Robust estimation for semi-functional linear regression models

Abstract

Semi-functional linear regression models postulate a linear relationship between a scalar response and a functional covariate, and also include a non-parametric component involving a univariate explanatory variable. It is of practical importance to obtain estimators for these models that are robust against high-leverage outliers, which are generally difficult to identify and may cause serious damage to least squares and Huber-type -estimators. For that reason, robust estimators for semi-functional linear regression models are constructed combining -splines to approximate both the functional regression parameter and the nonparametric component with robust regression estimators based on a bounded loss function and a preliminary residual scale estimator. Consistency and rates of convergence for the proposed estimators are derived under mild regularity conditions. The reported numerical experiments show the advantage of the proposed methodology over the classical least squares and Huber-type -estimators for finite samples. The analysis of real examples illustrate that the robust estimators provide better predictions for non-outlying points than the classical ones, and that when potential outliers are removed from the training and test sets both methods behave very similarly.

Keywords: -splines; Functional Data Analysis; Partial Linear Models; Robust estimation

AMS Subject Classification: 62G35; 62G25

1 Introduction

Many commonly used statistical models are either fully parametric or completely non-parametric. On the one hand, while a reasonable parametric model results in stable estimators and associated inferences, a misspecified one can lead to seriously misleading and biased conclusions. On the other hand, non-parametric methods may avoid misspecified models, but typically result in more variable estimators. A particular difficulty with non-parametric models is that in many applications they typically require multivariate smoothing which can be seriously affected by the well-known “curse of dimensionality”. This issue is even more serious when the model includes infinite-dimensional components.

One approach to deal with this problem is to consider semi-parametric models. Specifically, consider a scalar response variable and a vector of potential covariates . Partial linear regression models allow some components of to enter the model in a fully non-parametric way, while the rest are assumed to have a linear effect on . These models avoid the curse of dimensionality problem and are easier to interpret than fully non-parametric ones. An extensive review of partly linear regression models can be found in Härdle et al. (2000), and Härdle et al. (2004). Here we consider the extension of these models to situations including both functional and vector covariates. In what follows we will use lowercase letters to denote scalar random variables, and upper case letters for functional random elements.

Functional explanatory variables can be included in partial linear models either linearly or non-parametrically. Aneiros-Pérez and Vieu (2006) and Shang (2014) used a linear model for the effect of the scalar explanatory variables and a non-parametric component for the functional covariate. Lian (2011) proposed a linear regression model for the infinite-dimensional covariates and a nonparametric regression model for the other explanatory variables via Nadaraya-Watson kernel estimators. In this paper, we focus on the particular case where there is one real covariate, which was also considered by Zhou and Chen (2012). More precisely, we consider independent and identically distributed observations with the same distribution as the triplet , where the response is related linearly to the functional explanatory variable , and nonparametrically to the real covariate . In symbols: , where denotes the usual inner product, is a residual scale parameter, and is the error term, independent of . In this model the regression parameter is assumed to be in , although for estimation purposes some smoothness conditions may be required. As usual, the unknown regression function is only assumed to be smooth with compact support .

It is well-known that small proportions of outliers and other atypical observations can affect seriously the estimators for these models although not many robust methods exist in the literature. Qingguo (2015) studied -estimators for the linear slope using a monotone score function and a functional principal component approximation. Huang et al. (2015) proposed -estimators approximating both the linear slope and the nonparametric component with spline bases. These proposals have two main drawbacks: they are not scale equivariant since they do not consider a residual scale estimator, and they lack protection against high-leverage outliers. The lack of scale invariance may be a problem in practice since the magnitude of the residuals that are to be considered “large” (outliers) depends on their scale. This dispersion parameter needs to be estimated with a robust preliminary scale estimator, as it is generally done for linear regression models (see Maronna et al., 2019). In finite-dimensional linear regression models, it is well–known that using an unbounded loss function results in estimators that cannot protect against high-leverage outliers. We note that this type of atypical observations may also affect the estimation procedure described by Qingguo (2015), since functional principal components are also highly sensitive to small proportions of outliers.

Our proposal overcomes these problems by adapting best practices for robust multiple linear regression estimators to these partial linear models with functional covariates. More specifically, we use -splines to approximate both the functional regression parameter and the nonparametric component, and apply -regression estimators (Yohai, 1987) that are based on a bounded loss function and a preliminary residual scale estimator. These estimators are scale equivariant, robust against high-leverage outliers, and strongly consistent under standard regularity conditions. Furthermore, we derive convergence rates with respect to the mean squared prediction differences obtained with the true and estimated parameters.

We illustrate our approach with two real examples. We first consider hourly electricity prices in Germany between 1 January 2006 and 30 September 2008. The data consist of German power prices traded at the Leipzig European Energy Exchange, electricity demand, and eolic energy in the system. Our interest is in studying the relationship between hourly prices and the overall load of the system, while taking into account the proportion of the demand that can be satisfied from wind generators, which follows a different price regime. These data were also used in Liebl (2013) in the context of electricity price forecasting, and are available among the supplementary materials of that paper. Our second example is the well known Tecator data set (see Ferraty and Vieu, 2006). This food quality-control data was obtained from 215 samples of finely chopped meat with different percentages of fat, protein and moisture content. For each sample, a spectrometric curve of absorbances was measured using a Tecator Infratec Food and Feed Analyzer. Since obtaining a spectrometric curve is faster and less costly than the analytical procedure used to determine fat content, the interest is in building a model to predict the fat content of a meat sample using its protein and moisture contents as well as its absorbance spectrum. Boente and Vahnovan (2017) used the functional boxplot of Sun and Genton (2011) to show the presence of atypical curves among the second derivatives of the spectrometric curves in the Tecator data. Thus, reliable analyses of this data set require methods that protect against potential outliers in the functional explanatory variables.

The rest of the paper is organized as follows. The model and our proposed estimators are described in Section 2. Theoretical assurances regarding the consistency and convergence rates of our proposal are provided in Section 3, while in Section 4 we report the results of a simulation study to explore their finite-sample properties. Section 5 contains two real-data analyses, while final comments are given in Section 6. All proofs are relegated to the Appendix.

2 Model and estimators

The semi-functional linear regression model (see, for example, Zhou and Chen, 2012) assumes that the observations , , are independent and identically distributed realizations of the random element , where is the response variable, is a stochastic process on , the space of square integrable functions on the interval , and . The relationship between the response and the explanatory variables is given by:

| (1) |

where denotes the usual inner product, is the regression coefficient, is an unknown smooth function, is the unknown error scale parameter, and is independent of . We assume that and are compact intervals, and to simplify the notation, and without loss of generality, we will assume that . We allow the error distribution to have heavy tails by only requiring that have a symmetric distribution with scale parameter . Note that in order for to be identifiable we do no include an intercept term in (1). Just as in the finite-dimensional linear regression case, to obtain consistent robust estimators we need that , where .

To ensure that the regression coefficient in (1) is identifiable we will assume that the covariance operator of the stochastic process has infinite rank, i.e., that all its eigenvalues are positive (Cardot et al., 2003). To see that this condition is needed, let be the eigenfunctions of , with corresponding eigenvalues . The Karhunen-Loève representation of is , where and the scores are uncorrelated random variables with mean zero and variance . If has a null eigenvalue, then its kernel (here denotes the kernel of the self-adjoint operator , i.e., ). Hence, for any we have . Thus, for all , with probability one, , so that . This shows that when the regression parameter in (1) is not identifiable.

To define the -splines estimators, fix a desired spline order and let and be the number of knots to be used to approximate and , respectively. Recall that a spline of order is a polynomial of degree within each subinterval. Then, the corresponding (normalized) -splines bases have dimensions and , respectively (see Corollary 4.10 of Schumaker, 1981). Denote these bases by and , and to simplify the notation, denote their sizes with and , respectively. As usual when considering -spline approximations, consistency results will be valid when , i.e. both functions and are -times continuously differentiable, where and is the spline order. In particular, when cubic splines are considered, the results in Section 3 hold for twice continuously differentiable regression functions.

2.1 -estimators with -splines

Robust -estimators (Yohai, 1987) are defined using two steps: first an initial robust (but possibly inefficient) regression estimator is used to compute a residual scale estimator, and then a regression -estimator is calculated using a bounded loss function and standardized residuals. In what follows the loss function will be assumed to satisfy the following property:

-

R1

: The function is continuous, even, non-decreasing on , and such that . Moreover, and if with then . When is bounded, we assume that . Functions satisfying these conditions will be called -functions (Maronna et al., 2019).

A widely used family of -functions is given by Tukey’s bi-square: , where is a tuning parameter that determines the robustness and efficiency properties of the associated estimators.

To define our estimators, for any vectors and let , , be the residuals with respect to the corresponding spline approximations and :

| (2) |

where , , and .

First, we compute an -estimator of regression and its associated residual scale. Let be a bounded function and be the -scale estimator of the residuals given as the solution to the following equation:

| (3) |

where (this is needed for the estimators to be consistent). Note that we use instead of in (3) above to control the effect of a possibly large number of parameters () relative to the sample size (see Maronna et al., 2019). When is a Tukey’s bisquare function, , the choices and above yield a scale estimator that is Fisher-consistent when the errors have a normal distribution, and with a 50% breakdown point in finite-dimensional regression models.

-regression estimators are defined as the minimizers of the -scale above:

| (4) |

The associated residual scale estimator is

| (5) |

and the corresponding splines estimators are , and .

Let be a function such that and . As it is well known, if and , then when . We now compute an -estimator using the residual scale estimator and the loss function :

| (6) |

The resulting estimators of the regression function and the nonparametric component are given by

| (7) |

where and .

2.2 Selecting the size of the -spline bases

The number of elements of the -spline bases play the role of regularization parameters in our estimation procedure, and it is useful to have a criterion to select them. Since standard model selection methods can be highly affected by a small proportion of outliers, some robust alternatives have been proposed in the literature. For linear regression models, see, for example, Ronchetti (1985) and Tharmaratnam and Claeskens (2013).

Qingguo (2015) proposes using a criterion analogous to the Schwarz information criterion (1978) (see also He et al., 2002). However, the estimators of Qingguo (2015) do not take into account the residuals scale which is needed to determine which points are outliers according to the size of their residuals. Instead, we propose the following robust -type criterion

| (8) |

where , , are the residuals obtained using bases of dimension and when computing and , respectively, and is the corresponding scale. Note that when the expression above reduces to the usual criterion.

As is usual in spline-based procedures, in order to obtain an optimal rate of convergence, we let the number of knots increase slowly with the sample size. Theorem 3.2 below shows that when and are twice continuously differentiable and approximated with cubic splines (), the rate for the size of the bases is almost (see also assumption C4). Hence, a possible way to select is to search for the first local minimum of in the range , . Note that for cubic splines the smallest possible number of knots is 4.

2.3 Other functional regression models

Semi-functional models with varying coefficients

The estimators defined above can easily be extended to other semi-functional linear models, such as those involving varying coefficients. This extension will be relevant for our analysis of the Tecator data in Section 5.2. More specifically, consider the model

where is the intercept and , , is another explanatory variable. To define -estimators in this setting, for given bases dimensions and , define the residuals as , where, as before, . The estimators are now defined as before, but now minimizing over in (4) and (6).

Functional linear models

Our proposal is also immediately applicable to functional linear models such as , where are real-valued vectors of covariates. In this case we only need to set in the definition of the residuals in equation (2). In the particular case that , a robust estimator using the principal components basis was given in Kalogridis and Van Aelst (2019), while spline-based robust estimators were studied in Maronna and Yohai (2013).

Monotone components

In some applications, the non-parametric function or the regression function in the model (1) may be known to be monotone. In those cases it is preferable to take this information into account when computing the corresponding estimator. Neumeyer (2007) proposed the following method to construct such monotone estimators, which can be easily applied to our -estimators based on splines. For any Lebesgue-measurable function , define the function as , for any , where denotes the indicator function of the set . Note that is the inverse of when is strictly increasing, and its generalized inverse when is non-decreasing. Furthermore, is always increasing and Lebesgue-measurable. Given any function , Neumeyer (2007) considered the increasing modification as

which satisfies for any non-decreasing function . Hence, based on the estimators of defined in (6) and (7), a monotone estimator may be constructed as

| (9) |

These modified robust estimators are also strongly consistent (see Corollary 3.1) and have very good finite-sample properties (see Section 4).

3 Consistency results

In this section we prove that if conditions R2 - C5 below hold, then the estimators in (6) are strongly consistent. We will assume that:

-

R2

: The function is differentiable with bounded derivative , such that is bounded.

-

C1

: The random variable has a density function that is even, non-increasing in , and strictly decreasing for in a neighbourhood of .

-

C2

: For almost any , , for any , and , .

-

C3

: The true functions and are such that and . Furthermore, their th derivative satisfies a Lipschitz condition on , with , that is, where

Recall that for any continuous function , .

-

C4

: The smoothing parameters and are assumed to be of order , . Moreover, the ratio of maximum and minimum spacings of knots is uniformly bounded.

-

C5

: There exists such that , for any , , .

These conditions are discussed in more detail in Section 3.2 below.

Our first result shows the strong consistency of the scale estimators defined in (5). Let be the -scale functional related to the residuals that is, satisfies

For simplicity, we will assume that has been chosen so that . In this case we have that , and the scale estimators are strongly consistent.

Proposition 3.1. Assume that the function is bounded such that and satisfies R1 and R2. Then, if and C1, C3 and C4 hold, we have that .

Theorem 3.1 states the main result in this section, that is, the uniform strong consistency of the proposed estimators.

Theorem 3.1. Let be a bounded function with satisfying R1 and R2. Furthermore, let

where . Assume that C1 to C4 hold, and that C5 holds with . If, in addition, , then .

The following corollary shows that this consistency is maintained when is monotone and the estimator is modified as described in Section 2.3. This is a direct consequence of Theorem 3.1 above and Theorem 3.1 in Neumeyer (2007).

Corollary 3.1. Let be a bounded function with satisfying R1 and R2. Assume that C1 to C4 hold, and that C5 holds with and . Then, if is the monotone modified estimator in (9) based on and , we have that .

3.1 Rates of Consistency

In this section we find the rate of convergence of the proposed estimators when measuring the distance between two pairs of functions and through the mean square error of their prediction differences, that is, through . Note that when C2 holds is indeed a distance.

For that purpose, we will need the following additional assumption, where, as above, for any vectors of coefficients and , we write , and . Conditions ensuring that C6 holds are given in Lemma A.2.1 in the Appendix.

-

C6

There exists a neighbourhood of with closure strictly included in , and constants and , such that , for any such that and any .

Theorem 3.2. Let be a bounded function with satisfying R1 and R2. Assume that C1 to C4 hold, that , that C5 holds with and , that C6 holds, and that . Let be any sequence that satisfies and , then , where . Hence, if in C4, one can choose or , for arbitrarily small, where the latter yields a convergence rate, in terms of the prediction distance , that is arbitrarily close to the optimal one.

Remark 3.2. This theorem allows us to derive the order of convergence of , when and are independent and , as follows. Note that

Hence, from Theorem 3.2, we get that . Furthermore, from the proof of Theorem 3.2, there exists such that and . Using that and Lemma 7 of Stone (1986), we obtain that, for some positive constant independent of the sample size, which entails that . Assume now that and and , for . Taking into account that , we conclude that , with , leading to . When is monotone, this rate is also inherited by the monotone modification .

3.2 Comments on assumptions R2 and C1 to C5

Assumption R2 is an additional smoothness condition on the function which is standard in the robustness literature. Assumptions C1 to C4 refer to the error distribution (to ensure Fisher-consistency), to the smoothness of the regression parameter and the nonparametric component, as well as to the order at which the dimension of the bases increase. These assumptions are standard when using spline approximations. Assumption C2 guarantees that are the unique minimizers of (see Lemma A.1.1), which is a standard condition needed to obtain consistent regression estimators. Furthermore, C5 is the functional version of assumption (A.3) in Yohai (1987) adapted to partial linear models.

A sufficient condition for C5 to hold is that , for any , , . Hence, it is necessary that the kernel of the covariance operator of be equal to . Specifically, the Karhunen-Loève expansion of cannot have finitely many terms. Note that when the covariance operator, , of has finite rank , then , for , where , are the eigenfunctions of associated to the -th eigenvalue , with , which implies that C5 does not hold. Furthermore, is not identifiable since with also satisfies model (1).

Denote as the covariance operator of , that is,

Then, assumptions C2 and C5 hold when, for almost all , the kernel of equals which is analogous to the assumptions of Huang et al. (2015). To see this, assume that and denote as , then . We will show that C2 holds. Note that so that if and only if . Assume that C2 does not hold, then there exists and , such that . Hence, in particular, we have that , so that implying that . Thus, using that is a linear, self-adjoint and compact operator with finite trace, we obtain that , so , which implies that and , and we reach a contradiction. Similar arguments show that C5 holds. Hence, assumptions C2 and C5 are weaker than requiring . It is worth noticing that, if , for any and with , then .

4 Simulation study

We performed a Monte Carlo study to investigate the finite-sample properties of our proposed estimators for the semi-functional linear regression model:

| (10) |

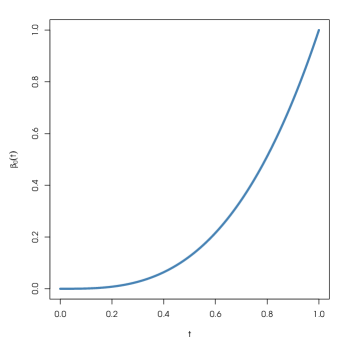

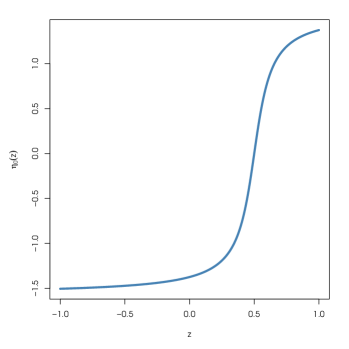

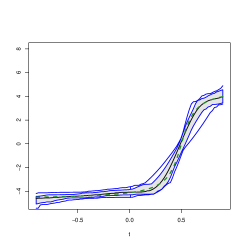

with , and . The model parameters were , , the basis , , , and the coefficients and , . The process that generates the functional covariates was Gaussian with mean 0 and covariance operator with eigenfunctions . For uncontaminated samples the scores were independent Gaussian random variables , and the errors , independent from and . Taking into account that when , the process was approximated numerically using the first 50 terms of its Karhunen-Loève representation. Figure 1 shows the functions and .

We compared three estimators: the classical procedure

based on least squares (ls), the -estimators proposed by

Huang et al. (2015) (m), and the -estimators

(mm) from Section 2.1.

Since the true function

is monotone, we also

included the modification, , based on

Neumeyer (2007).

As in Huang et al. (2015), -estimators were computed using a Huber function with tuning constant and no scale estimator. For the -estimators we used a bounded function to compute the initial -estimators and residual scale in (4) and also a bounded for the -step (6). For , we choose , the bisquare function, with tuning constants () and . All calculations were performed in R. The

code and scripts reproducing the examples in this paper are publicly available on-line

at https://github.com/msalibian/RobustFPLM.

For each setting we generated samples of size and used cubic splines with equally spaced knots. For the robust -estimators we selected the size of the spline bases ( and ) by minimizing in equation (8) over the 2-dimensional grid . For the least squares estimator we used the standard BIC criterion, and for the -estimator we used the criterion proposed in Huang et al. (2015).

To evaluate the performance of each estimator we looked at their integrated squared bias and mean integrated squared error. These were computed on a grid of equally spaced points on and , for and , respectively. More specifically, if is the estimate of the function obtained with the -th sample (), we compute

and

where are equispaced points on the domain of . These are numerical approximations to

and

respectively. To alleviate the concern that and MISE may be heavily influenced by numerical errors at or near the boundaries of the grid, we follow He and Shi (1998) and also consider trimmed versions of the above computed without the first and last points on the grid:

We chose which uses the central 90% interior points in the grid. Table 1 reports the squared bias and MISE and their trimmed counterparts for samples without outliers. We note that the boundary effect is more pronounced for the estimators of , but it is present for as well. Based on this observation, in what follows, we report the trimmed measures.

| Bias2 | MISE | Bias2 | MISE | Bias2 | MISE | |

|---|---|---|---|---|---|---|

| ls | 0.0126 | 0.1528 | 0.0197 | 0.0778 | 0.0221 | 0.0531 |

| m | 0.0123 | 0.1544 | 0.0248 | 0.0850 | 0.0261 | 0.0582 |

| mm | 0.0121 | 0.2039 | 0.0175 | 0.0871 | 0.0216 | 0.0593 |

| Bias | MISE | Bias | MISE | Bias | MISE | |

| ls | 0.0018 | 0.0865 | 0.0194 | 0.0615 | 0.0185 | 0.0442 |

| m | 0.0018 | 0.0869 | 0.0242 | 0.0680 | 0.0226 | 0.0493 |

| mm | 0.0017 | 0.1215 | 0.0173 | 0.0674 | 0.0171 | 0.0479 |

We considered two contamination scenarios. The first one contains outliers in the response variables and is expected to affect mainly the estimation of . The second one includes high-leverage outliers in the functional explanatory variables, as in the Tecator example (see Section 5.2), which typically affect the estimation of the linear regression parameter . Specifically, we constructed our samples as follows:

-

•

Scenario : here only the regression errors are contaminated in order to produce “vertical outliers”. Their distribution is given by , with the standard normal distribution function.

-

•

Scenario : in these settings we introduce high-leverage outliers by contaminating the functional covariates and the errors simultaneously. Outliers in the ’s are generated by perturbing the distribution of the second score in the Karhunen-Loève representation of the process. Specifically, we sample and then:

-

–

if , let and ;

-

–

if , let and , with for and .

The responses are generated as .

-

–

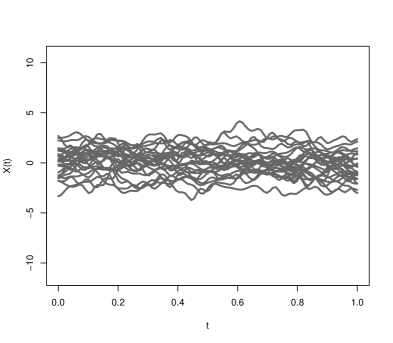

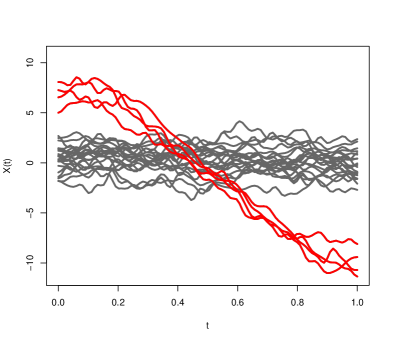

Both contamination settings above depend on the parameter . In this experiment we looked at the following values of : 8, 10, 12, 14 and 16. They produce a range of contamination scenarios ranging from mild to severe. As an illustration of the type of outliers generated with the second setting above, Figure 2 shows 25 randomly chosen functional covariates , for one sample generated under (with no outliers) and one obtained under .

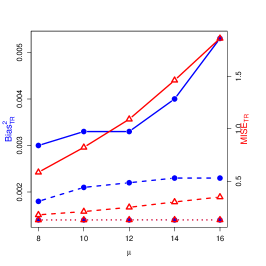

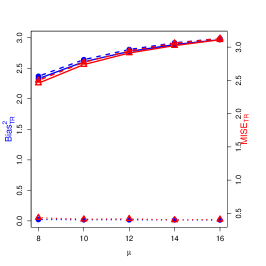

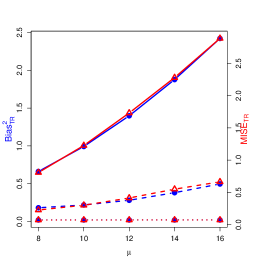

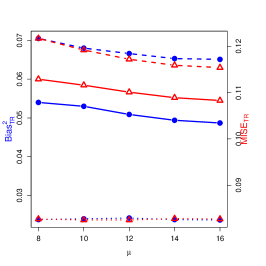

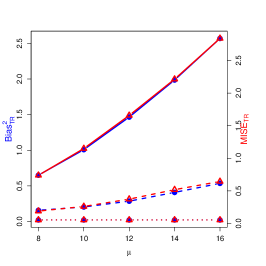

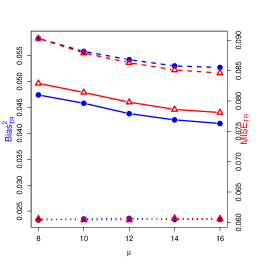

The plots in Figure 3 summarize the effect of the contamination scenarios for different values of . Each plot corresponds to one contamination scenario and one parameter estimator. Within each panel, the solid, dashed and dotted lines correspond to the measures for the least squares, the - and -estimators, respectively. There are two lines per estimation method: the one with triangles shows the trimmed MISE, and one with solid circles indicates the corresponding trimmed bias squared.

|

|

|

|

|

|

|

|

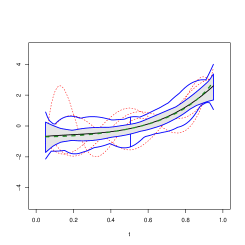

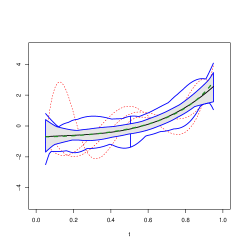

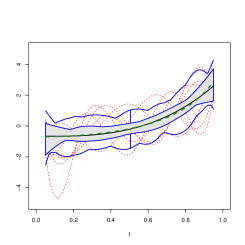

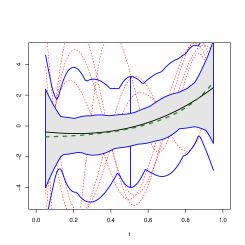

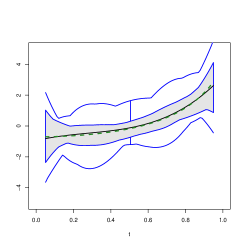

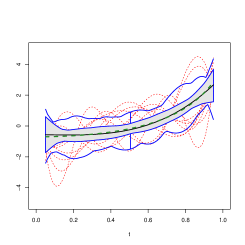

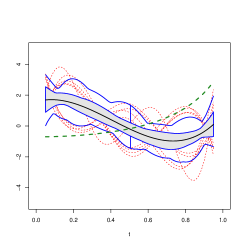

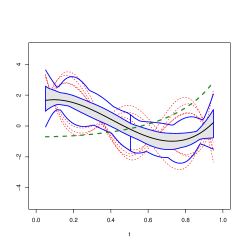

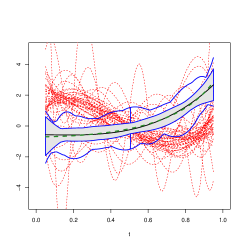

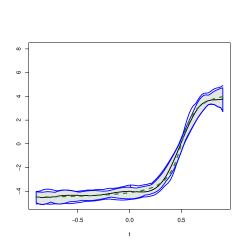

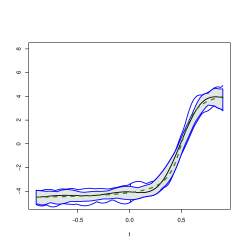

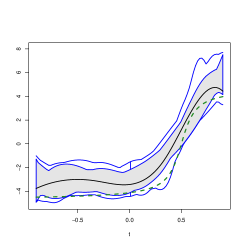

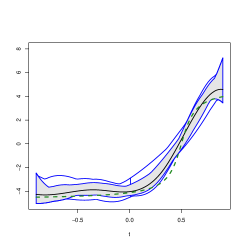

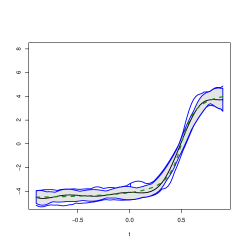

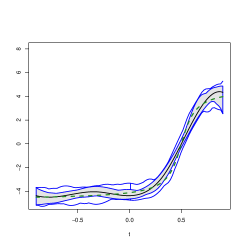

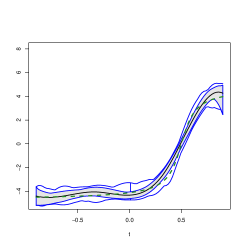

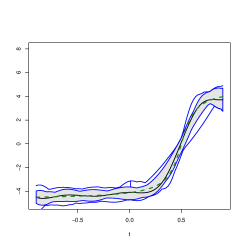

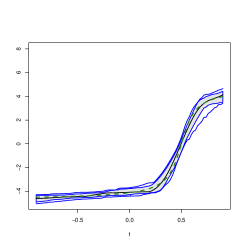

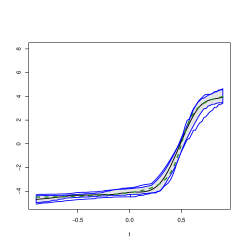

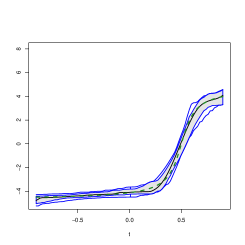

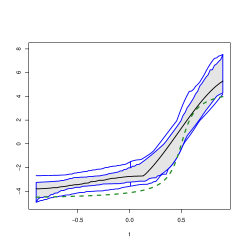

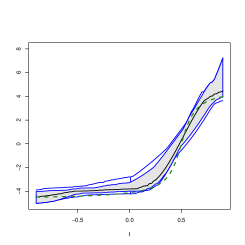

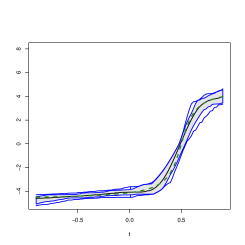

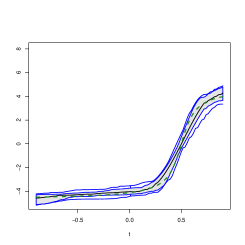

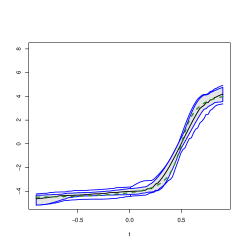

In order to also explore visually the performance of these estimators, Figures 4 to 6 contain functional boxplots (Sun and Genton, 2011) for the realizations of the different estimators for and under three contamination settings. As in standard boxplots, the central box of these functional boxplots represents the 50% inner band of curves, the solid black line indicates the central (deepest) function and the dotted red lines indicate outlying curves (in this case: outlying estimates or for some ). We also indicate the target (true) functions and with a dark green dashed line. To avoid boundary effects, we show here the different estimates or evaluated on the interior points of a grid of 100 equispaced points. In addition, to facilitate comparisons between contamination cases and estimation methods, the scales of the vertical axes are the same for all panels within each Figure.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

As expected, when the data do not contain outliers, all estimators behave similarly to each other (see Table 1). When estimating the regression coefficient , the less efficient robust -estimator naturally results in higher MISE’s. However, this efficiency loss is much smaller for the estimators of . The serious damage caused to the least squares estimators by a small proportion of outliers (10%) can be seen clearly in Figure 3 (solid lines). The integrated squared bias and the MISE of the least squares estimators of and are consistently much higher than those of the robust -estimators. The ways in which the different oultiers affect the classical estimators for can be seen in Figure 4. Note that under the classical becomes highly variable, but mostly retains the same shape of the true , which lies within the central box. However, with high-leverage outliers (as in ) the estimator becomes completely uninformative, and does not reflect the shape of the true regression coefficient . The effect of outliers on the classical estimator for can be seen in Figure 5 (and Figure 6 for its monotone modification). We see that vertical outliers cause a vertical bias in the least squares estimator , so that the central region of the functional boxplot fails to contain the true function for much of its domain. As expected, the effect of high-leverage outliers on is less marked, but certain upwards bias is apparent.

It is interesting to note that the -estimators behave similarly to the classical ones. Vertical outliers result in more variable functional regression -estimators , although this increase is less pronounced than what we saw for the least squares estimators. High-leverage outliers are very damaging to these estimators. In particular, note from Figure 3 that in this case their integrated squared bias and MISE for are almost the same as those for the least squares estimator. We can also see this in Figure 4 where the -estimators do not resemble the true function at all. Similar conclusions hold for the -estimators for . Vertical outliers produce an upward shift on the ’s, and a slight increase in variability, although this is less pronounced than what happened with classical estimators. The behaviour of the -estimator with high-leverage outliers is similar to that of the least squares estimators, although notably their integrated squared bias and MISE is worse than those of the least squares estimators (Figure 3).

In contrast, the -estimators display a remarkably stable behaviour across contamination settings. Their bias and MISE curves in Figure 3 show that the -estimators for and are highly robust against both types of contamination scenarios considered here. If we look at the behaviour of these estimators in Figure 4 we note that the central box and the “whiskers” for the -estimators remain almost constant in all three simulation scenarios (clean data, vertical outliers and high-leverage outliers), in sharp constrast to what happens to the other estimators considered here. The number of affected replicates for is higher for than it is for , but even in the former case this happened for only 45 of the 500 ’s. We expect some effect on the estimators under this type of particularly damaging contamination, and we note that the robust proposal is the only one that can resist it in the vast majority of samples. The results in Figure 5 tell the same story, but less strickingly so. The -estimators for are almost unaffected by the different types of outliers, and the functional boxplots remain very similar to each other.

| Max over | Bias | MISE | Bias | MISE | Bias | MISE |

|---|---|---|---|---|---|---|

| cl | 0.0053 | 1.8616 | 2.4201 | 2.8861 | 2.5686 | 2.8384 |

| m | 0.0023 | 0.3499 | 0.4974 | 0.6651 | 0.5350 | 0.6438 |

| mm | 0.0014 | 0.1317 | 0.0218 | 0.0739 | 0.0209 | 0.0529 |

| Max over | Bias | MISE | Bias | MISE | Bias | MISE |

| cl | 2.9685 | 3.1119 | 0.0540 | 0.1129 | 0.0474 | 0.0829 |

| m | 2.9891 | 3.1318 | 0.0705 | 0.1217 | 0.0583 | 0.0903 |

| mm | 0.0229 | 0.4341 | 0.0242 | 0.0828 | 0.0236 | 0.0607 |

Table 2 reports the maximum values of Bias and MISE over for the two contamination settings and . Regarding the behaviour of the estimators of the functional regression parameter , high-leverage outliers () are more damaging for the classical and -estimators than “vertical” ones (). The increase in square bias shows that the estimation is completely distorted for these estimators. Note that the trimmed squared bias increases more than 1000 times and the MISE more than 30 times with respect to those reported in Table 1. In contrast, the classical estimator of is only slightly affected by , since both the MISE are increased by a factor of at most 2.5 with respect to the ones obtained for clean samples. Vertical outliers, however, produce increases of more than times when where the maximum is attained (see Figure 3). Even though the -estimators of Huang et al. (2015) are affected by both contaminations, they deteriorate less than the classical ones. In particular, when estimating , the -estimator at least triples the under with respect to that obtained for clean samples (the worst effect is observed when , reaching 10 times the value under ). Finally, the -estimators are quite stable under the considered contaminations. In particular, under the values of Biasof are between 8 and 20 times larger than those of , even for their monotone counterparts (see Figure 3), while the increase of the of varies between 3 and 9. Regarding the performance of the estimators of , under , the differences between the -estimators and the -estimators are less pronounced than those between the - and the classical one. Under , the worst of is multiplied less than 5 times with respect to that obtained under . However, it is still only a sixth of the for the classical and -estimator, which suffer from a huge bias. In all cases, the of is smaller than that of .

5 Real data examples

5.1 German electricity prices

In our first example we look at the relationship between hourly electricity prices and the overall load of the German energy system. As discussed in Liebl (2013), such analysis needs to consider that eolic energy prices in this type of markets follow a different price regime. The data consist of hourly electricity prices in Germany between 1 January 2006 and 30 September 2008, as traded at the Leipzig European Energy Exchange, German electricity demand (as reported by the European Network of Transmission System Operators for Electricity), and the amount of eolic energy in the system (taken from the EEX Transparency Platform). The data set is available from the on-line supplementary materials of Liebl (2013). Weekends, holidays and other non-working days were removed from the dataset. Our model is

| (11) |

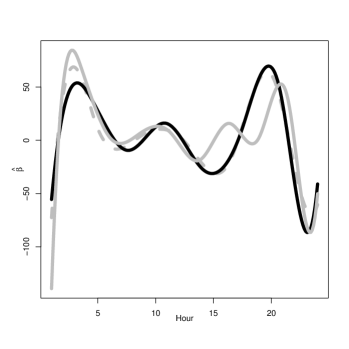

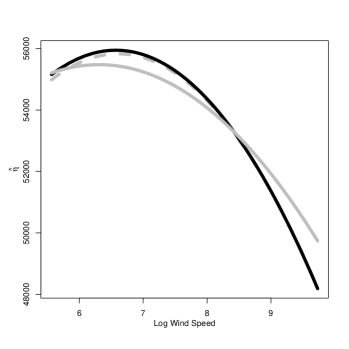

where is the daily average hourly energy demand, is the curve of energy prices (as a function of time) observed hourly, and is the mean hourly amount of wind-generated electricity in the system for that day. As usual, is a random variable centered at zero, and independent from and . The shape of the function can be used to identify times of the day when hourly prices are informative regarding the overall system demand.

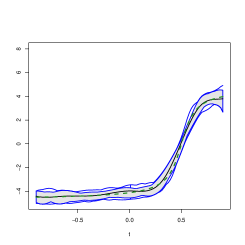

In addition to our proposed robust -estimators, we also computed the classical least squares and the -estimators of Huang et al. (2015). The robust -estimators were calculated using the same -functions as in our simulation study and we selected the size of the splines bases with the criterion (8). Following Huang et al. (2015), the -estimator was computed using a Huber function with tuning constant equal to and no scale estimator.

The estimators for and are shown in Figures 7(a) and 7(b), respectively. Solid black lines are used for the -estimator, and solid gray ones for the least squares one. The -estimators were indistinguishable from the classical ones and so we did not include them in these plots. Comparing the and classical estimators for , we note that the robust fit identifies two “peak” times (around 4am and 8pm) and two “slump” times around 3pm and 11pm, where prices have a larger (in magnitude) association with the daily average load in the system. However, the least squares fit appears to not include the early afternoon prices as important (note that the magnitude of the function is smaller than that of the robust estimator between 2pm and 8pm). On the other hand, although the estimators for are slightly different, their shapes are rather consistent with each other.

We next identified potential outliers in the data by using a boxplot of the residuals from the robust -fit. The dashed lines in Figures 7(a) and 7(b) correspond to the classical fit computed without these possible atypical observations. We note that the classical estimators computed without these potential outliers are very close to the robust ones. In other words, the robust estimator behaves similarly to the classical one if one were able to manually remove suspected outliers.

5.2 Tecator

The Tecator data set was analysed in Ferraty and Vieu (2006), Aneiros-Pérez and Vieu (2006), Shang (2014) and Huang et al. (2015), and it is available in the package fda.usc (Febrero-Bande and Oviedo de la Fuente, 2012). See also http://lib.stat.cmu.edu/datasets/tecator. These data contain measurements taken on samples from finely chopped meat with different percentages of fat, protein and moisture content. Each observation consists of a spectrometric curve, , which corresponds to the absorbance measured on an equally spaced grid of 100 wavelengths between 850 and 1050nm. The goal of the analysis is to predict the fat content () using the spectrometric curve () and the variables water () and protein contents ().

Huang et al. (2015) compared several models in terms of their predictive properties. They used the second derivative of the spectrometric curve as the functional covariate, which enters the model linearly, while the variables appear either through an additive non-parametric component or a varying coefficient model

| (12) |

where and is a smooth function of .

Following Aneiros-Pérez and Vieu (2006), the sample was divided into a training set (corresponding to the first observations) and a testing one with the remaining data points. As in Section 4, the -estimators of Huang et al. (2015) were computed using a Huber function with tuning constant and no scale estimator. The robust -estimators were calculated using the same functions as in our simulation study and we selected the size of the splines bases with the criterion (8). To compare the predictions obtained with the different estimators we computed the mean and median square prediction errors on the test set:

where contains the indices of the observations in the test set, denotes its size, and .

The first three columns and two rows of Table 3 report the mean and median square prediction errors for the classical, and -estimators. Although the least squares and fits have lower mean squared prediction errors than that of the robust one, their larger median suggests that most prediction errors may in fact be smaller for the robust estimator, but that a few outliers may be present in the test set.

| ls | m | mm | ls | |

|---|---|---|---|---|

| 2.52 | 2.44 | 4.56 | 4.83 | |

| 0.95 | 0.85 | 0.65 | 0.78 | |

| 1.47 | 1.42 | 1.33 | 1.40 |

To evaluate the ability of the procedure to predict non-outlying observations, we also computed the mean squared prediction errors over non-outlying points in the test set:

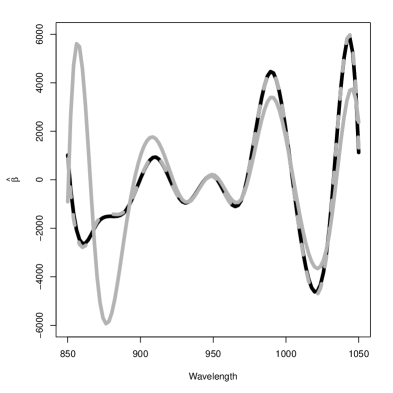

where if the -th observation was flagged as atypical, and 0 otherwise. To identify potential outliers in the data we used the boxplots of the residuals from the fits obtained using the -procedure both for the training and testing sets. The mean squared prediction errors of both estimators using the non-outlying points in the test set () are reported in the last row of Table 3. Note that now the for the -estimators is smaller than those of the least squares and -estimators. The fourth column () of that table displays the results obtained with the classical estimator when it was computed without the 13 potential outliers in the training set. Since the -estimators of Huang et al. (2015) behaved very similarly to the classical ones from now on, we only comment the results obtained when using the least squares and the -estimators.

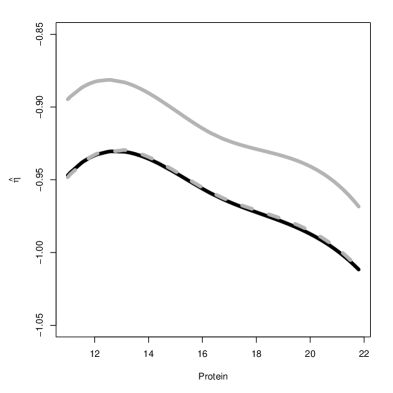

As in the German Electricity example, we note that the classical procedure trained after eliminating potential atypical observations gives very similar results to those obtained with the -estimator. The black and gray solid lines in Figures 8(a) and 8(b) show the estimators and obtained using the classical and robust estimators, respectively. On both panels we also overlay (in dashed gray lines) the corresponding least squares estimates computed on the “cleaned” training set. In both cases it is clear that the classical estimators are seriously affected by the atypical training points, while the robust estimator provides estimates similar to those that are obtained with the classical methods after removing possible outliers.

6 Conclusion

In this paper we propose robust estimators based on -splines for semi-functional linear regression models. Our estimators are robust against outliers in the response variable, and also in the functional explanatory variables. Furthermore, we propose a robust -type criterion to select the optimal dimension of the splines bases that works very well in practice. We prove that the estimators are strongly consistent under standard regularity conditions, and show how they can be extended rather straightforwardly to other semiparametric models with functional covariates that enter the model linearly. A simulation study shows that our proposed estimators have good robustness and finite-sample statistical properties.

We apply our method to two real data sets and confirm that the robust -estimators remain reliable even when the training set contains atypical observations in the functional explanatory variables. Moreover, the residuals obtained from the robust fit provide a natural way to identify potential atypical observations.

7 Acknowledgements.

The authors would like to thank Professor Ioannis Kalogridis for his careful reading of earlier versions of this manuscript and for pointing out a mistake in the proof of Theorem 3.2 which has been corrected in the current version. This research was partially supported by Universidad de Buenos Aires [Grant 20020170100022ba] and anpcyt [Grant pict 2018-00740] at Argentina (Graciela Boente and Pablo Vena), the Ministry of Economy, Industry and Competitiveness, Spain (MINECO/AEI/FEDER, UE) [Grant MTM2016-76969P] (Graciela Boente) and by the Natural Sciences and Engineering Research Council of Canada [Discovery Grant RGPIN-2016-04288] (M. Salibián Barrera).

A Appendix

A.1 Proofs of Proposition 3.1 and Theorem 3.1

In what follows, stands for a neighbourhood of with closure strictly included in . Furthermore, recall that we have denoted , , the space of functions whose th derivative satisfies a Lipschitz condition in :

We use the following norm

where stands for the -th derivative of . The unit ball in will be denoted as .

We begin by stating some Lemmas that will be used in the proofs of Proposition 3.1 and Theorem 3.1. Lemma A.1.1 entails that the functional related to the considered estimators are indeed Fisher–consistent, which is a condition needed to ensure that we are estimating the target quantities.

Lemma A.1.1. Assume that C1 holds and let be a function satisfying R1. Then, we have that, for any ,

-

a)

, where

-

b)

If in addition C2 holds, is the unique minimizer of .

Proof. Lemma 3.1 of Yohai (1987) together with R1 and the fact that satisfy assumption C1 imply that for all ,

| (A.1) |

and a) follows immediately.

To derive b), denote as and . Then, we have that

Note that (A.1) entails that, for any ,

where the last equality follows from the fact that the errors are independent of the covariates. Thus, using that from C2, we get

Let , , denote the linear spaces spanned by the -splines bases of size and :

Recall that and increase with the sample size . The Lemmas below will be useful to derive consistency of the proposed estimators. In particular, the next lemma shows that

converges to with probability one, uniformly over and .

Lemma A.1.2. Let be a bounded function satisfying R1 and R2 and assume that C4 holds. Let and . Then, we have that,

-

a)

.

-

b)

Furthermore,

Proof. b) follows immediately from a) noting that .

To prove (a) we need to introduce some notation. For any measure , and stand for the covering and bracketing numbers of the class with respect to the distance in , as defined, for instance, in van der Vaart and Wellner (1996).

Recall that we have denoted as and and define the class of functions

To obtain a), first note that the boundedness of and R1, entails that the class has envelope 1. Lemma S.2.1 in Boente et al. (2020) allows to bound, for any probability measure , the covering number as

| (A.2) |

where . Hence, using that and assuming without loss of generality that , we get from (A.2) that

for and some constant . Thus, using that from C4 with , we conclude that

which entails, (see, for instance, exercise 3.6 in van der Geer, 2000 with ), that

concluding the proof. ∎

Lemma A.1.3. Let be a bounded function satisfying R1 and R2. Assume that C1 to C4 hold. Then, if in addition , we have that, .

Proof. Recall that and stand for and which are assumed to be of order . Furthermore, we have denoted as , where , and , while

Lemma A.1.2 implies that

| (A.3) |

On the other hand, Lemma A.1.1 entails that , for any , so

with

Note that , which together with (A.3) leads to . Using a Taylor’s expansion of order one and assumption R2, we get that

where is an intermediate point, which together with the fact that lead to .

We will now bound . Using C3 and C4 and that , we get from Corollary 6.21 in Schumaker (1981) that there exist and such that

Hence, using that minimize , we obtain that , where , and . Note that the strong consistency of and the fact that and entail that can be bounded by , so that . Arguing as above when bounding , we conclude that . Finally, using that entail that for any , , together with the continuity and boundedness of and the bounded convergence theorem leads to . Hence, we get that

that is, , concluding the proof of a). Note that the fact that entails also that . ∎

Lemma A.1.4. Let be a bounded function satisfying R1 and R2 and such that . Let , and be such that . Assume that and that C3 and C5 hold with . Then, we have that, there exists such that .

Note that whenever , so if then and the condition was also a requirement in Yohai (1987).

Proof. Recall that is a compact set for the topology of the norm , that is, as merged in . Given , define such that for any ,

| (A.4) |

Let and fix . Let be a continuity point of the distribution of such that

Then, if is such that , where , we have that

Hence, noting that , we conclude that

| (A.5) |

Let us consider the covering of given by , where stands for the open ball with center and radius , that is, . The fact that is a compact set in entails that is also compact, so there exist , , such that with . Therefore, from (A.5), we obtain that

with , meaning that for any , there exist such that

| (A.6) |

Let be such that and for each , . Fix and let such that . Then, there exists such that for each , , where to strength the dependence on we have denoted .

We want to show that there exists such that, for , . For that purpose it will be enough to show that there exist such that,

Denote as . First note that, the independence between the errors and covariates entails that

Using that , we get that for any , there exists such that, for any such that ,

| (A.7) |

Choose , where is given in (A.6) and let be such that and

Denote as and , then , thus using (A.6), we obtain that there exists such that

Using that and denoting as , we obtain that whenever , which together with (A.7) leads to

where the last inequality follows from (A.6). Therefore,

The proof follows now easily noting that , so we can choose and consequently such that

so , concluding the proof. ∎

Proof of Proposition 3.1. Recall that we have defined and we have assumed that where is the solution of

meaning that . Besides, the scale estimators satisfy

To avoid burden notation, we will briefly denote and instead of and .

We will show that for any , with probability there exists such that for , we have .

Using Lemma A.1.2 with , we have that

Then, there exists a null set such that, for any ,

| (A.8) |

holds. On the other hand, the strong law of large numbers entails that

which together with the fact that implies that

Thus, there exists a null set such that, for any ,

| (A.9) |

Finally, taking into account that , from the strong law of large numbers and the fact that , we get that there exists a null set such that, for any ,

| (A.10) |

Fix .

We will begin by showing that, there exists such that , for . Using C3 and C4 and the results in Schumaker (1981), we get that there exists and such that

| (A.11) |

A Taylor’s expansion of order one leads to

where

and is an intermediate point. From (A.9), we get immediately that

Besides, the bound

together with (A.10) and (A.11) lead to . Hence,

Choose such that , then there exists such that for ,

| (A.12) |

Noting that

from (A.12) and the fact that is non-decreasing we immediately obtain that . Using that and the fact that and , we conclude that for , .

It remains to show that there exists such that for any , .

The fact that is non–decreasing together with C1 implies that (see Lemma 3 in Salibián–Barrera, 2006). Let be such that . Using that (A.8) holds, we get that there exists such that for any ,

Hence,

leading to

On the other hand, the fact that and is bounded implies that

so without loss of generality, we may assume that for any ,

Note that Lemma A.1.1 entails that , thus we get

which implies that for , concluding the proof. ∎

Proof of Theorem 3.1. For the sake of simplicity let and . From Lemmas A.1.3 and A.1.4 with , it will be enough to show that, for any ,

where and .

As in the proof of Lemma A.1.4, let be such that

and denote . Then, from the fact that is bounded, using the Arzela–Ascoli Theorem, we obtain that there exists a subsequence such that and converge uniformly to functions and . Denote as and the uniform limit of and , respectively. Hence, we have that , and , so that with . Using that is a bounded continuous function, from the Bounded Convergence Theorem, we obtain that implying that . Lemma A.1.1 together with the fact that , entail that concluding the proof. ∎

A.2 Proof of Theorem 3.2

Let us denote as and as , where is given in assumption C6. Note that, except for a null probability set, , for large enough. From now on, for a function we denote as , that is, the norm.

The following Lemma gives conditions under which C6 holds.

Lemma A.2.1. Let be a bounded function satisfying R1 and R2 and such that is continuously differentiable with bounded derivative and . If there exists such that , then C6 holds.

Proof. As in the proof of Theorem 3.1, denote and , then we have that

where is an intermediate point between and . Note that , hence if , we get that with probability 1.

The fact that and the continuity of entails that for small enough

Hence, if and , we have that

concluding the proof. ∎

Recall that for any vectors of coefficients and , and . In order to prove Theorem 3.2, we will need the following Lemma.

Lemma A.2.2. Let be a bounded function satisfying R1 and R2. Given and , let be such that and . Define the class of functions

with , , a fixed point and

for . Then, if , there exists some constant independent of , , and , such that

Proof. First note that, for any , , we have that there exist a constant depending only on the degree of the considered splines such that

| (A.13) |

where for a vector , (see de Boor, 1973, Section 3).

Then, we have that and , where , , ,

Recall that the ball can be covered by at most balls (with respect to the norm ) of radius , when , while if the covering number equals 1. Hence, using the upper bounds given in (A.13) and using that for any class of functions , , we obtain that

| (A.14) | ||||

| (A.15) |

for . Henceforth, using (A.14) and (A.15), we get that, for any , can be covered by a finite number of brackets , while can be covered by a finite number of brackets .

On the other hand, the set can be covered by balls of radius (when ) and center , , where .

Recall that is bounded, so that, for ,

Define where

Given , let , and be such that belongs to the bracket , that is, and , belongs to the bracket and . Denote as

Using a Taylor’s expansion of order one and the fact that is bounded, we get that

where the last inequalities follow from the fact that , , , so that and . Define the functions

Then, we have that and taking into account that , we obtain

which means that the total number of brackets of size needed to cover is bounded by

with , where we have used that , concluding the proof of the first inequality. ∎

The following Lemma is needed in the proof of Theorem 3.2. Its proof follows using similar arguments to those considered in the proof of Theorem 3.2.5 of van der Vaart and Wellner (1996), we include it for completeness. In the statement of Lemma A.2.3, , corresponds to the set , while as defined above.

Lemma A.2.3. Let be an stochastic process indexed by and where . Let be an estimator of such that where and denote as the minimizer of over , that is, , for any . Let be a fixed sequence such that and fix with for all . Assume that and , where is a fixed sequence. Furthermore, assume that there exists a function such that is decreasing on and that for any , we have

| (A.16) | |||||

| (A.17) |

where , the symbol means less or equal up to a universal constant and stands for the outer expectation. Then, if is such that and , for every , we have that .

Proof. Note that for each fixed ,

where . Let , then we have

For any such that , denote . Using (A.16), we get that, for any such that , and , , where is a universal constant independent of , . In particular, when and , we have

Besides, since minimizes over and . Thus, if we denote , we have that, whenever and ,

so

leading to

where the last inequality is a consequence of Markov’s inequality and (A.17) and is a universal constant.

The fact that is decreasing entails that

which together with the assumption that , implies that

which converges to 0 when . Thus, using that , and , we obtain that for any , there exists and such that for , , concluding the proof. ∎

Proof of Theorem 3.2. As in the proof of Lemma A.1.3, let and , such that , and denote . Furthermore, denote as and the vectors such that and where and .

In order to get the convergence rate of our estimator we will apply Lemma A.2.3. Let , where with , and is given in C6. The consistency of entails that , while from Theorem 3.1 we obtain that . Furthermore, the condition for any is trivially fulfilled.

The triangular inequality implies that , therefore

| (A.18) |

Using that , , and (A.18) we obtain that as required in Lemma A.2.3.

It remains to show that there exists a function such that is decreasing on for some and that for any , we have

| (A.19) | |||||

| (A.20) |

where and

Assumption C6 implies that for any , . Besides, the fact that the errors have a symmetric distribution and are independent of the covariates entail that

so

where and is an intermediate values between and . Thus, using (A.18) and that we obtain that

where the last inequality follows from the fact that , concluding the proof of (A.19).

We have now to find such that is decreasing in and (A.20) holds. Define the class of functions

with

for . The inequality (A.20) involves an empirical process indexed by , since

For any we have that . Furthermore, if using that for any , we have

and the fact that , we get that

Lemma 3.4.2 van der Vaart and Wellner (1996) leads to

where is the bracketing integral of the class .

Recall that , so that, for any , we have . Hence, with , and the bound given in Lemma A.1.6 leads to

for some positive constants and independent of , and . Therefore,

Note that as , hence there exists and a constant such that for any , . This implies that, for ,

If we denote , we obtain that for some constant independent of and ,

Choosing

we have that is decreasing in , concluding the proof of (A.20).

Note that, since and , we have that as required in Lemma A.2.3. To apply Lemma A.2.3, we have to prove that , since , for . Note that

where . Hence, to derive that , it is enough to show that , which follows easily since and , concluding the proof.

Hence, from Lemma A.2.3, we get that . On the other hand, together with the fact that entail that . Thus, from the triangular inequality we immediately get that , concluding the proof. ∎

References

- [1] Aneiros-Pérez G. and Vieu P., 2006. Semi-functional partial linear regression. Statistics and Probability Letters, 76, 1102-1110.

- [2] Boente, G., Rodríguez, D. and Vena, P., 2020. Robust estimators in a generalized partly linear regression model under monotony constraints. Test, 29, 50-89.

- [3] Boente, G. and Vahnovan, A., 2017. Robust estimators in semi-functional partial linear regression models. Journal of Multivariate Analysis, 154, 59-84.

- [4] Cardot, H., Ferraty, F., and Sarda, P., 2003. Spline estimators for the functional linear model. Statistica Sinica, 13, 571-591.

- [5] de Boor, C., 1973. The quasi-interpolant as a tool in elementary polynomial spline theory, in Approximation Theory (G. G. Lorentz et al., eds), pp. 269-276. Academic Press, New York.

- [6] Febrero-Bande, M., Oviedo de la Fuente, M. (2012). Statistical Computing in Functional Data Analysis: The R Package fda.usc. Journal of Statistical Software, 51(4), 1-28. URL: http://www.jstatsoft.org/v51/i04/.

- [7] Ferraty, F. and Vieu, Ph., 2006. Nonparametric Functional data analysis: Theory and Practice. Springer Series in Statistics, Springer, New York.

- [8] Härdle, W., Liang, H. and Gao, J., 2000. Partially linear models. Springer-Verlag.

- [9] Härdle, W., Müller, M., Sperlich, S. and Werwatz, A., 2004. Nonparametric and Semiparametric Models. Springer.

- [10] He, X. and Shi, P., 1998. Monotone B-Spline smoothing. Journal of the American Statistical Association, 93, 643-650.

- [11] He, X., Zhu, Z. and Fung, W., 2002. Estimation in a semiparametric model for longitudinal data with unspecified dependence structure. Biometrika, 89, 579-590.

- [12] Huang, L., Wang, H., Cui, H. and Wang, S., 2015. Sieve -estimator for a semi-functional linear model. Science China, Mathematics, 58, 2421-2434.

- [13] Kalogridis, I. and Van Aelst, S., 2019. Robust functional regression based on principal components. Journal of Multivariate Analysis, 173, 393-415.

- [14] Lian, H., 2011. Partial functional linear regression. Journal of Nonparametric Statistics, 23, 115-128.

- [15] Liebl, D., 2013. Modelling and forecasting electricity spot prices: a functional data perspective. The Annals of Applied Statistics, 7:3, 1562-1592.

- [16] Maronna, R., Martin, R., Yohai, V. and Salibián-Barrera, M., 2019. Robust Statistics: Theory and Methods (with R). Wiley, New York.

- [17] Maronna, M. and Yohai, V., 2013. Robust functional linear regression based on splines. Computational Statistics and Data Analysis, 65, 46-55.

- [18] Neumeyer, N., 2007. A note on uniform consistency of monotone function estimators. Statistics and Probability Letters, 77, 693-703.

- [19] Qingguo, T., 2015. Estimation for semi-functional linear regression. Statistics, 49, 1262-1278.

- [20] Ronchetti, E., 1985. Robust model selection in regression. Statistics and Probability Letters, 3, 21-23.

- [21] Salibián-Barrera, M., 2006. The asymptotics of MM–estimators for linear regression with fixed designs. Metrika, 63, 283-294.

- [22] Schumaker,L., 1981. Spline Functions: Basic Theory, Wiley, New York.

- [23] Schwarz, G., 1978. Estimating the dimension of a model. Annals of Statistics, 6, 461-464.

- [24] Shang, H.L., 2014. Bayesian bandwidth estimation for a semi-functional partial linear regression model with unknown error density. Computational Statistics, 29, 829-848.

- [25] Stone, C.J., 1986. The dimensionality reduction principle for generalized additive models. Annals of Statistics, 14, 590-606.

- [26] Sun, Y. and Genton, M. G., 2011. Functional boxplots. Journal of Computational and Graphical Statistics, 20, 316-334.

- [27] Tharmaratnam, K. and Claeskens, G., 2013. A comparison of robust versions of the AIC based on , and estimators. Statistics, 47, 216-235.

- [28] Van de Geer, S., 2000. Empirical Processes in M–Estimation, Cambridge University Press.

- [29] van der Vaart, A. and Wellner, J., 1996. Weak Convergence and Empirical Processes. With Applications to Statistics. Springer–Verlag, New York.

- [30] van der Vaart, A. (1998). Asymptotic Statistics. Cambridge Series in Statistical and Probabilistic Mathematics.

- [31] Yohai, V. J., 1987. High breakdown-point and high efficiency robust estimates for regression. Annals of Statistics, 15 642-656.

- [32] Zhou, J. and Chen M., 2012. Spline estimators for semi-functional linear model. Statistics and Probability Letters, 82,505-513.