algorithm with .

5.2.2 Minimizing CVaR of portfolios of assets

To minimize CVaR for a given portfolio, we consider the following optimization problem:

| (47) |

where the parameter and for . By solving (47), we obtain not only VaR for a given portfolio, but also the optimal weight for each asset in the portfolio such that CVaR is minimized.

For reasons of brevity, we assume here that the ’s, for , are i.i.d. one-dimensional random variables (with finite fourth moments). Our results can be naturally extended to the case of dependent data streams via the concept of -mixing as explained in [8].

Let , denote the first and second absolute moment respectively of . Moreover, let be bounded for any and . Note that this latter requirement is satisfied for a wide range of distributions, for example, the distributions shown in Table 3. Then, the stochastic gradient is defined as

where and for all are given by

and

where

for any with , and for . One notes that for any . Moreover, if Assumption 1 - 4 hold for and for any , then the assumptions hold for .

We first check assumptions for . Denote by

then . Assumption 1 holds with , , and . By taking into consideration the expression of and the construction of the problem, Assumption 2 is satisfied. Assumption 4 holds with and , which implies and . To check Assumption 3, one considers , and then calculates by assuming without loss of generality

where

To estimate , one writes

where we use the fact in the last inequality and denotes the upper bound of the density of . can be estimated by using similar arguments. Then, one obtains

which implies Assumption 3 holds with .

Next, we check assumptions for . Denote by

then . Assumption 1 holds with , , and . By taking into consideration the expression of and the construction of the problem, Assumption 2 is satisfied. Assumption 4 holds with and , which implies and . Then, we check Assumption 3 for , and the arguments stay the same lines for any other , . Consider . Then, one calculates

where the third inequality holds due to the fact that . Then, by using ,

| (48) | ||||

where , denote the first and the second absolute moment of ’s respectively, for any , is the upper bound of the function , and is the upper bound of the density of . Detailed calculations to obtain the last inequality in (48) is given in Appendix A.3. Thus Assumption 3 holds with .

| SGLD algorithm | Reference | ||||||||

| VaR* | CVaR* | ||||||||

| 0.00002 | 0.99998 | 0.025 | 0.03 | 0 | 1 | 0.016 | 0.021 | ||

| 0.000006 | 0.999994 | 0.016 | 0.25 | 0 | 1 | 0.016 | 0.021 | ||

| 0.111 | 0.889 | 1.615 | 2.004 | 0.11 | 0.89 | 1.617 | 1.999 | ||

| with d.f. | 0.917 | 0.083 | 1.567 | 1.975 | 0.9 | 0.1 | 1.531 | 1.971 | |

| with d.f. | 0.577 | 0.423 | 1.236 | 1.554 | 0.58 | 0.42 | 1.224 | 1.553 | |

| with d.f. | 0.503 | 0.497 | 1.15 | 1.46 | 0.5 | 0.5 | 1.165 | 1.461 | |

| with d.f. | 0.596 | 0.404 | 2.941 | 4.130 | 0.61 | 0.39 | 2.985 | 4.115 | |

| with d.f. | 0.172 | 0.828 | 1.743 | 2.290 | 0.17 | 0.83 | 1.779 | 2.286 | |

| with d.f. | 0.113 | 0.887 | 1.594 | 2.008 | 0.11 | 0.89 | 1.619 | 2.002 | |

| Logistic(0,1) | 0.775 | 0.225 | 1.422 | 1.816 | 0.78 | 0.22 | 1.442 | 1.813 | |

| Logistic(0,29) | 0.999 | 0.001 | 1.633 | 2.110 | 1 | 0 | 1.645 | 2.063 | |

| Logistic(2,10) | 0.997 | 0.003 | 1.650 | 2.101 | 1 | 0 | 1.648 | 2.065 | |

| Logistic(0,1) | 0.402 | 0.598 | 2.635 | 3.262 | 0.4 | 0.6 | 2.607 | 3.261 | |

| Logistic(0,29) | 0.998 | 0.002 | 4.284 | 5.145 | 1 | 0 | 4.284 | 5.116 | |

| Logistic(2,10) | 0.991 | 0.009 | 4.255 | 5.132 | 0.99 | 0.01 | 4.283 | 5.114 | |

| Lognormal(0,1) | 0.966 | 0.034 | 1.662 | 2.068 | 0.97 | 0.03 | 1.647 | 2.054 | |

| Lognormal(0,0.01) | 0.074 | 0.926 | 1.145 | 1.205 | 0.07 | 0.93 | 1.132 | 1.186 | |

| Lognormal(1,4) | 0.9997 | 0.0003 | 1.674 | 2.136 | 1 | 0 | 1.645 | 2.062 | |

| Lognormal(0,1) | 0.732 | 0.268 | 3.750 | 4.6050.74 | 0.74 | 0.26 | 3.771 | 4.599 | |

| Lognormal(0,0.01) | 0.010 | 0.0.989 | 1.173 | 1.301 | 0 | 1 | 1.179 | 1.230 | |

| Lognormal(1,4) | 0.997 | 0.003 | 4.266 | 5.194 | 1 | 0 | 4.292 | 5.129 | |

| Logistic(0,1) | Lognormal(0,1) | 0.817 | 0.183 | 2.797 | 3.727 | 0.81 | 0.19 | 2.814 | 3.724 |

| Logistic(0,1) | Lognormal(0,0.01) | 0.022 | 0.978 | 1.169 | 1.256 | 0.02 | 0.98 | 1.164 | 1.217 |

| Logistic(0,1) | Lognormal(1,4) | 0.997 | 0.003 | 2.961 | 4.030 | 1 | 0 | 2.947 | 3.971 |

| Logistic(2,10) | Lognormal(0,1) | 0.043 | 0.956 | 5.245 | 8.412 | 0.04 | 0.96 | 5.198 | 8.400 |

| Logistic(2,10) | Lognormal(0,0.01) | 0.009 | 0.991 | 1.184 | 1.315 | 0 | 1 | 1.179 | 1.229 |

| Logistic(2,10) | Lognormal(1,4) | 0.996 | 0.004 | 31.651 | 41.748 | 0.99 | 0.01 | 31.420 | 41.738 |

For the numerical experiments, we set , , , and the number of iterations . Tabel 3 illustrates VaR and CVaR obtained using the SGLD algorithm for a portfolio of two assets and with weights and respectively. The reference values , , VaR* and CVaR* are obtained numerically in the following way:

-

1.

First, we create 100 evenly spaced numbers over the interval .

-

2.

Then, for any given distributions of and , assign each of the 100 numbers to , which is the weight of , and calculate the CVaR for the combination .

-

3.

Finally, we obtain the minimum CVaR and the corresponding among the 100 values. We denote them as CVaR* and . Here , one notes that the corresponding VaR* can be calculated using the optimal weights and .

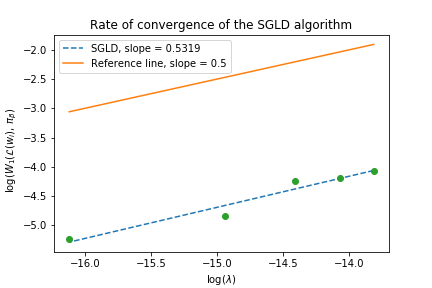

Figure 3 shows that the rate of convergence of the SGLD algorithm (2) for the parameter is 0.5319, which supports the theoretical finding in Theorem 1. One notes that the samples from is generated by running the SGLD algorithm with .

References

- [1] M. Barkhagen, N. H. Chau, É. Moulines, M. Rásonyi, S. Sabanis and Y. Zhang. On stochastic gradient Langevin dynamics with stationary data streams in the logconcave case. Preprint, 2018. arXiv:1812.02709

- [2] N. Brosse, A. Durmus and E. Moulines. The promises and pitfalls of stochastic gradient Langevin dynamics. Advances in Neural Information Processing Systems, 8268-8278, 2018.

- [3] M. Benaïm, J.C. Fort and G. Pagès, Convergence of the one-dimensional Kohonen algorithm. Advances in Applied Probability, 30(3), 850-869, 1998.

- [4] O. Bardou, N. Frikha and G. Pagès, Computing VaR and CVaR using stochastic approximation and adaptive unconstrained importance sampling. Monte Carlo Methods and Applications, 15(3), 173-210, 2009.

- [5] H. Cardot, P. Cénac and P. A. Zitt. Recursive estimation of the conditional geometric median in Hilbert spaces. Electronic Journal of Statistics, 6: 2535-2562, 2012.

- [6] H. Cardot, P. Cénac and P. A. Zitt. Efficient and fast estimation of the geometric median in Hilbert spaces with an averaged stochastic gradient algorithm. Bernoulli, 19(1): 18-43, 2013.

- [7] N. H. Chau, Ch. Kumar, M. Rásonyi and S. Sabanis. On fixed gain recursive estimators with discontinuity in the parameters. ESAIM Probability and Statistics, 23:217–244, 2019.

- [8] N. H. Chau, É. Moulines, M. Rásonyi, S. Sabanis and Y. Zhang. On stochastic gradient Langevin dynamics with dependent data streams: the fully non-convex case. Preprint, 2019. arXiv:1905.13142

- [9] H. Djellout, A. Guillin, and L. Wu. Transportation cost-information inequalities and applications to random dynamical systems and diffusions. The Annals of Probability, 32(3B), 2702–2732, 2004.

- [10] A. S. Dalalyan and A. Karagulyan. User-friendly guarantees for the Langevin Monte Carlo with inaccurate gradient. To appear in Stochastic Processes and their Applications, 2019.

- [11] B. Dupire, Pricing with a Smile. Risk, 7(1):18–20, 1994.

- [12] A. Durmus and É. Moulines. High-dimensional Bayesian inference via the unadjusted Langevin algorithm. Preprint, 2018. arXiv:1605.01559v3

- [13] A. Eberle. Reflection couplings and contraction rates for diffusions. Probab. Theory Related Fields, 166:851–886, 2016.

- [14] A. Eberle, A. Guillin and R. Zimmer. Quantitative Harris-type theorems for diffusions and McKean-Vlasov processes. In Press, Transactions of the American Mathematical Society, 2018. https://doi.org/10.1090/tran/7576

- [15] G. Fort, É. Moulines, A. Schreck and M. Vihola. Convergence of Markovian Stochastic Approximation with discontinuous dynamics. SIAM Journal on Control and Optimization, 54(2): 866–893, 2016.

- [16] C.R. Hwang Laplace’s method revisited: weak convergence of probability measures. The Annals of Probability, 8(6): 1177-1182, 1980.

- [17] R. Koenker and G. Bassett Jr. Regression quantiles. Econometrica: journal of the Econometric Society, 33–50, 1978.

- [18] Y. Nesterov. Introductory Lectures on Convex Optimization: A Basic Course. Applied Optimization. Springer, 2004.

- [19] M. Raginsky, A. Rakhlin, and M. Telgarsky. Non-convex learning via Stochastic Gradient Langevin Dynamics: a nonasymptotic analysis. Proceedings of Machine Learning Research, (65)1674–1703, 2017.

- [20] S. Sabanis. Stochastic volatility and the mean reverting process. Journal of futures markets, 23(1):33–47, 2003.

- [21] S. Sabanis. Stochastic volatility. International Journal of Theoretical and Applied Finance, 5(5):515–530, 2002.

- [22] I. Takeuchi, Q. V. Le, T. D. Sears and A.J. Smola. Nonparametric quantile estimation. Journal of machine learning research, 7(Jul): 1231–1264, 2006.

- [23] P. Xu, J. Chen, D. Zhou and Q. Gu. Global convergence of Langevin dynamics based algorithms for nonconvex optimization. Advances in Neural Information Processing Systems, 3122-3133, 2018.

Appendix A Appendix

A.1 Proof of the claim in Remark 3

We adapt the proof from [7, Lemma 4.7] and extend it to an -valued random variable . It suffices to consider , where , is bounded and jointly Lipschitz continuous, i.e. there exist such that for any , ,

and the intervals take the form with Lipschitz. One notices that the proof follows the same lines when takes the form , with Lipschitz. One writes,

where for any is defined in (5) and we assume without loss of generality for all . By taking expectation on both sides and by using Cauchy-Schwarz inequality, one obtains

where denotes the marginal density function of , is an upper bound of and is a Lipschitz constant for . Taking completes the proof.

A.2 Proof of the claim in Remark 4

A.3 Validity of Assumption 3 for VaR-CVaR algorithm in Section 5.2

We aim to show Assumption 3 is valid for . To achieve this, it is enough to prove

-

(1)

The inequality holds, and

-

(2)

the last inequality in (48) is satisfied.

To prove , recall that for every , ,

Then, one calculates

where the last inequality holds due to for all .

To prove the last inequality in (48) is satisfied, we assume without loss of generality . Then,

-

(i)

For , one calculates

(49) where

To estimate , one writes

The first term on the RHS of the inequality above can be further estimated as

where denotes the second absolute moment of ’s , is the upper bound of the density of , and we use for in the third inequality. Moreover, can be upper bounded by

The first term on the RHS of the inequality above can be calculated as

where denotes the first absolute moment of ’s and is the upper bound of the function . Thus, in the case , (49) becomes

-

(ii)

As for the case , the calculations are close to the above, however, one considers a different splitting as follows

(50) where

To estimate , one calculates

The first term on the RHS of the inequality above can be further calculated as

In addition, can be estimated as

The first term on the RHS of the above inequality can be upper bounded by

Thus for the case , we have

Combining the two cases, one obtains

A.4 Auxiliary results

Proof.

Proof.

Proof.

For any , by applying Itô’s formula to , one obtains, almost surely

Then, integrating both sides and taking expectation yield

which implies by using Assumption 4

Finally, one obtains

∎