Treatment Effects in Interactive Fixed Effects Models with a Small Number of Time Periods††thanks: We thank the editor and two anonymous referees as well as Nicholas Brown, Weige Huang, Pedro Sant’Anna, Emmanuel Tsyawo, Jeffrey Wooldridge, and seminar participants at Michigan State University, the University of São Paulo, the 26th International Conference on Panel Data, and the 2020 Southern Economics Association Conference for helpful comments. A previous version of this paper was circulated with the title “Treatment Effects in Interactive Fixed Effects Models.” Code for the approach suggested in the current paper is available in the R package ife which is available at https://github.com/bcallaway11/ife.

Abstract

This paper considers identifying and estimating the Average Treatment Effect on the Treated (ATT) when untreated potential outcomes are generated by an interactive fixed effects model. That is, in addition to time-period and individual fixed effects, we consider the case where there is an unobserved time invariant variable whose effect on untreated potential outcomes may change over time and which can therefore cause outcomes (in the absence of participating in the treatment) to follow different paths for the treated group relative to the untreated group. The models that we consider in this paper generalize many commonly used models in the treatment effects literature including difference in differences and individual-specific linear trend models. Unlike the majority of the literature on interactive fixed effects models, we do not require the number of time periods to go to infinity to consistently estimate the ATT. Our main identification result relies on having the effect of some time invariant covariate (e.g., race or sex) not vary over time. Using our approach, we show that the ATT can be identified with as few as three time periods and with panel or repeated cross sections data.

Keywords: Interactive Fixed Effects, Treatment Effects, Panel Data, Repeated Cross Sections, Treatment Effect Heterogeneity

JEL Codes: C21, C23

1 Introduction

One of the most common ways to identify the causal effect of a binary treatment (e.g., participating in a program or being affected by some economic policy) on an outcome of interest is to exploit variation in the timing of treatment across different individuals. In this sort of setup, the central idea is to impute the average outcome that individuals that participate in the treatment would have experienced if they had not participated in the treatment using a combination of their observed pre-treatment outcomes and the path of outcomes for a group of individuals that does not participate in the treatment. One can then estimate the average effect of participating in the treatment (for the group of individuals that participate in the treatment) as the difference in average observed outcomes and the average imputed value for individuals that participate in the treatment.

The most common version of this approach is difference in differences (DID) where the key identifying assumption is that, in the absence of treatment, the “path” of outcomes that the treated group would have experienced is the same, on average, as the path of outcomes that an untreated group did experience. The main motivating model for the DID approach is one in which untreated “potential” outcomes are generated by a two-way fixed effects model; that is, a model that allows for time invariant unobserved heterogeneity that may be distributed differently across the treated and untreated groups as well as allowing for time fixed effects. This model is consistent with the so-called “parallel trends” assumption underlying the DID approach (see, for example, [14, 16, 28]). However, the parallel trends assumption may not hold in many applications; often, a main concern is that the effect of some unobserved time invariant variable may change over time which would cause the parallel trends assumption to be violated. In those cases, researchers often resort to other approaches such as including individual-specific linear trends ([32, 65, 52]).

We generalize both the two-way fixed effects model and these alternative approaches by imposing that the model for untreated potential outcomes has an interactive fixed effects structure (also known as factor structure). These models allow for the effect of time invariant unobservables to change over time. In particular, we consider the following sort of model for untreated potential outcomes:

| (1) |

where is an individual’s untreated potential outcome in time period , is a time fixed effect, are unobserved, time invariant individual characteristics, and is a time varying effect of . Notice that this model generalizes the common two-way fixed effects model; in particular, they are the same when does not change across time (implying that the term does not change over time and standard DID approaches can be applied). This model also generalizes individual-specific linear trend models that are commonly used in applied work; in particular, this would be true when in all time periods.111The model in Equation 1 includes a single interactive fixed effect. This is a leading case as it generalizes all the most common approaches taken in the treatment effects literature; also, it corresponds to more structural interpretations where the researcher is concerned about a particular unobserved time invariant variable whose effect can change over time. In Section 5.1, we discuss the case when there can be more than one interactive fixed effect. A main motivation for this sort of model is one where a researcher worries that (i) there are time invariant unobserved variables that affect the outcome of interest that are not observed in the data, and (ii) the effect of one of those time invariant unobservables varies over time.

In the current paper, we develop a new approach to identifying treatment effects when untreated potential outcomes are generated from an interactive fixed effects model as in Equation 1. Unlike previous work on treatment effects in interactive fixed effects models, our approach does not require the number of time periods to go to infinity to consistently estimate the effect of participating in the treatment. We consider the case where a researcher observes a vector of time invariant covariates (e.g., race, sex, or education). The key assumption of our main approach is that the effect of at least one of the covariates on untreated potential outcomes does not change over time. The effect of this covariate is not identified, but we show that it can still be useful for identifying the effect of participating in the treatment. This sort of covariate is likely to be available in many applications in economics as it would be available in any model for untreated potential outcomes where some particular covariate “drops out” due to not varying over time (up to an instrument relevance condition that can be checked with the available data). In this case, we show that the ATT is identified with only three periods (this is the same requirement as for individual-specific linear trend models and one more time period than is required for DID models). In practice, our approach amounts to using this time invariant covariate as an instrument for the change in outcomes over time in a regression that “differences out” the individual fixed effects. This time invariant covariate is allowed to affect the level of untreated potential outcomes (just not to directly affect the path of untreated potential outcomes over time); we also do not use it as an instrument for participating in the treatment. Interestingly, this approach can be implemented with repeated cross sections data. We appear to be the first paper to propose a method allowing for interactive fixed effects that can be implemented with only repeated cross sections data.

We also develop estimators of the ATT using our approach. We propose a two-step estimator where, in the first step, we estimate the parameters in the interactive fixed effects model for untreated potential outcomes. In the second step, we plug these in to obtain estimates of the ATT. In the case with exactly three time periods and one covariate whose effect does not change over time, the ATT is exactly identified. With more than one covariate whose effect does not change over time, the ATT is over-identified and the restrictions that the effects of covariates do not vary over time can be tested. With more than three periods, one can conduct “pre-tests” for (i) the effect of participating in the treatment being 0 in periods before individuals become treated as well as for (ii) the effect of particular covariates not varying over time. We also extend our baseline results to the case where there is variation in treatment timing across individuals (as has been considered in recent work on DID such as [30, 18]).

We conclude the paper with an application on the effect of early-career job displacement on earnings. In the job displacement literature, researchers are typically concerned that “skill” is unobserved and cannot be directly controlled for. If the return to skill varies over time or with experience, then standard approaches such as difference in differences are likely to lead to biased estimates of the effect of job displacement. On the other hand, the approach proposed in the current paper can deal directly with this issue. Compared to difference in differences, the interactive fixed effects approach proposed in the current paper does somewhat better in pre-treatment periods (in the sense of estimating no effect of job displacement in pre-displacement periods) while finding somewhat smaller long-term effects of job displacement.

The outline of the paper is as follows. Section 2 provides our main identification arguments. Section 3 discusses some limitations of difference in differences and linear trends approaches in the context of interactive fixed effects models for untreated potential outcomes. Section 4 proposes an estimation and inference strategy. Section 5 provides a number of extensions to our main identification strategy. Section 6 provides Monte Carlo simulations related to comparing our approach to difference in differences and linear trends. Section 7 includes an application on job displacement. The Supplementary Appendix provides some alternative identification strategies; additional Monte Carlo simulations concerning (i) weak instruments, (ii) estimation with multiple interactive fixed effects, and (iii) selecting the number of interactive fixed effects; and some additional results for our application on job displacement.

Related Literature

There is a large literature on linear models with interactive fixed effects. Important early work in this literature includes [54, 9]. For estimation, these papers and much subsequent work require a large number of time periods (i.e., the number of time periods goes to infinity). Our paper is particularly related to [29, 66]. Like the current paper, these papers model untreated potential outcomes by imposing an interactive fixed effects structure. In the case where a researcher is interested in the effect of a binary treatment, this approach has a major advantage over imposing linear models for all outcomes — this setup places no restrictions on how treated potential outcomes are generated at all. Thus, one can allow for unrestricted forms of treatment effect heterogeneity, very general forms of selection into treatment, and treatment effect dynamics. The key difference between our approaches are that we do not require a large number of time periods, but we do require access to a covariate whose effect does not change over time. Our approach should ultimately be seen as complementary to the approaches taken in those papers and, in particular applications, the relative merits of these approaches mainly comes down to data availability and the plausibility of the condition that effects of covariate(s) do not vary over time.

The current paper is also closely related to work on factor models with a small number of measurements (for example, [5, 34, 20, 35, 64]). Related work on panel data models with interactive fixed effects and with a small number of periods includes [36, 4, 3, 56, 26, 44]. Of these, the most similar is [3]; like that paper, we obtain identification using a “differencing” approach and by providing some extra moment conditions. Our paper is different in that we specifically focus on a treatment effects setup (e.g., our approach allows for much more general forms of treatment effect heterogeneity than simply including a treatment dummy variable directly in an interactive fixed effects model). We also focus on the case with time invariant covariates (discussed in more detail below) rather than time varying covariates. Our paper is also related to [25]. That paper deals with a more general form of unobservables (time-varying rather than interactive fixed effects) that confound identifying the effect of the treatment; on the other hand, our approach allows for the excluded variable to be time invariant and to directly affect the outcome as well as allowing for more general treatment effect heterogeneity (though it would seem possible to extend their approach along this dimension). [27] allows for violations of parallel trends when individuals belong to a latent class in the case where there are a small number of time periods. Finally, a number of other approaches (particularly in the literature on synthetic controls and matrix completion) are motivated by an underlying interactive fixed effects model; see, for example, the discussion in [2]. These include [38, 46, 50, 39, 55, 7, 12, 24, 45, 8, 11, 51], among others.

2 Identification

2.1 Notation and Parameters of Interest

We use potential outcomes notation throughout the paper. Let denote an individual’s outcome in a particular period (we drop an individual subscript throughout much of the paper except where it enhances clarity). We assume that a researcher has access to periods of data. Individuals either belong to a treated group or untreated group. We set to be a treatment indicator so that for individuals in the treated group and for the untreated group. We assume that treatment occurs in period which is the same across all individuals (we discuss the case with variation in treatment timing in Section 5.4). Individuals have treated potential outcomes (the outcomes that would occur if an individual were treated) and untreated potential outcomes (the outcomes that would occur if an individual were not treated) at each time period. We denote these by and , respectively, for . In pre-treatment periods, i.e. , for all individuals; that is, we observe untreated potential outcomes for all individuals in these periods. When , ; that is, in period and subsequent time periods, we observe treated potential outcomes for individuals that participate in the treatment and untreated potential outcomes for individuals that do not participate in the treatment.

We also suppose that we observe a vector of covariates that are time invariant. Time invariance of the covariates is essentially standard in the literature on treatment effects with panel data ([33, 1, 18]).222There is an interesting difference between the econometrics literature and common practices in applied work in the presence of time varying covariates. The econometrics literature typically conditions on a single value of pre-treatment covariates in this case. This approach can allow for the treatment to have an effect on the covariates themselves; moreover, it can be rationalized under additional assumptions on how time-varying covariates would have evolved in the absence of participating in the treatment. On the other hand, applied work most often estimates two way fixed effects regressions that only include covariates that vary over time and that rely on additional functional form assumptions as well as exogeneity assumptions that rule out the treatment having an effect on the covariates. Unlike traditional panel data models, the objective in the treatment effects literature is not to estimate the effect of the covariates, but simply to control for them. Thus, time invariant (or pre-treatment) covariates allow us to compare outcomes or the path of outcomes for individuals who have the same characteristics rather than focusing on using variation in these covariates over time to identify their effects. A key difference between our approach and standard two-way fixed effects regressions is that we treat the treatment variable asymmetrically from the other covariates. Another concern about time varying covariates is that participating in the treatment may affect the path of some time varying covariates ([49, 15]). It seems possible to extend our results to allow for time varying covariates along the lines of marginal structural models ([57, 40, 13]), but we do not pursue this here.

The main parameter that we are interested in is the Average Treatment Effect on the Treated (ATT); we define as the average treatment effect on the treated in period . That is,

allows researchers to consider how treatment effects vary across time periods / length of exposure to the treatment. When is identified, it can also be aggregated into an overall across all post-treatment time periods

which is just the average of across all post-treatment time periods.

The first main assumption is about the data generating process for untreated potential outcomes. In particular, we impose the following structure on untreated potential outcomes in each time period.

Assumption 1 (Model for Untreated Potential Outcomes).

Untreated potential outcomes are generated by the following interactive fixed effects model

We assume that in all time periods, untreated potential outcomes are generated by an interactive fixed effects model that includes an individual fixed effect, a time fixed effect (to conserve on notation we absorb the time fixed effect into the term by having include an intercept and where the corresponding element of is equal to the time fixed effect), and a single time invariant unobservable whose “effect” can change over time.

Some important comments about the model in Assumption 1 are in order. First, Assumption 1 only puts structure on how untreated potential outcomes are generated. It does not put any structure on how treated potential outcomes are generated, and this allows for essentially unrestricted treatment effect heterogeneity. In particular, our setup allows for individuals to select into the treatment on the basis of having “good” treated potential outcomes relative to individuals who do not participate in the treatment. Not putting any structure on treated potential outcomes comes at the cost of not identifying more general parameters such as the average treatment effect (for the entire population). In particular, this means that it may be difficult to predict what the effect of participating in the treatment would have been for individuals that did not participate in the treatment; however, this is a standard issue for DID-type methods. Second, Assumption 1 allows for the distributions of , , and to be different for individuals in the treated group relative to the untreated group. In the spirit of fixed effects models, Assumption 1 also allows for these variables to be arbitrarily correlated with each other.

Third, having the coefficient on vary over time follows the difference in differences literature. If one removes the interactive fixed effect term from the model in Assumption 1, then this is exactly the sort of model that gives rise to conditional parallel trends assumptions that are common in the econometrics literature ([33, 1, 18]). Including the interactive fixed effect puts the unobserved into the model in the same way as the covariates. This means that, if we were to observe both and , then the path (not the level) of untreated potential outcomes that individuals in the treated group would have experienced if they had not not participated in the treatment is the same as the path of outcomes that individuals in the untreated group did experience conditional on having the same values of and . In other words, if we observed , then we could just use a conditional difference in differences approach, but, since we do not observe it, we need to make some modifications. Finally, Assumption 1 restricts the dimensionality of the interactive fixed effect term to be equal to one. We discuss the extension to multiple interactive fixed effects in Section 5.1.

We also make the following assumptions throughout the paper.

Assumption 2 (Observed Data).

The observed data consists of iid draws of , where denotes the sample size.

Assumption 3 (Treatment Timing).

and .

Assumption 4 (Factors).

.

Assumption 5 (Selection on observables and time invariant unobservables).

For all ,

Assumption 2 says that we observe panel data with time periods. We discuss extending the results to the case with repeated cross sections in Section 5.2 and note here that this extension is straightforward. Assumption 3 says that we have access to at least three periods of data, that treatment starts in period for all individuals that participate in the treatment, and that we have at least two pre-treatment periods for individuals in the treated group. Assumption 4 says that there is variation in in the two periods immediately preceding treatment. Practically, this assumption implies that differences in in pre-treatment periods lead to differences in average paths of outcomes in pre-treatment periods. Assumption 5 is the same as Assumption 2 in [29] and is similar to Assumption 1 in [27]. Moreover, it is similar to the assumption of selection on observables that is commonly invoked in the treatment effects literature with cross sectional data (see, for example, [42]); however, in our case, Assumption 5 holds after conditioning on the unobserved heterogeneity including the time invariant unobservable whose effect can change across time. In particular, it says that our main identification challenge is due to and being unobserved. It implies that, if one could observe and condition on both and , that average untreated potential outcomes would be the same in the treated and untreated groups. This would also imply that, were the unobserved heterogeneity and interactive fixed effect observed, one could use a variety of well known approaches (e.g., least squares regression, propensity score re-weighting, or matching) to estimate the ATT. In our case, where these time invariant variables are unobserved, this assumption is potentially helpful because untreated potential outcomes are not observed for the treated group (in some periods), but they are observed for the untreated group in all periods.

In the context of the model in Assumption 1, an important implication of Assumption 5 is that it is equivalent to

| (2) |

Equation 2 immediately implies that the time varying unobservables in Assumption 1 are uncorrelated with the observed covariates, with the time invariant unobservables in the model, and with whether or not an individual participates in the treatment. These are all typical assumptions in the interactive fixed effects literature. That these unobservables are uncorrelated with covariates and treatment status will eventually be a source of moment conditions that we use to identify the parameters in the model. Equation 2 also makes clear the main type of restriction that we place on how individuals select into participating in the treatment. In addition to allowing for individuals to select into the treatment on the basis of their treated potential outcomes, we allow for individuals to select into treatment on the basis of their time invariant unobservables that affect untreated potential outcomes , but we do not allow individuals to select into treatment on the basis of time varying unobservables, .

Next, we outline the challenges that a researcher faces for identifying when untreated potential outcomes are generated by the interactive fixed effects model in Assumption 1. As a first step, we discuss a “quasi-differencing” strategy in order to write down equations that do not depend on or .333Quasi-differencing is common in the interactive fixed effects literature especially in the case with a “small” number of time periods (see, for example, [36, 3]). Notice that, given the model in Assumption 1,

| (3) |

Because no one is treated before period , the researcher observes untreated potential outcomes in the two time periods immediately preceding treatment for both treated and untreated individuals. Further, one can immediately solve this equation for :

| (4) |

which follows by re-arranging the expression in Equation 3. Using similar arguments, it additionally follows that

| (5) |

where we define , , and where the second equality holds by plugging in the expression for in Equation 4 and re-arranging terms. The result in Section 2.1 holds for all for both the treated group and the untreated group, and, importantly, Section 2.1 has differenced out the time invariant unobservables.

Next, in order to think about identifying , notice that, for any time period ,

| (6) |

where the second equality holds by adding and subtracting , and the third equality holds by writing potential outcomes in terms of their observed counterparts, by Section 2.1, and by Assumptions 1 and 5. Section 2.1 suggests that the key identification challenge is to be able to recover the parameters and ; all the other terms in Section 2.1 are immediately identified from the sampling process. It is also worth pointing out that identifying is not as challenging as identifying itself in all time periods, and, in particular, notice that we do not need to impose any of the normalizations on that are common in the interactive fixed effects literature.

Because, in the post-treatment periods , is only an observed outcome for individuals in the untreated group, Section 2.1 therefore suggests recovering these parameters using the untreated group. That being said, and are not immediately identified in Section 2.1 because is correlated with by construction. We discuss our approach to identifying and (and hence ) next.

Remark 1.

The above arguments relied on differencing both and by , but there alternative differencing strategies that could eliminate the time invariant unobserved heterogeneity terms. One advantage of the present strategy is that it only relies on the interactive fixed effects model for untreated potential outcomes holding from period to period and is therefore robust to violations of this model in earlier time periods.444Imposing that the structure of the model holds over a large number of time periods may be restrictive in many applications. For example, in a related context, [7] note that “it may be difficult to find a simple specification…that fits well over the entire panel.” A main alternative would be to difference by . This strategy would require that the interactive fixed effects structure hold in all pre-treatment periods, though it would not require Assumption 4 (that ) but would instead require ; this might be attractive in cases where does not change across some time periods.

2.2 Identification through Covariates with Time Invariant Effects

In this section, we present our main identification strategy. As a first step, notice that Equation 2 combined with Section 2.1 provides a number of moment conditions that are relevant for identifying . In particular, the available moment conditions are

These moment conditions are equivalent to

| (7) |

To begin with (and for simplicity), consider the case where (i.e., the researcher has access to three periods of panel data). Then, Equation 7 contains moment conditions. However, there are parameters to identify; is and is an extra scalar parameter to identify. Hence, there are not enough moment equations to identify all the parameters.

Next, we introduce our main identifying assumption.

Assumption 6 (Availability of Covariate(s) with Time Invariant Effects).

There exists a set such that for all and for all time periods .

Assumption 6 introduces the central idea of our identification strategy. In particular, we suppose that at least one of the parameters does not depend on time. In many cases, this is a very weak requirement. In particular, researchers often omit time invariant covariates because they are “absorbed” into the fixed effect — this indeed does hold if the effect of some time invariant covariate does not vary over time. Thus, any covariate that a researcher would otherwise omit from the model because it does not vary over time is a good candidate here.

To formalize things, set which partitions the observed covariates into a group of covariates with time varying effects on the outcome and another group of covariates whose effects do not change over time; these satisfy . Correspondingly, partition where is a dimensional vector and is a dimensional vector that does not change across time periods, and likewise, partition .555 Given the definition of , if for all time periods, then that immediately implies for all time periods . Then, we write the model in Assumption 1 as

| (8) |

is not identified in Equation 8 and, in applications, information on is often completely discarded. However, the presence of still provides potentially useful moment conditions. In Equation 8 (and in each time period), there are now parameters to identify, and moment conditions available to identify them. Then, as long as (i.e., as long as there is at least one variable whose effect does not change over time), our approach satisfies the necessary order condition that .

The simplest version of this approach is the case where we have exactly three time periods, panel data, and is a scalar. Then, our idea amounts to estimating and using the sample of untreated individuals by estimating the model

using as an instrument for . In order for and to be identified here, we just require standard exogeneity and relevance conditions for instrumental variables estimation. Exogeneity holds by Assumption 6 (along with Assumption 5). Relevance will hold if . The main requirement here is that is correlated with after controlling for . This condition can be checked in particular applications.666A relevant intermediate case is when is a weak instrument for . Existing strategies for dealing with weak instruments can be applied in our setup. For example, standard diagnostics for weak instruments (e.g., [61, 47, 53, 59]) can be used. Alternatively, one could employ estimation strategies designed for the case with weak instruments (e.g., [31, 6, 62]). In fact, an alternative equivalent condition is that ; this condition says that is correlated with after controlling for . In other words, we need to find a variable whose effect on untreated potential outcomes does not change over time (i.e., this variable does not affect the path of untreated potential outcomes over time) and that is correlated with the time invariant unobservable whose effect changes over time.

To give an example, in the application in the paper, we study the effect of job displacement on earnings. There, we are concerned that the return to “skill”, which is unobserved, could vary over time. In this case, there are several possibilities for which variables to impose that their effect on untreated potential outcomes does not change over time. First, covariates such as race, sex, and education often “drop out” in applications on job displacement because they do not change over time. This suggests that any of these are potential candidates here.777It’s worth pointing out that just because a covariate does not vary over time does not automatically imply that the path of untreated potential outcomes does not depend on it. In Section 5.3, when there are extra available pre-treatment periods, we develop a test for covariates having time invariant effects in pre-treatment periods. This test can be used as a check on the validity of the restriction that a particular covariate does not affect the path of untreated potential outcomes (given that is included in the model). Another possibility is to use a proxy for unobserved skill. In our application, we observe each individual’s score on the Armed Forces Qualification Test (AFQT). This variable can be seen as a proxy for unobserved skill, and it seems plausible that earnings in the absence of job displacement do not depend at all (notice that this is a stronger condition than our approach actually requires) on AFQT score once “skill” is in the model.

We state a general identification result for the next. Define

In other words, is the difference between outcomes in particular post-treatment periods relative to the outcome two periods before the treatment started. is a vector where which is the total number of post-treatment time periods. Next, define

where is the identity matrix so that is a matrix, and define

which is a matrix. Finally, define the vector of parameters

which is a vector.

Then, the vector of moment conditions coming from Equation 7 is equivalent to

| (9) |

We make the following assumption.

Assumption 7 (Relevance).

The matrix has full rank.

Assumption 7 corresponds to the relevance condition discussed above that the covariates whose effects do not change over time are correlated with (or equivalently with ) after controlling for other covariates .

Next, we state our main identification result.

Theorem 1.

Proof.

For identifying for , the result holds immediately from Equation 9 under the conditions in the theorem. The result for holds because

where the second equality holds by adding and subtracting , and the third equality holds by Sections 2.1 and 8 (and using that the coefficients on do not vary over time) and by rewriting potential outcomes in terms of their observed counterparts. Then, the result holds because and are identified. ∎

In the expression for in Theorem 1, the first term is the mean path of outcomes that individuals in the treated group experienced between period and . The second term is the mean path of outcomes that individuals in the treated group would have experienced if they had not participated in the treatment and comes from the interactive fixed effects model for untreated potential outcomes in Assumption 1.

Remark 2.

We discuss two alternative approaches to identification in LABEL:app:alternative-approaches in the Supplementary Appendix. The first idea is to assume that the time varying unobservables, , in the model in Assumption 1 are uncorrelated over time; this sort of idea is common especially in the literature on factor models. A recent paper that uses this sort of idea is [41]. Second, we consider the case with time varying covariates and using covariates in other periods as instruments. Relative to our main approach, the main advantage of both of these approaches is that they do not require finding a covariate whose effect does not change over time. On the other hand, they introduce additional complications and additional assumptions that often make these approaches less appealing in applications. See LABEL:app:alternative-approaches in the Supplementary Appendix for an expanded discussion of these issues.

Remark 3.

The above arguments apply for identifying for (i.e., post-treatment time periods). In many applications, it may be useful to identify/estimate pseudo-ATTs in pre-treatment periods with the idea of pre-testing (i.e., testing that treatment effects are equal to 0 in pre-treatment periods). In particular, define which allows the “base period” (the period that outcomes are differenced with respect to) to vary based on whether or not is post-treatment or pre-treatment. In post-treatment periods is equal to so that the base period is the same as has been used so far throughout this section. In pre-treatment periods, is equal to so that the base period is the period two periods before the current period. Next, define . Similarly, define , be the block diagonal matrix with elements along the diagonal given by , and . Then under analogous exogeneity and relevance conditions as above and using essentially the same arguments, one can show that, for some positive definite weighting matrix , . Given this expression, which is identified for . For , one can pre-test the interactive fixed effects model for untreated potential outcomes by testing that .

Example 1.

Under the same conditions as above, consider the case with exactly three time periods, where is a binary variable, and there are no other covariates in the model for untreated potential outcomes.

Straightforward calculations show that

and

which implies that

For , notice that the difference in the numerator effectively differences out the time fixed effects (these are common across different values of ). And, in particular, . Thus, any differences in the numerator are due to and differences in the distribution of among untreated individuals with relative to untreated individuals with . The same sort of argument implies that the denominator is equal to . Thus, dividing the numerator by the denominator cancels the term involving and is equal to . However, notice that this strategy would not be available without exploiting the time invariance of the effect of the covariate . Once has been identified, it is straightforward to recover and .

3 Consequences of Ignoring Interactive Fixed Effects

Difference in Differences

The most common approach to identifying the effect of participating in a binary treatment when a researcher has access to repeated observations over time is difference in differences. Difference in differences is very closely related to two-way fixed effects models for untreated potential outcomes; i.e.,

| (10) |

Notice that the model in Equation 10 is a special case of the model in Assumption 1 — when the effect of does not vary over time, it can be absorbed into the individual fixed effect. Under the condition that for all (which is a standard condition and one that holds under our conditions for interactive fixed effects models), it follows that

| (11) |

for all time periods . The condition in Equation 11 is called the parallel trends assumption. It says that the path of outcomes that individuals in the treated group would have experienced if they had not participated in the treatment is the same as the path of outcomes that individuals in the untreated group actually experienced. It also immediately follows that888In this section, we focus on the in period , but similar arguments would also apply in other time periods.

| (12) |

However, if the model in Assumption 1 is correct instead of the model in Equation 10, the condition in Equation 11 no longer holds. In particular,

and, therefore, the condition in Equation 11 does not, in general, hold. This follows because, although is common across the treated and untreated groups, varies across groups. And the second term will differ across groups unless either (in this case, the interactive fixed effects term can effectively be absorbed into the time fixed effect) or if (in this case, the interactive fixed effect can be absorbed into the individual fixed effect). But these are both cases where the interactive fixed effect model reduces to the model in Equation 10.

Moreover, we can develop an expression for the bias that results from using a difference in differences approach when the actual model for untreated potential outcomes is the interactive fixed effects model. Let denote the expression on the right hand side of Equation 12 but allowing for the possibility that the parallel trends assumption does not hold (so that, in this case, may not be equal to ). In this case,

where the first equality holds from the definition of , the second equality plugs in potential outcomes for their observed counterparts and adds and subtracts , and the third equality holds by plugging in the interactive fixed effects model for untreated potential outcomes. Thus, in general, wrongly imposing the parallel trends assumption instead of the interactive fixed effects model for untreated potential outcomes will lead to estimators that do not converge to the true . This bias is likely to be particularly severe in cases where is much different from (i.e., the effect of is changing substantially over time) as well as when is much different from (i.e., the mean of is much different between the treated and untreated groups).

Models with individual-specific linear trends

In applied work, it is very common that, when researchers suspect that the parallel trends assumption mentioned above is violated, to estimate a linear trends model. These sorts of models (as well as more general versions) are considered in, for example, [32, 65, 52]. This sort of approach is motivated by the following model for untreated potential outcomes (as in the previous section, continue to consider the case without covariates)

| (13) |

The model in Equation 13 is a special case of the model in Assumption 1 when is equal to . Let generically represent some variable that depends on time, and define the operator . Then, the model in Equation 13 implies the following

| (14) |

for all time periods . This further implies, after some straightforward calculations, that

| (15) |

There are a couple of potential issues with the linear trends model. First, conceptually, the reason to use this sort of model is the same as the interactive fixed effects model in Assumption 1 — particularly, there is some time invariant variable (i) that is unobserved and (ii) whose effect varies over time. There are some notable drawbacks to this sort of model though. In particular, if the researcher observed , under conditions (i) and (ii) mentioned above, it would be most natural to condition on it in the model and allow for its effect to vary over time. This is exactly how the interactive fixed effects model treats this situation. On the other hand, the linear trends model allows for the effect of to change over time, but only in a very restrictive way. In particular, if were observed, it would be very unusual to impose a linear trend sort of specification and attach it to an observed covariate.

It is also helpful to consider the resulting bias in from incorrectly imposing the linear trends model. When the model in Assumption 1 is correct rather than Equation 13, the condition in Equation 14 will not hold in general. In particular, under the interactive fixed effects model

Thus, it is immediately clear that the condition in Equation 14 does not hold except in special cases; is common across groups but the second term, in general, varies across the treated and untreated group. As mentioned above, linear trends is a special case of the interactive fixed effects model that we consider — the interactive fixed effects model and the linear trends model coincide when . In this case, the second term is equal to 0 and therefore the condition in Equation 14 holds. The other case where Equation 14 holds is when , but, if the mean of is the same across groups, there is no reason to use a linear trends model or interactive fixed effects model — the term involving will be absorbed into the time fixed effect.

Using similar arguments, we can also quantify the bias from incorrectly imposing a linear trends model when the interactive fixed effects model is correct. Let denote the expression on the right hand side of Equation 15 but allowing for the possibility that the linear trends model in Equation 13 is not correctly specified (as for the DID case above, this allows for the possibility that is not equal to the ). Then,

where the first equality plugs in the definition of , the second equality plugs in potential outcomes for observed outcomes and adds and subtracts , the third equality cancels the terms involving , and the fourth equality plugs in the interactive fixed effects model for untreated potential outcomes. This expression demonstrates that there can be large biases from using a linear trends model instead of interactive fixed effects model in two cases: (i) when is much different from , or (ii) when is much different from .

4 Estimation and Inference

In this section, we propose a two step procedure for estimating . In the first step, we estimate all the parameters as well as , , , and . Then, we plug these into the expression for in Theorem 1. In the second part of this section, we derive the asymptotic distribution of our estimator of and propose an approach to conduct inference based on the multiplier bootstrap.

As a first step, it is helpful to re-write the expression for in Theorem 1 as

| (16) |

which just converts the conditional moments in Theorem 1 into equivalent unconditional moments. This expression suggests the following estimator for

| (17) |

Next, we provide the limiting distribution for our estimators of . Before doing that, we define some additional notation. First, define . Next, define where denotes an matrix of zeros, and so that for any , and define . Next, define

where is a scalar, is a -dimensional vector, and is a -dimensional vector. Further, define

Finally, define , , , and .

We make the following assumption

Assumption 8.

, , is positive definite, and which is positive definite.

Assumption 8 is a standard condition for establishing the limiting distribution of GMM estimators.

The next result provides an asymptotically linear representation for our estimator of and the joint limiting distribution of for .

The proof of Theorem 2 is provided in LABEL:app:additional-proofs in the Supplementary Appendix. Given the result in Theorem 2, one can immediately proceed to conduct inference by estimating . Instead of doing this, we conduct inference using a multiplier bootstrap procedure (see, for example, [48]) that involves perturbing the influence function. In particular, for some iid that has mean zero, variance one, and finite third moment and that is drawn independently of the data (common examples include drawing from a standard normal distribution, or setting to be equal to or each with probability ), we construct a bootstrap estimate by

where is the estimated version of that replaces population parameters with their estimates. Standard arguments show that, conditional on the original data, follows the same limiting distribution as in Theorem 2. Thus, for one can construct standard errors for by where and where is the -th sample quantile of (across bootstrap iterations) and is the -th quantile of the standard normal distribution. Relative to the nonparametric bootstrap, the multiplier bootstrap offers a number of practical advantages: (i) because it does not involve re-estimating the model at each bootstrap iteration, it is generally much faster; (ii) because it involves weights, it avoids cases where, in some bootstrap iterations, the nonparametric bootstrap may not be able to compute a bootstrap estimate.

Remark 4.

In cases where a researcher would like to “pre-test” the identifying assumptions (see discussion in Remark 3 for more details), similar arguments to the ones in Theorem 2 can be used to establish the joint limiting distribution of in pre-treatment periods (or across all pre- and post-treatment periods) which immediately leads to tests of for all .

Remark 5.

Although our main results consider the case with iid observations, it would also be straightforward to extend the result to account for clustering across individuals, allowing, for example, spatial correlations as long as the number of clusters is “large.” In that case, the asymptotic arguments would proceed with the number of clusters, rather than the number of individuals, going to infinity. It is likely that various bootstrap procedures could be adapted to this case as well (see, for example, [19]).

5 Extensions

This section expands our identification arguments from the previous section to allow for (i) multiple interactive fixed effects (and, relatedly, provides an approach for selecting the number of interactive fixed effects), (ii) repeated cross sections data, (iii) testing that particular covariates have time invariant effects when additional pre-treatment time periods are available, and (iv) variation in treatment timing across individuals.

5.1 Multiple Interactive Fixed Effects

The previous results dealt with the case with a single interactive fixed effect. This section generalizes those arguments to cases where there may be more interactive fixed effects.

Consider the case where there are interactive fixed effects so that

| (18) |

where and are each vectors, is a vector, and is a vector.

Next, for any time period , notice that

| (19) |

Next, define , , and . Further, define which is an dimensional vector of differences between all pre-treatment outcomes relative to the “base period” . Similarly, define (which is an matrix), (which is an matrix), and . We make the following assumption

Assumption 9 (Factor Rank).

has full rank.

This is the analogous condition to Assumption 4 in the case with a single interactive fixed effect.

Next, notice that we can write

which, under Assumption 9, implies that

| (20) |

Plugging this expression for into Equation 19, notice that, for any ,

| (21) |

where , , and .

This expression in Equation 21 is the natural generalization of Section 2.1 to the case with multiple interactive fixed effects. As in the earlier case, to recover , we do not need to recover entire vectors of parameters such as or , but rather we need only recover and . As before, the main complication is that, by construction, all the terms in are endogenous. Thus, a necessary condition for identifying in this case is that (the dimension of the time invariant covariates whose effects do not change over time) is greater than or equal to . In other words, to accommodate more interactive fixed effects, the researcher needs to be able to find more time invariant covariates whose effects do not change over time. Additionally, the arguments above for differencing out the interactive fixed effects rely on which involves untreated potential outcomes in all time periods from to — thus, including interactive fixed effects requires having access to at least pre-treatment time periods (as well as at least total time periods). Define , which is a matrix, and define which is a vector. We state the following result that generalizes Theorem 1 to the case with multiple interactive fixed effects.

Proposition 1.

In the model in Equation 18, and under Assumptions 2, 5, 6 and 9, and under the additional conditions that (i) and , (ii) , and (iii) has full rank, then and are identified for all . In particular, for any positive definite weighting matrix ,

In addition, is identified for all , and it is given by

The proof of Proposition 1 is provided in LABEL:app:additional-proofs in the Supplementary Appendix and follows from arguments that are similar to the ones in Theorem 1.

Selecting the Number of Interactive Fixed Effects

So far, we have considered the case where the researcher knows the number of interactive fixed effects. This may not always be the case though, and it is common in the interactive fixed effects literature to choose the number of interactive fixed effects in a data driven way. Suppose that the researcher chooses among interactive fixed effects and that so that there are enough covariates whose effects do not change over time to identify the parameters of the model for untreated potential outcomes. Building on existing work, we suggest three approaches to choosing the number of interactive fixed effects. First, we consider choosing the number of interactive fixed effects according to which one minimizes the Bayesian Information Criteria, where where and where is the vector of residuals from estimating the interactive fixed effects model for untreated potential outcomes in Equation 21 in post-treatment time periods.999The expression for BIC only uses post-treatment periods, but when there are “extra” pre-treatment time periods, it is straightforward to include those periods. Related approaches are proposed in [21, 10, 3, 56, 44].

Second, we consider leave-one-out cross validation using untreated observations. In particular, in a particular post-treatment period , for a particular individual in the untreated group, we estimate where the notation indicates the estimates of and that use all observations except observation . Then, we compute where denotes the set of untreated observations. And we choose that minimizes . A similar approach is proposed in [51].

Finally, we consider a cross-validation procedure based on choosing the number of interactive fixed effects using pre-treatment observed outcomes for the treated group. This is conceptually similar to the approach considered in [66]. In particular, for some time period (these are the common pre-treatment periods where pseudo-treatment effect parameters can be estimated), compute where denotes the set of treated observations. Then, we choose that minimizes .

5.2 Repeated Cross Sections

It is straightforward to extend our main identification arguments to the case when the researcher has access to repeated cross sections data rather than panel data. We appear to be the first paper to consider interactive fixed effects models with repeated cross sections data. That our approach can be extended to this case is in parallel with the literature on difference in differences which can often be implemented with repeated cross sections data. In our case, these arguments work because of (i) our differencing argument combined with the linearity of expectations and (ii) our focus on time invariant covariates. In our view, having results available for the case with repeated cross sections data is useful because repeated cross sections are often available, typically have larger sample sizes, and have fewer issues with attrition. These types of considerations are particularly important in policy evaluation applications which often exploit variation in local policies where typical panel datasets can frequently be too small to be able to be used once a researcher focuses on particular local policies. In this section, we let denote the time period when individual is observed. With repeated cross sections data, we replace Assumption 2 with the following assumption,

Assumption RC (Repeated Cross Sections Sampling).

Conditional on , the data are iid from the distribution of for all , and the joint distribution of is independent of .

Assumption RC implies that we observe draws from a distribution which may not correspond to the population distribution of outcomes, covariates, and treatments. That is, within each period, we observe iid draws from some underlying population, but we only observe outcomes for individuals in the particular period when they are observed in the sample and the sample sizes can vary across different periods. In particular, we observe draws from the mixture distribution

where . The second part of Assumption RC rules out compositional changes in outcomes, covariates, and treatment status across time periods (see [37] for a more extended discussion of compositional changes though we note here that this type of condition is common in the literature on DID with repeated cross-sections; e.g., [1, 60]). Let expectations with respect to the mixture distribution be denoted by (and population expectations continue to be denoted by ).

Notice that all the moment conditions in Equation 7 continue to hold, but, under Assumption RC, we do not have direct sample analogues of these moment conditions. First, for , let . Then, notice that for expectations of variables in a particular time period such as , under Assumption RC we can write ; and for expectations of variables that are time invariant such as , under Assumption RC, we can write . Then, exploiting the linearity of expectations, we can re-write Equation 7 in terms of expectations from the mixture distribution as

| (22) |

Given the modified moment conditions above, identification of follows from essentially the same arguments as for the case with panel data. We briefly state these arguments here for completeness. Next, let

which is a vector. The instrument matrix is exactly the same as in the case with panel data. Next, define

which is a matrix. Finally, we state an identification result for when repeated cross sections data is available.

Proposition 2.

The proof of Proposition 2 is provided in LABEL:app:additional-proofs in the Supplementary Appendix and follows using essentially the same arguments as in the proof of Theorem 1.

5.3 Testing for Covariates Having Time Invariant Effects

Our identification arguments rely heavily on finding a covariate whose effect on untreated potential outcomes does not vary over time. In many applications, it may be unclear whether a particular covariate has a time invariant effect on untreated potential outcomes or not. For example, in our application on job displacement, it seems likely that the covariate AFQT score (which is a proxy for individual skill/ability) does not have a time varying effect on outcomes after accounting for unobserved heterogeneity. But it is less clear if the other covariates, which are education and demographic characteristics, have time invariant effects. Even for AFQT, it would be nice to have quantitative evidence that it does not have time varying effects on untreated potential outcomes.

One idea here is a traditional over-identification test; i.e., when (the dimension of the covariates with time invariant effects) is greater than (the number of interactive fixed effects), one can jointly test the restrictions that the corresponding parameters do not vary over time. This is straightforward to do and is a byproduct of the first-stage estimation.

Unfortunately, this strategy is not available in the leading case where (that is, there is one interactive fixed effect and one covariate whose effect does not change over time) because the model for untreated potential outcomes is exactly identified in this case. A useful alternative approach is available in this case when an extra pre-treatment period is available in the data (i.e., when ). In that case, notice that the following additional moment conditions are available in periods ,

This is a vector of moment conditions and thus satisfies the necessary order condition in pre-treatment periods. The next proposition shows that and are identified for without requiring having access to a covariate whose effect does not vary over time.

Proposition 3.

For , under Assumptions 1, 2, 5, and under the additional conditions that and , that , and that is positive definite, then

where, along the lines of Remark 3, in pre-treatment periods we define and (i.e., here, parameters indexed by and take the place of parameters indexed by and as was the case in post-treatment time periods).

The proof of Proposition 3 is provided in LABEL:app:additional-proofs in the Supplementary Appendix. The key difference of Proposition 3 relative to Theorem 1 is that this result does not require Assumption 6 — that the effect of a particular covariate does not vary over time. Further, note that the entire vector of parameters is identified in Proposition 3 in pre-treatment periods. Moreover, given the definition of , an implication of a particular covariate having time invariant effects is that for all . This implies that one can therefore test for time invariant effects of a particular covariate in pre-treatment periods by estimating the model for untreated potential outcomes in pre-treatment periods using the result in Proposition 3 and then simply testing whether for all . Note that this is not a direct test that does not vary over time in post-treatment time periods, but it is similar to pre-tests that are extremely common in the DID literature. We also stress that it is likely not appropriate to choose which covariates to use as those that have time invariant effects based on this kind of pre-test (see [58] for related discussion on pre-testing in the context of difference in differences).

5.4 Staggered Treatment Adoption

Next, we consider the case where treatment timing can potentially vary across different individuals. We also address the issue of treatment anticipation in this section. These issues have been the subject of a number of recent papers in the difference in differences literature (e.g., [22, 30, 18]). Throughout this section, we make the following assumption.

Assumption 10 (Staggered Treatment Adoption).

For all , .

Assumption 10 says that once an individual becomes treated, they remain treated. This is a very common setup in applied work and common assumption in the econometrics literature. It would apply when a particular location implements a policy and the policy remains in place; it also applies in applications where treatments are “scarring” in the sense that when an individual becomes treated, the researcher considers them to be treated in future periods as well even if they do not repeatedly participate in the treatment. This is the case in our application on job displacement.

In this section, we slightly modify the notation used in the previous sections. Because treatment timing can vary across individuals, we define an individual’s “group” by the time period when they become treated; that is, for each individual, we define as the time period when an individual becomes treated, and (arbitrarily) we set for individuals that are not treated in any time period. Under Assumption 10, knowing an individual’s treatment timing implies that we know their entire path of participating in the treatment. We continue to define an individual’s untreated potential outcome by — this is the outcome an individual would experience if they did not participate in the treatment in any time period. But now we index treated potential outcomes by ; that is, is the outcome that an individual would experience in time period if they became treated in period . In all time periods, we observe which is the potential outcome corresponding to the actual time period when individual became treated. We make the following assumption.

Assumption 11 (Anticipation).

There exists a , such that, for all .

Assumption 11 allows for individuals to anticipate participating in the treatment and therefore have their outcomes affected before the treatment actually takes place. However, it says that, if we move back in time by enough periods, then the treatment does not have effects in those periods. Let denote the set of groups that ever participate in the treatment (and where the notation indicates that we continue to consider the case where there are at least two pre-treatment time periods available for all individuals). In the presence of anticipation, it is also useful to define the subset of groups that are treated late enough so that at least two periods of outcomes that are not affected by the treatment (either directly or through anticipation) are available. In particular, let ;101010In some applications it may also be desirable to limit to groups that are treated early enough (as well as early enough time periods) so that no anticipation effects could be occurring among the comparison group. For simplicity (as well as following standard approaches in most applications), we ignore this possibility here. we focus on identifying treatment effect parameters for this set of groups.

Following existing work on identifying treatment effect parameters under staggered treatment adoption ([18, 17]), we target identifying group-time average treatment effects

which is the average effect of participating in the treatment among group at time period . Similar to the arguments above, it is straightforward to show that, in periods (i.e., post-treatment periods),

| (23) |

where we define , . This suggests that, as earlier, identifying comes down to identifying the parameters and . We next provide a proposition showing that and are identified in post-treatment time periods in a staggered treatment setup with possible anticipation effects. Before we do that, we define (which is a vector that picks up covariates among individuals that (i) are not treated in the current period and are far enough away from participating in the treatment that they are not experiencing anticipation effects, or (ii) that never participate in the treatment), (which is a row vector with elements), and .

Proposition 4.

For any and time periods such that (i.e., post-treatment time periods for group ), and under Assumptions 1, 2, 5, 6, 10 and 11 and under the additional conditions that, (i) , (ii) , and (iii) that the matrix has full rank, and for any positive definite weighting matrix ,

Moreover, for all and time periods such that , is identified and is equal to

The proof of Proposition 4 is provided in LABEL:app:additional-proofs in the Supplementary Appendix. Given identification of , in many applications it is common to aggregate these into lower-dimensional parameters of interests. One popular option is

where which is the average effect of participating in the treatment for group across its post-treatment time periods. Another popular option is

so that corresponds to the average treatment effect across all individuals that ever participate in the treatment (averaged across all their post-treatment time periods), and provides the average effect of participating in the treatment by length of exposure to the treatment (ES stands for event study). See [18] for more aggregations of group-time average treatment effects that could be of interest in particular applications.

Remark 6.

This section has considered the setup with staggered treatment adoption. This framework is common in the literature, but it is possible to allow for more general treatment regimes (for example, allowing for individuals to move into and out of treatment) by defining groups by their entire path of participating or not participating in the treatment. In most cases, the main data requirement for identifying an -type parameter with complicated treatment regimes is access to a group of individuals who have not been affected by the treatment up to period . That being said, more general treatment regimes may run into practical problems (essentially a curse of dimensionality) in applications with a moderate number of observations as the number of observations per treatment path may become small. See [23] on difference-in-differences with general treatment regimes. It would seem possible to adapt those sorts of arguments to our framework.

6 Monte Carlo Simulations

In this section, we provide Monte Carlo simulations illustrating the finite sample properties of our estimation and inference procedure. In particular, we compare the performance of our approach to difference in differences and linear trends models. In the Supplementary Appendix, we provide additional Monte Carlo simulations related to (i) weak instruments, (ii) including multiple interactive fixed effects, and (iii) procedures to select the number of interactive fixed effects to include in the model for untreated potential outcomes.

We consider models of the form

We consider the case where (i) there are five time periods, (ii) no individual is treated until the fifth time period and there is no effect of participating in the treatment, (iii) , (iv) , (v) (i.e., is normally distributed with mean and variance 0.1), (vi) , (vii) we set where so that the mean of the interactive fixed effect varies across groups and governs how strong of an instrument is for (for now, we set ), (viii) , for all time periods, and (ix) for and we vary among across designs. When , DID is correctly specified but linear trends is not correctly specified; when , linear trends is correctly specified but DID is not; setting implies that neither parallel trends nor linear trends holds as the trend is in between these two cases; when , the assumptions underlying DID and linear trends are both severely violated. Finally, we vary among 100, 500, and 1000.

| Bias | RMSE | MAD | Rej. Prob. | |||||||||

| IFE | DID | LT | IFE | DID | LT | IFE | DID | LT | IFE | DID | LT | |

| -0.008 | 0.001 | -2.001 | 0.161 | 0.088 | 2.018 | 0.111 | 0.057 | 1.999 | 0.058 | 0.051 | 1.000 | |

| 0.000 | 0.002 | -1.998 | 0.074 | 0.039 | 2.002 | 0.049 | 0.026 | 1.997 | 0.070 | 0.043 | 1.000 | |

| -0.003 | -0.001 | -2.001 | 0.048 | 0.028 | 2.003 | 0.034 | 0.019 | 2.000 | 0.054 | 0.044 | 1.000 | |

| -0.006 | 2.008 | 0.006 | 0.290 | 2.022 | 0.159 | 0.172 | 1.999 | 0.101 | 0.073 | 1.000 | 0.062 | |

| 0.003 | 2.004 | 0.000 | 0.125 | 2.007 | 0.071 | 0.087 | 2.004 | 0.047 | 0.058 | 1.000 | 0.062 | |

| -0.003 | 2.002 | -0.001 | 0.083 | 2.003 | 0.050 | 0.059 | 2.002 | 0.034 | 0.043 | 1.000 | 0.052 | |

| -0.008 | 0.996 | -1.007 | 0.208 | 1.005 | 1.024 | 0.133 | 0.994 | 1.006 | 0.050 | 1.000 | 1.000 | |

| 0.003 | 1.000 | -0.993 | 0.095 | 1.002 | 0.997 | 0.062 | 1.003 | 0.995 | 0.066 | 1.000 | 1.000 | |

| 0.000 | 1.002 | -0.997 | 0.066 | 1.003 | 0.999 | 0.045 | 1.002 | 0.997 | 0.055 | 1.000 | 1.000 | |

| -0.037 | 7.966 | 5.972 | 0.757 | 8.011 | 6.008 | 0.507 | 7.960 | 5.972 | 0.064 | 1.000 | 1.000 | |

| -0.008 | 7.999 | 5.998 | 0.334 | 8.008 | 6.005 | 0.227 | 8.003 | 5.995 | 0.053 | 1.000 | 1.000 | |

| 0.008 | 7.986 | 5.990 | 0.226 | 7.990 | 5.994 | 0.156 | 7.985 | 5.996 | 0.053 | 1.000 | 1.000 | |

Notes: The columns labeled “IFE” use the interactive fixed effect approach introduced in the paper; the columns labeled “DID” provide results using a difference in differences approach; the columns labeled “LT” provide results using a linear trends approach. Columns labeled “Bias” simulate the bias of each approach, “RMSE” simulates the root mean squared error, and “MAD” for the median absolute deviation. Columns labeled “Rej. Prob.” contain the rejection probabilities for a test of the null hypothesis that (which is true here) at the 5% significance level. The rows vary and as discussed in the text. Results come from 1000 Monte Carlo simulations.

The results from the first set of simulations are provide in Table 1. These results are broadly in line with our earlier discussions. IFE generally performs well across each different value of , and all estimators tend to perform somewhat better with larger sample sizes. In the case where DID is correctly specified (i.e., when ), the DID estimator performs somewhat better in terms of root mean squared error and median absolute deviation than IFE though, as expected, linear trends does not perform well in this case. Similarly, in the case where linear trends is correctly specified (i.e., when ), linear trends performs somewhat better in terms of root mean squared error and median absolute deviation than IFE though both do substantially better than DID. In the intermediate case where , IFE substantially outperforms both DID and linear trends for all sample sizes. The last case that we consider is when , so that DID and linear trends are substantially misspecified. In this case, IFE continues to perform well while DID and linear trends perform poorly.

The inference procedure for IFE also works well across simulation setups. Across all sample sizes and values of , our IFE approach rejects the null of (which is true) at close to its nominal level. For DID and linear trends, inference works well in cases where they are correctly specified, but (as expected) there are severe distortions (particularly, over-rejecting) when they are not correctly specified.

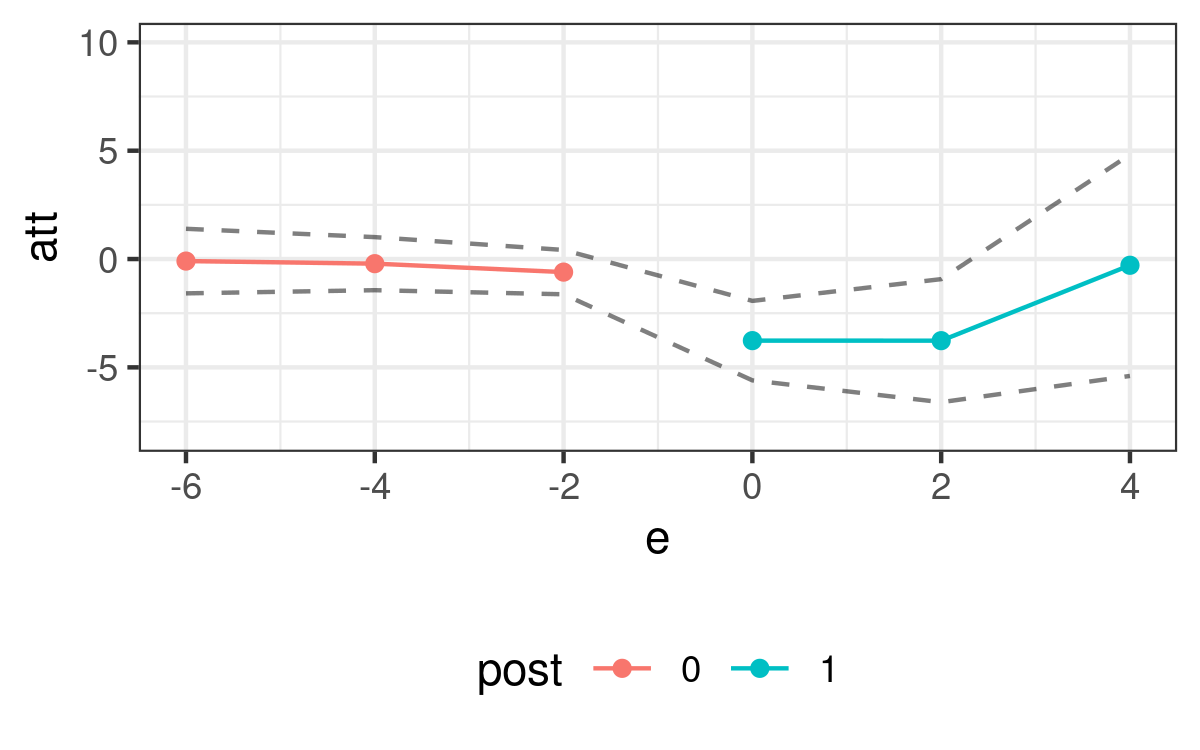

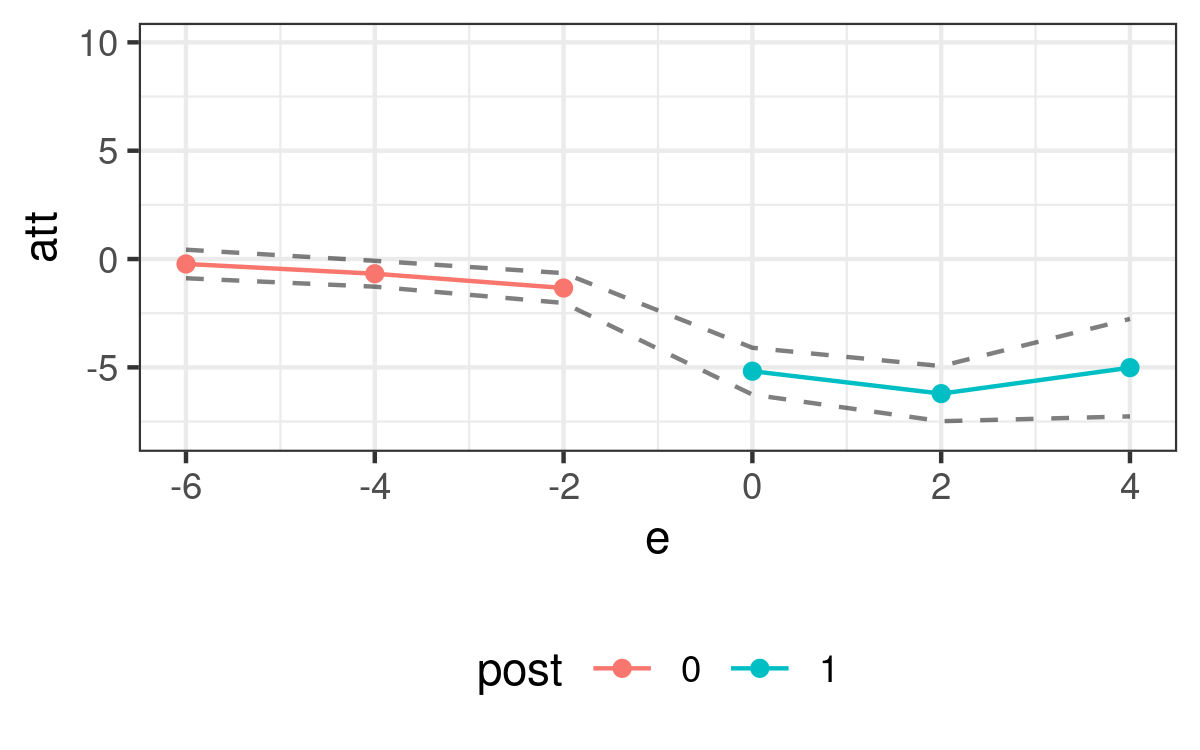

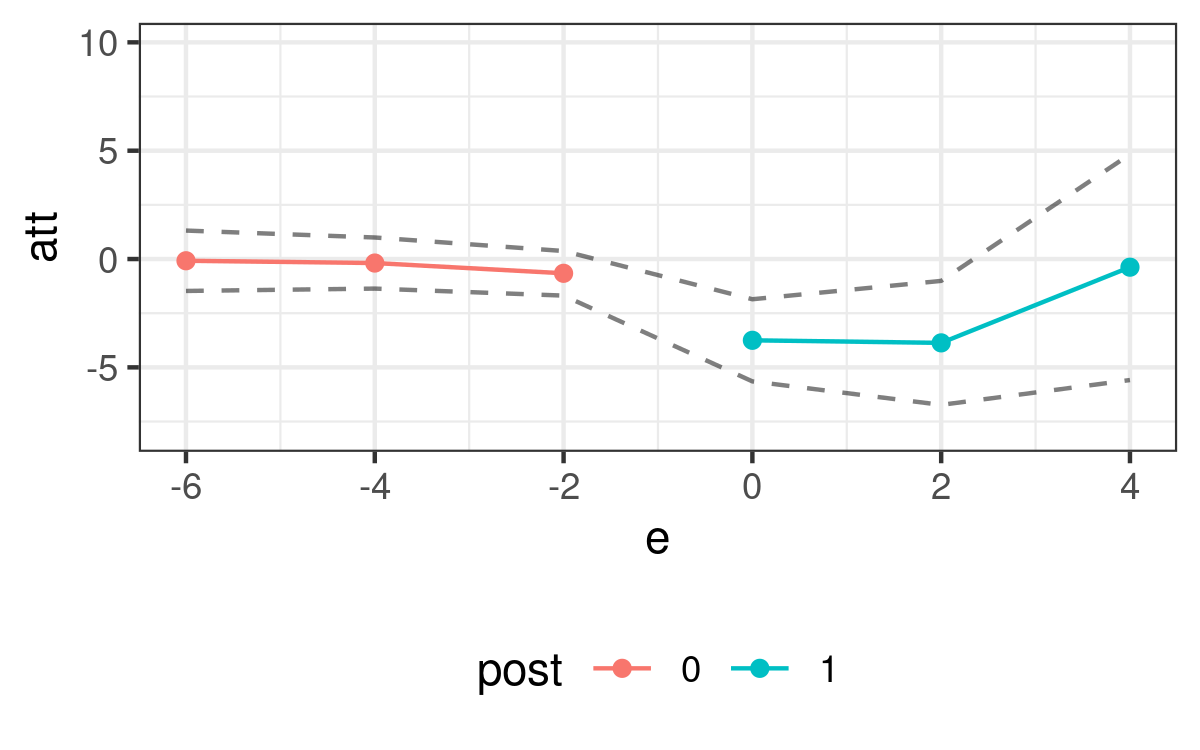

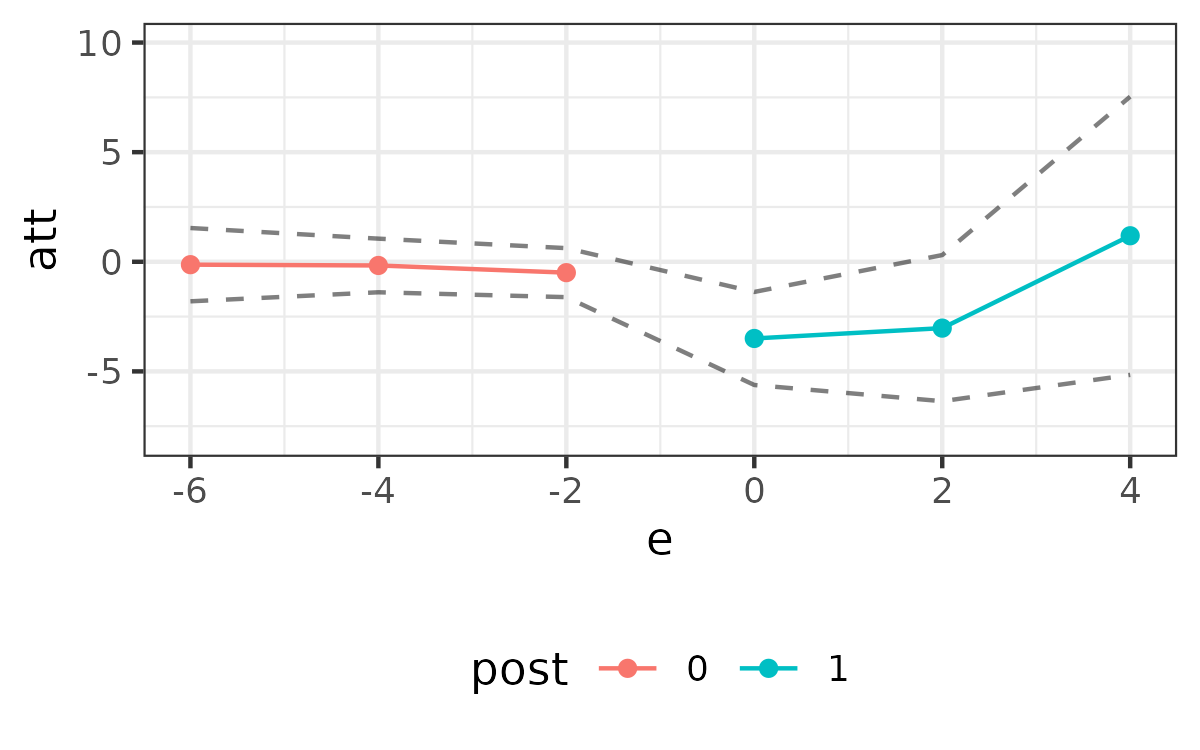

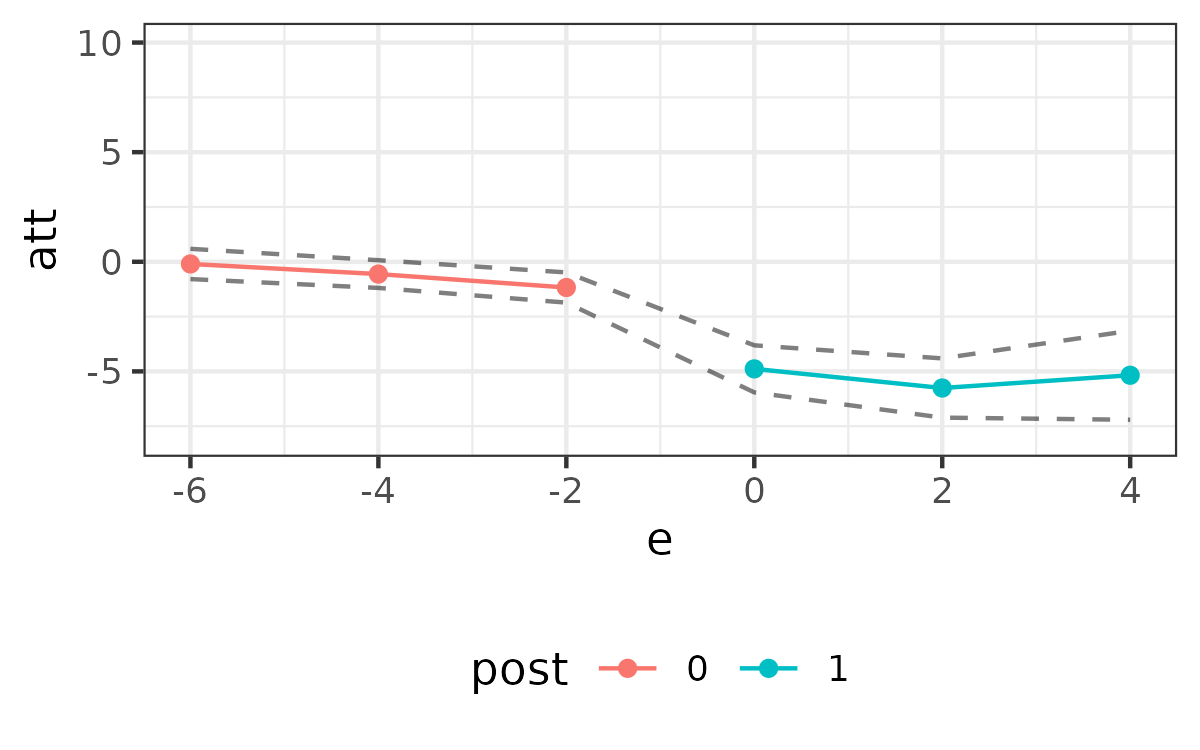

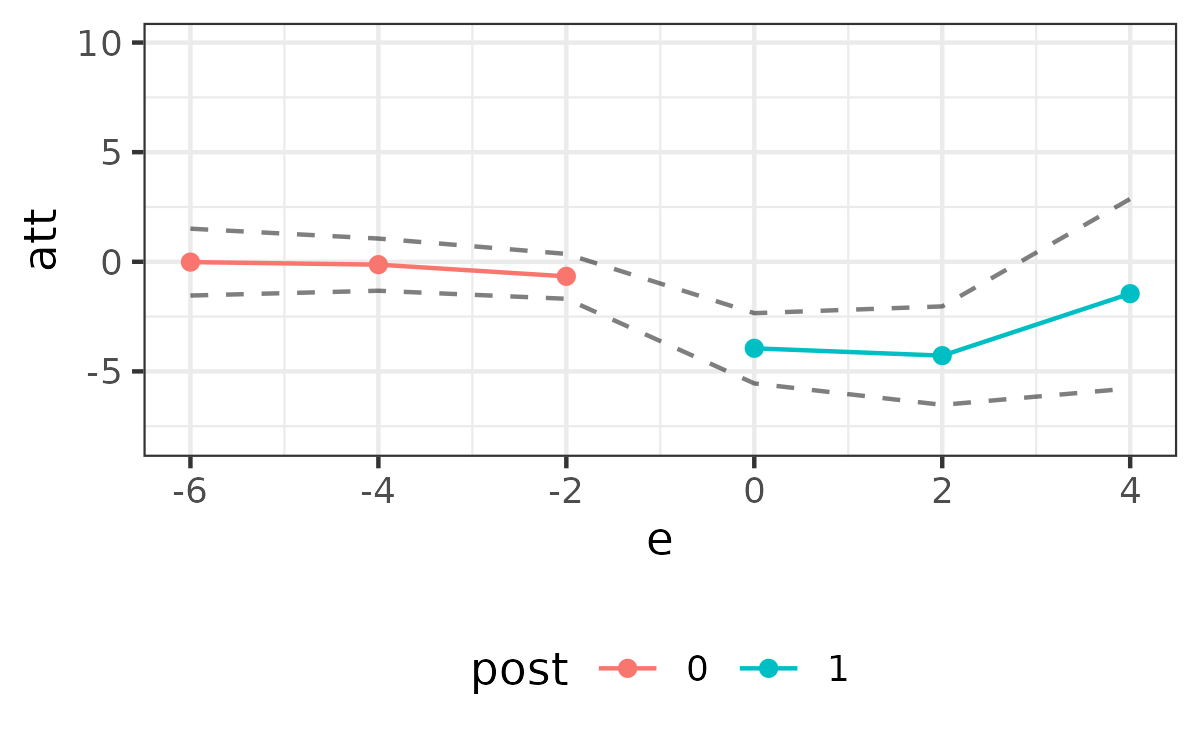

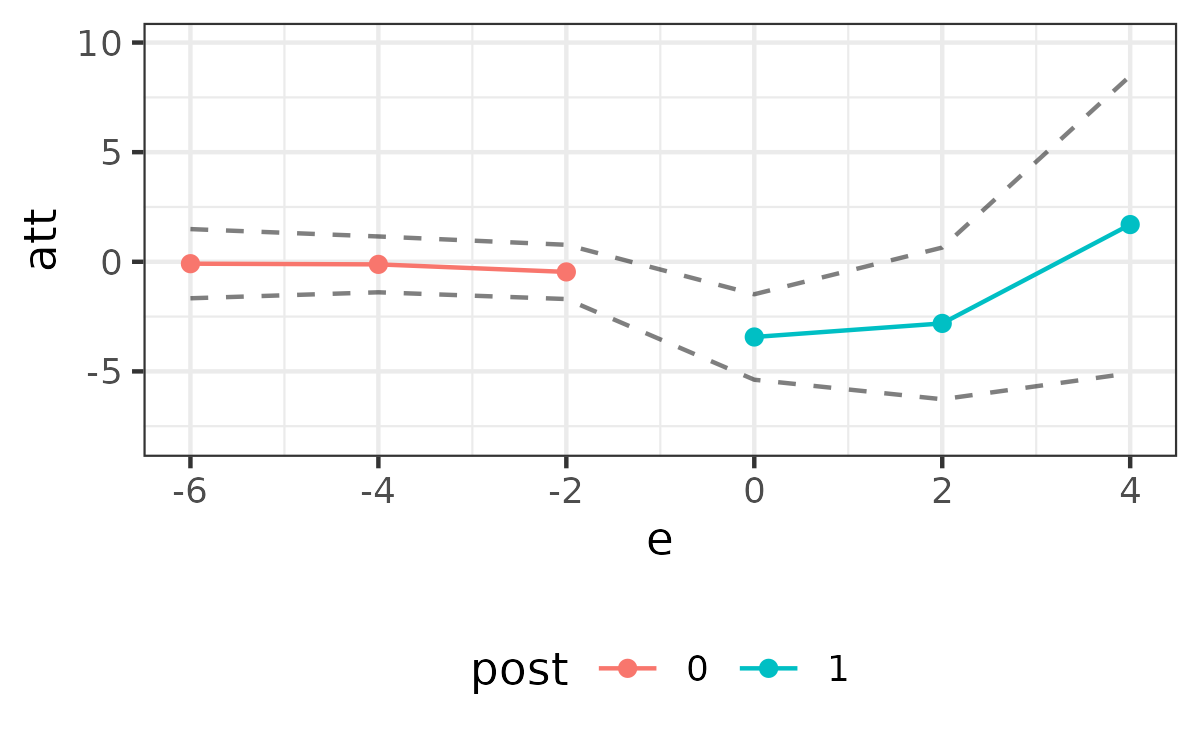

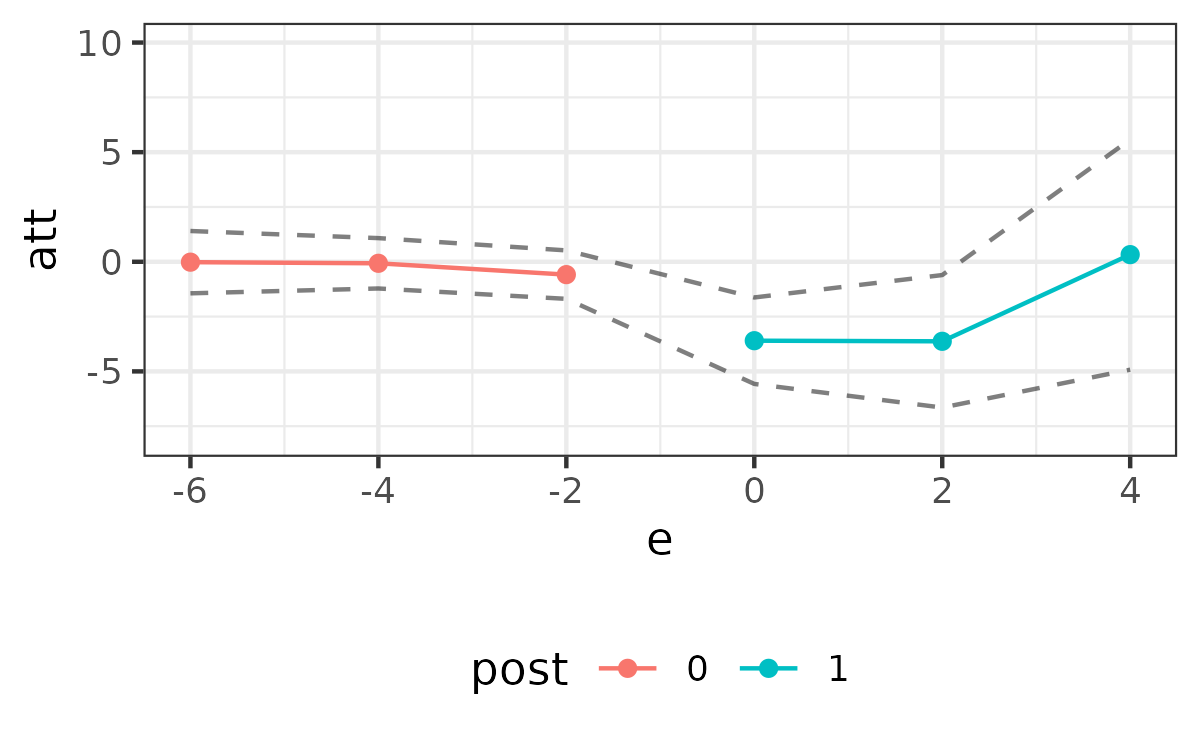

7 Application

In this section, we consider an application on the effect of early-career job displacement on earnings. Much of the literature on job displacement has been interested in the dynamics of the effects of job displacement (see, for example, [43] as well as many subsequent papers). Difference in differences has been a standard approach in this literature with the idea being that displaced workers may differ from non-displaced workers along dimensions, for example latent “skill”, that are unobserved by the researcher.

One potential issue with this approach is that the return to latent skill could vary over time (e.g., with the business cycle) as well as vary with experience. If skill were observed, it would be natural to include it in the model for untreated (non-displaced) potential outcomes while allowing its coefficient to vary over time. Although standard difference in differences approaches cannot handle this sort of issue, this setup mirrors the approach discussed in the current paper exactly. In addition, like the difference in differences approach, our setup allows for other unobserved, time invariant variables to affect an individual’s earnings in the absence of displacement and be distributed differently across displaced and non-displaced workers as long as their effect is time invariant as well.

7.1 Data and Setup

[caption=Summary Statistics, label=tab:ss, pos=t,]lD..-1D..-1D..-1D..-1\tnote[]Notes: The column “Displaced” aggregates summary statistics for workers that were displaced from their jobs between 1989 and 1993. Reported earnings are yearly and reported in thousands of dollars. The column “Diff” reports the difference between displaced and non-displaced workers. The column “p-val on diff” reports the p-value of a test for the equality of each variable for displaced and non-displaced workers.

Sources: 1979 National Longitudinal Study of Youth\FL Displaced Non-Displaced Diff p-val on diff \MLPath of Earnings\NN Earnings 1983 8.29 9.21 -0.910.02\NN Earnings 198511.6713.08 -1.400.00\NN Earnings 198714.8216.69 -1.880.00\NN Earnings 198916.5920.37 -3.780.00\NN Earnings 199117.1423.28 -6.140.00\NN Earnings 199318.4225.60 -7.190.00\MLCovariates\NN Less HS 0.13 0.07 0.060.00\NN HS 0.64 0.59 0.050.04\NN College 0.23 0.34 -0.110.00\NN Hispanic 0.23 0.16 0.070.00\NN Black 0.32 0.23 0.090.00\NN White 0.45 0.61 -0.160.00\NN Male 0.57 0.45 0.120.00\NN AFQT39.9251.36-11.440.00\NN[10pt] N 416 2434 \LL

We use data from the 1979 National Longitudinal Study of Youth (NLSY). The NLSY is an ongoing panel data survey of U.S. residents that were between 14 and 22 when the survey was started in 1979. Following standard approaches in the job displacement literature, we define workers as being displaced if they report no longer being at the same job as in the previous survey and the reason that they left their job is (i) layoff, (ii) plant closed, or (iii) company, office, or workplace closed. Importantly, this does not include individuals who were fired from their job or quit.

The main outcome that we consider is yearly earnings, and we use bi-annual earnings data from 1983-1993. Our treated groups come from workers who report being displaced from their job in the 1989, 1991, or 1993 waves of the survey. We also include workers that were not displaced in any period through 1993, but drop all individuals who were displaced in any period before 1989. To be included in the sample, we additionally require that individuals had positive earnings in both 1983 and 1985. This results in a total sample size of 2,850 individuals. For covariates, we observe workers’ educational attainment, race, and gender — all of these characteristics are commonly observed in micro-level data used in labor economics. In addition to these covariates, one of the interesting variables in the NLSY is an individual’s score on the Armed Forces Qualification Test (AFQT). Researchers using the NLSY have frequently used an individual’s AFQT score as a proxy for their unobserved skill/ability, most commonly including AFQT score directly as an additional covariate.

Summary statistics are provided in LABEL:tab:ss. To start with, it is worth pointing out a few suggestive patterns in the summary statistics. First, notice that in 1983 (before any workers in our sample have been displaced), non-displaced workers already have higher earnings than displaced workers. This suggests that making comparisons based on only the level of earnings over time for displaced and non-displaced workers is likely to lead to misleadingly large estimates of the effect of job displacement. Second, in 1985 (still before any workers in our sample have been displaced), the gap between earnings of displaced and non-displaced workers increases. This further suggests that, at least between 1983 and 1985, the trend in earnings over time was not the same for displaced and non-displaced workers which implies that a difference in differences approach to estimating the effect of job displacement would not have performed well (and would have been likely to over-estimate the effect of job displacement).

In addition, the gap between the earnings of displaced and non-displaced workers also tends to continue to widen over time. There are also noticeable differences in terms of other covariates. Relative to displaced workers, non-displaced workers tend to be more educated, more likely to be white and less likely to be black or Hispanic, more likely to be female, and have higher AFQT scores.

Determining which covariate(s) have time invariant effects on untreated potential outcomes is an important decision in our framework. We take two approaches here. First, we use AFQT score in this role (that is, in Equation 8, we treat unobserved skill as and AFQT score as .) The case for using AFQT in this role is strong. Since AFQT is often seen as a proxy for skill, it is probably reasonable to think that AFQT meets the stronger requirement that it does not affect earnings directly at all as long as “skill” is in the model. For our approach, we only require that the path of earnings in the absence of job displacement does not depend on AFQT as long as skill is in the model.