On the existence of optimal stationary policies for average Markov decision processes with countable states

Abstract

For a Markov decision process with countably infinite states, the optimal value may not be achievable in the set of stationary policies. In this paper, we study the existence conditions of an optimal stationary policy in a countable-state Markov decision process under the long-run average criterion. With a properly defined metric on the policy space of ergodic MDPs, the existence of an optimal stationary policy can be guaranteed by the compactness of the space and the continuity of the long-run average cost with respect to the metric. We further extend this condition by some assumptions which can be easily verified in control problems of specific systems, such as queueing systems. Our results make a complementary contribution to the literature in the sense that our method is capable to handle the cost function unbounded from both below and above, only at the condition of continuity and ergodicity. Several examples are provided to illustrate the application of our main results.

Keywords: Markov decision process, countable states, optimal stationary policy, metric space

1 Introduction

For finite Markov decision processes (MDPs), the optimality of various types of policies are well studied. For example, it is well known that the optimal value of finite MDPs with discounted or average criteria can be achieved by Markovian and deterministic policies, thus history-dependent and randomized policies are not needed to consider. More details can be referred to books on MDPs (Bertsekas, 2012; Puterman, 1994).

Countable-state MDPs are a type of widely existing models and are particularly useful for many problems, such as queueing systems, inventory management, etc. When the state space of MDPs is changed from finite to infinite (countable), the relevant analysis becomes more complicated and the algorithms need sophisticated discussion (Golubin, 2003; Meyn, 1997). Compared with the complete theoretical results for finite MDPs, there is no comprehensive theory for infinite MDPs with countable states and the long-run average criterion. The existence of an optimal stationary policy for countable-state MDPs needs specific discussion, and attracts research attention in recent decades. Although we can restrict our attention to stationary policies in finite MDPs, this is no longer true when the state space is countable. In general, the optimal value of a countable-state MDP may not be achievable by stationary policies, even not by history-dependent policies. Interesting counterexamples can be found in the excellent books on MDPs (see Examples 5.6.1&5.6.5&5.6.6 of Bertsekas (2012), Examples 8.10.1&8.10.2 of Puterman (1994), and Subsection 7.1 of Sennott (1999)).

Since a stationary policy is not necessarily optimal for countably infinite MDPs, there are literature works on the specific existence conditions of optimal stationary policies. Sennott studies the existence conditions for average cost optimality of stationary policies for discrete-time MDPs when state space is countable and action space is finite (Sennott, 1986, 1989). In Sennott’s studies, a distinguished state is introduced and the vanishing discount optimality approach is adopted to study the optimality inequality. Borkar (1989) also studies the condition of optimal stationary policies for discrete-time average cost MDPs with countable states, but from the characterization through the dynamic programming equations. For constrained MDPs with countable states and long-run average cost, Borkar (1994) further establishes the existence of stationary randomized policies for the general case of nonnegative cost functions (or unbounded from below), which uses the method of occupation measures. Lasserre (1988) studies the stationary policies of denumerable state MDPs for not only the average cost optimality, but also the Blackwell optimality. Meyn (1999) studies the similar problem based on the stabilization of controlled Markov chains with algorithmic analysis. Cao and Xie (2015) study the existence condition of optimal stationary policies for a class of queueing systems, also from the analysis of system stability. Cavazos-Cadena (1991); Cavazos-Cadena and Sennott (1992) give a fairly complete summary and comparison of different results on existence conditions for discrete-time average cost MDPs with countable state space and finite action sets.

For more general cases rather than countable state space, Hernández-Lerma (1991) studies the existence condition on average cost optimal stationary policies in a class of discrete-time Markov control processes with Borel spaces and unbounded costs, where the action space is assumed setwise continuity instead of a compact set. Feinberg and Lewis (2007) present sufficient conditions for the existence of an optimal stationary policy of MDPs with the average cost optimality inequalities, where the state and action space are Borel subsets of Polish spaces. The derived result is also applied to a cash balance problem with an inventory model. For continuous-time MDPs with infinite state in Polish spaces, Guo and Rieder (2006) study the existence of optimal deterministic stationary policies by using the Dynkin formula and two optimality inequalities for the average cost criterion. Some other systematic discussion on this issue can also be found in the excellent books on MDPs, see Bertsekas (2012); Hernández-Lerma and Lasserre (1996); Puterman (1994); Sennott (1999) for discrete-time MDPs and Bertsekas (2012); Guo and Hernández-Lerma (2009) for continuous-time MDPs.

In summary, most of the existing results are about the sufficient conditions, which usually require constructing a set of functions satisfying several sophisticated assumptions. Although these conditions are quite general, they may be not easy to verify and may encounter difficulty of function construction during the application to practical problems. In this paper, we study the optimality condition of stationary policies for average cost MDPs with countable states and finite actions available at each state. By defining a proper metric in the policy space, we study the continuity of the system’s average cost and the compactness of the policy space, and we show that such continuity and compactness can induce the existence of an optimal stationary policy. We further extend the continuity requirement by assuming some reasonable conditions on transition rates and uniform convergence of un-normalized probabilities in MDPs. Compared with the existing literature work, our result holds at a weak condition of requiring continuity and ergodicity, and it can handle the cost function unbounded from both below and above. While some general results in the literature require the cost function unbounded only from below (e.g., see (Borkar, 1994)) or -geometric ergodicity (e.g., see (Hernández-Lerma and Lasserre, 1999)), which partly demonstrates the advantages of our method. Moreover, our result may be easier to verify for some MDPs, especially for queueing systems. The main results of the paper are illustrated by several examples, for one of which the cost function is unbounded from above and from below, as discussed in Remark 2 at the end of Section 3.

The remainder of the paper is organized as follows. In Section 2, we derive the existence condition by studying the continuity of the average cost in a defined compact metric space of policies. In Section 3, an example of scheduling problem in queueing systems is provided to demonstrate the validation process of our existence condition of an optimal stationary policy. In Section 4, we further extend the existence condition to several reasonable assumptions which may be easy to satisfy in practical problems. Finally, we conclude the paper in Section 5.

2 The Basic Idea

In an MDP, the state space is denoted as , which is assumed to be countably infinite. Without loss of generality, we denote it as . Associated with every state , there is a finite action set . At state , if action is adopted, an instant cost will incur. Meanwhile, the system will transit to state with transition probability for discrete-time MDPs and with transition rate for continuous-time MDPs, respectively. Let denote a (deterministic) stationary policy which is a mapping on such that for all . Let denote the stationary policy space and , with “” being the Cartesian product. Let be the system state at time . Under suitable conditions, the long-run average performance measure for MDPs, which does not depend on any initial state , but depends on , is defined as :

| (1) |

or

| (2) |

for discrete-time and continuous-time ergodic MDPs, respectively, where the expectation operator depends on . However, such dependence is omitted below for notation simplicity. The goal of optimization is to find a policy such that

| (3) |

Assume that is bounded in , so is finite. We aim to find conditions under which such an optimal stationary policy exists.

Theorem 1.

Suppose is a compact metric space and the function is continuous in with the metric, then an optimal policy exists.

Proof: Let . By definition, there exists a sequence of policies, denoted as , , , such that

| (4) |

Because is compact, there is a subsequence of that converges to a limit (accumulation) point. Denote this subsequence as and the limit point as . Then

By continuity of , we have

By (4), we obtain

i.e., is an optimal policy.

Theorem 1 requires a compact metric space defined for . Below, we introduce such a metric in the policy space. Note that a policy can be denoted as

Choosing a real number , (e.g., ), we define the distance between two policies and as

| (5) |

in which

It is easy to verify that

and for any three policies , , and , the following triangle inequality holds

Thus, , , indeed defines a metric on .

Suppose for two policies and , for all . Then

| (6) | |||||

where the last inequality holds because we choose , so . By (6), we have

Lemma 1.

if and only if for all .

Proof: The “If” part follows directly from (6). Now we prove the “Only if” part using contradiction. Assume that there is an integer such that and . By (5), we have , which is in contradiction with the condition . Thus, the assumption is not true and the “Only if” part is proved.

The metric defined by the distance function induces a topology on . First, we define an open ball around a point as

| (7) |

We have for any . A set is called a neighborhood of a point , if there is an open ball for some such that .

By Lemma 1, we have the following fact: for all if and only if .

Remark 1. Lemma 1 reveals the advantage of the metric (5): It shows that all the policies in a small neighborhood of policy take the same actions in the first states. This property is very useful in proving the continuity of in many optimization problems, in which the steady-state probability of state , , goes to zero when goes to infinity; in other words, states are less important.

In a metric space , a limit point can be defined by the metric, i.e., for some sequence , if and only if . In this sense, a continuous function is defined in the same way as a continuous function defined in a real space.

Since is finite and is countable, it is well known that with the metric (5) the policy space is compact. In fact, every point is an accumulation (limit) point, and every policy is in . In order to apply Theorem 1, we have to prove the continuity of in for the specific problems. Below, we use some examples to illustrate the applicability of Theorem 1 in MDPs.

Example 1.

(A modification of Example 8.10.2 in Puterman’s book (Puterman, 1994)) Consider an MDP with . At each state , there are two actions and . If action is taken, then the state transits from to with probability and the cost is ; if action is taken, then the state stays at with probability and the cost is . The Markov chain (under any given policy) is denoted as , . A stationary policy is denoted as a mapping .

The performance measure for policy with initial state is the long-run average

| (8) |

Note that the performance may depend on the initial state, i.e., it is a function of both the initial states and policies. To prove the existence of an optimal policy, we need to fix the initial state. In (8), we choose . We wish to find a policy such that

We need to prove that such an optimal stationary policy exists.

Now, we prove that is continuous in with metric (5). Given a policy , for any small positive , we find the maximum satisfying . By Lemma 1, if we choose a policy satisfying , then all the actions of such policies and at states are the same. By the structure of defined in (8), we can conclude that

More precisely, since for all , we discuss it with two cases. Case 1: If for all , we have , thus . Case 2: If there exists some state such that , we denote the smallest such state as and we have , thus . In summary, for any , take such that , thus for all . Therefore, is continuous at .

Finally, by Theorem 1, the optimal stationary policy exists. Actually, it is easy to verify that the optimal policy is and the corresponding optimal cost is .

Example 2.

(Example 8.10.2 in Puterman’s book (Puterman, 1994)) Consider an MDP with . At state , there are two actions and . If action is taken, then the state transits from to with probability and the reward is ; if action is taken, then the state stays at with probability and the reward is . The Markov chain (under any policy) is denoted as , . A stationary policy is denoted as a mapping .

The performance measure for policy with initial state is the long-run average reward as follows.

| (9) |

We set the initial state always as and we wish to find an policy such that

The discussion is the same as Example 1, except that is NOT continuous at with , while for any neighboring policy with . Therefore, an optimal stationary policy may not exist for this example. Actually, it is easy to verify that the optimal reward of this problem is . A history-dependent policy which uses action 0 times in state , and then uses action 1 once, will yield a reward stream of . Thus, the history-dependent policy can reach the optimal reward . However, any stationary deterministic policy yields possible rewards as either 0 or , which cannot reach the optimal reward .

3 The -Rule in Queueing Systems

In this section, we show that, with the metric space defined by (5), the basic idea presented in Section 2 can be applied to a class of optimal scheduling problems in queueing systems, called the -rule problem, to establish the existence of an optimal stationary policy.

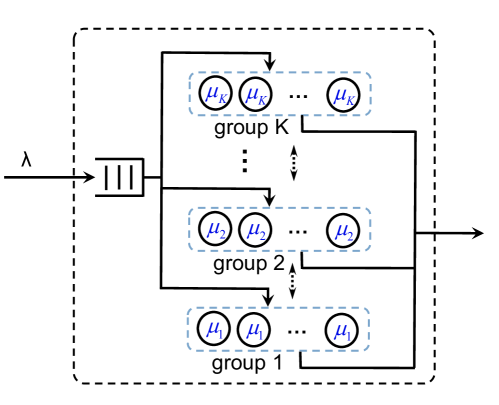

The problem is about the on/off scheduling control of parallel servers in a group-server queue. More details of the problem setting can be referred to (Xia et al, 2018) and we give a brief introduction as follows. Consider a group-server queue with a single infinite-size buffer and groups of parallel servers, as illustrated by Fig. 1. Customers are homogeneous and customer arrival is assumed as a Poisson process with rate . Arriving customers will go to the idle servers at status ‘on’. If all the servers at status ‘on’ are busy, the arriving customer will wait in the buffer. Servers are providing service in parallel and categorized into groups. Servers in the same group are homogeneous in service rates and cost rates, while those in different groups are heterogeneous. Group has servers with service rate and cost rate per unit of time, . Without loss of generality, we assume . The system cost includes two parts, the operating cost of servers and the holding cost of customers. The system state is the number of customers in the system. The state space is denoted as , which is countably infinite. We can turn on or off servers dynamically to reduce the system average cost. The action is the number of working servers at each group, which is denoted as , where is the number of working servers in group and . For any state , action space is a subset of , where is reasonable to guarantee the system ergodic. Define a stationary policy as , where is the action at state and is the number of working servers in group at state . The cost function at state under policy is

| (10) |

where is the holding cost rate at state . The system long-run average cost under policy is defined as

| (11) |

where is the system state at time . The optimal average cost is . We aim at finding the optimal stationary policy which achieves the optimal average cost, i.e., , where and is the stationary policy space. In (Xia et al, 2018), it is shown that the optimal policies (if one exists) follow the so called -rule: Servers in the group with smaller values of should be turned on with higher priority. Here, we want to verify that an optimal stationary policy does exist for this problem with countable states.

It is natural to assume that the holding cost is increasing in ; and thus, under optimal policies the queue should be ergodic. So we assume that is ergodic (under each policy in ) with a unique steady-state distribution , , , and the long-run average (11) does not depend on the initial state.

Since our queue is a birth-death process, we can derive the steady-state distribution as below.

| (12) |

where , and

| (13) |

and

| (14) |

The queue is stable if and only if which also indicates

| (15) |

The ergodicity of the system under a policy can indicate a necessary condition: for all . The stability of the system can be guaranteed by a sufficient condition: there exists an such that for all .

For an ergodic policy , under suitable condition, the long-run average (11) equals

| (16) |

For the analysis here, we need to make the following assumption:

Assumption 1.

We use the metric definition (5) to quantify the distance between any two policies and . In what follows, we will prove that when the two policies and are infinitely close, their performance measures and are also infinitely close to each other. Denote the two policies by and . By Lemma 1, we assume that

| (17) |

which means that .

First, we compare the difference of the normalization factors and of these two policies. We have

| (18) | |||||

where

| (19) |

Similarly, we can also have

| (20) | |||||

where

| (21) |

Therefore, we have

| (22) |

Let be determined by

| (23) |

Then,

| (24) |

With (12), (17), and (23), the steady-state distributions under these two policies and have the following relation.

| (25) |

Next, we study the difference between the associated long-run average costs under policies and . The cost functions are denoted by and , respectively. By (10) and (17), we have for . Therefore, we have

Applying (25), we have

| (26) |

Now we are ready to prove the continuity of in the metric space with metric (5). With (15), we have

Let be any small number. Under Assumption 1, by the uniformity of in (14) and (15), there exists a large integer such that if , we have for any . By (24), we have

Next, because (16) converges, there is a large integer such that

Furthermore, under Assumption 1, by the uniformity of the convergence of (16), there is a large integer such that

Finally, let . Then, by (26) and Lemma 1, we have

| (27) | |||||

Since is bounded, we conclude that is continuous at in the metric space. Therefore, the existence of optimal stationary policy for this -rule problem directly follows by Theorem 1.

Remark 2. The condition of uniform convergence in Assumption 1 is easy to validate in queueing systems. For example, we can set the condition for the control of our group-server queues as follows: \oldstylenums{1}⃝ there exists a constant such that for any , every feasible action always satisfies . Therefore, we define . We directly have , which indicates that the queueing system is stable and the normalizing factor in (14) converges uniformly in . Compared with (12), we further define a pseudo probability . Obviously, we always have for any policy and . Thus, for the performance limit (16), we have , where the first part is always finite and we only need to guarantee the second part bounded. Thus, \oldstylenums{2}⃝ any cost function polynomially increasing to infinity along with will be controlled by the exponential factor . Therefore, with \oldstylenums{1}⃝ and \oldstylenums{2}⃝, we can easily validate Assumption 1 that and converge uniformly, and thus an optimal stationary policy exists. More specifically, for the cost function (10), we have , where the operating cost is obviously bounded and the holding cost can be unbounded. From the above analysis, we can see that can be unbounded from both below and above sides. For example, we can set , which is unbounded both below and above while satisfies our condition \oldstylenums{2}⃝. However, this kind of cost function may not be handled by other methods in the literature (Borkar, 1994) because the cost function thereof is required to be unbounded from below. This is also one of the advantages of our method in this paper.

We have demonstrated the applicability of Theorem 1 for proving the existence of optimal stationary policies in a scheduling problem of queueing systems. In the next section, we further show that this approach also applies to more general cases.

4 More General Cases

In general, we consider a continuous-time MDP with a countable state space denoted as . Let be the steady-state probability of state under given policy , and be the transition rate from state to under action , . Obviously, we have for and , where can be understood as the total rates transiting out from state if action is adopted. Then we know that the steady-state probabilities ’s must satisfy the following equations.

| (28) | |||

| (29) |

where (29) is called a normalization equation. Given a policy , any sequence (depending on ), , that satisfies

| (30) |

is called an un-normalized steady-state vector. From (30), we have

is the steady-state probability.

In the rest of the paper, it is more convenient to deal with the un-normalized vector because it does not contain the denominator. Moreover, it is convenient to set to obtain an un-normalized probability.

First, we make the following assumptions to simplify the problem setting.

Assumption 2.

-

(a)

is bounded, i.e., , for all .

-

(b)

There is an integer such that , for all , and .

Assumption 2(a) indicates that the transition rate from any state has an upper bound , which is reasonable for most cases in practice. Assumption 2(b) means that the transition rate from state back to is 0 if state is far away from state . This assumption is also reasonable in many practical systems, especially it is usually true for queueing systems since state always transits back only to state caused by a service completion event.

Given any , at a state , we may take an action denoted by , which determines the value of , . Then denotes a policy. Let be the space of all policies. The steady-state probability at state is denoted by , which depends on policy . The reward or cost function at state with action is denoted by . We assume that the Markov processes under all policies in are ergodic and the long-run average performance under policy is

| (31) |

Denoting as the un-normalized steady-state vector satisfying (30) under policy , we give one more assumption as follows (cf. Assumption 1).

Assumption 3.

, with , converges uniformly in as , and converges uniformly in , as .

Assumption 3 holds for many Markov systems, especially when the system is stable under the neighborhood of policies. In fact, it holds if there is a sequence, denoted as , , such that and .

Example 3.

Consider a controlled queue with arrival rate and service rate (under a given control policy ) when the number of customers is , . Let be the Markov process of the queue. The un-normalized steady-state vector is . The process is stable if

Therefore, Assumption 3 is the same as Assumption 1, and if there is a bound and state such that for all policies and states , then Assumption 3 holds.

Now, let us understand the role of Assumptions 2 and 3. For any integer , we consider the first equations in (30), where . Given any , by Assumption 2(b), the summation in (30) is over only finitely many states, resulting in

| (32) |

which can be further rewritten as

| (33) |

For (33), the last summation is nonzero only if . Thus, only the last equations in (33) contain nonzero terms of the last summation, whose values are small enough to be ignored, as shown by the following analysis.

For any and , by Assumption 3, there is a large enough such that

| (34) |

By Assumption 2, the last summation of (33) can be written as

| (35) |

Substituting the above result into (33), we see that solving (33) becomes solving the following equations

| (36) |

where we have variables and linear equations. Thus, the variables ’s can be solved and we state the results as (37) in the following lemma, where denotes a function with variables , .

Lemma 2.

Note that we can set for solving (4) since is also a solution to (4) for any feasible solution , where is a constant. Moreover, ignoring the term of , (4) is a set of linear equations determined by the values of . Therefore, for any two policies and such that for all , ’s take the same form for such policies, .

With Assumptions 2 and 3, we can further extend the existence condition of optimal stationary policies in Theorem 1 and derive the following theorem.

Theorem 2.

Proof: Let be any integer and be any small number. Consider any two policies and , which determine the corresponding transition rates and , as well as the steady-state vectors and , respectively. By Lemma 2 and Assumption 3, if is large enough, then we have

and

where and .

By Lemma 1, if and are close enough such that , then for all . This means for all and . Therefore, we have

| (38) |

The rest analysis is similar to (18)–(25). First, we have

and

| (39) | |||||

With (38), we have

If is large enough (i.e., is small enough), it holds

Therefore,

with , where we use the preset condition .

The rest proof follows the same procedure as (20)–(25). First, as in (25), we can derive

| (40) |

where (with a large such that ), when is large enough. Then, similar to (26), we have

| (41) | |||||

Now we are ready to prove the continuity of in the metric space with metric (5). Let be any small number. First, as discussed above, under Assumptions 2 and 3, by the uniformity of , there is a large integer such that if , we have for any and . Next, because converges, there is an such that , for all . Furthermore, under Assumption 3, by the uniformity of the convergence of (31), there is a large such that for all , it holds

Therefore, by (41) and Lemma 1, for , we have

| (42) |

Thus, is continuous at in the metric space, and then the existence of optimal stationary policy follows from Theorem 1.

In summary, we have extended the existence condition of optimal stationary policies for average MDPs with countable state space from Theorem 1 for the -rule problem to Theorem 2 for the more general case. As stated by Assumptions 2 and 3, if the system has bounded and limited-distance backward transition rates, and with the uniformity of the convergence of the un-normalized probabilities and the performance sequences, the existence of optimal stationary policies can be guaranteed by Theorem 2. The theorem may be easily verified in practice, especially for queueing systems, as demonstrated in the aforementioned examples.

5 Conclusion

In this paper, we derive the existence conditions of optimal stationary policies for countable state MDPs with long-run average criterion. By defining a suitable metric on the policy space forming a compact metric space, the existence condition can be guaranteed by proving the continuity of the long-run average cost as a function in the policy space under the metric. With some assumptions on the transition rates and the uniformity of the convergence of the un-normalized probabilities of the processes, the existence of the optimal policies can be proved for the MDPs with countable states in a general form. Compared with other conditions studied in the literature, the condition in this paper may be easier to verify when applied to practical MDP problems, especially in queueing systems. Some examples are studied to illustrate the applicability of our results. Future research topics may include the extensions to MDPs with other criteria, such as the discounted ones.

Acknowledgement

The first author would like to thank Prof. Peter W. Glynn at Stanford University for his comments, which partly initiate the work of this paper.

This work was supported in part by the National Natural Science Foundation of China (11931018, 61573206).

References

- Borkar (1989) Borkar, V. S. (1989). Control of Markov chains with long-run average cost criterion: The dynamic programming equations. SIAM Journal on Control and Optimization, Vol. 27, pp. 642-657.

- Borkar (1994) Borkar, V. S. (1994). Ergodic control of Markov chains with constraints–the general case. SIAM Journal on Control and Optimization, Vol. 32, pp. 176-186.

- Bertsekas (2012) Bertsekas, D. P. (2012). Dynamic Programming and Optimal Control–Vol.2, 4th Edition. Boston: Athena Scientific.

- Cao and Xie (2015) Cao, P. and Xie, J. (2015). A new condition for the existence of optimal stationary policies in denumerable state average cost continuous time Markov decision processes with unbounded cost and transition rates. arXiv:1504.05674.

- Cavazos-Cadena (1991) Cavazos-Cadena, R. Recent results on conditions for the existence of average optimal stationary policies. Annals of Operations Research, Vol. 28, pp. 3-27.

- Cavazos-Cadena and Sennott (1992) Cavazos-Cadena, R. and Sennott, L. I. (1992). Comparing recent assumptions for the existence of optimal stationary policies. Operations Research Letters, Vol. 11, pp. 33-37.

- Feinberg and Lewis (2007) Feinberg, E. A. and Lewis, M. E. (2007). Optimality inequalities for average cost Markov decision processes and the stochastic cash balance problem. Mathematics of Operations Research, Vol. 32, pp. 769-785.

- Golubin (2003) Golubin, A. Y. (2003). A note on the convergence of policy iteration in Markov decision processes with compact action spaces. Mathematics of Operations Research, Vol. 28, pp. 194-200.

- Guo and Rieder (2006) Guo, X. and Rieder, U. (2006). Average optimality for continous-time Markov decision processes in Polish spaces. Annals of Applied Probability, Vol. 16, pp. 730-756.

- Guo and Hernández-Lerma (2009) Guo, X. and Hernández-Lerma, O. (2009). Continuous-Time Markov Decision Processes. Springer.

- Lasserre (1988) Lasserre, J. B. (1988). Conditions for existence of average and Blackwell optimal stationary policies in denumerable Markov decision processes. J. Math. Anal. Appl., Vol. 136, pp. 479-490.

- Meyn (1997) Meyn, S. (1997). The policy iteration algorithm for average reward Markov decision processes with general state space. IEEE Transactions on Automatic Control, Vol. 42, pp. 1663-1680.

- Meyn (1999) Meyn, S. (1999). Algorithms for optimization and stabilization of controlled Markov chains. Sadhana, Vol. 24, pp. 339-367.

- Hernández-Lerma (1991) Hernández-Lerma, O. (1991). Average optimality in dynamic programming on Borel spaces. Systems and Control Letters, Vol. 17, pp. 237-242.

- Hernández-Lerma and Lasserre (1996) Hernández-Lerma, O. and Lasserre, J. B. (1996). Discrete-Time Markov Control Processes: Basic Optimality Criteria. Springer, New York.

- Hernández-Lerma and Lasserre (1999) Hernández-Lerma, O. and Lasserre, J. B. (1999). Further Topics on Discrete-Time Markov Control Processes. Springer, New York.

- Puterman (1994) Puterman, M. L. (1994). Markov Decision Processes: Discrete Stochastic Dynamic Programming. New York: John Wiley & Sons.

- Ross (1971) Ross, S. M. (1971). On the nonexistence of -optimal randomized stationary policies in average cost Markov decision models. The Annals of Math. Statistics, Vol 42, pp. 1767-1768.

- Sennott (1986) Sennott, L. I. (1986). A new condition for the existence of optimum stationary policies in average cost Markov decision processes. Operations Research Letters, Vol. 5, pp. 17-23.

- Sennott (1989) Sennott, L. I. (1989). Average cost optimal stationary policies in infinite state Markov decision processes with unbounded costs. Operations Research, Vol. 37, pp. 626-633.

- Sennott (1999) Sennott, L. I. (1999). Stochastic Dynamic Programming and the Control of Queueing Systems. New York: John Wiley & Sons.

- Xia et al (2018) Xia, L., Zhang, Z. G., Li, Q., and Glynn, P. W. (2018). A c/-rule for service resource allocation in group-server queues. arXiv:1807.05367 [math.OC].