Regularized Online Allocation Problems: Fairness and Beyond

Abstract

Online allocation problems with resource constraints have a rich history in operations research. In this paper, we introduce the regularized online allocation problem, a variant that includes a non-linear regularizer acting on the total resource consumption. In this problem, requests repeatedly arrive over time and, for each request, a decision maker needs to take an action that generates a reward and consumes resources. The objective is to simultaneously maximize additively separable rewards and the value of a non-separable regularizer subject to the resource constraints. Our primary motivation is allowing decision makers to trade off separable objectives such as the economic efficiency of an allocation with ancillary, non-separable objectives such as the fairness or equity of an allocation. We design an algorithm that is simple, fast, and attains good performance with both stochastic i.i.d. and adversarial inputs. In particular, our algorithm is asymptotically optimal under stochastic i.i.d. input models and attains a fixed competitive ratio that depends on the regularizer when the input is adversarial. Furthermore, the algorithm and analysis do not require convexity or concavity of the reward function and the consumption function, which allows more model flexibility. Numerical experiments confirm the effectiveness of the proposed algorithm and of regularization in an internet advertising application.

1 Introduction

Online allocation problems with resource constraints have abundant real-world applications and, as such, have been extensively studied in computer science and operations research. Prominent applications can be found in internet advertising (Feldman et al., 2010), cloud computing (Badanidiyuru et al., 2018), allocation of food donations to food banks (Lien et al., 2014), rationing of a social goods during a pandemic (Manshadi et al., 2021), ride-sharing (Nanda et al., 2020), workforce hiring (Dickerson et al., 2019), inventory pooling (Jiang et al., 2019) among others.

The literature on online allocation problems focuses mostly on optimizing additively separable objectives such as the total click-throughout rate, revenue, or efficiency of the allocation. In many settings, however, decision makers are also concerned about ancillary objectives such as fairness across agents, group-level fairness, avoiding under-delivery of resources, balancing the load across servers, or avoiding saturating resources. These metrics are, unfortunately, non-separable and cannot be readily accommodated by existing algorithms that are tailored for additively separable objectives. Thus motivated, in this paper, we introduce the regularized online allocation problem, a variant that includes a non-linear regularized acting on the total resource consumption. The introduction of a regularizer allows the decision maker to simultaneously maximize an additively separable objective together with other metrics such as fairness and load balancing that are non-linear in nature.

More formally, we consider a finite horizon model in which requests arrive repeatedly over time. The decision maker is endowed with a fixed amount of resources that cannot be replenished. Each arriving request is presented with a non-linear reward function and a consumption function. After observing the request, the decision makers need to take an action that generates a reward and consumes resources. The objective of the decision maker is to maximize the sum of the cumulative reward and a regularizer that acts on the total resource consumption. (Our model can easily accommodate a regularizer that acts on other metrics such as, say, the cumulative rewards by adding dummy resources.)

Motivated by practical applications, we consider an incomplete information model in which requests are generated from an input model that is unknown to the decision maker. That is, when a request arrives, the decision maker observes the reward function and consumption function of the request before taking an action, but does not get to observe the reward functions and consumption matrices of future requests until their arrival. The objective of this paper is to design simple algorithms that attain good performance relative to the best allocation when all requests are known in advance.

1.1 Main Contributions

The main contributions of the paper can be summarized as follows:

-

1.

We introduce the regularized online allocation problem and discuss various practically relevant economic examples (Section 2). Our proposed model allows the decision maker to simultaneously maximize an additively separable objective together with an non-separable metric, which we refer to as the regularizer. Furthermore, we do not assume the reward functions nor the consumption functions to be convex/concave—a departure from related work.

-

2.

We derive a dual problem for the regularized online allocation problem, and study its geometric structure as well as its economic implications (Section 3 and Section 4.1). Due to the existence of a regularizer, the dual variables (i.e., the opportunity cost of resources) no longer necessarily lie in the positive orthant and can potentially be negative, unlike traditional online allocation problems.

-

3.

We propose a dual mirror descent algorithm for solving regularized online allocation problems that is simple and efficient, can better capture the geometry of the dual feasible region, and achieves good performances for various input models:

-

•

Our algorithm is efficient and simple to implement. In many cases, the update rule can be implemented in linear time and there is no need to solve auxiliary optimization problems on historical data as in other methods in the literature.

-

•

The dual feasible region can become complicated for regularized problems. By suitably picking the reference function in our mirror descent algorithm, we can adjust the update rule to better capture the geometry of the dual feasible set and obtain more tractable projection problems.

-

•

When the input is stochastic and requests are drawn are independent and identically drawn from a distribution that is unknown to the decision maker, our algorithm attains a regret of the order relative to the optimal allocation in hindsight where is the number of requests (Section 5.1). This rate is unimprovable under our minimal assumptions on the input. On the other extreme, when requests are adversarially chosen, no algorithm can attain vanishing regret, but our algorithm is shown to attain a fixed competitive ratio that depends on the structure of the regularizer, i.e., it guarantees a fixed fraction of the optimal allocation in hindsight (Section 5.2).

-

•

We numerically evaluate our algorithm on an internet advertising application using a max-min fairness regularizer. Our experiments confirm that our proposed algorithm attains regret under stochastic inputs as suggested by our theory. By varying the weight of the regularizer, we can trace the Pareto efficient frontier between click-through rates and fairness. An important managerial takeaway is that fairness can be significantly improved while only reducing click-through rates by a small amount.

-

•

Our model is general and applies to online allocation problems across many sectors. We briefly discuss some salient applications. In display advertising, a publisher typically signs contracts with many advertisers agreeing to deliver a fixed number of impressions within a limited time horizon. Impressions arrive sequentially over time and the publisher needs to assign, in real time, each impression to one advertiser so as to maximize metrics such as the cumulative click-through rate or the number of conversions while satisfying contractual agreements on the number of impressions to be delivered (Feldman et al., 2010). Focusing on maximizing clicks can lead to imbalanced outcomes in which advertisers with low click-through rates are not displayed or to showing ads to users who are most likely to click without any equity considerations (Cain Miller, 2015). We propose mitigating these issues using a fairness regularizer. Additionally, by incorporating a regularizer, publishers can punish under-delivery of advertisements—a common desiderata in internet advertising markets. Another related advertising application is bidding in repeated auctions with budgets constraints, where the regularizer can penalize the gap between the true spending and the desired spending (Grigas et al., 2021) or model advertisers’ preferences to reach a certain distribution of impressions over a target population of users (Celli et al., 2021).

In cloud computing, jobs arriving online need to be scheduled to one of many servers. Each job consumes resources from the server, which need to be shared with other jobs. The scheduler needs to assign jobs to servers to maximize metrics such as the cumulative revenue or efficiency of the allocation (Xu and Li, 2013). When jobs’ processing times are long compared to their arrival rates, this scheduling problem can be cast as an online allocation problem (Badanidiyuru et al., 2018). Regularization allows to balance the load across resources to avoid saturating them, to incorporate returns to scale in resource utilization, or to guarantee fairness across users (Bateni et al., 2018).

Finally, in humanitarian logistics, limited supplies need to be distributed to agents repeatedly over time. Maximizing the economic efficiency of the allocation can lead to unfair outcomes in which some agents or groups of agents receive lower relative amount of supplies. For example, during the Covid-19 pandemic, supply-demand imbalance leading to the rationing of medical supplies and allocating resources fairly was a key consideration for decision makers (Emanuel et al., 2020; Manshadi et al., 2021). In these situations, incorporating a fairness regularizer that maximizes the minimum utility across agents (or groups of agents) can lead to more egalitarian outcomes while slightly sacrificing economic efficiency (Bateni et al., 2018).

1.2 Related Work

| Resource | Input | |||

| Papers | Objective | constraints | model | Results |

| Mehta et al. (2007); Buchbinder et al. (2007); Feldman et al. (2009); Ball and Queyranne (2009); Ma and Simchi-Levi (2020) | Separable | Hard | Adversarial | Fixed comp. ratio |

| Devanur and Hayes (2009); Feldman et al. (2010); Agrawal et al. (2014); Devanur et al. (2019); Jasin (2015); Li and Ye (2019); Li et al. (2020) | Separable | Hard | Stochastic | Sublinear regret |

| Mirrokni et al. (2012); Balseiro et al. (2020) | Separable | Hard | Stochastic/ | Sublinear regret/ |

| Adversarial | Fixed comp. ratio | |||

| Jenatton et al. (2016); Agrawal and Devanur (2015); Cheung et al. (2020) | Non-separable | Soft | Stochastic | Sublinear regret |

| Devanur and Jain (2012); Eghbali and Fazel (2016) | Non-separable | Soft | Adversarial | Fixed comp. ratio |

| Tan et al. (2020) | Non-separable | Hard | Adversarial | Fixed comp. ratio |

| This paper | Non-separable | Hard | Stochastic/ | Sublinear regret/ |

| Adversarial | Fixed comp. ratio |

Online allocation problems have been extensively studied in computer science and operations research literature. Table 1 summarizes the differences between our work and the existing literature on online allocation problems.

Stochastic Input. Most work on the traditional online allocation problem with stochastic input models focus on time-separable and linear reward functions, i.e., the case when the reward function is a summation over all time periods and is linear in the decision variable (Devanur and Hayes, 2009; Feldman et al., 2010; Agrawal et al., 2014; Jasin, 2015; Devanur et al., 2019; Li and Ye, 2019). The algorithms in these works usually require resolving large linear problems periodically using all samples collected so far to update the dual variables or to estimate the distribution of requests. More recently, Balseiro et al. (2020) studied a simple dual mirror descent algorithm for online allocation problems with separable, non-linear reward functions, which attains regret and has no need of solving any large program using all previous samples. Simultaneously, Li et al. (2020) presented a similar subgradient algorithm that attains regret for linear reward. Our algorithm is similar to theirs in that it does not require to solve large problems using all data collected so far.

Compared to the above works, we introduce a regularizer on top of the traditional online allocation problem. The regularizer can be viewed as a reward that is not separable over time. The existence of such non-separable regularizer makes the theoretical analysis harder compared to traditional dual-based algorithms for problems without regularizers because dual variables, which correspond to the opportunity cost that a unit of resource is consumed, can be negative due to the existence of the regularizer. We present a in-depth characterization on the geometry of the dual problem (see Section 3.1), which allows us to get around this issue in the analysis.

Another related work on stochastic input models is Agrawal and Devanur (2015), where the focus is to solve general online stochastic convex program that allows general concave objectives and convex constraints. When the value of the benchmark is known, they present fast algorithms; otherwise, their algorithms require periodically solving large convex optimization problems with the data collected so far to obtain a good estimate of the benchmark. In principle, our regularized online allocation problem (see Section 2 for details) can be reformulated as an instance of the online stochastic convex program presented in Agrawal and Devanur (2015). Such reformulation makes the algorithms proposed in Agrawal and Devanur (2015) more complex than ours as they require keeping track of additional dual variables and solving convex optimization programs on historical data (unless the optimal value of the objective is known). Moreover, their algorithms treat resource constraints as soft, i.e., they allow the constraints to be violated and then prove that constrains are violated in expectation, by an amount sublinear in the number of time periods . Instead, in our setting, resource constraints are hard and cannot be violated, which is a fundamental requirement in many applications. Additionally, our proposed algorithm is simple, fast, and does not require estimates of the value of the benchmark nor solving large convex optimization problems. Along similar lines Jenatton et al. (2016) studies a problem with soft resource constraints in which violations of the constraints are penalized using a non-separable regularizer. Thus, different to our paper, they allow the resource constraints to be violated. They provide a similar algorithm to ours, but their regret bounds depend on the optimal solution in hindsight, which, in general, it is hard to control. Finally, Cheung et al. (2020) design similar dual-based online algorithms for non-separable objectives with soft resource constraints when offline samples from the distribution of requests are available.

Adversarial Inputs. Most of the previous works on online allocation problems with adversarial inputs focus on separable objectives. There is a stream of work studying the AdWords problem, the case when the reward and the consumption are both linear in decisions and reward is proportional to consumption (Mehta et al., 2007; Buchbinder et al., 2007; Feldman et al., 2009; Mirrokni et al., 2012), revenue management problems (Ball and Queyranne, 2009; Ma and Simchi-Levi, 2020), or more general separable objectives with non-linear reward and consumption functions (Balseiro et al., 2020). Compared to the above work, we include a non-separable regularizer. Similar to the stochastic setting, the existence of such non-separable regularizer makes the competitive ratio analysis more challenging than the one without the regularizer. As opposed to the stochastic setting in which vanishing regret can be achieved for most concave regularizers, in the adversarial case the competitive ratio heavily depends on the structure of the regularizer. In particular, Mirrokni et al. (2012) shows that no online algorithm can obtain both vanishing regret under stochastic input and can attain a data-independent constant competitive ratio for adversarial input for the AdWords problem. While AdWords problem is a special case of our setting, our results do not contradict their findings because our competitive ratio depends on the data, namely, the consumption-budget ratio.

There have been previous works studying online allocation problems with non-separable rewards in the adversarial setting, but most impose more restrictive assumptions on the objective function, which preclude some of the interesting examples we present in Section 2.1. For example, Devanur and Jain (2012) study a variant of the AdWords problem in which the objective is concave and monotone over requests but separable over resources. Eghbali and Fazel (2016) extend their work by considering more general non-separable concave objectives, but still require the objective to be monotone and impose restrictive assumptions on the reward function. Even though they do not consider hard resource constraints, they provide similar primal-dual algorithms that are shown to attain fixed competitive ratios. Tan et al. (2020) studies a similar problem as our regularized online allocation setting, but restrict attention to one resource.

Fairness Objectives. While most of the literature on online allocation focuses on maximizing an additively separable objective, other features of the allocation, such as fairness and load balancing, sometimes are crucial to the decision maker. Fairness, in particular, is a central concept in welfare economics. Different reasonable metrics of equity have been proposed and studied: max-min fairness, which maximizes the reward of the worst-off agents (Nash Jr, 1950; Bansal and Sviridenko, 2006); proportional fairness, which makes sure that there is no alternative allocation that can lead to a positive aggregate proportional change for each agent (Azar et al., 2010; Bateni et al., 2018); or -fairness, which generalizes the previous notions (Mo and Walrand, 2000; Bertsimas et al., 2011, 2012), and allows to recover max-min fairness and proportional fairness as special cases when and , respectively. The above line of work focuses on optimizing the fairness of an allocation problem (without considering the revenue) in either static settings, adversarial settings, or stochastic settings that are different to ours. In contrast, our framework is concerned with maximizing an additively separable objective but with an additional regularizer corresponding to fairness (or other desired ancillary objective).

A related line of work studies online allocation problems with fairness, equity, or diversity objectives in Bayesian settings in which the distribution of requests is known to decision makers. Lien et al. (2014) and Manshadi et al. (2021) study the sequential allocation of scarce resources to multiple agents (requests) in nonprofit applications such as distributing food donations across food banks or medical resources during a pandemic. They measure the equity of an allocation using the max-min fill rate across agents, where the fill rate is given by the ratio of allocated amount to observed demand, and design algorithms when the distribution of demand is non-stationary and potentially correlated across agents. In contrast to our work, fairness is measured across requests as opposed to across resources. Relatedly, Ahmed et al. (2017) and Dickerson et al. (2019) design approximation algorithms for stochastic online matching problems with submodular objective functions. Submodular objectives allow the authors to incorporate the fairness, relevance, and diversity of an allocation in applications related to advertising, recommendation systems, and workforce hiring. Ma and Xu (2020) consider stochastic matching problems with a group-level fairness objective, which involves maximizing the minimum fraction of agents served across various demographic groups. The authors design approximation algorithms with fixed competitive ratios when the distribution of requests is known in advance. Group-level fairness objectives can be incorporated in our model by adding a dummy resource for each group and then using a max-min fairness regularizer. Nanda et al. (2020) provide an algorithm that can optimally tradeoff the profit and group-level fairness of an allocation for online matching problems and present an application to ride-sharing. Our algorithm is asymptotically optimal for group-level fairness regularizers when the number of groups is sublinear in the number of requests. Agrawal et al. (2018) presents a simple proportional allocation algorithm with high entropy to increase the diversity of the allocation for the corresponding offline problem where all requests are known to the decision maker beforehand.

Preliminary Version. In a preliminary conference proceedings version of this paper (Balseiro et al., 2021), we present the basic setup of the regularized online allocation problem and the regret analysis for online subgradient descent under stochastic i.i.d. inputs. This paper extends the preliminary proceeding version by (i) introducing a competitive analysis for adversarial inputs, (ii) providing an in-depth study of the geometric structure of the dual problem, (iii) modifying the algorithm and its ensuing analysis to include online mirror descent, which leads to iterate updates with closed-form or simpler solutions.

2 Problem Formulation and Examples

We consider a generic online allocation problem with a finite horizon of time periods, resource constraints, and a concave regularizer on the resource consumption. At time , the decision maker receives a request where is a non-negative (and potentially non-concave) reward function and is an non-negative (and potentially non-linear) resource consumption function, and is a (potentially non-convex or integral) decision set. We denote by the set of all possible requests that can be received. After observing the request, the decision maker takes an action that leads to reward and consumes resources. The total amount of resources is , where is a positive resource constraint vector. The assumption implies that we cannot replenish resources once they are consumed. We assume that and . The above assumption implies that we can always take a void action by choosing to make sure we do not exceed the resource constraints. This guarantees the existence of a feasible solution.

Assumption 1 (Assumptions on the requests).

There exists and such that for all requests in the support, it holds for all , and for all .

The upper bounds and impose regularity on the space of requests and will appear in the performance bounds we derive. They need not be known by the algorithm. We denote by the norm and the norm of a vector.

An online algorithm makes, at time , a real-time decision based on the current request and the previous history , i.e.,

| (1) |

Note that when taking an action, the algorithm observes the current request but has no information about future ones. For example, in display advertising, publishers can estimate, based on the attributes of the visiting user, the click-through rates of each advertiser before assigning an impression. However, the click-through rates of future impressions are not known in advance as these depend on the attributes of the unknown, future visitors. Similar information structures arise in cloud computing, ride-sharing, etc.

For notational convenience, we utilize to denote the inputs over time . We define the regularized reward of an algorithm for input as

where is computed by (1). Moreover, algorithm must satisfy constraints and for every . While the regularizer is imposed on the average consumption, our model is flexible and can accommodate regularizers that act on other quantities such as total rewards by introducing dummy resource constraints (see Example 6 for more details).

The baseline we compare with is the reward of the optimal solution when the request sequence is known in advance, which amounts to solving for an allocation that maximizes the regularized reward subject to the resource constraints under full information of all requests:

| (2) | ||||

| s.t. |

The latter problem is referred to as the offline optimum in the computer science or hindsight optimum in the operations research literature.

Our goal is to design an algorithm that attains good performance, while satisfying the resource constraints, for the stochastic i.i.d. input model and the adversarial input model. The notions of performance depend on the input models and, as such, they are formally introduced in Sections 5.1 and 5.2 where the input models are presented.

2.1 Examples of the Regularizer

We now present some examples of the regularizer. To guarantee that the total rewards are non-negative we shift all regularizers to be non-negative. Many of our results can also be extended to negative regularizers. First, by setting the regularizer to zero, we recover a standard online allocation problem.

Example 1 (No Regularizer).

When the regularizer is , we recover the non-regularized online allocation problem.

Our next example allows for max-min fairness guarantees, which have been studied extensively in the literature (Nash Jr, 1950; Bansal and Sviridenko, 2006; Mo and Walrand, 2000; Bertsimas et al., 2011, 2012). Here we state the regularizer in terms of consumption, which seeks to maximize the minimum relative consumption across resources. In many settings, however, it is reasonable to state the fairness regularizer in terms of other quantities such as the cumulative utility of individual agents or the amount of resources delivered to different demographic groups, i.e., group-level fairness. As discussed in Example 6, such regularizers can be easily accommodated by introducing dummy resource constraints.

Example 2 (Max-min Fairness).

The regularizer is defined as , i.e., the minimum relative consumption. This regularizer imposes fairness on the consumption between different resources, making sure that no resource gets allocated a too-small number of units. Here is a parameter that captures importance of the regularizer relative to the rewards.

In applications like cloud computing, the load should be balanced across machines to avoid congestion. The following regularizer is reminiscent of the makespan objective in machine scheduling. The load balancing regularizer seeks to maximize the minimum relative availability across resources or, alternatively, minimize the maximum relative consumption across resources.

Example 3 (Load Balancing).

The regularizer is defined as , i.e., the minimum relative resource availability. This regularizer guarantees that consumption is evenly distributed across resources by making sure that no resource is too demanded.

In some settings, like cloud computing, firms would like to avoid saturating resources because the costs of utilizing the resource exhibit a decreasing return to scale or to keep some idle capacity to preserve flexibility. The next regularizer allows to capture situations in which it is desired to keep resource consumption below a target.

Example 4 (Below-Target Consumption).

The regularizer is defined as with thresholds and unit reward . This regularizer can be used when the decision maker receives a reward for reducing each unit of resource below a target .

To maximize reach, internet advertisers, in some cases, prefer that their budgets are spent as much as possible or their reservation contracts are delivered as many impressions as possible. We can incorporate these features by rewarding the decision making whenever the target is met.

Example 5 (Above-Target Consumption).

The regularizer is defined as with thresholds and unit reward . This regularizer can be used when the decision maker would like to consume at least units of resource and the decision maker is offered a unit reward of for each unit closer to the target.

The regularizers in the previous examples act exclusively on resource consumption. The next example shows that by adding dummy resource constraints that never bind, it is possible to incorporate regularizers that act on other quantities.

Example 6 (Santa Claus Regularizer from Bansal and Sviridenko 2006).

There are agents (i.e., the kids) and the decision maker (i.e., Santa Claus) intends to make sure the minimal reward (i.e., the presents) of each agent is not too small. Here we consider an additional reward function that gives the reward vector for each agent under decision . To reduce such problem to our setting, we first add auxiliary resource constraints that never bind, where is a uniform upper bound on the additional rewards and is the all-one vector. Then, the regularizer is .

3 The Dual Problem

Our algorithm is of dual-descent nature and, thus, the Lagrangian dual problem of (2) and its constraint set play a key role. We construct a Lagrangian dual of (2) by introducing an auxiliary variable satisfying that captures the time-averaged resource consumption and then move the constraints to the objective using a vector of Lagrange multipliers . The auxiliary primal variable and the dual variable are key ingredients of our algorithm. For we define

| (3) |

as the optimal opportunity-cost-adjusted reward of request . The function is a generalization of the convex conjugate of the function that takes account of the consumption function and the constraint space . We define

| (4) |

as the conjugate function of the regularizer . Define as the set of dual variables for which the conjugate of the regularized is bounded. For a fixed input , define the Lagrangian dual function as

Then, we have by weak duality that provides an upper bound on . To see this, note that for every we have that

| (5) | ||||

where the first inequality is because we relax the constraint , and the last equality utilizes the definition of and .

3.1 Characterization of the Dual Problem

In this section, we prove some preliminary properties that elucidate how the choice of a regularizer impacts the geometry of the dual feasible region , which is important for our algorithm and its ensuing analysis. Throughout the paper we assume the following conditions on the regularizers. As we shall see in Section 4.1, these conditions are satisfied by all examples discussed in the paper.

Assumption 2 (Assumptions on the regularizer ).

We assume the regularizer and the set satisfy:

-

1.

The function is -Lipschitz continuous in the -norm on its effective domain, i.e., for any .

-

2.

There exists a constant such that for any , there exists such that .

-

3.

There exists such that for all .

-

4.

The function is concave.

The first part imposes a continuity condition on the regularizer, which is a standard assumption in online optimization. We choose to use the norm in order to be consistent with Assumption 1, where we chose this norm to measure consumption (i.e., ). The second part guarantees that the conjugate of the regularizer has a bounded subgradient, which is a technical assumption required for our analysis, while the last part imposes that the regularizer is non-negative and upper-bounded. The assumption that the regularizer is non-negative is required for the analysis of our algorithm when the input is adversarial (as competitive ratios are not well defined when rewards can be negative). Our results for stochastic inputs hold without this assumption.

The next result provides a partial geometric characterization of the dual feasible region. Figure 1 plots the domain for a typical two-dimensional regularizer.

Lemma 1.

The following hold:

-

(i)

The set is convex and positive orthant is inside the recession cone of , i.e., .

-

(ii)

, where is the all-one vector in .

-

(iii)

Let . If , then .

-

(iv)

For any , we have that , where is the negative part of .

Property (i) shows that the feasible set is convex, which is useful from an optimization perspective, and unbounded as, for every point, all coordinate-wisely larger points lie in it. The Lipschitz continuity constant of the regularizer plays a key role on the geometry of the dual feasible set. In the case of no regularizer, we have and the properties (ii) and (iv) give that the dual feasible set is the non-negative orthant . This recovers the well-known result that the opportunity cost of consuming a unit of resource is non-negative in allocation problems. As we shall see, with the introduction of a regularizer the opportunity costs might be negative, which could induce a decision maker to consume resources even when these generate no reward. For example, in the case of max-min fairness, a resource with low relative consumption might be assigned a negative dual variable to encourage the decision maker to increase its consumption and, thus, increase fairness. Property (iv) limits how negative dual variables can get. In particular, it implies that for every resource . In other cases, the regularizer can force the dual variables to be larger than zero to reduce the rate of resource consumption. For example, in the case of load balancing, setting the opportunity costs to zero can lead to resource saturation and, as a result, the dual feasible set is a strict subset of the non-negative orthant. Property (ii) upper bounds the minimum value that dual variables can take. Taken together, properties (ii) and (iii) provide bounds on the lower boundary of the dual feasible region in terms of the Lipschitz constant. See Figure 1 for an illustration. We defer an explanation of property (iv) until the next section.

4 Algorithm

| (6) | ||||

| (9) | ||||

| (10) |

Algorithm 1 presents the main algorithm we study in this paper. Our algorithm keeps a dual variable for each resource that is updated using mirror descent (Hazan et al., 2016).

At time , the algorithm receives a request , and computes the optimal response that maximizes an opportunity cost-adjusted reward of this request based on the current dual solution according to equation (6). When the dual variables are higher, the algorithm naturally takes decisions that consume less resources. It then takes this action (i.e., ) if the action does not exceed the resource constraint, otherwise it takes a void action (i.e., ). Additionally, it chooses a target resource consumption by maximizing the opportunity-cost adjusted regularized (in the next subsection we give closed-form expressions for for the regularizers we consider).

Writing the dual function as where the -th term of the dual function is given by , it follows that is subgradient of at whenever decisions are not constrained by resources. To see this, notice that it follows from the definition of conjugate function (3) that and . Therefore

Finally, the algorithm utilizes to update the dual variable by performing the online dual mirror descent descent step in (10) with step-size and reference function .

Intuitively, by minimizing the dual function the algorithm aims to construct good dual solutions which, in turn, would lead to good primal performance. The mirror descent step (10) updates the dual variable by moving in the opposite direction of the gradient (because we are minimizing the dual problem) while penalizing the movement from the current solution using the Bregman divergence. Dual variables are projected to the set to guarantee dual feasibility. The target resource consumption and the geometry of dual feasible set capture the tension between reward maximization and the regularizer.

When the optimal dual variables are interior, by minimizing the dual function, the algorithm strives to make subgradients vanishing or, equivalently, set the consumption close to the target resource consumption, i.e., . Conversely, when optimal dual variables lie in the boundary of , we have that because the non-negative orthant lies in the recession cone of . By definition, we know that , which guarantees that the resource constraints are satisfied, i.e., on average at most unit of resources should be spent per time period. The actual value of target resource consumption is dynamically adjusted based on the dual variables and the regularizer.

In most of our examples, the regularizer plays an active role when the dual variables are low. When the dual variables are higher than the marginal contribution of the regularizer (as captured by its Lipschitz constant), property (iv) of Lemma 1 implies that and decisions are made to satisfy the resource constraints. Moreover, in this case the projection onto does not play a role because dual variables are far from the boundary. This property is intuitive: a high opportunity cost signals that resources are scarce and, as a result, maximizing rewards subject to resource constraints—while ignoring the regularizer—becomes the primary consideration.

Assumption 3 presents the standard requirements on the reference function for an online mirror descent algorithm:

Assumption 3 (Assumptions on reference function ).

The reference function satisfies:

-

1.

is either differentiable or essentially smooth in .

-

2.

is -strongly convex in -norm in , i.e., for any .

Strong convexity of the reference function is a standard assumption for the analysis of mirror descent algorithms (Bubeck, 2015). The previous assumptions imply, among other things, that the projection step (10) of the algorithm always admits a solution. To see this, note that continuity of the regularizer implies that is closed by Proposition 1.1.6 of Bertsekas (2009). The objective is continuous and coercive. Therefore, the projection problem admits an optimal solution by Weierstrass theorem. We here use the norm to define strong convexity in the dual space (i.e., in -space), which is the dual norm of the norm that, in turn, is the norm used in the primal space as per Assumption 1.

Algorithm 1 only takes an initial dual variable and a step-size as inputs, and is thus simple to implement. In practice, the step-size can be tuned, similar to other online first-order methods. We analyze the performance of our algorithm in the Section 5. In some cases, though, the constraint set can be complicated, but a proper choice of the reference function may make the descent step (10) easily computable (in linear time or with a closed-form solution). In the rest of this section, we discuss the constraint sets and suitable references function for each of the examples.

4.1 Application of the Example Regularizers

We now apply Algorithm 1 to each of the examples presented in Section 2.1. For each of these examples, we characterize the dual feasible set and the target resource consumption . Notice that with the introduction of a regularizer, the dual constraint set can become complex. For example, when the regularizer is max-min fairness, the set is a polytope with exponentially many cuts. As a result, the projection step in (10) sometimes may be difficult. Fortunately, mirror descent allows us to choose the reference function to capture the geometry of the feasible set, and a suitable reference function can get around such issues. Next, we present different choices of reference functions for each example, such that (10) has either closed-form solution or it can be solved by a simple optimization program. Proofs of all mathematical statements are available in Appendix B.

Example 1 (No Regularizer).

When , we have that and, for , and . In this case, the algorithm always uses as the target resource consumption, i.e., it aims to deplete resources per unit of time. The projection to the non-negative orthant can be computed in closed form. If we choose the reference function to be the squared Euclidean norm , the update (10) has the closed-form solution , where the maximum is to be interpreted coordinate-wise. This recovers online subgradient descent. If we choose the reference function to be the negative entropy , the update (10) has the closed-form solution where denotes the coordinate-wise product. This recovers the multiplicative weights update algorithm.

Example 2 (Max-min Fairness).

When , then , and, for , and . As a result, the target resource consumption is always set to and the regularizer impacts the decisions of the algorithm via the feasible region . To gain some intuition, note that the feasible set can be alternatively written as because only the constraints for resources with negative dual variables can bind in the original polyhedral representation (this set resembles the lower dotted boundary in Figure 1). Therefore, for any single resource we have that . By letting dual variables go below zero, the algorithm can force the consumption of a resource to increase. The intuition is simple: even if consuming a resource might not beneficial in terms of reward, increasing consumption can increase fairness. The constraint bounds the total negative contribution of dual variables and indirectly guarantees that only resources with the lowest relative levels of consumption are prioritized.

Note that there are exponential number of linear constraints in the domain . Fortunately, we can get around this issue when the reference function is chosen to have the form for some convex function by utilizing the fact that is coordinate-wisely symmetric in , where is the coordinate-wise product.

To obtain , we first compute the dual update without projection as

| (11) |

where is the convex conjugate of the reference function (see, e.g., Boyd et al. 2004, Excercise 3.40). Then, it holds that

| (12) |

After rescaling with , both the reference function and the domain are coordinate-wisely symmetric. Therefore, the projection problem (12) keeps the order of as is monotone.111This can be easily seen by contradiction as following: Suppose there exists such that and . Consider the solution which is equal to except on the coordinates and , in which we set and , then it holds by the symmetry of in that , and moreover, it holds that where the last inequality is due to the strong convexity of . This contradicts with the optimality of as given in equation (12). Therefore, if we relabel indices so that is sorted in non-decreasing order, i.e., we can reformulate (12) as:

| s.t. |

In particular, when , the latter problem is a -dimensional convex quadratic programming with constraints, which can be efficiently solved by convex optimization solvers.

Example 3 (Load Balancing).

When , then , and, for , and . As in the case of the fairness regularizer, the target resource consumption is always set to and the regularizer impacts the decisions of the algorithm via the feasible region . The feasible region is the non-negative orthant minus a scaled simplex with vertices . Recall that the load balancing regularizer seeks to maximize the minimum relative resource availability. When the opportunity cost of any single resource is very large, in the sense that for some , resource is so scarce that increasing its availability is not beneficial. In this case, resource would end up being fully utilized and, because the regularizer is zero, load balancing no longer plays a role in the algorithm’s decision. The load balancing regularizer kicks in when all resources are not-too-scarce. Recall that resources with typical consumption below the target would have dual variables close to zero. Therefore, to balance the load, the dual variables are increased so that the relative consumption of the resources match.

In this case is a polyhedron with a linear number of constraints and (10) can be computed by solving a simple quadratic program if we employ the squared weighted Euclidean norm as a regularizer. Interestingly, using a scaled negative entropy we can compute the update in closed form. In particular, consider the reference function . Let be the dual update without the projection as in (11), which in this case is given by . Then, the dual update is obtained by solving (12), which amounts to projecting back to the scaled unit simplex. For the scaled negative entropy, we have:

and, as a result, the dual update can be performed efficiently without solving an optimization problem.

Example 4 (Below-Target Consumption).

When , then and, for , and if and if . In this case, the dual feasible set is the non-negative orthant as in the case of no regularization. Therefore, the projection can be conducted as in Example 1. The regularizer impacts the algorithm’s decision by dynamically adjusting the target resource consumption . Recall that the purpose of the below-target regularizer is to reduce resource utilization by granting the decision maker a reward for reducing each unit of resource below a target . If the opportunity cost of resources is above , then reducing resource consumption is not beneficial and the target is set to . Conversely, if the opportunity costs of resources are below , then the target is set to and the algorithm reduces the resource consumption to match the target. Note that reducing the target to leads to smaller subgradients , which, in turn, increases future dual variables. This self-correcting feature of the algorithm guarantees that the target is reduced to , which can be costly reward-wise, only when economically beneficial.

Example 5 (Above-Target Consumption).

When , then and, for , and if and if . In this case, the dual feasible region is the shifted non-negative orthant and subgradient descent (i.e., a squared Euclidean norm) gives a closed-form solution to (10). The objective of the above-target regularizer is to increase resource consumption by offering a unit reward of for each unit closer to the target . Because the regularizer encourages resource consumption, the dual variables can be negative and, in particular, . If the dual variable of a resource is negative, increasing resource consumption beyond the target is not beneficial and the target is set to . When the dual variables are positive, the algorithm behaves like the case of no regularization.

5 Theoretical Results

We analyze the performance of our algorithm under stochastic and adversarial inputs. We shall see that our algorithm is oblivious to the input model and attains good performance under both inputs without knowing in advance which input model it is facing.

5.1 Stochastic I.I.D. Input Model

In this section, we assume that requests are independent and identically distributed (i.i.d.) from a probability distribution that is unknown to the decision maker, where is the space of all probability distributions over the support set . We measure the regret of an algorithm as the worst-case difference over distributions in , between the expected performance of the benchmark and the algorithm:

We say an algorithm is low regret if the regret grows sublinearly with the number of periods. The next theorem presents the worst-case regret bound of Algorithm 1.

Theorem 1.

Consider Algorithm 1 with step-size and initial solution . Suppose Assumptions 1-2 are satisfied. Then, it holds for any that

| (13) | ||||

where , , and .

A few comments on Theorem 1: First, the previous result implies that, by choosing a step-size of order , Algorithm 1 attains regret of order when the length of the horizon and the initial amount of resources are simultaneously scaled. Second, Lemma 1 from Arlotto and Gurvich (2019) implies that one cannot hope to attain regret lower than under our assumptions. (Their result holds for the case of no regularizer, which is a special case of our setting.) Therefore, Algorithm 1 attains the optimal order of regret. Third, while we prove the result under the assumption that the regularizer is non-negative a similar result holds when the regularizer takes negative values because the regret definition is invariant to the value shift.

The proof of Theorem 1 combines ideas from Agrawal and Devanur (2015) and Balseiro et al. (2020) to incorporate hard resource constraints and regularizers, respectively. We prove the result in three steps. Denote by the stopping time corresponding to the first time that a resource is close to be depleted. We first bound from below the cumulative reward of the algorithm up to in terms of the dual objective minus the complementary slackness term . In the second step, we upper bound the complementary slackness term by noting that, until the stopping time , the algorithm’s decisions are not constrained by resources and, as a result, it implements online mirror descent on the dual function because are subgradients. Using standard results for online mirror descent, we can compare the complementary slackness term to its value evaluated at a fixed static dual solution, i.e., for any dual feasible vector . We then relate this term to the value of the regularizer and the performance lost when depleting resources to early, i.e., in cases when . To do so, a key idea involves decomposing the fixed static dual solution as where and is a carefully picked dual feasible point that is determined by the regularizer (such decomposition is always possible because the positive orthant is in the recession cone of ). By using the theory of convex conjugates, we can relate to the value of the regularizer. In the third step, we upper bound the optimal reward under full information in terms of the dual function using (5) and then control the performance lost from stopping early at a time at in terms of by choosing based on which resource is depleted.

Theorem 1 readily implies that Algorithm 1 attains regret for all examples presented in Section 2.1. The only exceptions are Example 1 with the negative entropy regularizer and Example 3 with the scaled negative entropy regularizer, which lead to closed-form solutions for the dual update. The issue is that the negative entropy function does not satisfy Assumption 3 because its strong convexity constant goes to zero as the dual variables go to infinity. Using a similar analysis to that of Proposition 2 of Balseiro et al. (2020), we can show that the dual variables remain bounded from above in both examples. By restricting the reference function to a box, we can show that the strong convexity constant of the negative entropy remains bounded from below, which implies that Algorithm 1 attains sublinear regret.

5.2 Adversarial Input

In this section, we assume that requests are arbitrary and chosen adversarially. Unlike the stochastic i.i.d. input model, regret can be shown to grow linearly with and it becomes less meaningful to study the order of regret over . Instead, we say that the algorithm is asymptotically -competitive, for , if

An asymptotic -competitive algorithm asymptotically guarantees fraction of at least of the best performance in hindsight over all possible inputs.

In general, the competitive ratio depends on the structure of the regularizer chosen. The next theorem presents an analysis for general concave regularizers.

Theorem 2.

Suppose there exists a finite and , such that for any it holds

| (14) |

Consider Algorithm 1 with step-size . Then, it holds for any that

where , , and .

Theorem 2 implies that when the step-size is of order , Algorithm 1 is asymptotic -competitive. Condition (14) can be shown to hold with finite if or if and is locally linear around zero. We next discuss the value of the competitive ratio for the examples presented in Section 2.1. Proofs of all mathematical statements are available in Appendix C.3.

Example 1 (No Regularizer).

When , then Algorithm 1 is -competitive with . This recovers a result in Balseiro et al. (2020), which is unimprovable without further assumptions on the input. The competitive ratio captures the relative scarcity of resources by comparing, for each resource, the worst-case consumption of any request as given by to the average resource availability . Naturally, the competitive ratio degrades as resources become scarcer.

Example 3 (Load Balancing).

When , then Algorithm 1 is -competitive. Notably, introducing a load balancing regularized only increases the competitive ratio by one and the competitive ratio does not depend on the tradeoff parameter .

Examples 4 and 5 (Below- and Above-Target Consumption).

In this case, the competitive ratio is . The competitive ratio is similar to that of no regularization with the exception that resource scarcity is measured with respect to the targets instead of the resource constraint vector . Because , the introduction of these regularizers deteriorates the competitive ratios relative to the case of no regularizer. Interestingly, the competitive ratios do not depend on the unit rewards in the regularizer.

Example 2 (Max-min Fairness)

Unfortunately, Theorem 5.2 does not lead to a finite competitive ratio for the max-min fairness regularizer. For this particular regularizer, we can provide an ad hoc competitive ratio analysis from first principles.

Theorem 3.

Consider Algorithm 1 with step-size for regularized online allocation problem with max-min fairness (i.e., ). Then:

- 1.

- 2.

The first part of Theorem 3 provides an analysis for online matching problems in which the objective is to maximize reward plus the max-min fairness regularizer. Online matching (without regularization) is a widely studied problem in the computer science and operations research literature (see, e.g., Karp et al. 1990; Mehta 2013). In online matching, the decision maker needs to match the arriving request to one of resources and each assignment consumes one unit of resource. The reward function is arbitrary. Here, we consider a variation in which the objective involves maximizing the revenue together with the max-min fairness of the allocation. Notice that in the case of no regularization, the competitive ratio for this problem is . Therefore, the introduction of the max-min fairness regularizer increases the competitive ratio by one and, as before, the competitive ratio is independent of the tradeoff parameter .

The second part of the theorem extends the result to generic online allocation problems with the max-min fairness regularizer. The parameter is similar to in that it compares the worst-case resource consumption of any request to the average consumption. The parameter is more subtle and measures the distance of the resource constraint vector to the set of achievable resource consumption akin to the Minkoswki functional. That is, it captures how much we need to scale the set for to lie in it. The parameter is guaranteed to be bounded whenever for every request. Unfortunately, if for some request, Theorem 3 does not provide a bounded competitive ratio. Intuitively, in such cases, the adversary can make max-min fairness large by first offering requests that consume all resources and then switching to requests that do not consume resources that were not allocated in the first stage. We conjecture that when the conditions of Theorem 3 do not hold, no algorithm that attains vanishing regret for stochastic input can achieve bounded competitive ratios in the adversarial case.

6 Numerical Experiments

In this section, we present numerical experiments on a display advertisement allocation application regularized by max-min fairness on consumption (Example 2).

Dataset. We utilize the display advertisement dataset introduced in Balseiro et al. (2014). They consider a publisher who has agreed to deliver ad slots (the requests) to different advertisers (the resources) so as to maximize the cumulative click-through rates (the reward) of the assignment. In their paper, they estimate click-through rates using mixtures of log-normal distributions. We adopt their parametric model as a generative model and sample requests from their estimated distributions. We consider publisher 2 from their dataset, which has advertisers. Furthermore, in our experiments, we rescale the budget so that in order to make sure that the max-min fairness is strictly less than . This implies that the maximal fairness value is .

Regularized Online Problem. The goal here is to design an online allocation algorithm that maximizes the total expected click-through rate with a max-min fairness regularizer on resource consumption as in Example 2. Advertiser can be assigned at most ad slots and the decision variables lie in the simplex . Denoting by the click-through rate of the -th ad slot , we have that the benchmark is given by:

| (15) | ||||

where is the weight of the regularizer. In the experiments, we consider the regularization levels and lengths of horizon .

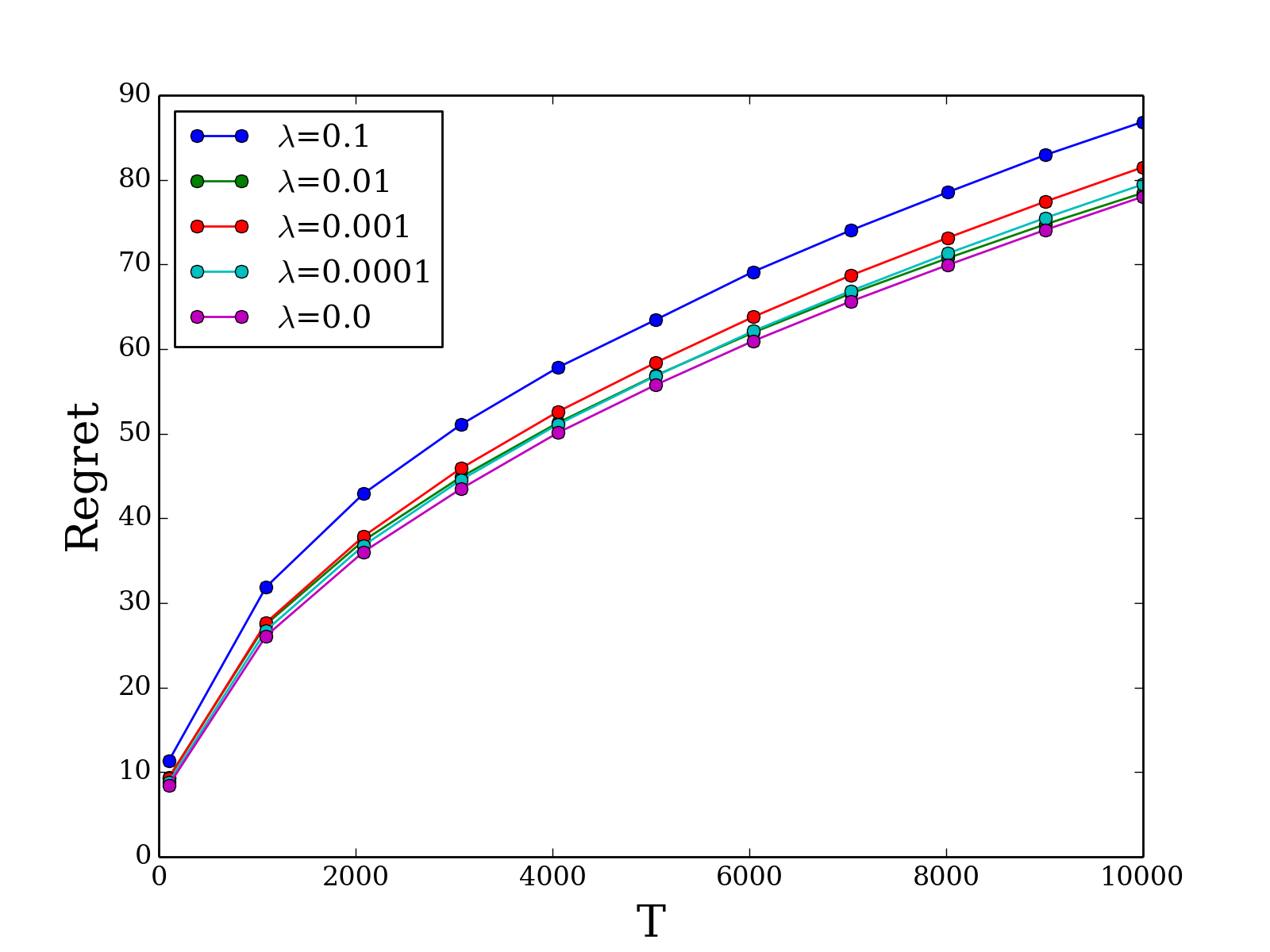

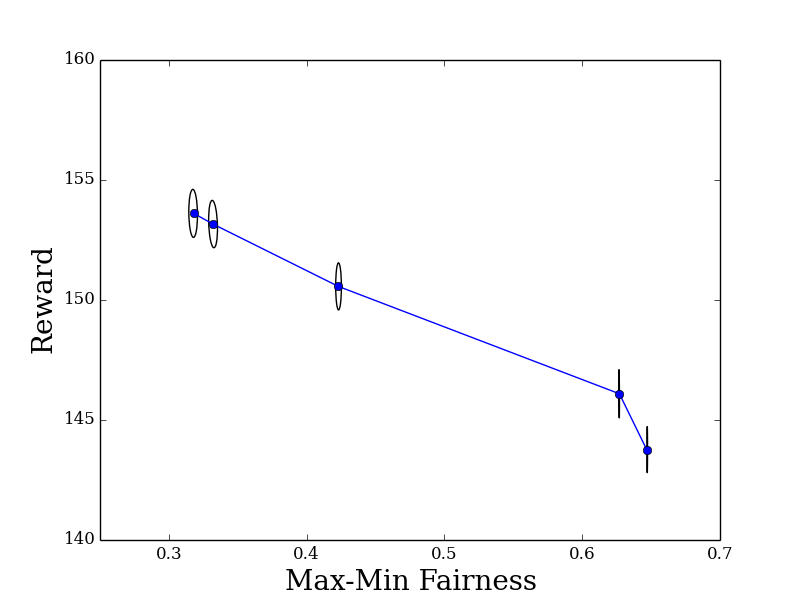

Implementation Details. In the numerical experiments, we implemented Algorithm 1 with weights and step-size . The dual update (10) is computed by solving a convex quadratic program as stated in Section 4 using cvxpy (Diamond and Boyd, 2016). For each regularization level and time horizon , we randomly choose samples from their dataset that are fed to Algorithm 1 sequentially. In order to compute the regret, we utilize the dual objective evaluated at the average dual as an upper bound to the benchmark. We report the average cumulative reward, the average max-min consumption fairness, and the average regret of independent trials in Figure 2. Ellipsoids in Figure 2 (b) give 95% confidence regions for the point estimates.

Discussion. Consistent with Theorem 1, Figure 2 (a) suggests that regret grows at rate for all regularization levels. Figure 2 (b) presents the trade-off between reward and fairness with the 95% confidence ellipsoid. In particular, we can double the max-min fairness while sacrificing only about of the reward by choosing . This showcases that fairness can be significantly improved (in particular given that the highest possible fairness is ) by solving the regularized problem with a small amount of reward reduction.

7 Conclusion and Future Directions

In this paper, we introduce the regularized online allocation problem, a novel variant of the online allocation problem that allows for regularization on resource consumption. We present multiple examples to showcase how the regularizer can help attain desirable properties, such as fairness and load balancing, and present a dual online mirror descent algorithm for solving this problem with low regret. The introduction of a regularizer impacts the geometry of the dual feasible region. By suitably choosing the reference function of mirror descent, we can adapt the algorithm to the structure of the dual feasible region and, in many cases, obtain dual updates in closed form.

Future directions include extending the results in this work to other inputs such as non-stationary stochastic models. Another direction is to consider other regularizers and develop corresponding adversarial guarantees using our framework. Finally, it is worth exploring whether the competitive ratios we provide are tight (either unimprovable by our algorithm or by any other algorithm) for the regularizers we explore in this paper.

References

- Agrawal and Devanur (2015) Shipra Agrawal and Nikhil R. Devanur. Fast algorithms for online stochastic convex programming. In Proceedings of the Twenty-Sixth Annual ACM-SIAM Symposium on Discrete Algorithms, SODA ’15, page 1405–1424, USA, 2015. Society for Industrial and Applied Mathematics.

- Agrawal et al. (2014) Shipra Agrawal, Zizhuo Wang, and Yinyu Ye. A dynamic near-optimal algorithm for online linear programming. Operations Research, 62(4):876–890, 2014.

- Agrawal et al. (2018) Shipra Agrawal, Morteza Zadimoghaddam, and Vahab Mirrokni. Proportional allocation: Simple, distributed, and diverse matching with high entropy. In International Conference on Machine Learning, pages 99–108, 2018.

- Ahmed et al. (2017) Faez Ahmed, John P Dickerson, and Mark Fuge. Diverse weighted bipartite b-matching. In Proceedings of the 26th International Joint Conference on Artificial Intelligence, pages 35–41, 2017.

- Arlotto and Gurvich (2019) Alessandro Arlotto and Itai Gurvich. Uniformly bounded regret in the multisecretary problem. Stochastic Systems, 9(3):231–260, 2019.

- Azar et al. (2010) Yossi Azar, Niv Buchbinder, and Kamal Jain. How to allocate goods in an online market? In European Symposium on Algorithms, pages 51–62. Springer, 2010.

- Badanidiyuru et al. (2018) Ashwinkumar Badanidiyuru, Robert Kleinberg, and Aleksandrs Slivkins. Bandits with knapsacks. J. ACM, 65(3), March 2018.

- Ball and Queyranne (2009) Michael O. Ball and Maurice Queyranne. Toward robust revenue management: Competitive analysis of online booking. Operations Research, 57(4):950–963, 2009.

- Balseiro et al. (2020) Santiago Balseiro, Haihao Lu, and Vahab Mirrokni. The best of many worlds: Dual mirror descent for online allocation problems. arXiv preprint arXiv:2011.10124, 2020.

- Balseiro et al. (2021) Santiago Balseiro, Haihao Lu, and Vahab Mirrokni. Regularized online allocation problems: Fairness and beyond. In International Conference on Machine Learning, pages 630–639. PMLR, 2021.

- Balseiro et al. (2014) Santiago R Balseiro, Jon Feldman, Vahab Mirrokni, and Shan Muthukrishnan. Yield optimization of display advertising with ad exchange. Management Science, 60(12):2886–2907, 2014.

- Bansal and Sviridenko (2006) Nikhil Bansal and Maxim Sviridenko. The santa claus problem. In Proceedings of the thirty-eighth annual ACM symposium on Theory of computing, pages 31–40, 2006.

- Bateni et al. (2018) Mohammad Hossein Bateni, Yiwei Chen, Dragos Ciocan, and Vahab Mirrokni. Fair resource allocation in a volatile marketplace. Available at SSRN 2789380, 2018.

- Bertsekas (2009) Dimitri P Bertsekas. Convex optimization theory. Athena Scientific Belmont, 2009.

- Bertsimas et al. (2011) Dimitris Bertsimas, Vivek F Farias, and Nikolaos Trichakis. The price of fairness. Operations research, 59(1):17–31, 2011.

- Bertsimas et al. (2012) Dimitris Bertsimas, Vivek F Farias, and Nikolaos Trichakis. On the efficiency-fairness trade-off. Management Science, 58(12):2234–2250, 2012.

- Boyd et al. (2004) Stephen Boyd, Stephen P Boyd, and Lieven Vandenberghe. Convex optimization. Cambridge university press, 2004.

- Bubeck (2015) S. Bubeck. Convex optimization: Algorithms and complexity. Foundations and Trends® in Machine Learning, 8(3-4):231–357, 2015.

- Buchbinder et al. (2007) Niv Buchbinder, Kamal Jain, and Joseph (Seffi) Naor. Online primal-dual algorithms for maximizing ad-auctions revenue. In Lars Arge, Michael Hoffmann, and Emo Welzl, editors, Algorithms – ESA 2007, pages 253–264, Berlin, Heidelberg, 2007. Springer Berlin Heidelberg.

- Cain Miller (2015) Claire Cain Miller. When algorithms discriminate. The New York Times, 2015. URL https://www.nytimes.com/2015/07/10/upshot/when-algorithms-discriminate.html. Accessed on 2021-10-19.

- Celli et al. (2021) Andrea Celli, Riccardo Colini-Baldeschi, Christian Kroer, and Eric Sodomka. The parity ray regularizer for pacing in auction markets. 2021. URL https://arxiv.org/abs/2106.09503.

- Cheung et al. (2020) Wang Chi Cheung, Guodong Lyu, Chung-Piaw Teo, and Hai Wang. Online planning with offline simulation. Available at SSRN 3709882, 2020.

- Devanur and Hayes (2009) Nikhil R. Devanur and Thomas P. Hayes. The adwords problem: online keyword matching with budgeted bidders under random permutations. In Proceedings of the 10th ACM conference on Electronic commerce, EC ’09, pages 71–78. ACM, 2009.

- Devanur and Jain (2012) Nikhil R. Devanur and Kamal Jain. Online matching with concave returns. In Proceedings of the Forty-Fourth Annual ACM Symposium on Theory of Computing, STOC ’12, page 137–144, New York, NY, USA, 2012. Association for Computing Machinery. ISBN 9781450312455.

- Devanur et al. (2019) Nikhil R. Devanur, Kamal Jain, Balasubramanian Sivan, and Christopher A. Wilkens. Near optimal online algorithms and fast approximation algorithms for resource allocation problems. J. ACM, 66(1), jan 2019.

- Diamond and Boyd (2016) Steven Diamond and Stephen Boyd. Cvxpy: A python-embedded modeling language for convex optimization. The Journal of Machine Learning Research, 17(1):2909–2913, 2016.

- Dickerson et al. (2019) John P Dickerson, Karthik Abinav Sankararaman, Aravind Srinivasan, and Pan Xu. Balancing relevance and diversity in online bipartite matching via submodularity. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 33, pages 1877–1884, 2019.

- Eghbali and Fazel (2016) Reza Eghbali and Maryam Fazel. Designing smoothing functions for improved worst-case competitive ratio in online optimization. In Advances in Neural Information Processing Systems, pages 3287–3295, 2016.

- Emanuel et al. (2020) Ezekiel J. Emanuel, Govind Persad, Ross Upshur, Beatriz Thome, Michael Parker, Aaron Glickman, Cathy Zhang, Connor Boyle, Maxwell Smith, and James P. Phillips. Fair allocation of scarce medical resources in the time of covid-19. New England Journal of Medicine, 382(21):2049–2055, 2020.

- Feldman et al. (2009) Jon Feldman, Nitish Korula, Vahab Mirrokni, S. Muthukrishnan, and Martin Pál. Online ad assignment with free disposal. In Proceedings of the 5th International Workshop on Internet and Network Economics, WINE ’09, pages 374–385. Springer-Verlag, 2009.

- Feldman et al. (2010) Jon Feldman, Monika Henzinger, Nitish Korula, Vahab S. Mirrokni, and Cliff Stein. Online stochastic packing applied to display ad allocation. In Proceedings of the 18th annual European conference on Algorithms: Part I, ESA’10, pages 182–194. Springer-Verlag, 2010.

- Grigas et al. (2021) Paul Grigas, Alfonso Lobos, Zheng Wen, and Kuang-Chih Lee. Optimal bidding, allocation, and budget spending for a demand-side platform with generic auctions. Allocation, and Budget Spending for a Demand-Side Platform with Generic Auctions (May 7, 2021), 2021.

- Hazan et al. (2016) Elad Hazan et al. Introduction to online convex optimization. Foundations and Trends® in Optimization, 2(3-4):157–325, 2016.

- Jasin (2015) Stefanus Jasin. Performance of an lp-based control for revenue management with unknown demand parameters. Operations Research, 63(4):909–915, 2015.

- Jenatton et al. (2016) Rodolphe Jenatton, Jim Huang, Dominik Csiba, and Cedric Archambeau. Online optimization and regret guarantees for non-additive long-term constraints. arXiv preprint arXiv:1602.05394, 2016.

- Jiang et al. (2019) Jiashuo Jiang, Shixin Wang, and Jiawei Zhang. Achieving high individual service-levels without safety stock? optimal rationing policy of pooled resources. Optimal Rationing Policy of Pooled Resources (May 2, 2019). NYU Stern School of Business, 2019.

- Karp et al. (1990) Richard M Karp, Umesh V Vazirani, and Vijay V Vazirani. An optimal algorithm for on-line bipartite matching. In Proceedings of the twenty-second annual ACM symposium on Theory of computing, pages 352–358, 1990.

- Li and Ye (2019) Xiaocheng Li and Yinyu Ye. Online linear programming: Dual convergence, new algorithms, and regret bounds. 2019.

- Li et al. (2020) Xiaocheng Li, Chunlin Sun, and Yinyu Ye. Simple and fast algorithm for binary integer and online linear programming. arXiv preprint arXiv:2003.02513, 2020.

- Lien et al. (2014) Robert W. Lien, Seyed M. R. Iravani, and Karen R. Smilowitz. Sequential resource allocation for nonprofit operations. Operations Research, 62(2):301–317, 2014.

- Ma and Simchi-Levi (2020) Will Ma and David Simchi-Levi. Algorithms for online matching, assortment, and pricing with tight weight-dependent competitive ratios. Operations Research, 68(6):1787–1803, 2020.

- Ma and Xu (2020) Will Ma and Pan Xu. Group-level fairness maximization in online bipartite matching. arXiv preprint arXiv:2011.13908, 2020.

- Manshadi et al. (2021) Vahideh Manshadi, Rad Niazadeh, and Scott Rodilitz. Fair dynamic rationing. EC ’21, page 694–695, New York, NY, USA, 2021. Association for Computing Machinery. ISBN 9781450385541.

- Mehta (2013) Aranyak Mehta. Online matching and ad allocation. Foundations and Trends® in Theoretical Computer Science, 8(4):265–368, 2013.

- Mehta et al. (2007) Aranyak Mehta, Amin Saberi, Umesh Vazirani, and Vijay Vazirani. Adwords and generalized online matching. J. ACM, 54(5):22–es, October 2007. ISSN 0004-5411.

- Mirrokni et al. (2012) Vahab S. Mirrokni, Shayan Oveis Gharan, and Morteza Zadimoghaddam. Simultaneous Approximations for Adversarial and Stochastic Online Budgeted Allocation, pages 1690–1701. 2012.

- Mo and Walrand (2000) Jeonghoon Mo and Jean Walrand. Fair end-to-end window-based congestion control. IEEE/ACM Transactions on networking, 8(5):556–567, 2000.

- Nanda et al. (2020) Vedant Nanda, Pan Xu, Karthik Abhinav Sankararaman, John Dickerson, and Aravind Srinivasan. Balancing the tradeoff between profit and fairness in rideshare platforms during high-demand hours. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 34, pages 2210–2217, 2020.

- Nash Jr (1950) John F Nash Jr. The bargaining problem. Econometrica: Journal of the Econometric Society, pages 155–162, 1950.

- Shalev-Shwartz et al. (2012) Shai Shalev-Shwartz et al. Online learning and online convex optimization. Foundations and Trends® in Machine Learning, 4(2):107–194, 2012.

- Tan et al. (2020) Xiaoqi Tan, Bo Sun, Alberto Leon-Garcia, Yuan Wu, and Danny HK Tsang. Mechanism design for online resource allocation: A unified approach. In Abstracts of the 2020 SIGMETRICS/Performance Joint International Conference on Measurement and Modeling of Computer Systems, pages 11–12, 2020.

- Xu and Li (2013) Hong Xu and Baochun Li. Dynamic cloud pricing for revenue maximization. IEEE Transactions on Cloud Computing, 1(2):158–171, 2013.

Appendix A Proofs in Section 3

A.1 Proof of Lemma 1

Proof.

We prove each part at a time.

Part (i). Convexity trivially follows because dual problems are always convex (see, e.g., Proposition 4.1.1 of Bertsekas 2009). Suppose , namely . Then it holds for any and that

thus , which finishes the proof by definition of recession cone.

Part (ii). With , it holds for any that

where the first inequality follows from Lipschitz continuity and the second from for every vector . Thus, , which finishes the proof by definition of . ∎

Part (iii). Suppose there is an , such that . Fix . Define such that for every and otherwise. Then it holds that

which goes to when by noticing . Thus , which finishes the proof by contradiction.

Part (iv). We prove the result by contradiction. Let be an optimal solution with . Consider the solution with and for . Because these two solutions only differ in the -th component, we obtain using Lipschitz continuity

where the second inequality follows because and . Therefore, cannot be an optimal. ∎

Appendix B Proofs in Section 4

Proposition 1 presents the conjugate functions , the corresponding domain , and optimal actions for each example stated in Section 2.1.

Proposition 1.

B.1 Proof of Proposition 1

We prove Proposition 1 for each example at a time.

Example 2

Performing the change of variables or we obtain that

and the result follows from invoking the following lemma.

Lemma 2.

Let and for . If for all subsets , then and is an optimal solution. Otherwise, .

Proof.

Let . We first show that for . Suppose that there exists a subset such that . For , consider a feasible solution with for and otherwise. Then, because such solution is feasible and we obtain that . Letting , we obtain that .

We next show that for . Note that because is feasible and . We next show that . Let be any feasible solution and assume, without loss of generality, that the vector is sorted in increasing order, i.e., . Let . The objective value is

where the second equation follows from rearranging the sum and the inequality follows because is increasing and for all . The result follows. ∎

Example 3

Performing the change of variables or we obtain that

and the result follows from invoking the following lemma.

Lemma 3.

Let and for . If and for all , then and is an optimal solution. Otherwise, .

Proof.

Let . We first show that for . First, suppose for some . Consider the feasible solution for , where is the unit vector with a one in component and zero otherwise. Then, because such solution is feasible and we obtain that . Letting , we obtain that . Second, suppose that . For , consider a feasible solution with where is the all-one vector. Then, because such solution is feasible and we obtain that . Letting , we obtain that .

We next show that for . Note that because is feasible and . We next show that . Let be any feasible solution and assume, without loss of generality, that the vector is sorted in increasing order, i.e., . The objective value is

where the first inequality follows because for all since is increasing and , and the last inequality follows because and . The result follows. ∎

Example 4

Notice that

Because the conjugate of the sum of independent functions is the sum of the conjugates, we have by Lemma 4 that for and otherwise.

Lemma 4.

Let for , and . Let . Then, for , and for . Moreover, for , is an optimal solution; while, for , is an optimal solution.

Proof.

We can rewrite the conjugate as

where the second equation follows by performing the change of variables and the last from setting .

First, suppose that . For any , we have that . Letting yields that . Second, consider . Write . The objective is increasing for and decreasing for . Therefore, the optimal solution is and . Thirdly, for a similar argument shows that the objective is decreasing in . Therefore, it is optimal to set , which yields . The result follows from combining the last two cases. ∎

Example 5

We have

Because the conjugate of the sum of independent functions is the sum of the conjugates, we have by Lemma 5 that for and otherwise.

Lemma 5.

Let for , and . Let . Then, for , and otherwise. Moreover, for , is an optimal solution; while, for , is an optimal solution.

Proof.

We can rewrite the conjugate as

where the second equation follows by performing the change of variables and the last from setting .

First, suppose that . For any , we have that . Letting yields that . Second, consider . Write . The objective is decreasing for and increasing for . Therefore, the optimal solution is and . Thirdly, for a similar argument shows that the objective is increasing in . Therefore, it is optimal to set , which yields . The result follows from combining the last two cases. ∎

Appendix C Proofs in Section 5

C.1 Proof of Theorem 1

Theorem 1 is an extension of Theorem 1 in Balseiro et al. (2020) to include the concave non-separable regularizer . The proof of Theorem 1 follows a similar proof structure of Balseiro et al. (2020). In order to deal with the regularizer, the major differences of our proofs compared with that of Balseiro et al. (2020) include: (i) we involve the regularizer and its conjugate , and utilize them throughout the proof; (ii) the choice of the reference value (see step 2 in the proof for more details) is chosen critically to handle the existence of the regularizer.

We prove the result in three steps. First, we lower bound the cumulative reward of the algorithm up to the first time that a resource is depleted in terms of the dual objective and complementary slackness. Second, we bound the complementary slackness term by picking a suitable “pivot” for online mirror descent. We conclude by putting it all together in step three.

Step 1 (Primal performance.)

First, we define the stopping time of Algorithm 1 as the first time less than that there exists resource such that

Notice that is a random variable, and moreover, we will not violate the resource constraints before the stopping time . We here study the primal-dual gap until the stopping time . Notice that before the stopping time , Algorithm 1 performs the standard subgradient descent steps on the dual function because .

Let us denote the random variable to be the type of request in time period , i.e., is the random variable that determines the (stochastic) sample in the -th iteration of Algorithm 1. We denote .

Consider a time so that actions are not constrained by resources. Because , we have that

Similarly, because , we have that

Let be the expected dual objective at when requests are drawn i.i.d. from . Adding the last two equations and taking expectations conditional on we obtain, because and , that

| (16) |

where the second equality follows the definition of the dual function.

Consider the process , which is martingale with respect to (i.e., and ). Since is a stopping time with respect to and is bounded, the Optional Stopping Theorem implies that . Therefore,

Using a similar martingale argument for and summing (C.1) from we obtain that

| (17) |

where the inequality follows from denoting to be the average dual variable and using that the dual function is convex.

Step 2 (Complementary slackness).

Consider the sequence of functions

| (18) |

which capture the complementary slackness at time . The gradients are given , which are bounded as follows . Therefore, Algorithm 1 applies online mirror descent to these sequence of functions , and we obtain from Proposition 2 that for every

| (19) |

where is the regret of the online mirror descent algorithm after iterations, and the second inequality follows because and the error term is increasing in .

We now discuss the choice of . For , we have that

| (20) |

where the inequality follows because because , and the equality is because for since and since is closed, concave, and proper by Assumption 2.

We let , where non-negative is to be determined later. Note that because the positive orthant is inside the recession cone of (see Lemma 1). Putting these together, we bound the complementary slackness as follows

| (21) | ||||

where the first inequality follows from (19), the equality follows from linearity of , and the second inequality from (20).

Step 3 (Putting it all together).

For any and we have that

| (22) |